S&P Futures Surge 20 Points In One Tick On $2BN MOC Buy Imbalance

In a mirror image of yesterday’s last 10 minutes action, when the S&P dumped by 40 points in seconds, when a $2.4BN “market on close” sale imbalance was announced at 3:50pm ET…

… moments ago, at exactly 350pm again when the market on close imbalance was unveiled, and revealed that there was $2 billion left to buy, the Emini future (i.e., the S&P500) spiked higher by 20 points, from 2,732 to 2,752, which was also the session high as algos scrambled to frontrun the residual buy orders in the last minutes of trading.

As a reminder, this is at least the 4th time in the past two weeks – it started on March 26 – that the MOC imbalance announcement has led to a stunning move in the market, a striking phenomenon which is attributable to one simple thing: there is absolutely no liquidity in the market, and as a result the headline MOC announcement is sufficient to send the entire market surging or tumbling just due to the end of day rebalance, which as we reported last night, is now wreaking havoc on both option pricing and realized volatility.

Nelson Peltz’s Trian Partners Down 16% In March As Unhedged Bets In Food & Beverage Slammed

Nelson Peltz and Trian Partners were amongst those not “immune” to the coronavirus impact on markets to start the year, with his portfolio taking a 16% hit in March alone.

Year to date, it puts the asset manager down nearly 25%, far exceeding the S&P’s nearly 18% drop YTD, according to Bloomberg. Trian investments General Electric and Proctor and Gamble saw their shares drop 37% and 9.7%, respectively, for the year.

Trian also owned shares of food distributor Sysco, which fell disproportionately to the rest of the market as its customer base shut down across the U.S. and Europe. Sysco shares are down 46% on the year and the company has since said it’s going to suspend its share buyback program. It also drew down $1.6 billion of a $2 billion credit line.

Trian is also the largest holder in Wendy’s, which is down 33% from the beginning of the year. Wendy’s also suspended its share buyback program.

One of the Trian’s newest investments, plumbing equipment maker Ferguson Plc, is also down about 26% this year. Trian expects that things could get worse, stating that Ferguson’s business could be “significantly impacted” by the ongoing lockdown.

Trian said: “Despite the current economic disruption caused by Covid-19, we believe that Ferguson is positioned to withstand a market downturn and continue to believe it will generate attractive returns over a long-term holding period.”

Specifically, Trian’s “long only” focus and “lack of hedges” makes the fund more vulnerable than usual when markets turn lower, Bloomberg noted.

Peltz joins a long list of big name investors who, despite being heralded as geniuses during an 11 year Fed-induced “bull market”, were unable to predict or mitigate the impact of the coronavirus on markets.

In mid-March, for example, we reported that Ray Dalio’s macro fund was crushed 20% when the market crashed weeks after Dalio claimed “cash is trash”.

Morgan Stanley Spots Something Very Strange About This Rally

Following an earlier note from Morgan Stanley’s quants which observed that the rally in stocks and the plunge in the VIX has been abnormally fast for a country sliding into a deep recession, something which Reuters picked up on later in the day…

… a follow up report has found something outright bizarre about the current bear market rally: namely, that while both the S&P the SX5E rally from 2300 to 2600 lacked participation, it was even worse beyond 2600. In other words, not only is there no buying, but there isn’t even short covering or forced “stop outs.”

Among the observations highlighted by the bank, there has been:

ZERO HF re-grossing (fundamental or systematic)

ZERO covering of the $33bn net short in Futures (and volumes falling)

ZERO new build in call ownership (and volumes falling).

Furthermore, the moves have been “gappy” and there is little evidence investors are being “stopped in.” And while the improving virus-related data and some optimism about exit-strategies had put a floor on the market, the economic impact (as yet unknown) remains a major headwind for bullish flow and Morgan Stanley expects the SX5E to be in a range between 2400-2900 for the time being.

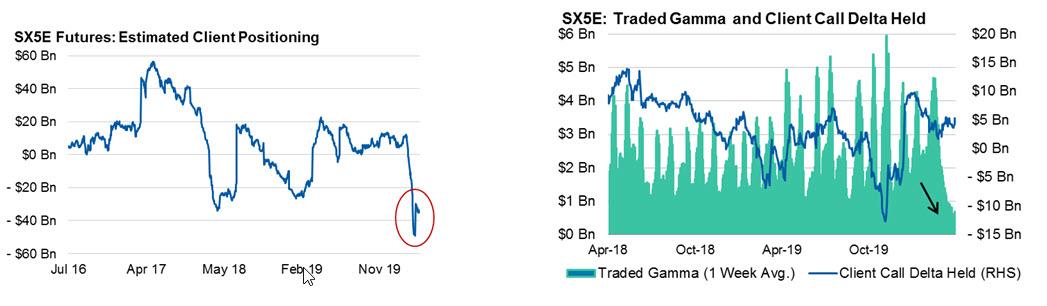

Some more details: on Monday, SX5E spot rallied +5% but for a move >4.5% it was the lowest volume rally since 2010 (sample size = 10 days). Meanwhile, the participation on the way down was ~3x larger than on the way up (left chart below), a legacy pattern observed when either central banks or stock buybacks are the dominant buyers of stock.

At the same time, on the cash side, hedge fund re-grossing simply isn’t happening, and historically, as long as HF P&L Volatility remains greater than 7v, re-grossing is unlikely (10 day HF P&L vol is 18v, 30 day is 14v).

Going further back, the 2300 to 2600 rally saw at the end of March a lot of short covering in SX5E futures (~$20bn worth) but beyond 2600 Morgan Stanley estimates clients actually started to re-hedge adding ~$2bn of net new shorts., We estimate total outstanding short balances (net) are now -$35bn (left chart below).

Another remarkable observation: the “digging in” on the short futures is linked to a lack of options activity. Tactical Put and Call volumes continue to drop, with on average just $550MM/day of gamma trading in the last week (lowest in 2Y, right chart below). In delta terms, call volumes are now 60% below the March peak of $14bn/day, Put volumes are 90% lower vs. the $40b/day March peak.

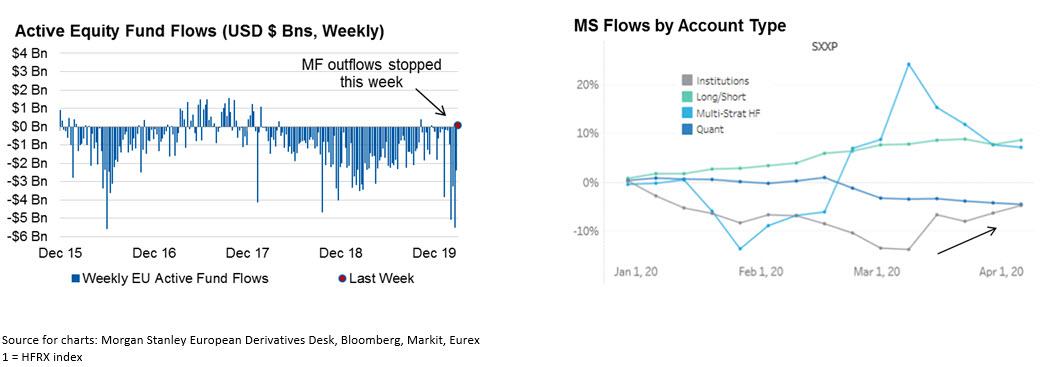

There was one bright spot in all the confusing flows: after a record $17BN of Actively Managed EU Equity Funds saw redemptions in March, the first week of April saw that come to an end indicating that supply from retail investors is slowing, at least in the near term.

