Now that Tesla’s most recent numbers are out it may be time to revisit what the company is worth. While the numbers came in solid and better than some analysts expected they did not blow the doors off the hinges and leave investors in awe. Lurking in the shadows are concerns at just how honest Tesla’s numbers really are. History has shown time and time again that markets can hide from reality for only so long. Tesla’s stock price continues to hang on but continuing signs of the company’s challenging path forward continue to leak out.

With over 100 different electric cars expected to hit the market by 2025, it is difficult for a realist to envision Tesla being able to remain in the position it is today. The rapid approach of real competition into the rather small Electric Vehicle market is occurring at a time when auto sales may be on the wane. This could translate into tight profit margins and a situation similar to what we witnessed in 2008 when the automobile industry fell off a cliff resulting in a government bailout of GM and Chrysler.

Needless to say, a great number of factors influence how a stock is valued. A huge part of the sugar high allowing Tesla’s valuation continues to be that climate change exists and the idea electric vehicles are a big part of the answer to halting it. It could be said that Elon Musk is the “Pied Piper” of EVs leading society down a path that may eventually disappoint even his most loyal followers. Musk appears to have a great deal riding on government favors paving Tesla’s way forward with generous subsidies. Whether EVs live up to their reputation of being environmentally friendly is a matter still being debated and many people have come to the conclusion that EVs do not live up to their promise.

Several other issues haunt Tesla, one has to do with China. A few days ago the video of a protestor at the Shanghai Auto Show “went viral” after he stood on top of a Tesla vehicle and decrying the car’s brakes. Shortly after the incident, a CCTV broadcaster has called for an investigation into Tesla’s brake failures, some people are taking this as a sign China’s love affair with Elon musk is coming to an end.

Tesla Has Made China A Key Part Of Its Future

This could have huge ramifications for the future of both Musk and Tesla because of the huge investment the company has made in China.The notion that Chinese state media has turned negative and is looking for answers underscores the idea China may have initially embraced Tesla in order to steal its technology.

Also, issues concerning the overall quality of Tesla’s cars, or lack of it, have garnered a great deal of attention. While this has been brushed aside by the majority of Tesla lovers, Tesla’s US made vehicles are scoring in the cellar when it comes to quality. As Electrec reported earlierthis year, Tesla ranked lowest on J.D. Power 2020 quality study, with 250 problems per 100 cars. The quality survey was based on roughly 1,250 Tesla owners with most of the respondents being the proud owners of a Model 3.

Needless to say, much of the “aura” surrounding Tesla continues to flow from Musk himself. It appears many people view this man as almost god-like, a genius with superman qualities. Somehow they are able to overlook the fact the words coming out of his mouth often conflict with reality. Musk skeptics such as myself, are appalled at how so much of his empire has been grown from a foundation of government subsidies.

Government support is a major theme of all Elon Musk’s companies, and without it, none of them would exist. Woven into this is the issue of “corporate incest” and Tesla’s acquisition of ailing SolarCity in an all-stock $2.6 billion merger. At the time Musk owned 22% of SolarCity which was founded by his cousins. The merger was promoted on the idea that Tesla’s mission since its inception was part of Elon Musk’s overall “Secret Tesla Motors Master Plan” to expedite the world’s transition to sustainable energy and away from a fossil fuel economy.

Tesla’s valuation remains a bit over the moon considering on Friday it closed with the stock at a whopping P/E ratio of 710 times earnings and a market cap of over 649.8 billion dollars. Those of us without a great love for Tesla or Elon Musk see this as the poster child of absurdity. By comparison, Volkswagen, which sold over 10 million vehicles last year has a market cap of $79 billion and auto giant Toyota around $246 billion.

While valued as the most valuable car company in the world, recent earning for Tesla indicates its profits were based on $518 mm of regulatory credit sales and a $101 positive gain from its Bitcoin position and sales. Strip these out and it seems that Tesla lost $181mm selling cars. Still, it is difficult to deny another major factor keeping Tesla aloft is the promise of a shit load of government money flowing from Biden’s new $2 trillion infrastructure package. Many Tesla enthusiasts are counting on this transfer of wealth to move the company forward.

While Tesla sported a valuable advantage by being the first big player in the electric vehicle (EV) category it is not protected by a great number of patents. The big advantage Tesla has enjoyed with other manufacturers being slow to release EV cars is not expected to last. Much of Tesla’s technology is easy to replicate and most auto manufacturers have lines of EVs finally rolling off their production lines this year and next. Many of these cars will come at far cheaper prices and Tesla’s competitors will also be offering their customers service shops and trade-ins.

Ford’s New F-150 Will Challenge Tesla

This means Tesla’s first mover advantage may vanish overnight. A great deal will depend on how Tesla’s new pickup truck fairs against such rivals as Ford’s new electric F-150. Any sign of failure on the part of Tesla could result in a major fall from grace and bring into question Tesla’s staying power in the industry.

Ironically up until now, Musk’s greatest strength may have been that so many investors doubt his ability to perform. This means that a slew of impatient clowns have shorted Tesla stock in search of quick profits. These bearish investors have continually shot themselves in the foot by constantly finding reasons to rush to the exits in short-covering panics. This not only invariably brings the share price back up but has created a self-feeding loop accounting for much of the companies success and oversized profile in the automobile sector.

When all is said and done, the 64,000 dollar question remains, what is Tesla worth? Still more important is, what will it be worth in the future. Sadly, this article is not about to predict a number considering Elon Musk has proved he has more lives than a cat. Time and time again reports of his demise have proven to be premature. It seems every week creates a slew of new articles about Tesla and what is occurring in the highly speculated electric vehicle sector. Like many people that are predisposed to discount hype from the media, you should color me skeptical about how well Tesla will deal with the coming onslaught of competition.

You Know It’s Bad When… CNN Calls Out Biden Over Anti-Science Mask Use

President Biden is coming under fire from both sides of the aisle for constantly wearing a mask despite announcing that vaccinated people no longer require face coverings when outdoors. In other words, it’s simply virtue signaling at this point.

As The Hill (!?) notes, days later after announcing the loosened guidelines from the CDC, “Biden was spotted with a mask while walking outside to Marine One with first lady Jill Biden, even though both have been vaccinated and no others were around.”

The president again donned a mask at a Georgia drive-in rally while his wife spoke a few feet away, despite nobody else being on stage.

Biden has strived to set an example for Americans by wearing a mask in public frequently during his first months in office, pleading with the public that it was a key tool to end the pandemic. But health experts say the country is reaching a tipping point where Biden now must alter his behavior to reflect how vaccines can lead to a return to normal. –The Hill

“I actually think it would do so much good for the president to be modeling at this point the really critical times when people should be wearing a mask, and letting people know here is the benefit of the vaccine: You don’t need to be wearing a mask during these other times,” said ER physician and former Baltimore health commissioner, Leana Wen.

Biden, however, can’t seem to quit masks.

Biden made a point to walk away from the podium without a mask after outlining the new guidance, and White House press secretary Jen Psaki said the president and senior staff would abide by the CDC recommendations that no longer required masks outdoors for vaccinated individuals.

But the president has been slow to put the updated recommendations into practice, as reflected by his trip to Georgia.

