Minutes after CNN reported that Bernie Sanders would be joining Joe Biden for a “special announcement” shortly, media reports have confirmed that Sanders plans to endorse Biden, just as he ended up kowtowing to Hillary Clinton four years ago.

The Junior Senator from VT said he would do all he could to help Biden defeat President Trump in November.

Fortunately, thanks to COVID-19, instead of criss-crossing the country, like he did for Hillary Clinton, Sanders might simply be able to fire off a few filmed messages of endorsement and a couple pre-recorded stump speeches and be done with it.

Sanders’ legion of young ‘democratic socialists’ who despise Biden and the Democratic elite are about to be *very* disappointed…as is perhaps his most visible supporter, podcast host Joe Rogan, who said recently that he would back Trump over Biden.

A Country In Lockdown: States Accounting For 86% Of GDP Are Frozen, And What The Reopening Could Look Like

Although the federal government has played the leading role in providing stimulus and relief in response to the coronacrisis, state governments have shaped the economic sudden stop through hundreds of emergency orders that imposed restrictions on commerce and social activity. The fifty states have adopted different approaches at different times to handling the threat to public health since the outbreak of the virus.

Over the past month, states shut down economic and social activity largely in three steps:

closing schools,

issuing stay-at-home orders,

closing non-essential businesses.

To understand when and how extensively these shutdowns occurred across the United States, Goldman compiled a database of dates when each state governor issued these three types of orders. The bank then aggregated the state orders into a daily national average weighted by state GDP to track the share of the US economy subject to each order over time. Goldman also then focuses on school closures, stay-at-home orders, and nonessential business closures because they are legally binding and fairly consistent across states.

Governors swiftly closed schools in states accounting for over 90% of US GDP by March 20, just one week after the first statewide closure in Washington state on March 13. These orders prevented many people who had to care for children from going to work, which in some states allowed affected individuals to access unemployment insurance benefits.

Statewide stay-at-home (or shelter-in-place) orders began with California on March 19, followed by New York and Illinois on March 20. These orders restrict movement and require some degree of social distancing. The orders range in their restrictiveness and in how they can be legally enforced. States comprising half of GDP had issued stay-at-home orders within a week of California’s order and today 90% of the US economy is subject to a statewide order.

Orders to close nonessential businesses often occurred alongside stay-at-home orders. Each state maintains its own list of essential vs. nonessential services, though many states have followed the same federal guidelines for these definitions. Within two weeks of the first state order to close nonessential commercial activity, 70% of GDP was subject to a nonessential business restriction.

The chart below shows Goldman’s three national series that track these orders as well as an overall US Lockdown Index that averages the three. As of April 9, the US Lockdown Index stood at 86%.

Over this period the federal government also took actions that likely influenced state decisions. For example, on March 16, the White House encouraged social distancing by limiting gatherings of more than 10 people and discouraging face-to-face commercial activity.

Goldman then complements its newly created lockdown index with a US social distancing index based on data from Google’s Community Mobility Reports that track individuals’ visits to and time spent at work, at stores, in transit, and at home. The measures show that people began curbing most out-of-home activity slightly before states ordered lockdowns, and that both lockdowns and social distancing continued to gradually increase over the second half of March.

Following up on its lockdown index, the bank next creates an overall US social distancing index comparable to our US lockdown index by taking an average of the residential activity measure and the inverted values of the four measures of out-of-the-home economic activity. The red line in Exhibit 2 shows the social distancing index.

The next chart compares Goldman’s US lockdown index with our social distancing index. People began curbing their out-of-home activity slightly before states began ordering lockdowns. This is particularly true of workplace and transit activity, though the initial stocking-up at grocery stores causes the overall social distancing index to fall slightly later. Over the second half of March, social distancing continued to rise as state orders went into effect.

Looking at the data, Goldman then draws three conclusions.

First, all three types of state orders reduced economic activity and increased time spent at home.

Second, while state-level shutdown orders played a meaningful role in the decline in activity, they account for only a minority of it.

Third, there was greater social distancing in states with faster daily growth of new virus cases.

In summary, each state was locked down and began practicing social distancing within a fairly short period of time. In contrast, state governments will likely remove these lockdown measures in a much more disparate manner than they applied them, reflecting differences in local virus conditions and differences in balancing public health risks against the costs of keeping the economy shut down.

Goldman’s analysis leads to two key implications for the eventual reopening of the economy.

First, lifting state lockdown orders—likely in a more disparate manner across states than they were applied—should provide a boost to economic activity, but will not be sufficient on its own to bring most economic activity back unless the virus is also under control.

Second, reducing the local rate of spread of the virus should increase economic activity, even with lockdown orders still in place.

Scaramucci’s SkyBridge Plunges 22% After Structured Credit Fiasco

One of the best performing hedge fund investments in recent years was structured credit, or highly-levered claims on streams of cash flows, such as mortgages, credit cards and corporate loans, which printed outsized returns for much of the past decade as rates were low, volatility was lower and investors could use up to 10x leverage (via repo) to extract generous returns from such products. And, inversely, structured credit was also one of the hardest hit strategies in March when stocks and credit plunged and when cash flow across the economy ground to a halt as a result of the economic paralysis resulting from the coronavirus pandemic.

That was especially bad news for Anthony Scaramucci, whose SkyBridge Fund of Funds (or FoF) just happened to have handed most of its $5.9 billion in capital to hedge funds that has invested in such highly leveraged products. Worse, not only did the performance of SkyBridge’s clients plunge, but many of them gated Saramucci, who would find himself unable to pull out his clients’ capital – an especially precarious situation if he were to suffer a surge in redemptions. In effect, SkyBridge was not only a second-degree bet on structured credit – arguably the worst hit space in capital markets in March – but it was stuck holding all the downside without even having access to its funds.

As the WSJ reports, Scaramucci’s SkyBridge – a FoF which invests billions of dollars in hedge funds for wealthy clients, which was prominently featured in that disaster of a movie, Wall Street 2, and which is best known for organizing the annual SALT Las Vegas boondoggle where shitty investors hang out with even shittier capital allocators but because they are surrounded by strippers, everyone feels really important – lost 22.5% in March in its flagship fund, and down 21.9% YTD. Amusingly, some of SkyBridge’s hedge funds “have blocked SkyBridge and other investors from withdrawing money as they grapple with redemption pressures or less liquid markets.”

