Still not over…

The Dow is back below yesterday’s lows, down 350 points on the day

And NAsdaq is down 11% from its highs – entering correction…

via Zero Hedge http://ift.tt/2ERXmXb Tyler Durden

another site

Still not over…

The Dow is back below yesterday’s lows, down 350 points on the day

And NAsdaq is down 11% from its highs – entering correction…

via Zero Hedge http://ift.tt/2ERXmXb Tyler Durden

Just over a week ago, President Trump delivered the State of the Union speech. The president gave a speech with a decidedly optimistic tone. This was certainly welcome with the increasingly fractured and divided American political landscape. But it’s important to focus beyond the political theater and take a hard look at where the US economy really is and where it is heading. Unfortunately, the political rhetoric doesn’t always line up with economic reality.

As Peter Schiff has said on numerous occasions, President Trump has taken full ownership of the current bubble economy. In doing so, he’s setting himself up as the fall-guy when things turn sour. Peter put it in pretty stark terms during an interview with Stock Pulse at the Vancouver Resouce Investment Conference.

He is so caught up in this bubble now in the stock market. He’s branded it … The stock market has a big ‘T’ on it for Trump, like one of his buildings.”

So, how exactly does the political rhetoric coming out of the Oval Office stack up against the current economic realities?

Dan Kurz at DK Analytics provided a pretty good breakdown of some key issues where the positive talk doesn’t line up with what’s actually going on.

1. What used to be an ugly stock market bubble that would be pricked by higher interest rates, according to candidate Trump, is now proof that president Trump is doing a great job. Yet, the S&P 500 is currently trading nearly 25x EPS, the broader Wilshire 5000 Index has rocketed higher, and margin debt is nearly $600 billion – a record.

2. In the interim, a recession, which is way overdue, will crush earnings; US aggregate debt rises between $1 trillion and $2 trillion a year; and interest rates are rising smartly, which will pummel valuations if it continues, especially with a recessionary EPS downdraft of 50% plus being likely in the near future based on precedents. (We review such a scenario in some detail in posts #25 and #24, wherein we quantify the rising interest rate impact on the S&P 500’s NPV and wherein we remind investors that markets are “reversion beyond the mean” machines, respectively.)

3. What used to be a fake unemployment rate when Trump was a candidate is now lauded as the “real deal,” even as the civilian labor force participation rate of 62.7% hovers near four-decade lows and two or three low-paying, no-benefit part-time jobs swell the employed ranks while full-time positions continue to be culled. This is insincere.

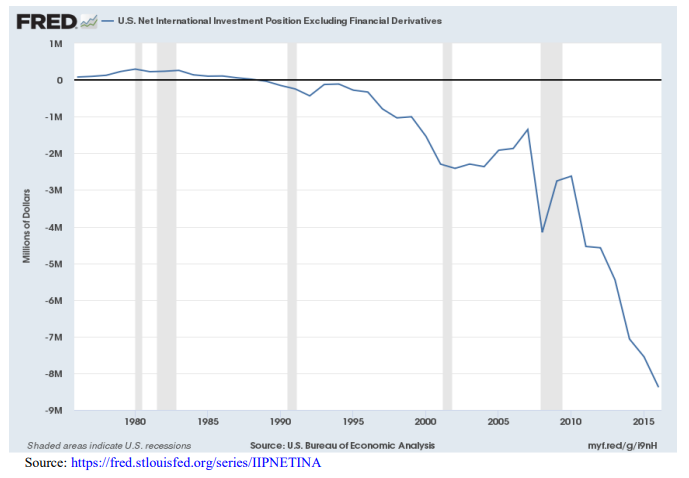

4. During the address, Trump also stated, “Under my administration, wealth is starting to return to America instead of leaving it.” Mr. President, sadly the opposite has been happening, at least so far, as evidenced by a continued rise in the US trade deficit, a substantial portion of which is due to rising oil import prices (and no, Donald Trump, we are not energy self-sufficient. We remain net importers of oil, and our gap could expand as the fracking bubble collapses). Once again, the president’s claims here are misleading at best.

5. President Trump talks a lot about regulatory reform liberating businesses to hire and invest. According to the American Action Forum outfit, regulatory relief of $560 million p.a. from Executive Order 13,771 (two struck for every new regulation or “reg”) can be expected. While praiseworthy, this is but a rounding error compared to an estimated $2 trillion-plus in annual regulatory compliance costs for US economy. While a sharp reduction in federal register pages (where federal rules and regs are published) from Obama’s “out the door” bloat looks promising, we wonder how any true or lasting reforms can be achieved until regulatory agencies are shut down and statist/leftist bureaucrats are fired, esp. given the risk that the GOP control of the fed government could prove only temporary — which Trump himself recently warned about.