Biden also wore a mask into and out of the House chamber for his speech to a joint session of Congress, despite most of those in attendance being distanced and vaccinated. -The Hill

Now, even CNN‘s Jake Tapper is calling out the president for sending mixed signals over mask use while vaccinated.

“Should the president start following these guidelines and stop wearing a mask outdoors, stop wearing a mask indoors when with small groups of other vaccinated Americans, to show the American people there is a benefit to getting the vaccine?” Tapper asked guest Anita Dunn – to which Dunn replied that Biden “has always taken his role as sending a signal to follow the science very seriously,” but that people should instead follow CDC guidelines.

>> @JakeTapper to Anita Dunn: “Should the president start following these guidelines and stop wearing a mask outdoors, stop wearing a mask indoors when with small groups of other vaccinated Americans, to show the American people there is a benefit to getting the vaccine?” pic.twitter.com/3YiAs3nJlq

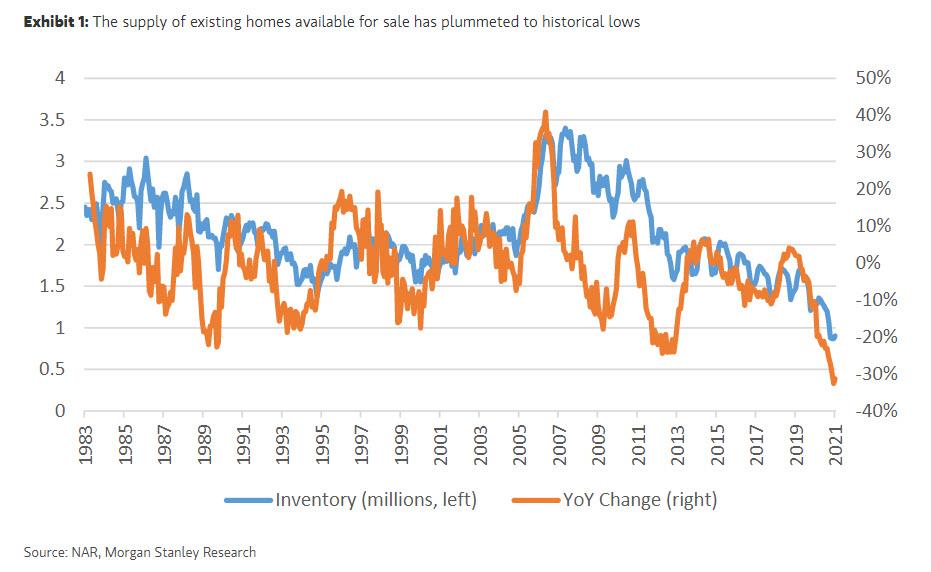

“This Time Is Indeed Different” – Why Morgan Stanley Sees No Housing Bubble

By Vishwanath Tirupattur, Managing Director in Credit Securitized Products Research and Strategy at Morgan Stanley

US housing is on a hot streak. Home prices as measured by the S&P Case-Shiller Index rose 12.2%Y, with prices surging across all 20 of the metropolitan areas tracked by the Index. That amounts to an increase of $35,000 in the median selling price for homes from just a year ago and marks the fastest pace of increase since 2006.

Unsurprisingly, any comparison to the 2006 boom in home prices brings unhappy memories, considering the bust that followed, which culminated in the global financial crisis (GFC) in 2008. However, we argue that this time is indeed different. Unlike 15 years ago, the euphoria in today’s home prices comes down to the logic of demand and supply, and we conclude that the sector is on a sustainably sturdy foundation. We are not at all suggesting that home price appreciation will maintain its current torrid pace. Home prices will continue to rise, but more gradually. We have strong conviction that we are not experiencing a bubble in US housing.

Much has been written about the run-up to the pre-GFC housing bubble. We would boil it down to layers upon layers of leverage in the housing sector that led to a spectacularly painful bust. But contrary to the narrative that loose lending to people with lower credit scores – the ‘sub-prime’ borrowers – was central to the excesses, we think it was more about the type of credit they had access to. Mortgage credit risk consists of (1) borrower risk and (2) mortgage product risk. Borrower risk captures the metrics we typically use to assess the likelihood of default on a mortgage, such as credit score, loan-to-value, and debt-to-income. Product risk lies in giving a borrower a type of mortgage that has a higher risk of default, even controlling for those borrower characteristics. These so-called ‘affordability products’ included mortgages where the payment could vary significantly throughout the life of the loan. As James Egan, our US housing strategist has explained, product risk increased significantly more than borrower risk during the pre-GFC housing boom. The affordability products were inherently risky because they effectively required home prices to keep rising and lending standards to remain accommodative so that homeowners could refinance before their monthly payment became unaffordable. When home prices stopped climbing, these mortgages reset to payments that borrowers could not make, leading to delinquency and foreclosure. As foreclosures and the subsequent distressed sales piled up, home prices fell further, creating a vicious cycle.

Affordability products made up almost 40% of all first lien mortgages from 2004 to 2006. Today their share is down to 2%. Furthermore, the Mortgage Bankers Association’s index of credit standards, which peaked at nearly 900 in 2006, has stayed well below 200 for almost a decade and fell further to the low 100s post-COVID-19. Not only are lending standards much tighter this time around, but the leverage in the system has also been reduced dramatically. Prior to the GFC, the total value of the US housing market peaked at $25.6 trillion in 2006, with total mortgage debt outstanding of $10.5 trillion for an estimated loan-to-value (LTV) of 41.2% for the entire housing market. Today, the value of the housing market has jumped to $33.3 trillion, while total mortgage debt has only increased to $11.5 trillion with an estimated aggregate LTV of just 34.5%. These changes give us confidence that the current system of housing finance is healthy and on a sustainable footing.

Demand and supply factors remain a tailwind for home prices. Thanks to the demographic dividend, millennials continue to drive household formation at a rate 30-50% above the long-run rate of new household formation. Thus, demand for shelter is likely to remain robust for some time to come. As James points out in his latest Housing Tracker, affordability remains good despite sustained increases in home prices and mortgage rates inching higher. Monthly mortgage payments as a percentage of income remain near the most affordable levels in the last five years. Against this backdrop, there is a nationwide shortage of supply. The number of existing homes available for sale has plummeted to historical lows while the supply of new homes remains muted, hence the overall supply of homes sits near record lows.

Robust demand and highly challenged supply along with tight mortgage lending standards augur well for home prices. Higher interest rates and post-pandemic moves will likely slow the pace of appreciation, but their upward trajectory remains on course.

“The Costs Are Up, Up, Up. We’re Seeing Substantial Inflation” Admits A Surprised Warren Buffett As Powell, Yellen See Nothing

We already touched on two of the more colorful exchanges from Saturday’s Berkshire annual videoconference, both of which incidentally starred the traditionally far more outspoken Charlie Munger, who first crushed a generation’s monetary dreams saying that today’s Millennials will have “a hell of a time getting rich compared to our generation”, and then infuriated tens of millions of cryptofans and diamond hands (such as Dan Loeb) when he said that “the whole damn development” of crytpocurrencies “is disgusting and contrary to the interests of civilization.”

Yet while those two incidents may prompt the most Monday morning watercooler talk, what was most relevant from a macro and markets standpoint was Buffett’s observation of something the Fed and Treasury are terrified to admit: that a tidal wave of inflation has been unleashed upon the US and it’s only getting worse.

