The annual Munich Security Conference, a Cold War era trans-Atlantic focused meeting to address severe military challenges, but which has over the years grown to include nations from around the world addressing pressing security issues, kicked off late this week on a pessimistic note. “The whole liberal world order appears to be falling apart,” Wolfgang Ischinger, chairman of the Munich Security Conference, wrote in an essay introducing the conference. “We are experiencing an epochal shift; an era is ending, and the rough outlines of a new political age are only beginning to emerge.” And on Saturday German Chancellor Angela Merkel warned of a “disintegration of international political structures” while stressing the importance of NATO as “an anchor of stability on a stormy sea”.

But concerning this “disintegration” the conference has already included a significant overture made by the Russian representative hoping to open the door to negotiations with the United States over the future of now shaky arms treaties between the two countries following the historic US withdrawal from the Intermediate-Range Nuclear Forces Treaty (INF) within the last month. In the tit-for-tat accusations and lashing out that followed at the beginning of February, Putin alarmingly accused Washington of also imperiling in the long term the landmark New START treaty, signed in 2010 and set to expire in 2021. It aims to reduce the total number of strategic nuclear missile launchers by half.

Munich Security Conference 2018, via MSC Media

Russian Foreign Minister Sergey Lavrov said at the Munich Security Conference on Saturday, according to TASS:

President Putin has repeatedly said that we are ready to launch the talks on extension of the New START. It only expires in 2021, though time flies fast, and we have suggested to the US that such discussions be launched, considering the necessity to clear up certain issues that we are worried about.

He explained that the Russian worries center on the US’ decision to denuclearize certain nuclear submarines and heavy bombardment aircraft. “The agreement stipulates that kind of denuclearization, though only using the means technically acknowledged as reliable by the other side of the agreement. However, no fairly meaningful consultations have been offered to us so far, though we continue our efforts,” Lavrov added.

Set to expire in two years, it stipulates that Russian and US arsenals be restricted to no more than 1,550 deployed strategic warheads and less than 700 deployed strategic missiles and bombers. Russia has previously expressed desire to extend it to 2026, though at the start of Trump’s taking the White House, he reportedly told Putin the New START was “one of several bad deals negotiated by the Obama administration” during their first official phone call.

Indeed there’s been no response from the American side to Lavrov’s overture during his Saturday address to the Munich conference. Lavrov also lambasted the United States’ attempts to modify the international Chemical Weapons Convention after it alongside Canada and the Netherlands put forward a proposal to include certain chemical substances connected with the Skripal affair in the Chemical Weapons Convention’s Annex, which Moscow sees as motivated by political humiliation.

Lavrov said of the issue, “They are unwilling to let the international law remain as the Chemical Weapons Convention defines it. They want to use their own rules for interpreting that convention.” Lavrov said the Trump administration has to yet agree to hold any “meaningful consultations” on New START or other weapons agreements, according to Bloomberg.

US Vice President Mike Pence met with an icy reception during his speech to the conference on Saturday:

Other crucial comments of Lavrov included highlighting that Russia cannot be excluded from efforts to maintain stability in tense regions; simultaneously, he said there’s a current global trend for initiatives to resolve security crisis that are merely “NATO-oriented” or “NATO-centric”. He said, “We cannot strengthen one’s security at the expense of others.”

Meanwhile US President Mike Pence, fresh off the US-initiated Warsaw conference wherein he urged the world to “confront” top “terror sponsor” Iran, also addressed the Munich conference by continuing his message of demanding that the EU withdraw from the Iran deal, and that it cease attempts to financially circumvent US sanctions.

Notably, Pence also addressed the Venezuela crisis, repeating Washington’s call for the EU to fully recognize Guaido as Venezuela’s rightful leader, though a number of individual countries and key US allies already have.

via ZeroHedge News http://bit.ly/2SF7FrT Tyler Durden

China is taking its renewable energy push to new heights, literally, after the country’s scientists revealed plans to build and launch in orbit a space solar station that could capture the Sun’s rays 24/7, Chinese media report.

China has already started to build an early experimental space power plant in the city of Chongqing, The Sydney Morning Herald reported, citing an article in China’s Science and Technology Daily.

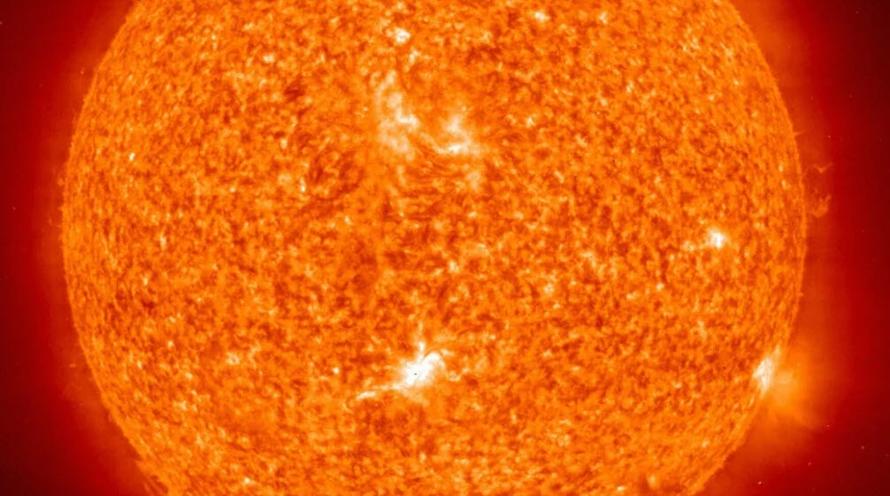

The sun photographed by NASA’s Extreme Ultraviolet Imaging Telescope

The space solar station, planned to orbit the Earth at 36,000 kilometers (22,370 miles) could provide “an inexhaustible source of clean energy for humans,” according to Pang Zhihao, a researcher at the China Academy of Space Technology Corporation.

Such solar power technology could supply reliable energy 99 percent of the time and have six times the intensity of the solar farms that work on the earth, the scientist says.

China will start by launching small solar stations between 2021 and 2025, while a possible next step would be a Megawatt-level station planned to be built in 2030.

The energy from the space solar station would be converted into a microwave or laser beam that would be sent to the earth.

However, the project has two major hurdles to overcome in order to become a practical solution. One is the weight of a space solar station, expected to be more than two times the weight of the International Space Station. The other is the safety impact of laser or microwave beams sent to the earth.