One final note: we previously flagged that systematic accounts were the quickest to de-lever: the last 2 weeks of Feb were the biggest outflows since 2014, coinciding with a period where Quantitative directional funds P&L fell -7%. And while systematic flows are still mildly negative but have slowed sharply since (right chart below), the one group net accumulating equity over the past 2 weeks are Real Money/Institutional Accounts (bottom right chart).

Google Bans Zoom Software From Company Computers Over Security Concerns

Zoom has had quite a ride over the past few weeks, from darling WFH stock to virtually a piece of malware, as we declared earlier, especially now that attorneys general from at least 27 states have either raised questions or requested more information from Zoom about alleged privacy lapses that look more like negligence – or worse, greed.

And now, Buzzfeed reports that Google has banned employees from using Zoom on company laptops and computers because of the security risks associated with the software, according to internal company emails.

It’s unclear why Google allowed employees to use Zoom on company equipment since Google has its own competitor app, Hang. The app has become wildly popular during the quarantine, as people have used it to do “virtual hangouts” including happy hours and workout sessions.

But though Google of course has an ulterior motive, this certainly isn’t a vote of confidence, and if more companies follow suit, that could be all she wrote for Zoom.

FDA Fast-Tracks Promising COVID-19 Treatment From Johns Hopkins

While the use of hydroxychloroquine to treat COVID-19 has dominated headlines for weeks, a new method of treatment developed by Johns Hopkins Hospital has just been given special approval by the FDA to be fast-tracked.

Known as convalescent serum therapy, the antibody-rich blood plasma from COVID-19 survivors is drawn, bagged, and given to critically ill patients.

While the FDA began allowing limited use of the therapy on March 24 for hospitals in Houston and New York City (with an “expanded access program” pending), Johns Hopkins is concurrently developing the therapy with the goal of preventing otherwise healthy front-line medical staff from getting sick. The university is awaiting FDA approval for a second clinical trial on patients who are slightly to moderately ill to see if it can reduce or eliminate COVID-19.

Under the leadership of immunologist Arturo Casadevall, the Johns Hopkins team is collaborating with physicians and scientists around the country to establish a network of at least 40 hospitals and blood banks in 20 states for the collection, isolation, and processing of blood plasma.

People who recover from an infection develop antibodies that circulate in the blood and can neutralize the pathogen. Researchers hope to use the technique to treat critically ill COVID-19 patients and boost the immune systems of health care providers and first responders. Currently there are no proven drug therapies or effective vaccines for treating the novel coronavirus.

“At the end of January, I knew this disease was going to get out of China, and I knew there was a huge history of the use of plasma and serum in the 20th century,” says Casadevall, a Bloomberg Distinguished Professor of molecular microbiology and immunology and infectious diseases at the Johns Hopkins Bloomberg School of Public Health and School of Medicine. “This [medical effort] has become a juggernaut… We’re racing to deploy this.”

Thousands of survivors might soon line up to donate their antibody-rich plasma, according to physicians. But that’s only if early promising studies on the therapy done in China are confirmed by U.S. trials that show “dramatic effects and improvements” in patients, according to Tobian. He is optimistic the therapy will do just that. “I absolutely think this could be the best treatment we have for the next few months.”

This passive-antibody therapy has been used since the 1890s to combat diseases as wide-ranging as measles, SARS, Ebola, H1N1 flu, and polio—and holds the promise of keeping the virus at bay until a vaccine can be developed. (Current estimates are that a vaccine for emergency use could be available by early 2021.) During the SARS outbreak in 2002–2003, an 80-person trial of convalescent serum in Hong Kong found that people treated with it within two weeks of showing symptoms had a higher chance of being discharged from hospital than did those who weren’t treated.

The beauty of the therapy, says Casadevall, is that it involves the well-established—and safe—method of blood donation. Except in this case, survivors’ plasma (or serum), which contains the antibody to COVID-19, is separated from red blood cells and transfused into the three categories of recipients: the critically ill as a last-stop “compassionate care” measure; patients who are slightly or moderately ill to keep them out of ICUs and off scarce ventilators, and front-line medical workers to prevent them from getting sick. Nearly a cup of the serum (200 milliliters, or one unit) would be administered to each recipient, according to Tobian, with each donor providing enough serum for up to four patients. (Each donor, depending on body size, can provide two to four units.)

Casadevall had the vision for this treatment. He also had the wisdom not to micromanage his team of doctors, whom he set free to create their own fast-flowing mini-teams. Together, they united with peers around the world in a marathon of selfless, round-the-clock work toward an urgent common goal—to overwhelm and crush the COVID-19 virus. “Looking forward to another day of working with an incredible set of colleagues,” tweeted Casadevall in late March. “Day began at 4 a.m. and will go to near midnight.” In this process, doctors, researchers, and regulators from as far away as Israel and Ethiopia banded with Hopkins doctors to create treatment protocols, open labs, win regulatory and institutional approvals, identify donors, compile data, and organize and share vital information. The research effort received a welcome boost in late March with a gift of $3 million from Bloomberg Philanthropies and $1 million in funding from the state of Maryland.

From the beginning, Casadevall knew he faced more than a medical problem. Plasma therapy’s history was unknown to most people, so he needed to draw public attention to his cause. Realizing a medical journal commentary would reach a limited audience, Casadevall shopped around an editorial that urged the use of convalescent serum. The essay, published in the Feb. 27 edition of The Wall Street Journal, told the story of an ingenious Pottstown, Pennsylvania, doctor who in 1934 arrested a measles outbreak at a boys boarding school by using serum therapy. “A remarkable victory against a highly contagious disease,” Casadevall wrote.

Casadevall fired off the essay to dozens of colleagues who encouraged him in his plan to also publish a scholarly paper that conveyed sufficient technical information to prove to the medical community he had done his homework. In four days, he and long-time collaborator Liise-anne Pirofski, head of the infectious diseases department at the Albert Einstein College of Medicine in New York City, wrote what Casadevall calls “maybe the most important paper in my life”—’The Convalescent Sera Option for Containing COVID-19,’ which appeared in the Journal of Clinical Investigation on March 13. Written in the cool, precise language of clinical experts, the paper concluded, “We recommend that institutions consider the emergency use of convalescent sera and begin preparations as soon as possible.” But its final sentence carried a sharp and decidedly unscholarly sounding warning—”Time is of the essence.”

The result? “Everything took off,” says Casadevall. “Its publication coincided with the major increase in cases in the United States. The media jumped on it.”

Had it not been for a tropical pet bird whose guano infected its owner in 1995, Casadevall’s path might never have crossed with that of infectious disease specialist Shmuel Shoham, an associate professor of medicine at the School of Medicine. “That was how we bonded,” recalls Shoham, who hammered out the first protocol for the treatment of potential COVID-19 patients.

