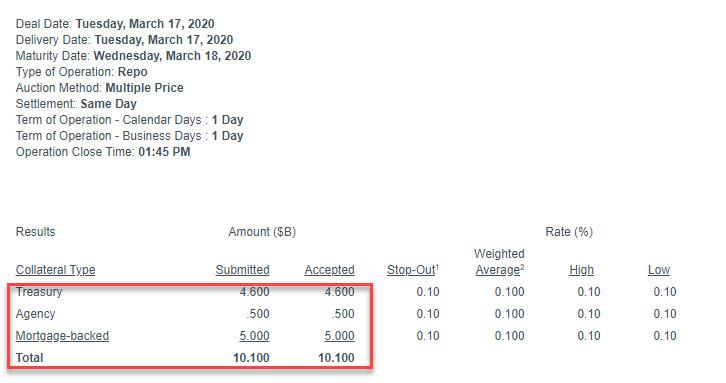

The Wrong Bazooka: Dealers Take Just $10BN Of $500BN Repo

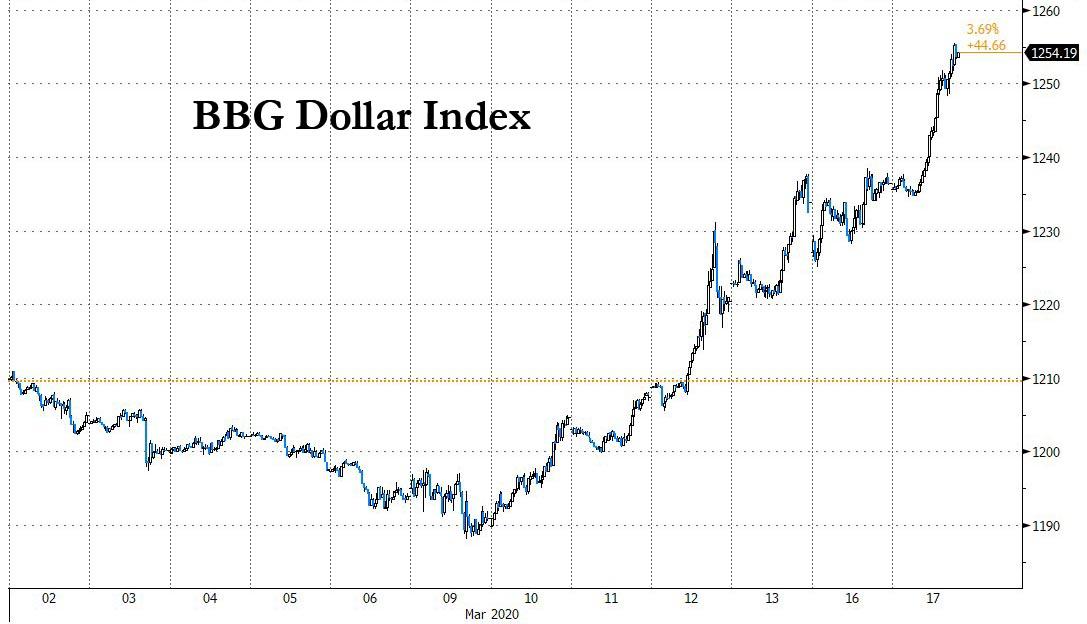

The Fed may have hoped that when it announced up to $5 trillion in monthly repo capacity last week, it would ease the funding crisis that has dragged the dollar to three year highs.

Alas, as Zoltan Pozsar explained earlier (when he demanded a Fed backstop of virtually anyone, anywhere), so far it is failing as just confirmed by the latest ad hoc repo operation that was announced earlier today, supposedly to reverse the spike in overnight GC funding, yet which saw the lowest submissions of any of the Fed’s expanded repo operations yet: with up to $500 billion in total capacity, the repo operation saw only $10.1 billion in submissions, or just over 2%!

So if domestic repo lines are not the panacea that is needed to thaw the dollar market, what is? For the answer we point readers to the rather draconian conclusion offered by Zoltan Pozsar earlier today, which was the following:

backstop not only the banks at the core of the financial system, but also markets and non-banks. The market backstops should include the CD and CP market where we need a buyer of last resort as the structural buyers of paper are losing cash fast; the backstop of the FX swap market should include daily operations at more points along the FX curve.