Speaking to Berkshire’s millions of shareholders on Saturday, Buffett said that he was surprised by the “red hot” US economic rebound and warned the company was being hit by inflationary pressures.

“We’re seeing very substantial inflation,” the 90-year-old billionaire who apparently does not have a Fed charge card, said in his nearly 6 hour long address to investors. But it’s what he said that was especially ominous: “It’s very interesting. We’re raising prices. People are raising prices to us and it’s being accepted.”

Why does this matter? Because the ability to pass on price increases and have them stick, means the surge in prices will not be transitory, no matter how many times the Biden admin, the Fed or the Treasury lie and vow the opposite.

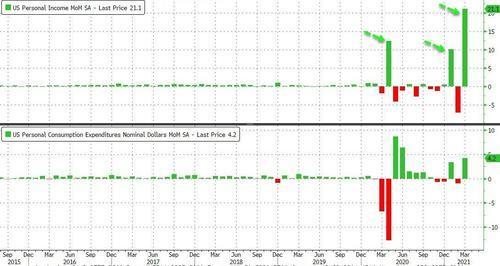

Buffett’s comments came one day after the US revealed that household incomes rose by the most in recorded history in March as the latest round of Biden stimmies hit bank accounts.

This has also pushed the total amount of government transfer payments to a record 34%. That’s right: a third of all US household income is now from the state. Marx would be proud.

The surge in income which for now has resulted in record excess savings of roughly $2 trillion, has sent reverberations throughout financial markets, with investors’ inflation expectations over the next decade rising to an eight-year high.

“It just won’t stop,” Buffett added. “People have money in their pocket and they’ll pay the higher prices…. There’s more inflation going on that people would have anticipated six months ago or thereabouts” he added.

We urge readers to go over the full exchange because the world Buffett lives in and the one populated by the clueless career economists of the Fed are apparently totally different:

BECKY QUICK: I will ask this question from Chris Freed from Philadelphia. And whoever wants to take this on stage, “From raw material purchases by Berkshire subsidiaries, are you seeing signs of inflation beginning to increase?”

WARREN BUFFETT: Let me answer that, then Greg can get more into that. We’re seeing very substantial inflation – it’s very interesting. I mean, we’re raising prices. People are raising prices to us. And it’s being accepted. Take home-building. I mean, you know, the cost of– we’ve got nine home builders in addition to our manufactured housing operation, which is the largest in the country.

So we really do a lot of housing. The costs are just up, up, up. Steel costs, you know, just every day, they’re going up. And there hasn’t yet been because the wage– the wage stuff follows. I mean, the– the UAW writes a three-year contract, we got a three-year contract.

But if you’re buying steel at General Motors or someplace, you’re paying more every day. So it’s an economy, really– it’s red hot. I mean, and we weren’t expecting it. I mean, all our companies, when they thought when they were allowed to go back to work at, well, various operations, we closed the furniture stores, I mentioned.

You know, they were closed for six weeks or so on average. And they didn’t know what was going to happen when they opened. And they can’t stop people from buying things. And we can’t deliver them. They say, well, that’s OK because nobody else can deliver them either, and we’ll wait for three months or something of the sort.

The backlog grows, and then we thought it would end when the $600– the payments ended, and I think around August of last year, it just kept going. And it keeps going and it keeps going and it keeps going. And I get the figures. Every week, we go over, day by day, what happened at the three different stores in Chicago and Kansas City and Dallas.

And it just won’t stop. People have money in their pocket, and they pay the higher prices. And when corporate prices go up in a month or two– and that was the price increase for April 1– our costs are going up, supply chain’s all screwed up for all kinds of people. But it’s a buy– it’s almost a buying frenzy, except certain areas, you can’t buy at.

You know, you really can’t buy international air travel. And so the money is being diverted from a little– some piece of the economy into the rest. And everybody’s got more cash in their pocket than– except for, meanwhile, it’s a terrible situation for a percentage of the people.

I haven’t worn a suit for a year, practically. And that means that the dry cleaners just went out of business. I mean, nobody’s bringing in suits to get dry cleaned, and nobody’s bringing in white shirts the place where my wife goes.

The small business person, if you didn’t have takeout and delivery services for restaurants, you got killed. On the other hand, if you’ve got takeout facilities, then, same-store sales at Dairy Queen are up a whole lot, and they adapted. But it is not a price-sensitive economy right now in the least. And I don’t know exactly how– what shows up in different price indices. But there’s more inflation going on than– quite a bit more inflation going on than people would have anticipated just six months ago or thereabouts.

CHARLIE MUNGER: Yeah, and there’s one very intelligent man who thinks it’s dangerous. And that’s just the start.

WARREN BUFFETT: Greg, you probably are in a good position to comment.

GREG ABEL: Yeah, well, Warren, I think you touched on it. When we look at steel prices, timber prices, any petroleum input, you know, fundamentally there’s pressure on those raw materials. I do think something you’ve touched someone, Warren, and it goes really back to the raw materials.

There’s a scarcity of product right now, of certain raw materials. It’s impacting price and the ability to deliver the end product but, you know, that scarcity factor is also real out there right now, as our businesses address that challenge. And it may be the sum of that’s contribute– or arisen from the storm we previously discussed in Texas. When you take down that many petrochemical plants in one state that the rest of the country is very dependent upon it, we’re seeing it flow through both on price, but overall in scarcity of product, which obviously go together. But there’s challenges, that’s for sure.

Buffett’s admission was also remarkable because it was in opposition to all the official manure spoon fed to the gullible peasants by the President and his economic henchmen (or is that sexist: perhaps henchpeople is more apt?). Case in point, today former Fed chair and current Treasury Secretary Janet Yellen said that Biden’s multi-trillion economic plan is unlikely to create inflation pressure in the U.S. because the boost to demand will be spread over a decade.

“I don’t believe that inflation will be an issue. But if it becomes an issue, we have tools to address it,” Yellen said Sunday on NBC’s leftist Meet the Press show. “It’s spread out quite evenly over eight to 10 years. So, the boost to demand is moderate,” she said of the proposed spending.

Yellen also said the U.S. has the “fiscal space” to make investments in its economy, with interest rates low and likely to remain so, but over the long haul, budget deficits need to be “contained.”

In other words, all those soaring prices, including the Costco shrinkflation seeking to mask a 14% price increase with small offerings… well, just ignore that for a few more years until the “transitory” period ends. Assuming it ends, of course. It didn’t quite end in the 1970s when inflation was also supposed to be transitory.

Yellen said on that while the administration needs “fiscal space to be able to address” emergencies like the pandemic, it needs to do so with a long-term plan in mind. “We don’t want to use up all of that fiscal space, and over the long run deficits need to be contained to keep our federal finances on a sustainable basis,” she said.

Asked about the proposed tax increases that would come with Biden’s spending plan, Yellen focused on the U.S. proposal for a global minimum corporate tax, and efforts to clamp down on tax loopholes in the U.S. “An important way of paying for this is increasing tax compliance,” she said. “It’s estimated that underpayment of taxes that are really due is costing us, the federal government, about $7 trillion over a decade.”

