North Korea Slams “Intolerable” Biden Comments, Lashes Out At “Human Wastes” In South Korea

It looks like US-North Korea relations are almost back to their “daily test ICBM launch” level.

On Sunday, North Korea lashed out at Joe Biden’s recent comments labeling the country a serious threat, while unleashing a torrent of insults at South Korea for not stopping activists from sending anti-Pyongyang leaflets across the border.

North Korea’s outburst followed a Washington Post report that the Biden administration has decided to pursue a phased agreement that leads to full denuclearization in North Korea. Kwon Jong Gun, director general of the country’s Department of U.S. Affairs of the Foreign Ministry, said in a statement that Biden’s comment on North Korea was “intolerable”, and also followed a statement by White House Press Secretary Jen Psaki who said Friday the U.S. has completed a review of its North Korea policy.

“This becomes an evident sign that it is girding itself up for an all-out showdown,” North Korea’s foreign ministry said of the U.S. in a statement issued by KCNA. “We have warned the U.S. sufficiently enough to understand that it will get hurt if it provokes us.”

The hollow threat also comes as Biden is scheduled to meet South Korean President Moon Jae-in on May 21, with Seoul saying that North Korea would be high on the agenda. As Bloomberg notes, Moon is set to become the second foreign leader to visit the White House since Biden’s inauguration, after Japan’s prime minister, and the announcement comes as Biden’s administration is reviewing its policy on trying to end North Korea’s nuclear ambitions.

In a separate statement, North Korea warned that Seoul will pay a price for allowing a defector group in the South for sending 500,000 leaflets on the brutality of the Kim Jong Un regime.

“We regard the maneuvers committed by the human wastes in the South as a serious provocation against our state,” Kim Yo-jong, the sister of North Korean leader Kim Jong Un, said in a statement carried by the official Korean Central News Agency, adding that Pyongyang will “look into corresponding action.”

Of course, not a day seems to pass these days without North Korea threatening to obliterate its southern neighbor, and in this case the “first sister” warning echoed her warning from June that South Korea would pay a “dear price” if it continued to allow “mongrel dogs” to send the leaflets. Shortly after that, North Korea blew up a $15 million joint liaison office built by South Korea north of the border that served as a de facto embassy — destroying one of the most tangible symbols of Moon’s rapprochement efforts.

Moon’s progressive camp passed legislation in December that criminalizes sending leaflets to North Korea, months after Kim’s regime demanded action to stop what it called the “human scum” behind the messages.

Hedge Fund CIO: “Biden Is Betting The Voters That Brought Trump To Power Can Be Bought”

“I know some of you at home are wondering whether these jobs are for you. So many of you, so many of the folks I grew up with, feel left behind and forgotten in an economy that is rapidly changing. It’s frightening,” said Biden, sketching out his ‘Blue-collar Blueprint to build America.’

He claims 90% of the new jobs won’t require college degrees, 75% won’t require associate degrees.

The presumption is that these voters brought Trump to power and inexplicably supported him despite his $1.5trln in tax cuts for corporations and the wealthy.

Biden is now betting they can be bought. Most folks can.

“Trickle-down economics has never worked,” said Biden, scratching out the policy first drawn-up in crayon on a napkin by Reagan in 1981.

“We’re going to reward work, not wealth,” said Biden, unsure what that means, but liking the sound of it, unveiling an utterly unprecedented $6 trillion in new federal spending: The American Families Plan, American Jobs Plan, and American Rescue Plan.

The scorched-earth spending plans covered every inch of Joe’s paper, to benefit all but the 1%. Had such a sketch been unveiled when Biden first became a senator in 1973, stocks, bonds and the dollar would have simultaneously collapsed.

But after decades of disinflationary policies that favor capital over labor, inflation-expectations are so muted and investors are so convinced the Fed can maintain calm, that markets barely budged.

This illusion will remain vivid until the day it dissolves. In a flash.

But until then, America’s bitter political battle will intensify as Democrats attempt to secure near-permanent power by any means necessary, fearing that a return of Republicans will result in that party securing the same. Biden’s approach will be to spend whatever it takes to paper over the Red and Blue lines of national division, redrawing them as Capital versus Labor.

And no one can know if it will sell, we only know it will be the most expensive blueprint ever drawn.

SpaceX Capsule Successfully Returns 4 Astronauts From ISS In First Nighttime Splashdown Since 1968

Four astronauts have successfully returned to Earth from the International Space Station early Sunday morning in a “splashdown” that took place in the Gulf of Mexico.

Returning in a SpaceX capsule, the astronauts marked the first nighttime return to earth for NASA “in decades”, according to the Wall Street Journal.

The Crew Dragon Resilience made its “soft splashdown” at 2:57am on Sunday and was then hoisted into a recovery vessel near Panama City, Florida. The astronauts had been in space for 168 days, completing SpaceX’s first “operational round trip mission”.

The crew, consisting of National Aeronautics and Space Administration astronauts Michael Hopkins, Victor Glover, and Shannon Walker and Soichi Noguchi of the Japan Aerospace Exploration Agency, was brought into orbit last year, before docking with the ISS.

NASA and SpaceX are reportedly falling into an operational “cadence” with one another, with the return of the four astronauts marking the latest in a series of milestones for the two agencies. The two agencies “have regularly scheduled human shuttles to and from space using the company’s commercially built rockets and capsules,” according to the Journal.

Another crew of four is also at the International Space Station, beginning their mission, after being launched into orbit last month on a SpaceX rocket.

SpaceX intends on launching 7 capsules for NASA, including three cargo variants, over the next 15 months, the report said.

Apollo 8 was the last nighttime splashdown, which occurred after the mission orbited the moon in 1968.

While the American Rescue Plan is changing the course of the pandemic and delivering relief for working families, this is no time to build back to the way things were. This is the moment to reimagine and rebuild a new economy. The American Jobs Plan is an investment in America that will create millions of good jobs, rebuild our country’s infrastructure, and position the United States to outcompete China. Public domestic investment as a share of the economy has fallen by more than 40 percent since the 1960s. The American Jobs Plan will invest in America in a way we have not invested since we built the interstate highways and won the Space Race.

By increasing government spending, the Biden administration seeks to address infrastructure like highways, ports, and airports, as well as the electrical grid and broadband internet.

For a longer list of the goals of the bill, read the full statement here.

This move, of course, will be lauded by many and disputed by others.

But it does not seem too much to assume that both sides will miss the main problem with this bill.

The Left will adore it for its brave use of the state to improve the lives of Americans, while the Right will abhor the bill since it is not their preferred form of big government spending (how dare we spend perfectly good money on infrastructure that could be used to murder innocent people in the Middle East?).

What both sides fail to recognize is the economic reality of any and all state actions, a reality pointed out to us by Murray Rothbard in his 1956 article, “Toward a Reconstruction of Utility and Welfare Economics.” In that article, without having to rely on a single ethical judgment, Rothbard concludes the apodictic advantages of the market and the perennial waste of government expenditure.

Rothbard begins his reconstruction with two scientific principles: the unanimity rule and demonstrated preference.

In Rothbard’s words, Wilfredo Pareto’s Unanimity Rule (reintroduced by Lionel Robbins) states, “We can only say that ‘social welfare’ (or better, ‘social utility’) has increased [sic] due to a change, if no individual is worse off because of the change (and at least one is better off).”

