While the majority of the country has been laser-focused on the coronavirus, stocking up on decades worth of toilet paper, and mass purchasing Clorox wipes, the United States House of Representative wrote a bill that will ban “assault weapons.”

Representative Hank Johnson, a Georgia Democrat who sits on the House Judiciary Committee, introduced H.R. 5717 on January 30, which would, among other items, ban the purchasing and possession of assault weapons, according to USA Today. Senator Elizabeth Warren, D-Mass., introduced in February the Senate version of the bill, S.3254. Not long after, the coronavirus hype was all over mainstream media burying the news of this draconian legislation.

The legislation introduced a variety of reforms with the intent to “end the epidemic of gun violence and build safer communities by strengthening Federal firearms laws and supporting gun violence research, intervention, and prevention initiatives.”

It would require state law enforcement authorities to be notified when a background check is denied and mandate the attorney general to issue an annual report to Congress detailing the number of background check denials.

It would also necessitate all firearm owners to obtain a federal firearms owner’s license, although purchases made before the enactment of the bill are exempt.

And the bill, as correctly stated by the Military Arms Channel, would make it illegal “to import, sell, manufacture, transfer, or possess, in or affecting interstate or foreign commerce, a semiautomatic assault weapon.”

The bill defines a semiautomatic assault weapon as any firearm with the capability to “accept a detachable magazine” and either a pistol grip, forward grip, grenade launcher, barrel shroud, threaded barrel or a folding, telescoping or detachable stock.

The government is, of course, exempted from the assault weapons ban. Law-enforcement officers (and other state agents) can possess these firearms as can those who are providing security at nuclear energy facilities. Firearms that are “manually operated by bolt, pump, lever or slide action,” have “been rendered permanently inoperable” or are antique are exempt from the ban as well.

Neither bill has passed, and it would still be needing President Donald Trump’s signature to become law. However, we thought it important to let you all know what’s going on behind the screens while we direct our attention to a viral outbreak. If you thought things were totalitarian now, just wait…it could get much uglier.

* * *

GOOGLE Is Doing Whatever It Can To De-Monetize SHTFplan.com And Shadow-Ban us. During these TOUGH financial times, we ASPIRE to stay completely independent and pay our full staff, so we can continue to deliver VALUE to you. It is possible for you to HELP us, by supporting our COVID-19 expert survival report HERE! Thank You, ShtfPlan.com Staff

Calls For Global Debt Jubilee Grow Louder As ‘Anything Goes’ Policy Mania Takes Over

About 140 global organizations and charities are calling for a worldwide Debt Jubilee to avoid some of the world’s poorest countries from collapsing into chaos amid the COVID-19 crisis,reported BBC News.

The British-based Jubilee Debt Campaign is leading the movement ahead of the G20 meeting this week.

“Developing countries are being hit by an unprecedented economic shock, and at the same time face an urgent health emergency,” said Sarah-Jayne Clifton, director of the Jubilee Debt Campaign.

“The suspension on debt payments called for by the IMF and World Bank saves money now, but kicks the can down the road and avoids actually dealing with the problem of spiraling debts.“

Clifton is urging for the immediate cancellation of 69 of the world’s poorest countries’ debt payments this year, which would free up at least $25 billion for the countries in 2020, and up to $50 billion if the jubilee was extended to the end of 2021.

“This is the fastest way to keep money in countries to use in responding to Covid-19, and to ensure public money is not wasted bailing out the profits of rich private speculators,” added Clifton.

The latest call for a Debt Jubilee should come as no surprise to ZeroHedge readers.

Over the last several decades, governments across the world have added insurmountable debts, leadingBill Buckler via The Privateer to say back in 2012 that the world has dived down a deep hole and into a trap that has “ensnared Japan more than two decades ago.”

And maybe Buckler’s Japanification fears for the rest of the world were right, because eight years later in 2020, central banks across the globe are still trying to print themselves out of a recession and or depression and into prosperity. And look at how it turned out for Japan, quantitative easing has failed and will continue to fail.

The problem today is that can-kicking yesterday’s problems has reached its limit.

Over the last several decades, governments across the world have added insurmountable debts. Sprott Money points out that debt-loads exceed 100% of GDP in many countries. The “ever-worsening indebtedness, and ever-larger interest payments on these unpayable debts, the precise definition of Debt Slavery. Throughout virtually the entire Western world, we are now well past this point-of-no-return,” warned Sprott Money.

This debt slavery has also become evident in emerging markets where countries are experiencing collapsing currencies, commodity prices, export earnings, and service and tourism revenues threaten to send many governments into default.

But calls for a Debt Jubilee are not limited to just emerging markets, but also developed economies. We noted several years ago that over the last 15 years, American consumers have taken out student loan debt, credit card debt, medical debts, personal loan. On a sovereign scale, the national debt is exploding, underfunded pension liabilities are rising, and Medicare costs are soaring.

The issue with both emerging and developed markets is how to manage all this debt as the virus has exposed the fragility of the financial system, with possible financial Armageddon nearing as world trade collapses.

And after decades of “kicking the can down the road” – it appears the piper finally wants his money. And why the talk of Debt Jubilee is starting to gain traction.

For some historical context of a Debt Jubilee, here is The Hutch Report’s take:

“Historians have counted around thirty episodes of general debt cancellations from 2400 to 1400 BC, noting they were occasions of great festivity which often involved the physical destruction of the tablets on which liabilities were recorded. One of the most famous episodes of debt forgiveness comes from ancient Babylon (modern-day Iraq). In 1792 BC, the self-proclaimed King Hammurabi of Babylon forgave all citizens’ debts owed to the government, high-ranking officials, and dignitaries.”

“Debt forgiveness was also practiced during the time of the Old Testament. In Jewish Mosaic Law, every seventh Sabbath year saw the wiping away of all debts, where creditors cancelled all the obligations of their fellow Israelites. Every 49th year (seven Sabbath years) was the ‘Year of the Jubilee’ when freedom from all debt and servitude was proclaimed throughout the land.”

Paul Craig Roberts has routinely pointed out that America is in dire need of a Debt Jubilee as wealth inequality is at extremes and insurmountable debts are mounting, rendering society unstable. In periods of economic collapse, like what is unfolding across the country today, the risk of a “social bomb” could be imminent.

To resolve the possibility of a nation imploding, Buckler, in 2012, said a modern Debt Jubilee is characterized as “quantitative easing for the public.” And now that MMT and helicopter money has become de rigueur, why not push the endgame of monetary malarkey – a global debt jubilee.