The pressure, according to the WSJ, “is among the most imposing Mr. Scaramucci and SkyBridge have faced.”

A former Goldman Sachs Group Inc. broker, “The Mooch” has long been a prominent voice in the hedge-fund industry. In 2017, he gained a national platform as the White House’s director of communications. That ended after only 10 days on the job, after the New Yorker magazine published an expletive-filled interview with him in which he attacked other top staffers in the White House. Scaramucci subsequently returned to SkyBridge, which managed $5.9 billion at the end of January. A managing partner at SkyBridge, he regularly makes media appearances to discuss markets, the economy and his critique of the Trump administration.

SkyBridge’s infatuation with structured credit began in 2016, when its main product called Series G made a big bet on hedge funds that invest in structured credit. And, as noted above, the move proved profitable, helping SkyBridge grow in size over the past few years.

But that party ended with a bang in March when the firm’s Series G structured credit vehicle – which had invested more than $4.8 billion at the end of February – suffered dramatic losses after being positive for the year for the first two months of 2020.

The value of credit-related investments collapsed as investors fled low-rated debt amid worries the new coronavirus pandemic would crush consumers and other borrowers. Some of those markets suffered from limited trading. The troubles caused steep losses for a wide swath of funds in SkyBridge’s portfolio, partly because a number of them used leverage, or borrowed money, to juice their returns. That forced many of the funds to scramble to meet margin calls from lenders.

Angelo Gordon’s AG Mortgage Value Partners fund, one of Series G’s biggest investments, was down 31% for the month. Another SkyBridge investment, Metacapital Management LP, lost more than 50% in March in one fund SkyBridge is invested in and was selling assets in recent weeks to meet margin calls, according to people familiar with the firm.

Adding insult to injury, some of the funds SkyBridge had invested in including the EJF Debt Opportunities fund, Medalist Partners Harvest Fund and Metacapital Mortgage Opportunities Fund, recently told SkyBridge and other clients they wouldn’t be able to withdraw their money.

Another firm with SkyBridge money, Hildene Capital Management, is restructuring two funds into different share classes, letting clients choose how quickly to get their cash back.

But wait, there’s more: SkyBridge also was hit by the returns of some funds that don’t invest in credit. JD Capital Management’s Tempo Volatility Fund, a relative-value volatility fund, lost 75% or more for the month.

“It’s a battle for all of us,” a hedge-fund manager who invests in structured credit told the WSJ.

And indeed it is: a furious battle to the death for billionaires to stay in the tres comas club, or else suffer the indignity of being only multi-millionaires if not bailed out by the Fed.

* * *

That said, the full magnitude of losses for many funds SkyBridge invested in is unclear because the funds are awaiting administrator valuations for their fund assets, but the funds generally have provided clients with estimates of losses, according to the WSJ.

Amusingly, some of SkyBridge’s funds told their investors they believe technical issues have led to dysfunctional credit markets and that asset prices will recover in the long term. Hildene and Axonic Capital, another fund SkyBridge is invested with, are seeking to raise or have raised new money to invest.

Because what better way to not prove to the world you are a Ponzi scheme than to demand new capital even as you gate old capital from being withdrawn.

Meanwhile, the next time Scott Wapner defends the Fed’s intervention in capital markets by purchasing junk bonds or claiming the bailout of Wall Street is for the benefit of everyone, what he really means is that it is the Fed’s sworn duty to make sure that millionaires such as Anthony Scaramucci are made whole. Everyone else can just wait for their $1,200 “stimulus” paycheck from the Treasury.

President Trump is not going to fire Dr. Anthony Fauci from his coronavirus task force after sharing a tweet with the hashtag #FireFauci on Sunday, according to the White House.

“This media chatter is ridiculous — President Trump is not firing Dr. Fauci,” said spokesman Hogan Gidley in a statement, adding “Dr. Fauci has been and remains a trusted advisor to President Trump.”

Trump shhared a tweet from former GOP congressional candidate DeAnna Lorrainee criticizing Fauci’s Saturday interview with CNN in which he suggested that if Trump had listened to medical experts earlier he could have saved more lives, which included the #FireFauci hashtag.

“Fauci was telling people on February 29th that there was nothing to worry about and it posed no threat to the US public at large,” the tweet continues.

Sorry Fake News, it’s all on tape. I banned China long before people spoke up. Thank you @OANNhttps://t.co/d40JQkUZg5

“The President’s tweet clearly exposed media attempts to maliciously push a falsehood about his China decision in an attempt to rewrite history,” Gidley told People, while lauding the “bold decisive action” of the Trump administration’s late-January decision to halt travel from China, which Trump has repeatedly noted drew scrutiny from the left.

“It was Democrats and the media who ignored Coronavirus choosing to focus on impeachment instead, and when they finally did comment on the virus it was to attack President Trump for taking the bold decisive action to save American lives by cutting off travel from China and from Europe,” Gidley added.

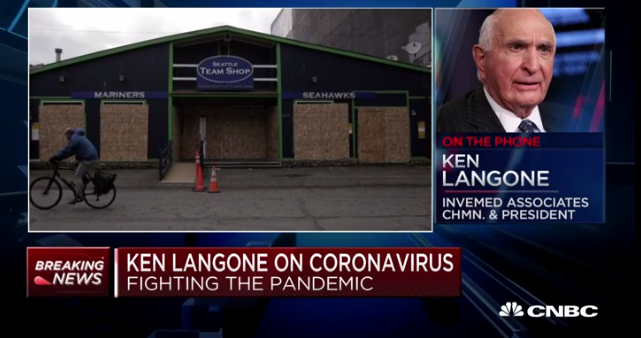

“We Will Survive This” – Billionaire Ken Langone Blasts “Disgusting” Media Over Virus Coverage

Ken Langone, the co-founder of Home Depot Inc., was on CNBC’s ‘Squawk Box’ Monday morning and blasted the media’s coverage of the COVID-19 pandemic.

Langone started the interview by saying the media gets a “big fat F” for its coverage on the pandemic and is inciting division at a time when the country needs to unite.

“The point is, let’s talk about the positives. I’m tired of me having a feeding frenzy. And by the way, I’ll tell you when all the Postmortems are done? On all the Postmortems are done. The media and my opinions, it’s gotta get a big fat F. Its done nothing. It’s nothing but incite differences. At a point in time where the house was on fire, there out there putting gas on it because its fun or whatever they think it is right now. We need unity like never before, and we’re getting it but getting it done.”

