Impeachment has ended in the acquittal of President Donald Trump and all we have to show for it is a legion of op-eds praising Mitt Romney, the only Republican senator to vote to convict on one of the two articles. (You can read my more skeptical take on Romney here.)

The whole affair ultimately fizzled out, even though John Bolton threatened to inject some excitement into the proceedings as recently as last week. Why in the end did this end up being a party-line affair, sans Romney?

1. The public hearings made the impeachment inquiry look partisan.

Republicans were outraged by the House Democrats’ process, which included a lot of closed door hearings and leaking to the press. But that was the only time period where there was an undeniable uptick in popular support for impeachment. Adam Schiff and company learned from the Robert Mueller report that you needed a clear narrative of wrongdoing, not a nuanced document about which competing arguments could be made. The House’s initial approach allowed Democrats to get their side of the Trump-Ukraine story out without the American people seeing any Democrats. Eventually, however, some kind of transparency was going to be needed (notwithstanding calls for the Senate to remove Trump by secret ballot) and once impeachment became a television show in which Democrats and Republicans did battle, momentum in the polls stalled.

Once that occurred, there was little incentive to cross party lines. Impeachment was popular enough, especially with the progressive base, that Democrats couldn’t abandon it. It was too unpopular, especially among grassroots conservatives, to compel many Republicans to break ranks. Trump isn’t as popular with Mormons as he is evangelicals, so Utah’s Romney could afford to vote for one of the articles of impeachments. Even Justin Amash, who represents Gerald Ford’s old congressional district in Michigan, had to leave the party once he decided he was pro-impeachment based on the Mueller report before Trump-Ukraine. (I defended Amash’s integrity and conservatism.) Zero Republicans ended up voting for impeachment in the House. Trump’s removal was always going to require 20 Republican senators to break ranks and that was an extremely tall order under these political conditions.

2. Democrats didn’t really expect to convict Trump.

Once it was clear that this was going to be a partisan impeachment, of the kind Schiff and House Speaker Nancy Pelosi had previously wanted to avoid, it could serve only two purposes: damage Trump in the 2020 election and fire up progressives who wanted congressional Democrats to go through with this. Jim Geraghty outlined a serious case that could have pried loose some Republican this side of Amash and Romney (or at least made acquittal votes tougher to justify).

But Democrats never thought enough Republican votes were in play to matter nor did they think their activists would be satiated by an impeachment over the Impoundment Control Act. Instead they stirred together a strange cocktail of maximalist liberal Trump-Russia conspiracy claims and neoconservative talking points about the need to fight Russians over there rather than over here. The whole thing relied on hyperbole and self-serving narratives that the the White House was an Aaron Sorkin program before Trump got there.

3. The break between Trump and Senate Republicans never came.

Bolton aside, the big risk for Trump—who does not boast relationships with the senators in his own party as strong as Bill Clinton’s—was that he would become enraged when GOP lawmakers did not go as far in defending him as he preferred. Trump said the Ukraine phone call was “perfect,” many Republican senators believed it was inappropriate but not worth removing a president in an election year. In the end, Trump’s lawyers and House Republicans offered the defense the president wanted. Senators like Lamar Alexander explained the rationale for his votes the way he wanted. No split came, which left Romney by himself.

4. It’s an election year.

At the end of the day, “Let the people vote” triumphed over Democratic arguments that asking for an investigation of the Bidens and Burisma (and still releasing the aid when nothing of consequence happened) constituted election interference that needed to be dealt with immediately. The voters are going to get to decide what they want to do with Trump.

5. It’s the Trump era.

The news cycle has moved quickly ever since Trump’s famous escalator ride. On the day of his acquittal by the Senate, impeachment was perhaps the third biggest story. Even world historical events don’t feel like an especially big deal for longer than 72 hours or so. Trump powers through them and the public tunes into something else. Some other pols, like Virginia Gov. Ralph Northam, have learned from his example.

Ohio Pension System Slashes Health-Care Benefits To Stave Off Insolvency

Pension-fund managers from across the US stopped to take note of an unsettling development in their industry, and perhaps thought to themselves: ‘There but for the grace of God go I’.

For the first time in years, a major public pension system has slashed benefits for retirees: The Ohio Public Employees’ Retirement System voted last week to cut health care benefits provided to the pension’s current and future retirees beginning in 2022 to try and prevent the fund from plunging into insolvency in the not-too-distant future.

It’s just the latest reminder that America’s ‘pension timebomb’ isn’t as far off into the future as many retirees, investors and public officials would like to believe.

According to Chief Investment Officer and the Bond Buyer, if these changes had not been enacted, the fund would run out of money in about 11 years, executive director Karen Carraher said during a board meeting. The measure passed by a 9-2 vote.

“There is no available funding for health care,” a report from the board said. “All of the employer contribution[s] must be allocated to pension funding until that funding improves. Based on current projections, no funding will be available for health care for 15 or more years.”

The vote, which was undertaken after polls showed members would be open to the changes to preserve their retirement benefits, eliminated the system’s group health-care plan and replaced it with stipends that will defray costs for members who purchase plans on the state ObamaCare exchange.

Beneficiaries will receive a wide variety of quantitative cuts, depending on their age of retirement, the year in which they retired, and the number of years working in the state. “Surveys indicate members willing to accept changes/reductions in health care in the interest of preserving it,” the board’s report said.

Nearly everyone in OPERS likely will be affected by these changes. The board’s vote constituted the elimination of the pension’s healthcare group plan, and replaced it with a stipend that will help supplement for some members the cost of a new healthcare plan on the marketplace.

“Pre-Medicare group plan is unsustainable for OPERS and members as risk core and costs continue to increase,” the report said. The board “needs to reduce the cost of health care to preserve current health care trust fund until such time funding can resume.”

“Our objective is to continue offering health care. To accomplish this, we need to implement changes that will extend the solvency of the health care trust fund,” the board’s report said.

As CW reminds us, it’s irresponsible management and policymaker – like bequeathing state employees with ever-more-lavish benefits when the tech boom left the fund (temporarily) at 128% funded.

Not mentioned is CalPERS dropping employer contributions to near zero for two years and sponsoring a state worker pension increase, SB 400 in 1999. Its generous Highway Patrol formula, adopted by local police and firefighters, is said by some to be unsustainable.

But during market downturns, the state is left on the hook as employers and employees see their contributions cut.

A CalPERS pamphlet told legislators SB 400 would not cost “a dime of additional taxpayer money.” State contributions expected to remain for a decade below the fiscal 1998-99 level, $766 million, actually turned out to be $3.9 billion in 2009 for various reasons.