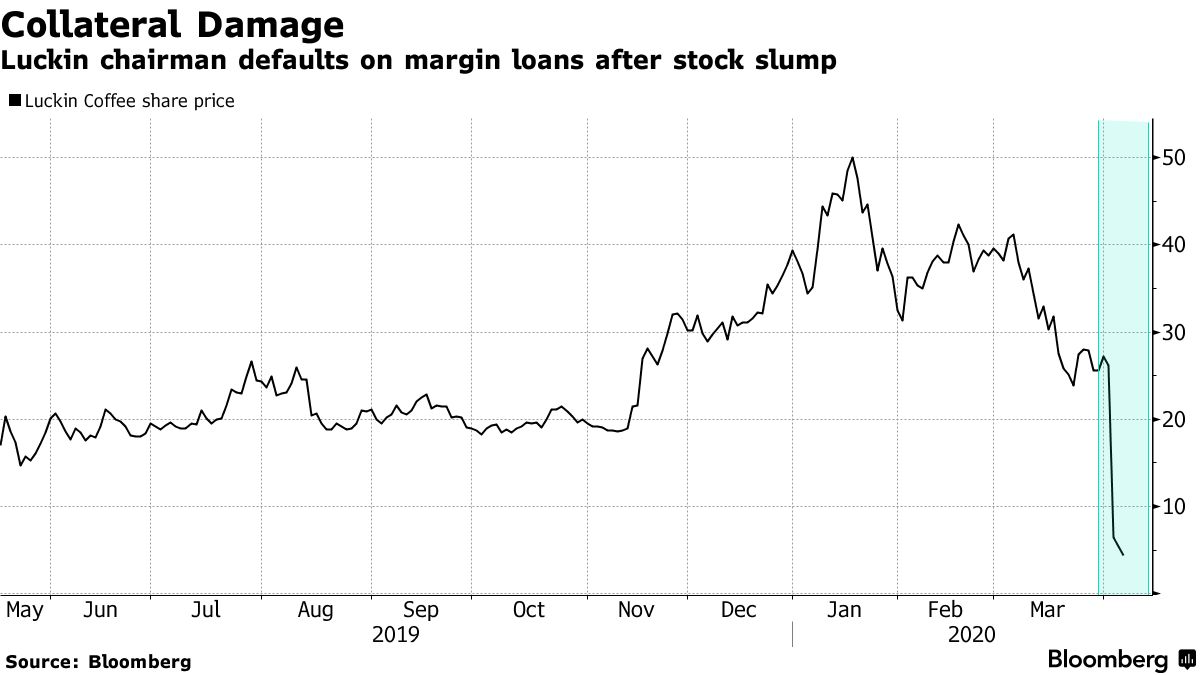

Morgan Stanley Was One Of The Biggest Margin-Loan Providers To Luckin Coffee’s Founder

Among the banks who made margin loans to Luckin Coffee’s founder, one stands out in particular: Morgan Stanley.

Morgan Stanley was part of a consortium of banks that extended loans to Lu Zhengyao across three different funding rounds. Morgan Stanley is said to have put up about $100 million of a total of over $340 million in loans. Credit Suisse Group AG and Haitong International Securities Group were also named as lenders.

The recent fraud allegations at the company caused the loans to default, according to Bloomberg.

Additionally Goldman Sachs said that an entity controlled by Lu’s trust reneged on $518 million of margin debt and that lenders had seized up to 76.4 million LK shares as a result. It’s unclear whether or not the shares have been sold yet.

Goldman and Barclays’ were said to have about $70 million in exposure, each, to the loans. Credit Suisse and other banks that helped the company IPO and subsequently helped it raise convertible debt, have been sued as a result of the stock plunge.

Meanwhile, Morgan Stanley is also one of the largest lenders to Elon Musk, with the Tesla CEO taking $50 million from the bank and mortgaging five homes with their help back in early 2019. The bank was also part of a consortium of lenders to Alibaba’s Chairmen back in 2015.

Recall, on April 2, we reported that Luckin Coffee had brought to the attention of the board information indicating that COO Jian Liu and several employees engaged in certain misconduct, including fabricating certain transactions, starting in Q2 of last year. It was estimated that total ‘fake’ revenue was around $310 million.

If you yearn for the days before COVID-19 swept across the planet, I regret to inform you that those days are gone.

This isn’t a warm and fuzzy blog post telling you that everything is going to be all right. If you’re looking for reassurance that “we’ve got this,” I’m afraid I can’t provide it. This article wasn’t written to console or coddle you, so if that’s what you’re seeking, you’re going to want to stop reading right now.

If, however, you want a reality check on what I believe we’re really facing, I’m not going to hold back. You’ve been warned.

We’re not even halfway through.

You may have seen some optimistic reports recently that the “worst” is behind us. It would certainly be lovely if that’s the case, but in my opinion, this ordeal is just getting started. I wrote an article previously about how long we could expect our current state of lockdown to last using the timelines of China and Italy as points of comparison, and based on that, we are 17 days in as of the writing of this article on April 8.

The lockdown of Wuhan is expected to last 77 days. If our own timeline continues to echo that of China, then we’re not even halfway there. We have at least 2 months left and this doesn’t include any new clusters when the lockdowns are totally lifted or any second waves. We’ve barely begun living in our current state of purgatory and this will continue (and most likely worsen) for quite some time.

So if you’re seeing this as a little break after which you’ll pick up with your life exactly where you left off, you’re going to be extremely disappointed. You need to adapt now because if you don’t, the future is going to be very hard on you mentally.

Use this time to think about the changes you can make to meet the needs of your family. Learn new skills, practice old ones, and get your head in the game.

The supply chain may never be the same.

Nearly every store in America (the ones that are still open, anyway) has glaring bare spots on their inventory. Who would have expected paper products to be the “gold” of our apocalypse? There was an original run on supplies back in early March when the general public realized, “Hey, this is for real!” and razed store shelves bare. Even though preppers already had most of their supplies put back by the time this happened, we were no less vilified by the media as panicked shoppers got into physical altercations over toilet paper and macaroni.

Government officials told everyone to “calm down” and “just shop for the week.” They promised that if we did, everything would be back in stock in no time. Many of us knew even then that this wasn’t true. The ports in California were empty of shipping containers from China where many of our essential goods are produced. There’s no inventory with which to replenish the inventory.

It’s been more than a month since that first shopping frenzy and unfortunately, supplies are still limited in most parts of the country. A reasonably-sized package of toilet paper can’t be had for love or money, nor can one easily locate cleaning wipes, paper towels, 20-pound bags of rice, and bottles of bleach. Other supplies are available, but sparsely and often in limited quantities: meat, eggs, butter, dried goods like pasta and rice, and canned goods. Prices have approximately doubled on many items.

Don’t expect this to clear up any time soon. Abundant inventory may well be a thing of the past. Many of the products sold in American stores are made in China. Even much of our meat that is a “product of the USA” is processed in China. Obviously, China is going to replenish its own inventory before exporting goods to us. Here’s a list of goods that we import from China that we may not be receiving in the same quantities in the future.