Langone goes on to say there’s a lot of positive stories of Americans “making sacrifices” for the benefit of the country. He said all Americans must do their part via ‘obeying’ public health orders to flatten the curve. Langone then adds, the only people not doing their part is the mainstream media that continue to overhype the pandemic.

“The doctors, the nurses, the truck drivers go on and on, and the bus drivers, things are happening, people are making sacrifices for the benefit of all this. The least we can do is do our part, our part as citizens should be stay home, obey separation, all the things they want you to do. It is working. It is working well. Who’s not doing their part? My opinion, the media, both side. Stop, stop right now, tell the American people warm story, a wonderful story.”

CNBC’s Andrew Ross Sorkin responds to Langone’s comment by saying:

“We can argue all these points. And going back was this, and I’m not trying to start a fight with anybody but I don’t I don’t see it frankly. Had the media been allowed to do its job in China, which is a place that doesn’t allow the media to do its job. In January, we might not have this problem because the media’s job is to blow the whistle. That’s the job of the media. So when you read articles that that talk about what was going on inside the administration or not going on inside the administration or warning people about the possibilities of these things. And then the government not taking the right steps or taking the right steps. That’s The job of the media. That’s what the media is supposed to do and not to tell you warm and happy stories every day.”

Langone responds by saying: “Andrew, you are doing and what the media does, never admit they might have made a mistake,” adding that the American people will vote this November and be the final judge of the administration.

Sorkin says, “if you don’t have a thriving media that can provide real information, factual information to the public, and not information that’s being skewed left and right. And I agree, by the way, it’s not always skewed the way you want it to be. But without it, you don’t have a functioning democracy. And you see what happens in countries where it doesn’t exist.”

Langone responds: “Let me make a confession. Democracy dictates and needs vibrant, objective media.” He provides a recent example of how a reporter in an interview twisted his story. Langone said it was “disgusting.”

“I’m tired of the media having a feeding frenzy here,” says Ken Langone. “When all the postmortems are done the media, in my opinion, is going to get a big fat F.” pic.twitter.com/FhIeZOdDbo

“On the front lines you can’t believe the heroism–the enormous effort being made by the doctors, nurses,” says legendary investor Ken Langone. “I’m seeing heroism, generosity–the effort that is being made is magnificent. It should make you feel so proud to be an American.” pic.twitter.com/BPfR8rq2nV

Langone has been a supporter of President Trump for years. His appearance on CNBC comes as the mainstream media has demonized the president’s response to contain the virus.

The Federalist provides a solid timeline of the president’s response to the virus, which by the way, shows he was “on top of it while Joe Biden was mocking” the outbreak.

The hypocrisy by the media is stunning, the New York Times tweeted on January 9: “There’s no evidence that the virus, a coronavirus, is readily spread by humans, and it has not been tied to any deaths. But health officials in China and internationally are watching it carefully.”

There’s no evidence that the virus, a coronavirus, is readily spread by humans, and it has not been tied to any deaths. But health officials in China and internationally are watching it carefully. https://t.co/7PPJvjyCox

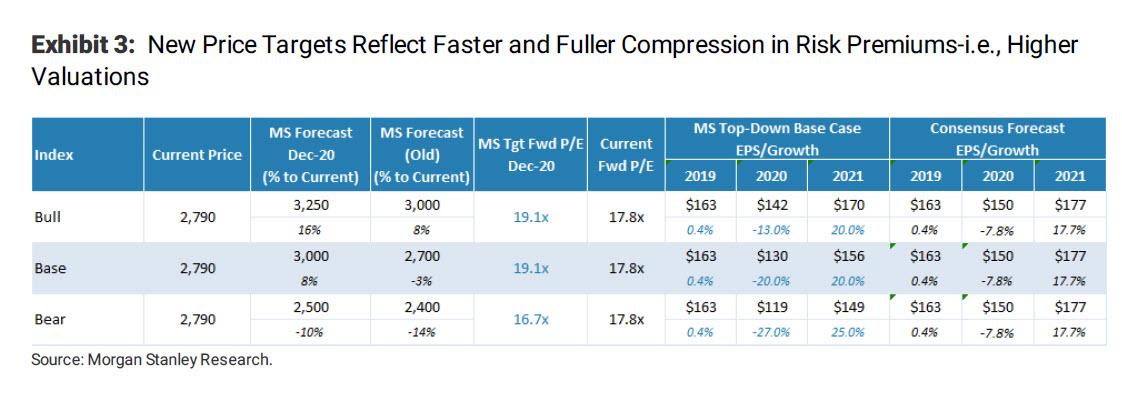

“Don’t Fight The Fed”: Wall Street’s Former Biggest Bear Goes All In, Raises S&P Price Target To 3,000

For much of 2019, Morgan Stanley’s chief equity strategist Michael Wilson issued a weekly sermon of fire and brimstone in his Monday Morning market takes, which contrasted with the euphoric pronouncements by his peers at other banks – most notably Goldman, which in December hilarious declared that the US economy is “structurally less recession-prone today” (which also meant especially depression-prone), which probably explains why three months later the same bank cut its Q2 GDP estimate to -34%…

… earning him the moniker of Wall Street’s biggest bear (a few permabearish exceptions such as Albert Edwards were excluded from the tally), not to mention quite a few angry clients.

Then, in November, just as the melt up phase of the post “Not QE” market was kicking in sending stocks to all time highs every single day, Wilson got the proverbial tap on the shoulder, and threw in the towel raising his S&P “bull case” price target to 3,250, however not without a slew of warnings that the most likely outcome was another retest in stocks lower.

In retrospect, Wilson should have held fast to his bearish conviction as the unprecedented March market crisis confirmed he was spot on (even if for different reasons).

And yet, demonstrating just how fickle Wall Street fates can be, just as Goldman turned beyond bearish (before again flipping today and chasing the market, now expecting a rebound in stocks removing its downside case of S&P 2,000 and expecting the index to rise to 3,000 by year end) Wall Street’s “biggest bear”, Michael Wilson turned bullish when two weeks ago when, paraphrasing Michael Hartnett who famously says that “markets stop to panic when officials start to panic”, he said that “crises lead to bailouts and this time it’s extreme given health angle. As a result, the inevitable credit crunch could be truncated this time, leaving us buyers of dips.”

