Dr. Fauci: I Don’t Think We Should Shake Hands “Ever Again”

Dr. Anthony Fauci, the director of the National Institute of Allergy and Infectious Diseases (NIAID) was optimistic yesterday (and the media crowed about his sudden about-face) as he said he hopes to see a “light at the end of the tunnel” by the end of April in the fight against COVID-19.

However, what went under-reported was a comment he made on a Wall Street Journal podcast. Specifcally, the best-known member of the White House coronavirus task force, on Wednesday suggested that Americans should never shake hands again.

“When you gradually come back, you don’t jump into it with both feet. You say, what are the things you could still do and still approach normal? One of them is absolute compulsive hand-washing. The other is you don’t ever shake anybody’s hands.“

“I don’t think we should ever shake hands ever again, to be honest with you. Not only would it be good to prevent coronavirus disease; it probably would decrease instances of influenza dramatically in this country,” the doctor added.

So, there is “light” at the end of the tunnel that we will return to normal but that ‘new normal’ will mean no handshakes, hugs, or venturing outside without full PPE?

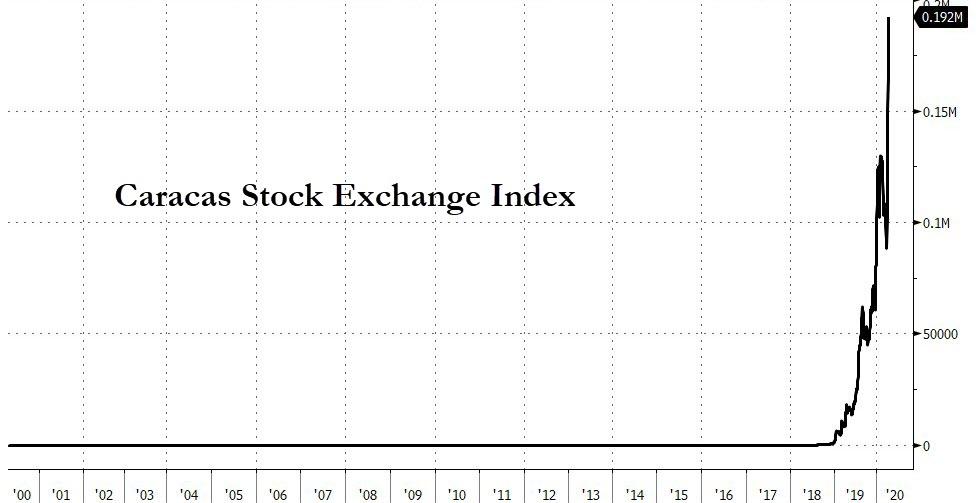

Today, stock market investors are hoping desperately for Weimar-style hyperinflation to boost equities prices to dizzying heights in what some call a “crack-up boom”. In terms of money creation, we are not there yet, but such levels of fiat printing could happen within the next year. Unfortunately for investors, this “boom” in stocks may not happen again. In fact, it already happened over the course of the past several years, and now the party is over.

In the past few months, the U.S. dollar has entered a massive liquidity crisis, and despite all expectations, the Fed’s attempts to compensate with stimulus measures have done little to boost markets back to their previous glory.

In Weimar Germany, stocks did get an epic rally, until it all came crashing down in 1924 and then again in 1927. The notion of the endless fiat-driven bull market is a lie perpetuated by central bankers and their cheerleaders.

[ZH: And then there’s the more recent example of Venezuela… just think how well their economy must be doing for stocks to be soaring so high…]

As I warned in pastarticles, when the Fed finally decided to step in to “stall the crash”, it was after it was far too late. The Fed has no intention of stopping the crash, they WANT a crash; they created all the conditions necessary for the collapse of the Everything Bubble to happen. Their goal now is only to make it appear as though they “did everything they could” to save the economy while staging the collapse of the final bubble: the U.S. dollar and its global reserve currency status.

The problem for markets is not just the coronavirus pandemic, but I’ll get to that. The real issue is that the primary support pillar for equities has disappeared; namely corporate stock buybacks. The new bailouts might actually create a ban on the practice in the future, which guarantees declining market values unless the central banks step in to purchase stocks directly. Even then, asset values will probably still fall over time, but at a slower pace.

Keep in mind that the trillions of dollars in loans that have been feeding corporate share prices through buybacks over the past few years just went up in smoke due to the downturn. Companies have been using central bank repo loans to juice stocks beyond all reason. In the past three years, the valuations have been ridiculous compared to the dismal earnings of the same businesses. All that cash was wasted, and these corporations remain in debt up to their eyeballs.

But perhaps they don’t care anymore. I’m sure many CEOs understand that while their companies might flounder in the midst of a pandemic crisis and economic crash, they as individuals will be well taken care of. No banker, no CEO, no high-level politician is going to be punished for the financial calamity that is on our doorstep. Just as in the 2008 crash, they will all be given a seat at the table and their sabotage of the economy will be ignored. The only consequences they might face will be if the public becomes enraged enough that the torches and pitchforks are finally brought out.

For now, the populace is absorbed in the drama of the viral outbreak, and I don’t think economic concerns have quite struck the majority yet. They will soon, though, as people begin to realize this event is going to last a lot longer than they have been told. Even if the infection numbers diminish over the course of this month, as many assume, the greater threat at hand is that governments will assert that this is because the “lockdowns work”. If the lockdowns “work”, then the lockdowns will continue.