Demonstrated preference is the idea that we can only know anything about someone’s value scale by observing actual decisions they make, usually in a market exchange. Any assessment of someone’s words would be psychological in nature and irrelevant for economics. With demonstrated preference, we can say that every voluntary exchange must ex ante apodictically result in an increase in social utility, for every exchange demonstrates a perceived expected benefit for both parties involved. Whenever an exchange is prohibited or mandated by the state, there must, definitionally, be some party that benefits and some party that is harmed, which makes it impossible to make any statement on total social utility given the impossibility of comparing utility interpersonally. Moreover, the presence of a harmed party means these actions violate the unanimity rule. We can confidently conclude, then, that any government interference with exchanges can never be said to increase social utility.

But the analysis does not stop there. All government action ultimately rests on its power to levy taxes. Taxation, though, is nothing more than a coerced exchange between the people and the state. Given this insight, not only can government interference never increase social utility, but no action a government could ever make could increase social utility.

All this leads to the following two conclusions:

(1) the free market always increases social utility, and

(2) the government can never increase social utility.

The main problem with the American Jobs Plan is now clear.

It is not the fact that it calls for more spending on infrastructure and promoting supposedly green technology, as opposed to, say, the military. Its problem is that it calls on the state to do anything at all. Biden’s call for increased government action will do nothing more than waste our precious finite resources. There is nothing proactive in the bill that can be said to lead to an increase in social utility, and the restrictions it places on the free market will fail to lead to a more prosperous society as well. The plan is to restrict the free market, the only mechanism capable of promoting the general welfare, and expand the role of the government, an institution that can never promote the general welfare. A job well done, Mr. President.

California To Offer Early Release To Over 63,000 Violent Felons

California Gov. Gavin Newsom is giving 76,000 inmates – 63,000 of which are violent and repeat felons – the chance to leave prison early, allowing inmates with good behavior to shorten their sentences by 1/3 instead of the 1/5 instituted in 2017, according to the Associated Press.

The benefits will extend to nearly 20,000 inmates serving life sentences with the possibility of parole, while over 10,000 prisoners convicted of a second serious (nonviolent) offense under the state’s “three strikes” law will be eligible for release after serving just half their sentences, vs. the current time-served credit of 1/3 of their sentence.

The rule, which takes affect Saturday, may take months or years before any inmates receive their early release. According to corrections officials, the goal is to reward inmates who improve themselves in prison, while critics argue this will endanger the public.

Meanwhile, all minimum-security inmates in work camps, including those fighting the state’s annual wildfires, will be eligible for the same month of earlier release for every month they spend in the camp, regardless of their crime.

“The goal is to increase incentives for the incarcerated population to practice good behavior and follow the rules while serving their time, and participate in rehabilitative and educational programs, which will lead to safer prisons,” said spokeswoman Dana Simas with the state’s Office of Administrative Law. “Additionally, these changes would help to reduce the prison population by allowing incarcerated persons to earn their way home sooner.”

Simas said the department was granted the authority to make the changes without public comment by making them “emergency regulations.” The department must now submit permanent regulations next year, after which there will be a public hearing and an opportunity for public comment.

That said, according to Kent Scheidegger – legal director of the Criminal Justice Legal Foundation which represents the victims of crime – ‘good behavior’ credits are a misnomer.

“You don’t have to be good to get good time credits. People who lose good time credits for misconduct get them back, they don’t stay gone,” he said. “They could be a useful device for managing the population if they had more teeth in them. But they don’t. They’re in reality just a giveaway.”

Also criticizing the Newsom administration for unilaterally deciding to make the changes was GOP state Sen. Jim Nielsen, who said: “He’s doing it on his own authority, instead of the will of the people through their elected representatives or directly through their own votes.”

“This is what I call Newsom’s time off for bad behavior. He’s putting us all at greater risk and there seems to be no end to the degree to which he wants to do that.”

California has been under court orders to reduce a prison population that peaked at 160,000 in 2006 and saw inmates being housed in gymnasiums and activity rooms. In 2011, the U.S. Supreme Court backed federal judges’ requirement that the state reduce overcrowding.

The population has been declining since the high court’s decision, starting when the state began keeping lower-level felons in county jails instead of state prisons. In 2014, voters reduced penalties for property and drug crimes. Two years later, voters approved allowing earlier parole for most inmates.

Before the pandemic hit, the population had dropped to 117,00 inmates. In the last year, 21,000 more have left state prisons — with about half being held temporarily in county jails. -AP

Democratic lawmakers and advocacy groups have been calling for more releases or shortened sentences, while the state announced in mid-April that they will close a second prison as a result of a shrinking prison population.

We can’t help wonder which communities early prisoner release will impact most?