While Yellen touched on rising taxes, there were several other items she refused to touch upon:

How about the increased

– deficits

– national debt

– resulting #QuantitativeEasing

– resulting reliance on China to buy our debt

– increased taxes resulting in 1.1MM lost jobs

– stagnant econ growth

It wasn’t just Yellen lying to the people: another top Biden administration economic adviser said inflation now apparent in certain pockets of the economy is “transitory” as the nation exits the pandemic. Cecilia Rouse, chair of the White House Council of Economic Advisers, said supply chain issues and labor market shortages are “bumps along the way” to recovery.

There’s no sense for now that these price increases are becoming “de-anchored,” she said on “Fox News Sunday,” while promising to remain vigilant on inflation pressures.

“For the time being we expect at most transitory inflation, that is what we expect coming out of a big recession,” she said. It wasn’t clear what would happen when her expectation was proven to be wrong.

Yellen and Rouse spoke following last week’s unveiling of the latest economic plan from the Biden administration, which is proposing a combination of $1.8 trillion in spending and tax credits for areas such as education, child care and paid family and medical leave. This comes on top of almost $2.25 trillion in infrastructure, home health care and other outlays that the administration proposed at the end of March, not to mention the $5 trillion that the government has injected into the economy through the three pandemic relief packages passed by Congress during the past 14 months.

In short, we are looking at $10 trillion in new government handouts in the coming years, give or take a few trillions.

None of this matters to the “big man” himself – and no, not the nearly 80-year-old Biden, of course, who is merely a puppet for whoever writes the lines into his teleprompter – but Fed Chair Jerome Powell, who shrugged off such concerns last week, telling reporters that the reopening of the economy may lead to a single episode of price increases, but not a long-running bout of inflation.

Finally, for those who missed it, here are the main highlights from Berkshire’s nearly 6 hour Saturday tour de force annual meeting, (courtesy of Bloomberg):

SPACs, Robinhood and day trading. We got plenty of opinions from Buffett and Munger on these trends that have gripped the markets over the past year. Buffett called the SPAC boom a “killer” when it comes to creating more competition for Berkshire’s dealmaking desires. But he acknowledged that the stock market has become more of a casino with all the day trading and it creates its own reality for a while until it all blows up. On Robinhood, Buffett acknowledged that gambling isn’t bad but taking advantage of that instinct isn’t the most admirable part of society.

Buffett made some big moves last year, dumping airline stocks and paring back bank bets. He acknowledged today that airlines could have had a different outcome on federal relief if they had a super rich company as a top shareholder, but even then, he wouldn’t buy airlines given the slump in international travel.

Buffett admitted to a few missteps over the past year. Haven, the health care venture, failed eventually and Buffett said that they couldn’t really tackle the “tape worm” of health care. He added that last year, amid the airline sales, wasn’t Berkshire’s greatest moment. Plus, it was a mistake to sell some Apple stock last year, he added.

We only got a potential new clue about succession. At one point, Charlie Munger mentioned that Greg Abel would maintain the culture at Berkshire. Abel has been seen as the most likely successor — he’s younger and controls a lot of Berkshire businesses. But no successor has been publicly announced, so that little comment might be picked up by a few investors eager to know who will take over.

Two shareholder proposals — one on climate change and one on diversity — got a lot of attention ahead of the meeting with proxy advisers Glass Lewis and ISS pushing back against some of Berkshire’s views. But both of those ended up being voted down at the end of the meeting.

And here is a detailed breakdown courtesy of @TheRationalWalk

Starting a thread for the Berkshire Hathaway 2021 annual meeting which has just started. $BRKA $BRKB

Abel and Jain are present on stage, although off to the side from Buffett and Munger.

Buffett is spending a few minutes talking about Jain and Abel to introduce them to the shareholders.

Very good to have all of them available for Q&A on the same stage.

Buffett is pointing out how the accounting rule change a few years ago distorted quarterly (and annual) earnings by including unrealized gains and losses from investments in net income.

This makes periodic earnings swing dramatically and misleads many investors.

Buffett has a slide of the top 20 companies in the world by market cap, 5 of the top 6 U.S. based which led into a pep talk on the United States, which he does so well.

“The system has worked unbelievably well.”

Now Buffett puts up a slide of the top 20 companies in the world from 1989. None of the 20 from 30 years ago are on the present list. Zero. And 13 of the 20 were from Japan!

The top company in 1989 had a market cap of $104 billion – Industrial Bank of Japan.

Buffett is directing this very good history lesson at new investors, but most will just see an old man talking about Henry Ford and disregard his statements. Too bad for them.

Buffett has a list of auto companies from the early 20th century that eventually went bust. Dozens of auto companies just starting with the letters “Ma”. Thousands of entrants. Incredible future. Most failed.

“It’s not as easy at it sounds.”

Referring to entering new and exciting markets that will change the world.

First question asks why Buffett was defensive early in the pandemic. A lot of hindsight bias in that question. Of course it wasn’t the right call … given the history that played out.

Buffett talks about his role controlling risk at Berkshire.

Buffett implies that if Berkshire was still in the airlines, they might not have received the aid that they did. That’s very interesting. He’s implying that Berkshire’s exit from the airlines in some way facilitated the fact that government bailed them out.

Next question is why Berkshire didn’t deploy more cash at the lows in March 2020. More hindsight bias in that question …

Interestingly, Buffett notes that the $20 billion minimum cash balance is going to be increased given Berkshire’s current size.

The day before the Fed acted, Buffett thinks that even Berkshire could not have issued debt. Markets were closed. He’s praising Powell for acting, praising Congress for acting. “It did the job.”

Buffett did not think that it was a “sure thing” that government would act as they did. He was unwilling to COUNT on government acting as they did in March 2020. He won’t rely on the kindness of anyone. And that’s how I like it, and I suspect most shareholders agree.

Munger says that the questioner is “out of their mind” to think that Berkshire could bottom tick the market in March 2020.

Q: Should long term Berkshire shareholders diversify into an index fund?

A: Munger prefers holding Berkshire to holding an index fund. Buffett recommends the S&P 500 index fund, has never recommended Berkshire to anyone.

Buffett “likes Berkshire” but suggests that people who don’t know anything about stocks or no “special feelings” about Berkshire should buy the S&P 500 index.

Buffett is going out of his way to not talk up Berkshire, which is fine, but I question the idea of suggesting the S&P 500 index at current valuations. I don’t think that does anyone any favors.

In the context of dollar cost averaging into index over a long lifetime, S&P 500 is OK, but the question was from a longtime shareholder asking if he should diversify into an index. It would seem nuts to sell BRK to buy the S&P 500, in my opinion. Munger seems to agree.

BREAKING: Munger would prefer to have a son-in-law who works at Chevron rather than as an English professor at Swarthmore.

Buffett doesn’t use the word “asinine” often, but tears into the ESG proposals which I assume will be discussed more fully during the formal shareholder meeting when the matter comes up for a vote.

“We don’t do things just because we have a department of this or a department of that … what’s important is what we are doing at BHE and the railroad…”

Buffett is really fired up talking about renewables and how you can’t turn off the coal plant until you have transmission from wind power to where it is actually used.

I can tell he’s pissed about Berkshire getting a bum rap on the environment.

