The Retail Daytrading Euphoria Has Finally Peaked: Here Come The Sellers Tyler Durden

Wed, 06/17/2020 – 09:58

In the latest installment tracking the retail euphoria phase of the bubble now known by everyone as “Jay’s Market” (recall that for much of the past decade, the recurring complaints among bulls was that there was zero retail participation so it wasn’t really a bull market, well… how about now), Bloomberg profiles not the now infamous Robinhood trading platform which has emerged as the “battleground” for an entire generation of 10-year-old traders, but rather its derivative – the website that tracks the action on Robinhood and which we have frequently used to show recent moves and changes in retail trading momentum: Robintrack.

As Bloomberg reports this morning, RobinTrack – which is not affiliated with the Robinhood investing app, but uses information gleaned from it to show trends in positioning among the brokerage’s users – is a two-year old product of Casey Primozic, “who was wrapping up his undergraduate years at Valparaiso University in Indiana. He was also building a website — for fun. Little did he know it would grow into a Wall Street obsession.”

Now in 2020, his college side project, Robintrack.net, has seen site traffic explode as everyone from day traders to institutions flock there for a picture of what retail investors are buying. Primozic says there’s evidence hedge funds are scraping his data. The 23-year-old programmer can hardly keep up with an overflowing email inbox and is getting barraged with pitches from advertisers.

Why is Robinhood – and by extension Robintrack – so popular among trend watchers? Because “no other brokerage provides this data publicly and directly – making Robinhood users a proxy for all individual investors.”

Robinhood displays stock ownership data publicly for informational purposes, according to a company spokesperson.

… the result has been a reflexive cottage industry of Robinhood “analyst”, or as Peter Tchir, head of macro strategy at Academy Securities says, there’s a “cult of Robinhood watchers developing.”

Anywhere between 20,000 and 50,000 unique users now visit Robintrack on an average day, according to Primozic. Before this year, a typical day would only see up to 4,000 visitors. In the seven days before Monday, the website attracted 167,000 unique users and 286,000 separate sessions. The spike began back in late April, as Robinhood users piled into the United States Oil Fund LP (USO) amid negative crude prices.

On the other hand, as SocGen quant Andrew Lapthorne wrote in a note Monday: “The number of ‘odd’ trades coupled with the availability of Robinhood data via Robintrack.net, has increased the noise level.” Yet in world where markets make no sense, coupled with their own reflexivity, the noise generated by millions of retail daytraders chasing momentum is neatly repackaged as “big data” (i.e. trends and paterns), as “strategists” seek to justify investing theses based on what a bunch of teenagers are buying or selling at any given moment:

Primozic has had to make a couple changes to the site’s operations to keep up with the overflow. Visitors to the site aren’t just perusing. Rather, many are pulling the available data into their own programs.

“These days, especially, there’s at least three or four people who will run these scrapers at any given time,” he said. “I’ve actually had to limit the rate at which they can do it just to prevent them from overloading my hardware.”

So starved is Wall Street for noise signal that according to Primozic, there is “evidence that users at hedge funds including D.E. Shaw & Co. and Point72 have looked into or are directly collecting data from Robintrack. Representatives of the firms declined to comment on whether they’re plugging into Robinhood.”

I’ve confirmed one more hedge fund to be looking into Robintrack data: Capital Fund Management from Paris.

That brings the total up to 4 so far: D. E. Shaw, Point72, Two Sigma, and CFM

In case you were wondering if this data is useful, here’s proof the pros are interested too! pic.twitter.com/7EXDKSUEpD

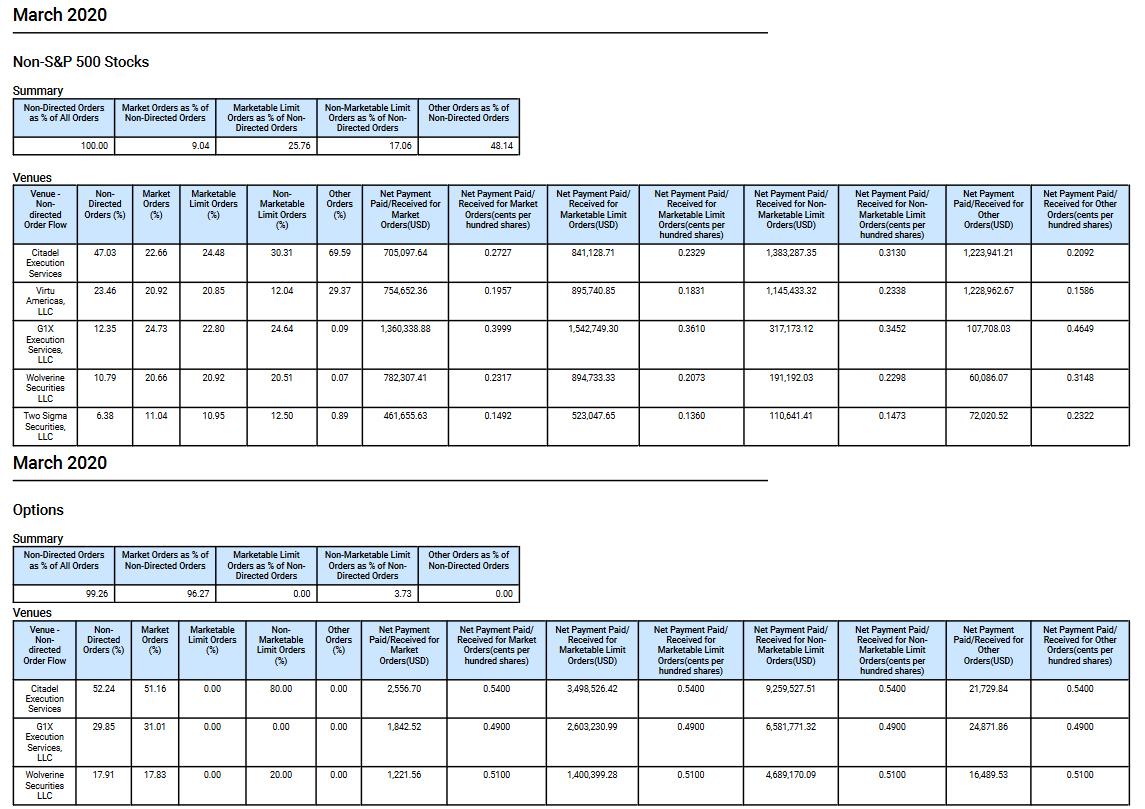

What was left unsaid by the Bloomberg expose (and we may have an idea why) is that by the time the RH trade data hits Robintrack, it’s extremely stale and virtually non-actionable except for those looking at very big picture trends (on Wall Street nanoseconds matter – minutes do not) which is why HFT firms pay tens of millions in dollars to Robinhood every month for its orderflow enabling the “free brokerage” model in the first place– to have real-time access and in some unspoken cases to frontrun, the massive retail orderflow.

Below is an example of how much various HFT venues paid Robinhood in March alone to “execute” its stock and option trades, based on the company’s latest 606 statement.

It goes without saying that if firms are paying millions for this orderflow, one can be absolutely certain that they are making hundreds of times more in revenue on the same Robinhood data.

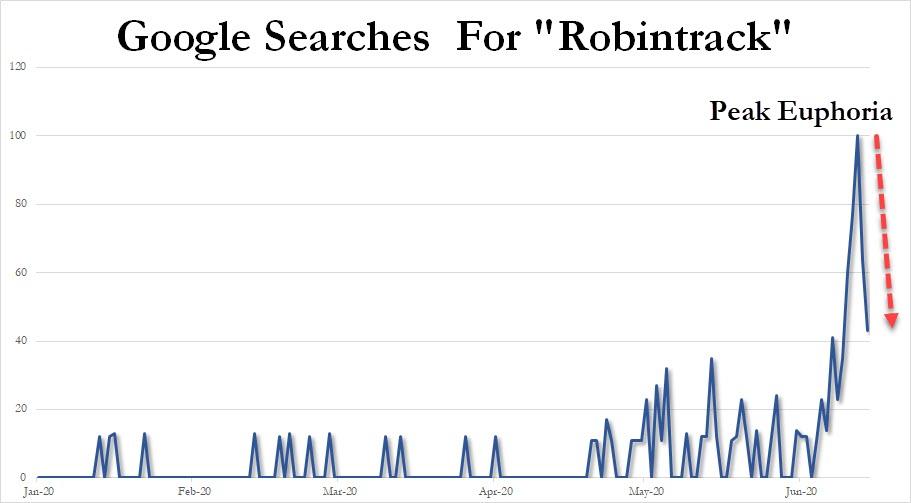

Yet if Robintrack is a first derivative of Robinhood, which in turn is a derivative of overall retail euphoria in the market, then traffic and search interest in Robintrack is a second derivative, and based on Google searches for Robintrack, the retail euphoria peaked some time last week – probably around the time bankrupt HTZ market cap hit $900 million, and is finally rolling over.

Remember: Robinhood – and retail daytrading in general – is all about momentum, and it just turned down.

