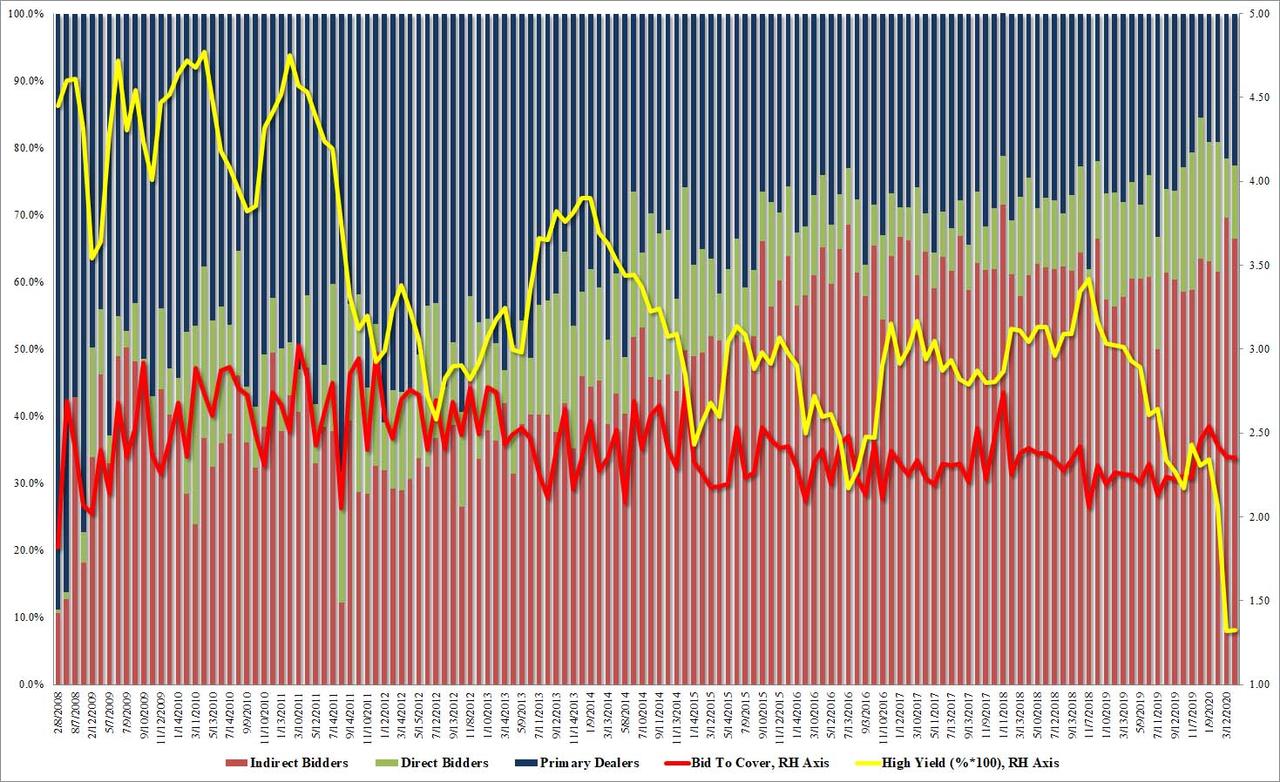

30Y Auction Prices Just Off All Time Low Yield Amid Stellar Buyside Demand

After two consecutive mediocre auctions, when the sales of 3Y and 10Y debt earlier this week tailed modestly, moments ago the Treasury concluded this week’s coupon issuance (which comes alongside a biblical flood of Bill and CMB sales), when it sold $17BN in 30Y paper (technically a 29-Year, 10-Month reopening) in what was a very strong auction.

The high yield of 1.325% was just 0.5bps above last month’s record low yield of 1.32%, and also stopped by 0.5bps through the When Issued.

The bid to cover was almost unchanged from last month’s 2.358, dripping fractionally to 2.352%, which was also just below the 6 auction average of 2.377%.

The internal was also a bit softer than last months, as Indirects took down 66.4%, down from 69.5% which however was above the 62.5% recent average, and with Directs taking down 11%, more than the 8.9% in March, Dealers were left with 22.6%, a slightly higher than average number, and one which Dealers will promptly make sure eases as they sell the long end back to the Fed.

Overall, this was a solid, stopping through auction and one which underpinned the long-end of the curve.

“These Numbers Are Ugly” – WTO Forecasts Collapse In World Trade, Recovery For 2021

The World Trade Organization (WTO) published a new report on Wednesday that is truly apocalyptic, and crushes all hopes that a V-shaped recovery would be seen this year (similar to what Morgan Stanley said last week):

“World trade is expected to fall by between 13% and 32% in 2020 as the COVID 19 pandemic disrupts normal economic activity and life around the world,” the WTO report said.

The Geneva-based body does not see a recovery in global trade until 2021, and even then, the outcome of recovery is mainly dependent “on the duration of the outbreak and the effectiveness of the policy responses.” The economic recovery could be anywhere from 21% and 24%.

“This crisis is first and foremost a health crisis which has forced governments to take unprecedented measures to protect people’s lives,” WTO Director-General Roberto Azevêdo said.

“The unavoidable declines in trade and output will have painful consequences for households and businesses, on top of the human suffering caused by the disease itself.”

“The immediate goal is to bring the pandemic under control and mitigate the economic damage to people, companies and countries. But policymakers must start planning for the aftermath of the pandemic,” he said.

