Submitted by Nick Colas and Jessica Rabe of DataTrek

Three points to cover today:

New York City is bracing for “Peak COVID-19” this week but there are hopes that we can avoid the worst-case outcomes.

The 2008 Playbook calls for 2-3 weeks of volatile stability for the S&P 500.

The 1973/1974 history is another guide for what happens when investors reset corporate earnings expectations sharply lower: a 2-year bear market and a 37% decline (just like 2008).

#1: Update from New York City:

Driving around town doing food shopping yesterday we saw very few people out and about. The local supermarket was well stocked (ex cleaning supplies and TP, of course).

Even the hardiest local store owners are increasingly choosing to close up for now. Our local corner bodega, owned/run by 2 Korean families, has been shuttered for a week. They are normally open 24/7/365.

Overall, the city is amazingly quiet. Anecdotal evidence says Manhattan families have left New York to isolate themselves at weekend/rental properties outside the city with more room for their children. Younger single New Yorkers, in many cases reliant on the city’s hospitality/services industries, have gone home to be with their families while they wait for unemployment checks.

Many businesses and individuals are simply not paying April rent, and obviously May is not looking good either. There is lots of chatter about apartment buildings with heavy Airbnb exposure that will see many broken leases in the coming weeks.

Bottom line: New Yorkers actually go into the week with some modest hope that our peak-infection/hospitalization rate, due in the next 7-14 days, may not as be as bad as the worst-case scenarios. That’s what the latest data says, anyway, and no one will be happier than New Yorkers if the models prove dramatically incorrect. Anything better than awful will feel like a huge win at this point.

#2: 2008 Playbook Update: what’s happened so far…

19 days into 2020’s COVID-19 Crisis the S&P 500 is down 9.4% from March 9th, the first down +5% day of this period that we use as our starting point.

That is roughly half the 20.8% decline from September 29th, 2008 to October 24th, 2008, which had the same number of trading days as the 2020 comparison noted above and also started with a down +5% day.

The reason for that better 2020 performance is the speedy response by the Federal Reserve and Congress to address financial market liquidity concerns and household/business cash flow stresses.

Last week’s daily changes in the S&P 500 closely mirrored the ones from October 20th – 24th 2008 (the analog week then-to-now) in freakishly similar fashion: Monday (+4.8% then, +3.4% now), Tuesday (-3.0%, -1.6%), Wednesday (-6.1%, -4.4%), Thursday (+1.3%, +2.3%) and Friday (-3.5%, -1.5%).

The net result: in the 2008 Financial Crisis, the S&P fell by 6.8% in its comparable week to now; in 2020, the decline was 2.1%.

And what it says to expect over the near term:

Over the next 2-3 weeks: a lot of volatility that doesn’t really take us anywhere. In 2008’s comparable period the S&P ranged from 877 (the equivalent of Friday’s 2,489 level) to a high of 1,006 (+15% over 7 days) but closed the 3-week sequence essentially unchanged at 873.

Worth noting: the analogous 2008 forward 3-week period to now includes a US general election, where the S&P 500 dropped 10% over 2 days right after Barack Obama’s win.

Also worth a mention: the 2008 lows came in the week after the 3-week holding period we’re describing here. The S&P 500 fell 14% from November 14th to the 20th and bottomed on the latter date at 752.

Takeaway: even if 2020 continues to run a half-the-damage version of the 2008 Playbook, the next 2-3 weeks will still see pronounced day-to-day volatility and no net change in stock prices at the end of that period, but… The 2008 experience says to expect a fast flush after this, which:

If 2020 holds to its 50%-as-bad ratio would take the S&P 500 to 2314 (down 7% versus down 14% in 2008). That would be a minor new low from March 23rd’s close of 2,237.

If 2020 hews more closely to the 2008 final flush, that would take the S&P 500 to 2,140 (the full 14% drawdown from Friday’s close).

#3: 1973/1974 Playbook

You have to go back to the 1973 – 1974 oil shock to find a time when investors had to reset corporate earnings expectations because of a truly unexpected and profound exogenous shock. It is an imperfect comparison, of course, to now.

We got to wondering how the S&P 500 traded starting in October 1973 through December 1974.

At the start of October 1973, the S&P 500 was already down 8.1% on the year.

As the Saudi oil embargo kicked in during October and through the rest of 1973, the S&P fell by a further 10.0% through year end. Its total return in 1973 was -14.3%.

The index then fell through most of 1974, bottoming in October down 36% on the year before rebounding 10% to close the year with a negative 25.9% total return.

Takeaway: as we’ve highlighted regularly since the virus crisis started, the S&P 500 at 2,500 expresses essentially 100% confidence that structural corporate earnings power remains solid. That level is 21x trailing 10-year average S&P 500 earnings of $122/share; in 2009 we bottomed at 10x trailing S&P earnings.

Pulling these 3 points together:

New York City is not just the US epicenter of the virus; it is also Wall Street’s most-watched case study of peak health system stress and eventual economic recovery. Once the daily hospitalization rates start to convincingly stabilize (1 to 2 weeks away), the conversation will inevitably shift to restarting the city’s economy. How that happens and at what pace will be the market’s template for the rest of the United States.

