Tesla Registrations Crash In California As Morgan Stanley Reiterates Underweight Over China Demand Tyler Durden

Wed, 06/17/2020 – 13:45

It was less than 24 hours ago that we were pondering why, exactly, Tesla would be slashing the price of its long range Model S by $5,000 heading into the end of the quarter. I mean, we knew the answer, but we had to ask anyway.

Regardless, it now appears we have our answer. Tesla registrations have plunged in California, a key market for the EV maker, over the last two months, according to research firm Dominion Enterprises.

Registrations were down 37%, combined, for April and May. California is Tesla’s largest market and the state saw registrations fall 16% in April before plunging 70% in May. There were 6,260 vehicles and 1,447 vehicles registered in April and May, respectively.

Across all of the states that Dominion tracks, including New York, Florida and Texas, registrations were down 33% to 14,151 vehicles.

The plunge paints a stark contrast to Tesla’s Q1 report, which had many on Wall Street speculating that the company wasn’t being dealt a meaningful blow from the coronavirus pandemic.

To add insult to injury, Tesla was also reiterated at underweight by Morgan Stanley on Wednesday morning on continued worries about demand in China. Less than a week ago, we highlighted that both Morgan Stanley and Goldman had downgraded Tesla shares.

Among concerns from MS analyst Adam Jonas at the time were capital needs and near-term demand – issues we feel like we have been hearing about for years, all the while Tesla stock has squeezed higher and higher.

“We’re Underweight due to our concerns around China, competition, capital needs and near term demand. The RR skew for TSLA is consistent with an Underweight rating,” the note read five days ago.

The company was separately downgraded to Neutral from Buy at Goldman Sachs after the stock shot past their price target.

Goldman said they remained positive on Tesla but that recent price cuts and production challenges with the Model Y could cloud the company’s near term outlook, despite issuing the downgrade in a broader note about its auto industry sales forecast, which has improved.

Goldman also cited valuation for its reasons to downgrade Tesla: “While Tesla has long been an expensive stock, and we recognize that valuation has expanded for the entire market, we believe that there is a higher bar for Tesla’s fundamentals than other stocks that may have challenging near-term results given Tesla’s premium absolute multiple along with the historical volatility of Tesla shares.”

Goldman was surprised by the company’s price cuts at the time: “Tesla recently cut pricing on several models (which we hadn’t anticipated occurring outside of the China market and consider to be a modest negative).”

At the same time, Goldman upgraded GM, who it said was “well positioned” for the U.S. pickup truck market and China’s recovering auto market.

via ZeroHedge News https://ift.tt/3ec6dUx Tyler Durden

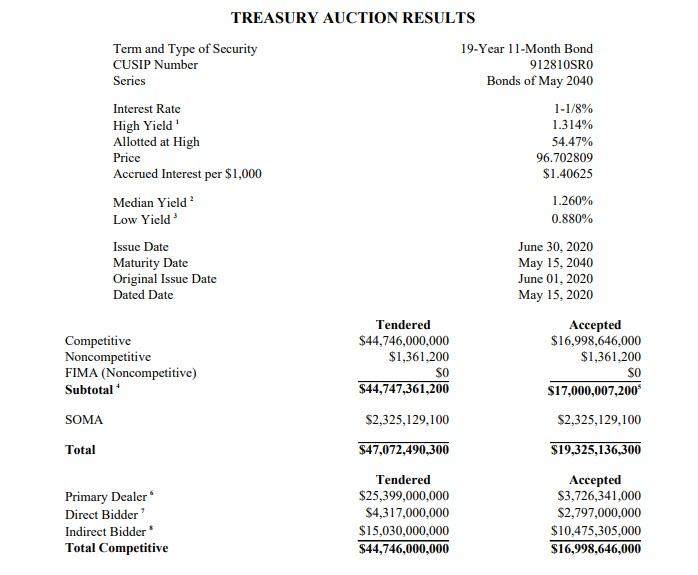

Blistering Demand In 20Y Treasury Auction; Stops Through By 1.5bps Tyler Durden

Wed, 06/17/2020 – 13:41

One month after the first 20Y auction in 34 years, priced at a yield of 1.22% amid surprisingly strong demand, moments ago the Treasury sold its second batch of the recently restarted 20Y Treasury in the form of a $17 billiion reopening of the original cusip (SR0), which priced at a high yield of 1.314%, which while higher than last month’s 1.22% yield was unexpectedly strong, stopping through the When Issued 1.329% by 1.5bps.

