A new alarming parallel between today’s eviction crisis and the sub-prime mortgage crisis which helped spur the Great Recession has surfaced. The economy is sending warning signs to those who choose to take heed.

The eviction crisis is worsening to the point that Georgia State University authors feel that protections should be put in place to safeguard renters, such as longer eviction notices and legal protection, according to Market Watch. However, that could make the crisis much worse by homeowners simply refusing to rent their properties out at all. More government intervention (whether it’s designed to protect people or not) will only make a very bad situation worse.

Evictions have become a real visible effect of the volatility in today’s economy. Stable housing is increasingly out of reach for many Americans, as both rentalsand homes to own grow more expensive, options dwindle, and wages remain stagnant. But some scholars at Georgia State University, in conjunction with a ProPublica journalist, completed a new study which shows that not all evictions are created equal.

The researchers who conducted the study examined “serial” eviction filings (those done repeatedly by a landlord against a tenant). By comparing serial evictions to ordinary ones, the researchers found patterns of landlord “behavior and intentions”, some of which are reminiscent of the worst of the housing crisis a decade ago.

Similarly to the foreclosure crisis that foreshadowed the Great Recession in 2009, there appears to be a race element that needs to be discussed. Evictions are currentlydisproportionately hitting African-Americans. Black women in Milwaukee, for example, were evicted at a rate three times their share of the population, and black renters in metro Seattle were evicted four times as frequently as whites there, according to earlier research. This data bears mentioning, but keep in mind, that there’s no reasoning behind the whys of these evictions. If people aren’t paying rent, they will and should be evicted especially if a contract is signed.

“Filings can be the beginning of a forced removal process, but they are also frequently a tool used to enforce the collection of rent and fees,” the researchers noted. Which is incredibly fair, when taking emotion out of the equation. A contract is a contract, but this eviction crisis is a symptom of the larger problems with the economy rather than the media hyped narrative of “the rich are keeping the poor down” which was basically the conclusion of the Georgia State University study.

Protecting oneself and one’s family against eviction is usually as simple as having an emergency fund. If you can, save up three to six months worth of expenses so that in the event of an emergency or decrease in income, you will not be breaking your contract (which is your word you signed off on) with a homeowner who has agreed to let you live in a home they own in exchange for a monthly fee (called rent.)

Saving can seem like a daunting task, but if you buckle down when times are good, a catastrophic emergency becomes nothing more than an inconvenience.

via ZeroHedge News https://ift.tt/2UkqRLp Tyler Durden

US-backed self-declared “Interim President” Juan Guaido has been barred from holding public office in Venezuela for 15 years by the Maduro government, Reuters reports, citing Caracas officials.

Venezuelan state comptroller Elvis Amoroso in public statements on Thursday said it was the maximum punishment allowable by law, and charged that Guaido had “inconsistencies in his personal financial disclosures and a spending record that did not match his level of income,” according to Reuters.

Image source: Getty

After the shock announcement it remained unclear what this means in terms of Guaido’s immediate fate as majority leader of the National Assembly.

Crucially Guaido’s being banned from public office came less than 24 hours after the opposition leader announced plans for his supporters to launch “tactical actions” starting next week as part of his “Operation Freedom” to overthrow President Nicolas Maduro.

He began publicly referencing the plan earlier this month at opposition rallies and described it as a “full-fledged revolution in all states of Venezuela simultaneously.”

¡Atención!

Anunciamos el inicio de la fase preparatoria de la #OperaciónLibertad para lograr el cese de la usurpación. Llegó el momento de la organización, la movilización y la estrategia para liberar a Venezuela.

This has even included talk of “Operation Freedom” operatives and mass protesters ultimately marching on the Miraflores presidential palace – home to President Maduro.

Tweeting with the hashtag #VamosOperaciónLibertad, Guaido further appealed to “constitutional forces” within the Venezuelan army to rise up and switch loyalties.

Washington’s very overt promotion of Guaido as “legitimate” leader of Venezuela has resulted in threats from Maduro himself to have Guaido arrested. White House efforts to ramp up pressure on Maduro included hosting a delegation headed by Guaido’s wife, Fabiana Rosales, at the White House on Thursday.

“Eighty percent of the population in Venezuela has no power. They are trying to break our morale,” Venezuela’s new Interim First Lady said at the White House today. “But let me tell you that there is light, and the light is here.”

Notably the White House called Rosales “Venezuela’s new Interim First Lady” in statements related to the event.

No doubt, Caracas is now sending its own firm message in banning Guaido for public office for 15 years, something sure to result in a swift US reaction.

via ZeroHedge News https://ift.tt/2HYZoYZ Tyler Durden

The Federal Reserve is an often misunderstood entity, not only in the mainstream, but also in alternative economic circles. There is this ever pervasive fantasy on both sides of the divide that the central bank actually “cares” about forever protecting the US economy, or at least propping up the US economy in an endless game of “kick the can”. While this might be true at times, it is not true ALL the time. Things change, agendas change, and sometimes the Fed’s goal is not to maintain the economy, but to destroy it.

The delusion that the Fed is seeking to kick the can is highly present today after the latest Fed meeting in which the central bank indicated there would be a pause in interest rate hikes in 2019. As I have noted in numerous articles over the past year, the mainstream media and the Fed have made interest rates the focus of every economic discussion, and I believe this was quite deliberate. In the meantime, the Fed balance sheet and its strange relationship to the stock market bubble is mostly ignored.