Any local NYC or national restart will be unpredictable in terms of cadence and industry-specific fundamentals. Some days will bring good news, others bad. That narrative fits with the 2008 playbook of volatile meandering over the next 2-3 weeks.

The 2008 and 1973/1974 Playbooks highlight what we need to avoid: a wholesale market rethink of corporate earnings power. The effectiveness of US fiscal and monetary stimulus will need to act as the counterweight to those concerns until the domestic economy starts to come back to life.

Jamie Dimon Warns Of Coming “Bad Recession,” Repeat Of 2008 Crisis In Annual Letter

Sounding a markedly more somber note about the global economy than he has in the past few years, JPMorgan CEO Jamie Dimon released his annual ‘investor letter’ Monday morning, warning the world that, from Dimon’s vantage point, at least, the US appears to be on the verge of a “bad recession” that could be exacerbated by “financial; stress similar to the global financial crisis of 2008.”

Though, leaving off on an optimistic note, he warned that while the challenge ahead might be great, he believes the US economy can emerge from it “stronger” than in the past.

“We have the resources to emerge from this crisis as a stronger country,” Dimon said in the letter. “America is still the most prosperous nation the world has ever seen.”

This, after sell-side banking analysts have spent the last two weeks telling CNBC’s audience that the banks are much better capitalized this time around (though excessive corporate debt is keeping some up at night).

“At a minimum, we assume that it will include a bad recession combined with some kind of financial stress similar to the global financial crisis of 2008,” Dimon wrote in the letter to shareholders. “Our bank cannot be immune to the effects of this kind of stress.”

The fact that the CEO’s 23-page letter is his shortest in more than a decade (since March 2008, just months before the global economy nearly collapsed) is hardly a surprise: Dimon suffered a sudden ‘heart tear’ requiring him to have sudden, emergency surgery earlier this month. The letter is roughly one-third the length of last year’s screed, where Dimon laid out his vision of a more ‘responsible’ and ‘equitable’ iteration of American capitalism, while also warning that ‘democratic socialism’ was not the way to go.

As far as JPM is concerned, Dimon reminds us that the bank’s 2020 submission to the annual Fed stress tests indicate that even in an “extremely adverse scenario,” JPMorgan can lend out an additional $150 billion for clients. The New York-based bank had $500 billion in total liquid assets and another $300 billion in borrowing ability from Fed sources, he added.

Notably, while JPM “will participate in government programs to address the severe economic challenges, we will not request any regulatory relief for ourselves,” Dimon added, echoing language he used during the financial crisis.

Because of his illness, Dimon hasn’t weighed in publicly about the virus since late February, during the bank’s annual investor day.

For a quick rundown, see CNBC’s Wilfred Frost below:

Futures Soar On Optimism Worst Of Virus Pandemic Is Behind Us (But Is It)

As prompted by Trump’s optimistic speech on Sunday evening in which the president said he saw signs the pandemic is beginning to level off, which came after a sharp drop in the latest number of NY corona cases, an optimistic mood of trader euphoria that the peak of the coronavirus pandemic is behind us helped boost stocks around the globe, and sent US equity futures as much as 4% higher.

Besides a potential inflection point in the global coroanvirus epicenter of New York, which however was challenged that there appears to be an odd decline for the second weekend in a row which then rebound sharply…

… Equity investors were encouraged as the death toll from the virus slowed across major European nations including France and Italy. London’s FTSE raced up 2%, indexes in Paris and Milan rose 3% and Germany’s DAX gained more than 4% after Japan’s Nikkei finished with similar gains overnight. Safe havens such as Treasuries and the yen fell, even as the dollar stay oddly strong and gold soared as new global coronavirus cases declined for two days in a row.

* “Global deaths 4.7k, down two days in a row

* NY: Gross new hospitalized down two days in a row; .. peak strain now exp within a week

In Europe, the Stoxx Europe 600 Index jumped led by automakers and travel and leisure shares after Italy and Spain said they had the fewest deaths in more than two weeks, and Germany and France reported the lowest numbers in days. Corona-optimism was so widespread it allowed traders to ignore the total collapse in the economy: iInvestor morale in the euro zone fell to an all-time low in April and the currency bloc’s economy is now in deep recession due to the coronavirus, which is “holding the world economy in a stranglehold”, a Sentix survey showed. Orders for German-made goods had already dropped 1.4% in February, German data showed. British car sales slumped 40% last month and Norweigen Air’s traffic plummeted 60%.

“Never before has the assessment of the current situation collapsed so sharply in all regions of the world within one month,” Sentix managing director Patrick Hussy said. “The situation is … much worse than in 2009,” Hussy said. “Economic forecasts to date underestimate the shrinking process. The recession will go much deeper and longer.”

