Tesla Sales In China Are “Doomed” For A “Sharp Fall” In The Second Quarter, Global Times Says

The next chapter in the “China vs. Elon Musk” saga looks like it could be ready to begin – and, indeed, it looks like Tesla’s honeymoon in China could be over.

The Global Times, China’s closest major media organization to the state, published a scathing review of Tesla’s earnings on Tuesday morning, stating that “despite record earnings” for the quarter, “Tesla’s sales in China are expected to drop sharply in the coming months due to a public relations crisis that has put the image of the otherwise popular brand at serious risk”.

“…sales in China are doomed to experience a sharp fall in the second quarter,” the report read.

While one analyst said: “It is undeniable that Tesla has widespread recognition in the Chinese market, especially in first-tier cities. The company’s fans are buying into its luxurious brand image and avant-garde intelligent system,” the report follow up by saying Tesla’s image is in “serious trouble” and that recent protests against the company were “a watershed”.

“…the company’s destiny hinges on whether a safety investigation involving a crash in Central China’s Henan Province points to a brake malfunction,” the Global Times wrote. “…if Tesla is found to have hidden quality defects from the public, the company could lose its foothold in the Chinese market, analysts warned.”

“If the results point to a malfunction, Tesla needs to recall cars with this defective brake system and immediately stop selling similar types,” independent car analyst Feng Shiming said. “The Model 3, which is sold at less than 300,000 yuan (46,260), targets medium-end consumers, whose tolerance for defects is much lower than high-end buyers, and that is partly why complaints over Tesla’s quality have erupted since last year.”

Zeng Zhiling, managing director of LMC Automotive Consulting in Shanghai, said: “For Tesla, the Chinese market is even more important than the US because the Chinese government has rolled out more support policies for new-energy vehicles (NEV), making the country the world’s largest NEV market. China is also an important production base for Tesla.”

Zeng continued: “Tesla also had problems in communication at the start. With denial and a cocky attitude, Tesla put itself on the opposite side of consumers, which is not a good thing for its image.”

Recall, just last week, the Global Times said that Tesla’s “blunder” in handling its recent PR crisis in the country could “inflict serious damage” on the Chinese market. We warned then it was a “a statement worth noting due to the Global Times’ ties to the CCP.”

The Global Times also wrote last week: “The response quickly elicited criticism from the Chinese public and various authorities in China, where many called the statement arrogant and overbearing. The simmering pressure of public opinion eventually made Tesla bow its head, with an apology letter, in which it vowed to respect consumers and abide by laws and regulations. The apology marked a 180-degree turn from its initial response; however, it may have been too late, as criticism continues to fly in.“

Additionally last week, China’s Xinhua News Agency said that Tesla’s apology for its poor service “lacks basic sincerity”. Tesla “didn’t give a ‘substantive’ response to the customer’s complaints and public concerns, and the apology letter was no more than crisis management,” the news agency reportedly said.

The number of container ships stuck at anchor off Los Angeles and Long Beach is down to around 20 per day, from 30 a few months ago. Does this mean the capacity crunch in the trans-Pacific market is finally easing? Absolutely not, warned Nerijus Poskus, vice president of global ocean at freight forwarder Flexport. “It’s not getting better. It’s getting worse,” he told American Shipper in an interview on Monday.

“What I’m seeing is unprecedented. We are seeing a tsunami of freight,” he reported.

“For the month of May, everything on the trans-Pacific is basically sold out. We had one client who needed something loaded in May that was extremely urgent and who was ready to pay $15,000 per container. I couldn’t get it loaded — and we are a growing company that ships a lot of TEUs [twenty-foot equivalent units]. Price doesn’t always even matter anymore.”

Restocking driving volumes higher

Poskus said that trans-Pacific import volumes are still rising. He noted that January trans-Pacific imports were up 10% versus 2019 (comparisons to 2020 numbers are skewed by COVID) and 13.5% in February, then jumped 51% in March. “So, we’re now at 1.5 times pre-pandemic levels.”

With imports far outpacing retail sales growth, he attributed volumes to inventory restocking. “The restocking is actually affecting the trade even more than growth in demand. That tells me that this will last even longer. Let’s say U.S. consumer demand slows down in Q3 and Q4. That’s not expected, but even if it does, [capacity availability and rates] shouldn’t improve quickly, simply because of the huge restocking demand.”

Poskus also believes there is a growing export backlog piling up each day in Asia, awaiting available ship slots. If that backlog grows too big, he said, “I honestly don’t know what’s going to happen.” As a result of the backlog and restocking demand, he thinks “prices will remain high and shipping will probably remain difficult for the rest of this year. And then after that, you have the peak for Chinese New Year in 2022.”

About to get even worse

He said that the situation today is the worst he’s witnessed — and he believes it’s about to get even more severe.

“Buckle up. The month of May will be the worst people have ever seen,” he predicted. Because some shippers will have to wait in line behind the growing backlog in Asia, he expects “what’s going to happen soon is that some importers won’t even be able to get on the boat. For them, it will almost feel like trade is coming to a halt.”

Poskus’ comments mirror cargo bookings data. FreightWaves’ SONAR platform features a proprietary index of shippers’ ocean bookings (SONAR: IOTI.USA). Bookings to the U.S. are measured in TEUs on a 10-day-moving-average basis as of the scheduled date of overseas departure. As of Monday, the index was at a new all-time high and forward bookings data showed a continued rise ahead.

