Another Doctor Reports Dramatic Improvement In COVID-19 Patients Using Trump-Touted Treatment

As pro-establishment mouthpieces downplay the efficacy of hydroxychloroquine to treat COVID-19 as “anecdotal” with “little evidence that the treatment is effective,” yet another doctor treating has claimed dramatic improvement in coronavirus patients within hours of taking the anti-malaria drug in combination with two other medications.

Los Angeles doctor Anthony Cardillo says he’s seen very promising results when the Trump-touted drug is combined with zinc for severely-ill coronavirus patients.

“Every patient I’ve prescribed it to has been very, very ill and within 8 to 12 hours, they were basically symptom-free,” Cardillo told Eyewitness News, adding “So clinically I am seeing a resolution.”

Cardillo, CEO of Mend Urgent Care, says that the drug must be used in conjunction with Zinc, as the hdroxycholoroquine opens a ‘channel’ for the mineral to enter cells and prevent the virus from replicating.

Los Angeles Doctor, Dr. Anthony Cardillo speaks of potential benefits of Hydroxychloroquine combined with Zinc. pic.twitter.com/fQ68HpsKup

Commonly used for lupus and arthritis, hydroxychloroquine has been approved by the FDA for limited emergency authorization to treat COVID-19 patients.

That said, Cardillo warns that the treatment should only be reserved for those with moderate to severe symptoms due to concerns over shortages.

“We have to be cautious and mindful that we don’t prescribe it for patients who have COVID who are well,” he said, adding “It should be reserved for people who are really sick, in the hospital or at home very sick, who need that medication. Otherwise we’re going to blow through our supply for patients that take it regularly for other disease processes.”