Still, it wasn’t one of those days when data would spoil trader mood, and Wall Street S&P500 emini futures were up almost 4%, close to their upper limit too, bouyed by comments from U.S. President Donald Trump that his country was also seeing a “levelling off” of the crisis. “What is driving the market is the evidence that the number of new cases has started to turn the corner,” said Rabobank’s Head of Macro Strategy Elwin de Groot. As well as a slowdown in deaths in Italy, he said, improvements were starting to become visible in Spain and even in the United States there had been a little bit of a let-up. “When you see that happening you can start gauging when lockdowns can start to be gradually lifted. That gives a little bit more visibility and that is vital,” he added, although he stressed there were still huge uncertainties and risks.

Earlier in the session, Asian stocks were also mostly higher, with Australia’s benchmark index up 4.33%, Japan’s Nikkei added 4.24% even as that country moved closer to declaring a state of emergency. South Korea’s KOSPI index climbed 3.85%. Hong Kong’s Hang Seng index was 2.18% higher. That sent MSCI’s broadest index of Asian shares outside of Japan up 2%, on track for its best performance in more than a week. Markets in mainland China were closed for a public holiday.

The upbeat tone follows another negative week, and the mood among investors remains divided. As Bloomberg notes, bulls are pointing to more attractive valuations, unprecedented stimulus and now slowing death rates in several major countries. Bears are fretting the continued spread of the disease, dismal economic data and the rising corporate costs of the pandemic and subsequent shutdown.

“We are still optimistic that the administration will be able to get this virus under control and reopen the economy by the end of April, early May,” Lindsey Piegza, chief economist at Stifel Nicolaus & Co., said on Bloomberg TV. “If that does occur, it’s likely that we’re able to control the downturn from a depressionary scenario into a recessionary scenario.”

Worryingly, the number of new coronavirus cases jumped in China on Sunday, while the number of asymptomatic cases surged too as Beijing continued to struggle to extinguish the outbreak despite drastic containment efforts. “Focus in markets will now turn to the path out of lockdown and to what extent containment measures can be lifted without risking a second wave of infections,” National Australia Bank analyst Tapas Strickland wrote in a note. “Key to a strong rebound in China will be the ongoing lifting of containment measures, with Wuhan – the epicentre of the outbreak – set to lift containment measures on April 8.”

Optimism aside, there was plenty of news to demonstrate just how brutal the virus has been: eye-popping plunges in car sales and air travel in Europe, Britain’s prime minister being hospitalised, and Japan preparing to declare a state of emergency. But the markets appeared hopeful.

Beside the ramp in stock, the other big overnight move was in crude which pared a decline of as much as 11% though it remained lower as uncertainty swirled over a proposed meeting of the world’s top producers.

In FX, the dollar barely budged against the euro; the yen weakened as haven demand receded and Japanese Prime Minister Shinzo Abe said he will propose to declare a state of emergency in prefectures including Tokyo and Osaka for about a month. Commodity currencies advanced, led by Norway’s krone, after the reported death tolls in some of the world’s coronavirus hot spots showed signs of easing over the weekend. The Mexican peso slumped over 3% to a record low in Asian trading before paring losses after the nation’s stimulus pledge fell short of some investors’ expectations The pound fluctuated before turning higher even as U.K. Prime Minister Boris Johnson was admitted to hospital for tests after suffering from the coronavirus for 10 days.

In rates, the 10Y yield jump as high as 0.67% after trading around 0.60% on Friday; yields on safe-haven German government bonds crept higher in fixed income markets too, reflecting the slightly brighter tone in world markets despite some painful data.

Market Snapshot

S&P 500 futures up 3.6% to 2,572.75

STOXX Europe 600 up 2.5% to 316.64

MXAP up 2.5% to 135.67

MXAPJ up 2.1% to 437.12

Nikkei up 4.2% to 18,576.30

Topix up 3.9% to 1,376.30

Hang Seng Index up 2.2% to 23,749.12

Shanghai Composite down 0.6% to 2,763.99

Sensex down 2.4% to 27,590.95

Australia S&P/ASX 200 up 4.3% to 5,286.81

Kospi up 3.9% to 1,791.88

German 10Y yield rose 1.8 bps to -0.423%

Euro down 0.06% to $1.0794

Italian 10Y yield rose 8.3 bps to 1.379%

Spanish 10Y yield fell 2.0 bps to 0.722%

Brent futures down 2.2% to $33.36/bbl

Gold spot up 0.7% to $1,632.32

U.S. Dollar Index up 0.2% to 100.74

Top Overnight News from Bloomberg

Germany saw the lowest number of new coronavirus cases in six days, a tentative sign that lockdown measures are easing the outbreak

Oil pared earlier losses amid signs Saudi Arabia and Russia are making progress on an agreement to curb crude output as the coronavirus wreaks havoc on the global economy

Congress‘s near unanimity on last month’s $2.2 trillion coronavirus rescue bill has given way to partisan finger-pointing that threatens to poison the debate when lawmakers try to construct another emergency boost to the struggling economy

The Bank of Japan set itself up to buy more bonds in the key 5-to-10 year maturities, showing an intent to maintain yield-curve control amid growing expectations of further debt-fueled stimulus from the government

