After Blasting “Russian Troll Attacks,” Swedish Ministers Admit Local Grandma Stoked Anti-5G Fears

Swedish Minister of Energy and Digital Development Anders Ygeman accused Russia “of destabilizing the Swedish 5G debate” by deploying Russian trolls on Facebook in late 2019. A new report by Swedish national broadcaster (SVT) found there was no evidence of Russian bots posting upwards of 2,000 anti-5G posts in total, but rather a granny in Sweden running a grassroots social media group, who was opposed to cellular network radiation.

The posts began in December 2019, when Ygeman pointed out to the Swedish press that thousands of negative 5G comments were showing up on his Facebook account. He immediately blamed “Russian trolls,” and the mainstream media took his word as face value, reported RT News.

“There is a Russian political interest in disrupting and hindering other countries’ development of 5G,” Ygeman told Swedish reporters earlier this year. He said the thousands of negative posts were from “Russian trolls.”

Dagens Nyheter, a leading newspaper in Sweden, ran a headline that was titled “Ygeman target for Russian net attack” with no credible evidence that Russia launched a troll attack on him. Earlier this year, Russian Embassy rejected his claims:

“Our special congratulations go to Anders Ygeman. As we have learned, the popularity of his Facebook page has increased dramatically, which we wholeheartedly congratulate him on!” the Russian Embassy wrote, adding that the government minister “suffers from paranoia in search of ‘Russian trolls.'”

As it turns out, SVT traced the posts back to a local grassroots group called “WiFi Radiation Health Risks Stop 5G,” which is led by Katarina Hollbrink, 64, who describes herself as a granny that is against 5G and lives in Södermalm, Stockholm. The Swedish paper quoted Hollbrink, who said it’s kind of “ridiculous” for the government to accuse “ordinary Swedish citizens of being Russian trolls.”

The Russian Foreign Ministry’s Facebook page posted a meme on Sunday that poked fun at Ygeman’s outlandish comments from late last year, blaming a “Russian troll attack,” while, “in fact, carried out by a domestic tinfoil-hat group,” the post read.

The controversy comes as Sweden is introducing 5G telecoms networks across the country, allowing citizens and businesses to experience lighting fast upload and download speeds that are far superior to existing 4G technology. Sweden didn’t exclude Chinese tech giant Huawei from building out its 5G network, unlike many other Western nations.

The European Union’s Food Safety Authority has approved the sale of bugs as “novel food,” meaning that they are likely to be mass produced for human consumption throughout the continent by the end of the year.

Can’t wait.

“These have a good chance of being given the green light in the coming few weeks,” the secretary-general of the International Platform of Insects for Food and Feed, Christophe Derrien, told The Guardian.

Since 1997, the EU has required a “novel food” classification to allow the sale of products that had no history of being consumed by humans, meaning that the sale of bugs has been banned in countries like Spain, France and Italy for over two decades.

However, with the new approval, mass production of bug-based food is set to ramp up later this year. This means that locusts, crickets, grasshoppers, and mealworms may all appear on supermarket shelves by the autumn.

Christophe Derrien is looking forward to the sale of bugs as both a stand alone food and incorporated into existing products, arguing that they are a great source of protein and the production of bug food doesn’t harm the planet.

“The sort of foods ranges from whole insects as an aperitif or as snacks to processed insects in bars or pasta or burgers made out of insects,” he said.

As we have previously highlighted, eating bugs has been heavily promoted by cultural institutions and the media in recent years because people are being readied to accept drastically lower standards of living under disastrous global ‘Green New Deal’ programs.

This will be exacerbated by the expected economic recession, or even depression, caused by the coronavirus outbreak.

This is why globalist publications like the Economist have been promoting the idea of eating bugs despite the fact that the kind of elitists who read it would never consider for a second munching on crickets or mealworms.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

“All The Jobs Are Gone” – Africa Facing ‘Complete Economic Collapse’ As Virus Spreads

The COVID-19 pandemic and lockdowns across the African continent could trigger an economic collapse, according to one United Nations (UN) official, who spoke with Associated Press (AP).

Ahunna Eziakonwa, the UN Development Program regional director for Africa, warned that the pandemic would likely result in job losses for millions of people, many of whom are already low-income, have no savings, and have no access to proper healthcare.

“We’ve been through a lot on the continent. Ebola, yes, African governments took a hit, but we have not seen anything like this before,” Eziakonwa said. “The African labor market is driven by imports and exports and with the lockdown everywhere in the world, it means basically that the economy is frozen in place. And with that, of course, all the jobs are gone.”

We’ve warned over the last month that a virus crisis looms in Africa. A little more than half of the continent’s 54 countries have imposed lockdowns, curfews, and or travel bans to mitigate the spread of the virus.

Places like South Africa, where the military has enforced “unprecedented” Martial law-style lockdowns through mid-April, is an attempt to thwart social uprisings as 370,000 jobs have likely been lost.

South Africa’s military has begun enforcing a #coronavirus lockdown, which includes bans on alcohol sales and even dog-walking.

For the 1.3 billion that inhabit the continent, widespread lockdowns are triggering vicious economic downturns, couple that with a public health crisis, and it could be a perfect storm that results in social unrest.

Eziakonwa said unless the virus spread can be controlled – then up to 50% of all estimated growth for Africa’s travel, services, mining, agriculture and the informal sectors could be lost. An extended period of subpar economic growth could be seen across the continent in the quarters ahead.

“We will see a complete collapse of economies and livelihoods. Livelihoods will be wiped out in a way we have never seen before,” she warned.

Top oil-exporting countries, such as Nigeria and Angola, could lose up to $65 billion in revenue with collapsed commodity prices – indicating that those governments will struggle to balance budgets, the UN Economic Commission for Africa (UNECA) said.

