Authored by Lance Roberts via RealInvestmentAdvice.com,

The recent stock market correction, and subsequent rally, revealed the many mistakes that investors consistently make when managing their money. Emotionally-driven decisions almost always turn out badly and ultimately impair the long-term investment goals individuals are attempting to achieve.

Given that individuals are consistently promised investing in the financial markets is the only way to financial success, it is worthwhile to review the common mistakes most investors make. After all, if investing is “so easy,” why are the majority of American’s so broke?

Let’s dig into the myths, the mistakes and the steps to redemption.

Financial pundits across the country consistently promote the myth that one simply buys a basket of ETF’s, or individual stocks, and returns will compound at 8, 10 or 12% a year,

Nothing could be further from the truth.

On a nominal basis, it is true that if one bought an index, and held it for 20-years, they would have most likely made money. Unfortunately, making money, and reaching financial goals, are two ENTIRELY different things.

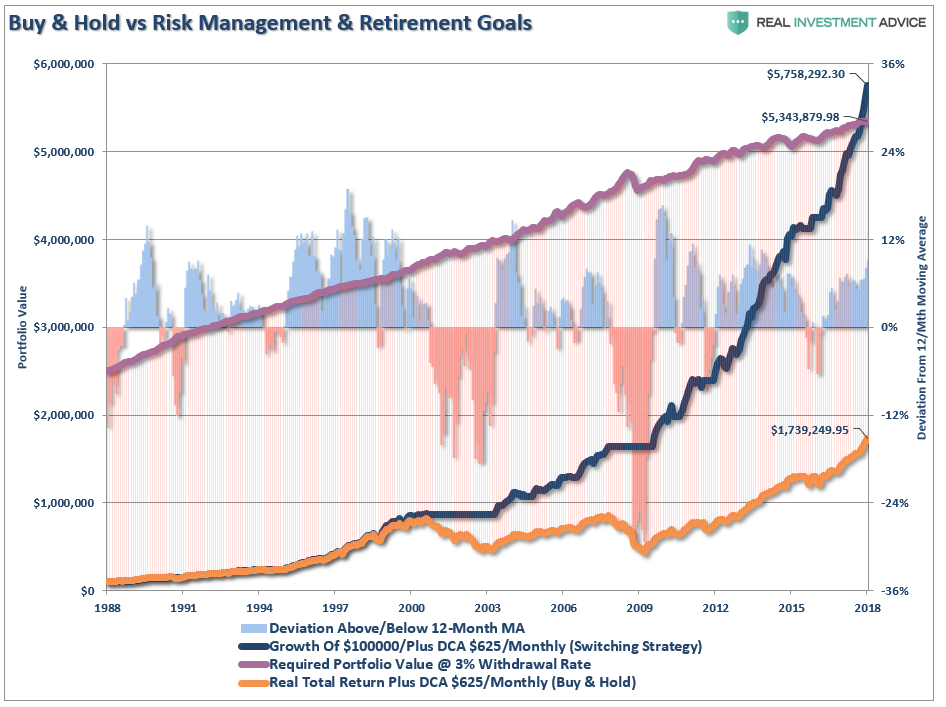

“The chart below shows the difference between two identical accounts. Each started at $100,000, each had $625/month in additions and both were adjusted for inflation and total returns. The purple line shows the amount of money required, inflation-adjusted, to provide a $75,000 per year income to Bob at a 3% yield. The only difference between the two accounts is that one went to “cash” when the S&P 500 broke the 12-month moving average in order to avoid major losses of capital.”

For the majority of Americans, investing has never worked as promised.

The problem, as I have discussed many times previously, is that most individuals cannot manage their own money because of ‘short-termism.’

Despite their inherent belief that they are long-term investors, they are consistently swept up in the short-term movements of the market. Of course, with the media and Wall Street pushing the ‘you are missing it’ mantra as the market rises – who can really blame the average investor ‘panic’ buying market tops and selling out at market bottoms.”

Sy Harding summed this point up in his excellent book “Riding The Bear:”

“No such creature as a buy and hold investor ever emerged from the other side of the subsequent bear market.”

Statistics compiled by Ned Davis Research back up Harding’s assertion. Every time the market declines more than 10% (and “real” bear markets don’t even officially begin until the decline is 20%), mutual funds experienced net outflows of investor money. Fear is a stronger emotion than greed.

The research shows that it doesn’t matter if the bear market lasts less than 3 months (like the 1990 bear) or less than 3 days (like the 1987 bear). People will still sell out, usually at the very bottom, and almost always at a loss.