As well, the days of just “running to the store” to replace things or pick up a single ingredient are gone. Now, in many parts of the country, you have to walk through a cordoned off maze to enter a Walmart or Costco store. Only a certain number of people can be there at a time. Shopping means you’re risking your own health if someone else is ill, or you are ill and don’t realize it, you’re risking the health of others. It’s no longer quick, easy, inexpensive, or pleasant in any way.

And the generous offerings of days gone by are disappearing. In some areas, the store may have things you want but because the government there doesn’t consider them “essential,” you won’t be allowed to buy them. Ordering online may soon be your only option for things like craft supplies, clothing, decorative items, and shoes. And even when you order online, it may take quite some time before the goods arrive. Amazon has said it is prioritizing necessities, leaving people with uncertain shipping times.

The rules will get more restrictive and violence will ensue.

Every state with some form of movement restriction (lockdown for lack of a better word) has its own set of rules which are handed down by the respective governors in the form of an executive order. Some states are more restrictive than others and a small handful of states have no restrictions whatsoever.

The other difference between states is the methods of enforcement. Some states have the rules on the books but do little to enforce them. Others are levying fines. One municipality in Louisiana found it amusing to announce the beginning of the curfew with the Purge siren, terrifying people who were already on edge.

Don’t expect this gentle approach to continue. While I don’t think we’ll go full-Wuhan and weld people into their apartments, our Constitutional rights are already being trampled in numerous ways.

Expect as the rules and enforcement efforts become more stringent for people to balk. As the money being dished out by the government dwindles to a trickle and as promises made by the government get broken, people will become more and more desperate.

Imagine. Your ability to make a living was suddenly taken away through no fault of your own. You’re all but under house arrest. Your government is threatening you with fines, incarceration, and even possible violence. Your family is hungry and you have nothing to feed them. What would you do in that situation?

There’s virtually no way this continues without violence ensuing, either out of rebellion or hunger or possibly both. Fewer and fewer police officers are available to respond as more of them get diagnosed with COVID-19. In New York City, nearly ten thousand first responders are ill. When you put all this together, it’s a recipe for violent crime.

The economy will be devastated.

We’re already watching our economy get destroyed right in front of our eyes. Never in history – including the Great Depression – have so many Americans been unemployed. And the fact that they all became unemployed at once is even worse. By the end of March, 7.1 million people had filed for unemployment due to COVID-19.

Many of the people who lost their jobs are the ones who are least able to afford it – hourly workers. Those who work at or around minimum wage are less likely to have a savings account to see them through the rough spot.

Then there’s the fact that the government appears to have lied. Others who became unemployed were initially told they qualified, but now the application process is proving impossible. Gig workers, such as drivers for Uber, Lyft, and Doordash, are being asked to supply pay stubs, something they just don’t have. It just isn’t how it works.

Those who have applied are waiting weeks to hear back from state unemployment programs. Their applications will likely be rejected, leaving them without any income for an indefinite amount of time. The advice for these workers?

A spokesperson for the New York State Department of Labor says the guidance requires workers who are not usually eligible for unemployment benefits to apply to state programs, get rejected, and then apply again for the federally funded pandemic assistance. (source)

So for all the big talk about making unemployment easy to get and simple to apply for, it isn’t working out that way at all for many people.

And of course, the economic issues are bigger than that. Small businesses are in big trouble. Those who are not able to find a way to operate during these difficult times still have overhead and bills. They have rent and utilities for their place of business. Many have inventory payments that were due net-30. Restaurants that can’t make the conversion to takeout and delivery, fitness studios, gyms, clothing stores, and many more independent businesses may never reopen after the government-imposed hiatus.

One by one, families across America are looking at disappearing income, higher prices, and with shelter-in-place orders nearly everywhere, no real way to seek new employment. Unemployment, if and when it comes, is only a short term solution. If ever there as a chance to usher in Universal Basic Income and see people welcome it with open arms, this crisis would be it. Of course, UBI brings with it many problems, not the least of which is a lord-and-serf relationship and a slippery slope toward the social credit system, also brought to us by China just like the COVID-19 outbreak.

As the economy continues to plummet because people are only purchasing the bare necessities, we’ll see other issues arise. How will you pay your rent or mortgage if your job qualifications are in a field that is now considered a luxury? How will you keep your utilities on when you’re not making any money? How will you feed your family, keep a roof over your head, pay for medical care, and maintain a vehicle?

If you’ve never been through personal financial hardship before, you could be in for a terrible reality check when the cost of your most basic essentials is out of reach. But many of us have been there. We can tell you that it often makes you feel powerless – it’s difficult and humiliating, but you can get through it.

If you’re a business owner, how will you keep operating if you have no working capital? How can you hire people if you don’t know whether you’ll be able to keep them on board for more than a couple of pay periods? How can you buy more inventory and can you even acquire that inventory anymore? Will you be able to get the parts you need to repair items if you run a repair service business?

As you can see, there are more questions than answers. (source)

We’re just at the beginning of this bumpy ride, and there’s really no place that it leads except to an economic depression even worse than the one that took place in the 1920s.

We’ll never “get back to normal.”

For all the people wondering when we’re going to get back to normal, I’m very sorry to say, the answer to that is “never.”

There are jobs lost that are never coming back. Businesses that were successful may never reopen, and if they do, unless they can pivot to cater to necessities, they won’t last long in an economy with widespread unemployment.

And medically speaking, we are a long way from “normal” too.

Dr. Anthony Fauci, the director of the National Institute of Allergy and Infectious Diseases, told a coronavirus press briefing on Monday that the world may never return to the “normal” that was known before the outbreak.

…”When we get back to normal, we will go back to the point where we can function as a society,” he said. He continued, “If you want to get back to pre-coronavirus, that might not ever happen in the sense that the threat is there.” (source)

What’s more, the virus will be back for another wave.

Fauci said Sunday that people must be prepared for a resurgence next year, which is why officials fighting the pandemic are pushing for a vaccine and clinical trials for therapeutic interventions so “we will have interventions that we did not have” when this started. (source)

We could be looking at on and off periods of social distancing for eighteen months to two years before this is over. Here’s what the models suggest:

Under this model, the researchers conclude, social distancing and school closures would need to be in force some two-thirds of the time—roughly two months on and one month off—until a vaccine is available, which will take at least 18 months (if it works at all). They note that the results are “qualitatively similar for the US.”

Eighteen months!? Surely there must be other solutions. Why not just build more ICUs and treat more people at once, for example?

Well, in the researchers’ model, that didn’t solve the problem. Without social distancing of the whole population, they found, even the best mitigation strategy—which means isolation or quarantine of the sick, the old, and those who have been exposed, plus school closures—would still lead to a surge of critically ill people eight times bigger than the US or UK system can cope with…

…How about imposing restrictions for just one batch of five months or so? No good—once measures are lifted, the pandemic breaks out all over again, only this time it’s in winter, the worst time for overstretched health-care systems.

