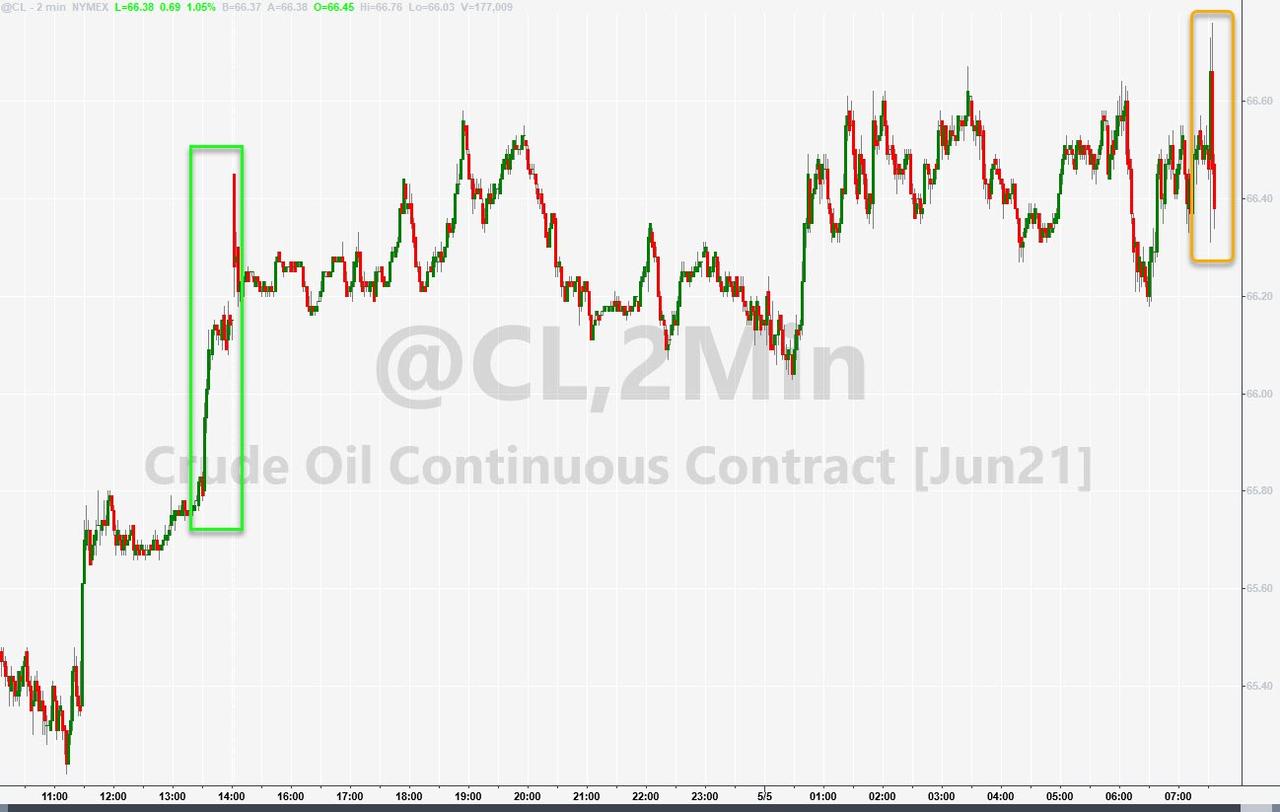

Oil prices are up for a third straight day this morning as the easing of lockdowns in the US and parts of Europe prompted hopes of an increase in fuel demand over the summer months and offset concerns about rising COVID-19 infections in India and Japan.

“A return to $70 oil is edging closer to becoming reality,” said Stephen Brennock of oil broker PVM.

“The jump in oil prices came amid expectations of strong demand as Western economies reopen. Indeed, anticipation of a pick-up in fuel and energy usage in the United States and Europe over the summer months is running high,” he said.

Last night’s surprisingly large crude draw (reported by API) also helped support prices and traders will be looking at the official data to confirm the trend.

API

Crude -7.688mm

Cushing +548k

Gasoline -5.308mm

Distillates -3.453mm

DOE

Crude -7.99mm

Cushing +254k

Gasoline +737k

Distillates -2.896mm

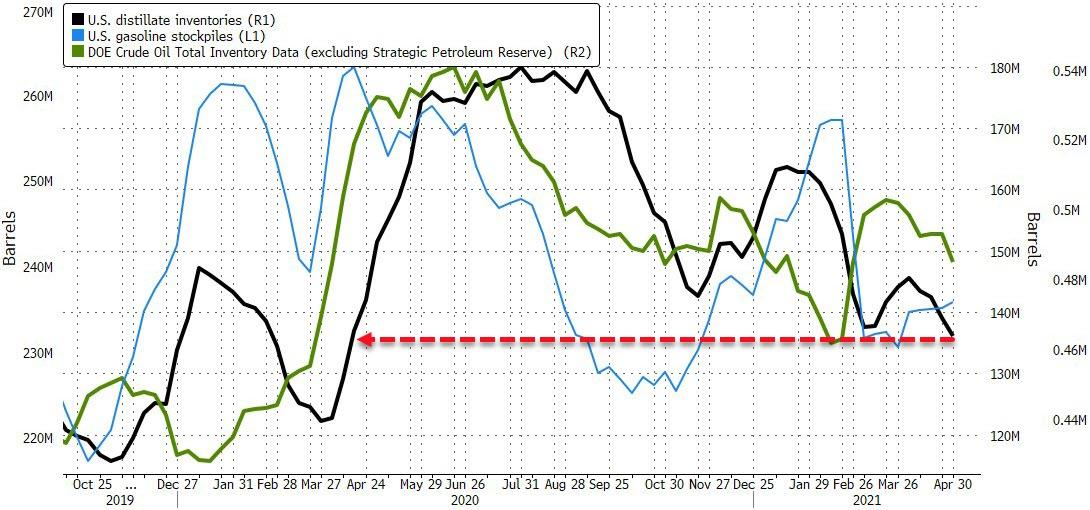

Official DOE data confirmed API’s big crude draw but the major product draws were not as gasoline stocks rose unexpectedly and distillates stocks fell but less than API…

Source: Bloomberg

Distillates stocks fell to their lowest since April 2020 and crude inventories fell to 10-week lows…

Source: Bloomberg

US crude production remains ‘disciplined’ despite surging prices and rising rig counts…

Source: Bloomberg

WTI traded above $66.50 ahead of the official inventory/production print.

“The partial lifting of mobility restrictions, the expectation that tourism will return in the near future, and the lure of the psychologically important $70 mark are all likely to have contributed to the price rise,” Commerzbank analyst Eugen Weinberg said.

This has offset a drop in fuel demand in India, the world’s third-largest oil consumer, which is battling a surge in COVID-19 infections.

“However, if we were to eventually see a national lockdown imposed, this would likely hit sentiment,” ING Economics analysts said of the situation in India.