As of Friday, the Freightos Baltic Daily Index assessed the Asia-West Coast spot rate (SONAR: FBXD.CNAW) at $4,797 per forty-foot equivalent unit (FEU) and the Asia-East Coast rate (SONAR: FBXD.CNAE) at $6,306 per FEU — both near all-time highs.

But that’s only part of the rate story. “Indexes are not bills. Premiums are not reflected in the indexes,” said Poskus. Earlier this year, some of the premium charges came down as container availability in Asia improved. That’s reversed, said Poskus, who noted that the Ever Given incident in the Suez Canal pulled container equipment from the market. “Container shortages in Asia are again very bad because of the Ever Given, and it will take another four to six weeks to come back to normal.”

The added premiums to get spot cargo loaded “are back and they’re higher than before,” he said. “They are $2,000-$3,000 above FAK [spot price] and that’s the best case.”

Spot cargo that was booked 21 days prior and was forecast within the shipper’s allocation is still getting FAK pricing on spot, he noted. However, “everything last minute is basically a free-for-all auction. You are basically offering as much money as you can and hoping somebody will take it. Many importers are now struggling. We’re seeing so many new customers approaching us asking for help because they can’t get loaded.”

Poskus’ numbers are around double Xeneta’s. “We are seeing fixed-price increases of slightly over 100% on Asia-West Coast and about 75% on Asia-East Coast,” he said. “Also, almost every single contract rate is subject to peak season surcharges [PSSs], so the prices aren’t exactly fixed. I think the PSSs will reduce the gap between the spot and fixed market.”

Asked about shippers who have yet to conclude their annual contracts, he said, “If you want a fixed price in today’s market, the answer you’ll get from the carriers is that it’s too late. We advised many importers to sign early because the trans-Pacific contract season would close [early] because there’s more demand than supply. And that’s exactly what happened.”

There are exceptions, such as larger shippers with June-to-June contracts who began discussions with carriers earlier this year. “But if you are just a simple importer and you are yet to sign your fixed contract, you will be in the spot market,” said the Flexport vice president.

Advice to importers

Poskus offered several pieces of advice to importers scrambling to get container loads to the U.S.

He noted that carriers need reefers in the U.S. market for refrigerated exports to Asia. On the way back from Asia, these reefers are powered down and can be used as non-operating reefers (NORs) to transport dry cargo. “Believe it or not, carriers are still moving some NORs empty because importers don’t like them. This is a missed opportunity to move cargo in NORs. My advice is: Take that option. If you’re searching for the best solution in this market, you’re going to see even more delays.”

He also suggested moving cargo via less-than-container-load (LCL) shipments. “LCL is still moving. Of course, you cannot move thousands of containers LCL, but if you have something urgent, you can still get space for LCL on May sailings. Instead of waiting, break your some of your shipments down into LCL shipments and at least get some inventory,” he said.

Yet another option: Be creative with routings. For example, direct China-West Coast sailings may be sold out, but cargo can be routed from China through the Panama Canal to Cartagena, Colombia, then back through the canal to the West Coast. “It has a longer transit time but it can be loaded in the same week and it’s an option versus waiting a month and a half to get loaded [for the direct route],” he said.

“Just get your cargo to the continent of North America and from there you can get it to where it needs to go, whether it’s with NORs or LCL or transshipping [through hubs like Cartagena] or shipping it to Canada and then putting it on rail to Chicago and trucking it to New York. It will be expensive, but at least it will get there.

“You have to be flexible. Look for any routing and be creative. It’s a moving target. And don’t wait. If something opens up, act fast.”

“They’re Guessing” – ‘Bond King’ Gundlach Rejects The Fed’s “Inflation Is Transitory” Narrative

Don’t believe your lying eyes, will be the message tomorrow from The Fed’s Jay Powell as he hypnotizes investors to believe that “inflation is transitory” and they have “the tools” to manage it.

‘Bond King’ Jeff Gundlach is not buying that line and told BNN Bloomberg in an interview this morning.

“…more importantly, I’m not sure why they think they know it’s transitory… how do they know that?”

“…there’s plenty of money-printing that’s been going on, and we’ve seen commodity prices going up massively… home prices in the US are inflating very substantially… so there’s a lot of inflation that’s already baked in to input prices.”

Gundlach does admit that Powell has a point in the very near term as the prints were about to see “which could be as high as 4% [for CPI]” are off of year-ago, very depressed levels. “…what he means by transitory is that the base effect will lead to problems in the next few months but then the base effect will become less problematic.”

But, Gundlach adds, “it’s not clear to me that inflation is going to go back down to around 2 to 2.5%… we don’t know, nobody knows… but we’re most concerned with the fact that The Fed thinks they know.”

This is worrisome because The Fed’s track record is anything but inspiring…

“when I go back to the global financial crisis, when we almost had a complete meltdown of the financial system, Ben Bernanke completely missed all of the problems that led to the crisis.”

Bernanke’s infamous “contained to subprime… and subprime is only a sliver of the market” comments could be about to be trumped by Powell’s “inflation is transitory” comments as Gundlach warns “there’s plenty of indicators that suggest inflation is going to go higher and not just on a transitory basis.”

The Fed is “trying to paint the picture” of control, but Gundlach tries to make clear: “they’re guessing.”

So, what does that mean for markets?