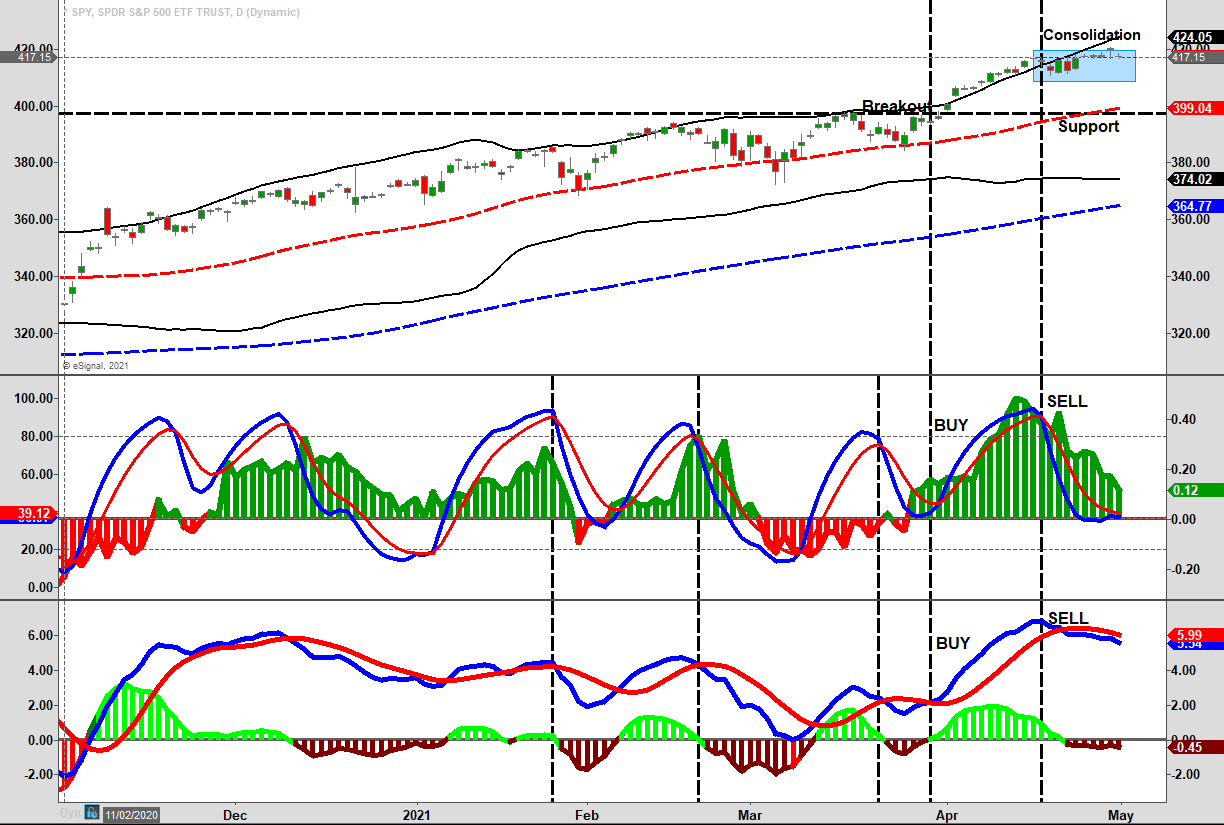

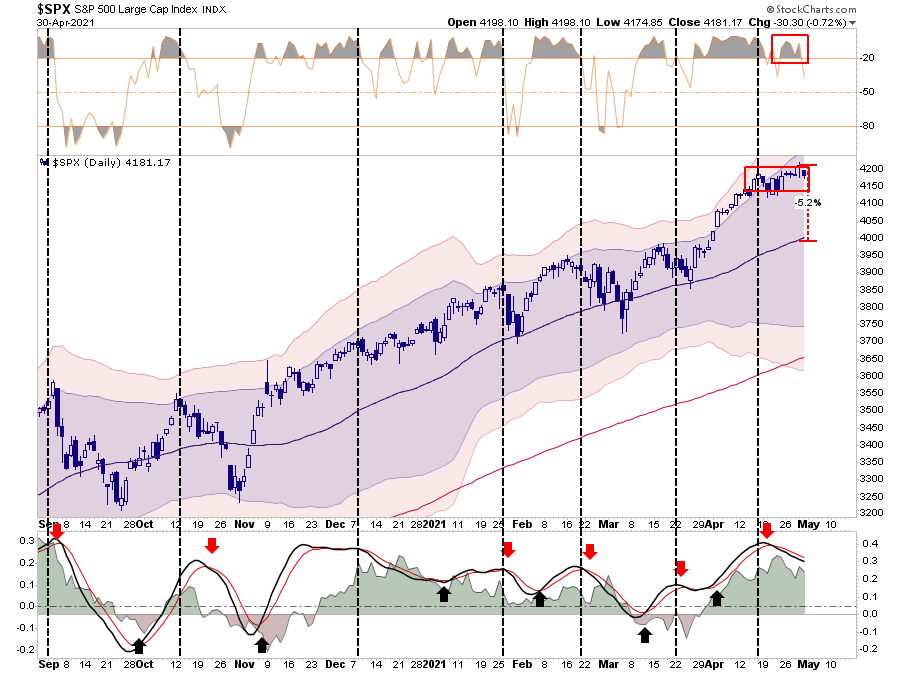

“The market is trading well into 3-standard deviations above the 50-dma, and is overbought by just about every measure. Such suggests a short-term ‘cooling-off’ period is likely. With the weekly ‘buy signals’ intact, the markets should hold above key support levels during the next consolidation phase.”

“As shown above, that is what is currently occurring. While the market remains in a very tight range, the “money flow” sell signal (middle panel) is reversing quickly. Importantly, note that the money flows (histogram) are rapidly declining on rallies which is a concern.”

While the “sell signal” remains intact, not surprisingly, the breakout above the consolidation on Thursday failed, with the selloff on Friday putting the market back where it started the week. Furthermore, the MACD “sell signal” in the lower panel also suggests that prices may remain somewhat capped for the time being.

As noted, the concern remains of the decline in actual money flows. While the market is holding up near all-time highs, the support of positive money flows continues to deteriorate. Weakening money flows with the market remaining at more overbought conditions also suggest upside is limited over the next few weeks.

For now, the market trend remains bullish and doesn’t suggest a sharp decrease of risk exposures is required. However, after reducing equity exposure previously, we are starting to look for the next short-term opportunity to increase risk. However, we aren’t expecting much before we get into the summer months, where, as we will discuss, the risk begins to rise markedly.

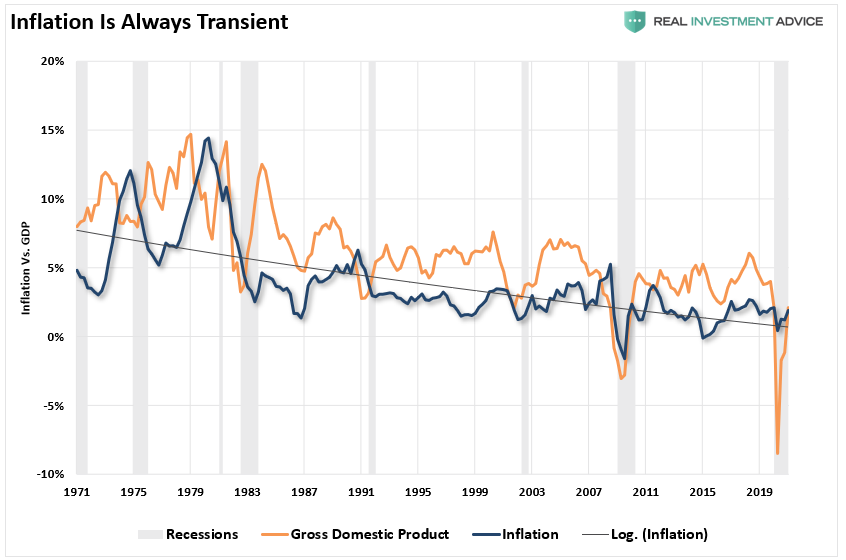

“Inflation jumped as predicted, and so was the Fed comment about transitory.”

As Mish discusses, inflation depends much on how you measure it and who it impacts. However, inflation is and remains an always “transient” factor in the economy. As shown, there is a high correlation between economic growth and inflation. As such, given the economy will quickly return to sub-2% growth over the next 24-months, inflation pressures will also subside.

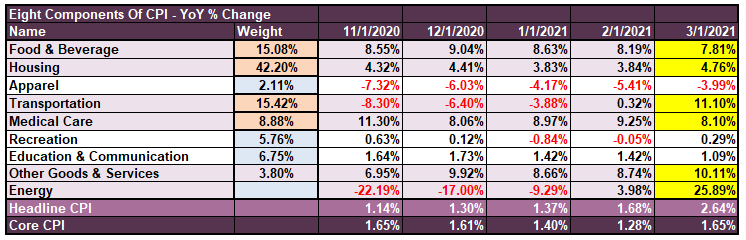

Significantly, given the economy is roughly comprised of 70% consumption, sharp spikes in inflation slows consumption (higher prices lead to less quantity), thereby slowing economic growth. Such is particularly when inflation impacts things the bottom 80% of the population, which live paycheck-to-paycheck primarily, consume the most. The table below shows the current annual percentage change in the various categories.

