An economy of rackets designed to enrich the few at the expense of the many is brittle because self-serving rackets snuff out competition, accountability and transparency.

What’s remarkable about the lockdown isn’t the hue and cry about the economic damage–it’s the absence of any critical curiosity as to how our economy became so fragile that only the wealthiest contingent can survive a few weeks on savings or rainy-day funds.

A healthy, resilient economy would be able to survive a few weeks of lockdown without a multi-trillion dollar bailout of every racket in the land. A society that wasn’t threadbare financially and socially would be able to function and accept individual sacrifices for the common good.

Rather than being organized to serve the common good, our economy and social order is little more than overlapping rackets: rigged “markets” operated by quasi-monopolies to enrich the few at the expense of the many; brittle bureaucracies bound by thousands of pages of mindless “compliance” and exploitive neofeudal structures in which debt-serfs are paid just enough to service their debt but not enough to afford skyrocketing costs for housing, healthcare, higher education, childcare, junk fees and taxes.

While everyone is busy screaming about the damage done by the lockdown, nobody’s asking why costs are so high that few can survive a few weeks on their own means. Nobody dares look at the soaring costs imposed by cartels and monopolies (including government and government-funded rackets such as healthcare and higher education) because it might shine a light on the money-trough they’re feeding from. (Crush every racket but mine…)

If costs weren’t so crushing, more households and enterprises might have savings. Empires don’t collapse because everyone ran out of money; they collapse when the costs exceed earnings.

Put another way, the skyrocketing costs of self-serving sclerotic complexity, a.k.a. convoluted inefficiencies imposed by institutions which lack any accountability, far exceed the gains in productivity and resource mining needed to pay for the productivity-draining complexity.

As for innovation–please don’t make us laugh. All the rackets work overtime to avoid being disrupted by the forces of productivity and transparency. Just look at higher education: all the technology was available a decade ago to radically reduce the costs of effective education, (as I outlined in my 2012 book The Nearly Free University), but the higher education cartel fought to maintain its monopoly on credentials, squandering hundreds of billions of dollars on layers of administrators and self-glorifying buildings.

Just as Wall Street destroyed the private-sector mortgage market by financializing it, healthcare has been destroyed by Corporate America’s financialization of what was once for the common good, turning it into a hollowed-out profit machine for the few at the expense of the luckless serfs who have no choice but to serve the Financial Nobility. (You can pick any health insurer you want–but there’s only two, heh, and their prices are the same: Kafkaesque in their opaque complexity, and high enough to bankrupt all but the wealthiest.)

An economy of rackets designed to enrich the few at the expense of the many is brittle because self-serving rackets snuff out competition, accountability and transparency. As I noted in The Convergence of Marx, Orwell and Kafka (July 25, 2012), Marx understood that predatory, parasitic Monopoly Capitalism melts any social norms that restrict its dominance into air, while Kafka understood that the the more powerful and entrenched the bureaucracy, the greater the collateral damage rained on the innocent, and the more extreme the perversion of justice.

Orwell understood that the State’s ontological imperative is expansion, to the point where it controls every level of governance, markets and society. Once the State escapes the control of the citizenry, it is free to exploit them in a parasitic predation that is the mirror-image of Monopoly Capital. For what is the State but a monopoly of force, coercion, data manipulation and the neofeudal enforcement of crony-capitalist private monopolies on powerless serfs?

Neofeudal exploitation has hollowed out the economy, leaving a fragile, brittle shell of rackets, self-serving cartels and institutions that have squandered the public’s trust in their greedy rush to accumulate as much private wealth as they can before the whole rotten corrupt structure collapses under its own weight.

Watch: Cops Called After Report Of Man Strangling Young Females For Not Social Distancing

The social unrest that comes with locking an entire country down for 45 days is starting to bubble to the surface.

At least, that was the case in Louisville, Kentucky, where police are reviewing Facebook video of a confrontation that took place after a man reacted violently to teenagers not following social distancing rules.

Police were called out to a community called Norton Commons last Friday night after it was reported that a man had “shoved several young females and tried to strangle another”, according to WAVE 3 News.

Video of the altercation made its way onto Reddit, where it was posted under the title “Man strangles teenage girl for failing to social distance.”

No arrests have been made and the suspect has yet to be identified. Local police put out a statement over the weekend, saying:

We are aware of this video and officers from the 8th Division responded to a call to this incident (Friday) and took a report.

Obviously, we do not advise individuals concerned about social distancing to take matters into their own hands and confront people about it, especially in any physical way. We ask people who are concerned about large gatherings to call 311 or 911 to report their concerns.

On Monday, it was confirmed that the man in the video is an independent contractor who works as a physician for Baptist Health. He is on administrative leave pending an investigation.

We guess he forgot the part in the hippocratic oath where it says “do no harm, including strangling random people on the street”.

Neighbor Chris Shinn said: “For someone to lay their hands on a child, I don’t care who you are or what they did. We don’t need this here and it’s ridiculous.”

Louisville Urban League President and CEO Sadiqa Reynolds also had to weigh in: “These are grown people who assaulted young people. They’re kids, and we need to deal with it like that has to be stopped, and he and his wife have to be held accountable.”

A police spokeswoman concluded: “We know people are out there saying, ‘Hey guys, you should probably social distance’. That’s one thing, if you’re being polite and it’s your neighbors, we don’t want you to take it into your own hands, and you certainly should never get physical.”

The first draft of the civil rights-eroding USA PATRIOT Act was magically introduced one week after the 9/11 attacks. Legislators later admitted that they hadn’t even had time to read through the hundreds of pages of the history-shaping bill before passing it the next month, yet somehow its authors were able to gather all the necessary information and write the whole entire thing in a week.

