Air Force Aborts ICBM Test Flight Just Before Launch For Unknown Reasons

On Wednesday the US Air Force was moments away from a planned test of an unarmed nuclear Minuteman III intercontinental ballistic missile but aborted prior to launch, according to an official statement.

It was supposed to happen in the early morning hours at Vandenberg Air Force Base in California, but “experienced a ground abort prior to launch,” the Air Force Global Strike Command said. No further explanation was given as to why the test launch was shut down, other than the service indicating that the “cause of the ground abort is currently under investigation.”

The news release did however note that ballistic missiles are only launched when “all safety parameters with the test range and missile are met,” according to the news release. The launch is expected to be rescheduled pending the results of the investigation.

As a report in The Hill highlights, a debate is currently raging on Capitol Hill and in the halls of the Pentagon over the near-future viability of the program. “The failed test comes as lawmakers debate whether to proceed with the program to replace the aging Minuteman III missiles or try to extend the life of the missiles,” The Hill writes.

Currently some 400 three-state Minuteman III missiles form the critical land-based ‘last defense’ element in the US nuclear triad, and were first deployed in 1970 with an initial expected 10-year service life. But after undergoing multiple life extensions the Air Force has long argued for their complete replacement, but this would come at a hefty $1.2 trillion or more price tag.

US Strategic Command chief Adm. Charles Richard, who oversees America’s nuclear arsenal, has been pushing for the Ground-based Strategic Deterrent (GBSD) program to immediately replace the ageing systems.

“We simply cannot continue to indefinitely life-extend Cold War leftover systems,” Richard told Congress last month. “I do not see an operational reason to even attempt to do that.”

The Jackpot Chronicles Scenario #4: Atlas Shrugged

Never mind The Great Reset. Here comes The Great Reject.

It occurred to me that I never did finish the final instalment of last summer’s Jackpot Chronicles, wherein I posited four possible post-Covid scenarios.

For a quick refresher, The Jackpot is concept I cribbed from William Gibson. It’s a term he uses across a few of his near-future cyberpunk novels that describes a series of rolling global catastrophes that set in sometime around 2016 (his stories span multiverses, and timelines, but the common theme is that somewhere around 2016, some kind of irrevocable glitch in the matrix occurred that put a permanent end to normalcy as it has been understood up until that point).

If there was a Jackpot, whatever it was, it could arguably have happened at many points throughout the 20th century, or if we wanted to confine our speculation to the 21st century then, 9/11 or the GFC would do. Everything after that being symptomatic as opposed to causal.

And then… 2020 and COVID hit. That’s when the fabric of time cleaves us into the before times and The Jackpot.

The other post-pandemic scenarios from the rest of my Jackpot series were:

Force Majeure: The wheels come off completely and the system comes unglued. Mad Max.

Tin Foil Hat: It really is one Big Conspiracy and we’re into a New World Order.

I had thought the fourth scenario would be the one themed Deglobalization, and to a certain extent it still is. In the original outline I described that Deglobalization:

“Is where multi-national corporations, so shaken from this Near Death Experience, realizing their error of betting the farm on just-in-time supply chains, labour cost arbitrage and having zero buffers, begin pulling manufacturing back home.

The smart ones start building cushions and shock absorbers into their business logic, and they begin to eschew leverage after being on the wrong side of a series of cascading liquidity implosions. In other words, businesses begin to transition themselves into what I called “Transition Companies” as posited in the inaugural posting for [this blog]”.

I also went on to say that I considered this one most desirable yet least likely. My view on this scenario has changed somewhat, and I also think that the staggering government ineptitude and duplicity at all levels in all jurisdictions (with few notable exceptions) has made our regeared “4th scenario” more likely given that it’s in progress. Mass demonstrations, mass exoduses, crypto-currencies are symptoms of a Great Reject, or as I’ve renamed this scenario “Atlas Shrugged“.

The TL,DR of the novel, Atlas Shrugged is that once the institutional sclerosis of the ruling class was understood to be both incorrigible and irreversible, the only other option was a global opt-out. There was no Great Reset in Atlas Shrugged. They got The Great Reject instead.

Under the Atlas Shrugged scenario, deglobalization is just one of numerous motivating factors, but it’s mainly an outcome of a larger dynamic where all non-ruling factions in society lose faith in the prevailing structure of Neoliberal Globalism (a.k.a “Mr. Global”). With Mr. Global’s viability in question, people begin to look for the exits.

This begins to occur on two fronts. What Vilfredo Pareto called “the non-governing elites” begin to realize that the system which used to accommodate them, even rely on their tacit support, is now becoming hostile toward them. At the very least, the ruling elites are undermining their interests. This is part of the dynamic of Peter Turchin’s “elite overpopulation” that we looked at recently.

The other front is the comparatively powerless underclass, which, in pace with Pareto’s Theory of Elite Cycles, lose their moorings and standing within the system they are expected to adhere to. The social contract no longer seems to be a matter of middle-class protections and living standards but instead becomes starkly authoritarian and one-sided. What is clear is that the existing institutions are now functioning to defend the position of the overclass, not to uphold the rights and liberties of the underclass.

The culmination of multiple super-cycles (Pareto’s Elite Cycles, Turchin’s long term dynamics of sociopolitical instability, debt, a Fourth Turning, and a Maunder Minimum for good measure) combined with an accelerated onslaught of technological innovation: Internet, crypto-currencies …biotech? Nanotech? Micro nuke? Fusion? Quantum computing? We have all the necessary components for a complete breakdown of existing institutions and the total loss of legitimacy of the current governing elite class.

So it goes in our Atlas Shrugged scenario. Various interests of many forms and myriad factions, from dissident states (like Florida), to decentralized and virtual companies, emergent DAO’s, all the way to individuals and cultural tribes all begin to experience these moments of clarity in their own way. From there they will act in their own rational self-interests and cooperate with others doing the same in order to navigate the breakdown of Mr. Global.

In spite of this, Mr. Global’s prevailing policymakers and governance structures will frantically maneuver and spin narratives of fear and fantasy in order to keep the existing system on the rails.

They walked back the second one, but not the first one.

That is what The Great Reset really is: it’s an attempt at a zeitgeist-level rationalization that doubles-down on institutional failure on the part of the entire governance structure of Mr. Global, and gives them a new lease on life to remain in charge. Reimagined by the Davos crew, amplified by the mainstream media, lubricated by Big Tech.

The antidote to all of this are crypto-currencies, smart contracts and decentralization.

That antidote also brings significant upside regardless of which one of our four possible scenarios plays out.

When I listen to people who are complete denial about crypto, I realize that there is a common thread in their objections (what made me think about all this today was listening to Michael Pento’s criticisms of Bitcoin on George Gammon’s Rebel Capitalist. Pento’s 2012 book on the inevitable bursting of the bond bubble is a must read. That book helped be form the basis on what I think is the funds flow that is actually putting a floor under crypto. I don’t begrudge Pento for not seeing it, because as I’ll explain, he’s looking at it through the wrong lens)

We could go on for hours about how most of these people haven’t really delved into the technology or what it means, how their criticisms at the defects around Bitcoin apply even more accurately to US dollars (“backed by nothing”, “infinite supply”, “uses too much energy”, et al). But what they all have in common is that they all posit that whether Bitcoin and cryptos succeed or fail is premised on whether the existing establishment will permit it.