Given that most stocks have been in a bear market for two years or longer, we recommend investors start buying stocks now because we cannot be sure if the next pull back will lead to lowers lows or not given we already experienced forced liquidation. Bottom line, we believe 2400-2600 on the S&P 500 will prove to be very good entry points for those with a time horizon of 6-12 months. – Michael Wilson, March 30

Fast forward to today when, as noted earlier Goldman also capitulated on its brief infatuation with bearishness and turned bullish expecting the S&P to ramp right back to 3,000, Wilson doubled down and urging his clients “not to fight the Fed” on Monday morning raised his S&P500 base case to 3,000 from 2.750, to wit:

Don’t Fight the Fed. The Fed surprised again last week, this time offering up to $2.3T in loan support while moving further down the quality curve with their secondary market purchases pushing into high yield. This move is in-line with our prior view that investors should have no doubt about the Fed’s resolve to do whatever it takes to make sure this recession does not turn into a depression.

Wilson then notes that while “most investors have been expecting more out of the Fed, based on our conversations with many clients on Thursday and over the long weekend, this salvo from the Fed far surpassed expectations in terms of size and scope.”

Amusingly, Wilson almost goes so far as to agree with Deutsche Bank that free markets no longer exist when he notes that “in fact, [the Fed] now appears to be trying to limit the healthy damage we typically get from a garden variety recession. As noted in our prior research, we think the nature of this recession–the unprecedented suddenness and trajectory of the contraction centered on a health crisis–has provided absolute cover for policy makers to go well beyond traditional support.”

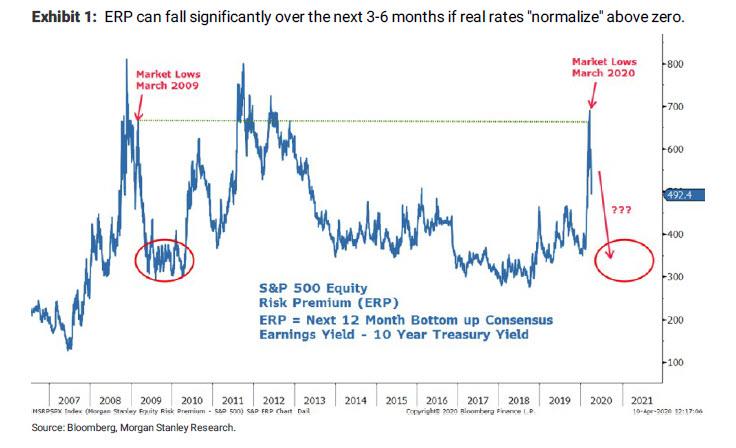

As a result, Wilson – agreeing with Goldman and virtually everyone else that the Fed will not allow another drop in stocks – is raising his year-end S&P Bear/Base/Bull Targets to 2500/3000/3250:

Our target increases are purely a reflection of higher multiples resulting from a faster and fuller normalization of the equity risk premium. If there is one lesson we have learned during the financial repression era it’s that when risk premium appears, you better take it before it quickly disappears.

Ironically even as he hikes his S&P price targets, Wilson lowers his 2020 EPS forecasts while our 2021 forecasts, and concludes that while a “pullback is likely after last week’s run but we think it will be shallower (i.e. 2550- 2650) than the consensus.” Finally, echoing what he said on March 31, the MS strategist repeats that “pullbacks should be bought (aka “Buy the Dips”).” Some more details:

The price target increases are purely a reflection of higher multiples that result from a faster normalization of the equity risk premium (ERP) much like we are seeing with credit spreads [ZH: where the Fed is now active in the market by openly purchasing bonds]. We see no reason investors won’t begin to discount the Fed’s direct intervention into equity markets if necessary, which by definition reduces the tail risk and therefore the risk premium. At Friday’s closing price of 2790, the S&P 500 is now sporting an ERP of just 492bps which is well below the peak of 700bps at the March lows. However, bear in mind that the average ERP is closer to 350bps in the post GFC, financial repression era–an era we are clearly still in. Some may argue it’s too early to see a compression of the ERP back to normal while we are still in this crisis, and we would agree. However, by year end that will not be the case and that is what our price targets reflect…year end, not today.”

Finally, Wilson thinks it’s “instructive” to look at the GFC as a equally uncertain time for financial markets and highlights that following the ERP of 700bps at the March 2009 market lows, “it only took 3 months for it to fall back into a range of 300-400bps in which it remained for the next year. If there is one lesson we have learned during the financial repression era it’s that when risk premium appears, you better take it before it quickly evaporates. We don’t see why this time it’s any different given policy makers have once again illustrated what they are capable of doing.”

There is another reason why Wilson is doubling down on bullish: the coming runaway inflation, as he first hinted two weeks ago:

Another counter argument to this view is one we were making before the market dropped so sharply–that the ERP should be higher when real 10-year yields are in negative territory, like today. As discussed last week, we believe inflationary pressures may be building more than appreciated given the massive targeted fiscal stimulus, in conjunction with other ongoing trends in populism, nationalism, de-globalization and a worldwide pushback to the US dollar as the only reserve currency. As these inflationary pressures become more apparent, we suspect nominal and real interest rates can rise more than the consensus believes as market participants begin to demand a greater term premium. A materially weaker US dollar would accentuate such a new trend. As is usual with new trends that go against the consensus, they tend to be slow at first and then accelerate quickly, which is why it’s imperative to be thinking about them before they happen.

The bottom line, Wilson writes “is that stocks are beneficiaries of rising inflation. The recent rise in breakevens has been much greater than the recent rise in nominal yields, leaving real rates in negative territory. The rapid fall in ERPs over the past few weeks suggests the equity market may be moving ahead of the rates market in anticipation of the changing regime described above. If the Fed wants higher equity prices as a means of loosening financial conditions, we believe it could stop buying long dated Treasuries and let the back end move up with breakevens until real rates move into positive territory. 50-75bps real 10 year rates seems to be the sweet spot for equity valuations.”