China is not the only country studying the potential of harnessing the power of the Sun in space.

Caltech for example has its Space Solar Power Project, which has researched the use of ultralight, foldable, 2D integrated elements, Caltech has developed a prototype which collects sunlight, converts it to RF electrical power, then wirelessly transmit that power in a steerable beam.

According to Caltech’s research, “Collecting solar power in space and transmitting the energy wirelessly to Earth through microwaves enables terrestrial power availability unaffected by weather or time of day. Solar power could be continuously available anywhere on earth.”

via ZeroHedge News http://bit.ly/2BBGyTW Tyler Durden

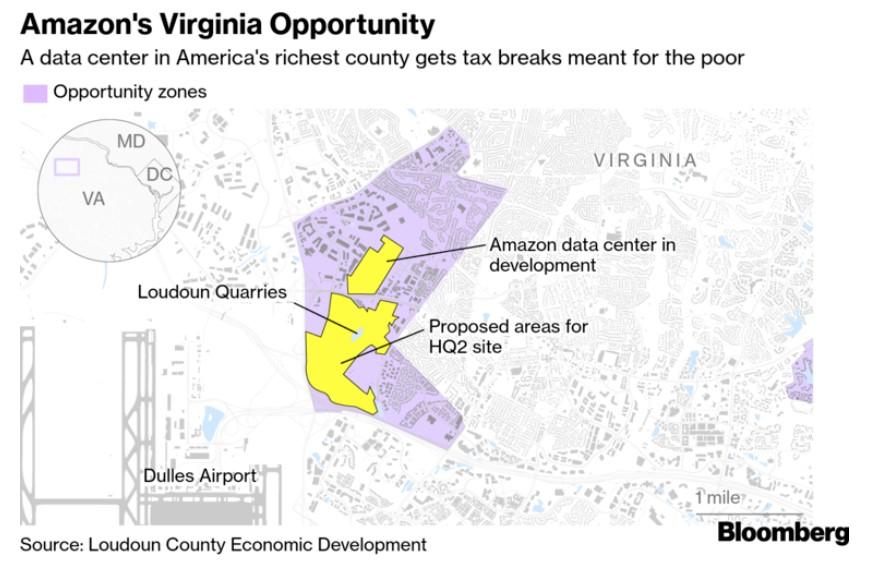

Even though Amazon walked away from billions in subsidies in New York, the company may still wind up qualifying for federal tax breaks that are intended to help distressed communities by building a new data center in Virginia.

About 30 miles west of Washington, Amazon and its partners are preparing to build a facility to house infrastructure for the rapidly growing Amazon Web Services, according to Bloomberg. AWS went into contract on the property last year after executives held two meetings with Virginia’s embattled Governor Ralph Northam, who subsequently selected the area as a “qualified opportunity zone”. The property is 107 acres and the designation will entitle Amazon to claim millions of dollars in federal tax breaks.

But in yet another potential scandal, Northam claimed that he hasn’t discussed the tax break with Amazon executives and that he didn’t select that area as an opportunity zone to help attract Amazon. Amazon echoed these sentiments, saying that the opportunity zone designation was never discussed with officials in Virginia and that it played no role in the company‘s decision to build there.

The tax subsidy available to AWS, which hadn’t been previously reported, is the latest catalyst to spur questions about whether the opportunity zone program is simply a giveaway to wealthy individuals that expand in relatively affluent areas. As everybody knows by now, Amazon drew criticism for deciding to build in an opportunity zone in a gentrifying area of Queens – plans that were subsequently scrapped days ago.

Amazon didn’t comment on whether not it would forgo the opportunities from the subsidy, claiming simply that “AWS doesn’t disclose or discuss details about its data centers.”

The point of opportunity zones is to allow governors to select up to a quarter of their census tract to qualify for subsidies. Investors who help develop or fund businesses in these zones are often able to defer capital gains and profit taxes. Virginia chose a mix of poor and affluent areas, including two in Loudoun County, which had a median household income of $135,842 in 2017. This is more than double the national average and the highest of any county in the nation. In the county where Amazon is building its data center, the median income is $88,657.

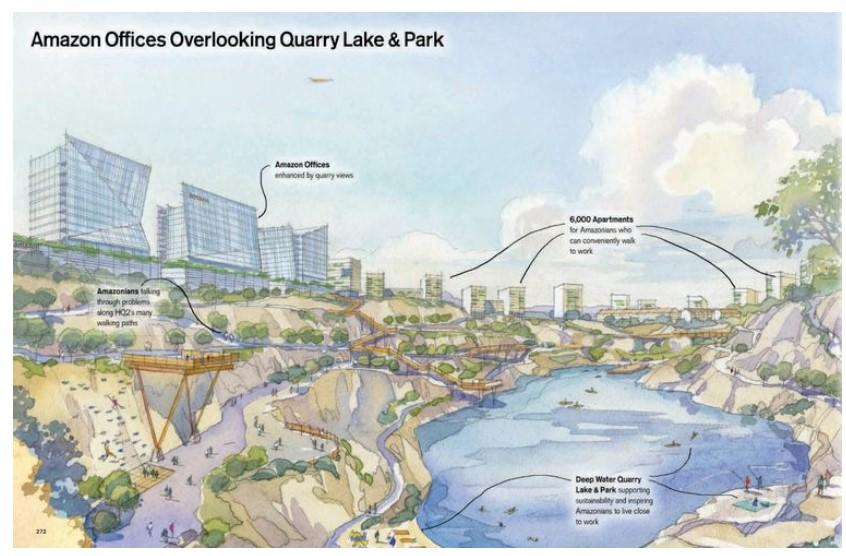

A lot of the details of the negotiations haven’t been released publicly because Amazon and community officials often sign nondisclosure agreements. But public documents and interviews indicate that negotiations with Amazon about the data center and its new headquarters were closely aligned. The site that AWS chose for its data center is next to a larger tract of land that Virginia was pitching as a possible location for Amazon’s second headquarters. The economic development official in Virginia who nominated the census tract as an opportunity zone, Buddy Rizer, had been talking to Amazon executives about both properties and said he considered the matters separate because he didn’t believe Amazon would be able to use the opportunity zone credit at either location.

The overlap between these processes is drawing criticisms of the program. The main critique is simply that the law and regulations surrounding opportunity zones are very loosely written and they permit state and local officials to use federal dollars to draw the favor of large companies instead of focusing on blighted communities.