This was because most of the work had already been done. CNET reported the following back in 2008:

“Months before the Oklahoma City bombing took place, [then-Senator Joe] Biden introduced another bill called the Omnibus Counterterrorism Act of 1995. It previewed the 2001 Patriot Act by allowing secret evidence to be used in prosecutions, expanding the Foreign Intelligence Surveillance Act and wiretap laws, creating a new federal crime of ‘terrorism’ that could be invoked based on political beliefs, permitting the U.S. military to be used in civilian law enforcement, and allowing permanent detention of non-U.S. citizens without judicial review. The Center for National Security Studies said the bill would erode ‘constitutional and statutory due process protections’ and would ‘authorize the Justice Department to pick and choose crimes to investigate and prosecute based on political beliefs and associations.’

Biden’s bill was never put to a vote, but after 9/11 then-Attorney General John Ashcroft reportedly credited his bill with the foundations of the USA PATRIOT Act.

“Civil libertarians were opposed to it,” Biden said in 2002 of his bill. “Right after 1994, and you can ask the attorney general this, because I got a call when he introduced the Patriot Act. He said, ‘Joe, I’m introducing the act basically as you wrote it in 1994.’”

I point this out because it is now more important than ever to be aware that power structures (and their goons like Biden) can and will seize on opportunities to roll out pre-existing authoritarian agendas. We know it happened after 9/11, and we may be absolutely certain that it is happening now.

Good thread compiling the many, many authoritarian measures which governments around the world have implemented and are preparing to implement to deal with the virus. https://t.co/cZ3KnMzdPp

Commentator and satirist CJ Hopkins has a long, long, long, long ongoing thread on Twitter right now compiling dozens and dozens of creepy Orwellian steps that have been taken by governments around the world and by Silicon Valley tech giants in response to the virus over the last three weeks. I emphasize how long the thread is because if you think you’ve finished scrolling through it you probably haven’t; make sure you keep clicking “more replies” until you get to the current entries.

I strongly encourage everyone to scroll through the thread when you get a chance to get a sense of the scale and scope of the drastic measures that are being implemented around the world, and maybe bookmark it and keep checking back now and then for updates. The entire thread is comprised of mainstream media articles with excerpts; some entries are more jarring than others, but taken as a whole it becomes clear that we’re looking at a whole lot of power being handed over to the kinds of institutions which historically don’t do good things when given a lot more power.

And these are just the steps we know about.

To what extent are these drastic, intrusive, authoritarian measures justified? The answer, in my estimation, isn’t clear yet. There are too many unknowns about the virus, too many unknowns about the responses to it, and too many unknowns about exactly what is going on behind the veil of secrecy in opaque government agencies around the world. There’s an argument expert epidemiologists are making that there’s no time to get perfectly certain of these things before dealing with a pandemic, that speed is of the essence and hesitating due to fear of maybe getting something wrong can cost millions of lives. Maybe that’s true; I’m not an epidemiologist and I do not know.

What I do know is that enormous changes are happening, and that powerful people are definitely conspiring to advance their own interests as this unfolds. There are many theories about who specifically is conspiring with whom and the specific manner in which they are doing so, and they’re being dismissed by establishment loyalists as “conspiracy theories” as though that in and of itself constitutes some sort of argument. That conspiracies are happening is actually just a fact that is obvious to any adult with a mature understanding of the world, and it can be useful to come up with theories about how that might be occurring; calling theories about conspiracies the thing that they are in a disparaging tone does not actually invalidate them.

There are a ton of theories about what’s going on behind the scenes with this pandemic and the policies that are being put in place to respond to it. Some are smart and relatively well-founded, some are stupid and rooted in generalized paranoia or partisan idiocy, many contradict each other, and many could potentially fit together in some way. I personally haven’t seen enough evidence for any one theory to throw my weight behind it, but I am watching carefully, and I am glad that the hive mind is chewing on this riddle.

One thing I will put my weight behind right now is the prediction that those of us who are dedicated to truth are going to have to drastically revise our worldviews in the coming months. There are such large-scale shifts happening in such an unclear information environment that the only thing we should expect is the unexpected; this virus is shaking things up (and being used to shake things up) in ways we don’t really understand yet, and even before the virus the world’s dominant power structures were acting very weird. This means our ideas about what’s going on in the world will likely have to undergo some revising in the relatively near future; the bigger the revelations, the more revision will be necessary.

Right now that’s the primary piece of advice I have to offer: stay skeptical, stay intellectually honest, and keep your perspectives malleable. If we are more interested in the truth than we are in being proven right or in feeling smug, then we are likely on a collision course with future revelations that will change our ideas about how the world is functioning in some pretty significant ways. If this doesn’t sound possible to you, it’s only because you currently lack the humility, intellectual honesty and cognitive flexibility to understand that you may not be seeing the full picture yet.

Things are shifting; all we can do is keep our minds agile enough to shift with them. Prepare to have your worldview obliterated.

Grenell Lashes Out Against ‘Politicized Press Leaks’ Over Schiff DNI Letter

Congressional Democrats have been accused of using their media proxies again in their ongoing war on the Trump administration.

On Tuesday, House Intelligence Committee Chair Adam Schiff (D-CA) fired off four-page letter to Acting Director of National Intelligence Richard Grenell, accusing President Trump’s top intelligence official of undermining “critical intelligence functions” by failing to notify Congress about organizational changes under his watch.

Except, Schiff’s letter reportedly made its way to the press before Grenell received it.

His letter was sent to the press before it was sent to me. These press leaks politicizing the intelligence community must stop. https://t.co/hdWIzGWvZr

An aide for the House Intelligence Committee disputed Grenell’s claim – saying it was shared with the press 14 minutes after it was sent to his office.

