Roughly a month ago on the afternoon of Sunday, March 8th, Fed Chairman Powell had an emergency staff meeting.

Powell: I want the nuttiest money printing plan ever. What action plans do we have that are prepared and ready to initiate?

Admin: Well, we have this one named “GFC 2.0”

Powell: Sounds tame and sedate. Won’t impress anyone.

Admin: What about this one named “Whatever It Takes”

Powell: Lemme look… Meh… I want more shock and awe. This needs at least two more zeros.

Admin: Well, we have this other one named “Project Zimbabwe” but it’s so ridiculous that the Fed would forever lose all credibility…

Powell: hmmm… I like the sound of “Project Zimbabwe.” Just makes you want to turn dollars into toasters and washing machines to preserve wealth. This one will force guys so far out on the risk curve that they’ll think crypto-coins are value investments.

Admin: Yeah, it’s absolutely Wuhan-bat-shit nutty. We’d be criminally insane to unleash this on a population that isn’t prepared for hyperinflation…

Powell: Perfect!! Let’s have a press conference.

A few hours later…

Powell: Mr. President, I finally took rates to zero and launched QE infinity. Can you stop trolling me on twitter already? I can’t take any more of my wife cracking jokes about your tweets.

Trump: Be a man. You got it easy. Wait until you see what I do to Biden. He puts the “Dem in Dementia” haha…

Powell: Please, no more nasty tweets. Even my kids laugh at me.

Trump: Fine, but you’re thinking too small with “Project Zimbabwe.” Figure out how to print more aggressively. Look at what Mnuchin is doing with all his bailout programs. He’s gonna blow $10 trillion by early summer, then try to double that by election time. You better crank up that printing press of yours. I’ll stop tweeting if you keep monetizing the “Mnuchin Money.”

Look, everyone knows the bull thesis for gold, so I won’t wade into the weeds here.

It was never a question of if, but of when. I’d say that if not now, then when?

With every government and Central Bank in full-on Weimar-mode, gold’s potential upside will surprise people, especially as mines shut down from COVID-19 and limit supply. The best part is that margin calls and liquidations have capped the gold price, giving investors one last chance to get in before the run. As people catch their breath and realize what’s happening with simultaneous monetary and fiscal stimulus, gold will be going higher.

Never has a trade been this well telegraphed by this many government officials in my lifetime. Do you have enough gold to survive “Project Zimbabwe”…???

Disclosure: Funds that I control are long gold. I personally own gold.

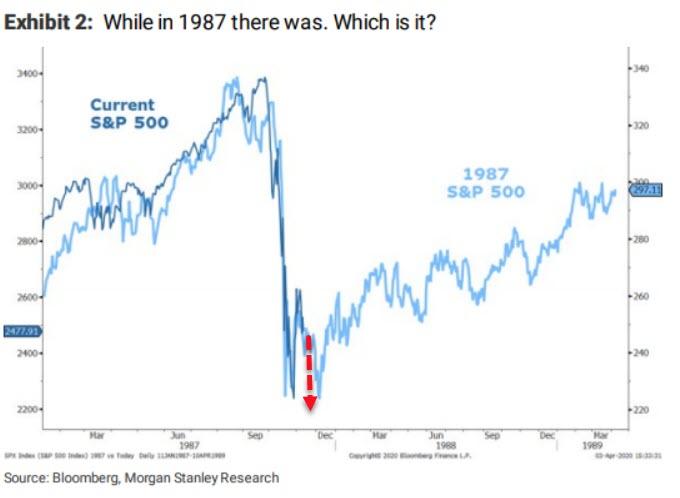

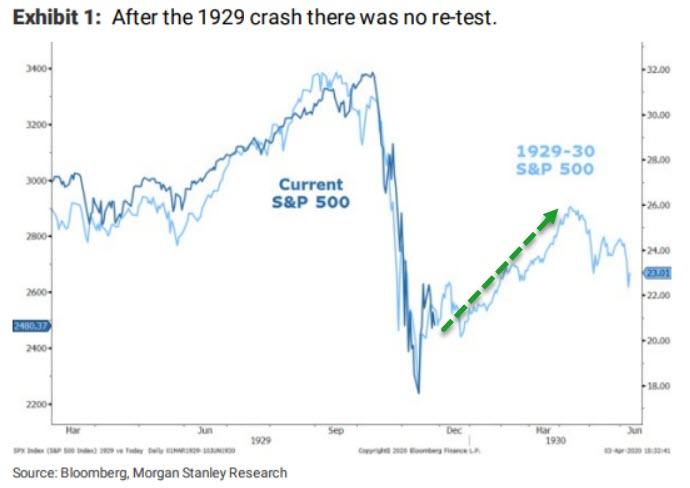

Will We Revisit The Lows? The Answer – Is It 1987 Or 1929

Two weeks ago, on quad-witch Friday March 20 which (so far) marked the lows of the coronavirus crisis, when US stocks plunged to levels not seen since late 2016, we showed a staggering chart from BofA putting the crash of 2020 in its historic context: in less than a month, the US stock market has crashed faster than both the Great Depression and Black Monday, and in terms of the total drawdown, the crash of 2020 is now worse than 1929 and is fast approaching 1987.

And while we have shown that the initial drop of the current crisis was more violent and rapid than the first leg of either the Black Monday crash or the Great Depression, the far more relevant question asked by traders, is what happens next if we use the 1987 and 1929 benchmarks as a reference. Will we “retest”, or was March 20 the low, something which Morgan Stanley says is “the number one question we continue to discuss with clients”, the same “number one” question that Goldman’s clients were asking a week ago.

To answer that question we show Morgan Stanley’s updates to these charts as they both remain remarkably on track for one of these episodes to play out.

In other words, if we are now re-living 1987, then a retest of the lows is imminent at which point the last of the bulls will be cleared out, leading to more near-term pain but also a faster recovery.

Alternatively, if 2020 “is” 1929, then prepare for a lengthy period of pain as stocks struggle for the next decade, with the silver lining that at least they won’t drop below the late-March lows.

But, be careful what you wish for as that 1929 ‘no retest’ ended very, very badly…

What does Morgan Stanley think? The bank, which as we noted on Sunday has now become one of Wall Street’s most prominent bulls in a dramatic almost-overnight reversal in sentiment, is predictably cheerful, with Michael Wilson writing this morning that while the bank appreciates these analogs always break down at some point, “we stand by our view at the time of the first publication that even in the very bad outcome of the 1930s, there was an extraordinary and tradeable rally from those initial price lows (Exhibit 1).”

For what it’s worth, Morgan Stanley notes that it does not think we will have full retest of the lows nor do we think this is the beginning of a depression” which is surprising to say the least for a bank whose economists not only expect GDP to crash 38% in Q2, but for the full GDP loss to be recovered only by the end of 2021.

Indeed, ignoring its own economic forecast, the Morgan Stanley equity stratey team says that “as we have discussed in prior notes, we think this is the end of a cyclical bear market that began 2 years ago in the context of a secular bull market that began in 2011.”