And what if we decided to be brutal: set the threshold number of ICU admissions for triggering social distancing much higher, accepting that many more patients would die? Turns out it makes little difference. Even in the least restrictive of the Imperial College scenarios, we’re shut in more than half the time.

This isn’t a temporary disruption. It’s the start of a completely different way of life. (source)

For the foreseeable future, it appears that this is our life.

What will the future look like?

At this point, it’s pretty difficult to imagine what a future filled with waves of a pandemic virus, a devastated economy, and great loss will look like.

But some of the things we can expect are intermittent periods of social distancing, periods of interaction. Businesses like restaurants, movie theaters, bars, malls, travel experiences, and sports venues will never be the same and if they survive, will only be able to operate intermittently.

Homeschooling will be a long-term thing – children will not be able to be in a regular school setting during outbreaks.

We’re going to be looking at an entirely different world, one full of six-foot distances, immunity passports, and dystopian tracking methods using our phones.

One particularly unsettling possibility is a picture is painted by Technology Review.

We don’t know exactly what this new future looks like, of course. But one can imagine a world in which, to get on a flight, perhaps you’ll have to be signed up to a service that tracks your movements via your phone. The airline wouldn’t be able to see where you’d gone, but it would get an alert if you’d been close to known infected people or disease hot spots. There’d be similar requirements at the entrance to large venues, government buildings, or public transport hubs. There would be temperature scanners everywhere, and your workplace might demand you wear a monitor that tracks your temperature or other vital signs. Where nightclubs ask for proof of age, in future they might ask for proof of immunity—an identity card or some kind of digital verification via your phone, showing you’ve already recovered from or been vaccinated against the latest virus strains.

We’ll adapt to and accept such measures, much as we’ve adapted to increasingly stringent airport security screenings in the wake of terrorist attacks. The intrusive surveillance will be considered a small price to pay for the basic freedom to be with other people.

As usual, however, the true cost will be borne by the poorest and weakest. People with less access to health care, or who live in more disease-prone areas, will now also be more frequently shut out of places and opportunities open to everyone else. Gig workers—from drivers to plumbers to freelance yoga instructors—will see their jobs become even more precarious. (source)

Never let a good crisis go to waste, right?

This is necessarily how it’s going to happen – it’s only one possible scenario of the many unpalatable futures that are currently emerging. None of them are scenarios that embrace freedom or the joy of anonymity.

The life we knew is not coming back. But it’s better to know this and begin to think about how to mitigate these changes. Think about how you can earn a living, how you can teach your children about freedom in an unfree world, and how you can resist being a figure on a screen, constantly monitored for a spike in temperature.

And who knows? Maybe Americans will return to their independent ways and say, “No more.” But the changes that took place after 9/11 suggest otherwise. Unless a fearful populace can be convinced that freedom is more important than safety, this will lead to more restrictions and some kind of Pandemic Patriot Act 2.0.

We don’t know what’s coming, but it will be different.

Facing uncertainty is always difficult. But by focusing on the things you can do, it can be managed.

I can’t tell you exactly what the future holds. But I can tell you that the lives we lived prior to COVID-19 are not going to re-emerge like nothing ever happened. And every day the lockdowns continue lessens the possibility of that even more.

You need to accept that now so you can best figure out how to navigate the post-COVID world that awaits. This doesn’t mean you’ll never be able to be happy again. It doesn’t mean you’ll lose everything. It means that things are going to be different and if you don’t accept that, your acclimation period will be dangerously long. As Selco always says, the sooner you understand the new rules, the better off you’ll be.

Just How Bad Is It Going To Get: JPMorgan Halts All Non-Government Guaranteed Small Business Loans

With America’s small and medium businesses suffering from cardiac arrest now that the economy is in a indefinite coma, it is hardly a surprise that the largest US bank, JPMorgan Chase has been inundated with more than 375,000 requests for $40bn of loans under the $350bn small business rescue scheme, a higher number of applications than any other bank, its consumer head Gordon Smith told President Donald Trump on Tuesday.

It is in this context that the FT reports that Chase has temporarily stopped accepting applications for small business loans outside the government’s Paycheck Protection Program. A Chase spokeswoman told the FT that the bank was now devoting all of its small business underwriting resources to processing these applications and had “temporarily suspended” taking other applications from small businesses. The bank was continuing to process non-PPP applications already in train, she said, and would revisit the issue of new applications next week.

This means that any small business that have borrowing needs beyond the PPP’s limits, or if they want to borrow for purposes beyond wage bills, they would need to seek other facilities or other lenders.

Ok fine, JPM is so busy trying to bail out mom and pop shops, it doesn’t have time to deal with anyone else. Why is that a story? Here’s why.

First of all, even before the Treasury announced it would hand out PPP loans to eligible business, the issuance of commercial and industrial loans exploded, and in the past month, soared by nearly $400 billion, the fastest increase on record.

There is a good reason for this surge, and it has to do not only with a surge in demand but also supply – after all such loans are some of the highest margin products US commercial banks offer, in fact one can argue that it is not prop trading or frontrunning the Fed, but issuing loans that is the primary business of – you know – commercial banks!

Furthermore, loans are not only extremely profitable over their lifetime, they are also secured by assets, effectively eliminating downside risk for the bank lender. Said otherwise, of all bank products, these are the ones US commercial banks want to flow no matter what. One final point: bank lending is the most scalable, as it involves a minimum amount of upfront work which creates an extremely lucrative revenue stream since traditionally only a tiny percentage of loans default, at which point the bank’s loan workout teams kick in.

Unless… that’s no longer the case.

Which brings us to what is the much more likely reason why the largest US commercial bank has decided to suddenly no longer participate in the one product that is the bread and butter of large US commercial banks.

As a reminder, there is one way that PPP loans are unique – they are guaranteed by the Treasury, which means that JPMorgan carries absolutely no risk when it issues the loan. Worst case, the loan defaults and the bank issues a refund request to Uncle Sam who makes JPM whole. Simple enough.

But all those other loans that flooded the system, see they don’t have a government guarantee. And even though they would normally pay generous interest over the lifetime of the loan, that is not the case if JPMorgan’s default assumptions have soared alongside the surge in new issuance.

Said otherwise, the only reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is if the bank expects a default tsunami to hit. And it would expect that if JPM’s risk managers have recalibrated their default assumption models and now see a wave of corporate bankruptcies hitting. After all, why issue loans that will default in months if not weeks, when JPM can stick to the 100% risk free issuance of government-guaranteed small-business loans, especially if it makes JPM look patriotic by doing its duty to bail out America.

If indeed it is the case that JPMorgan is quietly stepping away from the non-government backstopped lender market, expect one after another bank to do the same, and other big and not so big US banks such as BofA, Citi, and Wells Fargo to follow just as quietly in JPM’s footsteps and halt loans to all small business across America due to fears of a default tsunami.