“These numbers are ugly – there is no getting around that. But a rapid, vigorous rebound is possible. Decisions taken now will determine the future shape of the recovery and global growth prospects. We need to lay the foundations for a strong, sustained and socially inclusive recovery. Trade will be an important ingredient here, along with fiscal and monetary policy. Keeping markets open and predictable, as well as fostering a more generally favourable business environment, will be critical to spur the renewed investment we will need. And if countries work together, we will see a much faster recovery than if each country acts alone.”

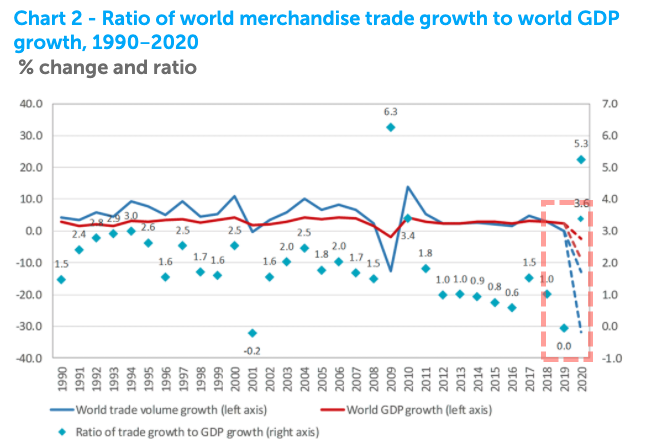

Shown in the chart below, the WTO has modeled three scenarios of world trade through 2022 against a trendline from 1990-2008 and a trend line from 2011-2018. Notice the giant gap forming verses both trend lines as the global economy is undoubtedly in trouble.

WTO said world trade was already slowing before the virus outbreak, mainly because of the trade war.

“Trade was already slowing in 2019 before the virus struck, weighed down by trade tensions and slowing economic growth. World merchandise trade registered a slight decline for the year of ‑0.1% in volume terms after rising by 2.9% in the previous year. Meanwhile, the dollar value of world merchandise exports in 2019 fell by 3% to US$ 18.89 trillion.”

Chart 2: Ratio of world merchandise trade growth to world GDP growth, 1990‑2020 (% change and ratio)

Chart 3: New export orders from purchasing managers indices, Jan. 2008 – Mar. 2020 (Index, base=50)

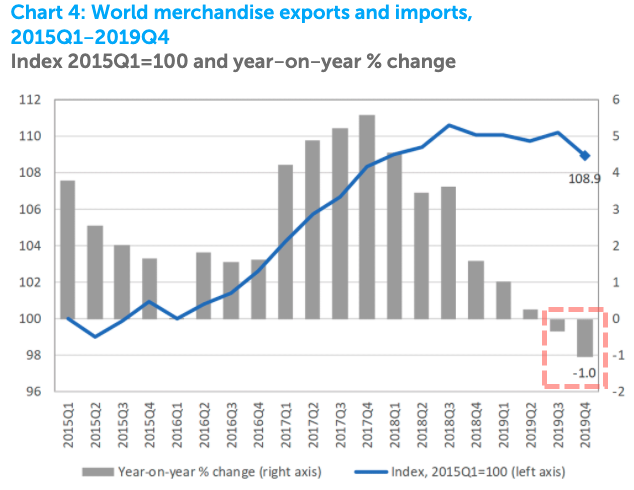

Chart 4: World merchandise exports and imports, 2015Q1‑2019Q4 (Index 2015Q1=100 and year‑on‑year % change)

And to confirm WTO’s thoughts on collapsing global trade, the OECD was also out with a report outlining all major economies had plunged into a “sharp slowdown,” or as some like to say: depression.

Seperate from the WTO press release, WTO’s Azevêdo was quoted in a headline on Wednesday that read: “crisis shouldn’t mean reversal of globalization.”

In recent decades, flu season has often peaked sometime from January to March, and this is a major driver in total deaths. The averagedaily number of deaths from December through March is over eight thousand.

So far, total death data is too preliminary to know if there has been any significant increase in total deaths as a result of COVID-19, and this is an important metric, because it gives us some insight into whether or not COVID-19 is driving total death numbers well above what would otherwise be expected.

Indeed, according to some sources, it is not clear that total deaths have increased significantly as a result of COVID-19. In a March 30 article for The Spectator, former UK National Health Service pathologist John Lee noted that the current number of deaths from COVID-19 does not indicate that the UK is experiencing “excess deaths.” Lee writes:

The simplest way to judge whether we have an exceptionally lethal disease is to look at the death rates. Are more people dying than we would expect to die anyway in a given week or month? Statistically, we would expect about 51,000 to die in Britain this month. At the time of writing, 422 deaths are linked to Covid-19—so 0.8 per cent of that expected total. On a global basis, we’d expect 14 million to die over the first three months of the year. The world’s 18,944 coronavirus deaths represent 0.14 per cent of that total. These figures might shoot up but they are, right now, lower than other infectious diseases that we live with (such as flu). Not figures that would, in and of themselves, cause drastic global reactions.