What will the Fed do? What if the government bans it? Won’t the World Bank just create their own CBDC?

This is completely inverted. They have it backwards. It’s not up to the existing system, because the existing system is over. That’s the part they don’t get.

The existing system should be looking for its place in the new reality of network states, not pontificating how it will run the new landscape. The coming system will be multipolar in not just the geopolitical dimension, but across cyberspace and the network dimensions as well.

Instead, the incumbent system is busy banning menthol cigarettes, imposing negative interest rates and undergoing mass conversion to a peculiar new religion called Wokeness.

It won’t work, and it brings to mind a particularly vivid example I once heard about a balloon disaster that still makes me cringe when I think of it:

A group of people were embarking on a balloon ride and as they were just a foot or two off the ground, the burner erupted into flames. The balloon pilot realized immediately what this meant and he leapt from the gondola which was still only a few feet off the ground.

One or two of the passengers were quick witted enough to realize what this meant and followed him. This set off a feedback loop: as the fire expanded, its hot air forcing the balloon higher, combined with the weight reductions as the first few people bailed out, the situation very quickly escalated past a point of no return.

The balloon had accelerated very rapidly to heights from which it was no longer possible to leap safely. The unfortunates who had hesitated and were trapped in a gondola being propelled higher by a fireball, to their inevitable doom.

That’s what our entire situation feels like today. The balloon is still hanging a foot or so above the ground, the canopy is on fire, and the people who have figured out what this means are bailing out while they can and in doing so they are accelerating the ultimate burn-then-crash of the entire system.

In Rand’s book they went to a hidden valley called “Galt’s Gulch” and used their skills and their resources to restore new communities while the old systems imploded. If this scenario plays out we’d be looking for people creating a decentralized, network of gulches. Seeking each other out who are pursuing this same goals, creating open protocols to to rebuild civil societies and autonomous communities built on the ageless principles of free markets, liberty and prosperity.

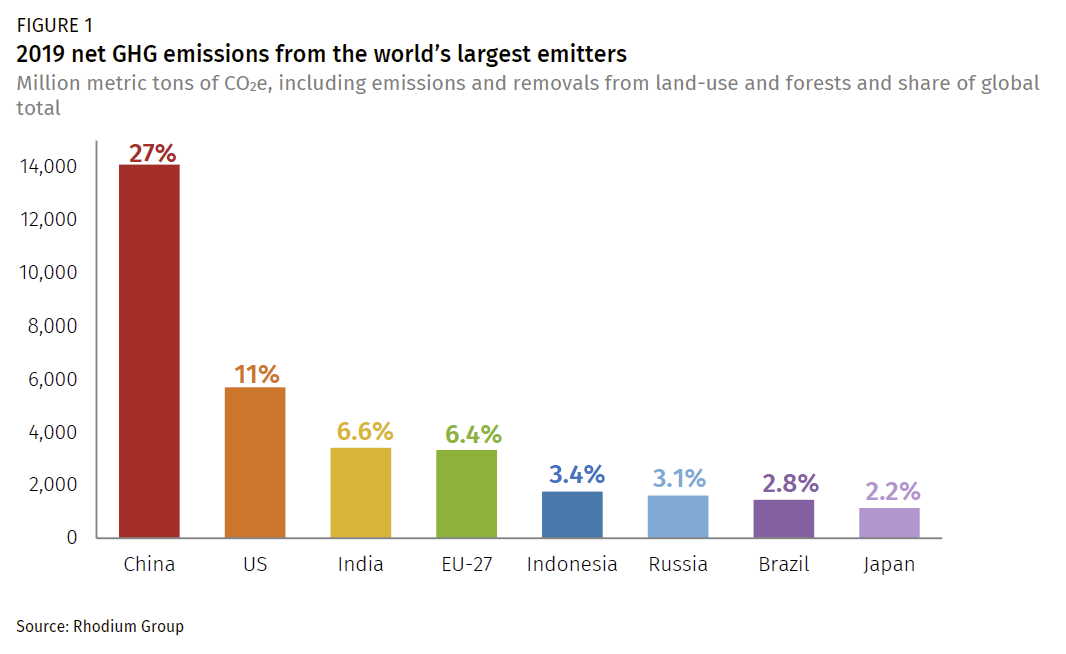

China Pollutes More Than US And All Developed Countries Combined: Report

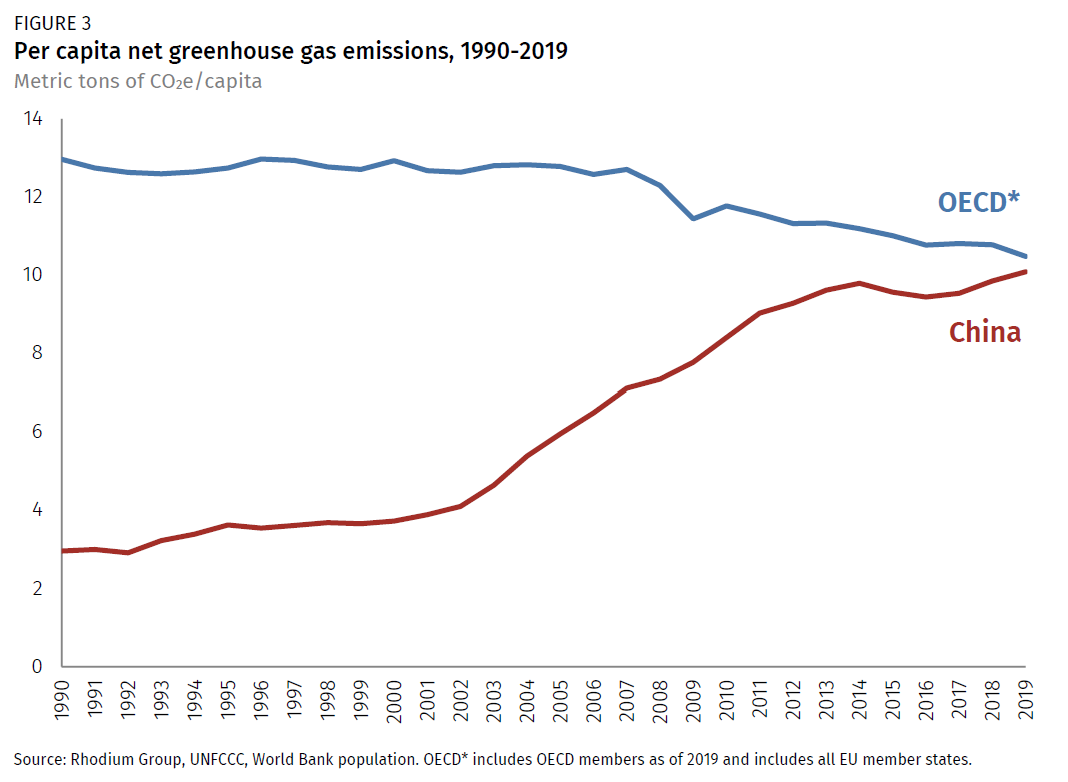

China’s 2019 greenhouse gas emissions exceeded those of the United States and the rest of the developed world combined, according to CNBC, citing a Thursday report by the Rhodium Group – a New York-based advisory group founded in 2003 by China expert Daniel H. Rosen.