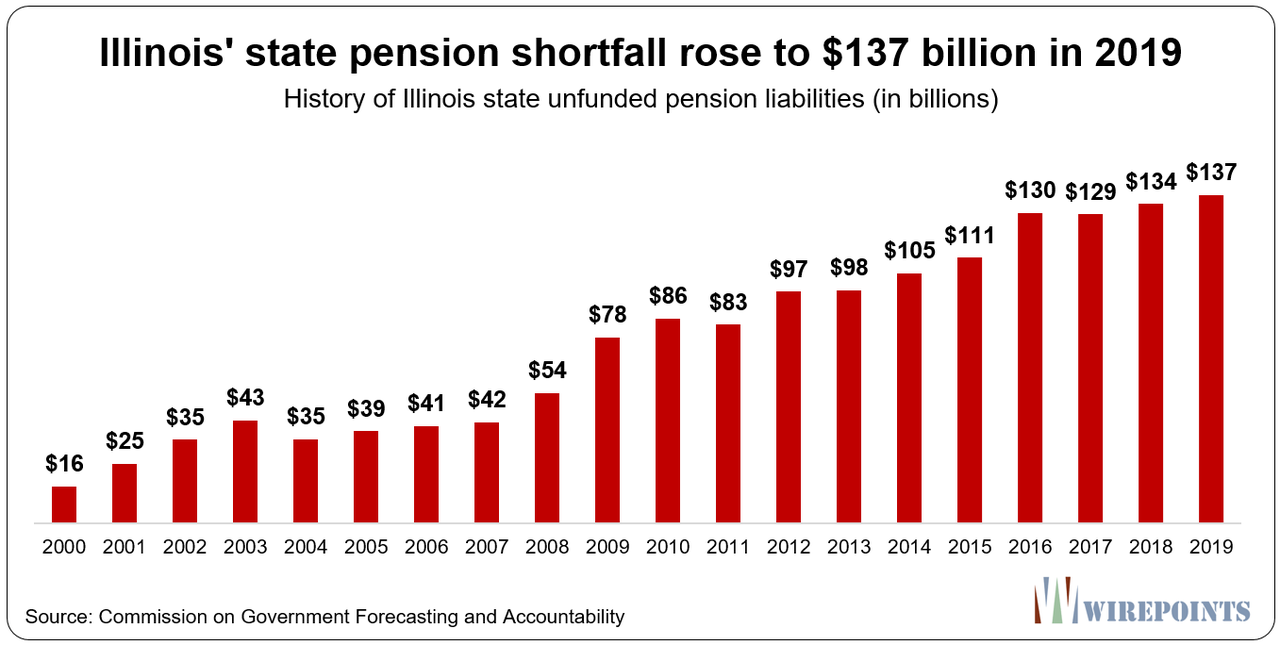

This continues to this day. Despite the state’s new Democratic governor and his promises to fix the pension crisis, Illinois’ public pension systems’ aggregate unfunded liabilities for the year was $137 billion.

And with the coronavirus outbreak threatening to monkey hammer global growth, the failures of CalPERS, and pension systems in Illinois and New Jersey, among others, leave all of these funds vulnerable. They’re just one major investment loss away from their funding ratios dropping below 50%.

The year 2020 could emerge as the start of the era of relative global chaos or major upheaval. It is the era we have been anticipating, as the impact of core population decline meets economic dislocation, and security and structural uncertainty.

Changes in the fundamental sociological framework of global society, due to the end of the population growth cycle – and with it the end of the economic growth cycle based on expanding market size – were beginning to become evident by the beginning of 2020. It was apparent that 2020 was likely to see a major evolution in this transformation.

The three “inevitable” trends which had been promoted in recent decades:

the “inevitable” rise of the People’s Republic of China;

the “inevitable” decline of the United States of America; and

the “inevitable” consolidation of the European Union into a strategic superpower

…had all, by 2020, retreated into the swamps of vainglory.

A broad-brush landscape view of 2020 must include at least the following:

The People’s Republic of China and the BRI Framework:

The Communist Party of China (CPC) should be expected to face unprecedented challenge in 2020-21, not only for its control of the economy of the People’s Republic of China (PRC), but to its ability to project the PRC’s physical power in its immediate region, and across its suzerain empire, expressed through the Belt & Road Initiative (BRI) network of states.

The PRC economy has been faltering for several years, and growth in gross domestic product (GDP) figures have only been sustained by artificial construction transactions, which are now becoming unsustainable. It is now estimated that the PRC was in actual economic decline at a time, which will lead to a faltering in its foreign investment and loan capacity to sustain the BRI program.

The BRI concept has become an ideology for the projection of the CPC’s influence, far more than an economic platform, but it is one which has a real financial cost to the PRC and which is expressed in monetary terms. It was created as a de facto ideology to buy strategic space globally when traditional maoist-marxist ideology could not make any meaningful penetration.

The CPC’s ability to “buy hearts and minds” was made possible by the Chinese economic growth, which had been funded by the Chinese private sector, unleashed by PRC leader Deng Xiaoping (1978-92) after the death of Mao Zedong. The state economic sector did not contribute to this rise.

By 2019, and even earlier, Pres. Xi Jinping had begun to curb the private sector and favor the state-owned enterprises (SOEs, which had not contributed to the “economic miracle”), in order to gain more control over society. It was a de facto return to maoism and economic stagnation at a time when urbanization and other factors were already stressing the PRC’s capability to sustain growth.

Moreover, the PRC has almost 20 percent of the global population and only seven percent of its water (and that water supply is decreasing due to consistently declining snowfall on the Tien Shan mountain range), and what water it does have is heavily polluted. Its food production is now totally compromised.

The PRC has extensive foreign exchange holdings and holdings of US debt paper, but these are now beginning to erode as Beijing is forced to now expand its imports of foreign foodstuffs. The reason for the PRC’s total capitulation to the US in the so-called trade war with the signing of “Phase One” of January 15, 2020 was (a) for the PRC to begin to cope with its growing food and economic crises, and (b) to ensure, for US Pres. Donald Trump, that the PRC’s economy would not completely collapse in 2020, the year of pivotal US elections.

So the PRC was already on economic life-support by the time the coronavirus pandemic began to become known by the end of January 2020. It was clear that the CPC was already well aware of the reality that the coronavirus had begun its broad contagion – with the consequent impact on the PRC economy – when it signed the “trade deal” with Pres. Trump.