Based on all of the above, the Morgan Stanley strategist is raising his base and bull price targets for the S&P 500 by 250 points to 3000, and 3250, respectively. His bear case rises by only 100 points to 2500 given the severity of the negative tail outcome. With respect to his earnings forecast, the 2020 bull and base case revert to our prior base and bear cases while our bear case moves to the GFC outcome we analyzed in our last 2 weekly warm-ups.

In short, Morgan Stanley is lowering its EPS forecasts today for 2020 to reflect a worse near term outlook. For 2021, the snap back is related to the severity of the decline in the 2020–the worse the decline the bigger the bounce: “The net effect of this is that our EPS forecasts don’t change much for 2021 which is the year that really matters for stocks. As we have said many times, the market now views 2020 as a write off and is trying to figure out the path of earnings in 2021.”

What does this mean in practice? It means that to get to a 3,000 price target in the S&P and applying the “base case” EPS of 130, Wilson is using a 23x forward P/E multiple to get there, the highest PE multiple in this cycle! Is that high? Why yes, it is, but ignore 2020 earnings, Wilson says, because he is confident that he will be correct about his 2021 earnings forecast of 156… which is a far more “reasonable” 19.1x PE.

This, ladies and gents, is called goalseeking to reach a specific target, one which confirms that the present market and the underlying fundamentals are not only completely disconnected, but also which takes a priced to perfection forecast of the future which as every strategist admits is unpredictable due to the unprecedented nature of the current economic depression, yet which everyone is absolutely certain will have a happy ending. Why? Because of the Fed, the same Fed which has been forced to nationalize capital markets to avoid an up to 80% drop in stock prices.

Doctors Fear Coronavirus Survivors May Have Lasting Damage To Multiple Organs

Doctors treating coronavirus patients have begun to worry that survivors may sustain lasting damage to several organs – not just the lungs, according to the Los Angeles Times.

For the sickest patients, infection with the new coronavirus is proving to be a full-body assault, causing damage well beyond the lungs. And even after patients who become severely ill have recovered and cleared the virus, physicians have begun seeing evidence of the infection’s lingering effects.

In a study posted this week, scientists in China examined the blood test results of 34 COVID-19 patients over the course of their hospitalization. In those who survived mild and severe disease alike, the researchers found that many of the biological measures had “failed to return to normal.” –Los Angeles Times

One alarming observation have been test results indicating that recovered patients continue to have impaired liver function after patients had been cleared for discharge.

Another concern from cardiologists are the immediate effects of COVID-19 on the heart, raising questions over how long the damage may last. As the Times notes, “In an early study of COVID-19 patients in China, heart failure was seen in nearly 12% of those who survived, including in some who had shown no signs of respiratory distress.“

Heart damage can easily occur when the lungs cannot deliver sufficient oxygen to the body, however when this happens without respiratory distress, “doctors have to wonder whether they have underestimated COVID-19’s ability to wreak lasting havoc,” according to the report.

“COVID-19 is not just a respiratory disorder,” according to Yale cardiologist Dr. Harlan Krumholtz, who added “It can affect the heart, the liver, the kidneys, the brain, the endocrine system and the blood system.”

Of course, there are no long-term survivors of the disease – which was unknown to mainstream science less than five months ago. Even its first victims in China are just over three months removed from their ordeal, while physicians swamped with the ongoing pandemic have been too busy treating critical patients to closely monitor the some 370,000 patients classified as ‘recovered.’

Still, doctors are worried that in its wake, some organs whose function has been knocked off kilter will not recover quickly, or completely. That could leave patients more vulnerable for months or years to come.

“I think there will be long-term sequelae,” said Yale cardiologist Dr. Joseph Brennan, using the medical term for a disease’s downstream effects.

“I don’t know that for real,” he cautioned. “But this disease is so overwhelming” that some of the recovered are likely to face ongoing health concerns, he said. –Los Angeles Times

Meanwhile, questions have emerged over whether COVID-19 actually leaves the body – possibly lying dormant for years only to re-emerge later in a different form.

Several viruses already do this such as chicken pox – which can come back as shingles, and hepatitis B, which can cause liver cancer years after the primary infection clears up. Ebola is another example – hiding in the vitreous fluid of victims’ eyeballs in some cases, causing blindness or impaired vision in 40% of survivors.

Of course, then there’s the lungs – which the novel coronavirus tends to target first. In another closely related coronavirus, severe acute respiratory syndrome (SARS), around 1/3 of recovered patients had impaired lung function after three years – though they largely resolved over the next 15 years. And, 1/3 of those who survived Middle East Respiratory Syndrome (MERS) had permanent scarring of the lungs known as fibrosis.

According to a mid-March publication which tracked a dozen COVID-19 patients discharged from a Hong Kong hospital, two or three reported having difficulties with activities they had no problem performing in the past.

Dr. Owen Tsang Tak-yin, director of infectious diseases at Princess Margaret Hospital in Hong Kong, told reporters that some patients “might have around a drop of 20 to 30% in lung function” after their recovery.

Citing the history of lasting lung damage in SARS and MERS patients, a team led by UCLA radiologist Melina Hosseiny is recommending that patients who have recovered from COVID-19 get follow-up lung scans “to evaluate long-term or permanent lung damage including fibrosis.”

As doctors try to assess organ damage after COVID-19 recovery, there’s a key complication: Patients with disorders that affect the heart, liver, blood and lungs face a higher risk of becoming very sick with COVID-19 in the first place. That makes it difficult to distinguish COVID-19 after-effects from the problems that made patients vulnerable to begin with — especially so early in the game. –Los Angeles Times

And while doctors and researchers are still discovering COVID-19’s secrets, what they do know is that when patients show signs of infection, several organ systems are affected – and that when one begins to fail, others often follow. This is all wrapped in an inflammatory response, which can pry “plaques and clots from the walls of blood vessels and causing strokes, heart attacks and venous embolisms,” according to the report.

Dr. Krumholtz, the cardiologist, says the infection can cause damage to the heart and the sac which encases it, causing heart failure and arrhythmias in some patients during the acute phase. This means that former COVID-19 patients can become lifelong cardiology patients after they ‘recover’ from the primary illness.

What’s worse, blood abnormalities that can make clots more likely can persist as well.

In a case report published this week in the New England Journal of Medicine, Chinese doctors described a patient with severe COVID-19, clots evident in several parts of his body, and immune proteins called antiphospholipid antibodies.