While some fear “we ain’t seen nothing yet” in terms of yields rising (and multiple contraction), Gundlach notes that “it really depends on just how much manipulation the authorities are willing to do.”

The billionaire fund manager notes that yields are “still very low… well below the current inflation rate… so we have negative yields everywhere on the yield curve.”

It’s also “hard to figure out who’s going to buy the bonds,” he notes, “as we are about to see issuance like we have never seen before.” Foreigners have been selling bonds for years and domestically there is little demand, so Gundlach notes the only one left to soak up all this extra supply is The Federal Reserve, which has already expanded its balance sheet massively in the last 12 months.

“Who’s going to buy all these many trillions of dollars of bonds? Foreigners have been selling for years and they’ve accelerated their selling in the last several quarters, domestic buyers are not exactly selling, but they’re not adding to their holdings. So what’s left to absorb all of the spawn supply is the Federal Reserve.“

“Left to true, free markets, bond yields at the long-end would obviously be higher than they are now.”

And so who will buy all these bonds with negative real yields – The Fed… “and they have been transparent about their willingness and ability to buy bonds and expand their balance sheet with no ceiling.”

Gundlach is talking about Yield Curve Control, reminding viewers that “The Fed can set the long-end wherever they want it… there’s a precedent for this from back in the 1940s into the 50s,” in order to ease the pain of the debt from World War II.

Of course, Gundlach warns ominously, “once they stopped the yield curve control, we went into a 27 year massive bear market in bonds, because of ‘guns-n’butter’ policies… which look like our policies today.”

Simply put, he sees “an echo [in current markets and policies] of what happened in the late 1970s into the early 1980s.”

His forecast is that “The Fed will allow the market forces to take yields to higher levels [10Y 2.25%] before stepping in.”

The Bond King also note that the US stock market is very overvalued by virtually every important metric, and especially so versus foreign markets such as Asia and even Europe.

“I bought European equities a couple of weeks ago, literally for the first time in many years. I can’t remember the last time I did it. And that’s largely because I think the U.S. dollar is almost certain to decline over the intermediate to long term.”

There’s a lot more in the interview on the impact of Biden’s stimmies and potential tax hikes…

Most people view the Federal Reserve as an important policying-making body driving the economy. But in this clip from an interview with Jay Matin at Cambridge House, Peter Schiff says the Fed’s primary role is that of a marketing firm selling the populace on bad economics and trying to convince everybody that everything is great.

Peter said he thinks a large part of the Fed’s job today is public relations and spin.

To try to create a false sense of confidence in the US economy and the US dollar.”

Peter referenced an interview he saw with former Federal Reserve Chairman Ben Bernanke. The interviewer played clips of Bernanke back in 2005 and 2006 as he claimed everything was great and there was nothing to worry about. Bernanke said there was no housing bubble and any problems in the subprime mortgage market were contained. The interviewer asked Bernanke how it felt to be so wrong.

Look, you couldn’t have been more wrong. And here you were chairman of the Federal Reserve. You had all this information. More than anyone else. Now, he didn’t say, ‘Peter Schiff was out there saying it’s a housing bubble. We’re going to have a financial crisis.’ He didn’t bring me up. But he’s basically saying, ‘You had more information than everybody, yet you were so completely wrong.’ Instead of saying, ‘Yeah, I really feel kind of dumb now that I look back. God, what was I thinking? I was so clueless,’ what Ben Bernanke said, to basically save face, his answer was, ‘Well, you know, I couldn’t exactly speak forthrightly or honestly.’ I can’t remember if he said honestly. But, ‘I couldn’t actually say what I actually thought because I was part of the administration.’ And I’m thinking, what? This is what he just said? Because the Fed is supposed to be independent.”

The former Fed chair just put a spike through the myth of central bank independence. He admitted he was toeing the line for the administration. And as Peter points out, Bernanke was basically saying he got it wrong because he wasn’t even trying to get it right.

[Bernanke was saying] ‘I was just trying to reassure everybody that everything was fine and there was nothing to worry about because I was part of the administration.’ I just never believe anything they say at the Fed. I mean, I don’t believe what politicians say either.”

This should give us pause when we hear Jerome Powell assuring us that inflation is “transitory.” Is this just PR spin? Does he know the truth? Is he refusing to tell us because he’s “part of the administration?”

Interestingly, nobody was outraged at Bernanke’s confession. Nobody seemed particularly concerned that a former Fed chair basically admitted he lied to protect a political narrative.

More disturbingly, Peter said on his podcast that he suspects the same thing is happening today.

Either the Fed knows that we have a huge inflation problem on its hands and is lying about it, or it’s completely clueless and doesn’t realize it.”

Neither scenario is particularly comforting.

The Federal Reserve is hanging its hat on the fact that it printed a bunch of money over the last 10 or 20 years and price inflation never reared its ugly head. Therefore, we can do this forever. But as they say in the investing world, past performance doesn’t guarantee future results. Peter said he thinks this will ultimately go down as the Fed’s biggest blunder.

Much more so than the mistake in its bad read on subprime problems being contained. The idea that inflation was transitory is going to be an even bigger mistake and an even bigger policy failure, because, by the time the Fed is forced to admit that they were wrong and inflation wasn’t transitory, they will have waited too long to do anything about it.”