All of this, coupled with the economic impact of the revolt of Hong Kong against the PRC – effectively removing Hong Kong as one of the key economic contributors to the PRC’s “economic miracle” – meant that the PRC’s already-delicate economic condition was now in an unavoidable and dramatic decline. At the same time, the Hong Kong example meant that Beijing’s steady pressure to dominate the elections in the Republic of China (ROC: Taiwan) collapsed, resulting in a severe loss of prestige for the CPC.

The Taiwanese “intransigence” meant that “two Chinas” continued to exist. The CPC could not claim total victory in the Chinese Civil War when the original state – albeit now reduced to a rump geography on Taiwan and other islands – continued to exist as a taunt to the legitimacy of Chinese maoism.

The question was, then, what Beijing would do about the situation to prevent a domestic backlash and the collapse of the substantial BRI infrastructure which had developed throughout Eurasia and Africa, and through the Pacific. Pres. Xi must do something, if only to contain the unrest within the CPC, let alone within the PRC population.

Was it possible that he would initiate military action against Taiwan? Or against Vietnam (perceptionally, an easier target, but one which embarrassed the PRC in 1979)? Or elsewhere? Xi must do something, and it will be disruptive, and possibly have significant negative impact on his own rule.

US Pres. Trump, assuming he wins re-election in November 2020, may decide in 2021 to take the PRC off life support and re-start the trade war. The downstream ramifications are significant.

Western Europe After Brexit, and the Re-Shaping of the Heartland/Maritime Balance:

The myth of the European Union (EU) was finally shattered when the United Kingdom – despite ruthless pressures from the EU – left the EU on January 31, 2020. The EU was already in a delicate economic condition before that occurred, and would now lose significant traction as a result of the UK departure (Brexit). This raises questions:

1. Would the economic malaise which was likely to deepen in the EU in 2021 (unless it could achieve a tariff-free trade deal with the UK before that time) cause other EU members to question the value of the alliance?

2. Would the rump EU become more susceptible to influence from Moscow because of energy dependency on Russia? [And come under greater PRC pressure because of an economic dependency on PRC loans and investments?]

3. Would the EU attempt rapid increases in “state-building” to create an actual sovereign entity out of the Union? This approach, which had been the long course of action by EU leaders, defies the fact that the EU lacks a coherent defense capability as a requisite for actual superpower influence. The ideology of Brussels has been that the EU would build a “third way” of “soft power”, something which indicates that the proponents of this do not actually comprehend the necessity to have a comprehensive arsenal of “soft” and “hard” power resources.

The EU has moved into a position, particularly with Brexit, of massively reduced influence globally. On the other hand, the move by the UK back to fully sovereign status means a re-galvanized position for the community of maritime powers, and for the Commonwealth. Despite a period of “sorting out” in 2020, the maritime powers (the UK, US, Canada, Australasia, possibly Japan, India, Taiwan, and so on) and the Commonwealth, have now begun to re-coalesce.

The ongoing weakness of the EU, however, has significant ramifications for stability in the Mediterranean Basin, and particularly related to actions by Turkey toward Cyprus, Greece, Libya (and by stealth, toward Egypt), and the Levant. There is an increasing likelihood of France continuing to take a sovereign view of strategic issues, and work closely with the UK. Moreover, some EU states – particularly Greece, Poland, and the Baltic States – will reinforce a new momentum in NATO, which should be expected to re-orient away from a purely “North Atlantic” context to become the basis of a global capability.

The United States Moving To and Through Pivotal Elections:

The US continues to be a nation divided at levels of polarization not seen since 1860. This is likely to worsen until (and beyond) the November 3, 2020, Presidential and Congressional elections.

The internal US schism profoundly hampers both the attention which the US President can devote to strategic issues, and the prestige which gives the office influence. Thus, most of the strategic actions by the incumbent President fail to get attention in the US polity, such as initiatives to cement a new economic and power framework in Central Asia, extending through a resolution of the Afghanistan conflict, and linking to the Indian Ocean via Pakistan. And attempts since 2017 to break up PRC strategies (BRI) to control Eurasia and Africa.

Of primary importance, then, is whether the US misses great opportunities in 2020 and possibly fails to start to regain unity in 2021, and whether the US can itself regain cohesion at all. It is not inconceivable that the US could see greater moves toward secession by some states, or toward violence between urban-controlled state structures against nationalist elements.

In the US, it is the society-level schism which could work profoundly against the success of the state, as opposed to the PRC where it is the state which is now moving (again) against society.

A Turning Point for Africa:

The collapse of the PRC’s suzerainty over much of Africa has meant a collapse of security there, and a return to corruption at a leadership level in those particular states.

The absence of accountability or major-power pressure means that rapid decline should be expected in 2020 in South Africa, Nigeria, Zimbabwe, and elsewhere on the Continent. Problems persist in the Horn of Africa and North Africa. This instability is being exploited substantially by Turkey, working alone and through Muslim Brotherhood (Ikhwan) conduits, and by Iran.

The fundamental decline in PRC investment and loans (and the pressure by Beijing for African states to deliver resources and other outcomes), as well as a tapering off of PRC purchases of resources from African states, will mean growing economic malaise in Africa. This will lead to an impetus toward mass migration to Europe (in particular) at a time when the EU states are increasingly less able to cope economically with this.

A similar scenario could apply to much of Latin America and for similar reasons.

The Transformation of the Middle East-Mediterranean:

There was, as 2020 dawned, a kind of “calm before the storm” emerging in the Middle East. Iran’s clerics, after a period of panic after the death (long anticipated) of Quds Force leader Qasem Soleimani, were now looking more soberly at whether they could carry through with their planned new war against Israel. After initial euphoria about possible victory against Israel, there was the start of sober evaluation as to whether Iran could prevail.

Meanwhile, Saudi Arabia and the UAE, which had briefly abandoned the US in 2019 to seek Moscow’s and Beijing’s support in keeping Iran from attacking them, had by 2020 begun to rebuild their relations with the US. Internal challenges in Saudi Arabia remained, and the task of restructuring Yemen in the wake of a collapse of the Saudi-UAE war there was beginning, but without Saudi influence.

Meanwhile, Turkey continued to lash out with initiatives in Libya designed to help Ankara get access to the Egyptian-Israeli-Cypriot gasfields of the Mediterranean. Turkey, facing growing economic and social challenges, became the principal area of instability, which was likely to cause its President to undertake precipitate action in 2020.

Is Chaos Likely to be Expressed as Paralysis and Distraction?

As very real crises begin to emerge, what is significant is that urban societies tend to avoid all consideration of them and turn to the distractions of belief systems, particularly climate change politics (which is separate from actual climate change science). These drive internal societal passions, but paralyze capabilities to deal with actual strategic challenges.

