Following the significant disappointment of January’s existing home sales, hopes were high for a rebound in new home sales (+3.5% expected after December’s 9.3% plunge) but those hopes were crushed as January new home sales crashed 7.8% MoM.

This is the lowest level since August, even as the supply of homes at current sales rate climbed to 6.1 months from 5.5 months.

This is the biggest two-month drop in new home sales SAAR since August 2013.

The Median price dropped from $336,700 to $323,000 – the lowest since October…

16% of new homes sold in January cost more than $500,000, down from 22% last month.

As sales in the Northeast collapsed:

Northeast -33.3%, from 36K to 24K

Midwest +15.4%, from 65K to 75K

South -14.2%, from 351K to 301K

West +1.0%, from 191K to 193K

So we are saure NAR will blame ‘inclement’ weather – as opposed to soaring rates and plunging affordability.

Just as we warned previously, the following chart shows, that surge in rates will have a direct impact on home sales (or prices will be forced to adjust lower) as affordability collapses…

In a decision that could allow DACA protections to remain in place past the March deadline, the conservative-majority Supreme Court has rejected a request to hear the administration’s challenge to a judge’s ruling – made earlier this year – mandating that the DACA program must remain in place until all litigation is resolved.

Several state attorneys general sued to block President Trump’s September decision to cancel the program. On Jan. 9, San Francisco-based US District Judge William Alsup ruled that DACA must remain in place while the litigation is resolved. A week later, the DOJ said it would ask the Supreme Court to overturn that decision.

“It defies both law and common sense for DACA … to somehow be mandated nationwide by a single district court in San Francisco,” Attorney General Jeff Sessions said at the time.

As the Hill pointed out, the DOJ’s request was unusual in that it asked the Supreme Court to jump ahead of the 9th Circuit Court of Appeals in reviewing the case. The nation’s highest court typically will only bypass an appellate court when there’s an emergency involving foreign affairs, a serious separation of powers concerns or when it has already agreed to hear another case dealing with the same question.

JUST IN: Supreme Court declines to hear Trump bid to immediately end program protecting ‘Dreamers’ from deportation pic.twitter.com/zpNDi4rMfn

The court said the government’s request for the court to hear its case is denied without prejudice, and that the court expects the appeal will swiftly be handled by the Ninth Circuit.

“It is assumed that the court of appeals will proceed expeditiously to decide this case,” the court said.

The justices provided no further explanation for their decision. It takes four justices to agree to hear a case.

The decision is surprising in that Trump recently appointed a conservative justice, Neil Gorsuch, to maintain the court’s conservative majority following the death of Antonin Scalia.

It also begs the question: Has the Supreme Court turned against Trump?

Amid the growing debate whether rates will keep rising once they hit 3.00%, or they will fall as asset managers find the new level attractive enough to dip their toes and buy duration, one analyst laughs at everyone calling for lower rates from here onward, In a note published overnight, Deutsche Bank credit strategist Jim Reid writes that “rates and yields will continue to structurally move higher in the quarters and years ahead regardless of any short-term moves, and we hope policymakers won’t be derailed by the inevitable macro issues that this will bring.”

While we will share some more details from this note, the first in a series of why Deutsche believes that global yields have nowhere to go but up, we wanted to highlight one chart which according to Deustche does not make any sense in the context of the ongoing debate of potentially lower yields: the projection of global debt to GDP forecasts for the next 30 years.

According to Reid, “notwithstanding the short-term low supply expectations in Europe, a real head-scratcher going forward is how the market will cope over the years and even decades to come with the central case scenario of higher and higher government debt around the world. Figure 13 looks at the US, Germany and Japan government debt/GDP with forecasts from the US CBO and BIS.”

And here is the chart that is at the crux of Reid’s conundrum: this is the same chart which prompted Fed president Robert Kaplan to suggest that the US debt trajectory is headed toward unsustainability.

Reid’s summary:

This may mean that QE eventually has to become a regular feature of markets for many cycles to come. However, given other forces, it will still likely occur at structurally higher levels of yields but with the main intention of ensuring real yields don’t rise to prohibitive levels as they might in a free market with all the extra supply that is likely.