The word “capitulation” is getting thrown around quite haphazardly in reference to the Fed’s tightening policy. And yet, even now after all the pundits have declared the Fed “in retreat” or “trapped in a Catch-22”, the Fed continues to tighten, and is set to cut balance sheet assets straight through until the end of September. Perhaps my definition of capitulation is different from some people’s.

One would think that if the Fed was in retreat in terms of tightening, that they would actually STOP tightening. This has not happened. Also, one might also expect that if the Fed is going full “dovish” that they would have cut interest rates in March instead of holding them steady at their neutral rate of inflation. This has not happened either. In fact, I’m not exactly sure how anyone can claim with a straight face that the Fed has given up on Quantitative Tightening (QT). Despite the many assumptions out there that the Fed is going to reverse on interest rates, I believe this is wishful thinking and that the Fed will not reverse rates in 2019.

What I do see is the Fed using rhetoric and head fakes to give the impression that they plan to go dovish in the future. And, this is being wrongly interpreted as the Fed being dovish now. But why is the Fed doing this while also continuing to dump its balance sheet? In my view, it is because they are almost finished with the task they set out to accomplish with QT in the first place, and they now have to make it appear as though they want to accommodate as the system breaks down.

In my article ‘Party While You Can – Central Bank Ready To Pop The Everything Bubble’, I outlined a process or tactic which the Fed has used on many occasions in the past: The creation of economic bubbles through inflation and artificially low interest rates, followed by abrupt tightening and higher interest rates into economic weakness. This tactic is highly effective in accomplishing ONE GOAL – financial collapse.

It is the same strategy the Fed used at the beginning of the Great Depression. It is also what the Fed used to trigger the crash of 2008. And, in 2018-2019, the Fed is doing it again.

For over two years now the Fed has been instituting tightening measures after inflating perhaps the largest economic bubble in modern history, also known as “the everything bubble”. The Fed did this despite extreme weakness in economic fundamentals, and is continuing forward until the fourth quarter of this year despite nearly every sector of the economy showing steep declines or a greatly reduced pace of growth.

It is perhaps not a coincidence that the Fed announced it would be cutting assets until September just as the Treasury Yield curve inverted for the first time since 2007. The same thing happened just before the crash and recession that started in 2008. An inverted yield curve is generally a sure sign of a decelerating economy or recession/depression.

What bewilders me are the numerous claims in the mainstream and alternative media that the Fed is somehow oblivious to what it is doing. This is simply not true. Jerome Powell in his statements in the Fed Minutes of October 2012 explains plainly exactly what would happen if and when the Fed tightened policy into weakness. He essentially admits that a crash will occur.

Four years later in the wake of the Trump presidency, Powell somehow conveniently finds himself the Chairman of the Fed, and what does he do? He tightens policy into economic weakness fully aware of what would happen next. I’ll repeat this point again because I don’t think some analysts out there get it: The central bankers KNOW that they are causing a crash. They are doing it deliberately. The question we need to ask is, why?

Over the past ten years the Fed may have acted as a crutch for markets, but this was not their true goal. Rather, the 2008 credit bubble collapse was used by the bankers as a rationale to create an even bigger bubble; a bubble that now encompasses every aspect of our financial structure. QT was needed to pop this bubble, and so the Fed tightened.

For many months now the Fed has stated that the US economy is “strong” and “in recovery” despite the evidence at hand. In March, they did not reverse tightening; they only admitted in an indirect way that the economy is not in recovery. They have until September to finish using QT for a controlled demolition of the Everything Bubble. This is more than enough time.

As noted in recent articles, US housing, autos, credit, retail, and even employment are faltering, while prices in most necessities remain high or are climbing. All that is left is for stock markets to follow the fundamental indicators down (as they usually do). This trend started at the same time as the Fed’s tightening began. All that was needed to set the avalanche in motion were moderate rate hikes and asset cuts.

The timing of the current crash is perfect for the banking elites for a number of reasons. Most importantly, they now have a scapegoat to pin the crash on in the form of “populist movements”. I warned about this ploy way back in early 2016 before the Brexit vote and the presidential elections. It is the reason why I predicted the Brexit vote would succeed and that Donald Trump would be president. The elites needed someone to blame for the collapse of the everything bubble they have been planning for the past 10 years.

The Brexit has turned into a three ring circus, a major distraction from the ultimate intended end game which I have long believed will be a “no deal” scenario. A no deal event is being painted in the mainstream media as a kind of economic doomsday for Europe, and I believe it will be, but not for the reasons they describe. Europe has been set up for a fall, just like the US, for many years now. Government and corporate debt levels are at extreme highs and major banks in Germany and Italy are on the verge of implosion.

A hard Brexit is useful to the elites as a scapegoat for a crash that was going to happen anyway.The bankers don’t plan on facing the music, they want “populist” groups to get the blame.

Trump has been a very effective ally to the banking class. After loading his cabinet with these “swamp creatures”, he then went on to take full credit for the very stock market rally he originally criticized during his campaign as a fraudulent bubble created by central bank stimulus. Then, he started a trade war which has dragged on for many months. It has shown no signs of slowing, and, is providing excellent cover for the Fed as it pulls the plug on life support for the economy.

Trump’s exoneration in terms of the Mueller probe and the Russiagate farce was easy to see coming. I have been saying for the past two years that Trump will never be impeached (or never impeached successfully) exactly because the banking elites WANT him right where he is. Russiagate was meant to drive leftists even further into extremism, it was NOT meant to unseat Trump.