A sense of “social distress” is likely to become exacerbated in major urban societies as the economic decline of the PRC begins to bite the global economy.

This will further polarize societies and impact funding for technological evolution.

“We’d Rather Die At Home” – Chinese Citizens Rebel Against Mandatory Quarantine As Lockdown Expands

Thousands of athletes around the world breathed a sigh of relief on Thursday when Japanese Prime Minister Shinzo Abe confirmed that the Summer Olympics in Tokyo won’t be delayed. Then again, if the outbreak continues to worsen in Japan and the broader region, who is going to want to come if they don’t feel safe?

As the second week of global pandemic panic comes to a close, China, increasingly frustrated that their ruse with the WHO didn’t manage to calm the international community, again registered its “strong objections” to the growing number of travel bans directed at its citizens.

The warning followed a decision by Taiwan’s health authority to ban all international cruise ships from docking at the island from Thursday as the number of suspected outbreaks aboard cruise ships grows.

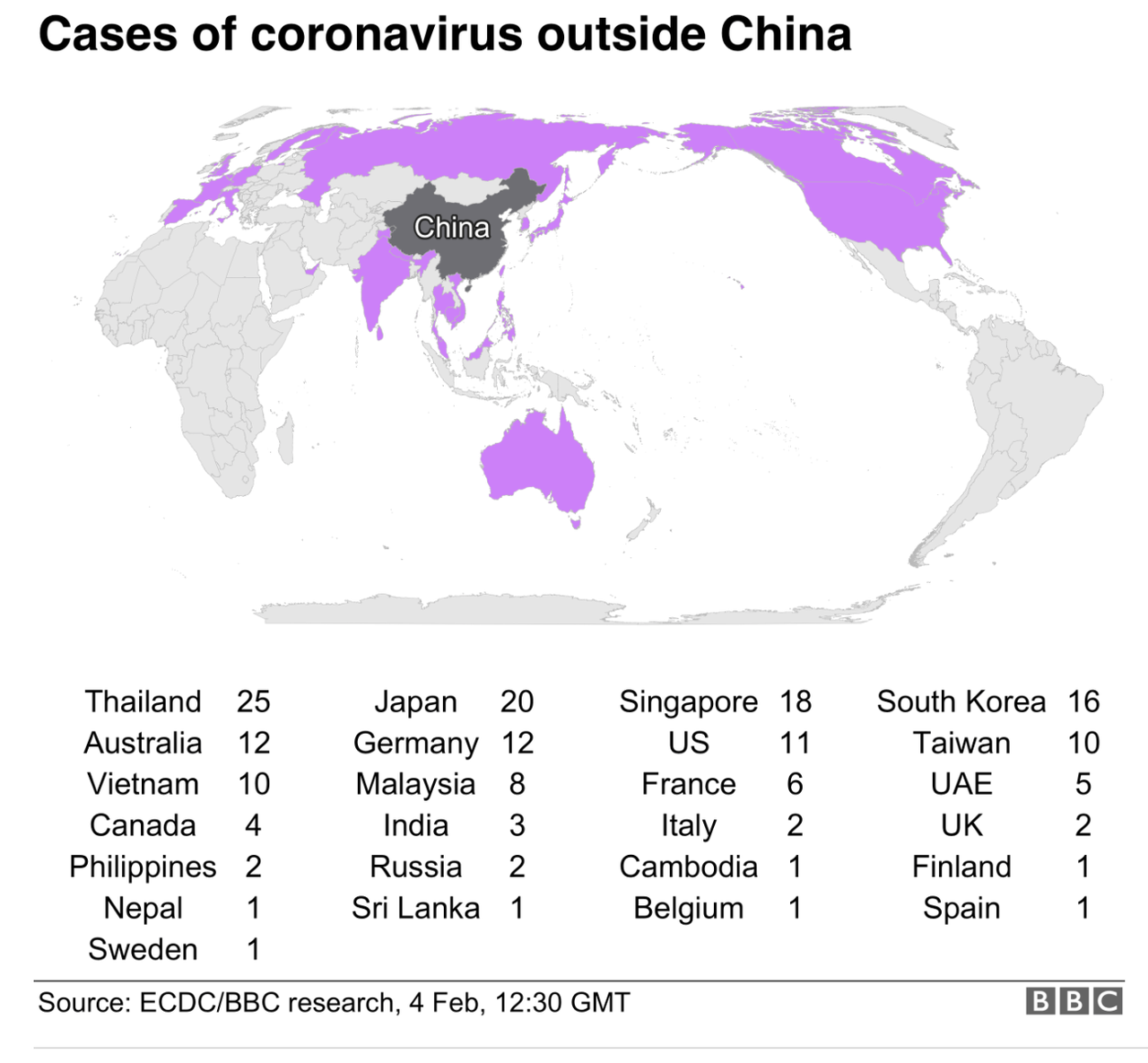

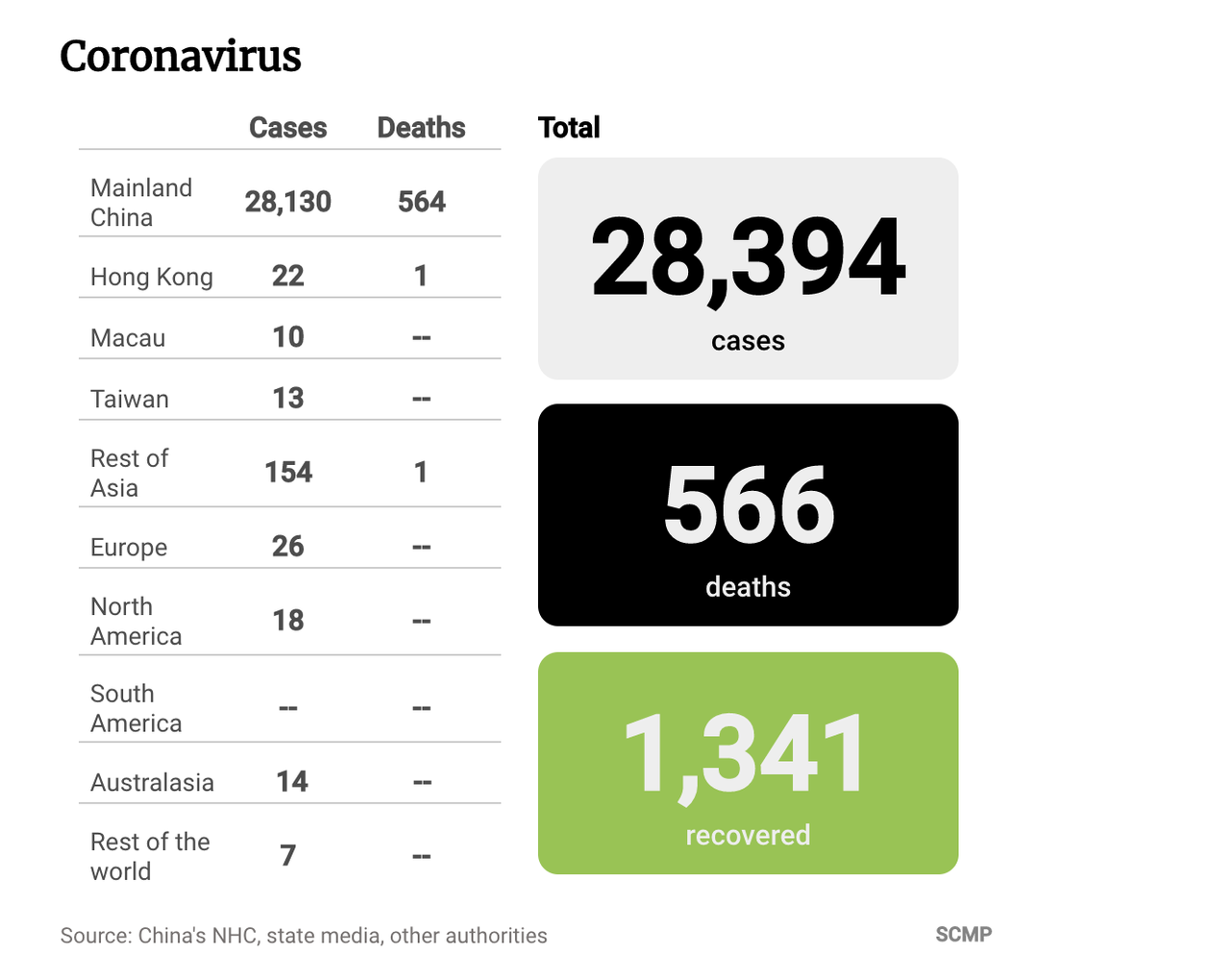

The global death toll has ticked higher, reaching 566 overnight, while the total number of confirmed cases has broken above 28,000 to 28,384.

More than a dozen countries have imposed some kind of restriction on foreigners who have recently visited China. Within China, images of police clad in hazmat suites and touting infrared thermometers have become frighteningly common. Many airlines cancelled passenger routes to China, and some are extending those cancellations out to March or April.

“China is strongly concerned and dissatisfied,” said a spokeswoman for China’s Foreign Ministry. “We hope relevant countries will bear in mind overall relations and people’s interests and resume normal operation of flights to guarantee normal people-to-people exchange and cooperation.”

“I must stress that certain countries’ ill-advised decisions to suspend flights to and from China are neither cool-headed nor rational,” she added.

But while Beijing tries to spin the narrative to accuse other countries of racism, some brave journalists have shared the stories of families brave – or foolish – enough to speak out against the regime.

One resident of Wuhan who has been stuck in the city since the quarantine told the BBC that his uncle died in a quarantine because of supply shortages.

The image of life in Wuhan is every bit as bad as the most chilling conspiracies would have you believe.

“My uncle actually died in one of the quarantine points because there are no medical facilities for people with severe symptoms. I really hope my father can get some proper treatment but no-one is in contact with us or helping us at the moment.”

“I got in touch with community workers several times, but the response I got was, ‘there’s no chance of us getting a bed in the hospital.'”

Beijing, which just announced a spate of new treatment-related projects in Wuhan and the surrounding area, seemingly can’t get beds online fast enough. Because the government is literally condemns some elderly patients to die in their homes.

But for people like us, we can’t even get a bed now, let alone get one in the new hospitals.