The auction metrics are as follows:

Bid to Cover: 2.63x, compared to 2.53x in the inaugural auction last month

Indirects: 61.6%, higher than last month’s 60.7%

Directs: 16.5%, also well above May’s 14.7%

Dealers: 21.9%, obviously lower than last month’s 24.6%

One potential reason for this is the recent selloff on the back end of the curve which has led to attractive concessions for foreign buyers, leading to the jump in the Indirect bid.

Of course, since there is just one auction in recent history to compare today’s auction to, superficially the auction was quite strong, although one look at the curve shows that the 20Y is somewhat “kinky” on the curve.

As a result of the surprisingly strong auction, the long-end of the curve found buyers, while the benchmark 20-year flipped 1 basis point richer on the session, and the 5s30s curve flattened back below 120bp after the results.

via ZeroHedge News https://ift.tt/3hB23Yr Tyler Durden

Fremdschämen is a noun of the German language. It translates this way:

Embarrassment for those incapable of feeling embarrassment.

Today we suffer embarrassment for Mr. Jerome Powell and his fellows of the Federal Reserve…

For no action they take lowers their heads in shame… or blushes their cheeks with embarrassment.

Mr. Powell is simply in the hands of Wall Street… and on his knees to Wall Street.

Well does he know the taste of shoeblack.

Yesterday Mr. Powell got a fresh coat on his tongue. Details to follow.

But first, let us look in on his masters…

A Banner Day on Wall Street

Wall Street was in full roar yesterday.

The Dow Jones jumped an additional 582 points. The S&P gained 58 points; the Nasdaq, 169 points of its own.

CNBC, by way of explanation:

Stocks rose on Tuesday as a record jump in retail sales — coupled with positive trial results from a potential coronavirus treatment and hopes of more stimulus — sent market sentiment soaring.

Government number-torturers reported yesterday morning that May retail sales jumped a record 17.7%.

The chronically erring Dow Jones survey of economists had projected a 7.7% increase.

Yet we are not surprised by the surge. April’s numbers were true abominations. But certain economic restrictions were waived in May.

A trampolining back was therefore expected.

Meantime, a medicine named dexamethasone – a widely available medicine – is evidently effective in the treatment of deathly ill coronavirus patients.

It reportedly axed hospital deaths by perhaps one-third.

Thus the market had its spree yesterday. But it merely added to Monday afternoon’s joys…

Powell Licks Wall Street’s Shoes

The Dow Jones had been off 762 points in early trading Monday, quaking with coronavirus-related fear.

But then Mr. Powell sank to his knees… and tongued Wall Street’s wingtips…

For the Federal Reserve announced it intends to purchase individual corporate bonds — not merely ETFs.

By its own admission, it will:

Begin buying a broad and diversified portfolio of corporate bonds to support market liquidity and the availability of credit for large employers.

We will not burden you with the plan’s intricacies. You need only know this:

Monday’s announcement “pressed the risk-on button,” as money man Bill Blain styles it…

“Central Banks Are Now de facto Guarantors of the Corporate Bond Market”

Fears about the rising number of reopening coronavirus hotspots and economic threats were superseded by unbounded joy as the Fed announced it will buy secondary market corporate bonds direct[ly] rather than through ETFs, without any need for companies to certify their eligibility. That pressed the risk-on button — and markets recovered.

And so the free market sinks deeper into oblivion:

Central banks are now de facto guarantors of the corporate bond market.

What has all this QE Infinity and ZIRP interest rates created?… Where market prices have become meaningless as a result of financial asset inflation? Where junk bonds are priced like AAA securities, allowing private equity funds to thrive?

I am beginning to wonder if there is any point in thinking about markets any more… Just follow the central banks… don’t think. Just buy.

“Don’t think. Just buy.”

We think the proper advice might rather run this way: “Don’t buy. Just think.”

Yet we do not dispense financial advice.

Picking Winners and Losers

Our own Nomi Prins penetrates to the core of yesterday’s message. Nomi rings dead center when she says:

As if the Fed hasn’t done enough to destroy honest markets, now it plans to start buying individual corporate bonds. It’s just another step closer to the Fed deciding the winners and losers in the market.