The only way to avoid the “buy high/sell low” syndrome – is to avoid owning stocks during bear markets. If you try to ride a bear market out, odds are you’ll fail.

And if you believe that we are in a new era where Central Bankers have eliminated bear market cycles, your next of kin will have my sympathies.

Let’s look at some of the more common trading mistakes to which people are prone. Over the years, I’ve committed every sin on the list at least once and still do on occasion. Why? Because I am human too.

1) Refusing To Take A Loss – Until The Loss Takes You.

When you buy a stock it should be with the expectation that it will go up – otherwise, why would you buy it?. If it goes down instead, you’ve made a mistake in your analysis. Either you’re early, or just plain wrong. It amounts to the same thing.

There is no shame in being wrong, only in STAYING wrong.

This goes to the heart of the familiar adage: “let winners run, cut losers short.”

Nothing will eat into your performance more than carrying a bunch of dogs and their attendant fleas, both in terms of actual losses and in dead, or underperforming, money.

2) The Unrealized Loss

From whence came the idiotic notion that a loss “on paper” isn’t a “real” loss until you actually sell the stock? Or that a profit isn’t a profit until the stock is sold and the money is in the bank? Nonsense!

Your portfolio is worth whatever you can sell it for, at the market, right at this moment. No more. No less.

People are reluctant to sell a loser for a variety of reasons. For some, it’s an ego/pride thing, an inability to admit they’ve made a mistake. That is false pride, and it’s faulty thinking. Your refusal to acknowledge a loss doesn’t make it any less real. Hoping and waiting for a loser to come back and save your fragile pride is just plain stupid.

Realize that your loser may NOT come back. And even if it does, a stock that is down 50% has to put up a 100% gain just to get back to even. Losses are a cost of doing business, a part of the game. If you never have losses, then you are not trading properly.

Take your losses ruthlessly, put them out of mind and don’t look back, and turn your attention to your next trade.

3) More Risk

It is often touted that they more risk you take, the more money you will make. While that is true, it also means the losses are more severe when the tide turns against you.

In portfolio management, the preservation of capital is paramount to long-term success. If you run out of chips the game is over. Most professionals will allocate no more than 2-5% of their total investment capital to any one position. Money management also pertains to your total investment posture. Even when your analysis is overwhelmingly bullish, it never hurts to have at least some cash on hand, even if it earns nothing in a “ZIRP” world.

This gives you liquid cash to buy opportunities and keeps you from having to liquidate a position at an inopportune time to raise cash for the “Murphy Emergency:”

This is the emergency that always occurs when you have the least amount of cash available – (Murphy’s Law #73)

If investors are supposed to “sell high” and “buy low,” such would suggest that as markets become more overbought, overextended, and overvalued, cash levels should rise accordingly. Conversely, as markets decline and become oversold and undervalued, cash levels should decline as equity exposure is increased.

Unfortunately, such has never actually been the case.

4) Bottom Feeding Knife Catchers

Unless you are really adept at technical analysis, and understand market cycles, it’s almost always better to let the stock find its bottom on its own, and then start to nibble. Just because a stock is down a lot doesn’t mean it can’t go down further. In fact, a major multi-point drop is often just the beginning of a larger decline. It’s always satisfying to catch an exact low tick, but when it happens it’s usually by accident. Let stocks and markets bottom and top on their own and limit your efforts to recognizing the fact “soon enough.”

Nobody, and I mean nobody, can consistently nail the bottom tick or top tick.

5) Averaging Down

Don’t do it. For one thing, you shouldn’t even have the opportunity, as a failing investment should have already been sold long ago.

The only time you should average into any investment is when it is working. If you enter a position on a fundamental or technical thesis, and it begins to work as expected thereby confirming your thesis to be correct, it is generally safe to increase your stake in that position.

6) You Can’t Fight City Hall OR The Trend

Yes, there are stocks that will go up in bear markets and stocks that will go down in bull markets, but it’s usually not worth the effort to hunt for them. The vast majority of stocks, some 80+%, will go with the market flow. And so should you.

It doesn’t make sense to counter trade the prevailing market trend. Don’t try and short stocks in a strong uptrend and don’t own stocks that are in a strong downtrend. Remember, investors don’t speculate – “The Trend Is Your Friend”

7) A Good Company Is Not Necessarily A Good Stock

There are some great companies that are mediocre stocks, and some mediocre companies that have been great stocks over a short time frame. Try not to confuse the two.

