MSNBC producer Ariana Pekary explained that the reason for her deciding to quit her job was that the mainstream media blocks “diversity of thought” in favor of promoting hysterical voices for ratings and that a TV veteran admitted to her “we are a cancer and there is no cure.”

Pekary, who was an “integral member” of Lawrence O’Donnell’s primetime show, says that the media’s obsession with Trump is actually costing lives because it is preventing reasoned discussions about how to fight the coronavirus pandemic.

“This cancer risks human lives, even in the middle of a pandemic.

The primary focus quickly became what Donald Trump was doing (poorly) to address the crisis, rather than the science itself. As new details have become available about antibodies, a vaccine, or how COVID actually spreads, producers still want to focus on the politics.

Important facts or studies get buried,” Pekary explained.

This cancer, the Virginian notes correctly, risks our democracy,

“…even in the middle of a presidential election. Any discussion about the election usually focuses on Donald Trump, not Joe Biden, a repeat offense from 2016 (Trump smothers out all other coverage)…

Context and factual data are often considered too cumbersome for the audience.”

The former producer also revealed that a “successful and insightful TV veteran” acknowledged to her that,

“We are a cancer and there is no cure,” adding, “But if you could find a cure, it would change the world.”

Pekary also highlighted how the very model by which the corporate press is structured guarantees that voices of dissent are silenced in favor of hysterical political extremists, something that has come to fore over the last two months with the media’s relentless promotion of Black Lives Matter narratives.

“The model blocks diversity of thought and content because the networks have incentive to amplify fringe voices and events, at the expense of others… all because it pumps up the ratings,” she wrote.

Pekary’s resignation follows that of former New York Times columnist Bari Weiss, who said she was smeared by her own colleagues as a racist and a Nazi for daring to engage in “wrongthink” by not echoing fringe social justice rhetoric.

* * *

There is a war on free speech. Without your support, my voice will be silenced. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

via ZeroHedge News https://ift.tt/3kaAlD2 Tyler Durden

A mixed bag in the headline data with a revenue miss and earnings beat but it was the disappointing Disney+ subscribers that sparked some anxiety among investors (especially amid lockdowns and everyone looking for entertainment).

Good – *DISNEY 3Q ADJ EPS 8C, EST. LOSS/SHR 63C

Bad – *DISNEY 3Q REV. $11.78B, EST. $12.39B

Ugly – *DISNEY 3Q DISNEY+ SUBSCRIBERS 57.5M, EST. 59.4M

“Despite the ongoing challenges of the pandemic, we’ve continued to build on the incredible success of Disney+ as we grow our global direct-to-consumer businesses,” said Bob Chapek, Chief Executive Officer, The Walt Disney Company. “The global reach of our full portfolio of direct-to-consumer services now exceeds an astounding 100 million paid subscriptions — a significant milestone and a reaffirmation of our DTC strategy, which we view as key to the future growth of our company.”

But we do note that ESPN and Hulu subs beat expectations:

3Q ESPN+ Subscribers 8.5M, Est. 8.26M

3Q Total Hulu Subscribers 35.5M, Est. 33.8M

Even more troubling -and not entirely unexpected – was the Parks, Experiences, and Consumer products group with suffered an operating loss of $1.96 billion in Q3 and Disney sees a further $2.9 billion COVID impact in Q4 across all its businesses.

Bonds & Bullion Bid To New Records As Stocks See-Saw On Stimulus Scares Tyler Durden

Tue, 08/04/2020 – 16:01

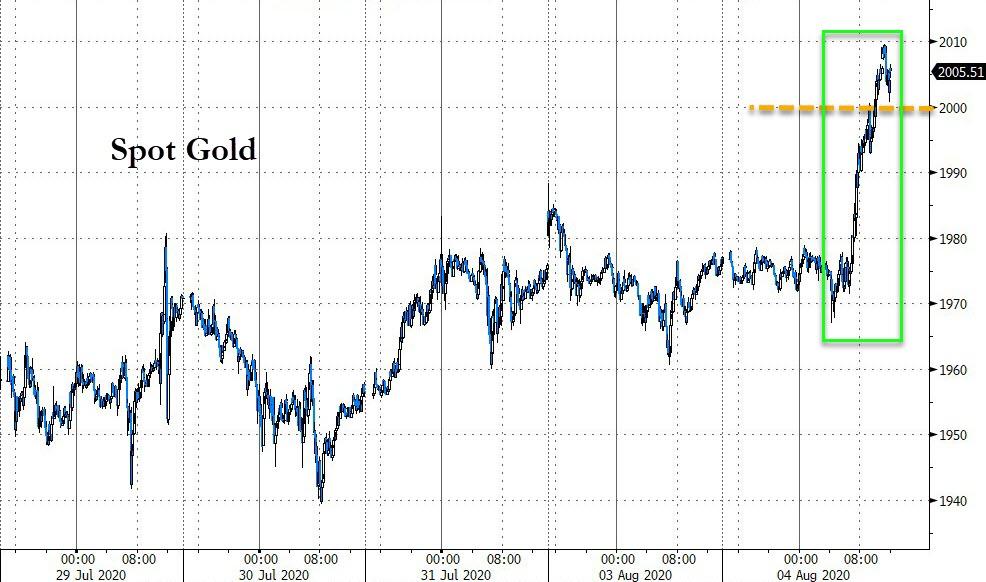

Spot Gold prices settled above $2,000 for the first time in history today…

Source: Bloomberg

After a series of confusing headlines about virus relief talks sparked anxiety (in some) stocks, and sparked a bid in bonds and bullion and selling of the dollar.

1142ET Pelosi: “doesn’t think there will be a deal this week.”

1415ET *SEN. PERDUE SAYS SENATE STIMULUS TALKS MAY TAKE ANOTHER 2 WEEKS

1425ET *MCCONNEL: WILL NOT FIND TOTAL GOP CONSENSUS ON VIRUS RELIEF

1450ET *SCHUMER SAYS NOT GOING TO STRIKE A DEAL JUST FOR THE SAKE OF IT

1455ET *SCHUMER SAYS HE IS HOPEFUL, TALKS MOVING FORWARD BIT BY BIT

Algos were crazy on words like “hope” and “nope” pinging markets around like a f**king cannabis/blockchain penny-stock…

Nasdaq underperformed most of the day (but the machines managed to get it green late on) as Small Caps were just panic-bid at every excuse.