Perhaps the government stimulus money that millions of bored Millennials and teenagers were using to fund their trading accounts h as finally ran out?

Whatever the case, as retail investors realize that upside momentum is suddenly missing – and one look at HTZ stock shows that last week’s upside insanity is long gone – watch as the euphoric scramble ensues in reverse, and all those trading warriors who were buying suddenly turn sellers as even retail investors realize that once the euphoria peak is behind us, those who sells last are the biggest losers.

via ZeroHedge News https://ift.tt/30Snj5N Tyler Durden

On Tuesday, Federal Reserve Chairman Jerome Powell testified before the Senate Committee on Banking, Housing, and Urban Affairs.

It was classic Fed “open mouth operations” as Powell tried to talk up the central bank’s policies and assure everybody that everything is under control. But is it, really?

Peter Schiff hit some of the highlights of Powell’s testimony during his podcast.

The stock market is way up. The unemployment situation is better than expected. (At least that’s the mainstream view.) There are signs that the economy is rebounding from the government shutdowns. Why is the Fed still upping the ante on its monetary stimulus?

Powell gave us a hint. He insisted the central bank is not “an elephant running through the bond market” but said they felt they had to “follow through” and buy bonds because the plan was announced in March.

In the first place, as Peter points out, when Powell claims the bond-buying program isn’t really impacting the market, he’s blowing smoke. The whole point of the program is to impact the market.

Well, if the Fed wasn’t having an impact on the market, then why do it? The purpose of this program is to impact the market. Otherwise, the Fed would not be doing it, if it had no impact.”

As far as feeling obligated to follow through on its promise to buy corporate bonds, Peter asks the poignant question – why?

It really shows you that the Fed is beholden to Wall Street speculators. Those are the ones who are counting on the Fed buying those bonds. Because they already bought those bonds. They front-ran the trade. As soon as the Fed announced its intention to buy corporate bonds, what did speculators do? They ran into the market and bought up corporate bonds and bid up their prices. So, now you have a bunch of overpriced corporate bonds. And how do these speculators get out? They sell to the Fed. That’s the reason they bought — so they could sell to the Fed. And now the Fed is coming forward and saying, ‘Well, even though the prices have gone way up, they’re not way down where they were when we said we were coming to the rescue, even though we’ve had this recovery in the markets, we’re going to buy them anyway because we made a commitment.’ So, what they’re saying is they want to honor their commitment to the speculators. They want to make sure the people who followed the Fed’s advice get rewarded.”

The central bankers know they need those speculators so they can talk up the markets.

It wants speculators to know that when the Fed says something, it means something, so its ‘open mouth operations’ actually have teeth. Because if the Fed didn’t follow through, then the next time they cried wolf, nobody would come running and buy those bonds.”

This reveals what the Fed’s monetary policy is really all about. It’s not about the economy. It’s about propping up Wall Street.

Powell also said he’s not concerned about inflation because the Federal Reserve knows what to do if inflation becomes a problem. But as Peter said, knowing what to do and doing what you know are two different things.

Yes, the Fed knows what to do. Raise interest rates sharply and shrink your balance sheet, right? Contract the money supply. Sell Treasuries. Sell corporate bonds. Take money out of the economy and sell the assets you bought to expand the money supply and jack up interest rates. Is the Fed going to do that? Not a chance! What would happen if the Fed did that? The economy would crash like it’s never crashed before. So, the Fed knows how to fight inflation. It just knows that it can’t fight inflation with what it knows. Because it also knows what it will do to the bubble that it inflated.”

We have said the Fed doesn’t have an exit strategy. Powell so much as admitted this when Sen. Robert Kennedy asked how the central bank plans to shrink its balance sheet to a level that isn’t “other-worldly.” In fact, the chairman actually laughed at the question and then talked about “the peaceful period” from 2014-2017 when the Fed just froze the size of the balance sheet, letting the economy grow into it.

His entire plan to shrink the balance sheet is to stop growing the balance sheet and hope the economy continues to grow so that whatever the balance sheet is when he stops expanding it, it becomes a smaller percentage of the economy. Basically, he’s saying the balance sheet is never going to shrink in actual terms. It’s never going to go down.”

Keep in mind, when the Fed started trying to normalize after the ’08 crisis, the markets went into convulsions.

Powell is really admitting again, as if people didn’t know by now, I mean, how many times do you got to be hit on the head, that this is QE infinity, that the Fed’s balance sheet is never going to shrink.”

It was the anticipation of normalization that caused the dollar to bounce back and gold to sell off after the 2008 crisis.

That whole bubble, that whole recovery was predicated on the ability of the Fed to shrink its balance sheet and normalize interest rates. Well, now that everybody should know, because the Fed has told them that neither of those things are ever going to happen, the bottoms got to fall out of the dollar and gold’s going to go through the roof, and this whole house of cards is going to come tumbling down.”

via ZeroHedge News https://ift.tt/3hDI7UE Tyler Durden

HSBC Resuscitates 35,000 Job Cut Plan As Banking Troubles Persist Tyler Durden

Wed, 06/17/2020 – 09:12

Back in February, HSBC, Europe’s largest bank and troubled lender, announced a plan that would slash upwards of 35,000 jobs. Shortly after, the lender put restructuring plans on hold for three months due to the COVID-19 outbreak. Now, Bloomberg reports, HSBC is resuming plans to cut tens of thousands of jobs as a way to boost profitability in today’s challenging environment.

“Since February, we have pressed forward with some aspects of our transformation program, but we now need to look to the long term and move ahead with others, including reducing our costs,” CEO Noel Quinn wrote in a memo obtained by Bloomberg.

“Against this backdrop, I’m writing to let you know we now need to lift the pause on job losses,” Quinn said. “I know that this will not be welcome news and that it will create understandable concern and uncertainty, but I want to be open with you about the reality of the current situation.”

Quinn unveiled plans to “remodel” large parts of the bank in late 2019. The actual restructuring wasn’t revealed until February — which said the global lender’s 235,000 workforce will be lowered by 35,000 over the next three years. As the lender shrinks its footprint, it expects to save $4.5 billion at underperforming units.

“Europe and the U.S. are expected to face the brunt of the cuts as HSBC attempts to turn around its businesses in regions where it has struggled to make money. The lender’s global banking and markets business, which houses its corporate advisory and market units, is expected to face significant reductions in areas such as equities sales and trading.

“HSBC is eyeing the sale of some of its businesses and is already looking for a buyer for its French retail operations, the disposal of which would take several thousand staff off its payroll,” Bloomberg notes.

A downturn in the global economy, no recovery for several years, and a harsh operating climate, HSBC is expected to announce deeper cuts:

“Despite banks’ commitments to retain staff through the pandemic crisis, we believe it is only a matter of time before substantial further cost-trimming plans are announced, with efficiencies identified as we work through the COVID crisis important in this context too,” John Cronin, an analyst at Goodbody, wrote in a note.