Buffett turns over the question to Abel who has slides prepared regarding Berkshire’s environmental record at the energy group. Goes back to a 2007 conference where he discussed climate change, policy, innovation, etc… These guys are prepared for the ESG proposals…

Buffett asks “How many other energy companies were there” when Abel talks about a group of companies that made commitments regarding the Paris climate agreement. Abel says “none”.

Buffett: “We’d spend $100 billion on infrastructure” referencing Biden’s speech on Wednesday stating that we need more infrastructure spending.

If we get a 10% return, I’m all for it as well.

Good question on prospects for insurance when Buffett and Jain are no longer involved. Should Berkshire then focus on short-tail lines?

Jain talks about pricing for the unknowns unknowns – a good answer, but not really addressing succession.

Buffett: “We are willing to lose $10 billion in a single event” if paid appropriately for taking on a risk.

Sounds like a big number but not relative to Berkshire’s current size.

“Warren and I don’t have to agree on every damn thing we do.”

Charlie’s answer when asked about differences of opinion between him and Buffett on Costco and Wells Fargo.

Having Jain and Abel on stage interacting with each other is quite valuable for shareholders.

“In three more years, Charlie will be aging at 1% per year. No one is aging less than Charlie.”

Very funny, Warren …

Jain talking about GEICO and Progressive – very candid about Progressive as a formidable competitor and the relative advantages of GEICO and Progressive.

I can tell Jain doesn’t engage in BS. At all.

Buffett talking about $AAPL. Munger thought that Buffett selling a little was a mistake.

Charlie: “Yes”

Buffett is talking about how Apple products are indispensable to customers.

He’s right about some people picking their phone over a car if they had to choose between the two.

People are addicted to their damn phones.

Buffett talking about how interest rates are like financial gravity when asked about stock valuations.

Buffett looking for a clipping from a … paper WSJ … noting that the government sold 4 week t-bills at an average price of 100.000000. Free money for Uncle Sam.

Buffett notes that there has been an incredible change in anything that produces money because the risk free rate is now zero.

And of course he’s right. But for how long will this last? Is it “safe” to price stocks as if the risk free rate will be zero forever?

“The most interesting movie we have ever seen.”

Buffett characterizing the current economic environment.

Buffett: Low interest rates reduce the value of float substantially but Berkshire has options for investing that others don’t have.

As noted earlier today, Buffett shuns fixed income securities for this very reason.

Buffett notes that most SPACs have a two year limit for deploying cash. If you have a gun to your head, then you’ll buy something.

The meeting is half over and no Bitcoin, Dogecoin, Elon, or Crypto questions yet, unless I missed it.

Buffett says that he has roughly $70-80 billion that he would love to put to work.

$20 billion is not the minimum cash level anymore, as he alluded to earlier. It is probably double of that or more, but he has not specified.

Charlie: “Bernie Sanders has won.” Referring to the millennials having trouble rising as far as earlier generations. Um….

Buffett defends the logic of repurchases vs. dividends as a way of cashing out shareholders who want cash, leaving the rest of us alone to continue compounding.

Tax efficiently, I might add.

Munger: Critics are bonkers.

Amen.

I feel very good about not receiving a surprise dividend from Berkshire anytime soon.

Which I suspect will remain the case as long as Buffett and Munger are around since they don’t want to pay the taxes any more than I do.

Buffett stresses that he doesn’t speak for Berkshire when providing his personal views on taxes.

He punts on tax questions. Although he certainly has spoken in the past on taxes at prior meetings.

I like the new policy.

Munger: “I wouldn’t move across the street to save my children $500 million in taxes.”

But … “Who in the hell would drive out the rich people?”

The government owns “Berkshire Class AA stock”. They can take a percentage of earnings without owning any of the company. Indeed.

Buffett thinks that his wealth will accomplish more utility in private philanthropy run by smart people. It won’t make a “damn bit of difference” if it goes to the Federal government. I agree.

I suspect (or at least hope) that Buffett has spoken to the President about tax policy, especially the folly of even thinking about thinking about taxing *unrealized* gains annually, one of the more bonkers ideas to ever be proposed in Washington. Truly nuts.

Buffett: Valuation for Kansas City Southern deal would not be happening without interest rates at current levels. A combination would have a small impact on BNSF and Union Pacific.

Buffett: Biggest single “risk factor” never appearing in a company filing is a CEO who is personable and everyone likes but doesn’t know what he or she is doing.

CRYPTO/BITCOIN QUESTION!!!

Buffett dodges the question. He doesn’t want 400,000 people mad at him and 2 people happy.

Charlie: “You’re waving a red flag at a bull.” Rant follows on bitcoin and other things invented out of thin air … Disgusting, contrary to the interests of civilization…

Q: Why is BRK’s proposal for TX grid better than Musk’s proposal?

Abel: BRK’s proposal is the best they could come up with. If Elon’s proposal is better, then Texas should pursue it. Notes that battery solution isn’t as robust in terms of duration of power supplied.

Buffett: We know what we can do for TX grid. If someone can provide a solution cheaper and faster, they should do it.

Notes that Berkshire is backing proposal with $4 billion penalty if they fail to deliver.

Q for Ajit: Would you underwrite an insurance policy for Elon Musk’s mission to Mars?

“No thank you, I will pass.”

Buffett: Depends on the premium. And on whether Elon is on the mission or not. Skin in the game.

Ajit: “I would be very concerned about writing an insurance policy with Elon Musk on the other side.”

Q: Why aren’t Ted and Todd available to answer questions?

Buffett: Why would we make Ted and Todd available to talk stocks and share ideas with competitors?

Munger is convinced that China will allow companies to flourish. They “changed communism” because they didn’t want to stay poor. A remarkable change coming from such a place. And it has worked like gangbusters. Munger very complimentary.

This will trigger many people.

Q:What happened to the joint health care initiative with Amazon and J.P. Morgan?

Buffett: We learned more about health care in decentralized Berkshire subsidiaries and is one place where centralization could save some real money.

Very hard to change the overall system.

Buffett notes that when companies pay healthcare costs for employees, its an abstraction to employees. They don’t realize that they are really paying in the form of lower wages. And they like that.

Munger: “No kidding”

Buffett notes that U.S. pays 17% of GDP for healthcare while no other major country pays more than 11% yet we get poorer results.

Rational Walk: “No kidding”

Buffett on the failure of the joint healthcare initiative with J.P. Morgan and Amazon:

“We were fighting a tapeworm, and the tapeworm won.”

Question: What do Jain and Abel read on a daily basis?

90% of Ajit’s reading is related to insurance. Abel focuses on the operating businesses he’s in charge of.

Blocking and tackling.

Buffett: Nothing illegal or immoral about gambling on Robinhood but you can’t build a society around it. Not admirable. Will read prospectus.

Munger: “Waving a red flag at a bull.” Godawful. Deeply wrong. State lotteries: States pushed aside mafia in numbers game.

Q: Signs of inflation in subsidiaries?

Buffett: Very substantial. We are raising prices. People are raising prices to us. It’s being accepted. Take homebuilding. Cost up up up. Every day. cc @federalreserve

Buffett is clearly seeing inflation pressure. Doesn’t sound like he thinks it is “transitory”.

Who do you believe? Warren Buffett or Jay Powell and his army of phd economists?

I am paraphrasing, but the transcript will be posted soon, the video will be available, and I’d encourage everyone to read his statements on cost pressures verbatim.

