- JPMorgan $13 Billion Mortgage Deal Seen as Lawsuit Shield (BBG)

- J.P. Morgan Is Haunted by a 2006 Decision on Mortgages (WSJ)

- World powers, Iran in new attempt to reach nuclear deal (Reuters)

- Keystone Foes Seek to Thwart Oil Sands Exports by Rail (BBG) – mostly Warren Buffet?

- How Would Fed Deal With Debt Ceiling Crisis? Look to Minutes for Clues (Hilsenrath)

- Anything to prevent the loss of prop trading: ‘Volcker Rule’ Faces New Hurdles (WSJ)

- BOE Sees Case for Keeping Record-Low Rate Beyond 7% Jobless (BBG)

- Obama Backs Piecemeal Immigration Overhaul (WSJ)

- Abenomics Seen Cutting Japan Bad-Loan Costs to 2006 Low (BBG)

- Bernanke Signals Fed Target Rate to Stay Low Long After QE (BBG)

- As Trader’s Trial Begins, Name of One Insider Stands Out (NYT)

- U.S. Companies Split on Tax Plan (WSJ)

- Sinopec in talks on Canada site for LNG project (Reuters)

- Zurich Insurance Exiting New China Life (WSJ)

Overnight Media Digest

WSJ

* President Obama, in an interview, said he would accept a piecemeal approach to revamping the immigration system, a shift from calls for comprehensive reform.

* The discovery of a 2006 meeting in which JPMorgan executives decided to continue selling shoddy mortgage securities despite red flags led to the biggest settlement between the government and a U.S. company.

* Two top regulators are raising new-and late-objections to the Volcker rule, arguing it is too soft on banks and threatening to further delay its implementation beyond the year-end deadline set by the Obama administration.

* Devon Energy is nearing a deal to buy GeoSouthern Energy for approximately $6 billion.

* Johnson & agreed to pay at least $2.5 billion to resolve thousands of lawsuits filed by patients who alleged they were injured by the company’s artificial hips.

* A Senate committee chairman released a sweeping proposal to overhaul the U.S. system for taxing corporations’ overseas profits, aiming to improve American firms’ global competitiveness while reducing their ability to dodge taxes offshore.

* Fed Chairman Ben Bernanke said that short-term interest rates may stay low “well after” the jobless rate falls below 6.5 percent, the latest effort by the central bank to assure markets that rates will remain low.

* Banks including Barclays Plc that are enmeshed in the global investigation into potential manipulation of foreign-exchange markets are looking into the possible roles played by their salespeople, according to people familiar with the matter.

* Top officials of the federal agency that regulates vehicle safety said Tuesday they support efforts by auto makers and digital technology companies to develop cars that can drive themselves, but cautioned it will be years before regulators are comfortable allowing fully autonomous vehicles on the road.

FT

JPMorgan Chase agreed to pay $13 billion for mis-selling mortgage securities, in a landmark settlement with the U.S. Department of Justice and state authorities.

Fund managers in the U.S. have been making multi-billion-dollar bets on the recovery of eurozone banks over the past four months, believing that Europe’s stuttering economic recovery will soon gather pace.

A spate of scandals at the Co-operative Bank, the financial services arm of the UK’s largest co-operative, has suddenly tarnished the reputation of mutual and co-operative ownership in the United Kingdom.

Rupert Murdoch and Wendi Deng Murdoch are moving towards an ‘amicable’ divorce settlement this week, according to people familiar with the situation.

Mail.ru, Russia’s largest internet company, is expanding into the United States, by keeping its data centres in the Netherlands.

About a quarter of staff at stockbroker Oriel Securities have left the company in the past few months, highlighting the difficulties of the small-cap broking sector.

NYT

* President Obama is receiving surprising support among some states on allowing the renewal of canceled insurance plans: Of the 13 states that have said they will allow it, all but four are led by Republicans.

* JPMorgan Chase and the Justice Department reached a record $13 billion settlement on Tuesday, wrapping up a series of state and federal investigations that offer a rare glimpse into Wall Street’s mortgage machine before the financial crisis, when it churned out billions of dollars in securities that later imploded.

