As Bloomberg notes, the spread of Libor to overnight index swaps should tighten as the Federal Reserve ramps up the reinstated Commercial Paper Funding Facility (CPFF).

Though we think the Fed and the Treasury are generally concerned about liquidity, a freezing of the CP market for industrial companies is a larger risk than for financial firms during the current crisis, in our view.

In 2007-09, asset-backed CP was the major risk, but today that’s less of a worry.

Industrial companies have few options other than CP for short-term financing, unlike financials, which can tap the discount window and other liquidity sources.

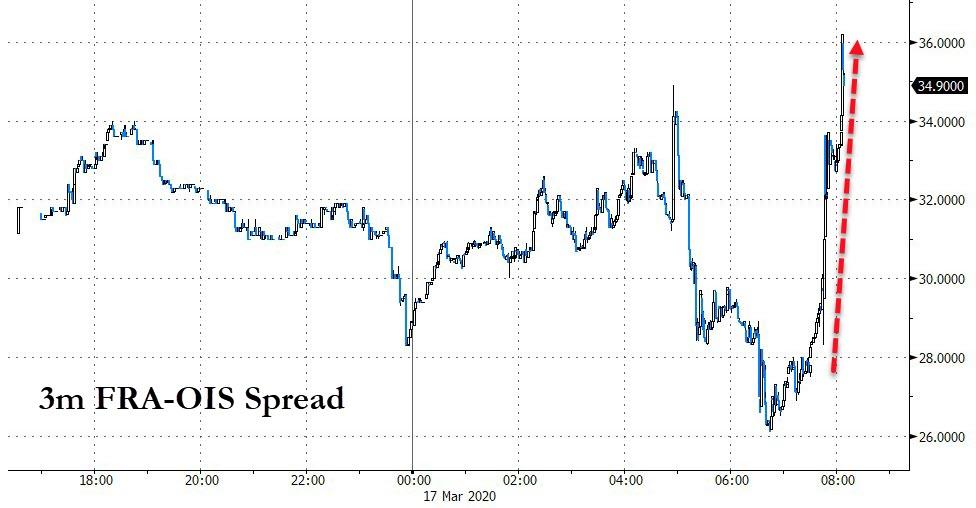

However, the FRA-OIS spread has spiked higher indicating rising stress in the financial system’s liquidity markets…

It would appear The Fed’s “whack-a-mole” may have ‘solved’ one problem (corporate liquidity crisis) but the dollar/liquidity shortage in the global financial system is worsening (which is odd, since if companies did not have access to CPFF they would be forced to drawdown all revolvers and crush the financial system further).

Additionally, as BofA warns:

“This facility does nothing to assist the money funds trying to raise cash and address outflows” implying The Fed will have to unleash another backstop.

“Given the size of our economy relative to where it was 10–15 years ago, it would probably be appropriate for Congress to pass a TARP-style program of $2 trillion,” Minerd said in the note.

Minerd’s expectation is that there is no economic growth in the near term, that we’ve probably already entered a global recession.

Watch Live: White House Holds Daily Coronavirus Task Force Briefing

With US stocks back in the green, White House is holding yet another press conference to discuss the latest progress in the response. Will Trump announce the massive $850 billion stimulus package that has been kicking around all morning?

For the last several months, we have been issuing repeated warnings about the market. While such comments are often mistaken for “being bearish,” we have often stated it is our process of managing “risk” which is most important.

Beginning in mid-January,we began taking profits out of our portfolios and reducing risk. To wit:

“On Friday, we began the orderly process of reducing exposure in our portfolios to take in profits, reduce portfolio risk, and raise cash levels.”

Importantly, we did not “sell everything” and go to cash.

Since then, we took profits and rebalanced risk again in late January and early February as well.

Our clients, their families, their financial and emotional “well being,” rest in our hands. We take that responsibility very seriously, and work closely with our clients to ensure that not only are they financially successful, but they are emotionally stable in the process.

This is, and has been, our biggest argument against “buy and hold,” and “passive investing.” While there are plenty of case studies showing why individuals will eventually get back to even, the vast majority of individuals have a “pain point,” where they will sell.