Using the wave model of conditioning, governments will allow the public brief moments of breathing room in which lockdowns are lifted for a short time; maybe a month or less, followed by a resurgence of infections and then hard lockdowns return for another couple of months. This process is not going away anytime soon. Understand that there are over seven billion people on the planet, and we have a long way to go before the majority of the population has either recovered from the virus or died from it.

This means endless cycles of suppressed business activity, supply chain breakdowns, business closures and job losses. The central banks and governments have created an environment in which the ONLY source of relief is monetary policy and Universal Basic Income (UBI). Ultimately, nationalization of most “essential businesses” will have to occur under this model. Eventually the Defense Production Act will be fully implemented. This means that dollar devaluation will accelerate beyond anything we saw during the credit crisis ten years ago, as governments bond completely with corporations to form a megalith of socialist production control.

To summarize: The Fed will have to finance corporations directly through stock purchases, or the government will have to take control of them outright, and the Fed will have to finance government to an unprecedented level of debt creation.

Foreign central banks are dumping U.S. Treasuries on a large scale right now, partially because the liquidity crisis has forced them to sell assets to accumulate dollars, but also because with the Fed moving into what looks to be an infinite stimulus model, U.S. Treasuries are no longer a viable means to protect wealth or make a profit. This means the only buyer left to fund the U.S. government will be the central bank.

In 2008, this process took place, but never on a scale that is needed today. With so many small businesses closing shop, corporations drowning in historic levels of debt, and the average consumer losing their jobs and their income, the establishment is about to become the sugar daddy to everyone that is not self-sufficient. The level of dollar creation that will be needed just to keep the system running for the next six months will be staggering; I am talking tens of trillions of dollars.

Will the dollar as we know it survive this? No, not a chance. The dollar will continue to lose value, causing painful price inflation, and eventually its global reserve status will be destroyed. But the elites already have all this figured out. Indeed, they actually benefit from it.

First, small businesses will be crushed, and all assets absorbed into the banks and major corporations. Small business loans under the new government bailout will in most cases only cover payroll for employees for a short time during the lockdowns and will not necessarily ensure business survival. Just as in the Great Depression, when thousands of small private banks defaulted and were devoured by JP Morgan, trade and production during Great Depression II will be gobbled up and centralized into very few hands. Get ready for the big box stores like Walmart and Costco to become the only options in your area.

Second, the crash will allow the establishment to test out their “Modern Monetary Theory” model and entice the public into accepting the idea of monthly UBI. This money will not be enough to keep many people afloat for very long without reversion to third world standards, but if the economic situation becomes desperate enough, large portions of the public might see it as “better than the alternative”, which would be starvation on the level of a refugee camp.

Third, the collapse of the dollar along with the pandemic opens the door to implementation of a cashless society, a goal long desired by the elites. Even now, there are bills being presented in the Senate which call for a digital dollar and digital wallet policy to be instituted in the U.S., the Fed is considering the prospect on their own, and other central banks around the world are increasing their pace of cash removal in the name of “preventing the spread of the virus”.

With the amount of fiat creation that is necessary to support almost the entirety of the U.S. economy for the next several months, I suspect the dollar’s global reserve status will come under question before the end of the year. In the meantime, the establishment will attempt to force the idea of a digital currency system into daily public discussion.

With a dollar collapse, the populace will have little choice but to either bow down to the new digital system or go rogue and start building their own systems using their own production, barter, local scrip, and gold and silver. This is the world we are heading into, make no mistake. Be ready for it.

* * *

With global tensions spiking, thousands of Americans are moving their IRA or 401(k) into an IRA backed by physical gold. Now, thanks to a little-known IRS Tax Law, you can too. Learn how with a free info kit on gold from Birch Gold Group. It reveals how physical precious metals can protect your savings, and how to open a Gold IRA. Click here to get your free Info Kit on Gold.

Media On ‘Jihad’ Against Anti-Malaria COVID-19 Treatment Since Trump Endorsed Use: AG Barr

Ever since President Trump endorsed the use of an anti-malaria drug to treat COVID-19 patients, the media has been on a “jihad” against it, according to Attorney General William Barr.

Touted as a “game changer” by President Trump, hydroxychloroquine – a treatment whose epidemiological ancestor is derived from the bark of a South American tree and used for centuries by indigenous Peruvians to treat fever – has been used by doctors around the world to treat coronavirus patients with stunning efficacy reported when combined with zinc and azithromycin (Z-Pac).

During a Wednesday evening interview with Fox News‘s Laura Ingraham, Barr says the media was “fair and balanced” about the drug’s efficacy until Trump “said something positive about it,” after which “the media has been on a jihad to discredit the drug.“

“It’s quite strange,” he added. “The stridency of the partisan attacks on him has gotten higher and higher, and it’s gotten disappointing to see.”

Barr says he’s disappointed about partisanship during the pandemic because the President has acted statesmanlike and worked with all the governors while dealing with gotcha questions from the media. He goes on to accuse the media of leading a jihad against Hydroxychloroquine pic.twitter.com/fW2NLDOzB7

The attorney general also praised Trump’s handling of the pandemic, labeling his efforts early on as “statesmanlike,” while accusing the White House press corps of asking “snarky gotcha questions.”

The president began touting the drug last month after a flawed study conducted in France showed promising results. His first reference to the drug came a day after the results of the study were aired on Fox News.

At a White House coronavirus task force briefing last weekend, Trump announced the administration had purchased “a tremendous amount” of hydroxychloroquine, which will be distributed to the states after the Food and Drug Administration issued an emergency approval for its use among coronavirus patients.