Many countries in the Sub-Saharan region are heavily indebted and could come into severe financial distress with budget constraints in a downturn. That is why the calls for stimulus among some African leaders have already begun:

“Ethiopian Prime Minister Abiy Ahmed has spoken of an “existential threat” to Africa’s economies while seeking up to $150 billion from G20 nations. A meeting of African finance ministers agreed that the continent needs a stimulus package of up to $100 billion, including a waiver of up to $44 billion in interest payments.

South African President Cyril Ramaphosa backed the calls for a stimulus package, saying in a recent speech that the pandemic “will reverse the gains that many countries have made in recent years.” Several African nations have been among the fastest-growing in the world,” Ap notes.

The International Monetary Fund (IMF) said last month that 20 African countries had requested financial assistance, with an expected ten more countries to need some form of aid. The IMF has already cleared credit facilities for Guinea and Senegal.

In the quarters ahead, socio-economic challenges will persist for Africa as the latest lockdowns due to the virus pandemic will contribute to negative economic outlooks for the region.

UNECA has said emergency stimulus programs are needed to protect 30 million jobs at risk of evaporating.

Ghanaian President Nana Akufo-Addo recently said, “We do know what to do to bring the economy back to life. What we don’t know is how to bring back people to life.” He has created a virus fund that will distribute food and salaries to some citizens for three months.

In Kenya, President Uhuru Kenyatta has launched temporary tax relief programs for citizens and created a $94 million fund to protect low-income families.

Benin’s President Patrice Talon said the rich African countries are unleashing stimulus to boost their economies. He said for poor African countries, like his, they don’t have the financial capability to stimulate.

To sum up, Africa is being swallowed whole by a pandemic that has forced many countries to implement lockdowns to mitigate the spread, which has led to vicious economic downturns. Much of the continent will likely remain in financial distress this year as the global economy has ground to a halt.

China has “defeated” the coronavirus and declared “victory,” Communist Party media tells us.

A funny thing happened on the way to victory, however. The virus is hitting China in a second wave. The second wave is claiming victims, including the Party’s propaganda narratives. The most dangerous of these narratives is that ruler Xi Jinping, with heaven’s mandate, has an obligation to dominate the international system.

China, after reporting no new infections on March 19, said the virus had been contained. Since then, Beijing has been reporting dozens of new cases each day but has maintained that virtually all of them were “imported” — in other words, the infected were individuals arriving from other countries.

Of the very few in-country transmissions, most, Beijing maintained, were transmissions from the imported cases.

China’s official numbers of deaths and new infections, however, must be bogus. Chinese officials are taking actions that are, as a practical matter, inconsistent with the no-new-infection reports.

For instance, on March 27 Beijing closed all theaters nationwide, after re-opening them just the previous week.

In Shanghai, tourist attractions that had just resumed operations were shut again. For instance, the municipality re-closed the observation deck of the Shanghai Tower, the tallest building in China, and the nearby Oriental Pearl Tower. The Jin Mao Tower is now shuttered “to further strengthen pandemic prevention and control.” Madame Tussauds, the Shanghai Ocean Aquarium, and the Shanghai Haichang Ocean Park are now dark, along with the indoor portions of another 25 attractions.

Shanghai Disneyland? “Temporarily Closed Until Further Notice.”

Shanghai is not the only metropolis turning out the lights. In Chengdu, karaoke bars and internet cafes were also shut just days after Sichuan province opened up all entertainment venues.

Fuyang in Anhui province ordered the closure of “entertainment spots” and indoor swimming pools. Henan province locked down internet cafes.

On March 31, ESPN reported that the Chinese central government had delayed the resumption of team sports.

The nationwide university-entrance exams, the gaokao, have been postponed a month, to July.

The regime has also not rescheduled its premier political events, the annual meetings of the National People’s Congress and the Chinese People’s Political Consultative Conference, both originally scheduled for early March.

Finally, the authorities in Jiangxi province are not allowing people from next-door Hubei to enter, indicating they do not believe the epidemic in that disease-ridden province is over.

Does any of this matter? It does: Xi Jinping thinks he should rule the planet.

“China, the country where the virus first appeared and claimed its first several thousand lives, is now using the global spread of the disease to bolster an increasingly vocal, assertive bid for global leadership that is exacerbating a yearslong conflict with the U.S.,” the Wall Street Journal wrote on April 1.

To push America aside and seize global leadership, China got Tedros Adhanom Ghebreyesus, the director-general of the World Health Organization (WHO), to say that China’s response to the coronavirus showed the “superiority of the Chinese system and this experience is worthy of emulation by other countries.” Then Beijing set about making a big show of “donating” medical equipment and diagnostic kits, most notably to stricken Europe.

Finally, Xi Jinping, beginning around the first week of February, forced China back to work to demonstrate that China had ended the epidemic.

None of these showy displays will convince anyone, however, if the virus ravages China again. Unfortunately for Xi, that is what is happening: people in China are re-infecting each other. For instance, in industrial Dongguan in southern Guangdong province, workers returning to their jobsites have been carrying the coronavirus, and this has forced health officials to quarantine other workers. China’s leader can jump-start the economy or throttle the coronavirus, but he cannot do both at the same time.

When the second wave of coronavirus infections hits China hard, Xi Jinping’s boasts about the superiority of Chinese communism will begin to sound hollow, absurd even.

Xi’s initial policies turned a local outbreak into a pandemic, and now they are making even more people sick and forcing China into another pit of disease. China’s inaccurate diagnostic kits and substandard protective gear donated around the world along with the new infections will show the truth: communism is incompetent if not downright malign.

Incompetent and malign communism in turn means Xi’s predicted decline of America will again have to be pushed back to another day.

