Tesla Posts Video Of Engineers Working On Ventilator Prototype Made From Tesla Car Parts

Just days after we reported that Elon Musk had sent several boxes of sleep apnea machines to New York under the guise of buying ventilators for help with the coronavirus, Tesla has now posted a video of their engineers working on a “prototype” ventilator.

The “prototype”, posted on Sunday night, relies heavily on using Tesla car parts, according to one of the engineers in the video.

And despite Musk saying more than two weeks ago that he was going to open his factory to produce ventilators – and while other companies are already setting up factory space for a ventilator production line – there was no timeline for production specified in Tesla’s video, according to Reuters.

“There’s still a lot of work to do, but we’re giving it our best effort,” an engineer in the video said.

Recall, in late March Ford said they aimed to produce 50,000 ventilators over the course of 100 days at a plant they have in Michigan, in cooperation with General Electric.

It was one day later that Musk said he was going to supply FDA approved ventilators free of cost to NY hospitals. Then, he donated several boxes of 5 year old sleep apnea machines instead.

As for Tesla’s ventilators? We honestly hope they can get them off the line and produced.

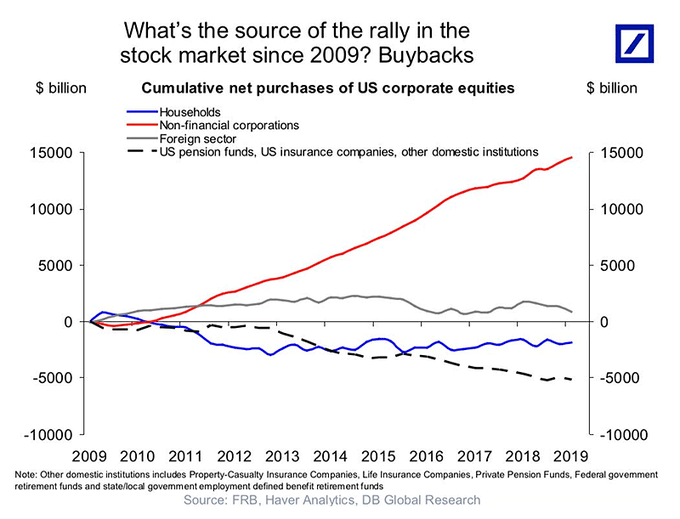

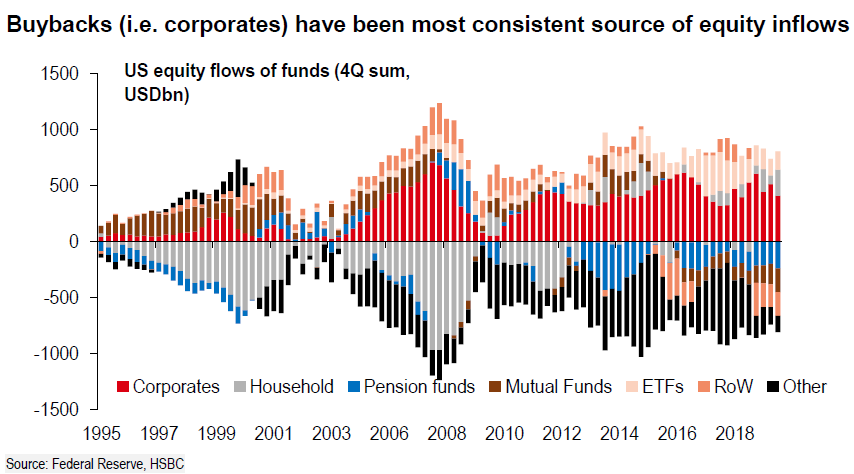

Since the passage of “tax cuts,” in late 2017, the surge in corporate share buybacks has become a point of much debate. I previously wrote that stock buybacks were setting records over the past couple of years. Jeffery Marcus of TP Analytics, recently confirmed the same:

“U.S. firms have been the biggest incremental buyer of stocks in each of the past four years, with their net purchases exceeding $2 trillion – Federal Reserve data on fund flows compiled by Goldman Sachs showed.”

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.