“This effort appears to be proceeding despite the Coronavirus pandemic and amid indications … of political interference in the production and dissemination of intelligence,” reads the letter, according to Politico.

Schiff noted that every single Senate-appointed official in the DNI’s heirarchy had been removed (drained, if you will) – and Congress has not been consulted regarding the implications of the reorganizations.

“President Trump did not nominate you for confirmation as permanent DNI,” wrote Schiff, “and it would be inappropriate for you to pursue any additional leadership, organizational or staffing changes to ODNI during your temporary tenure.”

Grenell, who Trump installed as acting DNI last month to replace the previous temporary head Joseph Maguire, was moved to the position after a stint as U.S. ambassador to Germany. Democrats raised concerns at the time that Grenell, who has limited national security experience, was being installed in the high-level intelligence post because of his loyalty to Trump. Schiff is demanding that Grenell produce by April 16 a detailed written explanation of all of his organizational changes.

In his letter, Schiff also sounds the alarm on Trump’s abrupt removal of intelligence community watchdog Michael Atkinson, whose handling of a whistleblower report related to Trump’s conduct toward Ukraine led the House to impeach him last fall. He is asking Grenell to indicate whether he every exercised his authority to prevent Atkinson from completing any of his unfinished work before Trump placed him on administrative leave and initiated his firing. –Politico

In addition to removing Atkinson, Trump recently removed the acting director of the National Counterterrorism Center, Russell Travers.

Watch Live: White House Delivers Tuesday Press Briefing As BBG Reports On New Plan To Revive The Economy

Despite Tuesday afternoon’s epic market flop, President Trump and the White House task force reportedly have some news about reopening the economy that they’re reportedly ready to share:

Just minutes before Trump & Co. were slated to go on, Bloomberg reported on a new plan to reopen the economy that is in the “early stages of planning.”

Most importantly: The plans reportedly will rely on testing to determine who is, and who isn’t, suitable to venture back into the workplace. Such a plan has been raised by conservatives who favor reopening the economy sooner rather than later, while many liberals are calling for an even longer shut down – some as long as 10 weeks – to ensure the virus is destroyed.

The only problem is that most of the people making predictions like that (ie Bill Gates) aren’t desperately hoping to get back to work. This isn’t a “relaxing break” for them – this is a waking nightmare.

WHITE HOUSE IN EARLY STAGES OF PLANNING TO REOPEN ECONOMT

TRUMP TEAM PREPS PLANS TO REOPEN ECONOMY THAT DEPEND ON TESTING

PLANS DEPEND ON TESTING MORE AMERICANS THAN HAS BEEN POSSIBLE

POSSIBLE PLATEAU IN NEW YORK REVIVING WHITE HOUSE OPTIMISM

“We Remain Open” – Wall Street Banks Are Already Calling Traders Back To The Office As Greed Trumps Fear

Wall Street’s famously type-A culture has always prized those who sacrifice their own well-being – physical, emotional or otherwise – for the good of the firm.

Never before has this conviction been put to such a high-stakes test. Late last week, WSJ broke a story claiming 20 traders on a desk at JPM’s Manhattan headquarters had all been sickened after the bank asked traders to come into the headquarters on March 9, a day that will be remembered as one of the most brutal sessions in market history, which presumably netted the bank a major windfall in trading revenue (that day, the bank traded more equities than it ever did during a single day).

Because some of the WFH and back-up offices across the river were having technical difficulties, the bank had asked all of its traders to return to its Manhattan headquarters, despite widespread worries abut the virus.

Now, those traders will likely be celebrated by their colleagues once all of this over for refusing to be cowed by the corona.

While Larry Kudlow and Steven Mnuchin have promised that the administration won’t reopen the economy until it’s safe, it looks like the big banks and their trading desks simply can’t wait that long. With their “essential” employee designation making it easier to call them back, Bloomberg reports that more banks are asking employees to return to the office, or back-up emergency spaces, because trading desks simply can’t handle all the volume without all of their equipment handy.

One JPM trader in London said the bank never seemed to put his team’s health first; initially, they were crammed into a basement in a back-up building outside London with a bunch of back-office humps. Then, the humps were moved, but the traders still didn’t have enough space to social distance.

Understandably, the handling of the situation has led to something of a hit to moral, like a similar incident at Bank of America, where a trader was actually exposed. Some traders at Cantor Fitzgerald affiliate BGC Partners, a high-frequency trading firm, told BBG that management sent emails with conflicting messages.

Inside BGC Partners, an affiliate of Cantor Fitzgerald, workers received a memo marked “important” last month notifying them that no government orders were stopping them from showing up. “We remain open,” the memo said. “Driving to the offices and using mass transit are permitted in order to travel to and from our office.” Some BGC employees privately complained they felt pressured to keep coming downtown — even as other memos laid out the option of working from home. A BGC spokesman declined to comment.

Though, to be fair, others said the firm acted responsibly by assigning skeleton crews to run trading floors at disaster recovery sites or the main office. Several traders shared stories about managers sending their entire desks to work from home after one worker got sick.

One member of a JPM sales team said management’s naming-and-shaming tactics were on full display in an email chain connecting 100 people at the bank as they sought to work out in-office scheduling for the ‘skeleton crews’.

One worker on the sales team noticed a colleague wasn’t on the list and asked where he’d be.

“Corona Town, U.S.A.,” the person wrote back. Then one of the bank’s credit-trading leaders, Nicholas Adragna, weighed in: “The trading desk will be in the office unless they have a medical condition with a dr’s note.”

More than 100 employees were on the message chain seen by Bloomberg, and some were horrified. It came soon after an outbreak of Covid-19 inside JPMorgan’s Madison Avenue headquarters, in which at least 16 people tested positive on a single trading floor. Some employees complain they’re getting conflicting messages from middle and senior managers about coming into offices, where billions of dollars of profit are at stake, and that they would rather follow the advice of government officials to hunker down at home.

