The head of Russia’s Federal Security Service (FSB) has warned that dangerous non-state actors now possess the capability of equipping drones with chemical weapons and biological weapons in order to maximize mass casualty events.

Speaking at a major conference hosting the security agencies of Commonwealth of Independent States (CIS) on Tuesday, FSB chief Alexander Bortnikov highlighted the ever growing sophisticated and high-tech arsenal of global terrorists, including that “The criminals have materials, technology and infrastructure for the production of chemical weapons and biotoxins,” according to one Russian English language report.

Israeli drone filmed dropping Tear Gas on Gaza protesters on March 30, 2018.

He specifically highlighted the jihadist threat from the war-torn Middle East in places like Syria and Iraq, where Russia intervened starting in 2015 at the request of Damascus. “Although international terrorist organizations suffered great losses in Syria and Iraq, they still have enough resources, particularly provided by their foreign sponsors, to carry out attacks around the world,” Bortnikov said, according to TASS.

The longtime FSB chief said further that, “large jihadist units have been defeated but now they are trying either to regroup in areas not controlled by the Syrian government or to take shelter in refugee camps.”

He also sounded an alarm which has now for years been a familiar worry for Europe – the return of foreign fighters who had previously traveled illegally to Europe. “We know about intentions of the leaders of international terrorist organisations to use widows, wives and children of militants who come back en mass,” he said.

Among ISIS’ top military leadership, for example, are Russian and Chechen jihadists from Muslim populations along Russia’s peripheries.

The FSB chief’s highlighting of the “chemical drone attack” threat was likely in response to repeat drone attacks on Russia’s main Syrian air base, called Hmeymim air base in Latakia Province, over the past year. As recently as Monday of this week Russia’s Defense Ministry said its forces had repelled yet another drone and missile attack from nearby entrenched Hayat Tahrir al-Sham (formerly Nusra Front or al-Qaeda in Syria).

Recent international reports have highlighted ISIS’ capabilities for deploying weaponized Unmanned Aerial Vehicles (UAVs).

Though “chemical and biological warfare delivery drones” is a concept which sounds like something out of a sci-fi movie, one recent western military analysis study said that it’s already becoming reality, and it is indeed jihadist terrorists at the forefront of such development.

Two CBRN and defense tech exports recently produced a study entitled, “Drones of Mass Destruction: Drone Swarms and the Future of Nuclear, Chemical, and Biological Weapons,” wherein they concluded the following:

Drone swarm technology is likely to encourage chemical and biological weapons proliferation and improve the capabilities of states that already possess these weapons. Terrorist organizations are also likely to be interested in the technology, especially more sophisticated actors like the Islamic State, which has already shown interest in drone-based chemical and biological weapons attacks…

Indeed, swarms have the potential to significantly improve chemical and biological weapons delivery. Sensor drones could collect environmental data to improve targeting, and attack drones could use this information in the timing and positioning for release, target selection, and approach. For example, attack drones may release the agent earlier than planned based on shifts in wind conditions assessed by sensor drones.

The study also pointed out that “As the technology underlying drone swarms matures and spreads, the barriers to entry will almost inevitably fall.” It specifically cites Islamic State and other terror groups in Syria who have shown incredible sophistication in the way they’ve adapted drones.

The report also noted the fact that merely one drone is enough to shut down an entire international airport, such as last December’s Gatwick incident.

via ZeroHedge News http://bit.ly/2VEob7O Tyler Durden

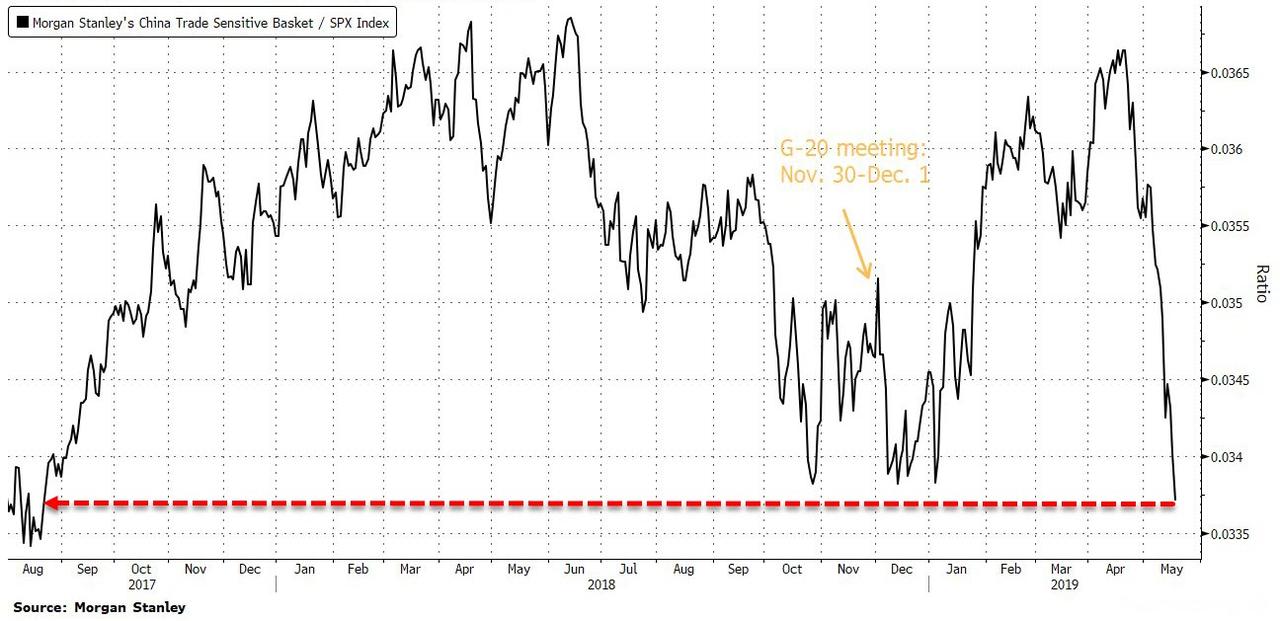

How the U.S.-China trade war plays out is key to the future of U.S. stocks, and while hope is rife on every ‘inspirational’ “constructive” headline, Bloomberg macro strategist Mark Cudmore clarifies the way forward by applying Occam’s razor to the situation, leaving him no choice but to be bearish.

And while headline indices may be rallying overnight on Huawei reprieve hopes, the trend in China-sensitive stocks is not your friend…

Via Bloomberg,

As Cudmore explains, there are obviously a host of other macro inputs. Most that are likely are largely priced and therefore relatively marginal. Unforeseen events, or black swans, significantly skew toward being negative surprises since uncertainty and volatility reduce the risk-reward of having cash tied up in investments.

The trade war is not the only driver of U.S. stocks, but it’s a very large one where the status quo isn’t yet priced and the uncertainty remains high. This arguably makes it the key driver for the rest of 2019 that we can strategize for right now.

There are essentially three scenarios:

1) The trade war escalates further and more barriers are implemented; clearly bad news for stocks

2) The trade war ameliorates and already-implemented measures are lifted; good news for stocks

3) There’s no change to the current situation; equities have a long way to fall as they have not priced in the hit to earnings and the economy from the recently implemented tariffs being a permanent part of the landscape.

I have no extra insight on which way the trade war will play out. Occam’s razor dictates that the outcome that requires the least speculation is most likely to be correct. That means the one where there’s no major shift from the present U.S.-China trading relationship that exists today. That suggests S&P 500 downside, as outlined below…

The recent escalation in the U.S.-China trade war is a game-changer which could put overvalued American stocks through months of pain — for at least the rest of the year.