Late last month, the Kingom of Bahrain reported that the use of hydroxychloroquine had made a “profound” impact on patient outcomes, according to the Bahrain News Agency – echoing reported results in China, South Korea and Belgium.

In Brussels, meanwhile, similar early success has been reported and the country has begun longer-term clinical trials on its efficacy to treat COVID-19 patients.

The Arizona House Republicans approved a bill to ban transgender women, those born as biological males, from competing in women’s sports.

Rep. Nancy Barto, a Phoenix Republican, is the sponsor of the Save Women’s Sports Act which prevents transgender women from participating in women’s sports because of the inherent biology of “chromosomal” and “hormonal” differences between males and females.

Barto told ABC News that, “…[the] bill is about fairness. That’s it. What is fair on the field, the court, the track, and in the pool.”

“Recent research actually verifies that even with cross-sex chromosomes, men have an unequivocal advantage. They’ve got stronger bones, they’ve got greater lung capacity,” she told Fox News.

The bill requires that any student disputing their assigned sex at birth be required to present a physician’s statement identifying the student’s sex after a DNA test.

House Democrats have dubbed the bill the “show me your genitals” criticizing since-removed portions of the bill that requires a physical exam.

Rep. Isela Blanc called the bill “completely inappropriate” adding that “[the bill] is completely wrong, inhumane, unkind, inappropriate, and mean-spirited.” But the sponsor of the bill, Republican Rep. Nancy Barto, told Campus Reform, “This bill isn’t anti-anyone – nor does it ban anyone from playing competitive sports. It simply clarifies which team individuals may participate on so women can continue to compete on a level playing field in their own sports. Ignoring this issue violates both the intended purpose and the spirit of Title IX.”

The bill passed along party lines by a vote of 31-29.

After the bill passed, Rep. Daniel Hernandez took to Twitter, saying that the bill is not “pro-women” or “pro-business” and that it was ultimately “a sad day for Arizona.”

Today is sad day for Arizona. After almost 6 hours of debate an anti-trans bill was passed in the house. 2706 is not pro woman and it is bad for AZ and bad for business. Poorly written and rammed through despite 100s of businesses opposed. #TransGirlsAreGirls

— Representative Daniel Hernandez Jr (@danielforaz) March 4, 2020

In a statement to Campus Reform, the Alliance Defending Freedom’s Senior Counsel Matt Sharp noted that “science and common sense tell us that there are real physiological differences between boys and girls that affect athletic performance…” Sharp added, “women fought long and hard to earn equal athletic opportunities, and these bills safeguard those victories for another generation.”

ADF is currently involved in a legal battle in Connecticut where it is challenging a school’s transgender policy.

In a statement to Campus Reform, Arizona Federation of College Republicans Communications Director Joseph Pitts also reacted to the bill.

“This is an issue of biology, and a vast majority of Americans are in agreement with this,” Pitts said.

However, in response to the now-deleted provisions of the bill that required physical exams to determine biological sex, Pitts added, “While we do see worrying invasions of privacy in the bill—such as the provision requiring genital checks (which is medieval and not a good policy whatsoever)—the general intent of the bill is not controversial.”

Arizona Gov. Doug Ducey has not indicated whether he would sign the bill if it reaches his desk.

Arizona State University College Democrats, ASU transgender advocacy group TransFam, and Blanc did not respond to Campus Reform’s request for comment in time for publication.

Insanity: As The US Enters A Depression, Stocks Are Now The Most Overvalued Ever

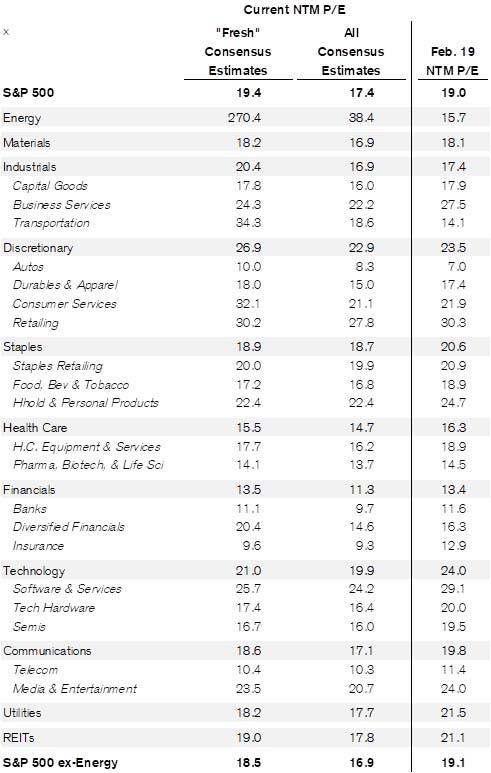

Two days ago, when a platoon of clueless CNBC hacks said that stocks were extremely undervalued, and must be bought (on their fundamentals, not because the Fed was about to nationalize the entire bond market and is set to start buying equity ETFs in the next crash), we showed just how “undervalued” the market was.

That’s when Credit Suisse chief equity strategist Jonathan Golub – usually one of the most bullish Wall Streeters – published a chart showing that any “temporary” cheapness in stocks hit in late March was long gone for the simple reason that forward earnings have plunged. As a result, as of noon on March 7, when the S&P 500 had risen as much as 22% from March 23 lows, forward stock multiples had surged right back 19.0x.

Why is this notable? Because as Golub wrote, “this is the same level the S&P500 held on Feb 19, the all-time high.”

In other words, at the start of the week stocks were valued the same as they were at the February all time highs.