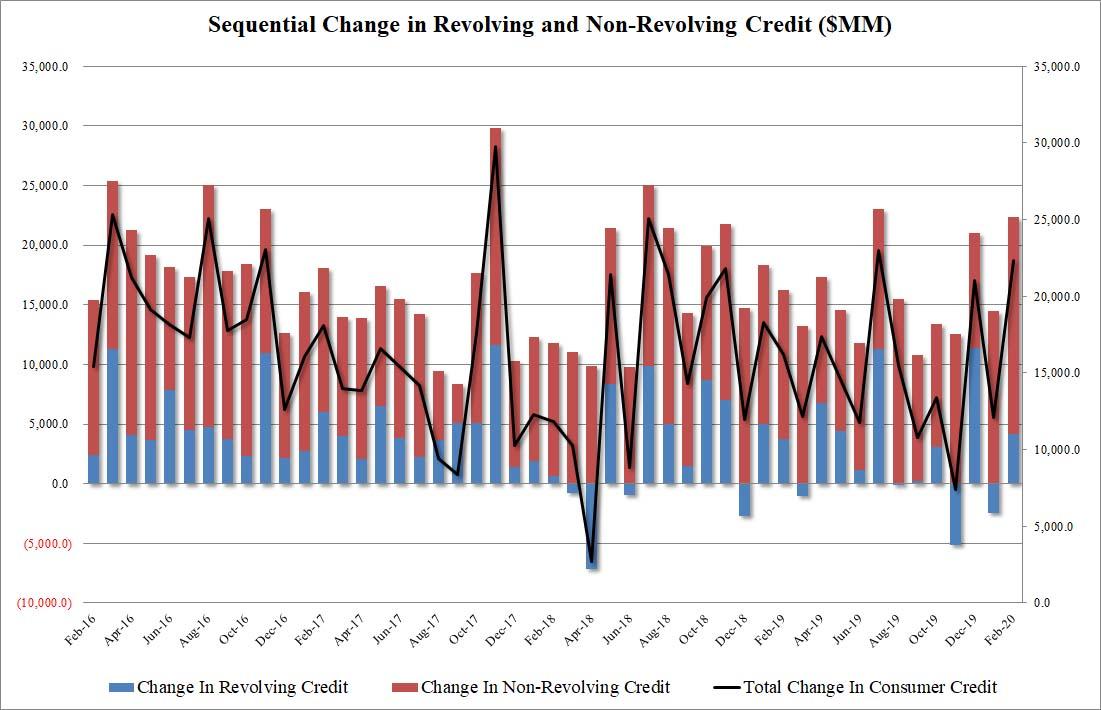

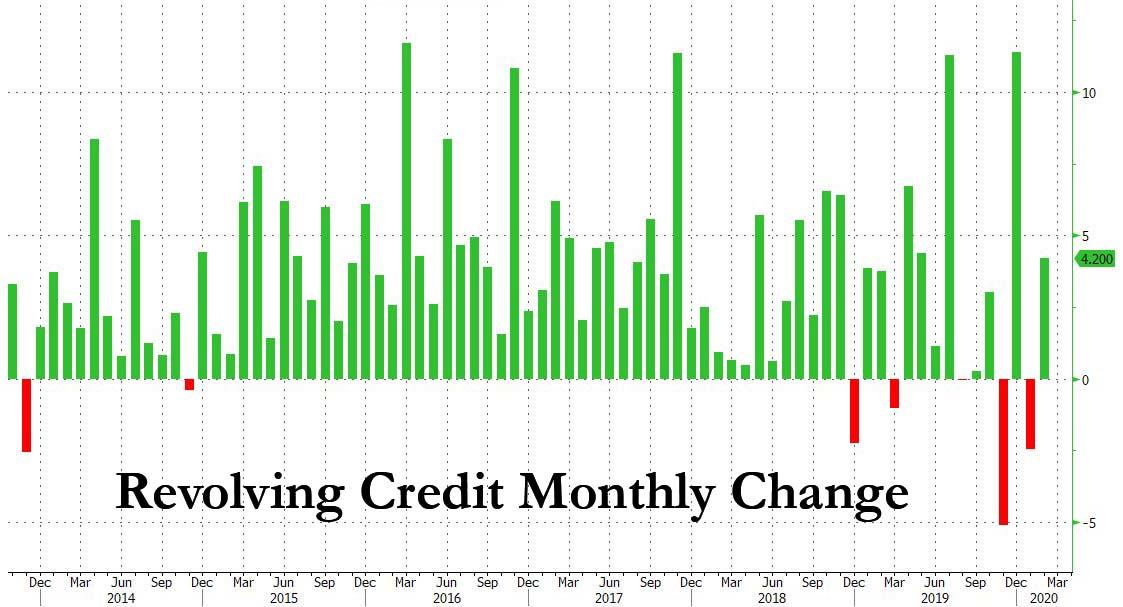

Consumer Credit Soared In February, Just Before The Economy Shut Down

Just like today’s JOLTS report, which as we reported earlier came in far stronger than expected, so today’s consumer credit report was largely meaningless, covering the month of February which unfortunately represented a different world. That said, coming in at $22.331BN this number also shattered expectations of a modest increase in consumer credit from $12BN to $14BN in February, printing nearly twice as high as expected. Whether or not one sees a higher number compared to expectations as a beat or a miss will depend on whether one is a Keynesian or Austrian economist.

Specifically, in February, Revolving credit rose by $4.2BN to a record $1.096 trillion, after shrinking by $2.5 billion the month prior.

At the same time, nonrevolving credit – mostly auto and student loans – rose $18.1BN, also hitting a new all time high of $3.129 trillion.

Alas, as noted above, none of this matters as the world was flipped upside down in March, however next month’s data will be extremely interesting, as it will show whether when faced with an upcoming economic crisis, American households splurged and used their credit card to buy everything they could, or conversely, they hunkered down and entered a savings hibernation. Needless to say, the former could be catastrophic for an economy where 70% of GDP is a function of consumer spending.

One thing however is certain: non-revolving debt, which is incurred mostly when purchasing cars, will plunge in March and may stay at or near zero for a long, long time.

In a new survey of small business owners, almost half (43%) say their livelihood is on the line and they are going to be forced to close permanently if they cannot resume normal activities soon. One in 10 (11%) are less than one month away from permanently going out of business thanks to the government’s response to the coronavirus outbreak.