So, we approach portfolio management from a perspective of “risk management,” but not just in terms of “portfolio risk,” but “emotional risk” as well. By reducing our holdings to raise cash to protect capital, we can reduce the risk of our clients hitting that “threashold” where they potentially make very poor decisions.

In investing, the worst decisions are always made at the moment of the most pain. Either at the bottom of the market or near the peaks.

Investing is not always easy. Our portfolios are designed to have longer-term holding periods, but we also understand that things do not always go as planned.

This is why we have limits, and when things go wrong, we sell.

So, why do I tell you this?

On Friday/Monday, our “limits” were breached, which required us to sell more.

Two Things

Two things have now happened, which signaled us to reduce risk further in portfolios.

“After an emergency 50-basis-point rate cut on March 3, the Federal Reserve doubled down Sunday evening, lowering its benchmark rate by an additional 100 basis points to a range of 0%-0.25% following another emergency meeting.

After ramping up its $60 billion of monthly Treasury bill purchases to include Treasuries of all maturities and offering $1.5 trillion of liquidity to the market via repurchase agreements on March 3, the Fed doubled down Sunday evening with announced purchases of at least $500 billion of Treasuries and at least $200 billion of agency mortgage-backed securities.

In addition, the Fed reduced reserve requirements to zero, encouraged banks to borrow from its discount window at a rate of 0.25%, and, in coordination with five other central banks, lowered the price of U.S. dollar swap arrangements to facilitate dollar liquidity abroad”

We had been anticipating the Federal Reserve to try and rescue the markets, which is why we didn’t sell even more aggressively previously. The lesson investors have been taught repeatedly over the last decade was “Don’t Fight The Fed.”

One of the reasons we reduced our exposure in the prior days was out of concern the Fed’s actions wouldn’t be successful.

On Monday, we found out the answer. The Fed may be fighting a battle it can’t win as markets not only failed to respond to the Fed’s monetary interventions but also broke the “bullish trend line” from the 2009 lows. (While the markets are oversold short-term, the long-term “sell signals” in the bottom panels are just being triggered from fairly high levels. This suggests more difficulty near-term for stocks.

“As you can see in the chart below, this is a massive surge of liquidity, hitting the market at a time the market is testing important long-term trend support.”

It is now, or never, for the markets.

With our portfolios already at very reduced equity levels, the break of this trendline will take our portfolios to our lowest levels of exposure.

What happened today was an event we have been worried about, but didn’t expect to see until after a break of the trendline – “margin calls.” This is why we saw outsized selling in “safe assets” such as REITs, utilities, bonds, and gold.

Cash was the only safe place to hide.

We aren’t anxious to “fight the Fed,” but the markets may have a different view this time.

Use rallies to raise cash, and rebalance portfolio risk accordingly.

We are looking to be heavy buyers of equities when the market forms a bottom, we just aren’t there as of yet.”

On Monday morning, with that important trendline broken, we took some action.

Did we sell everything? No. We still own 10% equity, bonds, and a short S&P 500 hedge.

Did we sell the bottom? Maybe.

We will only know in hindsight for certain, and we are not willing to risk more of our client’s capital currently.

There are too many non-quantifiable risks with a global recession looming, as noted by David Rosenberg:

“The pandemic is a clear ‘black swan’ event. There will be a whole range of knock-on effects. Fully 40 million American workers, or one-third of the private-sector labor force, are directly affected ─ retail, entertainment, events, sports, theme parks, conferences, travel, tourism, restaurants and, of course, energy.

This doesn’t include all the multiplier effects on other industries. It would not surprise me at all if real GDP in Q2 contracts at something close to an 8% annual rate (matching what happened in the fourth quarter of 2008, which was a financial event alone).

The hit to GDP can be expected to be anywhere from $400 billion to $600 billion for the year. But the market was in trouble even before COVID-19 began to spread, with valuations and complacency at cycle highs and equity portfolio managers sitting with record-low cash buffers. Hence the forced selling in other asset classes.

If you haven’t made recession a base-case scenario, you probably should. All four pandemics of the past century coincided with recession. This won’t be any different. It’s tough to generate growth when we’re busy “social distancing.” I am amazed that the latest WSJ poll of economists conducted between March 6-10th showed only 49% seeing a recession coming”.