A few months ago, an increase in bilateral tariffs was seen as 2019’s negative tail-risk. In hindsight, that looks optimistic and U.S. stocks have yet to price in the resulting slowdown in growth and earnings

There’s an assumption it’s just part of negotiations and will soon be resolved. The evidence provides little support for such complacency

The tone in state-sponsored Chinese media has shifted markedly more belligerent this month. Anti-U.S. sentiment is growing rapidly, as shown by a trade war song going viral in Beijing

And the trade tensions are no longer just about tariffs and their drag on growth: The targeting of tech giant Huawei is directly disrupting supply chains. The impact here is perhaps even more damaging for a U.S. equity bull market that has been so dependent on the tech sector

Many U.S.-based investors seem to be slow in registering where the world’s consumer power now lies. Asia has more than 50% of the world’s population, with almost 20% in China alone. This is a tech-savvy, consumption-focused middle-class population with a rising disposable income

Focusing on just the hit to U.S growth misses a large chunk of the negative earnings impact to come for all those Amercian multinationals

After being very bullish U.S. equities for 2019, I turned bearish on April 30 via this column. I highlighted stretched valuations but expected only a multi-week correction before fresh highs later in the year

That was before the trade war escalated. The landscape has changed enormously and those valuations now look far more out of whack

The Bloomberg U.S. economic surprise index has been below zero for almost five months — during a time when most were optimistic toward the trade negotiations. The months ahead will see the outlook deteriorate further

The S&P 500’s blended 12-month forward-looking price-earnings ratio stands at 16.3 versus the 10-year average of 15. Worryingly, that’s before analysts slash estimates further, meaning an even longer way to fall to hit that long-term average

The price-to-book ratio is 3.3, versus the 10-year average of 2.6. The price-to-free-cash-flow ratio is 22 versus the 10-year average of 16.5

And these frighteningly expensive valuations are for just the S&P 500, let alone some of the more-tenuously priced unicorns and tech stocks

It’s not that the world economy is set to collapse. It’s not even that positioning is overly stretched or liquidity conditions are particularly tight. It’s just the value proposition in U.S. equities has suddenly vanished and will only look more negative by the week

When you add in the fact the credit cycle is turning, it gets a little more scary. Then you consider that any Fed power to support financial assets has been significantly diminished with rate cuts already well-priced into markets

At best, the Fed delivers the monetary easing that’s priced, but that’s no guarantee. And how will investors react to the signal of a rate-cutting cycle? The last time they experienced one was in 2008, so it may spark some worrying flashbacks

Cudmore concludes rather ominously:

“I’ve been a structural bull on U.S. equities for many years. I’ve had periods of being tactically bearish that have lasted for several months. The most recent one began April 30. But, for the first time since long before I joined Bloomberg News in 2014, I’m wondering if it’s time to become a structural bear on U.S. stocks.

All I know for sure is that the game has changed significantly and investors have not yet realized. That makes me very nervous…”

But there is a silver lining (of sorts) as Bloomberg’s Richard Breslow reminds investors, it’s not the economy, it’s not the trade-deal, and it’s not earnings… It’s the central banks, stupid!!

Here’s what’s on the other side of the ledger from a stock market that is easy to hate but continuously holds the levels it has to: dovish central bankers who are receiving very little pushback, trillions of dollars worth of negative-yielding debt, and credit swaps that look like they have taken a pause from tightening. Add to that emerging markets that are looking decidedly squishy and a dollar that has remained stubbornly bid.

It’s certainly reasonable to argue that equities may have put in a top for now. Maybe for longer than now. But it is too early to call the market broken until it breaks. Easy for me to say, I know, because there is a lot to be pessimistic about. Maybe we’ll finally see an episode where political risk does overwhelm the rate-setters. It just hasn’t happened yet with lasting effect. While the indexes sometimes look ugly and the news sounds even worse, the fact remains that the strong hands are still the ones most constructive for the long haul.

Equities have dealt with non-believers for years during the whole way up. The bulls put it down to skill and the bears describe a less flattering view of things. Every time the market holds a level and the dip is bought, Willie Nelson’s lyrics come to mind: “The winners tell jokes and the losers say deal. Lady Luck rides a stallion tonight. And she smiles at the winners and she laughs at the losers. And the losers say now that just ain’t right.”

All sounds a little bit ‘Dirty Harry’ to us: “Do you feel lucky, punk?”

via ZeroHedge News http://bit.ly/2HunA59 Tyler Durden

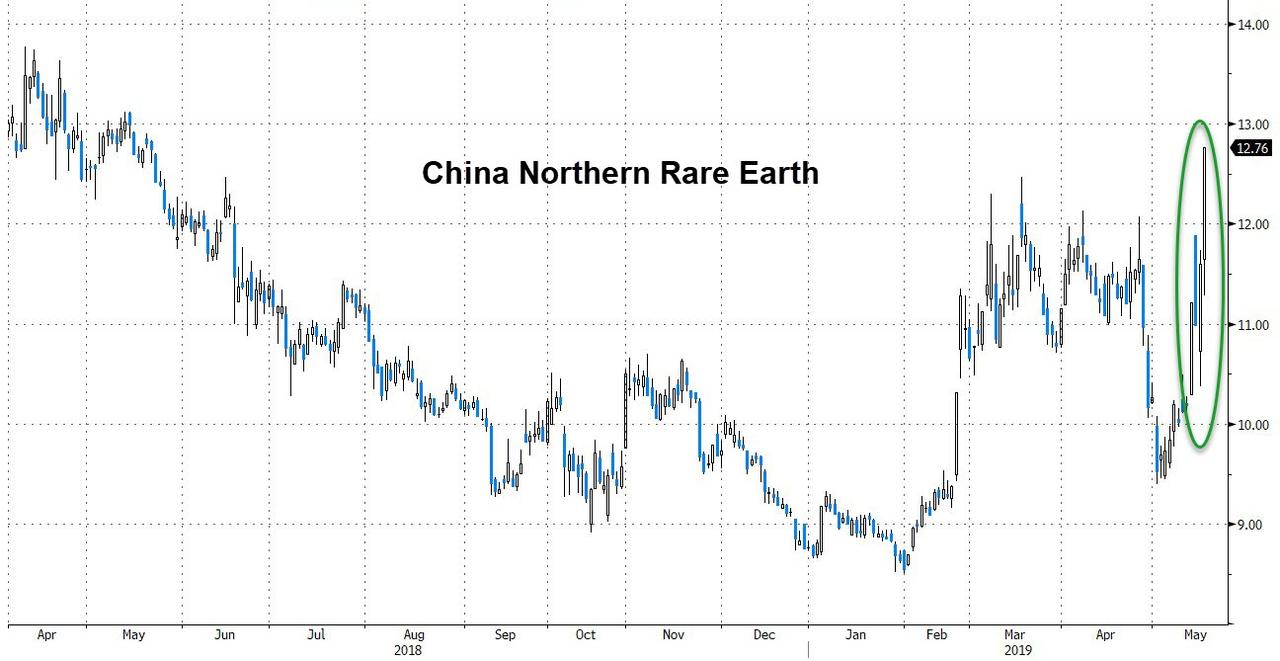

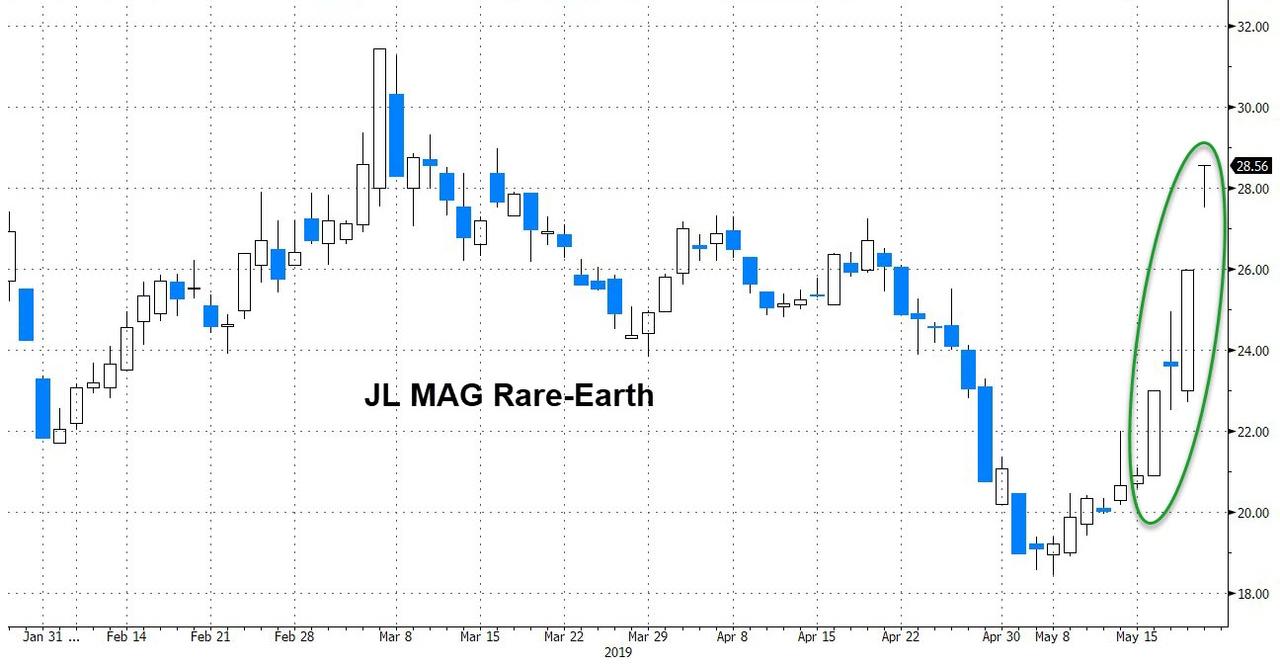

As Bloomberg notes, China Northern Rare Earth, Shenghe Resources, China Minmetals Rare Earth, and JL MAG Rare-Earth all spiked by the 10% daily limit in mainland trading, extending Monday’s similar gains…