6. Trump protectionism – a disconnect. On the heels of going to Davos and touting that America is again open for business thanks to tax cuts and regulatory reform, Trump was quick to slap high tariffs on solar panels, washing machines, and on select steel imports. Three issues here: first, lots of stuff just isn’t made in America anymore, so higher tariffs line government pockets and hurt consumers and producers alike — such as those installing foreign made solar panels that stand to lose customers or those using cheaper foreign steel in high value-added finished products that are exported — while they raise inflation. Second, raising tariffs on US imports will quickly result in higher tariffs on US exports. Third, we all know what can happen to the global economy if countries get into trade wars. It’s spelled Smoot Hawley, revisited and the 1930s depression.

7. Speaking of policy destructiveness; bloated federal government spending is up 3.8% year-over-year and is set to increase faster as Trump touts various new spending initiatives from (what will sadly ultimately prove to be) pork barrel, crony infrastructure projects to “offensive capacity” military spending growth de facto financed by the “rest of the world.” In the interim, tax rate reductions will pressure tax receipts. Finally, weaker economic growth will dramatically increase government spending on welfare and transfer payments. Talk about a perfect deficit-widening storm dead ahead! And this is before secular challenge known as an aging society and its impact on public sector solvency! Is any of this discussed, much less addressed, in Washington D.C.?

8. We could see a $1.5 trillion – $2 trillion plus dollar federal deficit within a few years if not sooner. And if the Fed really sells $600 billion of Treasuries a year, at what price — how high of a yield — will investors and the rest of the world be willing to soak up between $1.5 trillion – $2.6 trillion worth of US Treasuries possibly coming on to the market annually for a time?

9. The above is of particular concern as the rest of the world finances a US goods and services deficit that averages about $500 billion a year and expanded to $600 billion in 2017. Meanwhile, America is a net debtor nation to the tune of $8.4 trillion. In such a world, when you openly state that the US government would welcome a weaker dollar in a period of low interest rates, great external financing dependency, a weakening currency, and rising inflation, you are driving away potential investors and thus de facto raising the cost of borrowing, especially if sentiment shifts or confidences wanes. And, by the way, if currency debasement helped to reduce trade deficits, America, having the tailwind of a dollar that has fallen about 80% since Bretton Woods dollar-gold standard was terminated nearly 47 years ago, should have huge annual trade surpluses by now in place of gaping deficits.

10. You cannot simultaneously grow a spendthrift federal government, cut taxes, and then be sanguine. You can’t grow spending by $300 billion-plus, reduce tax revenues by an estimated $280 billion, and add it to a $666 billion deficit and over $21 trillion in debt and expect good things.

11. In short, Trump is NOT leveling with the American people in terms of what really needs to be done for the benefit of future generations who will otherwise be hobbled by mountains of debt and the related financing costs, namely: focus on cutting government spending, achieving a balanced budget, aggressively pursuing litigation reform (US liability costs are 2.6 times the EU average), securing long-lasting regulatory relief, and pursuing the solid money that Andrew Jackson pursued when he killed the second US central bank. Noteworthy, the portrait of Andrew Jackson, who Trump greatly admires, adorns the oval office.

12. America is some $68 trillion in debt when combining federal, state, corporate, and individual/family level debt. US GDP is nearly $20trn. Each one percentage point higher borrowing costs from abnormally low interest rates increases America’s cost of funding by roughly $680 billion p.a. (most debt, including the US government’s, is not long-term in nature, thus susceptible to higher refinancing costs if interest rates keep rising). In fact, if the average cost of borrowing rose by just two percentage points — say 10-year Treasuries yielded 4.8% — the US’s financing cost would quickly soar by $1.36 trillion or by 7% of GDP.

13. As we have stated and written, markets are reversion beyond the mean machines. And given the mountains of debt we have accumulated, both solvency and inflation risks (in terms of printing even much more money) suggest that we could easily have a 10-year Treasury that someday yields 7.8% or 8.8% — recall that we exceeded 15% during Volcker’s “tough love” in the early 80s with a fraction of the debt. Five percentage points higher funding costs than today would raise America’s aggregate borrowing cost by roughly $3.4 trillion p.a. from current levels, or by 17% of current GDP. A non-starter. Our point: given the huge indebtedness, relatively feeble manufacturing capacity, and income and debt constrained consumers, higher interest rates could easily choke off and even reverse the positive impact of lower tax rates because they are financed by yet more debt instead of through government spending cuts.

14. Sadly, too many of Trump’s policies will ultimately rely on the very printing press that has gotten us deeper and deeper into debt, into yield starvation, into huge misallocations, into cratering productivity growth, and into accelerating solvency risks and inflation risks. Inflation is the largest stealthy property thief for the average person, and especially for retired folks, who are dependent on a fixed income stream and bond investment returns.