“There’s more inflation going on that people would have anticipated six months ago or thereabouts.”

Listening to that exchange just now makes me want to take out a large thirty year fixed rate mortgage as soon as possible even if I might be paying a high price for a property.

Buffett notes that while rich people can change states relatively easily, a business with plants cannot change so quickly and must be very careful about the pension deficits in various jurisdictions.

Q: Biggest lesson over the past year?

Buffett: “Listen more to Charlie.”

Munger: “We are in uncharted territory.”

Buffett talks about the long term prospects for Berkshire over the next many decades, etc.

No break between the 3 1/2 hour Q&A session and formal meeting. Buffett is 90. Munger is 97.

The formal meeting is a foregone conclusion in terms of the outcome of the two shareholder proposals so I’ll conclude this thread here.

David Parker is the CEO of Covenant Logisticsand he was blunt with analysts who follow the company on its earnings call Tuesday.

“How do we get enough drivers?” he said in response to a question from Stephens analyst Jack Atkins. “I don’t know.”

Parker then gave an overview of the situation facing Covenant, and by extension other companies, in trying to recruit drivers. One problem: With rates so high, companies are encountering the fact that a driver doesn’t need to work a full schedule to pull in a decent salary.

“We’re finding out that just to get a driver, let’s say the numbers are $85,000 (per year),” Parker said, according to a transcript of the earnings call supplied by SeekingAlpha. “But a lot of these drivers are happy at $70,000. Now they’re not coming to work for me, unless it’s in the ($80,000s), because they’re happy making $70,000.”

What’s happening, he said, is that drivers are looking at the fact that they can make $70,000 “and stay home a little more.”

The result is a tightening of capacity. Parker said utilization in the first quarter at Covenant was three or four percentage points less than it would have as a result of that development. “It’s an interesting dynamic that none of us have calculated,” he said.

To put the numbers in perspective, Todd Amen, the president of ATBS, which prepares taxes for mostly independent owner-operators, said in a recent interview with the FreightWaves Drilling Deep podcast that the average tax return his company prepared for drivers’ 2020 pay was $67,500. He also said his company prepared numerous 2020 returns with pay in excess of $100,000.

Parker was firm that this was not a situation likely to change soon. “There’s nothing out there that tells me that drivers are going to readily be available over the medium [term in] one to two years,” he said. “And that’s where I’m at.”

Paul Bunn, the company’s COO and senior executive vice president, echoed what other executives have said recently: Additional stimulus benefits are making the situation tighter. He said that while offering some hope that as the benefits roll off, “that might help a bit.”

But what the government giveth the government can sometimes taketh away. Bunn expressed another familiar sentiment in the industry today, that an infrastructure bill adding to demand for workers would create more difficulty to put drivers behind the wheel. Construction, Bunn said, is “a monster competitor of our industry” and if the bill is approved, “that’s going to be a big pull.”

Labor is going to be a “capacity constraint” through the economy, Bunn said, while conceding that trucking is not unique in that. And because of that labor squeeze, capacity in many fields is going to be limited. “The OEMs, the manufacturers are limited capacity,” Bunn said. “They’re not ramping up in a major, major way because of labor, because of commodity pricing, because of the costs.”

All that means is that capacity growth is going to be “reasonable,” Bunn said. “It’s not going to be crazy, people growing fleets [by] significant amounts.”

“It’s all you can do just to hold serve,” he added.

While the driver situation is tough, it didn’t notably hurt the first-quarter performance of Covenant. To open the call, Joey Hogan, Covenant’s co-president, highlighted some of the company’s first-quarter numbers: a 6% growth in operating revenue on a strategic reduction in the number of company tractors and the best first-quarter net income figure in its history.

Beyond the market for drivers, Parker said the freight market is “hot” and likely to stay that way.

“We are at 7%, 8% GDP growth, that goes to 5%, well, probably, or it could stay 7% or 8%,” he said. “But it’s still going to be numbers that you and I have never sensed or felt from a freight standpoint. And so I don’t see that letting up, I see that a solid couple of years of being in that kind of environment.”

Given that, Parker and other Covenant managers used the occasion of the earnings call to drive home with more detail a point the company made in its earnings statement a day earlier: It intends to get higher rates out of some of its Dedicated customers. While the company’s Expedited division saw its operating ratio improve to 91% from 102.3% a year earlier, the Dedicated division saw its OR remain above 100%.

The Dedicated division, Bunn said, has two types of customers. One is a group with high returns, “and we want more of those,” he said. “We’re going to go to the customers [where] we have that and say, ‘Can we have more of your business?’”

The other are customers that Bunn referred to as “commoditized.” Those customers are going to need to “value” the Dedicated service provides “or we’re going to give those trucks to somebody who’s in the first bucket.”

Trucks won’t just get “yanked” out, Bunn said. But “we’re not going to run Dedicated with a 98, 99 or 100 OR,” he added.

But even though Covenant, like other carriers, has leverage in negotiations given the tight market for capacity, it does need to be handled with a certain degree of aplomb, Hogan said. Hogan was talking about the company’s Expedited division when he said that in price negotiations, a company needs to be “respectful” as prices get up to “that line where they say, ‘Well, I’m going to grow my own [transportation].’”

Another possibility: rail. “When does the price push them to the rail?” he asked.

However, the Expedited division is “in a good spot for at least a couple of years,” Hogan said. That’s aided by the fact that inventories are “stupid low” across the supply chain, he added.

‘Work-From-Home’ To Dent Spending In Large Cities By Up To 10%, Study Says

The work-from-home (WFH) experiment ushered in by the virus pandemic will become more permanent, resulting in quieter metro areas, less crowded office buildings, and a decline in traffic jams.

A new working paper titled “Why Working From Home Will Stick” by UChicago researchers said the days of an office-based 9-to-5 job is over as hybrid telecommuting and other WFH technologies make remote working possible for millions of Americans.

The post-pandemic shift from the office to home will decrease spending in major metropolitan areas by up to 10%, researchers Jose Maria Barrero, Nicholas Bloom, and Steven Davis said. For more crowded areas like Manhattan, the researchers projected consumer spending would drop by 13%.

So what about the economic revival policymakers and central bankers keep promising us? Well, perhaps a robust recovery in city centers may be an unattainable goal. Once again, office workers drive spending – and with some of them working at home, longstanding consumer trends within many metro areas will suffer permanent declines.

“Higher levels of WFH will present pointed challenges for urban areas, especially cities with high rates of inward commuting by well-paid professionals in the pre-COVID environment. As these workers cut back on commuting, they will spend less on food, shopping, personal services, and entertainment near workplaces clustered in city centers. In preliminary calculations that exploit our survey data, we project that overall consumer spending will drop 5 to 10 percent or more (relative to the pre-pandemic situation) in San Francisco and Manhattan because of declines in net inward commuting and less spending near employer premises. Their central business districts will see considerably larger spending drops relative to the pre-pandemic levels,” researchers said.

In July 2020, we first previewed, via a KPMG International report, how WFH would impact the economy and result in declines for “automakers, retailers, and industries directly or indirectly related to transportation will take a massive hit for the next several years.”