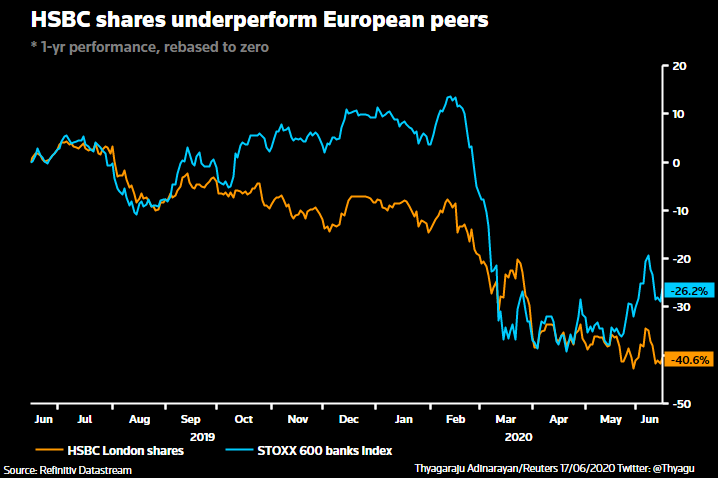

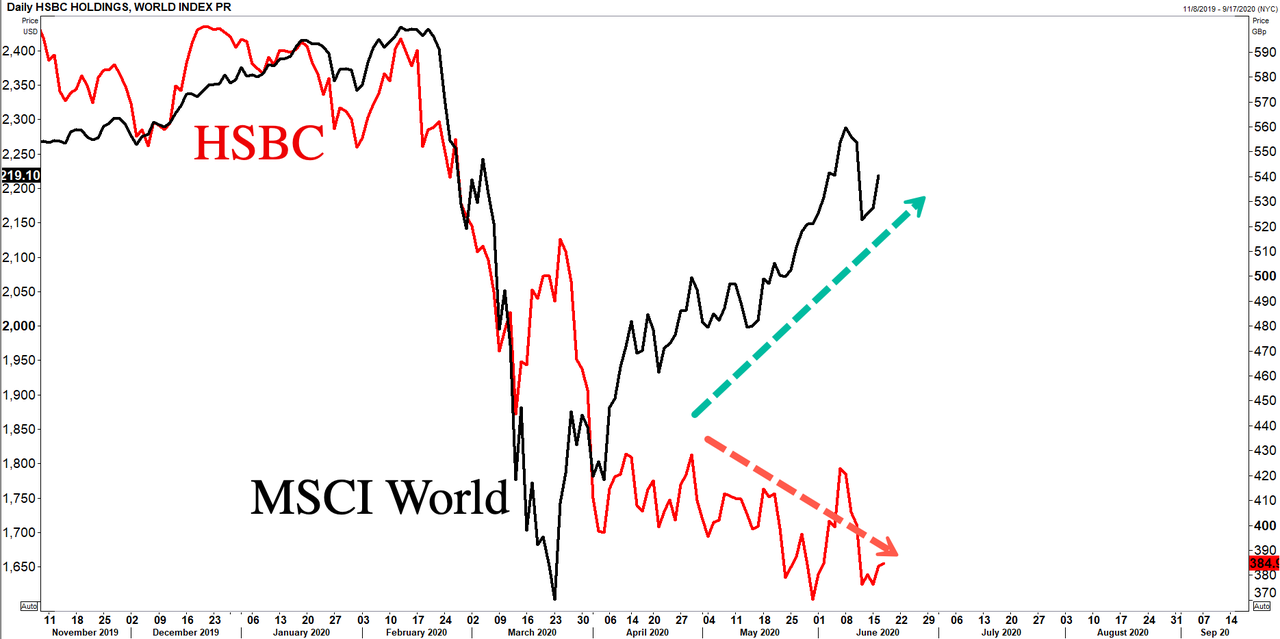

HSBC shares have widely underperformed European peers

HSBC negatively diverges global stocks

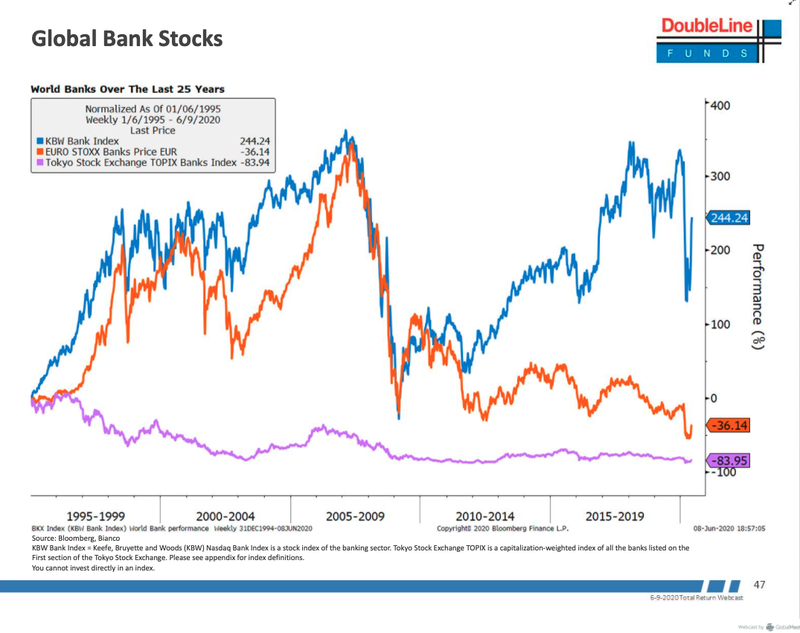

European banks have been operating in an ultra-low interest rate environment, strict regulations, and a continually evolving industry where fintech companies have upended old banking business models.

Doubleline Capital CEO Jeffrey Gundlach recently said in his DoubleLine Total Return Bond Fund webcast that negative interest rates had killed bank stocks in Europe and Japan.

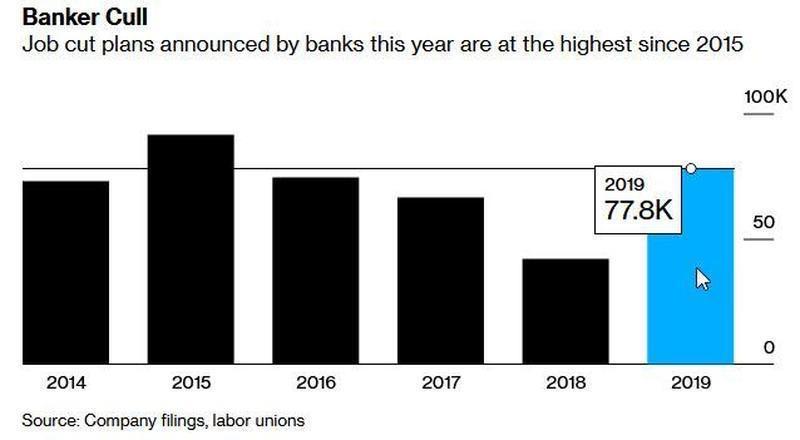

We noted in late 2019, 50 banks laid off 77,780 jobs, the most since 91,448 in 2015 — we’re assuming by now, in a post-corona world, where the global economy is in recession — that a record number of banking jobs will be lost from now until the end of 2021.

Most of the HSBC job cuts will be based in Europe and the US.

via ZeroHedge News https://ift.tt/2UUWevf Tyler Durden

Rabobank: The Fed Will “Only” Intervene If Stocks Go Lower, Or Yields Go Higher Tyler Durden

Wed, 06/17/2020 – 08:53

Submitted by Michael Every of Rabobank

Waking up to the Bloomberg headlines today feels a bit odd. The main story is “BORDER CLASH” (which was then subsequently changed to “FIREFIGHT”) as 20 Indian soldiers have died and China has almost certainly suffered casualties too. The acerbic Global Times makes that clear but it says Beijing is refusing to release the figure “to de-escalate”: US intelligence sources estimate the figure could be as high as 43. That’s two nuclear powers and neighbours, and the two most populous countries on earth, fighting each other (and apparently in melee combat) for the first time since 1975.

The second story is North Korea blowing up the North-South Korea liaison office and moving military police into the DMZ and other strategic locations between the two states (who are still technically at war). That’s a proto nuclear-armed power acting rouge – and it had already stated it has no interest in ever speaking to the US again.

The headlines are odd because both of these were things to be worrying about yesterday, when they happened. Yesterday’s headlines, however, were instead about a USD1 trillion White House infrastructure package that is unlikely to arrive any time soon. It seems that we really don’t see things as one world even when we strive to.

Regardless, Asia had a risk-off session so far today largely because it realises that the above events do matter. It is not the immediate risk of war between the Koreas or between India and China, either of which would be devastating: yet both are necessarily still fat tail risks. It is more a recognition that Asia has fault-lines running through it which are only going to deepen now that the era of “Chimerica”-led globalisation is coming to an end.

How does one resolve North Korea? No good answers. A few years ago people were discussing when India would sign the RCEP trade deal with China: does that look likely now? The more realistic question is how quickly India instead integrates with countries around China such as the Five Eyes group, Indonesia, Japan, and Vietnam. As the world faces more and more binary ‘US or China?’ product choices this will mean disruption of the kind that business does not like. Consider the recent editorial from Singapore’s Prime Minister worrying that this won’t be the Asian century after all if a new Cold War splits the region. (Against which backdrop note that publication of former US National Security Advisor John Bolton’s warts-and-all book about his time in the White House is being delayed by legal action claiming it will compromise US national security: is it called “Spy Kvetcher”?)

Naturally such a scenario would not be win-win: there would instead be winners and losers. On which front, Nikkei Asian Review is running a story today that Huawei has delayed production of parts for its newest flagship smartphone series in response to tighter US export controls. Let that sink in for a moment: China’s flagship firm is having difficulty with its flagship product; and things are only going to get worse from here for it if the US is serious about the legislation and executive orders it has been rolling out from a hawkish production line.

Of course, Asia was also gloomy about the fact that the virus situation in Beijing appears serious. Schools are closed again, for example. Then again, in the UK they still haven’t even opened, and that does not seem to stop the government/public from pressing ahead with all manner of lockdown unwinding.

The virus is clearly also still spreading in the US: yet it seems to be focusing more on shopping. Retail sales jumped 17.7% in May, as we saw yesterday, which was a huge beat of consensus. Yes, that is encouraging, and largely reverses the equivalent plunge seen the previous month as shops re-opened again. However, can we do a little maths, people? Start at 100 and go down 20%: you get to 80. Start at 80 and go up 20% to reverse the fall: you get to 96. That’s 4% down from where you started – which used to be called a recession. Furthermore, this is while federal government cheques are still boosting people’s bank accounts, and as my colleague Christian Lawrence correctly points out, in 30 of the 50 US states current government support is above the median salary level. It’s not that we can’t see a sustained rebound or a V-shape; it’s that it will take a whole lot more to achieve it….and ironically the stronger the numbers like yesterday’s look, the harder it will be to persuade Congress to pass such legislation.