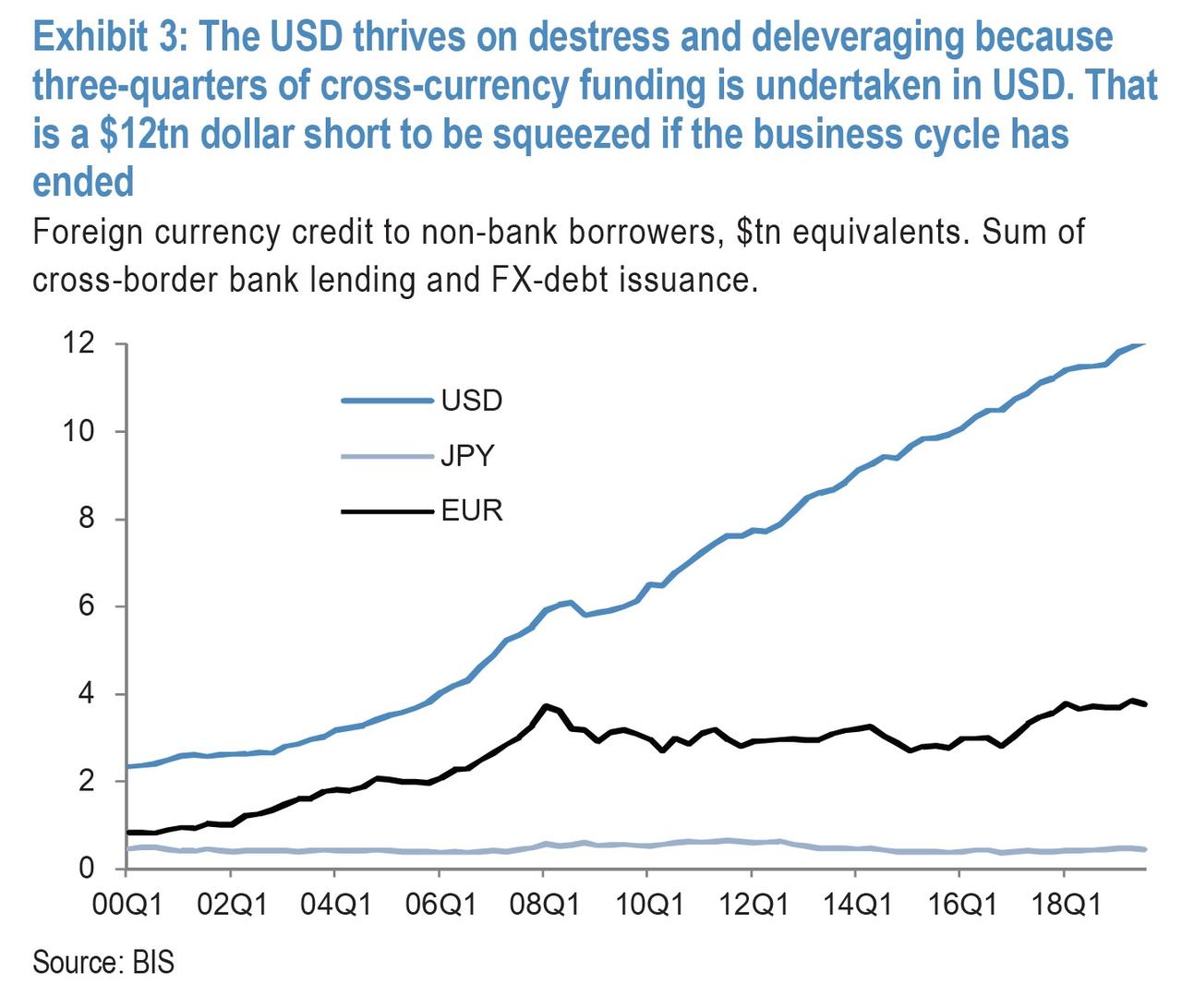

In other words, we have cross a rubicon where absent a backstop and bailout of pretty much any USD-denominated financial asset anywhere will lead to an acceleration of the already acute dollar short squeeze which JPM calculated to be as large as $12 trillion.

“Bloody Tuesday”: In Unprecedented Move, China Expels All Foreign Journalists Working For NYT, WSJ, WaPo

In the latest escalation of tensions, China announced on Tuesday that it would expel all foreign journalists working for the New York Times, WSJ and the Washington Post. It also demanded that those outlets – as well as VOA and Time Magazine – provide the Chinese government with detailed information about their operations in the country, the NYT reports. These include “all written materials” including staff finances, operations and real estate information in China.

Experts described the move, which was retaliation for the Trump Administration limiting the numbers of Chinese citizens who can work for Chinese media agencies in the states

Hua Chunying, a prominent government spokesperson for China’s Ministry of Foreign Affairs, said these were necessary countermeasures to fight back against the Trump Administration’s “cold war mentality.”

The decisions are entirely necessary countermeasures that China has been forced to take because of the unreasonable oppression that Chinese media organizations experience in the US. They are legitimate, justified self-defense in every sense.

One American reporter described the move as “unprecedented.”

Bloody Tuesday.

Chinese Ministry of Foreign Affairs just announced it is expelling all the American reporters at Wall Street Journal, New York Times, and Washington Post.

Though the decision was likely in the works for weeks, as Beijing threatened retaliation after Trump expelled the reporter, it’s notable that these expulsions are arriving following Trump’s decision to double down on the phrase “Chinese Virus” to refer to the novel coronavirus.

The journalists being expelled include the NYT’s Edward Wong, a diplomatic correspondent for the NYT and Harvard Nieman Fellow.

Shortly before the news broke, Wong tweeted that Chinese diplomats around the world are pushing propaganda to try and “bury” the flaws in the Chinese governance model that helped perpetuate the Wuhan outbreak, which could have easily been nipped in the bud.

Chinese diplomats around the world are now engaged in pushing propaganda to try to bury how flaws in the Chinese Communist Party’s governance model — notably its lack of transparency — helped lead to the Wuhan outbreak months ago. This effort damages China’s credibility. https://t.co/50dCET5a8d

Breaking: China retaliates against new US policy on Chinese state-run media. Says 5 US organizations are now “foreign missions.” Demands US citizens working for NYT, Wash Post & WSJ turn over press cards in 10 days & stop work. Can’t report in HK or Macau. https://t.co/nnpvlg2aD9

Of course Beijing is furious that President Trump keeps calling Covid-19 the “Chinese Virus” – but not because it’s racist, because the CCP is trying to convince the Chinese people that the virus came from the US.

Facebook Employees To Receive $1,000 Bonus During COVID-19 Outbreak

Facebook is giving every employee a $1,000 bonus in order to help with bills during the coronavirus outbreak, according to The Information.

CEO Mark Zuckerberg announced the cash relief in an early Tuesday internal company notice, adding that he wants to support employees working from home due to the pandemic, according to two people familiar with the matter.