KPMG predicted WFH “accelerated powerful behavioral changes that will continue to shape how Americans use automobiles. We believe the changes in commuting and e-commerce are here to stay and that the combined effect of reduced commuting and shopping journeys could be as much as 270 billion fewer vehicle miles traveled (VMT) each year in the US.”

Without workers flooding city centers every morning and stacked inside office buildings, metro areas will suffer a permanent drop in spending, which means many service jobs will be lost and a labor market deeply scarred.

UChicago’s researchers support the idea that WFH is accelerating urban flight.

… and the million-dollar question is what does Wall Street think about WFH?

To answer that question, Deutsche Bank credit strategist Jim Reid polled Wall Street professionals who said the best thing about WFH is the lack of a commute, among other perks…

So the combination of WFH and moving to the suburbs will leave lasting impacts on city centers that will experience permanent declines in consumer spending. So much for that robust recovery policymakers keep telling us about…

Reading Jonathan Culbreath’s “Modern Monetary Theory for Conservatives” one can’t help but think of Murray Rothbard’s quip that “it is not a crime to be ignorant of economics … but it is totally irresponsible to have a loud and vociferous opinion on economic subjects while remaining in this state of ignorance.“

Culbreath’s case for modern monetary theory (MMT) rests on an ignorance of basic economic principles regarding the role of money in a free market economy. Money—whether precious metals, fiat currency, crypto, or some other good—is more than the unit of account that makes exchange possible. Money is also a key part of the equation of the price system, which allows market participants to discover the highest use of goods and services as determined by the demonstrated preferences (i.e., what they willing to spend their money on) of consumers, investors, workers, and business owners. A freely functioning price system and a stable currency are thus the key to a proper functioning market.

The most important information conveyed by prices is the price of money itself, which is the interest rates. When central banks increase the money supply to facilitate government spending, they artificially lower interest rates. This distorts the information interest rates convey to market actors. This results in investors sinking money into projects not supported by underlying market conditions. This leads to a boom which is inevitably followed by a bust. MMT’s policy of never-ending increases in the money supply would create more (and bigger) bubbles, leading to more (and bigger) busts.

Culbreath, like most “mainstream” economists, misidentifies inflation as a “rise in the price levels.” But rising price levels are an effect, not a cause, of inflation. Inflation is the very act of money creation by a central bank.

Inflationary policies, such as those embraced by proponents of MMT, benefit those already at the top of the economic and political ladder. This is because those at the top of the financial pyramid are the first to receive the newly created money. This means they enjoy an increase in purchasing power before the central bank’s actions cause prices to increase. In contrast, by the time middle- and working-class Americans see a (nominal) boast in their incomes, the Fed’s inflationary policies have already caused prices to increase. These price increases are usually greater than the increase in wages. So, their real wages decline. This “inflation tax “is the most insidious tax of all, because it is both regressive and hidden.

Contrary to proponents of MMT, inflation’s pernicious effects are not limited to times of “full employment.” Instead, they are felt any time the central bank artificially lowers interest rates. Full employment itself is nothing but an arbitrary number chosen by economists and bureaucrats and is thus easily manipulated to make the economy seem stronger than it is.

Government statistics can also be manipulated to understate the true unemployment rate. One way this is done is to not count people who have given up looking for a job in the headline rate. Instead, one must delve deeply into the data to discover the extent to which discouraged workers have been forced out of the labor market.

Government statistics also understate the effects of inflation. One way they do this is via the Chained Consumer Price Index. The Chained CPI does not consider an individual to be negatively impacted by central bank–caused price increases if they can still afford lower-priced “substitute” goods. So even if you can no longer afford steak, you have not been negatively impacted by rising prices if you can still buy hamburger. Of course, if hamburger were really an adequate substitute for steak, individuals would have been buying cheaper hamburger when they were able to afford both hamburger and steak.

MMT Relies on Trusting Government “Experts” to Plan the Economy

The way government officials manipulate economic statistics points to another major flaw in Culbreath’s case for MMT: accepting it requires placing an enormous amount of trust in the integrity and wisdom of government officials.

For MMT to work, the Federal Reserve must have the ability to know exactly how much the money supply needs to increase in order to support expansion of government without damaging the economy. Congress, with the help of government “experts” must know when the economy has reached full employment. When the economy reaches full employment, Congress must be able to determine exactly how much to increase taxes and which taxes to increase to keep inflation from damaging the economy.

The great Austrian economist Ludwig von Mises demonstrated that government planners could not manage the economy without damaging people’s standard of living. This is because the only way to know the value of goods is by how much individuals pay for them. Government’s use of force to take control of those resources makes it impossible to know their true value, thus making it impossible to perform rational economic calculation. Mises’s student, Nobel Laureate F.A. Hayek pointed out that there is no way central planners—including democratically elected politicians and central bankers—could have the knowledge necessary to effectively manage an economy.

One need not have read the works of Mises, Hayek, and other Austrians to understand the folly of thinking government “experts” (much less politicians) can successfully run the economy. A cursory exclamation of the numerous failures of attempts at central planning throughout history will show that government “management” of the economy inevitably fails.

As should be obvious, the critique of modern monetary theorists’ claim that an expansionist monetary policy can fund the government is not an endorsement of “paying for” big government via income or some other form of taxes. Taxation also distorts the economy, making rational economic planning impossible.

Pandering to Conservative Fears of Economic Stagnation

Mr. Culbreath urges conservatives to embrace MMT in order to free themselves from worrying about the debt and instead join a conservation effort about what programs the government should spend the newly created money on. Culbreath seems unaware that Republicans only concern themselves with deficit spending when a Democrat sits in the oval office.

Culbreath also seems to think that this “conversation” will result in more spending benefiting the “average American.” But even assuming MMT works as promised, the fact is that those already tied in with the political class—which means crony capitalists and other special interests—will still be the ones with the time and resources to devote to influencing government policies. So, the result of Mr. Culbreath’s “conversation’ will be a corporatist system that benefits the military-industrial complex, Big Pharma, big banks, Wall Street, and other special interests, leaving welfare crumbs for the ordinary Americans.

Mr. Culbreath also ignores how MMT, by encouraging a more “active” federal government, violates the principles—embedded both in the constitutional doctrine of federalism and the Catholic doctrine of subsidiarity—that social programs should be provided by the level of government closest to the people. Of course, the best way to provide education, healthcare, and charity is through private and religious institutions.

The Federal Reserve’s currency deprecation undermines the virtue of thrift and encourages short-term thinking. The growth of the welfare state that MMT is designed to facilitate undermines the virtues of self-reliance and reliance on family, friends, private charities, and churches and replaces them with reliance on government welfare. Expansion of government-provided welfare also encourages the mentality that one is entitled to live off the fruits of their fellow citizens’ labor. These seem odd goals for a conservative to be promoting.

It also seems odd for a conservative Catholic to promote expansion of the role of the same government that funds abortions and is aggressively waging war on religious believers who refuse to live by their beliefs, even it if means refusing to bake cakes for same-sex couples or objecting when boys demand to play girls sports.

Modern monetary theory is nothing more than a new version of the old myth that governments need not worry about restraining spending because a government-controlled central bank can pump money into the economy.

MMT suffers from the same flaws as every other version of this fairy tale. The only long-term benefit of the adoption of MMT is that it will hasten the inevitable collapse of the welfare-warfare fiat money system.