Thus the Federal Reserve is a referee who has taken a bribe, a butcher who thumbs the scales, a rogue, a traitor to justice.

A central banker with a conscience might lower his head in shame… and a red flush of embarrassment might stain his cheeks.

Yet Mr. Powell holds his head high and puffs his chest, proud as any peacock.

His cheeks, meantime, are pale.

Yet ours are scarlet — scarlet with embarrassment for the man incapable of embarrassment.

“From Lender of Last Resort to Stockjobber”

The Federal Reserve was originally fashioned to be the “lender of last resort.” Yet that designation is presently a cruel and mocking jest.

It has passed from lender of last resort to stockjobber.

Economist Thomas M. Humphrey is the author of Lender of Last Resort: What It Is, Whence It Came, and Why the Fed Isn’t It.

From which:

While there exists such an entity as the classical lender of last resort (LLR) — the traditional, standard LLR model, to be exact — the Fed has rarely adhered to it… The Fed has deviated from the classical model in so many ways as to make a mockery of the notion that it is an LLR. In short, the Fed may be many things, crisis manager included. But it is not an LLR in the traditional sense of that term.

What is the proper function of the central bank, by Humphrey’s lights?

Six Mandates of Sound Central Banking

As summarized by Wikipedia, a central bank exists to:

(1) protect the money stock instead of saving individual institutions;

(2) rescue solvent institutions only;

(3) let insolvent institutions default;

(4) charge penalty rates;

(5) require good collateral; and

(6) announce the conditions before a crisis so that the market knows exactly what to expect.

A word of explanation, perhaps, on “penalty rates.”

The central bank should charge interest rates above the market rate.

Otherwise the central bank would be a lender of resort — not the lender of last resort.

A high rate further encourages debtors to retire their debts rapidly… to shake loose the heavy burden as soon as circumstances allowed.

Yet what does the Federal Reserve’s actual record reveal?

(1) “Emphasis on credit (loans) as opposed to money,”

(2) “taking junk collateral,”

(3) “charging subsidy rates,”

(4) “rescuing insolvent firms too big and interconnected to fail,”

(5) “extension of loan repayment deadlines,”

(6) “no pre-announced commitment.

Professional Incompetence

That is, the Federal Reserve takes sound central banking and knocks it 180 degrees out of phase.

It wars against all six mandates — and massively against Nos. 1, 2, 3, 4 and 5.

Imagine a plumber who does not patch leaks but creates leaks… a doctor who does not mend bones but cracks bones… a head shrinker who does not shrink heads but expands heads.

Now you have the flavor of it.

Yet the Federal Reserve’s professional pride is unruffled. It displays no embarrassment, no shame at a job done wrong.

In fact, it believes it is a job done right…

via ZeroHedge News https://ift.tt/2UURWnv Tyler Durden

NORAD Jets Scrambled In 8th Russian Bomber Intercept Off Alaska This Year Tyler Durden

Wed, 06/17/2020 – 13:05

At a moment “World War 3” happens to be trending on Twitter, there’s been another major US-Russian ‘intercept’ incident of Alaska’s coast.

For those keeping count, Tuesday’s night’s intercept involving NORAD F-22 Raptors and others including KC-135 Stratotankers and US surveillance aircraft marks the eighth such incident involving Russian planes coming close to North American airspace this year alone.

NORAD F-22 Raptors, supported by KC-135 Stratotankers and an E-3 Airborne Warning and Control System, successfully completed two intercepts of Russian bomber aircraft formations entering the Alaskan Air Defense Identification Zone last night. pic.twitter.com/9iSZK0Vu2F

— North American Aerospace Defense Command (@NORADCommand) June 17, 2020

It also marks the fourth wave of Russian bombers making an approach near Alaska in a mere week.

“NORAD F-22 Raptors, supported by KC-135 Stratotankers and an E-3 Airborne Warning and Control System, successfully completed two intercepts of Russian bomber aircraft formations entering the Alaskan Air Defense Identification Zone last night,” the North American Aerospace Defense Command (NORAD) said in a tweet.