BMO: The US Recession Is About As Subtle As A Network Outage At Netflix

Authored by BMO Capital Markets rates strategists Ian Lyngen, Ben Jeffery, and Jon Hill

It’s an optimistic start to the week in decidedly pessimistic times. With chatter that Spain and Italy may have crossed the Covid-19 apex and a slowing of US fatalities, global risk assets have outperformed overnight and Treasury yields increased. It’s a holiday shorted week with limited data of note except for the March CPI release; this is, however, a uniquely non-tradable event given it prints on April 10 when the market is closed for Good Friday. It’s not inconceivable that it would be brought forward, but as it currently stands odds favor an ignorable report – if for no other reason than the drop in energy prices will impact the headline figure to such a degree as to undermine its relevance in influencing medium-term inflation expectations. March data has taken on a dismissible character given the distortions created by the coronavirus.

US rates has lost all correlation with economic data. The number of releases which would have warranted massive repricing, but instead have been largely ignored by investors is lengthy – and surprising insofar as they have primarily been related to the labor market. It follows intuitively that the ISM series, durables, housing data, etc. would be dismissed as irrelevant in assessing the economic damage from the pandemic; employment on the other hand will prove to be the beginning (and eventual end) of the recession which is surely upon us.

At the beginning of 2020 we highlighted the risk that the US would slip into a recession so subtly that investors might be caught unaware until after the fact; couldn’t have been wronger (it really should be a word). Not only is it blatantly obvious the recession is nigh; but it’s about as subtle as a network outage at Netflix. We physically shudder at the thought. This has altered the timeline of trading the hit to the domestic economy and the path of rates going forward – as well as led to a collective disinterest in the incoming data.

We’ve been on about how economic reports are in the process of being defined in three stages: pre-virus, mid-virus, and post-virus. This logic continues to hold; although we’ll add another nuance – as we’ve seen investors willing to use the pandemic’s path in Europe as a guide for US expectations, so will be the case for any eventual recovery.

Of course, this will not be one-for-one as the structures and risks on the Continent differ significantly from those in the US – to state the obvious. Nonetheless, in the coming weeks/months it is reasonable to assume the market will be anxiously watching the depths of the European recession for guidance on the magnitude of what to anticipate domestically. This will function with a discount of applicability – but still prove the next phase in trading the pandemic. This presupposes the transition from apex to reopening is forthcoming as the realities of the shutdown remain close at hand.

The day ahead holds remarkably little to occupy investors in terms of incoming information; there is a 3-year auction which promises to gauge the market’s appetite for new Treasury notes in the present environment. Our expectation is for the event to come and go, leaving no discernable impact on the outright level of yields or sentiment. As the largest 3-year offering since April 2010 and the backdrop of a Fed actively monetizing the deficit, we’re reminded that March’s comparable issuance tailed 2.9 bp. In an homage to Bobby Zimmerman’s newest release; Rub a Dub Dub, An Auction so Foul. Hats off not only for the artist still recording at 78, but also for offering an anthem for a pandemic.

“Money Doesn’t Grow On Trees… It Floats On The Ocean”

“There’s oil all over the oceans right now. That’s where they are storing oil; we have never seen anything like that,” Trump, rather oddly bringing up such an archaic topic, said this week from the podium of the White House.

“Every ship is now loaded to the gills.”

And he was right.

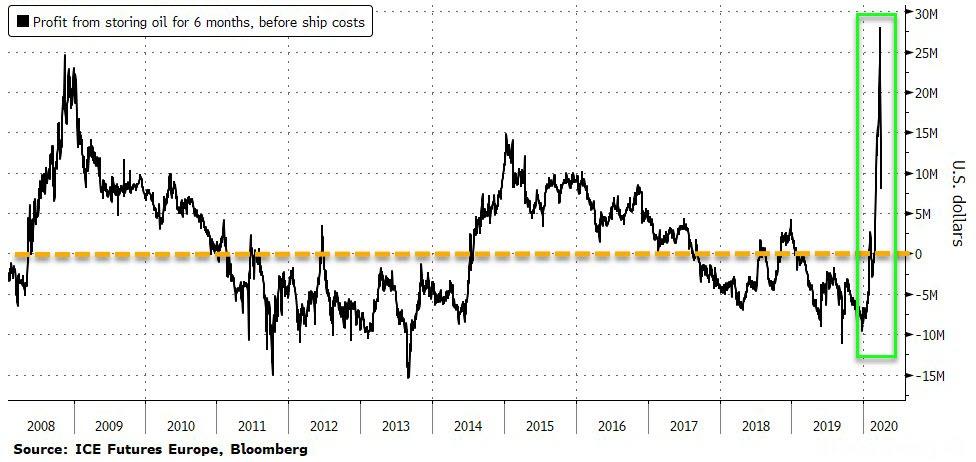

With oil demand in freefall, traders are resorting like never before to using the world’s fleet of supertankers as temporary floating storage facilities, filling them with millions of unsold barrels until better times.

As Bloomberg’s Javier Blas notes, it’s an unusual trade, but one that’s among the most lucrative around right now, just when everyone on Wall Street struggles to make money.

What Trump didn’t say is that the most intriguing facet of the floating storage trade is just how profitable it is. In the industry, it’s often described as a money printing press: traders buy oil on the cheap, and immediately sell their cargo forward in the futures market, locking in a chunky profit – with very little risk.

Before oil prices rallied on Thursday on talk of an OPEC+ output cut, traders were easily able to lock-in a 20% annualized return on their money.

In fact the profits from storing oil at sea have soared massively in March as money no longer grows on Wall Street trees, but lives on the oceans…

I have followed tankers for two decades now. Ever since 2009, every spike was short-lived as there was incessant oversupply. This one is truly different. No national leader wants to end lock-down too soon and then have people die. Instead, the incentive is to be as aggressive as possible with the lock-down, strangle the economy and look like they’re doing something to protect people from something terrifying that most people don’t understand. Which politician wouldn’t want to stand up there on national TV, flanked by important sounding people and talk about what they’re doing to protect you, while giving you free stimulus money? It’s the greatest election campaign ever. Even Trump is getting in on the act and we all know that he’s singularly focused on the stock market.

And sure enough, as Platts detailed earlier, some super tankers are being booked to store crude for up to three years – potentially the longest ever duration for floating storage – as traders seek to profit from hoarding oil to cope with the current oil demand and supply shocks. The race to secure floating storage has picked up significantly in recent weeks, with up to 40 VLCCs and 20 Suezmaxes already placed on long-term chartering, according to S&P Global Platts estimates.

“There’s been a huge interest in storage and that’s helped to lift freight rates,” said Halvor Ellefsen, a tanker broker at Fearnley’s A/S.

“The bottom line is that everybody in the shipping market is acutely aware of the contango, and the profits it can give traders.”

Freight rates and storage costs have ballooned as the market faces the prospect of more oil just as demand destruction due to the spread of coronavirus escalates.

This has raised the stakes over how the world’s biggest producers, the US, Russia and Saudi Arabia will confront the challenges of competition over market share, lower prices and potentially a lack of buyers for their crude.