And in case you wondered why – which you really shouldn’t by now – it was another major short-squeeze day…

Source: Bloomberg

FANG Stocks have been unable to extend after the huge gap higher on last Thursday night’s earnings…

Source: Bloomberg

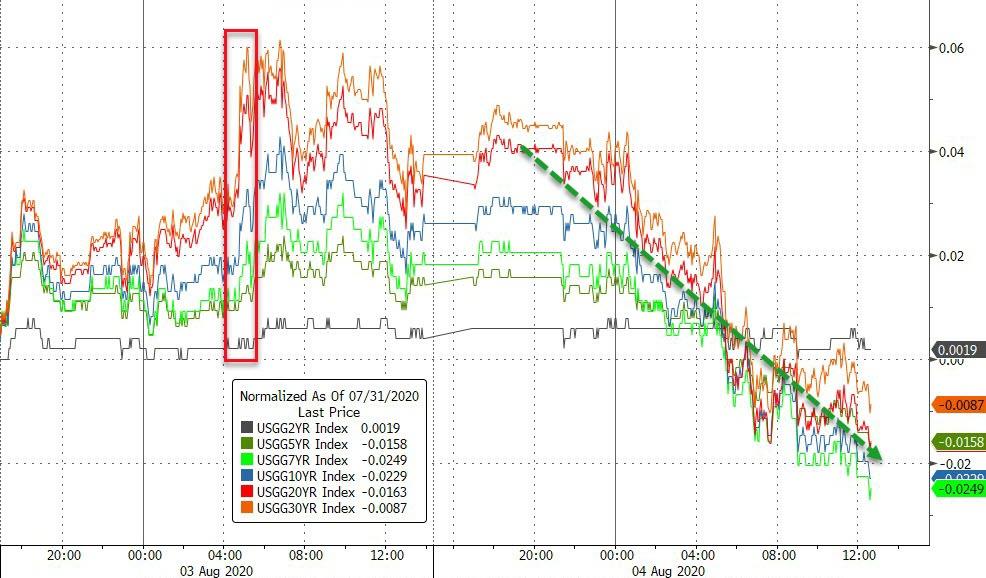

Treasury yields tumbled led by the long-end (30Y -5bps, 2Y -0.5bps)…

Source: Bloomberg

With 10Y Yields back to a 50bps handle – a record closing low…

Source: Bloomberg

In fact, record low closing yields for the entire curve aside from 30Y…

Source: Bloomberg

But stocks still don’t care…

Source: Bloomberg

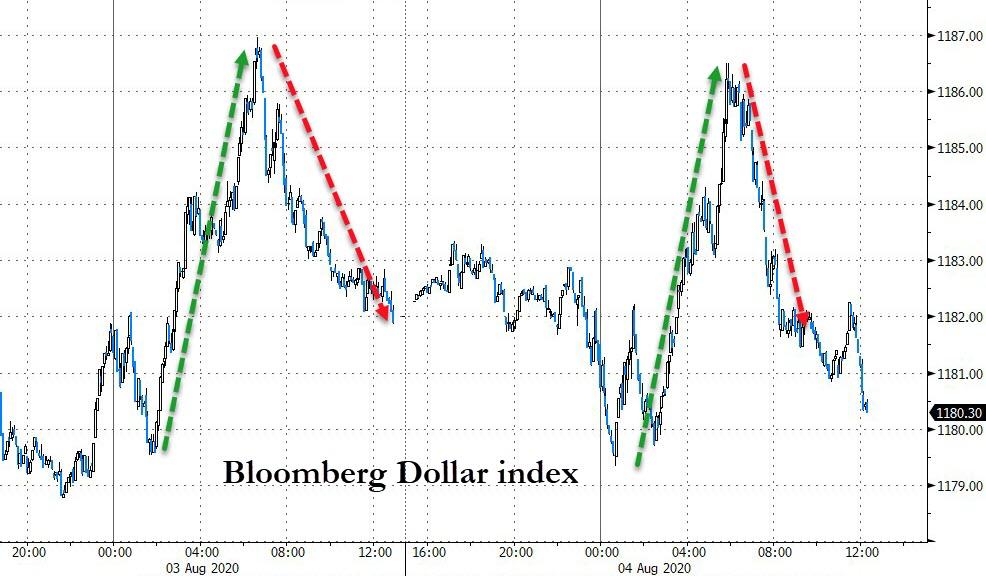

The Dollar mirrored Monday almost perfectly with a buying panic during the European day and selling in the US session…

Source: Bloomberg

Ripple and Ethereum are up on the week with Bitcoin and Litecoin just in the red from Friday…

Source: Bloomberg

Bitcoin continues to hold half its flash-crash loss…

Source: Bloomberg

Gold futures surged and closed above $2,000

Gold is notably overbought but the last few times it has been this overbought there has been consolidation and new high…

Source: Bloomberg

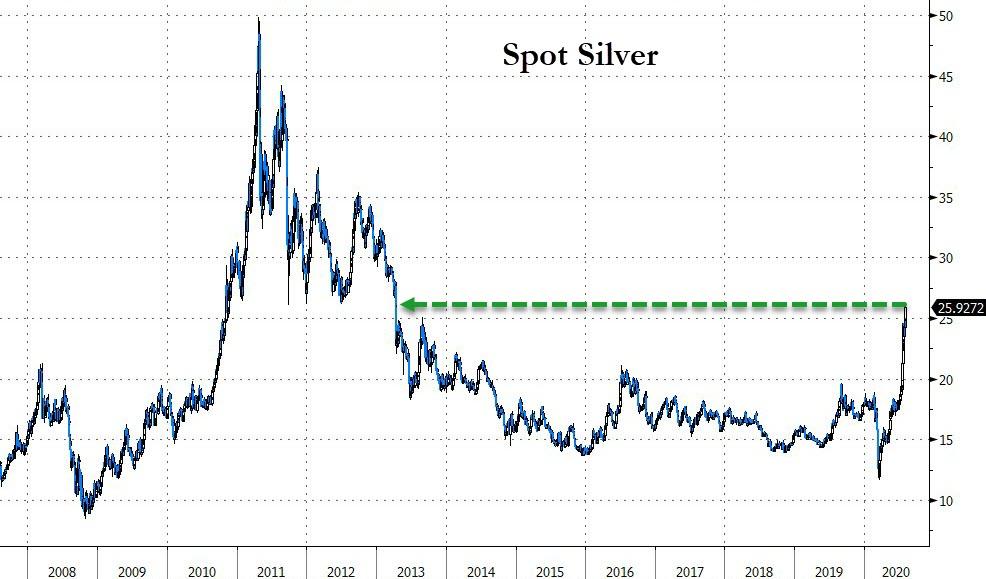

Silver futures hit $26…

Spot Silver is back at its highest since April 2013…

Source: Bloomberg

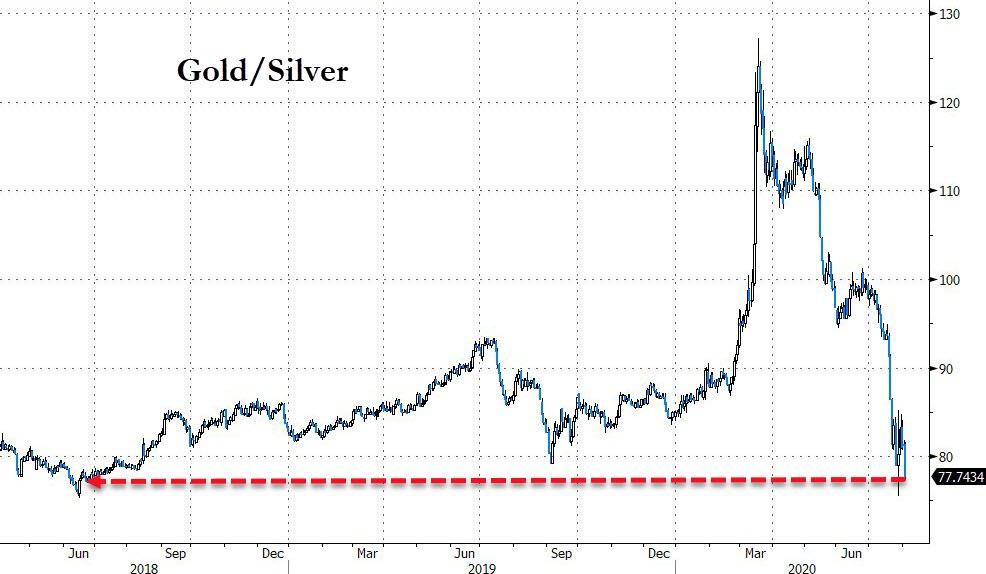

Silver’s outperformance sent the Gold/Silver ratio back to its lowest close since June 2018…