If the markets were to tank this year (in January I predicted they would retest December lows starting at the end of March through April), then Trump would get total credit in the mainstream for the crisis and the Fed would avoid the majority of the blame.

Once again, lets consider the timing of current events – The Fed is tightening until September but pretending as if it is backing off. The yield curve has inverted. Major fundamentals are dropping exponentially. At the same time, we have Europe on the verge of a fabricated crisis in the form of a potential no deal Brexit, and we have US trade negotiations which have been delayed once again, perhaps until June, maybe longer.

I don’t believe in the “perfect storm” as a matter of coincidence, but I do believe according to the evidence that perfect storms can be deliberately engineered. Bottom line, no matter what the mainstream says in the coming months, the Fed knew what it was doing.

There are many advantages to an engineered crash. As noted, it was going to happen eventually anyway. It is simply delusion to think that the central bank can prop up the system forever. We sometimes hear the claim that this was done in Japan, but the Fed increased its balance sheet to $4.5 Trillion dollars in the span of two years – it took the Bank of Japan decades to get to the same level. There comes a point in which stimulus and increased debt provides diminishing returns when trying to hide economic weakness, and the Fed has already hit that point.

The Fed is crashing the system now because they have sovereignty activists and nationalists to point the finger at. They are also crashing the system now because the everything bubble is at its peak. Corporate and consumer debt are at historic highs, and the bankers are looking to cause maximum damage. Finally, the banking establishment has loyalties to certain agendas which are far outside national interests, including the often mentioned Agenda 2030 and the “global economic reset”. These agendas call for greatly increased global centralization of economic power as well as geopolitical power; in other words, global governance.

No matter what the mainstream media says over the course of this year, I want readers to remember that this was a disaster at least ten years in the making. It is not something that suddenly fell out of the sky. It was not something that was unexpected or unpredictable. It was highly predictable to those with the eyes to see. It was NOT a mistake.

* * *

If you would like to support the work that Alt-Market does while also receiving content on advanced tactics for defeating the globalist agenda, subscribe to our exclusive newsletter The Wild Bunch Dispatch. Learn more about it HERE.

via ZeroHedge News https://ift.tt/2FBI1L5 Tyler Durden

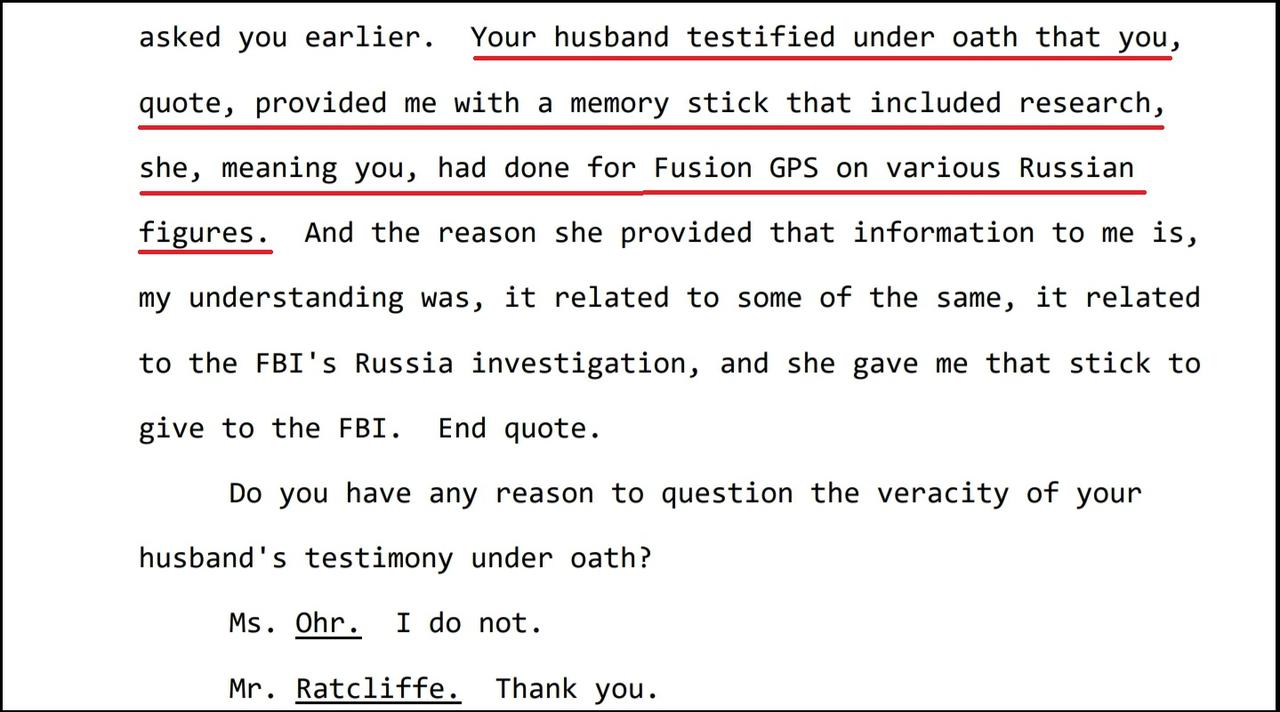

The wife of former Justice Department #4 official Bruce Ohr conducted extensive opposition research on Trump family members and campaign aides while working for Fusion GPS – the firm paid by the Clinton campaign to produce a ‘salacious and unverified’ Russian-sourced dossier which would later be used against Trump and his campaign.

