8/ But in this case they are refusing to offer any opinion in writing to the industry on what should be allowed and why, and instead are engaging in intimidation tactics behind closed doors. Whatever their theory is here, it feels like a reach/land grab vs other regulators.

Update as of 5pm ET, Friday, September 17th: we are not launching the USDC APY program announced below

Our goal is to create great products for our customers and to advance our mission to increase economic freedom in the world.

As we continue our work to seek regulatory clarity for the crypto industry as a whole, we’ve made the difficult decision not to launch the USDC APY program announced below.

We have also discontinued the waitlist for this program as we turn our work to what comes next.

We had hundreds of thousands of customers from across the country sign up and we want to thank you all for your interest.

We will not stop looking for ways to bring innovative, trusted programs and products to our customers.

No longer is crypto-currency lending a fringe asset class operating in the wild wild west of the internet; the time has come for the sheriff to lay down the law. This move by the SEC should be seen a significant warning sign that they intend on going head to head with crypto-related businesses.

In the coming year, it’s likely that the financial regulators around the world will turn their sights to Crypto businesses and require them to comply with specialized regulations that are still being drafted as well as traditional securities laws.

The only exception will be to those companies that are already regulated to sell securities or are regulated banks and will have the benefit of continuation of trade and will likely have a poll position for any changes in the requirements.

…

Coinbase and other large crypto-lending companies like BlockFi and Celsius have a strong position now but the future of the Crypto business will likely have more to do with regulatory approval than white papers, branding, and well-designed smartphone apps.

The disruptors are facing serious disruption as the whole industry finds itself on the radar of global regulators who have been given the go-ahead to start cleaning things up.

The central bank should start pulling back on its $120 billion monthly bond purchases and signal when it will lift rates, but it probably won’t.

It has been only 17 months since the biggest unthinkable in the oil market – the price turning negative – illustrated vividly that the global economy was experiencing an unprecedented shock that required an exceptional policy response by the government and the Federal Reserve. This week, Fed policy makers will discuss how to unwind two of its three chief components over time.

The oil unthinkable was the result of the collapse in demand that accompanied the first stages of the 2020 Covid-19 economic shock. Stranded by storage facilities that were either full or extremely expensive, holders of oil scrambled to liquidate their excess supply, with some even willing to pay buyers to take it off their hands.

The dominant general theme at that time, that of deficient demand relative to available supply, was not new. It had dogged policy makers since the 2008 global financial crisis, albeit much less extreme but more generalized. It had led central banks to run extremely loose financial monetary policies characterized by unusually low interest rates, huge injections of liquidity through large-scale asset purchases and aggressively loose forward policy guidance. Indeed, what the Fed did in 2020, while remarkable in size and scope, actually built on a decade of extraordinary monetary policy.

Today, the macroeconomic landscape is much different.

The household and corporate sectors — in aggregate though not every member — have strong balance sheets having benefited from ample fiscal transfers and subsidized debt refinancings. Demand and sentiment remain solid.

The only thing blocking an even bigger demand boom is the Covid delta variant, and even that is not strong enough to hold back retail sales, as last week’s upside data surprise illustrated.

That alone is enough reason for the Fed to detail this week how and when it intends to withdraw two of the emergency measures that are still in place more than a year after the worse of the Covid economic and financial shock. The central bank should announce the immediate initiation of a tapering of quantitative easing with a goal of eliminating the $120 billion of monthly purchases in the first half of next year; and it should signal through its forward policy guidance a gradual lifting of near-zero interest rates starting in the second half of next year.

But while deficient aggregate demand is no longer a problem, the supply side is and will remain so for a while. As detailed here, what ails supply chains, transportation and worker availability goes well beyond temporary and quickly reversible factors. Longer-term structural forces are also in play, raising the specter of inflation that remains higher and more persistent than the Fed has repeatedly forecast until now.

That, too, suggests that the Fed should start gradually easing its foot off its pedal-to-the-metal QE and signal its intention to tap the brakes down the road in an orderly fashion via higher interest rates. This would be best done if, on its side, Congress were to open the door for fast progress on the Biden administration’s infrastructure plan, physical and human, and if financial regulators were to coordinate better, nationally and internationally, to strengthen prudential policies, especially as they pertain to dampening excessive risk-taking among nonbank market participants.

Yet the Fed is unlikely to do so this week for several reasons, from the inability to embrace sufficiently yet the extent to which the demand and supply paradigm has shifted to concerns about triggering a disorderly correction of elevated asset prices after the excessive risk-taking encouraged by years of ample and predictable liquidity injections.