Back then Casadevall was at Albert Einstein in the Bronx while Shoham was at Boston University, but thanks to a mutual friend, they co-authored a ground-breaking paper in the Annals of Internal Medicine that was picked up by The New York Times. Their research proved the hitherto unknown link between human fungal illness and “cockatoo poo,” as Shoham puts it.

Over the years, their careers took them to different cities and in separate directions, but when Casadevall arrived at Hopkins five years ago, they renewed their friendship and became key collaborators again. In mid-February, when Italy reported mounting cases, Shoham began thinking: “If there’s a hole in the boat, it doesn’t matter if it’s on my side or your side, we’re all going down. If this is happening in Italy, there is absolutely no reason why this could not happen in Baltimore.” Then he saw a tweet from Casadevall: “Plasma is going to be the solution.” At first, Shoham pushed back, saying the therapy hadn’t worked on influenza patients. But those patients were too ill, Casadevall replied, and in a flurry of back-and-forth tweets, he won over his colleague to his point of view.

With the virus beginning to rage in the U.S., Casadevall convened a 7:30 a.m. conference call on March 4, five days after his WSJ op-ed appeared, with a group from Hopkins’ Division of Infectious Diseases. Shoham hopped on the call while driving to work. “I told them we had to do [something],” Casadevall recalls. “This was something that was just not on the radar screen. There was silence, and I said, ‘We’re going to need a protocol.'”

Shoham volunteered to write it. Although he typically spends two-thirds of his time with patients, by fortunate happenstance he had few patients on his calendar, and that gave him time to dive into COVID-19. By the next day he had pounded out the bare bones of a protocol to prevent infection by administering the plasma to those who had been exposed. “It was sort of a really messy protocol with highlights like a ‘This Space Left Intentionally Blank’ place holder,” Shoham says. He finished a more detailed, but still rudimentary, draft in time for Casadevall’s next conference call a few days later.

Casadevall fired off the protocol to a Mayo Clinic colleague, who converted it into one for the treatment of early-to-moderate disease, which Hopkins doctors further refined and revised in collaboration with Mayo doctors. This pattern of rapid, long-distance collaboration would be repeated endlessly among other doctors for other needs in the days to come.

“All of a sudden, centers all over the country were saying, ‘Oh, my God, this is something we can do.‘ So, then we had big conference calls with dozens of centers,” says Shoham, who is now the FDA’s principal investigator for the prophylaxis study, which makes him responsible for all execution and oversight of clinical research on that protocol.

The team had to know how to collect donor serum and how to transfuse it. So, pathologist Tobian and his colleague Evan Bloch, an associate professor of medicine, came aboard. Today, Tobian and Bloch help lead the transfusion group. “We get emails every single day from other hospitals on how we start collection, how we work on the regulatory aspects,” Tobian says. “And we’re in touch with transfusion medicine physicians across the nation numerous times a day.” The pace has been “crazy,” adds Bloch, a specialist in neglected infectious diseases.

In a sign of these high-tech times, Casadevall has never met either man. “I don’t even know what Evan Bloch looks like,” he says, “and I talk to him all the time. These men are magnificent. They rise to the occasion.” In-person meetings happen but are mostly regarded as “a luxury” they can’t afford because they would put people at risk, says Shoham.

To analyze the serum, Casadevall called in Pekosz. Until March, Pekosz, a basic researcher, had not thought he would be so directly involved in such an effort. But after Casadevall shared his plans, Pekosz realized some of his work could support the need to measure antibodies in the blood before transfusions were done.

“It became a whirlwind, a tornado we got swept up in, part of a massive effort to treat patients and make a direct impact on the pandemic,” says Pekosz. In late March, Casadevall emailed Pekosz to say Vice Provost for Research Denis Wirtz had provided $250,000 in funding to launch a new lab to assess COVID-19 antibody responses in serum earmarked for the hospital’s patients.

Arturo Casadevall

“Arturo said I needed to set up a lab to do this because this may be a really daunting task in terms of the number of patients we want to treat,” Pekosz recalls. “At that point, I really understood, ‘Wow, this is going to be a beast unto itself.'”

A big piece of Pekosz’s job—besides supervising six new lab employees, a staff that may soon double—entails advising other hospitals on how to proceed. “I can’t even remember the number of institutions that have contacted me who want to do the same thing. We’re trying to work with them to be as close to each other’s test results as possible, so we can have consistency across sites.”

After Casadevall’s initial burst of enthusiasm and organizational action, he confesses there was a moment when things seemed dark. “You realize the magnitude of what you’re trying to do, and, in particular, you realize there could be huge regulatory issues,” he says. He reminded himself that projects like this had been done by prior generations and in other countries, and with determination, he says, “I never for a minute doubted we could pull it off.“

The FDA’s approval process is a two-edged sword, according to Shoham, who says one of the biggest issues is the regulatory environment. Seemingly antiquated FDA requirements have sometimes left doctors shaking their heads. A submission of an IND (the application for an investigational new drug) is not official unless it is physically mailed with numerous copies of paperwork. “We could have sent an email [with PDF attachments],” says Tobian, referring to an IND that Hopkins prepared. “Instead we [were] trying to find who can make all these photocopies and send a FedEx package, and everyone’s mostly been told they need to be working from home.”

Nonetheless, neither he nor Casadevall believes the old-fashioned delivery system slowed the FDA’s decisions or their work. “The FDA has an impossible job,” Casadevall says. “I would never criticize them. They are working really hard. Their job is safety, and our job is to get this done.”

Lysander, the Spartan admiral who conquered Athens in 405 B.C., is Casadevall’s hero. “He did something that was unheard of at the time,” Casadevall marvels. “He spared the city, and by sparing the city, he preserved Athens.

“To me, my heroes are always humanists—people who do their job, but there is a humane aspect to how they do it,” he says. “The greatest thing about being human is the capacity for empathy, the ability to care for others and be optimistic in the worst of times.”

Casadevall’s team lavishes praise on his leadership. “He is a force of nature,” says Shoham. Brilliant, charismatic, enthusiastic, and generous is how Bloch describes him.

“Arturo pulled off what few people could do,” Pekosz adds. “He got multiple institutions across the nation to pull together in this project to create the momentum that led the FDA to say, ‘We have to do this, because people are moving forward.’ There was such a groundswell of enthusiasm for this approach, the FDA had to pay attention to us.”

For most of the team, there’s been little rest for weeks. When asked how much sleep he’s been getting, Bloch replies, “Last night wasn’t bad—about four to five hours. It’s just continuous work through weekends, through nights.” What drives him is partly the worst-case scenario forecasts he reads which he says are “frightening. … You’re thinking about the people in the background—the health, social, and economic impacts. Having insight into what is going on can be a little bit stressful.”

“There isn’t going to be a day off for many, many months,” Casadevall says.

People in medicine often think about delayed gratification, according to Shoham, because they never know whether some bit of knowledge they possess today might be needed tomorrow for an unforeseen reason.

“We’re not thinking about the next thing,” he says. “This is it. This is the one.”

Results from the trials in the two New York City hospitals are expected around the end of April. How widely serum therapy is used after that for the time being remains unclear.

“We want now to get the clinical trials done,” Casadevall insists. “Compassionate use is going to be available [in the trials]. Convalescent sera is going to be used in the country, there’s no question about that. It’s already been deployed in Europe. I think the next task is to learn if, when, and how to use it, and for that, we have to do clinical trials.”