While fundamental analysis will identify great companies it doesn’t take into account market, and investor, sentiment. Analyzing price trends, a view of the “herd mentality,” can help in the determination of the “when” to buy a great company which is also a great stock.

8) Technically Trapped

Amateur technicians regularly fall into periods where they tend to favor one or two indicators over all others. No harm in that, so long as the favored indicators are working, and keep on working.

But always be aware of the fact that as market conditions change, so will the efficacy of indicators. Indicators that work well in one type of market may lead you badly astray in another. You have to be aware of what’s working now and what’s not, and be ready to shift when conditions change.

There is no “Holy Grail” indicator that works all the time and in all markets. If you think you’ve found it, get ready to lose money. Instead, take your trading signals from the “accumulation of evidence” among ALL of your indicators, not just one.

9) The Tale Of The Tape

I get a kick out of people who insist that they’re long-term investors, buy a stock, then anxiously ask whether they should bail the first time the stocks drops a point or two. More likely than not, the panic was induced by listening to financial television.

Watching “the tape” can be dangerous. It leads to emotionalism and hasty decisions. Try not to make trading decisions when the market is in session. Do your analysis and make your plan when the market is closed. Turn off the television, get to a quiet place, and then calmly and logically execute your plan.

10) Worried About Taxes

Don’t let tax considerations dictate your decision on whether to sell a stock. Pay capital gains tax willingly, even joyfully. The only way to avoid paying taxes on a stock trade is to not make any money on the trade.

“If you are paying taxes – you are making money…it’s better than the alternative”

Steps to Redemption

Don’t confuse genius with a bull market. It’s not hard to make money in a roaring bull market. Keeping your gains when the bear comes prowling is the hard part. The market whips all our butts now and then, and that whipping usually comes just when we think we’ve got it all figured out.

Managing risk is the key to survival in the market and ultimately in making money. Leave the pontificating to the talking heads on television. Focus on managing risk, market cycles and exposure.

STEP 1: Admit there is a problem… The first step in solving any problem is to realize that you have a problem and be willing to take the steps necessary to remedy the situation

STEP 2: You are where you are… It doesn’t matter what your portfolio was in March of 2000, March of 2009 or last Friday. Your portfolio value is exactly what it is rather it is realized or unrealized. The loss is already lost and understanding that will help you come to grips with needing to make a change.

STEP 3: You are not a loser… You made an investment mistake. You lost money. It has happened to every person that has ever invested in the stock market and anyone who says otherwise is a liar!

STEP 4: Accept responsibility… In order to begin the repair process, you must accept responsibility for your situation. Continue to postpone the inevitable only leads to suffering further consequences of inaction.

STEP 5: Understand that markets change… Markets change due to a huge variety of factors from interest rates to currency risks, political events to geo-economic challenges. Does it really make sense to buy and hold a static allocation in a dynamic environment?

The law of change states: that change will occur and the elements in the environment will adapt or become extinct and that extinction in and of itself is a consequence of change.

Therefore, even if you are a long-term investor, you have to modify and adapt to an ever-changing environment otherwise, you will become extinct.

STEP 6: Ask for help… Don’t be afraid to ask or get help – yes, you may pay a little for the service but you will save a lot more in the future from not making costly investment mistakes.

STEP 7: Make change gradually… Making changes to a portfolio should be done methodically and patiently. Portfolio management is more about “tweaking” performance rather than doing a complete “overhaul.”

STEP 8: Develop a strategy… A goal-based investment strategy looks at goals like retirement, college funding, new house, etc. and matches investments and investment vehicles in an orderly and designed portfolio to achieve those goals in quantifiable and identifiable destinations. The duration of your portfolio should match the “time” frame to your goals. Building an allocation on 80-year average returns when you have a 15-year retirement goal will likely leave you in a very poor position.

STEP 9: Learn it…Live it…Love it… Every move within your investment strategy must have a reason and purpose, otherwise, why do it? Adjustments to the plan, and the investments made, should match performance, time and value horizons. Most importantly, you must be committed to your strategy so that you will not deviate from it in times of emotional duress.

STEP 10: Live your life… The whole point of investing in the first place is to ensure a quality of life at some specific point in the future. Therefore, while you work hard to earn your money today, it is important that your portfolio works just as hard to earn your money for tomorrow.

I hope you found this helpful.

via Zero Hedge http://ift.tt/2EZocMs Tyler Durden