And if that indeed happens, and if America is about to be flooded with thousands if not millions of corporate bankruptcies, what happens then? Will the Fed expand its functions to become “bankruptcy court of last resort” for all of America and offer unconditional DIP loans to millions of small and medium businesses, while equitizing their existing lenders?

And since this is unlikely, inquiring minds want to know just how bad will the US depression get over the next few months if JPMorgan has just battened the hatches and has put up a “closed indefinitely” sign on its window.

I have to wonder if our state government’s lockdown of the population, curtailment of civil liberties, destruction of job opportunities, and denial of basic medical, education, and cultural needs would have been necessary and legally justified had each of us been equipped with our own supply of masks.

At the beginning of the self-declared State of Emergency, Washington Governor Jay Inslee declared, among many other restrictions, that access to basic medical services, such as routine doctor visits, dental procedures, diagnostic services were to be prohibited, ostensibly on the fact that masks should be diverted from these services and conserved to supply hospitals and critical care centers that were lacking in preparedness and woefully out of stock. He further reiterated that because the public will spread corona virus, we were ordered to self-quarantine, resulting in tens of thousands of job losses, an upset in daily life and the general loss of liberty.

Before the next virus crises hits, I propose we adopt a new symbol of American Freedom and Liberty–The N95 Mask–and shield ourselves from the next outbreak of panic legislation and overreach by executive and administrative power

Washingtonians, can debate whether or not the actions of our state government was reasonable or necessary, but the fact is that what is happening here provides a strong lesson in what life is like when freedom is taken away, and of the great importance of preventing a similar environment. It was not the corona virus that led to this, the upheaval was the result of mandates forced upon us by politicians and agency bureaucrats. Surely COVID-19 was the impetus, but government proclamations were the instrument. And that instrument can be wielded in the future regardless if there is an actual threat or enemy if we do not learn how to restrain government overreach.

We are told that we cannot hunt for food, attend funerals for those who are not of our immediate family, attend church, peacefully assemble, purchase clothing, work in some of our chosen occupations, visit public parks and forests, visit our dentist or doctor for needed but not emergency health care, travel outside our areas of residence, and in other states be outside our homes past 9:00 p.m. If we do so we are subject to arbitrary restrictions under threat of arrest. Presumably this was partially due to shortages of masks and the transmission potential of viruses. Health care workers are permitted to attend to COVID-19 patients, is there any reason we cannot live a lifestyle of our own choosing if we all instead simply adorned ourselves with N95 masks when in the public arena or at work?

I find it difficult to believe that the Courts here would not frown upon the governor and state agencies claiming a legitimate state interest in curtailing liberty as we have seen recently had each of us had the universal ability to wear masks and go about our lives as we did previously. Had hospitals not failed to adequately stock their warehouses with PPE supplies such as masks and other sundries and not relied on the economics of “Just in Time” supply chain strategies the state could not fully justify the mandate for dental offices and basic health care providers to cut services on the rubric of masks being in short supply. How could the state also justify restricting the public’s right to assemble in public, keep their shops open, or engage in their chosen profession when we each have masks that would make transmission of disease negligible? The Courts do not view the power of government to restrain freedom during an emergency as absolute.

Rather than punishing society and coercing us under penalty of arrest through proclamations of emergency, we should instead demand that we be accomodated to protect our liberty by allowing us or giving each household a supply of protective masks and gloves.

We might actually save more lives than we are by treating the symptoms of disease at the expense of jobs and freedom.

Perhaps we should go from politicians promising a chicken in every pot, to a box of N95 masks in every medicine cabinet. It would actually be much cheaper in the end than wrecking our economy and our livelihoods.

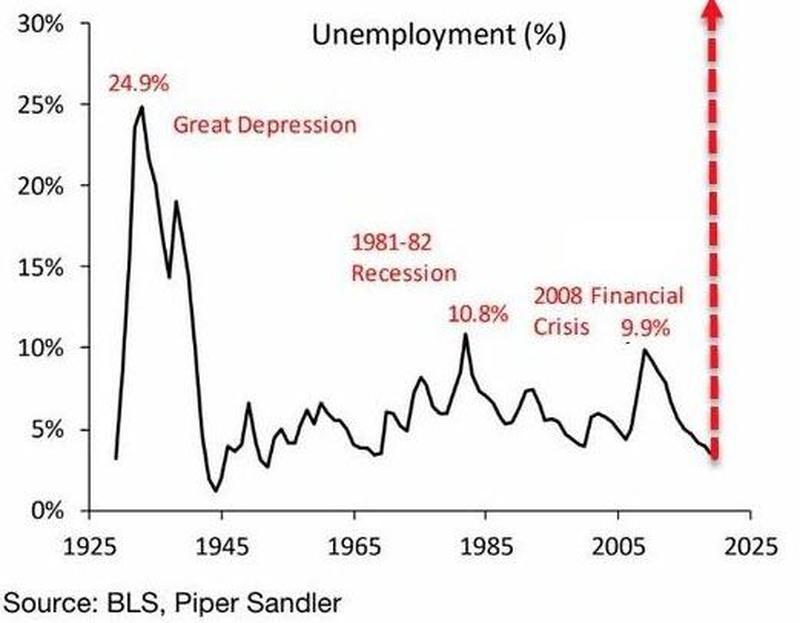

Over the past month, the American economy has collapsed into a depression, with the most significant unemployment spike in history. Millions of people have just lost their jobs, and as we’ve been documenting, food bank networks across the country are becoming overwhelmed.

We recently said that some food banks had seen an eightfold increase in the number of people asking for food. The National Guard has been deployed to food banks in Cleveland, Pittsburgh, and Phoenix, to make sure supply chains do not breakdown, which if food shortages did materialize, it could lead to a “social bomb,” triggering civil unrest.

“I’ve been in this business over 30 years, and nothing compares to what we’re seeing now. Not even when the steel mills closed down did we see increased demand like this,” said Sheila Christopher, director of Hunger-Free Pennsylvania, which represents 18 food banks across 67 counties.