Rather than proceed with a taper now and signal the initiation next year of a measured and gradual normalization of interest rates, the Fed is likely to adopt a more dovish approach. This could include signaling the possible start of a taper later this year or early next year, reiterating that the taper decision is decoupled from the policy rate decision, signaling a delayed and slower interest rate normalization and packaging all of this in highly conditional language.

I suspect that most market participants, including long-term investors, would much prefer this course of action to the alternative, which I believe is necessary and feasible. “QE infinity” remains their top policy choice for the Fed given the extent to which central bank liquidity has turbocharged asset valuations, allowing for such a historical decoupling from underlying economic fundamentals.

Yet as appealing as this seems, it would be rather shortsighted because it would allow economic and financial risks to continue to rise unduly, threatening the long-term inclusive recovery needed not just for sustainable economic well-being but also for underpinning genuine financial stability. Indeed, by the time the Fed finds itself forced to hit the brakes, the window for doing so in an orderly fashion may prove worrisomely tight.

Gunman Kills At Least 6 At Russian University – Terrified Students & Faculty Jumped From Buildings

A horrific school shooting in Russia’s large central city of Perm has left at least six people dead and 28 injured. Terrified students and faculty were filmed jumping out of windows at a university campus as a gun-wielding young man walked across campus and into buildings opening fire.

CNN reports that “A suspect in the shooting was arrested and wounded after resisting law enforcement officers, according to Russia’s Investigative Committee, a state body that handles major crimes.” Unconfirmed social media video appeared to show the shooter suffered multiple wounds and paramedics initiated life-saving steps at the scene.

The Russian Ministry of Health later said that 19 of the injured were in local hospitals for gunshot wounds. Others among the wounded may have been injured trying to escape, as shocking video showed people dangling from second story windows before falling.

They were desperately attempting to escape the killer’s rampage inside the building.

Gunman attacks a university in the Russian city of Perm. Deaths and injuries being reported.

According to media reports, the person believed to be the gunman may be a student at the university, and posted a social media image of himself posing with a rifle and bullets, as well as a black helmet:

The gunman reportedly said, “I’ve thought about this for a long time, it’s been years and I realized the time had come to do what I dreamt of.” The post was eventually taken down.

The Monday incident comes months after seven school children were killed and 16 injured at a school in Kazan. Similarly a young man went on a rampage and methodically murdered people as he strolled through campus.

Video of the alleged shooter walking across campus

After the Kazan shooting, Putin urged his government to impose more stringent gun ownership regulations and requirements.

Until these latest incidents, such mass shootings were relatively rare in Russia and Eastern Europe in general when compared to prior years in the United States, where multiple mass shootings would happen yearly.

The narrative that black people are driving the ‘abolish the police’ calls, specifically in Minneapolis, has been again disproven as a survey found that way more white people support the move than black people do.

KARE 11 reports that a poll found that 51 percent of white voters support replacing the Minneapolis Police Department with a new Department of Public Safety, while only 42 percent of black voters support the measure.

In addition, 75 percent of black voters believe the police force should not be reduced in size, compared to 51 percent of white voters.

The news agency also reported that “More white voters support reducing the size of the force than Black voters, but there wasn’t a majority among either demographic, 33% compared to 14%.”

The survey was carried out by The Star Tribune, MPR News, KARE 11 and FRONTLINE.

Predictably when split along political affiliation, the results are stark with 55% of Democratic voters saying they support total replacement of the police force, yet only 7% of Republicans being on board with that.

Last week, extreme leftist representative Ilhan Omar fumed about the measure to replace the police in Minneapolis being blocked by a court.

“This ballot measure should be on the ballot,” Omar declared, adding “As you can tell, I’m pretty upset about it,” and charging that “The leaders who are opposed to progress in this city are not nameless or faceless.”

Omar added, “There’s a judge, there’s a mayor, there’s a police chief, and their monied friends who are telling us we can’t have a city that is flexible to our needs and our demands. How else are we supposed to make progress if we can’t do that?”

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. We need you to sign up for our free newsletter here. Support our sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Also, we urgently need your financial support here.

Canadians Head To The Polls In Election That Could Oust Justin Trudeau And Return Conservatives To Power

With polls suggesting an extremely tight race, Canadians are heading to the polls on Monday to vote in a snap federal election that was called last month by Prime Minister Justin Trudeau to try and achieve an outright parliamentary majority by Trudeau’s Liberals.