Source: Bloomberg

Oil prices chopped around as algos followed the same stock algos on headlines and ended higher ahead of tonight’s API inventory data (also helped by the dollar’s demise during the US session)…

Finally, as nominal gold reaches a record high…

Source: Bloomberg

…on an inflation-adjusted basis, it has room to run…

Source: Bloomberg

And if the world’s central banks keep doing what they’re doing (and does anyone really believe there will ever be a normalization now), then negative-yielding global debt will force allocations increasingly to bullion and bitcoin…

Source: Bloomberg

via ZeroHedge News https://ift.tt/3i5MtDw Tyler Durden

Teens Trash Trump For Destroying TikTok “Safe Space” As ‘Influencers’ Migrate To Instagram Tyler Durden

Tue, 08/04/2020 – 15:55

Across the US, millions of ‘Generation Z’ believe that evil ol’ Donald Trump is about to take away their favorite new toy – TikTok – after a brave cadre of courageous young people took to their keyboards and sabotaged his big campaign comeback event.

For the past few days, gen x influencers purportedly worried about the blowback to the influencer economy from the collapse of TikTok have been whining to reporters at the New York Times and Bloomberg, and those reporters have been publishing the choicest bits with nary an eye to accuracy.

Bloomberg reports that there’s been a “mass migration” to Instagram, where the veteran TikTokers have been sharing a funereal procession of their greatest hits from the app…as if a sale to Microsoft would somehow end the freewheeling atmosphere allowed by the Communist Party. One such user described TikTok as “fundamentally an escape for a generation right now in isolation, especially, that needs it.”

Late last week, the president said he planned to shut down Facebook’s most formidable challenger: Chinese-owned video-sharing app TikTok. That threat sparked a panic among users that their digital clubhouse would soon be taken away or sold to Microsoft Corp. – and sent many popular TikTokers racing to move their creative endeavors to Instagram, the rival mobile app owned by Facebook. But shifting to Instagram is an unsatisfying solution, said Max Beaumont, who built a following on TikTok documenting his journey of self-improvement with videos about diet and skin care. TikTok has become “fundamentally an escape for a generation right now in isolation, especially, that needs it,” he said. “Just because you can have a massive following on something like TikTok doesn’t necessarily translate over to YouTube or to Instagram or to some of these others.”

Another source, 25-year-old Brooklynnn Shrum, from Nashville, Tennessee, claims the app was a “safe and welcoming place for people in the LGBTQ community” (the implication is, Twitter, Facebook and other US-based social media platforms aren’t).

“TikTok gave an entire generation a voice, a platform, and power and that terrifies a lot of people, including President Trump,” said Brooklynn Shrum, 25, who downloaded TikTok earlier this year. “If you’re banning it because of a cyber security risk is one thing, but if you don’t let an American company buy it, that’s pure politics.”

Shrum lives outside of Nashville, Tennessee, and said TikTok provided a safe and welcoming place for people in the LGBTQ community like herself “to be themselves, without judgement.” It also gave young people a platform for activism, even though some of them can’t vote.

Shrum, who goes by @brooklyn322 on TikTok, posted an online tribute to the app last month and directed her followers to Instragram. “Follow me there in case the app goes down,” she said. “It’s been real.”

But the real gems were found in the NYT story, written by ace millennial reporter Taylor Lorenz, a social media star who has amassed a sizable social media following (which apparently qualified her to write about the topic for the NYT).

One of Lorenz’s sources, a 21-year-old named “Hootie Hurley”, complained that TikTok has helped “put food on the table”…and now mean old President Trump is going to cast them adrift in the middle of an election.

“If TikTok did shut down, it would be like losing a bunch of really close friends I made, losing all the progress and work I did to get a big following,” said Ashleigh Hunniford, 17, who has more than 400,000 followers on the app. “It’s a big part of who I’ve become as a teenager. Losing it would be like losing a little bit of me.”

There are also those for whom TikTok is their livelihood. “It has put food on our table,” said Hootie Hurley, 21, who has more than 1.1 million followers on the app. He said that a TikTok ban would be particularly devastating right now.

Even more ridiculous, Lorenz helped peddle a narrative that TikTok was an important source of pro-BLM content, helping to mobilize an army of teenage “activists”, and implying that this might be another reason Trump wants it shut down.

In addition to giving young people a place to meet and entertain each other, TikTok has also been a platform for political and social justice issues.

“I think this will drastically affect political commentary among teenagers,” Ms. Hunniford said. “TikTok is an outlet for a lot of protest and activism and people talking about their political beliefs. Banning that would not carry well among people my age.”

Lorenz’s reporting also suggested that hopping from one platform to another would be nearly impossible. While that’s true for some, any TikToker making good money on their following is probably already well diversified across platforms. A whole generation of social media influencers has endured the death of Vine.

Influencers who watched the fall of Vine, another popular short-form video app, in 2016 learned the importance of diversifying one’s audience across platforms. But even for TikTok’s biggest stars, moving an audience from one platform to another is a huge undertaking.

“I have 7 million followers on TikTok, but it doesn’t translate to every platform,” said Nick Austin, 20. “I only have 3 million on Instagram and 500,000 on YouTube. No matter what it’s going to be hard to transfer all the people I have on TikTok.”

So why have both Bloomberg and the NYT so willingly parroted these adolescent narratives about TikTok, lending credibility to the notion that the Trump Administration is targeting the app in retaliation for the Trump’s Tulsa rally. As we reported at the time, reports of teens actually using the app to interfere with the event were overblown by a mainstream press willing to boost these ridiculous narratives for the sake of traffic.

To be clear: the notion that the Trump administration is barring TikTok in retaliation for Tulsa is as much of a ‘whimsical conspiracy’ as anything readers might find on Zero Hedge, if not more.

via ZeroHedge News https://ift.tt/2XoCmBO Tyler Durden

Tyler Fitzgerald (Jim Backus aka Thurston Howell III from Gilligan’s Island): Anybody can fly a plane, now here: I’ll check you out. Put your little hands on the wheel there. Now put your feet on the rudder. There. Who says this ol’ boy can’t fly this ol’ plane? Now I’m gonna make us some Old Fashioneds the old-fashioned way – the way dear old Dad used to!

Benjy Benjamin (Buddy Hackett): What if something happens?

Tyler Fitzgerald: What could happen to an Old Fashioned?

– It’s a Mad, Mad, Mad, Mad World (1963)

I’m guessing some readers won’t remember this all-star, Oscar-winning classic. Indeed, it was made well before even my time, but I remember watching it on the ‘tube’ on more than one Sunday night in the late 1970s. I’d watch it with my Dad, who’d howl with laughter. I decided to watch it once again with my son. If you’ve never seen it, it’s worth the time. They just don’t make existential comedies like this one anymore. The story begins after a reckless driver named Smiler Grogan (Jimmy Durante) roars past a handful of cars on a winding California road and ends up launching himself over a cliff. Before (literally) kicking the bucket, he cryptically tells the assembled drivers that he’s buried a fortune in stolen loot… under a mysterious ‘Big W.’ He says: “350G’s. I’m givin’ it to ya’ but watch out for the bulls. They are everywhere.” Yes, they are, albeit he had a different sense in mind. With little moral reservation, the motorists set out to find what they now consider their fortune.

