Watch Live: Nancy Pelosi Discusses 25th Amendment Plan Trump Denounced As A “Coup” Tyler Durden

Fri, 10/09/2020 – 10:10

As she promised last night, Nancy Pelosi, along with Democratic Rep. Jamie Raskin, are expected to hold a press briefing at 1015ET to discuss a new bill that would wrest power to invoke the 25th Amendment away from Trump and his cabinet, and place it in the hands of Congress and the speaker.

.@SpeakerPelosi: “Tomorrow, by the way, tomorrow, come here tomorrow. We’re going to be talking about the 25th Amendment.”

Pelosi first ominously suggested that more would be said about the 25th amendment “tomorrow” during her Thursday morning weekly press briefing with reporters on Capitol Hill. A few hours later, her office emailed reporters advising them about a 1015ET press briefing involving the Speaker and Raskin to unveil a new plan related to triggering the 25th amendment.

The House and Senate will hold “pro forma sessions” at 1000ET, which essentially means, since Congress is currently out of session whoever wants to can show up to hear Pelosi outline her “plan” to force President Trump to hand over power to Mike Pence, a move that would temporarily elevate her to Vice President. The briefing is supposed to start at 1015ET.

Rabobank pointed out in a note to clients published Friday morning that Pelosi’s 25th amendment push is doomed to fail. Even if it passes the House, it will die in the Senate. And even if, by some miracle, it managed to pass the Senate and be signed by the president, it would only succeed in placing Pence in the top job for a few days, before Trump could self-certify his own fitness to serve.

Exhibit B: Nancy Pelosi will today push a bill to give the House, not the Cabinet, power to remove a president from office for medical reasons under the 25th amendment. A few quick comments:

1) Is this needed by a party up 14-16 points in the polls and three weeks away from a sweep of the White House, House, and Senate?;

2) It will not remove Trump from office. Even if passed in the Democrat-majority House, the bill requires passage in the Republican-majority Senate and a presidential signature – which won’t happen;

3) If it did, it would just put Mike Pence into office for a few days, after which Trump could self-certify himself fit to take over again, and over-ruling that would require a two thirds majority in both the House and the Senate;

4) The move is likely to fire up the base – but possibly the Republicans more as Trump is selling it as an “attempted coup”

Earlier, White House Press Secretary Kayleigh McEnanay, who is still likely suffering from COVID-19, called in to Fox News to blast Pelosi’s latest rerun of impeachment as “an absurd proposition”.

WH’s McEnany on Fox on 25th Amdt/Pelosi: It’s an absurd proposition from Pelosi. The only one who needs to look at 25th Amendment is Pelosi herself..there’s no reason to consider it for the President but maybe for Pelosi

McConnell Says “We Do Need” Another Covid Aid Package, But “Unlikely In Next Three Weeks” Tyler Durden

Fri, 10/09/2020 – 10:03

With headline-scanning algos focused only on soundbites related any new stimulus deal and changes in the probability of a fiscal stimulus getting done soon, moments ago stocks were whiplashed when moments ago Senate majority leader Mitch McConnell said during an event in Kentucky that “we do need another Covid-19 aid package”, but then immediately poured cold water on “optimism” when he warned that a new stimulus deal is “unlikely in the next three weeks.”

New stimulus deal “unlikely in the next three weeks” McConnell saying in event in KY

McConnell also said that there’s “widespread agreement airlines need aid” and added that the economy is struggling to get back to normal.

The KY Senator then reiterated that he hasn’t seen Trump in person since August but they speak almost every day. “The telephone was invented in the late part of the 19th century and it works quite well.”

McConnell also refused to say when he was last tested for covid. “Have I ever been tested? Yeah. But am I going to make a daily report? No. It’s not necessary.”

Of all those, algos only cared about the first, and amid some initial confusion…

… sent the Russell 2000 – which had benefited in recent days amid surging “stimulus optimism” -lower…

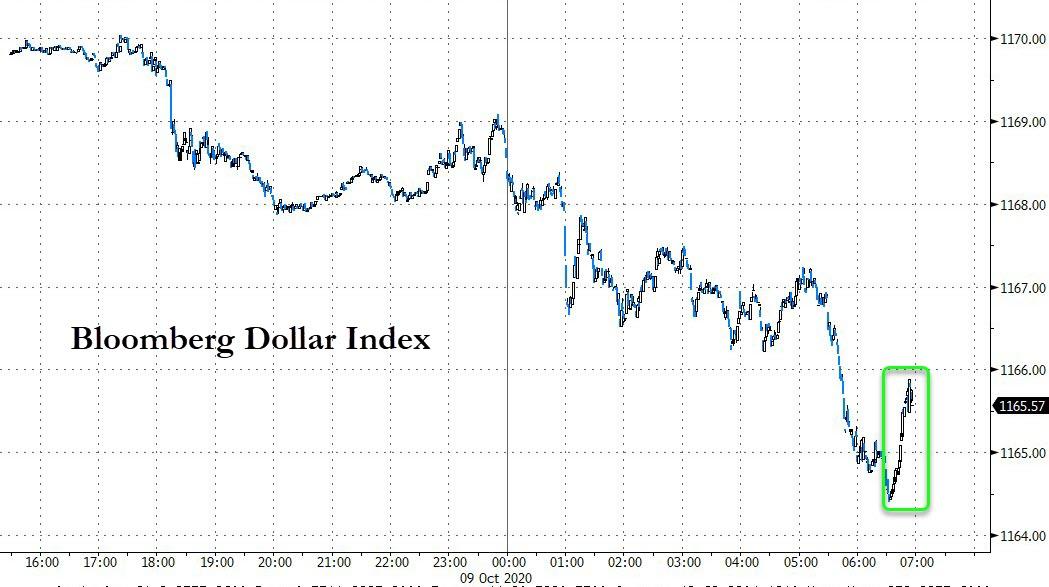

… while the dollar posted a modest bounce.

via ZeroHedge News https://ift.tt/30NGSLX Tyler Durden

Durham Report Won’t Be Ready By Election: AG Barr Tyler Durden

Fri, 10/09/2020 – 09:50

Attorney General Bill Bar has begun telling Republican leaders that the DOJ’s sweeping review into the ‘Russiagate’ investigation won’t produce results before the election, according to Axios.

Recall last month that Democrats were frothing at the mouth over the investigation, conducted by US Attorney John Durham – with the Democratic chairs of four House committees demanding an “emergency investigation” into the probe out of fear of an “October surprise.”

US Attorney John Durham

Now, it looks like that was much ado about nothing – as Barr “has made clear that they should not expect any further indictments or a comprehensive report before Nov. 3,” according to the report.

“This is the nightmare scenario. Essentially, the year and a half of arguably the number one issue for the Republican base is virtually meaningless if this doesn’t happen before the election,” a GOP aide told Axios.

And as Politico notes, “Senate Republicans running similar investigations were told of the intention within the last week — and it’s why they’ve been stepping up their releases of declassified documents.”

“BUT TRUMP AND HIS ALLIES were pushing for much more than that; they wanted DOJ to indict their Obama-era foes as they seek to rewrite the Russia investigation and turn it against Democrats. The president channeled his grievances by retweeting supporters demanding that Barr immediately arrest and jail Trump’s political enemies like Barack Obama, Joe Biden and Hillary Clinton. Late Wednesday afternoon, Director of National Intelligence John Ratcliffe said his office ‘has now provided almost 1,000 pages of materials to the Department of Justice in response to Mr. Durham’s document requests.’” –Politico

In recent weeks, we’ve learned that US intelligence officials forwarded an investigative referral to former FBI officials James Comey and Peter Strzok concerning allegations that Hillary Clinton approved a plan to smear then-candidate Donald Trump by tying him to Russian President Vladimir Putin and Russian hackers, according to information given to Sen. Lindsey Graham by the Director of National Intelligence.

Notably, former CIA Director John Brennan briefed then-president Obama on Hillary’s alleged approval.