Greg Leroy, executive director of Good Jobs First, a Washington-based labor-funded organization critical of corporate subsidies told Bloomberg: “The idea that a company headed by the richest person on the planet could get a tax exemption in the richest county in the country completely summarizes the deceptive packaging of the whole program. Poor people are the bait. But the switcheroo is that the rich people get all the government handouts.”

via ZeroHedge News http://bit.ly/2IhPmnQ Tyler Durden

Both of America’s great national parties are coalitions.

But it is the Democratic Party that never ceases to celebrate diversity – racial, religious, ethnic, cultural – as its own and as America’s “greatest strength.”

Understandably so, for the party is home to a multitude of minorities.

It is the domain of the LGBTQ movement. In presidential elections, Democrats win 70 percent of Hispanics, Jews and Asian-Americans, and 90 percent of African-Americans.

Yet, lately, the party seems to be careening into a virtual war of all against all.

Democratic Governor Ralph Northam and Attorney General Mark Herring of Virginia have both admitted to using blackface.

Northam imitated Michael Jackson’s “moonwalk” in a 1984 dance contest. Herring, in 1980 at the University of Virginia, did a blackface impression of rap icon Kurtis Blow, who called it ugly and degrading.

The resignations of both have been demanded by Virginia’s black leadership. Northam and Herring, however, are defying the demands.

Meanwhile, Lt. Gov. Justin Fairfax, only the second black ever to win statewide office, has been charged by two women with rape. And the demands for his resignation are growing louder and most insistent.

Yet if Fairfax is forced out, while the white governor and white attorney general get a pass, black leaders warn, all hell is going to bust loose.

The Democratic Party of Virginia was already convulsed over all the monuments, statues, schools, parks, highways and streets that bear the names of slave owners, Confederate soldiers and 19th- and 20th-century segregationists.

Across the Potomac, Ilhan Omar, the first ever Somali-American to serve in Congress, and a Muslim, ignited a firestorm last week when she gave this as the reason Congress faithfully votes the AIPAC line on Israel: “It’s all about the Benjamins, baby.”

The reference is to $100 bills, on which Ben Franklin’s face appears. The line is a rap lyric from a 1997 song by Puff Daddy.

Omar was saying Congress has been bought.

The House Democratic leadership demanded and got an apology from Omar for her use of an “anti-Semitic trope.”

But Omar now his company in the House. Palestinian-American Rep. Rashida Tlaib, also a Muslim, shares and airs her views on Israel.

The problem for Democrats?

These provocateurs are magnets for media. They speak for a rising minority in the party that regards Israel as an apartheid state that oppresses Palestinians. And they find an echo among millennials on the party’s socialist left.

As Thursday’s Washington Post headlined, this Omar flap “could forecast a Democratic divide on Israel.”

Indeed, it may have already done so.

When Senate Republicans proposed legislation to allow states to refuse to hire individuals or contractors who support the BDS movement to boycott Israel, Senators Kamala Harris, Cory Booker, Elizabeth Warren and Bernie Sanders all voted no.

The four say they are supporting freedom of speech to condemn Israeli policy. But to others it looks like a progressive Democratic blessing for those urging that Israel be treated the same way Ian Smith’s Rhodesia and apartheid South Africa were treated.

Within the Democratic coalition, Asian-Americans are now in conflict with blacks and Hispanics over admission policies at elite schools and universities.

Asian-Americans are “overrepresented” where students are admitted based on test scores or entrance exams. Black and Hispanic leaders are demanding that student bodies, regardless of test scores, look like the community. And if this requires affirmative action based upon race and ethnicity, so be it.

The LBGTQ community is now in court demanding all the rights and protections of the civil rights laws of the ’60s. This will bring gay groups into constant collisions with religious communities that adhere to traditional moral views on homosexuality.

The minorities of color in the Democratic coalition are growing, as the base of the GOP is aging and shrinking. But these minorities are also becoming more rivalrous, competitive and demanding. And the further they move left, they more they move outside the American mainstream.

The pledge of allegiance this writer recited every day of school, reads: “I pledge allegiance to the flag of the United States of America, and to the republic for which it stands, one nation under God, indivisible, with liberty and justice for all.”

Today, the antifa left desecrates the flag, as liberals praise NFL players who “take a knee” during the national anthem. Militant migrants march under Mexican flags to protest border security policies. The “republic” has been by “our democracy.”

We are no longer “one nation … indivisible” We have almost ceased talking to one another. As for “under God,” added in 1954, Democrats at their Charlotte Convention sought to have God excised from the party platform.

“Liberty” has been supplanted by diversity, “justice” by equality.

But as Revolutionary France, Stalin’s USSR, Mao’s China, Castro’s Cuba and Hugo Chavez’s Venezuela proved, regimes that promise utopian and egalitarian societies inevitably reveal themselves to be undertakers of freedom, America’s cause.

via ZeroHedge News http://bit.ly/2trimPH Tyler Durden

Israel Defense Forces (IDF) conducted a massive military exercise last week which was designed to prepare soldiers for combat operations in “topographical conditions” comparable to those in Lebanon, The Times of Israel reported.

Carried out by the 401st Brigade of the Armored Corps, the exercise was the largest in years.

IDF forces completed the field training exercise alongside the Israeli Air Force, in addition to the engineering and intelligence corps.

According to the IDF and also seen on specific Twitter feeds, dozens of armored personnel carriers, main battle tanks, attack aircraft, and helicopters were deployed in the training zone in the Jordan Valley

נסראללה בלחץ? חטיבה 401 של חיל השריון ביצעה השבוע תרגיל גדול שנועד לדמות לחימה בלבנון, ובו התאמנו הלוחמים על תיאום עם כוחות של חיל האוויר, ההנדסה והמודיעין | צפו בתיעוד מהאימון @ndvori

One Twitter user said, “IDF temporarily evicted 291 people from 4 communities in the northern Jordan Valley, to conduct military drills on their lands.”

PALESTINE: routines of the occupation— On Feb 06, 2019, IDF temporarily evicted 291 people from 4 communities in the northern Jordan valley, in order to conduct military drills on their lands. https://t.co/A8AFAaaS1L

The brigade’s commander, Col. Dudu Sonago, said Hezbollah, the Lebanese Militant Group, has gained experience and developed sophisticated battle techniques after fighting in neighboring Syria’s civil war.

“As the situation in Syria stabilizes, Hezbollah is returning its forces to Lebanon,” Col. Dudu Sonago told Channel 12. “They are no longer a guerrilla organization, but a real army. They fought there in regiments of companies and battalions, very similar to the military.”