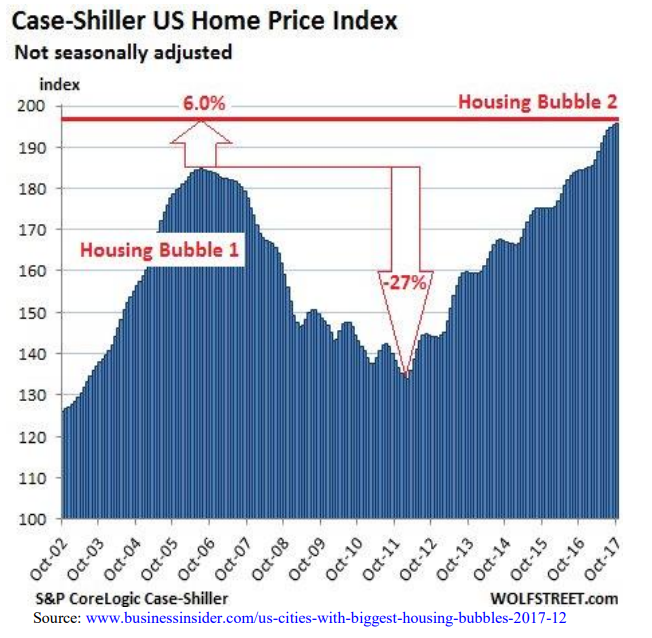

15. Year-over-year wage growth is 2.4% overall and but 2.2% in supposedly robust manufacturing while inflation is picking up, the housing bubble has eclipsed the 2006 highs, and mortgage rates are rising briskly — in short, housing is increasingly unaffordable for most Americans. In a related sense, we wonder how a 65-year low in the unemployment rate and low wage growth rates are possible at the same time?

16. The personal savings rate has plummeted to 2.4% from 5.9% two years ago as record auto loans ($1.1 trillion) and student loans ($1.5 trillion plus) suggest tapped out consumers. It also implies substantial demand has been borrowed from the future, i.e., that it won’t be there this year or next. If the “consumption function” is over 70% of GDP, this isn’t an academic issue.

And in the past when confidence soared and the savings rate collapsed, things did not end well…

via Zero Hedge http://ift.tt/2BiQjqS Tyler Durden

Amid a relentless barrage of doom and gloom – and then some more doom for good measure – establishment forecasts about the future of cryptocurrencies, including everyone from Goldman, to the BIS, to the World Bank, all of which have been some iteration on how cryptos have no future, this morning an unexpectedly objective and somber view on the future of bitcoin came from none other than the organization that prints (out of thin air) the nemesis to bitcoin: the Federal Reserve.

While the emphasis of the Q&A with New York Fed economists Michael Lee and Antoine Martin, which we have republished below, is the issue of “trust” and how it defines monetary exchange, there are several things that attracted our attention.

The first is the Fed’s take on what we have been saying since 2015, and the reason behind bitcoin’s original surge in 2015/2016, namely its use for illicit purposes:

The Drug Enforcement Administration reports a sharp decline in bulk cash smuggling in 2016, which is the traditional payment method for drug shipments and suggests that payments may have shifted toward cryptocurrencies. Cryptocurrencies are more convenient than cash for many illegal activities that now take place online.

… cryptocurrencies are ideal for circumventing legal or regulatory authorities, because they aren’t governed by any. China, which actively controls capital flow, banned banks from dealing with bitcoin in 2013 (this was relaxed later), because it was thought to be used for money laundering. North Korea is reportedly responsible for state-sponsored hacks to steal cryptocurrencies, which help bypass economic sanctions that are enforced through the cooperation of financial institutions and countries.

This – the ability to hide and store dramatic amount of wealth in a tiny space – is also the reason why according to Goldman cryptocurrencies are really cryptocommodities, as they are not backed by a monetary authority like the Fed. This what Goldman said earlier this week: “Unlike other storage commodities like oil, gold, platinum, diamonds, and even cash, there is no need to hold much physical material to own bitcoin; even a technology as obsolete as the 3½ inch floppy disk can hold almost 30,000 private keys. There is no theoretical upper limit to the value of bitcoins in a wallet, but if we assume each wallet secured by this disk contains as much as the largest wallet today (180,000 BTC), this single disk could “hold” all bitcoins in existence and remain less than 0.5% full. Assuming a bitcoin market cap of roughly $190bn (as of late January), this disk would be the equivalent to either: 95% of the 4,583 tons of gold in Fort Knox, or 1,344 Very Large Crude Carrier supertankers of oil.“

Next follows an exchange that many opponents of bitcoin have been leery to engage in, namely why does cryptos have value if they aren’t backed by anything. The Fed’s response – the admission that the dollar is in the same boat thanks to Nixon – is needless to say , surprising.

Q. If virtual currencies aren’t backed by anything real, gold or some other physical commodity, does that mean they all eventually will be worthless?

A. You’re right that they are not backed by a physical commodity, but then neither is the dollar and most other modern currencies. It’s long been known that currencies that are intrinsically worthless, mere pieces of paper, are recognized as valuable because payments with money are so much easier than the alternative, barter. The problem with barter, when everyone trades goods and services directly, is the dreaded “double coincidence of wants.” If I want to have dinner at my favorite restaurant but the cook is not interested in trading a meal for a bitcoin lecture, I have to keeping searching until I find a restaurant that I like where, coincidentally, the cook can’t hear enough about bitcoin.

Money, even intrinsically worthless paper money, cuts the “double coincidence” problem in half. I just need to find someone willing to pay me some of that paper for my lecture, then use that paper to pay for dinner. As long as I trust that someone will accept the paper, I’m willing to accept it in exchange for my lecture. It’s trust that the “worthless” piece of paper is actually worth something to other people that makes it an acceptable medium of exchange.