Others described at-times intense pressure from managers for sick workers to continue working when they should be resting. Another banker said he kept working until his symptoms were too severe, and once he reached that point, managers gave him plenty of time off to recover.

The final press has been quick to bash the banks for prioritizing their own greed over employees’ well-being, not exactly new territory for Wall Street.

But here’s the thing: As we explained earlier, with equity markets still seeing massive swings, many are worried about liquidity drying up with so many traders working from home. Many dealers working remotely don’t have the full capacity to transact. The result is wider spreads, less efficient price discovery and – sometimes – face-melting selloffs.

Just How “Cheap” Is The Market? Here Is The Shocking Answer

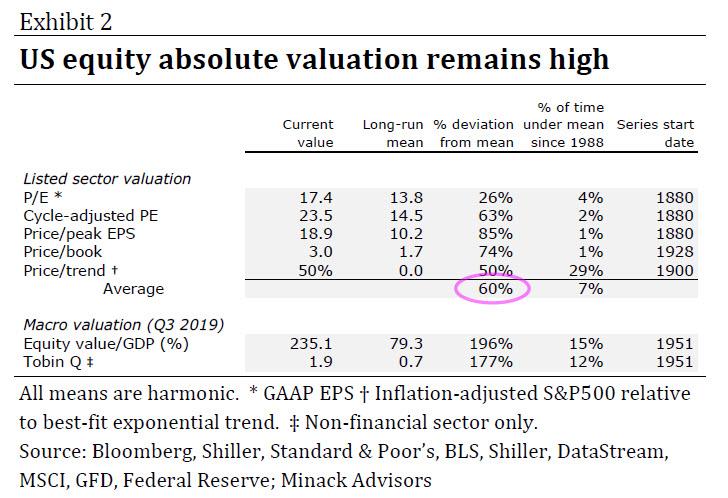

Two weeks ago, when stocks had plunged as lows as 2,250 and staged a modest rebound after the Fed went all in with its “nuclear” intervention, one emerging narrative used by the bulls to justify buying stocks was that equities had dropped to a much cheaper level from a valuation perspective.

However, as Gerry Minack from Minack Advisors wrote at the time, that was hardly the case, and while equities were indeed cheaper, they were hardly “cheap.” As Minack wrote in a daily note from March 25, “while US equities are cheaper now than they were, they are not cheap relative to long-run averages. That is true for all the absolute valuation measures I follow”

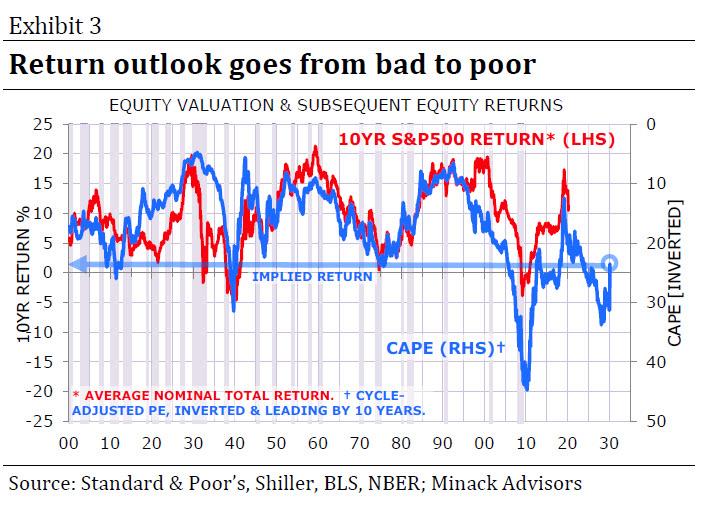

One also has to consider the context: in January the absolute valuation measures were, on average, 111% above their long-run averages. Consequently, as Minack wrote, “the return outlook was terrible. Now valuations point to higher, but still poor, returns. Exhibit 3 shows one example.”

Another problem: nobody has any idea where earnings will end up as a result of the coronavirus “coma”, which has ground the global economy to a halt. Yet even if one assumes a material drop in S&P EPS, one also has to shrink P/E multiples as the US economy is entering a recession, if not depression.

Which is why, as Minack wrotes, “valuation is rarely a good timing guide for investors. But cheap markets generally generate above-average returns over the medium term, and therefore provide investors with a margin of safety when they do buy an asset. However, equities now are not very cheap. US equities are expensive. Prospective returns on US equities remain poor and they now offer very little margin of safety.”