As a reminder, over the weekend Goldman warned that a 4.5% yield on the 10Y would result in a 25% – or more – crash in stocks. The chart above suggests that the question is not “if” but “when”, and just “how much more…”

The peso is tumbling back to earth after last week’s excitement following a 2% plunge YoY in Mexican retail sales in December – the biggest drop since 2013.

It is perhaps no coincidence that Mexico’s retail sales peaked in November 2016 – the month President Trump was elected – and have fallen ever since.

This is the 5th straight month of annual declines in Mexico retail sales…

And the reaction was swift in the peso…

Fascinating that both Mexico and Canada are seeing major downturns and disappointments in their macro data in recent weeks, just as NAFTA negotiations reach the vinegar strokes.

If a comparison to a dotcom foursome holds true, the rally in the vaunted F.A.N.G. stocks may be coming to an end.

Around Thanksgiving time in 2015, we posted what is still among our most popular charts and blogs we’ve ever published. At the time, 2 big things were going on in the equity market. First, it was a tumultuous period for the broad U.S. market as stocks were sandwiched between a pair of 10% corrections. Second, there was one group of stocks that was famously not experiencing any form of tumult whatsoever – the quartet affectionately known as F.A.N.G.

Of course, the acronym FANG stands for Facebook, Amazon, Netflix and Google (Alphabet). At the time, the four stocks were all the rage in the investment world. In fact, a composite of the 4 stocks would have been up roughly 500% in the 3 years leading up to that point. And, despite the rocky footing in the overall market, the FANG stocks were still technically well-positioned for further leadership.

With FANG stocks at dizzying levels, and the broad market looking dicey, we were inspired to write that Thanksgiving 2015 post. In the post, titled Is It Too Late To Sink Your Teeth Into F.A.N.G. Stocks?, we pondered the prospects for further FANG gains. And the context of that pondering revolved around a comparison between the 4 FANG stocks and another prolific foursome of a couple decades prior.

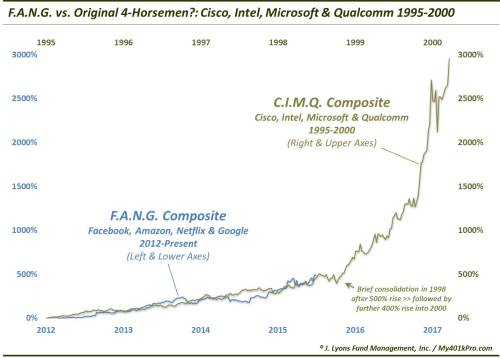

Specifically, we compared the move in FANG to a composite of 4 of the poster children of the dotcom bubble, namely, Cisco, Intel, Microsoft and Qualcomm, aka, C.I.M.Q. But the comparison was between the 2012-2015 FANG stretch and the 1995-1998 CIMQ period. It did not encompass the 2000 bubble top as we had a different point we wanted to emphasize.

As it turns out, the 1995-1998 CIMQ composite experienced a similar 500% price appreciation as the FANG run into 2015, eerily similar in fact. Here is the comparison of the 2 composites that we presented back then.

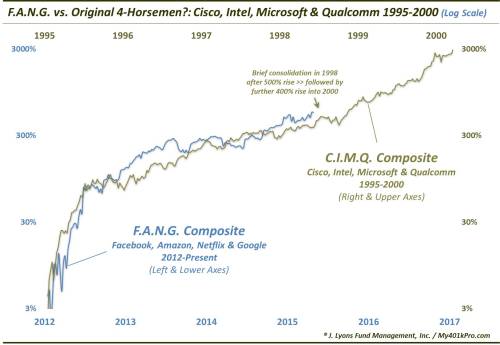

Or in log form:

As one can see, the 2 composites had experienced similar, monster 3-year runs. One of the points of our post back then, however, was that while most investors were skeptical that the already stratospheric FANG run could persist much longer, it was indeed still possible. And in fact, it would not be unprecedented. As the chart shows, following a brief consolidation in 1998, the CIMQ stocks, fresh off a 500% rally, would embark on a further 400% rally over the next 2 years into the 2000 bubble top.