As we reported yesterday, a government plan to give each American adult $1,000 has been picking up steam after Sen. Mitt Romney (R-UT) endorsed the idea on Monday. Sen. Tom Cotton also says he’s working on legislation that would include cash stipends for Americans affected by the outbreak.

Meanwhile in Chicago, restaurant workers, delivery drivers and other low-wage employees who receive tips can now access emergency cash if they are affected by the pandemic, according to CBS2 Chicago.

The One Fair Wage campaign has launched an emergency cash relief fund and is offering $213 in cash for any tipped worker affected after some states including Illinois temporarily shut down bars and restaurants to stop the spread of the virus. The organization is also seeking donations to help fund the effort. –CBS2 Chicago

“This global health crisis for all of us is also an acute economic crisis for tipped workers and service workers,” said co-founder of One Fair Wage, Saru Jayaraman. “These are the workers who have trouble making ends meet in good times. In hard times like this, they need our help. We’re hoping to raise as much money as possible to give as many workers as possible cash assistance of $213.”

“We chose that amount as a nod to the horrific $2.13 federal sub-minimum wage for tipped workers.”

Illinois bars and restaurants were closed on Monday following an announcement from Gov. JB Pritzker. While the closure is scheduled to last through March 30, Pritzker said the state was looking for solutions to keep restaurant kitchens open in order to provide food delivery to people’s homes. Meanwhile, drive-through and curbside pickup are still available.

Governments love crises because when the people are fearful they are more willing to give up freedoms for promises that the government will take care of them.

After 9/11, for example, Americans accepted the near-total destruction of their civil liberties in the PATRIOT Act’s hollow promises of security.

It is ironic to see the same Democrats who tried to impeach President Trump last month for abuse of power demanding that the Trump Administration grab more power and authority in the name of fighting a virus that thus far has killed less than 100 Americans.

Declaring a pandemic emergency on Friday, President Trump now claims the power to quarantine individuals suspected of being infected by the virus and, as Politico writes, “stop and seize any plane, train or automobile to stymie the spread of contagious disease.” He can even call out the military to cordon off a US city or state.

State and local authoritarians love panic as well. The mayor of Champaign, Illinois, signed an executive order declaring the power to ban the sale of guns and alcohol and cut off gas, water, or electricity to any citizen. The governor of Ohio just essentially closed his entire state.

The chief fearmonger of the Trump Administration is without a doubt Anthony Fauci, head of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health. Fauci is all over the media, serving up outright falsehoods to stir up even more panic. He testified to Congress that the death rate for the coronavirus is ten times that of the seasonal flu, a claim without any scientific basis.

On Face the Nation, Fauci did his best to further damage an already tanking economy by stating, “Right now, personally, myself, I wouldn’t go to a restaurant.”

He has pushed for closing the entire country down for 14 days.

Over what? A virus that has thus far killed just over 5,000 worldwide and less than 100 in the United States? By contrast, tuberculosis, an old disease not much discussed these days, killed nearly 1.6 million people in 2017. Where’s the panic over this?

If anything, what people like Fauci and the other fearmongers are demanding will likely make the disease worse. The martial law they dream about will leave people hunkered down inside their homes instead of going outdoors or to the beach where the sunshine and fresh air would help boost immunity. The panic produced by these fearmongers is likely helping spread the disease, as massive crowds rush into Walmart and Costco for that last roll of toilet paper.

The madness over the coronavirus is not limited to politicians and the medical community. The head of the neoconservative Atlantic Council wrote an editorial this week urging NATO to pass an Article 5 declaration of war against the COVID-19 virus! Are they going to send in tanks and drones to wipe out these microscopic enemies?

That is not to say the disease is harmless. Without question people will die from coronavirus. Those in vulnerable categories should take precautions to limit their risk of exposure. But we have seen this movie before. Government over-hypes a threat as an excuse to grab more of our freedoms.

When the “threat” is over, however, they never give us our freedoms back.

Zoltan Stares Into The Abyss: Here Is What The Fed Must Do Right Now To Avoid Global Devastation

Two weeks ago, on March 3, before a liquidity panic had gripped capital markets, corporations and global banks, Credit Suisse repo icon and former NY Fed staffer, Zoltan Pozsar issued a recommendation to halt the funding crisis early in its tracks, writing that the Fed should “combine rate cuts with open liquidity lines that include a pledge to use the swap lines, an uncapped repo facility and QE if necessary.” Unfortunately, since then the coronavirus supply chain (and payments) crisis has been joined by the oil price war, which has crippled the petrodollar exchange system by sending the price of oil sharply lower and exacerbating the global dollar funding shock.

And even though the Fed belatedly followed through with all of Pozsar’s March 3 policy recommendations, going so far as throwing a commercial paper bailout facility which was also recommended by BofA’s Marc Cabana (another former NY Fed staffer), the market remains unconvinced that any of this is enough, especially with JPMorgan warning that the world is facing an unprecedented dollar margin call, as a result of the $12 trillion synthetic dollar short, some 60% of US GDP.

Faced with this unprecedented dollar shortage, the Fed has so far failed to assure the world it can provide all the funding needed. Furthermore, as we said yesterday, in some ways we sympathize with the Fed, as every day something new breaks among this record funding strain:

One day it is ETF NAV discounts blowing out;

The next day the treasury Treasury Cash/Swap basis surges and funds suffer a historic VaR shock amid forced liquidations;

Day three sees the FRA/OIS explode higher as a massive dollar funding margin call strikes;

Then, day four sees the same repo crisis that was supposed to be fixed back in September return with a vengeance, as banks freak out about counterparty risk.

As we further said, “what the Fed needs is the monetary equivalent of Dr. House: someone who can diagnose what is actually wrong with the monetary plumbing, instead of using the same old shotgun approach of shoveling trillions in blunt liquidity into the market, which clearly is not working anymore.”