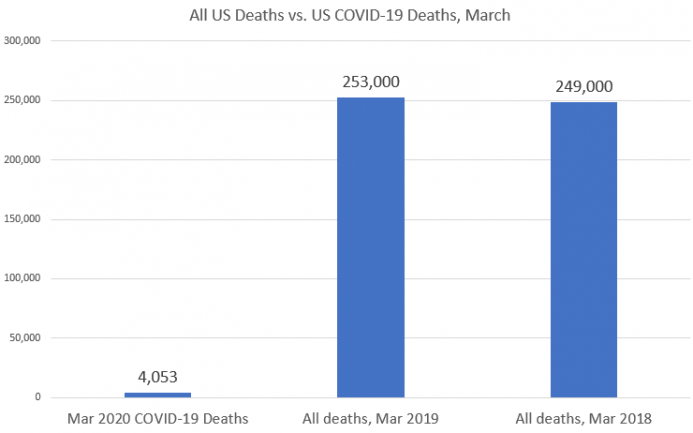

How do these numbers look in the United States? During March of 2020, there were 4,053 COVID-19 deaths according to Worldometer. That is 1.6 percent of total deaths in March 2019 (total data on March 2020 deaths is still too preliminary to offer a comparison). For context, we could note that total deaths increased by about four thousand from March 2018 to March 2019. So for March, the increase in total deaths is about equal to what we already saw as a pre-COVID increase from March 2018 to March 2019.

As Lee notes, total COVID-19 deaths could still increase significantly this season, but even then we must ask what percentage of total deaths warrants an international panic. Is it 5 percent? Ten percent? The question has never been addressed, and so far, a figure of 1 percent of total deaths in some places is being treated as a reason to forcibly shut down the global economy.

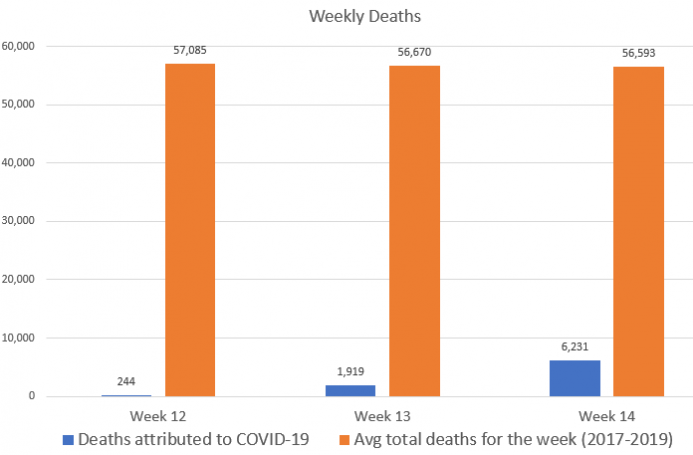

Yet, as a CDC report recently noted, pneumonia deaths have often been far more common than COVID-19 deaths are right now: “Based on National Center for Health Statistics (NCHS) mortality surveillance data available on March 26, 2020, 8.2 percent of the deaths occurring during the week ending on March 21, 2020 (week 12), were due to [pneumonia and influenza].”

Meanwhile there is a trend toward to attributing more of those pneumonia deaths to COVID-19 rather than influenza, although this doesn’t actually mean the total mortality rate has increased. The CDC report continues: “the percent of all deaths with Influenza listed as a cause have decreased (from 1.0% to 0.8%) over this same time period. The increase in pneumonia deaths during this time period are likely associated with COVID-19 rather than influenza.” This doesn’t represent a total increase in pneumonia deaths, just a change in how they are recorded.

This reflects an increased focus on attributing deaths to COVID-19, as noted by Lee:

In the current climate, anyone with a positive test for Covid-19 will certainly be known to clinical staff looking after them: if any of these patients dies, staff will have to record the Covid-19 designation on the death certificate—contrary to usual practice for most infections of this kind. There is a big difference between Covid-19 causing death, and Covid-19 being found in someone who died of other causes. Making Covid-19 notifiable might give the appearance of it causing increasing numbers of deaths, whether this is true or not. It might appear far more of a killer than flu, simply because of the way deaths are recorded.

Given this rush to maximize the number of deaths attributable to COVID-19, what will April’s data look like? It may be that COVID-19 deaths could then indeed number 10 or 20 percent of all deaths.

But the question remains: will total deaths increase substantially compared to April 2019 or April 2018? If they don’t, this will call into question whether or not COVID-19 is the engine of mortality that many government bureaucrats insist it is. After all, if April’s mortality remains “about the same” as the usual total and comes in around 230,000–235,000, then obsessive concern over COVID-19 would be justified only if it can be proven April 2020 deaths would have plummeted year-over-year had it not been for COVID-19.

Update:

Meanwhile the CDC is instructing medical staff to report deaths as COVID-19 deaths even when no test has confirmed the presence of the disease. In a Q and A on death certificates published by the CDC on March 24, the agency advises:

COVID-19 should be reported on the death certificate for all decedents where the disease caused or is assumed to have caused or contributed to death. Certifiers should include as much detail as possible based on their knowledge of the case, medical records, laboratory testing, etc. If the decedent had other chronic conditions such as COPD or asthma that may have also contributed, these conditions can be reported in Part II. [emphasis in original.]

This is extremely likely to inflate the number of deaths attributed to COVID-19 while pulling down deaths attributed to other influenza-like illnesses and to deaths caused by pneumonia with unspecified origins. This is especially problematic since we know the overwhelming majority of COVID-19 deaths occur in patients that are already suffering from a number of other conditions. In Italy, for example, data shows 99 percent of COVID-19 deaths occurred in patients who had at least one other condition. More than 48 percent had three other conditions. Similar cases in the US are now likely to be routinely reported simply as COVID-19 cases.

Unfortunately, because total death data is not reported immediately, we have yet to see how this plays out.