Market Pleasantly Surprised By Unexpectedly Solid 7Y Auction

After two mediocre auctions on Monday, when both the 2Y and 5Y sales saw tepid market interest, some rates traders were worried that today’s 7Y auction would be ugly. Not February 2021 ugly, mind you, which we remind readers was the closest the US has had to a failed auction and sparked the furious dump across the curve which spilled over into stock, but still ugly.

Well, besides the smallest possible tail of 0.1bps, it actually was a pretty solid 7Y auction.

Yes, the high yield of 1.306% was the highest since January 2020, rising just above the 1.300% in March, and yes, it did tail the 1.305% When Issued (just barely), but the other indicators were relatively solid.

The Bid to Cover rebounded from last month’s 2.230 to 2.314, the highest since December and well above the catastrophic 2.045 in February.

The internals were similarly solid, with Indirects of 57.1%, in line with last month’s 57.3% and while this was below the 57.7% six-auction average, it was well above the record low 38.1% hit in February. Furthermore, in keeping with recent trends in other tenors, the Direct takedown rose to 20.6%, well above both the March 18.0% and the recent average of 17.1%, leaving Dealers with 22.3%, the lowest since January and below the recent average of 25.2%.

Overall, this was a surprisingly solid auction, and the market reacted accordingly, with the 10Y dipping from session highs of 1.60% just before the auction to 1.59%, in line with yesterday’s highest yield.

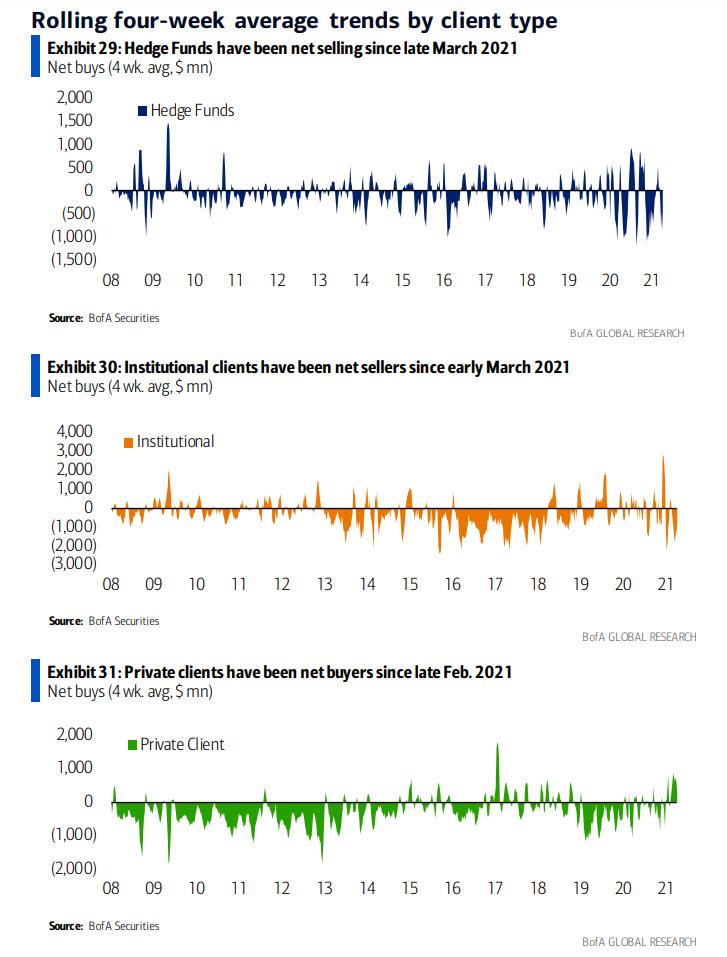

Selling Frenzy Among BofA Clients Accelerates, But Buybacks Soar Sending Market To Record High

One week ago, Bank of America warned that it had observed a sharp reversal to “increasingly euphoric sentiment” among its institutional, hedge fund and HNW clients, all of whom sold in the previous week even as stocks continued their grind higher. This happened around the time that Goldman’s Prime Brokerage had observed a startling streak as hedge funds sold stocks for 7 days out of 8, which prompted us to warn that a short squeeze was coming… we were right, because just a few days later the S&P was back at all time highs on – you guessed it – another whopping short squeeze.

But what about BofA’s “smart money” clients? Did the sharp reversal in “euphoric sentiment” reverse, and is everyone bullish again?

Not at all – according to the latest weekly client flow trends report from BofA’s Jill Carey Hall, bearish sentiment accelerated and for the second week in a row the bank’s clients were net sellers (-$2.0B) of US equities with net sales in both single stocks and ETFs (only the third time this year clients sold ETFs).

Not surprisingly, retail clients were the “least dumb money”, and according to BofA were once again the only client group to buy stocks, albeit at the weakest level since mid Feb.

That said, retail clients have been net buyers for nine straight weeks as hedge funds and institutions have pared back. In fact, institutional clients sold stocks for the second week in a row while hedge fund clients, which led outflows, sold for the fourth week (largest outflow in over a month).

Considering the skepticism among institutions and hedge funds, it will hardly come as a surprise that what stock clients bought (and they were net buyers of seven of 11 sectors) it was led by defensives/growth (Health Care, Tech, and Utes), while net sales were largest in interest-rate sensitive sectors (Comm. Svcs. and Financials) as well as Cons. Disc.