“The world is overproducing oil at a historic rate,” said Robert Hvide MacLeod, the head of Frontline Management, one of the world’s largest operators of supertankers.

“Land-based storage is limited and selling out fast. Storage on ships will be the only solution.”

I know what the obvious next question is; what if the Saudis stop flooding the market? My response is, “who cares?” We’re all on lock-down. I’m watching out my window. Car traffic is down by half. Cruises aren’t going past my pool deck as frequently and air travel is down dramatically. We’ll eventually beat this flu, but by then, there will be billions of excess barrels to deal with.

The Saudis are a rounding error in all of this. Our government is saying this could go on for 18 months or longer. Are you kidding? Where will all the oil go? This is the time to be greedy on tankers.

Kupperman discloses that funds that he controls are long: DHT, EURN, LPG, STNG, TNK

3Y Auction Tails On Muted Buyer Demand Despite Unlimited Fed QE

Last month’s 3Y auction, which tailed by 2.7bps or the most in at least 4 years, was ugly as a result of the total chaos that hit the market in the second week of March as both the oil price war and the corona pandemic hit at the same time, and led to a liquidation in both bonds and stocks, certainly not sparing the 3Y auction.

April’s 3Y auction wasn’t quite as bad, and moments ago the US Treasury sold $40BN in 3Y paper – the largest offering for this tenor since April 2010 – it came on the backdrop of the Fed massively monetizing, well, everything, why is probably why despite the near record low yield of 0.348%, the lowest since April 2013, it tailed the When Issued by a much more modest 1.2bps.

The bid to cover also improved modestly, rising from 2.20 in March – the lowest since Dec 2008 – to 2.27, which still was the second lowest in 11 years.

The internals were in line, with Indirects rising modestly from 52.3 to 55.4, Directs taking down a modest 4.1%, which while up from 3.7% last month was still well below the 16% six auction average, and Dealers were left holding on to 40.5%, bonds which they will quickly sell back to the Fed.

In summary, a lackluster auction which despite the near record low yield tailed and the BtC was modest as foreigners showing muted interest. As a result, the 10Y yield rose to session highs after the auction and was last seen at 0.666%, the HOD.

Clarmond: The Virus Exposed That Treasury Collateral Is Anything But Stable

Authored by Mustafa Zaidi, head of Research and Development at Clarmond Wealth

My father’s dark brown attache case, with its light, soft suede interior, lay invitingly open on his bed. The case was filled with intriguing goodies for a 10yr old to examine. There were files and photos of building sites (he was an engineer), a cluster of pens and a case of well sharpened Staedtler pencils, his passport, current and old stapled together and a multitude of colourful bank notes that I took out and spread out on the bed, making a pile of each kind. There were super large French Francs, small Deutsche Marks, crisp Japanese Yen, grimy UAE dirhams, grand looking British Pounds, AMEX travellers’ cheques, but the largest stack was of inky green US Dollars.

As I finished my piles, my father, who was watching, motioned me to bring the globe from his desk. “Can you match the notes to the countries on the globe.” I nodded and started from Japan, making my way to the United States. Putting his hand on the world he said – “you can pay for things with these notes – pointing to the francs, marks, yens, pounds – only in their own country, but these” – pointing to the dollars – “you can pay for anything….everywhere” “Wow”, as I held up the Dollar, “this is magic money;” he flashed a brief smile. “Yes, now put it all back in the briefcase.” Magic money……I was hooked.

Over the last four weeks this ‘hook’ has felt more like black magic and all my previous crises (1987, 1998, 2001, 2008) have felt as if rolled into this last month. Perhaps we all need a step back from the daily market fury and see what this pandemic has exposed. In January and February we all saw the events in Wuhan and the cruise ship in Yokohama; the market shrugged. But abruptly in March the virus mattered. Why?

The Asian supply chain was shut down; this is a 90 day credit chain and by March it had run out of credit and needed more. Suddenly there was a demand for US Treasury collateral with which to create credit and this collateral became unstable, with the Treasury yield falling 70% in a few weeks. This collateral was assumed to be stable given it is the keystone of the future global financial architecture.

The lesson from the 2008 crisis is that we needed secured lending rather than unsecured lending to create credit. This therefore meant a move from the old LIBOR system to the new SOFR (Secured Overnight Financing Rate); this transition is due in January 2021. What Covid-19 has done is give this future SOFR system an early test by fire.

The virus exposed the fact that the collateral is anything but stable. As the treasury collateral became unstable all assets around it became unhinged, from investment grade bonds, to high yield, to munis, to commercial paper, to US$s for settling trade and finally to equity markets.

Given the Covid-19 test the upcoming SOFR system has shown vulnerability on two counts: first, collateral can be unstable and second, there are not enough trade dollars for settlements. The Fed will have to address the first by actively controlling the yield curve and the second by opening up substantial US$ swap lines to other central banks. The Fed’s balance sheet cannot be challenged so it will either the castrate levered / hedge fund money so they cannot destabilise the treasury market again or they will temporarily lift the leverage regulations on the banks, as the banks assist the Fed in its policy rather than take it on like a hedge fund.

Our payment system is a credit system, and we need to have enough credit to settle our payments, even if we have no money. And this credit system needs a stable collateral and lots of US$s to work efficiently.

Four and a half decades may have passed but the world still needs its magic money found neatly stacked in my father’s briefcase. Hoping to see you post isolation.

Trump Weighs Legal Action Against China Over PPE Hoarding As International ‘Mask Wars’ Heat Up

The Trump administration is considering legal action against China after leading US manufacturers of medical safety gear say Beijing has prohibited them from exporting goods in what the New York Post says was a bid to “corner the world market” in personal protective equipment (PPE).

“In criminal law, compare this to the levels that we have for murder,” said Trump re-election campaign senior legal adviser, Jenna Ellis, who says that legal options include filing a complaint with the European Court of Human Rights or working ‘through the United Nations.”

“People are dying. When you have intentional, cold-blooded, premeditated action like you have with China, this would be considered first-degree murder,” she added.

Executives from 3M and Honeywell told US officials that the Chinese government in January began blocking exports of N95 respirators, booties, gloves and other supplies produced by their factories in China, according to a senior White House official.

China paid the manufacturers their standard wholesale rates, but prohibited the vital items from being sold to anyone else, the official said.

Around the same time that China cracked down on PPE exports, official data posted online shows that it imported 2.46 billion pieces of “epidemic prevention and control materials” between Jan. 24 and Feb. 29, the White House official said. –New York Post

In total, nearly $1.2 billion in gear – which included over 2 billion masks and 25 million “protective clothing” items which came from EU countries, along with Australia, Brazil and Cambodia according to the White House official.

“Data from China’s own customs agency points to an attempt to corner the world market in PPE like gloves, goggles, and masks through massive increased purchases — even as China, the world’s largest PPE manufacturer, was restricting exports,” they added.

‘Mask wars’

The shortage of vital protective equipment has pitted neighboring countries – and even US states – against each other, resulting in accusations of theft and modern piracy, according to the CBC. The United States, in particular, has been accused of stymying efforts by allies to procure said equipment – by allegedly attempting to scuttle European deals for purchases from China, as well as attempting to halt exports of US-made N95 masks to Canada and Latin America last week.