Like a similar incident a week ago involving two waves of four Russian aircraft each, including long-range Tu-95 nuclear-capable bombers, this latest intercept involved a significant group of multiple aircraft, among them Su-35 fighter jets and a Russian surveillance plane.

“For the eighth time this year, Russian military aircraft have penetrated our Canadian or Alaskan Air Defense Identification Zones and each and every time NORAD forces were ready to meet this challenge,” NORAD Commander General Terrence J. O’Shaugh said in a statement.

The Russian warplanes reportedly stayed in international airspace, but came within just over 30 miles of US territory, according to reports.

The tense encounters are becoming more frequent of late, not only over the Bering Sea, but over the Mediterranean, Baltic, and Black Sea regions as well.

via ZeroHedge News https://ift.tt/3hBukxP Tyler Durden

The BBC’s correspondent in China has warned that the communist government may be in the midst of a second coronavirus cover up, as a massive police and medical response to a new cluster in Beijing doesn’t tally with the reported number of cases.

The Chinese government has locked down the capital city, instituted travel bans, and is rounding up residents, putting them on buses and placing them in quarantine:

The footage was shot by activist Jennifer Zeng, who claims that seven hotels in the city were requisitioned by the government to be used as quarantine sites.

However, Beijing only reported 27 new infections yesterday, and 106 in the past five days, prompting many to wonder, just what the hell is going on here.

More footage shows hundreds of people lining up outside Youan hospital in Beijing for virus screening:

Massive amounts of fruit and vegetables have been discarded after Beijing shut down Xinfadi wholesale market:

Earlier in the week huge amounts of police were deployed to the market:

The BBC’s Stephen McDonell noted that the Chinese government is either being “super cautious”, or they are again not giving accurate figures on the new infection rate.

#Beijing Govt spokesman Xu Hejian described the city’s #coronavirus situation as “extremely severe”. That either means the relatively low infection tally doesn’t reflect the facts on the ground or they’re being super cautious, trying to mobilise the population to stop the spread

In terms of new #coronavirus measures: #Beijing residents from “high risk” groups are not allowed to leave the city (I guess that means living near/ contact with XinFaDi Market) . Taxis and Didi cars are also not allowed to leave the city limits.

Practically speaking it’s now very difficult for anyone to leave #Beijing. The Chinese capital is going into a #coronavirus prevention bubble. 1255 flights were cancelled this morning. That’s 70% of all flights in and out of #Beijing. #China#coronavirus

So that’s from 50+ days with zero #coronavirus cases in #Beijing to 137 official* infections with symptoms in 6 days and the Chinese capital is now being effectively cut off from everywhere else. Four other provinces have reported cases emanating from #Beijing’s #XinFaDi Market.

Owners of the market that was shut down in Beijing are reportedly claiming that the ‘more infectious’ strain of the virus came from Europe via some dodgy salmon, however the Chinese Centre for Disease has said there is no evidence to support the claims.

If this fresh outbreak is ‘very severe’ as authorities are claiming, then where are the infected?

Will Europe move to block flights coming from China this time, or once again allow transmission of the virus unhindered?

One more intriguing theory of what is happening comes from professor Steve Tsang of the School of Oriental and African Studies, who has contended that China is using Covid-19 to ‘divide and conquer’ Europe.

“China is essentially trying a divide and rule approach to the EU,”Tsang told the Daily Express, adding “Some of the EU countries are being enticed to be much closer to China and to break away from European norms. And that is a serious problem.”

China has sent coronavirus aid to countries that have not received it quickly enough from the EU.

“The pandemic hasn’t helped but the problem with the pandemic is not so much in eastern European countries as it is with Italy.” Tsang added.

Since 2012, China has heavily invested in the infrastructure of 17 eastern and central European countries, including the likes of Hungary and Greece, via the Belt and Road Initiative.

Many see this as a way of exerting dominance in global trade. With the emergence of the Covid-19 pandemic, and the lax response of the EU in helping its member states, China has everything to gain.

via ZeroHedge News https://ift.tt/2C9q3S2 Tyler Durden

Facebook ‘Solves’ Censorship Controversy By Allowing Users To Block All Political Ads Tyler Durden

Wed, 06/17/2020 – 12:31

As controversy rages over major social media platforms intervening when it comes to users expressing political viewpoints, and with the Trump administration lately escalating its burgeoning feud with Silicon Valley over tech giants’ “liability shields”, Facebook has announced it will now allow users to block political ads altogether.