(Getty Images; AP; The Epoch Times; Photo illustration by The Epoch Times

According to a newly released transcript of Nellie Ohr’s closed-door Congressional testimony, Ohr – who speaks fluent Russian, explored relationships between then-candidate Donald Trump and Russian organized crime, according to Fox News.

“I was asked to research Trump’s family broadly in connection with any—any Russian connections,” Ohr stated, adding that she “did some research on all of them, but not in much depth.”

Ohr explained that she researched Donald Trump Jr. and Ivanka Trump, specifically their “travels.”

She added that she was looking “to see whether they were involved in dealings and transactions with people who had suspicious pasts, or suspicious types of dealings.” –Fox News

Also interesting from the transcripts is that Nellie passed Bruce research she had done for Fusion GPS on a memory stick.

Nellie Ohr was also tasked with researching former Trump campaign chairman Paul Manafort, former campaign aide Carter Page, and former national security adviser Michael Flynn – who had relationships in both Russia and Turkey. Earlier this year the Daily Caller revealed portions of Ohr’s committee interview, but the transcript was only made available Thursday.

Ohr worked with Fusion GPS between October 2015 and September 2016. She also admitted during testimony that she favored Hillary Clinton as a candidate, and would have been less comfortable researching her Russia ties (P. 105).

In 2010, she represented the CIA’s “Open Source Works” group in a 2010 “expert working group report on international organized crime” along with Bruce Ohr and Fusion GPS founder Glenn Simpson.

Nellie Ohr, the wife of demoted DOJ official, Bruce Ohr, not only worked for Fusion GPS, but has also represented the CIA’s “Open Source Works” group. https://t.co/u5HPgJwvWdpic.twitter.com/ZPhAIzR6wv

Meanwhile, some have wondered if Nellie’s late-life attraction to Ham radios was in fact a method of covertly communicating with others about the Trump-Russia investigation, in a way which wouldn’t be surveilled by the NSA or other agencies.

was Nellie Ohr’s late-in-life foray into ham radio an effort to evade the Rogers-led NSA detecting her participation in compiling the Russian-sourced Steele dossier? Just as her husband’s omissions on his DOJ ethics forms raise an inference of improper motive, any competent prosecutor could use the circumstantial evidence of her taking up ham radio while digging for dirt on Trump to prove her consciousness of guilt and intention to conceal illegal activities. –The Federalist

Bruce Ohr was demoted twice after the DOJ’s Inspector General discovered that he lied about his involvement with Simpson – who employed dossier author and former British spy, Christopher Steele.

Last August, emails turned over to Congressional investigators revealed that Steele was much closer to the Obama administration than previously disclosed, and his DOJ contact Bruce Ohr reported directly to Deputy Attorney General Sally Yates – who approved at least one of the FISA warrants to surveil Trump campaign aide Carter Page.

Steele and the Ohrs would have breakfast together on July 30, 2016 at the Mayflower Hotel in downtown Washington D.C., while Steele turned in installments of his infamous “dossier” on July 19 and 26. The breakfast also occurred one day before the FBI formally launched operation “Crossfire Hurricane,” the agency’s counterintelligence operation into the Trump campaign.

Bruce Ohr was a key contact inside the Justice Department for ex-British spy Christopher Steele, who authored the anti-Trump dossier, which was commissioned by Fusion GPS and funded by the Hillary Clinton campaign and the Democratic National Committee through law firm Perkins Coie.

The FBI relied on much of Steele’s work to obtain Foreign Intelligence Surveillance Act (FISA) warrants against the Trump campaign—specifically Carter Page, redacted versions of the FISA warrants released last year revealed. –Fox News

On Monday, Senate Judiciary Committee Chairman Lindsey Graham (R-SC) announced that his panel would do a “deep dive” into the “other side” of the Trump-Russia investigation. He also called for the appointment of a new special counsel to look into abuse between the DOJ and Obama administration while investigating Donald Trump and his campaign.

On Wednesday, Trump vowed to release the full and unredacted FISA warrants and other documents that the FBI used to surveil his campaign and Page.

“I have plans to declassify and release. I have plans to absolutely release,” Trump said during a Tuesday night interview on Fox‘s “Hannity.”

“I have some very talented people working for me, lawyers, and they really didn’t want me to do it early on. … A lot of people wanted me to do it a long time ago. I’m glad I didn’t do it. We got a great result without having to do it, but we will. One of the reasons that my lawyers didn’t want me to do it, is they said, if I do it, they’ll call it a form of obstruction.”

“At the right time, we will be absolutely releasing.”

via ZeroHedge News https://ift.tt/2Yvwqps Tyler Durden

According to Agriculture Secretary Sunny Purdue, there “may be as many as a million calves lost in Nebraska” due to the catastrophic flooding that has hit the state.

This is not a rumor, this is not an exaggeration, and this is not based on any sort of speculation. This number comes to us directly from the top agriculture official in the entire country, and it means that the economic toll from the recent floods is far greater than most of us had anticipated. You can watch Purdue make this quote on Fox Business right here, and it is important to remember that this number is just for one state. It is hard to imagine what the final numbers will look like when the livestock losses for all of the states affected by the flooding are tallied up. This is already the worst agricultural disaster in modern American history, and the National Weather Service is telling us that there will be more catastrophic flooding throughout the middle portion of the nation for the next two months.