Additionally, about one in four (24%) small businesses have already shut down temporarily in response to the government’s demands to do so during the COVID-19 panic and overreaction. Among those that have not, 40% say they are likely to close at least temporarily within the next two weeks. This means a total of 54% of all small businesses report that they have closed or expect to close temporarily in the next 14 days.

When asked what proposals might offer the most relief, small businesses indicated support for three key provisions included in the recently enacted Coronavirus Aid, Relief, and Economic Security (CARES) Act:

56% of small business say direct cash payments to Americans would be the most helpful form of aid from the government,

followed by loans and financial aid (30%), and

suspending payroll taxes (21%).

“As the poll results show, small business owners are looking for loans and financial aid to ensure they do not have to shut their doors or go bankrupt because of the coronavirus. American banks are ready to help, but they need clear guidelines from the Administration,” said Neil Bradley, chief policy officer at the U.S Chamber of Commerce.

“American banks will be on the front lines to help businesses survive during this pandemic.”

The biggest help will come in the form of being allowed to reopen and conduct business as they had done. Getting the economy up and running again is going to go the furthest when it comes to saving lives and helping people. At this point, the statistics of the outbreak provided by healthcare professionals no longer support a lockdown, economic shutdown, and the ramifications that have already followed. The government’s overreaction has done more harm than good.

Some small businesses still feel optimistic, however, according to the survey reported by U.S. Chamber. Almost one in four (23%) small business owners expect to hire in the next year.

As a society, we need to do right by those who offer services and get them reopened and return our lives to normal; before the authoritarian government takeover. This pandemic is not the problem and has not been the problem for the past month. The problem is the government’s response to it and the subsequent obedience of many Americans thanks to their own fears pushed down their throats by the mainstream media. Far too many have been inclined to comply with the government’s commands to their own detriment and the fallout is going to be something we have never seen.

The sooner the government backs off the economic shutdown, the better this will be for everyone.

Facing Catastrophe: Loss Of Working Hours To Equal 195m Full-Time Jobs According To UN Agency

Worldwide working hours will be cut by nearly 7% in the second quarter of 2020 due to the coronavirus pandemic, according to a Tuesday statement by the UN’s International Labor Organization. The loss will be equivalent to 195m full-time workers.

Nearly two-fifths of the 3.3 billion global workforce – some 1.25bn workers, are employed in hard-hit sectors, from food services to manufacturing, to real estate and accommodation. According to the report, over 80% of the global workforce live in countries subject to either partial or full lockdowns.

“Workers and businesses are facing catastrophe, in both developed and developing economies,” according to ILO director-general Guy Ryder. “It will hit the most vulnerable the hardest.“

According to the Financial Times, the sheer scale and speed of job losses due to coronavirus has taken world leaders by surprise – after nearly 10 million people in the US filed initial jobless claims during the last two weeks in March. The ILO has warned that the pandemic could result in 25 million lost jobs in 2020 – more than those lost in the 2008 financial crisis.

Many economists expect the US unemployment rate too quickly rise above 10%, with similar results to follow in Europe – which has provided a government wage subsidy to many workers which is designed to limit long-term unemployment.

Mr Ryder said it now seemed likely that more than 30m jobs were lost in the first quarter alone, and the ILO now expected a much more severe short-term impact, using more timely data from business surveys and Google search trends to illustrate what it called “the dire reality of the current labour market situation”. –FT

According to the ILO, the number of working hours globally will decline by 6.7% in Q2 of 2020 vs. the prior quarter – which reflects both layoffs and other temporary reductions in working hours. The equivalent would be 195m full-time jobs based on a 40-hour work week. They came to this conclusion using the historical relationship between working hours and a survey of business conditions among purchasing managers which is published on a monthly basis in various countries.

That said, the surveys may or may not be a reliable guide, as they show most businesses expecting conditions to worsen, but provide no indication of how severe they expect the downturn to be, or how long it’s likely to last. Still, it’s the most timely international data available, as only a handful of nations publish up-to-date administrative data on claims for wage subsidies and benefits.