If we follow the government’s guidelines, the only place we can go now is to those quarantine points. But if we went, what happened to my uncle would then happen to dad.

So we’d rather die at home.

Many are saying that if they knew authorities would lock down Wuhan last week, they would have left for the holiday earlier.

What I want to say is, if I knew they were going to lock down the city on 23 January, I would have definitely taken my whole family out, because there’s no help here.

If we were somewhere else, there might be hope. I don’t know whether people like us, who listened to the government and stayed in Wuhan, made the right decision or not.

In news from outside China, Indonesia is reportedly planning to build a quarantine center on an uninhabited island to isolate coronavirus victims, even though Indonesia has yet to record a single case of the virus, though 243 have been quarantined on the island of Natuna.

Across the globe, health officials are racing to develop treatments and testing methods for the virus. Wuhan, ground zero of the outbreak, opened an emergency test laboratory on Wednesday to begin human trials.

Over in Hong Kong, a top public health official has declared a community outbreak, according to the SCMP.

A day after the city government revealed that it would impose a mandatory 14-day quarantine on anybody crossing into Hong Kong from China, the city government has provided some more details on how it will combat the crisis. Most of the new cases in the city are being caused by human-to-human transmission. Six people have been diagnosed with the coronavirus over the past few days, five of whom had not left the city recently. Of the 21 cases in total, eight are believed to have no travel history relevant to the coronavirus.

Circling back to the mainland, local authorities in the city of Tianjin announced on Thursday that it would ban the exit and entry of its villages and compounds, becoming the latest city to essentially quarantine its entire population. Over in Wuhan, authorities are now demanding that all residents report their temperatures at least once per day.

So, that’s 60+ million people under quarantine in China. And though the pace of new cases in the country has slowed slightly, the virus is accelerating, especially in Asia.

Once again investors are made to believe that nothing matters. Only 2 trading days after Friday’s sell off $NDX made new all time history highs. Only 3 days after Friday’s sell-off $SPX made a new all time closing high. Only 4 days after Friday’s sell off $DJIA, $SPX and $NDX make new all time human history highs in premarket. Fours day, four up gaps, all unfilled at the time of this writing. The market of the overnight gap ups.

Why? Because the economic impact of the coronavirus is over or contained? Of course not, it’s far from any of that. Shutdowns persist, warnings of individual companies are mounting i.e. $TSLA, tumbling a day after the technical warning issued, global economic growth estimates are coming down and with them invariably take downs in earnings estimates.

What do markets do? Make new all time highs, back on the multiple expansion game from 2019 when no slowdown in earnings mattered as the liquidity injections from our central bank overlords overrode everything.