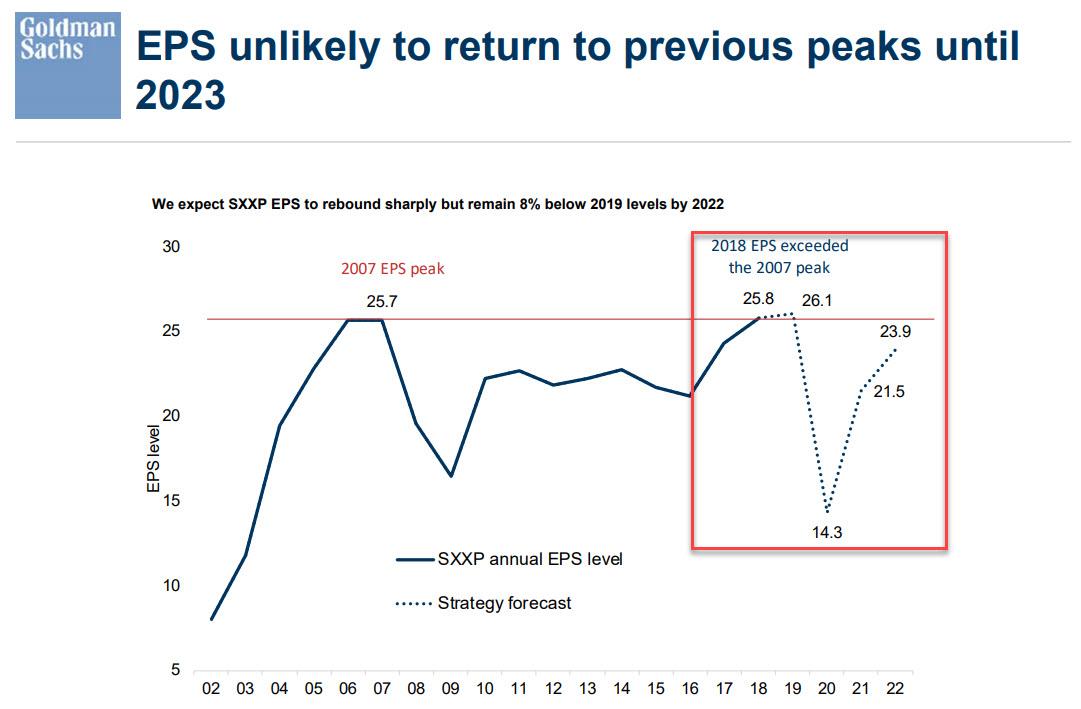

Adding to the confusion is that as of late March, stock markets were expecting only a relatively modest EPS decline.

Looking at the chart above, the former Morgan Stanley strategist, said that the it “seems optimistic” predicting that “there is likely to be a Depression-like decline in activity in the near term” and concluding that “the risk-reward tilts towards buying equities if, say, the S&P500 is 40-50% down from its recent peak, which is 20-30% below its latest close.

In retrospect he was right, because just a few days later Goldman predicted a drop of up to 45% in 2021, which meant that earnings would not return to prior peaks until 2023 (assuming everything worked out as expected).

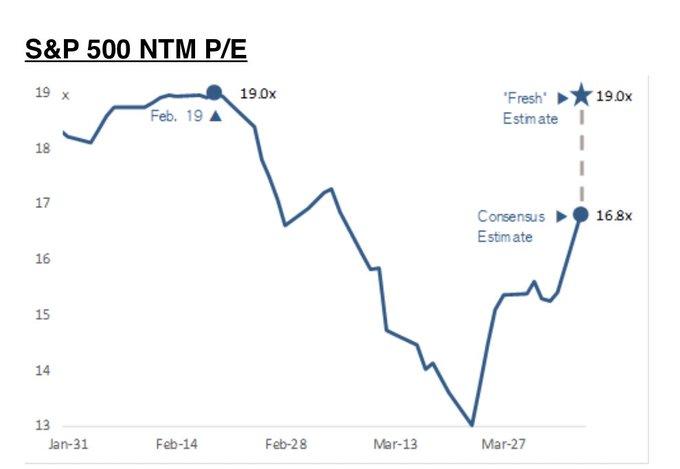

Fast forward to today, when Credit Suisse chief equity strategist Jonathan Golub – usually one of the most bullish Wall Streeters – posted a quick observation suggesting that any “temporary” cheapness in stocks hit in late March was long gone for the simple reason that forward earnings have plunged. As a result, as of noon when the S&P 500 had risen as much as 22% from March 23 lows, forward stock multiples had surged right back 19.0x.

Why is this notable? Because as Golub writes, “this is the same level the S&P500 held on Feb 19, the all-time high.”

In other words, anyone buying stocks today, at least before the violent last hour swoon, was paying for the earnings multiple one could buy in late February, when stocks were at all time high above 3,330. And that, in a nutshell, is how cheap stocks are today ahead of the imminent breathtaking plunge in corporate profits which will be revealed next week when companies report Q1 earnings and reveal their expectations for the second quarter and rest of the year.

Burglaries, Thefts Up More Than 75% In Major Cities Amid Coronavirus Lockdown

Burglaries and thefts have been spiking in major cities across America, as police have been told to curtail enforcement activities during the coronavirus lockdown, and prisons across the country let low-level offenders out early to prevent outbreaks in overcrowded facilities.

In Seattle, burglary cases in the city’s west precinct were up 87% over the preceding 28 days, according to the Seattle PD’s internal crime database, which includes downtown Seattle. The spike coincided with a county policy prohibiting most misdemeanor jail bookings.

“This is a number we’re going to work very hard to reverse in the coming weeks,” SPD spokesman Sgt. Sean Witcomb told the“Jason Rantz Show” on KTTH.

In New York City, burglaries of commercial establishments are up 75% between March 12, when a state of emergency was declared by Mayor Bill de Blasio, and March 31. 254 burglaries of businesses were recorded vs. 145 for the same period last year, according to the Wall Street Journal.

“We knew with the closing of many stores that we could see an increase and, unfortunately, we are,” said NYPD Chief of Crime Control Strategies Michael LiPetri.

Last week, masked thieves made off with $1.3 million in jewelry from a Bronx jewelry store by entering an adjacent business, drilling a hole in the wall, and entering through a closet.

Also contributing to the spike in crime is New York’s new no-bail law which went into effect on January 1st. The new law prohibits pretrial detention for most misdemeanors as well as certain nonviolent felonies.

On the bright side, while commercial burglaries have increased during the pandemic – rapes, murders and assaults have fallen approximately 20% in New York vs. the same period in 2019 – dropping from 4,670 to 3,740 a year earlier.

In Houston, burglaries have risen nearly 20%, while aggravated assaults of spiked by 19.3%. Domestic violence incidents have risen six percent, according to KTRK. The increases come as Harris County readies a list of nonviolent inmates for release amid the pandemic.