Fast forward to today when the Fed’s latest “shock and awe” nuclear bomb announcement which included purchases of junk bond ETFs and muni debt – and by implication terminally disonnects risk prices from any fundamental values and instead only the size of the Fed’s balance sheet matters – sent the S&P as high as 2,818. And, in doing so, the forward PE multiple on the S&P has risen from the record 19.0x reached in February to a new all time high of 19.4x.

In other words, the market has never been more overvalued than it is right now.

That’s not all.

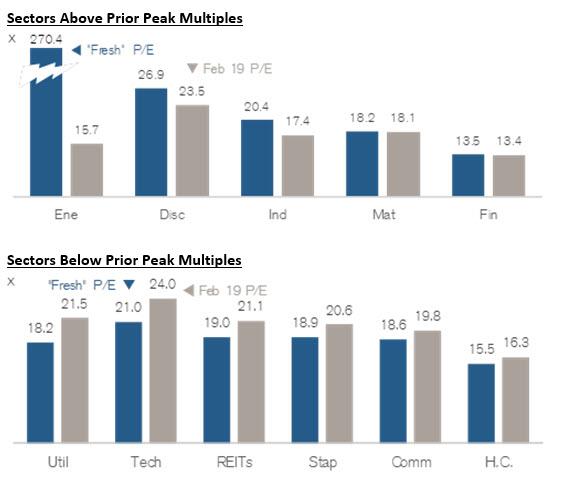

As Golub writes today, “we’ve expanded this analysis to cover sectors and sub-groups. Multiples for cyclical groups (Energy, Materials, Industrials, Discretionary, Financials) have surpassed prior P/Es. Valuations for defensive sectors (Staples, Utilities, Health Care, REITs) as well as Tech and Communications remain below Feb 19 levels.”

And a full sector breakdown.

So congratulations Jerome Powell: you have succeeded in the impossible – with the US economy entering a depression, with US GDP set to plunge as much as 50%, with US unemployment already 15% and set to hit 20% or more, the Fed chair has single-handedly disconnected stocks from all fundamental anchors and made the S&P the most overvalued in history as its forward P/E hits the highest number ever recorded.

The Trump administration has approved roughly $100 billion of the $350 billion allocated for emergency loans to small businesses devastated by the coronavirus outbreak, Treasury Secretary Steven Mnuchin told lawmakers on Wednesday.

But the figure has done little to ease the rising fears of smaller businesses still struggling to access the funds — and growing ever-more concerned that the program is tilted in favor of larger enterprises with existing relationships with banks.

The concern from small businesses is simple: they fear the money will run out before they can access it.

“A lot of money [is] first-come, first-serve, and many unbanked people who are underbanked or unserved … don’t have banking relationships, sophisticated in a way that others do,” House Speaker Nancy Pelosi (D-Calif.) said Wednesday in an interview with NPR.

Money Might Run Out

Let’s tap into that idea that money might run out with an investigation of the Small Business Loan Rules.

The program offers loans of up to $10 million to cover eight weeks of payroll plus some additional expenses, like rent and utilities.

The loan can effectively turn into a grant. Most, and in some cases all, of the loan will be forgiven if a company uses the money to retain workers or hire back positions it had to cut. The S.B.A. has waived many of its usual requirements for these loans and will not require collateral for them.

Businesses can have their loans forgiven in full if they maintain their full-time equivalent head count (based on a 40-hour workweek) and wages for eight weeks after the loan is disbursed, the Treasury Department said. The agency said that “not more than 25 percent” of the forgiven amount may be used for nonpayroll costs, like rent.

Companies can borrow up to two months of their average monthly payroll costs for the past year, plus an additional 25 percent, up to $10 million. “Payroll costs” include salary, wages, tips, commissions, paid leave benefits, employer-paid health insurance premiums, and state and local payroll taxes.

The CARES Act text says that you can claim your “wage, commission, income, net earnings from self-employment or similar compensation,” up to $100,000 a year.

You’ll have two years to pay off the balance, at a 1 percent interest rate. No payments are due for the first six months after you get the loan.

Hooray I am Qualified!

Check this out.

Self-employed people are eligible for benefits.

Benefits will be based on previous income, using a formula from the disaster unemployment assistance program.

Self-employed workers are also eligible for the additional $600 weekly benefit provided by the federal government as part of the CARES Act.

Moreover, one does not even have to request an amount.

The S.B.A. will determine how much someone like me can borrow using a formula intended to approximate six months of my operating expenses.

This is despite the fact that I have not lost a penny in earnings.

Let that sink in.

I cannot find any requirement anywhere that prevents someone like me from making an outright bundle.

Hooray! Six Months Double Income

Nowhere does the application (that I am aware of) ask me if I have lost any income.

Even if it did, all I would have to do is stop paying myself salary, let the profits accumulate, and use the loan to cover my previous income.

Since the loan is used to pay salary, (my own), it would be forgiven. Heck, I could even hire my wife and kids except for the fact I have no kids.

On top of that, and despite the fact I have not lost a dime, I will receive an automatic check because the government is sending out blanket $1,000 checks to everyone.

Moral Hazard?

You bet. I will not take advantage but under the rules I easily could.

Some will.

From the Bank Perspective

Assume the banks are getting flooded with loan requests.

Who do they want to lend to?

Someone who does not need the money at all and is no credit risk OR

Someone who might go out of business

Any reasonable credit scoring algorithm would direct these loans to the safest place, category number one.

Lesson of the Day

When government fires money out of cannons, it generally does not get into the hands that government intended.

The more cynical will believe it actually does get to the intended people, just not the alleged beneficiaries.