BREAKING: According to handwritten notes, Brennan briefed Obama on Hillary’s approval of a proposal to attack Trump in the 2016 election by tying him to Putin pic.twitter.com/lnwTFwjoAf

As part of his investigation, Durham has interviewed Brennan and others, allegedly regarding the CIA’s assessment that Russian President Vladimir Putin was behind interference in the 2016 US election in order to help President Trump.

In an August 13th interview, Barr said he expects “significant” developments to come out of the investigation before the election. Days later, former FBI lawyer Kevin Clinesmith pleaded guilty to fabricating evidence used to obtain surveillance warrants on former Trump adviser Carter Page. Clinesmith -who worked on both the Hillary Clinton email investigation and the Russia probe, was part of Special Counsel Robert Mueller’s team, and interviewed Trump campaign advisor George Papadopoulos.

We can’t help but wonder if Durham’s report will look the same if Biden wins in November.

via ZeroHedge News https://ift.tt/2GM3cOS Tyler Durden

Earlier in the week I warned of a lot more US election wackiness to come.

Well, Exhibit A: The debate commission decided the upcoming presidential debate on 15 October will be virtual rather than in person, logical given President Trump has Covid-19; and Trump refused to attend a virtual debate….perhaps understandable given the experiences many of us have had recently: “I can’t use Teams, do you have Skype? No? Can I use Zoom? It’s banned? Oh.” And can you imagine a debate which was all “Hello? Hello? Can you hear me?“ Not that live debates are seeing any answers to the key questions though. Even the Vice Presidential debate was actually akin to the 1970’s Two Ronnies’ Mastermind sketch:

Q: Your chosen subject last time was answering questions before you are asked. This time, you`ve chosen to answer the question before last, each time, is that correct?

A: Charlie Smithers.

Q: And your time starts now. What is palaeontology?

A: Yes, absolutely correct.

Q: What is the name of the directory that lists members of the British peerage?

A: A study of old fossils.

Q: Correct. Who are Len Murray and Sir Geoffrey Howe?

A: Burkes.

Q: Correct. What is the difference between a donkey and an ass?

A: One is a Trade Union leader, the other one is a member of the cabinet.

Q: Correct. Complete the quotation “To be or not to be…”

A: They are both the same.

Q: Correct. What is Bernard Manning famous for?

A: That is the question.

Q: Correct. Who is the current Archbishop of Canterbury?

A: He is a fat man who tells blue jokes.

Trump has now been given a clean medical bill of health to start public events again from Saturday, and is holding a rally…so is the rescheduled debate date of 22 October still virtual? Joe Biden is doing an ABC Town Hall on 15 October now; will Trump do one too? Might it be with Joe Rogan, as Twitter is urging? Confusion reigns. Clear and substantive debate does not.

Exhibit B: Nancy Pelosi will today push a bill to give the House, not the Cabinet, power to remove a president from office for medical reasons under the 25th amendment. A few quick comments:

1) Is this needed by a party up 14-16 points in the polls and three weeks away from a sweep of the White House, House, and Senate?;

2) It will not remove Trump from office. Even if passed in the Democrat-majority House, the bill requires passage in the Republican-majority Senate and a presidential signature – which won’t happen;

3) If it did, it would just put Mike Pence into office for a few days, after which Trump could self-certify himself fit to take over again, and over-ruling that would require a two thirds majority in both the House and the Senate;

4) The move is likely to fire up the base – but possibly the Republicans more as Trump is selling it as an “attempted coup”; and

5) That should be relative risk off for markets, if they can read the political tea leaves – but I am not sure they cocoa, as said in the UK in the era of the Two Ronnies.

Exhibit C: The shocking news of the arrest of anarchist/”extremist libertarians” who had planned to kidnap Michigan governor Whitmer and hold a “treason trial” over her virus-related restrictions. This should underline just how worrying downside scenarios are in this present crisis.

Exhibit D: We are apparently closer to a comprehensive fiscal stimulus after all(?), after the Democrats had rejected offers for a series of clean bills for airlines and households. Perhaps Mnuchin and Pelosi can find a window today to continue their push-me-pull-you as the Fed sits in the background with its head in its hands. Rosengren yesterday called this all “tragic”, and for once it’s hard to disagree with the Fed. “The Fed can ease financial conditions. We can’t replace lose income, though. That’s uniquely suited to fiscal policy.”

On which (lost income), more pubs are closing in the UK, as people old enough to remember the Two Ronnies sadly start to fill the hospitals again. The UK looks set to go back to shielding the vulnerable indoors again for months. Spain is also following suite with a 15-day emergency lockdown in Madrid, while a Spanish virologist warns of up to two years of mask-wearing ahead.

Meanwhile, also very important at the margin is that last night the US imposed sweeping sanctions on another 18 Iranian banks, which now effectively cuts Iran off from the global financial system completely. The US may be a house divided at home, but abroad it is still capable of major action: critics say this US masterplan will backfire, but the campaign of maximum pressure continues. Markets must not forget that there are other countries potentially heading for similar treatment for a variety of different reasons – some of their currencies are recognising it, while one is merrily going on its way as if that kind of thing can’t happen to it. Quite the Masterminds at work there answering the previous question of financial inflows rather than the current one of (more) potential sanctions.

Of course, whether you are long or short MXN or RUB, as just two examples, is now very dependent on what you think is going to happen on 3 November; which is why you have to keep looking at the election campaign in all its shambolic glory.

via ZeroHedge News https://ift.tt/34EJqgD Tyler Durden

Microsoft Allows Employees To “Permanently” Work From Home Tyler Durden

Fri, 10/09/2020 – 09:12

One of the most significant changes forced by the virus pandemic has been companies allowing their employees to work from home. A couple of months after Microsoft unveiled its plans to reopen US offices in January 2021, the software maker is now letting some employees work from home on a “permanent” basis, according to The Verge.

Microsoft’s new internal guidance on remote working, viewed by The Verge, outlines the workplace of the future, or rather the “hybrid workplace,” that allows “employees to work from home freely for less than 50 percent of their working week, or for managers to approve permanent remote work.”

The Verge noted some employees “will be able to easily take advantage of the less than 50 percent working from home option,” though certain roles within the company might find remote working challenging, or near impossible to transition to remote permanently.

Microsoft said specific roles within the company would require those to return to the company’s offices. Those who work in hardware labs, data centers, along with in-person training, will still need access to buildings.

Under the “hybrid workplace,” employees will be allowed to relocate domestically with approval from management. There are options for certain employees, that could allow them to work remote in foreign countries.

“While Microsoft employees will be allowed to move across country for remote work, compensation and benefits will change and vary depending on the company’s own geopay scale. Microsoft will be covering home office expenses for permanent remote workers, but any that decide to move away from Microsoft’s offices will need to cover their own relocation costs. Flexible working hours will also be available without manager approval, and employees can also request part-time work hours through their managers,” The Verge said.

Earlier this week, Microsoft CEO Satya Nadella said online meetings could make employees tired and make it difficult to focus.

“When you are working from home, it sometimes feels like you are sleeping at work,” Nadella said.

Microsoft unveiled a new product that attempts to address this problem, called Together Mode, where participants are on video calls in a virtual space.

Of course, with Microsoft becoming the latest big tech company to throw support behind a future of “flexible” work, the tech industry is positioning itself to use this as another ‘perk’ to attract the ‘top talent’ from America’s colleges – while JP Morgan pushes Wall Street to call employees back to the office – regardless of the risks – for fear of diminishing “creative intelligence.”

via ZeroHedge News https://ift.tt/34EXGpp Tyler Durden

“The problem is once you accept the false premise that government stimulus actually helps the economy – that it really is a stimulus – then you’ve kind of lost the argument. Because if borrowing and printing $1.6 trillion, if that’s a good thing, why isn’t borrowing and printing $2.4 trillion a better thing? Because you put the Republicans in the position of arguing that 2.4 trillion is too much of a good thing — that somehow, if we just create 1.6 trillion out of thin air and spend it, that’s really going to help. But if we push it to 2.4, it’s actually going to hurt. Why? I mean, when does something good suddenly become something bad? “

Is this the start of a herd-panic at the prospect of $7 trillion in Biden/Harris/AOC stimulus/MMT?

via ZeroHedge News https://ift.tt/2SCG0VU Tyler Durden

A California-based media outlet late Thursday posted a story falsely reporting that Vice President Mike Pence tested positive for COVID-19, sparking conspiracy theories among the left.