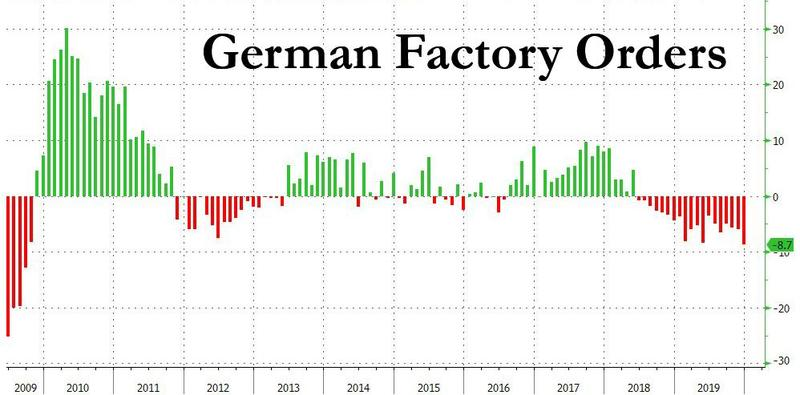

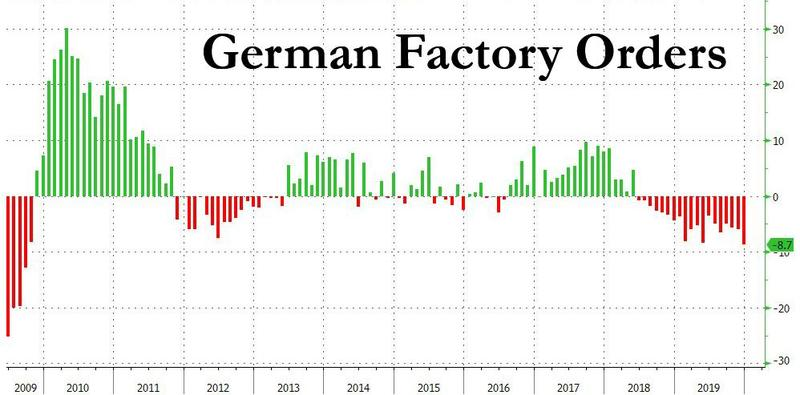

And so markets continue on their path of never pricing in any bad news and continue to disconnect farther and farther from the underlying size of the global economy no matter the ongoing data:

German factory orders:

Baltic Dry Index:

But there are no bubbles central bankers tell us. Don’t insult our intelligence I say. Especially since they perfectly well know that policies and words are closely followed by markets and are market impacting:

Lagarde: Traditionally, as central bankers we have been more comfortable speaking to experts and markets than to the general public. Markets closely follow what we do and what we say, and surveys and studies find that we are well understood by them.

Yet in the same breadth they tell us their polices are not to blame for the distortions created in markets.

Here’s ECB president Lagarde today in full denial mode:

They’re in denial:

Lagarde: “I wouldn’t draw the conclusion that our current monetary policy has actually been the main factor in the rise of housing prices, has actually been the main factor in the declining profitability of some banks”https://t.co/xiDgJzlH5b

But there is no inflation they same in the same breath.

Any wonder there are trust issues:

We don’t trust you until you are honest about the distortions central bank policies have unleashed on financial markets and come clean about what would happen if you ever normalize rates or your balance sheet. https://t.co/1PTLWECXfv

It’s a historic absurdity we are witness to and an ultimate tragedy unfolding before our eyes.

Central banks are in denial about the existence of the financial bubbles and distortions they themselves have created.

For to admit them would be to take responsibility and acknowledge that asset prices are sky high overvalued which in itself could lead to a risk off event as the admission of bubbles would lead to a loss in confidence, confidence which must always be maintained.

Central banks are residing in glass tower la la land. There is no trust, no transparency, no accountability. Only denial.

And so we see a market running on nothing but optimism despite continued disappointment about the reality on the ground:

Lions and tigers and bears. Oh my!

Virus optimism

Trade optimism

and rate cut optimism

Overnight futures ramped on the news that China proactively cut tariffs. You think that’s a sign of China thinking the economic impact of the virus is contained and happy days a here again?

I wonder:

How long before people realize that China proactively capitulating on tariffs is a sign of how serious the economic impact of this virus situation actually is?

Look, this tariff reduction was already agreed to. This in itself is not a rationale for further multiple expansion in markets, especially as one of the reasons for last year’s multiple expansion was based on supposed phase one terms which are now being walked back due to the coronavirus.

So you see there’s a circular drain that’s flushing down justifications for support of ever widening multiple expansion in lieu of growth projections again coming down.

Central banks are wanting you believe their policies cause no asset price distortions, don’t cause bubbles and will surely tell you they are not to blame when this bubble, that they deny to exist, eventually pops.

Central banks may have entered the state of denial, doesn’t mean investors have to. The economic impact of the coronavirus is real, but sentiment is managed with new highs in equity prices. For now. While the virus will at some point be properly contained as of now there is no verified cure and no clear visibility as of yet when the economic impacts will be alleviated, the longer it drags on the more profound the effects. The death toll has not anywhere near reached the annual deaths tolls from the common flue, but the impact is already lager then SARS and nobody knows as of this moment how far this will ultimately go, not the WHO, not China and certainly not central banks.

Reality is markets are getting ever more stretched and investors keep piling into tech even as $NDX is screaming a major warning signal.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Tesla Shares Plunge Again As Company Says It Will Shutter China Stores Due To Coronavirus

Following yesterday’s record 17% drop, Tesla shares are down again in pre-market trading on Thursday after the company announced it is temporarily closing stores in mainland China as of February 2. Tesla shares dropped another 5% in early trading Thursday morning ostensibly on a combination of the China news, and what probably is just a badly needed reality check after a 72-hour parabolic binge due to a short squeeze, gamma-hedging frenzy and increasing numbers of hysteric retail traders.

The company announced in an online post to its employees that it temporarily closed its stores beginning last Sunday. The move follows suit with the rest of China, which has ground to a standstill to try and control the coronavirus, which has (according to the Chinese government) killed more than 500 people. That number is in dispute.

CNBC translated a note that was sent to Tesla China employees on WeChat regarding the closures. It stated:

“From today on, Tesla stores are all closed throughout China. But I will answer questions online, around the clock. Online orders are still welcome. We suggest all of you stay home, and take good care of your health.”

Tao Lin, a Tesla VP in China, also helped along the company’s 17% decline on Wednesday when he announced on Weibo that cars scheduled for delivery in early February would be delayed due to the spread of the virus. Shanghai has ordered local businesses not to resume work before February 10, which means that Tesla’s production factory is also shut down.

This, of course, led us to ask why Tesla doesn’t just set up another quarantine tent for production like they did in Fremont?

Tesla has 24 stores in mainland China and its Chinese operations have been a large catalyst for hype around the stock over the last several months, since the company’s Shanghai plant was completed.