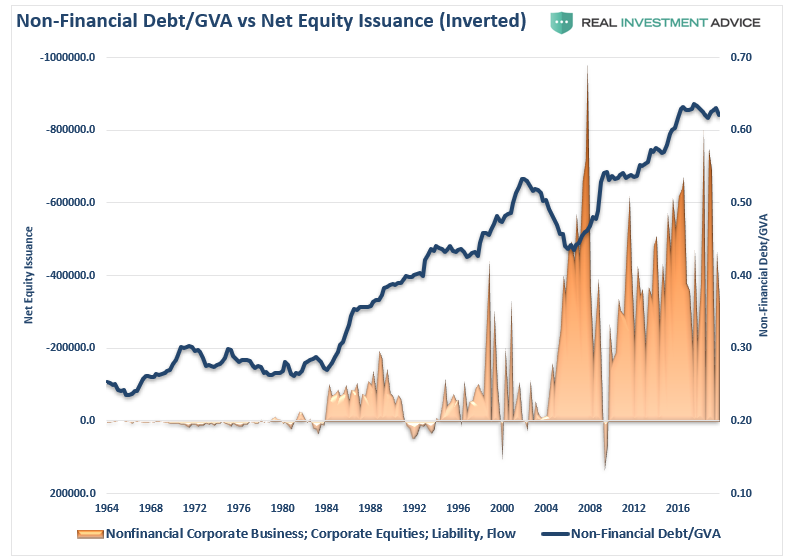

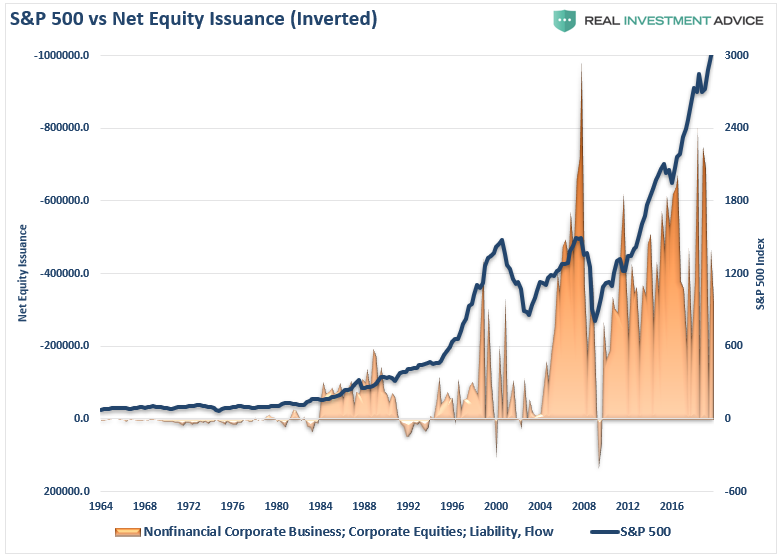

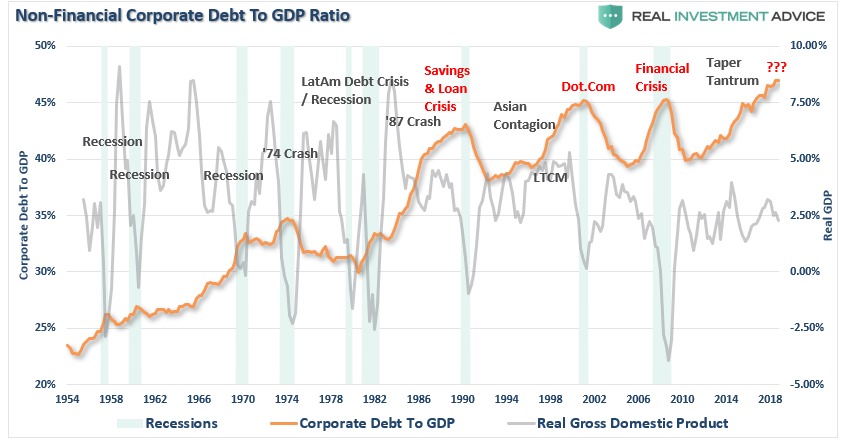

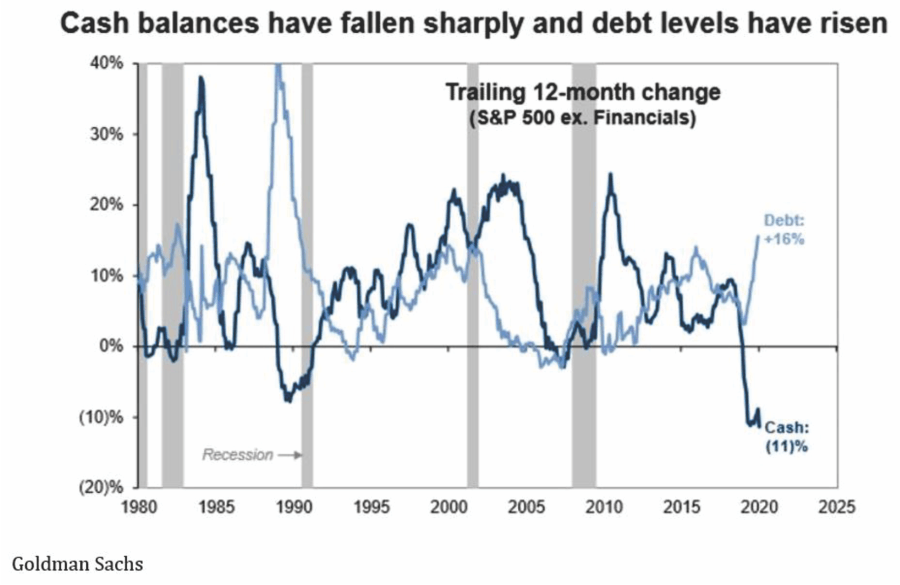

Of course, as a corporation, you can’t spend all of your cash buying back shares, so with near-zero interest rates, debt became the most logical option. As shown below, much of the debt taken on by corporations was not used for mergers, acquisitions, or capital expenditures, but the funding of share repurchases and dividend issuance.

Unsurprisingly, when you are issuing that much debt for share repurchases, there is a correlation with asset prices.

“The explosion of corporate debt in recent years will become problematic during the next bear market. As the deterioration in asset prices increases, many companies will be unable to refinance their debt, or worse, forced to liquidate. With the current debt-to-GDP ratio at historic highs, it is unlikely this will end mildly.”

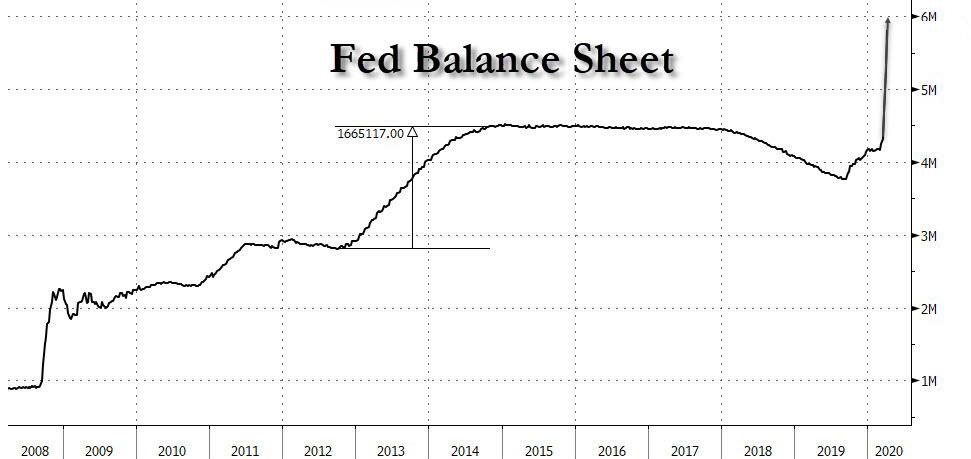

While that warning fell mostly on “dear ears,” the debt is now being bailed out by the Fed through every possible monetary program imaginable.

No, Buybacks Are Not Shareholder Friendly

Let’s clear something up. Buybacks are NOT shareholder-friendly.

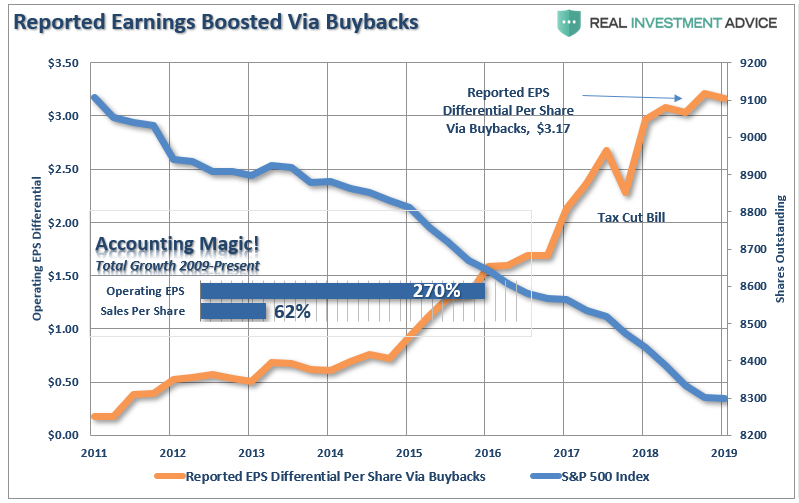

The reason that companies spent billions on buybacks is to increase bottom-line earnings per share, which provides the “illusion” of increasing profitability to support higher share prices. Since revenue growth has remained extremely weak since the financial crisis, companies have become dependent on inflating earnings on a “per share” basis byreducing the denominator.

“As the chart below shows, while earnings per share have risen by over 270% since the beginning of 2009; revenue growth has barely eclipsed 60%.”

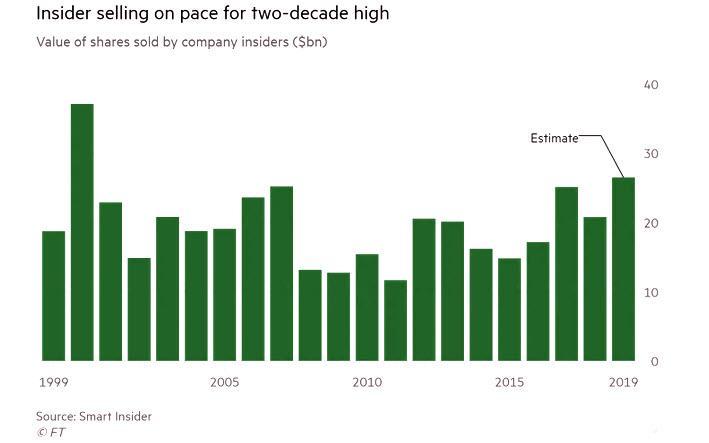

Yes, share purchases can be good for current shareholders if the stock price rises. Still, the real beneficiaries of share purchases are insiders where changes in compensation structures have become heavily dependent on stock-based compensation. Insiders regularly liquidate shares that were “given” to them as part of their overall compensation structure to convert them into actual wealth. Via the Financial Times:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

That statement was supported by a study from the Securities & Exchange Commission which found the same issues:

SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks, Yahoo Finance reports.