Deadline Hollywood claimed that Pence tested positive for the new disease. The headline stated, “PREP. DO NOT PUBLISH UNTIL THE NEWS CROSSES.”

“The two most powerful men in America now have coronavirus,” the story began. It then said Pence announced on Wednesday that he had tested positive.

Katie Miller, Pence’s director of communications, criticized the story, calling it“IRRESPONSIBLE & UTTERLY FALSE.”

Deadline later removed the story.

“A draft post of a story about Vice President Mike Pence testing positive for coronavirus that was never meant to publish was accidently posted on Deadline. It was pulled down immediately. It never should have been posted and Deadline will take steps to see this kind of thing never happens again. Apologies to the Vice President and our readers. We regret the error,” the outlet said in a correction notice.

The story sparked conspiracy theories among the anti-President Donald Trump crowd, who said the story, though removed, must mean something was going on.

“Never meant to be published but the actual article has quite a lot of detail. it’s not just some blank webpage. What are you guys hiding,” one wrote on Twitter.

“The fact that specific details were included and that chances were pretty slim that Mike got covid makes me wonder,” another said.

Deadline was started in March 2006. It is described on its website as “the authoritative source for breaking news in the entertainment industry.”

The outlet is still running a story about “Daily Show” host Trevor Noah claiming there was a real chance Pence contracted COVID-19.

Trump tested positive for COVID-19, the disease caused by the CCP (Chinese Communist Party) virus, last week. He received treatment at Walter Reed National Military Medical Center but returned to the White House on Monday. His doctor said earlier Thursday that Trump is able to resume public engagements this weekend.

President Donald Trump looks over at reporters and photographers as he departs Walter Reed National Military Medical Center in Bethesda, Md., on Oct. 5, 2020. (Jonathan Ernst/Reuters)

Speculation about Pence’s condition stemmed from the cancellation of a planned appearance in Indianapolis.

Marty Obst, senior political adviser for Pence, told WISH-TV that the schedule change “was merely a scheduling issue and definitely not health-related.”

Pence tested negative for COVID-19 on Thursday morning, Devin O’Malley, his spokesman, said. Pence has tested negative each day for months.

Both Pence and Trump are tested every day, according to White House officials.

via ZeroHedge News https://ift.tt/2IdecFL Tyler Durden

London Mayor Says Another Lockdown “Inevitbale” As Global COVID-19 Cases Near Record Daily Highs: Live Updates Tyler Durden

Fri, 10/09/2020 – 08:37

Summary:

London mayor says lockdown “inevitable”

Netherland reports latest record jump

Spain declares “public health emergency” in Madrid

France places more cities on lockdown

Confirmed COVID-19 cases neared daily record yesterday

Russia reports new record

Takeda enrolls first patients for new drug trial

China joins WHO vaccine initiative

Iran bars hospitals from taking non-urgent cases as COVID hammers country

* * *

France reported more than 18,000 new cases yesterday, and now its third-largest city, Lyon, is joining Paris and Marseille in closing bars and other non-essential businesses in the coming days as COVID-19 infection rates surge in the countries hot spots. As the French government continues to insist that national lockdowns will only be a measure of last resort, public health officials are doubling down on the targeted approach as COVID-19 patients fill the country’s hospital beds.

Yesterday, French Health Minister Olivier Veran said Lyon, Lille, Grenoble and Saint-Etienne would go on maximum coronavirus alert level from Saturday. This means they will have to close their bars for two weeks in coming days, as Paris did on Tuesday and Marseille, France’s second-biggest city, did earlier this month.

And more localized measures could be implemented in Toulouse and Montpellier; those cities could see their alert level raised to the maximum s of Monday. Dijon and Clermont-Ferrand would also see their alert levels rise on Saturday. “Unfortunately, the health situation in France continues to deteriorate,” Veran said at his weekly COVID-19 briefing, per Reuters.

Minutes ago, London Mayor Sadiq Kahn told the LBC that new London lockdown restrictions are “inevitable” as officials have tightened restrictions in and around Manchester in the north of England. Meanwhile, Spain declared a public health emergency in Madrid, as expected.

Additionally, the Netherlands just reported another 5,983 new cases, a new daily record, while 69 new patients were reported in the country’s hospitals, bringing that total to 1,139, while deaths climbed by 14 and ICU cases climbed by 11 to 239.

As of earlier this morning, global cases had reached 36,435,290, according to Johns Hopkins data, while the global death toll had climbed to 1,060,869. New cases were just shy of the record set on Sept. 24, with 359,337 new cases confirmed yesterday, along with 6,234 deaths. The surge in new cases is being driven by Europe, Russia, the US, India, Brazil and Southeast Asia. The Czech Republic, which, along with Poland, yesterday announced new restrictions to try and slow the raging outbreak. The Czech Republic reported 5,394 new infections on Friday, its highest daily total yet. The country has now recorded 15% of its entire COVID-19 outbreak tally in the past 3 days. Poland, meanwhile, just reported 4,739 new cases Friday, the third-straight record day.

Russia shot passed its peak from May on Friday as it recorded another 12,126 new infections and 201 virus-linked deaths in the 24-hour period leading up to Friday.

In a lengthy report published in Friday’s FT, the paper examines how a resurgence in the Brazilian city of Manaus, which was hit hard in the spring, only for the virus to slink away over the summer, is raising serious questions about the prospects for herd immunity. The trend “poses fresh challenges…and difficult questions for the scientists and policymakers worldwide who have been edging towards herd immunity policies as an alternative to economy-crushing lockdowns.

This comes after a group of scientists in the US and UK published the Great Barrington Declaration earlier this week. The document calls for public policymakers to examine a strategy of “focused protection” to try and build up herd immunity as safely as possible. The virus, they argued, should be allowed to circulate among the young and healthy, while the elderly and the sick should be shielded. In Western Europe, antibody surveys have determined that roughly 8% of the population has already been infected, and the WHO recently declared that it believes 11% of the global population has already had the virus.

However, it seems, many of the same ‘hot spots’ from the spring are suffering again in the fall. This could also be a factor of population density, however.

As Eli Lilly and Regeneron apply for EUAs from the FDA for their antibody therapeutics, CNBC had Gilead CEO Dan O’Day on Friday morning to talk about the latest remdesivir trial results.

Gilead CEO Daniel O’Day shares 3 key findings from Remdesivir study results with @megtirrell:

-Helped people recover faster

-Prevented people from getting sicker

-Reduced number of people who died by 70% in the largest subgroup of patients — those receiving oxygen pic.twitter.com/vhY39TBGVa

At any rate, here’s some more COVID-19 news from Friday morning, as well as overnight.

Iran’s health ministry has prevented all hospitals from admitting non-urgent cases after the military also designated all its hospitals for coronavirus patients in response to a new surge in infections (Source: FT).

Japan’s Takeda Pharmaceutical says an alliance of drugmakers it spearheads has enrolled its first patient in a global clinical trial of a blood plasma treatment for COVID-19 after months of regulatory delays. The Phase 3 trial by the group, known as the CoVIg Plasma Alliance, aims to enroll 500 adult patients from the United States, Mexico and 16 other countries. Patients will be treated with Gilead Sciences’ remdesivir alongside the plasma treatment, which will be provided by CSL Behring, Takeda and two other companies (Source: Nikkei).

China will join a World Health Organization initiative aimed at ensuring fair distribution of Covid-19 vaccines when they become available, the country’s foreign ministry announced on Friday (Source: FT).

India reports 70,496 cases of COVID-19 in the last 24 hours, down from 78,524 the previous day, bringing the country’s total to over 6.9 million. The death toll jumped by 964 to 106,490 (Source: Nikkei).