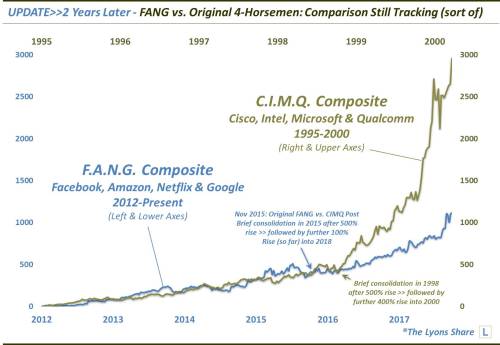

Now, 2 years (and a few months) later, we can update the comparison and see if the FANG stocks were able to defy skeptics (and gravity) and continue the march higher like their CIMQ predecessors. As it turns out, they did, to a large extent.

Now again, given the stock market’s meteoric rise over the past 2 years, it may be hard to remember how unlikely most market observers in 2015 thought it was that the FANG stocks would be able to continue to climb for much longer – or at a continued rapid pace. Yet, that is exactly what they have done, doubling from their levels of 2 years ago. That is impressive, and a testimony to the concept of momentum. On the other hand, relative to what CIMQ was able to do, i.e., quadruple, in the 2 years following 1998, it does pale in comparison.

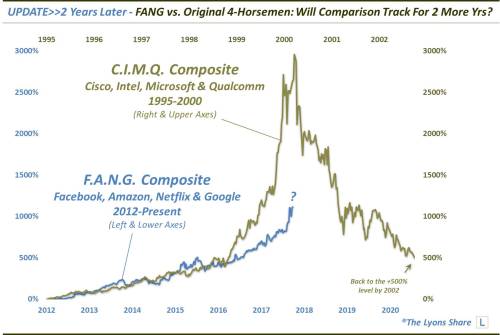

So what now? The FANG stocks still show relatively little inclination to reverse their ascent. However, if the CIMQ analog is still relevant, the cycle may hold some bad news for those still wanting to sink their teeth into FANG. That’s because the 2 year, 400% spurt into 2000 obviously marked the end of the road for the CIMQ rally. Not only that, but the bubble would subsequently burst with a vengeance. By 2 years later, in 2002, the CIMQ composite would be right back down to their 1998 levels. Yes, meaning an 80% decline.

Is FANG destined for a similar fate? Maybe not to that degree, but probably by some magnitude therein. The question is when? We don’t have an answer for that. This is essentially a hand-picked comparison and the FANG path does not have to continue to bear any resemblance whatsoever to CIMQ. It is merely an illustration to show what is possible (i.e., a substantial giveback of FANG gains), despite its seeming improbability.

As we stated in the 2015 post, these studies are not meant as predictions. Rather, the takeaways are more philosophical:

Trends last longer than one often thinks likely or possible

The inexorable FANG ascent can, and likely will, eventually suffer an ignominious fate along the lines of CIMQ (though, perhaps not to the degree?)

The CIMQ phenomenon was a veritable bubble, and despite the considerable rally in FANG (and stocks, in general), it doesn’t come close to the bubbly dotcom conditions

Comparisons/analogs like this usually lose their relevance as soon as they are discovered, or published (we should take the past 2 years’ semi-accurate tracking record and cut bait!)

* * *

If you’re interested in the “all-access” version of our charts and research, please check out our new site, The Lyons Share. You can follow our investment process and posture every day — including insights into what we’re looking to buy and sell and when. Thanks for reading!

It’s been almost five months exactly since the New York Times launched the #MeToo movement with its initial expose about disgraced Hollywood studio head Harvey Weinstein’s decades-long history of sexual predation – which was enabled, the paper explained, by the silence of his peers and a flurry of NDA-clad settlements. And today, after a $500 million deal involving a former Obama administration official reportedly fell apart, Variety is reporting that the Weinstein Co. will declare bankruptcy.

To wit, TWC’s board released a letter Sunday evening to investors Ron Burkle and Maria Contreras-Sweet, the leaders of the bid group, breaking off negotiations. According to the letter, the company is in dire need of operating cash, but the bidders have so far refused to provide interim financing.