The Red Cross is seeking people who are fully recovered from COVID-19 and may be able to donate plasma to help current patients with serious or immediately life-threatening COVID-19 infections, or those judged by a health care provider to be at high risk of progression to severe or life-threatening disease. For more information, visit the website of the American Red Cross.

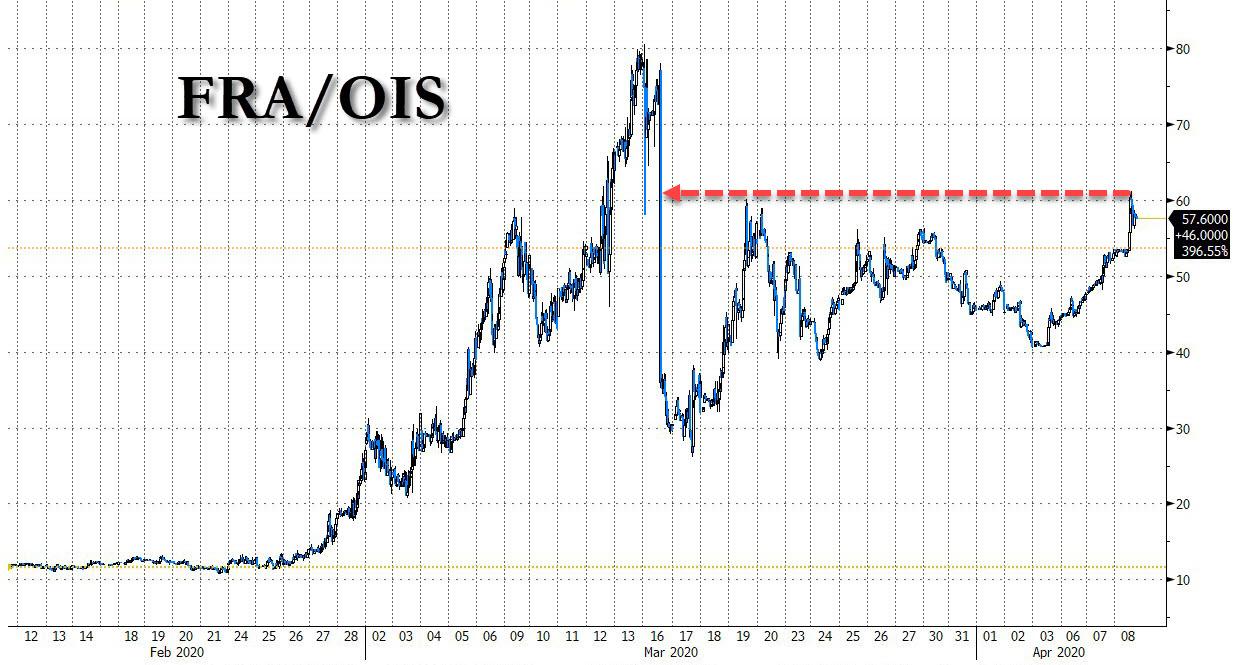

The Liquidity Crisis Is Quickly Becoming A Global Solvency Crisis As FRA/OIS, Euribor Soar

One month after turmoil was unleashed on capital markets, when the combination of the Saudi oil price war and the sweeping impact of the coronavirus pandemic finally hit developed nations, what was until now mostly a liquidity crisis is starting to become a solvency crisis as more companies realize they will lack the cash flow to sustain operations and fund debt obligations.

As Bloomberg’s Laura Cooper writes, cash-strapped companies are finding little relief from stimulus measures, and from Europe to the US, cash in hand has been hard to come by even as governments pledge funds for small businesses to bridge the financial gap until lockdowns are lifted:

US: The March NFIB survey of U.S. small businesses noted challenges in submitting loan applications and the urgent need for federal assistance

UK: A British Chamber of Commerce survey showed only 1% of companies reported being able to access funds dedicated for business. A complex application process for the U.K. Coronavirus Business Interruption Loan Scheme comes as 6% of U.K. firms say they have run out of cash while nearly two-thirds have funding for less than three months

Canada: A proposed six-week roll out of emergency funds is unlikely to prevent 1 in 3 companies from laying off workers. More than 10% of the labor force has already filedemployment claims

Europe: existing structures are aiding in the deployment of funds, but concerns remain that more is needed with EU leaders failing to reach agreement on further initiatives

As we have noted previously, small businesses – everywhere from China, to Europe, to the US – make up the majority of firms in advanced economies and account for a sizeable share of private sector employment. Quick delivery of stimulus measures is needed to curb widespread insolvencies. This could mean the difference between a short, yet sharp recession and a prolonged erosion to the labor market and economy regardless of containment of the health crisis.

Meanwhile, as we get increasingly more urgent reports that the lack of available funding is starting stress corporate solvency, liquidity itself is getting worse, and on Wednesday the closely watched June FRA/OIS – an indicator of intrabank funding stress – spiked, reaching 61.2bp, the highest level since its March 16 collapse after the Fed’s emergency rate cut.

The spread was as much as 6.5bp wider on the session with most of the move occurring after 3-month dollar Libor fixed 0.85bp lower than Tuesday at 1.31138%, its third straight decline.