The characters exemplify some of human nature’s best and worst qualities. At times, they are wildly creative and improvisational. However, they work together only to the extent necessary – double-crossing each other repeatedly. They lie. They cheat. They steal without a second thought. They have a singular focus: treasure – at any cost. Their sense of entitlement is overwhelming. In the scene quoting Tyler Fitzgerald, who is a high-society alcoholic, two of the treasure seekers (played by Mickey Rooney and Buddy Hackett) convince him to fly them to Sant Rosita in a brand-new Beechcraft twin. Blinded by greed, they seem to care little that he is too drunk to stand. In the end, they all find the Big W together along with the treasure beneath – but only to be bamboozled out of it. Eventually, the money ends up being lost completely and redistributed from atop a fire escape to a crowd in ‘Santa Rosita square.’ Helicopter money of sorts – easy come, easy go. Greed is not only their foremost motivation, but it’s their ultimate undoing.

There are more than a few similarities between the Mad, Mad, Mad, Mad World characters and today’s market participants.

So far at least, myopic greed and speculation have paid well. Analysis has been a handicap. Unprecedented fiscal policy stimulus combined with the Fed’s debt monetization has thus far maintained a pretense of normalcy in markets. There will be consequences to ballooning balance sheets (both corporate and federal). Few seem to be considering that the ultimate consequence of massive deficits is at the very least potentially crushing taxation. Or worse, if the Fed ever stops QE in an attempt to normalize policy by shrinking its balance sheet (soon to be an anachronistic concept), rates would likely rise steeply. The Fed is too busy bailing out the bottom of the boat to raise the sails.

Deficits are now so large that Treasury issuance monetization must occupy the vast majority of the Fed’s attention. This close the zero bound, the Fed can no longer significantly lower rates, it simply must prevent rate market dislocations due to massive supply. Fed action is no longer stimulative; rather, it is only palliative. Importantly, it’s not Fed ‘liquidity’ feeding market participants’ emotional impulse. While it remains an enabler, it’s fiscal policy that is putting money directly into gamblers’ bank accounts. This distinction is crucial to whether fiscal policy continues to provide enough liquidity for a return to the casino later this year. It seems that equity markets are priced for an aggressive second round of fiscal policy action, an efficacious vaccine by year end, and a healthy corporate America – free from defaults.

Takeaways

This time, there’s no treasure under the Big W. It’s just a big ‘W.’ We remain in a bear market with highly unfavorable return characteristics for large and small cap U.S. equities alike.

Equity and credit market performance is no longer all about monetary policy; it’s mostly about market participant emotion, which is largely dependent upon the pandemic fiscal policy response.

The Fed that is now hamstrung – now ‘forced’ to monetize massive, and otherwise unsustainable, policy deficits.

Fiscal policy stimulus has found its way directly into U.S. equity markets – particularly speculative names and technology.

Pre-existing fragility – especially excessive leverage – will make escape velocity for markets and the economy particularly difficult to achieve.

Liquidity will likely evaporate when personal and business defaults eventually sop up fiscal policy liquidity. The Fed is ill-positioned to act efficaciously. It’s too busy mopping up Treasury issuance.

Loans create deposits and without creditworthy borrowers, even a continued, fiscal-policy driven expansion of M2 may not result in higher asset prices.

Risk-asset markets are not correctly pricing the coming explosion in prospective personal, corporate, and commercial real estate (CRE) defaults.

Liquidity Trap

Let’s start with the often-cited reason to be long equity markets now. As the story often goes:

“Take a look at the money supply. The Fed has printed money… so much money. Just look at the monetary base and M2. It has exploded. It’s bound to find its way into equities. Don’t fight the Fed.”

Old Fashioned, anyone? Proponents of this rationale may be right on the result (higher equities) for a time, but they’d be right for the wrong reason. This time is different. First, the Fed ‘printing money’ is an anachronistic phrase I wish well-paid strategists would stop using all together. The Fed’s creation of excess reserves (‘money printing’) and subsequent purchases of assets are no longer lowering interest rates sufficiently to stimulate real economic growth. Rates are already low. It’s not the quantity of money that stimulates growth or increases inflation; it’s first and second order effects of lower capital costs – i.e. lower rates or yields. Now, the Fed’s reserve creation is solely for the purpose of preventing a rates market dislocation. After the GFC, the Fed lowered capital costs considerably; now, it’s simply treading water to keep them low. Importantly, not only does this make it more difficult for the Fed to stimulate the economy, but it also makes it tough for the Fed to help prevent corporate loan defaults when cash flows deteriorate. Thus, the Fed’s direct impact on risk-asset markets has diminished greatly, and I’ll soon explain why it matters.

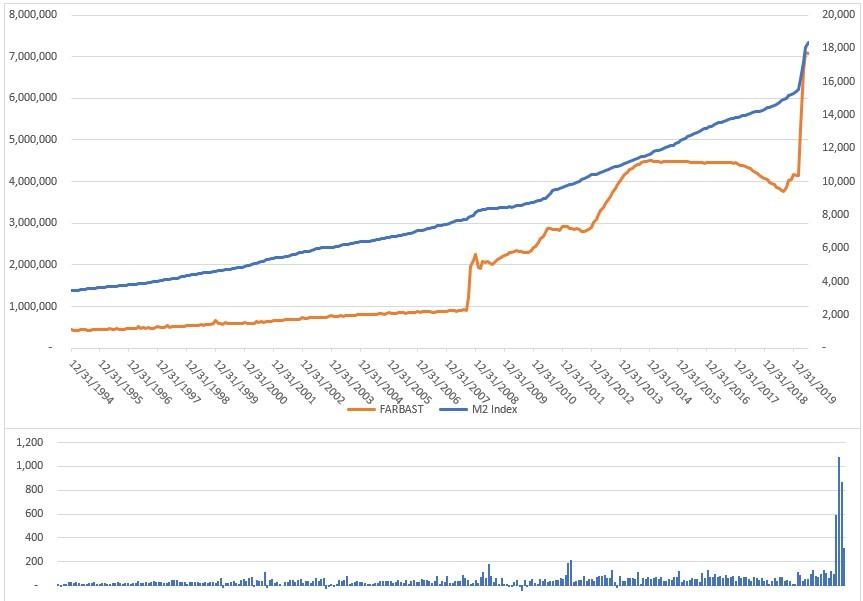

For one, it’s helpful to understand that the Fed has often implemented QE without a consequent outsized increase in M2, to which so many have pointed as supporting equities now. The connection is more complicated. Frist, risk assets have often rallied without any M2 increase. Contrary to popular belief, the more or less consistent growth in M2 (due to natural growth of currency in circulation as loans are made) generally sees spikes when there is aggressive fiscal policy response. As Figure 1 shows, the Fed’s balance sheet expansions (the asset side of the balance sheet identity for reserve liability creation) often do not correspond well with significant M2 increases. This is particularly clear during the $1 trillion 2013 quantitative easing program; money supply growth didn’t budge above trend. In contrast, in both 2008, 2011 and most recently, M2 did increase. Those instances accompanied fiscal policy stimulus, and in each case M2 increased in line with the amount of the fiscal stimulus. For obvious reasons, the impact of recent fiscal stimulus on M2 has been outsized.