The importance of his commentary is that from an “investment standpoint,” we can not quantify whether this “economic shock” has been priced into equities as of yet. However, we can do some math based on currently available data:

The chart below is the annual change in nominal GDP, and S&P 500 GAAP earnings.

I am sure you will not be shocked to learn that during “recessions,” corporate “earnings’ tend to fall. Historically, the average drawdown of earnings is about 20%; however, since the 1990’s, those drawdowns have risen to about 30%.

As of March 13th, Standard & Poors has earnings estimates for the first quarter of 2020 at $139.20 / share. This is down just $0.20 from the fourth quarter of 2019 estimates of $139.53.

In other words, Wall Street estimates are still in “fantasy land.”

If our, and Mr. Rosenberg’s, estimates are correct of a 5-8% recessionary drag in the second quarter of 2020, then an average reduction in earnings of 30% is most likely overly optimistic.

However, here is the math:

Current Earnings = 132.90

30% Reduction = $100 (rounding down for easier math)

At various P/E multiples, we can predict where “fair value” for the market is based on historical assumptions:

20x earnings: Historically high but markets have traded at high valuations for the last decade.

18x earnings: Still historically high.

15x earnings: Long-Term Average

13x earnings: Undervalued

10x earnings: Extremely undervalued but aligned with secular bear market bottoms.

You can pick your own level where you think P/E’s will account for the global recession but the chart below prices it into the market.

With the S&P 500 closing yesterday at 2386, this equates to downside risk of:

20x Earnings =-16% (Total decline from peak = – 40%)

NOTE: I am not suggesting the market is about to decline 60-70% from the recent peak. I am simply laying out various multiples based on assumed risk to earnings. However, 15-18x earnings is extremely reasonable and possible.

When Too Little Is Too Much

With our risk limits hit, and in order to protect our clients from both financial and emotional duress, we made the decision that even the reduced risk we were carrying was still too much.

One concern, which weighed heavily into our decision process, was the rising talk of the “closing the markets” entirely for a week or two to allow the panic to pass. We have clients that depend on liquidity from their accounts to sustain their retirement lifestyle. In our view, a closure of the markets would lead to two outcomes which pose a real risk to our clients:

They need access to liquidity, and with markets closed are unable to “sell” and raise cash; and,

When you trap investors in markets, when they do open again, there is a potential “rush” of sellers to get of the market to protect themselves.

That risk, combined with the issue that major moves in markets are happening outside of transaction hours, are outside of our ability to hedge, or control.

This is what we consider to be an unacceptable risk for the time being.

We will likely miss the ultimate “bottom” of the market.

Probably.

But that’s okay, we have done our job of protecting our client’s second most precious asset behind their family, the capital they have to support them.

The good news is that a great “buying” opportunity is coming. Just don’t be in a “rush” to try and buy the bottom.

I can assure you, when we see ultimately see a clear “risk/reward” set up to start taking on equity risk again, we will do so “with both hands.”

And we are sitting on a lot of cash just for that reason.

Online Searches For “Unemployment Benefits” Soar After Virus Crashes Gig-Economy

It was only Monday when we reported New York’s unemployment website crashed as tens of thousands of people out of work tried to file a claim all at once.

Last week, we warned that the gig-economy and service industry was expected to implode as a “coronavirus winter” unfolded across America.

The CDC has just banned gatherings over 50 people, which means stores, clubs, restaurants, bars, and hotels are voluntarily shuttering indefinitely as the economy grinds to a halt.

About 55 million folks, or about 44% of all US workers, aged 18-64, are considered low-wage and low-skilled, have insurmountable debts (with limited savings), including auto, student, and credit card debts, work in the gig-economy and services. These folks are the most vulnerable and are getting axed by employers. Cities across the country that were once vibrant with economic activity have now transformed into ghost towns.

The immediate impact can be seen if you take a drive down the street and look at the empty parking lots of bars and restaurants. With the unemployment rate hovering at a generational low, it’s only a matter of time before gig-economy/service workers hop on government welfare to weather the virus storm, a move that would undoubtedly reverse employment trends.

