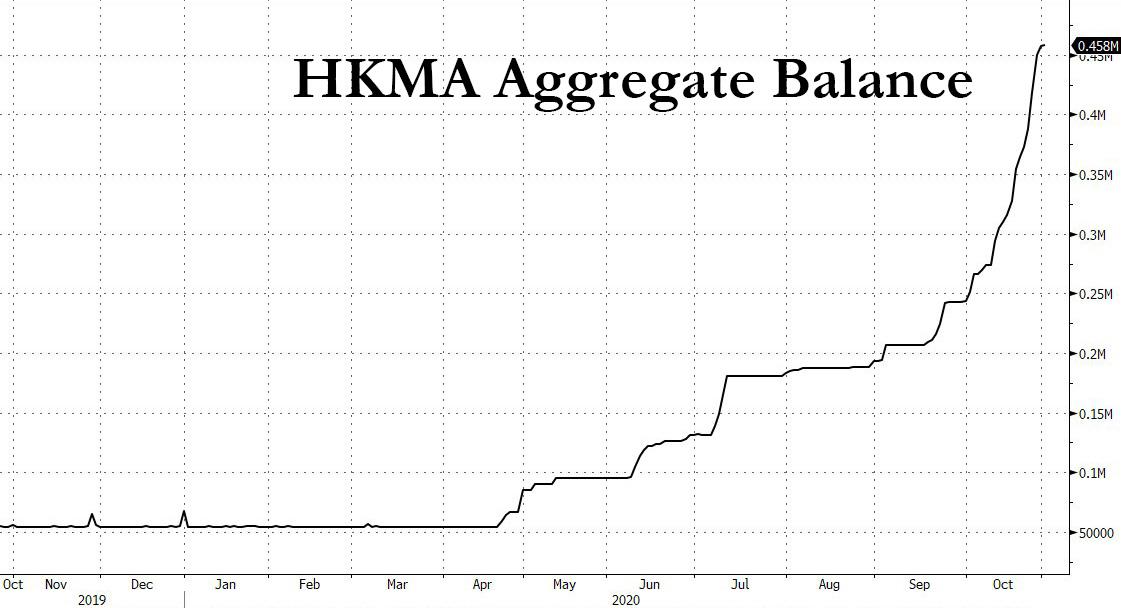

Peter Schiff: The Worst Pre-Election Stock Market Ever

Tyler Durden

Mon, 11/02/2020 – 11:15

The US stock market is coming off its worst week since March. It was also the worst pre-election stock market in history. In his latest podcast, Peter talked about the market, the election and what’s likely ahead.

![]()

A weak stock market right before election day doesn’t bode well for President Trump’s reelection, given that he’s touted the stock market as his great accomplishment. Peter has said he doesn’t think Trump will win and that the stock market would ultimately sell off on the reality of a Biden presidency – that it would be “buy the rumor, sell the fact.”

Well, apparently they’re not waiting for the fact and they’re selling on the rumors. They bought on the rumor Biden was going to win and now they’re selling on the rumor that he’s going to win, because a Biden victory is not good for the stock market. It means much higher taxes and that is not going to be offset by the Federal Reserve.”

Most people seem to think that regardless of who wins, even if we have a contested election and don’t know a winner for days or weeks, it really won’t be a problem for the markets because the Federal Reserve will step in and backstop it. Everybody seems confident that the Fed has their back.

The only leg that this market is standing on is the Federal Reserve and money printing. But ultimately, that’s not going to be enough. The market is not going to be able to survive when that is the only support.”

Tech stocks were hit particularly hard during last week’s sell-off. The NASDAQ had the biggest decline on Friday and is down over 11% from its September high. But even with the drop, many tech stocks still have sky-high valuations.

Typically, a big selloff in stocks means a strong bond market, but last week, the bond market was also relatively weak. Long-term interest rates were up. Normally, when you see people running to get out of stock, they move into bonds.

There was no refuge this week because even if you had a diversified portfolio, you were down on your stocks and you were down on your bonds. Yes, your bonds went down less than stocks, but everything went down and nothing went up.”

Peter said he thinks this will compound problems in the stock market. Typically, a surging bond market during a stock market selloff helps mitigate the pain. When bonds rise as stocks fall, the lower interest rates help stock valuations. Rising bond prices also offset stock losses for those with diversified portfolios. But if both stocks and bonds are falling at the same time, you have no gains to offset losses. You just have losses on top of your losses.

So, I think this is going to be particularly brutal, because not a lot of people have hedges that are outside of traditional US stocks and bonds. There’s not a lot of investors that have gold or gold stocks that are hedging their portfolio. I think eventually they will. As I’ve been saying for a while, I think gold is going to be the last safe haven standing and ultimately that’s where all the safe-haven money is going to flow.”

Gold also sold off this week. As we have reported, it looked an awful lot like early March with everything selling off. But gold wasn’t down significantly and it rallied a bit on Friday. Peter doesn’t think we’re going to see a significant drop in gold this time around, even if stocks really crash.

Given where the Fed is, given how much money has already been printed, given how much money is going to be printed, I just don’t think you’re going to see any kind of significant weakness in the price of gold. So, any weakness that you get is going to be a buy signal.”

Meanwhile, the Fed has already thrown out one lifeline, lowering the limit on its Main Street lending program to small businesses to $100,000. Peter asked a key question: why does the Fed even need to run such a program? Why can’t small businesses just get these loans from their banks? Answer: they aren’t credit-worthy.

They know they’re not going to get the money back because these companies are bad credit risks and so private lenders don’t want to make the loans. Now, why should the government do that? If these businesses can’t repay the loans, why is the government lending them any money? And it’s not really a loan. If you’re loaning money to businesses that can’t repay it, it’s not really a loan, it’s a grant, or it’s a gift. But you know it sounds a lot better if you can pretend it’s a loan. But this is all pure inflation. The Fed is just printing up money and handing it out to small businesses.”

Peter said he thinks this explains the number of small businesses being created in the midst of an economic collapse. They can take advantage of this giveaway and get money from the government.

Of course, none of this is constitutional. And it’s bad economics. Peter said the craziest thing is nobody even seems to care.

via ZeroHedge News https://ift.tt/35Y7Oug Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}