The sectors most exposed to big falls in output are labour-intensive and employ millions of often low-paid, low-skilled workers who will feel the effects especially badly, the ILO said. They account for the highest proportion of employment in the Americas, Europe and central Asia.

But the ILO also warned that the virus is now spreading to countries where a high proportion of the workforce had no access to social protection; excluding agriculture, more than 70 per cent of workers are in the informal sector in Africa and 90 per cent in India. –FT

A full-year forecast was not provided by the ILO, as it said that the overall unemployment picture will depend on policies adopted by countries to boost labor demand as the economy begins to recover. It suggests the need for cash payments and the transfers of basic goods to the most impacted around the world.

“We are going to be tested ever more strongly as the pandemic extends its reach into the developing world,” said Ryder.

CNN has published a lengthy article suggesting that wearing face masks to guard against coronavirus is racist due to African-Americans not being able to wear them over fears they will be treated like criminals.

Yes, really.

Noting that the CDC has encouraged all Americans to wear face masks in the fight against COVID-19, Trevor Logan, an economics professor at Ohio State University, says he “will not be following this guidance.”

“We have a lot of examples of the presumed criminality of black men in general,” Logan, who presumably isn’t knowledgable about FBI crime statistics, told CNN.

“And then we have the advice to go out in public in something that … can certainly be read as being criminal or nefarious, particularly when applied to black men,” he adds, noting how a black man wearing a face mask “looks like almost every criminal sketch of any garden-variety black suspect.”

On social media and in interviews with CNN, a number of people of color — activists, academics and ordinary Americans — expressed fears that homemade masks could exacerbate racial profiling and place blacks and Latinos in danger. https://t.co/hgJ435erKz

CNN Fernando Alfonso III then references how on social media “a number of people of color — activists, academics and ordinary Americans — expressed fears that homemade masks could exacerbate racial profiling and place blacks and Latinos in danger.”

In other words, the government advising Americans to wear face masks is discriminatory because blacks and hispanics who wear them may be mistaken for criminals.

Whether that is more closely related to institutional racism or the fact that black people and hispancis are overrepresented in crime statistics, I’ll leave to the reader to decide.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

“Fade The Rip”: BofA Warns “Bear Market Far From Over Unless We Escape A Recession”

“Have we hit the bottom?”

Ask 100 traders what their biggest concern about the market is right now, and that will be the answer roughly 100 times. And while the frazzled bulls will be quick to point to the recent massive surge as proof positive the lows have been hit, those with actual market experience such as Nomura will tell you that what we have seen in recent weeks is nothing but a massive short squeeze.

Yet while that may explain the market moves in the recent past what about the future: after all what traders want to know is where stocks go from here, not how we got here.

To answer that question we go to the derivatives team at Bank of America, according to who this – and by “this” we mean the reaction to the unprecedented stimulus unleashed by the Fed on March 23, when Powell unveiled unlimited QE, purchases of corporate bonds, and a slew of other measures, which also marked the lows so far this crisis – may be as good as it gets, because as BofA’s Benjamin Bowel writes overnight, “history shows markets still need to generate significantly more “total volatility” before the bear market ends” which prompts him to recommend to “Fade the rip.“

Here’s how the derivatives strategist deliver his bad news to the bulls expecting nothing but smooth sailing from now on: “bear market rallies are common and historical analogs suggest the S&P could rally to near 3000, but still roll-over and touch new lows before staging a full-fledged recovery.”