Not surprisingly, as corporate share buybacks are hitting record highs, so was corporate insider selling.

The misuse, and abuse, of share buybacks to manipulate earnings and reward insiders clearly became problematic.

Furthermore, share repurchases are the “least best” use of company’s liquid cash. Instead of using cash to expand production, increase sales, acquire competitors, make capital expenditures, or buy into new products or services, which could provide a long-term benefit. Instead, the cash was used for a one-time boost to earnings on a per-share basis.

Now, all the companies that spent years issuing debt, and burning their cash, to buy back debt are now begging the Government for a bailout.

“Perhaps no other industry illustrates the awkward position that corporate America finds itself in more than airlines. Major airlines spent $19 billion repurchasing their own shares over the last three years. Now, with the coronavirus virtually paralyzing the global travel industry, these companies are in deep financial trouble and looking to the federal government to bail them out.” – The New York Times

And who gets the privilege to PAY for those bailouts – YOU. The U.S. Taxpayer.

Loss Of Support

As we warned previously, when CEO’s become concerned about their business, the first thing they will do is begin to cut back, or eliminate, stock buyback programs. To wit:

“CEO’s make decisions on how they use their cash. If concerns of a recession persist, it is likely to push companies to become more conservative on the use of their cash, rather than continuing to repurchase shares. If that source of market liquidity fades, the market will have a much tougher time maintaining current levels, or going higher.”

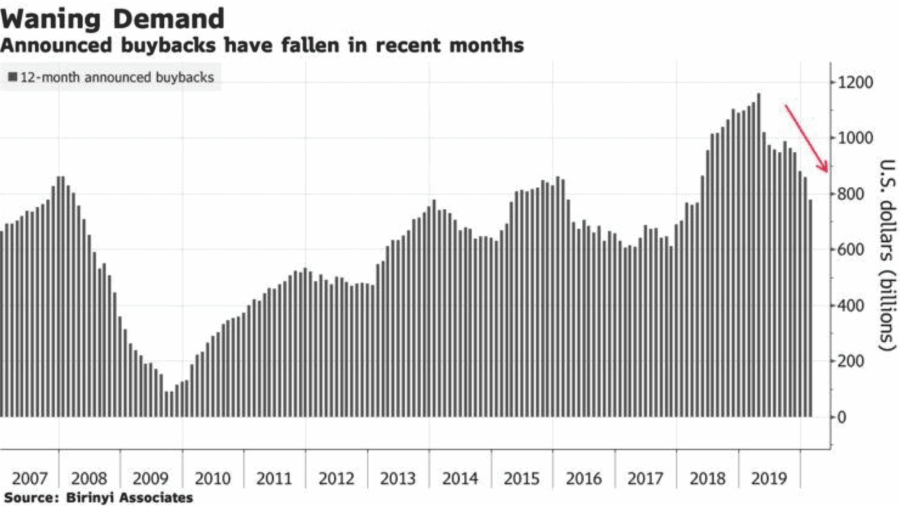

Yes, companies are indeed reacting to the “coronavirus” pandemic currently. However, they were already in the process of cutting back on repurchases in 2019. As noted recently by Jeffery Marcus:

“Birinyi Associates, the leading firm that does research on buybacks, shows below that announced buybacks have declined significantly in 2019… ‘ it’s the biggest drop to start a year since 2009.’”

This is also because cash balances fell sharply, as corporations loaded-up on debt.

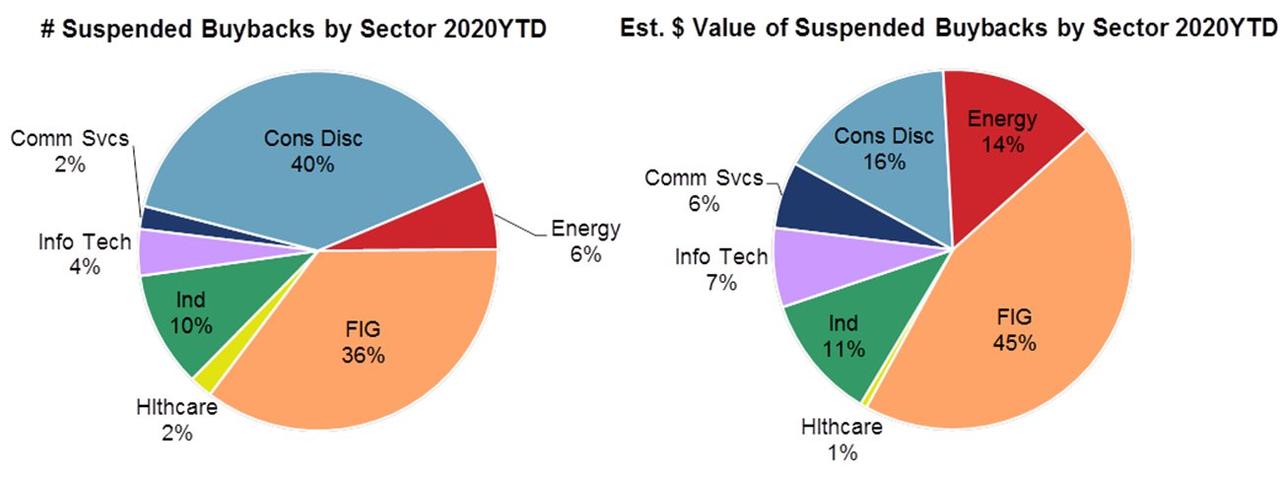

As the impact of the “economic shutdown” deepens, corporations are scrambling to protect their coffers. As noted on Friday, 75% of announced buyback programs have been cancelled.

Corporate buybacks have been the largest source of demand the last few years. 75% of announced buyback programs have been cancelled. So who is the incremental buyer with Boomers retiring in droves who hold the majority of wealth? pic.twitter.com/1IlRrruxDX

Greg’s tweet has a complete table, but here is the relevant chart. There is a tremendous amount of support being extracted.

Do not dismiss the data lightly.