Search trends across the country for “unemployment benefits” have surged in the last three days, to levels not seen since the global slowdown in 1Q16, as the government is enforcing social distancing to flatten the curve to slowdown infections.

Searches for “unemployment benefits” have jumped the most in New York, New Jersey, Rhode Island, Nevada, and Connecticut. Some of these states have hundreds of confirmed virus cases that prompted local and state officials to shutter businesses.

Other search-related queries that are in breakout patterns are “unemployment benefits for tipped employees;” “enhanced unemployment benefits;” “covid unemployment benefits;” “emergency unemployment compensation 2020,” and “covid unemployment benefits.”

So is Covid-19 about trigger a reversal in the unemployment rate?

Nomura: ‘Quad Witch’ Friday Could Trigger “Un-Sticking” Of Insanely High Volatility

It’s ‘quad witch’ week, which historically has meant a collapse in vol and surge in stocks – no matter what the news. But, this week (and last) has been different, to say the least.

However, as Nomura’s Charlie McElligott explains below, this Friday’s option expiration may stall that chaotic volatility… at least to some extent.

While volatility has been extreme across all asset-classes, in equity markets, McElligott notes we are approaching the “nitty gritty” of tomorrow’s VIX expiry and Friday’s “Serial” Options Expiration, which is set to be the largest notional on record – and all with no CBOE floor operation.

The potential for an “un-sticking” catalyst from this insanely high absolute level of Vol and “Vol of Vol” (VVIX at 208, all-time highs dating-back to ’06) is very real then, because our current assessment of combined SPX / SPY options Gamma shows approx. 36% of $Gamma is set to drop-off after Friday’s expiry (approx. 2- to 3- x’s “normal” drop).

Again recall that much of this “Negative Gamma” position Street-wide is due to the two huge buyers of protection in the March expiry (the large S&P Put Wing from last Fall, and the multi-month VIX “Call Wing” buyer)

This *could* then mean that price-movements simply begin to get a little less crazy after expiry (ranges tighten) and that investors may again begin to initiate “short vol” positions, on account of the multi-month tectonic shift “from extreme LONG to extreme SHORT” Gamma (as discussed here ad nauseum) would seemingly then see Dealers much less “Short Gamma” thereafter, and thus, not as sensitive to changes in the Delta, which recently have been seeing their hedging amplify moves in both directions (in mkt ‘down’ moves having to sell more to remain neutral, or in ‘up’ moves having to buy more)

Other “constructives” for the market include that:

nearly 2600 of 3100 NYSE names are currently in “short sale restricted”;

Street-wide PB’s saw MAJOR covering days in short-books yday;

and market “internals” with lighter selloff volume, better adv / decline ratio and overall breadth improvement which might show that “sell supply” may be waning

Additionally, McElligott notes that systematic funds have “little left to sell” (Risk Parity ‘Equities gross-exposure’ at 0.1%ile since ’10; Target Vol / Vol Control Equities exposure at 0.0th%ile; CTA’s already “-100% Short” signal, although the position gross-exposure can be leveraged-up in-time).

The current selling risks continue to come from the “still long” Asset Manager position in S&P futures (still 76th %ile despite recent reduction) and HF L/S, which are increasingly de-grossing it seems judging by the negative reversal seen in “1Y Price Momentum” factor and broad / massive “short” outperformance over “longs” in the past two sessions.

Lehman Playbook Is Back: Fed Announces Bailout Of Commercial Paper Market – Here’s The Bad News

It was supposed to be announced late on Sunday (recall “Fed Expected To Announce CP Bailout Facility Within Hours Or Risk Money Market Panic“), but instead Powell hoped that the bazooka of QE/ZIRP/FX swaps would be sufficient to ease the funding panic. It wasn’t, and instead, with a 2-day delay, moments ago the Fed announced that, just as we reported earlier, it will establish a Commercial Paper Funding Facility (CPFF) – the same facility that was unveiled during the last financial crisis – “to support the flow of credit to households and businesses.”

Commercial paper markets directly finance a wide range of economic activity, supplying credit and funding for auto loans and mortgages as well as liquidity to meet the operational needs of a range of companies. By ensuring the smooth functioning of this market, particularly in times of strain, the Federal Reserve is providing credit that will support families, businesses, and jobs across the economy. The CPFF will provide a liquidity backstop to U.S. issuers of commercial paper through a special purpose vehicle (SPV) that will purchase unsecured and asset-backed commercial paper rated A1/P1 (as of March 17, 2020) directly from eligible companies.