“They operate in civilian areas and are ready with a large quantity of anti-tank missiles,” added Sonago. “This is a challenge the IDF must train for.”

The Times of Israel says tensions between Israel and Lebanon “have heightened in recent months ” following IDF operations to “locate and destroy Hezbollah cross-border attack tunnels reaching into the country.”

Hezbollah leader Hassan Nasrallah dismissed the effectiveness of the Israeli operation, which ended in January.

Nasrallah criticized Israel earlier this month over Prime Minister Benjamin Netanyahu’s warmongering attitude against Lebanon over the “inclusion of the Iran-backed organization in the country’s new government,” said The Times of Israel.

On Tuesday, Lebanese Prime Minister Saad Hariri said the new government would allow Hezbollah to keep its weapons, which some of the military hardware was used against Israel in 2006 and are used regularly to threaten Jerusalem.

Former Defense Ministry Ombudsman Maj.-Gen. Yitzhak Brick has recently claimed that IDF forces are not ready to wage war on Hezbollah, arguing in a damning report that the military is “worse than it was at the time of the Yom Kippur War” in 1973.

With war drums beating between Israel and Hezbollah (and even maybe Iran), the IDF has completed its latest large scale war drill, simulating a fierce battle between its adversaries.

With the global economy going down the tubes, Zero Hedge readers must be on the watch for geopolitical flashpoints in the coming quarters.

via ZeroHedge News http://bit.ly/2TRacM4 Tyler Durden

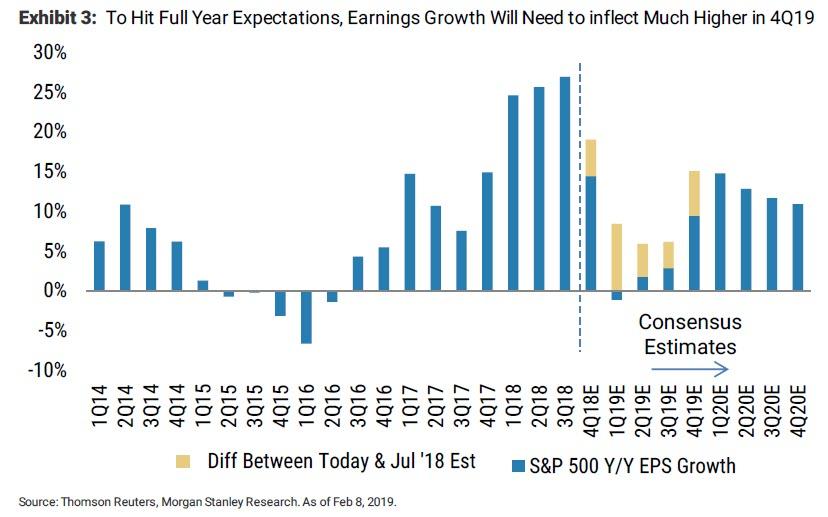

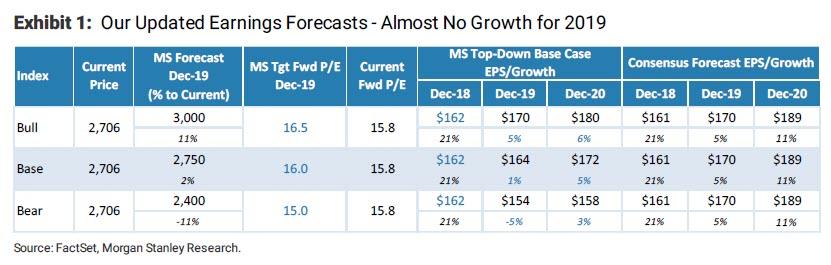

Last week, Morgan Stanley’s resident bear, Mike Wilson, slashed his EPS outlook for the S&P, declaring that an earnings recession has arrived, not just for Q1 earnings, where EPS are now forecast to decline 2.2% Y/Y, the first drop in three years, and how now expects full year EPS to grow just 1%, down from 4.3%, as the kind of hockeystick rebound expected by consensus in the second half is unlikely to materialize.

Still, while Morgan Stanley revised its earnings numbers lower, surprisingly, its bull, base, and bear case year end price targets remain unchanged for one simple reason: the bank hiked its PE multiple target as “the lower rate environment provides support for higher year end target multiples”, i.e., the Fed comes to the rescue again.

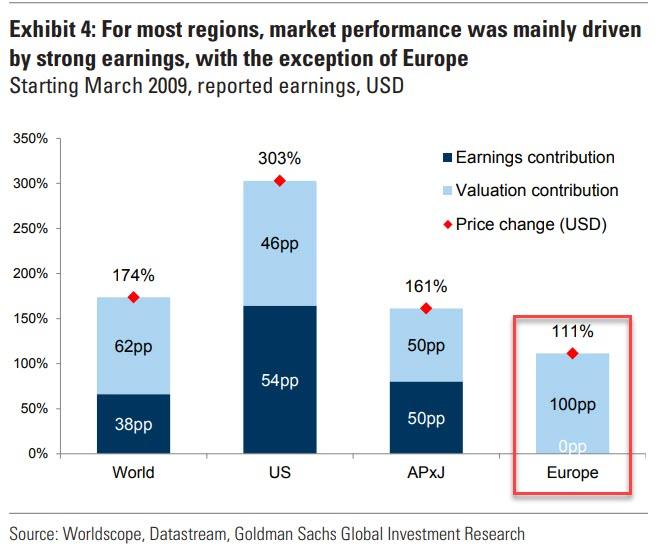

Which brings up an interesting point: how much of the global, central-bank induced bear market of the past decade has been the result of earnings growth, and how much due to multiple expansion?

The answer come for a recent report by Goldman, which warns that while a market crash is unlikely, returns going forward are likely to be low from here because valuations are now unlikely to rise and the bulk of prospective returns are likely to come from earnings.

Which goes back to our point: how much of the price change since the market lows has been from earnings, and how much is PE expansion? According to Goldman, in the US, the answer is roughly half and half – valuation expansion has contributed 46% to the price increase since the financial crisis which the bank says “owes to a great extent to years of falling interest rates and QE. This is odd, because during a normal bull market, and the past decade has been anything but, P/E expansion would typically drive around 25% of bull market returns.

Yet in a truly stunning observation, while in the US earnings have been responsible for roughly half of the 303% rise in stock prices, in Europe valuation expansion has been the sole driver of the 111% growth in equity prices. In other words, Europe has seen no earnings growth over the past decade!