Guggenheim’s Scott Minerd summed up exactly what The Fed has done with its actions today:

“The Fed has made it clear that it will not tolerate prudent and responsible investing.”

The Fed just went full Leeroy Jenkins…

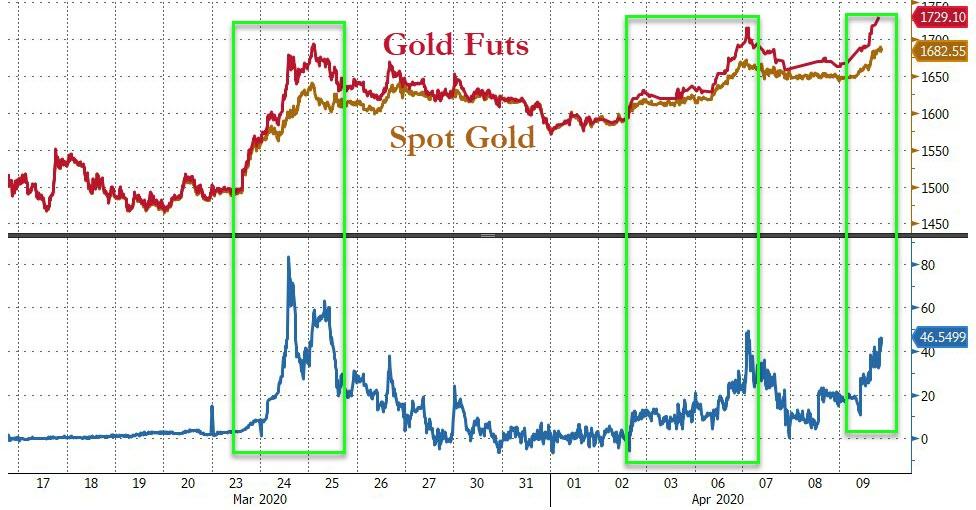

And gold is starting to signal fears over fiat…

Something is brewing…

And the spot-futures markets are decoupling as physical (geographic) shortages rear their ugly heads again…

Source: Bloomberg

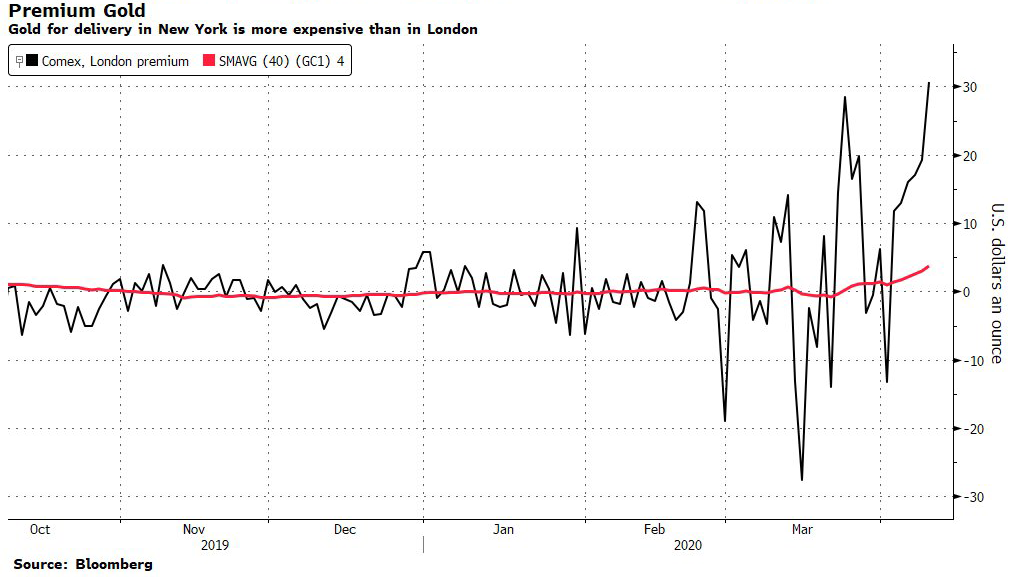

As Bloomberg notes, the internal mechanics of the gold market are again showing strains under this rally. Gold futures are trading more than $50 above the spot price in London.

Until recently, that was unheard of in a metal that’s so utterly fungible, so easy to transport and where trade channels are so deeply established. But with planes grounded and refining capacity severely restricted, don’t expect the arbitrage to break down immediately.

Bloomberg’s Garfield Reynolds was quick to note, the global business environment is being transformed – we are all socialists now.

This is about more than just the failure of earnings estimates to keep up with the virus impact – investors need to disregard projections that an end to the crisis will restore the pre-outbreak status quo.

Decades of pushing government out of business are being reversed in mere weeks, with policy makers telling companies where, how and if they should operate – whether they can pay dividends, buy back stock or fire employees.

In other words, governments are almost fully taking over free markets, with the profit principle dethroned as the key business driver.

With the events of the past three weeks, the perversion and conversion to a dystopian capital market and economic system is virtually complete.

As for me, with the Fed’s announcement of unlimited QE and its “will buy or support almost anything,” along with the pending passage of a $2-2.5 trillion stimulus package, this is the end of the capital markets as we have known them.

We have now entered unlimited QE and MMT where there is no escape.

It is the Roach Motel all over again.

In Chairman Bernanke‘s 2010 Washington Post op-ed, he argued that QE would lead to a virtuous economic cycle; therefore, the Fed would eventually be able to exit from its QE operations. I argued that once initiated, a reversal would be impossible. It would be like the Roach Motel, “You can check in, but you cannot check out.”