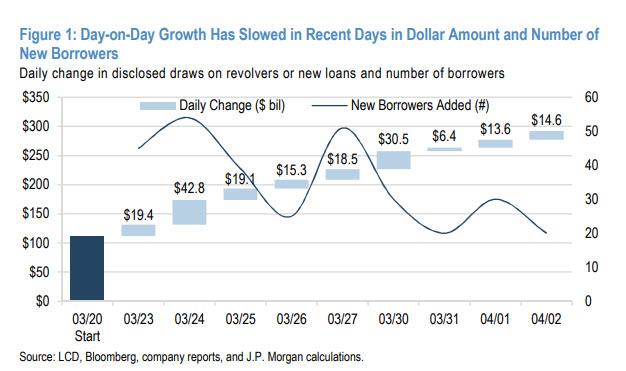

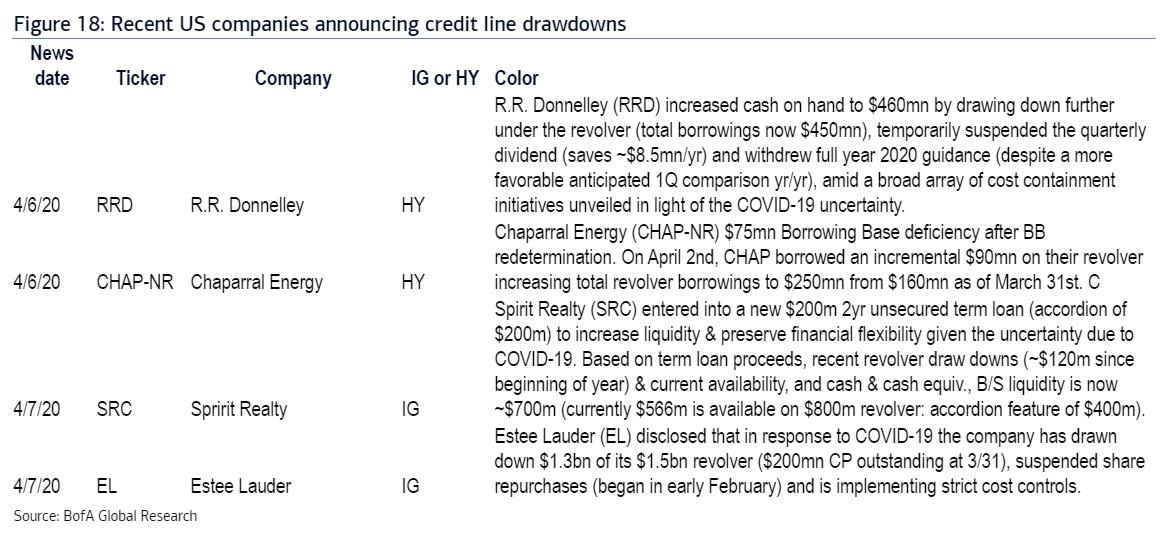

One possible reason for the accelerating shortage of bank liquidity is the sharp rise in demand from corporates, which as we reported over the weekend, has manifested itself in a record $293BN in credit facility dradowns as of last Thursday…

… a number which has only risen following several prominent revolver drawdowns so far this week.

At the same time, coupled with the fact that some investors have been borrowing in euros and swapping them into the dollars, euribor’s rise to the highest since May 2016 was also inevitable, and as of Wednesday morning, the three-month Euro Interbank Offered Rate advanced a third day to minus 0.254%.

The increase comes despite the European Central Bank relaxing its collateral rules on Tuesday, which didn’t really channel “new money” to banks, according to Frederik Ducrozet, global strategist at Banque Pictet & Cie.

As Bloomberg adds, there’s also evidence in European markets that corporates are stockpiling cash. Not only did the three-month Euribor climb 3.9 basis points to minus 0.254%, but its spread over OIS rates jumped to over 20 basis points, the highest since 2014. It also signals companies have increased their activity in funding markets over the past month.

At the same time, accessing cash in Europe’s commercial paper market is becoming more expensive for corporates. There’s been a modest widening of where new issues in commercial paper markets are pricing.

There was some good news: 3-month A1/P1 rated commercial paper rates dropped another two basis points on Tuesday, a fourth consecutive decline. Spreads over OIS tightened as volumes and activity in the underlying markets improve. That suggests current Fed measures are supportive and the prospect of looming Commercial Paper Funding Facility on April 14 is boosting sentiment.

Country after country has reported extremely dark economic numbers. The gigantic jobless claims, 6.6 million from the U.S. last week, are just the tip of the iceberg. For example, the service sector PMIs have been simply ghastly across the globe. We are now in a crisis of epic proportions.

But, how massive can the crisis eventually get? Since our inception, in 2012, we have contemplated three scenarios as a part of our quarterly forecasts. While we have not referred to them in each report, we have repeated them periodically. They are: the optimistic, the most probable and the pessimistic.

But at this point our main worry is the approaching realization of the pessimistic, or the worst, scenario. It’s likelihood, while still low, is increasing fast in our estimate.

Underpinning its severity is not the virus, but the fragility of the global economy.

Breeding chaos: failed clean-ups and bad policies

The Global Financial Crisis (GFC) was considered a Black Swan event to many. However, it was no such thing. It was a massive failure of hedging and diversification within the global banking system, most notably in the U.S., and a number of prominent analysts saw it coming. See our blog, 10 years from Lehman. And nothing has been fixed, for an insight view on that crisis.

While banks were wound down and recapitalized in the U.S. after the GFC, an equivalent restructuring did not happen in Europe. Stricken European banks were left to linger in a state of permanent financial distress.

“Outright Monetary Transactions” or “OMT”, negative interest rates, and ECB’s QE program all aggravated the predicament of European banks. The failure to resolve the 2008 crisis ‘zombified’ the European banking sector, a situation which persists today. (See Q-Review 3/2019 for a detailed account).

Another pivotal moment for the world economy came in March of 2009, when the Fed vastly expanded its asset purchase program of U.S. Treasuries and mortgage-backed securities. This became known as the notorious Quantitative Easing or “QE” program, and has persisted in one form or another ever since. (See Q-Review 1/2018 for a detailed explanation.)

Central banks quickly assumed the role of “lender of first resort” in the capital markets, and their balance sheets ballooned. Asset prices rose to never-before-seen heights. Continuous market bailouts, culminating in the ‘pivot’ of the Fed in early January 2019 and its repo-bailout in September, removed all market discipline and incentivized investors to wild speculation (see Q-Review 4/2019 for details).

The giant with (debt) clay feet

Chinese leaders also reacted quickly when the financial crash of 2008 precipitated a global recession.

China initiated a massive infrastructure programs that jump-started the world economy to a renewed upward trajectory. These programs were financed by credit issued by state-controlled banks, which Beijing can compel to lend, and the banks responded by doubling the volume of loans YoY. Between 2007 and 2015, 63% of all new money created globally came from China, and most of this increase was created by commercial banks.

During 2016, China unleashed a never-before-seen credit bonanza, tripling the size of the “shadow banking sector” as a response to a slump in the Chinese housing market, which had become the backbone of the Chinese economy over the past two decades.

By the end of 2017, the assets of the shadow banking sector stood at a mind-boggling 367% of GDP. The commercial banking sector has also become extremely levered, posting over 500% growth in credit since 2008.

Alas, the Chinese banking sector is now totally incapable of coping with any significant shock, and these Chinese economy became riddled with unprofitable investments.

Into the Abyss

These fragilities, combined with the massive economic impact of the coronavirus, leads us to our most pessimistic scenario.

In it we assume that

Many governments will not be prudent enough in suppression measures, which will lead to severe global pandemic peaking in summer.

Due to the worsening outbreak and delays in containment, suppression measures will eventually be prolonged and they become draconian (“Wuhan style”).

The massive stimulus measures enacted by governments and central banks will be ineffective in providing support for the economy, as the tardy application of draconian suppression measures lock people at home in several key countries of the global economy for a prolonged period of time.

Global economic activity plunges to never-before-seen lows.

European banking sector breaks.

Eurozone unravels violently.

China ‘lands hard’.

Global financial system collapses.

A systemic crisis engulfs the world.

A systemic crisis simply means that the banking sector and financial markets collapse. In practice, this implies that most banking services will stop and funding through financial markets will cease. This also means that the monetary system is likely to collapse (see Q-Review 4/2019 for a detailed explanation).

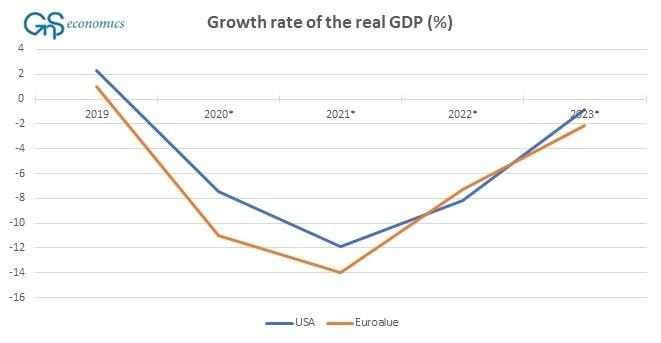

It should be acknowledged that we have never faced such a scenario on a global scale (though the collapse of the Soviet Union could certainly be classified as “systemic meltdown”). That is why the sheer scale of such an apocalyptic scenario will be horrifying. They are presented in the Figure below.