“Based on the events of the past week, however, we must conclude that your plan to buy this company was illusory and would only leave this Company hobbling toward its demise to the detriment of all constituents,” the letter stated. “Despite your previous statements, it is simply impossible to avoid the conclusion that you have no intention to sign an agreement – much less to close one – and no desire to save valuable assets and jobs.”

The sale was close to being announced exactly two weeks ago, when New York Attorney General Eric Schneiderman stepped in and filed a suit accusing the company of enabling Harvey Weinstein’s sexual abuses. The lawsuit scrambled the deal, creating the possibility of an outside monitor or other intrusive provisions. Schneiderman also objected to the investors’ plan to hire David Glasser, the COO under Weinstein, as CEO.

Schneiderman met on Wednesday with Contreras-Sweet, Burkle, and representatives of the Weinstein Co. board. After the meeting, it appeared that a deal could be reached that would meet with Schneiderman’s approval.

However, it appears that the added stress on the transaction exposed conflicts between the two sides. According to the Weinstein Co. letter, the two sides continued to have conflicts over Glasser’s role, a week after the board fired him.

After a relatively quiet, holiday-shortened week, the coming five days are shaping up to be volatile and extremely busy on the political, data and speaker front, where a barrage of economic updates is set to hit in both the US and across the globe, while Fed Chair Jay Powell will dominate the highlights on Tuesday with his testimony before the House, the week will culminate on March 4 with the Italian election and the SPD “Grand Coalition” vote.

On the political side, while many expect a hung parliament in Italy and a small majority in favour of a Grand Coalition in Germany, uncertainty remains high. Meanwhile, in the US, Fed chair Powell’s testimony will be closely watched on Tuesday, as will Draghi’s appearance in Brussels on Monday. Core inflation in the euro area should rise slightly while confidence should fall, while spending in the US could see a weak start to the year.

In the US: Fed Chair Powell’s first semi-annual monetary policy testimony is on Tues. The speech will likely have a similar tone as the FOMC minutes, noting that growth has picked up and the FOMC has become more convinced of continued momentum. Powell is expected to sound cautiously optimistic, reiterating the need for patience when it comes to the hiking cycle. This will not be the place for Powell to hint at 4 hikes for this year. Meanwhile, there are a number of data releases this week, with the most important being Thursday’s personal income report. Real spending may have posted a drop in January, which would get Q1 real GDP off to a weak start versus consensus expectations of a sustained 3% pace this year.

Euro area: Italian and German politics to take the limelight away from muted inflation This week looks set to be a long wait for the Italian election and the German SPD vote on a new Grand Coalition on Sunday. While most analysts expect a hung parliament in Italy and a small majority in favour in Germany, uncertainty remains high. Euro area headline inflation is likely to continue to decrease for a third straight month to 1.2% yoy in February, which would be the trough this year. Otherwise, credit growth should accelerate above 3.0% yoy.

United Kingdom: Finally, the Brexit plan? The long-awaited speech by the Prime Minister, finally spelling out the “Road to Brexit: A Future Partnership” will surely be delivered this week. It was originally scheduled for last week, but, like so many of the UK’s plans on Brexit, has been delayed. Time is running out. Trade talks are meant to start after the 22, 23 March EU summit.

Emerging Markets: There are monetary policy meetings in Korea, Israel and Ukraine. Sovereign rating reviews in Romania and Lebanon. Real GDP releases in Brazil, India and Poland.

Bloomberg highlights the key weekly events:

ECB President Mario Draghi speaks in Brussels on Monday.

Bank of Korea has policy decision and briefing on Tuesday.

Powell testifies before a House panel on Tuesday. He’ll discuss the Fed’s Semi-Annual Monetary Policy Report and the state of the economy. Powell returns on March 1 before a Senate committee.

Companies announcing earnings this week include: Vale, BASF, Standard Chartered, Bayer, Lowe’s, Galaxy Entertainment Group, Anheuser-Busch InBev, Peugeot, WPP, and London Stock Exchange Group.

U.K. Prime Minister Theresa May delivers a speech on Britain’s relationship with the European Union after Brexit.