Meanwhile, gas prices at the pump have surged to a critical level…

Head petroleum analyst Patrick DeHaan at GasBuddy noted in tweets this week that gasoline and diesel prices are roughly level to where they were at this time in 2019. That suggests it might be a normal summer ahead for driving.

And it all comes in the context of what could be the first average $3 retail gasoline in the U.S. since 2014 as part of inflation in the economic recovery.

Peloton Recalls All Treadmills After Dozens Of Injuries, One Death

Exercise equipment maker Peloton is recalling its Tread+ and Tread treadmill machines after dozens of injuries and the death of a child.

Shares of the company are down more than 6% on heavy volume, trading around the $90 handle.

Peloton is advising customers who have already purchased the treadmills to stop using them, contact the company for a full refund, or other qualified remedies.

Three weeks ago, the US Consumer Product Safety Commission (CPSC) released a scathing report over the dangers of treadmills.

CPSC has said there’s been “70 incidents and one child death” related to the treadmills.

This is a massive reversal by Peloton, who called the CPSC report last month “misleading and inaccurate.”

We wonder if JPMorgan Chase & Co. analyst Doug Anmuth is still advising clients to buy the Peloton dip?

Over the years I have published numerous articles with “investing laws” from some of the great investors in history. These laws, or rules, are born of experience, tested by markets, and survived time.

Throughout history, individuals have been drawn into the more speculative stages of the financial market under the assumption that “this time is different.” Of course, as we now know with the benefit of hindsight, 1929, 1972, 1999, and 2007 were not different. They were just the peak of speculative investing frenzies.

Most importantly, what separates these individuals from all others was their ability to learn from those mistakes, adapt, and capitalize on that knowledge in the future.

Experience is an expensive commodity to acquire, which is why it is always cheaper to learn from the mistakes of others.

Importantly, you will notice that many of the same lessons are not new. This is because there are only a few basic “truths” of investing that all of the great investors have learned over time.

The next major down market cycle is coming, it is just a question of when? These rules can help you navigate those waters more safely, because “you’re different this time.”

The Rules 1-10

Common sense is not so common.

Greed often overcomes common sense.

Greed kills.

Fear and greed are stronger than long-term resolve.

There is no vaccine for being overleveraged.

When you combine ignorance and leverage – you usually get some pretty scary results.

Operate only in your area of competence.

There is always more than one cockroach.

Stocks have a gravitational pull higher – over long periods of time equities will rise in value.

Long investing generates wealth.

The Rules 11-20

Short selling protects wealth.

Be patient and learn how to sit on your hands.

Try to get a little smarter every day and read as much as humanly possible – an investment in knowledge pays the best dividends.

Investors sometimes think too little and calculate too much.

Read and reread Security Analysis (1934) by Graham and Dodd – it is the most important book on investing ever published.

History is a great teacher.

History rhymes.

What we have learned from history is that we haven’t learned from history.

Investment wisdom is always 20/20 when viewed in the rearview mirror.

Avoid “first-level thinking” and embrace “second-level thinking.”

The Rules 21-30

Think for yourself – those who can make you believe absurdities can make you commit atrocities.

In investing, that what is comfortable – especially at the beginning – is most often not exceedingly profitable at the end.

Avoid the odor of “group stink” – mimicking the herd and the crowd’s folly invite mediocrity.

The more often a stupidity is repeated, the more it gets the appearance of wisdom.

Always have more questions than answers.

To be a successful investor you must have accounting/finance knowledge, you must work hard and you have to be keenly competitive.

The stock market is filled with individuals who know the price of everything but the value of nothing.

Directional call buying, when consumed as a steady appetite, is a “mug’s game” and is often a path to the poorhouse.

Never buy the stock of a company whose CEO wears more jewelry than your mother, wife, girlfriend or sister.

Avoid “the noise.”

Rules 31-40

Directional call buying, when consumed as a steady appetite, is a “mug’s game” and is often a path to the poorhouse.

Never buy the stock of a company whose CEO wears more jewelry than your mother, wife, girlfriend or sister.

Avoid “the noise.”

Reversion to the mean is a strong market influence.

On markets and individual equities… when you reach “station success,” get off!

Low stock prices are the ally of the rational buyer – high stock prices are the enemy of the rational buyer.

Being right or wrong is not as important as how much you make when you are right and how much you lose when you are wrong.

Too much of a good thing can be wonderful – look for compelling ideas and when you have conviction go ahead and overweight “bigly.”

New paradigms are a rare occurrence.

Pride goes before fall.

Rules 41-50

Consider opposing investment views and cultivate curiosity.

Maintain a healthy level of skepticism as you never know when the Cossacks might be approaching.

Though doubt is uncomfortable, certainty is ridiculous and sometimes dangerous.

When investing and trading, never let your mind dwell on personal problems and always control your emotions.

‘Rate of change’ is the most important statistic in investing.

In evaluating the attractiveness of a company always consider upside reward vs. downside risk and ‘margin of safety.’

Don’t stray from your investing and trading methodologies and timeframes.

“Know” what you own.

Immediately sell a stock on the announcement or discovery of an accounting irregularity.

Always follow the cash (flow).

When new ways of earnings are developed – like EBITDA (and before stock-based compensation) – substitute them with the word… “bullshit.”

2-Bonus Rules

Favor pouring over balance sheets and income statements than spending time on Twitter and r/wallstreetbets.

Always pay attention to what David Tepper and Stanley Druckenmiller are thinking/doing. (Trade/invest against them, at your own risk).

The biggest investing errors come not from factors that are informational or analytical, but from those that are psychological.” – Howard Marks

The biggest driver of long-term investment returns is the minimization of psychological investment mistakes. As Baron Rothschild once stated: “Buy when there is blood in the streets.” This simply means that when investors are “panic selling,” you want to be the one that they are selling to at deeply discounted prices. The opposite is also true. As Howard Marks opined: “The absolute best buying opportunities come when asset holders are forced to sell.”

As an investor, it is simply your job to step away from your “emotions” for a moment and look objectively at the market around you. Is it currently dominated by “greed” or “fear?” Your long-term returns will depend greatly not only on how you answer that question but how you manage the inherent risk.

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham

As I stated at the beginning of this missive, every great investor throughout history has had one core philosophy in common; the management of the inherent risk of investing to conserve and preserve investment capital.

“If you run out of chips, you are out of the game.”