Australian states and territories report 16 cases in the past 24 hours, down from 28 a day earlier. They also report no deaths for two days — the first time Australia has gone 48 hours without a COVID-19 death since July 11 (Source: Nikkei)

via ZeroHedge News https://ift.tt/33H4Quc Tyler Durden

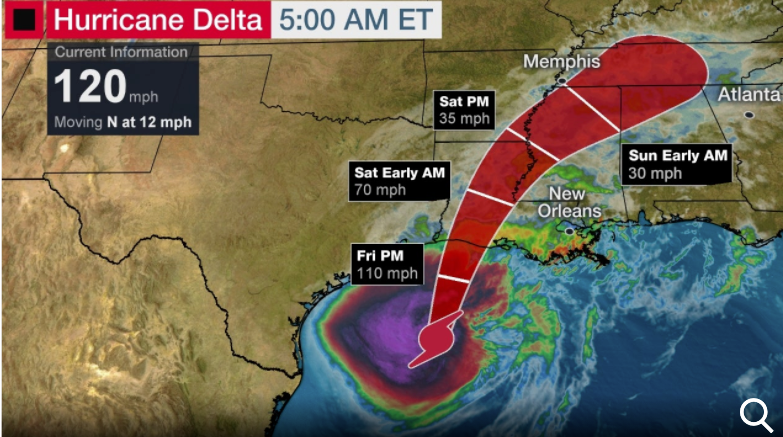

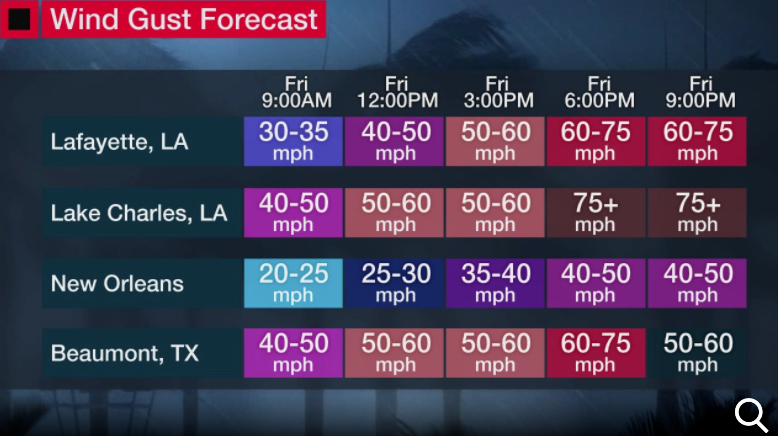

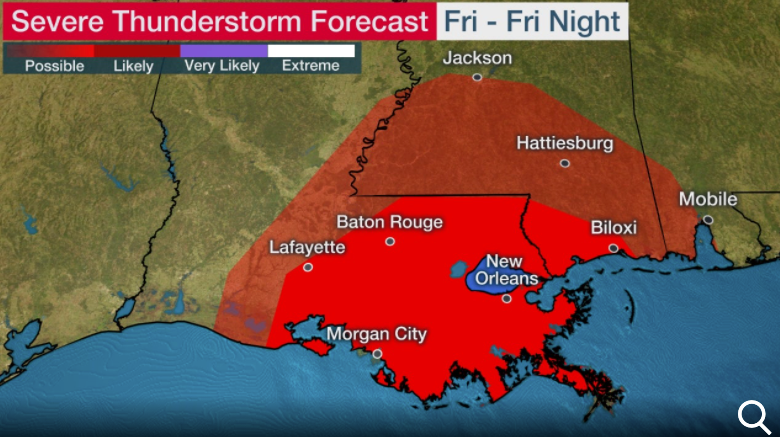

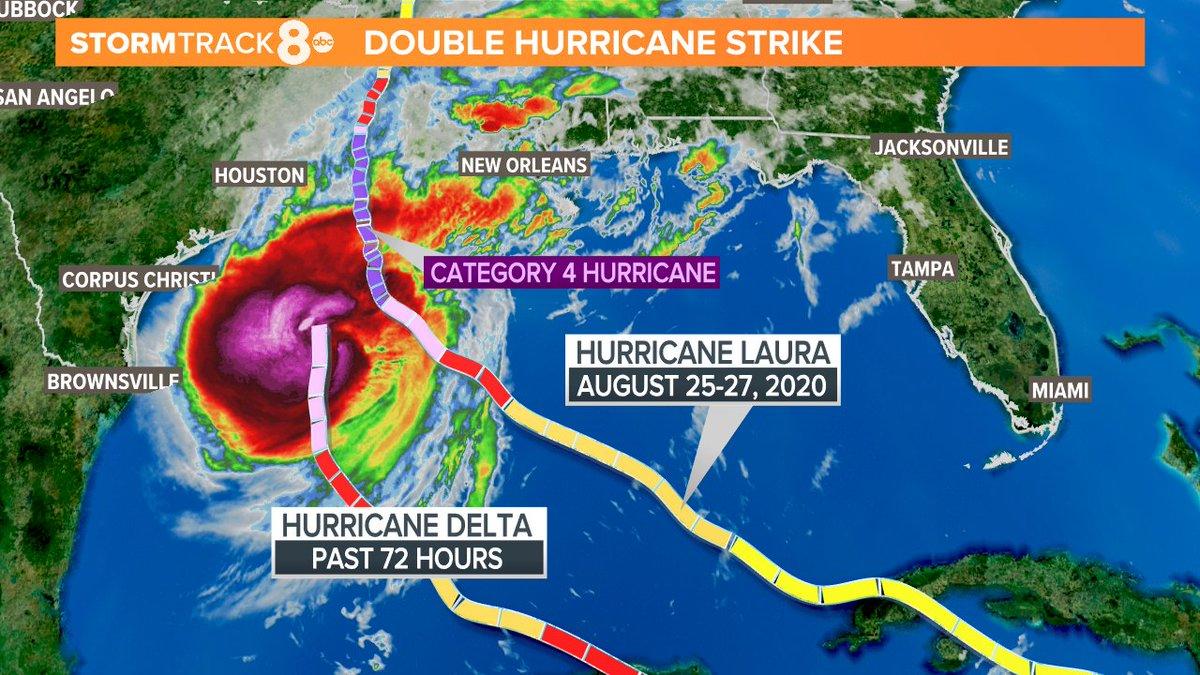

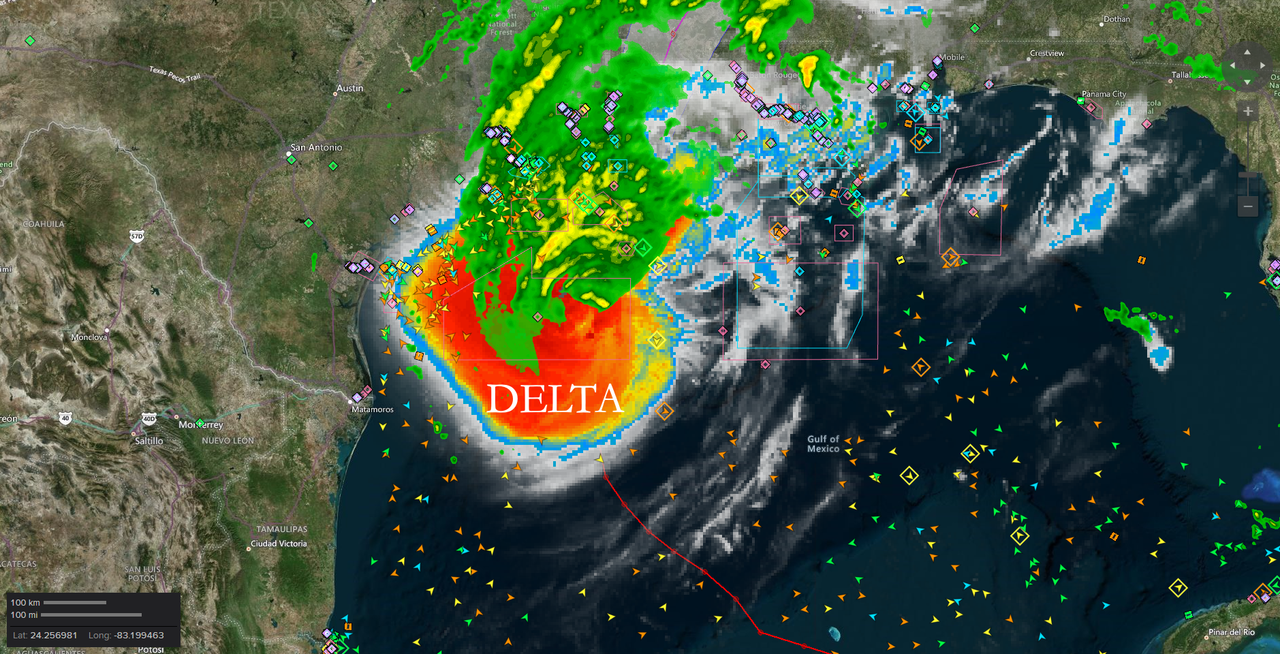

According to the latest National Hurricane Center’s tropical advisory update, Hurricane Delta is a Category 3 storm, expected to bring life-threatening storm surge, damaging winds, and rainfall flooding to Louisiana and east Texas to Mississippi on Friday evening.

As of 0500 ET, Delta is 200 miles south of Cameron, Louisiana, with maximum sustained winds around 120 mph, making it a major hurricane, and is expected to strike the same area ravaged by Hurricane Laura in late August.

Hurricane Delta Update

On Wednesday, Delta made landfall on the Yucatan Peninsula. By Thursday, the storm quickly intensified over warmer Gulf of Mexico water as its strength on Friday morning appears to be leveling off with 120 mph winds.

The Weather Channel said hurricane warnings had been posted from High Island, Texas, to Morgan City, Louisiana, including Lake Charles and Lafayette, Louisiana; and Port Arthur, Texas.

Watches And Warnings

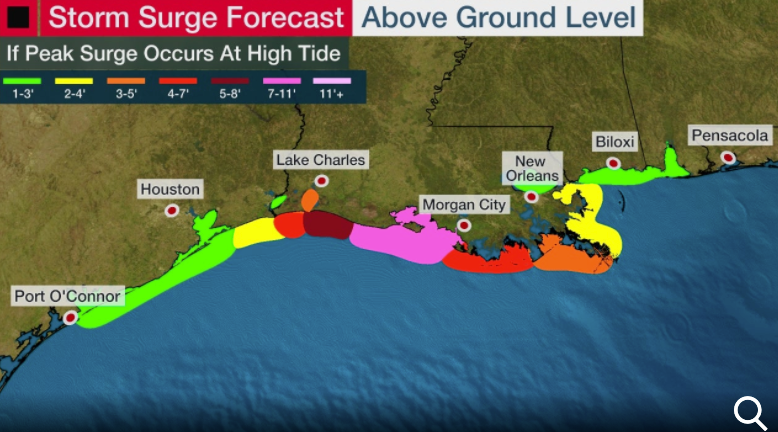

A storm surge warning has also been issued from High Island, Texas, to the Pearl River, Louisiana, including Calcasieu Lake, Vermilion Bay, and Lake Borgne.

Storm Surge Forecast Above Ground Level

Hurricane Delta, the 25th named storm of the super active 2020 Atlantic hurricane season, is expected to make landfall this evening around the Cameron, Louisiana.

Up to 15 inches of rain could be dumped across the southwest into south-central Louisiana through Sunday.

Rainfall Potential Through Sunday

Wind Gust Forecast Throughout Friday

Power Outage Potential

Severe Thunderstorm Forecast

On Thursday night, Louisiana Gov. John Bel Edwards said Delta was set to make landfall near areas already affected by Laura in late August.