A barrage of data is expected out of Japan including retail sales and industrial production Wednesday, and capital spending Thursday.

In China, the official and Caixin purchasing managers’ indexes on Wednesday and Thursday respectively may show growth momentum slowed slightly in February, though the signal may be clouded by the holidays.

Deutsche Bank with its usual breakdown of key daily events:

Monday: We start the week with the UK’s January Finance loans for housing. Across the pond, the January Chicago Fed National activity, February Dallas Fed manufacturing index and new home sales data are also due. Onto other events, the ECB’s Draghi will addresses the EU Parliament while the incoming ECB VP Mr De Guindos will also attend his confirmation hearing at the Parliament. Elsewhere, the ECB’s Coeure, BOE’s Cunliffe and the Fed’s Bullard will speak. The UK’s opposition leader Corbyn is expected to set out the Labour Party’s Brexit position today with the party set to announce that they would stay in the Customs Union. This will cause problems for Mrs May who has said the country will leave. Parliament is generally in favour of staying so this raises the possibility of a lost vote somewhere down the line.

Tuesday: Germany’s flash February CPI and the Euro area’s money supply and credit aggregates are due. Then a range of February confidence indicators are due for the Euro area, France and Italy. In the US, the February Richmond Fed and CB consumer confidence index are due. Further, a range of data including: January advanced goods trade balance, wholesale and retail inventories, durable and capital goods orders along with the December FHFA and S&P corelogic house price index are also due. Onto other events, the Fed’s Powell testifies in front of the House Financial services committee. Elsewhere, the ECB’s Weidmann and Mersch as well as BOE’s Sam Woods will speak. The Brookings Institution will host a conversation with the former Fed Governor Yellen and Bernanke. Finally, the EU negotiator Barnier will brief European affairs ministers.

Wednesday: Overnight, Japan’s January IP and retail sales along with China’s February composite and manufacturing PMI will be out. In early morning, the GfK consumer confidence index for the UK (Feb.) and Germany (March) are also due. Later on, the flash February CPI readings for the Euro area, France and Italy will also be out. Elsewhere, France’s January PPI and 4Q GDP along with Germany’s February unemployment rate are also due. In the US, the February Chicago PMI, second reading on the 4Q GDP and Core PCE as well the January pending home sales data will be due. Onto other events, the EU negotiator Barnier will brief permanent EU representatives on Brexit and the withdrawal text is also expected to be published.

Thursday: In Asia, the February manufacturing PMI for Japan (Nikkei) and China (Caixin) along with Japan’s consumer confidence index will be due. Then the final readings on February manufacturing PMIs across Europe are also due. Elsewhere, the Euro area and Italy January unemployment rate will be out. In the UK, the January net consumer credit lending and mortgage approvals along with the February flash manufacturing PMI are all due. In the US, a range of data will be out, including: January PCE Core, February ISM manufacturing index, personal income and spending, weekly initial jobless claims and continuing claims. Onto other events, the Fed’s Powell is back again in front of the US Senate while the US Transportation Secretary Ms Chao also testifies before the Senate on Trump’s infrastructure plan. The ECB’s Nouy and Lane along with the BOJ’s Kataoka will speak. Elsewhere, senior officials from Euro area finance ministries discuss the banking union and the future role of the ESM.

Friday: Overnight, Japan’s January unemployment rate and February CPI will be out. Then the Euro area’s January PPI, Germany retail sales and the final reading for Italy’s 4Q GDP are due. In the US, the final reading for the February Uni. of Michigan’s consumer sentiment will also be out. Onto other events, the BOE’s Carney and the ECB’s Mersch will speak. The UK’s PM May is expected to outline her vision for a post Brexit trade deal with the EU. Then on Saturday, China’s annual national legislative meetings will start and expected to run for two more weeks.

Finally, here is Goldman with a detailed look at the key US events together with consensus estimates:

The key economic releases this week are the second vintage of Q4 GDP on Wednesday and ISM manufacturing on Thursday. In addition, there are several scheduled speaking engagements from Fed officials this week, including Chair Powell’s semi-annual Monetary Policy Report to Congress on Tuesday and Thursday.