We do know historically, however, that deaths attributed to flu and pneumonia over the past decade have tended to make up around five to ten percent of all deaths, depending on the severity of the “season.” Last week (week 14, the week ending April 4) was the first week during which COVID-19 deaths exceeded flu and pneumonia deaths, coming in at 11 percent of all death for that week. The prior week, (week 13, the week ending Mar 28) COVID-19 deaths made up 3.3 percent of all deaths.

Until we have reliable numbers on all deaths in coming weeks, it will be impossible to know the extent to which COVID-19 are “cannibalizing” flu and pneumonia deaths overall. That is, if the COVID-19 totals skyrocket, but total deaths remain relatively stable, than we might guess that many deaths formerly attributed simply to pneumonia, or to flu, are now being labeled as COVID-19 deaths. Potentially, this could also be the case for other patients, such as those with advanced cases of diabetes.

Iran Pleads For $5BN IMF Loan As Deaths Soar Past 4,000; US To Block Funds

Iran is desperately pleading for the International Monetary Fund to approve a $5 billion emergency loan to help the outbreak-ravaged country to survive.

“I urge international organizations to fulfill their duties… we are a member of the IMF… There should be no discrimination in giving loans,” President Hassan Rouhani said in televised remarks Wednesday.

He further slammed US sanctions on the Islamic Republic as “economic and medical terrorism” — given the US-led near total economic blockade of the country has severely hampered Tehran’s response to the COVID-19 pandemic. There are currently over 64,500 confirmed cases and as of Wednesday this includes a grim milestone of surpassing 4,000 deaths after months ago Iran became the first epicenter outside China, followed by Italy.

The U.S. plans to block Iran’s requested $5 billion emergency loan from the International Monetary Fund for funding Tehran says it needs to fight its coronavirus crisis.

Advocates for sanctions relief say that current sanctions will ultimately make the global response to the pandemic worse for populations in other countries as well, given without Iranian hospitals having necessary access to supplies and crucial medicines, the virus will continue to fester there even after the rest of the world pivots toward recovery.

But as the WSJ reports, Tehran is unlikely to see a single penny in IMF relief:

The IMF has said it is in talks with officials in Iran to determine its eligibility for the loan.

However, the Wall Street Journal reported on Wednesday that the US – the IMF’s largest shareholder – planned to block the request.

It cited senior Trump administration officials as saying that Iran’s government had billions of dollars in bank accounts still at its disposal, and that the loan might be used to help its economy rather than on combating Covid-19 or fund terrorist operations.

In early March Iran’s Central Bank chief Abdolnaser Hemmati first addressed a letter to the head of the IMF requesting the five billion dollars from the RFI emergency fund “to help our fight against the coronavirus”.

US administration gleefully takes pride in killing Iranians citizens on #Nowruz—our New Year.

The White House takes its “maximum pressure” to a new level of inhumanity with its utter contempt for human life.

At that time Iran’s death toll was 500, but now stands at just over 4,000.

Iran has argued that it is “a dues-paying member of the IMF and has not had a loan in decades,” according to the assessment of Mohammad Marandi, professor of American Studies at Tehran University.

“As a country that has paid its dues and without any debt to the IMF, Iran is entitled to a loan to fight the coronavirus pandemic at the time when the US has weaponised the virus against Iran,” Marandi added.

Fed Minutes To Reveal The Sheer Chaos As Fed’s Entire Worldview Imploded

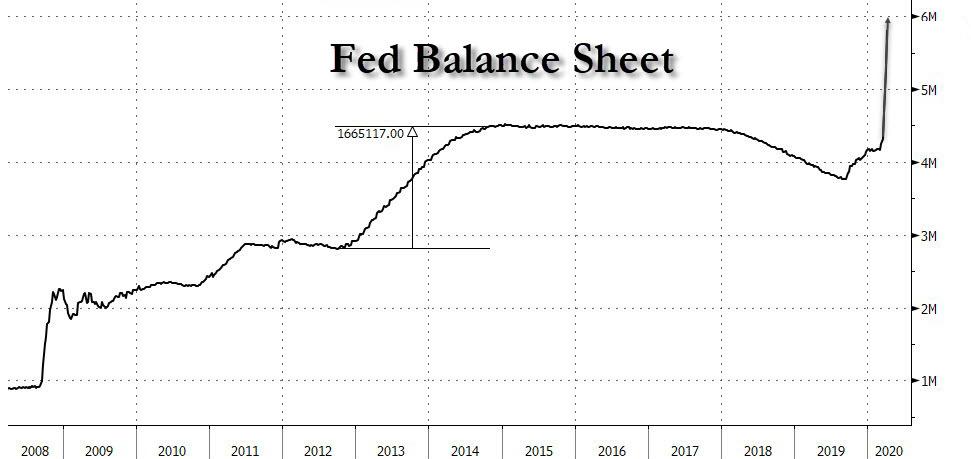

Starting a week of historic central bank interventions, at the 15th March weekend meeting, the Fed threw the proverbial kitchen sink at the market, taking aggressive measures (slashing rates by 100bps to 0.25%; committed to at least USD 700bln of QE; eased regulatory pressure on banks to free up capital, and announced dollar swap lines with other central banks), reaching decisions that may shape the global economy for decades to come in the space of a few frantic weeks. This was followed with a barrage of other measures which included the boosting of QE and MBS purchases on Mar 23, expanded repo for foreign central banks on Mar 31, and also announced six further facilities, including the commercial paper facility, de facto backstopping the entire market except equities and junk bonds.