In Hong Kong, where there is no restrictive upside/downside limit, China Rare Earth Holdings surged as much as 132%…

As we noted previously,the reason for the dramatic market response is that the presidential visit flags policy priorities, and “rare earths have featured in the escalating trade spat between the U.S. and China.”

Specifically, as Bloomberg notes, China raised tariffs to 25% from 10% on American imports, while the U.S. excluded rare earths from its own list of prospective tariffs on roughly $300 billion worth of Chinese goods to be targeted in the next wave of measures. And just in case the White House missed the message, Xi was accompanied on the trip to JL MAG by Liu He, the vice premier who has led the Chinese side in the trade negotiations.

Why does China have a clear advantage in this area? Simple: the U.S. relies on China, the dominant global supplier, for about 80% of its rare earths imports.

The visit “sends a warning signal to the U.S. that China may use rare earths as a retaliation measure as the trade war heats up,” said Pacific Securities analyst Yang Kunhe. That could include curbs on rare earth exports to the U.S., he said.

Xi’s visit came just hours after the Trump administration on Friday blacklisted Huawei and threatened to cut it off from the U.S. software and semiconductors it needs to make its products. A spokesman for China’s foreign ministry told reporters Monday to “please wait and see” how the government and companies respond.

Finally, to those looking to trade a potential rare-earth export ban, one place would be to go long the REMX rare earth ETF, which after hitting an all time high of $114 in 2011 during the first rare-earth “scare” during the China-Japan trade war, is trading some 90% lower as the market has all but discounted any possibility of a price spike…

…until the last two days…

Needless to say, should China lock out the US, the price of rare earths could soar orders of magnitude higher.

via ZeroHedge News http://bit.ly/2YFjYmk Tyler Durden

Existing home sales were the odd one out in March (falling as new- and pending-home-sales spiked) but expectations were for a catch-up rebound in April, but did not, dramatically missing the expectation of a 2.7% rise by dropping (again) by 0.4% MoM…

This 0.4% decline comes after existing home sales fell 4.9% MoM in March with a tumbling mortgage rate seemingly not affecting the secondary market…

Single-family units fell 1.1% MoM but Condos/Co-ops jumped 5.6% in April (erasing March’s 5.3% drop).

Supply increased from 3.8 to 4.2 months (the highest since Oct 2018) as median prices jumped to their highest since July 2018.

Only The West saw an increase in sales (up 1.8% MoM) in April, with the Northeast worst, down 4.5% MoM.

Worse still, existing home sales are still down 4.4% year-over-year…

This is the 14th month in a row of annual declines – the longest stretch since the housing crisis over a decade ago…but that’s probably nothing!!

via ZeroHedge News http://bit.ly/2WbTxax Tyler Durden

Out of all the speculation about the fallout from Washington’s Huawei blacklisting, this analyst comment offers perhaps the most spectacularly apt summation of what’s in store for Huawei’s smartphone business now that Google has suspended its Android developer license.

“As far as overseas markets go, this move just turned Huawei’s upcoming phones into paperweights,” said Bryan Ma, vice-president of client devices research at IDC Asia-Pacific. “The phones won’t be very useful any more without Google apps on them, and other apps will be unable to call on Google Play services.”

Though Google has temporarily reversed this decision after the White House temporarily eased restrictions, that delay will only last 90 days. Though Huawei has already started building its own operating system, losing access to Android would make Huawei phones significantly less attractive to consumers.

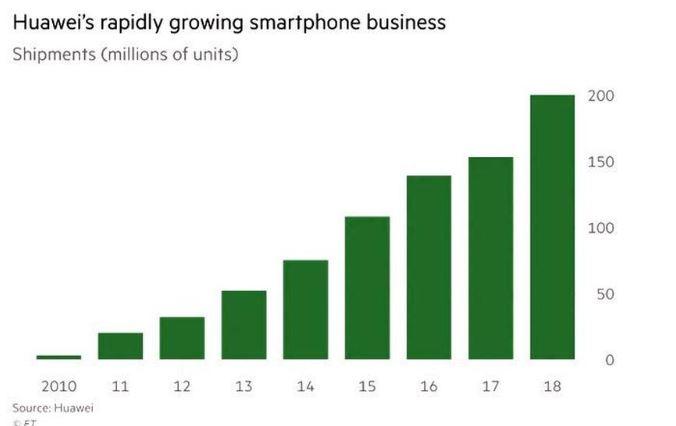

This could be a huge boon for Samsung, the largest player in the global smartphone market, and even smaller Chinese firms like Xaomi stand to benefit, according to analysts. Huawei’s shipments exploded 50% YoY during Q1, capping off a period of torrid growth for the company’s smartphone business that saw it usurp the global No. 2 spot from Apple.

But it could soon surrender much of this advance. One student in Singapore said Google’s decision to cut ties with Huawei made him think twice about buying a new Huawei phone.

He’s decided to hold off on his purchase…for now, at least.

Some consumers are already shying away from Huawei because of future uncertainty. Germaine Wong, a postgraduate student in Singapore, recently considered purchasing a Huawei P30 smartphone to replace her current Samsung S7 Edge, but is now having second thoughts about using a Huawei device.

“I originally considered buying a Huawei P30 or P30+ for my next smartphone because the camera specifications are very good, and I’m already an Android user,” Wong said. “But now I’m concerned about whether Huawei phones will be able to function optimally in the future, or if I will have the latest updates from Google.”

For now, Wong has decided to hold off on her purchase and do more research before buying a smartphone. “After all, there are still other alternatives to Huawei, such as Samsung,” she said.

If Huawei does deploy its own operating system, convincing consumers to adapt to it will be a daunting task, particularly in the ‘Internet of Things’ age when seamless integration is essential.

Huawei confirmed earlier in March that it had built its own operating system for smartphones and computers in case it could one day no longer rely on Android. But deploying and maintaining its own OS for its devices will be a “daunting task”, said Tarun Pathak, associate director at Counterpoint Research, especially as the company looks to compete in the premium segment.

Moreover, the US restrictions on Huawei come at a bad time for the Chinese giant, just as its efforts to narrow the gap with Samsung were gaining momentum.

“The premium segment is growing fast, and seamless integration of hardware and software is now a must to drive consumer experience,” said Pathak. “In the absence of an Android licence, Huawei will have its work cut out to build something that can live up to the Android experience.”

But where Huawei might suffer, other Chinese smartphone firms are the best positioned to benefit.

In the medium term, smaller Chinese smartphone players who have been making a bigger overseas push, such as Xiaomi and Oppo, are also likely to benefit from any dip in demand for Huawei devices. Xiaomi, for example, was Europe’s No 4 smartphone maker by shipments in 2018, and already has a presence in markets like Spain, the UK, France and Italy.

“In the medium-term, brands like Xiaomi and Oppo that are entering Europe and really trying to capture market share, will benefit,” said Francisco Jeronimo, associate vice-president for European devices at IDC. “This potentially can be an opportunity for these brands to grow.”

Assuming Google reinstates the ban once the White House reimposes the new restrictions, the Silicon Valley tech giant probably won’t be able to escape some blowback.