Alas, that is not a credible option, meanwhile the Fed’s liquidity injections are failing with the BBG dollar index – the simplest proxy of dollar demand alongside FRA/OIS and FX basis swaps – continuing to surge as various actors rush to procure what, with all due respect to Ray Dalio, is the opposite of trash.

Confirming our take that everything the Fed does, including this morning’s Commercial Paper facility restart, is either insufficient or targeting the wrote underlying cause (today even BofA’s Marc Cabana who pushed for the CPFF slammed it, saying “this facility does nothing to assist the money funds trying to raise cash and address outflows”), is none other than Zoltan Pozsar who in his latest note published this morning, writes that “all segments of funding markets – secured, unsecured and FX swaps – continue to show growing signs of stress”, prompting him to conclude that “the Fed may have to do more still.”

Scratch “may”, and replace with “will”, unless Powell wants to watch the dollar short squeeze go all “Volkswagen” on him.

So what can the Fed do? Well, according to Zoltan, the time for half-measures is over (incidentally, he too panned the Fed’s CFPP writing that “the Fed needs to become a buyer of CDs and CP, but not through the CPFF”), and instead the printer of the world’s reserve currency has to become the bank of last resort not only for US institutions, where access should be expanded to non-banks, but also banker to the entire world in the form of unlimited, 24/7 swap lines open with every central bank, not just the G7.

Below we present a summary of his must read “Fed must act or else” note:

The Fed’s liquidity injections appear not to be working.

All segments of funding markets – secured, unsecured and FX swaps – continue to show growing signs of stress. The Fed may have to do more still.

In the U.S., we watched, but didn’t feel the funding impact of large banks in other countries being asked to help their economies. Now that U.S. banks are asked to do the same, dollar funding markets are starting to feel the impact.

As U.S. banks increase their lending to the real economy as corporations draw on credit lines and banks lend more to households and firms, lending will consume more balance sheet and risk capital, and that will leave less room for market making and arbitrage, which under current circumstances are “luxury”.

The breakdown of o/n repo markets yesterday tell us that balance sheet is now getting scarce to conduct even the most basic type of market making.

As banks are pulling back from market making, the Fed and other central banks need to assume the role of dealer of last resort…

The Fed needs to become a buyer of CDs and CP, but not through the CPFF.

The Fed needs to offer dollars on a daily frequency through the swap lines, and other central banks need to lend dollars on to both banks and non-banks.

The Fed needs to broaden access to the swap lines to other jurisdictions as dollar funding needs are large in Scandinavia, Southeast Asia, Australia and South America, not just in the G-7. The dollar funding needs of both banks and non-banks is what’s at risk and the assets that are being funded are U.S. assets – Treasuries, MBS and credit – so the Fed has a vested interest.

A hallmark theme of the post-QE global financial order has been the secular growth of FX hedged fixed income and credit portfolios at non-bank institutions like life insurers and asset managers from negative interest rate jurisdictions – the new shadow banking system, epitomized by money market funding (FX swaps) of capital market lending (Treasuries and the full credit spectrum).

Carry makes the world go round and as banks do more for the economy central banks will have to backstop the shadow banking system – yet again…

Summarizing the above is simple: Pozsar is basically recapping what we said in “The World Is Hit With A $12 Trillion Dollar Margin Call“, and explains that to fix this potentially catastrophic margin call, the Fed must grant access to virtually every global entity in need of dollars, including those shadow banks which over the past decade scramble to lever themselves to the gills, fully aware that when the day came, the Fed would bail them out.

That day has arrived, and it Pozsar’s proposal is accepted – and in the past everything he has suggested was promptly pursued by the US central bank – it means that the Fed is about to bail out the world.

The repo export than notes that he is most concerned about four key areas which the Fed has so far failed to address:

liquidity in the CD and CP markets;

the frequency with which the Fed plans to do swap line operations and the FX points where it’s active;

the funding needs of institutions;

the regions that aren’t embraced by the swap lines.

Going down the list, Pozsar first focuses on the initial shock to the CD and CP markets which he notes came from the equity market collapse and the flows it triggered whereby cash started to flood back from securities lenders’ cash collateral reinvestment accounts to short sellers’ accounts.

Given that secured lenders invest cash in the CD and CP markets and short sellers invest mostly in Treasury bills, these flows turned sec-lenders into net sellers of CD and CP, precisely when issuance from corporations and banks is picking up. Outflows from prime money funds have been small to date, but given ongoing stresses in funding markets and heightened risk aversion, prime funds could see more outflows this week as investors take refuge in the safety of government money funds. Such a rotation would further hurt demand for CD and CP this week and will continue to pressure funding spreads including U.S. dollar Libor-OIS.

This is notable because it explains why Pozsar does not think that the right solution now is to reactivate the CPFF, as the Fed just did:

The legal aspects of onboarding issuers takes time and liquidity can kill you quick. Our recommendation would be for the Fed to come to an agreement with the U.S. Treasury whereby the latter provides a “first-loss buffer” on any financial or non-financial CP the New York Fed buys in the primary or secondary market. The first loss buffer would ensure that the Treasury takes the credit risk and the Fed only takes the liquidity risk such that the Fed feels “secured to its satisfaction” – which is what the Fed cares about most in a crisis situation.

The money to fund such a first loss buffer is already in the system – it’s sitting in the Treasury General Account. Putting up $50 billion of the $400 billion sitting idly at the Fed would provide sufficient comfort for the Fed and near immediate support for the market – the Bank of Japan and the Bank of Canada already buy CP in their domestic jurisdictions.