“And we believe that there will be hurricane-force winds and storm surge in southwest Louisiana, in the area of our state that is least prepared to take it,” Edwards said at a press conference.

As for the oil and gas assets that sit offshore, Reuters reports Delta could be one of the “greatest blow to U.S. offshore Gulf of Mexico production in 15 years, halting most of the region’s oil and nearly two-thirds of its natural gas output.”

“Delta has shut 1.67 million barrels per day, or 92% of the Gulf’s oil output, the most since 2005 when Hurricane Katrina destroyed more than 100 offshore platforms and hobbled output for months,” Reuters said.

Offshore Gulf Of Mexico Production Assets

Residents are fleeing Lake Charles, again, as Delta approaches.

In addition to Hurricane #Delta , we are tracking a tropical wave located several hundred miles SW of the Cape Verde Islands expected to move West or WNW with a low potential of cyclone development over the next 5 days. Hurricane Season isn’t over until end of November! @CBSMiamipic.twitter.com/48Mc5AQWSx

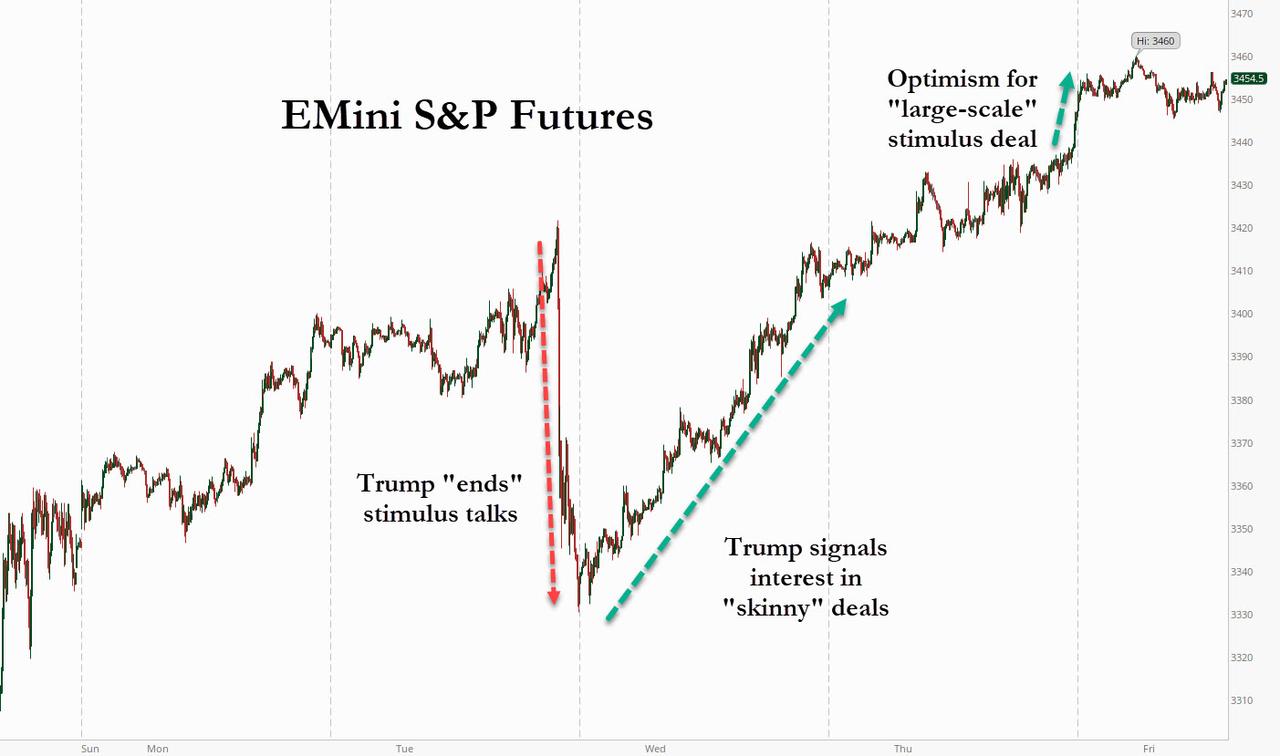

Futures Jump On “Large-Scale” Deal Optimism Tyler Durden

Fri, 10/09/2020 – 08:11

Just two days after a Trump tweet “crushed” hopes for any more fiscal stimulus talks, optimism for not just a stimulus deal but for a “large-scale” deal is back front and center, after the White House reversed again late on Thursday after media reports that Trump was concerned by the market reaction to him walking away from stimulus discussions, and signaled that the administration is again leaning toward a large-scale stimulus bill after House Speaker Nancy Pelosi pushed back on the idea of individual measures for parts of the economy hit by the Covid-19 crisis. According to a Pelosi spokesman, Mnuchin told Pelosi in a 40-minute call that President Donald Trump wants agreement on a comprehensive stimulus package, which was enough to send futures blasting higher, and hitting 3460 overnight, a level last seen on Sept 4 just after the market slumped from its all-time highs. The MSCI world equity index was up 0.1% at a more than one month high; yields and the dollar dropped, while the Chinese yuan and gold surged.