Nebraska Governor Pete Ricketts says that this is the worst flooding that his state has ever experienced. Ricketts originally told us that 65 out of the 93 counties in his state have declared a state of emergency, but that number has now risen to 74. Hundreds of millions of dollars of damage has been done in his state alone, and that is just an initial estimate.

It deeply offends me that the big mainstream news channels have spent so little time covering this disaster. This is the biggest news story of 2019 so far by a very wide margin, but because it happened in the middle of the country they are not giving it the attention that it deserves.

In the short-term, food prices will not rise too dramatically because the stores are selling the food that has already been produced. But as the months roll along, you will start to notice food prices steadily increase. Millions of bushels of wheat, corn and soybeans have been destroyed by the flooding so far, and thousands of farmers will not be able to plant crops at all this year. And the livestock losses that we have already experienced will be felt for many years to come.

Beef will never be lower in price than it is right now. So if you are a beef lover, you may want to stock up.

When the flooding initially came, it happened so fast that many farmers were powerless to do anything about it. In Sherman County, farmer Richard Panowicz says that ice and debris were “exploding from the river”…

“Within 15 minutes it was devastation,” Panowicz said, with water, ice and debris exploding from the river with nothing to stop it.

He described some ice chunks as 3 feet thick and the size of an extended-cab pickup.

Panowicz said a lot of the dead calves he’s picked up have had broken legs. Many of the carcasses were found by neighbors.

In other cases, farmers were faced with a heartbreaking choice between saving their animals or saving their neighbors. One farmer that rushed to help his neighbors ended up losing 30 calves to the floodwaters…

Before Mahon could think about his animals, he needed to help his neighbors. As the water rose, he rescued one with his tractor, the floodwater lifting it up and spinning him 180 degrees. He helped save three more people — including an 85-year-old woman and a 9-month-old baby — with a boat, he said.

Then he could start counting his losses. He estimated the flood carried away 30 calves and almost as many cows, nearly $50,000 out of his pocket. It might be more.

Can you imagine the grief that these farming families are enduring right now?

Many of them are financially ruined and will never be able to go back to farming again.

Dave Eaton’s family has been farming the same plot of land for 152 years. But now the Missouri River has swallowed his farm, and with much more flooding still to come, he anticipates that his farm with be underwater “all year”…

The farm has been in his family 152 years. He was born there. He’s been thinking about what he’s learned about the Missouri’s upstream reservoirs and the mountain snowpack, and what it means for his land.

“It’s not like I’m new to the area,” he said. “My gut feeling is we’re going to be under water all year.”

And he is definitely not the only one that has had his year ruined.

Panowicz says that the hay and silage that were meant to feed his cattle this season were soaked “in 3 to 4 feet of water”…

The hay and silage to feed his cattle are soaked after sitting in 3 to 4 feet of water.

Sand now covers much of the pastureland he uses to graze his herd of commercial Angus cows and purebred Charolais bulls.

And 40 of his recently born calves died in the flood.

So what is he supposed to do?

Some Nebraska ranchers will bravely try to rebuild, but for Panowicz it appears that the end has come…

“I’ll probably sell the (remaining) cows and calves and get out of the cattle business,” said Panowicz, 65. “I’ve been around cows since the early 1970s.”

I could go on and on, but I think that you get the point.

America’s farmers have been utterly devastated. America’s cattle producers have been utterly devastated. Food production is going to be way, way below expectations, and food prices are going to escalate dramatically in the coming months. This is the kind of scenario that I have been warning about, and this crisis is going to continue to get worse as all the snow from one of the snowiest winters on record melts. In Minnesota, there are still more than 20 inches of snow on the ground in some places, and all of that water has to go somewhere.

This is the biggest national crisis that has hit the United States in many years, but the mainstream media and millions of Americans that do not live in the affected areas still do not seem to get it.

Of course once food prices start getting painfully high at our supermarkets everyone will start complaining, but there will not be any easy solutions.

via ZeroHedge News https://ift.tt/2uzv5jW Tyler Durden

Having seen Education Secretary Betsy DeVos slammed today as she tried to defend the department’s proposed budget cuts – including the elimination of funding for the Special Olympics – in a hearing before House lawmakers this afternoon, President Trump has – for the second time in a week – overridden his administration, telling a pool of reporters that the Special Olympics will be funded.

“The Special Olympics is not a federal program. It’s a private organization. I love its work, and I have personally supported its mission. Because of its important work, it is able to raise more than $100 million every year,” DeVos said in a statement.

“There are dozens of worthy nonprofits that support students and adults with disabilities that don’t get a dime of federal grant money. But given our current budget realities, the federal government cannot fund every worthy program, particularly ones that enjoy robust support from private donations,” she added.

According to Education Week, the proposal released earlier this month would gut at least 29 programs in an attempt to save some $7 billion, including the elimination of $17.6 million in funding for the Special Olympics, roughly 10 percent of the group’s overall revenue.

“We had to make some difficult decisions with this budget,” DeVos told a House subcommittee.

“Madam Secretary, I have to say, and maybe it’s offensive: Shame on you,” Rep. Rosa DeLauro (D-Conn.) said per CNN.

But now, having faced widespread backlash from the decision, President Trump told reporters at the White House Thursday,

“I’ve overridden my people for funding the Special Olympics.”