* In a speech in Washington, the central bank’s chairman, Ben Bernanke, said that even as the stimulus wound down, efforts would remain in place to keep interest rates low.

* Jefferson County, Alabama, will ask a federal court on Wednesday to approve its plan for exiting bankruptcy, including court oversight for a period of 40 years.

* A proposal from Max Baucus, chairman of the Senate Finance Committee, seeks to start the process of lowering corporate tax rates while slowing the flow of jobs and money abroad.

* Johnson & Johnson and lawyers for patients injured by a flawed hip implant announced a multibillion-dollar deal on Tuesday to settle thousands of lawsuits, but it was not clear whether the deal would satisfy enough claimants.

* After a third battery fire in a Tesla car in six weeks, the National Highway Traffic Safety Administration said Tuesday that it had started a formal investigation.

* The chairman of the Federal Communications Commission said on Tuesday that the agency would begin “a diverse set of experiments” next year that would begin to move the nation’s telephone system from its century-old network of circuits, switches and copper wires to one that transmits phone calls in a manner similar to that used for Internet data.

Canada

THE GLOBE AND MAIL

* Less than 24 hours after its debut on Monday night, Sun News axed “Ford Nation”, its highly touted TV talk show starring Toronto Mayor Rob Ford and Councillor Doug Ford

, despite record ratings for the network.

* Still reeling from its $1 billion gas-plant debacle, Ontario’s Liberal government says it will avoid making commitments for large-scale new power projects.

Reports in the business section:

* Relations between the Canadian federal government and the wireless industry have sunk to a historic low, raising the prospect that Canada’s Big Three carriers will face increasing pressure from regulators on issues such as domestic roaming charges.

* An order from low-cost airline flydubai announced at the Dubai Air Show illustrates one of the problems Bombardier Inc faces trying to crack the Airbus-Boeing duopoly with its single-aisle C Series aircraft.

NATIONAL POST

* Toronto city hall has begun the transition to a new world order as key members of Mayor Rob Ford’s staff moved to the office of newly empowered Deputy Mayor Norm Kelly. Ford’s chief of staff Earl Provost moved to the deputy mayor’s office by his own accord, Kelly told reporters Tuesday afternoon.

* Architect Frank Gehry says there are only two buildings in Toronto worth saving: Old City Hall and Osgoode Hall. Everything else is fair game to be torn down, Gehry suggested to Toronto and East York Community Council on Tuesday morning.

FINANCIAL POST

* TransCanada Corp is playing up anxiety over crude-carrying trains in an explicit warning that the growing number of tank cars crisscrossing the continent poses a risk to public safety.

* Canada’s billionaire Weston family is bolstering its luxury presence yet again in preparation for the debut of Nordstrom and this country’s looming luxury showdown.

China

PEOPLE’S DAILY

– The ruling Communist Party of China set up a special group to go around the country to promote the leadership’s latest reform plan, seen as the boldest reforms planned in three decades.

CHINA DAILY

– The northeastern city of Harbin in Heilongjiang province has been hit by its heaviest snowfalls since records began after snow fell for nearly 60 hours, leaving snow piled as high as 50 millimetres in some areas. The storm caused four deaths in neighbouring Jilin province but no casualties were reported in Heilongjiang.

SHANGHAI SECURITIES NEWS

– The plan announced by the Chinese leadership this month to quicken the pace of economic reforms, including stepping up the pace to make the Chinese currency yuan fully convertible, heralds a new phase of active cross-the-border capital flows in and out of China, economists say.

– The Shanghai International Energy Trading Centre, a unit of the Shanghai Commodity Exchange, will start operations on Friday, the latest step taken by the exchange to prepare the launch of China’s first crude oil futures, possibly in the first half of next year.