China can lie with statistics, but the virus gets the last word. “Victory” over both COVID-19 and the United States is still far out of sight.

Austria Becomes First European State To Start Reopening Its Economy

American liberals are having a field day right now bashing President Trump for ‘botching’ the federal response to the coronavirus outbreak. But before they get too excited, we’d like to point out a couple of things to keep in mind: first, the outbreak isn’t over yet, and although 300k cases seems like a lot, the projections for both the US and globally are calling for many millions more, in the US, as well as in Europe and Asia.

Another, is that the Trump Administration and the CDC weren’t the only organizations blinded by “institutional hubris” – as WaPo described the situation at the CDC in its big expose published over the weekend.

Even WaPo conceded that if there was one indisputably great call made by Trump, it was his decision to seal off the US to most flights from China in February. If anything, he should have sealed off slights from all of Europe, too.

But in Brussels, bureaucrats with the EU took the China-influenced advice from the WHO claiming that closing borders wasn’t appropriate at face value, and pushed member states to prioritize other methods of combating the virus instead of border closures and travel bans. Unfortunately, epidemiologists now understand that these are among the most effective tactics for combating the pandemic.

As if to underline that point, Austrian Chancellor Sebastian Kurz and his government on Monday announced plans to reopen their economy as soon as next week.

Flanked by senior government ministers, Kurz announced on Monday a new timetable to restart the Austrian economy, detailing a series of phased steps to bring life back to normal while minimizing the risk.

This will make Austria the first major European country to reopen its economy, a gamble that the FT pointed out will be heavily scrutinized by its neighbors.

But the reason Austria is even in this situation is because it was one of the first major European economies to eschew the advice from Brussels by ordering businesses to close, imposing a strict nationwide ‘lockdown’ and – most importantly – closing the country’s borders to its plague-ridden southern neighbor, Italy.

The country’s lockdown was in place by March 11.

The country of 8.8 million has still reported a number of cases and deaths, though with lower totals than its neighbors. The number of active COVID-19 cases fell for a third straight day on Monday, as recoveries once again outnumbered new infections. That ‘total active’ – the key figure for an economy considering reopening – stood at just over 12,000 in a country of 8.8 million. Sixteen people died in the last 24 hours, bringing the total to 220. The number of patients requiring intensive care remained stable over the past four days at around 250.

During Monday’s speech, Kurz warned Austrians not to engage in Easter celebrations, or he could cancel or alter the plans. The lockdown must continue to be scrupulously adhered to, he said, or the reopening would not happen. Per Kurz’s plan, some shops would start reopening as soon as next week, with others reopening the following week, with reopenings happening gradually by industry until restaurants and bars (expected to be the last on the list) are allowed to reopen by the end of next month (according to the current timeline).

So far, Kurz’s handling of the pandemic, and the performance of his health minister, the coalition-partner Green party’s Rudolf Anschober, has been incredibly popular at home. Now, if he manages to upstage neighboring Germany by reopening the Austrian economy swiftly and safely, Kurz will likely go down as one of the most celebrated leaders of Austria since WWII.

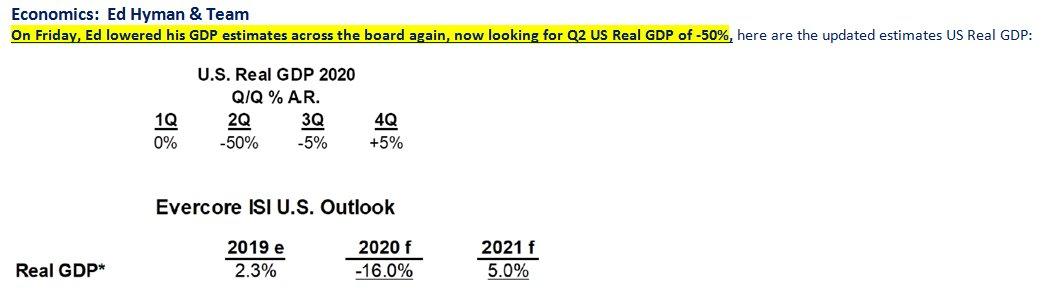

As US Consumers Slide Into Depression They Have Never Been More Bullish On Stocks

Not even in Khruschev’s wildest dreams did central planners ever conceive of anything so absolutely batshit insane as what is taking place in US “markets” right now.

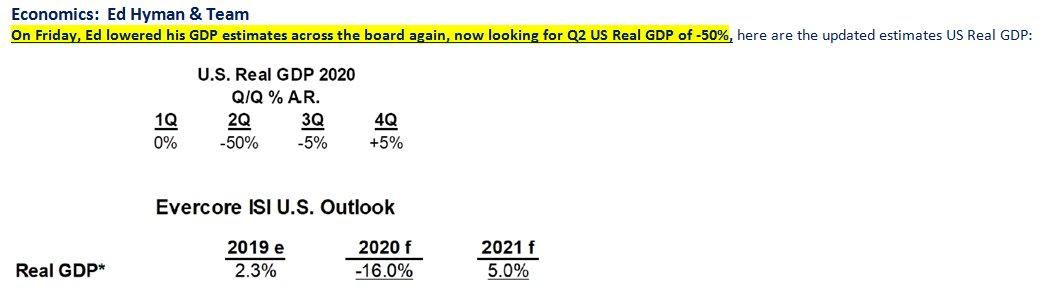

With the US economy sliding into a depression which will last at least one quarter, and if Evercore’s Ed Hyman is correct well into the second half if not 2021…