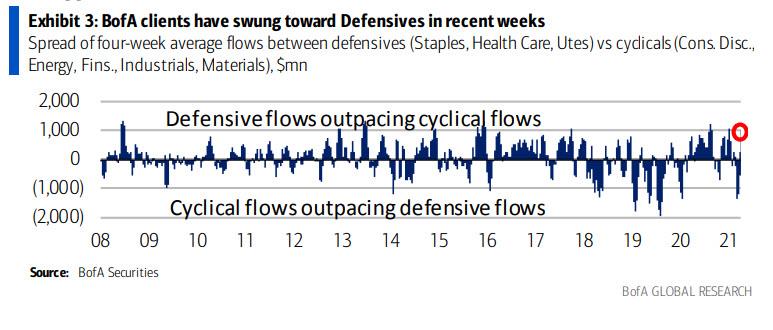

As BofA’s Jill Carey Hall summarizes, flows suggest “increasingly defensive positioning in recent weeks (cover chart): last week marked six straight week of outflows from Cons. Disc., and five straight weeks of outflows from Fins. which was also the largest weekly outflow in nearly a year and in the bottom 98th percentile. Meanwhile, Staples saw net inflows for the second week in a row after seven straight weeks of outflows and inflows into Health Care were the largest since early Jan (top 98th percentile).”

That said, we may be on the cusp of a reversal: according to the bank, defensive vs cyclical flows have crossed above 1 std. dev. which typically coincides with peak defensive flows and a shift towards cyclicals.

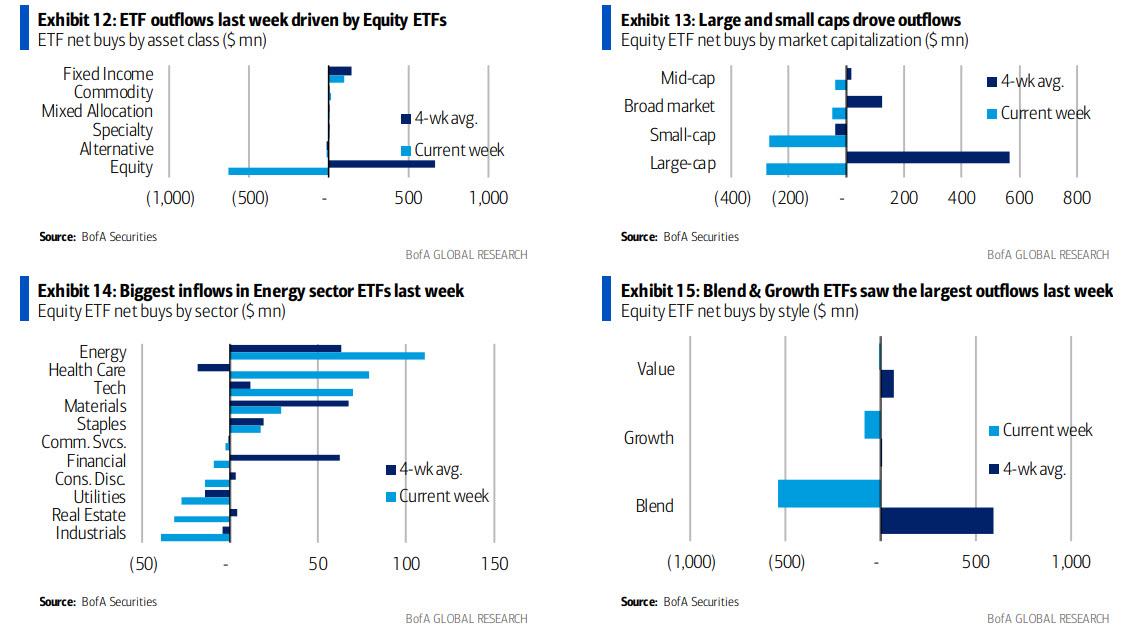

Away from single stocks, BofA clients sold both Growth and Value ETFs with bigger outflows from Growth ETFs: this was the first weekly outflow from Value ETFs since mid-January. Some more details at the ETF level:

Clients were net buyers in five of 11 sector ETFs. Flows at the sector level were mixed into:

value (Energy),

defensive (Health Care), and

growth (Tech) areas of the market.

Meanwhile, Industrials and bond proxies (Real Estate and Utes) saw the biggest outflows.

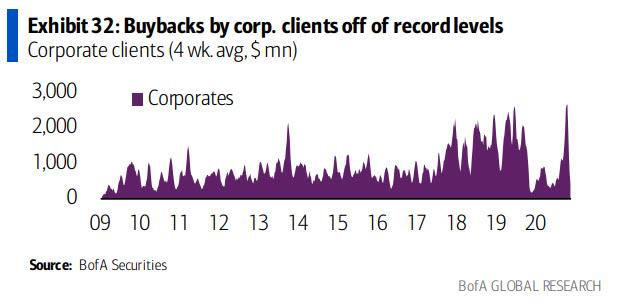

One final question: if most BofA clients were dumping, how did stocks rise to new all time highs? Simple: the same reason we listed in “The Catalyst For The Next Leg Higher: Buyback Blackout Period Just Ended” – according to BofA, buybacks accelerated vs the prior week and reached the highest level since the start of reporting season, driven by Fins. The easing of capital restrictions is one reason we’re bullish Fins. but we believe corporate cash priorities broadly may shift towards capex.