That said, a Berlin senator who accused the US of “piracy” by diverting a shipment of protective masks slated for delivery in the German capital has reversed his position – saying that no US firms were involved in the case of the still-missing masks.

The CBC suggests that ‘the apparent desperation of some of the wealthiest countries on earth’ comes as a surprise which has ‘justifiably raised eyebrows in less fortunate parts of the world’ which are now preparing for coronavirus to hit, yet with a fraction of the resources.

Striking selfishness

“It’s normal for countries to take care of their own citizens first,” said University of Ottawa professor of international affairs and former Trudeau adviser, Roland Paris – who added that the selfishness and lack of coordination among leading countries “is striking.”

“We’re unfortunately seeing a mad scramble to grab whatever’s available, to hell with the other guy,” added Paris, who’s apparently unfamiliar with game theory.

Even more stark, the mask wars have seen American and other buyers scuttling European and Brazilian deals, some even snatching shipments already promised to other jurisdictions by outbidding them—even “on the tarmac” as planes prepared to take off. Some shipments reportedly just disappear. –CBC

Not just masks…

While global PPE supplies have run critically short, nearly half the supply of hydroxychloroquine – the Trump-touted treatment for COVID-19, comes from India – which has banned exports of all form of the ‘game-changing’ drug.

Consequently – while China is without a doubt the biggest antagonist to the US, India is beginning to grate on Trump’s nerves despite his nominally cordial relationship with Modi. According to data compiled by Bloomberg Intelligence, 47% of the U.S. supply of the drug last year came from India makers. Only a handful of suppliers in the top 10 are non-Indian, such as Actavis, now a subsidiary of Israeli generics giant Teva Pharmaceutical Industries Ltd. Still, it’s likely that some of their production facilities are nevertheless located in India.

India’s export ban on the drug is aimed at ensuring it has enough supply for domestic use after the American president’s endorsement sparked global stockpiling of the medication. Now, Trump’s decision to tout the drug will cause major shortages in the US.

Imagine if the United States hadn’t exported the manufacture of just about everything?

In this week’s pick of energy and commodity charts to watch, super tankers are in high demand to store oil while prices remain at historic lows. Plus, regional gas prices converge around all-time lows, European steel and aluminum demand plummets, and Asian gasoline markets expect little relief from oversupply.

1. Global crude oil glut creates demand for long-term floating storage

What’s happening? Some super tankers are being booked to store crude for up to three years—potentially the longest ever duration for floating storage—as traders seek to profit from hoarding oil to cope with the current oil demand and supply shocks. The race to secure floating storage has picked up significantly in recent weeks, with up to 40 VLCCs and 20 Suezmaxes already placed on long-term chartering, according to S&P Global Platts estimates.

What’s next? Freight rates and storage costs have ballooned as the market faces the prospect of more oil just as demand destruction due to the spread of coronavirus escalates. This has raised the stakes over how the world’s biggest producers, the US, Russia and Saudi Arabia will confront the challenges of competition over market share, lower prices and potentially a lack of buyers for their crude.

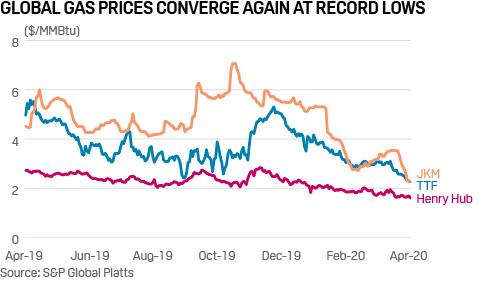

2. Weather, oversupply pressure gas prices across regions

What’s happening? Global gas prices have again converged, this time around record lows, pressured by the mild northern hemisphere winter, high gas stocks and a still oversupplied global market. The JKM benchmark LNG price has fallen to an all-time low of just $2.26/MMBtu for the front month, bringing it down closer toward the prompt TTF and Henry Hub prices.

What’s next? With winter now behind us and the start of the LNG shoulder season, there is little optimism in the market for a recovery in prices, especially with European stocks significantly higher than in previous years and concerns over the demand impact of the coronavirus. Producers are feeling the pinch and industry is watching closely for signs of any supply curtailments in the coming weeks.

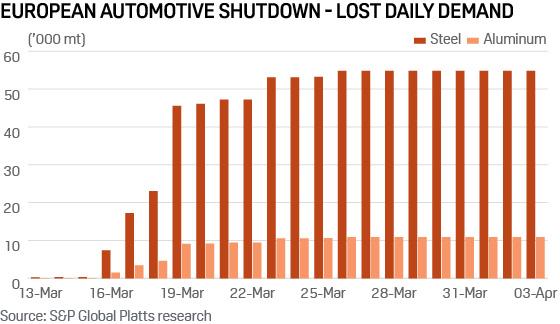

3. European aluminum and steel demand decimated by automaker shutdowns

What’s happening? European automakers have been shutting down production since March 13 in response to the outbreak of coronavirus. With the automotive industry a major consumer of both steel and aluminum in Europe, the shutdowns have had a marked impact on demand, reducing daily consumption by an estimated 55,000 mt of steel and 11,000 mt of aluminum.

What’s next? Blast furnaces across Europe have idled in response, and players up and down the aluminum value chain have done likewise. Looking ahead, there is little light at the end of the tunnel as car manufacturers continue to revise dates for restarts.

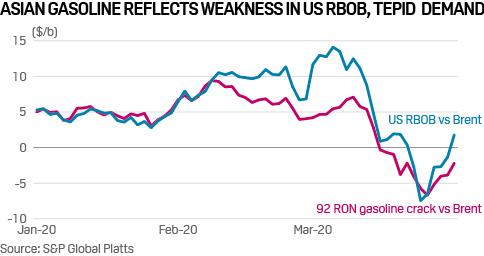

4. Coronavirus effect could erase expected gasoline demand peaks in Asia

What’s happening? The Asian gasoline market has been hit hard by the coronavirus pandemic. Traditionally, Indonesia’s peak gasoline demand occurs during the Muslim fasting month of Ramadan, which begins toward the end of April and lasts till the end of May this year, followed by the Islamic holiday of Eid al-Fitr. More stringent containment measures could derail this trend. State-owned Pertamina has already tapered its pre-Ramadan intake of gasoline to around 10 million-11 million barrels of gasoline in April, down from the 12.236 million barrels the country imported in April 2019, according to market sources. In India, the country’s transition to Bharat Stage VI fuels from April 1, which was expected to result in a demand surge for motor fuels with low sulfur content, has so far had a muted impact on demand as its “Janta Curfew” and nationwide lockdown have dampened both market sentiment and consumption.

What’s next? Market participants will be closely watching the US RBOB/Brent crack as well global economic growth indicators. Asian gasoline crack spreads closely track movements in the US RBOB/Brent crack, with the latter typically rising during summer, from April to October. However, given the weakness in the US RBOB/Brent crack and global GDP, the downward pressure on the gasoline market is likely to persist in Q2.