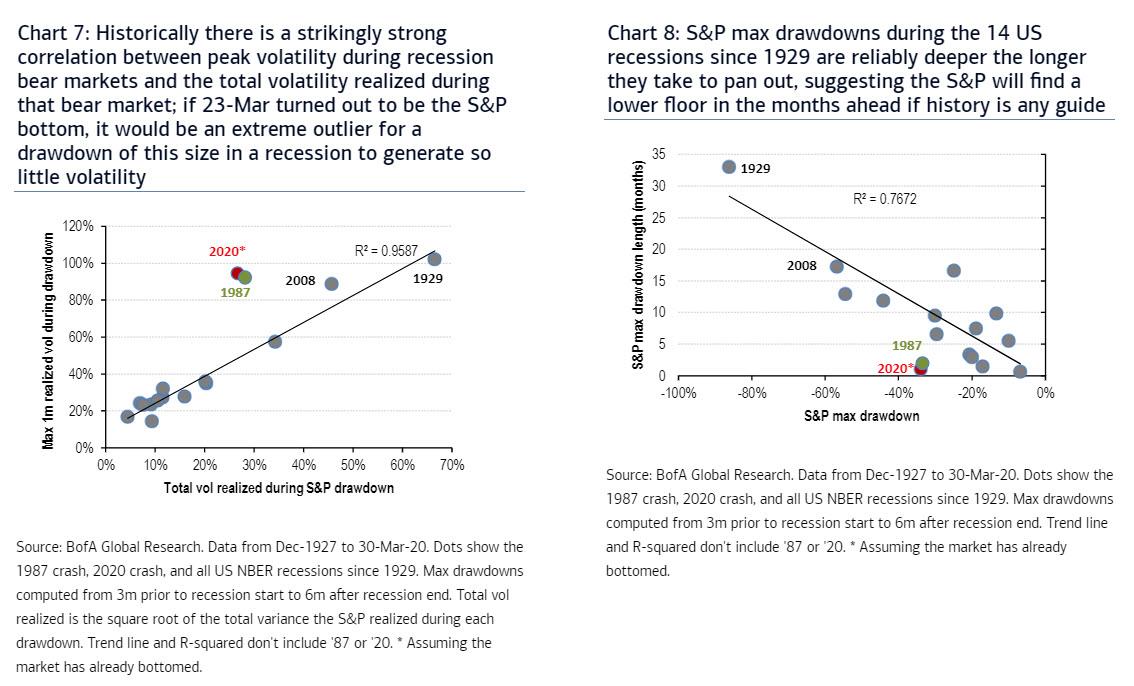

Picking up on what Morgan Stanley said yesterday, BofA writes that looking at markets since 1929, it would be unprecedented if the S&P failed to re-test or even fall below its Mar 23rd low, given the size of the recent drawdown (-34%) and assuming a recession ensues.

Furthermore, unlike a technical shock such as the ’87 crash which did not result in a recession, bear markets that coincide with recessions have very strong relationships between their depth and length, in part as economies carry significant momentum. Among the strongest relationships is between peak volatility and the total volatility generated during the bear market, as volatility decays at a very consistent rate during recessions.

As such, and given 1-month S&P vol recently peaked at 95%, implies we are only about 50% of the way through this bear market (in vol terms). Additionally, BofA’s finding that a recession bear-market of this size on average has lasted about 11 months strengthens the argument that we will likely retest the lows.

There is just one possible wait out: “Only if we were to escape recession (which no one expects) would the Mar-23 low be consistent with history.”

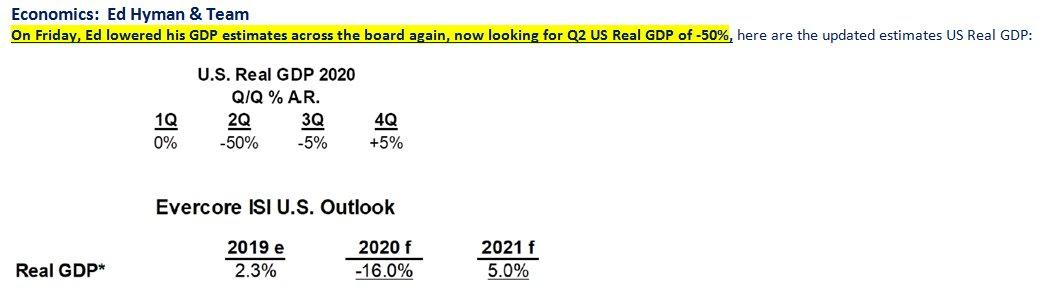

Alas, with GDP set to plunge as much as 50% in Q2 according to Evercore ISI’s Ed Hyman…

… and barely rebound in subsequent quarters (as a reminder a 50% drop has to be followed by a 100% surge to get back to even), the recession – if not depression – will be with us for a long time.