The decision comes amid pressure especially from Democrats and the Left to get Facebook to fact-check political ads to root out alleged “disinformation”. Instead the company has opted to roll out a feature allowing its some two billion individual users to essentially turn off or mute“all social issue, electoral or political ads from candidates and Super PACs.”

The ‘opt out’ feature will be available on Instagram as well, and seeks to ease the pressure of the question of social media platforms becoming ‘arbiters of truth’. The move is a huge defeat for the Biden campaign, which called for censoring political posts nebulously deemed “disinformation” and “offensive”.

AFP via Getty

The Biden campaign previously urged Facebook to “proactively stem the tide of false information” in an open letter to CEO Mark Zuckerberg, including fact-checking political ads two weeks head of any election.

Facebook has been resistant to this call, with the new feature unlikely to satisfy Democrats seeking to shut down what they see as pro-Trump “disinformation” as well as conservative sources.

Starting today for some people and rolling out to everyone in the US over the next few weeks, people will be able to turn off all social issue, electoral or political ads from candidates, Super PACs or other organizations that have the “Paid for by” political disclaimer on them. You can do this on Facebook or Instagram directly from any political or social issue ad or through each platform’s ad settings.

But no doubt there will further be controversy over what constitutes “political”.

The company says users will be able to ‘flag’ content they think is political but still made it through the filters: “if you’ve selected this preference and still see an ad that you think is political, please click the upper right corner of the ad and report it to us,” the statement added.

The feature will be available for some users starting as early as Wednesday.

via ZeroHedge News https://ift.tt/3hGp7VQ Tyler Durden

The next iteration of monetary policy may well be “yield curve” control?

Debt and interest rates have become the predominant driving force of our economy. Unfortunately, a majority of the debt is unproductive, resulting in declining long-run economic and productivity growth rates.

In the 1950s, each dollar of debt drove nearly 70 cents of economic growth. It has fallen ever since. Recently, each dollar of debt bought less than 30 cents of growth. That number has deteriorated further in the last few months.

The Fed, as manager of monetary policy, can use policy to either encourage long term prosperity or shorter-term economic activity. They have chosen the latter and, as a result, have dug themselves into quite a hole. Each dollar of debt drives less growth than the prior dollar of debt, thus requiring even more debt.

This article explores Yield Curve Control (YCC), a policy tool at the Fed’s disposal to keep digging even deeper into the hole.

The Hole

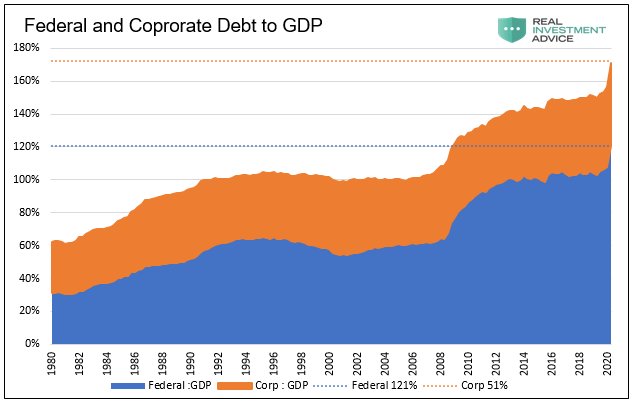

Government and corporate debt levels are currently increasing at unprecedented rates. Total non-financial debt rose nearly 12% in the first quarter. The amount will surely be much higher when second-quarter data is released.

The federal deficit in the current fiscal year is expected to top $4 trillion. To put that in context, it took 192 years between 1789 and 1981, for America to amass its first $1 trillion of debt.

Only halfway through the year, corporations exceeded $1 trillion of issuance, putting them on par with annual totals from the prior few years.

The graph below shows the ratio of non-financial corporate debt and federal debt to GDP. They both sit at record levels and will rise rapidly when second-quarter GDP is released.

As the ratio of debt to GDP increases, even more debt is needed tomorrow just to maintain current economic activity. For a Fed overly concerned about short-term economic activity, this dilemma creates a self-reinforcing problem. The situation is akin to a Ponzi scheme that needs constant feeding.