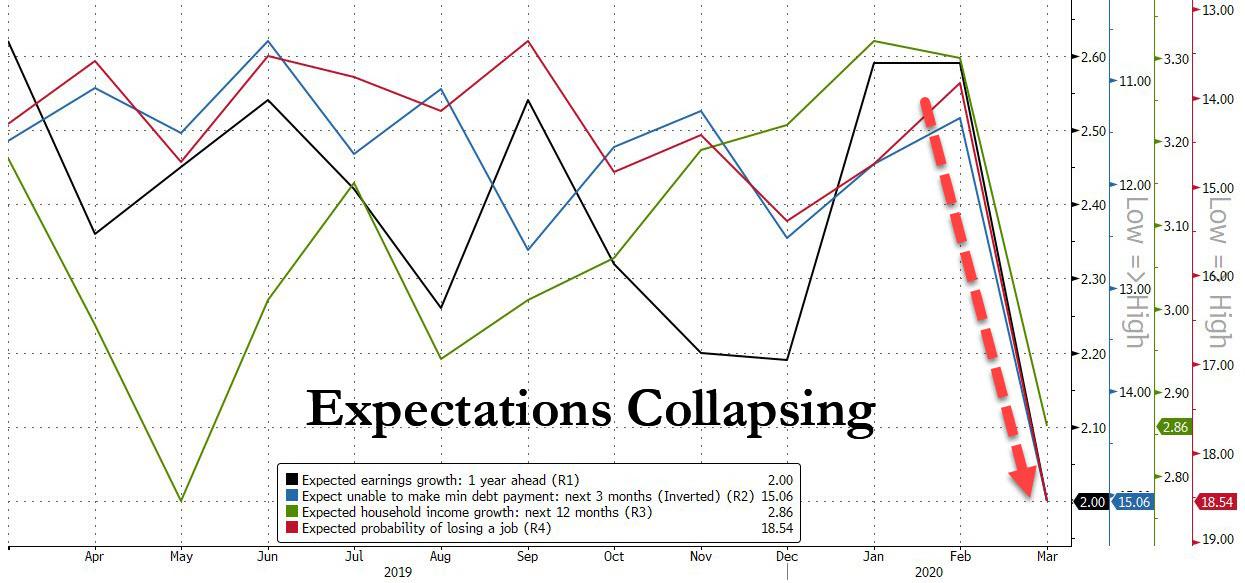

… it is not a surprise that according to the latest New York Fed survey of consumer expectations, virtually every metric having to do with one’s financial well being – income, wealth, debt sustainability and earnings expectations – is cratering. For example the expected probability of losing one’s job jumped to an all-time high of 18.5%; the probability of missing a minimum debt payment over the next three months surged to 15.1%, and expected earnings growth tumbled to just 2%.

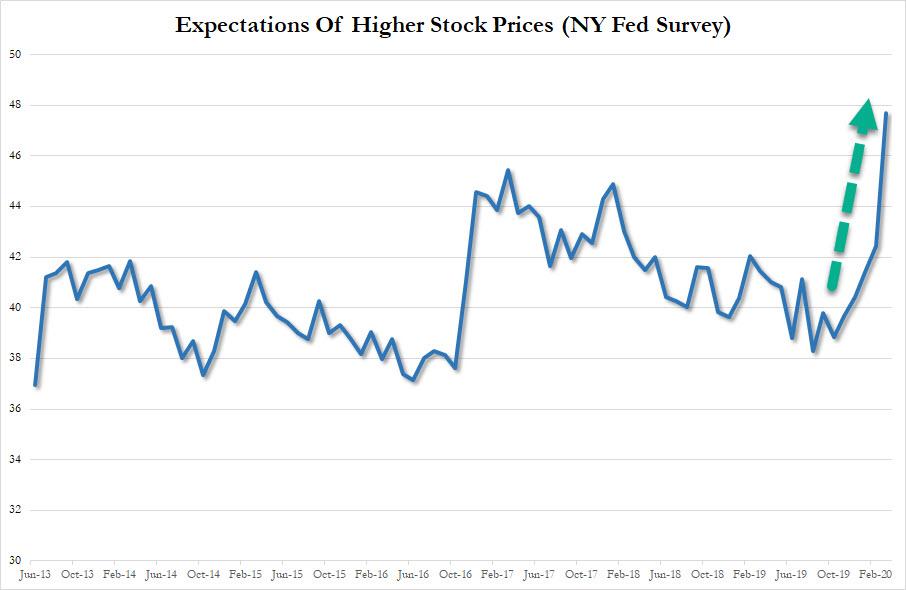

While the above data may not have been surprising, what was shocking is what the Fed reported was the average consumer expectation for stock prices in the future: according to the NY Fed, the mean probability that US stock prices will be higher one year from now surged to 47.7%, the highest on record.

Right… because with his job gone, his $400 dollars of emergency savings just spent on a roll of toilet paper, his bank preparing to foreclose on his home, all while a deadly virus lurks in every corner, all Joe Sixpack can think of is how to get his “money on the sidelines” into the stock market as it is about to soar to all time highs.

And so, thanks to the Fed’s now grotesque interventions in all capital markets, including the purchase of over $1 trillion in securities in the past two weeks, the stock market is now perceived by conventional wisdom as a countercyclical indicator, one which surges the worst the economy gets, and with the economy sliding into a depression it is only “logical” – we use the term loosely – that expectations of higher stock prices have never been higher.

That of course is the absurdist interpretation of the above “data’. There was, naturally, a serious way of looking at this delightfully ridiculous data and lacking a sense of humor, David Rosenberg applied just that, tweeting that “I was so close to turning more bullish (less bearish?) until I see this metric was released by the New York Fed on consumer expectations. Since when do bear markets end on record optimism?”