Monday, February 26

08:00 AM St. Louis Fed President Bullard (FOMC non-voter) speaks: St. Louis Fed President James Bullard will give a speech on the U.S. economy and monetary policy at the 34th annual NABE Economic Policy Conference in Washington, D.C. Audience Q&A is expected.

10:00 AM New home sales, January (GS +4.0%, consensus +3.6%, last -9.3%): We expect new home sales to rebound 4.0% in January, following a 9.3% drop last month that we believe was partially weather-related. We expect a favorable fundamental backdrop and the solid trend in single-family building permits to mitigate the negative impact of higher mortgage rates on new homes sales activity.

10:30 AM Dallas Fed manufacturing index, February (consensus +30.0, last +33.4)

03:15 PM Vice Chair for Supervision Quarles (FOMC voter) speaks: Federal Reserve Vice Chair for Supervision Randal Quarles will give a speech titled “An Assessment of the U.S. Economy” at the 34th annual NABE Economic Policy Conference in Washington, D.C. Q&A is expected.

Tuesday, February 27

08:30 AM Durable goods orders, January preliminary (GS -1.3%, consensus -2.5%, last +2.8%); Durable goods orders ex-transportation, January preliminary (GS +0.9%, consensus +0.4%, last +0.7%); Core capital goods orders, January preliminary (GS +0.9%, consensus +0.5%, last -0.6%); Core capital goods shipments, January preliminary (GS +0.3%, consensus flat, last +0.4%): We estimate durable goods orders fell 1.3% in January, reflecting a sharp pullback in commercial aircraft orders. However, we expect the core measures to firm, reflecting the timing of the Chinese New Year and the scope for core orders to rebound. Industrial production of the capex-sensitive business equipment was also quite strong in January.

08:30 AM U.S. Census Bureau Report on Advance Economic Indicators; Advanced goods trade balance, January (GS -$71.0bn, consensus -$72.0bn, last -$72.3bn); Wholesale inventories, January preliminary (last +0.4%): We expect the goods trade deficit to narrow $1.3bn to $71.0bn in January, reflecting a pullback in imports related to the relatively late Chinese New Year, which is likely shifting the timing of imports from January to February/March and could also pull forward some capital goods exports.

09:00 AM S&P/Case-Shiller 20-city home price index, December (GS +1.0%, consensus +0.6%, last +0.7%): We expect the S&P/Case-Shiller 20-city home price index to rise 1.0% in the December report following a 0.7% increase in the prior month. The measure still appears to be influenced by seasonal adjustment challenges, and we place more weight on the year-over-year increase, which climbed to 6.4% in November.

09:00 AM FHFA house price index, December (consensus +0.4%, last +0.4%): Consensus expects the FHFA house price index to rise 0.4% month-over-month, in line with the December pace. The FHFA house price index has a wider geographic coverage than the S&P/Case-Shiller home price index, but is based only on properties financed with conforming mortgages. On a year-over-year basis, FHFA home prices rose at a 6.5% pace in November.

10:00 AM Fed Chair Powell appears before the House Financial Services Committee: Federal Reserve Chair Jerome Powell will appear before the House Financial Services Committee in the first of two days of testimony to deliver the Fed’s semi-annual Monetary Policy Report to Congress and answer questions from lawmakers. The text of his prepared remarks will be released at 8:30 AM ahead of his testimony.

10:00 AM Conference Board consumer confidence, February (GS 127.0, consensus 126.0, last 125.4); We expect consumer confidence to move up 1.6pt to 127.0 in February. Our forecast reflects encouraging consumer sentiment measures in February as well as a rebound in the stock market.

10:00 AM Richmond Fed manufacturing index, February (consensus +15, last +14)

Wednesday, February 28

08:30 AM GDP (second), Q4 (GS +2.4%, consensus +2.5%, last +2.6%); Personal consumption, Q4 (GS +3.7%, consensus +3.6%, last 3.8%): We expect a two-tenths downward revision in the second estimate of Q4 GDP to +2.4%, featuring a one tenth downward revision to personal consumption (to +3.7%) and additional downward revisions to government spending and exports.