And since this is effectively a partial Fed bailout of corporate America, certainly its overnight funding needs, the Fed referred to authority granted to it under Section 13(3) of the Federal Reserve Act, with approval of the Treasury Secretary, as now that the Lehman playbook is in play, the bailout of Corporate America is suddenly very political.

The Fed had some more observations on the lock up in the CP market, which as we explained on Sunday, prompted a gradual bank run within US money markets:

The commercial paper market has been under considerable strain in recent days as businesses and households face greater uncertainty in light of the coronavirus outbreak. By eliminating much of the risk that eligible issuers will not be able to repay investors by rolling over their maturing commercial paper obligations, this facility should encourage investors to once again engage in term lending in the commercial paper market. An improved commercial paper market will enhance the ability of businesses to maintain employment and investment as the nation deals with the coronavirus outbreak.

As part of the CP facility, the Treasury will provide $10 billion of credit protection to the Federal Reserve in connection with the CPFF from the Treasury’s Exchange Stabilization Fund (ESF). The Federal Reserve will then provide financing to the SPV under the CPFF. Its loans will be secured by all of the assets of the SPV.

A brief description of the program is attached (see link). More detailed program terms and conditions and an operational calendar will be subsequently published.

Commercial Paper Funding Facility 2020: Program Terms and Conditions

Effective March 17, 2020

Facility

The CPFF2020 will be structured as a credit facility to a special purpose vehicle (SPV) authorized under section 13(3) of the Federal Reserve Act. The SPV will serve as a funding backstop to facilitate the issuance of term commercial paper by eligible issuers.

The Federal Reserve Bank of New York will commit to lend to the SPV on a recourse basis. The New York Fed will be secured by all the assets of the SPV. The U.S. Treasury Department—using the Exchange Stabilization Fund (ESF)–will provide $10 billion of credit protection to the FRBNY in connection with the CPFF.

Assets of the SPV

The SPV will purchase from eligible issuers three-month U.S. dollar-denominated commercial paper through the New York Fed’s primary dealers. Eligible issuers are U.S. issuers of commercial paper, including U.S. issuers with a foreign parent company.

The SPV will only purchase U.S. dollar-denominated commercial paper (including asset-backed commercial paper (ABCP)) that is rated at least A-1/P-1/F-1 by a major nationally recognized statistical rating organization (NRSRO) and, if rated by multiple major NRSROs, is rated at least A-1/P-1/F-1 by two or more major NRSROs, in each case subject to review by the Federal Reserve. 1

Limits per issuer

The maximum amount of a single issuer’s commercial paper the SPV may own at any time will be the greatest amount of U.S. dollar-denominated commercial paper the issuer had outstanding on any day between March 16, 2019 and March 16, 2020. The SPV will not purchase additional commercial paper from an issuer whose total commercial paper outstanding to all investors (including the SPV) equals or exceeds the issuer’s limit.

Pricing

Pricing will be based on the then-current 3-month overnight index swap (OIS) rate plus 200 basis points. At the time of its registration to use the CPFF, each issuer must pay a facility fee equal to 10 basis points of the maximum amount of its commercial paper the SPV may own.

Termination date

The SPV will cease purchasing commercial paper on March 17, 2021, unless the Board extends the facility. The New York Fed will continue to fund the SPV after such date until the SPV’s underlying assets mature.

Now the bad news: commenting on the facility, TD Securities rates strategist Gennadiy Goldberg said that the fact that the spread on the Federal Reserve’s resurrected commercial paper funding facility at 3-month OIS+200bp is larger than it was in 2008, when it was 3-month OIS+100bp, which “may limit the efficacy of the facility.”

Why? Because according to Goldberg, “the Fed is probably hoping banks go to the discount window while non-financial corporates go to this facility.”

The seemingly punitive rate may also “limit how much relief the facility provides to FRA-OIS. This is the exact opposite of the approach the have taken via the repo facility, where repo amounts on offer are effectively unlimited,” and begs the question why does the Fed keep shooting itself in the foot when on one hand it appears to be offering unlimited liquidity at least until one reads the fine print.