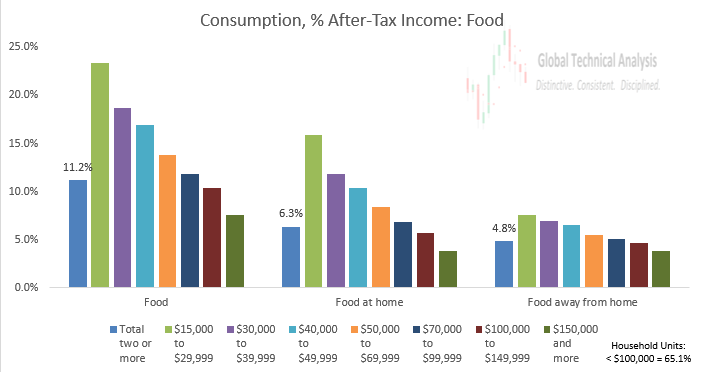

As shown above, food and beverage prices make up 15.08% of the CPI calculation. The chart below from Brett Freeze breaks down how consumers spend their money based on income classes. The lowest income earners, making $15,000 to $29,999, pay almost 25% of their earnings on food. That compares to only 7.5% for families making more than $150,000.

Housing comprises 56.3% of spending for the lowest income class and only 20% for the highest. The CPI inflation calculation does not accurately portray how inflation affects a large percentage of the population. (This is also the group whose entire boost in income from the stimulus will get absorbed by higher prices)

The Fed May Be Right For The Wrong Reason

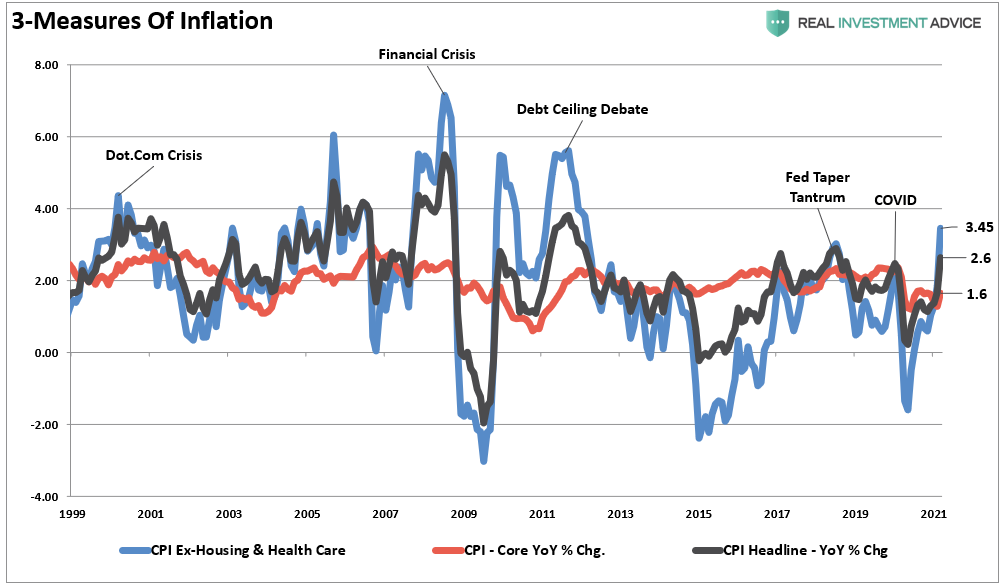

With double-digit rates of change in essential items like transportation (going back to work), food, goods and services, and energy, the impact on disposable incomes will come much quicker than expected. If we strip out “housing and healthcare,” which are fixed budget items (mortgage and insurance payments), we see that “household” inflation is pushing 3.5% annualized.

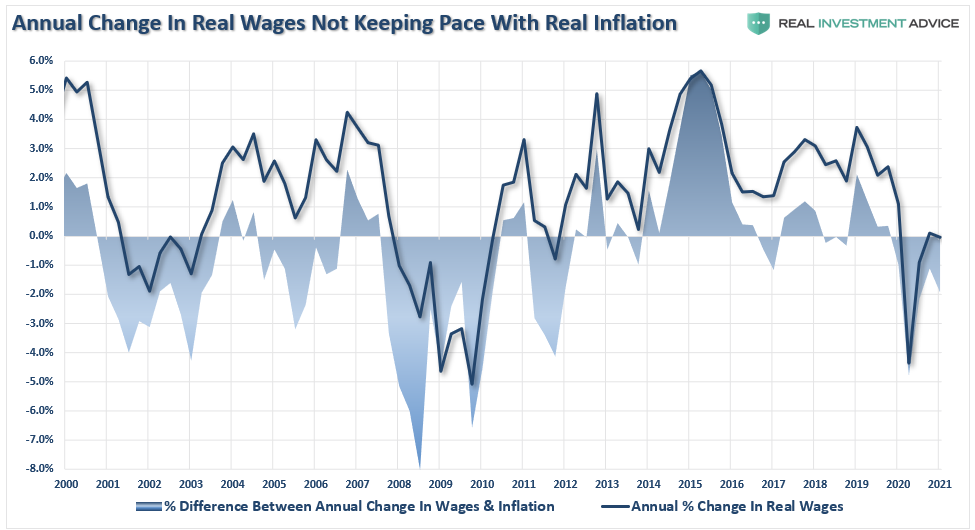

Such is particularly problematic when wages aren’t keeping up with inflation.

The Fed is probably right. Inflation will be transitory, but for all the wrong reasons.

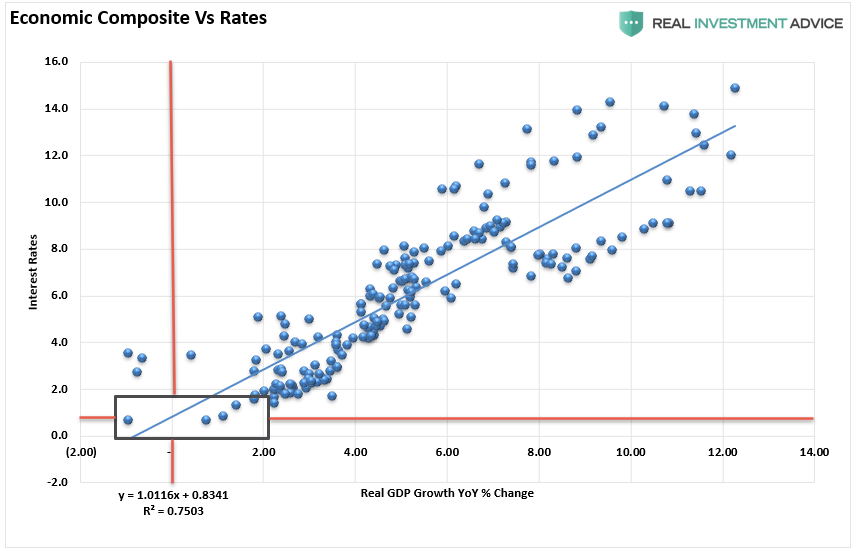

Rates Tell The Same Story

As discussed in Friday’s #MacroView, interest rates also tell us that economic growth will deteriorate markedly over the next few quarters.

“The correlation should be surprising given that lending rates get adjusted to future impacts on capital.

Equity investors expect that as economic growth and inflationary pressures increase, the value of their invested capital will increase to compensate for higher costs.

Bond investors have a fixed rate of return. Therefore, the fixed return rate is tied to forward expectations. Otherwise, capital is damaged due to inflation and lost opportunity costs.

As shown, the correlation between rates and the economic composite suggests that current expectations of sustained economic expansion and rising inflation are overly optimistic. At current rates, economic growth will likely very quickly return to sub-2% growth by 2022.”