DeVos said she “wasn’t personally involved” in pushing for elimination of the funding, but she defended it as her agency seeks to cut $7 billion from the 2020 budget.

This ‘override’ follows Trump’s decision to go against his administration’s plans to place further sanctions on North Korea.

via ZeroHedge News https://ift.tt/2YvrYae Tyler Durden

Boeing shareholders probably breathed a sigh of relief Thursday afternoon when the Oracle of Omaha himself declared that, although Boeing has “a lot of work to do, very promptly,” the airline industry as a whole is still “unbelievably safe.” Because Warren Buffett’s tentative vote of confidence in Boeing was the best news the company had all day.

Shortly after Boeing unveiled the fixes to the controversial MCAS anti-stall software on its 737 MAX 8 jets – software that is suspected of having contributed to two plane crashes that left more than 350 people dead – the family of a passenger who died on Ethiopian Airlines flight ET302 has filed the first lawsuit against the aerospace company in a US federal court.

According to Reuters, the suit was filed by the family of Jackson Musoni, a citizen of Rwanda. He was one of 157 people who died during the March 10 crash. In a further bad look for the company, the lawsuit alleges that MCAS’s design was defective. That comes as Boeing has reconfigured the software to stop it from mistakenly triggering the nose-down behavior that is believed to have contributed to the two crashes. The company’s shares traded slightly higher on Thursday.

Boeing is still dealing with a lawsuit filed by the family of a man who was killed aboard the Lion Air crash, which took place on Oct. 29 when a 737 MAX owned by Lion Air plunged into the Java Sea just minutes after takeoff. The suit alleges that the 737 was “unreasonably dangerous” and is calling for what would be an embarrassing jury trial in Chicago, per Reuters.

But the lawsuit was the only disappointing headline for Boeing traders to digest. The WTO ruled on Thursday that the US had failed to comply with an earlier ruling calling for it to end illegal subsidies for Boeing, setting the stage for potentially damaging retaliatory damage from the EU, according to WSJ.

Meanwhile, the backlash over revelations that Boeing charged extra for certain safety features is intensifying after the acting head of the FAA and the secretary of the Department of Transportation sat for Congressional hearings. Sen. Dianne Feinstein and a group of senators publicized a letter they sent to Boeing demanding that all “optional” safety features be included in every plane sold.

Safety features on jets that fly hundreds of passengers should never be sold as a la carte add-ons. Boeing should include all safety-critical systems necessary for safe operation as part of the standard cost to the airlines. pic.twitter.com/0RgySKIesG

That’s because the EU’s retaliation can be commensurate with the damage done to France’s Airbus, Boeing’s biggest rival, not to the benefit received by Boeing. Specifically, the WTO ruled that Washington State tax breaks for Boeing’s Renton factory, as well as a federal export-import tax break.

The WTO ruliing comes at a particularly sensitive time for US-EU trade relations, as Trump threatens to impose damaging tariffs on foreign cars, and the EU has refused the Trump administration’s demands to open its markets to more US agricultural goods.

Having taken over in October 2016 after his predecessor stepped down amid the scandal, Chief Executive Officer and President Timothy J. Sloan has informed the board of his decision to retire from the company, effective June 30, and to step down as CEO, president and board member immediately.

An external search process will now begin for the new CEO and President, but the Board has elected C. Allen Parker as interim CEO and President.

Ironically, this retirement comes just minutes after Warren Buffett (Wells largest shareholder) expressed his confidence in Sloan.

Under so much pressure and negative political pressure, it is perhaps no surprise that Sloan has stepped down…

Full WFC Statement:

Wells Fargo & Company (NYSE: WFC) announced today that Chief Executive Officer and President Timothy J. Sloan has informed the Company’s Board of Directors of his decision to retire from the Company, effective June 30, 2019, and to step down as CEO, president, and Board member effective immediately. The Board has elected C. Allen Parker, who served as the Company’s General Counsel, as interim CEO and President (and member of the Board), effective immediately. An external search process will now begin for the Company’s new CEO and President.

Wells Fargo Board Chair Betsy Duke said, “Tim Sloan has served this Company with pride and dedication for more than 31 years, including in his role as CEO since October 2016. He has worked tirelessly over this period for all of our stakeholders in the best long-term interest of Wells Fargo. His decision, and today’s announcement, reflect that commitment and his belief that a new CEO at this time will best position the Company for success.”

Sloan said, “I have been very fortunate to work for such a great Company, and with so many dedicated team members, for more than 31 years, and I am very proud of what we have accomplished together. In my time as CEO, I have focused on leading a process to address past issues and to rebuild trust for the future. We have made progress in many areas and, while there remains more work to be done, I am confident in our leadership team and optimistic about the future of Wells Fargo. However, it has become apparent to me that our ability to successfully move Wells Fargo forward from here will benefit from a new CEO and fresh perspectives. For this reason, I have decided it is best for the Company that I step aside and devote my efforts to supporting an effective transition.”

Regarding the external search for a new CEO, and the interim CEO role, Duke added, “The Board has a continuous succession planning process through which we identify potential successors within the Company. Although we have many talented executives within the Company, the Board has concluded that seeking someone from the outside is the most effective way to complete the transformation at Wells Fargo. Accordingly, we will immediately initiate an external search and have selected Allen to serve as interim CEO. During this search period, the Board and I will work closely with Allen and the Company’s leadership team to continue to move forward on Wells Fargo’s goals and commitments. Since joining in early 2017 as our General Counsel, Allen has brought thoughtful and independent points of view to business, strategy, and governance matters, and he has earned the respect and full confidence of our Board and executive team as he takes on this interim CEO role.”