Xiaomi’s chief financial officer Chew Shou Zi said in an earnings call on Monday that it was “paying a lot of attention” to Google’s move to curtail business with Huawei, but said there was “no direct impact” on the company.

Analysts pointed out that the Google ban on Huawei will also have a negative impact on the US internet giant.

“Huawei is the second-largest Android player and a major client, so if they cannot sell anything to Huawei any more, Google will suffer from that,” said Jeronimo.

via ZeroHedge News http://bit.ly/2JBXvDx Tyler Durden

“Price is what you pay, value is what you get.” – Warren Buffett

Just recently, I discussed the importance of valuations as it relates to investors who are close to retirement age. To wit:

“Unless you have contracted ‘vampirism,’ then you do NOT have 90, 100, or more, years to invest to gain ‘average historical returns.’ Given that most investors do not start seriously saving for retirement until the age of 35, or older, they have about 30-35 years to reach their goals. If that period happens to include a 12-15 year period in which returns are flat, as history tells us is probable, then the odds of achieving their goals are severely diminished.

What drives those 12-15 year periods of flat to little return? Valuations.”

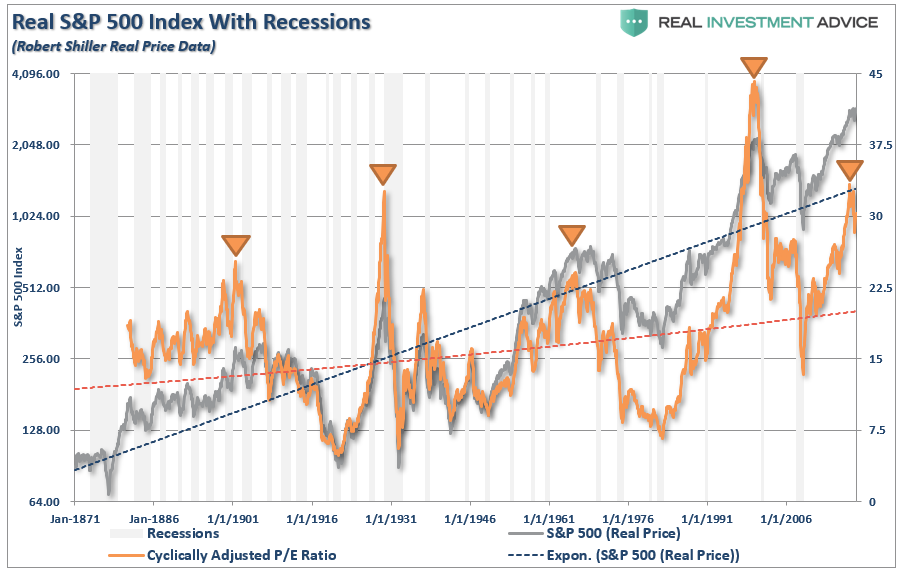

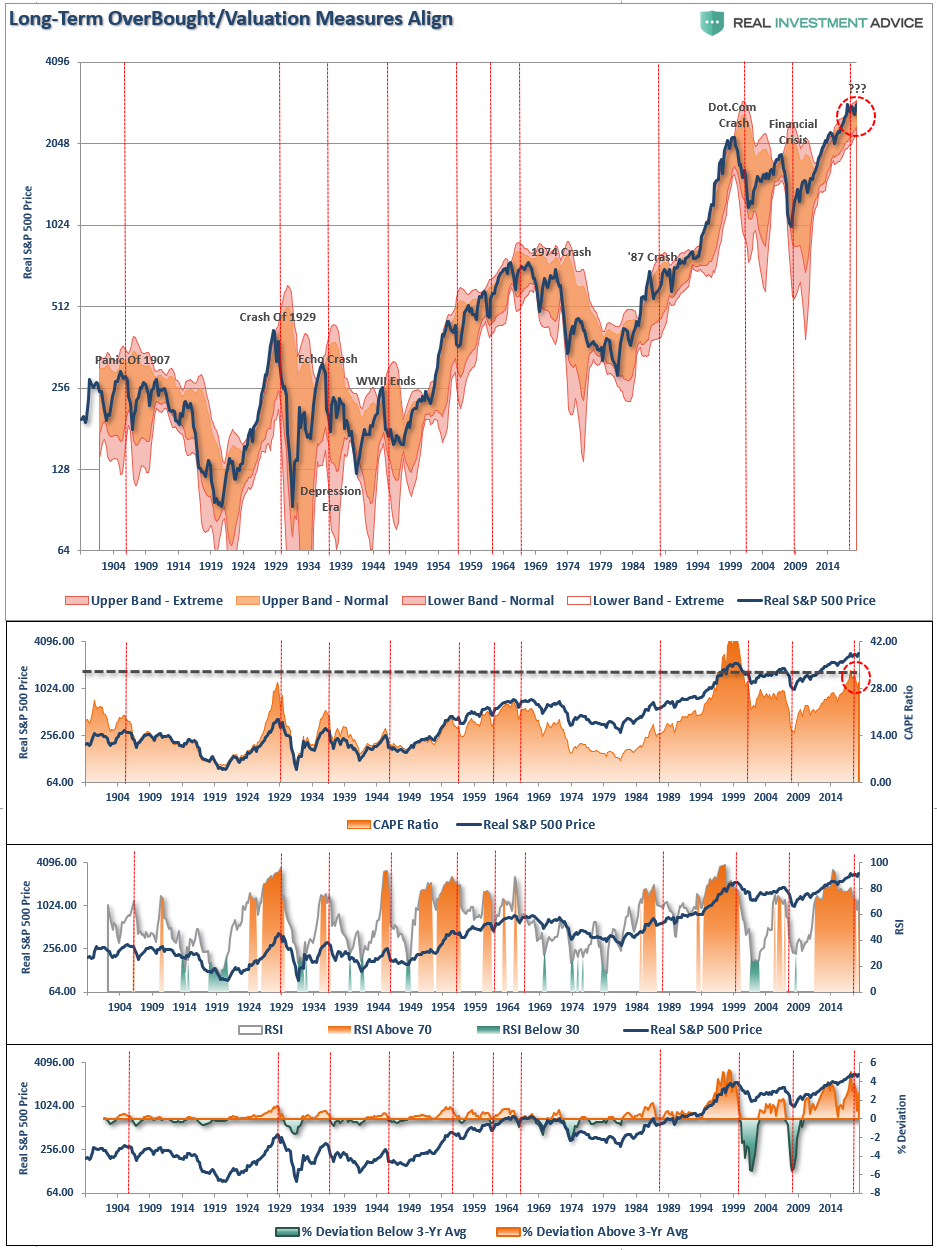

Despite commentary to the contrary, the evidence is quite unarguable. As shown in the chart below, the cyclical nature of valuations and asset prices is clear.

In the short-term, a period of one year or less, political, fundamental, and economic data has very little impact on the market. This is especially the case in a late-stage bull market advance, such as we are currently experiencing, where the momentum chase has exceeded the grasp of the risk being undertaken by unwitting investors.

What investors most often overlook, due to this “short-termism” or the “fear of missing out,” is the risk being undertaken which will lead to less optimistic outcomes over the investment time frame of 10 to 20-years.

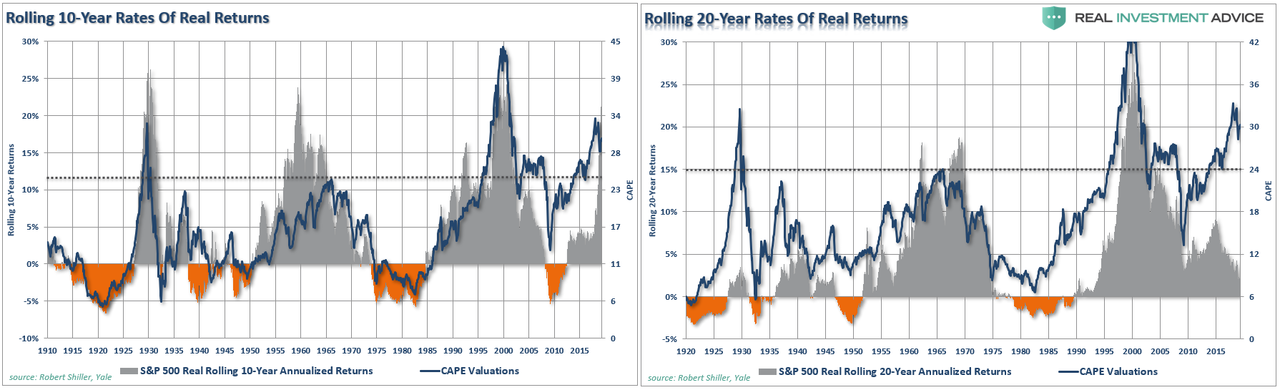

Just remember, a 20-year period of one-percent returns is indistinguishable from ZERO with respect to meeting savings goals. However, our focus today is looking at future returns over the next decade from current valuation levels which, again, are expected to be low to negative.