And from some elephants in the room, India and geopolitics/Cold War, to another, the Fed. Yesterday Chair Powell stated to the Senate “I don’t see us wanting to run through the bond market like an elephant snuffling out price signals and things like that.” There’s a quote for the ages. He continued: “We want to be there if things turn bad in the economy or if things go in a negative direction.” Did he mean “stocks” when he said “things”? Because that is how the market has been reading it. (I recall once seeing a baby elephant in Thailand trying to sneak across the floor on all fours to steal some spilt milk. You could see in its eyes that it genuinely thought it was being stealthy “Nobody can see me!”: it was still four-feet high in that position and had all the subtlety of a central bank.)

Powell also mentioned Yield Curve Control (YCC), noting the Fed had been briefed on what the BOJ and RBA have done on that front. “Absolutely no decision” had been made on it so far, but he admitted it might be used if Treasury rates were “to move up a lot, and for whatever reason, we wanted to keep them low to keep monetary policy accommodative, [then] we might think about using it on some part of the curve.” So YCC won’t be used unless Treasury yields go a lot higher…in just the same way the Fed does not act on stocks/things unless they go lower. It’s a market; in one direction. Moreover, can you also think of “whatever reason” the Fed might also have to keep yields low? How about the fact that the last time they used YCC was back in the early 1950s to help ensure that debt built up in WW2 could be inflated away?

So ironically some elephants in the room are now front-page news – which should be risk-off for emerging markets; and yet the Fed-ephant is stomping on volatility anywhere it sees it, which is risk-on for emerging markets. Short-term, which elephant should you back? And longer term? How did those WW2 era debs occur in the first place?

via ZeroHedge News https://ift.tt/2USkLkG Tyler Durden

In effect, the DoJ proposal would rollback protections centered in Section 230 of the Communications Decency Act of 1996, something that’s gaining bipartisan support (albeit for vastly different reasons).

The proposal calls for the rolling back of legal protections that online platforms have enjoyed for more than 20 years to try and make tech companies more responsible in how they police their content, CNET reports. The proposed reforms, to be announced later on Wednesday, are designed to require social media platforms like Twitter, Facebook or YouTube (owned by Google parent Alphabet) to be more active in policing sites for illicit or harmful content, while also requiring them to be more consistent in decisions to remove content they find objectionable.

If adopted by Congress and passed, the bill would effectively make some of the changes outlined in an executive order signed by Trump late last month the law of the land: It would rollback protections for these digital ‘platforms’ that engage in active political censorship of users on said platforms.Because of this, it represents a serious escalation of the Trump Administration’s fight against Big Tech, which President Trump has long criticized for discriminating against conservatives and their ideas.

The new framework might gain more traction on capital hill, particularly after the events of yesterday, when a journalist-activist employed by NBC News published a story claiming that the “far-right” websites Zero Hedge and the Federalist (two sites that have both been described as about as conservative as the Drudge Report) were recently demonetized by Google. Shortly after, Google clarified that it was working with the two publishers to rein in hate speech in comment sections.

Furthermore, Jonathan Turley, a law professor at GW who often writes on free speech issues, criticized an NBC News report on the “de-monetization” (later denied by Google) of Zero Hedge and the Federalist) and argued that Google’s actions support the DOJ legislative proposal and the Trump Administration’s incipient anti-trust effort.

As we discussed earlier in regards to Twitter, Google seems to be making the case for not only pushing forward with anti-trust inquiries but stripping it and other companies of immunity protections. Indeed, the Justice Department just announced that it is moving forward with proposals to strip away protections. Google and other companies were given protections under Section 320 because it has claimed to being a neutral supplier of virtual space for people to speak with one another. It is now effectively shutting down sites because they allow others to comment freely on their sites. This biased targeting of sites has led to congressional objections and renewed threats to amend the federal law. Indeed, Google is undermining the support with some of us who viewed protections are fostering free speech values. It is now using its role to stifle and regulate speech, the very antithesis of not just free speech but the federal protections.

The White House has made it abundantly clear that it won’t tolerate social media platforms continuing to censor and de-monetize conservative speech while ignoring similar behavior by radical leftists. If these platforms want to continue to ‘curate’ the information and speech found therein, then they should be treated more like a publisher than a platform.

via ZeroHedge News https://ift.tt/30PuKe5 Tyler Durden

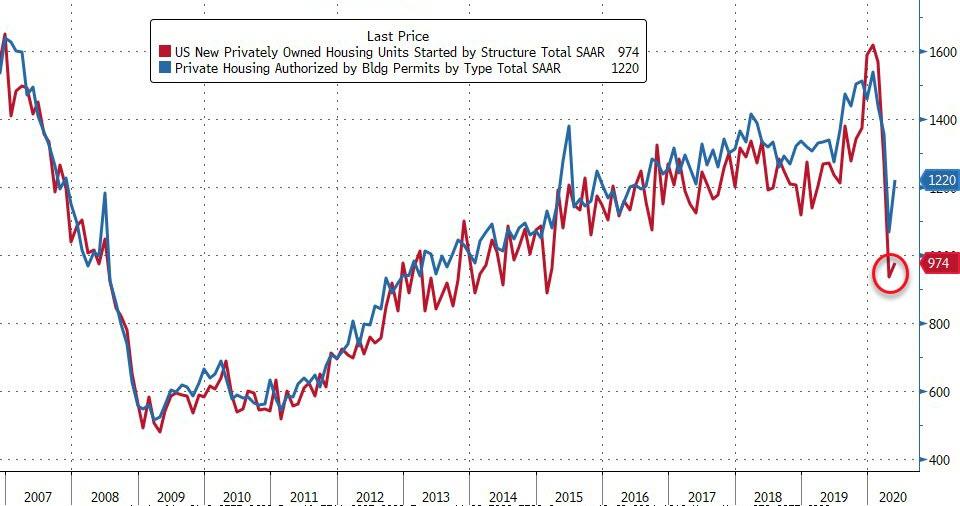

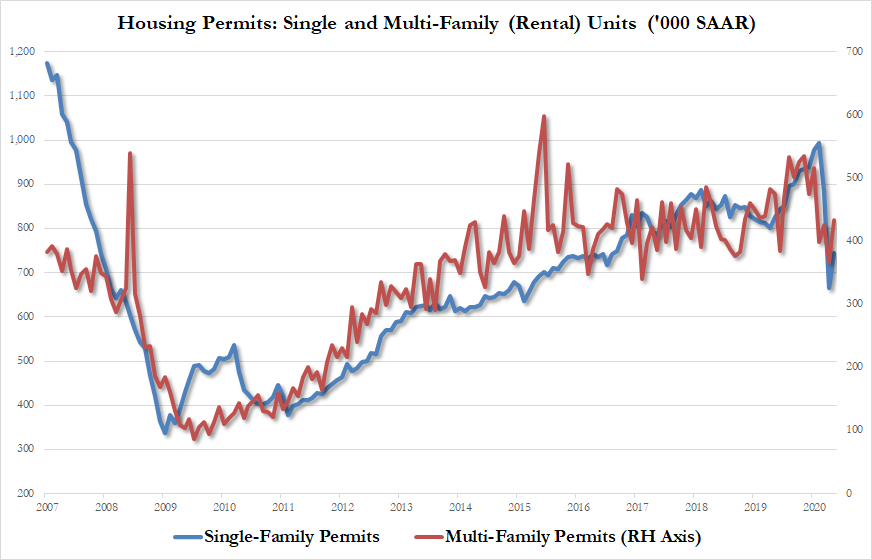

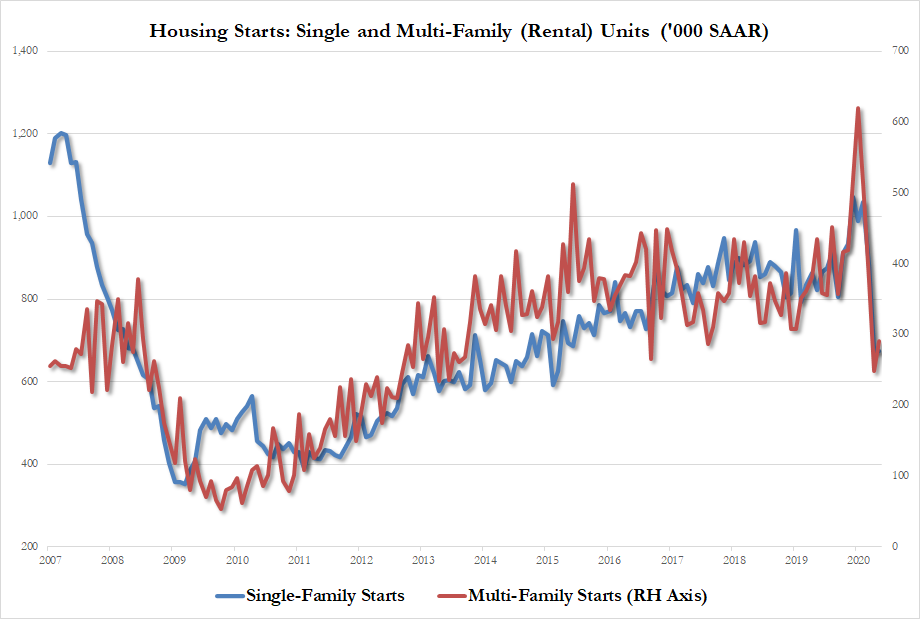

No ‘V’ Here – US Housing Starts Hugely Disappoint Tyler Durden

Wed, 06/17/2020 – 08:39

Following April’s bloodbath to five year lows, housing starts and permits were expected to rebound V-like in May (despite lockdowns being in full swing that month). And as we suspected, the data disappointed with a massive miss in Housing Starts (+4.3% MoM vs +23.5% MoM expected). Building Permits rebounded more than Starts but also disappointed (rising 14.4% MoM against expectations of a 16.8% surge).