Unfortunately for Trudeau, in the weeks since he called the election, the Liberals have seen their lead slide, and are now running virtually neck-and-neck with the Conservatives. Souring support for Trudeau means it’s entirely possible that the political scion could lose the premiership after six years in power, leaving Erin O’Toole and his conservatives to form a new government.

While the New Democratic Party and the Greens attacked Trudeau from the left, the conservatives have slammed Trudeau’s flashy, “entitled” persona while arguing that Trudea’s mishandling of the economy has created “Liberal inflation” squeezing Canadians by raising the cost of living.

Candidates scrambled to attend to packed schedules of last-minute campaigning on Monday, with Trudeau (who launched the “snap” election with a short walk to Rideau Hall on Aug. 15) kicking off the day with an event in Montreal. He’s expected to touch down in several provinces before Tuesday, although he’s not expected to speak with reporters – and, unsurprisingly, there’s a good reason for that.

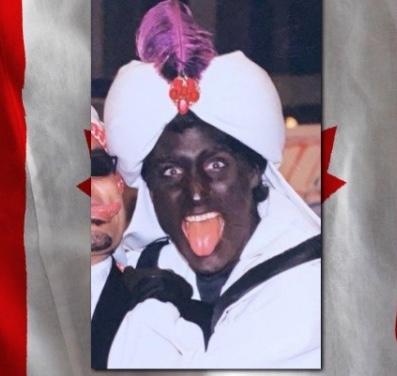

On Monday, with voters heading to the polls, Trudeau’s enemies released a new (and this time, in color) photo of the PM wearing blackface at an event back in 2001. While previous photos have emerged from the event showing Trudeau wearing a ridiculous Middle-Eastern getup complete with the dark face makeup, the earlier photos were (ironically) black and white. As we have reported, Trudeau has appeared in public wearing blackface at least three times during his younger years, long before the start of his political career (which comes courtesy of the fact that he’s the son of a former premier, although some have contested the ‘official’ story about his parentage, speculating that he might be the son of a different former world leader).

Shifting back to the beginnings of the campaign, Trudeau claimed Canadians deserved a say in how Canada would recover from the COVID pandemic in a transparent excuse to try to capitalize on strong polling numbers. O’Toole has accused Trudeau of putting Canadians’ health at risk in pursuit of his own political ends. The premier has spent his 6 years in power without a unilateral majority, making it more difficult to implement his agenda.

As Trudeau’s initial lead evaporated, the Liberals’ message morphed, changing into a mix of asking voters whom they trust to end the pandemic, along with a series of attacks against the Conservatives on climate, guns and vaccine policy. Trudeau said Sunday that Canada is at a “crossroads”.

Perhaps unsurprisingly, Trudeau has dedicated most of his time to campaigning in recent weeks. More than any other leader, the PM has spent the campaign on the defensive, visiting more ridings currently held by Liberals than those controlled by opposition parties, according to an analysis of the leaders’ schedules by the CBC.

O’Toole has gained ground in the polls partly by pursuing a moderate policy stance with a platform that focuses on issues like jobs and the economy, mental health and includes pitches to workers.

“I want you to know if you’re frustrated, if you’re angry anywhere in this country, I want you to know something. I get it. Conservatives get it,” O’Toole said at a Saturday rally in Kitchener, Ont.

“Now is the time for Canadians to make a choice,” O’Toole said Sunday in Markham, Ont. “We can choose to settle for second-best — for a party that hardly tries and barely delivers. Or we can choose to believe in a brighter, better, more united future.”

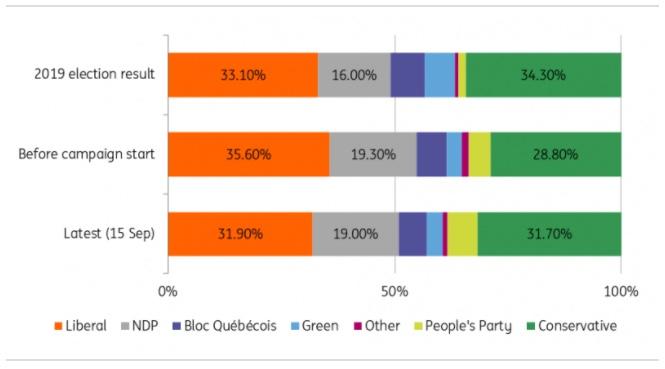

Until just a few days ago, the Conservatives had held a substantial lead over Trudeau’s Liberals in the polls, before a decline brought them to a statistical tie in national support with the Liberals, according to CBC’s Poll Tracker. A snapshot of polling numbers from ING shows how public sentiment has shifted over time, with opposition parties eating away at the Liberals’ lead.