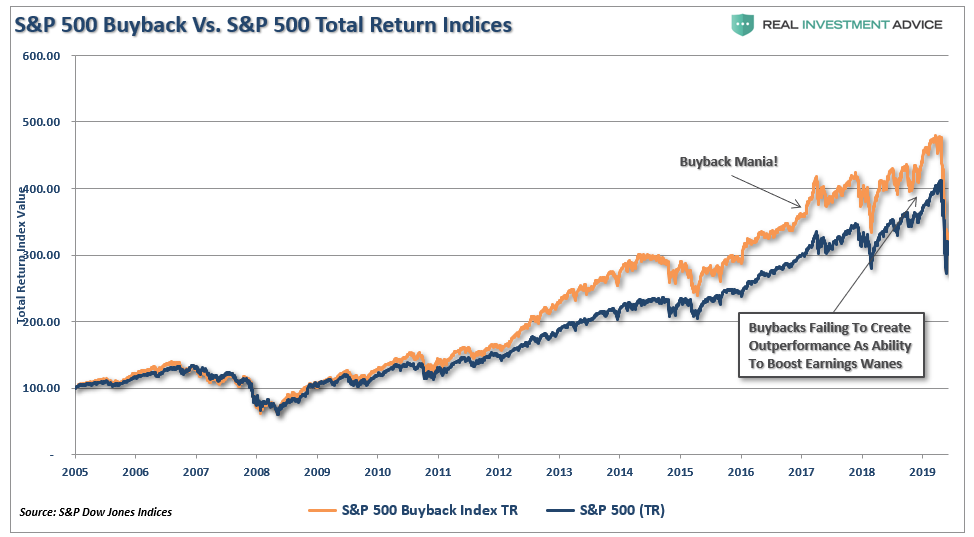

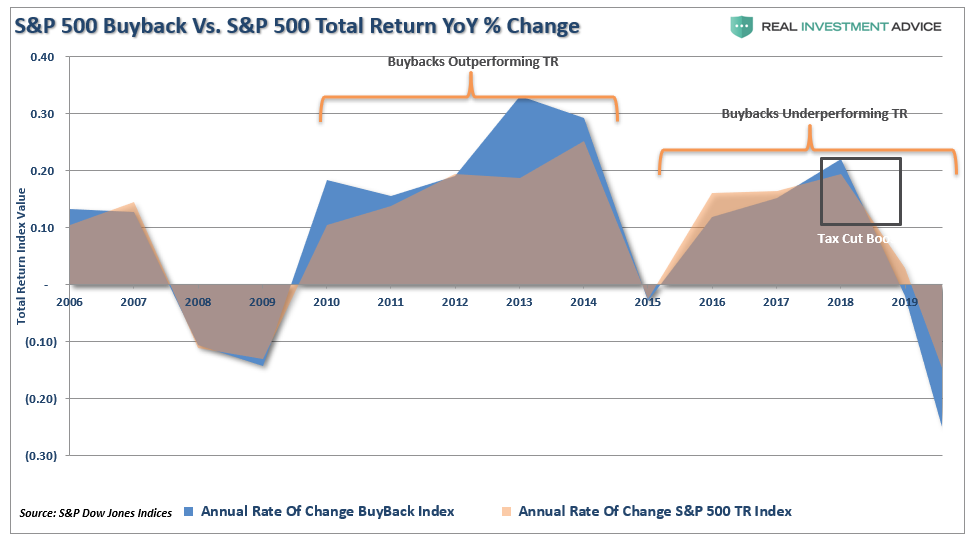

The chart below is the S&P 500 Buyback Index versus the Total Return index. Following the financial crisis, as companies began to lever up their balance sheets to increase stock buybacks. There was a marked outperformance by those companies leading up to the crisis.

However, while corporate buybacks have accounted for the majority of net purchases of equities in the market, the benefit of pushing asset prices higher, outside of the brief moment in 2018 when tax cuts were implemented, allowing for repatriation of cash, performance has waned. Now, those companies which engaged in leveraging up their balance sheet to engage in repurchases shares are significantly underperforming the total return index.

Without that $4 trillion in stock buybacks, not to mention the $4 trillion in liquidity from the Federal Reserve, the stock market would not have been able to rise as much as it did over the last decade.

Conclusion

As I stated, CEO’s make decisions on how they use their cash. With the economy shut down, layoffs in the millions, and no clear visibility about the economic recovery post-pandemic, companies are going to become vastly more conservative on the use of their cash.

Given that source of market liquidity is now gone, the market will have a much tougher time maintaining current levels, much less going higher. As noted by the Financial Times:

“The rebound in equities has sparked optimism that we may be past the worst. However, we still believe it is too early to the call the bottom. From a positioning perspective we still believe there hasn’t been a full capitulation.

Hedge funds and risk-parity funds have reduced their equity exposure considerably. But institutional active funds and passive products have room for further outflows. The fiscal bill passed by the US government also allows individuals to withdraw up to $100k from their 401k, without penalty. We believe this could result in over $50bn of further outflows from the retail community.As well, over 50 companies in the S&P 500 have already suspended their share repurchase programs, which accounted for over 25% of buybacks in 2019. We believe the slowdown in buybacks could result in $300bn of lost inflows in the next two quarters.” – HSBC

Be careful.

The bear market isn’t over yet… not by a long shot.

Oil Spikes After Russia Says Ready For “Substantial Output Cut”, But Warns 10MMb/d Cut Not Enough

Over the weekend, following the biggest ever oil short-squeeze in history following rampant hopes that Saudi Arabia and Russia were considering putting their differences aside and cutting up to 10mmb/d in oil output, we said that in a world where oil demand has plunged by as much as a quarter due to the coronavirus pandemic, or as much as 26mmb/d, such a cut would “not be nearly enough to balance the oil market but at least it was a start.”

Then, moments ago, oil which had been drifting in Monday’s session after the report that a new burst of animosity between Saudi Arabia and Russia has pushed back today’s virtual R-OPEC meeting to later in the week, oil spiked after a Reuters rehash of headlines over the past 3 days, namely that Russia is ready to discuss very substantial oil output cuts “due to global demand collapse“, but – just as we warned over the weekend – Russia dded that “global oil output cuts of 10mmbpd might not be enough to balance the market.”

Well, yeah: with demand down 26mmb/d, supply would have to drop by a similar amount to balance the market.

As a result, Dow Jones reported separately that Saudi Arabia has also invited non-OPEC member Norway, UK and Brazil to the summit in hopes of getting everyone nation to agree to cut output, not just R-OPEC and potentially US shale producers. And as DJ also added citing sources, according to OPEC Plus – which now hopes to hold its summit on Friday – the output cuts would be contingent on G-20 cooperation. In short, while Saudi Arabia destroyed OPEC when it flooded the world with oil last month, it now hopes to not only recreate the oil producing cartel to include every single oil producing nation in the world but to convince said cartel to ease production.

Good luck with that.

In any case, since Brent shorts are now just shy of all time highs…

… any even remotely favorable news is being used by algos to spark a short covering squeeze, and this latest report was no different, sending WTI to session highs…

… even as the real news hit quietly after the flashing red healines, namely that OPEC+ countries still cannot agree on quotas to reduce oil production, and that Saudi Arabia is becoming dangerously petulant…

“IF THERE IS NO DEAL, WE WILL HAVE SOME NICE NUMBER OF FLOATING TANKERS GOING NOWHERE,” AN OFFICIAL IN SAUDI ARABIA SAID: WSJ

… repeating something else we said, namely that oil storage is running out.

Yellen Blames “Enormous Debt And Buybacks” For Coming Default Wave; Morgan Stanley Says It’s All The Fed’s Fault

In June 2017, Janet Yellen decided to wave a red flag before the bulls of fate, and responding to a question on financial system stability, the then-Fed chair said post-crisis regulations had made financial institutions much “safer and sounder”, and as a result she went on to predict that there would never again be a financial crisis “in our lifetimes” to wit:

“Will I say there will never, ever be another financial crisis? No, probably that would be going too far. But I do think we’re much safer and I hope that it will not be in our lifetimes and I don’t believe it will.”

While the bulls cheered this idiotic prediction, some were quick to compare this statement by Yellen to Neville Chamberlain’s infamous – and very, very wrong – “peace in our time” speech. In retrospect the some were right because less than three years later, the world is going through the biggest financial crisis in every living person’s lifetime, which has resulted in the most aggressive central bank market stabilization and intervention in history.

Also in retrospect, it is clear that Yellen didn’t have any bloody idea what she was talking about (then, or any other time when she was boring traders and analysts to death with her droning, narcoleptic monotone) even as we – among others- were warning that it was her monetary policy decisions that guaranteed the next crisis would put 2008 to shame. And sure enough, while the current crisis was sparked by the coronavirus pandemic, it is what comes next that the financial crisis will truly strike home as thousands of companies that loaded up on cheap, cheap debt during the Bernanke, Yellen and Powell Feds, default.