The problem for the Federal Reserve, and as quoted by Mish, is that the fiscal and monetary stimulus imputed into the economy is “dis-inflationary.”

“Contrary to the conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year end and will undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.” – Dr. Lacy Hunt

The point here is that while economic growth may be booming momentarily, inflation, which is destructive when not paired with rising wages, will be transient. Given the massive surge in prices for homes, autos, and food, the reversal will cause a substantial disinflationary drag on economic growth.

The Fed Should Be Hiking And Tapering Now

There is a significant difference between a “recovery” and an “expansion.”One is durable and sustainable; the other is not.

Following the financial crisis, the Federal Reserve cut rates and flooded the markets with liquidity. As discussed in “The Fed Continues To Make Policy Mistakes,” the Fed should have acted sooner to prepare for the next economic downturn.

“The Fed should have started lifting rates as the spike in economic growth occurred in 2010-2011 as both the Fed and Government flooded the economy with liquidity. While hiking rates would have slowed the advance in the financial markets, the excess liquidity sloshing around the system would have offset tighter monetary policy.”

The Fed is again suppressing rates but should be using the massive liquidity injections and economic recovery for hiking rates and taper bond purchases to prepare for the next downturn.

“The majority of market participants are expecting an undramatic event including an upgraded economic outlook, a reiteration of uncertainties and signaling of no policy changes. Unfortunately, it’s an outcome that kicks the policy can down the road when the central bank should be thinking now about scaling back extraordinary measures.

The longer it takes to do so, the harder it will be to pull off eventual normalization without risking both significant market volatility and damaging what should and must be a durable and inclusive economic recovery.”

By not hiking rates now, they run the risk of being late once again.

Given the Fed waited too long to hike rates previously, such will be the same this time as they start hiking rates just as economic growth peaks due to the roll-off of stimulus.

There have been ZERO times in history when the Fed started a rate hiking campaign that did not lead to a negative outcome.

Something Is Going To Break

The “frenzy” of investors to get into the market is unlike anything we have seen since 1999.

The Fed’s problem is that in 1999 there was a bubble in “Dot.com” stocks but not in many other areas of the market. In 2007, it was a mortgage market bubble, but valuations were not extremely elevated in stocks.

Today, we are:

Pushing the second-highest level of valuations in history

Many other valuation measures such as Price-to-Sales, Tobin’s-Q, and Market-Cap to GDP are at a record.

Investors are rushing to buy the most speculative assets from various Cryptocurrencies, to Non-Fungible Tokens (NFT’s), to highly speculative companies.

Wall Street is rushing IPO’s to market at the fastest pace on record.

SPAC’s are the new asset class.

A large portion of the Russell 2000 companies have no income.

The bonds with the highest risk of default are trading at historically low rates.

Individuals are rushing to pay the highest prices on records for housing and used cars.

And, it’s all done with the highest margin debt levels in history.

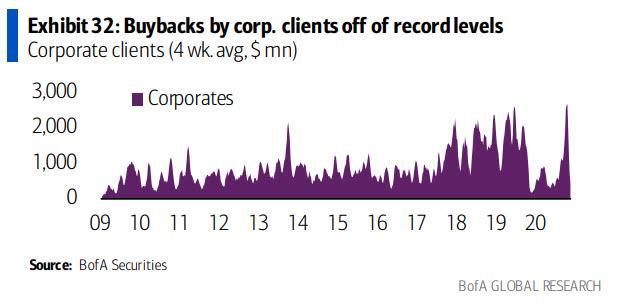

Of course, corporations are in on it as well, buying back their shares at a record pace (just after asking the government for a taxpayer-funded bailout in March 2020.)

Trapped With No Escape

In other words, it isn’t just one bubble the Fed will have to deal with during the subsequent market melt-down. It will be all of them. The magnitude of the meltdown of multiple asset classes at one time will likely be larger than the Fed can bailout.

Importantly, I believe they know this already and hope that an inflationary push will help deflate some of the risks before the bubble bursts. As my colleague Doug Kass wrote on Thursday:

“From my perch, and in the end, of course, all violation of the fundamental laws of economic and financial common sense are paid for – but every Bull thinks he will unload before the break.

John Kenneth Galbraith once wrote that “What we do know is that speculative episodes never come gently to an end. The wise, though for most the improbable, course is to assume the worst.”

I believe that there are numerous other bubbles or inflated values. Moreover, I see numerous headwinds that could reset broad valuations lower. Such includes higher corporate and individual tax rates, inflation, and inflated bullish investor sentiment.

It is easy enough to burst a bubble. To incise it with a needle so that it subsides gradually is an operation of undoubted delicacy.”

I agree.

The bottom line is the Fed is trapped. If they hike rates, they bust the bubble and destroy economic growth. If they do nothing, the bubble inflates to a point it breaks under its weight.

In my opinion, not that it matters; it seems the risk of doing nothing far outweighs doing something. Taking small actions today to slowly deflate risk seems a much better alternative to the eventual bust.

Portfolio Update

As noted above, we will trigger the next short-term “buy signal,” likely next week. As we have discussed regularly, given the daily “sell signal” was offset by a weekly “buy signal,” there was little downside risk. Such turned out to be the case.

We can now start adding some additional exposure to areas that we need, but with equity holdings at near target weights, only minor adjustments need to get done. We still carry a very short-duration bond portfolio currently as interest rates continue to push towards our target of 1.8-1.9%. At that level, we will start accumulating long-duration bonds and increasing portfolio hedges.

Another reason we don’t expect a lot of upside to markets because the recent “consolidation” failed to work off any of the overbought conditions. Notably, the market remains more than 5% above its 50-dma, which is historically extreme. Such gets corrected, usually through a price decline or a consolidation.

Over the last two weeks, we had suggested cleaning up portfolios and rebalancing risk. With that complete, portfolios should be in an excellent position to participate in whatever rally we get over the next couple of weeks.

As we head into summer, we will likely see our weekly and daily signals align with “sell signals” in late May or early June. Such will likely coincide with a realization of peak earnings and economic growth. While we don’t expect a significant reversion at this juncture, given the ongoing liquidity support, a 7-10% correction is possible and well within annual norms.

Could it be more? Absolutely.

But that is something we will navigate once we get there.

Senator Mitt Romney was raucously booed this week at the Utah Republican Party’s organizing convention, where he was trying to stumble his way through a speech about the state of Joe Biden’s first 100 days in office.

Video of his speech hit the internet on Saturday and showed a crowd of more than 2,100 Republican delegates booing him at the Maverik Center, the Salt Lake Tribune wrote. The jeers started almost instantly upon Romney’s chance to speak.

As soon as Romney takes the podium he is granted by a loud chorus of boos. “Thank you, thank you,” Romney tells the crowd.

“Aren’t you embarrassed?” Romney later asked the crowd, who was antagonizing him. He continued, trying to defend himself to the crowd: “I’m a man who says what he means, and you know I was not a fan of our last president’s character issues.”

“I understand I have a few folks that don’t like me terribly much,” Romney finally said, as the boos wouldn’t let up for more than a minute and a half.

Some in the crowd can even be heard accusing Romney of being a “traitor” or a “communist”. Romney said: “You can boo all you like. I’ve been a Republican all of my life. My dad was the governor of Michigan and I was the Republican nominee for president in 2012.”