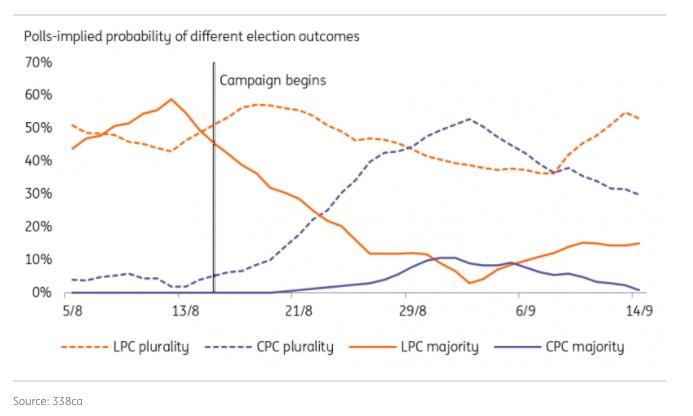

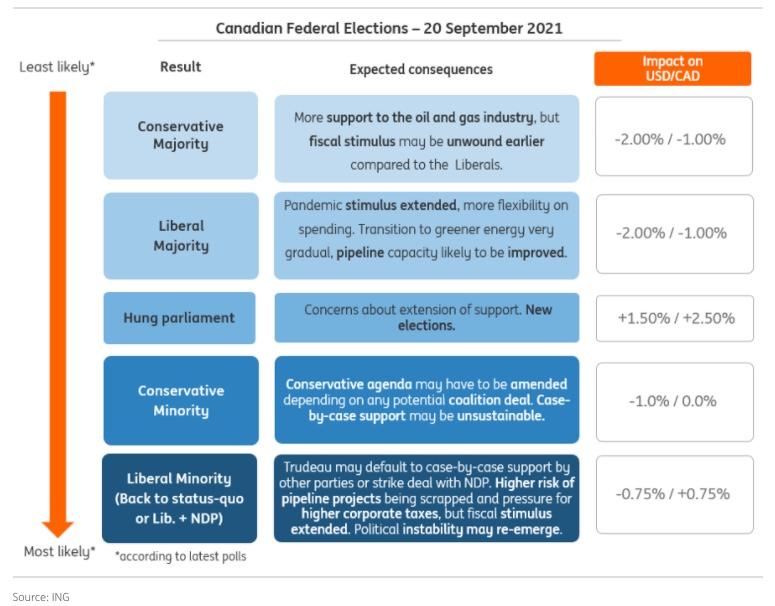

The Liberals currently hold 155 of the 388 seats in the House of Commons. Polls suggest the risks are skewed towards them losing a few of those seats rather than being able to add. They would need to pick up 15 seats in order to reach the 170 seat threshold that would allow them to govern without the support of another party. If anything, polls suggest that a minority Conservative win is more likely than a majority win by the Liberals, as shown in the polls-implied probabilities in the chart below.

In a note to clients, ING explains that the election has implications for markets, with the two main ones being the impact on fiscal stimulus plans, along with energy/pipeline policy.

Here’s a breakdown of the most important issues for markets courtesy of ING strategists and economists led Francesco Pesole and James Knightley:

1. Fiscal spending: markets should welcome a continuation of Trudeau’s support

Trudeau’s massive fiscal support programme was a pillar of his government’s pandemic-response strategy, with total support nearing 20% of GDP.

Pandemic-induced stimulus is gradually being unwound, but based on the latest campaign pledges, the general feeling is that the Liberals will be more relaxed with further deficit expansions, while the Conservatives have pledged to balance the budget over the long term. Consequently, there is the expectation that they will scale back stimulus quicker than the Liberals, which would likely see slower growth, less inflation and lead to a lessened probability of a major Bank of Canada policy tightening outlook.

The complicating factor is if there isn’t a majority for either party and they need the support of the New Democrat Party (NDP) which is advocating higher corporate, capital gains and income taxes for top earners. If they end up supporting the liberals it may not have as much as an influence on policy thrust as if they partner with the Conservatives.

One caveat concerns Trudeau’s promise to hike tax rates (from 15% to 18%) on all earnings over CA$ 1bn for banks and insurers. Such a measure may send some shockwaves across banking stocks in Canada, but for the moment we think that the prospect of extended fiscal stimulus should be the primary driver of the market response and benefit the Canadian dollar through expectations that fiscal support will allow the Bank of Canada to remain on its policy-normalisation path.