I was so close to turning more bullish (less bearish?) until I see this metric was released by the New York Fed on consumer expectations. Since when do bear markets end on record optimism? pic.twitter.com/Gddwl5JDbj

Oh David, “since when” do you still think that anything you observe in this economy or market, both stuffed to the gills with trillions and trillions in freshly printed fiatscoes, matters or makes sense. And to answer your question: bear markets end when the Fed says so, and proceeds to do to stocks what it did to IG bonds – and start buying directly.

And incidentally David, you may want to reasses your nothing can beat deflation thesis. Albert Edwards already has, and has said farewell to his “great ice age” thesis that defined his work for the past 30 years. We wonder how long it will take you to realize that we now live in a time of helicopter money and that markets – by any definition – no longer exist, and what comes next it a tsunami of debt and money much of which will finally make its way, kicking and screaming into the broader economy.

Don’t believe us? Just take one look at gold, where the beginning of the end is finally starting to be priced in.

Whitehead: Civil Liberty Attacks In The Age Of COVID-19 Threaten To Expose The American Police State

In an exclusive for MintPress, constitutional attorney John Whitehead warns that the COVID-19 pandemic threatens to bring the American Police State out into the open on a scale we’ve not seen before.

You can always count on the government to take advantage of a crisis, legitimate or manufactured.

This coronavirus pandemic is no exception.

Not only are the federal and state governments unraveling the constitutional fabric of the nation with lockdown mandates that are sending the economy into a tailspin and wreaking havoc with our liberties, but they are also rendering the citizenry fully dependent on the government for financial handouts, medical intervention, protection and sustenance.

Unless we find some way to rein in the government’s power grabs, the fall-out will be epic.

Everything I have warned about for years—government overreach, invasive surveillance, martial law, abuse of powers, militarized police, weaponized technology used to track and control the citizenry, and so on—has coalesced into this present moment.

The government’s shameless exploitation of past national emergencies for its own nefarious purposes pales in comparison to what is presently unfolding.

Deploying the same strategy it used with 9/11 to acquire greater powers under the USA Patriot Act, the police state—a.k.a. the shadow government, a.k.a. the Deep State—has been anticipating this moment for years, quietly assembling a wish list of lockdown powers that could be trotted out and approved at a moment’s notice.

It should surprise no one, then, that the Trump Administration has asked Congress to allow it to suspend parts of the Constitution whenever it deems it necessary during this coronavirus pandemic and “other” emergencies.

It’s that “other” emergencies part that should particularly give you pause, if not spur you to immediate action (by action, I mean a loud and vocal, apolitical, nonpartisan outcry and sustained, apolitical, nonpartisan resistance).

In fact, the Department of Justice (DOJ) has been quietly trotting out and testing a long laundry list of terrifying powers that override the Constitution.

We’re talking about lockdown powers (at both the federal and state level): the ability to suspend the Constitution, indefinitely detain American citizens, bypass the courts, quarantine whole communities or segments of the population, override the First Amendment by outlawing religious gatherings and assemblies of more than a few people, shut down entire industries and manipulate the economy, muzzle dissidents, “stop and seize any plane, train or automobile to stymie the spread of contagious disease,” reshape financial markets, create a digital currency (and thus further restrict the use of cash), determine who should live or die…

You’re getting the picture now, right?

These are powers the police state would desperately like to make permanent.

Bear in mind, however, that these powers the Trump Administration, acting on orders from the police state, are officially asking Congress to recognize and authorize barely scratch the surface of the far-reaching powers the government has already unilaterally claimed for itself.

Unofficially, the police state has been riding roughshod over the rule of law for years now without any pretense of being reined in or restricted in its power grabs by Congress, the courts or the citizenry.

This current pandemic is a test to see whether the Constitution—and our commitment to the principles enshrined in the Bill of Rights—can survive a national crisis and true state of emergency.

Here’s what we know: whatever the so-called threat to the nation—whether it’s civil unrest, school shootings, alleged acts of terrorism, or the threat of a global pandemic in the case of COVID-19—the government has a tendency to capitalize on the nation’s heightened emotions, confusion and fear as a means of extending the reach of the police state.

This coronavirus epidemic, which has brought China’s Orwellian surveillance out of the shadows and caused Italy to declare a nationwide lockdown threatens to bring the American Police State out into the open on a scale we’ve not seen before.

Every day brings a drastic new set of restrictions by government bodies (most have been delivered by way of executive orders) at the local, state and federal level that are eager to flex their muscles for the so-called “good” of the populace.

This is where we run the risk of this whole fly-by-night operation going completely off the rails.

It’s one thing to attempt an experiment in social distancing in order to flatten the curve of this virus because we can’t afford to risk overwhelming the hospitals and exposing the most vulnerable in the nation to unavoidable loss of life scenarios. However, there’s a fine line between strongly worded suggestions for citizens to voluntarily stay at home and strong-armed house arrest orders with penalties in place for non-compliance.

More than three-quarters of all Americans have now been ordered to stay at home and that number is growing as more states fall in line.

Schools have canceled physical classes, many for the remainder of the academic year.

In Washington, DC, residents face 90 days in jail and a $5,000 fine if they leave their homes during the coronavirus outbreak. Residents of Maryland, Hawaii and Washington state also risk severe penalties of up to a year in prison and a $5,000 fine for violating the stay-at-home orders. Violators in Alaska could face jail time and up to $25,000 in fines.

New York City, the epicenter of the COVID-19 outbreak in the U.S., is offering its Rikers Island prisoners $6 an hour to help dig mass graves.

In San Francisco, cannabis dispensaries were included among the essential businesses allowed to keep operating during the city-wide lockdown.

New Jersey’s governor canceled gatherings of any number, including parties, weddings and religious ceremonies, and warned the restrictions could continue for weeks or months. One city actually threatened to prosecute residents who spread false information about the virus.

Rhode Island has given police the go-ahead to pull over anyone with New York license plates to record their contact information and order them to self-quarantine for 14 days.