According to the study co-authored by a former Obama admin climate policy official, energy modelers and emissions experts (just go with it), China is now responsible for 27% of total global emissions – more than the combined total produced by the United States (11%), India (6.6%)and the 27 EU member nations together (6.4%).

In 2019, China’s emissions not only eclipsed that of the US—the world’s second-largest emitter at 11% of the global total—but also, for the first time, surpassed the emissions of all developed countries combined (Figure 2). When added together, GHG emissions from all members of the Organization for Economic Cooperation and Development (OECD), as well as all 27 EU member states, reached 14,057 MMt CO2e in 2019, about 36 MMt CO2e short of China’s total. -Rhodium Group

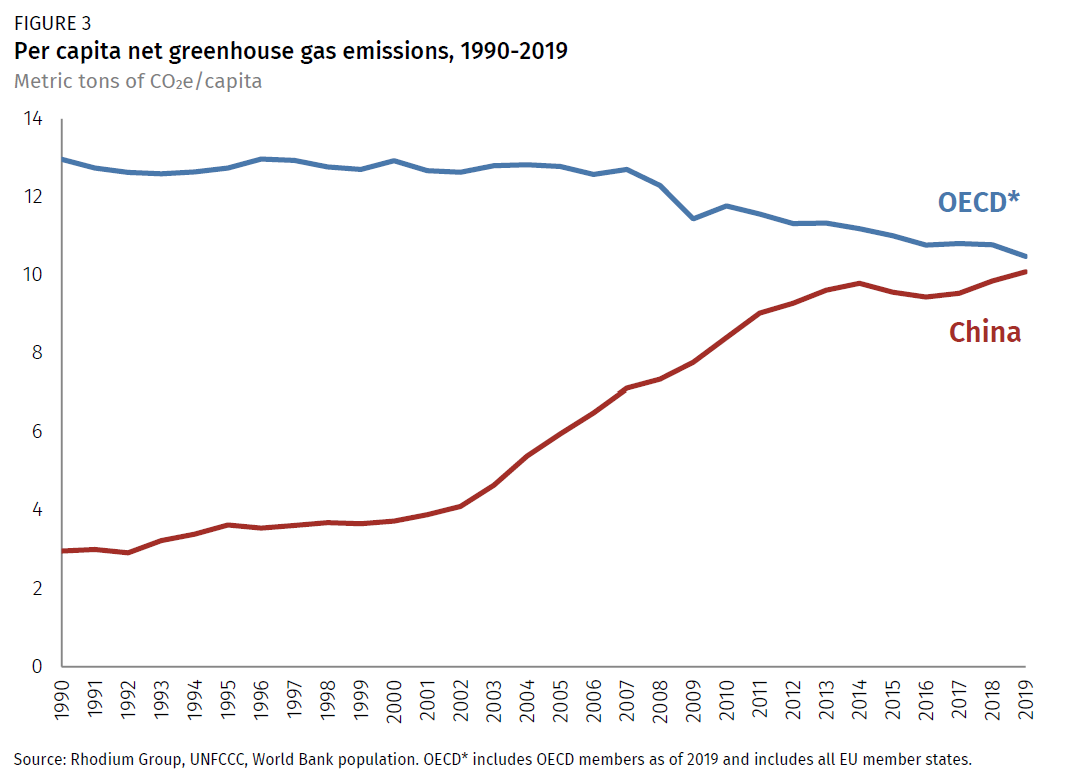

That said, the Rhodium Group also gives China somewhat of a pass for their climate sins – noting that since it’s home to over 1.4 billion people, they’re not quite so evil per capita.

To date, China’s size has meant that its per capita emissions have remained considerably lower than those in the developed world. In 2019, China’s per capita emissions reached 10.1 tons, nearly tripling over the past two decades (Figure 3). This comes in just below average levels across the OECD bloc (10.5 tons/capita) in 2019, but still significantly lower than the US, which has the highest per capita emissions in the world at 17.6 tons/capita. While final global data for 2020 is not yet available, we expect China’s per capita emissions exceeded the OECD average in 2020, as China’s net GHG emissions grew around 1.7% while emissions from almost all other nations declined sharply in the wake of the COVID-19 pandemic.