Figure 1: Top Panel – M2 (blue) and Fed Balance Sheet (orange); Lower Panel – Change in M2 (blue bars); Source – Bloomberg Data

To cut to the chase, M2 growth is supporting equities, but it’s not a monetary policy phenomenon – it’s fiscal policy one. While fiscal policy is driving both investor sentiment and the beginnings of an economic recovery, the Fed still plays a critical role. Without its current “QE to infinity” approach, the massive supply of Treasuries would have little place to go. Rates would likely move considerably higher, especially on the long end of the curve as demand would most certainly fall short of supply. Why? Precisely because of the massive policy deficits – already supersized even before the pandemic – required to combat the enormity of the pandemic shock. Fiscal policy is now the key – the Fed is the enabler but no longer the main actor.

Indeed, especially near the zero bound, low rates may lose their real-world stimulative efficacy. A liquidity trap typically occurs when interest rates are low yet consumers and businesses tend to save. Indeed, since last year, I have advocated for gold (in part) because of this phenomenon. Such behavior renders monetary policy ineffective. First described by economist John Maynard Keynes, during a liquidity trap, investors may choose to keep their funds in cash savings because they believe interest rates could soon rise, because they need to repair balance sheets, or because they wish to prepare for upcoming financial stress. At the same time, central bank efforts to spur economic activity are hampered as they are unable to lower interest rates sufficiently to incentivize corporations and consumers to invest or to consume, respectively. This is precisely why central bankers had been advocating for a fiscal policy response long before the pandemic shock. Ironically, because market participants no longer seem to perceive equities as a risky asset, saving appears to manifest vis-a-vis equity market speculation!

Fiscal Dominance

So, what is next on the fiscal policy front? Well, it seems this stimulus round is shaping up more modestly than the initial round. Over $500 billion in paycheck protection (PPP) and another almost $300 billion in direct to consumer programs (including supplementary pandemic unemployment insurance relief) accounted for the lion’s share of a ~$1 trillion increase in M2 (Figure 1). According to Bloomberg, after the White House dropped the idea of including a payroll tax cut, White House and Senate Republicans now have a “fundamental agreement” on a GOP plan for another round of pandemic relief. Instead of a payroll tax cut, the GOP will now back $1,200 checks for individuals who make up to $75,000 a year, just as in the March stimulus bill. Moreover, last week, Treasury Secretary Steven Mnuchin told CNBC that the Republican coronavirus relief plan will extend enhanced unemployment insurance “based on approximately 70% wage replacement.” Presumably, this will be something less that the current $600 for most Americans. In aggregate, the Republicans reportedly are looking to propose $1 trillion in relief versus over $3 trillion from Democrats. The timetable for releasing legislative text, which is key to beginning negotiations with Democrats, is uncertain. One thing seems clear: the package’s scope will be more limited than the initial round of stimulus.

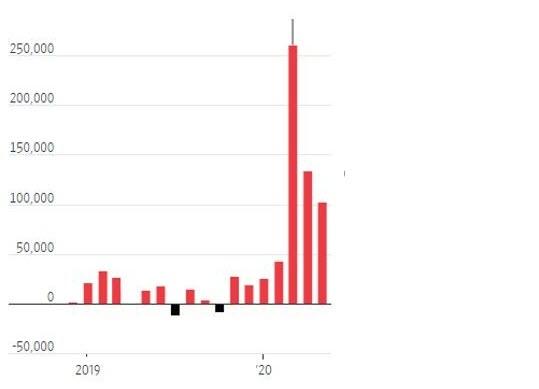

While likely smaller, the second round of fiscal policy response will once again put cash into checking accounts. This will once again help increase M2 and may also help to support equities. This is what’s so different about this equity market. With an assurance that the economy will be directly supported by more consumer directed stimulus, retail market participants are driving the rally – not unlike the late 1990s. Just this weekend the WSJ put an exclamation point after the sentence. Figure 2 from the Journal shows the number of new E*Trade accounts retail investors opened in march. It dwarfs any previous month. It’s generally the same dynamic for the Robinhood platform about which I began writing in September of 2019. My favorite quote from the story is a woman who proclaims that her trading style is aggressive because ‘scared money makes no money.’ According to the Journal, “she read ‘Trading for Dummies,’ watched YouTube videos, opened an E*Trade account and dove in.” That sounds about right.

Figure 2: New E*trade Retail Accounts by Month; Source – WSJ

This is now the sixth month of a pandemic that has not yet significantly abated in the U.S. In order to continue unwaveringly towards the Big W, it would seem to require market participants believe an efficacious vaccine is not only assured but that it is also distributed quickly to the population. Moreover, there remains much unknown about the immune response and evidence is growing that immunity may be short-lived. Nobody even seem to recall the slowdown that was already afoot before the pandemic occurred. In light of an extended first wave of virus cases and with continuing unemployment claims still above 16 million, how much long might market participants throw caution to the wind? (Figure 3 – not shown – illustrates just how enormous that unemployment statistic is.) Just how long will banks and investors continue to loan money based on a stimulus-based recovery thesis? The answer to the latter question is critical to not only asset prices but also to the main-street economy.

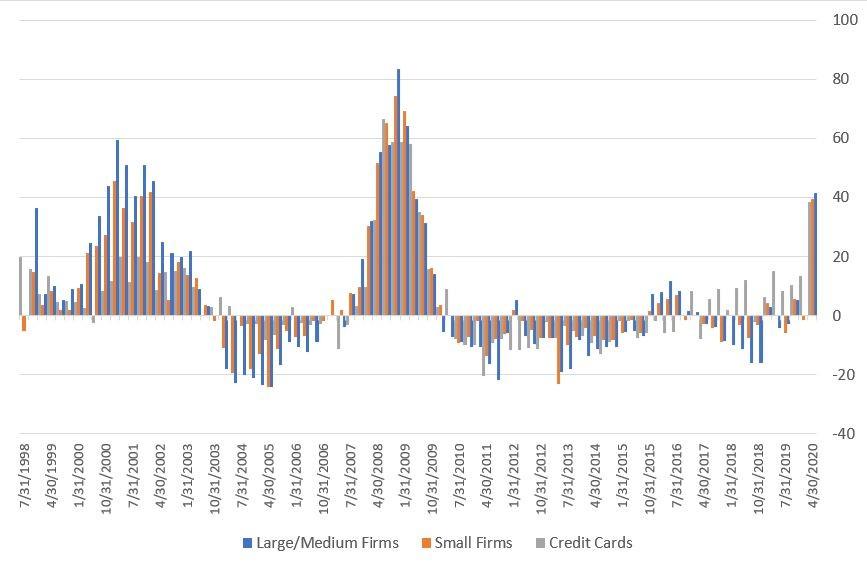

In the absence of unusual fiscal policy stimulus programs (as present) and under normal circumstances, loans create deposits. Deposits, in turn, contribute to a capital base for yet more loans. Defaults and delinquencies are surely one thing that destroys the loan-deposit cycle. Defaults will slowly start to sop up liquidity – as they always do. Lending standards, which had already begun to tighten in 2019, are now tightening significantly… it’s likely just the beginning (Figure 4 above). Corporate and consumer lending will continue to slow, and as the corporate sector begins to experience even more strain as leverage grows, speculative behavior should begin to dissipate. That’s when the narrative changes from ‘there’s so much liquidity out there’ to ‘what the heck happened to all the liquidity.’ Easy come, easy go.