Many businesses throughout Harris County have been closed for the past two weeks, during which we have seen an 18.9 percent increase in burglary of businesses.

Let’s hope people who burglarize vehicles, resideces, and buildings aren’t released in large numbers.

In the hours after Harris County Judge Lina Hidalgo confirmed the intention to release certain inmates from a “ticking time bomb” situation, Acevedo, whose police department is the largest user of the jail, revealed he had not discussed the plan with county leadership.

“While I can’t speak to a plan I have not seen or been consulted on, my position on release is well documented on my Twitter feed and in previous media interviews,” the chief tweeted. “Let’s hope people who burglarize vehicles, residences and buildings aren’t released in large numbers.” –KTRK

San Francisco, meanwhile has seen a slight increase in motor vehicle theft and robbery, though assaults, burglaries and larceny has dropped over between January 1st and April 5th vs. the same period in 2019 according to the city’s crime dashboard. That said, domestic violence incidents are on the rise, and restaurants have been targeted by vandals and break-in attempts despite covering their windows and doors with plywood, according to SF Eater.

We wonder what these cities will look like in another four months?

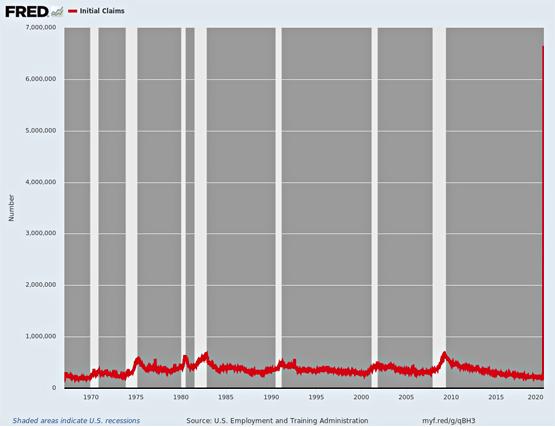

Based on the shocking 6.6 million of new unemployment claims, we’d bet they’ll be some explosive political fireworks soon in this country about Covid-containment versus keeping the main street economy alive. There have now been an unprecedented, off-the charts 9.96 million new unemployment claims in the last two weeks.

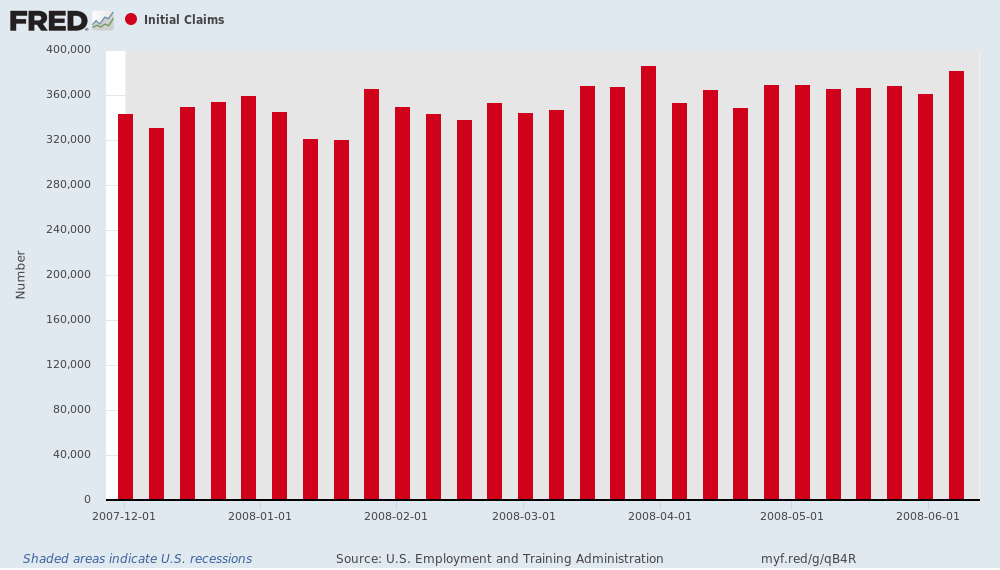

For point of reference, it took fully 28 weeks to generate the same level of cumulative new claims after the beginning of the Great Recession. During that interval, the largest weekly number was 387,000 during the week of March 29, 2008.

Even when you scroll forward (not shown) to the worst week after the Lehman Bankruptcy meltdown commenced on September 15, the peak number was only 665,000 during the week of March 28, 2009. So today’s new claims number was 10X higher!

So, yes, some politically incorrect pundit is likely to note that there are now:

47 jobless workers for every confirmed coronavirus case;

320 jobless for every hospitalization; and

2,112 jobless for every coronavirus death.

Moreover, it virtually certain that cumulative initial claims will hit 20 million before the end of April, thereby doubling the above ratios. That is to say, do they really want 100 jobless workers for every case of a bad winter flu?

Well, yes, it seems that our establishment betters can’t get rabid enough urging on a total shutdown of the US economy.

Indeed, the thinly disguised subtext in the whole daily MSM narrative for the last couple of days has been that the benighted governors of the Red States are not doing their part to order their economies into instant cardiac arrest. But it took the perennially obnoxious liberal columnist for the New York Times, David Leonhardt, to come right out and say it.

Thus, opined Leonhardt: Donald’s Trump’s minions have been putting the public health in grave danger.

Much of red America is finally going on lockdown.

After resisting the pleas of public health experts for days, the governors of Florida, Georgia, and Mississippi – all states won by President Trump in 2016 – announced yesterday that they will be ordering their residents to stay home, effective Friday.

The turnabout from Florida’s governor, Ron DeSantis, was especially stark….These new lockdowns are welcome, because they will help slow the virus. But they are also coming much later than they should have, A big reason that the virus has been recently spreading more rapidly in the United States than in Europe or Asia is the slow response from American political leaders.