CHINA SECURITIES JOURNAL

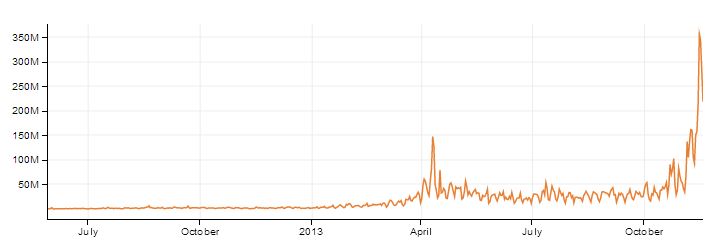

– More and more Chinese are now trading bitcoins, with the daily volume of Chinese trading even exceeding that on the professional platforms of Mt.Gox and BitStamp on Monday, statistics issued by Bitcoinity.org showed.

– Despite a consolidation of China’s stock market on Tuesday, stock index futures continued trading in premiums against spots, indicating optimism sparked by the country’s latest bold reform plan still prevails the markets.

SECURITIES TIMES

– Yields of China’s benchmark 10-year government bonds have hit multi-year highs recently due to the central bank’s tight liquidity stance and are likely to rise above the main 5-percent resistance soon.

CHINA BUSINESS NEWS

– Some Chinese banks are set to suffer losses in the looming bailout plans of Suntech Power, with policy bank China Development Bank possibly losing 1.6 billion yuan ($262 million).

SHANGHAI DAILY

– Anhui province is experimenting with letting farmers mortgage or transfer control of the publicly owned land they farm as China tries to finds ways to create a land market. However, the farmers will not be granted ownership of the land.

Fly On The Wall 7:00 AM Market Snapshot

ANALYST RESEARCH

Upgrades

Best Buy (BBY) upgraded to Buy from Neutral at Citigroup

Cabot Oil & Gas (COG) upgraded to Outperform from Market Perform at Bernstein

Green Plains (GPRE) upgraded to Overweight from Neutral at Piper Jaffray

Layne Christensen (LAYN) upgraded to Neutral from Sell at UBS

Mobile TeleSystems (MBT) upgraded to Equal Weight from Underweight at Barclays

ONEOK Partners (OKS) upgraded to Neutral from Sell at Goldman

Pearson (PSO) upgraded to Buy from Neutral at BofA/Merrill

priceline.com (PCLN) upgraded to Conviction Buy from Buy at Goldman

Downgrades

Boeing (BA) downgraded to Perform from Outperform at Oppenheimer

C.H. Robinson (CHRW) downgraded to Hold from Buy at Deutsche Bank

Dick’s Sporting (DKS) downgraded to Underperform from Market Perform at BMO Capital

Heartland Payment (HPY) downgraded to Market Perform from Outperform at Wells Fargo

Patterson Companies (PDCO) downgraded to Neutral from Buy at UBS

WhiteHorse Finance (WHF) downgraded to Hold from Buy at Wunderlich

Workday (WDAY) downgraded to Market Perform from Outperform at Cowen

Initiations

Allegion (ALLE) initiated with an In-Line at Imperial Capital

Computer Programs (CPSI) initiated with a Hold at KeyBanc

Dunkin’ Brands (DNKN) initiated with a Neutral at Buckingham

FEI Company (FEIC) initiated with a Neutral at Goldman

Flowserve (FLS) initiated with an Outperform at Cowen

IDEX Corp. (IEX) initiated with a Market Perform at Cowen

ITT Corp. (ITT) initiated with a Buy at Stifel

Laredo Petroleum (LPI) initiated with an In-Line at Imperial Capital

Mueller Water (MWA) initiated with a Market Perform at Cowen

Nuverra Environmental (NES) initiated with an Outperform at Cowen

Pall Corp. (PLL) initiated with a Neutral at Goldman

Pennaco Energy Inc Pentair (PNR) initiated with a Buy at Stifel

Rentech Nitrogen (RNF) initiated with a Market Perform at BMO Capital

Starbucks (SBUX) assuming coverage with a Buy at Buckingham

Symmetry Medical (SMA) initiated with a Buy at Wunderlich

Twitter (TWTR) initiated with a Neutral at BTIG

Vitacost.com (VITC) initiated with an Outperform at Imperial Capital

Watts Water (WTS) initiated with a Market Perform at Cowen

Xylem (XYL) initiated with an Outperform at Cowen

HOT STOCKS

Novatek, Gazprom (OGZPY) purchased Eni (E) stake in SeverEnergia for $2.94B

JPMorgan to pursue WaMu receivership funds in separate litigation

Yahoo (YHOO) raised share buyback program by $5B

GE Capital Real Estate (GE) to acquire portfolio of commercial property loans valued at GBP1.4B from Deutsche Postbank