With the initiation of the Fed’s complete takeover and control of the US financial economy, there is now absolutely no accurate pricing discovery in the capital markets and we have entered a period of total manipulation. In light of this, the only markets I have an interest in are those where the heavy hand of government is not involved or only minimally involved. This leads me to rare commodities and collectibles. The public equity and debt markets are now nothing more than greater fool markets that are led by the greatest fools of all, the Fed and the Congress. US capital markets, RIP!

This is no small matter!

When everything is essentially socialized as to risk, a return vs risk evaluation is essentially meaningless since the risk side of the equation has been truncated.

Over a period of time which I cannot estimate yet, I will continue my preparation for a far different economic and financial environment.

Capital deployment strategies will likely have to change from what has been the norm in the post WW2 environment. We are in a New World Order.

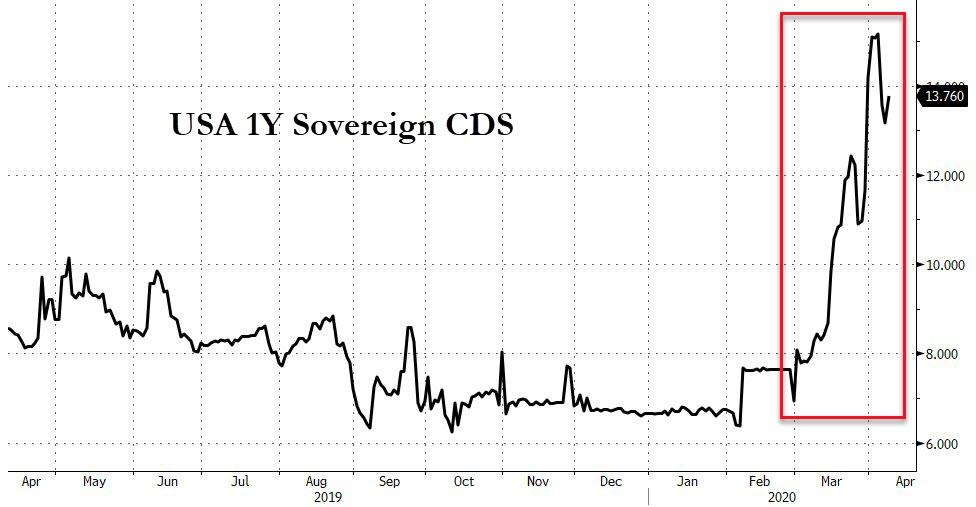

So let’s survey the damage from The Fed’s “there’s no limit to what we can do” words and actions this morning… and that is perhaps why USA’s sovereign credit risk is beginning to show some cracks…

Source: Bloomberg

First things first, the market knows best as to when and how the virus peaks…

Source: Bloomberg

Because the market did a great job of understanding the virus when it first broke out…

Source: Bloomberg

Stocks loved The Fed’s actions but as futures show, the effect of yet another $2.3 trillion in promises wore off fast…

Small Caps were best on the day as Nasdaq lagged…

This (admittedly shortened) week was among the market’s all-time best week’s ever…Small Caps were up a stunning 17%-plus and The Dow gained over 12.63% – the second best week since 1938 (+12.845% 2 weeks ago, +12.59% Oct 1974, +14.15% Jun 1938)

This was the biggest short-squeeze week ever…

The Dow tagged a 50% retracement, then fell…

The Dow is up 30% from its lows…

The other big story of the day was OPEC’s utter failure – after spreading rumors of a possible 20mm production cut… they managed less than half of that for just two months…

…and WTI went from +12% to -8% on the day…

The Dollar traded lower today…

Source: Bloomberg

As The Fed’s actions may have alleviated short-term dollar liquidity stress…

Source: Bloomberg

Treasury yields were lower today (even with stocks bid), but the curve continued to steepen with the short-end outperforming…

Source: Bloomberg

10Y remains rangebound…

Source: Bloomberg

The Fed’s “we’ll buy any and all of your crap” policy sent HY credit markets soaring with HYG having its best day ever…

Notably, HY “caught down” to VIX today again…

Source: Bloomberg

Crytpos were flat to modestly lower today, holding the week’s gains…

Source: Bloomberg

While gold and oil stole the headlines, silver was best among the major commodities…

Source: Bloomberg

This week’s ugliness in crude and strength in silver has left the Oi/Silver ratio at a record low… well below the apparent ‘floor’ of 1.5 ounces of silver per barrel that has been in place for 35 years…

Source: Bloomberg

Kyle Bass once said, “Buying Gold Is Just Buying A Put Against The Idiocy Of The Political Cycle. It’s That Simple!”

Source: Bloomberg

It seems that insurance is starting to pay off.