Figure 4: Lending Standards for Large/Medium Firms (blue), Small Firms (orange) and Consumer Credit Cards (gray); Source – The Fed

Corporate sector leverage – particularly speculative grade loans and bonds – has been at the top of the list of concerns for at least the past twelve months. If it was a concern pre-pandemic, it is of far greater concern now – even taking into account the scope of fiscal and monetary policy action. Banks typically slow lending and non-bank lenders typically curtail funding when credit fundamentals begin to deteriorate. Policy action, especially fiscally funded support for performing corporate credit, has helped suspend lower-rated paper from wires above. While prices have rebounded, credit fundamentals are not improving. As Bloomberg’s Philip Brendel puts it:

“Distressed-debt supply fell by $3 billion in June to $195 billion, a 47% correction from the cycle’s March peak of $366 billion. The stock market’s rally, seemingly without a conscience, seems to be comforting credit markets as investors shrug off record Covid-19 cases and an upcoming parade of horrific 2Q earnings results. Yet sharp corrections are common in highly volatile distressed cycles, and we think the exuberance may mirror spring 2008’s similar two-month window of calm, which didn’t last.”

According to Bloomberg data and analysis, despite 26 issuers in North America already having become fallen angels as of June 30, about 47% of corporate debt carrying BBB tier ratings has either a negative outlook or is on credit watch negative. That’s about $2.6 trillion of BBB tier debt that carries a negative outlook or is on credit watch negative. This includes over $89 billion at risk of becoming high yield. Importantly, financials are the most at risk accounting for about 33% of the total (including issues from Intesa Sanpaolo, Discover Financial and Deutsche Bank).

Importantly, non-bank lenders and loan syndication vehicles are also challenged – specifically, collateralized loan obligation (CLO) and business development companies (BDCs). The CLO market is about $700 billion and supports the $1.2 trillion speculative grade loan market. BDCs account for over $200 billion of speculative grade loans outstanding. CLOs provide banks with a syndication mechanism, which helps them keep loans off their books and shifts the risk to third parties. BDCs on the other hand, originate loans and rely upon equity issuance to help fund loans. While best of breed BDC equities have rallied, second tier lenders have continued to struggle greatly. This will leave the smaller, capital constrained companies they were designed to serve without capital access. As reported by Bloomberg, about 30% of CLOs are forecast to have tripped OC tests with some being able to trade their way out by selling the CCCs and buying BBs at a discount. While playing defense, it’s difficult for CLO sponsors to promote new vehicles; thus, this important source of investor loan demand begins to evaporate. Credit expansion is an essential source of liquidity and M2 growth. It will be difficult for even extreme fiscal policy measures to supplant credit expansion indefinitely.

Conclusion

As I suggested in the Portnoy Top in early June, recklessness and bravado had become so extreme it seemed likely to have reached a crescendo that might correspond to a market top. Such extremes are indeed difficult to gauge – after all, what’s irrational can stay that way for some time. So far at least, the broader indices like the NYSE composite and the Russell 2000 appear to have topped on June 8th. Breadth has continued to narrow as a handful of large cap tech names are responsible for the advance in the S&P 500 ad Nasdaq. Technology shares have pushed even farther beyond the limits of rationality. When over a third of the S&P 500’s market cap is large-cap tech, that is a bad sign for market health. Trading for Dummies should add a chapter on that. Scared money may not make money today, but at least it lives to fight another day…

The monetary policy guardrails upon which so many have come to rely are flimsy. Monetary policy is no longer providing the safety it once did. Why is that important? Because we must all now be focused on fiscal policy above all else when assessing near-term sentiment and market action. Even with fiscal policy support increasing money supply by direct deposit, a liquidity trap is likely. Perhaps even more ironically, for now at least, this trap is somehow supporting equities because of a new breed of reckless equity market participant, who regards the equity market as a form of saving.

Ultimately, defaults and corporate distress will steamroll greedy bravado and force a reconnect of equity prices and economic reality. It’s happened once already this year. It will likely happen again. We don’t know for sure, but presumably Smiler was on his way the Big W when he went over the cliff. As he said, he spent twenty years earning every penny of that fortune, but he failed to live long enough to see it. Today, there’s no treasure under that Big W – it’s just a big ‘W.’ Live to fight another day, Smiler.

via ZeroHedge News https://ift.tt/3ike9Vx Tyler Durden

Florida Man Shoots And Kills Burger King Employee After Order Takes Too Long Tyler Durden

Tue, 08/04/2020 – 15:25

Today in “2020 couldn’t even surprise us if it tried anymore” news…

A woman in Orange County, Florida was so upset about the time it took for her to get her order at a Burger King, she commissioned a man to return to the restaurant and shoot one of its employees.

Deputies said that when they arrived, they found 22 year old employee Desmond Armond Joshua suffering from a gunshot wound in the parking lot. He was then taken to the area hospital where he was pronounced dead.

Video recovered from the scene showed Joshua in a physical altercation with a “male who had him in a headlock,” according to Click Orlando. One witness said the restaurant was busy the night of the incident and the drive-thru was backed up, causing customers to have to wait longer than usual.

One woman was so mad about waiting, she got out of her car and threatened to have “her man” return to the restaurant. The Burger King refunded her $40 and asked her to leave. She waited in the parking lot in her black sedan for a few minutes before driving away. Later, she returned in a white truck with 37 year old Kelvis Rodriguez-Tormes, who demanded that Joshua fight him.

A witness intervened in the fight when Rodriguez-Tormes put Joshua in a headlock and started to choke him.

Deputies then said Rodriguez-Tormes then went to his truck and got his gun, telling Joshua: “You got two seconds before I shoot you.”

Shortly thereafter, he shot Joshua and fled in the white truck. In an interview with police after the shooting, Rodriguez-Tormes said he dismantled the gun and placed it “in a location which cannot be located”.

Rodriguez-Tormes is now being charged with first-degree murder with a firearm, destruction of evidence and possession of firearm by a convicted felon. The woman has not been arrested.

Authorities said Joshua had just started working at the Burger King, days earlier.

Burger King commented: “We are deeply saddened to hear of the tragic incident that took place at the Burger King on 7643 E. Colonial Drive and passing of team member Desmond Joshua. At Burger King, the safety of team members and guests is our top priority. The franchisee who owns and operates the restaurant is fully cooperating with authorities on this matter. Any questions should be directed to local authorities.”

via ZeroHedge News https://ift.tt/2Pn14Oq Tyler Durden

Milton Friedman famously said, “Inflation was always and everywhere a monetary phenomenon.” But Friedman didn’t live through the QE years here in the U.S. and blatantly ignored the twenty plus years of Japanese deflation despite QE and insane levels of money printing during the latter years of his life.

Because Friedman, like a lot of modern economists, adhered strictly to the Quantity Theory of Money (QTM).

And as an Austrian economics kinda guy I somewhat agree with the QTM. I agree with Ludwig von Mises on this, as you would expect. So, how do we square the QTM with the evidence that QE in all of its guises has resulted in deflation, as expressed by the general price level, where ever it has been tried?

Martin Armstrong asks this question all the time and is openly hostile to the QTM. And his arguments have some merit, because, as he rightly points out the QTM only looks at the supply side of the money equation.

It cares not about the demand side. He’s right about that. What he’s wrong about is that the Austrians, like von Mises, haven’t considered this either.

Demand for money is just as important as the supply of it. And during a crisis, the demand side of the equation for any particular currency may, in fact, be more important.

This is what the Fed has struggled with for the past twelve years. The demand for the U.S. dollar has far outstripped the increase in supply, causing a far lower aggregate price rise than anticipated by the QTM.