The timing of the Fed’s announcement and the scope of the measures was a surprise: as NewsSquawk writes, it was the Fed’s “whatever it takes” commitment to ensure the smooth functioning of markets amid the virus fallout. Since then, it has flooded the market with liquidity, resulting in the premium for dollars easing.

Since then, its balance sheet has ballooned to by USD 1.5trln to a new record high USD 5.86trln, and it has seen wide take-up of its liquidity facilities from banks and other central banks.

Fast forward to today, when at 2pm the first detailed accounts of that debate will be released when the central bank publishes minutes of the meetings.

The minutes will provide detail on the Fed decisions announced on March 3 and March 15 after Fed Chair Jerome Powell convened emergency meetings as the scale of the pandemic and its risk to the U.S. economy became clear. The readout may also include their discussions of a slate of related actions that flowed from those two meetings.

Amusingly, just five weeks before the surprise rate cut on March 3, Powell and his colleagues had wrapped up their first meeting of the year on Jan. 29 with an air of cautious optimism, and it even looked like 2020 could be a year of steady growth and continued strength in the job market, a fresh updraft after a rocky 2019 in which the Fed cut rates three times to blunt the effects of the Trump administration’s trade war with China.

Fast forward to today, when most Fed officials now agree the U.S. economy is in a recession that may cut U.S. output by double digits in the second quarter and throw 20 million people or more out of work, at least temporarily, due to measures taken to contain the spread of COVID-19, the illness caused by the coronavirus.

Wednesday’s minutes may show just how dire a threat officials saw in those earliest moments and what spurred them to action. The first move came on Feb. 28.

With the S&P 500 Index tumbling 15% from its record high in just seven sessions and corporate credit spreads widening fast, Powell released an unscheduled statement at 2:30 p.m. pledging that Fed officials would “use our tools and act as appropriate to support the economy.”

The following Tuesday – March 3 – the Fed cut its benchmark lending rate by half a percentage point to a range of 1.00% to 1.25%.

“The fundamentals of the U.S. economy remain strong,” the U.S. central bank said. “However, the coronavirus poses evolving risks to economic activity.”

One month later, the US economy was in a recession, or perhaps a depresion.

That said, today’s minutes are unlikely to contain anything to spook markets, given that it has rolled-out measures to assuage market concerns, and will likely reiterate its pledge to support the financial system. Of most interest will be whether there was any discussion in the minutes of if, when and under what, the Fed would start buying stocks.

Chicago Mayor Lori Lightfoot issued an executive order April 7 allowing illegal immigrants and refugees in the city, regardless of birth country or current citizenship status, access to relief benefits amid the CCP (Chinese Communist Party) virus pandemic.

The order says it will “ensure that all Chicagoans have fair and equal access to benefits, opportunities, and services provided by the City,” including anything provided as disaster relief to help fight the CCP virus pandemic.

“This order is more than just an official decree, it is a statement of our values as a city and as Americans,” Lightfoot said in a statement.

“Since COVID-19 first reached our city’s doorstep, we have been working around the clock to ensure all our residents are secure and supported, including our immigrant and refugee communities, who are among the most vulnerable to the impact of this pandemic.”

“Here in Chicago, saying ‘we are all in this together’ means that during this crisis, no one gets left out and no one gets left behind,” she said.

Illegal immigrants who have no legal status in the United States do not meet the criteria for state unemployment insurance or other economic assistance, or the stimulus checks the federal government is sending out to all registered tax-payers part of the $2 trillion coronavirus relief bill Congress passed in March.

According to the National Review, at least 280,000 illegal immigrants were working in Illinois in 2018 based on a WBEZ analysis of census data. They were mostly concentrated around the sanctuary city of Chicago.

Under the new order, the illegal migrants will be able to receive benefits through Chicago’s Housing Assistance Grant program, which provides disaster relief aid for the housing costs faced by those impacted by the current CCP crisis.

Students will also be offered online Enrichment Learning Resources through Chicago Public Schools, and small businesses will have access to the $100 million Chicago Small Business Resiliency Fund, which provides disaster relief cash flow to any entrepreneur, including immigrant business owners.

Michael Rodriguez, who serves as alderman of the 22nd Ward in Chicago, said “these Chicagoans are vital community members who work in various industries and help our great city to thrive every day,” and are “family members, co-workers, neighbors, and friends.”

Chicago and Illinois are currently under a statewide Stay at Home order that was issued on March 20 until at least April 30.

The order mandates all residents to stay home, unless traveling for essential needs or business, and requires businesses not engaged in essential activities to cease all activities except for minimum basic operations.

According to the latest figures published on the official City of Chicago website, 5,511 cases of CCP virus have been confirmed in Chicago as of April 7, and 13,549 in Illinois. The majority of the known cases in Chicago are in individuals aged between 50-59, while the majority of deaths have occurred in individuals aged 70 or over.