2. Energy sector: Trudeau is pro-pipeline, but his potential coalition partners are not

The energy sector contributes to approximately 10% of Canada’s GDP every year, but aside from the headwinds generated by the pandemic in the past year, the industry has been looking at some longstanding structural issues that may dent its ability to take advantage of higher oil prices.

A major issue remains the lack of pipeline capacity, as many Canadian oil and gas producers remain heavily dependent on the more expensive rail system as a means of transportation. Trudeau has been historically in favour of expanding Canada’s pipeline network, but new projects have found increasing opposition from environmentalist parties (like the Greens and the NDP). Also, this year, US President Joe Biden’s opposition caused the cross-border Keystone XL expansion project to be scrapped.

Despite the Liberals’ official stance for increasing pipeline capacity, the parties that are most likely to join a coalition (like the NDP) are explicitly against it. This means that the more Trudeau will have to rely on coalition deals with left-wing parties to govern, the less likely the pipeline situation is going to be resolved.

The Conservatives are openly in favour of new pipeline projects and retain in general the friendliest stance to the traditional oil-and-gas industry among all parties. Their plans for a transition away from carbon fossil fuels looks likely to be more gradual than that proposed by the other parties, and they plan to actually provide more subsidies to the struggling industry.

Bottom line: A workable majority is what matters the most for CAD

The Canadian dollar has likely discounted some degree of political uncertainty lately as polls showed the Liberal party’s hopes for an outright majority becoming more and more distant. Some evidence of this is the risk premium currently embedded into USD/CAD. According to our short-term fair value model (which includes rate differentials, relative equity performance, risk sentiment and commodity factors as variables) USD/CAD is currently 2% overvalued, a level that is above the 1.5 standard-deviation upper bound – as shown in the chart below.

When discussing the two main policy themes that we think markets are mostly keeping an eye on in this Canadian election campaign, we suggest that a minority win by the Liberals could see CAD benefit from better fiscal stimulus prospects, and a minority win by the Conservatives may mean CAD being supported through a better outlook for the oil and gas industry in Canada.

Ultimately, however, we think the market reaction will depend much more on whether the vote will allow room for a workable majority to emerge and guarantee political stability in the coming years, rather than which party will come up as the winner.

The best-case scenario for CAD is undoubtedly a majority win by either one of the two parties, but that seems to be a low-probability outcome if the latest polls are to be trusted. The most likely scenario of either the Liberals or the Conservatives winning most seats but having to rely on other parties (either on a case-by-case basis like the latest government, or through coalition deals) to govern may ultimately have a quite contained impact on CAD.

However, a minority win would pave the way for a potential hung parliament. We should know more on Tuesday, as post-election comments start to outline the different possible political scenarios, but from an FX point of view, we think that any political-noise risk premium embedded in CAD may remain in place until a clear working majority materialises.

* * *

As far as the other candidates are concerned, Bloc Québécois Leader Yves-François Blanchet is hoping to pick up seats for his party to help protect Quebec’s independence. NDP Leader Jagmeet Singh hasn’t held back when it comes to criticizing Trudeau from the left. Green Party Leader Annamie Paul is finishing her campaign in Toronto Centrer, her own riding (for the Americans who aren’t familiar, a riding is like a Congressional district), which she has rarely left over the past five weeks. Weakened by internal conflict, the Greens may struggle to defend their two seats in Parliament.

Finally, Lee Friday from the Mises Institute mused in a recent piece that all three candidates are guilty of various transgressions and broken promises and none are particularly exciting, about the vote that Canadians might be better off voting “none of the above”. Given the close polling, it’s likely a clear winner won’t be known until Tuesday, or perhaps later in the week.

In the Atlantic provinces, polls open at 0830 and close at 2030 local time. In the Eastern time zone, which encompasses nearly all of Quebec and Ontario as well as part of Nunavut, polls will be open between 0930 and 2130. Those voting in the election for Canada’s 44th Parliament must bring proper identification to vote.

As far as elections go, the Canadian is the first of two major elections among the G-7 during the latter half of September. On Sept. 26, Germans will take to the polls to elect a successor to Chancellor Angela Merkel. It’s a vote where “the unthinkable has become possible”. Read more here to find out why.