But money, like all commodities, goes to where it is most demanded by thos that obtain it. And Bernanke’s QE post-2008 crisis didn’t go to the people, it went to the banks and the banks and the government who did what they thought was best with it.

In trying to prop up asset values the Fed, however, blew bubbles in not only equities but also home prices, cars, education, health care, government regulation etc.

Offsetting that has been the destruction of price in things like food and energy, which are now far cheaper in real terms (and as a percentage of disposable income) than they’ve been in decades.

And this dynamic couldn’t change in the post-Lehman years under Bernanke if the Fed, like the Bank of Japan before them and the other major central banks today, allowed the money printed to actually circulate.

The QTM seems to fail because the money never circulated.

Bernanke ‘sterilized’ the new money, paying banks not to lend but rather hold the money on reserve with the Fed paying a nominal interest rather than engaging in traditional lending.

Because if he had done that the QTM would have risen up to bite him in the ass.

Bernanke understood that he had a demand problem. There was too much demand for dollars to service non-performing debt. But if he had let those trillions circulate it would have touched off an inflationary spiral as most of the money wouldn’t have gone to debt service but to bid up the price of base commodities.

So he chose to slowly bleed out the excesses of the previous credit-induced boom through time and attrition, just like the Bank of Japan, and slowly build the unavoidable inflation through the expansion of the money supply while demand returned to normal.

While the QTM ignores the demand side of the money equation, when the definition of the money supply and, more importantly inflation itself, doesn’t accurately describe reality the QTM becomes a hindrance to understanding what’s going on.

This is summed up in the question, “If Bernanke printed all these trillions, why is there no inflation?” To which Gary North, writing for Lew Rockwell all those years ago answered, “IOER.”

IOER = Interest on Excess Reserves.

To Bernanke he beat the QTM by paying IOER. Previous to Bernanke, excess reserves hovered around zero. The market always paid a better return than the Fed’s 0.25%.

The Federal Reserve can re-ignite monetary inflation at any time by charging banks a fee to keep excess reserves with the FED.

Anyone who predicts an inevitable price deflation does not understand that the present scenario is the product of legitimately terrified bankers and the Federal Reserve’s Board of Governors. At any time, the FED can get all of the banks’ money lent. But the FED knows that this will double the money supply within weeks. This will create mass price inflation.

Bernanke paid the banks not to lend and therefore most of the money printed didn’t circulate. It wasn’t part of the supply and therefore couldn’t cause inflation.

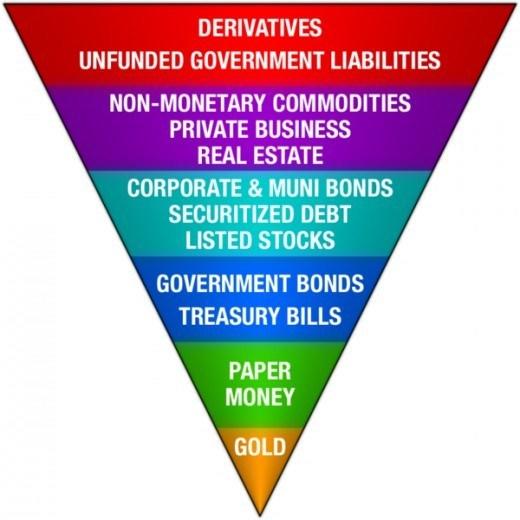

Moreover, credit money was contracting at that time. The top of Exter’s Pyramid was collapsing and Bernanke was trying to widen the base of the Pyramid by printing trillions in base money.

John Exter’s Money Pyramid

Back then it was there was a fight pitting the inflationists led by Peter Schiff versus the deflationists led by Harry S. Dent, and to a lesser extent Martin Armstrong.

Some of that money circulated through the growth in government spending and the returns generated as second-order effects of rising stock prices, the so-called ‘wealth effect.’

In the end we got what the Austrians would expect. Asset bubbles in the things people buy on time at zero-bound rates — cars, houses, medical bills, college degrees, military weapons, war — and deflation in legacy maturing financial assets and high depreciation cost assets like infrastructure through capital starvation, waste and fraud.

The Yellen and Powell years were marked by them hoping to withdraw these ‘temporary’ funds from the banking system by raising rates and doing QT – Quantitative Tightening.

It didn’t work at all, precipitating a credit collapse last year thereby, again, invoking the threat of the QTM. Because now the world was used to these assets at zero-cost of carry, zero-bound rates, which inflated their prices..

And those prices were way too high relative to that old supply of money. Withdraw the funds and watch the money markets seize up.

This is why we Austrian types kept saying the “Fed was trapped!” There was no way to go back to the way things were because while the Fed may have run out the clock on the 2008 toxic asset pile, it created an all-new even bigger pile of toxic-assets-in-waiting by the time we get to 2020…

… exactly as predicted.

Worse than that the Fed internationalized that pile, spreading the cancer out the world over, by turning the dollar into the ultimate carry-trade currency.

The real pandemic we should be scared of in 2020 isn’t COVID-19, it’s the immense pile of un-payable loans of all types, commercial or otherwise. With the rise of MMT now we’re just openly admitting the debts aren’t payable.

And the Fed has done nothing so far to say that it has any cures for this disease other than mo’ money.

It may be the first bit of honesty we’ve ever gotten from them.

So, color me not shocked when I see the latest proposal to come out of the Fed to stave off the deflationary vortex, directly pump money into everyone’s bank account.

The response was striking: they two propose creating a monetary tool that they call recession insurance bonds, which draw on some of the advances in digital payments, which will be wired instantly to Americans.

As Coronado explains the details, Congress would grant the Federal Reserve an additional tool for providing support—say, a percent of GDP [in a lump sum that would be divided equally and distributed] to households in a recession. Recession insurance bonds would be zero-coupon securities, a contingent asset of households that would basically lie in wait. The trigger could be reaching the zero lower bound on interest rates or, as economist Claudia Sahm has proposed, a 0.5 percentage point increase in the unemployment rate. The Fed would then activate the securities and deposit the funds digitally in households’ apps.

As Potter then elucidates, “it took Congress too long to get money to people, and it’s too clunky. We need a separate infrastructure. The Fed could buy the bonds quickly without going to the private market. On March 15 they could have said interest rates are now at zero, we’re activating X amount of the bonds, and we’ll be tracking the unemployment rate—if it increases above this level, we’ll buy more. The bonds will be on the asset side of the Fed’s balance sheet; the digital dollars in people’s accounts will be on the liability side.”

Bringing us right back to Milton Friedman and, more importantly, von Mises and the QTM. Because now the Fed is not talking about injecting sterilized reserves into the money supply to create fictions of bank balance sheets.

Because, as Mises pointed out, once there are no more vacancies at the debt hotel now the QTM can be fully expressed. More supply equates to more inflation.

Now Friedman will be proven prophetic.

Because the Fed would be injecting money directly into the economy to stimulate aggregate demand because there are no more places to hide it and get any kind of future return.

Most of the world’s debt trades at a negative yield. IOER is 0.10%. National budgets are running at 20% to GDP deficits. Pension systems are trillions in arrears.

Now we’re at that moment where the old thought exercise of what happens when you inflate the money supply by 10% prices occurs. The answer is prices will go up by 10%.

Critics of the QTM, like Armstrong, argue that the Fed et.al. are obsessed with creating 2% price inflation in a deflationary environment. That’s not completely true. Because if they charge those excess reserves they can create whatever inflation rate they want in a heartbeat.

What they are obsessed with is doing that and bailing out the banks at the same time.