* * *

Below we excerpt the key section from BofA’s latest note, explaining why “this market is still not trading like a recession bear market”

Looking last week at S&P drawdowns during recessions, we concluded that the S&P will find a lower floor in the months ahead (i.e. it is highly unlikely 23-Mar was the low), if history is any guide. We reiterate here that the length and size of the max S&P drawdowns in the 14 US recessions since 1929 are highly correlated; i.e. during recessions specifically there is a strong positive relationship between the length of bear markets and the size of the drawdown. This is not necessarily the case in bear markets outside of recessions, which can be more technical.

The S&P has so far dropped -34% peak to trough this year in around one month, a sharp selloff more similar to the technical, non-recessionary ’87 crash than to a bear market coinciding with a recession. Hence, assuming a recession firmly built into consensus, this year’s drawdown would be an extreme outlier if the S&P ends up not falling to new lows (Chart 8).

An even stronger historical relationship uncovered by BofA is that between peak volatility (max 1m realized vol) and the total vol generated by recession bear markets, as shown in Chart 7. As shown in Chart 8, the current drawdown has so far been more similar to the 1987 crash, and it would be an extreme outlier for a drawdown of this size in a recession (particularly one as deep as it is forecasted to be) to generate so little volatility.

BofA’s conclusion, again, “we think it’s instead more likely that we haven’t seen the bottom in equities yet.”

The cascading failures that have been set into motion by this “coronavirus shutdown” are going to make the financial crisis of 2008 look like a Sunday picnic. As you will see below, it is being estimated that unemployment in the U.S. is already higher than it was at any point during the last recession. That means that millions of American workers no longer have paychecks coming in and won’t be able to pay their mortgages. On top of that, the CARES Act actually requires all financial institutions to allow borrowers with government-backed mortgages to defer payments for an extended period of time. Of course this is a recipe for disaster for mortgage lenders, and industry insiders are warning that we are literally on the verge of a “collapse” of the mortgage market.

Never before in our history have we seen a jump in unemployment like we just witnessed. If you doubt this, just check out this incredible chart.

Millions upon millions of American workers are now facing a future with virtually no job prospects for the foreseeable future, and former Fed Chair Janet Yellen believes that the unemployment rate in the U.S. is already up to about 13 percent…

Former Federal Reserve Chair Janet Yellen told CNBC on Monday the economy is in the throes of an “absolutely shocking” downturn that is not reflected yet in the current data.

If it were, she said, the unemployment rate probably would be as high as 13% while the overall economic contraction would be about 30%.

If Yellen’s estimate is accurate, that means that unemployment in this country is already significantly worse than it was at any point during the last recession.

And young adults are being hit particularly hard during this downturn…

As measures to slow the pandemic decimate jobs and threaten to plunge the economy into a deep recession, young adults such as Romero are disproportionately affected. An Axios-Harris survey conducted through March 30 showed that 31 percent of respondents ages 18 to 34 had either been laid off or put on temporary leave because of the outbreak, compared with 22 percent of those 35 to 49 and 15 percent of those 50 to 64.

As I have documented repeatedly over the past several years, most Americans were living paycheck to paycheck even during “the good times”, and so now that disaster has struck there will be millions upon millions of people that will not be able to pay their mortgages.

It is being projected that up to 30 percent of all mortgages could eventually default, and when you add the fact that millions upon millions of Americans will be deferring payments thanks to the CARES Act, it all adds up to big trouble for the mortgage industry…

A broad coalition of mortgage and finance industry leaders on Saturday sent a plea to federal regulators, asking for desperately needed cash to keep the mortgage system running, as requests from borrowers for the federal mortgage forbearance program are pouring in at an alarming rate.

The Cares Act mandates that all borrowers with government-backed mortgages—about 62% of all first lien mortgages according to Urban Institute—be allowed to delay at least 90 days of monthly payments and possibly up to a year’s worth.