In other words, whereas in the US the Fed was responsible for roughly half the upside in the market in the past decade (assuming low rates did not also benefit earnings, which they did) in Europe if it weren’t for central banks, there would have been no market appreciation at all since the March 2009 lows.

Incidentally, this is not good news now that profits have peaked, and as Goldman concludes, “we see little reason for valuation expansion to be a major driver of returns from here. At the same time, our earnings forecasts remain low in every region, marking a sharp downturn from last year, particularly in the US.”

via ZeroHedge News http://bit.ly/2SahEQV Tyler Durden

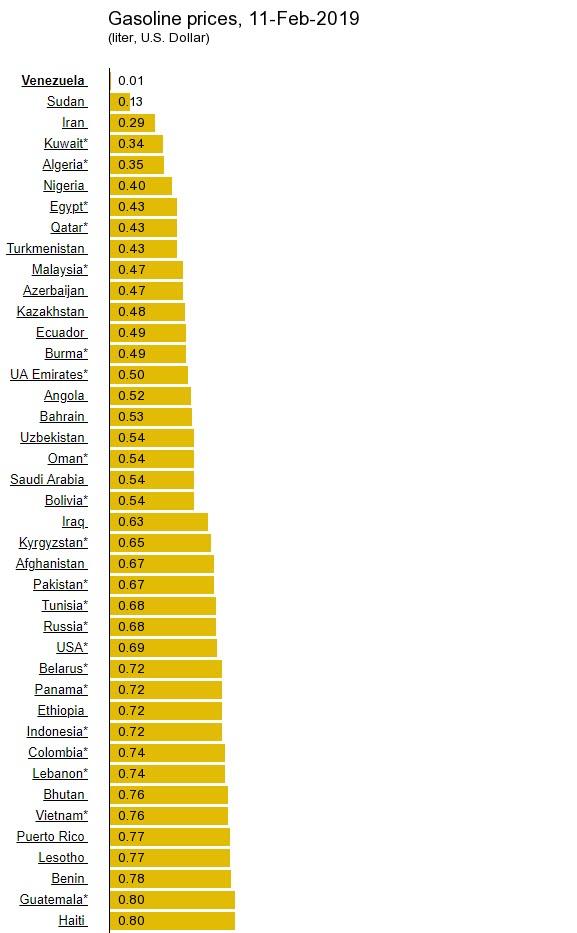

Amid the political turmoil of Washington’s attempted coup, Venezuela’s socialist utopia has sparked an entrepreneurial spirit among its repressed citizens who are making 1000% returns, taking advantage of the distorted centrally-planned economy’s prices for goods, by crossing the Colombian border with gasoline, flour, rice, and cheese spread.

While the west attempts to send truckloads of ‘humanitarian aid’ into Venezuela – currently blocked by President Maduro – enterprising smugglers are flooding ‘cheap, subsidized’ goods out of Venezuela to sell at dramatic markups on the side-streets of Colombian border towns.

As Bloomberg reports, market shelves in the scruffy Colombian town of Puerto Santander are loaded with Venezuelan maize flour, rice, cheese spread and more, heavily subsidized consumer goods smuggled by government officials and ordinary citizens alike and sold at big mark-ups.

Commerce is brisk at the market stalls in Puerto Santander, where packets of Venezuelan maize flour that are used to make arepas, a staple in both countries, go for 2,500 pesos, or about 80 cents. That’s some 30 percent less than what Colombian groceries selling licit products charge. And in Venezuela? The subsidized price for the flour is about 7 cents.

Additionally, gasoline is ferried from Venezuela too, as people cash in on the arbitrage opportunities created by extreme price distortions.

Venezuelan gasoline is the cheapest in the world…selling for the equivalent of $0.01 per gallon.

But, as Bloomberg notes, along a nearby highway in Colombia, dozens of makeshift gasoline stations openly sell Venezuelan fuel. The going rate: $10.60 for a six-gallon jug, compared to $14 at a local regulated Colombian pump. And there were none of those anywhere in sight on the highway.

That’s quite a return, but as Bloomberg points out,armed gangs that control the commerce charge a tax of 4,000 pesos, the equivalent of $1.30, for every container. Since gasoline in Venezuela is virtually free, the biggest costs are bribing officials in that country and paying off the mafia in Colombia. The mark-up on the contraband petrol can dwarf what cocaine traffickers make.

In the past, the two governments have worked together to crack down on this greatest arbitrage in the world, but since the political turmoil has exploded, no more.

“There’s no communication now,” said Colonel Carlos Giron, head of the customs police in the Colombian province of Norte de Santander, even “with a border as turbulent as this one.”

However, while gasoline is still plentiful in Venezuela, the latest U.S. sanctions – imposed last month on the state-owned oil company – could lead to supply disruptions, and ruin the greatest arbitrage trade in the world.

via ZeroHedge News http://bit.ly/2GSzB4v Tyler Durden

Though he missed the torrid rebound in stocks during the first six weeks of 2019 (US stocks have, by at least one measure, experienced their best start to a year since 1991, when Gundlach didn’t expect the rebound to start until later in the year), Doubleline Capital founder Jeffrey Gundlach’s warnings about the risks endemic to the US corporate debt market (and the ballooning deficit) still resonate with thousands of investors, who are warily approaching the end of the business cycle with a mounting sense of paranoia. His warnings about how the deficit blowout has generated “artificial” growth are particularly poignant in light of the growing signs of an economic slowdown in Europe and China (though, as we pointed out yesterday, the PBOC appears to be doing everything in its power to change the narrative), as well as some weak indicators in the US (think retail sales and business sentiment).

And in an interview with Yahoo Finance, Gundlach once again expounded his view that, though the typical recessionary leading indicators are still only flashing “yellow-to-green”, and though the Fed’s promise to “pause” its QT program has soothed the equity markets worries – for now at least – there are still plenty of risks lurking beneath the surface.

And the most immediate of these, as Gundlach has previously explained (and as we have also pointed out in our own analysis), is the state of the corporate bond market, which, Gundlach believes, could tilt the next recession into a full-blown debt crisis. The corporate bond market has $700 billion in bonds maturing this year alone. What Gundlach is most worried about is the combined effect of this bonds rolling over alongside the Fed’s balance sheet runoff, which he said could lead to a flood of issuance, particularly in the long-end of the curve. As the next recession begins, we could see short term rates fall, but long term rates blow up, leading to a punishing steepening of the yield curve (leading to the type of “bear steepener” trade about which Nomura’s Charlie McElligott has also warned).