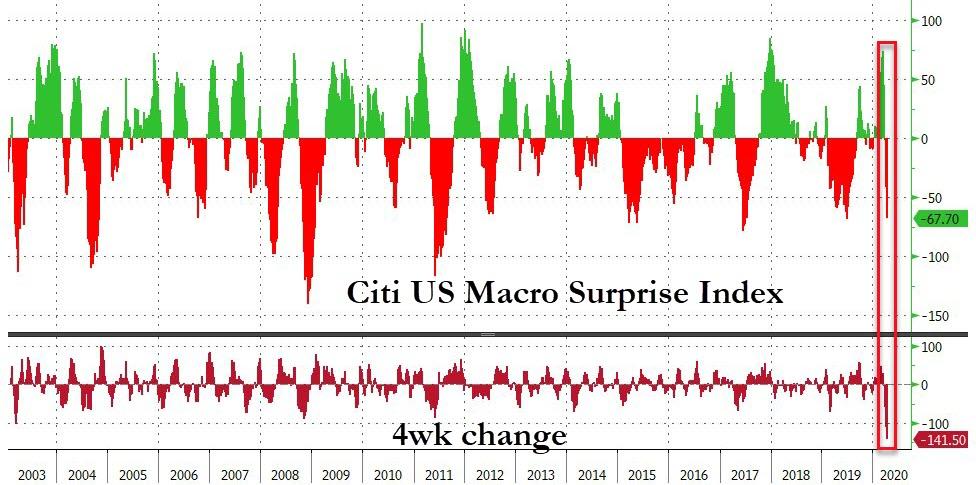

So stocks have two of their best weeks ever… and the US economic data suffers its worst monthly crash ever…

Source: Bloomberg

The reason stocks rallied…

Fun-durr-mentals? Nope!

Source: Bloomberg

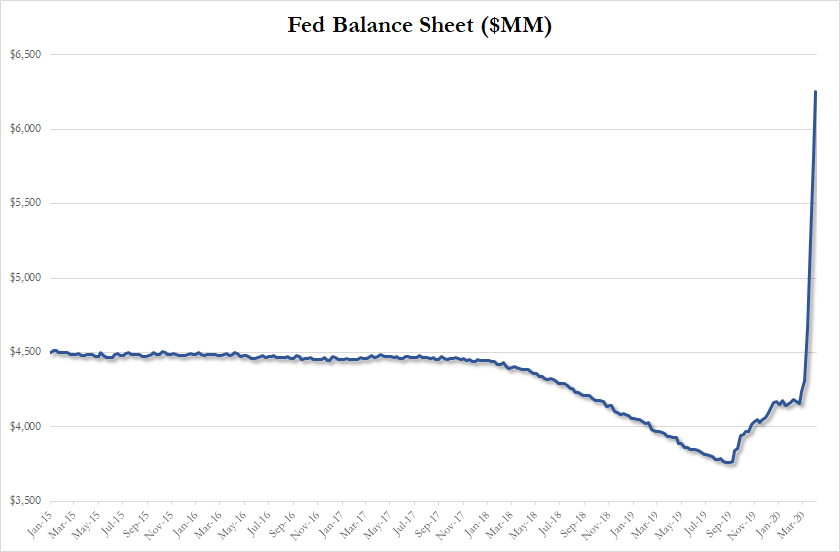

Simple! – The Fed injected $440BN in last week, total is now $6.3 trillion

And stocks are now more expensive than they were at the peak in price…

Finally as Mercutio McG (@JAMcGinley), noted so poignantly, “if the market gets back to ATHs while we are shutdown, it only proves the bears right. That the whole thing was a giant Fed fueled ponzi.”

A great deal of the coverage of the COVID-19 crisis has been apocalyptic. That is partly because “if it bleeds, it leads.” But it is also because some of the medical experts with media megaphones have put forward potentially catastrophic scenarios and drastic plans to deal with them, reinforced by assertions that the rest of us should “listen to the experts,” because only they know enough to determine policy. Unfortunately, those experts don’t know enough to determine appropriate policies.

Doctors, infectious disease specialists, epidemiologists, etc. know more things about diseases, their courses, what increases or decreases their rate of spread, and so on than most. But the most crucial of that information has been browbeaten into the rest of us by now. Limited and imperfect testing also means that the available statistics may be very misleading (e.g., is an uptick in reported cases real or the result of an increasing rate of, or more accuracy in, testing, which is crucial to determining the likely future course COVID-19?). Further, to the extent that the virus’s characteristics are unique, no one knows exactly what will happen. All of that makes “shut up and listen” advice less compelling.

More important, however, may be that in making recommendations to address COVID-19, those with detailed knowledge of the disease (the experts we have been told to obey) do not have sufficient knowledge of the consequences of their “solutions” for the economy and society to know what the costs will be. That means that they don’t know enough to accurately compare the benefits to the costs. In particular, because of their relative unawareness of the many margins at which effects will be felt, the medical experts we are being told to follow will likely underestimate those costs. When combined with their natural desire to solve the medical problem, however severe it might get, this can lead to overly draconian proposals.

This issue has been brought to the fore by the increasing number of people who have begun questioning the likelihood of the apocalyptic scenarios driving the “OMG! We need to do everything that might help” tweetstorms, on the one hand, and those who are emphasizing that “shutting down the economy” is far more costly than planners recognized, on the other.

Those who have brought up such issues (how long before they are called “COVID deniers”?) have been pilloried for it. Exhibit A is the vilification of President Trump for “ignoring the scientists,” such as the New York Times‘s claim that “Trump thinks he knows better than the doctors” after he tweeted that “We cannot let the cure be worse than the problem itself.”

One major problem with such attacks is the substantial literature documenting the adverse health effects of worsening economic conditions. For just one example, an analysis of the 2008 economic meltdown in The Lancet estimated that it “was associated with over 260,000 excess cancer deaths in the OECD alone, between 2008–2010.” That is a massive “detail” to ignore in forming policy.

In other words, the tradeoff is not just a matter of lives lost versus money, as it is often portrayed as being (e.g., New York governor Cuomo’s assertion that “we’re not going to put a dollar figure on human life”). It is a tradeoff between lives lost due to COVID and lives that will be lost due to the policies adopted to reduce COVID deaths.