In short: we are back to the pre-QE market where it wasn’t Fed purchases as much as (debt funded) stock buybacks that provided the relentless dry powder pushing risk assets to all time highs. There is just one difference – not only do we have record buybacks but we also have $120BN in monthly Fed liquidity injections. We say that just in case someone is naive enough to actually short the manipulated policy tool once upon a time known as “the market.”

A new judge has been assigned to oversee a legal challenge to a Senate-led audit of votes in Arizona’s largest county for the 2020 presidential election, the Superior Court of Arizona in Maricopa County announced Monday.

Judge Daniel Martin will be taking over the case after Maricopa County Superior Court Judge Christopher Coury, a Republican appointee, recused himself from the legal challenge on April 25.

Martin, who was appointed to the bench in 2007 by Democratic Gov. Janet Napolitano, is currently assigned to the civil division after having previously been assigned to the family, criminal, and juvenile court departments.

According to Martin’s Superior Court biography, he formerly worked as an associate at the law firm Brown & Bain—which merged with Perkins Coie—a leading pro-Democrat law firm—in 2004, after Martin’s time at the firm. Election attorney Marc Elias is a partner at that law firm, chair of Perkins Coie’s Political Law Group, and one of the Democratic Party’s top lawyers.

Elias previously suggested in a Twitter post that the Arizona GOP may receive “sanctions” for a prior lawsuit that sought a hand count audit in Maricopa County.

The announcement comes after Coury recused himself when he learned that attorney Chris Viskovic, with whom he had a prior working relationship, had joined the case.

According to a copy of the recusal first obtained by 12 News, the court received filings at 4 p.m. on April 25 that included names of new attorneys, including Viskovic, who worked at the office of Coury “as an extern within the past five years.”

Viskovic now holds a position as a junior associate at Kolodin Law Group PLLC, which is representing the Florida-based cybersecurity firm Cyber Ninjas in court. Cyber Ninjas is one of four firms hired by the state Senate to conduct the audit.

The recusal noted that in accordance with the state’s code of judicial conduct and rules of the Arizona Supreme Court, Coury must recuse himself from any further involvement in the case.

The audit started on April 19. Companies hired by the state Senate are examining 2.1 million ballots, testing voting machines, looking for IT breaches, and performing a hand count.

The state-issued subpoenas that were needed to execute the audit were ruled as valid on Feb. 25.

Real-time camera footage of Maricopa County’s large-scale audit of the 2020 election, Maricopa County, Ariz. (Screenshot/The Epoch Times)

Arizona Democrats filed an emergency request to block the audit on April 22. Coury granted the request the following day but only if the party would post a $1 million bond. Democrats refused, so the audit wasn’t paused.

Coury hasn’t been popular among Democrats, who campaigned to oust him last year from another four-year term on the bench over his ruling on an education ballot proposition called Invest in Ed.

The Maricopa County Democratic Party in October 2020 campaigned to oust Coury, creating a website that called him an “activist judge” after he ruled that the summary for the proposed tax hike for education was misleading.

The Superior Court has announced that all hearings previously scheduled under Coury are canceled. Each side of the legal challenge will have 10 days to tell Martin how they think the case should be handled moving forward.

After Martin was assigned to take over, the Arizona Democratic Party, however, requested an “immediate hearing,” 12 News reported. According to the news outlet, a new hearing has been scheduled for 11 a.m. on April 27.