“While daily, weekly, and monthly indications are useful, taking a look at ‘quarterly’ data can give us clues as to the ‘real risk’ investors are taking on at any given time. Is this the beginning of a major bull market cycle? Or, are we nearing the end of one? How you answer that question, given the relatively short time frame of the majority of investors (hint – you don’t have 100-years to reach your goals), can have an important impact on your outcome.

The problem for investors is that since fundamentals take an exceedingly long time to play out, as prices become detached ‘reality,’ it becomes believed that somehow ‘this time is different.’

Unfortunately, it never is.

The chart of the S&P 500 is derived from Dr. Robert Shiller’s inflation adjusted price data and is plotted on a QUARTERLY basis. From that quarterly data I have calculated:

The 12-period (3-year) Relative Strength Index (RSI),

Bollinger Bands (2 and 3 standard deviations of the 3-year average),

CAPE Ratio, and;

The percentage deviation above and below the 3-year moving average.

The vertical RED lines denote points where all measures have aligned”

Even after the sideways action over the last 18-months, the extended technical measures remain. Importantly, this doesn’t mean the market will mean revert tomorrow, it does imply that forward returns for current levels will be substantially lower than they have been over the last several years.

Yes, I know.

“P/E’s don’t matter anymore because of Central Bank interventions, low interest rates, accounting gimmicks, share buybacks, etc.”

It was the same in 2000 and 2007 when the “bull market psychology” makes such antiquated ideas like “value”seem irrelevant.

The important point to understand is that over the long-term investing period “value” and “returns” are both inextricably linked and diametrically opposed. As shown above, given current valuation levels, forward returns are expected to be lower than the long-term average.

Before we look at different valuation measures, let’s review what “low forward returns” does and does not mean.

It does NOT mean the stock market will have annual rates of return of sub-3% each year over the next 10-years.

It DOES mean the stock market will have stellar gains in some years, a big crash somewhere in between, or several smaller ones, and the average return over the decade will be low.

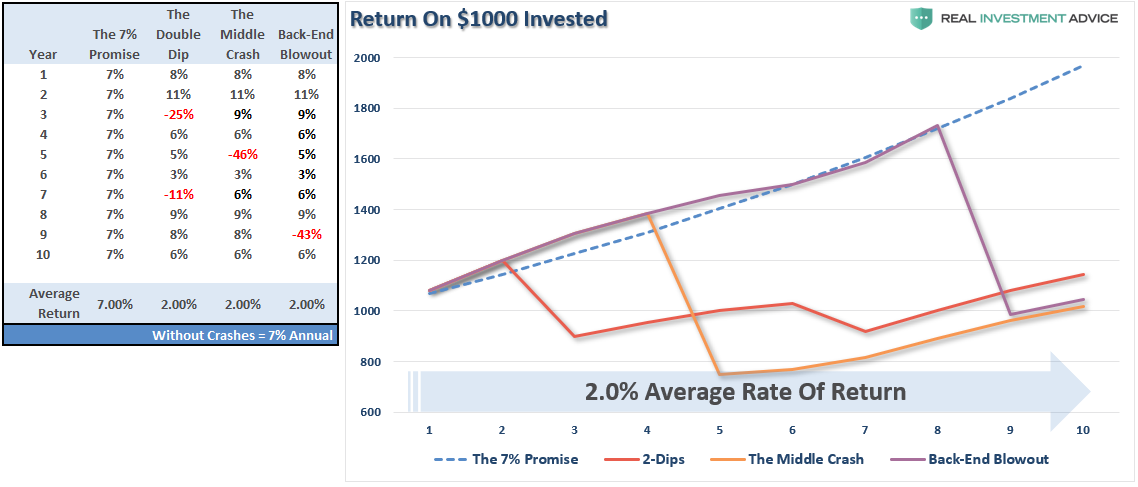

“This is shown in the table and chart below which compares a 7% annual return (as often promised) to a series of positive returns with a loss, or two, along the way. (Note: the annual average return without the crashes is 7% annually also.)”

“From current valuation levels, two-percent forward rates of return are a real possibility. As shown, all it takes is a correction, or crash, along the way to make it a reality.”

This isn’t a prediction, it is just statistical probability and simple math.

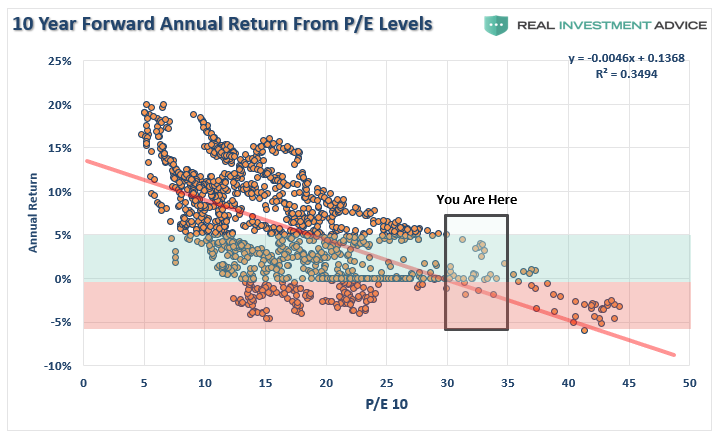

With the premise in mind, let’s take a look at a variety of valuation measures as compared to forward 10-year returns.