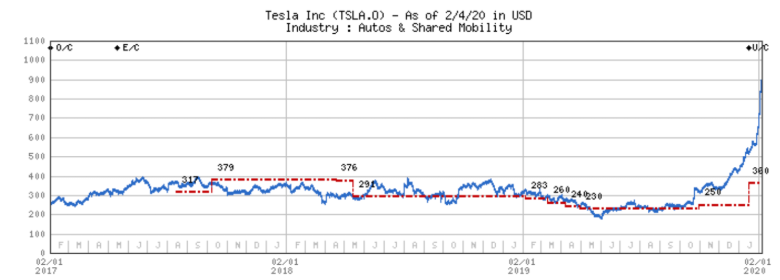

As for the stock, we wouldn’t be surprised to see the reality check continue. Even one of Tesla’s most ardent supporters, Adam Jonas at Morgan Stanley, issued a note Thursday morning with an underweight rating and a $360 price target – now about 50% downside – saying it is “too soon” to declare a winner in the global EV market.

He noted the astounding volume with which Tesla has traded. Jonas says that “Tesla traded over 48 million shares on Wednesday (over 25% of shares outstanding) for a value traded of approximately $36bn. For comparison, Apple, a company with roughly 10x the market cap of Tesla traded approximately $9.5bn of value yesterday. Tesla traded nearly 4x the value of the world’s most valuable public company.”

Tesla stock price (blue) vs. Morgan Stanley price target (red)

And he also was cautious about calling Tesla the winner in the EV space, given its new entrants: “Moreover, with US and global EV penetration at approximately 2% we believe it may be too early to declare the ultimate winner in the global EV market. At a minimum, there may be substantial risk to modeling the growth and market share of a market at such a low level of maturity today.”

He concluded by noting that even the bulls he was speaking sound like they are starting to change their tone:

“We continue to engage with investors in high volume on Tesla, but noted a slight change in feedback where even some bulls on the name we have spoken with have expressed a degree of uncertainty, and in some cases, concern around the recent price action..”

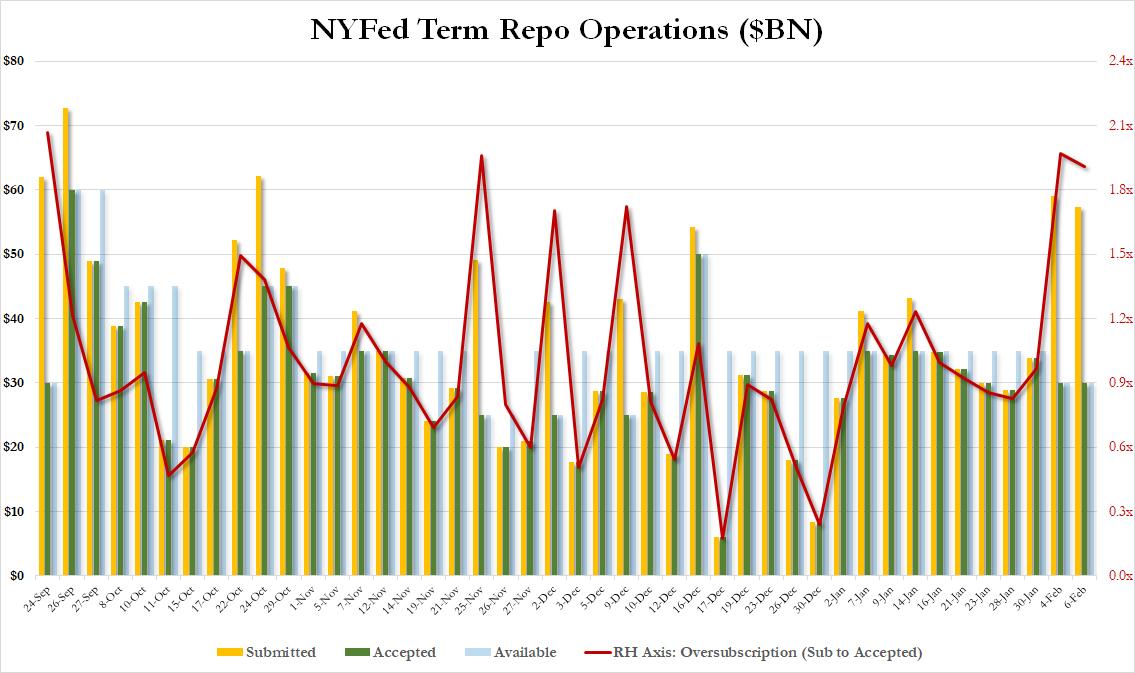

Another Massively Oversubscribed Term Repo Confirms Persisting Liquidity Woes

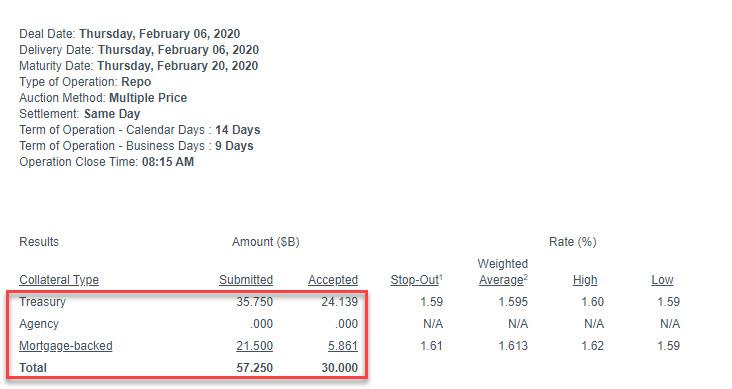

Two days after dealers unexpectedly flooded the first reduced term-repo (from $35BN previously to $30BN) offered by the Fed, the liquidity shortage in the repo market – which was supposed to be temporary and few if any strategists said would continue beyond year-end – persists, and today the Fed announced that in its latest 2-week term repo (maturing Feb 20), it was $57.25BN in submissions ($35.75BN in TSYs, $21.5BN in MBS) for a maximum $30BN in available reserves.

This means that for the second time in three days, the term repo operation saw a massive oversubscription, which at 1.9x was the 4th highest ever since the Fed restarted term-repos in late September, and just shy of the 2.0x submitted-to-accepted ratio recorded on Monday.

As we concluded on Monday, “the massive demand for term repo today means that the liquidity crisis that continues to percolate just below the surface of the market and has clogged up the critical plumbing within the US financial system, is getting worse, not better, and today’s massive oversubscription indicates that one or more entities continues to face a dire shortage of reserves, i.e., cash.”