However, opposition remains among Senate republicans for a large deal with some saying that enough stimulus has already been injected, and so time is very tight for any legislation to reach the president’s desk before the end of October. As Politico notes, to “get a deal, the White House needs to empower MNUCHIN to get something done — something they haven’t done yet; TRUMP needs to expend serious political capital to get a big vote in House as a signal to the Senate that it has cover voting yes.”

WAKE UP WHITE HOUSE! IT’S GO TIME!: To get a deal, the White House needs to empower MNUCHIN to get something done — something they haven’t done yet; TRUMP needs to expend serious political capital to get a big vote in House as a signal to the Senate that it has cover voting yes.

Meanwhile as Bloomberg notes, another obstacle to a successful outcome remains as both Trump and Pelosi are publicly questioning each other’s mental stability.

Democrats are set to announce a bill today that would set up a commission to evaluate using the 25th amendment which can remove a sitting president from office.

With recent trading on Wall Street – particularly in shares of U.S. airlines, which began mass furloughs after a previous payroll support package expired – dictated by negotiations between the White House and Democrats on more fiscal aid, the S&P airlines subindex jumped in the past two sessions and is on track for one of its best months this year after sinking 3% on Tuesday as Trump broke off aid talks. In company news, Xilinxsurged more than 17% after the WSJ reported that AMD was in talks to buy the chipmaker in a deal that could be valued at more than $30 billion. Shares of AMD fell 5.8%. Also overnight Citadel announced it would acquire IMC’s designated market-making unit, firming up its position as the largest floor broker on the NYSE.

Gains in U.S. stocks this week have been concentrated in small- and mid-cap firms, which stand to benefit more from a Biden victory than the large-cap companies that had so far fueled Wall Street’s recovery from the coronavirus lows hit in March, fund managers said. In a sign markets are pricing in a Biden victory, clean energy-related shares have outperformed in recent weeks. The iShares Global Clean Energy ETF has gained 14% so far this month, compared with 4% gains in the S&P 500 energy index. The November VIX contract dropped to 30.25, its lowest level in three weeks, another sign of reduced worries about a contested election.

“Biden seems to have a clear lead following the TV debate and a coronavirus cluster in the White House, which has raised questions about Trump’s crisis management capabilities,” said Mutsumi Kagawa, chief global strategist at Rakuten Securities.

Optimism also prevailed in Europe, where equities rose on Friday, and were set for a second consecutive weekly gain as investors were encouraged by stimulus prospects in the U.S. and positive guidance updates. The Stoxx Europe 600 index was up 0.3% at 730 a.m. ET led by miners and energy shares, while autos underperformed. European stocks also gained as a host of companies raised outlooks, from Denmark’s drugmaker Novo Nordisk to German online clothing retailer Zalando. Stocks fell in Spain, where the government declared a state of emergency for Madrid to control Covid-19. Italy’s 10-year bond yield fell a record low.

“The lower level of uncertainty with regards to the U.S. election combined with the prospect of additional stimulus measures is probably behind the latest positive inflection in equity markets,” says Sylvain Goyon, strategist at Oddo BHF. That’s because Democratic contender Joe Biden’s “increasing lead in the polls gives credence either to a ‘blue wave’ scenario and more stimulus, or more political pressure for President Trump to offer something prior to the vote.”

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.3%, inching closer to its Aug. 31 peak, which was its highest level since March 2018. China’s CSI300 index gained 2% after the Golden Week holidays. The Shanghai Composite Index rose 1.7%, with Ningbo Ronbay New Energy and Shandong Jinjing posting the biggest advances. In Japan, the Nikkei dipped 0.1% after reaching a seven-and-a-half-month high; while the Topix declined 0.5%, with Danto and Creek & River falling the most.

In FX, the dollar weakened, heading for its second weekly loss, as the White House signaled it was open to large-scale U.S. stimulus, while the Chinese yuan was the biggest beneficiary of the rising hopes of a Biden win, posting its biggest daily rise in more than four years after the holidays. The greenback declined against most Group-of-10 peers and hits lowest level since Sept. 21, as measured by the Bloomberg Dollar Spot Index which fell 0.3% Friday, set for its third straight day of declines; it came under pressure during Asia hours as emerging-market currencies advanced with the yuan better bid following an eight-day holiday in China. NZ’s kiwi led gains as the Swiss franc follows suit. The euro rose 0.1% to $1.1776.

Another notable mover was China’s yuan which rose sharply in onshore trading, catching up with gains seen in offshore trading the past week, as mainland markets reopened after the Golden Week holiday. The yuan climbed as much as 1.4% on Friday while in offshore markets the currency strengthened 0.6%, with both reaching their strongest since April 2019.

The People’s Bank of China put the daily fixing at a stronger-than-expected level. Amid the risk-on mood, the 10-year yield on Chinese sovereign debt reached its highest level since December. Friday’s currency and equity gains “have staying power. Chinese markets will still be supported next week,” said Moh Siong Sim, foreign exchange strategist from Bank of Singapore. He added both asset classes will also be supported by recovering Chinese consumer spending while Joe Biden’s widened poll lead in the U.S. “is also good for Chinese assets as his policy would be less confrontational” than President Donald Trump’s.

In another sign that investors look for a Brexit trade deal to be reached in the end, leveraged funds stepped in to fade a sharp drop in cable following a report that there has been insufficient progress in the talks, a Europe-based trader says. GBP/USD rose earlier 0.3% to 1.2973 high amid broad greenback weakness, only to erase the advance and stabilize around 1.2940.

In rates, Treasuries inched higher after advancing during Asia session and European morning. Treasury yields lower by 0.5bp to 2.2bp across the curve, flattening 2s10s, 5s30s by 1.8bp and 0.9bp; 10-year yields around 0.764%, slightly outperforming bunds while lagging behind gilts. Yields remain higher on week in which prospects for a stimulus agreement helped drive steep gains for stocks on Monday and Wednesday; The 10-year is up by more than 6bp, with 50-DMA on cusp of crossing above 100-DMA. Gilts outperformed following weak August U.K. GDP while in Asia session gains for Aussie bonds supported Treasuries. The 10-year German bond yield was unchanged at -0.525%. Other core yields were a touch lower.

“The rise in U.S. yields, particularly at the long end, suggests increased expectations of a blue wave in the election,” said Koichi Fujishiro, economist at Dai-ichi Life Research Institute.

In commodities, oil prices edged up, propelled by supply outages caused by a storm in the Gulf of Mexico and a strike of offshore workers in Norway. Both benchmark contracts were on course for their biggest weekly gains since early June. Brent was up 16 cents at $43.50 a barrel. WTI crude rose 14 cents to $41.33. A weaker dollar boosted gold which gained 1.1% to $1,914.28 per ounce.

Starting next week, attention turns to corporate America’s third-quarter earnings season, kicked off by JPMorgan Chase & Co, Citigroup Inc and drugmaker Johnson and Johnson. Looking at the day ahead, we get final August reading for wholesale inventories in the US. From central banks, the Reserve Bank of India will be deciding on monetary policy, while the Fed’s Barkin and the BoE’s Haldane will also be speaking.