Amazingly, it was again this same intellectual and otherwise midget, that last week had the audacity to deflect blame for the current crisis (which she said would never happen in her lifetime) when last Monday, Yellen said that choices by broad swaths of the financial industry and companies were going to make it harder for the economy to recover from the coronavirus crisis. Choices, which apparently, took place in a vacuum in which the Fed did not keep interest rates at the lowest level in history while blowing the biggest asset bubble ever. Or at least that’s how the recent past looks like through Yellen’s revisionist perspective.

Commenting on Yellen’s video broadcast hosted by the Brookings Institution, the WSJ wrote that while the banking and financial sector was in “generally in good shape” ahead of the crisis, problems were already taking shape according to Yellen, who three years failed to predict the future with her patently idiotic “no crisis in our lifetimes”, and now also appears unable to accurately discuss the past, where she just happened to be a key catalyst for the epic crash that is coming.

Blaming everyone but herself, Yellen said that “non-financial corporations entered this crisis with enormous debt loads, and that is a vulnerability. They had borrowed excessively” and they did it not so much for productive purposes like investment, but for buying back stocks and paying dividends to shareholders. And while these firms borrowed, investors also let their guards down in their hunt for high yields, the former central bank official said, shocking oblivious of the Fed’s role in permitting all of this behavior to continue for years and years, building up massive imbalances which are now finally being unleashed and forcing the Fed to do absolutely everything in its power to prevent true price discovery which would take place… about 60% below current S&P levels.

This blameless narrative continued, with Yellen having the gall to go so far as saying that the corporate borrowing binge – which she helped unleash – “creates risk to the economy. And I’m afraid we’ll see that in spades in the coming months, because it may trigger a wave of corporate defaults. Even where a company avoids default, highly indebted firms usually cut back a lot on investment and hiring, and that will make the recovery more difficult,” the former central banker said, once again hoping to never be named in the list of antagonists whose actions led to the biggest US depression in a century.

We are confident that history will have a different take that Yellen’s endlessly self-serving bullshit, and it was none other than Morgan Stanley’s Michael Wilson who best explained last week why the corporate bond bubble, which will over the coming weeks and months mutate into the biggest default wave in decades, is a direct consequence of the Fed’s actions in general, and Yellen’s stupidity in particular to wit:

We have never seen corporate leverage as high as it is now. Much of this credit was added because credit markets have rarely been so inviting to issuers. This is the direct result of the financial repression era orchestrated by central banks during and after the Great Recession.

In short, the abnormally low cost of borrowing has encouraged companies to lever up and use this financial leverage to drive better earnings growth in what has been a sluggish economic recovery.

Companies are capitalist entities and so they are simply acting in their fiduciary duty to shareholders when they behave in such a manner. Much of this financial arbitrage has been executed via share buybacks, which is now being criticized by members of Congress as they pass the largest fiscal stimulus in history.

It’s important to note that low growth is very different from negative growth. Now that we have entered a recession, the corporate bond market knows the risk of default is much greater – hence the dramatic moves we have seen in credit spreads in the past month. As an aside, the correction in stocks really took a turn for the worse when tensions between Russia and OPEC caused a collapse in oil prices.

This is what triggered the stress in corporate credit markets, in our view, which contributed significantly to the crash in stocks and the economy.

Many acknowledge that credit markets are more important to the functioning of the economy than equity. As bad as the moves were in stocks this month, they were much worse in credit than they were in equities on a risk-adjusted basis.

And while Yellen’s entire career, and her ability to “predict” the future are now the butt of all financial jokes, here is one forecast that we are absolutely certain will come true: when historians look at the cast of villains responsible for the coming second great depression, Yellen’s name will figure in the top three, and for her sake, one hopes that the US public – traditionally clueless when it comes to all maters Fed-related – remains clueless, or else when it comes to “lifetimes” hers may be materially tapered once the tribunals start rolling.

It took less than 5 minutes for Her Majesty to put us right last night:

“..we may have more still to endure, better days will return, we will be with our friends again; we will be with our families again, we will meet again.”

As is becoming normal, the coming week holds out the prospect of good and bad news.

Despite the crisis point of virus being upon us over the Easter Break, authorities sound increasingly confident. Lockdowns look to have worked. It’s likely the numbers have peaked in Spain and Italy, and may even be topping out in London and New York. Over the next few days the narrative is going to start to shift from the immediate crisis to recovery. We will start to hear talk about relaxing lockdowns, selective reopening, and easing social distancing to start economies working again.

That’s the hope.

There is the likelihood of exuberant markets on the improving outlook – there is already a feeding frenzy going on in corporate debt on the back of the billions of Central Bank monetary QE infinity. There is a story in Bberg about accounts switching wholly into investment grade debt: Top Fund Manager is “Hoovering Up” Hugh Amounts of Cheap Credit.

The fiscal support packages announced by Governments are creating the illusion anything can be done to maintain the status quo. On top of them – markets are likely to read any positive news on containing the virus as a screaming buy signal.

Authorities acted fast to preserve jobs, keep the structure of economies together, avoid bankruptcies deepening the shock and addressed the many of the consequences of the shock including economic slowdown and individual misery and misfortune. There will be problems and delays in policy deliverables, but it was a fine effort by government.

However, the reality of the virus tragedy seems to have become completely detached from the euphoric world of financial assets. And that can’t be a good thing.

Despite the negative newsflow from overcrowded hospitals, and still rising death tolls, the market is likely to accentuate any immediately positive news while ignoring the long-term economic consequences of 10 million unemployed Americans? Massive job losses and slowdowns across Europe? Companies ending the stock buybacks that drove the last 8 years of rally? Dividends stopped around the globe? Rising risks around EM economies? Oil prices? Whole sectors of the global economy stopped?

Any rally at this point will simply be markets arbitraging the policy interventions and gorging on ever greater amounts of government support.

Cynical, but that’s pretty much what markets do now. Fundamentals don’t count when policy speaks louder and offers opportunities.

If all that monetary policy interventions have done is keep markets artificially high, and kept investors from suffering losses, while maintaining massive income inequality – then you have wonder if they are the right policies…

Someone in government might just realise…

Fire up the helicopters. Time for a new approach….

Going back to the virus and the real world: How quickly can we reopen?

The reality of how quickly economies reopen depends on what (often inadequate) testing shows, the experience of second wave infections, and how politicians respond to the changing public mood.

I suspect there will still be loads of assumptions made, but these will switch from a slowing the virus bias, to getting economies functional again. For instance, don’t be surprised if the UK decides to assume far higher infection levels occurred in the general population despite our lack of random testing, and makes assumptions such as UK rates being in line with observed rates in countries, like Germany, that did test.

Also expect more reliance on anecdotal data. A few weeks ago my Economic modeller chum, Robert Hillman of Neuron Capital asked why can’t the government mobilise a mobile phone app to get a better idea of the infection spread? If the nation can vote for X-Factor and Strictly on our phones, then why act on reported symptoms widely across the networks. (I understand apps are there to do so, but they are not being pushed at the population through mainstream media like the BBC.) Apps to improve contact tracing are also likely to come to the fore, despite civil liberty concerns.

There will still be virus trouble ahead. The threat of second waves remains, it has re-emerged in guest-worker dorms in Singapore, and the rising doubts about how honest China is being sharing data – whatever really happened in China, it does look like they got the transmission rate down close to zero.