And since the Fed is now going, all in, Pozsar says that “this template could then be extended to corporate bond purchases by adding more buffer and as President Dudley would say “going out the curve and down the credit spectrum”. And why stop there, after corporate bonds the Fed can also buy stocks, and oil, and baseball cards, and why not fresh air… But not gold, never gold, at least not until the Fed is ready to fully devalue the dollar against the precious metal, which is also coming in the near future. But we digress…

Second, Pozsar is concerned that the Fed’s FX swap lines are now active “but it feels like the operational aspects of it need to be fine-tuned. Currently dollars are being offered weekly, but the FX swap market trades like they should be offered daily, and not only at weekly and three three-month maturities but at ultra-short tenors as well, similar to how the Fed lends in the repo market.”

Third, the swap lines (which we first profiled in late 2009) are open only for banks which is a legacy “fault line in the system.” The swap lines were originally designed to help the funding needs of banks during 2008; they work by the Fed lending dollars to other central banks which then lend it to banks. But since the financial crisis, non-banks eclipsed banks as the biggest borrowers in the FX swap market: a hallmark theme of the post-QE global financial order has been the secular growth of FX hedged fixed income and credit portfolios at non-bank institutions like life insurers and asset managers – the new shadow banking system epitomized by money market funding (FX swaps) of capital market lending (Treasuries and credit).

According to Pozsar, unless these non-bank entities get access to dollar auctions – from local central banks – FX swap spreads may remain wide if banks won’t serve as matched-book intermediaries; in other words, yet another half-baked liquidity bailout which will not reach the target audience. Additionally, there is a growing risk that such intermediation will fracture as the assets that FX swaps fund include not only Treasuries but credit and CLOs too. Credit quality is fast deteriorating across various sectors and that makes it riskier for dealers to fund some life insurers through FX swaps, just like it became riskier to fund some insurers during the 2008 crisis.

As Pozsar puts it, “over the past five years balance sheet and the availability of reserves were the main drivers of spreads in the FX swap market. It’s time to think about credit risk creeping in to funding markets through the asset side of some portfolios funded through FX swaps.” To this we will also note that counterparty risk – especially when a certain massive European bank is involved – is also starting to be a factor when making funding calculations… just like 2008.

Fourth, and final, the repo expert believes that the geographic reach of the swap lines is too narrow. The Fed has swap lines only with the BoC, the BoE, the BoJ, the ECB and the SNB, and that’s because the 2008 crisis hit banks mostly in these particular jurisdictions. But the breadth of the current crisis is wider as every country is struggling to get dollars. The dollar needs of Sweden, Norway, Denmark, Hong Kong, Singapore, South Korea, Taiwan, Australia and Brazil and Mexico seem particularly striking for a variety of reasons.

Scandinavia countries, like Japan have large dollar needs due to institutional investors’ hedging needs and only Norway is endowed with large FX reserves to tap into. Mexico is dealing with a terms of trade shock due to the collapse of oil prices. Southeast Asian countries that serve as banking centers need U.S. dollars to clear dollar payments and countries like South Korea and Taiwan have life insurers with meaningful hedging needs.

Finally, sooner or later, one will also have to include China – and its upcoming dollar maturity wall – to this list.

In short, “the Fed’s dollar swap lines need to go global, the hierarchy needs to flatten.”

* * *

Concluding the surprisingly short – for his standards note – Pozsar says that the message for central banks that emerges from this brief note is this:

backstop not only the banks at the core of the financial system, but also markets and non-banks. In short: backstop/bailout everyone. The market backstops should include the CD and CP market where we need a buyer of last resort as the structural buyers of paper are losing cash fast; the backstop of the FX swap market should include daily operations at more points along the FX curve.

Additionally, “Like primary dealers offer round the clock liquidity across timezones, dealers of last resort – the central banks of the swap network – should offer dollar liquidity round the clock too.”

Finally, like primary dealers, who trade with anyone with an ISDA, dealers of last resort should too: “the Fed by broadening access to other central banks and other central banks by broadening access to dollar auctions to non-banks like life insurers and asset managers.”

While free market capitalists will howl with rage at what the former Fed staffer is proposing, he makes a valid point that demand on bank balance sheets will increase from here to provide credit locally for the real economy – that will consume balance sheet and risk capital and will naturally leave less room for market making and arbitrage, which under current circumstances are luxury. Of course, none of this would have been an issue if instead of buying back trillions in their own stock, pushing the stock price to all time highs, corporations had simply saved for a rainy day… a day like today when it is pouring and hailing. But alas, while we warned repeatedly that a day of buyback reckoning is coming, nobody bothered to do anything at the time to reverse it. And now it’s too late.

In his final observation, Pozsar writes that “while it’s too much to ask central banks to lend to the real economy” – but why, after all if we are going there, why not load up the proverbial helicopter with money and just make it rain: why should just the financial sector benefit from this last systemic bailout – “it’s not too much to ask them to become more active in making markets as banks free up balance sheet for lending more to the real economy. The breakdown of o/n repo markets today tell us that balance sheet is now scarce to conduct even the most basic type of market making.”

He also points out that while charts showing Target2 balances became known as the visual representation of the ECB clearing payment imbalances between northern Europe and southern Europe through the balance sheet of local central banks within the eurozone, “it’s now time for the Fed to do the same globally with other central banks and for those central banks to lend broadly – after all what is at stake here is the funding of U.S. assets: Treasuries, MBS and credit.”

In short: bail out everyone… everywhere. The alternative is 107 years of fake price discovery and Fed market manipulation crashing upon themselves, ending the fiat system as we know it, and leading to the biggest social, economic and financial catastrophe of all time.