Given the Fed’s desire to avoid the slightest economic setback, surging debt levels means the Fed will have to become even more creative and active in managing interest rates. Are they prepared to impose negative interest rates on U.S. society? Although that tactic has been remarkably unproductive in Europe and Japan, the Fed has not formally ruled out negative rates.

Keep Digging

Fed Funds are at zero, and the Fed has not committed to negative interest rates. What else can the Fed do to keep debt flowing?

The Fed sets short term rates but can only indirectly influence long-term rates. Longer-term rates spanning from two-year maturities out to thirty years drive borrowing and consumption.

Quantitative Easing (QE) was introduced in 2008 when the Fed Funds rate hit zero. QE allows the Fed to purchase bonds in an effort to lower interest rates for longer-term maturities. During QE 1, 2, and 3, they bought Treasuries, mortgages, and agency bonds. Despite what one would think, on each occasion, longer-term rates rose. In the last month, they expanded their reach to include large-scale purchases of municipal bonds, corporate debt, and even junk-rated corporate bonds and ETFs.

Steering rates and setting rates are not the same. The question for the Fed is, how can they control interest rates for longer-term securities?

Yield Curve Control – A Bigger Shovel

QE 1, 2, and 3 ran systematically. The Fed set a predetermined amount and timing of QE in which to operate. It was useful in reducing the supply of Treasuries available and forcing investors into riskier assets like junk bonds and stocks. However, it did not allow the Fed to explicitly control the level of interest rates.

The Fed is now considering an enhancement to the way it manages QE. The “upgrade” is called yield curve control (YCC). YCC essentially allows the Fed to do unlimited amounts of QE with no time restraints. Embedded in YCC is the specific goal of targeting particular interest rates across the entire yield curve.

For example, assume the Fed set a 0.75% target yield on the 10-year U.S. Treasury note. They can then employ QE in any amount needed to buy 10-year notes when the rate exceeds that level. If successful, the rate would never exceed 0.75% as traders would learn not to fight the Fed.

It is essential to be clear about the definition of YCC. The Fed represents it as an option for helping them manage the economy through the difficulties the country currently faces. However, YCC is a euphemism for price controls. Price controls are government interference and regulation, establishing prices for specified goods and services.

In this instance, we are talking about the most fundamental component of any economic system, the price of money. Historically, in every case, the implications of price controls have been unfortunate.

Two examples of price controls leap out from recent history:

Those imposed on gasoline during the Arab oil embargo in 1973 and 1974 that created long lines of cars waiting to fill up at gas stations

Those set on electricity in the state of California, which contributed to rolling blackouts

Managing the Yield Curve

It is called yield curve control because the central bank effectively manages the shape of the yield curve. A steeper yield curve benefits the banks as they tend to borrow short term and lend long term. Larger profit margins increase their desire to lend and therefore stimulate debt-driven economic activity. Conversely, a flatter or inverted yield curve inhibits lending due to narrower bank profit margins, and consequently, it curtails debt issuance and economic activity.

The problem for the Fed is how they can steepen the yield curve to stimulate lending without letting longer-term rates rise too much? Under YCC, they may squirm out of one trap only to find themselves in a bigger trap.

History

The Fed would not break new ground with YCC. In fact, they would be reinitiating a previously used tactic. From 1942 to 1950, the Fed targeted rates to help manage funding costs for WWII. If you are interested in reading more on the U.S. experience with YCC, we suggest the following article from the Federal Reserve: How the Fed Managed the Treasury Yield Curve in the 1940s.

It is worth pointing out that after WWII ended, inflation spiked to double digits, yet the Fed held interest rates at artificially low levels. While bondholders may not have lost money on the bonds per se, they did lose dearly in their purchasing power, as shown below.

More recently, in 2016, Japan set a 0% yield target on its ten-year note. Currently, the bank of Australia is now targeting 0.25% for its three-year bond.

Summary

Federal Reserve Bank of New York President John Williams says that policymakers are “thinking very hard” about targeting specific yields on Treasury securities. Given what we have observed, it seems likely they will implement YCC and, in doing so, choose to keep digging and try to push problems out further into the future.

The problem with these actions is they engender anemic rates of economic growth. Equally concerning, they directly contribute to income inequality, a driving force for social unrest.