Whatever the CIA accuse China of doing, the real picture in The Middle Kingdom is probably one of balancing a cautious reopening against an urgent imperative to get the economy open again, but leaving all the mechanisms in place to quickly test, isolate, contact track and quarantine any new blooms quickly (and quietly, to demonstrate the party’s wisdom).

Whatever the Chinese are, they ain’t daft.

Let’s be brutally honest:

we’re getting away with strict social distancing in the West because the public has been persuaded its virtuous. If the mood changes, in the light of further testing delays, how the news flow develops, then perhaps the mood changes. The very last thing the Authorities need will be a warm hot summer while the lockdown continues.

European Sovereign Credit

Back in 2010 the World Bank produced a report on sovereign debt to GDP. It theorised that a “tipping point” existed around 77% debt to GDP, where additional point of debt would cause a fall in growth. Low debt equals higher growth. At some point rising state debt starts to strangle real growth.

If you believe in Modern Monetary Theory, then that’s not going to be a problem. Countries should just print more and more money – with the important caveat they have to be able to print money.

All around the globe, we are going to see Debt to GDP levels rise in coming months. Most countries will deal with the crisis by printing money – playing off the threat of rising inflation against the massive deflationary shock the virus has caused. They will then hope to demonstrate growth and credibility to avoid money printing degenerating into a debt crisis or hyperinflation.

It’s not so simple in Europe

Members of the Euro don’t have that fundamental right to print money. They don’t hold the keys to the Euro printing presses. The ECB can collectively decide to allow members to borrow (but is effectively a political body), and has reluctantly agreed some effective transfers, but for all the talk of “ever closer union” there is no prospect of debt mutualisation or joint and severality for ECB borrowers. Even the much heralded Coronabonds now look unlikely to find agreement.

The ECB is buying members’ debt at incredible rates, but largely pretending it’s just market, and not de-facto money printing.

Despite the ECB dither, European Debt To GDP levels are going to rise dramatically in coming months.

Italy – 2019 Debt/GDP 135.6%. Estimate for 2020: 157%

Spain – 2019 Debt/GDP 96%. Estimate for 2020: 113.5%

France – 2019 Debt/GDP 99.2%. Estimate for 2020: 114.4%

Germany – 2019 Debt/GDP 59.2%. Estimate for 2020: 68.3%

Germany can afford to borrow (not print) more, which could help rest of Yoorp. The rest are clearly in trouble. How will Spain recover when 12% of its economy depends on tourism? Italy looks headed for a social bustup.

Let’s spice it up with European banking weakness. There is a great article by Elisa Martinuzzi of Bloomberg: Bankers are Sitting on a Vast Mountain of Risky Trades. It examines the billions/trillions of dollars European banks are holding in highly risky, unclear and illiquid lending. Is that a story you have heard before? Read the story, and figure out just how wobbly European banks are…

Put the following factors together and decide if you are a buyer of European debt: Rising Debt. Rising Unemployment. Banking System in Crisis. Reliance on Someone Else’s Currency. Prospects for Growth. Political Stalemate.

Kudlow Says He “Likes” Cramer’s “War Bonds” Plan, Promises He’ll “Mention It” To Trump

Appearing on CNBC once again Monday morning, Larry Kudlow tried to throw more fuel on Monday’s market rally by insisting that the outbreak in the US was finally slowing, while defending the administration by insisting that “no one could have expected” the virus’s exponential spread (though about a dozen Zero Hedge articles published during the months of January and February would suggest otherwise).

Toward the end of the interview, Kudlow’s former TV co-host Jim Cramer asked if the administration would consider his plan to issue coronavirus “war bonds”, a scheme the CNBC host has been pushing every chance he gets for weeks.

But for the first time, on Monday, Kudlow seemed to indicate that Cramer’s idea was being taken semi-seriously by the White House. Kudlow responded that he “liked the idea” and promised Cramer that he would raise it with President Trump, offering a glimpse behind the curtain to an audience that got to see a little on-air lobbying.

“This is a time, it seems to me, to sell bonds in order to raise money for the war effort, in this the pandemic effort,” Kudlow said. “I’m all for it.”

Already, the US government, via the nation’s biggest banks, has issued about $38 billion worth of loans to small businesses as of Monday morning (far short of the tens, if not hundreds, of billions in loans that have already been requested, as we explained earlier).

But as Congress kicks around a potential fourth coronavirus relief bill, we suspect we’ll be hearing more about what might be in it over the coming week or so.

Following Kudlow, Former Fed Chairwoman Janet Yellen confirmed that she believes war bonds would be “an appropriate approach” as long as its done in a way so that the interest burden will be “manageable” for years to come.

Though while Yellen projected that the true unemployment rate in the US is already well into double-digit territory, and that the recovery might take longer than we’d ideally like, Kudlow insisted that the dynamic US economy would rebound within 4 to 8 weeks.

NYT Op-Ed Calls For People To Stop Using Toilet Paper

The New York Times has published an Op-Ed which shames people into the ‘correct’ way to clean up after dropping a steamer – arguing that amid an absurd toilet paper shortage due to coronavirus, people should simply ditch trees and begin using bidets to strip-mine their crevices.

Panic buying of toilet paper has spread around the globe as rapidly as the virus, even though there have been no disruptions in supply and the symptoms of Covid-19 are primarily respiratory, not gastrointestinal. In many stores, you can still readily find food, but nothing to wipe yourself once it’s fully digested.

This is all the more puzzling when you consider that toilet paper is an antiquated technology that infectious disease and colorectal specialists say is neither efficient nor hygienic. Indeed, it dates back at least as far as the sixth century, when a Chinese scholar wrote that he “dared not” use paper from certain classical texts for “toilet purposes.” –NYT

The author, Kate Murphy, educates us on the history of ass-wiping, writing that before TP was readily available for our bungholes, “people used leaves, seashells, fur pelts and corn cobs,” and that “The ancient Greeks and Romans used small ceramic disks and also sponges on the ends of sticks, which were then plunged into a bucket of vinegar or salt water for the next person to use.“

This is all according to forensic anthropologist and historical pooping expert Philippe Charlier, who wrote a 2012 book – “Toilet Hygine in the Classical Era.”

“It’s not sexy,” said Charlier. “but when you study poo from 2000 B.C. you can get a lot of information about alimentation, digestion, health, genetics and migration of populations.”

Modern, perforated toilet paper was invented by Seth Wheeler in 1891 according to a patent he took out on the concept.

Then we have the invention of the wet wipe – which any modern parent knows is far superior to toilet paper.

…they are now marketed aggressively to adults with gender specific brands like Dude-Wipes and Queen V. Sales reached $1.1 billion worldwide last year, up 35 percent from five years ago, according to Euromonitor International. The unfortunate result is that the wipes have begun to coalesce with grease in city sewer systems to form blockages the size of airliners. –NYT

The ultimate solution?A bidet.

According to Murphy, “experts agree that rinsing yourself with water is infinitely more sanitary and environmentally sound.”

According to Dr. H. Randolph Bailey, a colorectal surgeon (when he could have chosen literally any other specialty), said “A lot of people who come to see me have fairly significant irritation of their bottoms,” adding “Most of the time it has to do with overzealous cleaning.”

Bailey added that ‘you’re just never going to get as clean as rinsing with water.‘

Murphy, meanwhile, shames readers by comparing the rest of the world to Japan – which has “high-tech toilets capable of cleansing users with precisely directed temperature-controlled streams of water,” we’ve become bidet-averse.