As a result, the price of bitcoin fluctuates with news that vendors or firms accept or decline bitcoin as a mode of payment. Late last year, bitcoin prices jumped after Square, a payments firm, was reported to be testing bitcoin. Wider adoption and acceptance of cryptocurrencies as a payment option naturally increases what they are worth.

All those points are rather spot on, and usually are remiss from the defense arsenal of some of the even staunchest bitcoin advocates.

What was most interesting, however, was the Fed’s observation under what conditions cryptos could not only match, but supplant fiat as the dominant currency. The answer: bitcoin would dominate payment methods in a dystopian world, in other words a “decentralized” world, in which there is no more faith – or trust – in central banks.

Which, of course, is the whole point behind cryptocurrencies in the first place: to replace the dollar, and other fiat currencies, once the entire fractional-reserve lending platform, and last 100 years of monetary philosophy are exposed to be a fraud.

“Lunacy” you say? Well, it’s a conversation worth having after the next market crash, one which most likely will wipe out what little faith remains in central banks, in fractional reserve lending, in conventional economics and in fiat.

Incidentally, this is precisely what Deutsche Bank’s chief credit strategist, Jim Reid, predicted would be the ultimate endgame: the extinction of fiat, and the return to hard, or alternative, currency.

Here is the Fed:

Q: So are cryptocurrencies the future of money?

Martin: It will ultimately depend on how well they compete with other, already established payment methods—cash, checks, debit and credit cards, PayPal, and others. Cryptocurrencies arguably solve the problem of making payments in a trustless environment, but it is not obvious that this is a problem that needs solving, at least in the United States and other advanced economies. And solving that problem creates others. One is scalability; the process of picking random validators takes time, is expensive, and consumes tremendous amounts of energy.

Another issue lately is extreme volatility in the value of cryptocurrencies which makes them less useful as currencies. This volatility is an inherent feature by design. Since there is no central bank that adjusts the supply of bitcoin to accommodate changes in demand, bitcoin’s value can swing sharply with demand. In a world where all things were priced in bitcoin, this would likely translate into massive swings in inflation and economic activity. In contrast, providing an “elastic” currency to promote financial and price stability is a goal shared by the Federal Reserve System, the European Central Bank, the Bank of Japan, and many other central banks.

The trust-proofing provided by cryptocurrencies also comes at the expense of another key feature of a payment method: convenience. If we lived in a dystopian world without trust, bitcoin might dominate existing payment methods. But in this world, where people do tend to trust financial institutions to handle payments and central banks to maintain the value of money it seems unlikely that bitcoin could ever be as convenient as existing payment means.

That said, bitcoin and other cryptocurrencies are trying to improve scalability and convenience so perhaps in the future one of these cryptocurrencies could realistically compete with current payment methods. But, fundamentally, we wonder whether a payment method designed to function where trust in institutions is completely absent can ever be as convenient as one where trust is required, but also already exists.

The punchline, again:

If we lived in a dystopian world without trust, bitcoin might dominate existing payment methods. But in this world, where people do tend to trust financial institutions to handle payments and central banks to maintain the value of money it seems unlikely that bitcoin could ever be as convenient as existing payment means.

Which begs the question: what happens when the “trust” dies? The answer, of course, is the very existence of cryptos: to create a world in which not one network is reliant on “trust” and the presence of a master node.

Here the Fed truly hits it on the head: in an environment of “trust” fiat is perfectly viable. It is what happens after, when the trust – in financial institutions, in central and commercial banks, in contract relationships – ends, whether the result of a global monetary collapse, a systemic market crash, or something else, that is the question.

Full note below (link)

Bitcoin and other “cryptocurrencies” have been much in the news lately, in part because of their wild gyrations in value. Michael Lee and Antoine Martin, economists in the New York Fed’s Money and Payment Studies function, have been following cryptocurrencies and agreed to answer some questions about digital money.

Q: Let’s start simply. What even is cryptocurrency?

Martin: Cryptocurrencies are digital, or virtual, money. Bitcoin, which was created in 2009, is the first and probably the best known cryptocurrency, but many others have followed, such as Ethereum, Ripple, Bitcoin Cash, Litecoin, etc.

Q: Do they have utility that other forms of money lack?

Lee: Like any functioning form of currency, cryptocurrencies facilitate payments between parties and provide a store of value. What’s special about them is that they can serve those roles even in environments where trust—or lack of trust—is a problem.

Trust is implicit for practically any means of payment. Say I need to buy groceries. If I pay with a personal check, the grocer has to trust that the check isn’t “hot” (that I own the account and it has sufficient funds). Common payment methods, like debit or credit cards, also entail a surprising degree of trust. The grocer and I have to trust the banks that connect us when I swipe, trust the payment system or “plumbing,” whereby funds flow from my account to the grocers.