Outgoing party chair Derek Brown had to move Romney aside, take the podium, and “scold” the delegates to get the booing to stop.

“Please, thank you. Show respect,” he asked of the crowd.

Romney then stumbled on his next few sentences as he tried to make it through the rest of his speech. We can’t help but think: if Mitt is receiving such a warm welcome in Utah, perhaps its time for the Senator to consider hanging up his spurs.

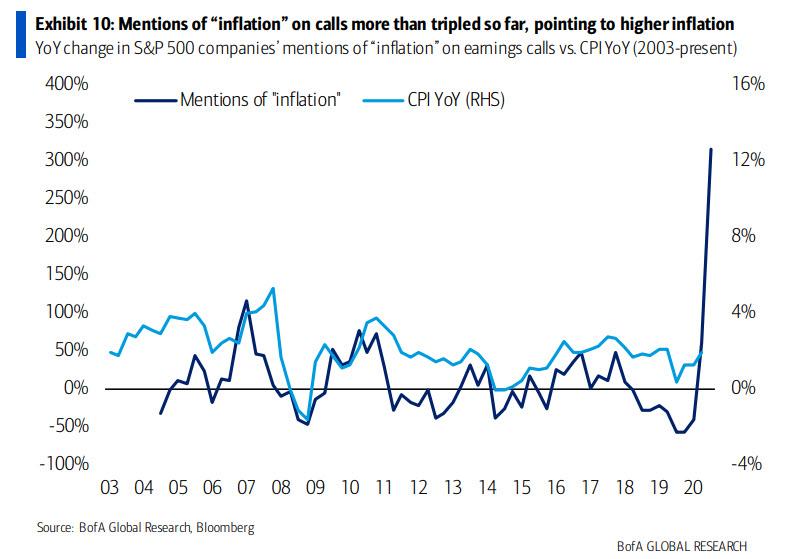

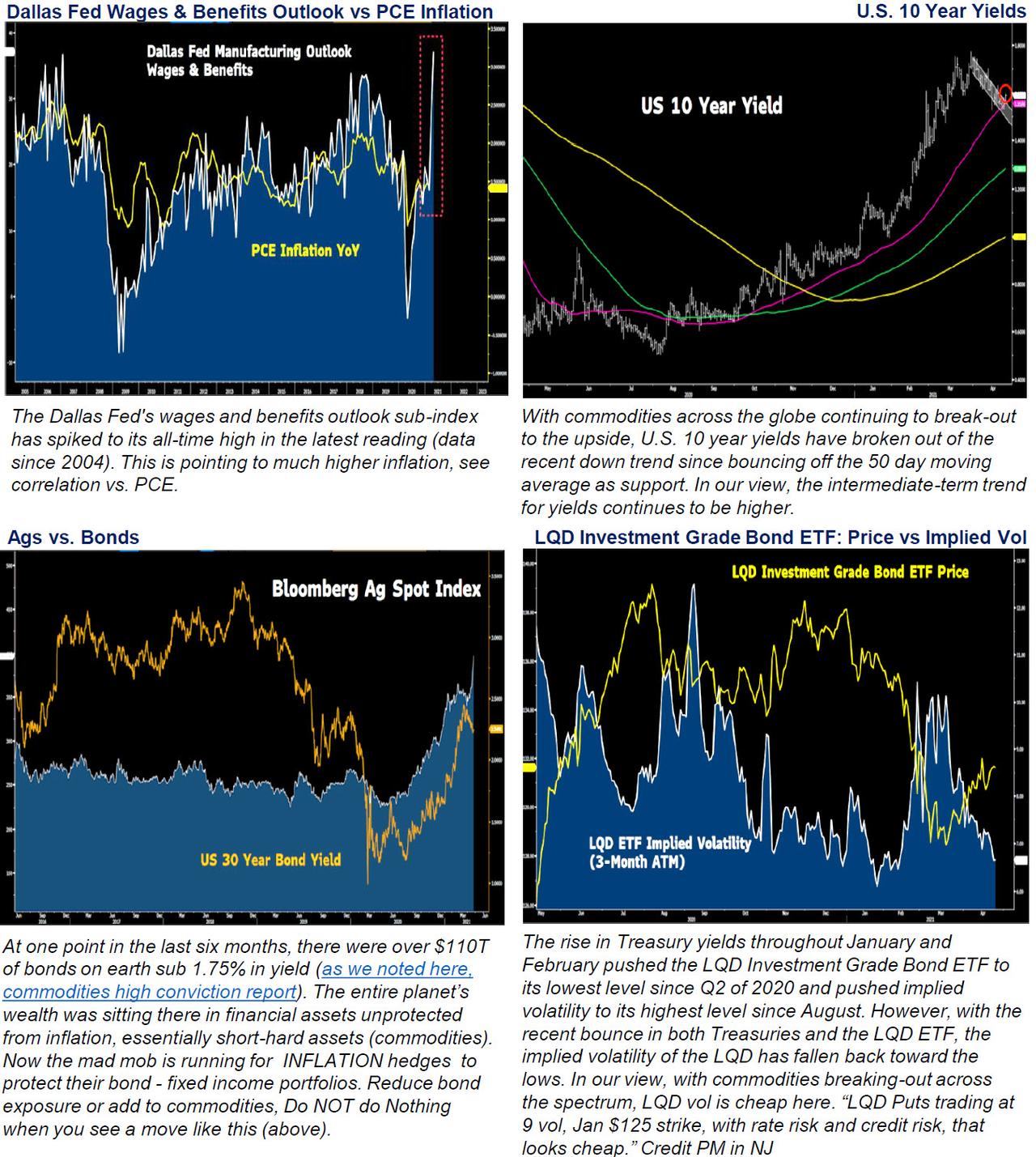

“We believe we are at the early stage of the biggest Cobra Effect in the history of economics. As the massive monetary and massive fiscal stimuli (over $15T globally) conjoin to save the economy from a deflationary depression, instead they risk hyperinflation – overweight commodities.”

Vaccination parties have broken out on many street corners as explosive human energy has come roaring out of the cage. To us, this is a preview of what is about to transpire around the planet and the “Cobra Effect” has entered the 4th inning. When governments tinker in capital markets there are always unintended consequences. Above all, we must keep in mind – what transpired in Q1 to Q4 2020 was NOT a mere tinkering.

We have just lived through a colossal public-private experiment where fiscal and monetary policy globally have been unleashed at unprecedented proportions. It is easy to sit back and think the 2021-2022 recovery will be much like the 2009-2010 vintage. This is a mistake.

A year ago when we laid out our high conviction reflation trade, inflation engines were limited to some supply chain disruptions. Today, we are looking at multiple inflation furnaces cooking away as we speak.

First, Uncle Sam has dramatically altered the employment picture with the private sector going toe to toe with Mr. Stimmy. Breaking news, when you pay human beings NOT to work it is very hard to get them back into the labor force. Friday’s employment cost index (ECI) print is simply an appetizer, with the main course shock coming to CPI (average hourly earnings) data in the months ahead.