Blame prudishness and puritanism, at least in part: Bidets, once ubiquitous in France, became associated with hedonism and licentiousness. Marie Antoinette had a red-trimmed bidet in her prison cell while awaiting the guillotine. And during World War II, American soldiers first saw bidets in French brothels, which made them think they were naughty. An often-told joke was that a wealthy American tourist in Paris assumed the bidet in her hotel room was for washing babies in, until the maid told her, “No, madame, this is to wash the babies out.”

But even in France, toilet paper has taken over. “Now, when constructing a new flat, nobody puts a bidet in it,” Dr. Charlier said. “There’s not room for it, particularly in Paris.” Although, when the bidet is incorporated in the toilet, as modern versions are, space is a nonissue. “Maybe there are also psychological reasons we do not embrace the newer technology,” he said. –NYT

So – with toilet paper flying off the shelves amid the coronavirus pandemic, is it time to start freshening up with a targeted blast of H20?

Rabobank: “There Will Be Attempts To Go Back To Normal After This Crisis, But It Will Be Impossible”

Submitted by Michael Every of Rabobank

The Grand National-ists

The weekend’s world-famous UK horse race, the Grand National, was won by Potters Corner, trained in Wales and ridden by Jack Tudor, at 18-1.That’s a little unusual – but not as much as the fact that this was all a virtual race run on a computer because the actual Grand National was cancelled for the first time since WW2 due to COVID-19.

I mention this because there is a lot of Grand National-ism about at the moment due to this virus. After all, Germany accused (then apparently retracted, to far less attention) claims of ”piracy” as 200,000 face masks in Bangkok destined for it ended up in the US instead: this is normally called “gazumping” in the UK, and in healthier times is seen as perfectly natural – which says something about how we used to operate. The US is also refusing to send medical gear to Canada. Germany itself had of course previously refused to send ventilators and masks to Italy when asked, and France requisitioned private-sector stocks weeks ago. Meanwhile, China has placed strict controls on the export of personal protective equipment (PPE), masks, and virus test kits – which is a problem given it is still the world’s bulk producer – though the Czechs, Dutch, Spanish, and Turkish have all reportedly returned such gear for being faulty, and one news report alleges Pakistan received a shipment of masks clearly made of women’s underwear.

In terms of medicine, there is also a struggle to access virus testing chemical reagents – Israel has had to scale back its testing as Germany has nationalised one of the chemical producers and South Korea has been forced to close one of its plants due to the virus itself. The US is trying to persuade India, the world’s bulk producer, to lift an export ban on hydroxychloroquine, an anti-malaria drug that some trials and one US president regard as having huge potential in fighting COVID-19. China still remains the bulk producer of the ingredients for many other drugs the whole world relies on, and is at least getting its supply chain slowly back in action – though the political good will is where other fears now lie.

The point is that suddenly, and in a crucial area at a vital time, free trade has collapsed. Borders are closed. Planes aren’t in the air. Key goods either aren’t available along supply chains, or national governments are stepping in to hoard or redirect supply for home use – and crucially there is no way politically any government is going to emerge from this crisis saying “Let’s get back to BAU and rely on global supply chains for XXX because its 2% cheaper.”

Yes, local production will take time and be more expensive and will often mean redundant capacity – but that is called crisis preparation. Just look at the human body. Why do we have two lungs? Two kidneys? Will those who preach efficiency donate (or sell) one of each pair – they won’t ever need them, after all. No takers? I thought not. No, for ourselves we take a more defensive stance.

So much is going to change. In oil, for example, the US and *Canada* are apparently in serious discussion about imposing tariffs on foreign oil in order to protect their own domestic industries if the Saudis and Russia cannot agree to sit down with the States and agree on a huge output cut. The fact that the date for that latter decision has been pushed back from today to Thursday has seen energy slump in the Asian session – but also underlines the risk that the US (and *Canada*!) will protect their own industries and workers regardless of what free-trade doctrine tells them to do.

That’s just one key example, but there is a growing recognition of what we already argued would be the case weeks ago in “28 Weeks Later”: yes, there will be an attempt to go back to business as usual after this crisis, but in many key respects this is likely impossible.

We were all stunned by Thursday’s 6.6 million US initial claims number, which was twice as bad as the previous week’s 3.3 million. Then on Friday we got a print in US payrolls just over -700K. If one cannot see the new political imperatives wrapped up in that kind of wrenching socio-economic disruption then perhaps one never will. But please don’t take my word for it. Listen to the serious and/or financial press:

Bloomberg argues “This is The End of Western Capitalism as We Knew It”;

The Atlantic argues “The Revolution is Under Way Already”, drawing historical parallels with the US today and the build-up to 1789 in France;

A Financial Times editorial argues we need radical reforms that reverse the policy direction of the last 40 years: governments must play a larger role in the state; public services must be seen as investments rather than liabilities; labour markets re-regulated; redistribution included on the agenda; and wealth taxes and universal basic income included in the mix; and

Spain’s Prime Minister has written an op-ed arguing that “Europe’s future is at stake in this war against coronavirus”, arguing “either we respond with solidarity or our union fails.” Fiscal solidarity, that is.

True, the ‘talking heads’ and politicians do like to talk. Yet it is very hard to imagine how, once we all finally get back to life as normal in X weeks or months, people will accept the status quo ante of unsustainable structural imbalances in the economic and financial system; of asset bubbles over salary; of lionising tech disruptors over their hard-working and insecure delivery drivers; and of economic resources always being steered towards the needs of “GDP” and business and/or finance, not to doctors, nurses, public transport, society, or even science. Add in the need for local production to allow a spare lung and kidney, and the global economy and markets will surely look very different. Of course, this is not even considering how we will deal with the massive new debt we are about to build up. Do we pay carry it like an albatross around our necks? Or do we default one way or another? The implications are enormous, whatever we decide.

Of course, it’s unclear what markets will look like a lot sooner than that. One wonders how long until we only have virtual markets to play with in AI computer simulations like the recent Grand National. (Then again, it might do less harm to the economy in the long run if all speculative cash just played a giant on-line game– while actual productive capital was ploughed into the real economy and social needs!)

Tesla Cutting “Hundreds” Of Contractors From California And Nevada Factories

Just weeks after Tesla decided to argue with the Alameda County Sheriff’s department in an attempt to keep its workers coming into work during a global pandemic lockdown, the gate is now swinging in the other direction.

Tesla is now reportedly cutting hundreds of contractors from its California and Nevada car and battery plants, according to CNBC.

The cuts will affect temporary workers at the company’s Fremont plant and its Reno Gigafactory. Many contractors working in temporary positions for Tesla were hoping to eventually move into full-time roles. Instead, they are likely heading back to the unemployment line or their respective staffing agencies.

“It is with my deepest regret that I must inform you that the Tesla factory shutdown has been extended due to the COVID-19 pandemic, and as a result, Tesla has requested to end all contract assignments effective immediately,” Balance Staffing was forced to tell its workers, via e-mail.

The agency said they would do their best to find the contractors other work and that the dismissals from Tesla were not a reflection of the quality of their work.

Other contractors employed at Tesla from similar agencies received the same types of notices. Recall, we reported on March 19 when Musk finally wound up suspending production at his Fremont factory, days after government mandated lockdown orders went into effect.

I had a lot of time away from screens this weekend which is probably a good thing. Always good to get to step away and get a different perspective away from the constant bombardment of news, opinions, and, dare I say, conspiracy theories.

People never lose their collective shit more than during times of crisis and uncertainty.

But I’m not here to talk about conspiracy theories, rather I just wanted to offer some perspectives. And feel free to disagree with them. We’re all working with an evolving set of data points (health, macro, interventions, etc.) and lots of global emotions ranging from ignorance to hysteria during a time of great uncertainty.