Asian equity markets traded mostly positive and US equity futures also began the week on the front-foot as participants saw a glimmer of hope from a slowdown in the pace of coronavirus deaths for several hotspots including New York, Spain and Italy in which the latter had its lowest daily death toll since March 19th. ASX 200 (+4.3%) was underpinned amid broad gains across its sectors and with notable outperformance in healthcare following reports that Australian scientists found that Ivermectin which is produced by Merck for treatment of parasites and head lice was successful in killing coronavirus within 48 hours and that the next phase will be for human trials. Nikkei 225 (+4.2%) coat tailed on the favourable currency moves and ahead of this week’s expected roll out of the stimulus package which is said to include increased subsidies, tax deferrals and cash payments to households. Hang Seng (+2.2%) was also positive following the recent monetary policy efforts in the region including the PBoC’s 100bps RRR cut announcement and with the HKMA halving the amount of reserves banks are required to set aside against bad loans, although gains were somewhat limited amid a lack of mainland participants due to the Ching Ming holiday in China. Finally, 10yr JGBs were lower with prices pressured amid gains in stocks and anticipation for increased supply with the Japanese government set to announce a stimulus package and state of emergency declaration which could occur as early as tomorrow.

Top Asian News

Japan’s Abe Moves to Declare Emergencies in Tokyo, Osaka Areas

Japan Banks Weigh Branch Cutbacks Ahead of State of Emergency

Japan Consumer Confidence Tanks to Lowest Since Financial Crisis

Singapore Adds S$5.1 Billion to Stimulus, Boosts Handouts

European equities remain firm (Eurostoxx 50 +3.8%) following a similarly positive APAC session, in which sentiment was bolstered amid positive COVID signals in key hotspots across Europe. In terms of regional performance, UK’s FTSE 100 (+2.0%) lags its peers across the channel as exporters in the index are weighed on by a firmer Sterling, whilst heavyweight energy names (Shell -0.5%, BP -2.5%) also pressure the index amid price action in the complex, with the latter also reducing production at three US refineries by ~15%. European sectors are mostly in the green (ex-energy) with cyclicals outpacing the defensives – reflecting risk appetite. Looking at the sector breakdown, Travel & Leisure leads the gains following multiple consecutive sessions of underperformance, while oil and gas reside at the bottom. Despite the energy sector overall on the backfoot, Tullow Oil (+47%) and Subsea 7 (+8%) see themselves at the top of the Stoxx 600, having seen detrimental losses from the oil market crash. Looking at other individual movers, Rolls-Royce (+14.8%) shares soared higher after announcing the securing of an additional GBP 1.5bln (vs. Exp. above GBP 1bln) revolving credit facility, thus increasing overall liquidity to GBP 6.7bln. Co. also announced that around GBP 300mln of headwinds are seen from COVID-19, whilst cost-cutting measures include a minimum 10% reductions in salaries across the global workforce this year. Rolls-Royce also confirmed it is withdrawing its FY20 guidance. GVC Holdings (+6.4%) sees strength on the back of an undrawn credit facility worth GBP 550mln, whilst expecting a virus impact of GBP 50mln per month. Pirelli (+1.9%) trades higher after announcing further cost-cutting measures, albeit the Co. reduced its FY revenue guidance to EUR 4.3-4.4bln from EUR 5.4bln whilst cutting its EBIT margin target to 14-15% from 17%. Elsewhere, NN Group (-9.5%) resides at the foot of the pan-European index after postponing its dividend and suspending its EUR 250mln share buyback scheme. Broker-led price action includes BBVA (+7.8%), ADP (+6.2%), Carrefour (+2.5%), Carlsberg (+1.5%) and Nokian Renkaat (-1.0%). Finally, as US equity futures hover near session highs, it is worth keeping tabs on today’s limit-up levels: E-Mini S&P (M0) 2601.50, E-Mini Nasdaq (M0) 7888.00 and E-Mini Dow (M0) 21972 – levels which have not yet been reached.

Top European News

Europe’s Virus Outbreak Shows Signs of Slowing on Lockdowns; Europe Stocks Rise Most in Nearly Two Weeks

Germany Tells Italy, Spain to Tap ESM If They Want Quick Aid

Dividend Halt Puts HSBC at Risk of Losing Core Investors

Tullow Jumps Most in at Least 31 Years; Volume Quadruples

In FX, Somewhat contrasting starts to the new week for the Euro and Pound as the former loses grip of the 1.0800 handle again vs the Dollar, but the latter pares losses close to 1.2200 and briefly trips stops at 1.2300 on the way to a circa 1.2320 recovery high on news that UK PM Johnson may be heading back to 10 Downing Street soon having been hospitalised over the weekend for nCoV related tests. Eur/Usd has been undermined by a sharp deterioration in the Eurozone Sentix Index and Eur/Gbp selling that has cushioned Sterling to an extent from a deeper than anticipated sub-50 collapse in the UK construction PMI.