Source: Bloomberg

On an aggregate basis, it’s clear the “V” was disappointing…

Source: Bloomberg

Both single- (+11.9%) and multi-family (+18.3%) permits rebounded…

Single-family starts barely rose at all in May (+0.1%), hovering near their lowest since March 2015. Multi-family starts rose 16.9% MoM…

All driven by a huge surge in The West (amid quarantine):

Northeast: 12.8%

Midwest: -1.5%

South: -16.0%

West: 69.8%

Finally, we note that these moves in forward-looking permits come as mortgage purchase applications continue to soar…

Source: Bloomberg

Is this just pent up demand in the usual seasonally strong sales period? And, or are homebuilders far less confident than their “sentiment” index would suggest about the “V”?

via ZeroHedge News https://ift.tt/3hEoPOU Tyler Durden

Trader Sees “Sense Of Confusion”, Not “Battle Of Wills” In Markets Tyler Durden

Wed, 06/17/2020 – 08:19

Authored by Richard Breslow via Bloomberg,

Plenty of Price Action Signifying Not So Much

You certainly wouldn’t know it by looking at your screens, but it has been a wacky day. Equity markets around the world have switched serially from risk-on to risk-off and back again. But volumes have been unimpressive.

Depending on when you took a look, the world seemed very different. All adding up to a sense of confusion, rather than a battle of wills. Investors are meant to buy, yet don’t really feel like it. That failure once it got back to flat on the year has really thrown a spanner into the works. A reality check if ever there was one. But, it will probably need to be retested. If it doesn’t happen soon, the significance of the level will be very high.

Bonds aren’t moving all that much, but trading volumes, especially in longer-duration maturities, have been quite high. Go figure. Sell on infrastructure spending. Buy on central banks.

The narrative changes faster than you can say “mine… no, yours.” Strong bond sales. Sloppy auctions. Something for everyone. Poor foreign exchange is left thinking these other markets are just crazy. And trading with no clear theme. With a lot of crosses in no man’s land. You can have your choice of picking a currency pair that expresses your mood. Is it any wonder that the August gold future just sits on top of its 21-day moving average.

Inflation was reported in the U.K. this morning. Well below target. Higher than recent staff forecasts. Bang on consensus. Score one for the economists out there. They were due a winner. The BOE meets tomorrow. Will they, won’t they, with added stimulus. Personally, I hope they do nothing and see how the reopening of High Street goes. And people need to stop speculating about negative rates. At some point, enough is enough without further proof. Nevertheless, Sterling gyrated as if it was suddenly in play because of this number. Up, down and back again. How appropriate that when it was all said and done it went back to unchanged on the day before starting to leak a bit. That seems right. The MPC is Thursday. Man City versus Arsenal is tonight. And cable will just have to wait.

The urge by central banks to become increasingly involved in the markets is overwhelming. The global economy is reeling and they are fully committed to helping out. They should be applauded for the efforts. But they also need to be careful that they don’t impair market liquidity to the extent that the normal flow of trading is dangerously impaired. And price discovery distorted. There are any number of fixed income markets around the world warning that liquidity is becoming a real problem. And the law of unintended consequences is an issue that can’t be ignored. This hasn’t become a big issue in the U.S., but elsewhere, fixed income funds are showing signs of having trouble meeting redemptions. In some cases having to set up gates. And when credit investors get uneasy, they tend to do so in groups. They often don’t have a choice. Central banks need to take into consideration the realities of how long-term investors need to continue to function in the markets and fulfill their own mandates. And what things might look like when this is finally over

via ZeroHedge News https://ift.tt/30QzPD9 Tyler Durden

Stocks Shrugs Off China Second Wave Fears, Asian Clashes, Rise On Stimulus Hopes Tyler Durden

Wed, 06/17/2020 – 08:01

For the third day in a row, global markets have shrugged off concerns about rising global coronavirus cases and that China is set to suffer a “second wave” as much of Beijing is once again under lockdown, with US equity futures advancing and European shares adding to their best gains in almost a month thanks to continued government and central bank stimulus and hopes of a rapid economic recovery.

As we accurately previewed earlier, Tuesday data showed US retail sales enjoyed a record 17.7% rebound in May, but new infections have hit record highs in six U.S. states, Brazil infections surged by a record 34,918, Iran warned it may need a new lockdown, and China cut flights and closed schools to contain a fresh outbreak in Beijing and a clear second wave in the country.

The theme of a strong global economic rebound “will need to be balanced against the 2nd wave COVID risks which are more difficult to assess, and we would argue investors have assumed to be perhaps more modest than in reality,” said MUFG’s Head of Research Derek Halpenny quoted by Reuters.

Geopolitical tensions also remain rife with India reporting 20 of its soldiers were killed in clashes with Chinese troops at a disputed border site, while North Korea rejected a South Korean offer to send special envoys and said it would redeploy troops at the border. However, in a world where only central bank liquidity matters, all geopolitical concerns were quickly forgotten.Sentiment was also boosted after a simple, cheap steroid, dexamethasone, used to reduce inflammation in other diseases such as arthritis, reduced death rates by around a third among the most severely ill COVID-19 patients admitted to hospital.

“It is one of the best pieces of news we’ve had through this whole crisis,” Britain’s Health Secretary Matt Hancock said.

As a result, MSCI’s index of World shares rose 0.2%, having climbed 2.2% the previous day to reclaim a good portion of the ground it lost last week. European shares rebounded, after early gains of 1% were trimmed in half but with increases in real-estate and construction-firm shares brought fresh momentum to the Stoxx Europe 600 Index.

Asian equities saw a modest move higher except for shares in South Korea, which were volatile in the wake of rising tensions with North Korea, with the won currency sliding against the dollar. Most other markets in the region were up, with Thailand’s SET gaining 1% and Australia’s S&P/ASX 200 rising 0.8%, while Japan’s Topix Index dropped 0.4% after jumping almost 5% on Tuesday for its biggest daily gain in three months. The Topix declined 0.4%, with Toho System and Enigmo falling the most. The Shanghai Composite Index rose 0.1%, with China Building Test and Nanjing Iron & Steel posting the biggest advances.

As Bloomberg notes, investor optimism toward risk assets is reflecting bets that new virus outbreaks won’t lead governments to pull back from gradually reopening their economies, even though Fed Chair Powell said the U.S. economy has a long way to go before it reverses the substantial damage done by the pandemic.

“Global markets could remain stretched between a health situation likely to remain a threat in several regions for some time on the one hand, and a stream of positive macro figures confirming that we have passed the low point on the other,” said Xavier Chapard, a global macro strategist at Credit Agricole. He added that “the Fed’s priorities are shifting from emergency actions aimed at preventing a market melt-down to long-lasting actions to support the fastest possible recovery in the real economy”, although we kinda disagree with that considering the Fed strategically re-announced the launch of its bond buying operation just as the market was about to drop below its gamma neutral level on Tuesday.

“There is little doubt that the global economy bottomed in April and is poised to post record-high growth rates over May and June, strongly lifting 3Q GDP above its 2Q trough,” wrote economists at JPMorgan. “But questions about the extent of lasting damage will have to wait for a number of months before being resolved.”

In rates, 30Y rose 2bps at 1.55%, having risen by the most in a month on Tuesday, and 10-year German Bunds led a flurry of similar rises in Europe ahead of a 5 billion euro bond sale. “The tension between better economic data and rising COVID-19 cases continues to drive market volatility,” said Antoine Bouvet, senior rates strategist at ING in London.

In FX, the Bloomberg Dollar Index swung between small gains and losses, though the upside seemed capped by the 200-DMA; the greenback advanced versus most Group-of-10 peers, though most traded in confined ranges. Risk-sensitive currencies were little changed against the dollar after earlier being weighed down on concern over the resurgence of the coronavirus outbreak, particularly in China. The euro reversed an early London-session gain; German bunds declined, with the oversubscription rate falling at an auction. The pound slumped; it had earlier bounced back from a slight decline after U.K. inflation data came in at its weakest since 2016, increasing expectations for more BOE stimulus.

In commodities, gold was stuck at $1,725 and well within the $1,670/$1,764 range of the past few weeks. Gains in oil prices slowed amid an increase in U.S. crude inventories. They had climbed 3% on Tuesday after the International Energy Agency (IEA) raised its oil demand forecast for 2020. Brent crude futures swung 1% higher to $41.35 a barrel, while U.S. crude ticked up 16 cents to $38.54.

Expected data include housing starts, mortgage applications reported earlier rose to the highest level since 2009.