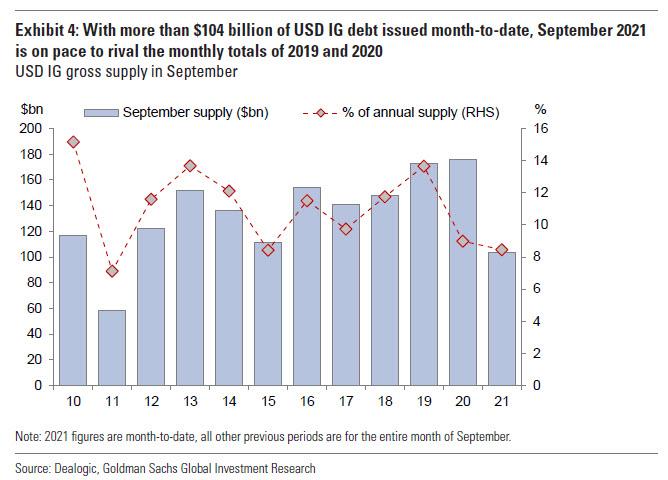

After a record post-Labor day bond offering frenzy, and a September calendar which has seen $104BN in IG debt issuance to date, and which Goldman believed (as of last week) will rival the monthly totals of 2019 and 2020…

… the mood has soured sharply, and on Monday, at least eight investment-grade companies are said to have pulled their bond offerings amid the crash in risk assets, according to Bloomberg which notes that “the issuance backdrop isn’t inviting with equity futures lower by about 1.5% and the IG CDX index trading over 6.5 basis points wider (largely due top the roll which put an extra six months of maturity on the new contracts).

Today’s pullbacks follow Friday’s vacuum when nothing priced amid the market’s sharp opex drop; last Monday some 13 deals priced.

That said, even without the Evergrande contagion, issuance was slowing: this week syndicate desks expect issuance to hit $20 billion to $25 billion, a slowdown from frenzied, record pace of sales since the market returned from the Labor Day holiday.

It is possible that most companies that had planned to come look again on Tuesday, but that will be contingent on stabilization in markets, which in turn will depend on what Beijing does in the next 24 hours.

Trump Treasury Secretary Steve Mnuchin Launches $2.5 Billion Private Equity Fund

Former Treasury Secretary Steven Mnuchin has just sent the clearest signal yet that he likely wouldn’t rejoin a potential second Trump Administration (despite being one of the more successful cabinet members) via reports that the ex-Goldmanite will raise $2.5 billion for a new private equity fund.

Mnuchin isn’t the only industry giant who is launching a new PE fund amid an explosion of dealmaking spurred in part by the Fed’s policy response to the pandemic. Back in July, former Apollo founder Josh Harris announced fundraising plans for his own billion-dollar fund.

According to the report, most of the money will come from the Middle East, including from Saudi Arabia’s Public Investment Fund. Remember, Mnuchin was a key player who helped build the Trump Administration’s increased closeness with the Middle East. Trump memorably visited Saudi Arabia for his first public official visit after taking office.