…

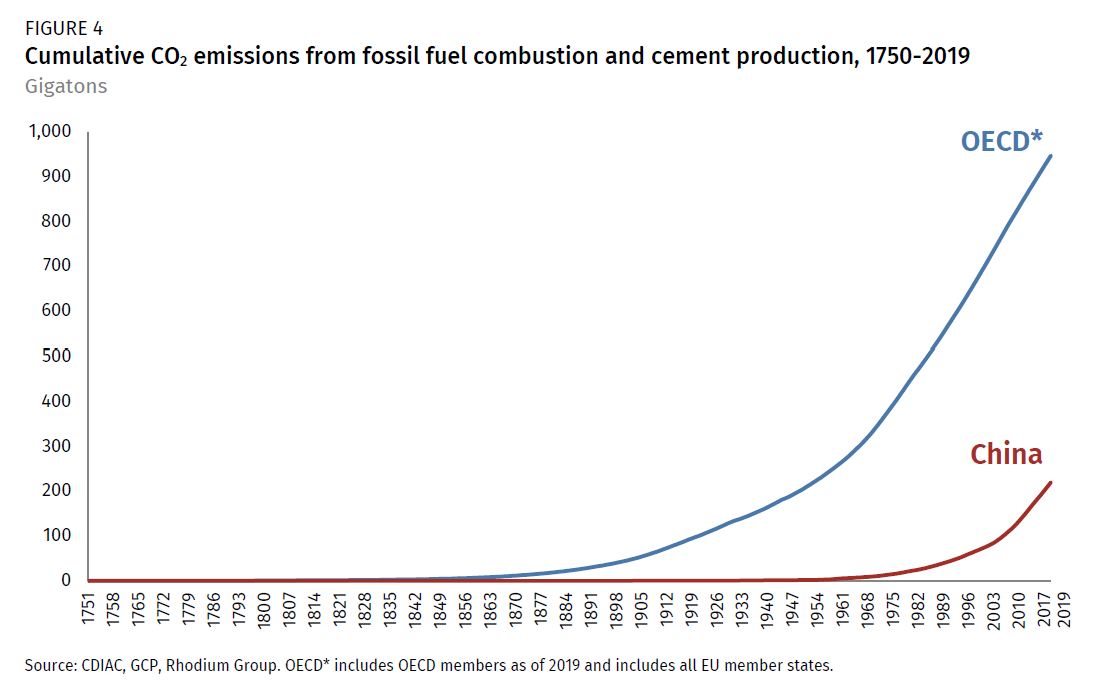

While China exceeded all developed countries combined in terms of annual emissions and came very close to matching per capita emissions in 2019, China’s history as a major emitter is relatively short compared to developed countries, many of which had more than a century head start. A large share of the CO2 emitted into the atmosphere each year hangs around for hundreds of years. As a result, current global warming is the result of emissions from both the recent and more distant past. Since 1750, members of the OECD bloc have emitted four times more CO2 on a cumulative basis than China (Figure 4). This overstates the relative role of OECD emissions in the more than 1 degree Celsius increase in global temperatures that has occurred since before the industrial revolution because a large share of annual CO2 emissions is absorbed in the earth’s carbon cycle in the decades after release. But China still has a way to go before surpassing the OECD on a cumulative contribution basis.

So of course, historically speaking, China has polluted far less – a point we’re still trying to understand.

As CNBC notes, “The findings come after a climate summit President Joe Biden hosted last month, during which Chinese President Xi Jinping reiterated his pledge to make sure the nation’s emissions peak by 2030. He also repeated China’s commitment to reach net-zero emissions by midcentury and urged countries to work together to combat the climate crisis.”

“We must be committed to multilateralism,” said Xi during brief remarks at the summit. “China looks forward to working with the international community, including the United States, to jointly advance global environmental governance.”

Xi also said that it would ‘control its coal-fired generation projects and limit increases in coal consumption over the next five years.’

As we noted on Tuesday, this means China needs to shutter 600 coal plants to meet its emissions goals of net zero greenhouse emissions by 2060. If they don’t meet that goal, we’re sure the virtuous masters of the universe will surely refuse to conduct further business with Beijing.

Is China aware that Blackrock, Bridgewater and Goldman will never, ever invest in it unless it shuts 600 coal-fired plants to hit its climate target?

He wants to continue to convince Americans they should get the experimental biological agent (AKA “the vaccine”), but, as Tucker Carlson pointed out last week, the administration and the CDC have offered no explanation as to why you need to continue to wear a mask after you have taken “the vaccine.”

Why would they want us to doubt the efficacy of the vaccine? Why would any sane person who is not in a high-risk group contemplate becoming a lab experiment subject if you are not allowed (yes, our rights are now derived from government and will be doled out based on compliance) to burn your mask and return to a pre-pandemic way of life?

That’s just bad salesmanship…until you think about the alternative.

Think about what would happen if they allowed (there’s that word again) people not to wear masks after being vaccinated.

Here’s a typical scenario.

The vaccinated test subject enters the supermarket.

The vigilante mob of leftists can’t wait to accost and demand compliance to their edict, using physical violence if necessary.

The test subject then proclaims that he has put his mask in his pocket.

A short time later, the test subject hears the man claim the same immunity.

In this fictional example, you can begin to see what the ramifications of this policy would be.

Within weeks, the majority of Americans would stop wearing masks.

(Along with social distancing, and lockdowns, and getting the vaccine).

People would actually begin to associate non-masking people with safety, while mask-wearing people would signal danger. The danger of the unvaccinated.

The government has just lost all control.

Do you really think these people will give up their newfound power so easily? I’m afraid not.

I imagine that their Big Tech partners are working furiously building a mandatory vaccine passport system as you read this.

Until that is up and running, you can expect the regime to continue requiring all people to wear masks, especially those who have been “vaccinated.”

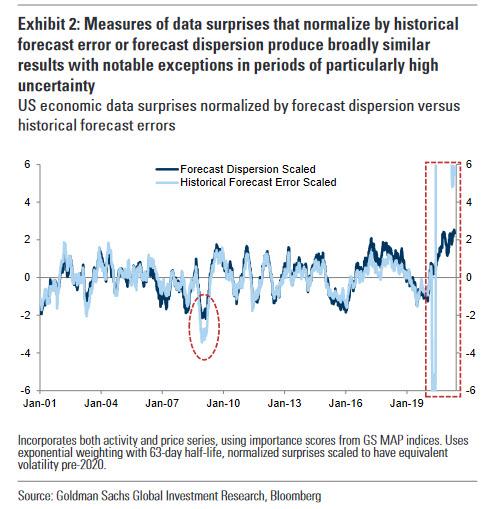

Why Have Bond Yields Gone Nowhere In The Past Month Despite Blowout Macro Data: Here Is Goldman’s Answer

After a turbulent start to the year for the treasury market, which posted its worst quarterly total return since 1980 as 10y Treasury yields rose more than 80bp, leaving markets to consider just how much further yields might move once the expected economic acceleration went from forecast to fact, Treasuries have found themselves stuck in a very narrow range, gripped by an eerie calm even as the US economy continues to power ahead and is on pace for the strongest expansion in GDP since the record Q3 of last year.

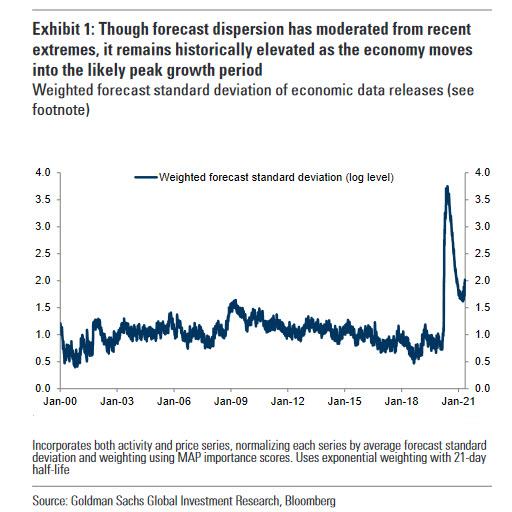

However, hile one can analyze CTA flows, extrapolate Japanese pension positioning and even speculate about stealth central bank intervention in seeking an answer for the recent bond market calm, there may be a far simpler reason why bond moves have fizzled out even as economic surprises continue coming hot and heavy: as Goldman’s William Marshall writes, yield sensitivity to data surprises tends to decline at higher levels of forecast uncertainty – a key feature of the macro environment since the onset of the pandemic. As a result, until there is some convergence in projections, “yield responses to data releases may remain muted by historical standards.”

Let’s back up.

As Marshall notes, after a torrid first three months of 2021, and despite a continuation of positive surprises across a range of significant releases last month – including payrolls, CPI, and retail sales – US yields finished the month lower on net, with yield responses to the data surprises ranging from muted to puzzling. A feature of data releases since the COVID shock has been and remains the high degree of forecast dispersion, which at this point likely reflects the range of views on both timing and magnitude of the acceleration.