Instead of trying to create conservative justifications for destructive monetary policy, conservatives should join libertarians and classical liberals in working to limit government power while restoring sound money and greater market freedom. Libertarians and conservatives should also work together to restore responsibility for education, charity, and other “social welfare” programs to local communities, churches, and families. Restoration of a free society will not only enable all to achieve prosperity, but will also create the conditions to allow individuals to pursue virtue.

After Ford’s Semi Shortage Meltdown, Morgan Stanley Says Industry Won’t Recover Until “Well Into 2022”

The ongoing supply-demand imbalance in the auto industry is set to continue “well into 2022”, according to a new note from Morgan Stanley.

We have been following the semiconductor shortage’s effect on the auto industry for about six months now, noting how it has bottlenecked production for numerous manufacturers due to the usage of chips in nearly all new automobiles.

Adam Jonas and Joseph Moore at Morgan Stanley contend that the constraints could last into next year. Of course, both analysts see it as an opportunity to “buy the dip” (when is it not?) and bet on the longer term EV opportunity, the analysts said in a note out late last week.

“Ford’s changed outlook was the first major profit warnings in auto since the worst of COVID,” the analysts wrote, calling the automaker’s report a “bit of a reality check” for investors who have been chasing momentum from OEMs.

Jonas and Moore said their U.S. semiconductor team were “very surprised” by the scale of Ford’s recent production cuts. Semi analyst Moore commented: “There’s capacity out there if you claimed it in time. Yes there is tightness and there have been exogenous shocks that have extended tightness, but all of the semiconductor companies are showing auto growth of approx[imately] 20% YoY… they’re shipping higher than pre-COVID levels and this is not all explained by higher content in the car.”

The analysts placed some of the blame on Ford, suggesting the automaker could be the “worst example of chip supply disruption impact” due to poor planning.

And the note concluded with the realization that “on-shoring and diversification of geographic supply sourcing” should be thrust into focus. Perhaps no one told Jonas and Moore: we don’t manufacture things in the U.S. anymore.

Recall, last week, Ford was the latest auto manufacturer to slash its expectations for full year production as a result of the shortage. The company noted:

Ford said it anticipates a 50% reduction in its planned second-quarter production due to the semiconductor shortage. That’s far worse than the 17% reduction in planned production in the first quarter.

Ford sees a $2.5 billion cost from the semiconductor shortage (at the high end of what CEO Jim Farley had said), but it hopefully expects Q2 “to be the trough of the” impact.

Ford CFO John Lawler’s commented on the chip shortage:

“Semiconductor availability, which was exacerbated by a fire at a supplier plant in Japan in March, will get worse before it gets better. Currently, the company believes that the issue will bottom out during the second quarter, with improvement through the remainder of the year.”

Two weeks prior to Ford’s report, we wrote about how the chip shortage was becoming a self-fulfilling prophecy, due to a shortage of chipmaking equipment. In the days leading up to that report, we wrote that Taiwan Semiconductor was also warning that the global chip shortage may extend into next year.

In early April, we wrote that U.S. exporters of semiconductor chipmaking tools were struggling to get licenses to sell to China. The U.S. government had been dragging its feet in approving licenses for companies to sell chipmaking equipment to Chinese semi company SMIC, we noted at the time.

The New York Times, The Washington Post, and NBC News have retracted earlier reporting that incorrectly stated former New York Mayor Rudy Giuliani was directly warned by the FBI that he was targeted by a Russian intelligence influence operation.

The stories came after federal investigators executed a search warrant at the home and office of the former New York mayor. The searches were allegedly linked to Giuliani’s dealings in Ukraine, while Giuliani said he believes the search warrant was issued because he allegedly failed to file with the Department of Justice (DOJ) for representing a Ukrainian national or office. He has since denied any wrongdoing.

The Post was the first to report the incorrect information. It also incorrectly stated that One America News had also received a similar warning from the FBI.

“This version has been corrected to remove assertions that OAN and Giuliani received the warnings,” the correct appended on the article states.

The NY Times made its correction on a story about Giuliani’s alleged role in the 2019 recall of ambassador Marie L. Yovanovitch.

“An earlier version of this article misstated whether Rudolph W. Giuliani received a formal warning from the F.B.I. about Russian disinformation. Mr. Giuliani did not receive such a so-called defensive briefing,” the correction states.

Meanwhile, NBC News elaborated on why it corrected the story, saying that a second source disputed the assertions of the first source as the briefing was only prepared for Giuliani and not delivered to him. Both sources were anonymously cited in the article.

“The report was based on a source familiar with the matter, but a second source now says the briefing was only prepared for Giuliani and not delivered to him, in part over concerns it might complicate the criminal investigation of Giuliani,” the NBC News correction reads.

The press offices of The NY Times, the Post, and NBC News did not immediately respond to questions about the corrections. Giuliani’s office did not respond to The Epoch Times’ request for comment.

In two statements on Twitter, Giuliani called for the Post and NY Times to reveal their sources for the incorrect information.

“On a Saturday, the Washington Post added this correction to their defamatory story about me,” Giuliani wrote on Twitter.

“The Washington Post and the NYT must reveal their sources who lied and targeted an American Citizen. #msnbc , #cnn forgot to mention the corrections today. #fakenews #badpeople.”

In a separate statement, he wrote: “Where did the original false information come from? @MSNBC @CNN @nytimes I couldn’t quite hear your apology?”

“I Just Wanted A Little More Time” – Texas Nurse Was Fired For Refusing COVID Vaccine

Many hospital systems around the country have been surprised by the number of nurses who have passed on being vaccinated (either because they had already been infected, or simply because they didn’t want the vaccine). But as federal public health officials crank up the pressure on Americans to submit to the vaccine as unused jabs pile up, one nurse in Texas complained to local journalists that she was fired simply because she refused the jab.

Nurse Michelle Fuentes told Dallas-Fort Worth CBS affiliate KRIV-TV that she had been terminated after working for 10 years at Houston Methodist Hospital, allegedly because she refused to accept the COVID-19 vaccine.

“I knew that the date was looming over my head of me to get the vaccine and we were constantly being pressured and pressured,” Michelle Fuentes said.

According to their report, at the start of April, Houston Methodist announced it would require all employees to get the COVID-19 vaccine by June 7. However, the hospital system asked employees who refused to get the vaccine to submit documentation for consideration for a medical or religious exemption. The paperwork was reportedly due by May 3.

Michelle Fuentes

Fuentes said she told her employer that she needed more time to make a decision to do more “research” on her own, but instead wound up turning in her two weeks notice.

“I just needed a little bit more time and little bit more research to be done,” Fuentes said.

A spokesperson for the hospital system said 90% of its employees are vaccinated, and that only two have resigned so far. Fuentes said when she didn’t agree to stay quiet about the reason for her departure, she was not allowed to complete her final two weeks and was immediately escorted out of the hospital by security.

Finally, Fuentes told the press that she wants to wait until all clinical trials are completed before she decides to get the vaccine or not. She stressed she is not against vaccines and gets the flu vaccine every year. Fuentes even volunteered to work in the COVID unit. Despite reassurances that vaccines are safe, and that their vast public benefit outweighs any risks, recent concerns about vaccine side effects have included incidents of rare but deadly cerebral blood clots, and also an impact on the menstrual cycle.