Market Snapshot

S&P 500 futures up 0.9% to 3,155.75

STOXX Europe 600 up 0.8% to 366.28

MXAP up 0.2% to 158.71

MXAPJ up 0.5% to 511.09

Nikkei down 0.6% to 22,455.76

Topix down 0.4% to 1,587.09

Hang Seng Index up 0.6% to 24,481.41

Shanghai Composite up 0.1% to 2,935.87

Sensex up 0.7% to 33,846.95

Australia S&P/ASX 200 up 0.8% to 5,991.80

Kospi up 0.1% to 2,141.05

German 10Y yield rose 6.2 bps to -0.365%

Euro up 0.06% to $1.1271

Italian 10Y yield fell 6.1 bps to 1.269%

Spanish 10Y yield rose 1.8 bps to 0.551%

Brent futures down 0.3% to $40.82/bbl

Gold spot down 0.2% to $1,722.58

U.S. Dollar Index up 0.2% to 97.12

Top Overnight News from Bloomberg

President Donald Trump’s trade chief, Robert Lighthizer, will tell U.S. lawmakers Wednesday that the time has come to renegotiate America’s fundamental tariff commitment at the World Trade Organization

Beijing reported new virus cases Wednesday, having closed schools and canceled more than 1,200 flights as authorities grapple with stemming the outbreak without sealing off the city

The European Commission on Wednesday will unveil a set of proposals to bolster local industries in fighting back against companies that receive aid from foreign governments. The plan could ban these non-EU firms from making acquisitions, or force them to divest assets, and allow the commission to impose fines

Italian Prime Minister Giuseppe Conte will likely seek parliament’s approval for about 10 billion euros ($11 billion) in extra spending soon, government officials said, in the latest step to revive one of Europe’s most vulnerable economies

South Korea warned North Korea against further provocations, after Kim Jong Un’s regime pledged to dismantle the last remnants of President Moon Jae-in’s legacy of rapprochement and move troops into disarmed border areas

The U.K. published its negotiating objectives for a trade deal with Australia and New Zealand, which the government said could boost exports by about 1 billion pounds ($1.3 billion) as it seeks to expand trade links after Brexit

Asian equity markets failed to fully sustain the positive handover from Wall St with regional bourses indecisive amid geopolitical tensions, COVID-19 fears and with early underperformance in Japan due to a firmer currency and weaker than expected trade data. ASX 200 (+0.8%) and Nikkei 225 (-0.6%) traded mixed as upside in consumer stocks and tech kept the Australian benchmark afloat, while sentiment among Tokyo exporters was subdued by a firmer currency and after the latest trade data showed a larger than expected slump in Exports Y/Y, with Japan’s US-bound exports at the fastest pace of decline since March 2009 and its trade surplus with the US at a record low. KOSPI (+0.1%) swung between gains and losses on increasing tensions in the Korean peninsula after North Korea demolished its inter-Korean liaison office in Kaesong yesterday and is reportedly to deploy the army to Kaesong and Mt. Kumgang. There were also criticism from North Korean leader Kim’s sister on South Korean President Moon which prompted a response from the Blue House that it will not tolerate North Korea’s senseless remarks anymore and the Defense Ministry warned that North Korea will pay the price if it takes actual military action. Hang Seng (+0.6%) and Shanghai Comp. (+0.1%) conformed to the non-committal tone after another net liquidity drain by the PBoC and amid concerns regarding the outbreak in Beijing where the city government raised its COVID-19 emergency response to level II from level III and resulted to the cancellation of 1255 flights. In addition, deadly clashes between India and China at the Himalayan border where 20 Indian soldiers were killed also contributed to the ongoing geopolitical concerns. Finally, 10yr JGBs were slightly higher after having rebounded off support just below 152.00 although the underperformance of Japanese stocks and BoJ’s presence in the market only provided marginal gains for JGBs.

Top Asian News

Citi Sees Higher Chance of Possible Default for Hilong Bonds

RBA Saw Australian House Prices Falling 7% Over the Next Year

Foiled Kidnapping Hurls Publicity-Shy Tycoon Into Spotlight

Yes Bank Is Said to Plan $1 Billion Public Share Offering

European equities had a tame start to the session as bourses opened with very modest gains following a mixed APAC handover, before the region edged higher since the cash open. Europe has since given up early gains [Euro Stoxx 50 +0.1%] to return to levels seen around the cash open. Peripheries lag with Spain’s IBEX (-0.9%) is the marked underperfomer thus far and Italy’s FTSE MIB (-0.1%) also in the red – potentially heading into the European Council meeting with pessimistic rhetoric from Chancellor Merkel and European Council President Michel on the likelihood of a concensus on the Recovery Fund being reached on Friday. The periphery could also be seeing jitters of a second wave having been hit hard by the initial outbreak. Sectors are mixed with defensives overall faring better than cyclicals, whilst the breakdown sees Travel & Leisure the laggard amid fears of further disruptions to operations due to a second wave. On that front, Carnival (-3.5%) shares continue to deteriorate alongside the update from Norwegian Cruse Line – who cancelled all voyages until October. Elsewhere, European Auto names and part makers remain under pressure as May car registrations slumped 57% YY, with Renault (-1.2%), Daimler (-1.1%), Continental (-1.8%) and Ferrari (-1.5%) all at the foot of their respective bourses. HSBC (+0.1%) trades choppy but just about holds onto gains amid reports the group is poised to cut headcount by some 35k over the medium term; however, the firm could be further embroiled in politics, with Global Times stating that some observers have said the Anglo-Sino bank may experience more severe consequences for their collusion with the US against Huawei.

Top European News

U.K. Inflation at Weakest Since 2016 Adds Pressure on BOE to Act

German CabinetOkays $70 Billion in Debt to Combat Recession

Brexit Heartlands Are Paying the Highest Price for Coronavirus

Forget This Year’s Highs for European Equities, Strategists Warn

In FX, a rather muted start to the midweek EU session, as the Dollar consolidates following yesterday’s revival on encouraging US economic recovery leads via retail sales. However, the DXY remains relatively underpinned within a narrow 97.264-96.796 band amidst similarly tight ranges vs major counterparts in the run up to Fed Chair Powell’s 2nd semi-annual testimony and more data that could provide further evidence for or against the circa April COVID-19 trough theory in the form of housing starts and building permits.

NOK/SEK/AUD/CHF/NZD – The Norwegian Crown continues to rebound from Monday’s deep risk aversion and crude retracement lows, with Eur/Nok testing support ahead of 10.7000 awaiting further confirmation from the Norges Bank tomorrow that benchmark rates have hit the lower (zero in this case) bound. Meanwhile, the Swedish Krona has also regained some poise amidst mixed NIER GDP forecast revisions and jobs data, as Eur/Sek hovers near 10.5100 compared to a high just shy of 10.5800. Similarly, the Aussie and Kiwi have regrouped after more volatile trade overnight and Tuesday’s even sharper swings to revisit 0.6900 and pivot 0.6450 against their US peer respectively, and with the latter now looking for independent inspiration from NZ GDP tonight. Elsewhere, the Franc and Loonie are both meandering, around 0.9500 and 1.3550, eyeing the SNB on Thursday and Canadian CPI later today.

JPY/GBP/EUR – Marginal G10 underperformers, with the Yen still restrained below 107.00 in wake of a wider than expected Japanese trade deficit on weak internals and stymied by decent option expiry interest at 107.25 (1.1 bn), while Cable topped out ahead of 1.2600 and the 200 DMA again, albeit holding around the 100 DMA (1.2526) after little reaction to in line/softer UK inflation metrics. The Euro is also fading from a test of round number/psychological resistance at 1.1300, and testing support through the 50 DMA (1.1233) that sits close to recent sub-1.1230 lows and stops said to be residing on a break of 1.1228.

EM – Broad sentiment is notably more fragile against the backdrop of several geopolitical hotspots that could spiral given recent developments, and on that note the Lira is underperforming as Turkey steps up its offensive against PKK/YPG targets in Northern Iraq, with Usd/Try back over 6.8500 at one stage in contrast to flat/fractionally softer trade in Usd/Zar and Usd/Mxn.

In commodities, WTI and Brent front-month futures initially grinded higher in early European trade, having had somewhat of a lacklustre APAC session with the complex pressured by Beijing curbing some 60% of its flights in a bid to stem a second virus outbreak, whilst a surprise build in Private Inventories added to the downside factors. Nonetheless, the complex has given up recent gains as traders eye the release of the OPEC Oil Market Report for June alongside the start of the JTC meeting, and against the backdrop of heightened geopolitical tensions. Tomorrow’s JMMC meeting will see the committee (composed of Saudi, Russia, Iraq, UAE, Kuwait, Nigeria, Algeria, Venezuela and Kazakhstan) reviewing secondary source data alongside current market fundamentals before proposing policy recommendations – no policy will be set at this meeting. In terms of compliance, reports note that Iraq is aligning its cuts with the OPEC+ pact, shipping data and industry sources suggest the second largest OPEC member’s exports have declined some 300k BPD thus far in June. WTI July reliquinshed the USD 38/bbl to the downside (vs. 37.21/bbl low) whilst Brent August similarly lost its USD 41/bbl handle (vs. 40.03/bbl low). In terms of other scheduled events, the weekly DoEs could provide some volatility (in the short term at least) – with headline crude stocks seen drawing 152k barrels (vs. Private Inventory build of 3.9mln barrels). Elsewhere, spot gold succumbs to a firmer Buck as the yellow metal prints fresh session lows. It’s worth noting for precious metals that ETFs increased holdings gold holdings for a fifth consecutive session in which it added almost 48k oz yesterday to bring this year’s net buying to 18mln oz. Copper prices see modest gains well within yesterday’s ranges amid the indecisive APAC tone – prices remain north of USD 2.50/lb but just under USD 2.60/lb.