“That ECI number is solid big” – CIO NY Based Hedge Fund. ECI spike was driven by a 1.0% jump in wages and salaries. If this is repeated over the next three quarters, the y/y rate will reach 4.1% by Q4. The Fed does not look like it will have an easy summer communicating its approach to markets. ECI wages and salaries, which follow positions (less compositional skew) jumped 4.0% SAAR in Q1. Core PCE inflation rose 0.4% MoM, +2.6% SAAR over the last three months. Why work when u have stimmy, Uncle Sam is forcing wages higher.

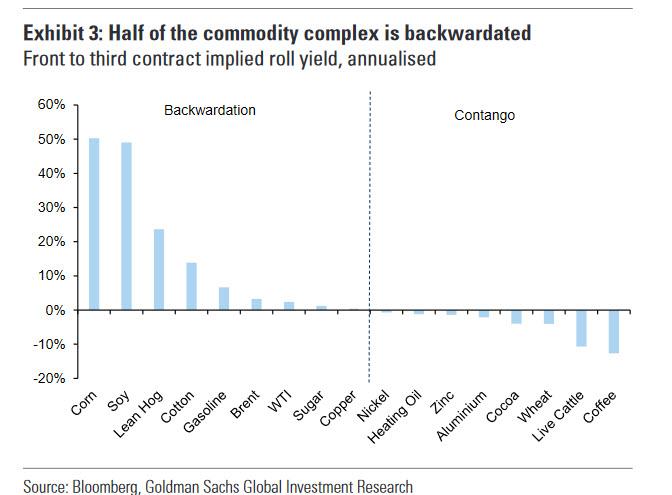

“The premium for commodities that can be delivered now versus later into the future is the highest it has been since at least 2007, signaling just how strong the world’s demand is for raw materials and how tight supplies are.” – Family Office CIO

Keep in mind, it was hot AHE data that triggered the February 2018 thirteen percent drawdown in the Nasdaq 100 and knocked the XIV Short Volatility ETF into retirement.

Today, we are looking at a whole new serpent, a far different beast. ESG inflation side effects are oozing through the commodity market (oil, gas, copper), and the agricultural inflation engine has rarely been stronger.

Real GDP in 2Q is on pace to print 12% q/q annualized rate -nearly double 1Q’s performance –with weekly tax data, weekly rail traffic, and monthly regional manufacturing indices are all surging, inflation risk highest in a decade.

For S&P 500 companies, the uncertainty factor on forward-looking profit margins has just moved from blue-sky to dark grey, in terms of true visibility.

Up until now, all the inflation-reflation forces we have witnessed have been supply-driven. As vaccinations reach critical broad distribution targets. We have yet to see real, vaccine-fired demand-induced inflation.

Risk:There’s a high probability this is it for the tech and the Nasdaq. Supply chains are a mess (disruption unquantifiable), labor shortages exploding as Uncle Sam is the private sector’s colossal drag, commodity inflation is entering a new phase, margin pressures across the SPX are developing exponentially. The Fed is digging in dovish heels which will just make all of the above-unintended consequences that much worse. It’s very similar to Q4 2018, tough guy Powell is playing a dangerous game. We remain short the NDX, long commodities (XLE, XME, etc).

“Despite printing more than $80bn in revenue, +50% YoY, the FAAMNG companies really have not moved YTD. Arguably, these big Tech companies are the world’s best businesses and are failing to catch a meaningful, sustained bid.” – JPM

Tech stocks will get destroyed as we move to the next act of this inflation beast.

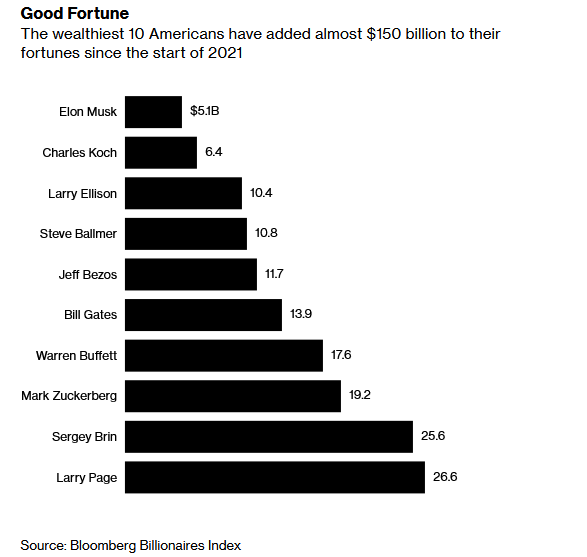

Richest Americans Add $195 Billion To Net Worth During Biden’s First 100 Days

As the Biden Administration and Congressional Democrats continue to spend money like Pretty Woman with Richard Gere’s credit card, the top beneficiaries of this ‘froth-inducing‘ stimulus have been America’s wealthiest 100 individuals – who’ve tacked on a combined $195 billion to their fortunes during President Biden’s first 100 days in office, according to Bloomberg.

The most recent gains have been fueled by the continued rise of the stock market since Biden was sworn in Jan. 20, along with the vaccination program’s fast rollout and a $1.9 trillion government stimulus package. The S&P 500 and Dow Jones indexes have both climbed more than 10% during that time.

Attempts such as Biden’s to refloat the economy can boost incomes and wealth at the very top, said Mike Savage, a sociology professor at the London School of Economics.

“We’ve seen that paradox since the 2008 financial crash with quantitative easing, which has mostly benefited people with assets, inflating their value significantly,’’ Savage said. -Bloomberg

What’s more, the richest 100 Americans saw their wealth grow by $267 billion before Biden’s inauguration if one counts gains since the 2020 election, for a total gain of $461 billion since Nov. 4. For comparison’s sake, between Donald Trump’s 2017 inauguration and last fall’s election, the same group of billionaires grew around $860 billion richer.

Biden’s coming for it though…

In addition to raising capital gains taxes and taxing inherited wealth, the Big Guy’s proposals will ‘recover’ trillions of dollars in wealth into government coffers after the wealthiest pay their ‘fair share.’

“Sometimes I have arguments with my friends in the Democratic Party,” said Biden during his first address to Congress on Wednesday. “I think you should be able to become a billionaire or a millionaire. But pay your fair share.”

Under his “American Families Plan” announced Wednesday, the top rate of personal income tax would increase to 39.6% for the highest 1% of earners from the current 37%, while the capital gains rate would be raised to the same level for those earning above $1 million, wiping out the discrepancy between income and capital gains tax rates that has benefitted many of the ultra-rich.

The wealthiest 1% currently pay 40% of all federal income taxes, according to Internal Revenue Service data, an amount that doesn’t include payroll taxes. -Bloomberg

“When you ask the American people what they want, they want corporations and millionaires and billionaires to pay higher taxes,” according to Erica Payne, founder of the Patriotic Millionaires, a group of progressive high-net-worth individuals. “It is politically a winner, it is economically the right thing to do and it is morally a no-brainer.”

Meanwhile, the Biden administration has also floated a proposal which would raise corporate taxes to fund infrastructure spending – a move which Amazon founder Jeff Bezos, the richest (known) person in the world – supported.

“We look forward to Congress and the administration coming together to find the right, balanced solution that maintains or enhances U.S. competitiveness,” said Bezos.

Conservatives, meanwhile, say the money grab is likely to backfire.