AUD/NZD/CAD/NOK/SEK – A clear risk on divide across the rest of the G10 currency spectrum, but with the Greenback gleaning more traction to counter post-NFP weakness via gains vs safer havens that have a greater weighting in the DXY basket. Indeed, the index is nudging the upper end of a 100.850-460 range even though the Aussie, Kiwi and Loonie are all benefiting from less angst over COVID-19 following a decline in the number of confirmed cases and fatalities recorded in epicentres outside China including Italy and Spain. Aud/Usd is firmly back up above 0.6000 eyeing Tuesday’s RBA policy meeting when rates are expected to remain unchanged after recent emergency and scheduled easing, although money market pricing is more even between another 25 bp reduction and no further move. Nzd/Usd has reclaimed 0.5900+ status ahead of NZIER Q1 confidence, while Usd/Cad is hovering around 1.4100 vs 1.4260 at one stage as oil prices recover from another sharp retreat on a degree of OPEC+ disappointment given a delay to the emergency meeting from today until Thursday, at least. Relative calm in crude is also underpinning the Norwegian Krona along with reports that the Government may mull cutting oil output if there is general international consensus, and the Swedish Crown is tagging along.

JPY/CHF – The major laggards amidst renewed risk appetite on the aforementioned seemingly encouraging coronavirus developments, as the Yen falls below 109.00 and Franc meanders between 0.9762-89 in the run up to BoJ and SNB FX reserves data due tomorrow that will be monitored to see how much intervention, if any has been curbing demand for the safe havens. On that note, latest weekly Swiss bank sight deposits already reveal hefty activity as Eur/Chf remains entrenched around 1.0560.

EM – Whippy trade in regional currencies as positive vibes from overall risk sentiment vie with far less upbeat independent factors, like the Rand having to digest another ratings cut following Fitch deciding to downgrade SA deeper into junk territory. However, Usd/Zar has managed to pare back from new 19.3400+ record highs and Eur/Huf is off its all time peak around 368.00 awaiting Hungarian PM Orban’s economic stimulus plan that could equate to 20% of GDP.

In commodities, WTI and Brent front-month futures remain subdued, albeit way off the lows posted at the electronic open in which the contracts fell some 10% after OPEC+ postponed its tentative meeting, whilst Saudi and Russia played the blame game over the weekend. In terms of where we stand, the OPEC+ meeting will now be conducted on Thursday instead of the initially planned Monday – with sources noting the delay was to convince other countries to join in on output curtailment plant. Prices were also pressured after Russian President Putin partly blamed Saudi Arabia for the collapse in prices, whilst the Kingdom points the finger at Moscow’s hesitation at the March OPEC meeting – sources also noted that a lack of US commitment is complicating talks. That being said, the CEO of RDIF Dmitriev noted that Moscow and Riyadh are said to be “very, very close” to a deal on oil production cuts. Meanwhile, US President Trump on the weekend said he was considering slapping tariffs on oil imports, or even take other such measures, in order to protect the US energy sector from falling oil prices; Canada is reportedly considering similar measures. Following calls by leading lawmakers in recent weeks for such action. For reference, the US’ imports of petroleum were around 9.1mln BPD in 2019, of which Saudi and Russian imports measured just over 500k each. WTI May futures dipped below its 21 DMA (USD 25.89/bbl) at the open to a low of USD 25.28/bbl before recouping losses amid the overall risk appetite and the prospect of US intervention in the oil markets. Similarly, Brent June printed a low of USD 30.00/bbl, ahead of its respective 21 DMA at USD 29.26/bbl, with prices eyeing USD 34/bbl at the time of writing. The spread between the contracts has also widened to ~USD 6/bbl from Friday’s almost USD 4/bbl. Elsewhere, spot gold gains ground above USD 1600/oz as the USD retreats, and from a technical standpoint, the yellow metal could see mild resistance at USD 1637.50/oz (30 Mar high) before some psychological play at USD 1640/oz. In terms of news-flow for gold, gold refiners PAMP, Valcambi and Argor-Heraeus have been given approval to restart operations at 50% max capacity, having been asked to shut operations in late March. Copper meanwhile remains contained within the tight USD 2.15-2.25/lb range seen over the past 4 sessions, with the red metal again mimicking price action in global stocks.

US Event Calendar

Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

I listened to a talk radio show on Saturday that was unsurprisingly centred around the current pandemic. A 95 year old dialled in and said he lived through the global flu pandemics of the late 1950s and 1960s and was amazed at how much our thinking had changed over the last 50 years. Back then he said that people had so many threats to life that they just accepted the health risks of a new virus and got on with everyday life. He cited that Polio killed over half a million people per year worldwide at its peak in the 1940s and 1950s. Other illnesses that are now trivial also killed numerous people. It made me think that our generation and that of our parents have been so brilliant and successful in minimising death by contagious infections and disease that we really struggle when we are exposed to a new threat. Maybe in around 300,000 years of human existence this is the first pandemic where we have a near zero tolerance for risk given all that we’ve achieved medically over the last several decades and as such this is the first that has prompted a near global economic shut down.