Trump spent almost two months falsely claiming the virus was going away…Many Republican governors have chosen to echo him, DeSantis, for instance, acted as if he could stop the virus by merely keeping New Yorkers out of his state.

There you have it – a shrill dump of left-wing agitprop and lies that are coming front and center to the debate real soon. Namely, the charge that Trump and his GOP minions caused the coronavirus crisis – so now the regulatory machinery and fiscal resources of the state must be mobilized without limit to wrestle the monster to the ground.

Then again, by the statistics you might conclude that DeSantis has a point about pulling the welcome mat from New Yorkers. As of yesterday, nearly 62,000 Floridians have been tested, but the infection rate has been just 10.2% compared to New York’s 37%; and it’s infection rate per 100,000 population was just 29 compared to New York’s 389.

That’s right. The infection rate in New York is 13.4X higher than Florida’s, while New York’s hospitalization and death rates are 21X and 22X higher, respectively.

Yet this sanctimonious Big Apple brat has the gall to accuse the governor of Florida of being a Republican moron or even criminal.

The fact is, DeSantis was right not to go full retard shutdown. For crying out loud, the coronavirus death rate in Florida to date is just one-third of a person per 100,000 population. At some point the idea of quarantining the aged, infirm and vulnerable rather than shit-canning the entire economy might make more sense.

But as of the moment, the liberal commentariat and it Washington collaborators are on their high horse and won’t rest until they have intimidated the entire country into a heretofore unimaginable Economic Cardiac Arrest. In fact, you might as well call it the Anderson Cooper/Chris Cuomo Memorial Depression and be done with it.

After all, it’s the same old shtick. Namely, that the liberals’ unhinged case for plenary economic shutdown is allegedly driven by “science” and that anyone who dares question the fashionable prescriptions is some kind of antediluvian rube.

Of course, in many ways the Donald is exactly that – such as with respect to the entire economic, financial and monetary policy file. There his views are downright neanderthalish.

But that’s what makes this whole Covid-19 imbroglio so forebodingly dangerous. The MSM and Washington political class are turning it into the next phase of the RussiaGate/UkraineGate/Impeachment inquisition against the Donald; and the litmus test of choice is, effectively, shut-it-down-and-lock-them-up at home from coast-to-coast; and keep them there until the Donald’s Greatest Economy Ever is pounded to smithereens.

Ordinarily, the main street economy would have a fighting chance against that kind of ad hoc statist assault on production, which is now accelerating to a full gallop. That’s because the business community – large, small and in-between – would be descending on Washington in waves that would put even the Zulu army to shame.

But not this time. The fact is, we have an Ersatz Socialist and economic primitive in the Oval Office who has managed to club to death like a baby seal whatever was left of GOP fiscal, monetary and free market orthodoxy.

So the $2.2 trillion Everything Bailout (soon to be $4 trillion) was effectively a giant advance from Uncle Sam to hold one-and-all harmless for any lost ground occasioned by the shutdowns which are now sweeping across America like a prairie fire.

In general terms, UI and helicopter money will be keeping paychecks close to 100% of take home, while trillions of easy-peasy loans/grants to business will also cover paychecks (double dip?) for employees – working and not working – as well as most other cash outflows for utilities, overheads, insurance, loan service and the CEOs’ paychecks.

Yet when nearly everyone is held harmless, three very bad things are sure to happen. To wit:

The statist/Dem push to shutdown the Trumpified economy will face far less resistance from business and workers and thereby be far more prolonged;

The normal processes of free market adjustments including economizing, layoffs, price/wage/cost cuts, negotiated rent and other payment deferrals, closure of businesses and malinvestments that weren’t viable anyway will be drastically thwarted; and

Uncle Sam will end up taking on trillions of needlessly incurred debt in order to temporarily back-fill GDP that the country could readily do without and to prop up a zombified business sector that will be a long-term albatross on growth.

But in the interim, the eruption of statist intervention and fiscal profligacy will reach literally hysterical excesses. That’s because the economic contraction now upon us is nothing like your grandfather’s recessions, which were triggered by the Fed and the collapse of credit and stock market cycles.

By contrast, this one was being prepped by the Fed for years as it fostered egregious excesses of debt, speculation and hand-to-mouth fragility throughout the system. But it is actually being triggered by sudden shutdown edicts from governors, mayors and public health authorities – amplified by both prudent and hysterical precautionary actions being undertaken by the broad public.

It is therefore proceeding with warp speed, as today’s claims data dramatically illustrates. When placed in historical context, the reported 6.6 million of initial unemployment claims (thin red line on the right margin) filed thru last Saturday truly give the notion of being “off the charts” a wholly new definition.

And here is where 30-years of incessant monetary and fiscal intervention and “stimulus” will take its toll. That’s because America’s chattering classes, politicians and business leaders alike have been house-trained on the misbegotten assumption that capitalism has a death wish; and that once it goes into a contraction there is nothing stopping it from disappearing into an economic black-hole, save for the heroic interventions of the state and its central banking branch.

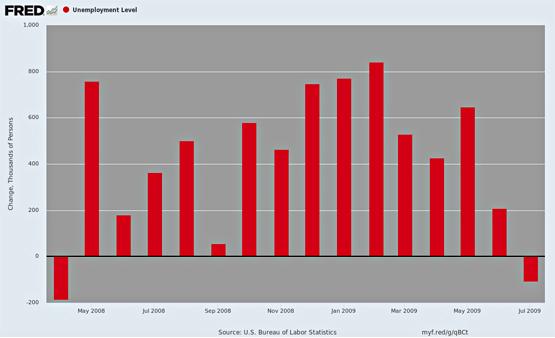

What is coming down the pike in terms of the “incoming data”, therefore, will generate sheer panic in the Imperial City and on Wall Street, too. Thus, as recently as February 19 when the stock market was 35% higher, the talking heads put the odds of recession at essentially zero. After two more weeks of the massive claims reported today, however, the BLS unemployment survey taken in mid-April is likely to find upwards of 15 million newly unemployed and a U-3 unemployment rate of 12-15%.