Some of these problems go away with cash because when I hand cash to the grocer, there is no need for trusted intermediaries. But if you think about it, even cash requires some trust. The grocer has to believe that the cash I pay with will retain its value and not be eroded by inflation or confiscatory monetary reforms. So she needs to trust the central bank.

Q: Have cryptocurrencies made progress toward solving the problem of mistrust?

Martin: One important element in any payment system is “validation,” determining which transactions can proceed through the system and which should be refused as invalid. For example, a validator could check if there are sufficient funds in the account of the person who wants to make a payment. If there is, the payment will go through. But if there isn’t, the payment will be refused. If you recall the last time you swiped your credit or debit card, the few seconds you had to wait was that validation. But if the merchant doesn’t trust the validator, and doubts she will ultimately be paid, she’s unlikely to accept your card.

With bitcoin there isn’t one designated validator. Instead, everybody in the bitcoin network could be picked, essentially at random, to validate recent transactions. The details are a bit technical and more details can be found in a recent St. Louis Fed paper on cryptocurrencies.

Q: Aren’t cryptocurrencies sometimes associated with illicit activities?

Lee: Definitely, and this is likely related to trust also. Criminals, who typically use cash for the anonymity and security it provides, may be moving to cryptocurrencies. The Drug Enforcement Administration reports a sharp decline in bulk cash smuggling in 2016, which is the traditional payment method for drug shipments and suggests that payments may have shifted toward cryptocurrencies. Cryptocurrencies are more convenient than cash for many illegal activities that now take place online. In 2013, following a government crackdown on Silk Road—an online marketplace that was used to trade illegal goods—bitcoin prices plunged. And for good reason too.

More broadly, cryptocurrencies are ideal for circumventing legal or regulatory authorities, because they aren’t governed by any. China, which actively controls capital flow, banned banks from dealing with bitcoin in 2013 (this was relaxed later), because it was thought to be used for money laundering. North Korea is reportedly responsible for state-sponsored hacks to steal cryptocurrencies, which help bypass economic sanctions that are enforced through the cooperation of financial institutions and countries.

Earlier, we talked about how a currency requires people to trust in its value. When Greece fell deeper into financial distress in 2015, Greek interests and trading in bitcoin rose quickly amidst fears of capital controls and the possibility of exiting the eurozone. Bitcoin became attractive as trust eroded.

Q: If virtual currencies aren’t backed by anything real, gold or some other physical commodity, does that mean they all eventually will be worthless?

Lee: You’re right that they are not backed by a physical commodity, but then neither is the dollar and most other modern currencies. It’s long been known that currencies that are intrinsically worthless, mere pieces of paper, are recognized as valuable because payments with money are so much easier than the alternative, barter. The problem with barter, when everyone trades goods and services directly, is the dreaded “double coincidence of wants.” If I want to have dinner at my favorite restaurant but the cook is not interested in trading a meal for a bitcoin lecture, I have to keeping searching until I find a restaurant that I like where, coincidentally, the cook can’t hear enough about bitcoin.

Money, even intrinsically worthless paper money, cuts the “double coincidence” problem in half. I just need to find someone willing to pay me some of that paper for my lecture, then use that paper to pay for dinner. As long as I trust that someone will accept the paper, I’m willing to accept it in exchange for my lecture. It’s trust that the “worthless” piece of paper is actually worth something to other people that makes it an acceptable medium of exchange.

As a result, the price of bitcoin fluctuates with news that vendors or firms accept or decline bitcoin as a mode of payment. Late last year, bitcoin prices jumped after Square, a payments firm, was reported to be testing bitcoin. Wider adoption and acceptance of cryptocurrencies as a payment option naturally increases what they are worth.

Q: So are cryptocurrencies the future of money?

Martin: It will ultimately depend on how well they compete with other, already established payment methods—cash, checks, debit and credit cards, PayPal, and others. Cryptocurrencies arguably solve the problem of making payments in a trustless environment, but it is not obvious that this is a problem that needs solving, at least in the United States and other advanced economies. And solving that problem creates others. One is scalability; the process of picking random validators takes time, is expensive, and consumes tremendous amounts of energy.

Another issue lately is extreme volatility in the value of cryptocurrencies which makes them less useful as currencies. This volatility is an inherent feature by design. Since there is no central bank that adjusts the supply of bitcoin to accommodate changes in demand, bitcoin’s value can swing sharply with demand. In a world where all things were priced in bitcoin, this would likely translate into massive swings in inflation and economic activity. In contrast, providing an “elastic” currency to promote financial and price stability is a goal shared by the Federal Reserve System, the European Central Bank, the Bank of Japan, and many other central banks.

The trust-proofing provided by cryptocurrencies also comes at the expense of another key feature of a payment method: convenience. If we lived in a dystopian world without trust, bitcoin might dominate existing payment methods. But in this world, where people do tend to trust financial institutions to handle payments and central banks to maintain the value of money it seems unlikely that bitcoin could ever be as convenient as existing payment means.