“Government investments are often sold to the public with the promise that they will improve lives and improve the economy,” said Tax Foundation president, Scott Hodge, in Congressional testimony this week. “In every case, the economic harm caused by the taxes would swamp any of the benefits from the new spending, leaving taxpayers and the economy worse off.”

Congressional Democrats are also gunning for tax loopholes in order to claw back gains made by America’s wealthy during the pandemic, with Sen. Elizabeth Warren (D-MA) proposing an Ultra Millionaire tax – which would hit those with fortunes above $50 million with a 2% annual tax on their wealth, and 3% for those with more than $1 billion.

That said, higher taxes aren’t “going to have very much effect in the long term on redistributing wealth,” according to Carnegie Mellon econ and statistics professor Robert Miller. “This focus on how we’re going to get the money is a bit misplaced – we should be thinking more about how we want to help the people that need help.”

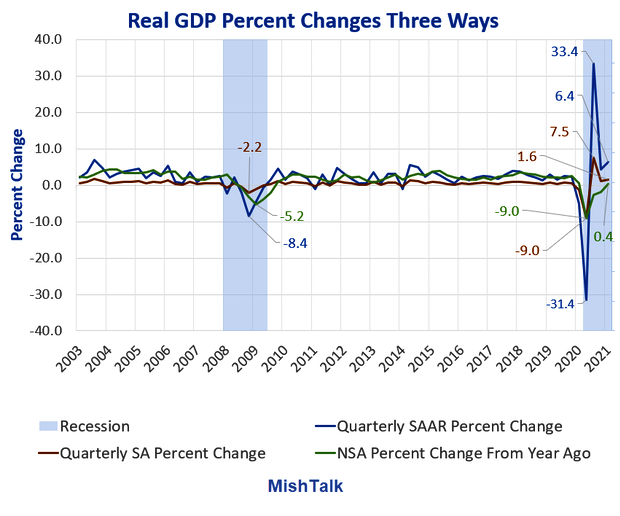

The traditional role of the committee is to maintain a monthly chronology of business cycle turning points. Because the BEA figures for real GDP and real GDI are only available quarterly, the committee considers a variety of monthly indicators to determine the months of peaks and troughs. It places particular emphasis on two monthly measures of activity across the entire economy: (1) personal income less transfer payments, in real terms, which is a monthly measure that includes much of the income included in real GDI; and (2) payroll employment from the BLS.

Although these indicators are the most important measures considered by the committee in developing its monthly business cycle chronology, it does not hesitate to consider other indicators, such as real personal consumption expenditures, industrial production, initial claims for unemployment insurance, wholesale-retail sales adjusted for price changes, and household employment, as it deems valuable. There is no fixed rule about which other measures contribute information to the process or how they are weighted in the committee’s decisions.

The committee’s approach to determining the dates of turning points is retrospective. It waits until sufficient data are available to avoid the need for major revisions.

The Keys

The two primary keys are personal income minus transfer payments and employment.

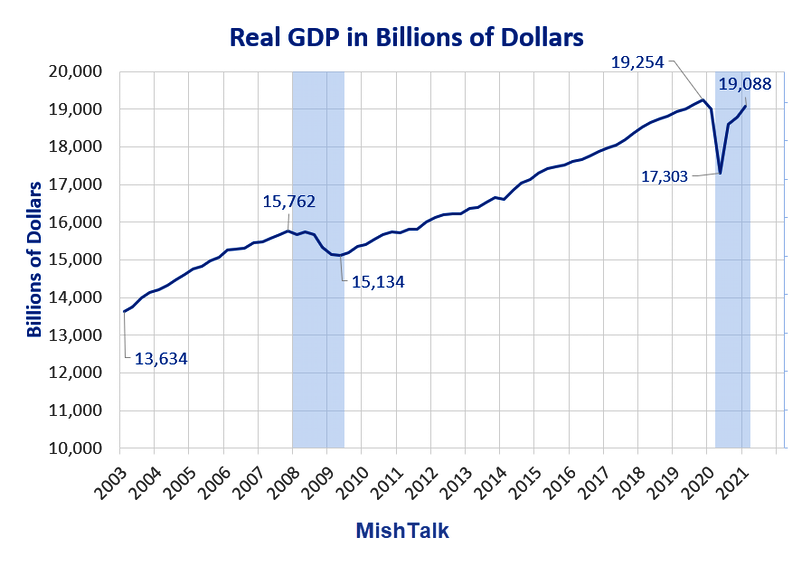

Curiously, the NBER seems to place little significance on GDP itself.

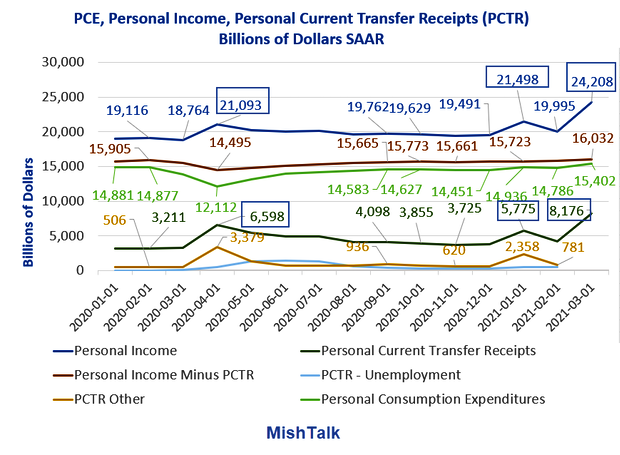

Personal Income Soars Over 21% on Third Round of Free Money

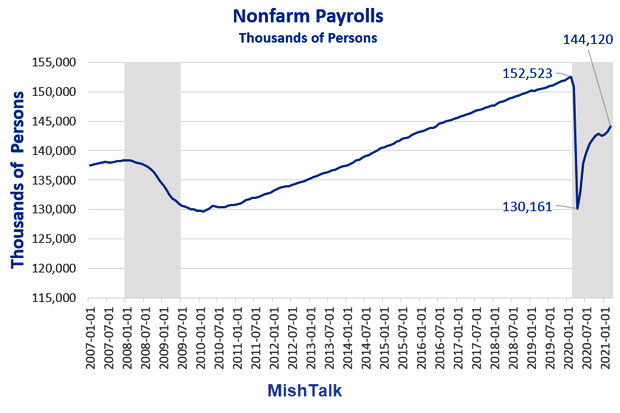

And the unemployment rate fell to 6.0%. But nonfarm payrolls tell another story.

Nonfarm Payrolls

The above chart puts a much needed perspective on the recovery.

Jobs are up 13,959,000 from the low in April 2020.

Jobs are still 8,403,000 from the February 2020 pre-covid high.

Some losses are permanent due to a surge in work-at-home and online shopping (less office space and malls needed).

What Happens When the Stimulus Efforts Stop?

That is the key question. Millions make more being unemployed than they did employed.

Also long-term rates have risen and that will impact housing.

The Fed inflated assets which have also propped up spending. Yet, despite a massive boom in housing and the stock market PCE has barely recovered.

NBER Patience

The NBER announced that the trough of the 2007-2009 recession occurred in June 2009 only on September 20, 2010. That was a lag of 15 months.

I do not know what the NBER will decide, but I do not expect a decision soon. There are too many issues and questions as well as a potential relapse as soon as the stimulus dries up.

Fed Says the Recent Jump in Inflation is Transitory