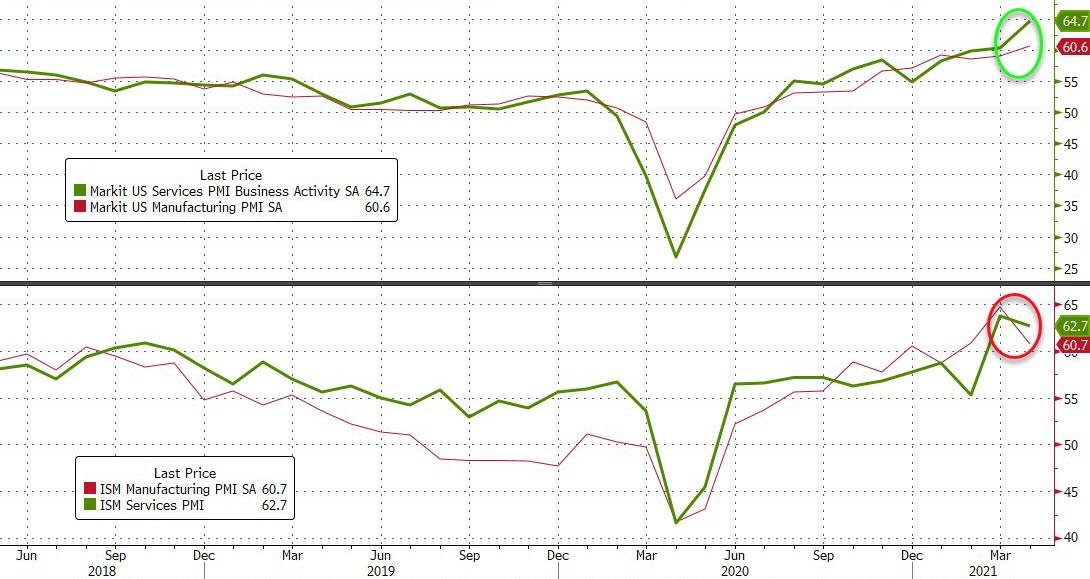

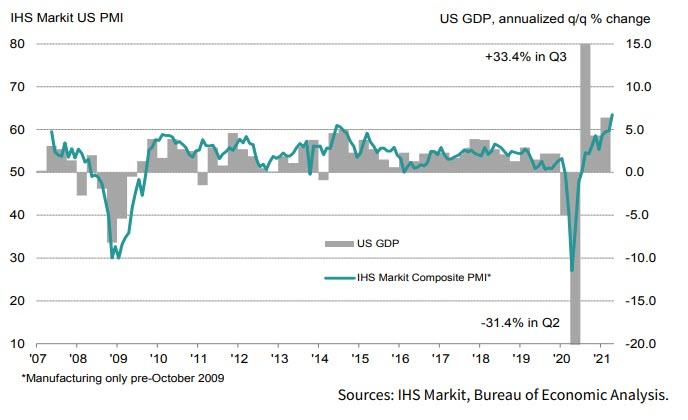

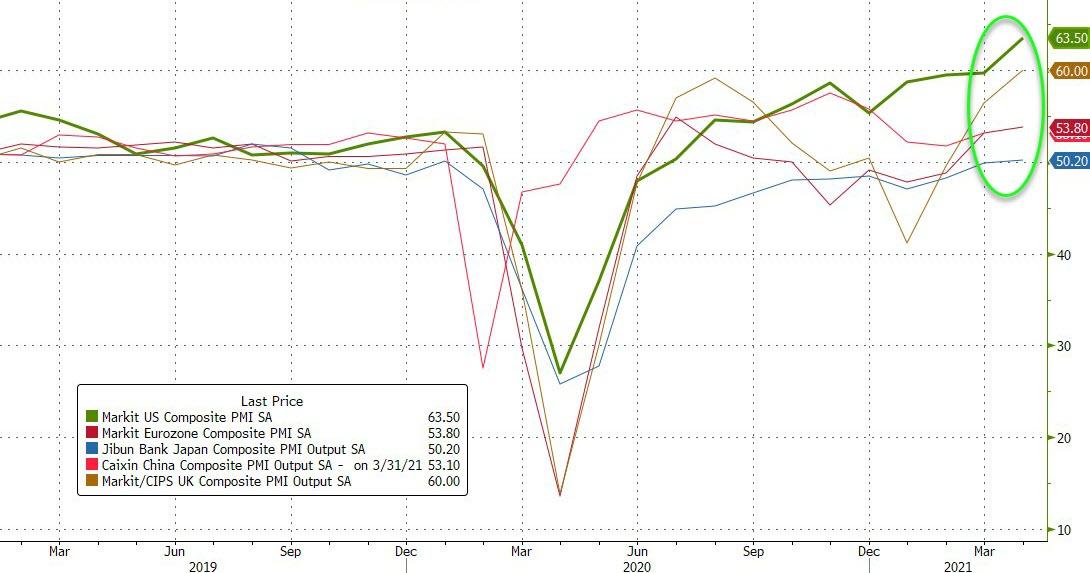

‘Anything But Transitory’ – US Services Sector Surveys Signal Serious Stagflation

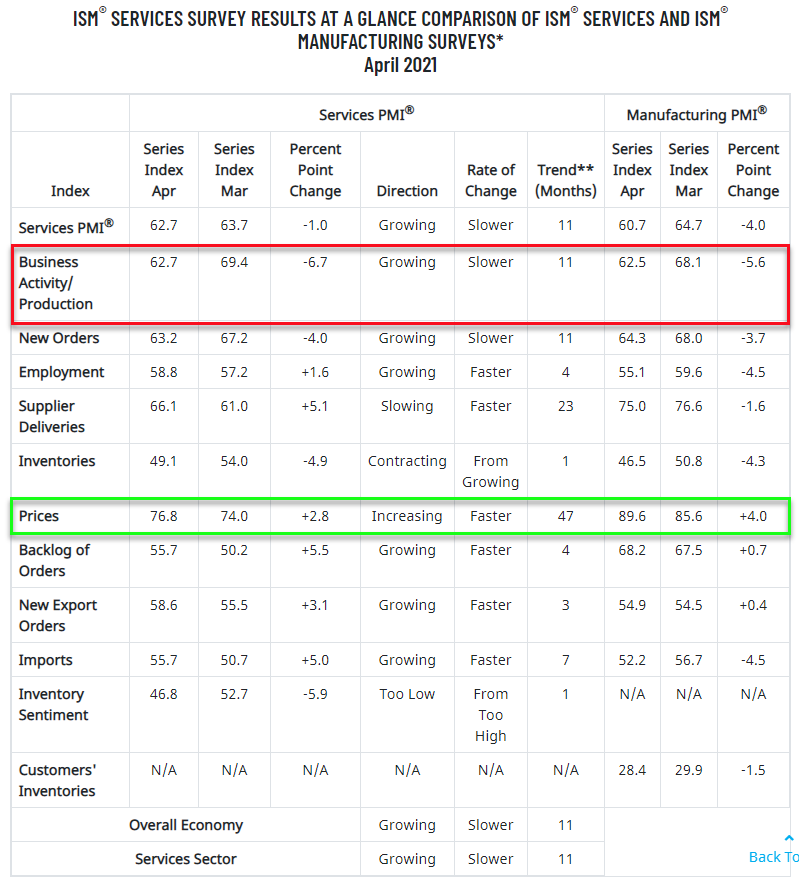

After the mixed picture from manufacturing surveys (PMI higher, ISM lower), analysts expected Services sector surveys to improve in April. And amid continued weakness in hard economic data, Markit’s Services sector survey thrashed expectations (64.7 vs 63.1 exp) and surged to record high (with its 11th month of expansion). However, like its manufacturing brother, ISM Services disappointed expectations and fell from 63.7 to 62.7 (well below the expected rise to 64.1)

Source: Bloomberg

Overall, the picture from ‘soft’ survey-land is ‘mixed’ at best…

Markit Manufacturingrose in April to record high

PMI Manufacturing plunged in April after reaching its highest since 1983 in March

Markit Services jump in April to record high

PMI Services dropped in April from record highs in March

Source: Bloomberg

Stagflation fears remain front and center…

As inflation soars…

“…input costs faced by service sector firms increased at an unprecedented rate in April. The substantial rise in cost burdens was often linked to hikes in supplier prices and greater transportation fees. Companies particularly noted higher costs of plastic, packaging, PPE and fuel.”