That said, bitcoin and other cryptocurrencies are trying to improve scalability and convenience so perhaps in the future one of these cryptocurrencies could realistically compete with current payment methods. But, fundamentally, we wonder whether a payment method designed to function where trust in institutions is completely absent can ever be as convenient as one where trust is required, but also already exists.

via Zero Hedge http://ift.tt/2sla7H1 Tyler Durden

XIV’s ramp into the open offered some hope, but just like yesterday, that hope is gone as stocks tumble back into the red and below yesterday’s lows…

XIV is fading…

Rate spiked back above 2.85%…

And so stocks faded back into the red…

Futures show the same trend yesterday…

via Zero Hedge http://ift.tt/2FXh1UX Tyler Durden

Interest-rates going up “for the right reason” is bullish, right?

Each time interest rates have surged up to their long-term trendline, a ‘crisis‘ has occurred…

h/t @IncomeDisparity

But this time is different right? Because rates are “going up for the right reason.”

Hhmm, the reaction in markets each time the yield on the 10-Year Treasury yield reaches its trendline is ominous…

So the question is – have interest rates ‘ever’ gone up for the right reason?

Or is this narrative just one more bullshit line from a desperate industry of asset-gatherers and commission-takers?

It does make one wonder what the relationship between US government ‘interest costs’ and global money flow really is. Does an engineered equity tumble spark safe-haven-buying and ease the pain as deficits and debt loads soar. It would certainly help as $300bn additional budget deals are passed, The Fed has left the game, and China is threatening to be a seller not a buyer…

via Zero Hedge http://ift.tt/2C8LNrN Tyler Durden

Authored by Guy Benson via Townhall.com,

We’ll bring you Wall Street Journal columnist Kimberly Strassel’s tweetstorm in a moment, but I’ll take a stab at answering her question about the media right out of the gate.

Three possibilities:

(1) The GOP hyped the Nunes memo, which quickly became the center of this whole firestorm — replete with counter-memos, FBI objections, etc. The press followed the spotlight.

(2) As we’ve been saying, there are so many complex pieces of this larger puzzle, following the plot is difficult. It’s not just news consumers wondering, “which memo is this now?” — it’s many of the people trying to cover this drama, too. The document in question here is a second, less redacted, version of a Senate memo that few people have even heard of.

(3) The Senate memo, produced by non-bomb-throwers Chuck Grassley and Lindsey Graham, is substantially more disruptive to the Democrats’ narrative than the Nunes document. And the press generally prefers Democratic narratives to Republican ones because most journalists are liberals.

My guess is that some blend of all three factors helps explain why the Grassley/Graham memo has barely registered on the national radar, even after we’ve endured multiple high-octane news cycles starring Nunes and Schiff. But on the substance, does Strassel have a point, or is this just the latest shiny object the right-wing is waving around to distract from “the real story,” now that the Nunes memo was arguably a bit of a dud? Here’s her case:

1) Why isn’t the (mostly) unredacted Grassley memo front page news? Here’s why: Because it confirms the Nunes memo and blows up the Schiff talking points (which the media ran with).

— Kimberley Strassel (@KimStrassel) February 7, 2018

2)It is confirmation that the FBI’s FISA application relied on the dossier and a news article, and worse, on the credibility of a source in the employ of the Clinton campaign.

— Kimberley Strassel (@KimStrassel) February 7, 2018

3) It is proof that the FBI did not tell the Court the extraordinarily partisan provenance of the dossier.

— Kimberley Strassel (@KimStrassel) February 7, 2018

4) It provides evidence that the FBI presented the FISA Court with materially false evidence, in the claim that Steele had not talked to the press. And then shows that even after Steele admitted under oath that he had, the FBI did not tell the FISA Court in its renewal.

— Kimberley Strassel (@KimStrassel) February 7, 2018

5) It provides evidence that Steele was getting information from the Clinton team itself! Via the State Department! So now, not only do we have a dossier based on unnamed shady Russians, but on Sidney Blumenthal. How much of this was engineered by the Clinton campaign from start?

— Kimberley Strassel (@KimStrassel) February 7, 2018

Does that all of check out? Allahpundit digs into the document (a much more redacted version had been released previously) and seems to agree that Grassley/Graham is a significantly bigger deal than Nunes. In our analysis of the latter document last week, we wrote that a major question was how much the DOJ relied on the Steele dossier itself to gain a FISA warrant against former Trump adviser Carter Page. According to Grassley/Graham, the answer is a lot. I posited that if investigators had used the unverified dossier as a starting point from which to chase down leads and produce more solid evidence to present to a FISA judge, that’d be one thing. But if they leaned heavily on Steele’s file itself as the “evidence,” that would be sketchier. According to the two GOP Senators, the FBI did the latter. From AP’s excellent summary (the relevant bits of the memo itself are here and here):

…“The bulk of the application” against Page was dossier material…

“The application appears to contain no additional information corroborating the dossier allegations against Mr. Page.”

In other words, they seem to have treated the dossier as evidence, not as a lead. That’s big news.