A hallmark of an autoimmune disease called antiphospholipid syndrome, these antibodies sometimes occur as a passing response to an infection. But sometimes they linger, causing dangerous blood clots in the legs, kidneys, lungs and brain. In pregnant women, antiphospholipid syndrome also can result in miscarriage and stillbirth. –Los Angeles Times

Yale’s Dr. Brennan says that at the end of the day, we just don’t have enough data to make a long term prognosis for coronavirus patients.

Global capital markets are not pricing in the growing likelihood that defaults by large corporate borrowers in emerging markets will rise, which will set up another cascade of market events like the downward trajectory we saw in 1997.

Despite the massive programs that have been swiftly put in place by central banks and fiscal authorities around the world, global capital markets remain extremely fragile. After a long cascade of negative shocks to the global economy, yet another lurks on the horizon. Many investors in the United States and elsewhere have yet to focus on the vulnerabilities faced by emerging market (EM) countries and corporations. Proof of investor complacency is clearly evidenced in the largest emerging markets bond exchange-traded fund (ETF). Currently, that ETF yields just 5 percent, not much higher than it yielded at the beginning of the year.

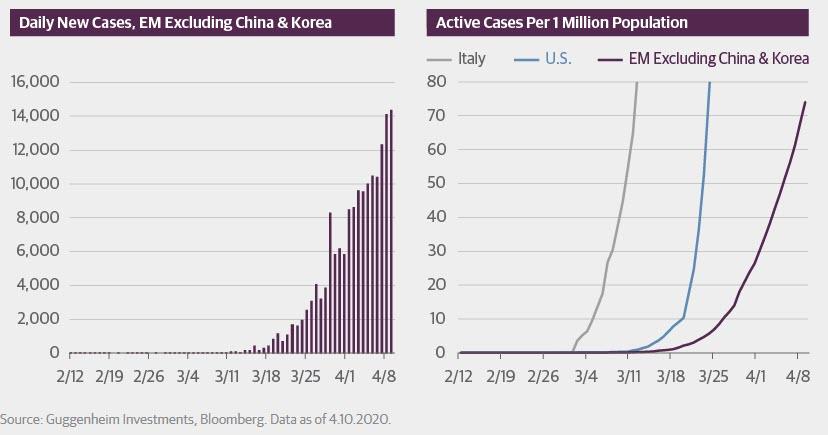

Investors seem to ignore the fact that while the global economic shutdown is synchronized, the spread of the virus is not. Daily new cases of COVID-19 are growing rapidly in EM countries (excluding China and Korea) as they begin to decline in parts of the developed world.

COVID-19 Cases Rising in the Emerging Markets

Source: Guggenheim Investments, Bloomberg. Data as of 4.10.2020.

The emerging markets soon will be hit very hard by the global pandemic. The pandemic will be followed by goods and food shortages, and social unrest. Before the virus hit them directly, EM countries had already been adversely affected by falling commodity prices and the economic impact of the shutdown in China and other parts of the developed world. Most EM countries have very weak healthcare systems, nowhere near enough hospital beds and respirators, crowded cities and slums, and large numbers of workers in the economy who are paid daily wages or work in the informal economy and can’t work remotely. For many EM countries, this pandemic will quickly escalate from a health crisis to a humanitarian crisis, and ultimately to a solvency crisis. Political stability will be the last domino to fall.

An Emerging Markets Crisis Could be the Next Shoe to Drop

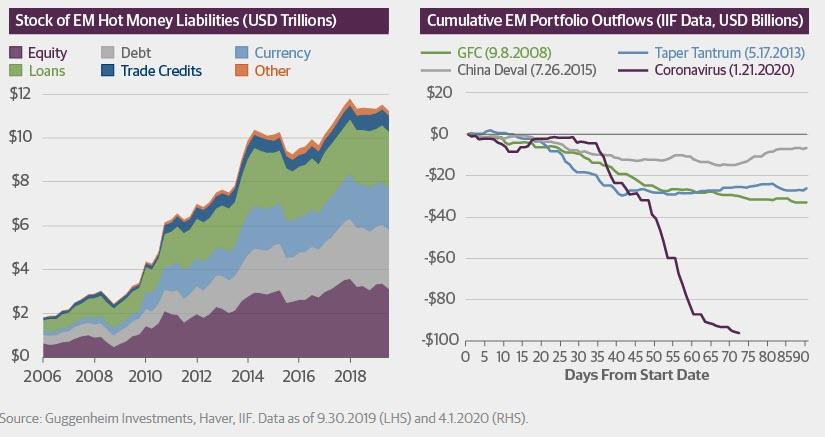

The current mispricing in the face of these challenges and the systemic risk that they pose to global markets is happening despite an unprecedented surge of capital flight from emerging markets. The outflows of hot money capital—equity, debt, currency, loans, trade credits—are weighing on foreign currency reserves holdings, as countries intervene to defend currency pegs, dampen volatility, prevent a spike in the local currency value of foreign currency obligations, and deter further capital outflows as a result of currency depreciation.

Capital Flight Weighing on EM FX Reserves

Source: Guggenheim Investments, IIF, Haver. Data as of 4.10.2020.

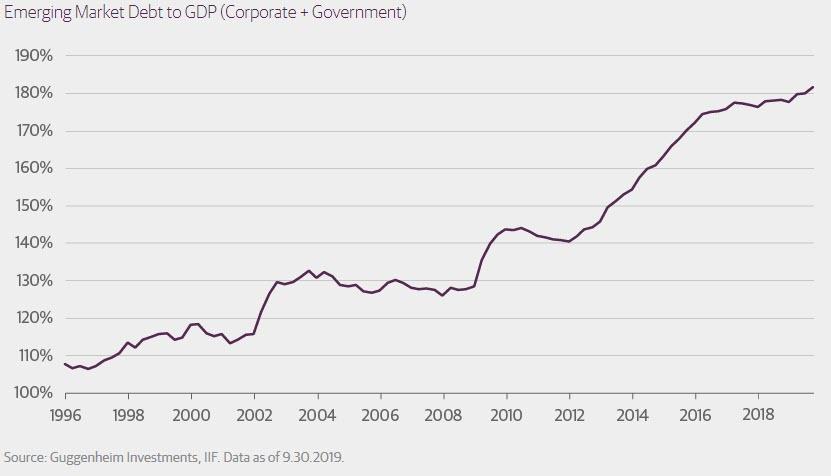

The total debt of EM governments and corporations as a percentage of gross domestic product (GDP) is significantly higher than it has ever been. Collectively it stands at over 180 percent, up from 110 percent during the Asian debt crisis. In recent months, many EM countries—such as Brazil, South Africa, Argentina, Ukraine, Nigeria, and Indonesia—have seen some market pressures reflected in widening credit default swaps (CDS) and cash bond spreads, in addition to currency depreciation.