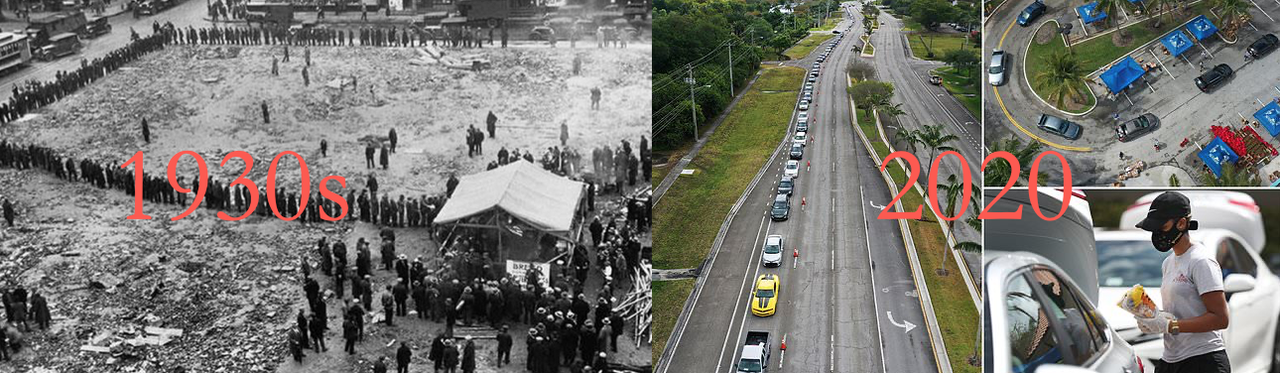

Today’s food bank lines resemble ‘breadlines’ from the 1930s. However, this time around, Americans are not standing around city blocks waiting for soup, they’re sitting in mile-long traffic jams outside donation centers waiting for a care package.

The run on food banks was first documented on March 30. Drone footage captured a traffic jam of hungry Americans waiting to pick up food aid at a facility in Duquesne, Pennsylvania.

As a reminder, to visualize how America went from “the greatest economy ever” to “Greater Depression,” in just one month, take a look at the chart below:

The run on food banks will only increase as the depression worsens in April.

On Monday, a drone captured dramatic footage outside a South Florida food bank that measured “miles-long” row of cars, reported Daily Mail.

The footage is from outside the Feeding South Florida food bank, located in Broward County.

The food bank reports a 600% jump in the number of people in recent weeks as South Florida’s services economy collapsed, resulting in hundreds of thousands of job losses.

Stephen Shelley, president and CEO of Farm Share, which distributes food to food banks, churches, schools, and other nonprofits, said the amount of people asking for food at food banks is unprecedented.

“The volume is at a level we’ve never seen before,” Shelley said, adding that his company is running at full capacity at the moment to handle the demand surge. He said the amount of food that he is moving to keep pace with demand is “overwhelming the system.”

A perfect storm is brewing deep in America, one where overwhelmed food bank networks could see supply chain disruptions that could trigger food shortages in various low-income regions, that would undoubtedly leave many people hangry – and possibly incite social unrest.

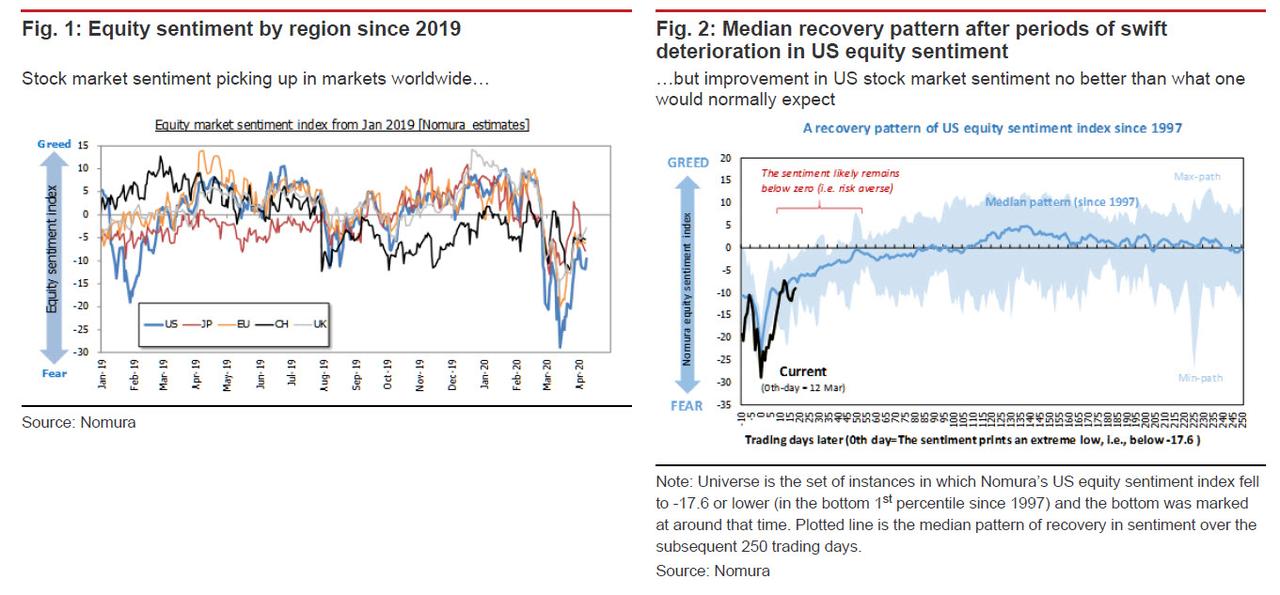

Nomura: “This Unenthusiastic, Inorganic Bear Market Rally” Faces An April 22 Day Of Reckoning

Just in case Nomura’s quant Masanari Takada wasn’t clear enough yesterday when he said that the current rally, which pushed the S&P back into a bull market from its March 24 lows was nothing more than a giant “bear squeeze” rally, driven by panicked exits from shorts that investors accumulated during the downturn, he doubled down today when in a note published overnight, he said that “the present rally should best be viewed as an unenthusiastic, inorganic bear market rally” and that “the stock market rebound across major world markets is being led by exits from bearish trades, including a squeeze on short positions held by systematic traders.“

Echoing Morgan Stanley which found that virtually nobody is participating in the current bear market rally, the Nomura quant writes that global equity market remain jittery as “most investors (apart from some with short investment horizons) are still in standby mode“, and in fact, “some may be inclined to sell whatever rallies come along.”

Meanwhile, as Takada shows in the charts below, the pick-up in investor sentiment looks like no more than the sort of spontaneous rebound in sentiment that one would normally expect under the circumstances.

As a reminder, looking at investor flows, Morgan Stanley was surprised that in the recent surge higher, there had been virtually no participation on the buy side, and even more perplexing, almost no short covering either, especially in the latest leg higher:

ZERO HF re-grossing (fundamental or systematic)

ZERO covering of the $33bn net short in Futures (and volumes falling)

ZERO new build in call ownership (and volumes falling).