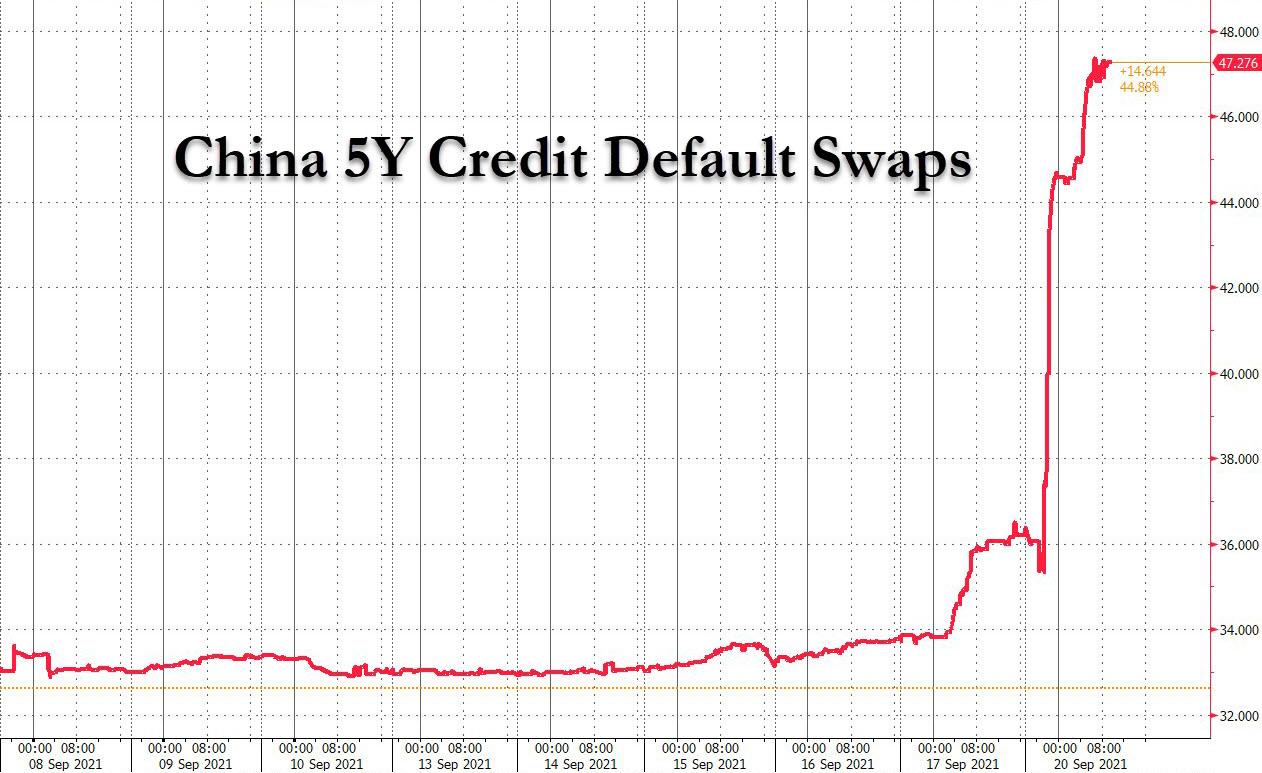

The Ultimate Contagion: China Sovereign Risk Is Starting To Blow Out

“Something historic will happen this week” was how we started to explain the process by which the collapse of Evergrande could spread contagiously across the world this week.

One glance at global markets this morning suggests, at a minimum, that risk is being de-grossed across everything from European utilities to cryptos to US materials stocks.

However, the biggest – and ultimate-est – contagion is that of China’s sovereign risk itself… and that is starting to blow out…

This sudden surge in default risk on China’s sovereign debt is very significant in the context of China’s constant reassurance to the rest of the world that it is solid-as-a-rock (just as Larry fink, but don’t ask George Soros). However, we do note that China CDS spiked to around 90bps in March 2020 (as the COVID crisis hit) and around 150bps in early 2016 (accelerating after China devalued the yuan in late 2015).

The question is, of course, where will this stop this time? How much ‘risk’ is China willing to take with its sovereign risk?

And Another: Shanghai-Based Property Developer Crashes 87% In Minutes Before It Is Halted

It’s not just Evergrande that is about to keel over. Overnight, one of its smaller peers, Shanghai-based Sinic Holdings Group which focuses on the development of residential and commercial properties in China, was halted trading after it shares cratered in a freak 87% plunge on Monday afternoon. The plunge slashed the market value to just under $230 million, which is laughable for a listed developer in the city.

There was no reason for the selloff – an officer at the firm’s Hong Kong office said there’s no one to attend to media inquires which is probably not a good sign – which was attributed to the general panic resulting from Evergrande’s imminent default, nor did the company give a reason for the trading halt in Hong Kong.

One thing was clear: selling volumes were off the chart, and as Bloomberg observes, the sudden selloff in the last two hours leading up to the suspension was accompanied by a surge in trading volume that was about 14 times its average in the past year. The liquidation may have been a margin call on a core shareholder who was forced to hit any bid, but we probably won’t know for a few days.

Unlike Evergrande, Sinic is not faced with an imminent default, but it does have a 9.5% $246 million bond due on Oct. 18 and Fitch Ratings revised its outlook to negative last week.

“It’s the same story as everywhere else — investors are concerned about the liquidity,” said Philip Tse, director and head of Hong Kong and China property research at Bocom International Holdings Co Ltd. “I think there are most likely some margin calls on some of the major shareholders” by looking at Sinic’s stock price pattern this afternoon.