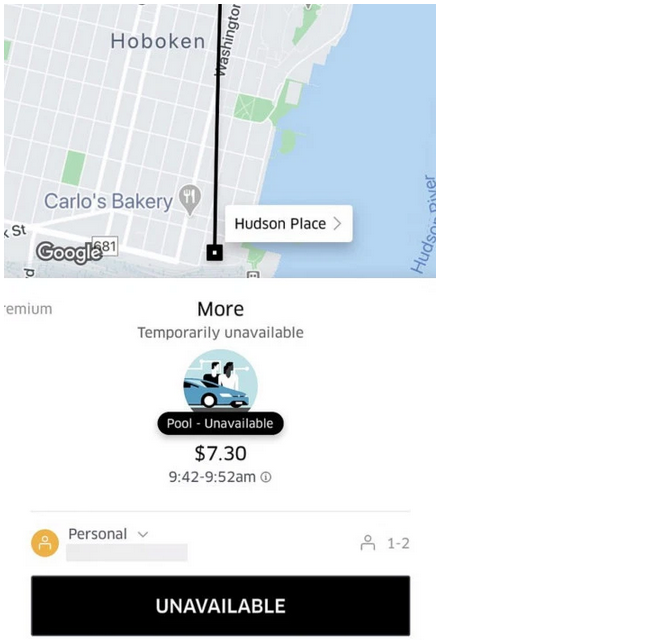

Uber and Lyft have suspended all shared rides in the United States and Canada amid the global coronavirus pandemic, according to The Sun.

“Our goal is to help flatten the curve on community spread in the cities we serve,” said Uber Senior vice president of Uber Rides and Platform, Andrew Macdonald. The company added that it would be monitoring services in other countries on a case-by-case basis going forward.

As of Tuesday morning, the Uber Pool option was listed as “unavailable” on the app – but that’s not the only measure the company are taking.

Uber has urged people to “travel only when necessary” in both Canada and the US, as well as urging users to wash their hands before and after they ride in an Uber to protect their drivers.

The carpooling company is also waiving delivery fees for independent restaurants in both countries after eateries and bars shut down en masse to curb the spread of the virus. –The Sun

Meanwhile, Uber’s food delivery service, Uber Eats has introduced a ‘leave at door’ option – similar to delivery services Door Dash, Postmates and GrubHub, following a model which began in China after McDonald’s, Starbucks and other companies began offering ‘contactless delivery’ to reach customers at home and minimize the risk of transmission.

Uber is waiving delivery fees for independent restaurants in the US and Canada after eateries and bars have been shut down to foot traffic.

“We know there are always people who, for health and other reasons, might prefer a non-contact delivery experience and we believe this will provide customers with that option,” said Postmates in a blog post.

Having seen central banks and politicians begin to address the issue – and fail so far, Minerd warns in his latest note to clients that “shock and awe has fallen short…”

Where are we now?

The Federal Reserve’s (Fed) attempt to go for shock and awe seems to have been made with the idea that doing something unusual on Sunday night, after the market closed out strong on Friday, would be good for confidence.

Of course, the market didn’t take it that way.

Instead of inspiring confidence, the market seemingly responded as if the Fed knows something we don’t know and it’s actually worse than we think.

Monetary policy is not designed to deal with pandemics. Monetary policy is designed to provide adequate liquidity to the financial markets to keep them functioning, and I think the Fed is doing a pretty good job at this.

The Fed still has a number of tools at its disposal that haven’t yet been implemented. Probably the most important of these is Section 13(3) powers.

Section 13(3) can only be invoked with the approval of the Treasury in the first phase. The second phase would allow for the establishment of programs like the Troubled Asset Relief Program (TARP) and the Term Asset-Backed Securities Loan Facility (TALF), only with the passage of legislation in Congress.

Given the size of our economy relative to where it was 10–15 years ago, it would probably be appropriate for Congress to pass a TARP-style program of $2 trillion.

Then on the back of that, the Fed would have the ability to introduce a TALF-style program again.

So, it’s going to take some major firepower to resolve the forthcoming problems or the slide will continue.

What is your economic outlook?

My expectation is that there is no economic growth in the near term, that we’ve probably already entered a global recession.

The Chinese, for the first quarter, will print a gross domestic product (GDP) number which will not truly reflect the economic damage to their economy. Our best estimates are that the Chinese economy is contracting in excess of 15 percent at an annualized rate, and I’ve seen numbers as big as negative 40 percent.

Europe is probably already in a fairly severe recession at this moment.

If the United States is not already in a recession, it will enter one shortly.

While shutting down restaurants, schools, and major events, a lot of people are going to be without a paycheck—people who probably don’t have $500 of savings in the bank—and they won’t be able to cover next month’s rent, their car payment, and their living expenses. Given this dynamic, I see this getting much worse.

The risk is that for the first time since the 1930s we are facing the possibility of a downward spiral into something akin to a global depression.

We have at least a 10–20 percent chance that that’s the path we are on if policymakers don’t act quickly.

It depends on the policy response that we get out of Washington, D.C. We desperately need programs like TARP and TALF, that were used in the financial crisis to shore up failing industries.

The idea that Congress can address one failing industry at a time—like the airlines now with the $50 billion proposed bailout package—is wrongminded.

As the economy continues to slow, crisis will start to cascade through many industries, and the problems will come faster and faster.

The Families First Coronavirus Response Act, the Coronavirus emergency funding bill currently in front of Congress demonstrates how long it takes to react to something. There really needs to be a dedicated pool of money that is available to step in and salvage viable companies that are struggling.

And remember, TARP was a money-making exercise for the government. We should get away from the idea that we are bailing people out. With TARP, the U.S. government becomes a distressed investor, and also is helping to sustain the economy and the working class.