Market Snapshot

S&P 500 futures up 0.4% to 3,450.25

STOXX Europe 600 up 0.2% to 369.09

MXAP up 0.05% to 175.13

MXAPJ up 0.3% to 579.54

Nikkei down 0.1% to 23,619.69

Topix down 0.5% to 1,647.38

Hang Seng Index down 0.3% to 24,119.13

Shanghai Composite up 1.7% to 3,272.08

Sensex up 0.5% to 40,387.55

Australia S&P/ASX 200 unchanged at 6,102.17

Kospi up 0.2% to 2,391.96

Brent futures down 0.4% to $43.19/bbl

Gold spot up 1.1% to $1,915.04

U.S. Dollar Index down 0.2% to 93.38

German 10Y yield fell 1.8 bps to -0.541%

Euro up 0.3% to $1.1792

Italian 10Y yield fell 2.7 bps to 0.555%

Spanish 10Y yield fell 2.7 bps to 0.174%

Top Overnight News from Bloomberg

While the lesson of the 2016 campaign was never to count out Donald Trump, his path to re-election is narrowing dramatically as Democrat Joe Biden’s lead continues to grow and voters sour on the president’s handling of the coronavirus pandemic

President Trump’s Dr. Sean Conley said in a statement that “since returning home, his physical exam has remained stable and devoid of any indications to suggest progression of illness; said he expects Trump to safely return to public engagements by Saturday, 10 days after his diagnosis

Pound traders who have grown used to Brexit brinkmanship between London and Brussels are making two assumptions: there’ll probably be a trade deal, and U.S. elections matter more right now

In 2016 investors were buying the Russian ruble and selling the Mexican peso in expectation the Republican candidate would mend relations with Russian President Vladimir Putin and cut trade ties with Mexico after winning the election. This time around, the trade has reversed as Joe Biden gains in the polls

Spanish Prime Minister Pedro Sanchez has called an extraordinary cabinet meeting on Friday to discuss a possible state of emergency for the region of Madrid, while German Chancellor Angela Merkel will speak with mayors of the country’s biggest cities about efforts to contain a recent surge in Europe’s largest economy

A quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mixed as US equity futures extended on the prior day’s gains amid stimulus hopes after House Speaker Pelosi and US Treasury Secretary Mnuchin continued their relief discussions, while President Trump also suggested optimism that talks are beginning to work and was said to be open to something larger than a skinny bill. Nonetheless, ASX 200 (U/C) was rangebound and took a breather following the outperformance seen for most the week and after the RBA Financial Stability Review noted that domestic banks were well placed to continue lending and supporting the economic recovery, as well as the financial system but added that business failures will increase substantially as loan repayment deferrals and income support end. Nikkei 225 (-0.1%) initially began on the front-foot but then stalled in tandem with a mild pullback in USD/JPY which gave up the 106.00 status and after weaker than expected Household Spending. Hang Seng (-0.3%) and Shanghai Comp. (+1.6%) were varied with outperformance in the mainland as participants returned from the holidays where spending rose by 6.3% Y/Y amid a bout of ‘revenge travel’ which saw Golden Week air passenger numbers recover to 91% of last year’s volume. Participants also welcomed private sector PMI data in which Caixin Services PMI topped estimates at 54.8 vs. Exp. 54.3 and Caixin Composite PMI was lower than previous at 54.5 (Prev. 55.1) but remained at a firm expansion. Finally, 10yr JGBs were steady amid the indecisive risk sentiment seen in Tokyo and as prices continued to eye the psychological 152.00 level, while the BoJ’s presence in the market for nearly JPY 1tln of JGBs has also provided a floor for government bonds.

Top Asian News

Hong Kong Small Cap Sinks 90% Amid Margin Call Speculation

India’s RBI Uses Unconventional Tools to Check Borrowing Costs

China’s Yuan Climbs, Stocks Gain in Upbeat Return for Traders

Foreigners Buy Most Turkish Assets Since 2018 After Rate Hike

Mixed trade in Europe as regional bourses diverged after opening with mild broad-based gains (Euro Stoxx 50 +0.2%) following on from a similar lead from the APAC region after Mainland China returned to the market following its Golden Week holiday. Meanwhile, US equity futures eke mild gains as hopes for resolution on some stimulus keeps State-side sentiment supported. Back to Europe, varying performance seen across the indices, with UK’s FTSE (+0.7%) outpacing peers on a favourable Sterling action, whilst the peripheries see underperformance after EU Budget talks between the European Parliament and EU ambassadors have been suspended after just an hour, after a German attempt to get a breakthrough failed, with the issue threatening a delay to the swift implementation of the Recovery Fund. Sectors are mostly firmer with Energy outperforming amid yesterday’s rise in the complex, with no risk profiled to be derived from the broader sectors. The breakdown sees Autos and Construction towards the bottom of the pile, whilst Basic Resources coat-tail on the broader gains across base metal markets. In terms of individual movers, Danish-listed Pandora (+14%) resides near the top of the Stoxx 600 after raising its guidance, with Novo Nordisk (+4.0%) also higher amid a forecast upgrade. British Land (+4.0%) is higher on the back of dividend resumption. LSE (+0.5%) is firmer after it announced the sale of Borsa Italian to Euronext (-3.7%) for EUR 4.325bln vs. Exp. ~EUR 4bln.

Top European News

Russian Covid-19 Cases Hit Record as Moscow Resists Lockdown

Europe Holds Crisis Talks as Spain Pushes for Emergency Powers

Italy’s Unflagging Bond Rally Drives Key Yield to Record Low

LSE Agrees $5 Billion Borsa Sale to Euronext, Italian Banks

In FX, no obvious catalyst, but the Kiwi has derived more than fellow G10 currencies from the Greenback’s deeper pull-back from 93.500+ levels in DXY terms to fresh w-t-d lows of 93.309, as Nzd/Usd breaches resistance at the psychological 0.6600 level that has been capping rebounds since the headline pair retreated from early October highs.

CHF/EUR/AUD/CAD/JPY – Also taking advantage of their US counterpart’s demise, with the Franc above 0.9150, Euro probing 1.1800 and Aussie eyeing 0.7200 again having cleared the 20 DMA (0.7176) following an encouraging FSR from the RBA. Meanwhile, the Loonie has extended recovery gains from midweek lows around 1.3340 towards 1.3160 ahead of Canadian jobs data and the Yen has rebounded from sub-106.00 levels after mixed Japanese household spending metrics, but may run into option expiry related offers given decent interest at 105.90-80 (1 bn) and then from 105.50 to 105.40 (1.2 bn). On that note, Eur/Usd expiries are well spread either side of 1.1800 and full details are available via the headline feed at 7.08BST.

GBP – Sterling was relatively resilient in the face of weaker than forecast UK data, and a particularly big miss in monthly GDP, but unable to weather the latest Brexit headlines suggesting insufficient progress in latest talks on trade before EU chief negotiator Barnier returns to Brussels. Cable has reversed through 1.2950 and Eur/Gbp is back over 0.9100 as the Pound awaits further fiscal support for the labour market from Chancellor Sunak and a speech by BoE’s Haldane.

SCANDI/EM – Only a modest loss of momentum for the Nok beyond 10.9000 vs the Eur in wake of softer than expected Norwegian CPI, while the Sek seems content between 10.4500-10.4100 parameters and unusually large option expiries in the Eur cross either side, especially at the 10.3000 strike where 4.1 bn rolls off vs 1.2 bn at 10.7500. Elsewhere, the Yuan has returned from China’s Golden Week break refreshed and raring to go as Usd/Cnh scales 6.7000 with the aid of a strong PBoC Cny midpoint fix (at 6.7796 vs 6.7905 projected and 6.8101 pre-market closure). Conversely, Lira losses accelerated to 7.9550+ before the CBRT stepped in with another aggressive move to arrest the slide via a 150 bp hike in Try swap rates, but 7.9000 as contained comeback efforts thus far. Ahead, Brazil’s Real in focus given inflation updates and services sector growth.