Figure. The forecasted (Y-to-Y) GDP growth rates in the U.S. and in the Eurozone in 2020 – 2023. Source: GnS Economics, OECD

Fragilities laid bare

The Covid-19 pandemic will reveal all the fragilities of the world economy. The near collapse of the U.S. capital markets in mid-March was averted only through unprecedented socialization of the financial markets. However, when the Flood of corporate bankruptcies begins, central banks will not be able to withstand the onslaught. Then we will face only extreme economic options.

The global collapse scenario, presented above, would bring in its wake massive unemployment, poverty, misery and the eventual re-structuring of our whole social and economic order. The world would be utterly and permanently changed as a result.

This is something we absolutely need to be prepared for, even though its likelihood is still relatively low.

But it is increasing fast, and that should worry us all.

Crude Soars, USO Halted After Algeria Says OPEC+ Production Cuts Could Reach 10MMb/d

Crude has exploded higher, in the process triggering a limit up circuit breaker of the biggest oil ETF, the USO…

… following a report quoting the Algeria oil minister that OPEC+ production cuts could reach 10mmb/d when OPEC+ meets in its teleconference call tomorrow.

Why this is news to the market is unclear, as a 10mmb/d cut has been discussed for the past few days as a potential outcome, one which however would require the US to participate in a coordinated global cut. The problem is that the as Ryan Sitton, the Texas Railroad Commissioner at the Texas Railroad Commission, who has quickly emerged as the coordinator behind any potential US production cuts, tweeted earlier that:

I’m not participating in the OPEC+ call tmrw but if I were I’d say at least 20mbpd in cuts are needed & the US will cut at least 4mbpd in next 3 mos organically. If nothing is done inventories fill up in 2mos, at which point the world will need to cut as much as 30mbpd.

I’m not participating in the OPEC+ call tmrw but if I were I’d say at least 20mbpd in cuts are needed & the US will cut at least 4mbpd in next 3 mos organically. If nothing is done inventories fill up in 2mos, at which point the world will need to cut as much as 30mbpd. #OOTT

Separately, RBC reported citing an unnamed person close to the Russian Energy Ministry, that Russia is ready to cut 1.6mmb/d in production (equivalent to 14% decrease from 1Q levels). However, as above, Russia’s condition is that non-OPEC countries would also be expected to take part in cuts including U.S. Brazil, Norway, Canada, Mexico, RBC says citing Energy Ministry.

And, as Sitton tweeted earlier, that is unlikely to happen especially since the US won’t even have a representative on the OPEC+ call.

Finally, as Goldman’s commodity analyst Damien Couravlin writes, even if a deal is reached and 10mmb/d in production is removed, this would not be nearly enough, and that any further cuts beyond 10mmb/d won’t happen as the “incremental burden would likely need to fall on Saudi Arabia to be effective.”

While the US announcement of production cuts last week was premature, many countries have since commented on their desire to participate, and we believe that a coordinated cut is now more likely than not. Assuming that a deal is reached, which is in no way certain, the key question will be whether its size and timing will improve global oil balances sufficiently to support prices above current levels.

Our updated 2020 global oil balance suggests that a 10 mb/d headline cut (for an effective 6.5 mb/d cut in production) would not be sufficient, still requiring an additional 4 mb/d of necessary price induced shut-ins. While this argues for a larger headline cut of close to 15 mb/d, we believe this would be much harder to achieve, since the incremental burden would likely need to fall on Saudi Arabia to be effective. Further, our price modeling suggests that Brent prices near $35/bbl already reflect such an outcome, with last week’s rally having brought crude prices to levels that likely slow the large-scale US production drop that are necessary to a deal in the first place.

Net, while the prospect of a deal can support prices in coming days, we believe this support will soon give way to lower prices with downside risk to our near-term WTI $20/bbl forecast. Ultimately, the size of the demand shock is simply too large for a coordinated supply cut, setting the stage for a severe rebalancing. While the path of the demand normalization will remain key to the subsequent price recovery, lasting supply cuts will matter too and could create upside risks to our $40/bbl October Brent forecast.

In short, anyone hoping that today’s oil spike will persist, will likely be disappointed.

* * *

Finally, in case anyone missed it earlier, here again is a preview of what Wall Street expects from tomorrow’s meeting, courtesy of RanSquawk:

SCHEDULE: The delayed OPEC+ webinar on Thursday will arguably be the most important gathering of ministers to date, with countries outside OPEC+ also poised to potentially tune into the discussions, thus presenting scope for coordinated action. The meeting is due to commence at 15:00BST, with a presser to follow – all times tentative, OPEC+ pressers tend to be delayed. This will be followed by a G20 Energy Ministers’ meeting on Friday, expected to start at 13:00BST. Argentina, Brazil, Canada, Colombia, Egypt, Indonesia, Norway, the UK, the US, and Trinidad & Tobago have also been invited to partake in Thursday’s meeting, although at pixel time, not all are confirmed to attend. Sources said no one from the Trump Administration was expected to attend Thursday’s call. Saudi and Russia have called for other global producers – namely the US, Canada, and Mexico – to share the burden of cuts.

KEY PLAYERS

OVERALL RHETORIC: Russia and Saudi have blamed each other for the collapse in oil prices. The two sides agreed to discussions following US President Trump’s recent intervention but made it clear that any cuts will have to be “fair”, and a joint global effort.

SAUDI (12MLN BPD OUTPUT IN APRIL): The Kingdom is mulling an output cut to beneath 9mln BPD on the condition other oil members join in. A Saudi official said if there was no deal, “we will have some nice number of floating tankers going nowhere”.

RUSSIA (11.29MLN BPD OUTPUT IN MARCH): Moscow’s participation is highly contingent on the US, and is unlikely to agree to output cuts if the US does not join the effort; separate reports said Russian producers are ready for oil curbs on the same proviso. Indeed, the CEO of The Russian Direct Investment Fund was optimistic, stating that Riyadh and Moscow are near an accord. The Kremlin has declined to signal Moscow’s position ahead of the meeting.

US (13MLN BPD OUTPUT AT END-MARCH): The US has leaned back on calls to commit to cuts. President Trump said he did not make concessions during talks with Saudi and Russia and has not agreed to a US domestic production cuts. Further, he said US producers have already cut back as a reaction to the market. Meanwhile, US independent oil producers reportedly have told OPEC that they will voluntarily cut output, but US oil majors worry about the antitrust issues around any coordinated effort.

OTHER PRODUCERS

BRAZIL (3.06MLN BPD OUTPUT IN FEBRUARY): State-owned Petrobras said it will curtail production by 100k BPD, according to a statement in March.

CANADA (5.78MLN BPD OUTPUT IN FEBRUARY): Alberta’s Energy Minister stated that the country will take part in the talks and will “keep an open mind”. A senior government official downplayed any suggestions that the country will go along with further production cuts. NOTE: Alberta, like Texas in the US, has the regulatory framework to force producers to curb supply.