Rhode Island National Guard Military Police direct a motorist with New York license plates to a checkpoint, March 28, 2020, David Goldman | AP

Of course, there are exceptions to all of these stay-at-home orders (in more than 30 states and counting), the longest of which runs until June 10. Essential workers (doctors, firefighters, police and grocery store workers) can go to work. Everyone else will have to fit themselves into a variety of exceptions in order to leave their homes: for grocery runs, doctor visits, to get exercise, to visit a family member, etc.

Throughout the country, more than 14,000 “Citizen-Soldiers” of the National Guard have been mobilized to support the states and the federal government in their fight against the coronavirus.

Thus far, we have not breached the Constitution’s crisis point: martial law has yet to be overtly imposed (although an argument could be made to the contrary given the militarized nature of the American police state).

It’s just a matter of time before all hell breaks loose.

If this is not the defining point at which we cross over into all-out totalitarianism, then it is at a minimum a test to see how easily we will surrender.

Generally, the government has to show a compelling state interest before it can override certain critical rights such as free speech, assembly, press, search and seizure, etc. Most of the time, it lacks that compelling state interest, but it still manages to violate those rights, setting itself up for legal battles further down the road.

These lockdown measures—on the right of the people to peaceably assemble, to travel, to engage in commerce, etc.—unquestionably restrict fundamental constitutional rights, which might pass muster for a short period of time, but can it be sustained for longer stretches legally?

That’s the challenge before us, of course, if these days and weeks potentially stretch into months-long quarantines.

At the moment, the government believes it has a compelling interest—albeit a temporary one—in restricting gatherings, assemblies and movement in public in order to minimize the spread of this virus.

The key point is this: while we may tolerate these restrictions on our liberties in the short term, we should never fail to be on guard lest these one-time constraints become a slippery slope to a total lockdown mindset.

What we must guard against, more than ever before, is the tendency to become so accustomed to our prison walls—these lockdowns, authoritarian dictates, and police state tactics justified as necessary for national security—that we allow the government to keep having its way in all things, without any civic resistance or objections being raised.

Most of all, don’t be naïve: the government will use this crisis to expand its powers far beyond the reach of the Constitution.

That’s how it starts.

Travel too far down that slippery slope, and there will be no turning back.

As I make clear in my book “Battlefield America: The War on the American People,” if you wait to speak out—stand up—and resist until the government’s lockdowns impact your freedoms personally, it could be too late.

Just because we’re fighting an unseen enemy in the form of a virus doesn’t mean we have to relinquish every shred of our humanity, our common sense, or our freedoms to a nanny state that thinks it can do a better job of keeping us safe.

Whatever we give up willingly now—whether it’s basic human decency, the ability to manage our private affairs, the right to have a say in how the government navigates this crisis, or the few rights still left to us that haven’t been disemboweled in recent years by a power-hungry police state—we won’t get back so easily once this crisis is past.

There is a saying: three things in life are certain: death, taxes and another Argentina default.

In the annals of sovereign debt there is no country that has defaulted more times on its debt, than the country formerly known as the pearl of South America – Argentina – which had defaulted exactly 8 times in just under 200 years. As of Monday, make that nine.

The first default came in 1827, just 11 years after independence; the most recent one was in 2014. In between, there were six others of varying size and form, according to Carmen Reinhart, a Harvard University economist. Almost all of them were preceded by boom periods as, perhaps most famously, when European migrants transformed Argentina into an agricultural powerhouse and one of the world’s wealthiest countries by the late 19th century. Invariably, however, profligate spending combined with easy access to capital supplied by overzealous foreign creditors, did the nation in.

1827: After declaring independence from Spain in 1816, Argentina’s economy quickly opened itself to foreign trade. Some historians would later refer to the early 1820s as the nation’s “happy experience,” a period of peace, prosperity and fascination with European aristocracy. That soon changed. Argentina had sold bonds in London to help finance its nationhood. That debt came under pressure when the Bank of England raised interest rates in 1825. Argentina defaulted two years later. It took another 30 years for the nation to resume payments on the debt.

1890: In the late 19th century, Argentina went on a borrowing spree to build trains and transform Buenos Aires into the cosmopolitan capital it is today. London’s Barings Bank aggressively invested in the nation’s railroads and other utility projects. The south of Argentina boomed, too, as sheep farming spread across the Patagonian grasslands and gold prospectors rushed to Tierra del Fuego. That euphoria faded when the commodities bubble burst. The nation halted debt payments, spurring a run on Argentine banks and the resignation of President Miguel Juarez Celman. That November, Barings teetered near insolvency. Argentina emerged from default four years later, buoyed by fresh capital from the U.K.

1951: An influx of immigrants and foreign capital fueled Argentina’s rise to one of the world’s most prosperous countries by the early 1900s. But World War I hit the nation’s economy hard, as did the Great Depression that followed a decade later. Unemployment and social unrest soared. In 1930, a coup brought the military into power, ushering in a period of political instability — eight presidents in two decades — and a policy of import substitution, which closed off the economy and helped trigger a default.

1956: The populist strongman Juan Peron rose to power in 1946 and proceeded to nationalize companies, redistribute wealth and assert greater government control over the economy. The policies he and his wife, Evita, carried out would become Argentina’s dominant governing principle for roughly half of the next seven decades. Initially, they stoked growth and expanded the middle class. But in 1955, Peron was ousted in a coup, plunging the economy into turmoil and leaving the country struggling to keep up with debt payments. The next year, the military junta struck a deal with the Paris Club of creditor nations to avert a larger default.