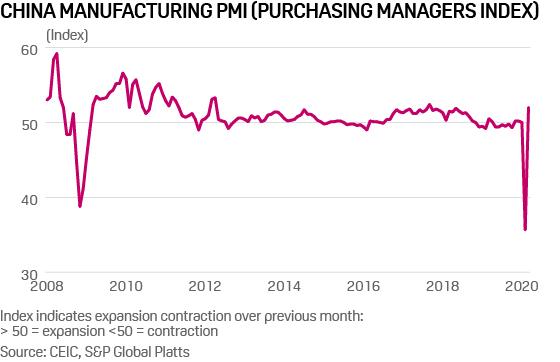

5. China’s PMI: A V-shaped recovery?

What’s happening? After falling to an all-time low of 35.7 in February, China’s manufacturing PMI, a keenly-watched indicator of economic health, rebounded to 52.0 in March, exceeding many analysts’ expectations. That doesn’t mean China’s economy is roaring back to life, just that over half of companies surveyed reported that their production, employment, new orders and the like were higher than last month – hardly an achievement given the economy was at a virtual standstill in February. Even the National Bureau of Statistics noted this reading did not mean that China’s economy had returned to normal.

What’s next? Government action to prevent a second wave of infections is likely to be a drag on economic activity. China has cut the number of international flights allowed into the country and closed cinemas again. Shanghai’s government has gone further, ordering tourist attractions to close in April. Sinopec, the country’s largest refiner, expects domestic oil product consumption to more or less recover in the second-half of the year. An S&P Global Platts survey found that Sinopec’s refinery operating rate was 72% in March, well up from the historical low of 64% in February, but still well under Sinopec’s average utilization rate last year which was more than 90%. More measures to close the economy will be a drag on demand meaning that, unlike the PMI, the shape of the recovery is likely to be far from V shaped.

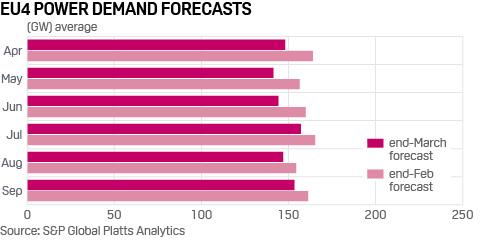

6. EU power demand set to dive 10% in Q2 on shutdowns

What’s happening? European power demand is expected to fall 10% over the coming months due to coronavirus restrictions, with Italy and Spain the worst hit by extended lockdowns to non-essential activities. S&P Global Platts Analytics has cut its Q2 demand forecast for the four big Eurozone economies (Germany, France, Italy and Spain) by 16 GW, down 11% on year. Early indications for the second half of March show Italian demand down over 20%, while Germany was down 9%.

What’s next? April and May are generally low demand months for electricity, so additional cuts could be a challenge for system operators, as renewables’ share in the mix rises. A demand cut of 10% across the EU4 would be the energy equivalent of 70 standard LNG cargoes over the quarter. On the flipside, hydro resources are healthy and Europe’s wind and solar parks on a sustained run of output increases, reflecting on-going capacity additions. Daily load curves are changing as solar hours increase and morning peak demand flattens, reflecting the absence of industrial load. A low-demand, high-supply scenario tests system operation just as much as the reverse.

Tesla Posts Video Of Engineers Working On Ventilator Prototype Made From Tesla Car Parts

Just days after we reported that Elon Musk had sent several boxes of sleep apnea machines to New York under the guise of buying ventilators for help with the coronavirus, Tesla has now posted a video of their engineers working on a “prototype” ventilator.

The “prototype”, posted on Sunday night, relies heavily on using Tesla car parts, according to one of the engineers in the video.

And despite Musk saying more than two weeks ago that he was going to open his factory to produce ventilators – and while other companies are already setting up factory space for a ventilator production line – there was no timeline for production specified in Tesla’s video, according to Reuters.

“There’s still a lot of work to do, but we’re giving it our best effort,” an engineer in the video said.

Recall, in late March Ford said they aimed to produce 50,000 ventilators over the course of 100 days at a plant they have in Michigan, in cooperation with General Electric.

It was one day later that Musk said he was going to supply FDA approved ventilators free of cost to NY hospitals. Then, he donated several boxes of 5 year old sleep apnea machines instead.

As for Tesla’s ventilators? We honestly hope they can get them off the line and produced.

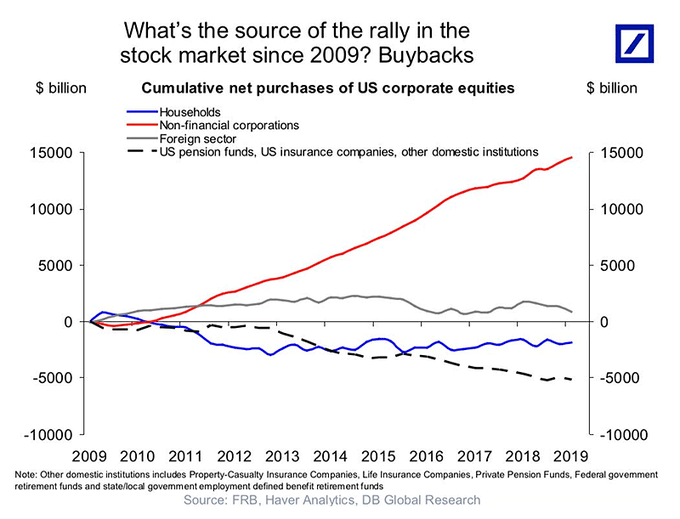

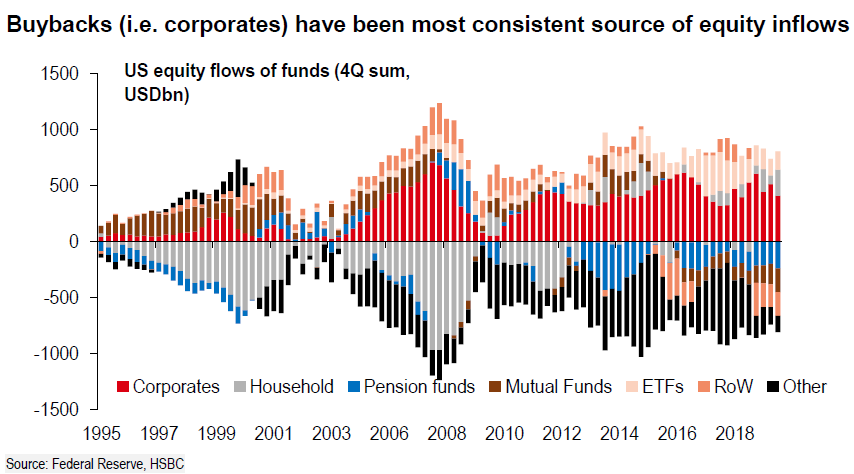

Since the passage of “tax cuts,” in late 2017, the surge in corporate share buybacks has become a point of much debate. I previously wrote that stock buybacks were setting records over the past couple of years. Jeffery Marcus of TP Analytics, recently confirmed the same:

“U.S. firms have been the biggest incremental buyer of stocks in each of the past four years, with their net purchases exceeding $2 trillion – Federal Reserve data on fund flows compiled by Goldman Sachs showed.”