Morgan Stanley Warns It Will Take At Least 7 Months For Markets To Normalize

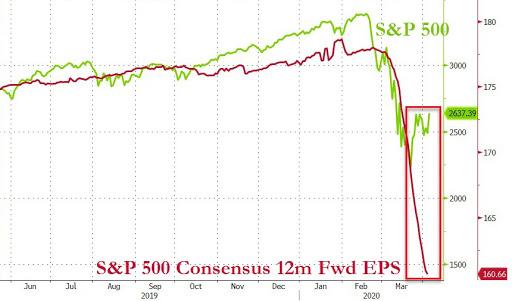

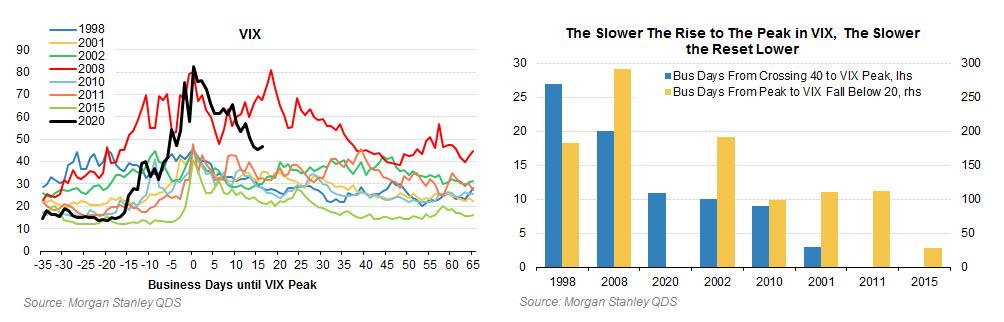

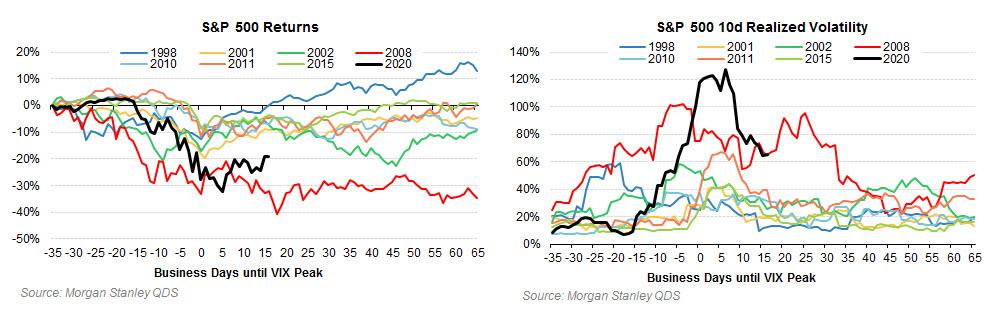

As Morgan Stanley’s Christopher Metli and Amanda Levenberg write this morning, there have been signs of health returning to the market, with the S&P 500 now more than 20% off the lows again and VIX 35+ points off its highs.

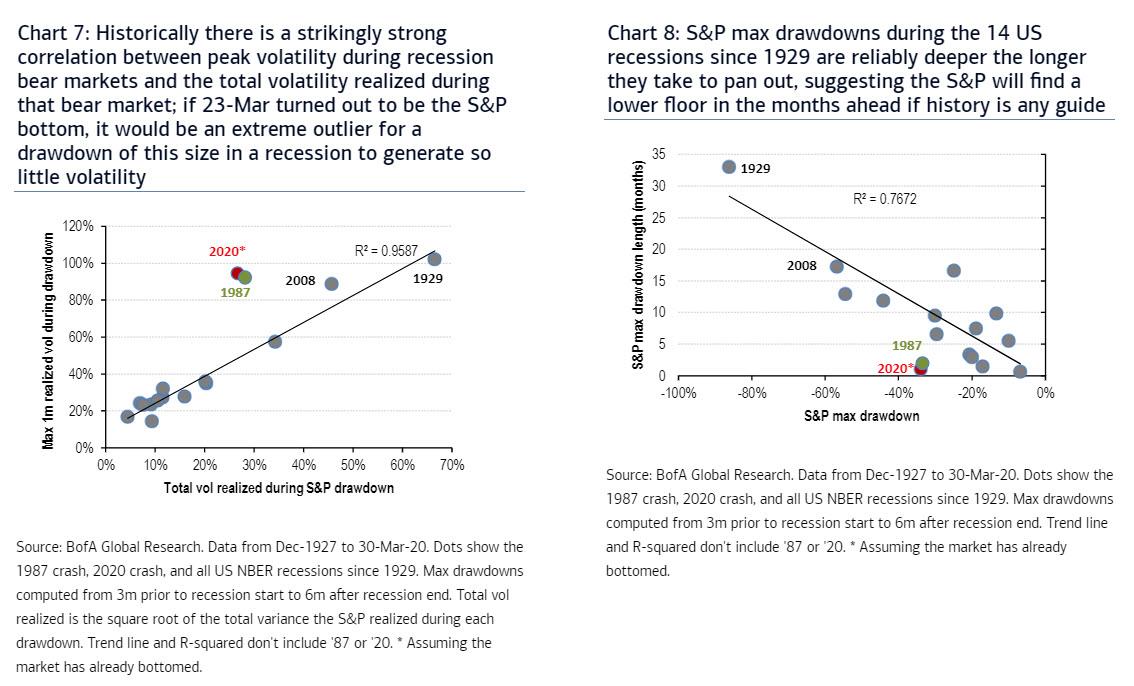

However, as we cautioned yesterday, the rally back has been sharp, and according to BofA, too sharp as “the current drawdown has so far been more similar to the 1987 crash, and it would be an extreme outlier for a drawdown of this size in a recession (particularly one as deep as it is forecasted to be) to generate so little volatility…

… unless the US can somehow avoid recession, which is now impossible, prompting BofA to conclude that “it’s likely that we haven’t seen the bottom in equities yet.”