And production/output falls…

The IHS Markit Composite PMI Output Index posted 63.5 in April, up from 59.7 in March, to signal the sharpest upturn in private sector output since data collection began in October 2009.

The overall expansion was supported by faster growth in both manufacturing and service sector activity.

“Thanks to the cocktail of a successful vaccine roll-out, the reopening of the economy, ultra-accommodative monetary policy and injection of fresh fiscal stimulus, businesses are reporting the strongest surge in demand seen for at least a decade.

“The upswing in demand has led to one of the strongest months of job creation yet recorded by the survey as business prepares for better times ahead.

“The biggest threat to the outlook remains new virus variants, which will inevitably mean international travel and associated business activity will stay under pressure for some time to come, but in the meantime the domestic economy is faring very well, especially consumer facing industries.

“Another concern is prices, with a record increase in service sector charges highlighting how inflationary pressures are by no means confined to the manufacturing sector. Indicators of price pressures and capacity constraints will need to be monitored closely to assess whether such price rises are transitory.”

Nuclear On Verge Of ESG Inclusion: White House To Subsidize Existing Plants

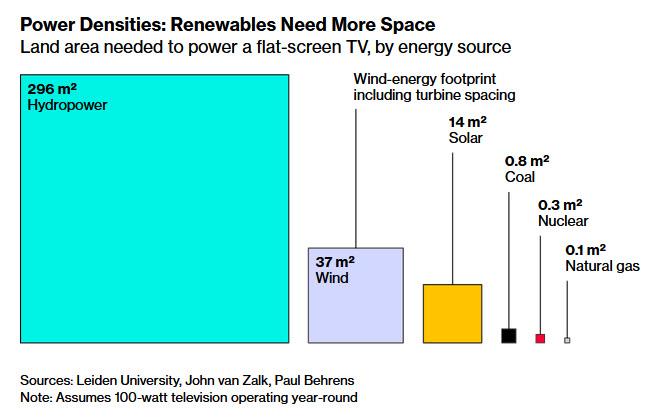

In a move that may infuriate environmentalists and delight investors in uranium stocks (who already saw a surge in their portfolios on Monday following our weekend report “This Is A Game-Changer For Uranium Stocks“) Reuters reports that the White House has privately signaled to lawmakers and stakeholders in recent weeks (so as not to reveal to the broader public) that it supports taxpayer subsidies to keep existing nuclear facilities from closing, bending to the reality that it needs these plants to meet its deliriously aggressively climate goals (which were dissected recently by Bloomberg in “The U.S. Will Need a Lot of Land for a Zero-Carbon Economy“).

The new subsidies in the form of “production tax credits,” would likely be swept into President Joe Biden’s multi-trillion-dollar legislative effort to invest in the nation’s infrastructure and jobs, the Reuters sources said. More importantly being on par with other more “green” sources of energy, it likely means that it is now just a matter of time before even the most rabid members of the ESG crew are forced to admit nuclear to their cool crowd. Wind and solar power producers already get these tax rebates based on levels of energy they generate.

As revealed last month, Biden wants the US power industry to be emissions free by 2035, a schedule which is unachievable without the benefit of nuclear power which as shown below has among the lowest land area footprints…

… and unless the US wants to be covered in reneweable sources of energy, it will have no choice but to support and expand its current NPP arsenal.

Biden is also asking Congress to extend or create tax credits aimed at wind, solar and battery manufacturing as part of his $2.3 trillion American Jobs Plan.

The US has more than 90 nuclear reactors, the most in the world, and the business is the country’s top source of emissions-free power generation. But as discussed here previously, these aging plants have been closing, some as recently as last month, due to rising security costs and competition from plentiful natural gas, wind and solar power, which are rapidly becoming less pricey.

Losing more nuclear plants could make Biden’s zero-emissions goal challenging, if not impossible, analysts have said.

And the punchline: a source quoted by Reuters engaged in the talks and familiar with the White House thinking, said what may be the magic word for far greater gains ahead for uranium stocks, namely that “there’s a deepening understanding within the administration that it needs nuclear to meet its zero-emission goals.”

As we reported earlier this week, New York state’s Indian Point nuclear power plant closed its last reactor on April 30. In Illinois, Exelon Corp threatened to close four reactors at two plants by November, if the state does not implement subsidies.

There is another reason why Biden will cave: the plants provide thousands of union jobs that pay some of the highest salaries in the energy business. Biden’s allies in the building trades unions have lobbied the White House for the production tax credits. The credits also have the support of Democratic Senator Joe Manchin, a moderate from the energy-rich state of West Virginia, who holds outsized power in the evenly divided Senate because he can to block his party’s agenda.

As Reuters adds, preliminary plans for a federal nuclear power production tax credit in deregulated markets bar companies from double-dipping in states that offer similar assistance, according to one of the sources. Companies also would have to prove financial hardship, the source said.

While Biden pledged in his campaign to boost spending for research on new generation of advanced nuclear plants, his White House, like the preceding Trump and Obama administrations, has struggled to devise a blueprint to save the existing reactors. The Biden administration has also supported a Clean Energy Standard (CES) in the infrastructure plan, a mechanism that could support existing nuclear plants.

A CES, which could co-exist with production tax credits, would set gradually more ambitious targets for the power industry to cut emissions until they hit net-zero. The production tax credit could be implemented on a faster timetable and could help save even the Illinois plants, some experts say.

“We’re racing to cut emissions, create jobs, and shore up local economies — allowing nuclear plants to close sets us back on all three fronts,” said Ryan Fitzpatrick, director of the climate and energy program at Third Way, a moderate think tank.