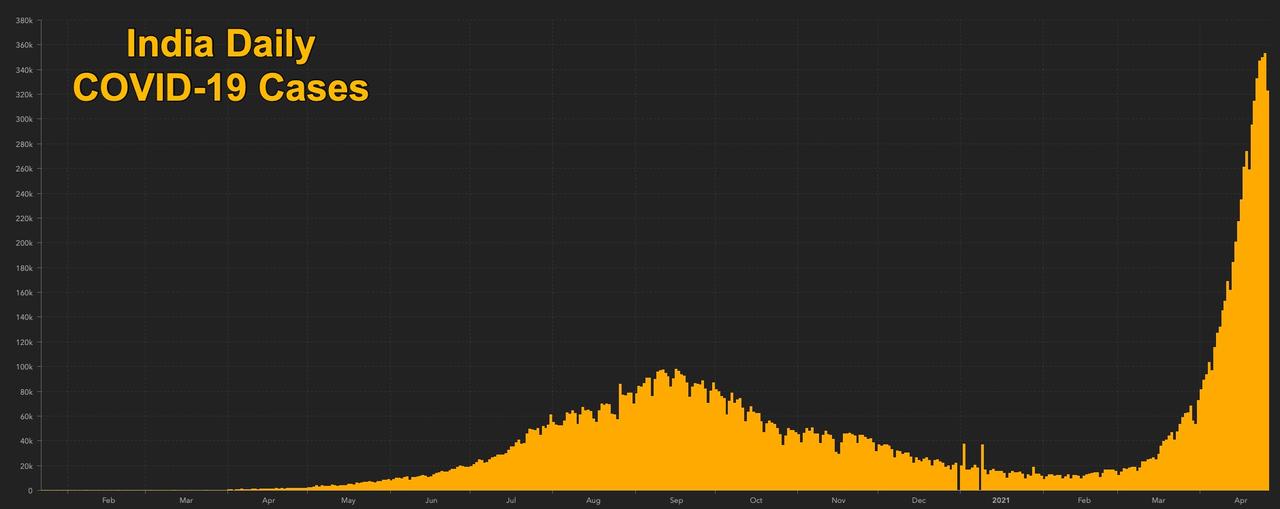

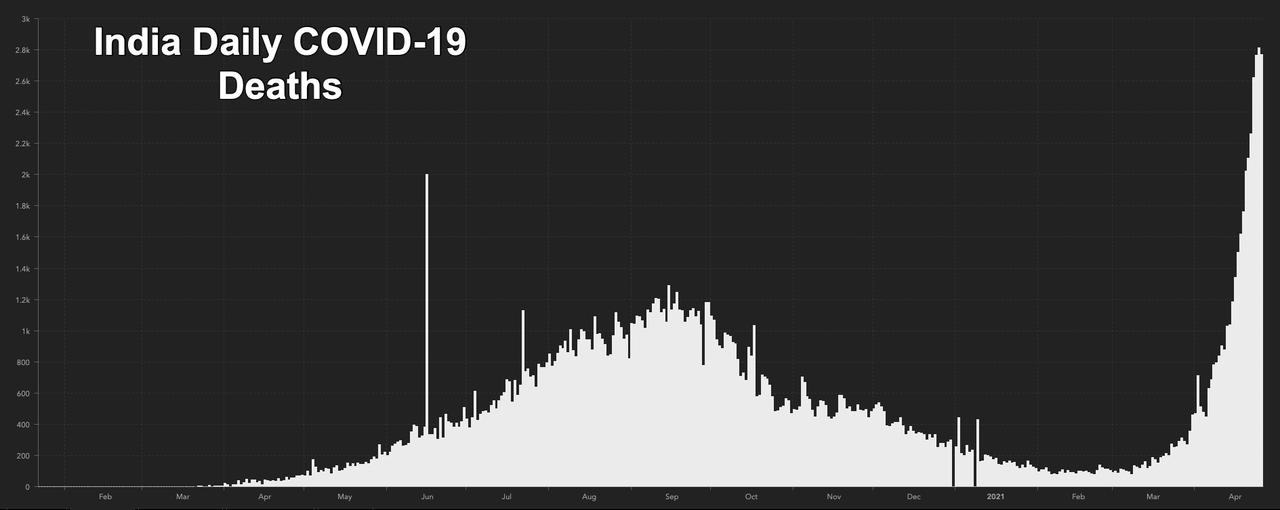

Shocking Video Shows Body Falling Out Of Indian Ambulance As COVID Crisis Worsens

India’s devastating second wave of COVID-19 continued to smolder overnight as Indian health officials reported more than 300K new cases for a sixth straight day (though the latest number is less than a record 353K cases reported Monday). India’s army pledged to provide urgent medical aid to help battle the staggering spike in new infections, yet oxygen supplies and beds remain low at hospitals across the country, but particularly in the capital city of Delhi, and other large population centers. Across India, another 2,771 COVID-19 deaths were reported, bringing the national death toll to 197,894.

These latest numbers bring India’s total to 3.8M new COVID-19 cases over the last two weeks. Citi analysts pointed out that states accounting for roughly 50% of India’s GDP have announced weekend lockdowns. As Australia joins a growing list of nations halting all commercial travel from India, analysts see growing downside risks to their 1QFY22 real GDP forecast (1.6% QoQ, saar).

Every day, it seems, there’s some new viral story emerging out of India’s COVID-19-induced misery. Last week, westerners were warned about crematoriums across India working overtime due to the surging deaths. Well, on Tuesday, video showing a patient’s body falling out of the back of an ambulance went viral on western social media networks.

The incident, which took place on Friday, has sparked an uproar in the central state of Madhya Pradesh. In the video, the ambulance can be seen leaving the gates, then swerving a corner. A side panel falls open and a shrouded body falls out onto the road. Family members can then be heard yelling in protest.

Shocking! In Vidisha people are alleging that dead bodies are not being handed over to them, an ambulance is taking away a deadbody people noticed after the dead body fell from the ambulance as the driver panicked! @ndtv@ndtvindia@manishndtv@GargiRawatpic.twitter.com/RGVkcM0bAt

A medical official told reporters that the ambulance was old and had been donated by an unspecified NGO.

As western nations including the US, Germany and others rush to send aid to India, Gilead Sciences announced Tuesday that it would give India at least 450K vials of its COVID-19 drug remdesivir and donate active pharmaceutical ingredients to boost production, as infections surge in the country. India has an official tally of 17.31 million infections and 195,123 deaths, health ministry data shows, although health experts say the figures likely run higher.

Fears that India’s latest outbreak might spread across Asia intensified as Thailand, another closely watched country which had been lauded for its success in battling the virus, reported 15 new deaths on Tuesday, a new daily high, as its third-wave of the outbreak continued to intensify. The health ministry also reported 2,179 more cases. Thailand for months had suppressed the virus but a new outbreak emerged several weeks ago.

Finally, after a third state of emergency measure was ordered across Tokyo, Osaka and Kyodo, Japan’s self-defense force is planning to open a mass vaccination center in Tokyo next month. The Defense Ministry tweeted it had been asked by PM Yoshihide Suga to set up the Tokyo vaccination centre by May 24 with plans for it to operate for three months. The facility will service residents in the capital and the surrounding prefectures of Saitama, Chiba, and Kanagawa.