This week brings the first look at April data, with economists projecting even stronger job gains (consensus is now just around 1 million new jobs) Goldman takes a look at the likely responsiveness of US rates to data surprises in this environment.

In tracking the evolution of data surprises, the standard approach is to normalize individual releases by some measure of historical forecast error. This approach helps in providing historical grounding for the magnitude of a given surprise. However, in periods where data is somewhat more volatile than normal — such as at present —using realized forecast errors may significantly under-represent the degree of uncertainty around individual releases. For markets, identifying the level of perceived noise around economic data is useful in gauging how much of a signal a given data point can provide. To this end, using forecast dispersion to normalize data surprises(rather than historical forecast errors) may provide a better picture of the information content in a particular release for markets by directly capturing the level of uncertainty surrounding the print. In general, both approaches (the more standard normalization by historical errors or normalizing each surprise by Bloomberg forecast standard deviation) produce highly correlated results until 2020; however, the last year or so and to a lesser extent the period around the GFC stand out as notable exceptions as shown in the chart below.

Intuitively this makes sense: if the underlying data volatility is orders of magnitude higher than some “calm” baseline, the information value of every outlier print is reduced exponentially as the very next month we may see a sharp reversal.

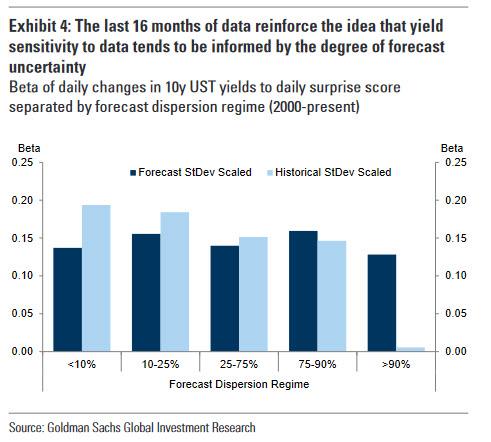

To gauge how markets respond to data surprises in different forecast uncertainty regimes, Goldman regressed daily yield changes on daily surprise scores, splitting the sample into regimes of forecast dispersion using the series shown in Chart 1. Pre-COVID (2000-2019) evidence suggests that when forecast dispersion is relatively high, the beta of yields to data surprises normalized by historical forecast errors is somewhat lower than in periods where forecast dispersion is low.

Meanwhile, the relationship between yield sensitivity to surprises and the level of forecast uncertainty is less apparent when scaling surprises by forecast dispersion. An interpretation of this initial observation is that periods of higher forecast uncertainty tend to be associated with lower sensitivity of yields to data by historical standards. Expanding the sample to include the last year firmly reinforces this pattern.

So what does this mean? Here is some more analysis from Goldman guaranteed to make your brian bleed as it tries to put in scientific terms what is ultimately a very simple concept:

There is a clearer negative relationship between forecast uncertainty yield sensitivity to data surprises normalized by historical standard errors, particularly when forecast dispersion is in the top decile. Normalizing by forecast standard deviation, meanwhile, generates somewhat more stable sensitivities across forecast dispersion regimes, suggesting that the impact of a given data surprise on yields is more reliably informed by the level of uncertainty around any given release — what may be a market-movingsurprise in the context of low levels of dispersion among forecasters is little more than noise when said dispersion is high.

Got all that – it certainly is a smarter way to say that data no longer matters…

Anyway, the simple implication of all this is that for now – until the data volatility returns to normal – it’s likely that yield sensitivity to data will be muted by historical standards, owing to the wide range of expectations (e.g., the standard deviations of forecasts for April non-farm payrolls is more than 3x its historical average).

That is not to say that data won’t matter — US rates rallied on the back of the softer than expected ISM manufacturing earlier this week, and in the accumulation of better than consensus data will take yields higher into mid-year (and vice versa). However, it likely means that more historically “normal” yield responses to data will require some amount of convergence among forecasters, instead of the prevailing “throw a dart at the wall” chaos.

It’s reasonable to expect that convergence to occur later this year, though that may take place in the context of less volatility in the data itself. In other words, don’t be surprised if we get an absolute blowout beat (or miss) tomorrow, and the 10Y does… nothing.

I have had the privilege of teaching politics and history to college students for well over a decade, and I noticed a significant change among my students in the past few years: their interest in politics and political engagement is far greater than when I began. My first group of students were Millennials, and while some were deeply interested in politics and the socio-historical world, this was the exception, not the norm. Today, my Gen Z students are deeply passionate about political change and not politically dogmatic. The 2020 election revealed their significant level of turnout, potentially setting the stage for a more vibrant polity going forward.

The survey presented 15 questions on political history and civics, asking the identity of the current the Chief Justice of the U.S. Supreme Court to noting the historical fact that the 13th Amendment ended slavery, not Lincoln’s Emancipation Proclamation. Overall, 75 percent of the respondents correctly answered 10 of 15 items, although the average number of correct responses was 8, a bit over half.

When the data is broken down by generation, Gen Z is not an outlier. Members of the Silent Generation are the most knowledgeable, with an average of 8.8 correct answers, while Millennials are the least knowledgeable at only 6.7 correct answers on average. Gen Z is comparable to Gen X at around 7.5 correct answers, marginally lower than the national average.

Digging deeper, there were cases where Gen Z was notably better compared to their grandparents. Consider the question of what Harriet Tubman was best known for. Respondents were given a selection of choices, including serving as a Civil War medic, organizing marches on Washington and various boycotts, and guiding slaves through the Underground Railroad, the correct answer. Tubman undertook at least 13 missions that rescued over 70 enslaved people via the Underground Railroad. In aggregate, 78 percent of the population knew this fact; 77 percent of Gen Zers knew this, compared to 65 percent of Silents.

When asked about what government action guaranteed women the right to vote, Gen Zers were not off the average. Fourty-five percent of the overall sample selected the correct answer of the 19th Amendment, though a sizable portion of Americans – 30 percent – believed this right was guaranteed by the Equal Rights Amendment, an idea that has been around for almost a century but has never been adopted by Congress. Nevertheless, 47 percent of those in the Silent Generation and 49 percent of Boomers answered this question correctly. Fifty-four percent of Gen Zers answered this correctly, compared to just 41 percent of Millennials. Clearly, the youngest cohort is more aware of voting rights than both their grandparents and their immediately preceding cohort.

Of course, there are examples where Gen Z could benefit from a deeper understanding of history. For instance, one question covered who the architect of the New Deal was; overall responses were split. Fifty-five percent of the total sample replied Franklin D. Roosevelt – the correct choice – but the next greatest percentage picked Alexandria Ocasio-Cortez at 18 percent. Seventy percent of the Silent Generation knew the answer was FDR, and just 11 percent answered AOC. In contrast, only 43 percent of Millennials answered FDR with 22 percent thinking that the correct answer was AOC. Gen Z was notably better, with 60 percent correctly answering FDR and just 12 percent choosing AOC. While AOC has been talking about a Green New Deal, younger Americans should certainly know that her ideas were cribbed from the FDR-initiated New Deal.