The policies the Fed staunchly defends are adverse to the healthy economic and social environment the country so desperately needs. While in crisis mode, investors will cheer them on unaware of the adverse effects it will have on the economy. As they say, there is no such thing as a free lunch.

via ZeroHedge News https://ift.tt/37FdUAg Tyler Durden

UK Prime Minister Boris Johnson In Car Wreck After Convoy “Targeted By A Protester” Tyler Durden

Wed, 06/17/2020 – 11:47

Given the world beheld scenes last week of Black Lives Matters protesters overrunning parliament square in London while vandalizing and defacing statues and monuments ranging from war memorials to Winston Churchill to even an Abraham Lincoln statue, with police appearing at times to sit back at let the destruction happen, it was only a matter of time before something like the below.

UK Prime Minister Boris Johnson was involved in a car wreck whena protester ran out in front of the convoy as it departed Westminster on Wednesday.

The whole dangerous close call in which Johnson escaped unscathed was caught on video and happened in broad daylight. There were no reports of injuries despite clear damage to the vehicle carrying the prime minister.

The prime minister’s convoy had been making the short drive to Downing Street when the accident happened.

Though one man is seen darting in front of the cars as they turned onto the street, reportedly a Kurdish protester demanding British action against Turkey, some reports suggesteda group of demonstrators had surged toward the convoy just before the accident.

Boris Johnson’s vehicle after a collision as it departed the Houses of Parliament Wednesday, via Reuters.

Sky News reported that Johnson’s car had been “targeted by a protester” in an attempt to draw as much attention as possible.

The prime minister’s office confirmed that Johnson had indeed been inside the car, but that he was unhurt. “Yes, that was the PM’s car,” a spokesperson said. “I think the video speaks for itself as to what happened. No reports of anybody being injured.”

Media reports described a “minor fender-bender” but video showing a closer side angle reveals Johnson’s car suffered severe impact.

Downing St says there are no reports of injuries after Prime Minister Boris Johnson’s car was involved in a collision outside parliament as it left the gates following PMQs.

A different angle shows that while damage was relatively minor, Johnson’s car was hit with significant impact.

Police immediately jumped on and apprehended the man seen charging the convoy to cause the wreck.

With over the past weeks various protests outside of key government buildings in both the UK and US getting increasingly out of control, and turning into chaotic scenes of rioting and vandalism, this latest incident is perhaps a ‘wake-up’ call for police at such sensitive sites to get the situation under control.