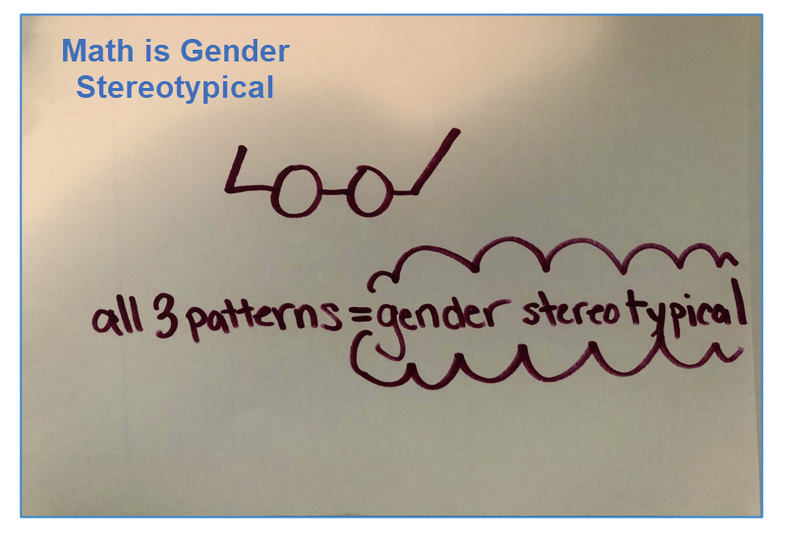

I like to verify things myself and you can do so as well by reading the California Department of Education Mathematics Framework.

In its framework, the Department of Education seeks “Culturally responsive mathematics education.”

Introduction Highlights

Active efforts in mathematics teaching are required in order to counter the cultural forces that have led to and continue to perpetuate current inequities. Mathematics pathways must open mathematics to all students, eliminating option-limiting tracking. [i.e. no advance classes].

implementation of this framework and the standards, teachers must be mindful of other considerations that are a high priority for California’s education system including the Environmental Principles and Concepts (EP&Cs) which allow students to examine issues of environmental and social justice.

Teaching for Equity Highlights

The evolution of mathematics in educational settings has resulted in dramatic inequities for students of color, girls, and students from low income homes.

Teachers are encouraged to align instruction with the outcomes of the California ELD Standards, which state that linguistically and culturally diverse English learners receive instruction that values their home cultures.

Need to Broaden Perceptions of Mathematics

I did not go through all the chapters. Reason uncovered these gems.

The inequity of mathematics tracking in California can be undone through a coordinated approach in grades 6–12.

Middle-school students are best served in heterogeneous classes.

The push to calculus in grade twelve is itself misguided.

To encourage truly equitable and engaging mathematics classrooms we need to broaden perceptions of mathematics beyond methods and answers so that students come to view mathematics as a connected, multi-dimensional subject that is about sense making and reasoning, to which they can contribute and belong.

Sabotage the Best

Reason concludes, and I agree “If California adopts this framework, which is currently under public review, the state will end up sabotaging its brightest students. The government should let kids opt out of math if it’s not for them. Don’t let the false idea that there’s no such thing as a gifted student herald the end of advanced math entirely.”

Instead, and in the name of “equity”, the proposed framework aims to keep everyone learning at the same dumbed down level for as long as possible.

The intention is clear. The California Board of Education intends to sabotage the best and brightest, hoping to make everyone equal.

The public does not support these polices. Indeed, it is precisely this kind of talk that nearly got Trump reelected.

Biden should speak out against such nonsense, but he won’t. He is beholden to Teachers’ Unions and Boards of Education.

Care to complain? If so the California Department of Education posted these ways.

Phone Number and Address

Phone: 916-319-0598

Instructional Quality Commission

1430 N Street, Room 3207

Sacramento, CA 95814

Fax: 916-319-0172

Social and Mathematical Justice Q&A

Q: Who is the arbiter of environmental, mathematic, and social justice?

A: The California board of Education. They intend to cram it down your child’s throat and dumb down gifted kids no matter what their parents believe or how vigorous the objections.

If you wish to protest these absurd policies, phone or write the board of education as posted above.

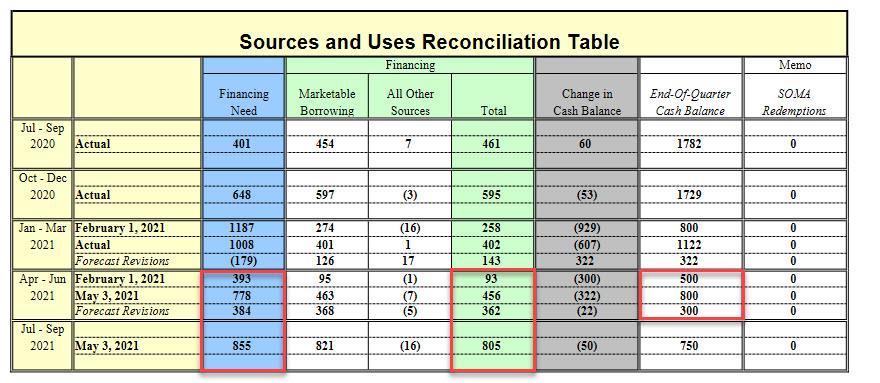

Treasury Keeps Bond Auctions Sizes Unchanged At Record High As It Warns On Debt Ceiling

Two days after the US Treasury surprised rates watchers by unveiling that it would sell nearly 5x more Treasuries in the current quarter than previously expected ($465BN vs $95BN) and $1.3TN over the second half of the fiscal year, while reducing the amount of cash released from the TGA…