US Event Calendar

7am: MBA Mortgage Applications, prior 9.3%

8:30am: Housing Starts, est. 1.1m, prior 891,000; MoM est. 23.46%, prior -30.2%

8:30am: Building Permits, est. 1.25m, prior 1.07m; MoM est. 16.79%, prior -20.8%

DB’s Jim Reid concludes the overnight wrap

This morning we are hurtling deep into the 21st century here at DB Research as we have launched a new trial video research format. In this first trial you’ll see me talk through June’s market sentiment survey for four and a half minutes. It might be worth watching just to see the results of my wife’s attempts to style and pimp my WFH set up. We have guitars, books and a copy of an old master on an easel. The painting on the easel was a creative way of blocking out light from a window which is a bit of a VC nightmare. The painting was left over from my last house where we commissioned art students in Russia to paint replicas of old paintings at a very reasonable price and make them look old. Not obvious pieces but nice ones. Given my wife went to Art College she hated this philistine approach from me but I said I wasn’t prepared to pay for many antique oils. If anyone can recognise the painting then I’ll be very impressed!! Here is the link to the video. Let us know if the format is interesting to you and what you’d like to see on it from DB Research (link here).

In another WFH appearance from my crib, this Thursday (12:30pm London time) I’m taking part in a small fireside roundtable webinar on China, commodities and the reflation trade organised by our mining and metals team but containing macro content from our Chinese economist, China strategist, our commodities strategist and also myself. Feel free to register here.

While we are in full advertising mode, yesterday Henry Allen on my Thematic team put out a report that we’ve been working on looking at what might be the next massive tail risk after Covid-19, looking at events including further pandemics, volcanoes, solar flares, wars and earthquakes. The main takeaway is that there’s a one-in-three chance that the next decade will see at least one of a major flu pandemic killing more than 2m people; a globally catastrophic volcanic eruption; a major solar flare; and a global war. So some pretty striking stuff. You can read the full report here.

The most exciting thing today is the return of the English Premier League. I’m not sure I’ll ever be so happy to see Aston Villa vs Sheffield United or indeed ever watch that fixture again. Hopefully one of the tail risk disasters mentioned above won’t come before Liverpool are crowned champions within the first few games of the restart. In terms of markets, yesterday felt like one of those children’s football matches where one minute everyone rushes up the pitch towards the opposition’s goal to try to score before the other side then do exactly the same at the opposite end thus ensuring no formation, no structured defending and no tactics. Just an end to end slug fest. Indeed markets went from bullish, to worried, to extreme bullish to worried and back to bullish again.

By the end of the session, the S&P 500 was up +1.90% in its 3rd straight move upwards, with every sector moving higher on the day and only 35 stocks down. The VIX volatility index continued to unwind from its intraday peak early yesterday morning London time (44.44) with a further -0.73pts fall to close at 33.67. Energy stocks led the move higher in the US, with WTI up +2.67% and Brent crude up +2.79%. The latter closed above $40/barrel for the first time since risk assets dropped sharply last Thursday.

So going through the bewildering array of headlines, let’s begin with the pandemic. The good news yesterday was that an Oxford University trial reported that the steroid dexamethasone was found to reduce coronavirus deaths by a third in patients who required ventilation. In fact it was described by England’s Chief Medical Officer on twitter as “the most important trial result for COVID-19 so far.” On the other hand, there were some less positive developments elsewhere, with Beijing announcing that schools would be shut and online classes resuming for all grades, following a new cluster of cases in the city, that has also seen them raise their Covid-19 emergency response to the second-highest level. Further, the city has also ordered that people will have to be tested for the virus before being allowed to leave the city and has imposed restrictions on visits to all residential compounds with those in areas with medium and high-risk areas being barred from accepting visitors.

Over in the US the news wasn’t exactly positive either as the case numbers in certain states continued to move in a concerning direction. In Florida they reported a +3.6% rise in cases yesterday, above the 7-day average of +2.5% and the most absolute cases reported in a day since the pandemic started. While in Texas, which has been something of a hotbed recently, the number of virus hospitalisations rose by +8.3%, the most in nearly 2 weeks. Cases in the state rose by +3.7% – the most in week – with the absolute number (3,358) the largest during the pandemic. California new cases rose by +2.3%, above the weekly average of 2.1% while confirmed hospitalisations rose by 7.5% to 3,335 across the state, the most since the first week of May. Much like we’ve previously highlighted in the Corona Crisis Daily in countries like the UK and France, there appears to be a Tuesday effect in some US states, where the Sunday and Monday reporting is slightly lower and then cases rise more sharply on Tuesday. Texas, California, Arizona, and Florida all have seen a noticeable rise in case growth on 4 out of the last 5 Tuesdays when compared to the 2 days prior. Remember our usual case and fatality tables are in the full report today. Click on “view report” at the top.

Against the worrying virus backdrop, a stunningly strong US retail sales report for May offered further hope to investors that the economy might be able to bounce back quicker than many had expected. The headline figure saw an increase of +17.7%, more than double the +8.4% expected, while the previous month’s decline was revised to show a smaller -14.7% contraction (from -16.4%). Autos dragged up the overall number, with vehicles and parts seeing a +44.1% rise in May, but even the ex-auto number at +12.4% (vs. +5.5% expected) came in stronger than anticipated, with increases in every category on the month. President Trump expressed his approval, tweeting that “Wow! May retail sales show biggest one-month increase of ALL TIME, up 17.7%. Far bigger than projected. Looks like a BIG DAY FOR THE STOCK MARKET, AND JOBS!”

We also saw a couple of geopolitical flare-ups yesterday, which in another world could have easily blown the rally off course. Firstly, we got the news not long after going to press yesterday that North Korea had blown up an inter-Korean liaison office on their side of the border, which comes against the backdrop of escalating threats from North Korea towards the south in recent weeks. North Korea has said overnight that it will be deploying troops on its side of the border where it had joint projects with South Korea, and to the Mount Kumgang tourist area. Secondly, there was a clash between Indian and Chinese soldiers yesterday in which at 3 Indian troops were confirmed to have been killed during a fight, before a further 17 passed away from injuries according to a New York Times report. A Chinese foreign ministry spokesman said that two Indian soldiers had crossed into Chinese territory on Monday, and that “They provoked and attacked the Chinese side, leading to a severe physical brawl.” By the looks of things it seems as though both sides are trying to de-escalate the situation, but this is nevertheless a very unwelcome development in an environment not short of possible risks.

In terms of the broader market moves, as mentioned the S&P 500 saw its 3rd upward move in a row, while the Dow Jones (+2.04%) and the NASDAQ (+1.75%) also saw strong performances. European equities outperformed their US counterparts, with the STOXX 600 up +2.90%, while the DAX, FTSE MIB, and IBEX were all up over 3%. Core sovereign bonds sold off as investors moved out of safe havens, with yields on 10yr US Treasuries (+3.1) and bunds (+1.9bps) both climbing. That said, there was another notable narrowing of peripheral spreads in Europe, with the spread of Greek 10yr yields over bunds falling by -7.8bps to their tightest level since late February. 10yr BTP spreads narrowed by -8.0bps.

The rally has taken a pause overnight with bourses slightly lower in Asia. Indeed the Nikkei (-0.81%), Hang Seng (-0.03%), Shanghai Comp (-0.10%) and Kospi (-0.03%) are all in the red with only the ASX (+0.54%) currently up. The geopolitical tensions we noted above have weighed on the Korean Won (-0.71%) and the Indian Rupee (-0.24%) while yields on 10y USTs are down -2.5bps and futures on the S&P 500 are trading down -0.25%. WTI oil has also retraced 3%. In other overnight news, Japan’s trade surplus with the US dropped -97% yoy in May to $96mn, the lowest in data going back to 1979, as car shipments declined by -79% yoy.