On this it is still unclear to me what the exit strategy will be in the West from the lockdowns. In our note of the same name from last week (link here ) we used our Hubei model to speculate that restrictions would likely start to be lifted around mid-May with some countries slightly earlier and some slightly later. These restrictions would be eased in phases with domestic functioning economies prevailing with limited international travel for a while. At the point of publishing I felt the risks were balanced between a slightly better outcome than this and a worse one. However in a week where we’ve seen new cases emerge (albeit in relatively small numbers) in HK, Singapore and China with new restrictions being put in place, I’m starting to wonder how you can loosen restrictions in the West very quickly without seeing new cases increase again. Another argument for a later date of restrictions being lifted is the fact that while those most advanced through the cycle, namely Italy and Spain, are seeing their new case and fatality growth rate slow encouragingly, if you look at the graphs in our Corona Crisis Daily they are not falling as quickly as Hubei province did. I suspect to successfully reopen economies without fear of subsequent mini shutdowns or holding back significant amounts of activity we will need the antibody test rolled out so that a certain part of the population can work through regardless of the state of the viral spread. That will be the real breakthrough until we get a vaccine. Without that I fear it’s going to be tough to fully control the virus in the West. The U.K. is on the more liberal side of the lockdowns restrictions at the moment and from media reports it was noticeable that a very sunny weekend led to a number of people using parks and outdoor places more than the current restrictions intended. All this and we are only coming to the end of the second week of official lockdown here. It wouldn’t be a surprise if the U.K. felt the need to move to more strict rules in the days ahead.

In terms of new cases and fatality rate growth rates the U.K. had a better weekend as you’ll see in the Corona Crisis Daily. However we did see a similar trend over the last two weekends with the numbers not catching up until early in the “working” week. So if Monday and Tuesday’s numbers continue to see percentage growth rates slow then this is good news. But we need to be cautious for now. Elsewhere Italy and Spain growth rates in both variables continue to slow but as discussed above the absolute number of deaths are not falling on a daily basis as aggressively as Hubei/China saw at a similar stage. Overall global new case growth and fatalities are slowing but are they slowing quickly enough to work out when economies can reopen?

As we start Easter week, Asian markets are on the front foot this morning with the Nikkei (+2.33%), Hang Seng (+1.11%) and Kospi (+2.55%) all up. Chinese markets are closed for a holiday and futures on the S&P 500 are up +3.36%. In FX, Sterling is down -0.28% after Prime Minister Boris Johnson was admitted to hospital for tests after suffering from the coronavirus for 10 days. Elsewhere, yields on 10y treasuries are up +3.1bps to 0.628%.

Oil has fallen overnight with Brent currently down -2.23% and WTI -3.99% however that does compare to drops in the double digits when markets opened. This follows news over the weekend that the OPEC+ meeting planned for today has been pushed back and only tentatively rearranged for Thursday with the main protagonists in behind the scenes chat as to whether there is scope for production cuts.

Overnight, Bloomberg is reporting that the Japanese government will release the economic stimulus package in response to the coronavirus pandemic in two phases with the first phase of measures designed to prevent job losses and bankruptcies. The second phase of the package will be implemented once the spread of the virus is contained to support a V-shaped recovery. Meanwhile, various Japanese media outlets are reporting this morning that PM Shinzo Abe is set to declare a state of emergency within days, after coronavirus cases in Tokyo jumped over the weekend to top 1,000 for the first time and raised worries of a more explosive surge. The Yomiuri newspaper reported that Abe will announce the plan as soon as today, with the formal declaration for the Tokyo area coming as early as Tuesday.

In other overnight news, the FT has reported that the largest US banks will defend their plans to pay dividends in their annual capital plans due for submission to the Federal Reserve. Elsewhere, President Donald Trump and Vice President Mike Pence said overnight that they are seeing signs that the US coronavirus outbreak is beginning to level off or stabilize, citing a day-to-day reduction in deaths in New York.

The highlight this week could be the Eurogroup meeting held tomorrow via video conference which follows the invitation from the European Council on 26 March for the Eurogroup to present proposals within two weeks. I had the fortune of speaking to DB’s Mark Wall yesterday who gave me some advice on what to expect tomorrow. He said that various press reports suggest that the Eurogroup will be debating a three-part proposal for a centralised response. This is said to consist of a healthcare funding plan from the ESM worth up to EUR200bn, EIB credit guarantees worth as much as EUR200bn and an EU-wide short-shift or partial unemployment scheme from the European Commission modelled on the German Kurzarbeit scheme worth EUR100bn. A package of this size would be an impressive 4.5% of GDP. The ESB, EIB and Commission each issue the equivalent of common European bonds, so the need for a “coronabond” would be circumvented in the interest of expediency. The details will matter and the three elements are only temporary. As the risk of a protracted pandemic rises, so too does the need to follow up this plan with a centralised demand stimulus package, for example, a large-scale EIB investment programme. So a big meeting to watch.