Larry O’Connor put this well at Townhall when he wrote:

Why should the scientific analysis of doctors solely focusing on the spread of the coronavirus carry more weight than the very real scientific analysis of the deadly health ramifications of shutting down our economy? Doesn’t the totality of the data make the argument for a balanced approach to this crisis?

This issue reminds me of a classic discussion of specialists and planning in chapter 4 of F.A. Hayek’s The Road to Serfdom. “The Inevitability of Planning” is well worth noting today:

Almost every one of the technical ideals of our experts could be realized…if to achieve them were made the sole aim of humanity.

We all find it difficult to bear to see things left undone which everybody must admit are both desirable and possible. That these things cannot all be done at the same time, that any one of them can be achieved only at the sacrifice of others, can be seen only by taking into account factors which fall outside any specialism…[which] forces us to see against a wider background the objects to which most of our labors are directed.

Every one of the many things which, considered in isolation, it would be possible to achieve…creates enthusiasts for planning who feel confident…[of] the value of the particular objective…But it is…foolish to quote such instances of technical excellence in particular fields as evidence of the general superiority of planning.

The hopes they place in planning…are the result not of a comprehensive view of society but rather of a very limited view and often the result of a great exaggeration of the importance of the ends they place foremost…it would make the very men who are most anxious to plan society the most dangerous if they were allowed to do so—and the most intolerant of the planning of others…there could hardly be a more unbearable—and much more irrational—world than one in which the most eminent specialists in each field were allowed to proceed unchecked with the realization of their ideals.

Panic has seldom improved the rationality of decision-making (beyond the “fight or flight” reaction to facing a “man-eater,” when to stop and think means certain death). However, much of media coverage has fed panic. But the illogical and intemperate media attacks against those questioning the rationality of draconian “solutions” drown out, rather than enable, objective discussion of real tradeoffs. And if “Democracy dies in darkness,” as the Washington Post proclaims, we should remember that it does not require total darkness. The same conclusion follows when people are kept in the dark about major aspects of the reality they face.

Wimbledon Just Got Paid $141 Million On “Pandemic Insurance” They’ve Been Paying For The Last 17 Years

Somebody at Wimbledon is definitely earning their keep.

As the pandemic hit this year, the tournament was far more prepared than most organizations. For the last 17 years, Wimbledon has paid $2 million per year in “pandemic insurance” to prevent against exactly the type of scenario that prevented the tournament from happening this year.

We’re not sure what type of meetings and pitches needed to happen to convince the Board at Wimbledon to continue to shell out $2 million per year in insurance for a possible catastrophe that most people would have bet would have never happened in their lifetimes.

The insurance was first highlighted by The Times back in late March.

But it probably wasn’t always easy to part with the $2 million each year.

Over almost two decades, while most public companies looked for ways to stay unhedged, lever their cash flow streams, buy back at much stock as possible and cut their budgets, Wimbledon never abandoned their pandemic insurance.

Wimbledon paid into the insurance for 17 years, netting a total spend of $34 million. For 2020, that hedge returned $141 million, according to the Boston Globe.

German Tennis Federation Vice President Dick Horsdorff, told Sky Sports at the end of March: “Wimbledon was probably – as the only Grand Slam tournament many years ago predictive enough to insure itself against a worldwide pandemic, so that the financial damage should be minimized there.”

The organization’s foresight and preparedness will help soften a $309 million revenue blow that the tournament will suffer this year. The event was set to run from June 29 to July 12 this year.

It is the first time Wimbledon has been cancelled since World War II.

Mexico Folds, Agrees To Join OPEC+ Output Cut After Dramatic Objection

Update: Well, that didn’t take long. Less than an hour after news of its objection to the OPEC+ production cut hit, with Mexico even threatening to quit OPEC and become an observer, the OPEC member state has folded and has agreed to join the flock.

MEXICO AGREES TO OPEC PLUS PRODUCTION CUTS, SOURCES SAY

ALL OPEC PLUS MEMBERS AGREE TO CUT OUTPUT, SOURCES SAY

It’s unclear what the terms of the backroom deal were that prompted Mexico to change its mind, but the fact that Mexico will now produce even less out despite the slump in oil prices, will only add further pressure on the Mexican economy and soon lead to new all time lows in the MXN peso.

* * *

There is a reason why we noted earlier that the “deal” reached between Russia and Saudi Arabia had not been ratified by any other R-OPEC members: because it was unlikely the draconian caps and production terms imposed by the two super producers (23% across the board cuts for everyone) would be accepted by all oil producing nations.

Sure enough, just a few hours after the deal emerged, we got latest OPEC+ drama twist, Mexico – whose economy is already reeling between a collapse in production and a surge in covid cases – and refused to go want to go along with the cuts and has asked if it can withdraw from the OPEC+ group and become an observer.

As Bloomberg notes, “so far, its involvement had just seen it contribute natural declines in output, but it clearly doesn’t want to contribute active cuts.” But more importantly, Mexico’s threat “just goes to show the weakness at the heart of the OPEC+ arrangement. It welcomed countries that offered nothing but a natural decline in output as “cuts” simply to make the numbers look bigger. Now it has the embarrassment of watching one of them threaten to leave after being asked to make a real sacrifice.”

That said, as BBG concludes, losing Mexico seems a small price to pay for getting a deal done as it never contributed any real cuts anyway.

A bigger problem is that as Rystad Energy’s head of analysis Bjornar Tonhaugen says, echoing what we said earlier, the proposed output cuts are “far lower than what the market needs at the moment”, with the Mexican rejection suggesting that even those cuts may prove fragile.