Back to the US, and Fed Chair Powell appeared before the Senate Banking Committee yesterday, as part of the semi-annual monetary policy report to the Congress. In his prepared remarks, Powell said that in spite of indicators that pointed towards a stabilisation or a small rebound in activity, “the levels of output and employment remain far below their pre-pandemic levels, and significant uncertainty remains about the timing and strength of the recovery.” So clearly not wanting to let positive data like the jobs report let people think the economy is out of the woods yet. Given this testimony occurred only days after the FOMC this was never likely to move the dial much but Powell’s tone on corporate bond purchases were a bit confusing. He suggested that purchases will be switched from ETFs to bonds but maintaining the same dollar amount. In speaking to Craig who covers US credit and who is, to be fair, co-authoring this report today, he suggests that at face value this would suggest the Fed will buy far far less than the $250bn capacity that the SMCCF has. So far ETF purchases have averaged between $1-1.5bn per week for context. The expectation was that bond purchases would be in addition to ETF purchases and also that bond purchases would be greater given the larger available universe to purchase from. We will see if this was a misinterpretation issue or an actual policy announcement. Credit had earlier been on an almighty tear. From opening levels iTraxx Main, Crossover, US IG and HY CDX were -10, -65, -6 and -32bps tighter at their spread lows for the session before closing a slightly more subdued close at -6, -33, -1 tighter and +2bps wider respectively. Cash did seemingly have a better day however, with US HY and IG spreads in particular 47bps and 12bps tighter respectively.

Powell was not the only Fed speaker yesterday as Fed Vice Chair Clarida weighed in on the inflation debate citing the pandemic as a deflationary shock. He indicated that the Fed is placing a high priority on keeping inflation expectation anchored, amidst risks of long-term inflation expectations falling due to the economic fallout. He admitted that these are not new concerns saying, “that measures of longer-term inflation expectations were, when the downturn began, at the low end of a range that I consider consistent with our 2% inflation objective and, given the likely depth of this downturn, are at risk of falling below that range.”

Wrapping up with yesterday’s other data now. The industrial production numbers from the US weren’t quite as positive as the retail sales figures, though they did show a +1.4% rebound in May (vs. +3.0% expected). That said, the NAHB’s housing market index rose to 58 (vs. 45 expected), so all eyes will be on today’s housing starts and building permits data to see if that rebound in housing is evident in other releases. Here in the UK meanwhile, the headline unemployment rate for the 3 months from February to April unexpectedly remained at 3.9% (vs. 4.7% expected). However, digging further into the labour market data showed things weren’t quite so rosy. The number of weekly hours worked fell to the lowest seen since 2013, while the number of vacancies in the more up-to-date March-May period fell to 476k, the lowest since 2012.

To the day ahead now, and we’ll hear from Fed Chair Powell once again today before the House Financial Services Committee, while the Fed’s Mester will also be speaking. On the data front, we’ll get a bunch of data releases out for May, including UK CPI, EU27 new car registrations and the final Euro Area CPI reading. Over in the US, there’ll also be housing starts and building permits, while Canada will also release their CPI.

via ZeroHedge News https://ift.tt/3eawZfZ Tyler Durden

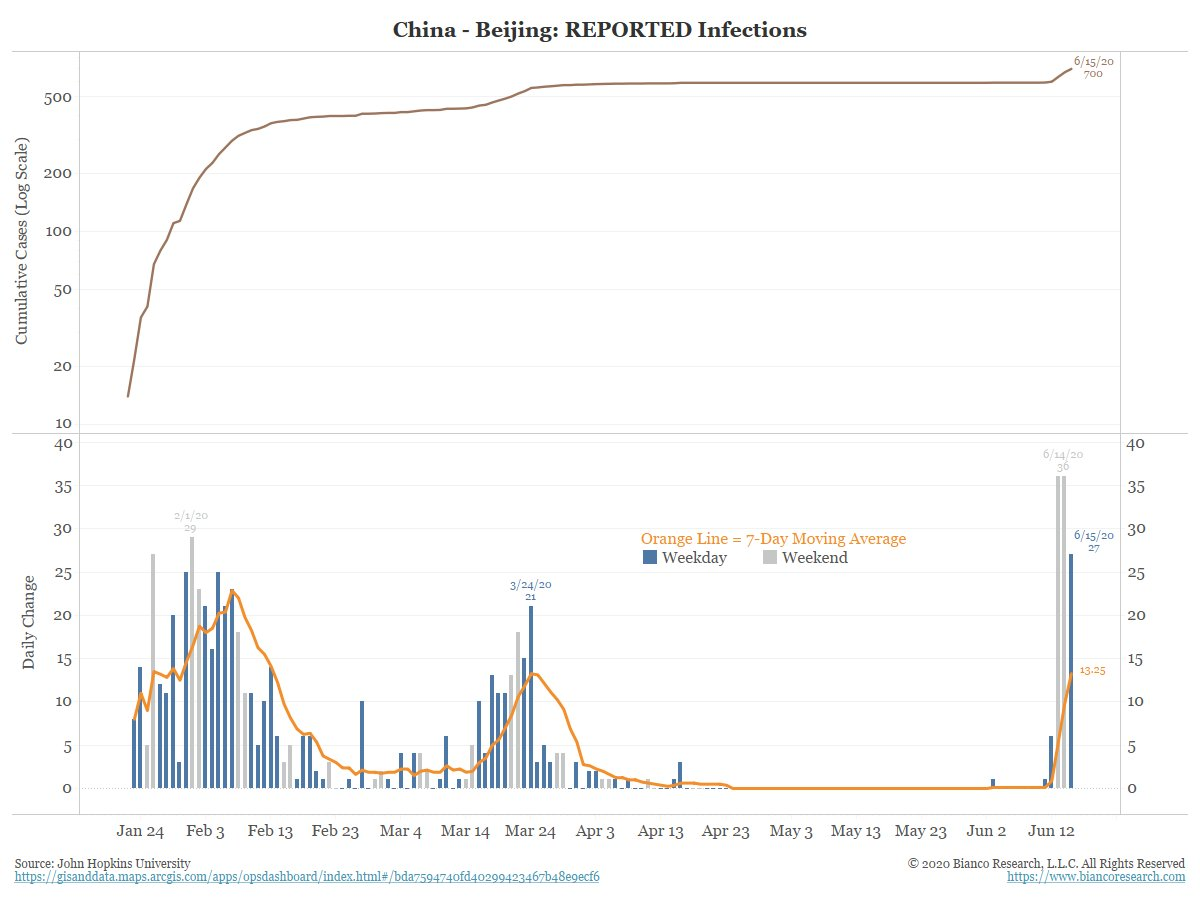

India Reports Record Jump In COVID-19 Deaths As China Struggles With “Textbook Second Wave”: Live Updates Tyler Durden

Wed, 06/17/2020 – 07:57

Nuclear-armed neighbors China and India may be enmeshed in a deadly border dispute with potentially serious ramifications for the global community, both countries are struggling with an alarming resurgence of COVID-19 cases, according to media reports.

Yesterday, Chinese officials ratcheted up restrictions in Beijing as nearly 150 new coronavirus cases have been identified in the city over the past week. More residential compounds were placed under ‘partial lockdown’ conditions on Tuesday. Beijing has already tested more than 350k people since Saturday, with a goal of testing a large chunk of the city’s population of ~20 million people.

According to Al Jazeera English, one of the few English-language news organizations with reporters still on the ground in Beijing, many locals were taken by surprise as the local government raised the emergency alert level to ‘II’, closed schools and markets and began imposing movement restrictions, particularly on those who live in “high risk” areas (ie areas near the Xinfadi wholesale food market where officials believe the outbreak originated).

Some Beijingers didn’t realize that their residential community had been placed on ‘partial lockdown’ with nobody allowed in or out until all residents have been tested. AJ says there are currently at least 27 communities under these conditions.

Nelson Quan had no idea he had been locked into his compound in the Yuquan district of Beijing until he arrived at the front gate and saw the barricade.

Four days earlier, on June 11, Beijing had reported its first COVID-19 case in almost two months. Now, Quan’s community and at least 27 others are forced to stay at home while they await the results of their nucleic acid virus tests. No one is allowed in, or out.

“Two months of things loosening up, and life feeling like it’s going to be normal, and all of a sudden we’re back to where we were in February,” Quan said in a phone call.

One official said Wednesday that Beijing cannot rule out the possibility that the number of cases in the city will stay at current levels for some time. Pang Xinghuo, a senior official for the Beijing disease control authority, says the epidemic is still growing in the city. On a lighter note, Chinese and Norwegian authorities have confirmed that Norwegian salmon was likely not the source of the novel coronavirus that was discovered on cutting boards in the Xinfadi market, the purported ‘epicenter’ of the Beijing outbreak, which has reportedly now spread to several surrounding provinces, while the city of Guangzhou struggles with an outbreak of its own.

More than 1,250 flights that were scheduled to depart from Beijing on Tuesday were cancelled, some 70% of the total scheduled flights, according to media reports.

Even more dire numbers were reported out of India on Wednesday, which registered 2,000 deaths in a day for the first time, a record-breaking total that took the Indian death toll to 11,903. Meanwhile, the number of confirmed infections surged over 354,000, as Mumbai and Delhi feel the brunt of the outbreak.

One analyst shared several charts illustrating how the latest outbreaks in China are “textbook” examples of a ‘second wave’ pattern.

Finally, the WHO has welcomed news that dexamethasone, a cheap and widely available and steroid, has helped save the lives of people with severe COVID-19. One rep described it as “great news.”

via ZeroHedge News https://ift.tt/2UThW2G Tyler Durden