Now the really bad news: by launching the Lehman playbook, the Fed is telegraphing that the US is now facing systemic risk crisis which also includes the banks and corporations, something which was missing until now. Which is why after a brief kneejerk reaction higher, markets may fade it all and crash to new lows, especially if the market demands to see what if any other ammunition the Fed has left, with expectations that sooner or later the Fed will do as Yellen hinted three months ago when she said that the Fed will eventually have to buy stocks.

Fed Again Announces Extra $500BN Repo To Stabilize Funding Markets

Earlier this morning, when discussing the latest Fed repo injections, which at $189BN between overnight and term repos, seemed insufficient to ease the stress in the repo market where GC repo jumped by 40bps to 60bps this morning…

we said that “with no other repos scheduled for today, and the next $500BN 84-day facility not due until Friday, banks may soon find themselves in another funding panic, and the Fed may respond as it did yesterday, with an ad hoc $500BN facility later in the day if funding conditions refuse to ease.”

Alas, funding conditions have indeed refused to ease, with the BBDXY surging to new session highs perhaps awaiting the Fed to validate earlier reports that a Fed Commercial Paper facility is imminent, and moments ago – just as we expected – the Fed, which is now literally flying blind and making up liquidity injections on the fly, the New York Fed announced that it would conduct an additional overnight repo operation for same-day settlement today from 1:30 PM ET to 1:45 PM ET. And, as yesterday’s ad hoc operation, this repo operation will be conducted for up to an aggregate offered amount of $500 billion with a minimum bid rate of 0.10 percent.

And, as yesterday, the Fed explained that this action “is taken to ensure that the supply of reserves remains ample and to support the smooth functioning of short-term U.S. dollar funding markets.”

The problem for the Fed is that these actions have done virtually nothing to facilitate the “smooth functioning of short-term U.S. dollar funding markets”, and the longer the Fed delays in unveiling just what can fix these markets, the greater the dollar shortage will be.

“Well, it has to happen. Because if it doesn’t happen, we hit the wall next week. We’re already in breach.”

Happy St Patricks day. Extra points for identifying the moment in Irish history in this morning’s quote…

Meanwhile… back in Today

Yesterday was another nasty day – uncertainty, panic and fear fuelling the worst fears for the market. The scale of capitulation was massive – Treasuries heading for zero percent, stocks biggest down day for 33 years, and gold sliding because investors literally have nothing else to sell to meet margin calls. If you aren’t out yet, you are stuck. Forget liquidity – it’s almost impossible to exit even liquid index ETFs.

Stop. Breathe deep. And relax.

Today looks like it might be an up day. The market is swinging madly because of uncertainty and we just don’t knows. After yesterday’s Fed all-in-rates to zero and essentially unlimited QE, Lagarde at the ECB effectively apologising for throwing Italy under the bus, and the G7 giving us a Mario Draghi “do whatever it takes” moment to address the virus – its entirely possible we’re headed higher today on hopes of a relief rally. In other words investors might find a plank of wood to cling to in this raging market maelstrom.

Hope is never a good strategy. Don’t be fooled. It will get worse before it gets better.

At this stage in the Coronavirus No-See-Em shocker, It’s all about uncertainty. We just don’t know how critical the virus will go, the scale of the dislocation to come, and how deep the economic damage will go.

What If We Knew?

What if we had a much clearer idea of what and when it’s going to happen? There is the brainpower, analytical and modelling experience out there in the marketplace to clearly model the multiple transmission, infection, and treatment scenarios plus the economic implications in terms of jobs, production, supply and demand, to give us a very clear idea of how this goes.

Here in the Shard Offices (actually, today I’m a home), we’ve been working out our own scenarios of when to put our buying boots on. We reckon the buy signal will be a slowing infection/transmission rate. That is when the market will start to anticipate recovery and we’ll see prices start to strengthen.

What if we knew, with a high degree of certainty when moment is going to come? What if we had a high degree of confidence in the implications for the economy?