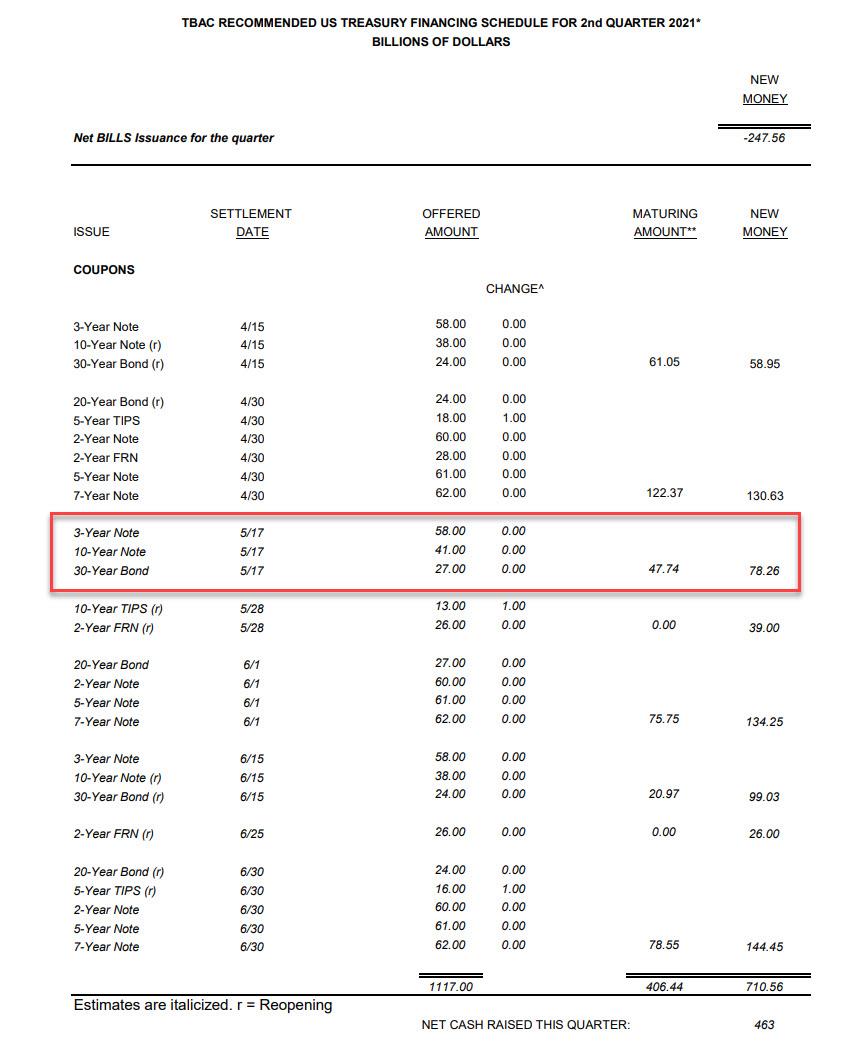

… at 830am on Wednesday in its latest quarterly Refunding Announcement, the Treasury announced that it would keep its quarterly auction of long-term coupon debt unchanged, and at an all time high, of $126 billion (vs $84 billion a year ago)to refund approximately $47.7 billion of Treasury notes and bonds maturing on May 15, 2021. This issuance will raise new cash of approximately $78.3 billion. The securities to be auctioned off are:

$58BN in 3-year notes maturing 2024 on May 11, unch from $58BN in February

$41BN in 10-year notes maturing 2031 on May 12, unch from $41BN in February

$27BN in 30-year bonds maturing 2051 on May 13, unch from $27BN in February.

As Bloomberg notes, this was the first time in more than a year that the refunding total hasn’t risen, “suggesting that financing needs have peaked.”

The Treasury said that other nominal note and bond auction sizes are expected to remain unchanged during the quarter as well, the Treasury said adding that as usual, the balance of Treasury financing requirements over the quarter will be met with weekly bill auctions, cash management bills (CMBs), and monthly note, bond, Treasury Inflation-Protected Securities (TIPS), and 2-year Floating Rate Note (FRN) auctions.

“Between April 2020 and February 2021, Treasury substantially increased issuance sizes for nominal coupon and FRN securities and has announced its intention to gradually increase TIPS issuance this year” the refunding announcement said. “Treasury believes that these previously announced changes continue to provide sufficient capacity for Treasury to address near-term projected borrowing needs. Accordingly, Treasury is announcing that it anticipates no changes to nominal coupon and FRN auction sizes over the upcoming May to July 2021 quarter.”

Discussing its projected financing needs, the Treasury said it “continues to face uncertain and sizable borrowing needs due to expenditures associated with the government’s response to COVID-19 as well as the impact of the pandemic on economic activity and government receipts.” It also said that it plans to address any seasonal or unexpected variations in borrowing needs over the next quarter through changes in regular bill auction sizes and/or CMBs.

The Treasury also warned that it may face challenges if Congress fails to suspend or increase the federal debt limit when the current suspension runs out at the end of July. On previous occasions, the Treasury has used various measures to keep servicing federal debt outstanding while lawmakers and the White House wrangled over raising the ceiling. But this year could bring added strains, the department said.

The Bipartisan Budget Act of 2019 suspended the debt limit through July 31, 2021.[1] Treasury expects that Congress will raise or suspend the debt limit in a timely manner. If Congress has not acted by July 31, Treasury, as it has in the past, may take certain extraordinary measures to continue to finance the government on a temporary basis. In light of the substantial COVID-related uncertainty about receipts and outlays in the coming months, it is very difficult to predict how long extraordinary measures might last. Treasury is evaluating a range of potential scenarios, including some in which extraordinary measures could be exhausted much more quickly than in prior debt limit episodes.

Consistent with guidance provided in November, TIPS (inflation-linked) auctions during the quarter will increase by $1b each relative to most recent comparable new issue or reopening; that would mean a $13b 10-year reopening in May, a $16b 5-year reopening in June and a $16b 10-year new issue in July:

10-year TIPS reopening in May of $13 billion

5-year TIPS reopening in June of $16 billion

10-year TIPS new issue in July of $16 billion

While flexibility will be maintained to adjust TIPS issuance plans at each quarterly refunding announcement, Treasury expects total gross issuance of TIPS to increase by $10BN to $20BN in CY 2021.

Also notably, there was no new guidance on issuance of 20-year bonds, a security the Treasury resurrected last year. But the department said FINRA which currently publishes aggregate statistics on Treasury securities volumes, detailed last week that it will modify that report in May to provide greater detail on the 20-year securities sector going forward.

The Treasury also didn’t provide any fresh insights on its continuing analysis of the idea of issuing debt linked to the Secured Overnight Financing Rate, the Federal Reserve’s preferred replacement rate to Libor.

The Treasury also addressed the all important topic of its cash balance and bill issuance, and continuing our observations from Monday, it said that it now expects its cash balance to decline to $450BN at the expiration of the debt limit suspension on July 31 resulting from reductions in bill issuance; which are expected to reduce bills outstanding by around $150BN. However, the actual cash balance on July 31 may vary from this assumption based on changes to expected outflows in that period. The reduction in the cash balance between now and July 31 will be achieved by using cash on hand to cover near-term outlays and modest reductions in bill issuance.

Based on current forecasts, Treasury estimates that the reduction in bills outstanding between now and July 31 could be about $150 billion, which is approximately one-third the size of the decline in bill supply that has already occurred since the February 2021 refunding. As expectations for receipts and outlays evolve over the coming months, this estimated reduction in bills outstanding may also change, but Treasury does not anticipate bill issuance to be as volatile as it has been in the past when prior debt limit suspensions expired.

As a reminder, the Treasury is still holding a huge (if smaller) cash pile and the prior ramping up in auctions means the Treasury doesn’t need to further boost its debt issuance even after the enactment of the $1.9 trillion March pandemic-relief bill. The Treasury accumulated a record cash balance of $1.8 trillion at one point last year.

Over the upcoming quarter, Treasury will also continue to supplement its regular benchmark bill financing with a regular cadence of CMBs. Treasury anticipates that weekly issuance of 6- and 17-week CMBs for Thursday and Tuesday settlement, respectively, will continue at least through the end of July. Maintaining these CMBs will provide the requisite flexibility to address potential changes in borrowing needs resulting from uncertainty associated with the fiscal outlook.

While there were no major surprises in this quarterly refunding, Bloomberg reminds us that big decisions on debt issuance loom later this year, with the government’s borrowing needs are set to shrink rapidly as Covid-19 stimulus spending ebbs and the economic recovery sets in (unless of course Universal Basic Income becomes a permanent fixture of the USSA). While President Joe Biden is calling for $4 trillion in further initiatives, those are aimed over several years, with tax hikes planned to help pay for them.