Parker, 64, served as Senior Executive Vice President and General Counsel at Wells Fargo from March 2017 to March 2019. Previously, he was presiding partner at the law firm of Cravath, Swaine & Moore from January 2013 until December 2016, where he was responsible for development and implementation of firm-wide strategy and day-to-day firm leadership, including financial analysis and reporting, business development, risk management, and public relations. While at Cravath, Parker also served as deputy presiding partner from January 2007 to December 2012 and as managing partner of the corporate department from January 2001 to December 2004. Parker joined Cravath in 1984 and was a partner from June 1990 to March 2017, and he was a member of the firm’s corporate governance and Board advisory practice. He has extensive experience in a broad range of finance, banking and related matters. He earned an undergraduate degree from Duke University, an M.A. from the University of Chicago, and a J.D. from the Columbia University School of Law.

“In my two years at Wells Fargo, I have been deeply impressed with the commitment of our 259,000 team members to move this great company forward and to build an even stronger foundation for the future,” said Parker. “I am fully committed to this role as we continue the important work at hand in support of all our stakeholders, particularly our customers, and prepare for a smooth and effective transition to a permanent CEO.”

Given Parker’s new role, Deputy General Counsel Douglas R. Edwards will serve as interim General Counsel and join the Company’s Operating Committee, effective immediately. A 24-year Company veteran, Edwards most recently led the Global Commercial and Securities Division of the Legal Department.

Chinese stocks trod water early on but faded into the close…

UK’s FTSE 100 was Europe’s outperformer while Spain and Italy were down 0.5% on the day…

US equities pumped at the open once again and then faded into the EU close (once again), only to reverse trend (once again)…Trannies outperformed, followed by Small Caps…

S&P tested back below 2800 once again today (and bounced)…

FANG stocks were flat on the day with no bounce after yesterday’s tumble…

Credit and equity protection costs plunged again today…

As opposed to yesterday’s ugly 5Y auction, today’s 7Y auction saw major demand, but that was not enough to cover the selling which saw yields up 2-4bps (except 30Y which was unchanged)…

30Y yields dropped below 2.80% for the first time since Jan 2018…

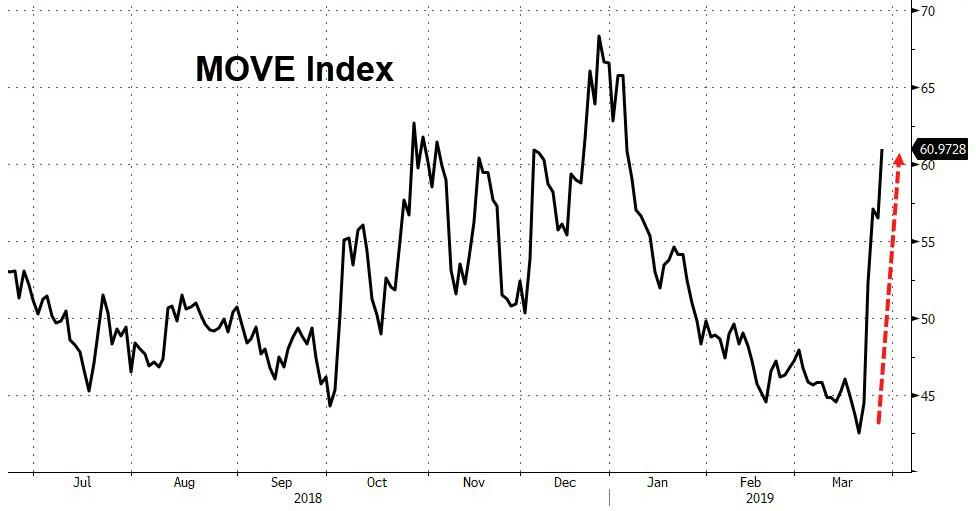

Bond vol exploded in the last week – the biggest spike since 2014…

Spiking to an important resistance level relative to stocks…

The dollar index spiked back above 97.00…

Trending higher in 2019…

The dollar gains were extended by cable weakness…

The Turkish Lira tumbled…

Leading EM FX into the red for 2019…

Cryptos were a snoozefest today…

Ugly day in PMs while copper and crude managed gains despite the stronger dollar…

Following up on yesterday’s data, Permian Nat Gas prices have plummeted into negative territory – yes, drillers are force to pay end-users to take the natgas off their hands…