With the Fed’s QE exhausted, and the federal budget deficit already blown out to a staggering degree, Gundlach warned that policy makers will have little recourse. To illustrate just how precarious the corporate bond market risks have become, Gundlach cited research by Morgan Stanley which showed that after nearly a decade of rock-bottom interest rates, corporations have binged on debt to such a degree that, if one were to base their credit analysis solely on leverage ratios, then nearly half of the investment grade corporate bond market would be relegated to junk.

Heavily leveraged US corporates could endure mass downgrades, as investment-grade angels plummet from the sky, and just like that – the next debt crisis will have gone from contained to systemic.

Just like in 2006, the long-term, big picture risks could be the most consequential. All other short-term risks would be merely trivial details. “Like back in 2006, the only thing that mattered was you understood there was a credit crisis coming. I think this time the only thing that really matters is this problem with the corporate bond market and the national debt issue when the next recession comes.”

And when the next recession finally comes “there’s going to be a lot of turmoil.”

Compounding the risks from the corporate bond market, the US’s fiscal situation is growing increasingly dire. Once one factors in all “off-budget” expenditures like the costs of fighting the US’s “Forever Wars” in the Middle East and cleaning up after natural disasters, the US budget deficit is, in reality, expanding at a rate of 6% of GDP. With 3% real growth, this suggests that, if it weren’t for the fiscally stimulative stance embraced by the Trump administration, we could be in a recession already. But once the inevitable slowdown finally arrives, the budget deficit would need to expand to 10% of GDP merely to maintain. Which would suggest that the floor is much closer to falling out than many realize.

With that being said, here’s a quick rundown on Gundlach’s comments on whether markets are accurately forecasting the likelihood of a rate cut by the Fed this year, what the legendary bond investor’s favorite recession indicators are telling us, his two cents on the burgeoning blowback to corporate buybacks, and his outlook for interest rates.

Interest Rates:

Gundlach – whose Total Return fund outperformed nearly all of its peers last year – believes that long-term rates will move higher in 2019, though he admits that he didn’t think the 30-year Treasury would dip back below 3% in the latter half of 2018. But if the 30-year rate crosses over 3.50%, it could go all the way to 4%.

Meanwhile, even if long-term rates climb, Gundlach believes short-term rates could move lower if “they’re manipulated by the Fed.”

JULIA LA ROCHE: OK, Jeffrey, before we’ve sent us back to New York, let’s get a prediction from you. Where do you think the 10 year will end this year?

JEFFREY GUNDLACH: I’ve long ago learned not to fall into that trap. There was one year when I said the 10 year would end at x, and it actually ended five days before year end exactly at x. And then there was a big move the last five days. And so, [? ended up being ?] off by like, 35 basis points or something. And I remember people saying I was wrong because I was off by 35 basis points when in fact, I was only off by five days.

I think- let me put this way. I’m not going to put a number on it. But I think long term interest rates are headed higher. I think what we had in response to the weakness in risk assets in the stock market– I think we had the Pavlovian reaction of oh, I’ve seen this movie.

When stocks get weak, you buy long term treasuries. And we had a decent rally, about 50 basis points, in long term treasuries. But now, we’re basically drifting higher again.

And I think that what I said earlier is going to start finding its way into people’s psyche, which is when the next weakness comes, there’s going to be so much debt, so many bonds, that it’s possible that short term rates drop if they’re manipulated by the Fed, and flight to safety leads people to find a 250 2 year to be OK. But I’m not really sure if people will find the 280 10 year to be OK when you’re staring down the barrel of trillions of dollars of bond issue.

And so I think interest rates are headed higher. I really didn’t think they would get back below 3% on the 30 year treasury. They did for a minute. And now they’re back above 3%. But I think when and if long term interest rates move up towards about 350 on the 30 year, I think you could see them accelerating higher. And so a nice round number to think about would be around 4% on the long term sort of treasury as we move towards the latter part of this year.

Buyback regulation

Gundlach believes the growing popularity of “Democratic socialism” is nothing short of dangerous, and the idea that lawmakers would try to tell corporations how to distribute their profits is equally absurd.

Socialism didn’t work out for the Soviet Union, Gundlach said. And it won’t work out for the US.

MYLES UDLAND: Jeffrey, Myles Udland here in New York. I want to ask you about share buybacks, which has gotten a lot more play among a number of politicians recently. You were just talking a moment ago about leverage ratios in the corporate bond market. Does anything about the conversation about buybacks concern you, just in terms of politicians I suppose, being a little bit more hostile towards corporate America?

JEFFREY GUNDLACH: Well, it’s pretty clear that the rhetoric from presidential hopefuls for 2020, on the left side anyway, has gotten very, very hostile. Obviously, to have legislators telling privately companies or public companies in this case, what they should be doing with their profits is a little bit disconcerting, to say the least.

So on the margin, you have to take legislation prohibiting or limiting buybacks as a negative for the stock market. It’s pretty clear that the leverage ratios in the corporate bond market have driven– have been hand in glove with buybacks. And the corporate economy is very leveraged. So I think what the politicians want is– their thought processes stop enriching the wealthy who are already disproportionately– wealth inequality is pretty bad– stop enriching them with boosting up stock prices. The idea might be to have more money for workers wages, which is obviously part of the wealth inequality problem.

So I can kind of see how all this– all different parts of the same picture viewed from different angles. But the politicians clearly are talking about socialism, democratic socialism. Just puts the word democratic in front of the word socialism, because it sounds good, that at least you’re voting for it, instead of being forced into it. But you know, socialism is not a very good way of building wealth, as shown by millennial– you know, hundreds of years of history, most recently down in Venezuela. That’s all you have to look at. I remember there was a thing called the Soviet Union, which had five year plans, and I don’t think they’re around anymore. So not a really good idea.

The National Debt

Gundlach isn’t a fan of high taxes. But the notion that the US total taxation rate has fallen to just 15% of GDP, its lowest level since 1949, while the national debt has ballooned past $22 trillion, is ridiculous. If politicians don’t have the temerity to reduce the size of government, they should at least be willing to pay for what they’re spending.

To illustrate the distortions caused by deficit spending, Gundlach caluclauted that, If we had a balanced budget in 2018, economic growth would have been negative.