RBA Financial Stability Review stated that Australian banks are well placed to continue lending and supporting the economic recovery, as well as the financial system but added that although the financial system is in a strong position, risks are elevated. Furthermore, it stated that overall household income has increased during H1 2020 but the number of households experiencing financial stress has increased and will increase further, while it noted that business failures will increase substantially as loan repayment deferrals and income support end. (Newswires)

In commodities, WTI and Brent front-month futures ebb lower after the holding pattern seen overnight following yesterday’s gains which were fueled by some supply side developments. 1) Hurricane Delta is poised to make landfall along the Gulf Coast later today as a major hurricane, with BSEE’s latest estimate showing 91.5% of oil production and 61.8% of natgas production shuttered ahead of the hurricane. 2) Reports yesterday, citing a senior Saudi oil adviser, noted that the Kingdom is mulling cancelling an output hike next year amidst the rising cases coupled by Libyan oil output slowly coming back online. JP Morgan analysts see potential for Saudi to drive incremental oil cuts at the upcoming November 30th meeting, with the upside scenario a deeper cut whereby the Kingdom reduces output below quota against the backdrop of weakening demand. Meanwhile more recently on the geopolitical front, Armenia and Azerbaijan are in Moscow in a bid to ease tensions – the French Presidency expects a truce to be declared in the Nagorno-Karabakh region by this evening or tomorrow, according to Sky News Arabia. WTI Nov and Brent Dec reside around session lows within a tight range after declining from USD 41.47/bbl and ~43.50/bbl respectively. Elsewhere, spot gold continues to grind higher above USD 1900/oz (vs. low USD 1893/oz) on Dollar-dynamics, with similar action seen in spot silver which remains north of USD 24/oz. In terms of base metals, Shanghai Copper futures ended the day with gains of some 1% with LME copper also trading with gains amid expected strikes at Chile’s mines. Meanwhile, Chinese steel and raw material prices rose after the Golden Week holiday amid touted supply woes alongside forecasts for higher demand in Q4.

US Event Calendar

9am: Bloomberg Oct. United States Economic Survey

10am: Wholesale Inventories MoM, est. 0.5%, prior 0.5%

10am: Wholesale Trade Sales MoM, prior 4.6%

DB’s Jim Reid concludes the overnight wrap

Back to the secondary poll going on at the moment and markets had another strong performance yesterday as optimism remained that a stimulus deal might still be achieved pre-election and also as investors increasingly bet on the likelihood of a Biden presidency (and hence further stimulus) from January. After President Trump’s Tuesday tweet that he was pulling out of the talks, he continued to soften his stance in a Fox Business interview yesterday, and said “I think we have a really good chance of doing something”, as a Politico reporter also tweeted that Secretary Mnuchin had floated restarting talks with Speaker Pelosi. Pelosi noted that any passage of a skinny deal would require an agreement on a larger follow-on bill. One voice that has remained constant throughout the recent talks has been Senate Majority Leader McConnell, who again said Pelosi was insisting on “an outrageous” sum of money and acknowledged that the election timing makes agreeing on a deal “challenging.”

Whether or not we’re actually likely to see further stimulus by Election Day (and it still looks less likely than not), risk assets climbed higher in response to this news flow, and by the end of the session the S&P 500 had risen a further +0.80% to its highest level in over a month, and the VIX index of volatility fell back -1.7pts to a one-week low. It was another broad-based rally as 23 of 24 industries in the S&P 500 rose on the day. Cyclicals outperformed large-cap tech yesterday with the NASDAQ ‘only’ rising +0.50%. Energy stocks led the way on both sides of the Atlantic (+3.73% in the US and +1.63% in Europe) as Brent crude oil prices closed above $43/bbl for the first time in nearly 3 weeks. European equities overall saw similar gains to those in the US, with the STOXX 600 (+0.78%) and the DAX (+0.88%) powering forward.

Updating our screens overnight, US equity futures have continued to be supported by the positive stimulus news, with S&P 500 futures up +0.57%. Meanwhile in Asia, there’s been a more mixed performance, with the Nikkei (-0.20%) losing ground and the Hang Seng (+0.10%) seeing a modest gain. Chinese markets have seen a stronger performance, however, as they reopened after a week-long holiday, and the Shanghai Comp is up +1.89%. Furthermore, the September Caixin PMI from China showed the composite reading at 54.5 (vs. 55.1 last month) and the services reading increase to 54.8 (vs. 54.3 expected).

Back to the election, and the main political news from yesterday was President Trump’s announcement that he wouldn’t take part in the second debate next week following the decision that it would be held virtually, as well as the news overnight from his doctor that the President would be able to safely return to public engagements by Saturday. On the debate, Trump campaign manager Bill Stepien said that “We’ll pass on this sad excuse to bail out Joe Biden and do a rally instead.” Meanwhile, the Biden campaign said that he would take voters’ questions instead. With President Trump trailing by nearly 10pts now in both FiveThirtyEight and RealClearPolitics’ polling averages, skipping on the debate means that the president is missing out on any late attempt to reset the trajectory of the race. But in terms of markets, what was noticeable was the increasing focus on a potential Biden presidency and a possible blue wave. His chances on FiveThirtyEight’s model ticked up further to 84%, and the Democratic Party’s chances of winning the Senate are up to 68%, raising the prospect of significant further stimulus in Q1. Along with the House of Representatives, which is heavily expected to remain with the Democrats, this would bring an end to the divided government that we’ve seen these last two years.

On the coronavirus, Europe saw some further troubling news yesterday, which came as the executive director of the European medicines Agency, Guido Rasi, said that a vaccine was “unlikely” to be ready by the end of the year. In terms of the numbers, the UK saw another 17,550 cases reported, while the number of patients in hospital in England rose above the 3,000 mark for the first time since June. Over in France, another 18,129 were reported, and the number of Covid-19 patients in intensive care rose to its highest since May, at 1,427. In response, the government has placed Lyon, Lille and Grenoble on maximum alert, with restrictions similar to those in Paris and Marseille. In Poland, it will be compulsory to wear masks in public from Saturday, while further restrictions were imposed in the Czech Republic, where all cultural events and indoor sporting activities have been banned. There has been some pushback amid the rise in restrictions across the continent with the most recent from a court in Madrid blocking the regional government’s new measures to reduce mobility. This comes as Spain has continued to register nearly 70,000 new infections per week over the last month.

Over in the US, New York Mayor de Blasio announced the closure of a further 61 schools, bringing the total to 169. There were further concerning signs from some first wave northeastern hotspots, as Massachusetts, New York and New Jersey all saw the highest number of new cases since May. Overall, the 7-day rolling sum of cases in the US rose over 316,000 for the first time since mid-August.

In other news, we got the ECB’s account of its September monetary policy meeting, where there were a number of mentions on the exchange rate. Furthermore, it noted that “the recent appreciation of the euro exchange rate had had a material impact on the inflation outlook in the September ECB staff projections.” The euro saw a modest weakening against the US dollar yesterday, and was down -0.03% by the close.

Over in the fixed income sphere, sovereign bonds rose yesterday, with yields on 10yr Treasuries (-0.2bps) and bunds (-3.0bps) both falling. There were also a number of records set in southern Europe, as yields on 10yr Greek debt fell -4.5bps to an all-time low of 0.89%, and yields on 10yr Italian debt fell -2.6bps to an all-time closing low, though they had been lower on an intraday basis back in September 2019.

In terms of yesterday’s data, the initial jobless claims in the US for the week through October 3 fell to 840k (vs. 820k expected though), down from an upwardly revised 849k in the week prior. That said the continuing claims reading for the week through September 26 fell to a post-pandemic low of 10.976m (vs. 11.4m expected), with the insured unemployment rate falling to 7.5%.

To the day ahead now, and the data highlights include UK GDP for August, along with French and Italian industrial production for that month. We’ll also get the Canadian employment report for September, and the final August reading for wholesale inventories in the US. From central banks, the Reserve Bank of India will be deciding on monetary policy, while the Fed’s Barkin and the BoE’s Haldane will also be speaking.

via ZeroHedge News https://ift.tt/2SCnYDe Tyler Durden

{kind=link}