But that’s not all. Grassley/Graham allege, based on intelligence, that the man behind the anti-Trump dossier was known to be unreliable by the FBI (they eventually severed ties with him) because he was caught lying either to US law enforcement or to British courts, telling each entity different stories about a key fact. Either way, FISA judges who approved and renewed the Page warrants weren’t told about the proven unreliability of the foreign agent whose work product was (apparently) the central basis for said warrants. The FBI might counter that Steele seemed credible at first, then they dumped him when he burned them, but that doesn’t mean their hands are clean, Allahpundit writes:

(a) that doesn’t solve the problem that the original FISA application against Page evidently relied “heavily” on information passed from a not-very-credible foreign agent and

(b) that doesn’t explain why the Bureau allegedly failed to tell the FISA Court in later applications to renew their surveillance of Page that Steele’s info maybe hadn’t been so credible…Grassley and Graham make another good point about Steele’s chattering to the press while his investigation was still ongoing: Once bad actors were aware that he was digging for dirt on Trump, they could have sought him out and fed him any amount of BS in hopes of it trickling through to the FBI and deepening the official suspicion surrounding Team Trump. That’s how Clinton cronies — maybe even Sid Blumenthal — got involved in this clusterfark. Because Steele was supposedly willing to accept even unsolicited tips about Trump, the Clinton team may have fed him rumors to help fill a dossier for which their boss was paying.

Two big points there:

Even after the FBI recognized Steele was an established liar, his dishonesty was not disclosed to judges deciding whether to keep the warrants active during renewal applications, which were largely predicated on Steele’s credibility.

And the topic about which he apparently lied was whether he blabbed to folks in the media about his work, which could have opened up the floodgates for disinformation from shady characters eager to make the anti-Trump case as juicy and brimming with salaciousness as possible.

That’s where Blumenthal and company, whom I wrote about here, may have come in. What a mess. Also, speaking of not revealing pertinent information to the courts, it looks like Nunes was technically incorrect that the judges weren’t made aware that the Steele dossier was paid political oppo research. But he was more broadly correct that the judges didn’t have even close to the full picture of who was behind the unverified partisan document upon which they were primarily basing the surveillance of a US citizen — who happened to be a former aide to a major presidential campaign from the out-of-power party.

“As Nunes himself later admitted, the Bureau apparently did disclose in a footnote that the material was paid political research. It just didn’t mention who, precisely, had paid for it,” AP writes. The memo reads, “in footnote 8, the FBI stated that the dossier information was compiled pursuant to the direction of a law firm that had hired an “identified US person” — now known as Glenn Simpson of Fusion GPS…the application failed to disclose that the identities of Mr. Simpson’s ultimate clients were the Clinton campaign and the DNC.”

So the disclosure came in a footnote and didn’t mention that the parties who paid for the unverified dossier were the Trump campaign’s explicit opposition. Maybe there was no misconduct in any of this, but even as someone who believes neither that suspicion of Carter Page was unreasonable, nor that this is all part of a grand anti-Trump conspiracy (remember, the Trump angle of the Russia probe started earlier, for an unrelated reason), there’s enough in the Grassley/Graham memo to make me uncomfortable with the standards by which Page was surveilled by the US government.

via Zero Hedge http://ift.tt/2C8ouy6 Tyler Durden

Despite reassurances from Goldman’s Jeffrey Curries that global demand is “rock solid,” it appears anxiety over US shale production, rising inventories, and questions over OPEC’s deal extensions (as well as insanely extreme long speculative positioning) has sparked significant weakness in oil prices…

Despite the selloff in equities and oil markets, fundamentals “are very much intact,” Jeffrey Currie, global head of commodities research at Goldman Sachs, says in comments on Bloomberg TV and radio.

Global financial markets are “getting a taste of” what oil market saw last year with corrections.

But WTI is back with a %59 handle for the first time since 2017…

Another leg of the stool just broke?

via Zero Hedge http://ift.tt/2sjqnID Tyler Durden

The House managed to approve a purportedly “bipartisan” budget deal early this morning after a marathon all-night session that was brought on by Sen. Rand Paul’s self-indulgent insistence that he needed to “make a point” about excessive government spending…less than two months after he voted to blow out the deficit with the Trump tax plan…

But now that the massive 600+ page bill has been passed, what, exactly, is in it?

For starters, it includes increases in both defense and non-defense spending…

…which will raise the annual deficit to $1.2 trillion, leading to even higher 10Y yields at least until the next recession hits…

Some highlights from the deal include:

Raises Spending Levels

The deal would increase government spending by nearly $300 billion over two years. It would increase discretionary defense spending by $165 billion over the spending caps that have been in place since the 2011 Obama-era budget ceiling battle left us with sequestration.

Non-Defense Spending

The $131 billion hike in non-defense spending would include $20 billion for infrastructure spending and $6 billion to combat opioid abuse and other mental health crises that President Donald Trump has promised to deliver, but has until now been reluctant to do anything aside from label the abuse epidemic a national health emergency.

Debt Ceiling

In one of the deal’s key components for markets, an extension of the government’s debt ceiling to March 2019 is one of the most pressing issues – even perhaps more pressing than the shutdown because of its potential to impact the US’s credit rating (remember when the US was downgraded AA+ and how markets reacted?). The Treasury Department has warned that without an extension in borrowing authority by Congress, the government would run out of its “emergency measures” early next month.”