Picking up on this, MS writes that the despite the sharp rally, realized volatility has remained elevated (perhaps for the end of day rebalancing reasons we highlighted yesterday) with S&P 500 10d realized volatility still above 60% and VIX is still above 40 (an average daily move of 2.9%).

This means that while the market recovery and vol compression are impressive, they are not enough to force material buying from systematic strategies (Vol Target Funds and Trend Following CTAs). To generate meaningful demand from Trend Followers, Morgan Stanley calculates that the S&P 500 would have to rally closer to 2900 (50d moving average, and many strategies wouldn’t even buy until prices are higher) and Vol Target Funds would only buy once falls down to 20 to 30% – and stays there. But volatility generally falls much more slowly than it rises, and history suggests that it could take several months for volatility to reset to ‘normal’ (sub-20) levels. After previous peaks in volatility, it took an average of 6 to 7 months for VIX to fall back down below 20.

Some more observations from MS:

VIX hit its closing peak just over 3 weeks ago on March 16th at 82.69 (intraday peak of 85.47 on March 18th) and has fallen to a 40 handle since then – its sharpest 3w decline ever which followed its fastest rise ever (first chart below). Many investors are comparing spot and vol dynamics over the past month to what happened during the Financial Crisis. While the level of expected volatility for the next several months (as priced by SPX options) is somewhere between the 2009 recovery and recoveries from after the GFC, the market is priced for a faster recovery than seen in 2008 (the shape of the curve is more in line with vol pricing after post-GFC selloffs). This pricing likely reflects the now large and well-known Fed put, which also existed during 2008 but was much more slowly to be deployed. Compared to prior days when VIX was at a similar level to where it is now, S&P 500 implied volatility across the term structure is more in line with post-2009 levels and well below 2008-2009 levels.

Echoing BofA, MS cautions, that despite VIX falling sharply and the S&P 500 term structure pricing in a quicker reversion in volatility than it did in 2008, there’s reason to believe that it may be a while before we see VIX back to ‘normal’ levels (sub-20).

After previous peaks in VIX, it took an average of 7 months for VIX to fall back below 20. There were naturally a wide range of outcomes though – 2015 was the quickest reversion back (at 29 business days) while 2008 was the longest (it took over a year). Also, the longer it took VIX to reach its peak after crossing 40, the longer it generally took for VIX to reset back below 20. If the VIX peak for this cycle does end up being on March 16th (11 days after initially crossing above 40), this relationship would imply that VIX should stay above 20 for about 6 to 7 months from now. To play for a floored fall in VIX over the next few months, the desk likes buying the Aug VIX 1×2 18 / 23 put spread for ~80 cents (ref: 32.05, pricing indicative).

During large shocks the market bottom often occurs after the peak in volatility, while the peak in vol and market bottom have occurred simultaneously in smaller selloffs (i.e. 1998).

So what does that mean for the market? In the near-term, Morgan Stanley’s quants are “balancing a concern of further market downside from retail/passive selling against unprecedented stimulus which could continue to accelerate the recovery. History suggests that regardless of the path of the underlying market, it could be several months before VIX fully normalizes.“

Fed Eases Wells Fargo “Growth Restrictions” So Bank Can Participate In Small Business Bailout

Following Wells Fargo’s complaint that it was unable to fully participate in the SBA’s Paycheck Protection Program, capping its small business bailout exposure to at most $10 billion, due to the Fed unprecedented 2018 enforcement action and restrictions on Wells Fargo’s balance sheet as punishment for the bank’s opening of millions of fake accounts which cost former CEO John Stumpf his job, it was only a matter of time before the Fed relented and eased the bank’s restrictions as the NYT reported two days ago.

And indeed, this happened moments ago when the Fed announced that “due to the extraordinary disruptions from the coronavirus, that it will temporarily and narrowly modify the growth restriction on Wells Fargo so that it can provide additional support to small businesses.”

Due to the extraordinary disruptions from the coronavirus, the Federal Reserve Board on Wednesday announced that it will temporarily and narrowly modify the growth restriction on Wells Fargo so that it can provide additional support to small businesses. The change will only allow the firm to make additional small business loans as part of the Paycheck Protection Program, or PPP, and the Federal Reserve’s forthcoming Main Street Lending Program.

However, in a curious twist, the Board said it would require profits and benefits from Well’s participation in the PPP and the Main Street Lending Program “to be transferred to the U.S. Treasury or to non-profit organizations approved by the Federal Reserve that support small businesses. The change will be in place as long as the facilities are active.”

In other words, the Fed will remove incentives for the remaining criminals on Wells’ staff to create fake bailout loans and profit from the Treasury’s guaranteed funds.

Some more details:

The Board’s growth restriction was implemented because of widespread compliance and operational breakdowns that resulted in harm to consumers and because the company’s activities were ineffectively overseen by its board of directors. The growth restriction does not prevent the firm from engaging in any type of activity, including the PPP, the Main Street Lending Program, or accepting customer deposits. Rather, it provides an overall cap on the size of the firm’s balance sheet. The change today provides additional support to small businesses hurt by the economic effects of the coronavirus by allowing activities from the PPP and the Main Street Lending Program to not count against the cap.

The Fed concludes that “the changes do not otherwise modify the Board’s February 2018 enforcement action against Wells Fargo. The Board continues to hold the company accountable for successfully addressing the widespread breakdowns that resulted in harm to consumers identified as part of that action and for completing the requirements of the agreement.”