via ZeroHedge News https://ift.tt/30NEbLf Tyler Durden

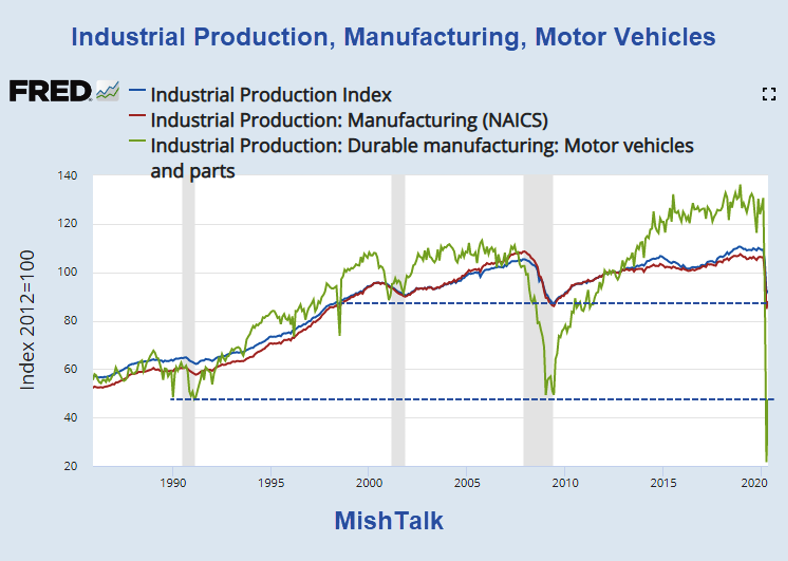

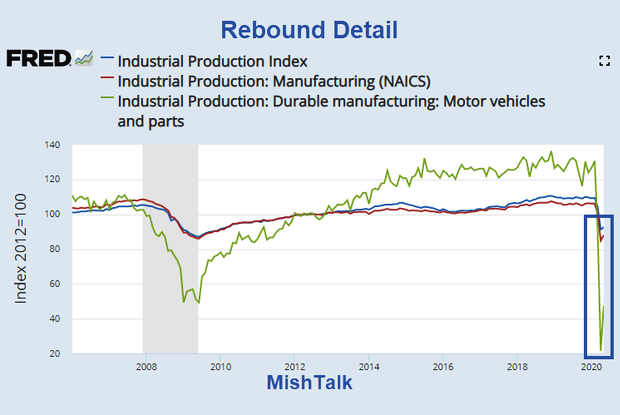

Industrial production increased a weaker than expected 1.4% in May. The Econoday consensus was 2.9%.

A negative revision took April from -11.2% to -12.5% so essentially there was no rebound at all.

Industrial production in May was 15.4% below its pre-pandemic level in February.

Manufacturing output rose 3.8% in May but languishes near the lows in the Great Recession.

At 92.6% of its 2012 average, the level of total industrial production was 15.3% lower in May than it was a year earlier.

Capacity utilization for the industrial sector increased 0.8 percentage point to 64.8% in May, a rate that is 15.0 percentage points below its long-run (1972–2019) average and 1.9 percentage points below its trough during the Great Recession.

Manufacturing and Motor Vehicles and Parts

Motor vehicles and parts production has “rebounded” to a level “below” the bottom of the 1990 recession.

Manufacturing is at a 1988 level

Rebound Detail

V-Shape Recovery?

These numbers are not remotely close to anything one would ever associate with a V-shaped recovery.

Pepsi Retires Aunt Jemima Brand Due To “Racist Past” Tyler Durden

Wed, 06/17/2020 – 11:09

Aunt Jemima survived 130 years: the Great Depression, two World Wars, the Civil Rights movement, Vietnam and 9/11. But the brand has finally been cast aside by Quaker Oats – which is owned by Pepsi – due to its “racist past” at the hands of today’s relentless cancel culture.

PepisCo’s packaged-foods unit said Wednesday it would remove imagery of the black woman from the Aunt Jemima brand’s pancake mixes, syrups and other products, and change its name. The company didn’t disclose the new name, but said packaging changes will appear throughout the fourth quarter.

The company told CNN: “As we work to make progress toward racial equality through several initiatives, we also must take a hard look at our portfolio of brands and ensure they reflect our values and meet our consumers’ expectations.”

The appearance of Aunt Jemima has changed over the years, the article notes. Its name is “based off the song ‘Old Aunt Jemima’ from a minstrel show performer and reportedly sung by slaves,” according to CNN. The logo was based on Nancy Green, who was a cook and missionary worker that NBC later disclosed had been born into slavery.

“We recognize Aunt Jemima’s origins are based on a racial stereotype. While work has been done over the years to update the brand in a manner intended to be appropriate and respectful, we realize those changes are not enough,” said Kristin Kroepfl, chief marketing officer at PepsiCo’s Quaker Foods North America business. The unit also sells Quaker Oats and Rice-A-Roni.

Despite its iconic history, there have been recurring calls to change the logo for years, with Cornell University professor Riché Richardson one of the latest voices to speak out against it in 2015. He called the logo “very much linked to Southern racism.”

He also said the logo was based on a “devoted and submissive servant who eagerly nurtured the children of her white master and mistress while neglecting her own.” In 2017, the husband of B. Smith called the logo the epitome of “female humiliation.”

But today the brand is just described by the company as standing for “warmth, nourishment and trust — qualities you’ll find in loving moms from diverse backgrounds who want the very best for their families.”

Gladys Knight was even a spokesperson for the brand in the 1990s, during such time the logo evolved. But that apparently is woefully insufficient in this day and age. Quaker Oats said: “While work has been done over the years to update the brand in a manner intended to be appropriate and respectful, we realize those changes are not enough.”

So it’s best to simply deleted over a century of history and pretend it never existed.

Additionally, the company announced that the Aunt Jemima brand will donate $5 million over the next five years “create meaningful, ongoing support and engagement in the Black community.”

As one user on social media pointed out, the lag time from satire to reality has sadly now become just 5 days.

{kind=link}

{kind=link}