09:45 AM Chicago PMI, February (GS 65.5, consensus 65.0, last 65.7); We expect the Chicago PMI to decline 0.2pt to 65.5 after moving down 2.1pt in the January report. Our above-consensus forecast reflects the mixed performance of manufacturing surveys balanced against firmer business confidence reports and encouraging commentary from industrial firms.

10:00 AM Pending home sales, January (GS flat, consensus +0.4%, last +0.5%): Regional housing data released so far were mixed in January. We estimate pending home sales were flat in January, and we note the current level looks elevated relative to other home sales measures. We have found pending home sales to be a useful leading indicator of existing home sales with a one- to two-month lag.

Thursday, March 1

8:30 AM Personal income, January (GS +0.3%, consensus +0.3%, last +0.4%); Personal spending, January (GS +0.2%, consensus +0.2%, last +0.4%); PCE price index, January (GS +0.39%, consensus +0.4%, last +0.1%); Core PCE price index, January (GS +0.30%, consensus +0.3, last +0.2%); PCE price index (yoy), January (GS +1.7%, consensus +1.7%, last +1.7%); Core PCE price index (yoy), January (GS +1.5%, consensus +1.5%, last +1.5%): Based on details in the PPI and CPI reports, we forecast that the core PCE price index rose +0.30% month-over-month in January, which would leave the year-over-year rate unchanged at 1.5%. Additionally, we expect that the headline PCE price index increased 0.39% in January, or 1.7% from a year earlier. We forecast a 0.3% increase in January personal income and a 0.2% gain in personal spending.

09:45 AM Markit US Manufacturing PMI, February (last 55.9)

08:30 AM Initial jobless claims, week ended February 24 (GS 225k, consensus 226k, last 222k): Continuing jobless claims, week ended February 17 (consensus 1,915k, last 1,875k); We estimate initial jobless claims moved back up 3k to 225k in the week ended February 24, after a sizeable decline in the prior week. The trend in initial claims appears to be falling, and we look for another low reading. Continuing claims – the number of persons receiving benefits through standard programs – declined sharply by 73k in the prior week.

10:00 AM ISM manufacturing, February (GS 59.2, consensus 59.0, last 59.1): Regional manufacturing surveys were mixed in February, and we expect ISM manufacturing to tick up to 59.2 in the February report. The Philly Fed (+3.6pt to 25.8) and Kansas City Fed (+1pt to 17) manufacturing sector surveys both strengthened while the Empire State manufacturing survey pulled back (-4.6pt to 13.1). On net, our manufacturing survey tracker—which is scaled to the ISM index—edged down 0.3pt to 58.7.

10:00 AM Construction spending, January (GS +0.6%, consensus +0.2%, last +0.7%): We expect construction spending to increase 0.6% in February, following a 0.7% increase in December that reflected stronger total private construction and public nonresidential construction activity.

10:00 AM Fed Chair Powell appears before the Senate Banking Committee: Federal Reserve Chair Jerome Powell will appear before the Senate Banking Committee in the second day of testimony to deliver the Fed’s semi-annual Monetary Policy Report to Congress and answer questions from lawmakers.

11:00 AM New York Fed President Dudley (FOMC voter) speaks: New York Federal Reserve President William Dudley will give a speech on trade and globalization at an event hosted by the Central Bank of Brazil. Audience Q&A is expected.

04:00 PM Total vehicle sales, February (GS 17.3mn, consensus 17.2mn, last 17.1mn): Domestic vehicle sales, February (consensus 13.2mn, last 13.1mn)

Friday, March 2

10:00 AM University of Michigan consumer sentiment, February final (GS 100.0, consensus 99.0, last 99.9): We expect the University of Michigan consumer sentiment index to edge up 0.1pt to 100 in the February final estimate, reflecting continued improvement among more timely measures of consumer confidence as well as the favorable stock market performance over the last two weeks. The University of Michigan’s survey of 5- to 10-year ahead inflation expectations was stable at 2.5% in the preliminary February report.