The Charts

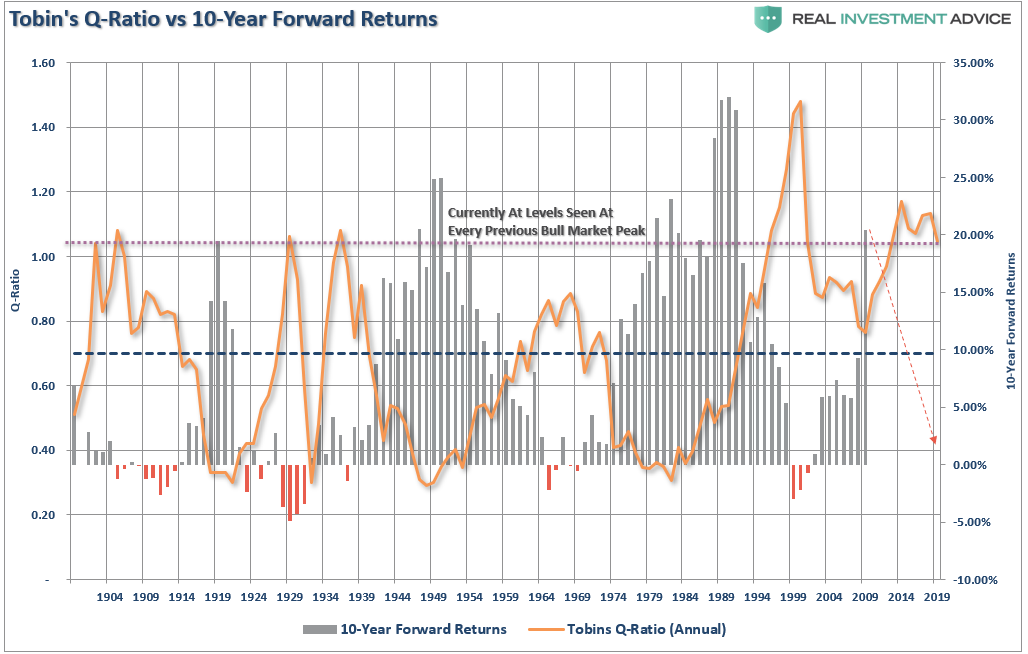

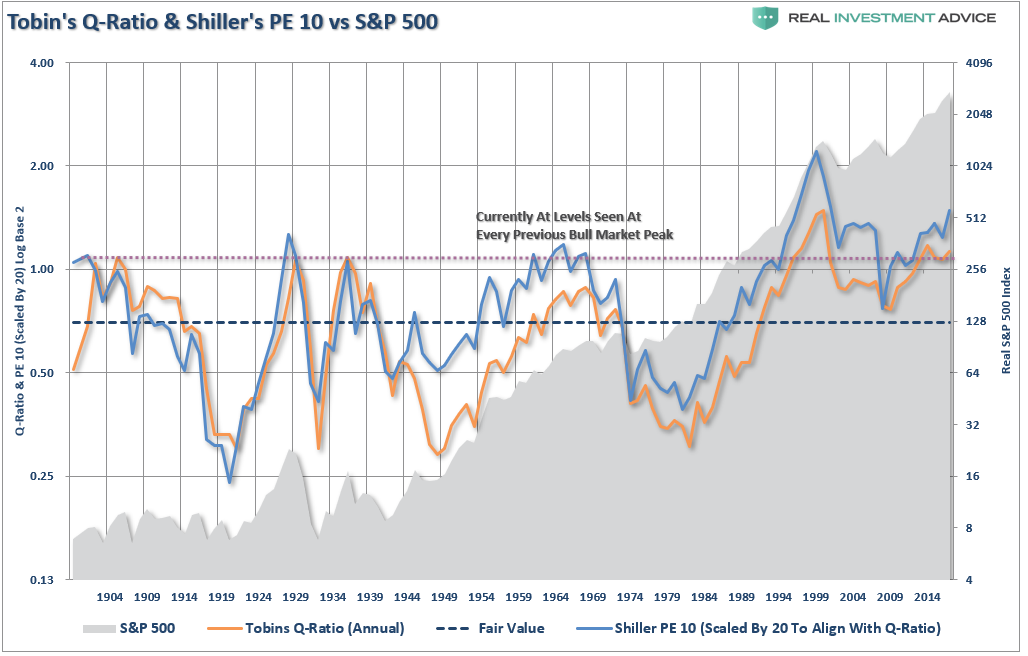

Tobin’s Q-ratio measures the market value of a company’s assets divided by its replacement costs. The higher the ratio, the higher the replacement costs resulting in lower returns going forward.

Just as a comparison, I have added Shiller’s CAPE-10. Not surprisingly, the two measures not only have an extremely high correlation, but the return outcome remains the same.

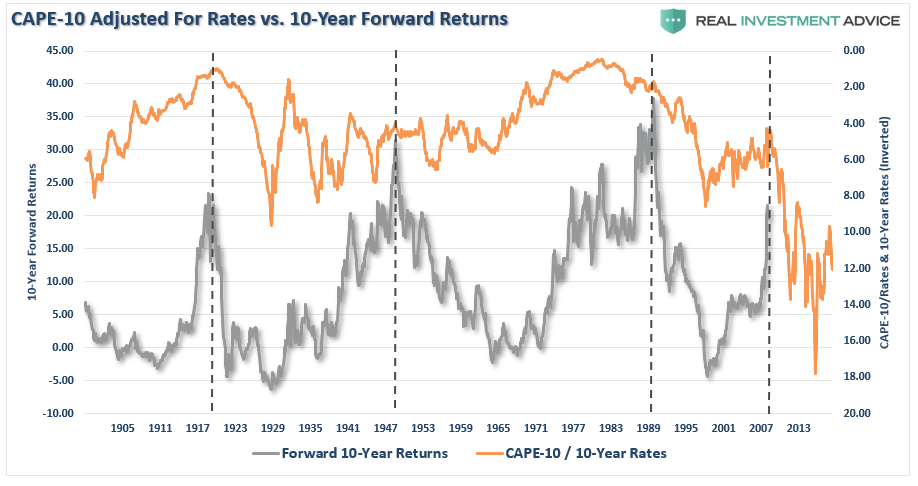

One of the arguments has been that higher valuations are acceptable because interest rates have been so low. As we can see below, when we take the smoothed P/E ratio (CAPE-10 above) and compare it to the 10-year average of interest rates (inverted scale) going back to 1900, the valuation to interest rate argument fails.

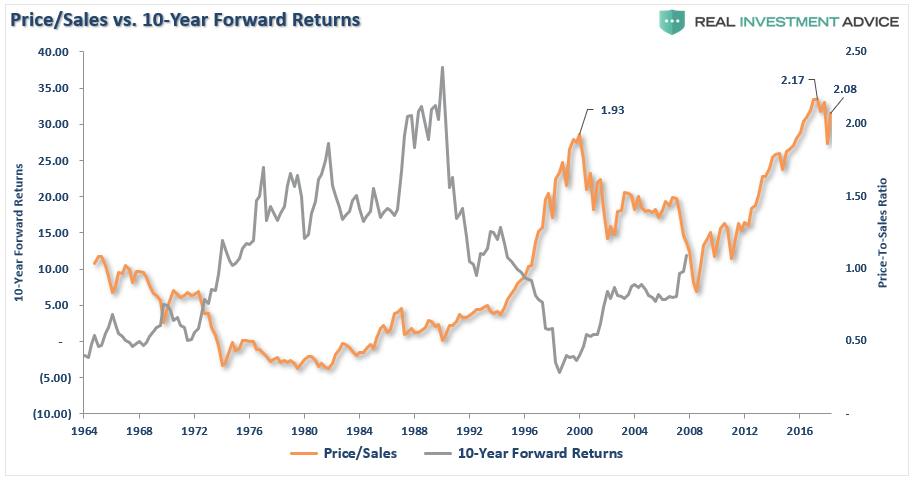

As noted above, historical valuation measures have been dismissed for a variety of reasons from Central Bank interventions to the rise of automation. However, while earnings can be manipulated through a variety of measures like share buybacks, accounting gimmickry, and wage suppression, “sales,” or “revenue,” which occurs at the top-line of the income statement is much harder to “fudge.” Not surprisingly, the higher the level of price-to-sales, the lower the forward returns have been. You may also want to notice the current price-to-sales is hovering near the highest level in history.

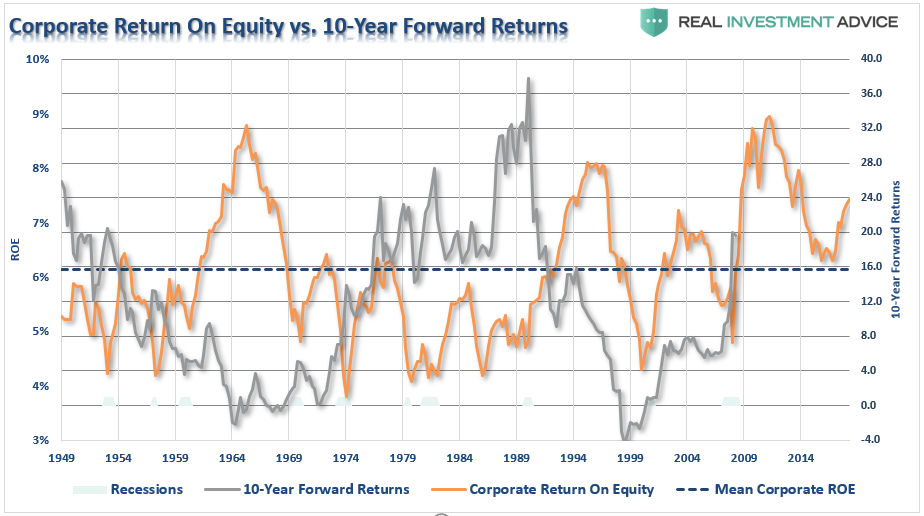

Corporate return on equity (ROE) sends the same message.