The PPP program, while much needed by mainstreet businesses, will in the comingyears be revealed as an unprecedented criminal “free for all”, as tens of billions in funds are funneled into illicit organizations and shady deals.

It seems the entirety of the financial media and many on Wall Street believe a “V” shaped economic recovery is in our future. While we hope they are right, we would be foolish to take such analysis and, quite frankly, unwarranted optimism, at face value.

If history teaches us one thing, it is that significant, life-altering events are rarely if ever followed by a quick return to normality. In this article, we raise a few considerations that may make you reconsider popular economic narratives. Today, the importance for investors to think outside of the box cannot be overstated. Or to put it another way, the parameters of “the box” have likely changed and, if so, we should be cognizant of those changes in our decision making.

If the future economic recovery does not resemble the “V” shape that the financial markets are depending on, the stock market may be even more over-valued than we think. To that end, consider the following graph showing where the S&P 500 could trade based on a range of historical valuations.

Data Courtesy Shiller

Short Term Prognosis

The COVID-19 Crisis may be short-lived or not. Although it seems as though progress is being made, there is nary a sign that a full-fledged cure or vaccine is at hand. Social distancing and mass closures of commercial enterprise appear to slow the exponential spreading of the virus considerably. While very effective in saving lives, these measures come with immense economic costs. The productive output of the global economy has ground to a near-total halt.

As the virus appears to have peaked in Asia and is starting to show signs of peaking in Europe, we are hopeful the U.S. will also peak shortly. Then what? From a health standpoint, the answer depends on whether a cure or vaccine is discovered.

If a cure or vaccine is found and can be produced, distributed, and administered quickly, then mandatory and self-regulated social distancing will end, and people will hopefully resume normal activities. This may be the rationale backing a “V” shaped recovery, but as we discuss later in the article, normal may not be the same normal we knew before February 2020.

If the spreading of the virus is significantly curtailed, but there is no cure or vaccine developed, the outcome may be very different. Just ask yourself, are you ready to stand in a crowded elevator, hop on a packed train, or stand shoulder to shoulder with other fans at a sporting event or concert? It is quite likely that in the bleaker scenario with no cure or vaccine, there will be some recovery, but most people will dramatically alter their everyday life. Such a change will radically reshape the outlook for human behavior on a vast scale.

As you consider those scenarios, also consider their respective economic impacts. The first scenario, a return to normal with a cure or vaccine, offers a higher probability of bringing about a “V” shaped recovery. We, however, would argue for a “U” shaped recovery as the damage already done is not easy to overcome so quickly. A “U” shaped recovery entails a prolonged period of slow to negligible growth versus a “V’s” sharp reversal higher of growth

We fear that the second, no cure/vaccine scenario will look much more like an “L” shaped stagnation.

Those two scenarios may help guide you in the short run, but left out of the discussion thus far is the long term change to our psyches and the effect it will have on our economic behaviors and decision making.

Long Term

In our daily discussions with neighbors, family, and friends, we are inundated with concern over economic well being. Jobs are at stake, and for the more fortunate, pay cuts are likely. As if those concerns were not enough, most people have seen a sharp decline in the value of their investment portfolios and retirement savings accounts. Almost overnight, many people saw their financial stability weaken dramatically.

The economic and financial concerns brought on by the current day stresses we are harboring will play a big role in the future.

If you have ever known someone that lived through the Great Depression, you probably noticed that their economic and financial behaviors are not what you might consider normal. Regardless of their financial standing, they tend to have considerable savings, of which a good portion resides in non-risky assets or cash. They also seek out the best deals and are never shy to pick up a penny or use a coupon. Some of these people are millionaires, but in many cases, onlookers would not have any clue by looking at their lifestyles.

These survivors learned that money for a rainy day is much more than a cute saying. A common motto during the Depression and one that survived long afterward was “use it up, wear it out, make do or do without.”

The current economic crisis has some similarities to the Great Depression. Still, so far, it pales in comparison as the duration of current hardships is only measured in weeks, not years. The Depression raged on for an entire decade.

The longer this crisis continues, the more likely our economic and financial preferences will change.

This experience will remind us why rainy day funds are so necessary, the value of frugality, and in general, it could put our economic behavior back on par with more historical norms. These norms are not at all primitive as we are re-learning, they are wise, they are prudent, and they are critical.

This experience may not rival the Great Depression in impact, but understand the crisis is reviving valuable lessons that were long forgotten. Many people will rethink their consumption habits and many companies and governments will assess the risks of globalization when this crisis ends. The repercussions will be large.

Summary

The possible changes in our behaviors described above will not only affect the economy but will also change investor behaviors. The longer the crisis rages and the deeper the market declines, the harsher and longer-lasting the lessons that will be imposed by the market. It seems reasonable that buying shares at extreme valuations from companies that perpetually lose money will cease to be a badge of honor. Cash, Treasury Bonds, active investment strategies, and value may all come back into fashion.

Like everyone else, we have no idea what the future holds. The virus may be cured, and life may go on as if nothing happened. If so, great, but that is not the lesson that history teaches.

We would be remiss not to consider at least that the COVID-19 crisis transforms our economic logic. This shift would be healthy but demands a new logic for investing in such an environment.

Sen. Bernie Sanders has suspended his campaign, according to a statement from the Vermont Senator.

“I wanted to just let everyone know that in a half hour I will be publicly announcing the suspension of our campaign. needless to say this is a very difficult and painful decision for me.” “There is no alternative”

{kind=link}