Emerging Markets Are Highly Vulnerable in this Environment

Emerging Market Debt to GDP (Corporate + Government)

Source: Guggenheim Investments, IIF. Data as of 9.30.2019.

One of the most disturbing aspects of emerging market debt is the record amount of dollar-denominated securities that have been issued by EM corporations during the past decade. This contrasts with the Asian debt crisis, when it was sovereign borrowers and banks that were unable to access hard currency to service debt and fund large current account deficits.

My biggest concern is that this crisis will be much deeper and more prolonged than people anticipate, which leaves a lot of space for another shoe to drop in the global financial crisis. A default or debt restructuring in the emerging markets will likely lead to an increase in borrowing costs just as their economies are contracting. Like in the United States, EM countries will engage in fiscal stimulus, which will cause fiscal deficits to balloon. Borrowing costs in most of these countries have already been rising over the course of the last month or so, and at some point, the debt will become prohibitively expensive. Rising borrowing costs will limit the fiscal flexibility needed to address the public health and economic crises in these countries.

Just as in the United States, EM countries will look to their central banks to monetize the debt, but monetary policy space is also constrained. Rich countries can drop helicopter money on their economies with relatively little consequence, but EM monetary and fiscal solutions will further weaken their currencies, making access to dollars even harder for corporations that are also experiencing a slowdown in cash flows. In time, EM corporate defaults will rise, adversely affecting the ability of other borrowers from the developing world to get access to credit in the global financial markets.

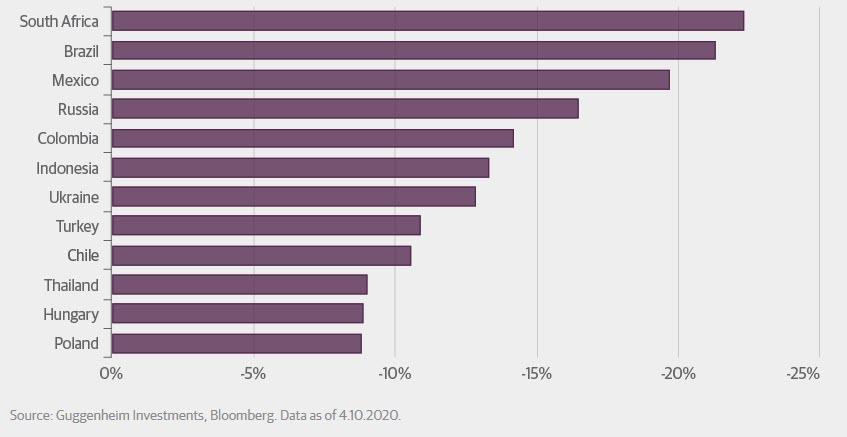

EM Currencies Have Been Battered by COVID-19, With More Pain to Come

Year-To-Date Currency Performance Versus the U.S. Dollar

Source: Guggenheim Investments, Bloomberg. Data as of 4.10.2020.

Multilateral institutions like the International Monetary Fund (IMF) were very effective during the Asian crisis because they were able to funnel dollars to governments that needed help when their local currencies collapsed, conditional on countries pursuing needed economic reforms. This time, however, it will be harder for the IMF to reach the entities in need of assistance because it doesn’t directly interact with EM business communities. The IMF will need to work with EM governments to build the infrastructure enabling corporate borrowers to obtain foreign currency, including dollars, as needed. Stabilizing economies and balance of payments dynamics will be much more challenging in light of the sudden stop in economic activity caused by COVID-19.

The scale of action required at this time is far greater than any of us would have contemplated even a few weeks ago. The global contraction in output will be very similar to the contraction during the second world war when a significant percentage of output was wiped out due to the destruction in Europe. Easily a 20 percent decline in the approximately $10 trillion in GDP outside G20 countries will result in a demand gap of about $2 trillion that will need to be filled to keep these economies functioning at their current levels. By comparison, in the United States we have about a $22 trillion economy, so the estimated 10–15 percent contraction in GDP will mean that a demand gap of about $2 trillion to $3 trillion will need to be offset with government stimulus.

Currently, the demand gap in the United States is being partially filled by aggressive fiscal and monetary policy. But it will be a challenge to fill the demand gap in emerging markets. I believe it will take a coordinated effort on the scale of Bretton Woods to develop a monetary infrastructure that will enable emerging market countries to manage through this and future crises. The IMF and World Bank, which were established at Bretton Woods, are well-situated to play a leading role in this effort, but they will need the rich countries of the developed world to coordinate and provide the resources. This is a huge challenge, not least because growing nationalism in various parts of the world, the rise of China as a geopolitical counterweight to the United States, and domestic fiscal strain at home will result in even less willingness to engage in international policy coordination.

In the short run, policymakers—including the IMF, which holds its Virtual Spring Meetings this week—are already discussing possible steps to address this looming problem. Some solutions have been tried in past sovereign debt crises, to varying degrees of effectiveness, while others are new ideas. For example, details are being worked out on an arrangement for the G20 countries to offer relief on bilateral loan repayments to 76 of the world’s poorest nations. It is a start, but this kind of debt moratorium will likely need to be expanded. Other possible remedies for addressing an EM debt crisis include governments and other supranational agencies providing credit enhancement and loan guarantee programs for corporate borrowers, or expanding the IMF’s Flexible Credit Line (FCL) to meet the demand for crisis-prevention and crisis-mitigation lending.

Fragile credit markets will be supported by the right policy measures, but the more important beneficiaries of these programs are the people of the developing world. They are at the mercy of a rampaging pandemic and an economic system that is not prepared to cope with it. The spread of the coronavirus is showing us how our interconnected world renders us all vulnerable to common health and economic risks. If policymakers in China, Europe, Japan, and the United States are well-informed about how damaging a collapse in the developing world would be, not only to themselves but to the rest of the G20, there would be greater support for building a framework to help stabilize and rebuild from the devastation we are about to experience.