Temporary Funding Measure

Since they’ve agreed to toss the caps, lawmakers’ and their staff need to set to work on actually drafting a two-year budget.

That could take weeks, so the bill also includes a temporary extension of funding to March 23. After that, Congress will need to approve an appropriations bill to pass a two-year budget.

Disaster Assistance

A disaster aid package of $90 billion for areas affected by Hurricanes Irma, Harvey and Maria, as well as the California wildfires, will also be included.

Immigration

Immigration legislation was famously not included in the deal expressly because of its divisiveness. Senate Majority Leader Mitch McConnell has said the Senate will begin debating immigration legislation next week. House Democratic leader Nancy Pelosi delivered a marathon, eight-hour speech earlier this week about young “Dreamer” immigrants in an attempt to extract the same promise from Ryan, who has refused to explicitly commit to a vote without the president’s OK.

Those are the obvious provisions. But, as is typical of Washington, where lawmakers are often judged by their ability to deliver lucrative projects and other federal-government goodies to their state, the bill contains many surprising provisions, including tax incentives that were scrapped as part of the tax overhaul, as the New York Times points out.

It also includes a series of unexpected spending increases, including restoring some provisions that were jettisoned from last year’s $1.5 trillion tax package. And the bill includes an extension of 48 different tax credits that expired at the end of 2016, including several incentives meant to help particular sectors like mining and horse racing.

Here are some of the provisions:

Medicare Cost Watchdog Removed

The bill would kill the Independent Payment Advisory Board, which was devised to help keep Medicare spending growth from rising above a set level. No one has ever been appointed to the board, and Medicare spending has experienced unusually slow growth in recent years. But the board was long denounced by Republicans as a rationing board, and disliked by some Democrats for taking payment policy authority away from Congress.

Funding Changes for Public Health Programs

The spending plan would cut $1.35 billion in funding to an Affordable Care Act program meant to improve public health and prevention funding for states and municipalities

Another CHIP Extension

The bill would extend funding for the popular children’s health-care program for four years.

Continued Fund For Abstinence Education

Rubbers are baaaaad m’kay?

A Break for Berea College

The spending bill restores a provision that was stripped out of the tax bill after becoming the center of controversy. The bill would exempt Berea College, a small private college in Kentucky that provides free tuition, from being subject to a new tax.

* * *

Of course, all of this won’t mean anything if Congress can’t push through the appropriations bill that – we hope – lawmakers are furiously setting to work upon as we write…

via Zero Hedge http://ift.tt/2slijab Tyler Durden

It appears the Cboe’s conference call last night – to explain how they are not dependent on crazed VIX-structure traders – did not work…

As we detailed last night, as the 4:30 ET call began, Ed Tilly, the CEO of Cboe, hopped on an analyst call Wednesday afternoon to dispel certain “misconceptions” about the events of Monday, which left many retail traders totally wiped out and forced the liquidation of one popular short-VIX ETF.

Questions and misconceptions – it’s largest single day increase on record. This is important because VIX continued to function as did the ETPs connected to it.

During the unprecedented surge, VIX and VIX-related ETPs continued to work as designed, said Tilley. Funds that were long volatility benefited, while those who were short suffered, Tilly said.

Of course, as we’ve noted in the past, there were formerly $22 trillion across all trading strategies and asset classes piled into the short volatility trade.

Products and strategy designed to respond to low volatility prove to be effective tools as volatility increased. This is in no way to minimize the impact this had on investors, Tilly said, but to take a step back ad look at the broader market implications.

“Trading in our products was orderly and liquid, and they overall worked as designed,” Tilley said.

Furthermore, he framed the selloff as “an opportunity to educate investors about how to trade volatility products.”

“The period that we’ve been trading, 2018, has been marked by a trend toward investors putting on larger positions in these products, presumably because the short volatility trade has been profitable these past few years,” Tilley said.

I think short vol has been around since options and derivatives were listed, and will continue to be an active strategy despite the events of this week.

After all, institutional traders have plenty of other options or shorting volatility, from buying put options to shorting long-VIX ETPs, some of which might find renewed interest.

In summary, the massive short-vol position has taken a massive hit – but its far from dead.

CBOE is now down around 30% from its highs and back at its lowest since August 2017…

via Zero Hedge http://ift.tt/2EVru49 Tyler Durden

Despite headline month-over-month data beating expectations, year-over-year growth in Wholesale Sales and Wholesale Inventories slowed notably.

Wholesale Inventories rose 0.4% MoM in December, better than the expected 0.2% growth and preliminary print but below November’s 0.6% growth.

Wholesale Sales rose 1.2% MoM in December, better than the expected 0.4% growth and preliminary print but well below November’s upwardly revised 1.9% growth.

However, on a YoY basis, things were notably weaker.

This is the 3rd monthly decline in annual inventory growth and the biggest slowdown in annual wholesale sales since June.

via Zero Hedge http://ift.tt/2nYzj0u Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}