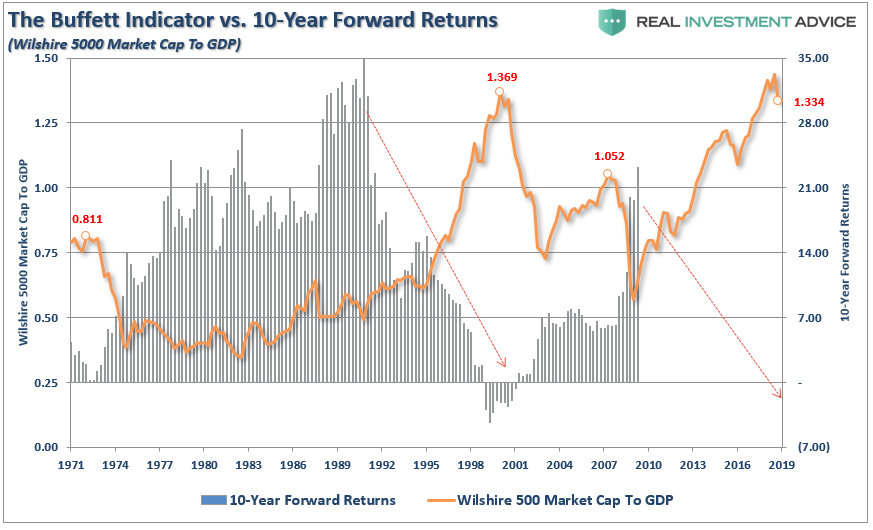

Even Warren Buffett’s favorite indicator, market cap to GDP, clearly suggests that investments made today will have a rather lackluster return over the next decade.

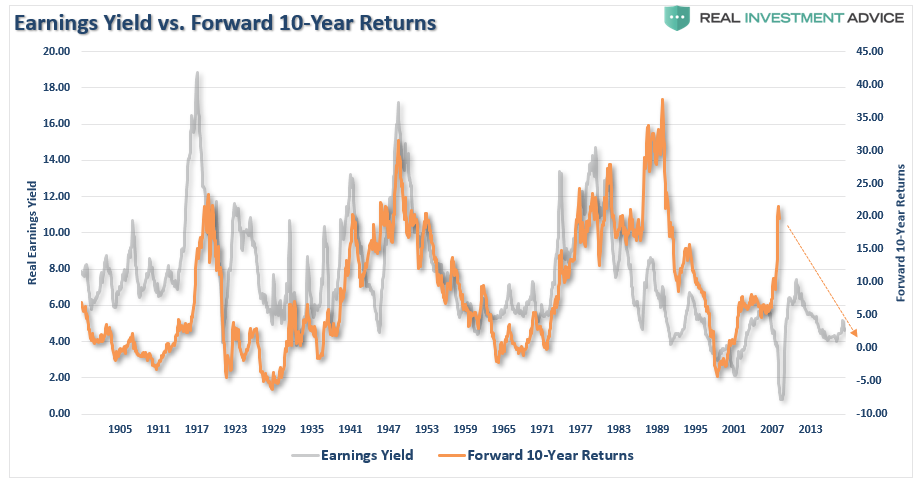

Even when we invert the P/E ratio, and look at earnings/price, or more commonly known as the “earnings yield,” the message remains the same.

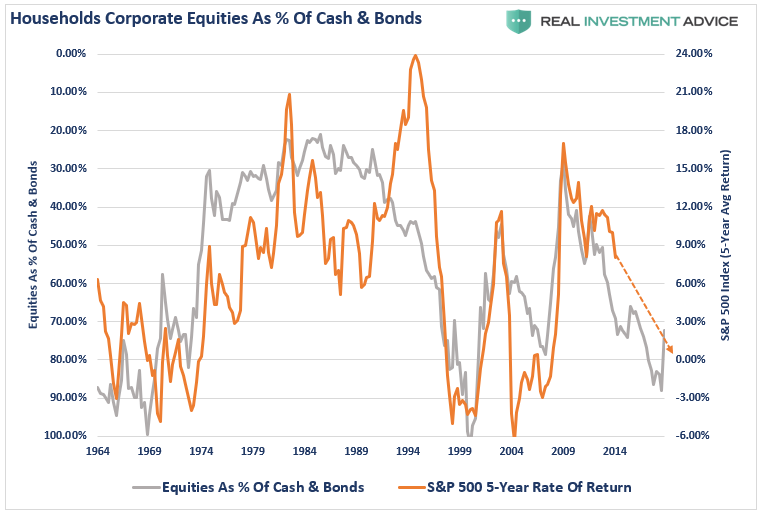

We can reverse the analysis, as noted last week, and look at the “cause” of excess valuations which is investor“greed.”

“As investors chase assets, prices rise. Of course, as prices continue to rise, investors continue to crowd into assets finding reasons to justify overpaying for assets. However, there is a point where individuals have reached their investing limit which leaves little buying power left to support prices. Eventually, prices MUST mean revert to attract buyers again.”

The chart below shows household ownership of equities as a percent of household ownership of cash and bonds. (The scale is inverted and compared to the 5-year return of the S&P 500.)

Just like valuation measures, ownership of equities is also at historically high levels and suggests that future returns for equities over the next 5, 10, and 20-years will approach ZERO.

No matter, how many valuation measures you wish to use, there is no measure which currently suggests valuations are “cheap” enough to provide investors with sufficiently high enough returns over the next decade to meet their investment goals.

Let me be clear, I am not suggesting the next “financial crisis” is just around the next corner. I am simply suggesting that based on a variety of measures, forward returns will be relatively low as compared to what has been witnessed over the last decade. Such results are historically NOT a factor of “just one” issue but rather a culmination of issues which are simultaneously ignited by a single, unforeseen, catalyst.

As Doug Kass noted on Monday, there is a growing list of issues which will coalesce given the right catalyst.

Slowing economic growth

Trade/Tariffs

Credit spreads have begun to widen

Geopolitical uncertainties (Russia, China, North Korea, Iran)

Fiscal policy uncertainty

Earnings growth at risk

A very crowded momentum trade (ETF)

Most importantly, as stated above, none of these factors or measures mean the markets will just produce single-digit rates of return each year for the next decade. The reality is there will be some great years to be invested over that period, unfortunately, like in the past, the bulk of those years will be spent making up the losses from the coming recession and market correction.

That is the nature of investing in the markets. There will be fantastic bull market runs as we have witnessed over the last decade, but in order for you to experience the up, you will have to deal with the eventual down. It is just part of the full-market cycle which encompass every economic and business cycle.

How you choose to handle the second-half of the full-market cycle is entirely up to you. However, “this time is not different,” and in the end, many investors will once again be reminded of this simple fact.

Unfortunately, those reminders tend to come in the most brutal of manners.

via ZeroHedge News http://bit.ly/2VEjgnz Tyler Durden

At a moment the US Navy conducted provocative military exercises in the Arabian Sea on Monday, Iran’s president responded to overtures by Trump that Tehran should “call me” with a firm line of, “No talks, only resistance.”

US military statements highlighted the Arabian Sea drills were specifically in response to heightened unspecified threats from Iran, and were led by the USS Abraham Lincoln Carrier Strike Group and the US Marine Corps to highlight American “lethality and agility to respond to threat” and to advance US security.

Iran’s President Hassan Rouhani, who oversaw the 2015 nuclear deal negotiations (JCPOA) with then president Obama, said he welcomed any US diplomatic overture but wouldn’t be coerced into new negotiations under economic sanctions and threat of military action.

“I favor talks and diplomacy but under current conditions, I do not accept it, as today’s situation is not suitable for talks and our choice is resistance only,” Rouhani said, according to Iran’s IRNA news agency.

“If we walked away from the JCPOA [Joint Comprehensive Plan of Action – the formal name of the nuclear deal] with the US provocative acts, then, in addition to the US, the UN and world would also impose sanctions on us,” he said.

It appears Trump has taken a “North Korea-style” approach to Iran that combines unpredictably aggressive threats and maneuvers – especially by other White House officials – with unexpected moments of reaching out a hand.

That tactic was certainly on display Monday when Trump expressed US willingness to meet any Iranian action against US interests with “great force” – yet followed it by saying it’s up to Iran to initiate conciliatory dialogue: “If they call, we will certainly negotiate, but this is going to be up to them,”he told reporters.

The amphibious assault ship USS Kearsarge sails in front of the USS Abraham Lincoln aircraft carrier on May 17, 2019, in the Arabian Sea. via US Navy/Military Times

That came a day after on Trump put Tehran on notice in a Sunday tweet saying, “If Iran wants to fight, that will be the official end of Iran” and to “never threaten the United States again”.