That they can’t do without destroying confidence which is a nice way of saying they are scared of the QTM calling their bluff.

Because no matter how you try to hand wave the arguments away, more money chasing the same number of goods is inflationary. One look at home, car, health care and education costs tells you exactly where all the inflation went.

Bernanke dreaded that scenario just like Dr. North said which is why he paid IOER while destroying the middle class through rising prices for real goods and wage stagnation.

He created trillions in latent inflation based on the U.S.’s capacity as the world’s reserve currency, stuffing the world with reserves it didn’t need to maintain asset prices it couldn’t sustain.

He undermined the validity of every other currency in the process to save the dollar. They’ve had to deal with the QTM biting them, but we only care about ourselves.

In an environment where most people’s time preference is short because they are literally fighting for their economic lives, this new stimulus money will go right into the things people needs right now — food, clothing, shelter.

Things are so bad for so many Americans now that they saved their first stimulus checks and only spent them on the bare necessities, forgoing any thought of paying down debt.

They used what’s left of their credit rating to feed themselves now on someone else’s dime and let the bank choke on their mortgage when the credit card is maxed.

This next round of stimulus money will circulate. The Fed will finally do what Bernanke tried desperately to avoid, print helicopter money.

Zerohedge is right, the Fed finally admitted that QE is deflationary because it signals to the markets that conditions are still too fragile after 12 years to invest in the future because there is no future.

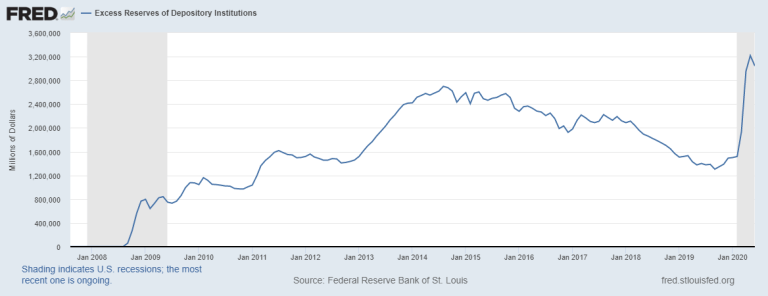

Therefore the money given to the banks is hoarded as excess reserves because the potential return on investment is lower than IOER. Today Jay Powell stopped paying IOER, it’s 0.10% lower than Bernanke’s 0.25% and he still can’t get the money moving.

Excess reserves are rising again. Same playbook, worse results.

That was the first phase of this crisis.

Now that we’re past that part and if the Fed adopts this policy, it will hand us money to keep asset prices from falling by creating fake demand. All that will do is undermine the confidence anyone holding dollars abroad has in the U.S., the dollar and our leadership.

And then the QTM will be our problem, not theirs. Because demand for dollars will collapse and the circulating supply will rise. Gold is sniffing this out now.

Then, and only then, will the Fed achieve its inflation target… and beyond. And Milton Friedman will look down and say, “I was right.”

And Mises will look back at him and say, “Yes, eventually.”

The movie V for Vendetta is set in an alternative reality where a neo-fascisttotalitarian regime has subjugated the United Kingdom under the guise of protecting the people from war, terror and disease. Yes, disease. Indeed, the following clip from this 15-year-old dystopian film looks awfully like the world we now live in today, does it not?

At the film’s catalyst, a freedom fighter (codenamed “V”) hijacks the feed for a major TV network in London and broadcasts a “sermon” to the nation wearing a Guy Fawkes mask. See how his words apply to the governments’ reaction to COVID-19:

“And the truth is, there is something terribly wrong with this country, isn’t there?Cruelty and injustice, intolerance and oppression,” says V as his masked face appears across television sets around the nation.

“And where once you had the freedom to object, to think and speak as you saw fit, you now have censors and systems of surveillance coercing your conformity and soliciting your submission.

“How did this happen? Who’s to blame? Well, certainly, there are those who are more responsible than others, and they will be held accountable. But again, truth be told, if you’re looking for the guilty, you need only look into a mirror.”

“I know why you did it. I know you were afraid. Who wouldn’t be? War, terror, disease.”

Starting around 1:00:

Are we not seeing this today? Where several billion people have been scared into voluntarily handing over their freedoms so that they can be kept safe from a virus.

“There were a myriad of problems which conspired to corrupt your reason and rob you of your common sense. Fear got the best of you, and in your panic you turned to the now high chancellor, Adam Sutler. He promised you order, he promised you peace, and all he demanded in return was your silent, obedient consent. “

I pray this not be a sermon we will deserve to hear in the years to come.

Already they have “conspired to corrupt your reason and rob you of your common sense.”

Let us remember that being “silent” is the same as giving our “obedient consent” to such totalitarian trickery.

As V says:

“Because while the truncheon may be used in lieu of conversation, words will always retain their power. Words offer the means to meaning, and for those who will listen, the enunciation of truth.”

via ZeroHedge News https://ift.tt/33sCWCy Tyler Durden

Shortly after House Speaker Nancy Pelosi said she did not expect a stimulus deal this week, Republican Senator Sonny Perdue warned that “Senate stimulus talks may take another two weeks”…

And stocks did not like that…

as investors reached for gold as a safe-haven…

Mitch McConnell also did not help by saying that he did not expect to reach a total GOP consensus on virus relief.

Democrats Up Stimulus Demand To $3.4 Trillion In Odd Negotiating Tactic Tyler Durden

Tue, 08/04/2020 – 14:15

House Speaker Nancy Pelosi just revealed that Congressional Democrats not only won’t budge on their $3 trillion stimulus package passed by the House in May – she’s upped the demand to $3.4 trillion in order to ‘settle’ on a deal.

Asked by CNN’s Manu Raju if she still wants a stimulus deal this week, and if she has a price tag she’d be willing to settle on, Pelosi replied “Yeah, $3.4 trillion.”

“We are just right now identifying the justification for what we’re saying it costs — how the money would be spent,” Pelosi said. “And we’re asking the same for some of the things they are talking about, so that we have a clear understanding. So it’s productive in that regard.“

White House Press Secretary Kayleigh McEnany described Pelosi’s new demand as ‘a mockery’ of the process.

.@PressSec on the administration working with Democrats on coronavirus relief: “It is Nancy Pelosi, it is Chuck Schumer, that are making an absolute mockery of this process.” pic.twitter.com/lmOCwJvfXZ

Meanwhile, Senate Majority Leader Mitch McConnell (R-KY) – who has called the $3 trillion Democratic proposal “another big laundry list” – has flat out rejected the left’s package, and has instead defended the Senate GOP’s $1 trillion stimulus bill.

The top Democratic and White House negotiators have held hours of talks this week in hopes of reaching a deal on another round of stimulus spending as key deadlines on extending a federal eviction moratorium and federal unemployment benefits have come and gone.

Pelosi, when asked if it’s really feasible to get a deal this week given how far apart the two sides are, said, “At some point you just have to freeze the design.” –CNN

The Speaker said she hopes lawmakers can reach a bipartisan agreement this week in order to hold a vote in the House by next week – which will require a Rules Committee meeting to determine the parameters for debate over the bill on the House floor.

“We are just right now identifying the justification for what we’re saying it costs — how the money would be spent,” said Pelosi. “And we’re asking the same for some of the things they are talking about, so that we have a clear understanding. So it’s productive in that regard. And now we just have to negotiate what comes next.“

via ZeroHedge News https://ift.tt/3frbyqL Tyler Durden