JEFFREY GUNDLACH: Well, there’s always some people somewhere in the government that are doing things right. But the biggest problem is that we have a growing economy, and yet, we have decided that debt doesn’t matter one bit. You know, Dick Cheney was famous for saying Ronald Reagan proved that deficits don’t matter. But the national debt just went over $22 trillion dollars yesterday, and it’s growing at over a trillion dollars a year during a growing economy.

And our taxation versus GDP has gone from around 20% a few years ago to about 15%. So 15%– it’s not the lowest level ever, it’s just the lowest level since 1949. So we have decided to run a large government with huge deficits and it seems that nobody’s interested in collecting the taxes for that. I wish government were smaller. I think it’s not a problem of taxation. But once you’re going to establish the size of spending the way it is, you’ve got to pay for it. And we’ve gone very, very far away from that.

And that’s an issue that is going to get a lot of attention because the deficit is going to continue to grow, and the Fed has been ripping interest rates. They’ve stopped for now. But the debt expense, the interest expense is at 1.25% of GDP right now, but the CBO says that by the mid 2020s, it’s going to be at 3%, which is a 1.74% increase relative to GDP. Which in a very simplistic framework means that GDP, all things being equal, will be 1.75% slower in the mid 2020s.

And we’re already struggling under insufficient economic growth. Think about the nominal GDP that the most recent one that was announced, which is through September 30, which is fiscal 2018. You know, the growth of nominal GDP was 5.3%. But the growth of the national debt was 6% of GDP. And part of economic growth is the delta in government spending so with the national debt growing by 6% GDP, and nominal GDP go up by 5.3%, it means if you had a balanced budget, the economy would have been negative during fiscal 2018.

But while the Trump Administration has behaved irresponsibly with its spending, Democrats like Elizabeth Warren calling for Medicare for All won’t do any better. Gundlach said he was stunned by Warren’s willingness to lie to the American people during her speech announcing her campaign.

So everything that we’re doing is based upon debt expansion. And it is not insignificant. And it is not true when you hear politicians– I listened to Elizabeth Warren’s speech when she said she was running for president. She looked right into the camera and lied to the American people, that it is not true that we can’t afford Medicaid for all, and free college tuition, and all the other goodies that the socialists want to bring out. She says, it’s just simply not true that we can’t afford them.

And I hear other politicians say, oh, it’s just World War Ii all over again. Well, taxes were raised massively during World War II. And not just taxes on the wealthy the taxes on the middle class and the lower middle class were raised massively to pay for World War II. Going into the 1930s, the tax rate for the average American household was 1.5%. By the 1944, it was 25%. So this is a massive tax increase. Taxation during World War II went from 5% of GDP to 20% of GDP.

Recession indicators

Despite the emergence of a narrative of a “synchronized global slowdown”, most leading indicators aren’t signaling an imminent recession – yet.

JEFFREY GUNDLACH: A little bit more than it was a year ago, what was really interesting about entering 2018 was that there was this narrative of a synchronized global expansion. That was true. Everything was really flashing green lights for the economy entering 2018. And yet, what’s interesting about that when things were flashing green light, most people don’t understand that it means it’s kind of the end of the game for risk assets. The global stock market peak January 26 of 2018. The US hung on until October, but the global stock market peaked January 26 of 2018.

Entering 2019, there was a narrative developing that is also true of some synchronized global slowdown. Yet the indicators that we look at for a recession are not even flashing fully yellow yet. It’s more of a yellowish green right now. We look at things like the leading economic indicators, kind of the granddaddy of them all that’s put out by the conference bureau.That year over year always has gone negative before the front end of a recession. And while it’s weakening from a very high level, it’s still pretty high at around 5% year over year. And the stock market being up in the last couple of months means that probably, the leading indicators will hang in there.

What is signaling recession a little bit more are sentiment surveys. The PMI surveys typically collapse in a very observable way before the front end of recession comes. They are collapsing sort of right now, but they’re still at high levels. Consumer sentiment same sort of thing. Unemployment rate is starting to flash yellow a little bit. Unemployment claims, the report every Thursday, have bottomed out and appear to be in a rising trend. And the unemployment rate now is above its 12 month moving average unemployment rate. And that’s a necessary condition to be talking about potential recession.

Watch the full interview below:

via ZeroHedge News http://bit.ly/2Ih3opF Tyler Durden

Jussie Smollett, the Empire star who claims he beat off two white men after they assaulted him in a 2am hate crime in late January, has retained Michael Monico – the high-powered criminal defense attorney representing former Trump fixer Michael Cohen.

Appearing on WGN‘s “The Roe Conn Show,” Monico was asked about his thoughts on Smollett, “but we can’t get your thoughts on Jussie Smollett because [of] this big developing story today, and it turns out you’re the attorney for Jussie Smollett, too,” said Conn.

“Yes, at the moment, I am,” replied Monico.

“Oh for god sakes,” Conn joked. “Can you stop getting clients so I can talk to you about the stories?”

Smollett, 36, alleges he was attacked around 2am on January 29 by two white men who shouted racist and homophobic slurs at him, doused him in a liquid that smelled like bleach, hung a thin rope around his neck and yelled “This is MAGA country,” before he was able to chase them off. Somehow Smollett was able to keep a grip on his Subway sandwich throughout the ordeal, which he was seen on surveillance still holding when he returned to his apartment.

“And above all I fought the fuck back,” said Smollett on February 2.

News of Smollett retaining a criminal defense attorney comes as Chicago police release on Friday night of two persons of interest without charges; Nigerian-born brothers who are acquaintances of Smollett.

The men have been confirmed to be the men seen on surveillance images of the scene of the alleged incident. Chicago Police tell ABC News the reason the men were on the scene is now central to the investigation.

“Yes, they are confirmed to be the men on scene by surveillance video,” Chicago Police said. “The reason why they were there is now central to the investigation and we can’t get into that at this time.” –ABC 7

“Due to new evidence as a result of today’s interrogations, the individuals questioned by police in the Empire case have now been released without charging and detectives have additional investigative work to complete,” said Chicago PD spokesman Anthony Guglielmi. The brothers were identified by the Daily Mail as Nigerian-born actors Abimbola “Abel” and Olabinjo “Ola” Osundairo – one of whom was an extra on “Empire.” They were arrested on Wednesday night at O’Hare Airport after returning from a trip to Nigeria to visit family.

Police raided the home shared by the brothers on Wednesday night, removing electronic devices, shoes and other items which could help their investigation.