That will rattle their teeth to the bone on both ends of the Acela Corridor. After all, last time they went into an end-of-the world panic mode during the Great Recession, it took the U-3 rate 31 months from the cyclical low of 4.4% in March 2007 to reach the 10.0% peak in October 2009.

Likewise, the worst quarterly GDP SAAR during that downturn was 8.7% in Q4 2008, while Q2 2020 could hit 3X that rate at negative 25% or worse.

Indeed, the shocker will come on the first Friday of May when the monthly number of newly unemployed workers will be reported for April.

During the bottom of the Great Recession in February 2009, that number peaked at 840,000, but April’s gain could come in at 15X-20X that level.

So get set for a hideous hair-on-fire orgy of monetary and fiscal stimulus demands on both ends of the Acela Corridor, as if we have not gone off the deep-end already.

Indeed, when you add in the automatic stabilizer outlays to the $2.2 trillion Everything Bailout, the hemorrhage of Federal spending and borrowing will be damn near incalculable.

By the end of April, for instance, there will easily be 15 million continuing unemployment insurance claims: Even under pre-existing eligibilities and benefit levels (which were massively expanded by the Everything Bailout) the annualized run rate of outlays would rise from $28 billion in FY 2019 to upwards of $250 billion.

In short, this is merely not your grandfather’s recession; it’s actually a Bubble Finance era Doomsday Machine.

With the establishment media keeping the US economy on lockdown – and we mean that literally, as even Dr. Fauci is now saying there should be no relaxation of the economic freeze until there are zero new cases and zero deaths – and the Trumpified GOP keeping the spending machine and Fed printing press at full throttle until at least the November election, it is truly impossible to imagine the level of madness ahead.

The tragedy, of course, is that the blistering fiscal and financial calamity ahead is totally unnecessary. Public health measures to contain the virus until the summer heat kills it off could be far more targeted and less intrusive via a policy of protective isolation for the vulnerable populations, and maximum flexibility and personal protection (masks, gloves etc.) for the workers and participants in daily commerce.

Trump Admin Wants To ‘Work Directly’ With Wuhan Institute Of Virology

Surprisingly, even CNN has much-belatedly and very unexpectedly started posing critical questions centered on the Wuhan Institute of Virology while doing a review of various theories as to COVID-19’s origins. CNN on Monday cited that “one expert, a chemical biology professor and bioweapons expert at Rutgers University, has suggested to several media outlets that the lab-accident theory has credence.”

“The possibility that the virus entered humans through a laboratory accident cannot and should not be dismissed,” Dr. Richard Ebright told CNN in an email Sunday. This comes more than two months after the mainstream media went ballistic over our posing the same questions. In late January we had asked whether a prolific Chinese scientist who was experimenting with bat coronavirus at a level-4 biolab in Wuhan China was responsible for the current outbreak of a virus which is 96% genetically identical – and which saw an explosion in cases at a wet market located just down the street.

And now this via Reuters Tuesday: “A senior Trump administration official urged China on Tuesday to allow the United States to work directly with laboratories in Wuhan on research into the novel coronavirus, saying this was critical to saving lives globally.”

Wuhan Institute of Virology, via Pharma Industry Review

“We would appreciate the opportunity to work directly with their Virology labs in Wuhan to share whatever research they have,” the Trump admin official said.

“Since the pandemic originated in Wuhan, we think cooperation with PRC medical and disease experts there is critical to saving lives globally.”

Well yes, it’s about time there’s some official movement centered on the very place most likely to hold the keys to the mystery of both COVID-19’s origins and how to combat it and/or prevent it.

The admin statement is specifically in response to an apparent fast thawing of tensions between Beijing and Washington on the outbreak, after a month-long war of words trading accusations over its handling. China’s ambassador to the US Cui Tiankai, said in a NYT op-ed Sunday that despite recent “unpleasant talk” between the two centered on the pandemic, it’s now time for “solidarity, collaboration and mutual support.”

Scientists inside the Wuhan Institute of Virology in Wuhan, China. AFP via Getty

In a rare belated moment, the senior Trump administration official zeroed in on the Wuhan Institute of Virology Biosafety Level 4 Laboratory, the county’s top lab dedicated to the research of severe infectious diseases, which again happens to be located a mere miles from the Wuhan wet market which witnessed the first cases:

“If Ambassador Cui is saying that China is willing to cooperate with the U.S., we would appreciate the opportunity to work directly with their Virology labs in Wuhan to share whatever research they have, since they’ve known about it and have been fighting it for at least a month longer than our scientists here in the U.S.,” the official said.

It also just so happens that Wuhan at the start of this week lifted its lockdown after infections have dramatically declined to near zero new infections per day.

It must be remembered that starting in February the director of the White House’s Office of Science and Technology Policy (OSTP), Kelvin Droegemeier, requested in a letter to the National Academies of Sciences, Engineering, and Medicine, that scientific experts “rapidly” look into the origins of the deadly COVID-19 outbreak.

The White House letter said this remained crucial “to inform future outbreak preparation and better understand animal/human and environmental transmission aspects of coronaviruses.”

Beijing’s response to this latest initiative to open up the Wuhan lab for cooperation with US scientists investigating the origins of the virus is sure to be interesting. And a potential lack of response altogether, a likely prospect, will also be telling.

{kind=link}

{kind=link}