I’ve now spent some time looking at a superb virus model with clear potential to crack the numbers, handle multiple scenarios, and can process all that data to provide some very clear signals. IT provides answers to the critical questions. I’m looking to introduce institutions to the team behind the model. Its operational now.

If you want to know more email me, or call me direct.

Recovery?

A number of firms have clearly been doing their own modelling of the crisis. Yesterday the Goldman Sachs crisis call suggested “Stock Markets should fully recover in the 2nd half of the year”.This morning Credit Suisse is on the wires saying something similar and positing a strong V-Shaped recovery, with markets swiftly undoing the damage this year.

What TF are these guys smoking? I want some…

It’s not going to be that simple. More than “psycological” damage has been done. It’s not about volatile market sentiment. This has been an economic shock and a correction.

Let’s be brutally honest about what’s happened in recent weeks (and I shall be posting a note on Virus Timeline later today):

Markets hit all-time record highs just a few weeks ago. Stocks hit record levels. Corporate bond spreads had never been tighter. Most of the globes sovereign debt was trading at sub-zero or barely positive yields. The bull market was unstoppable – no matter how bad the news about virus, trade wars, and rising debt seemed.

Everything was perfectly priced – mispriced.

The market’s final euphoric top wasn’t driven by economic reality, phenomenal growth expectations, accelerating corporate profitability or rising consumer incomes and discretionary spending. Nope. The only real driver was the continuing expectation/belief Central Banking Authorities would continue to juice the market and distort prices the way they’ve been doing since they stumbled on monetary experimentation, QE and NIRP since the last crisis.

Now we know they were not a cure. They were hits of monetary addiction.

Just how dangerous we will shortly find out – just how damaging the unintended consequences the last eight years of market distortion have been. I suspect unravelling the damage will be long-term and extremely destabilising.

For instance; the obvious one is corporate debt. $14 trillion of new corporate debt in the last 7 years needs to be repaid. Was it spent on building new productive assets? Nope. Most of it was spent on stock buybacks which created wealth for owners, but has simply leveraged companies to the hilt. There is enormous balance sheet damage to be corrected – and that is not stock positive in the next few months.

The wealth effect of stock buybacks juicing stock markets has fuelled property, art, and luxury businesses around the globe. Remove the multiplier and these wealth effect markets all look vulnerable.

And what about the consumers that have already lost jobs, spent their savings and are scrabbling to stay afloat today? I’m reading estimates saying 10 million US catering and entertainment jobs will be shuttered, furloughed or gone in next few weeks. They aren’t going to start consuming any time soon to drive recovery.

The consensus on Government debt is that nations can simply make QE debt effectively disappear. Maybe… but there will be a credibility gap at some point. The big one will be Yoorp – where the implausibility of agreeing de facto debt mutualisation (ie: persuading German car workers to fund French farmers pensions), ain’t going to happen unless its forced through in crisis.

They are so many reasons the market is not simply going to bounce back after the virus crisis has past. Unravelling the supply and demand side damage to the economy is not going to happen overnight. Mass tourism is not going to switch back on in a heart-beat. There will be millions of consumers who have seen their incomes collapse on the back of lay-offs. They will need time and opportunity to rebuild savings. Fear is going to be the primary driver.

In the long-run the global economy will recover – but it won’t be overnight in a V shape undoing of what’s going on now in terms of contraction. In the short-medium terms we face at least months, if not years of rebuild. Stock markets are not going back to February’s levels anytime soon. THat doesn’t mean we won’t new highs as a new bull market takes hold – but it could be years.

Asset Price recovery will be more nuanced. There will certainly be opportunities.

This morning I’m thinking of buying aviation bonds on the basis: “if all airlines will be bankrupt by May”, then its highly likely we will see governments step into support them. Which means they will keep paying the leases on their aircraft, and we’ll see medium term recovery in tourism and business travel – the clock is not going to roll back to the 1930s!

Is it time to buy Asian banks on the expectation Asia is going to recover faster than Europe? Or what about wide-spread Italian and Spain bonds on the basis the ECB will bail them out? What about European banks on the basis the ECB, and nations, can’t afford national champions (ha! Are there such things in Yoorp) going to the wall?