Elsewhere the Fed minutes from the unscheduled emergency meeting on March 15th will be released. This was the meeting they cut rates 100bps and announced that they would increase their holdings of Treasury securities by at least $500bn and of agency mortgage-backed securities by at least $200bn. Things have moved on since and they injected more stimulus and announced new schemes but it will still be interesting to see how they were thinking at the time. For the rest of the week ahead see the day by day guide at the end.

Looking back at last week and Friday now. Economic data across the world showed massive signs of deterioration last week, especially employment numbers and service sector PMIs, as the economic shutdowns continued to take their toll. Equity markets were relatively calm in the face of it though but with most of the big stimulus announced in the prior two weeks they struggled for positive momentum. Overall, after 3 weeks of over 8% absolute weekly moves, the S&P 500 fell a relatively tame -2.08% over the week (-1.51% Friday), even as the US became the clear epicentre of the coronavirus crisis with over one quarter of the total cases worldwide. The index now sits -26.5% down from the recent all-time highs. Large cap European equities outperformed their US counterparts slightly on the week, with the Stoxx 600 down just -0.59% (-0.97% Friday), though European banks in particular lagged the index, down -13.17% on the week (-3.52% Friday). Equities were down across the continent as countries extended lockdowns even as new case growth recedes in the harder hit regions – Spain and Italy in particular. The DAX fell -1.11% (-0.47% Friday), the IBEX dropped -2.90% (+0.11% Friday) with the FTSE MIB -2.61% (-2.67% Friday), after the three indices gained over 5% the previous week. Asian equities were mixed on the week. The Nikkei fell -8.09% (+0.01% Friday), while the CSI was mostly unchanged at +0.09% (-0.19% Friday) and the Kospi was up slightly at +0.45% (+0.03%) on the week. The VIX fell -18.7pts over the course of the week (-4.1pts Friday) to finish at 46.8 as the S&P 500 saw relatively smaller daily moves. On the back of China increasing oil reserves and President Trump citing the need for intervention in the Russia and Saudi Arabia oil price war, both Brent and WTI crude oil rallied strongly. Brent crude was up +36.82% (+13.93% Friday) and WTI was up +31.75% (+11.93%) on the week. It was the best week for Brent since the data starts in 1988 and far outpaces the next largest 1 week gain – +22.3% in January 2009, while WTI similarly had its best week on record, beating the previous 1 week gain of +28.4% in August of 1986.

Fixed income also saw smaller weekly moves as markets attempted to settle into the new QE regime. US 10yr Treasury yields fell -8bps (-0.2bps Friday) to finish at 0.595%, just 5.4bps from the lowest closing levels on record. Meanwhile in Europe, 10yr Bunds saw yields rise +3.3bps (-0.8bps Friday) to -0.44%. The bigger moves in sovereign bonds last week were with spreads widening to Bunds. French 10yr yields widened +10.0 bps on the week (+3.1bps Friday), while Italian yields widened +19.1bps over the 5 days (+9.2bps Friday), and Spanish 10yr bonds widened +17.0bps (+4.2bps Friday). Credit spreads bifurcated last week. US HY cash spreads were 44bps wider on the week (+26bps Friday), while IG was -16bps tighter on the week (+2bps Friday). In Europe, HY cash spreads were -13bps tighter over the 5 days (-1bp tighter Friday), while IG was 1bp tighter on the week (+1bps Friday).

Friday’s services and composite PMI readings from around the world showed large declines in activity. The final Euro Area composite PMI fell to 29.7, a record low and below the flash reading of 31.4. In February, the PMI had been at 51.6, above the 50-mark that separates expansion from contraction. Germany saw their composite index fall to 35 from 50.7, while the UK’s composite came in at 36.0, down 53.0 a month ago. The Italian numbers were the worst of the major European economies, with the composite PMI falling to 20.2 and the services PMI coming in at 17.4. Incredible numbers. The US Markit service PMI fell to 39.8, slightly up from the flash reading of 39.1. The composite came in at 40.9 vs the flash of 40.5, and down 8.7 points from a month ago.

Also in the US on Friday nonfarm payroll data was released, falling by -701k in March, far below the -100k decline expected. This is the first time nonfarm payrolls have shrunk since September 2010 and this is the largest monthly decline since the -800k reading in March 2009. Notably, the survey reference period was for the calendar week containing the 12th of the month, so the jobs report did not cover the second half of the month when the more serious levels of economic disruption occurred, when nearly 10 million jobless claims were filed. Given that shutdowns in the US are due to stretch to the end of April, next month’s data is likely to be off the charts.

Cops Break-Up Crowd Of Lockdown-Ignoring Mourners At Brooklyn Rabbi’s Funeral

After a week of an exponential rise in confirmed COVID-19 cases and deaths across five boroughs of New York City, Sunday figures showed growth rates in cases and deaths are slowing. However, that doesn’t mean social distancing rules are to be relaxed, as the New York City Police Department (NYPD) busted a large group of Hasidic Jews on Sunday in violation of the state’s social distancing rules.

The incident unfolded on 55th Street and 12th Avenue Borough Park, Brooklyn, where mourners gathered for at least one funeral, several other reports indicate there were multiple.