1982: During Argentina’s Dirty War, the military dictatorship borrowed, mainly from U.S. and British banks, to fund infrastructure projects and state industries. The nation’s foreign debt ballooned to $46 billion from $8 billion. Then commodity prices collapsed again when the Federal Reserve, under the leadership of Chairman Paul Volcker, raised U.S. interest rates to as high as 20% to tame inflation, spurring debt crises across Latin America and the rest of the developing world. Argentina became one of 27 nations, including 16 in Latin America, to reschedule its debt.

1989: A series of failures in the late 1980s to curb inflation — which climbed over 3,000% — triggered another default in 1989 and brought Peronist leader Carlos Menem into power. His government reduced inflation, privatized state companies and lured foreign direct investment, steering the nation from recession to double-digit growth by Menem’s second full year in office. Still, Argentina’s foreign debt surged to more than $100 billion, the result of Menem’s inability to rein in spending. By the time he left, the nation had fallen into recession once more amid rising unemployment, constrained exports and an overvalued peso.

2001: As the brutal recession entered its fourth year, wiping out about two-thirds of the nation’s gross domestic product, Argentines rioted around the rallying cry, “All of them must go!” The country had five presidents in two weeks, all while declaring what was at the time the largest default by a country in history. Payments were halted on $95 billion worth of bonds. That led to restructuring deals with creditors in 2005 and 2010 under Nestor Kirchner and his wife, Cristina Fernandez. Most bondholders agreed to take the 30 cents on the dollar offered, but a contingent led by hedge-fund billionaire Paul Singer held out and demanded full repayment.

2014: Haunted by a legal drama with Singer and other holdout creditors, Argentina defaulted once again, albeit on a lesser scale. Fernandez’s administration missed an interest payment after a U.S. judge ruled that Argentina couldn’t distribute the funds unless Singer’s Elliott Management Corp. and other so-called “vulture funds” got paid on their defaulted debt. That dispute was finally resolved in 2016, when the new president, Mauricio Macri, paid the holdouts so Argentina could regain access to international debt markets.

And now, with the credit-friendly regime of “reformist” Mauricio Macri a distant memory, we can add default number 9 because according to a decree late on Sunday, the government announced that Argentina plans to postpone payments on up to $10 billion of dollar debt that was issued under Argentina-law – and is thus not bound to international default arbitration – until the end of the year in a bid to relieve pressure over looming foreign currency payments.

The government’s decree of necessity and urgency (DNU), does not affect the roughly $70 billion in foreign currency debt issued under international law that Argentina is currently in talks to restructure with creditors. Argentina’s government has previously said it is looking to restructure $83 billion in foreign currency debt under both international and local law as it looks to avert a sovereign default that would hit its access to global markets.

The move to delay payments on the local-law debt could give Argentina breathing room and may enable it more easily to make payments on foreign-law bonds. As the debt was issued under local law, any creditors wanting to take legal action would need to do so in local courts. And make no mistake: any change to the payment terns, or rather non-payment, is an instant event of default. The only question is which international creditors, which are better known in the country as “vultures”, are bold enough to sue Argentina in its own court system in demanding payment.

The default will hardly come as a surprise: President Alberto Fernandez and Economy Minister Martin Guzman have repeatedly said Argentina cannot pay its public debts until it is given time to revive an economy that has been mired in recession for the last two years. The current coronavirus crisis only pushed the decision to the fore.

Argentina’s major creditor, the International Monetary Fund, which sunk billions into the biggest failed IMF rescue loan in history that is now terminally impaired, has supported the country’s stance saying its debts are unsustainable. It also means that IMF member states will be forced to make the organization whole on its losses.

And with local-law debt done, next up is the default under foreign law. Guzman is expected to soon make a proposal to private creditors to restructure the country’s foreign law bonds, a process that has been hit by delays amid the global coronavirus pandemic that has led to a nationwide lockdown in Argentina.

Beijing has a tough choice to make: tolerate an unprecedented hit to the economy or go for massive stimulus and risk explosive consequences…It should beware, a financial virus can be every bit as toxic as a biological one

The coronavirus outbreak has already taken a great toll on the Chinese economy, with all headline readings pointing towards a record slowdown in growth during the first two months of the year.But there is an even greater danger for what was once the world’s fastest-growing major economy: that Covid-19 will become the catalyst that will bring its many long-simmering problems to the boil. At the centre of these problems is a rising systemic risk in its banking and financial systems caused by a high level of debt accrued over the past decade.

The outbreak could not have occurred at a worse time. The past 10 years have not only seen the economy saddled with this debt, but it has also involved a steady structural slowdown that last year saw the growth rate fall to 6.1 per cent, the lowest in decades. Now, just at the very time the country might consider spending more to prop up that growth rate, a raging pandemic means it will be making much less money than usual.

The latest data from the Chinese Ministry of Finance shows fiscal revenue plunged by 9.9 per cent in the January-February period, the steepest drop since 2009. Overall tax revenue fell 11.2 per cent, driven by a 19 per cent slump in value-added tax (VAT) revenue, the main source of fiscal income. These drops come just as the government has offered a handsome tax cut in response to the pandemic.

Meanwhile, the escalation of the pandemic in the rest of the world will only further weigh on China’s economic growth, corporate profits and personal income. In turn, this will inevitably drag down government revenue in months to come.

Coronavirus: March 2020, the month Covid-19 changed the world

Beijing’s proposed stimulus spending will only exacerbate China’s already-massive debt pile, which had reached 310 per cent of gross domestic product by the end of last year, according to the Institute of International Finance. Many economies that have experienced such levels of debt have gone on to suffer a financial crash or economic crisis. China now accounts for about 60 per cent of the US$72.5 trillion emerging market debt.

A deleveraging campaign had reduced Beijing’s debt mountain in 2018. But it has since returned to credit-driven stimulus to support growth and combat the effects of its trade war with the United States.