In short, the data supports what I saw in my classroom and seminars: Gen Zers are indeed more politically knowledgeable than older Millennials. While the overall level of political and historical knowledge in the nation should be better, Gen Z does not lag far behind older cohorts. Our various institutions – schools, families, and community organizations – should do more to improve civic literacy. It would be a mistake to assume that Gen Z is simply ignorant of politics and history; Millennials are far more disconnected. Politicos and parties would be wise to cultivate this youngest generational cohort and not speak past them, as they are already aware of American history and how our republic functions.

Samuel J. Abrams is professor of politics at Sarah Lawrence College and a visiting scholar at the American Enterprise Institute.

Montana Is First State To Cancel Unemployment Benefits In Response To Unprecedented Worker Shortage

Three weeks ago, when looking at the unprecedented labor shortage that is crippling the US economy (even with some 100 million Americans not in the labor force)…

…we said that there is a simple reason for this paradoxical phenomenon: trillions in Biden stimulus are now incentivizing potential workers not to seek gainful employment, but to sit back and collect the next stimmy check for doing absolutely nothing in what is becoming the world’s greatest “under the radar” experiment in Universal Basic Income.

Consider the following striking anecdotes from Bloomberg:

Early in the Covid-19 pandemic, Melissa Anderson laid off all three full-time employees of her jewelry-making company, Silver Chest Creations in Burkesville, Ky. She tried to rehire one of them in September and another in January as business recovered, but they refused to come back, she says. “They’re not looking for work.”

Sierra Pacific Industries, which manufactures doors, windows, and millwork, is so desperate to fill openings that it’s offering hiring bonuses of up to $1,500 at its factories in California, Washington, and Wisconsin. In rural Northern California, the Red Bluff Job Training Center is trying to lure young people with extra-large pizzas in the hope that some who stop by can be persuaded to fill out a job application. “We’re trying to get inside their head and help them find employment. Businesses would be so eager to train them,” says Kathy Garcia, the business services and marketing manager. “There are absolutely no job seekers.”

Even more amazing: a stunning 91% of small businesses surveyed by the NFIB said they had few or no qualified applicants for job openings in the past three months, tied for the third highest since that question was added to the NFIB survey in 1993.

But what is most striking is the context on these figures: recall that just one year ago, the unemployment rate was a depression-era 14.8%. And while it has since dropped to 6%, it remains well above the 3.5% rate of February 2020, before the pandemic. So judging from the jobless rate – which the Federal Reserve tracks closely – there’s still plenty of slack in the labor market.

Only… if one goes by the complete lack of workers, there isn’t.

The key quote from NFIB Chief Economist Bill Dunkelberg was “Main Street is doing better as state and local restrictions are eased, but finding qualified labour is a critical issue for small businesses nationwide.” And the explicit admission that BIden’s “trillions” in stimulus are behind this predicament:

“Small business owners are competing with the pandemic and increased unemployment benefits that are keeping some workers out of the labor force.”

As if it wasn’t clear, the NFIB added that “finding eligible workers to fill open positions will become increasingly difficult for small business owners.”

Seven percent of owners cited labor costs as their top business problem and 24% said that labor quality was their top business problem. Finding eligible workers to fill open positions will become increasingly difficult for small business owners.

Illinois-based Portillo’s Hot Dogs LLC boosted hourly wages in markets including Arizona, Michigan and Florida, and is offering $250 hiring bonuses. The chain has hired social-media influencers and built a van called the “beef bus” to help recruit. Still, many of the chain’s 63 restaurants remain understaffed, said Jodi Roeske, Portillo’s vice president of talent.

“We are absolutely struggling to get people to even show up for interviews,” Ms. Roeske said.

To be sure, it’s not just entry level places that can’t find workers: full-service and high-end restaurants like Wolfgang Puck’s Spago Beverly Hills, where servers can earn $100,000 a year with tips, also are struggling to recruit workers. Puck said in an interview with the WSJ that expanded unemployment benefits and new options like personal chef gigs are contributing to staffing shortages at Spago and his other restaurants.

“I don’t think we should pay people to stay home and not work if there are jobs available,” he said.

Summarizing the data, Rabobank’s Michael Every wrote that Biden’s generous unemployment benefits are “ironically helping to push up wages, at least temporarily – which I am sure nobody intended, but underlines just how radical policy has to get in the US to make it happen.” His conclusion: ”the problem is that small businesses trying to get past Covid are least well placed to lead this socio-economic charge; and if this points to a wage-price spiral –which is still unlikely– then the bond market will soon be pointing its finger at the Fed.”

Well if it is unemployment benefits that is causing the labor shortage why not do away with said benefits?

Of course, that is far easier said than done: once Americans are used to collecting money for doing nothing, they would be extremely displeased – to put it mildly – once the money is gone. This is not lost on politicians who know that they would be the immediate target of popular ire.

And yet, one state is taking the much needed, if extremely unpopular step, of breaking this addition to stimmy handouts which has also led to this historic labor shortage.

According to Yahoo, Montana plans to stop some of its federally-funded unemployment benefits to address “the state’s severe workforce shortage,” according to its labor department, which will leave many out-of-work residents without any support at all.

“Nearly every sector in our economy faces a labor shortage,” Governor Greg Gianforte, a Republican, said in a statement on Tuesday, echoing what we said last month, namely that “The vast expansion of federal unemployment benefits is now doing more harm than good.”

Instead, the state will do the correct thing and begin offering return-to-work bonuses to help employers looking to hire.

Starting June 27, Montanans will lose access to the extra $300 in weekly unemployment benefits, but maintain their regular benefits. Contractors, gig workers, and others will also lose access to the Pandemic Unemployment Assistance (PUA) program, meaning those workers won’t get any benefits.

Those relying on the DOL’s Pandemic Emergency Unemployment Compensation (PEUC) program, which gives additional weeks of unemployment benefits to workers, will stop receiving benefits. The state also plans to reinstate the requirement that stipulates workers must be actively searching for a job to qualify for unemployment benefits.

Predictably, the decision sparked howls of outrage from those already habituated to Biden’s Universal Basic Income regime:

“Montana’s move to end these fully federally-funded UI programs, along with their COVID-19 exceptions, is cruel, ill-informed, and disproportionately harms Black and Indigenous People of Color and women,” Alexa Tapia, unemployment insurance campaign coordinator at the National Employment Law Project, told Yahoo Money, basically slamming the decision as both racist and sexist. “Ending these programs would leave 22,459 people unable to support their families and hurt thousands more.”

Alternatively, those 22,459 people can find a job.

Montana’s unemployment rate was 3.8% in March, down from its 11.9% pandemic peak in April 2020, according to data by the Labor Department.

The federally-funded unemployment programs run through September 6 nationwide. Montana’s cancellation would cost workers at least $3,000 per worker in supplement benefits if they couldn’t find work through the program expiration. Workers on PUA and PEUC would lose at least $4,500 in benefits because they no longer will be eligible for the base unemployment benefit.