What about corporate bonds on the basis it’s a buyer’s market and easy to buy bonds…

However, the really, really interesting thing is the opportunity for Governments to do the right thing.

Spend Money on Health

This crisis is not really about economics or market levels. It’s all about the ability of Health Services to cope with an unexpected shock and catastrophe levels of demand. Yet, anyone who uses the NHS regularly – as my dicky ticker requires – will know Health Services are financially stretched, in permanent semi-crisis, chaotic and understaffed. They are full of dedicated doctors and nurses, but inefficient managed by inflated bureaucracies.

In 2008 the UK government bailed out failing banks to the tune of some £500 bln. In 2019 we spent some £125 bln on the NHS. We are now at a stage where credible governments can borrow/create (via a QE trick) unlimited sums at essentially zero interest cost. We are now used to Boris describing this crisis in terms of a war we can win. We can – imagine using this opportunity to rebuild and refocus the NHS into something modern, ready and prepared for this happening again, paying nurses properly, introducing proper AI and management. The opportunities are legion.

Same thing in the US where the crisis will likely bite deepest. The US wins wars because it can outspend any enemy. In 2008 it spent $700 bln bailing the banks – and got the money back. Imagine if the US was to spend similar amounts on a proper free health service? That might truly make America Great Again.

Job Openings Soar Most In Three Years Just As US Economy Grinds To A Halt

Last month, the market was shocked when despite strong payrolls numbers, the closely-watched JOLTS report – which as a reminder was Janet Yellen’s favorite labor market indicator – showed that in the two months ended Dec 2019, the number of job openings in the US economy tumbled by the most since the crisis, an early warning indicator that something was badly broken in the job market and was likely not captured by the BLS’s Establishment Survey.

Well, moments ago the BLS reported its latest JOLTs report and so often happens, it was a mean reversion kitchen sink, with job openings soaring by 411K, the most in three years…

… and pushing the total back up to 7 million.

Commenting on the data, the BLS said that the number of job openings increased for total private (+370,000) and edged up for government (+40,000). Job openings increased in finance and insurance (+65,000), federal government (+38,000), and mining and logging (+8,000).

The irony of course is that job openings are surging… and nobody cares for two reasons:

First, the number is two months delayed (this was January data)

Second, we now know that tens of thousands are being mass laid off at this moment as the US economy shuts down due to the coronavirus, which means that job openings are now completely irrelevant and what matters will be weekly layoffs announcement which soon may be in the millions.

It also means that after 23 months in which there were more job openings that unemployed workers, this series is about to reverse with a vengeance, as posted openings crater and as hundreds of thousands of Americans suddenly find themselves without a job.

Not-So-Prime: Virus Sparks Delivery Delays, Shortages At Amazon

Amazon has informed customers in a blog post that it has sold out of some household items, and prime deliveries could be disrupted during the Covid-19 outbreak.

The online retailer updated its blog post on Saturday and told customers that “we are currently out of stock on some popular brands and items, especially in household staples categories.”

It said that certain items could experience longer than normal delivery times.

“We are working around the clock with our selling partners to ensure availability on all of our products, and bring on additional capacity to deliver all of your orders,” the post added.

In the last two months, Prime members have noticed notifications saying “inventory and delivery may be temporarily unavailable due to increased demand” for certain products, such as 3M N-95 virus masks. More recently, the shortage of products has significantly expanded to bottled water, hand sanitizer, toilet paper, and vitamins. Amazon noted that it has worked extremely hard to crack down on price gouging, especially seen with third-party sellers selling masks and hand sanitizers for many folds over the suggested retail price.

Social distancing has led to the max exodus of shoppers at brick and mortar stores, who have now gravitated to online shopping to prevent spreading.

“As COVID-19 has spread, we’ve recently seen an increase in people shopping online,” Amazon wrote. “In the short term, this is having an impact on how we serve our customers.”

Amazon is gearing up for increased online activity as the virus crisis is expected to worsen in the weeks ahead. A Wall Street Journal report on Monday said the online retailer is expected to add 100,000 workers to cope with the surge in new demand.

The virus crisis will forever change how consumers shop. Social distancing will ensure more online shopping. But in the meantime, Amazon has been caught off guard by the rapid surge and will result in shortages of products and shipping delays.