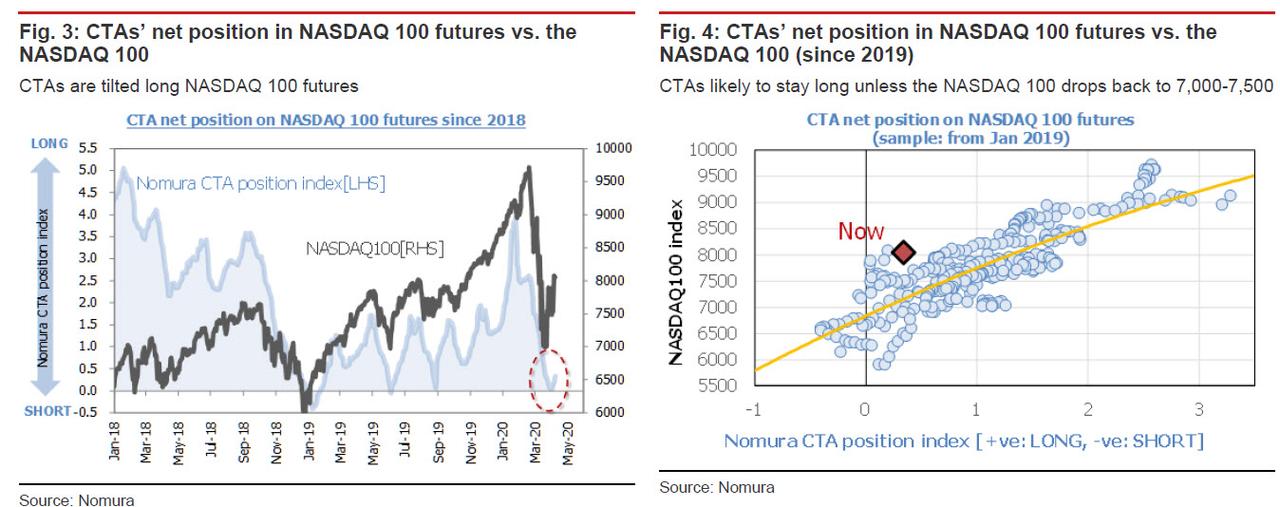

Yet while there is nothing explicitly new in the above which we had presented previously, where Takada did provide a new perspective was his estimate of how long this bear market rally will last. To do that, he analyzed the transition in the bullish flows “baton” between CTA and fundamental investors, warning that “should the baton get dropped, we would expect

CTAs’ net buying of NASDAQ 100 futures to wind down by 22 April.”

We think that periodically checking CTAs’ net position in NASDAQ 100 futures may give investors a sense of how long the bear market rally might last… It appears that CTAs were quick to swing long on NASDAQ 100 futures. To anyone looking to gauge the strength of technical investors’ inclination to buy, CTAs’ net position in NASDAQ 100 futures can be read as a leading indicator of what may happen in other equity futures markets.

Nomura expects CTAs to continue “tentatively chasing the market up for the moment, with a push from the decline in stock market volatility.” Futures prices have increased more quickly than the pace of growth in CTAs’ net long position would suggest, but even when adjusting for this, CTAs should remain inclined to buy unless the NASDAQ 100 drops down into the 7,000-7,500 range.

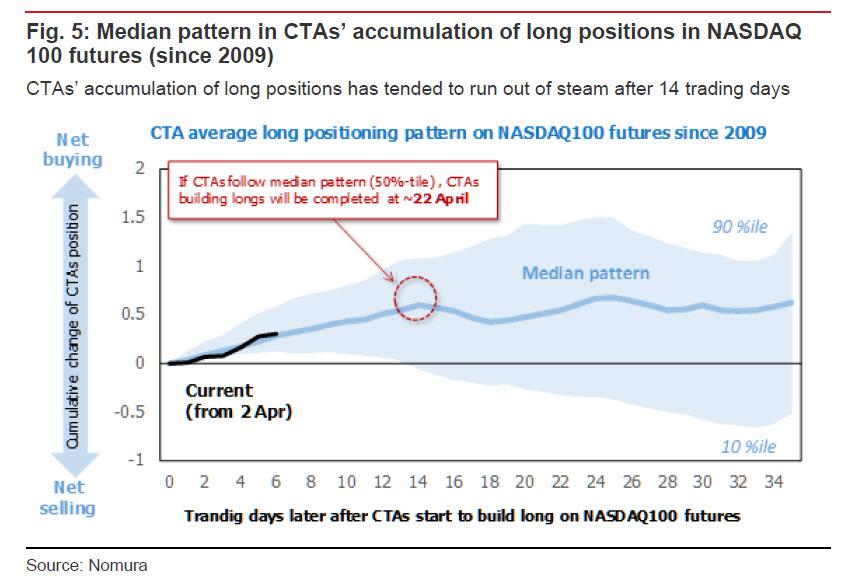

However, as Takada shows next, the record of periods in which CTAs have accumulated long positions in NASDAQ 100 futures since 2009 shows that on average, net buying by trend-following investors has tended to mark an initial peak about 14 trading days after the net buying started. This time around, we estimate that CTAs started going long on 2 April (or around then), so if precedent is any guide, Nomura expects the systematic buying to fizzle out by April 22 at the latest.

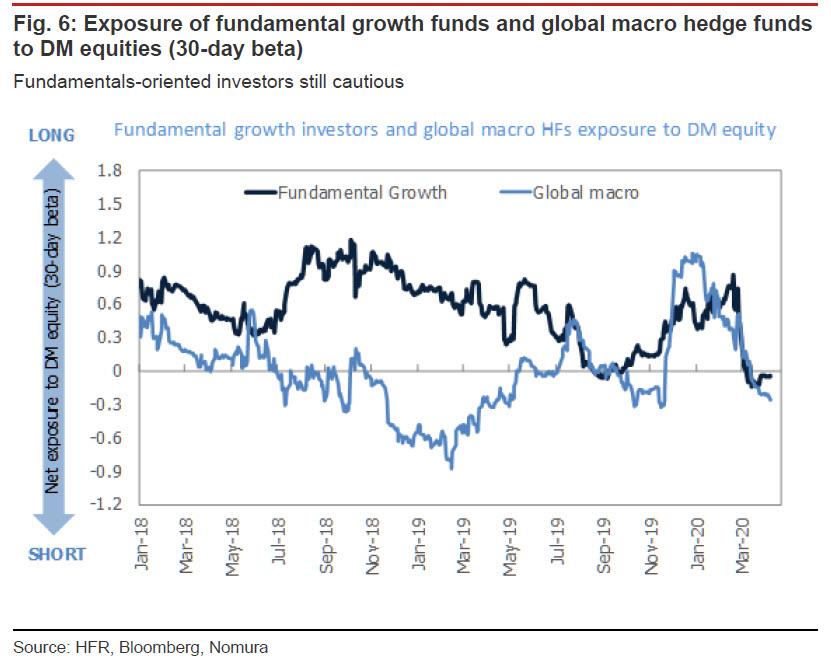

But while CTAs may have already gone long, fundamentals-oriented growth funds and macro funds are far more cautious, and as we showed earlier today, still have a negative net exposure. This is important, because the upward momentum behind a technical rally tends not to stabilize until heavyweight fundamentals-oriented investors like these start chasing the market up.