IRS Deposits First Batch Of Coronavirus Stimulus Payments To Broke Americans

Relief for Americans affected by the economic crash due to COVID-19 shutdowns started over the weekend when the IRS tweeted it began to deposit stimulus payments into the bank accounts of eligible Americans.

“#IRS deposited the first Economic Impact Payments into taxpayers’ bank accounts today,” the IRS tweeted.

“We know many people are anxious to get their payments; we’ll continue issuing them as fast as we can.”

The stimulus payments are the centerpiece of the $2.2 trillion rescue package to cushion the country during a collapse in economic growth triggered by the pandemic. A much broader disruption of the payments is expected this week.

Those who make $75,000 or less are expected to receive $1,200 checks. Married couples who make less than $150,000 will be issued $2,400 checks and $500 per child under 17.

A press release via the House Ways and Means Committee Republicans said the first round of payments would be made into people’s bank accounts who are eligible. The first round of payments could provide some form of relief for about 60 million people. Those who don’t use direct deposit will receive a check in the mail, that is expected to begin on April 20.

The IRS will base incomes from 2018 and 2019 tax returns to process the payments.

During the 2008 financial crisis, the government issued direct deposit stimulus payments that were distributed over three weeks, while paper checks took about ten weeks.

In terms of employment, today’s crisis is more severe than a decade ago, nearly 17 million people have filed for unemployment benefits in three weeks.

With the labor market in free fall, the difference between today and the 2008 crisis is that the unraveling has been the quickest ever. The unemployment rate has surpassed the 10% peak of the last recession, now somewhere around 13% or 14%, and likely to go much higher through April.

As for the stimulus checks, it will provide very little relief to consumers who have no savings, insurmountable debts, and are in a rent based society. There’s no timeline on when the economy will recover.

What I see is a global collapse of intangible capital that is invisible to most people.

It’s only natural that the conventional expectation is a return to the pre-pandemic world is just a matter of time. Whether it’s three months or six months or 18 months, “the good old days” will return just as if we turned back the clock.

I think the situation is much more akin to being injured. Since I worked for decades in construction, I’ve had numerous potentially serious injuries, including slipping off roofs, being perched on ladders that fell, my finger sliced open by a steel stud, high winds peeling a heavy sheet of plywood off a stack and sending it flying into me, etc.

Immediately after impact, your first instinct is to assess how badly you’re injured. Of course we all hope we’re not seriously hurt, but the initial adrenaline-fueled relief can be misleading: we might have suffered internal injuries that we can’t feel.

That’s the global situation: we want to assure ourselves the injury is minor and we’ll be back on our feet in no time, but I think the financial-economic injuries are severe and to some branches of global capital and labor, fatal.

Those in power around the world crave one thing above all else: control. If you can’t control the situation and key assets, then what good is your supposed power? If you can’t control the situation and key assets, your power is illusory.

Those in power cannot completely control the forces unleashed by the pandemic. The tide has turned, and everyone trying to return their corner of the world to its pre-pandemic conditions is swimming against the tide–or shoveling sand against the tide, if you prefer that analogy. In either case, they will exhaust themselves and the tide will continue on, regardless of their titanic efforts to print money and maintain control of their populaces.

In my recent book, Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World, I focused on intangible capital, which includes all the forms of capital that cannot be commoditized and purchased for cash like goods and services. Intangible capital includes social capital, social stability, a diverse, resilient local economy and control of one’s own capital.

What I see is a global collapse of intangible capital that is invisible to most people. This includes confidence, trust in institutions and a complacent sense that the tide is carrying us all to greater prosperity.

The tide has reversed, and the key dynamics are income, net worth and costs. As I explained in The New (Forced) Frugality (March 28, 2020), incomes are falling and will continue to fall. Since income is the foundation of asset valuations, asset values will also fall. This will reverse the “wealth effect” that supported the enormous increases in spending and borrowing globally.

When our net worth is rising, we feel wealthier and are more likely to borrow and spend more, confident that our rising wealth will support the debt and higher expenditures. When our assets are declining in value, we feel poorer and are less likely to borrow and spend.

Income is fragile and prone to instant decay, while costs are extremely resistant to declines.

Consider stock valuations: the core driver is profit, which is revenues minus costs. As revenues drop and costs rise, profits vanish literally overnight. That sudden erosion of profits is global, and it will affect companies previously perceived as bulletproof. Facebook and Google depend on advertising, and with the global economy in free-fall, what’s the point in wasting scarce cash on marketing? Essentially no one needs a $1,000 iPhone or a $40,000 Tesla. Aspirational spending is as fragile as income.

Consider real estate: commercial real estate is based on the income generated by enterprises renting space. If businesses fold or stop paying rent, the value of the property falls accordingly.

Even residential real estate is intimately connected to income: as household incomes plummet, the number of potential buyers plummets, too. Institutional buyers of houses base the value on rental income, just like commercial property. As household income plummets, fewer people can afford sky-high rents, and so supply exceeds demand and rents will fall accordingly.

Consider bonds: the value of any bond, government or corporate, is based on the yield paid to the owner. While the general expectation is that yields will fall to zero because central banks are buying bonds, this may be less of a guarantee than generally assumed. The volume of bonds being issued may well exceed central bank buying, and yields (and interest rates) will rise despite central bank intervention.

The world depends on expanding debt to pay for government services and private-sector spending. Debt is also dependent on income; lenders who issue loans to households and enterprises with faltering income are very likely to lose money as these marginal borrowers default.

As income falls, lending dries up, as lenders cannot afford to risk making loans to people and businesses that are practically guaranteed to default. This is especially true for borrowers who are already burdened by existing debts.

As incomes decline, asset values decline and borrowing dries up. Once borrowing dries up, spending dries up, and enterprises and governments must cut payrolls by any means available: don’t replace retiring employees, cut wages and benefits, and eliminate overtime and bonuses.

As stock values fall, so do the value of employee stock options–another example of the reverse wealth effect.

Meanwhile, costs will continue rising as cash-strapped governments eventually seek more tax revenues and supply-chain shocks lead to higher prices.

We cannot go back to the pre-pandemic side of the river of time, and it’s dangerous to focus on returning to a time that has already been lost. We cannot go back, we can only go forward.