NORWAY (2.07MLN BPD OUTPUT IN FEBRUARY): Norwegian Oil Ministry stated that it would consider partaking as an observer if there was broad participation but said, at the time, that there are no ongoing talks with oil companies on cuts. For reference, the country produces less than 2% of global supply.

PROPOSED CUTS

DURATION OF CUTS: Delegates has said that current options being considered range from a 10mln BPD cut to no reduction at all, with a three-month agreement being considered, according to some reports. Some question whether a three-month deal would be sufficient to balance the market. The pact could be extended, but may face resistance from Russia and US, and could be highly contingent on market conditions at the time. Separate reports noted proposals for a year-long agreement.

TOUTED SCENARIOS: Two scenarios will reportedly be put forward: 1) OPEC+ would no longer bound by production restrictions, which would see a continuation of the current situation. 2) OPEC alongside Russia and other producers would implement joint 10mln BPD reductions through to the end of the year. A separate report touted a joint 10mln BPD cut which would see the involvement of the US, Canada, and Brazil. The cuts will be distributed as follows: Saudi would cut a minimum of 3mln BPD from current levels, Russia 1.5mln BPD, Non-Saudi Gulf 1.5mln BPD, US, Canada, and Brazil almost 2mln BPD with Texas at least 500k BPD.

BASELINE: It is unclear which production month will be benchmarked in any cuts. This set level could prove to be significant given Saudi’s output hike. OPEC sources said there is a rift between Moscow and Riyadh regarding which baseline to use, with latter calling for the current production environment to be used as the base line.

HOUSE CALLS

Analysts at Credit Suisse outline five potential outcomes from the meetings:

1) NO OPEC+ DEAL (5%): Russia and Saudi talks will break down – Brent could be pushed lower to ~USD 20/bbl

2) NO US DEAL (20%): If the US refuses to partake, Russia and Saudi will also ditch talks – Brent could be pushed lower to ~USD 20/bbl

3) A “LARGE” DEAL (20%): around 15mln BPD cut from current levels supported by OPEC+, US and other producers for at least three months with possible extension – Brent could rise to around USD 35-40/bbl.

4) A “SMALL” DEAL (35%): Immediate OPEC+ cuts of 12-13mln BPD; US offers mild reductions in Gulf of Mexico and Shale output and the purchase of oil for the Strategic Petroleum Reserve (SPR) – Brent could see USD 30-35/bbl.

5) AN “EVEN SMALLER” DEAL (20%): US relies on natural output reductions and offers to purchase around 0.8-1.0mln BPD for the SPR. Brent could meander below USD 30/bbl with scope for a rise to ~USD 35/bbl should US production markedly decline naturally.

TARIFFS:

US President Trump on the weekend said he was considering slapping tariffs on oil imports, or even take other such measures, to protect the US energy sector from falling oil prices. For reference, the US imports of petroleum were around 9.1mln BPD in 2019, of which Saudi and Russian imports were just over 500k each.

G20 ENERGY MEETING:

The fallout from the OPEC+ meeting would set the stage for the G20 webinar on Friday. Energy Intel notes members outside OPEC+ will be asked pledge additional reductions, “over and above 10mln BPD”. A Senior Russian source noted that efforts to get the US involved in cuts will be on the agenda for Friday’s call. Desks remain sceptical a deal can be reached at this meeting. G20 members such as South Korea and Japan produce little oil, whilst others such as China, India, and the UK are more reliant on imports.

Following the meeting, Saudi Aramco, UAE’s ADNOC and Kuwait’s KPC are expected to release their OSPs for May.

There seems to be some optimism in the markets that the end of the coronavirus shutdown is getting closer. There is also this resistant myth that the economy will just fire back up at the snap of a finger. Peter Schiff recently appeared on RT Boom Bust along with Christy Ai to talk about the markets and the pandemic.

He said people are still far too focused on the pin and not the bubble that it popped.

The US stock market has had some strong rally days recently with this growing optimism that we could be nearing the coronavirus peak. So, has the stock market found its bottom? Peter doesn’t think so.

Too many people are focused on the pin and are ignoring the bubble that the pin pricked. You know, before the COVID-19 shutdown, the economy was long overdue for a severe recession, and the US stock market was long overdue for a bear market. So, I think the COVID virus simply accelerated the onset of both…

So I would not get excited about this rally. I think we still have a long way to go on the downside. And the economy, I think, is going to be even worse.”

Christy agreed with Peter saying this is not the real bounce and we still have a long way drop. She pointed out that earnings still have a long way to fall and there is a massive unemployment tail from the pandemic.

Peter was asked about the response to the government stimulus package signed by President Trump.

As you would expect, a lot of people are trying to line up for whatever free money the government is handing out. But it’s not free. There’s going to be a heavy price to be paid in terms of the loss of purchasing power of the US dollar as prices respond to all the new money being created.”

Peter said the programs are also doing far more harm than good.

What they are doing is exacerbating the downturn and they are going to push the recovery off even further into the future because the government is basically encouraging businesses that should be downsizing and kind of adjusting their cost structure to the new reality — instead, the government is encouraging them to hold on to employees that they would be better off letting go and freeing up to do something else.

Instead, they are going to keep some employees entrenched in companies that are probably going to end up failing because they refuse to lay off people. And so instead, they are going to have to lay off even more people later.

And I think a lot of these loans are never going to be repaid because even the people that don’t fire their workers, a lot of these businesses are going to go out of business because they didn’t fire their workers and then everybody’s going to be out of a job. And the government is not going to get any money back because the loans have no security and there’s no personal guarantee.”

Christy reiterated that the tail of the coronavirus is very long and will be very long-lasting. It won’t be a V-shaped recovery as many seem to expect. We have both a severe supply shock that is morphing into a demand shock.

On the day of the show, both gold and stocks were in the midst of strong rallies. Peter was asked why gold was up when it seemed to be a “risk-on” day.

I think the risk is inflation. The only thing that’s propping up the stock market is the Fed and other central banks printing money, which is creating inflation. So, you don’t have earnings going for the stock market. All you have is all the cheap money that’s being created. And inflation is much better for gold than it is for the stock market. And so, that’s why both stocks and gold are going up.

But I think eventually, gold is going to be going up much more than the stock market and I think gold is going to be going up even as the stock market rolls over and goes down. So, I think in terms of gold, stock prices are going to continue to fall. In fact, they’re going to fall precipitously regardless of what happens to nominal stock prices because of the massive inflation being unleashed by the Fed and other central banks.”