This is the scenario that leads to global depression. Should policymakers fail to get these sorts of programs in place quickly, there is increasing risk that we could fall into a deep, dark spiral.

What are you seeing in the markets?

We have yet to see wholesale panic.

From a value standpoint high-yield bonds or investment-grade corporates have only been cheaper relative to Treasurys 15 percent of the time. But valuation is a poor tool for timing the market. We’re not really seeing the kind of selling that you would see in a market capitulation. Selectively adding to risk is the prudent approach.

We have maintained the discipline of our robust investment process which is based on the belief that investors simply have not been compensated for taking on credit risk.

We believe our prudence leaves us positioned to deliver strong value for clients now and in the future by taking advantage of opportunities afforded to us in our position of strength.

I’m more concerned about the stock market. In the worst-case scenario, we could go back to the old highs of the market prior to the financial crisis. This would put the S&P 500 in the 1600 ZIP code. I’m not saying we’re going there, but it certainly makes me pause before I think about loading up on equities.

It is worth keeping an eye on emerging markets where interest rates have increased significantly. The next domino to fall as a result of the butterfly effect may well be here.

What would you advise investors?

At this stage it would be unwise to make a tactical play to reduce risk, then try to figure out where the bottom is, then get back in. For those types of investors, I think at this point you missed your chance to get out.

Investors panic too often and try to do too many tactical trades rather than just sticking with their long-term view. The opportunity to sell risk assets has passed.

Market Stalls As White House Task Force Warns “We’re Failing To Contain Virus”

The State Department’s Ambassador Deborah Birx poured some cold-water on Powell & Mnuchin’s coporate bailout rally when she told the American public that more must be done to contain this virus:

“If Americans continue going to bars, restaurants, other public places, we will fail in containing this virus.”

The Dow surged above Monday high stops, then tumbled on Birx comments…

Additionally, President Trump explained he was “not happy” with people who aren’t following the guidelines for self-quarantine, suggesting implicitly that the current “shelter-in-place” mandates may be elevated to full Italy/China-style lockdowns.

Did Obama-Era CDC Bureaucrats Botch The Coronavirus Testing Response?

By now, it’s become abundantly clear that the federal government’s sluggishness in distributing functioning tests to labs around the country is one reason why governors and big-city mayors across the country are closing schools and businesses in preparation for a de facto 2 week quarantine.

The government seemingly had the whole month of February to distribute tests, which it should have been receiving from the WHO, which had contracted with a small Germany biotech firm to to produce millions of tests.

Instead, the CDC had only distributed a few thousand tests at the end of last month, and seems to have only taken steps to fix the problem over the last week, after a hail of criticism from doctors and experts as thousands of patients complained they didn’t have access to tests.

Well, the left-wing press has been carrying out a campaign to place the blame for the agency’s failures squarely on the shoulders of President Trump, with the Washington Post lambasting him for closing a pandemic preparedness office set up by President Obama to combat Ebola – even as the official charged with dissolving the office, writing also in the Washington Post, that these charges are specious.

At any rate, we’ve noticed that these claims have largely been circulated by former Obama-era CDC officials, who have leapt at every chance to criticize the administration’s overall response, along with the ‘botched’ testing rollout, on cable news.

But in an investigative piece overnight, the Washington Post laid out how the CDC, acting mostly independently of the administration and in keeping with the precedent for epidemic response, strung the White House along by claiming to ramp up testing while many of the tests were defective. But even as some labs figured out how to fix the defects, and others carried out testing on their own, the CDC remained inexplicably inflexible until suddenly admitting that it had been wrong, then promising to do better, once the demand for tests hit a critical apex.

Fortunately, President Trump’s decision to strike partnerships with pharma companies, both established firms and startups, has helped swiftly compensate for the shortfall. But the lapse in surveillance during the month of February has dealt a serious blow to the effort.

To be sure, it seems Trump badly erred by appointing Alex Azar to lead DHHS and Dr. Robert Redfield to lead the CDC. Coming from the lobbying world and academia, they didn’t have the experience to lead the response, forcing them to rely on underlings inside the CDC, many of whom are career bureaucrats who resent the Trump Administration’s management of the bureaucracy.

When these underlings insisted that the ‘red tape’ was there for a reason, Redfield had little choice but to defer to their expertise, at least initially, before other outside experts started to complain.

Meanwhile, all the Obama-era employees and underlings responsible for getting their leaders up to speed (like Dr. Messonnier, who is mentioned several times in the WaPo report), repeatedly told their bosses that this is the standard response and that they must wait for the CDC to figure out this knot of problems before opening the gates to corporate partners.

And as far as Dr. Fauci is concerned, he actually works for the NIH.

Now, as WaPo mentions in the final paragraphs of its story, a former CDC director who led the agency during the Obama years is calling for an “investigation” of the CDC’s botched response.

Thomas Frieden, an infectious disease physician who served as CDC director under former president Barack Obama, called on Sunday for an “independent group” to investigate what went wrong with the CDC’s testing process. He said in the past, the CDC moved quickly to produce tests for diseases such as H1N1, or swine flu.

“We were able to get test kits out fast,” Frieden said on CNN. “Something went wrong here. We have to find out why so we can prevent that in the future.”

Frieden said the agency has been muzzled under President Trump and despite the multitude of problems with the rollout of testing, “the CDC is still the greatest public health institution in the world.”

We suspect he already knows where the bodies might be buried.

I’m beginning to believe the current “pandemic” is perhaps just the latest contrived “enemy of the state”. An opportunity taken by western governments that have, over the past 20 or 30 years, gotten bolder in their willingness to fabricate fear to secure a political end. Political ends are always about greater control, corruption, and ultimately, cover ups.