About 80 per cent of China’s debt stock was accumulated over the past decade as the country strived to achieve the politically significant milestone of doubling its economic size from 2010 to 2020. The milestone was a key goal in President Xi Jinping’s Chinese dream of “national rejuvenation”.

While the coronavirus threat has receded in China itself, any hope of an early recovery is forlorn as Covid-19 is still ripping through the major developed economies – essentially, China’s customers and trade partners. Plunging demand from abroad will create a second shock wave that will hit China’s export-oriented economy just as it is recovering from the first shock of having to lock down its cities.

China’s balance sheet will be hit by both dwindling revenue and a spiralling demand for spending. Rising corporate debt, surging local government borrowings, and soaring non-performing loans for commercial banks are three areas that could wreck its fragile financial and banking systems. The non-financial corporate debt-to-GDP ratio jumped from 93 per cent in 2009 to 153 per cent last year, one of the highest in the world. The Institute of International Finance warned that China was the major driver of global non-financial corporate debt. China’s bond defaults also hit records in 2018 and 2019.

Coronavirus could cause global food shortages by April as export curbs worsen supply chain problems

Meanwhile, China’s local government debts will jump as a result of more infrastructure-driven stimulus. This will add to a debt pile already worth up to 40 trillion yuan – about 40 per cent of the country’s 100-trillion-yuan GDP last year. S&P Global Ratings has singled out local government financing vehicles as being chiefly responsible for the accumulation of hidden debt. At issue is that while local governments want to spend more, their income from land sales, the main source of local fiscal revenue, is decreasing. The Ministry of Finance said revenue from land sales, which are off-budget, fell by 16.4 per cent in the first two months of the year.

China’s commercial banks also face a severe test as bad debts are likely to rise. Even before the outbreak, China’s banking system was a ticking time bomb, with the state having to step in to rescue a string of embattled medium-sized lenders. A Financial Stability Report released by the People’s Bank of China at the end of last year described 586 of the country’s almost 4,400 lenders as “high risk”. Data from the China Banking and Insurance Regulatory Commission shows there has been a steady rise in the non-performing loan balances of commercial banks since the middle of last year, a result of Beijing scaling back itsdeleveraging campaign.

China’s policymakers face a difficult choice: tolerate an unprecedented slowdown or go for massive stimulus and risk detonating a financial time bomb.

China’s economic planners have a habit of relying on massive levels of debt-financed stimulus whenever growth slows. The closed nature of its financial system affords policymakers the luxury of complacency, as they have a war chest of US$3.1 trillion in foreign exchange reserves.

Some China-made coronavirus test kits and face masks rejected as ‘unreliable’ in European countries

All the signals suggest this is what they will do once more, despite the risk. Leaks suggest Beijing has amended its 2020 budget to raise the deficit to 3.5 per cent of GDP from an original cap of 3 per cent to fund this massive stimulus. Analysts say the actual fiscal deficits could jump much higher than last year’s 4.9 per cent, which included off-budget sheet borrowing and spending. Indeed, a meeting of the politburo, China’s top decision-making body, on March 27 suggested scaling up the stimulus package, with calls to raise the fiscal deficit ratio, increase issuance of Special Treasury bonds, and raise the quota of local government special bond issuance. Policymakers have also directed commercial banks to tolerate a higher threshold for bad loans, hoping to keep thousands of small and medium-sized enterprises from collapsing. The government has already sped up the issuance of bonds. The issuance of special-purpose bonds almost tripled to 950 billion yuan in the first two months of 2020, compared with last year.

It is to be expected that China’s debt will rise substantively in coming months, as in all previous crises. However, Beijing should beware that this time its fiscal measures will be limited. They will help only the country’s internal issue of supply and do nothing for external demand. China should exercise extreme caution: a financial virus can be as toxic, contagious and lethal as a biological one if it is allowed to spread.

* * *

Cary Huang is a veteran China affairs columnist, having written on the topic since the early 1990s

New Zealand PM Adds “The Easter Bunny” & “The Tooth Fairy” To List Of ‘Essential Workers’

New Zealand Prime Minister Jacinda Ardern has won global plaudits for her “compassionate” handling of the coronavirus outbreak, the Washington Post reported, and Ardern won even more praise on Monday, when she added two new job categories to the country’s register of “essential” workers.

Ardern tweeted that with the Easter holiday coming up, she was officially adding the Easter Bunny, and his pal, the Tooth Fairy, to the country’s list of “essential” workers so they can make it to the homes of all the country’s children.

“You’ll be pleased to know that we do consider both the tooth fairy and the Easter Bunny to be essential workers,” she said. “But as you can imagine, at this time they’re going to be potentially quite busy at home with their family as well and their own bunnies.”

New Zealand prime minister Jacinda Ardern confirms Easter Bunny is classed as an “essential worker” but it might be “difficult for the bunny to get everywhere” in current circumstances.

And for those families whose financial situation doesn’t offer enough room for Easter egg hunts, gifts and candy, Ardern assured those children that, because of all the restrictions, it might be a bit difficult for the Easter Bunny to make it to every house this year.

“I say to the children of New Zealand, if the Easter Bunny doesn’t make it to your household, we have to understand that it’s a bit difficult at the moment for the bunny to perhaps get everywhere,” she said.

To help accommodate these children, Ardern suggested that neighborhoods set up ‘easter egg hunts’ by placing eggs in their windows, so that children can ‘spot’ them while they stroll through the streets with their parents. We can hear the groans from NZ’s “bad moms” from here.

On March 25, Ardern announced the most significant restriction on New Zealanders’ movements in the country’s history by declaring a four-week nationwide lockdown, instructing all residents to remain at home except for “essential workers” in health care, retail etc.

{kind=link}