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.

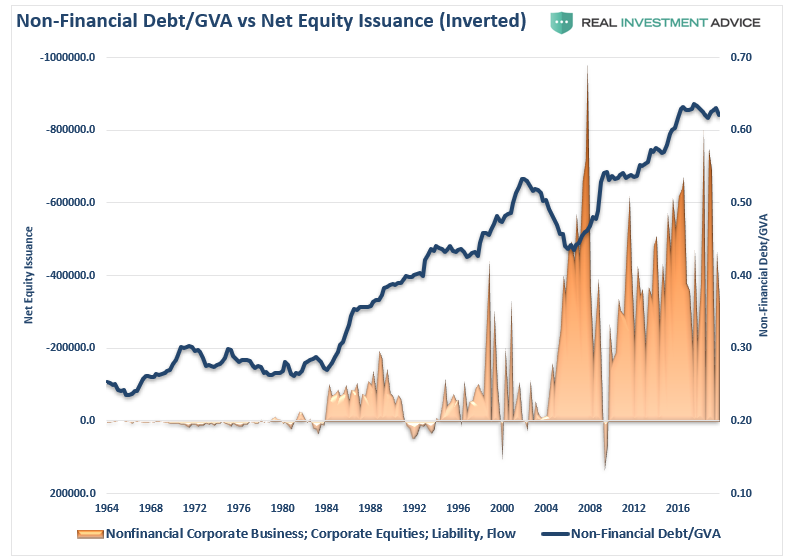

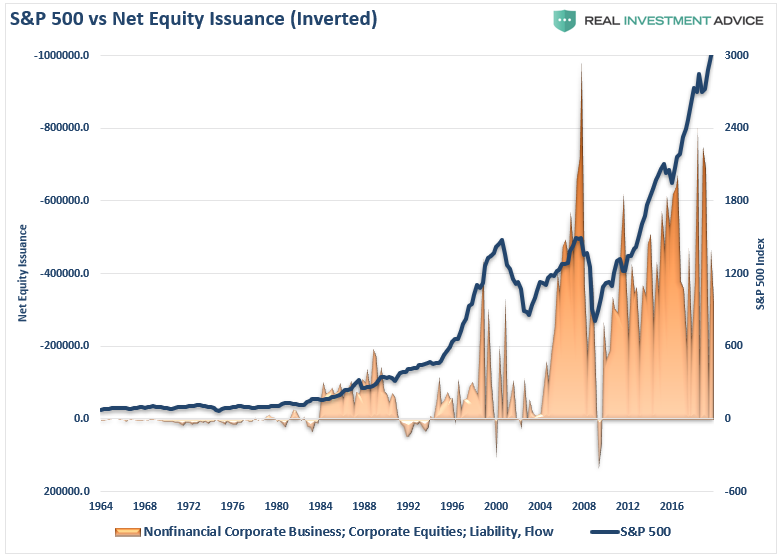

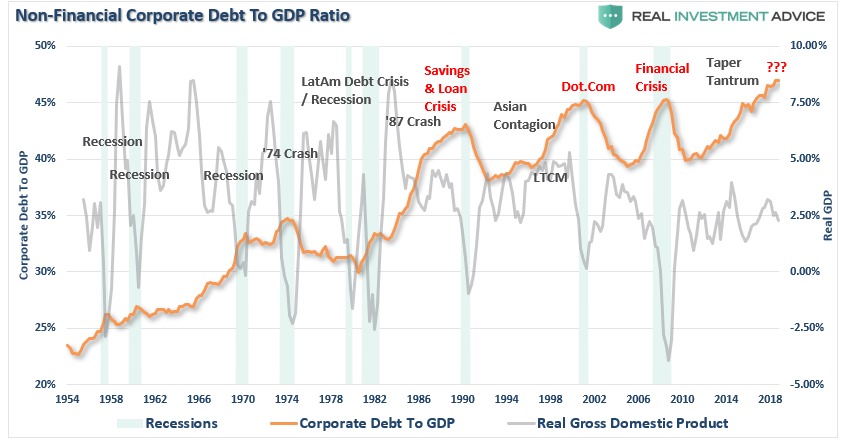

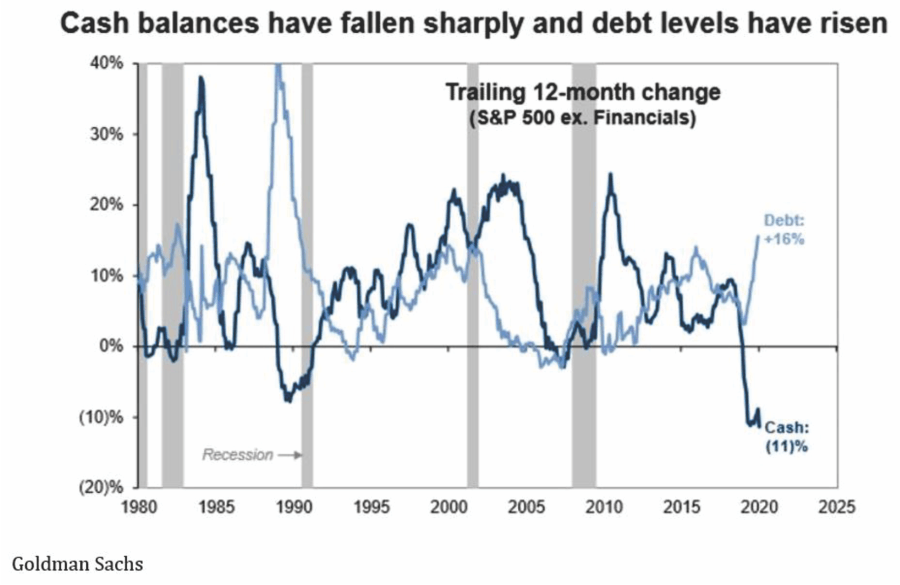

Of course, as a corporation, you can’t spend all of your cash buying back shares, so with near-zero interest rates, debt became the most logical option. As shown below, much of the debt taken on by corporations was not used for mergers, acquisitions, or capital expenditures, but the funding of share repurchases and dividend issuance.

Unsurprisingly, when you are issuing that much debt for share repurchases, there is a correlation with asset prices.

“The explosion of corporate debt in recent years will become problematic during the next bear market. As the deterioration in asset prices increases, many companies will be unable to refinance their debt, or worse, forced to liquidate. With the current debt-to-GDP ratio at historic highs, it is unlikely this will end mildly.”

While that warning fell mostly on “dear ears,” the debt is now being bailed out by the Fed through every possible monetary program imaginable.

No, Buybacks Are Not Shareholder Friendly

Let’s clear something up. Buybacks are NOT shareholder-friendly.