In the age where air has become second to digital noise in terms of ubiquity, and hyperbole has replaced truth as the journalistic objective, governments’ ability to leverage misinformation (i.e. propaganda) has become a precision tool. Like it or not, society has become confused by the amount of information thrown at us and that makes us susceptible.

But if this is contrived political hysteria, what is the objective?

I’ve heard people on either side of the aisle suggest it is to help or hurt Trump. And perhaps, it is that simple. However, given equally good points on both sides of that argument I am skeptical. So then what? Well, I think back to 9/11 and whether you believe it was an act of terrorism by our own government or some other group, the end result was the same – The Patriot Act, and a truckload of knock-on legislation that quietly edged out our individual rights and freedoms. All in the name of keeping us safe from harm.

Ok, but do we see any of that happening as a result of this current narrative? Of course. Right now a bill is making its way through Congress that most legislators, have admittedly, not read but are ready to approve. And perhaps the most glaring action is the $5 trillion financial bail out that took place over the weekend. This is by far, the biggest financial industry bailout ever to take place, at least on this planet. Most Americans have no idea a bailout is taking place and those that do will never come to know that the bailout began in early September. On September 2nd, the Fed began its second epic “bank bailout”. That is, it has nothing to do with the virus.

And it isn’t just banks but the entire sport of speculation that require a bailout. The leverage inherent in the sport of speculation, across all asset classes, has created an aggregate risk position so large there is no longer enough cash to cover the margin call.

And this is where we’ve run into trouble. In 2008, we had levered specific collateral instruments up using nonsensical economics. At the time I was studying financial engineering at Chicago Booth. I graduated in December 2008, after spending 2 years studying the models that were proving, in real time, to be absolutely wrong and creating massive pain for the bottom half of the economic food chain. To crawl out of that mess we printed trillions of dollars to bail out the large risk positions that had earlier created immense wealth for those on the top of the economic food chain.

This past weekend, once again the Fed announced a $5 trillion bailout and it went completely unnoticed by the public because we are distracted by a “world ending virus”. The largest financial bailout in the history of the world and nobody knows it happened because the focus is on a virus that to date, has resulted in 50 deaths in America (at the same time 8,000 deaths have resulted from the flu in America).

I am constantly having Italy being thrown at me evidence that the virus is going to wipe out humanity. So I decided to look into Italy, specifically. What I found is that each year in Italy has about 16K flu related deaths each year. That’s a little over 2K flu related each month of the flu 7 month flu season. And here are Italy’s Covid figures.

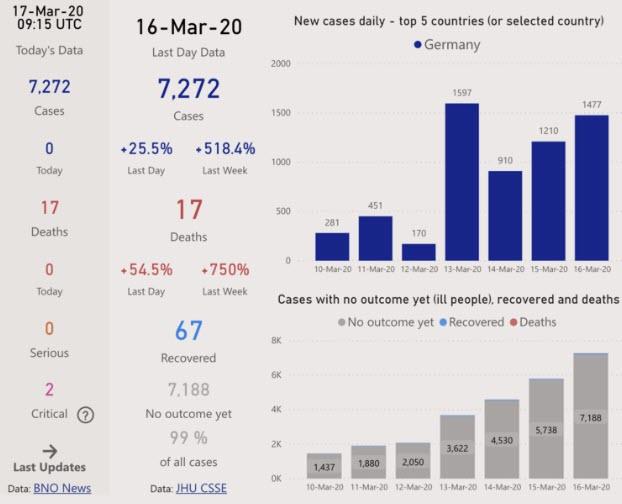

The new cases are in decline and the total death count in the 2 months since the outbreak began there, is at 2158, so about 1K per month (half that of the flu during the same period). And Italy is the worst case scenario in terms of mortality rate (fatality to recorded infections – yes this is a less than ideal statistic in terms of meaningfulness). Germany, for instance has an incredibly low mortality rate.

And let me be clear, I’m not saying we shouldn’t take this seriously. My point is whether or not the severe response from western governments is a reasonable response given the “threat”.

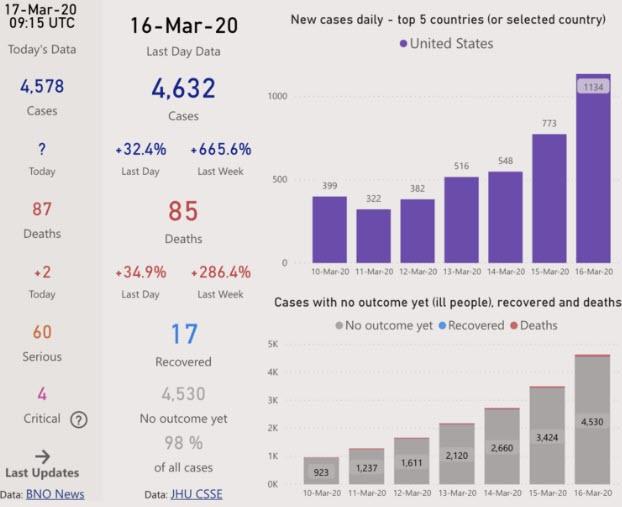

59 million Americans contracted Swine Flu, 265,000 were hospitalized, and 12,000 died from the 2009/2010 outbreak. Yet the public noise over that outbreak was so muted that I don’t even remember that it took place. Today, we have Covid, and in 2 months it has infected 4,600 Americans and 85 have succumbed to the virus.

If I were to show these figures to an alien and ask them to identify which scenario resulted in a lockdown of society, which do you suspect they’d point to? Exactly. 100% of you pointed to Swine Flu. 100% of you.

So how is it that the western governments picked Covid? And more importantly, why?