Liberal economists were also outrage, claiming that Universal Basic Income is a wonderful creation (it hasn’t worked out that great in any socialist nation where it has become a staple of social welfare, but whatever), with studies from such liberal bastions as the National Bureau of Economic Research all the way to Yale University claiming that the extra $600 in benefits distributed earlier in the pandemic had limited labor supply effects and likely didn’t disincentivize work. (narrator: they disincentivize work, just see Wolfgang Puck’s quote above).

“The 100% federally-paid unemployment benefits have boosted spending and contributed to the strong economic recovery,” Andrew Stettner, an unemployment insurance expert and senior fellow at the Century Foundation, told Yahoo Money. “It’s shortsighted for the state to sacrifice that economic stimulus based on the anecdotal labor shortages concerns of a few employers, especially given the limited evidence of work disincentives from unemployment pay during the pandemic.”

What he forgot to mention is that the artificial spending created by stimulus has led to soaring prices and out of control “transitory” inflation, which will lower the standard of living for everyone, not just those on the government’s dole, but again anything that goes contrary to the liberal mantra of “bigger government is always better” is anathema and must be crushed immediately.

So far, Montana is the first and only state to fully opt out of the federal unemployment benefit programs enacted in the pandemic and currently extended by the American Rescue Plan signed into law in March. As a way to incentivize workers to return to work, the state is offering a one-time return-to-work payment of $1,200, using money from the American Rescue Plan to fund the program. Only those who complete four weeks of work would receive the payment.

“Incentives matter,” Gianforte said. “Our return-to-work bonus and the return to pre-pandemic unemployment programs will help get more Montanans back to work.”

One can only hope that more states follow Gianforte’s extremely unpopular, if extremely prudent decision, before the US is mired in 1970s style hyperinflation.

Voting with your feet is a crucially important indicator of what is really going on, regarding the political economy. No, this does not refer to taking off your shoes and socks, entering the polling booth, pressing a button with your big toe instead of your thumb or index finger.

Rather, it denotes migration patterns as the best way to determine human welfare.

The island government 90 miles off the Florida shore can brag all it wants about its health care and educational systems that have “made Cuba great.” But massive numbers of people have rejected that sorry system as demonstrated by their migration away from it, often at great bodily risk, to enter our country. Yes, there might have been a Bernie fan or two who moved in the opposite direction (Senator Sanders spent his honeymoon not in Russia, but in the USSR), but these are the exceptions that prove the rule.

Were there any Jews attempting to enter Nazi Germany? Who knows; again, maybe one or two. But the virtual one-way traffic was in the very opposite direct. Ditto for the Berlin wall. In which way was the immense movement there? To ask this question is to answer it.

The U.S is a racist country that grinds down blacks? Then we ought to see large numbers of African Americans attempting to leave for greener pastures elsewhere, and observe very few people from sub Saharan Africa headed in the U.S. direction. But this does not occur. Indeed, the very opposite takes place. There is no better refutation to the claims of the Black Lives Matter Marxist movement. All the statistics about African American unemployment rates falling and a poverty rate of intact black families falling to single digits (before Covid) pales into insignificance compared to the primordial fact of migration patterns. Or, rather, lack of same.

What is the reaction of the governments from which migrants are fleeing? Some act responsibly, morally, justly: they do not try to shoot or incarcerate emigrants as they depart. Mexico is certainly an example of this, and ought to be congratulated for such civilized behavior. Similar accolades must be awarded to Namibia, Botswana, Zimbabwe (formally Rhodesia) and Mozambique. They did not violently prevent their residents from entering even apartheid South Africa.

But others act in the opposite direction, and reveal themselves to be in effect, gigantic jail cells. The cases in point are too numerous to mention, but the following are certainly examples:

All too many Cubans have resorted to making the passage to Florida on rafts supported by inner tube tires and were shot at or arrested by authorities of that nation.

East and West Germany and the infamous Berlin Wall; in which direction were the feet voters headed!!!

The traffic in the Korean peninsula eight decades ago, and even in the modern era, was from North to South, not in the opposite direction

Recent headlines blare: “Hong Kong Residents Formally Arrested.” Their “crime?” They were caught attempting to escape to Taiwan. So much for the “One Country, Two Systems” agreed upon in a treaty signed by both countries when Brittain in 1997 turned this island community over to the tender mercies of the People’s Republic of China. So far, no Uighurs have been imprisoned for fleeing, but it does not take too much imagination to suppose that if they had a prayer of succeeding in such a venture, they would also dearly love to do so.

Let us close with a U.S. example. In the 1930s, there was a strong pattern of African Americans leaving Alabama, Mississippi, and other Jim Crow southern states for Detroit, Philadelphia, Chicago, and other more receptive environs. Did the donor states attempt to in any way prevent this migration pattern? No. So they also garner honor roll mention in the litany of political jurisdictions that have eschewed the title of vast penitentiaries.

* * *

The political and economic climate is constantly changing… and not always for the better. Obtaining the political diversification benefits of a second passport is crucial to ensuring you won’t fall victim to a desperate government. That’s why Doug Casey and his team just released a new complementary report, “The Easiest Way to a Second Passport.” It contains all the details about one of the easiest countries to obtain a second passport from. Click here to download it now.

Beijing Cracks Down On Ant Group’s Popular “Mutual Aid” Service

Beijing’s crackdown on its tech giants is threatening a critical mutual aid service that millions of Chinese citizens have used to bail themselves out of a tough situation – often due to illness or unexpected injury.

As WSJ explains, Ant’s Xianghubao “mutual aid” service is crowdfunded medical coverage where signing up is free, and members are entitled to receive lump-sum cash payouts of up to $45K in cases of certain critical illnesses or life-threatening injuries. The theory is that there is strength in numbers, and many members contribute the equivalent of a penny (or less) toward each claim.

The service, the name of which means “mutual treasure”, has never earned a profit for Ant, even though it has skirted regulatory lines in China from Day 1. Ant has aggressively advertised the service, and although it has never earned a profit for the company, Ant Group believes it has helped its Alipay app compete with WeChat’s offering among key demographics, including the rural poor. According to Ant, 116,950 members of the service have received a total of $2.6 billion in the past two-plus years.

But now that Ant is being forced by Beijing to apply to become a financial bank holding company, the mutual aid product will almost certainly be transformed into a more traditional commercial product falling under the purview of China’s banking and insurance regulators.

At its peak, the mutual aid product had more than 100M users, although numbers have fallen since Ant’s IPO was scrapped last October after chairman Jack Ma, the billionaire who still controls the company, criticized Beijing at an obscure tech conference, eliciting the backlash that transformed into the current anti-trust crackdown on China’s biggest companies.

Xianghubao fell into a regulatory grey area, partly due to the fact that Chinese regulators weren’t particularly eager to oversee it.