J&J’s (JNJ) DePuy announced $2.5B U.S. settlement to compensate hip system patients

ONEOK Partners (OKS) to invest an additional $650M-$780M in Williston Basin

National Health Investors (NHI) to acquire 25 independent living facilities for $491M

EARNINGS

Companies that beat consensus earnings expectations last night and today include:

Sociedad Quimica (SQM), Gladstone Capital (GLAD), La-Z-Boy (LZB), Xueda Education (XUE)

Companies that missed consensus earnings expectations include:

Lowe’s (LOW), America’s Car-Mart (CRMT), Oculus (OCLS)

Companies that matched consensus earnings expectations include:

Staples (SPLS), Model N (MODN)

NEWSPAPERS/WEBSITES

- Two top regulators, the SEC and and the Commodity Futures Trading Commission, are raising new–and late–objections to the “Volcker rule,” arguing it is too soft on banks and threatening to further delay its implementation beyond the year-end deadline set by the Obama administration, the Wall Street Journal reports

- Electronics retailers (BBY, WMT, SNE, MSFT, RSH, SPLS) are bracing

for a tough holiday season, as already narrow profit margins are expected to be shaved even thinner, the Wall Street Journal reports

- Short-seller Jim Chanos of Kynikos Associates said that shares of international oil majors like Exxon Mobil (XOM) increasingly look like a value trap for investors as cash flows decline and return on capital slides. His comments came a week after Warren Buffett (BRK.A) disclosed a large position in Exxon, Reuters reports

- Sharp Corp. (SHCAY) may get an original equipment manufacturing deal to make copy machines under the Hewlett-Packard (HPQ) brand, sources say, Reuters reports

- Bank of America Corp. (BAC) exceeded $15.06 yesterday, the price on the day before Brian T. Moynihan became CEO about four years ago. The lender rose 1.9%, bringing this year’s gain to 31%. That follows last year’s 109% advance, the best in the DJIA, as Moynihan eased investor concern that mortgage costs would force the bank to issue more stock, Bloomberg reports

- Four Senate Republicans say they’re inclined to support Janet Yellen to be chairman of the Federal Reserve, leaving her nomination one vote short of the 60 needed for confirmation, Bloomberg reports

SYNDICATE

Aeterna Zentaris (AEZS) files to sell common stock and warrants

Atlantic Coast Financial (ACFC) files to sell $42M in common stock

Campus Crest (CCG) files to sell 9.95M shares of common stock for holders

Ceragon Networks (CRNT) files to sell common stock

Clovis (CLVS) files to sell 3.72M shares of common stock for holders

Cytori Therapeutics (CYTX) files to sell 8M shares of common stock for holders

Demandware (DWRE) 3.3M share secondary priced at $57.00 per share

Gladstone (GOOD) files to sell common stock

Graphic Packaging (GPK) to sell 47.87M common shares for holders

National Health Investors (NHI) files to sell 4.5M shars

Northwest Biotherapeutics (NWBO) to offer common stock and warrants

Norwegian Cruise Line (NCLH) files to sell 22M shares for holders

SeaWorld (SEAS) files to sell 15M shares of common stock for holders

Seaspan (SSW) files to sell 3.5M shares of common stock

Spark Networks (LOV) proposes secondary offering of common stock

Yahoo (YHOO) files to sell $1B of convertible senior notes due 2018

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/WlaOGp8Pkoo/story01.htm Tyler Durden