Needless to say, many in the mortgage industry are absolutely furious with the federal government for putting them into such a precarious position, and one industry insider is warning that we could soon see the “collapse” of the mortgage market…

“Throwing this out there without showing evidence of hardship was an outrageous move, outrageous,” said David Stevens, who headed the Federal Housing Administration during the subprime mortgage crisis and is a former CEO of the Mortgage Bankers Association.

“The administration made a huge mistake bringing moral hazard in and thrust extraordinary risk into the private sector that could collapse the mortgage market.”

Of course a lot of other industries are heading for immense pain as well.

At this point, even JPMorgan Chase CEO Jamie Dimon is admitting that the U.S. economy as a whole is plunging into a “bad recession”…

Jamie Dimon said the U.S. economy is headed for a “bad recession” in the wake of the coronavirus pandemic, but this time around his company is not going to need a bailout. Instead, JPMorgan Chase is ready to lend a hand to struggling consumers and small businesses.

“At a minimum, we assume that it will include a bad recession combined with some kind of financial stress similar to the global financial crisis of 2008,” Dimon, the CEO of JPMorgan Chase, said Monday in his annual letter to shareholders.

And the longer this coronavirus shutdown persists, the worse things will get for our economy.

Sunday on New York AM 970 radio’s “The Cats Roundtable,” economist Stephen Moore weighed in on the potential impact of the coronavirus to the United States economy.

Moore warned the nation could be “facing a potential Great Depression scenario” if the United States stays on lockdown much past the beginning of May, as well as an additional amount of deaths caused by the raised unemployment rate.

The good news is that the “shelter-in-place” orders all over the globe appear to be “flattening the curve” at least to a certain extent.

The bad news is that we could see another huge explosion of cases and deaths once all of the restrictions are lifted.

Of course that is only happening because most people are staying home, but having people stay home is absolutely killing the economy.

And if people stay home long enough, a lot of them will no longer be able to pay the mortgages on those homes.

Our leaders are being forced to make choices between saving lives and saving the economy, and those choices are only going to become more painful the longer this crisis persists.

Let us pray that they will have wisdom to make the correct choices, because the stakes are exceedingly high.

Credit Suisse Turned To Its Own Rich Clients For Emergency Funding

Why rely on central banks when your own clients have more capital than most central banks? That is the question the second biggest Swiss bank asked itself in recent weeks during the unprecedented market crash and collapse in liquidity, when it wasn’t clear when and under what conditions central banks would step in.

As a result, Credit Suisse turned to its own ultra-high-net-worth clients to bolster its balance sheet and its ability to lend as markets sank last month and companies started drawing down credit lines to weather the coronavirus pandemic, according to Bloomberg, which reported that institutional clients, family offices and billionaires were offered notes that pay a 2% interest on money that’s kept with the Swiss lender for a least a year, according to a person familiar with the matter.

The notes, which were issued as a form of structured product, were sold in the first weeks of March to shore up lending capacity as coronavirus infection rates began to rise sharply.

“Structured products are part of our product portfolio, specifically tailored to address the needs of professional investors and wealthy private clients,” Credit Suisse told Bloomberg.

“Typically, those products have terms of several years and can –- depending on their risk profile and lifetime — generate very attractive returns.”

Demonstrating vividly why its critical to have not just very wealthy friends, but even wealthier clients, the structured products drew interest from investors seeking higher yields amid negative interest rates on deposits in Switzerland (yes, 2% is now considered a very high yield). As a result, some clients moved money out of rival banks to buy the notes, according to another person, whose bank has seen investors leave to buy Credit Suisse’s products.

Of course, it’s only a matter of time before the rival banks offer a similar product with a slightly higher rate and the money is moved back from CS to them, but that’s the topic of another story 2 weeks from now.

With negative interest rates of 0.75% on deposits in Switzerland, Credit Suisse and its biggest rival UBS Group AG had previously begun to charge wealthy clients for excess cash holdings, leading to some outflows as investors sought better returns. While Credit Suisse already has sufficient liquidity – or so it claimed – it issued the notes to boost lending capacity further in anticipation of a period of increased volatility, a Bloomberg source said, not to mention even greater liquidity needs.