As such, Treasury Secretary Janet Yellen and her team will need to decide whether and how quickly to shrink sales of so-called coupon-bearing debt — securities that pay interest. Her predecessor Steven Mnuchin actively sought to lengthen the average maturity of Treasuries to take advantage of historically low longer-term rates. The majority of Wall Street bond dealers had predicted the Treasury would make no changes to nominal coupon-bearing debt auctions. Several forecast a reductions beginning as early as August. Sales of notes and bonds ranging from seven to 30 years have doubled in size thanks to Covid-19 spending, HSBC Holdings Plc estimates show.

“Even if Congress passes a large-scale infrastructure package which is funded over a five to 10-year horizon, Treasury’s current auction schedule leaves it more than adequately financed in coming years,” Jay Barry, a strategist at JPMorgan Chase & Co. wrote in a note last week. “Treasury should begin making cuts to its auction sizes in relatively short order.”

Refunding statement aside, the minutes from the TBAC’s most recent meeting noted that historically large issuance sizes in recent quarters had generated sufficient financing capacity at this time, and that coupon sizes could likely be reduced later this year or early next year. TBAC also debated whether it would be beneficial to make near-term cuts for specific maturity points, such as the 20-year bond, or to hold off on recommending any cuts until it becomes clearer that Treasury should begin more broad-based cuts.

Committee also recommended that Treasury continue to increase TIPS auction sizes at a pace consistent with the $10-20b increase in gross issuance for CY2021 that was announced at the November 2020 quarterly refunding, and suggested considering the high-end of the range by increasing the size of 5-year TIPS auctions by slightly more than the increases in other TIPS securities based on relatively high demand.

TBAC then reviewed a presentation on lessons learned from recent episodes of market volatility and stressed liquidity conditions in the Treasury market, examining market structure, dynamics in the non-bank financial sector, and potential ways to improve market functioning during periods of heightened uncertainty.

The presenting member suggested potential solutions designed to assist Treasury market participants in navigating periods of heightened volatility, rather than attempting to prevent these episodes. He also said that the most promising policy proposals were the adjustments to the leverage ratio and the standing repo facility

Fred Pietrangeli, director of the Office of Debt Management, noted that the September cash balance estimate of $750 billion assumes that Congress has taken actions to resolve the debt limit. Pietrangeli said that despite the net marketable borrowing needs, primary dealers anticipate Treasury will be overfinanced in upcoming fiscal years and may need to consider coupon cuts either later this year or early next year.

Debt Manager Kyle Lee described more details regarding dealers’ expectations for Treasury issuance, noting that dealers argued that for FY2022 and beyond, reductions in nominal coupon auction sizes could help avoid “a significant decline in bill supply” and were expected across the curve.

Some primary dealers suggested that Treasury could consider greater auction size reductions in tenors that appeared to have relatively less demand at auction or that were increased relatively more over the last year.

Facebook’s oversight board on Wednesday decided to uphold the company’s indefinite suspension of former president Donald Trump, claiming that “Trump’s posts during the Capitol riot severely violated Facebook’s rules and encouraged and legitimized violence.”

The Board also found Facebook violated its own rules by imposing a suspension that was ‘indefinite.’ This penalty is not described in Facebook’s content policies. It has no clear criteria and gives Facebook total discretion on when to impose or lift it.

“Mr. Trump created an environment where a serious risk of violence was possible,” the oversight board continues.

The oversight board also said “Facebook violated its own rules by imposing a suspension that was ‘indefinite.’” because “This penalty is not described in Facebook’s content policies.”

The Board’s decision is accompanied by ‘evidence’ in the Trump case which catalogues the former president’s actions leading up to the January 6th ‘insurrection’ at the Capitol.

Elections are a crucial part of democracy. On January 6, 2021, during the counting of the 2020 electoral votes, a mob forcibly entered the Capitol Building in Washington, D.C. This violence threatened the constitutional process. Five people died and many more were injured during the violence. During these events, then-President Donald Trump posted two pieces of content.

At 4:21 pm Eastern Standard Time, as the riot continued, Mr. Trump posted a video on Facebook and Instagram:

I know your pain. I know you’re hurt. We had an election that was stolen from us. It was a landslide election, and everyone knows it, especially the other side, but you have to go home now. We have to have peace. We have to have law and order. We have to respect our great people in law and order. We don’t want anybody hurt. It’s a very tough period of time. There’s never been a time like this where such a thing happened, where they could take it away from all of us, from me, from you, from our country. This was a fraudulent election, but we can’t play into the hands of these people. We have to have peace. So go home. We love you. You’re very special. You’ve seen what happens. You see the way others are treated that are so bad and so evil. I know how you feel. But go home and go home in peace.

At 5:41 pm Eastern Standard Time, Facebook removed this post for violating its Community Standard on Dangerous Individuals and Organizations.

At 6:07 pm Eastern Standard Time, as police were securing the Capitol, Mr. Trump posted a written statement on Facebook:

These are the things and events that happen when a sacred landslide election victory is so unceremoniously viciously stripped away from great patriots who have been badly unfairly treated for so long. Go home with love in peace. Remember this day forever!

At 6:15 pm Eastern Standard Time, Facebook removed this post for violating its Community Standard on Dangerous Individuals and Organizations. It also blocked Mr. Trump from posting on Facebook or Instagram for 24 hours.

On January 7, after further reviewing Mr. Trump’s posts, his recent communications off Facebook, and additional information about the severity of the violence at the Capitol, Facebook extended the block “indefinitely and for at least the next two weeks until the peaceful transition of power is complete.”

The Board also said that Facebook must review the decision, which also applies to Instagram, within six months. Trump has nearly 60 million followers across both platforms.

The decision comes one day after Trump announced a new ‘platform’ called ‘From the desk of Donald J. Trump,‘ which allows him to post comments, images and videos.

The site allows users to like or share posts on their own Facebook or Twitter accounts, but they cannot reply. People can also “sign up for alerts” delivered via email.

The tool is funded by Trump’s Save America and Make America Great Again political action committees.

“President Trump’s website is a great resource to find his latest statements and highlights from his first term in office, but this is not a new social media platform,” wrote senior Trump adviser Jason Miller, adding “We’ll have additional information coming on that front in the very near future.”