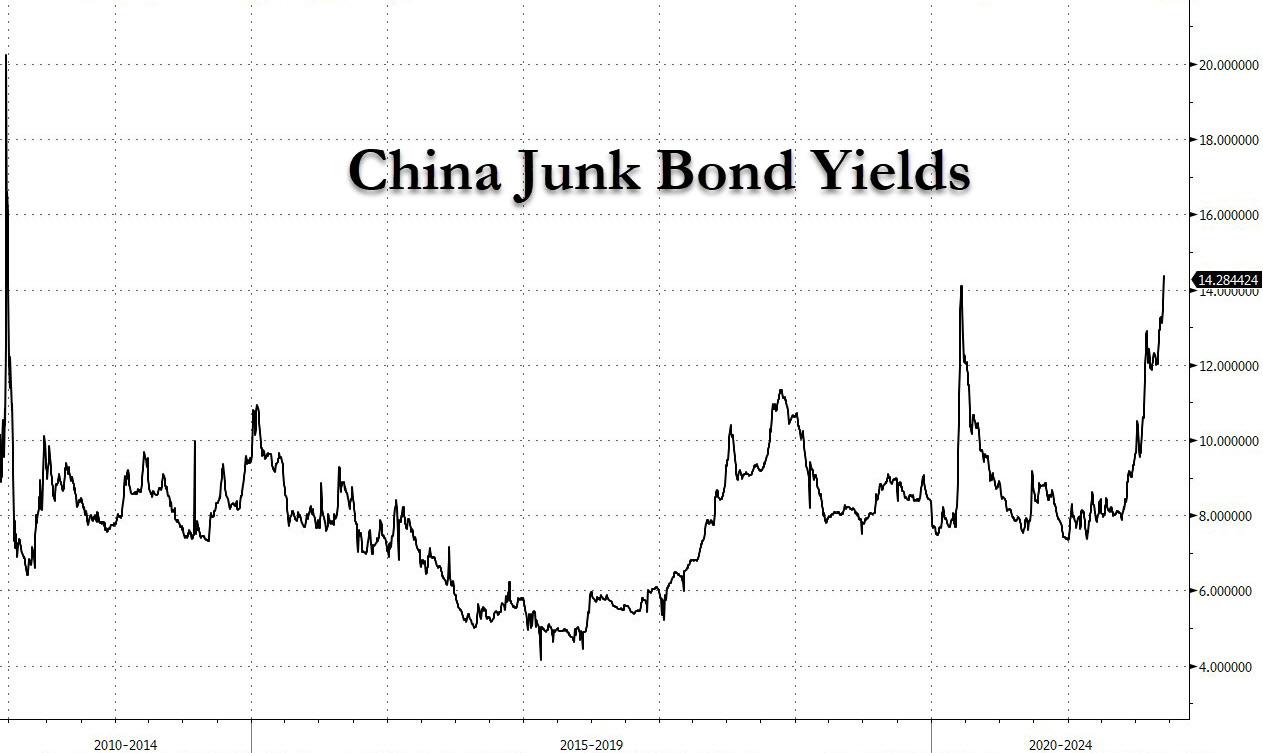

The crash came as Hong Kong’s property gauge plunged the most since May 2020 amid growing investor angst about China’s real estate crackdown and worries that Beijing may tighten grip on the city’s property sector in its “Common Prosperity” campaign. As discussed extensively last night, risk-off sentiment in financial markets exploded on Monday, with contagion from Evergrande spooking global markets, and as Chinese junk bond yields have soared to the highest level since 2011.

More ominously, even China’s CDS are starting to move sharply wider.

White House Finally Ends Ban On Travelers From EU & UK After 18 Months

Starting in November, any fully vaccinated traveler will able to visit the US from the EU and UK, according to Monday exclusive report from the FT.

The news briefly sent airline stocks like British Airways parent IAG (along with Lufthansa Air France and others) higher before they too succumbed to Monday morning’s broad-based global market selloff. The White House is expected to announce the official policy on Monday during a press conference.

Once it takes effect, the decision will mark the end of an 18-month blanket ban on travel between Europe & UK and the US (with certain exceptions for students etc.) first imposed by President Trump after he imposed a (more controversial though ultimately successfully prescient) ban between travel between China and US.

Patients who have received vaccines that are approved in the US but not Europe will be allowed to travel to the US, the Biden Admin sources say, while people participating in clinical trials for vaccines that are not yet approved in the UK will also be allowed to enter the US, a policy which will apply to roughly 40K people.

One of the FT’s sources said the new policy is part of a wider framework on travel. They added that hte Biden Administration is developing a system to cover all international travel that will replace the patchwork of bans and restrictions applying to different parts of the world.

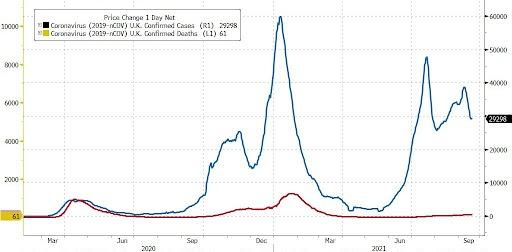

Both the US and EU have seen cases start to decline from their late summer peaks.

The UK has also seen cases decline from its recent peak, with deaths still relatively low.

Per the current policy, only American citizens, their immediate families, green card holders and those with national interest exemptions can travel to the US if they have been in the UK or EU in the previous 14 days.

The timing of the Biden Administration’s announcement is intended to coincide with the start of the first in-person UN General Assembly since the pandemic started.