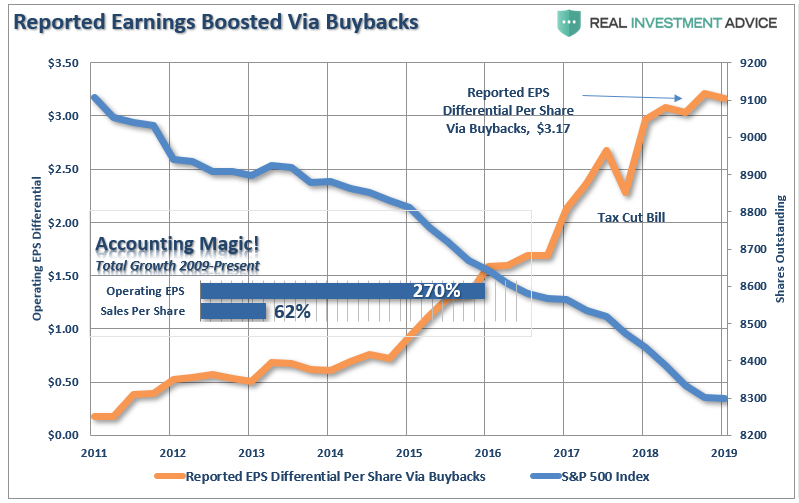

The reason that companies spent billions on buybacks is to increase bottom-line earnings per share, which provides the “illusion” of increasing profitability to support higher share prices. Since revenue growth has remained extremely weak since the financial crisis, companies have become dependent on inflating earnings on a “per share” basis byreducing the denominator.

“As the chart below shows, while earnings per share have risen by over 270% since the beginning of 2009; revenue growth has barely eclipsed 60%.”

Yes, share purchases can be good for current shareholders if the stock price rises. Still, the real beneficiaries of share purchases are insiders where changes in compensation structures have become heavily dependent on stock-based compensation. Insiders regularly liquidate shares that were “given” to them as part of their overall compensation structure to convert them into actual wealth. Via the Financial Times:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

That statement was supported by a study from the Securities & Exchange Commission which found the same issues:

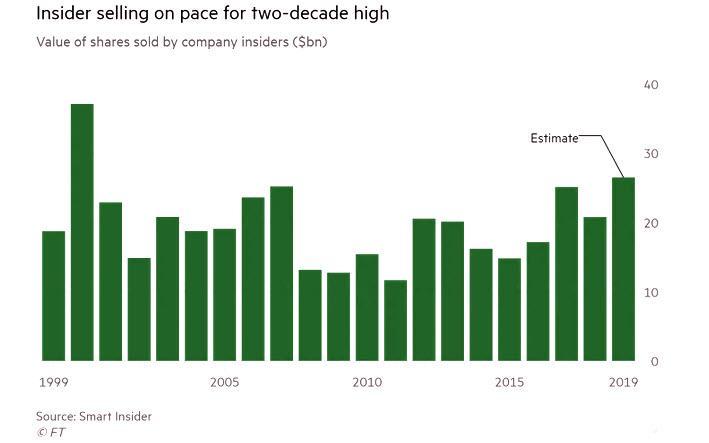

SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks, Yahoo Finance reports.

Not surprisingly, as corporate share buybacks are hitting record highs, so was corporate insider selling.

The misuse, and abuse, of share buybacks to manipulate earnings and reward insiders clearly became problematic.

Furthermore, share repurchases are the “least best” use of company’s liquid cash. Instead of using cash to expand production, increase sales, acquire competitors, make capital expenditures, or buy into new products or services, which could provide a long-term benefit. Instead, the cash was used for a one-time boost to earnings on a per-share basis.

Now, all the companies that spent years issuing debt, and burning their cash, to buy back debt are now begging the Government for a bailout.

“Perhaps no other industry illustrates the awkward position that corporate America finds itself in more than airlines. Major airlines spent $19 billion repurchasing their own shares over the last three years. Now, with the coronavirus virtually paralyzing the global travel industry, these companies are in deep financial trouble and looking to the federal government to bail them out.” – The New York Times

And who gets the privilege to PAY for those bailouts – YOU. The U.S. Taxpayer.

Loss Of Support

As we warned previously, when CEO’s become concerned about their business, the first thing they will do is begin to cut back, or eliminate, stock buyback programs. To wit:

“CEO’s make decisions on how they use their cash. If concerns of a recession persist, it is likely to push companies to become more conservative on the use of their cash, rather than continuing to repurchase shares. If that source of market liquidity fades, the market will have a much tougher time maintaining current levels, or going higher.”

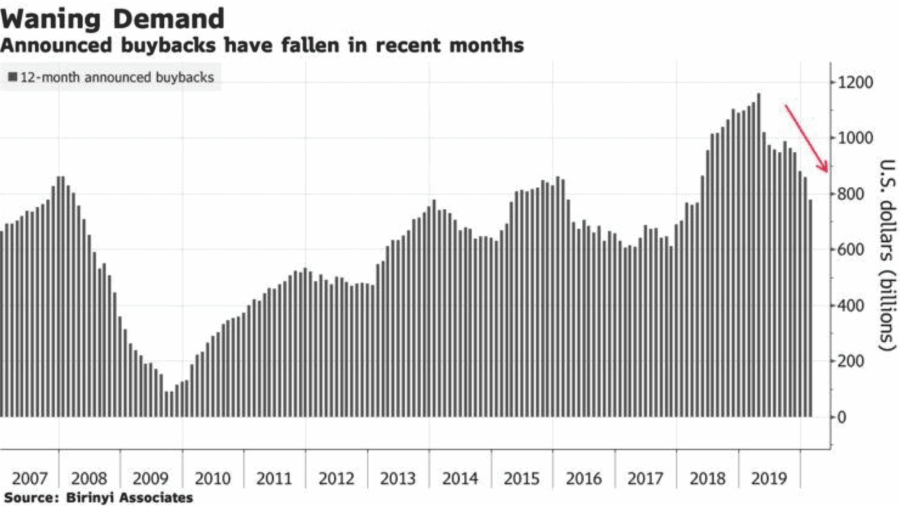

Yes, companies are indeed reacting to the “coronavirus” pandemic currently. However, they were already in the process of cutting back on repurchases in 2019. As noted recently by Jeffery Marcus:

“Birinyi Associates, the leading firm that does research on buybacks, shows below that announced buybacks have declined significantly in 2019… ‘ it’s the biggest drop to start a year since 2009.’”

This is also because cash balances fell sharply, as corporations loaded-up on debt.