FOMC Minutes Signal “Profoundly Uncertain” Outlook, Feared Treasury Market Disfunction

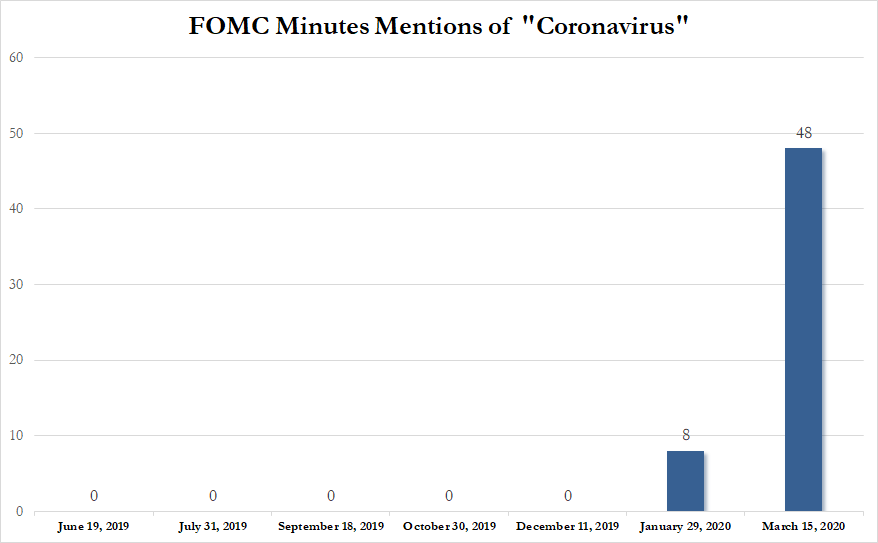

Today’s minutes will provide detail on the Fed decisions announced on March 3 and March 15 after Fed Chair Jerome Powell convened emergency meetings as the scale of the pandemic and its risk to the U.S. economy became clear. The readout may also include their discussions of a slate of related actions that flowed from those two meetings.

Amusingly, just five weeks before the surprise rate cut on March 3, Powell and his colleagues had wrapped up their first meeting of the year on Jan. 29 with an air of cautious optimism.

Since that emergency rate-cut (and the bazooka of all bazookas), The Dow is down around 9% and somewhat interestingly, the dollar, gold, and the long-bond are all up around 4%…

Source: Bloomberg

And at the same time, the volume of beta that The Fed will inevitably cut rates below zero has also surged…

Source: Bloomberg

As a reminder, today’s minutes may show just how dire a threat officials saw in those earliest moments and what spurred them to action.

The first move came on Feb. 28. With the S&P 500 Index tumbling 15% from its record high in just seven sessions and corporate credit spreads widening fast, Powell released an unscheduled statement at 2:30 p.m. pledging that Fed officials would “use our tools and act as appropriate to support the economy.”

The following Tuesday – March 3 – the Fed cut its benchmark lending rate by half a percentage point to a range of 1.00% to 1.25%.

“The fundamentals of the U.S. economy remain strong,” the U.S. central bank said.

“However, the coronavirus poses evolving risks to economic activity.”

One month later, the US economy was in a recession, or perhaps a depression.

That said, today’s minutes are unlikely to contain anything to spook markets, given that it has rolled-out measures to assuage market concerns, and will likely reiterate its pledge to support the financial system. Of most interest will be whether there was any discussion in the minutes of if, when and under what, the Fed would start buying stocks.

Despite all The Fed has done, financial conditions are extremely tight still…

Source: Bloomberg

So just how freaked out were they over those two hectic weeks…

The short answer is “very”!

Policy makers saw risks pointing to the downside and warranting a “forceful” response, according to a record of their emergency gathering Sunday, March 15.

“All participants viewed the near-term U.S. economic outlook as having deteriorated sharply in recent weeks and as having become profoundly uncertain,” minutes published Wednesday of the Federal Open Market Committee meeting showed.

At the unscheduled meeting, officials announced that they would cut their benchmark interest rate to nearly zero and relaunch massive bond-buying programs to pump cash into the financial system, as they sought to shelter the U.S. economy from the coronavirus pandemic.

Fed notes “extremely large degree of uncertainty” on outlook

In their consideration of monetary policy at this meeting, most participants judged that it would be appropriate to lower the target range for the federal funds rate by 100 basis points, to 0 to ¼ percent. In discussing the reasons for such a decision, these participants pointed to a likely decline in economic activity in the near term re-lated to the effects of the coronavirus outbreak and the extremely large degree of uncertaintyregarding how long and severe such a decline in activity would be.

Fed advocated “forceful” monetary response

In light of the sharply increased downside risks to the economic outlook posed by the global coronavirus outbreak, these participants noted that risk-management considerations pointed toward a forceful monetary policy response, with the majority favoring a 100 basis point cut that would bring the target range to its effective lower bound (ELB). With regard to monetary policy beyond this meeting, these participants judged that it would be ap-propriate to maintain the target range for the federal funds rate at 0 to ¼ percent until policymakers were con-fident that the economy had weathered recent events and was on track to achieve the Committee’s maximum employment and price stability goals

Fed on the severe strain in bond markets:

Trading conditions across a range of markets were severely strained. In corporate bond markets, trading ac-tivity and liquidity were at very low levels, although not back to the low point reached in 2008. Market partici-pants expected that actions taken to slow the spread of the virus could have significant effects on the credit wor-thiness of certain borrowers, particularly those at the lower end of the credit spectrum. Market participants also increasingly pointed to concerns in other segments of the debt market. In securitized markets, including those for asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS), primary market is-suance slowed, and secondary market trading had be-come less orderly, with money managers selling short-dated liquid products to meet investor redemptions.

Fed on Treasury Markets

In the Treasury market, following several consecutive days of deteriorating conditions, market participants re-ported an acute decline in market liquidity. A number of primary dealers found it especially difficult to make markets in off-the-run Treasury securities and reported that this segment of the market had ceased to function effectively. This disruption in intermediation was at-tributed, in part, to sales of off-the-run Treasury securi-ties and flight-to-quality flows into the most liquid, on-the-run Treasury securities

Fed on short-term funding markets

Conditions in short-term funding markets also deterio-rated sharply amid a decline in market liquidity and chal-lenges in dealer intermediation. Over recent days, the premium paid to obtain dollars through the foreign ex-change swap market increased sharply, and the volumes in term repurchase agreement (repo) markets dropped significantly. Issuance of commercial paper (CP) matur-ing beyond one week reportedly almost dried up at the end of the week before the meeting, and primary- and secondary-market liquidity for financial and nonfinancial CP was described as nearly nonexistent at a time when investor concern about issuer credit risk was rising.

Fed on stress in the housing market

…social distancing, by financial uncertainty—including difficulties that households and businesses would face in meeting mortgage or rental payments—and by volatility in the market for MBS. Participants stressed the major down-side risk that the spread of the virus might intensify in those areas of the country currently less affected, thereby sidelining many more U.S. workers and further damping purchases by consumers. Participants expressed con-cern that households with low incomes had less of a sav-ings buffer with which to meet expenses during the in-terruption to economic activity. This situation made those households more vulnerable to a downturn in the economy and tended to magnify the reduction in aggre-gate demand associated with the nation’s response to the pandemic.

On ZIRP

“With regard to monetary policy beyond this meeting, these participants judged that it would be appropriate to maintain the target range for the federal funds rate at 0 to 1/4 percent until policymakers were confident that the economy had weathered recent events…”

On NIRP:

A few participants also remarked that lowering the target range to the ELB could increase the likelihood that some market interest rates would turn negative, or foster investor expectations of negative policy rates. Such expectations would run counter to participants’ previously expressed views that they would prefer to use other monetary pol-icy tools to provide further accommodation at the ELB.

On Bank buybacks:

“Several participants commented that banks should be discouraged from repurchasing shares from, or paying dividends to, their equity holders.”

{kind=link}