But here’s a few thoughts to consider as we collectively navigate through this mess.

First off, this is not a drill, and everybody’s lives are affected in one or the other, many severely, many are losing their lives and it’s a horrid tragedy.

Yesterday I actually ventured on the roads here in England in earnest for the first time in a couple of weeks. It was not by choice, but as I had mentioned on twitter we had an unexpected house-guest. Not somebody we ever met before, but it was someone’s elderly mom who got stranded in Heathrow as the South African government shut down all flights. With hotels on lockdown she literally had nowhere to go and after a frantic phone call from her daughter in the US we agreed to take her in.

Her job and life is in South Africa, now she was in a foreign country with no place to go. Her job likely gone at this point. There are many horror stories like this. So we took her in and she stayed with us for 10 days with still no visibility as to when she can return home. A family friend agreed to take here in, but they live in Northern England and there was no practical way to get her there other than by car and I’m not going to drop a grandma off at the train with all the health concerns that come with it.

So we drove. And a trip it was.

I posted some impressions yesterday, just amazing to see the motorways so desolated for long stretches:

Drove hundreds of miles today to drop our stranded guest off at her new temporary home in Northern England.

Some impressions from the lonely journey on largely deserted freeways and roads in a country on lockdown. pic.twitter.com/CV3yEI0udd

So while I hear and see news reports that people are not taking lockdowns seriously, my experience on the road was quite a different one. That bridge in the video is Dartfort Crossing, it’s usually packed all the time. Hardly a car on it. So it was eerie.

Which brings me to a larger point: Most people we know here are seeing their livelihood in jeopardy. I see business owners seeing their operations blow up. Workers get furloughed and believe me: They are all saying government assistance is not enough.

You all know that to be true all over the place. For years we’ve been posting news items about how a larger portion of the population either live paycheck to paycheck or don’t even have enough savings to cover an emergency.

I even highlighted this again last year:

The consumer is in good shape as long as the consumer has a job.

78% are living paycheck to paycheck. 50% have no saving, no retirement & keep adding to revolving credit card debt to fund expenses.

The judge consumer health as good when things are at their best is a fool’s errand https://t.co/kwVbxMIrl2

And now we are finding out the hard way that the consumer is indeed in terrible shape despite a long running bull market driven by cheap money. Why? For many reasons, one of which of course was that wages did not keep up, poor paying jobs in many cases, yet housing prices skyrocketing by the very cheap money that again made housing unaffordable for many and of course the same sins as in every cycle, but perhaps worsened by this last cycle: The illusion that things will always be good and that with cheap money and low rates all kinds of debt can be sustained.

Take your pick or desired combination: Many people were incredibly vulnerable and are now paying the price.

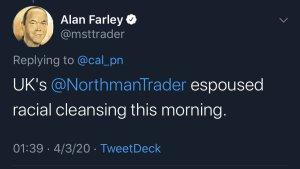

Which brings me to the difficult decision part. How long can shutdowns be kept up, hence my tweet a few days ago:

I hate to say this: But there may come a moment where ugly choices will have to be made.

You can’t keep the global economy on permanent shutdown.

This is not sustainable no matter how much the Fed prints.

Twitter being twitter my tweet prompted me being accused of calling for “racial cleansing”:

You can’t make this up. I despair sometimes at the utter stupidity thrown around sometime.

But that’s neither here nor there.

What is here are parents out of jobs or furloughed, dependent on government assistance with their kids out of school for months to come. This creates all of sort of stresses that go beyond just the financial component, but also to the mental health of children. Sure you can keep this up for a few weeks but not months on end. Zoom only goes so far as a social replacement. I suppose we are lucky to have these tools today, but it’s not a substitute in the long term.

Which brings me to the virus. We are now finally beginning to get some encouraging news of slowing of death rates and infections out of hard hit areas such as Italy and Spain.

A few comments on this: First generally my impression is that countries that have invested more in their medical infrastructure and are more quick to test appear to be able to manage this virus much better. Germany and South Korea come to mind. I’m not saying they are handling it perfectly, but it suggests that the virus can be managed better then it currently is or has been in other places.

The world is waiting for a vaccine which by all accounts (including Bill Gates) may still be 18 months away, a dreadful long time in a current period of need, but also super fast considering the historicity of developing vaccines to new viral agents. But there are no guarantees either.

But while we may be now getting good news on slowing infections and death rates in some cases how much of this is really the virus dying down versus just our social isolation efforts contributing to the slowing in growth? If it is really just the latter then we may be faced with a much more difficult task.

While there is still hope about seasonality such as the flu, the fact that this virus is global in many different climate zones raises the question whether it really is seasonal. We simply don’t know.

What I do know is that the pain and burdens on families are real. And on companies. The longer these shutdowns go on the more severe the long term damage and the long term consequences:

Fwiw: Any notion that we get back to where we were before this virus hit is a fantasy.

Companies will be under significant margin pressure to cope with the hit they just got. Many jobs will not come back any time soon.

There will be belt tightening.

Better yes. But not the same.

Workers currently furloughed may find out that for some, or many of them, the jobs will no longer be there when the lockdowns end.

The hope for a full and quick recovery may well be displaced. I can’t say of course, but we are facing this crisis with a financially vulnerable population, a globe already massively indebted and now adding more debt at a faster clip than ever before.

None of this is sustainable in the long term. The debate about the consequences will come once the immediate crisis is managed, but the solutions employed today may set the stage for the next crisis already.

But the really tough decisions for this crisis will come much sooner than that. When and how to get back to normal without a vaccine. Is it possible without seeing the virus flare up again and risking more lives?

Frankly one concern I have: I see more and more reports of younger people succumbing to the virus. Even people without underlying health conditions. And there are no clear explanations that I have seen. Why does the virus hardly affect some people but is so devastating in others? Science hasn’t been able to provide a definite answer which suggests many aspects of Covid-19 remain unknown.

This raises the concern that a return to normal anytime soon may be prohibitive from a medical perspective, but not to return to normal is economically and emotionally not viable either. Yes, we can all talk about adapting, but that’s easier said than done for millions without jobs or income other than government assistance which doesn’t make them whole.

Entire businesses can’t sustain themselves with crushed revenues and ongoing fixed costs. It’s impossible.

So tough decisions will have to be made and all of them will come with a heavy price tag. On a human, financial, economic, emotional and psychological level.

The longer this drags on the higher the probability that many jobs will not come back making this eventual recovery, while sharp at the beginning, also destined for a lower trajectory recovery as then the full consequences of the damage will come apparent.

Underneath it all there are again lessons crystalizing that were once again ignored: Those that saved during this cycle are able to withstand the shock, those that didn’t or couldn’t can’t. While this business cycle was the longest it didn’t magically extend. It was paid for with cheap money and constant central bank intervention. These very central bankers that once again are intervening at a new record pace created the illusion that they are all powerful. In 2019 there was even fantasy talk by people who should know better that recessions could no longer occur, that the boom and bust cycle had been eliminated. It hasn’t. The bust is here in a big and unexpected way. And it’s here to say.

So yes, hope for the best, take comfort in a slowing of a infections and deaths, take an optimistic view of human ingenuity finding ways to combat the virus, find relief once market rally again, but don’t lose sight of the long term damage inflicted and the short term damage that will be felt in consumer and business pocketbooks for years to come.

Spending plans once made will be reduced, hiring plans once made will be scaled back, budgets once in order are no longer. This shock will reverberate for years to come.

And also don’t lose sight of the fact that none of the tough decisions that will have to be made are clear, easy or consequence free. All have negative side effects.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.