Translation: the worst of the current crisis has yet to pass.

The COVID-19 pandemic has really highlighted how differently economists and noneconomists think. All over the world, variations of the same discussion have taken place over the last week or so. It goes as follows.

An economist discusses the cost of the governmental responses to the pandemic and is quickly met with accusations of cynically trying to “put a price on a life.” The economist camp tries to explain its reasoning while the noneconomist camp is horrified that anyone would “let old people die to protect the rich” or “prioritize economy over health.”

What is really going on here is that economists and noneconomists have vastly different mindsets. Economists are constantly thinking in tradeoffs. It is second nature. It lies at the very core of economics. All of the problems economists attempt to solve involve various possible choices and finding the most optimal one.

This is based on the understanding that we live in a world of scarcity. All means are scarce, so allocating them to serve certain ends must necessarily leave other ends unsatisfied. Economists attempt to ensure that scarce resources are used efficiently. This is not as simple as putting two numbers on a piece of paper and choosing the largest one. All choices happen under uncertainty. We do not have full knowledge, and as such there is always the possibility of making the wrong choice.

The concept of opportunity costs is one of the first things budding economists are taught. The benefit of every action should be weighed against the missed benefit of the action not taken. Opportunity costs are by definition unseen and thus can be easily overlooked.

Notice that the concept of priorities has deliberately not been introduced so far. Economists and noneconomists alike are generally looking for the choices that will bring the highest amount of human well-being, now and in the future. In this case, economists are questioning whether the extensive actions taken by governments to limit the spread of COVID-19 are hurting the economy too much. Now this is not because the economists are worried about the bank accounts of the richest people in the world, but because economic depressions carry a plethora of bad effects and limit our future options. It is well established that economic depressions lead to more stress-related deaths and suicides. But utilizing our scarce resources to battle COVID-19 at all costs, thus sacrificing our economic well-being and limiting our future growth, also means that we will be relatively poorer in the future and may then be unable to save as many lives then as in an alternative scenario where we do not use such drastic measures against the pandemic.

This basically equates to a trolley problem, the ethical thought experiment in which a runaway train is about to run over five people. The only way to save them is to actively divert the train to a sidetrack, killing another person in the progress. This, of course, represents a clash between utilitarianism and deontology such as Kantianism. It seems that noneconomists, met with discussions about the tradeoffs of the COVID-19 response, unwittingly refuse to acknowledge the limitations of the trolley problem. “We should save everyone—today and tomorrow!” But just as we cannot make the trolley fly and avoid either proposed outcome, we cannot at the same time commit all of our means to multiple ends. There simply has to be a tradeoff. It is no less of a law of nature than gravity.

What many economists these days are imploring is that the decision-makers remember this and do not blindly push all the chips to the middle of the COVID-19 table, with no concern for other valued ends. If they evaluate the benefit of the current efforts and find that they do indeed outweigh the cost, including the unseen opportunity cost, then great! Sharing the analysis with the public will most likely help convince the skeptics that the current course is the right one.

To conclude: no, economists are not cynical bastards who are so blindly obsessed with the stock market that they do not care whether your grandmother dies.

They, like everybody else, want to maximize human well-being. In general, when met with an opinion that seems crazy, there are two options: try to understand the argument or assume that the other person is stupid and/or evil.

These days, too many people are choosing the latter.

“The Fed Can Lend To Anybody”: Watch Live As Bernanke Holds Virtual Discussion On US Economy

None other than the man who saved the world, and “contained” subprime, is holding a Q&A live (over Zoom)…

In his prepared remarks, former Fed Chair Ben Bernanke suggested US GDP could shrink 35%-plus annualized in Q2 (while playing down any comparisons between the lockdowns and The Great Depression, claimed that much of the recent explosion in the Fed balance sheet is temporary, and said that “The Fed can essentially lend to anybody” based on its emergency powers.

Bernanke is expected to speak until around 1345ET:

:format(webp):no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/19866745/unemployment_chart_2_UPDATE.jpg){kind=link}