While US equity averages charge to new record highs, the resurgence in COVID-19 in India and Japan has weighed on equity benchmarks across the Continent. Japan has been one of the worst performers among major global equity markets in recent weeks. The Tokyo Stock Exchange’s blue-chip Nikkei Stock Average index has fallen over 2% in the last week and remains flat compared to a month ago. The broader Topix index has weakened nearly 3% in the past month.

Update (1220ET): Just as Fauci had hinted at, fully vaccinated people can venture outdoors without masks, according to updated guidance from the Centers for Disease Control and Prevention issued Tuesday. The guidance applies to fully vaccinated individuals, which health officials classify as two weeks after the second dose of the Pfizer or Moderna vaccines and two weeks after the single-dose Johnson & Johnson vaccine.

Vaccinated people can unmask while:

Doing physical activities outdoors alone or with members of your household like walking, running, hiking or biking.

Attending a small outdoor gathering either with fully vaccinated people or a mixture of vaccinated and unvaccinated people.

Dining at an outdoor restaurant with friends from multiple households.

Current guidelines on vaccinated people indoors and traveling still applies.

“CDC cannot provide the specific risk level for every activity in every community, so it is important to consider your own personal situation and the risk to you, your family and your community before venturing out without a mask,” CDC director Rochelle Walensky said in prepared remarks.

Health experts are insisting that the CDC should implement permanent mask mandates even after the COVID-19 pandemic ends.

Despite many areas of the U.S. beginning to open up again and anecdotal evidence suggesting a significant drop in the number of people routinely wearing masks, some are loathe to go back to normal.

“We have seen benefits of masking that occur,” Health Director Dr. Nicole Alexander-Scott told The Providence Journal.

“So there may be a new form of normalcy where masks don’t necessarily have to go away.”

His sentiments were echoed by Dr. Leonard A. Mermel, medical director of epidemiology and infection control at Rhode Island Hospital, who said making people wear masks all the time was worth it to stop the spread of other viruses aside from COVID-19.

“Within the Lifespan system we are seeing far fewer of all the respiratory viruses than we are used to seeing at this moment in the calendar year… So it’s impressive: the COVID preventative strategies are having an impact on other respiratory viruses, which just makes sense: they spread in a similar fashion,” said Mermel.

“It would not surprise me if that became a recommendation from the CDC,” he said.

“It’s a pretty low price to pay to try to reduce the risk to oneself and to particularly loved ones who may be at particular risk of these sorts of infections causing harm,” he added.

Other experts have argued that the impact of viruses will only be more severe in the long run if human immune systems are prevented from being tested by new infections, harming herd immunity.

Medical professionals are still attempting to have mask mandates become part of the “new normal” despite Dr. Anthony Fauci acknowledging yesterday that it would be “common sense” for the CDC to start relaxing measures.

“I mean, if you are a vaccinated person, wearing a mask outdoors, I mean, obviously, the risk is minuscule,” Fauci told ABC’s This Week.

“Obviously the risk is really very low, particularly if you’re vaccinated,” he added.

Meanwhile, a new study by the Massachusetts Institute of Technology has found that there is “little benefit” to 6 meter social distancing rules and that people who are as much as 60 feet away face the same risks.

“The distancing isn’t helping you that much and it’s also giving you a false sense of security because you’re as safe at 6 feet as you are at 60 feet if you’re indoors,” MIT engineering professor Martin Bazant told CNBC.

Navy Releases Video Of Iran’s IRGC Harassing US Coast Guard Patrols

The US Navy’s 5th Fleet has followed up yesterday’s revelation to The Wall Street Journal of a 3-hour swarming incident by Islamic Revolutionary Guard Corps (IRGC) boats of American ships in the Persian Gulf earlier this month by releasing partial video of the dangerous Iranian maneuvers to the public.

The incident happened on April 2 but had never been disclosed before Monday. The WSJ described “U.S. Navy officials confirmed that three fast attack crafts and one ship known as Harth 55, a 180-foot, twin-hulled support vessel, swarmed the two Coast Guard ships while they were patrolling international waters in the southern portion of the Persian Gulf.”

The above video shows a close-call moment wherein the Harth vessel comes within less than 100 yards, nearly colliding with the US Coast Guard ship.

“The larger vessel repeatedly crossed in front of the bows of the two U.S. vessels, the Monomoy and the Wrangell, coming as close as 70 yards away, officials said,” the WSJ noted further.

Here’s slightly fuller video of the incident…

“That forced the Wrangell to have to make defensive maneuvers to avoid collision, Navy officials said.”

It was considered by the Pentagon to be a major incident (unlike the more frequent, minor exchange of “warnings” between rival military vessels in the region) given the IRGC boats encircled and “buzzed” the US vessels for up to three hours.

The Harth 55 is perhaps the most distinctive somewhat recent addition to Iran’s Navy, considered a high-speed vessel capable of carrying a helicopter and up to 100 troops. As can be seen in the US Navy’s brief video clip, it is indeed highly maneuverable and quick given its large size.

The US Coast Guard is where now? On the other side of the planet from any US coast? And they’re being “harassed”, are they? Oh, by the Persians? Where are the Persians harassing them? Oh? In the Persian Gulf? The US Coast Guard is being harrassed in the Persian Gulf, by Persians?

Currently there’s speculation that the Pentagon never disclosed the incident when it happened in order not to negatively impact the Vienna nuclear talks. Likely the Iranian side kept mum on it for the same reason, while also thinking they can continue such actions without public condemnation out of Washington.