BREAKING:Police raided the home of two persons of interest in Jussie Smollett case last night. Both men are of Nigerian decent and have appeared as extras on the show. Police took bleach, shoes electronics and more.Officers asked family if they knew #Jussiesmollett. @cbschicagopic.twitter.com/PDSFtf5jwb

Following their release, the lawyer representing the two men said on Friday night that they gave police new evidence in the investigation, and are no longer considered suspects. On Friday morning, Guglielmi said that the two men “have a relationship with Smollett.”

On Thursday night, police said phone records provided by Smollett do show he was on the phone with his manager at the time of the attack. Both men told investigators Smollett’s attackers yelled slurs. –ABC 7

Multiple sources have told ABC7 Eyewitness News in Chicago that police have been investigating whether Smollett and the men staged the attack – “allegedly because Smollett was being written off “Empire.””

A source familiar with the investigation told the ABC7 I-Team that Smollett failed to appear for an interview with detectives earlier Thursday but has since spoken with police.

Chicago Police Superintendent Eddie Johnson contacted ABC7 to say they are continuing to treat Smollett as a victim and the investigation remains ongoing.

“Police are investigating whether the two individuals committed the attack – or whether the attack happened at all,” Chicago police told ABC News. –ABC 7

Smollett’s representatives as well as the writing staff for Empire deny he is being written off the show.

Speaking with Robin Roberts on Good Morning America Thursday, Smollett reflected on the alleged incident.

“It’s the attackers, but also the attacks,” he said – adding that those who don’t believe his account “don’t even want to see the truth.”

According to Chicago PD’s Guglielmi, Smollett’s comments on GMA are consistent with what he has told Chicago police.

via ZeroHedge News http://bit.ly/2IdqMEq Tyler Durden

The smart money is liquidating assets, paying off debt and moving capital into collateral that isn’t impaired by debt or speculative valuations.

The Federal Reserve’s sudden return to “accommodative” dovishness in response to the stock market’s swoon telegraphs its intent to fire up QE once the recession kicks into gear. QE (quantitative easing) are monetary policies designed to ease borrowing and the issuance of credit, and to prop up assets such as stocks and real estate.

The basic idea is that the Fed creates currency out of thin air and uses the new money to buy Treasury bonds and other assets. This injects fresh money into the financial system and lowers the yield on Treasury bonds, as the Fed will buy bonds at near-zero yield or even less than zero in pursuit of its policy goals of goosing assets higher and increasing borrowing/spending.

This is pretty much the Fed’s only lever, and it pulls this lever at any sign of weakness in stocks or the economy. That sets up an obvious question that few seem to ask: what happens when QE fails? What happens when the Fed launches QE and stocks fall as punters realize the rally is over? What happens when lowering interest rates doesn’t spark more borrowing?

What happens is the smart money sells everything that isn’t nailed down, a process that is arguably already well underway.

Why sell assets when QE has guaranteed gains in the past? Answer: exhaustion. There are limits to everything financial, and once those limits are reached, no amount of goosing will push the limits higher. Rather, further goosing only increases the fragility and vulnerability of the system.

Price-earnings ratios only go so high before reversing, rents only go so high before reversing, and so on. Once the trend has visibly stagnated, smart money sells out because the gains are minimal while the risk of reversal is rising by the day. Why wait for losses to pile up? Sell now and avoid the self-reinforcing decline as everyone starts selling.

The smart money is careful to mask the selling so as to avoid panicking the market. Smart money sells out slowly, in pieces small enough to avoid banging the bid lower. Alas, the Smart Money strategy is to count on greater fools to believe the shuck and jive of QE and the rest of the flim-flam: real estate never goes down, the economy will grow strongly through 2040, the next target for the S&P 500 is much higher, and so on.

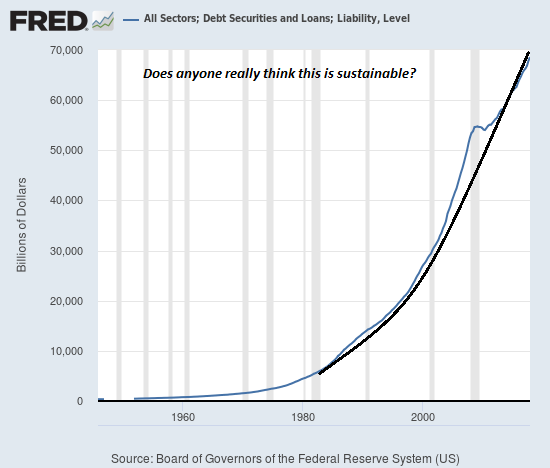

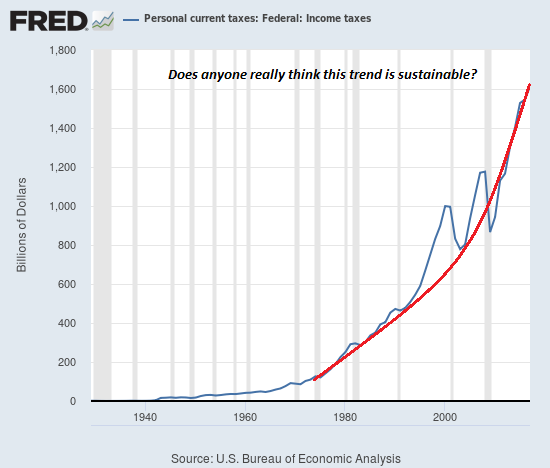

Take a look at these charts of total liabilities/debt and federal income tax collected and ask yourself: are these trends sustainable in an economy growing by a few percent a year?

Federal income taxes collected have practically doubled from the recessionary nadir of 2009: does anyone really think they can double again in the next 9 years?

These geometrically rising trendlines are the acme of unsustainability. The limits have been reached and reversal looms. Ask yourself why multiple bids for real estate have vanished and why the Fed is so anxious to publicly trumpet its dovishness. If the limits were far from being reached, why the tone of desperation?

As I noted yesterday, every injection of stimulus weakens the response of the following dose. After a decade of never-ending stimulus, the positive effects of stimulus have been exhausted. Increasing the stimulus is toxic to an exhausted system pushing its intrinsic limits.

As I observed yesterday, the smart money is liquidating assets, paying off debt and moving capital into collateral that isn’t impaired by debt or speculative valuations. The Smart Money has secured the good seats at the banquet of consequences, the seats reserved for those with no debt, unimpaired collateral and little dependence on central bank stimulus or central state statistical legerdemain.