But unlike with North Korea, this “maximum pressure” threat tactic doesn’t appear to be working, especially as Iran has many more international allies, and given six major powers had already agreed to the 2015 JCPOA, which the White House last May backed out of.

Meanwhile, Iran has signaled following Trump’s “call me” message given to Tehran’s leaders through press briefings that it’s ready to do the complete opposite, considering its official nuclear agency announced Monday it has“quadrupled its production of low-enriched uranium“.

Iranian President Hassan Rouhani, via the AP

Both the semi-official Fars and Tasnim news agencies cited Iran’s nuclear agency spokesman Behrouz Kamalvandi to say the country would reach the 300-kilogram limit set by the nuclear deal merely “in weeks”— in what appears counter-threat signalling to Washington.

via ZeroHedge News http://bit.ly/2w9XVrF Tyler Durden

“He knew everything about literature, except how to enjoy it…”

Waves of negative news headlines battering markets. Might have to wear a hat..

Huawei – Trade War Threat Level Rises

The Huawei embargo raises the trade war threat from undeclared to imminent shooting match. While it’s not quite “bullets fired at Archduke’s car”, it’s getting close. It feels like there is something of a tedious inevitability developing – a bellicose Trump realizes his political future depends on winning, and the Chinese refuse to lose face. Is it already too late to rein back?

Huawei being effectively barred from Occidental markets has triggered all kinds of market fears: a “digital iron-curtain”, the threat of an economic cold tech war, broken global supply chains, and knock-on effects we can only begin to imagine. It’s the End of Globalisation – scream the media. The Chinese hint at reprisals. The “temporary exemptions” granted last night by the US are just that – temporary: they won’t undo the sudden need of millennials to dump their Huawei phones. The damage has been done. Who will the Chinese punish in return?

Markets are now rife with speculation about “ripple” effects damaging tech dependent initiatives from autonomous cars, streaming, digitisation, and booking apps, triggering all kinds of real-world economic pain in sectors like tourism and luxury goods. While the market is fretting about how America will shod itself as tariffs are slammed on shoes made in China, it might be time to reassess market sectors where we expected long-term and ongoing China expansion, rising domestic consumption and demand to drive growth – I’m thinking areas from aviation, autos, machinery and plant, and energy. And, what are the implications for the UK – where the Chinese are building our nuclear power stations?

This doesn’t end well.

Powell wonders about Corporate Debt

In a fascinating Wall Street Journal article reporting Jerome Powell’s comments on the dangers of rising corporate debt to the US economy, he says he doesn’t rank the danger alongside what sub-prime mortgages did in 2007. Fair enough – but I think he may be underestimating the chain of consequences that could occur.

No matter how hard the trade war recession is, or how much the Fed raises rates, most corporates will not default. Sure, there will be pain, downgrades and re-trenchment. However, the “unintended consequences” of QE, low rates, hasty regulation and the transfer of risk from banks to the investment sector could magnify the scale of pain – and cause ructions in the corporate credit markets to trigger much wider financial pain, the next major crash.

Consider how much Junk and Near Junk Tech debt is out there – WeWork, Tesla, Uber and the rest. If the Tech bubble bursts, their bonds won’t be trading in the 80s, but in single digits.

Look at how much paper is BBB and the cusp of Junk. A small wobble could trigger massive enforced sales from holders unable to hold sub-prime, triggering further fixed income.

Read some of the nonsense written about how liquid Fixed Income ETFs are. If the crunch comes – I don’t see how they can retain value.

Don’t assume the investment sector will respond well if/when risk explodes. See yesterday’s porridge for more on this – the skills to manage and work out risk simply aren’t there…

10-years of monetising equity through debt fuelled buy-backs has made corporates weaker, not stronger, and created falsely valued stock markets. That realisation will trigger not ripples, but a Tsunami across all markets on a corporate debt shock.

Moving on.

Deutsche Bank

As the stock hits a new low, do I really need to ask? How much longer? Apparently a group of core investors have had enough are pushing for the exit of Chairman Achleitner. Meanwhile, the FT suggests Goldman should buy the bank – how amusing.

Jaguar Land Rover. Oh dear..

What does it say about Brexit Britain when our national car company is in serious need of reinvention? Jaguar Land Rover may have posted a small profit for this first few months of this year, but their $3.6 bln loss for the year after write-downs looks disastrous. There is little to suggest the company can turn itself around as Diesel cars remain almost unsellable, and Jaguars fail to excite buyers. Its failed to crack China, and car experts I’ve spoken with doubt the Indian owners have any real vision for the group. Its only decent selling the cars, the I-Pace and E-Pace are actually made by a separate firm and simply badged as Jags!

I have a simple solution for them: Cut prices and customer costs. I went into to look at a new Range Rover last year. A model essentially exactly the same as my current one, came with a £25k price hike from 3 years previously. More to the point, when I asked for financing options, they wanted to charge me a ridiculous usurious level – which I was quickly able to beat by calling another firm, but by then I was so peeved I decided just to keep my current car instead.

I probably don’t ever need to buy another new car – our current fleet of a 4-year old Rangey and a Roller Skate (Fiat 500) is pretty perfect for our purposes. She-Who-Is-Now-Mrs-Blain suggests there is room on the drive for something sporty, but I’m thinking an old Defender might be in order…

via ZeroHedge News http://bit.ly/2VzZ1Y8 Tyler Durden

Boeing shares are spiking, lifting the Dow, after the Wall Street Journal reported that US aviation authorities now believe a ‘bird strike’ may have triggered the sequence of events that led to the crash of Ethiopian Airlines flight 302.

Four weeks after faulty sensor data led a 737 MAX jet to crash in Indonesia last year, a high-ranking Boeing Co. executive raised and dismissed the possibility of a bird collision triggering a similar sequence of events that could cause a second accident.

Fears about the potential for a ‘bird strike’ to damage sensors on the jet appear to have been validated, though Ethiopian authorities aren’t convinced.

US aviation authorities regard a collision with one or more birds as the most likely reason for trouble with the sensor, according to industry and government officials familiar with the details of the crash investigation.

Ethiopian authorities disagree but haven’t provided any specifics to support their conclusion.

Boeing shares spiked 3% in premarket trading on the news, though WSJ’s report doesn’t exactly absolve Boeing. The company must now answer why, if senior executives feared ‘bird strikes’ could be a problem, it persisted in allowing MCAS, its anti-stall software that’s believed to have contributed to two deadly crashes, to rely on only one sensor.

Algos clearly interpreted the news as positive…after all, every American who has seen the movie ‘Sully’ probably remembers how much damage a flock of birds can do.

via ZeroHedge News http://bit.ly/2JTeS1D Tyler Durden

Another hit. It seems every day carries some news destined to make U.S.-China trade negotiations more difficult, with the ban against Huawei the latest example. The effects of the spat have started to show on currency markets and could deliver collateral damage, and European exporters could be big losers.

The escalation of tensions has pushed China’s yuan to year-lows against the dollar, near the 7.0 level seen as critical by several strategists at JPMorgan and Nordea. Further weakness could hurt Chinese asset prices and risk appetite globally, making it “the most important gauge worldwide currently,” Nordea says, and something that European equity investors can’t ignore.

The trade confrontation could drag on, according to Sebastien Galy, a senior macro strategist at Nordea Investment Funds. The next G20 meeting (June 28-29) could be decisive, and if no deal is in sight, the market will likely speculate on a devaluation of the renminbi and higher tariffs, providing a shock to the equity market, Galy writes.

Indeed, the U.S.-China dispute is the most significant hit to the early 2019 consensus of a cyclical global recovery, JPMorgan strategists write, adding that the Chinese Central Bank has been willing to act to prevent further weakness in the yuan.

“While it seems unlikely that China will let the yuan trend lower too durably beyond the 7 threshold, it appears equally unlikely to us that they will not be tempted to do so, just for a while, to test some nerves a bit,” Makor strategist Stephane Barbier De La Serre writes. The strategist has a 7.15 target for the currency, which would have a material impact on global equities, particularly on cyclicals and tech stocks.

The yuan has also lost ground against the euro, which is bad news for European firms selling goods overseas. JPMorgan strategists closed their overweight recommendation on European exporters this week, arguing the euro could be bottoming out.

via ZeroHedge News http://bit.ly/2w9z4o1 Tyler Durden

{kind=link}

{kind=link}

{kind=link}