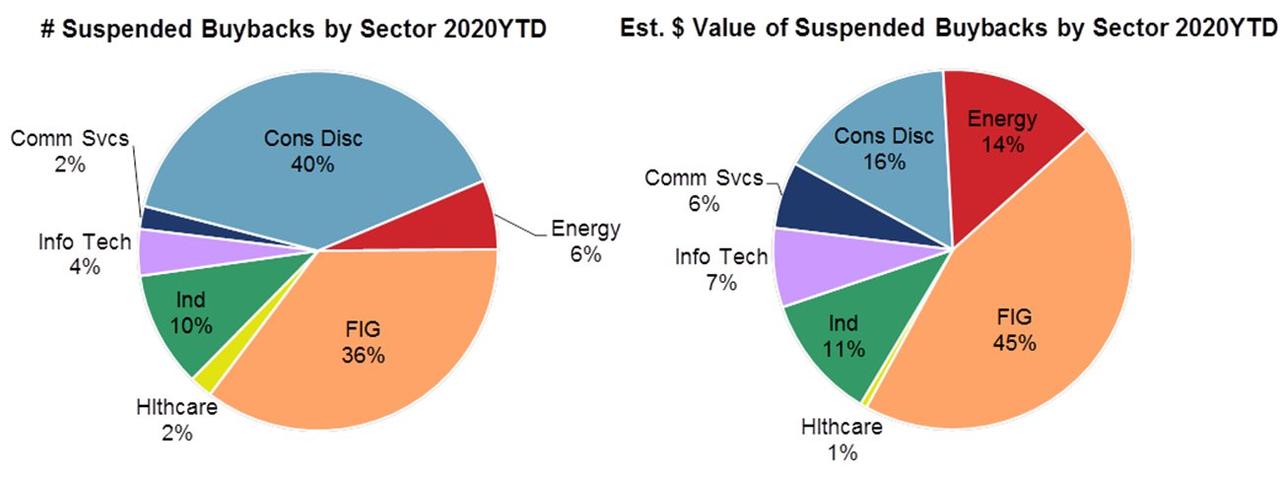

As the impact of the “economic shutdown” deepens, corporations are scrambling to protect their coffers. As noted on Friday, 75% of announced buyback programs have been cancelled.

Corporate buybacks have been the largest source of demand the last few years. 75% of announced buyback programs have been cancelled. So who is the incremental buyer with Boomers retiring in droves who hold the majority of wealth? pic.twitter.com/1IlRrruxDX

Greg’s tweet has a complete table, but here is the relevant chart. There is a tremendous amount of support being extracted.

Do not dismiss the data lightly.

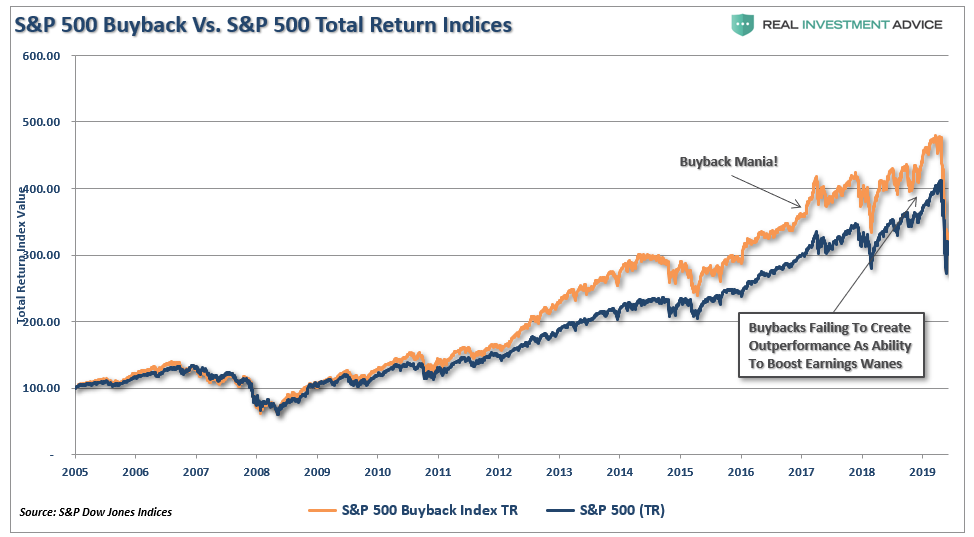

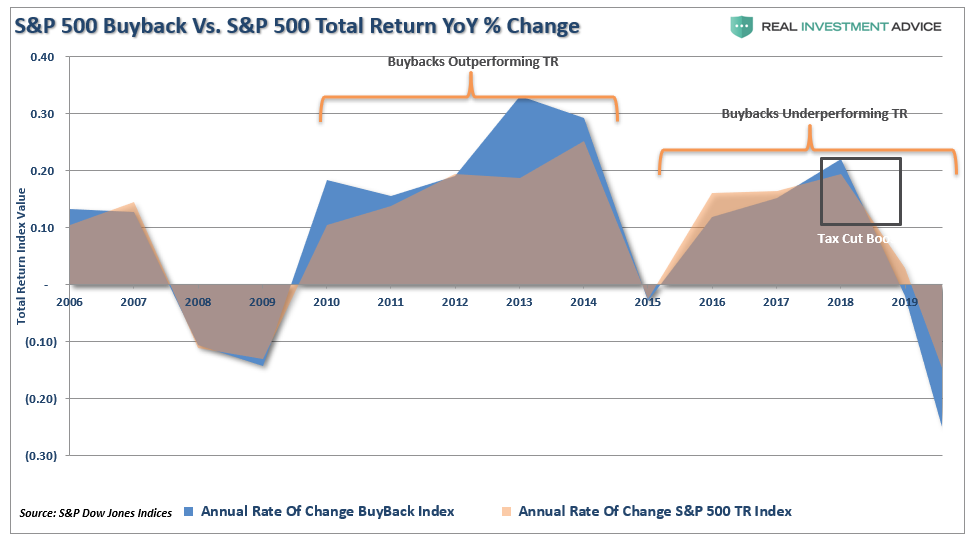

The chart below is the S&P 500 Buyback Index versus the Total Return index. Following the financial crisis, as companies began to lever up their balance sheets to increase stock buybacks. There was a marked outperformance by those companies leading up to the crisis.

However, while corporate buybacks have accounted for the majority of net purchases of equities in the market, the benefit of pushing asset prices higher, outside of the brief moment in 2018 when tax cuts were implemented, allowing for repatriation of cash, performance has waned. Now, those companies which engaged in leveraging up their balance sheet to engage in repurchases shares are significantly underperforming the total return index.

Without that $4 trillion in stock buybacks, not to mention the $4 trillion in liquidity from the Federal Reserve, the stock market would not have been able to rise as much as it did over the last decade.

Conclusion

As I stated, CEO’s make decisions on how they use their cash. With the economy shut down, layoffs in the millions, and no clear visibility about the economic recovery post-pandemic, companies are going to become vastly more conservative on the use of their cash.

Given that source of market liquidity is now gone, the market will have a much tougher time maintaining current levels, much less going higher. As noted by the Financial Times:

“The rebound in equities has sparked optimism that we may be past the worst. However, we still believe it is too early to the call the bottom. From a positioning perspective we still believe there hasn’t been a full capitulation.

Hedge funds and risk-parity funds have reduced their equity exposure considerably. But institutional active funds and passive products have room for further outflows. The fiscal bill passed by the US government also allows individuals to withdraw up to $100k from their 401k, without penalty. We believe this could result in over $50bn of further outflows from the retail community.As well, over 50 companies in the S&P 500 have already suspended their share repurchase programs, which accounted for over 25% of buybacks in 2019. We believe the slowdown in buybacks could result in $300bn of lost inflows in the next two quarters.” – HSBC

Be careful.

The bear market isn’t over yet… not by a long shot.