We hope that eventually someone at the Fed will address this ongoing issue which was supposed to be resolved over a month ago.

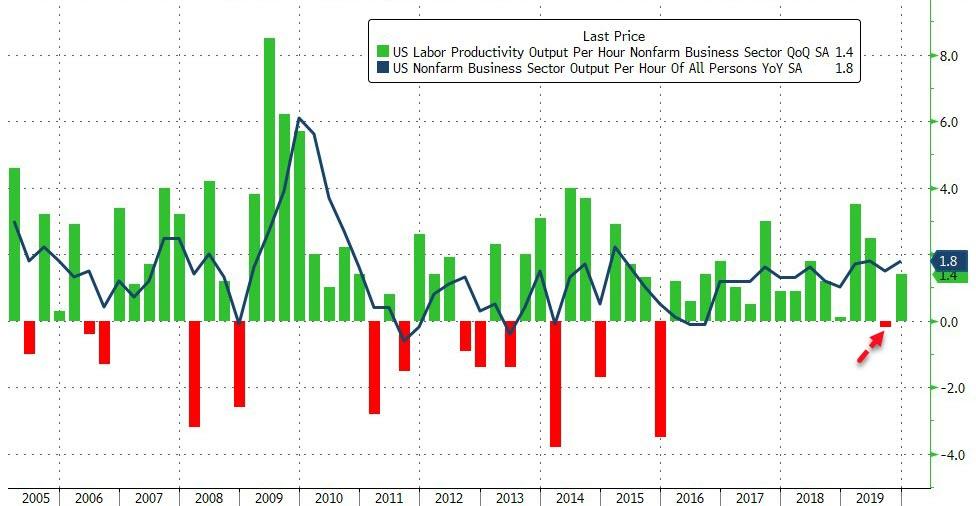

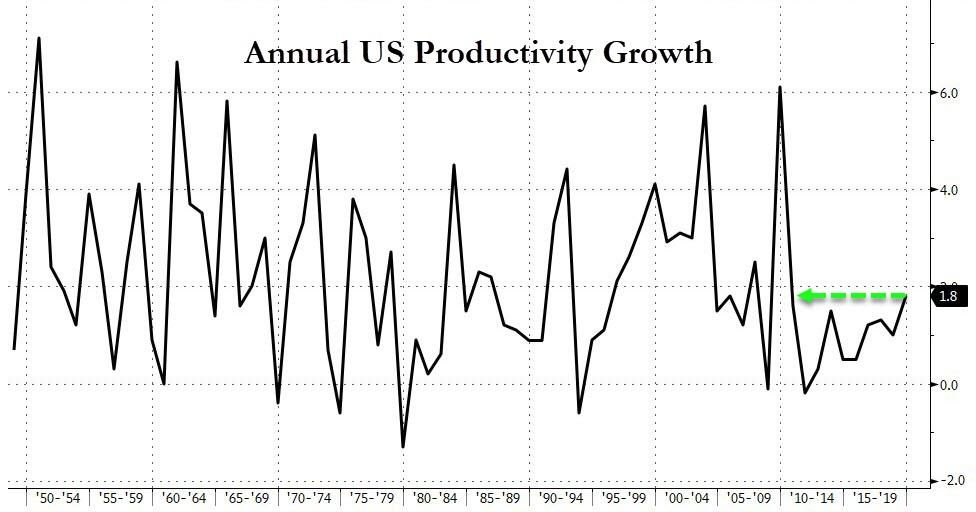

2019 US Productivity Rises Most In A Decade, Real Wages Jump Most Since 2015

After disappointingly contracting by 0.2% in Q3 2019, US Productivity was expected to expand by 1.6% QoQ in Q4, but while it did bounce back, the preliminary US productivity rose only 1.4% QoQ. This enabled a 1.8% YoY gain in productivity for 2019…

Source: Bloomberg

This is the biggest annual gain in productivity since 2009…

Source: Bloomberg

Unit labor costs were also up at a 1.4% rate following a 2.5% pace in the previous three months. The report showed inflation-adjusted hourly compensation averaged a 1.9% pace in 2019, the biggest gain since 2015.

Subdued productivity has been a long-running topic of debate among economists. In an October 2019 speech, Federal Reserve Chairman Jerome Powell pointed out several possible reasons, including that the productivity slowdown may be overstated due to mismeasurement.

Earlier this week, former Fed Chair Janet Yellen said slow productivity growth is a “huge concern.”

Will we wonder, what were we thinking? and marvel anew at the madness of crowds?

When we look back on this moment from the vantage of history, what will we think? Will we think how obvious it was that the coronavirus deaths in China were in the tens of thousands rather than the hundreds claimed by authorities?

Will we think how obvious it was that the virus would spread around the globe, wreaking havoc on the global economy and social order, even as the authorities claimed only a handful of cases had arisen outside China?

Will we be amazed at the delusional confidence that the U.S. economy would be untouched by the virus as stock markets quickly soared to new all-time highs while the world’s largest economy ground to a halt in a desperate attempt to close the barn door after the horses had already escaped?

Will we look back at the patently false data being promoted by authorities and wonder why the majority accepted it all as credible?

Will we re-examine all the smartphone videos posted on the web by average people and wonder why all the lies were given more credibility than actual videos?

Will we recall how content that didn’t parrot the approved narrative that everything was under control and the global impact would be near-zero was suppressed, banned, de-platformed or marginalized? Will we wonder at the complacency of all those who accepted this orchestrated suppression with such obedient passivity?

Will we look back at the claim that only twelve people in the entire U.S. had the virus, despite all the direct flights from Wuhan and the tens of thousands of people who’d traveled from China to the U.S. in January, and marvel at our credulity?

Will we look back at the wreckage left in the wake of the coordinated campaign to suppress the facts and lay the responsibility for all the carnage on the authorities who devoted more energy to hiding the realities of the pandemic than to preparing us for the impact?

Will we ponder the incredible grip of mass delusion on the human mind when we recall the confidence that the U.S. economy was invulnerable to the virus and the implosion of China, and the blithe quasi-religious faith that central banks would never let global stock markets decline even 2%?

Will we wonder how the mainstream could watch the Chinese economy shutting down and still remain absolutely confident that the global economy would be untouched as the spot of bother was sure to evaporate in a week or two and all would be restored to pre-virus euphoria?

Will we wonder what were we thinking? and marvel anew at the madness of crowds? Will we wonder why we embraced the delusion so readily, and relive the moment when the gate to reality creaked open? Will we relive our realization that we’d embraced an absurd fantasy floating on a tissue of lies, or will we bury that painful moment of truth?

{kind=link}