🚨President Trump’s website is a great resource to find his latest statements and highlights from his first term in office, but this is not a new social media platform. We’ll have additional information coming on that front in the very near future.🚨 https://t.co/m9ymmHofmI

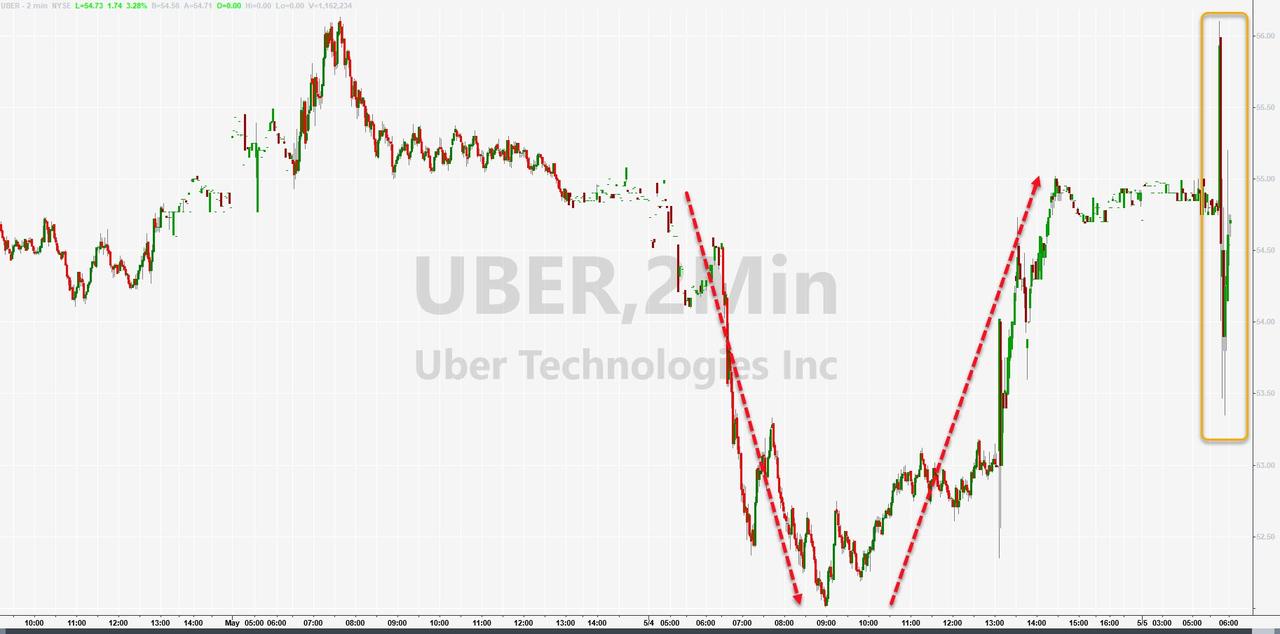

Uber And Lyft Now Face Driver Shortages, Biden Unveils More Anti-Business, ‘Gig Worker’ Regulatory Threats

Update (0915ET): The Biden administration has canceled a signature Trump-era rule that would’ve eased businesses’ ability to legally consider workers as independent contractors.

The U.S. Labor Department said the rollback was necessary to broadly extend wage protections while cracking down on employer abuses.

A final rule, issued Wednesday, rescinded the pro-business regulation without replacing it with a new interpretation of when workers can function as independent contractors and when they must be classified as employees under federal law, who are entitled to minimum wage and overtime pay.

For some reason the shares of Uber and Lyft are up on this anti-business move…

* * *

In addition to dealing with potential looming regulation nationwide that could turn “contractors” into “employees” – essentially eviscerating their entire business models – Uber and Lyft are also in the midst of dealing with a nationwide shortage in drivers.

“A lot of gig workers should be classified as employees,” U.S. Labor Secretary Marty Walsh said last week, according to Reuters. This added to President Joe Biden’s campaign promises of making sure that gig workers received benefits.

The comments cause shares of Uber and Lyft to temporarily plunge, with both names falling between 8% and 12%, before recovering.

In addition to the looming threat to their business models, the companies are also having trouble serving the increased demand. Reuters notes that “many U.S. drivers still unwilling to return to the road over safety and financial concerns, meaning the companies risk disgruntled customers or higher costs to incentivize drivers to return.”

Bernstein said in a recent note: “(It’s) a better problem to have, but one that could put wrinkles in profitability timelines it if persists.”

Lyft reported earnings on Tuesday after the bell, showing signs of a continued pandemic recovery and beating top and bottom line expectations, according to CNBC. Uber is expected to report earnings on Wednesday after the bell. The consensus EPS estimate for Uber heading into Wednesday is -$0.35 and revenue is expected to come in at $3.28 billion.

“We continue to believe there is still significant pent-up demand for mobility that will take time to play out,” Lyft CEO Logan Green said on the company’s conference call.

Infected Indian Foreign Minister Disrupts G-7 Summit In London

As India’s brutal second COVID-19 wave spills over its borders and across the region, a team of forecasters at the Indian Institute of Science in Bangalore has warned – using a mathematical model – that deaths could double as soon as next week, India’s foreign minister is now self-isolating after two delegates to recent G-7 meetings in London tested positive to the virus, Bloomberg reports.

India’s External Affairs Minister Subrahmanyam Jaishankar was reportedly informed that he had been exposed to somebody infected with the virus on Wednesday, one day after Jaishankar held a socially distanced in-person meeting with UK home secretary Priti Patel on Tuesday, where the two agreed on a “migration and mobility deal’ which will provide a “bespoke route” for young professionals from India looking to live and work in the UK. Jaishankar also met Antony Blinken, the US secretary of state, earlier this week.

Subrahmanyam Jaishankar meeting with US Secretary of State Antony Blinken

As one twitter wit pointed out, the incident is like a metaphor for India’s current situation, as more public-health experts warn that India’s worsening outbreak risks reviving outbreaks in the US and Europe. Many countries have moved to cut off all non-essential travel between India for exactly this reason.

Okay this is quite a metaphor

*INDIA MINISTER AT G7 TO SELF-ISOLATE ON POSSIBLE COVID EXPOSURE

As Bloomberg points out, the blowback could turn into an embarrassment for the US and the Biden Administration. The announcement could swiftly shut down a high-profile event that is supposed to mark the G-7 debut of Secretary of State Antony Blinken. The two-day event is being hosted by the UK.

Fortunately, according to the FT, members of the Indian delegation hadn’t yet attended G7 meetings in Lancaster House, London, where talks took place on Tuesday and continued on Wednesday.

The meetings, the first face-to-face gathering of the group’s foreign ministers in more than two years, were set to include representatives from Australia and India in some of the sessions alongside the G-7 advanced economies as the UK (and the US) seeks to strengthen its ties within the Indo-Pacific region.

British PM Boris Johnson defended the decision to hold the G7 meetings in person, arguing that it was important for the government “to try to continue as much business” as possible despite the pandemic.

“We have a very important relationship with India and with our G7 partners”, he said while campaigning ahead of Thursday’s local elections. “As I understand it, what has happened is the individuals concerned are all isolating now,” he said.

BoJo added that he would have a meeting with Jaishankar on Wednesday afternoon via Zoom.

Officials believe that, based on discussions with Public Health England, those who attended meetings with Jaishankar have a low risk of contracting the virus. Still, fears about possible spread are already disrupting the summit, and could force delegates to attend meetings remotely from their hotel rooms.

Meanwhile, India reported a record 3,780 deaths on Wednesday for an overall toll of 226,188, along with 382,315 new cases, taking its outbreak past 20.6 million infections.