After Beijing scuttled Ant’s blockbuster IPO, the central bank ordered Ant to return to its origins as a payments company and stop its “regulatory arbitrage.” Since the crackdown began, Ant has been forced to step up verification practices to protect against false claims are paid out. Several other Chinese firms have recently abandoned their mutual aid businesses after China’s banking and insurance regulator flagged the financial and social risks of these types of products.

In its place, Alipay’s loosely regulated “mutual aid” service will likely be replaced by more traditional health-insurance products. Some Chinese insurers have already been rolling out more affordable private policies. In April, the Shanghai government introduced a policy jointly underwritten by nine insurers. For an annual premium of just 115 yuan, the equivalent of $17.80, the one-year policy provides up to 2.3 million yuan, the equivalent of $355,000.

“Regarding the Great Depression,… we did it. We’re very sorry… We won’t do it again.”

– Ben Bernanke, November 8, 2002, in speech given at conference honoring Milton Friedman

Ninety-two years ago, as what was to become the Great Depression was setting in, the Federal Reserve made what is now widely regarded as a historic error. Instead of pursuing an expansionary policy and growing the money supply, it did the opposite, contributing to the decline. “Scholars believe that such declines in the money supply caused by Federal Reserve decisions had a severely contractionary effect on output,” as a Federal Reserve history puts it. Hence, that apology above by former Federal Reserve Chairman Ben Bernanke.

“Joined at the hip”: Treasury Secretary Janet Yellen and Fed Chair Jerome Powell

Today, with the economy reopening and a snapback recovery happening, the opposite blunder is underway. A previously unimaginable torrent of cash is pouring into the economy from both the federal government and the Fed, which are now “joined at the hip,” as former Fed economist Henry Kauffman recently wrote.

The consequences are already visible. Worker shortages are rampant, undermining the rebound and institutionalizing government dependence. The federal cash is finding its way into everything from homes to cryptocurrencies to stocks to raw materials, making it certain inflation will claw back much of the recovery in income. And everything is getting federalized, upending the system of decentralized government that served America well for so long.

The Torrent:

It’s key to first to get your mind around how much money Washington is pumping out, which isn’t easy. So far, lawmakers have enacted six major pandemic relief bills costing about $5.3 trillion. For a little perspective, that’s 27% more than the entire federal budget for 2019, the last fiscal year before the pandemic. And now the Biden Administration wants to spend an additional $4.5 trillion.

Through it all, the Fed has been the Treasury’s enabler. It has already wished into existence $3.5 trillion since the pandemic started, used to purchase notes and bonds. And it says it expects to continue that buying at a clip of $1.4 trillion per year while keeping interest rates low, rates that already are negative, being lower than inflation.

Here’s another bit of historical perspective. In 1988, Democratic Senator Lloyd Bentsen said this in a debate during his candidacy for Vice President: “You know, if you let me write $200 billion worth of hot checks every year, I could give you an illusion of prosperity, too.”

That $200 billion would be only $450 billion today. But this year’s projected federal deficit is five times higher than that even without the Biden Administration’s new spending proposal. The Fed is now creating as much money as Bentsen decried in today’s dollars every four months.

Granted, not everybody has benefited from federal largess. Some individuals have suffered immense financial hardship from the pandemic.

But that definitely has not been typical. Federal assistance has been so vast that total personal income in every state has actually been higher during the pandemic than before. As a Pew Research report put it, “The sharp increase in government transfer payments more than offset a slight decline in inflation-adjusted earnings, which include wages from work plus extra compensation such as employer-sponsored health benefits, as well as business profits.”

Nor have state and local governments suffered. Federal relief for almost all of them together with their own reserves has exceeded losses caused by the pandemic. Many needed no help at all, as we detailed here.

The Predictable Results:

Worker shortages are now rampant and severe.

Why work or return to normal if federal handouts keep coming?

The evidence is overwhelming in stories everywhere, across the nation and in multiple sectors. A few examples:

The National Federation of Independent Business found in a March survey of its own small business members that 42% had job openings they couldn’t fill.

Factories are “desperate for workers,” says a Reuters headline. “I’ve never seen it this bad,” said president of Look Trailers, based in Middlebury, Indiana, one of the examples Reuters cited.

In Chicago, where crime is often blamed on unemployment, summer jobs are going unfilled for lack of applicants, according to a report this week by the Chicago Sun-Times.

A Plainfield, Illinois restaurant is begging its customers to be patient because of its worker shortage. “To all of our loyal patrons, customers and friends, we ask you to remain patient with us as we deal with an abnormal shortage of employees.”

Former Treasury Secretary Larry Summers last month panned Biden’s focus on job creation in light of the labor shortage.

As many as 2.1 million manufacturing jobs will be unfilled through 2030, according to a study published this week by Deloitte and The Manufacturing Institute, cited by CNN. The report warns the worker shortage will hurt revenue, production and could ultimately cost the US economy up to $1 trillion by 2030.

Senior Biden economic officials have in recent weeks “been peppered by complaints from restaurant groups, the construction industry and other businesses about their inability to find enough workers as the U.S. economy begins to recover from the pandemic,” the Washington Post reported on Wednesday.

But so far that has fallen on deaf ears. Neither the Fed nor the Biden Administration have shown an inkling of interest in changing direction.

Yes, there are other reasons why some may be reluctant to return to work beyond monetary and fiscal policy. Though vaccines are now available to all adults, some still fear COVID-19, and not all employers are back to running normally.

But the lack of financial incentive is surely key. “Show me the incentives and I will show you the results,” as Charlie Munger, Warren Buffet’s partner says. The expanded federal unemployment benefits authorized by Congress last until September 6. That makes no sense whatsoever in light of Biden’s goal of returning to normalcy by July 4. Many states have already done so and even in Illinois, where lockdowns have been harsh, Gov. JB Pritzker is talking about a full reopening by July 4.

Aside from discouraging people from returning to work, the gush of federal money has other consequences.

First, inflation is now a certainty, most experts agree. “Everything screams inflation,” said a Wednesday Wall Street Journal headline. But the Fed and Treasury Department seem oblivious. Inflation lags policy that influence it by 12 to 18 months, the Fed often says, yet it continues to focus on current signals of inflation that it thinks are benign.

Second, with interest rates negative in real terms, retirees, pensioners and others that need fixed income are desperate. There are simply no suitable investments available to them that will produce any returns.

Third, everything is getting federalized, as we detailed earlier, turning America into one big, blue state, as others have put it. Many on the left have been quite open, as we wrote there, about their intention to create a culture of dependence on the federal government and make the federal cash flow permanent. It’s a warm-up for dependence on an all-powerful federal government. “It is a baby step toward universal basic income, or guaranteed income,” says the Brookings Institute. “The significance of this moment in U.S. social policy is hard to overstate.”

The grownups in the room telling the politicians to back off should be Treasury Secretary Janet Yellen and Federal Reserve Chairman Jerome Powell. They are failing.

It took decades for a consensus to form about the folly of federal policy at the outset of the Great Depression. This time, the reverse blunder and its consequences won’t take long to figure out. They are in plain view already.