There had been much speculation in recent days whether the only thing that matters for markets – Dennis Gartman’s short position – which he put on recently near the market lows and may have been largely responsible for the now traditional algo response to fade any reco from Gartman, had been stopped out as Gartman warned he was about to do on several last week occasions.

This morning, just a few days after Gartman’s “retirement” account blew up following his investment in crypto fraud Riot Blockchain, we can confirm that as of this morning it is once again safe to short stocks: Gartman has been officially stopped out. To wit:

STOCKS HAVE GONE GLOBALLY PARABOLIC TO THE UPSIDE and clearly… at least for the moment… we have been wrong in being short of equities, for there comes a time when the action of the market tells us that we have to admit the error of our ways. P/e multiples may be extended; Price/book value ratios may be egregiously extended; margin usage may be egregiously extended; the price of equities relative to commodity prices may be egregiously extended; the public’s participation may be egregiously extended; the fact that volume expands as markets weaken and that volume contracts as markets rally may be egregiously “extended,” but these facts make no difference for prices are higher… prices have been higher… and prices may move higher still. We may have been right on the bond market for several “units” and we might have been right on gold for a unit or two, and we might have been right on the grains, but we shall be measured most publically by our having been wrong regarding equities in global terms over the course of the past two and one half weeks.

What we shall not do at this point is turn suddenly bullish of equities for that would almost certainly only serve to cause us losses yet again. After 40+ years of being involved in the capital markets we’ve learned few lessons that have truly “stuck” with us; adding to losing trades is one lesson we want to learn yet again and “reversing” one’s position too swiftly after being rather publically wrong is another.

Clearly we have been wrong; clearly going to the sidelines is the proper course of action and clearly paying heed to what is going on in other markets where we have been right is the better course of action. We shall do precisely that.

And this:

Short one Unit of Global Equities: Wednesday, February 14th we sold US, Japanese and European shares, using our International Index as our “gauge” with the Index at 11,896. We sold one unit in total, risking 3% from our initiation point on the trade… or to 12,253… and we are wrong. We have had gold right; we have rather clearly had the bonds right; but of the equities we have clearly been wrong of and since our “stop” has been elected we have no choice but to accept the loss… which is approximately 3.4%…and run to the sidelines upon receipt of this commentary, living to fight another day

Finally, for those wondering what prompted the dramatic squeeze higher in Treasurys on Friday, read on:

We were, until Friday, aggressively short of the US bond market but with the commercial hedgers aggressively long and with the “small traders” rather aggressively short we thought it wise to go to the sidelines, sizeable profits in hand, with the intention of selling the rally in a week or two or three?

By all accounts, this is a fair assessment: there is however one problem.

Yesterday, in a lengthy post on stock buybacks, we showed that corporations – via share buybacks – have been the main buyers of shares in the U.S. since 2009. According to the Federal Reserve’s flow of funds data, non-financial corporates have repurchased a net US$3.9 trillion worth of US equities since 2009. By contrast, households and institutions (insurers and pension funds) have sold a net US$672 billion and US$1.2 trillion respectively over the same period, while mutual funds and ETFs have bought a net US$1.6 trillion.

Of course, none of this would be a problem if companies simply used organic cash flow to repurchase shares: after all it is up to a company, and its shareholders, to decide how to allocate capital in the most shareholder-friendly way.

There is just one rub: as the following chart from SocGen – which we won’t tired of showing – demonstrates, virtually every single dollar use for buybacks not only since the financial crisis, but this century has come from… borrowing money.

In other words, the increase in net debt has matched the increase in net buybacks almost on a dollar for dollar basis. In other words, eliminate the buybacks and corporate America would not have unleashed an unprecedented debt borrowing spree over the past decade.

The good news for corporate America is that so far rates have been low enough to avoid a rendezvous with the piper. However, with rates now rising, Buffett’s warning will soon prove all too prudent.

And in a delightful coincidence, it was none other than Buffett’s quote that we closed our post yesterday:

Buybacks have played far too big a role in the QE era not to cause complications as Quantitative Tightening progresses. In the words of Warren Buffett: “Only when the tide goes out do you discover who’s been swimming naked.”

For now, however, the naked swimming continues without interruption.