For the coming week or two, then, the critical thing to look out for is whether the CTAs that are currently driving the rally manage to smoothly pass the baton to fundamentals-oriented investors without anyone dropping it. And, as Nomura concludes, “should the baton get dropped, we would expect CTAs’ net buying of NASDAQ 100 futures to wind down by 22 April.”

Two weeks ago, President Donald Trump signed the largest stimulus bill in U.S. history: more than $2 trillion.

For once, both Republicans and Democrats agreed. The Senate voted 96-0. The House didn’t even bother with a formal vote.

At the White House, a reporter asked the president, pointing out that the bill includes $25 million for the Kennedy Center, “Shouldn’t that money be going to masks?”

“The Kennedy Center has suffered greatly because nobody can go there,” Trump responded.

“They do need some funding. And look — that was a Democrat request. That was not my request. But you got to give them something.”

“Something” they got. The bill includes $25 million for Congressional salaries, $50 million for an Institute of Museum and Library Services and lots of other wasteful things.

Only a few politicians were wary.

Rep. Thomas Massie complained that he wasn’t even allowed to speak against the bill.

Rep. Alex Mooney asked:

“How do you pay for it? Borrow it from China, borrow it from Russia? Are we going to print the money?”

Those are good questions.

Our national debt is already $24 trillion. Now it will jump, percentage-wise, to where Greece’s debt was shortly before unemployment there hit 27%.

But the United States can’t be bailed out by others.

How will we pay off our debt? That’s the topic of my new video.

There are really three options:

1. Raise taxes.

2. Print money.

3. Default.

Let’s consider each:

1. Raising taxes on rich people is popular. Even Michael Bloomberg wants “higher taxes on billionaires” like him.

But raising taxes on the rich often kills the wealth and jobs some rich people create. And it won’t solve our debt problem. Even if we took all the billionaires’ wealth — reducing their net worth to zero — it would cover only an eighth of our debt.

2. Some on the left now say, “Don’t worry about debt, just print money!”

This belief, called Modern Monetary Theory, destroys lives.

Zimbabwe’s dictator tried it. Eager to spend more money on wars, higher salaries for government officials and luxury for himself, he had his government print more money. But that meant more money pursued the same goods. That caused explosive inflation. Soon, a $2 bag of onions cost $30 million Zimbabwean dollars.

The more money the government printed, the more inflation there was. They eventually even issued 100 trillion dollar bills. Today those 100 trillion bills are worth about 40 cents.

Inflation wrecked lives in 1920s Germany, Argentina and Russia, and in modern-day Venezuela, too.

3. America could simply refuse to pay our debt. But that would betray everyone who invested in America, and bankrupt Americans who bought Treasury Bonds.

Defaulting on your debt wrecks economies, too. When Argentina defaulted, unemployment rose to 21%.

Once you’re deep in debt, no option is good.

How did we get to this point?

Presidents have talked about the dangers of debt for decades. But they didn’t deal with it; they just talked about it.

“We have piled deficit upon deficit, mortgaging our future and our children’s future,” warned Ronald Reagan. “We must act today to preserve tomorrow.”

Bill Clinton said, “We’ve got to deal with this big long term debt problem.”

Barack Obama called driving up the national debt “irresponsible” and then proceeded to do exactly that.

Donald Trump complained that Obama “doubled” the nation’s debt. But now, under Trump’s presidency and the new CARES Act, our debt will grow even faster.

This will not end well.

So far, the deficit spending hasn’t done enormous harm. But it will. You can stretch a rubber band only so far, until it breaks.

Our debt will wreck our children’s lives.

Yet, today politicians mostly talk about spending more.

* * *

John Stossel is author of “Give Me a Break: How I Exposed Hucksters, Cheats, and Scam Artists and Became the Scourge of the Liberal Media.” For other Creators Syndicate writers and cartoonists, visit www.creators.com.

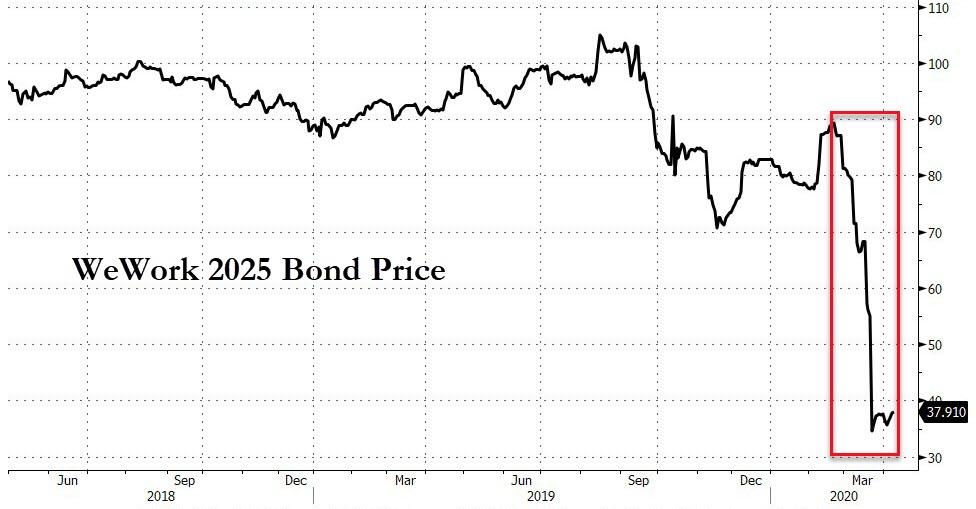

WeWork Has Stopped Paying Rent On Multiple Locations

Amid asset sales, boardroom battles, and seemingly endless litigation, WeWork has decided to jump on the “well, why should we have to pay according to a signed contract when no one else is” bandwagon and is reportedly skipping rent payments on numerous properties.

Amid an effort to aggressively cut costs as the economic downturn crushes any revenues, The Wall Street Journal reports, according to people briefed on the matter, that WeWork has yet to mail in its April rent check at numerous properties while it tries to renegotiate leases. (Quick aside – WeWork mails in its rent-checks?)

“WeWork believes in the long-term prospects of our locations and our relationships with landlords across the world,” a WeWork spokesperson said in a statement.

“Rather than implementing a companywide policy on rent payments, we are individually reaching out to our more than 600 global landlord partners to work in good faith towards finding asset-specific solutions that benefit all parties involved.”

WeWork isn’t treating all landlords the same. While some reportedly say they have been paid, others say they are still waiting for their checks.

One glance at the company’s bond price tells you all you need to know about the cash situation at this once almost $50 billion market cap mockery of an office space company.

Bloomberg’s Gillian Tan reports that WeWork executives have been pitching solutions including revenue-sharing agreements. Such deals would give landlords the chance to collect a portion of future revenue generated by each property. Early indications are that landlords are reluctant, people with knowledge of the matter said last week.