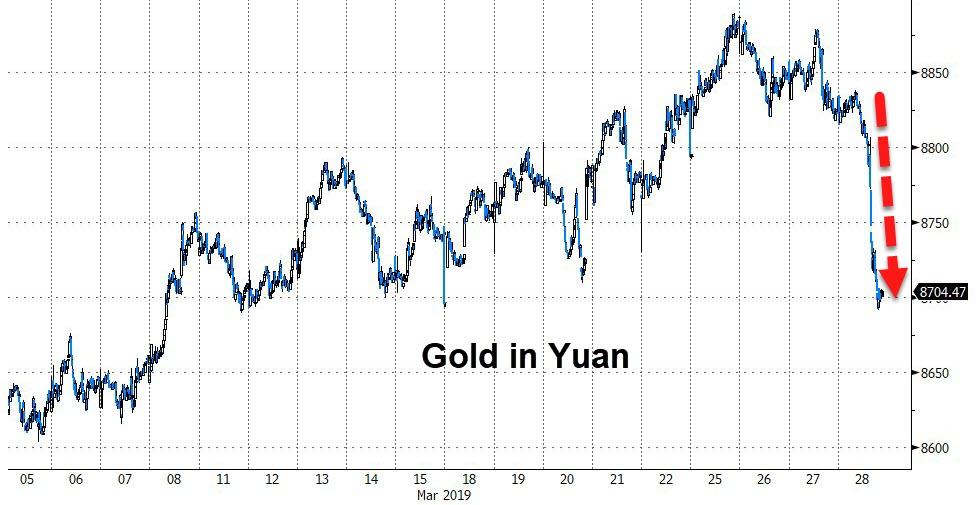

Gold fell on the day (against the dollar and yuan) – biggest drop against Yuan since June 2018…

But Gold in dollars broke below its 200DMA…

And back below $1300…

And silver slipped to its lowest since Boxing Day (12/26/18)…

Finally though, the gap between reality and perception remains near record highs…

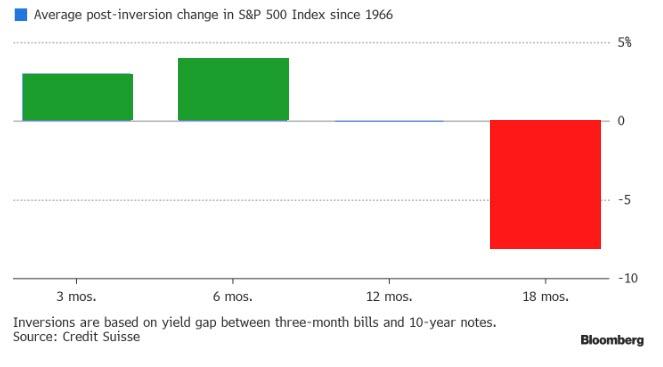

And don’t forget, a year after the yield on three-month Treasury bills rose above the yield on 10-year notes…

The S&P 500 was little changed on average.

Eighteen months later, the index had an average loss of 8 percent — typically because earnings turned lower, Andrew Garthwaite, a global strategist at Credit Suisse, wrote.

via ZeroHedge News https://ift.tt/2WtV4oD Tyler Durden

Over the past few days, many investors have asked why, with its currency in freefall again as its reserves evaporate, did Turkey take the drastic measure of sending its overnight swap rate above 1,000% in a clear attempt to crush the shorts. The answer may be simpler than most expect: if Turkey doesn’t prevent the panic from escalating, there may be nobody who can help it.

That was the implied message delivered today by the head of the Bank for International Settlements, Agustin Carstens, who said that International Monetary Fund does not have sufficient lending capacity to respond, if a major new emerging market crisis affecting several countries suddenly erupted.

Carstens, the former corpulent head of the Bank of Mexico, said that last reviews of IMF quotas, how much member countries pay in and the voting rights that go with that, had failed to ensure it had sufficient financial resources. Which, of course, leaves the question open: if the IMF no longer has the resources to rescue emerging markets and China’s economy is now contracting, who does?

BIS General Manager Agustin Carstens

“This leaves us with the problem of having inadequate resources and having to improvise in times of crisis. The mission of the fund is there,” Carstens told a conference at the French central bank. “If the Fund cannot do it others will have to do it otherwise the economic costs will be huge,” he added clearly hoping to pass the multi-trillion responsibility of bailing out EMs to someone a little more liquid.

But it’s not just emerging market that are woefully unprepared for the next crisis, and will suffer significantly should a “fat tail” event emerge: it turns out that Europe is in the same boat.

While the eurozone is in better financial shape than a decade ago, it is not solid enough to withstand another economic crisis, the head of the IMF, Christine Lagarde, said on Thursday. In a surprising moment of honesty from the Hermes-bag afficionado, Lagarde told a Paris conference that the currency union “is not resilient enough” to emerge unscathed from “unexpected economic storms”.

Lagarde acknowledged that the currency union was now “more resilient than a decade ago when the global financial crisis struck, “but it is not resilient enough,” she admitted.

“Its banking system is safer, but not safe enough. Its economic well-being is greater overall, but the benefits of growth are not shared enough,” Lagarde told the same gathering organized by the French central bank where Carstens spoke earlier.

Lagarde reveals the IMF’s last strategy.

It was unclear what the consequences are if as the IMF head claims, the eurozone will be crushed during the next crisis.

Lagarde’s warning comes as signs of slower economic growth across Europe are becoming increasingly more obvious, especially in the two core economies of Germany and France. On Friday, manufacturers in the 19-nation single currency bloc “reported their steepest downturn for six years” as pressure mounted from trade wars and Brexit fears, IHS Markit said.

On Wednesday, the European Central Bank added to growth worries when its chief Mario Draghi hinted that interest rates would stay low for longer than previously anticipated, to stimulate growth and inflation.

And with central banks now leery of injecting further liquidity via QE, while ZIRP and NIRP no longer suffice to boost economies, it remains unclear just who will provide a lifeline to either Europe or the EM when the next recession and/or global financial crisis strikes, some time over the next 12-18 months.

via ZeroHedge News https://ift.tt/2V3dDzI Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}