New York Daily News said a funeral was held for Rav Yosef Kalish, 63, who was hospitalized with the virus and died over the weekend.

A video posted on Twitter shows the NYPD arriving to break up the large crowd, in violation of the state’s and city’s social distancing rules. For fear of contracting the virus, police officers stayed inside the vehicle and played a prerecorded message that said:

“This is the NYPD. Due to the current health emergency, members of the public are reminded to keep a safe distance of six feet from others while in public places to reduce the spread of the coronavirus.”

New York Daily News said the crowd eventually dispersed.

According to the New York Post, funeral attendees asked the NYPD for more time to grieve for their recent loss. Officers on the scene gave the mourners five additional minutes.

It was evident in the video that many Hasidic Jews were violating the government enforced social distancing rules. Some attendees were wearing surgical masks, but many were not. Not one person was wearing a 3M N95 mask nor goggles or a face shield.

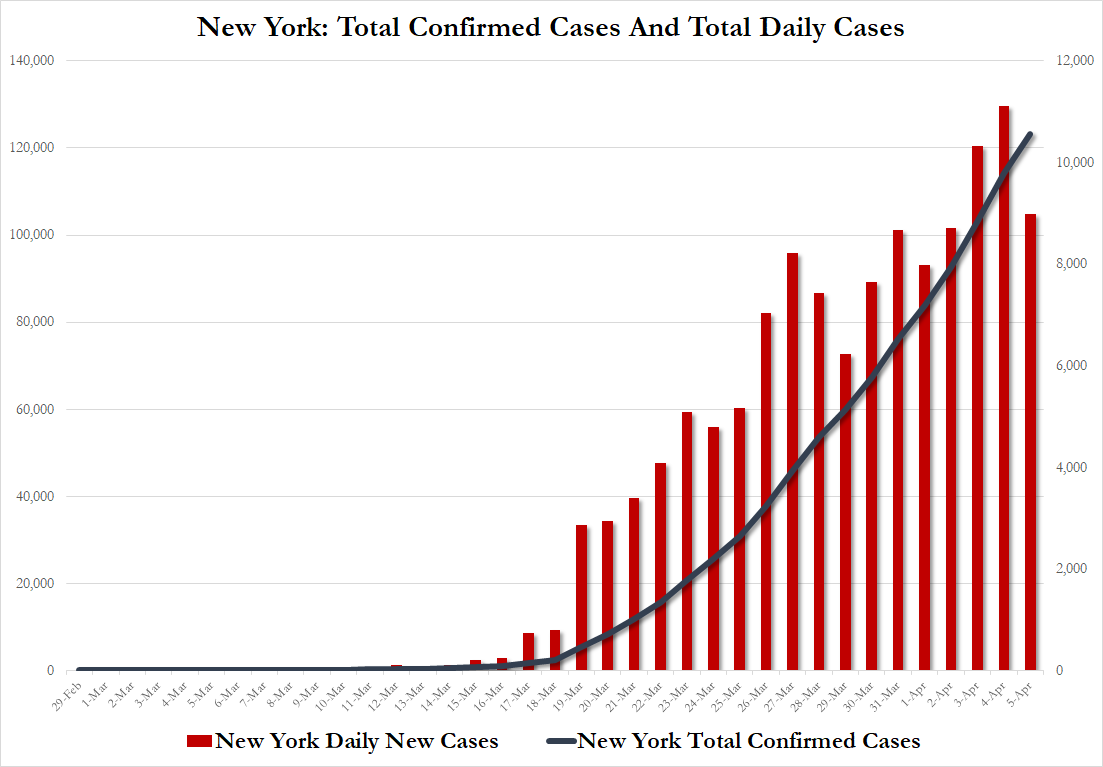

Last month, Hasidic Jews violated social distancing orders by hosting Brooklyn weddings, as the fast-spreading virus was silently ravaging the city, mostly because test kits were lacking. As test kits have become available in recent weeks, confirmed tests have exploded. As of Sunday night (April 5), there are 123,160 confirmed cases and 4,159 deaths.

Gov. Andrew Cuomo last month banned crowds of 50 or more, and President Trump advised Americans to avoid groups of more than 10 to mitigate the spread of the virus.

Cuomo recently said any resident who breaks social distancing rules would be subjected up to $500 fine.

Doubts Raised About Reported Drop In NYC Deaths As “The Hardest And Saddest Week Of Our Lives” Begins: Live Updates

During an appearance on “Fox News Sunday” yesterday morning, Surgeon General Jerome Adams told Chris Wallace that the upcoming week will be “the hardest and saddest week of most Americans’ lives,” calling it our “our Pearl Harbor, our 9/11 moment,” except that, unlike those attacks, this one won’t be “localized” – it will be unfurling across the US, almost simultaneously.

Nearly 12 hours later, President Trump and VP Pence said during the evening’s task force press briefing that the numbers reported out of Continental Europe and New York earlier that day were “very optimistic,” sending futures on what looks like their most bullish trading to kick off a new week since the end of the ‘rona rout (or at least, the first installment of it).

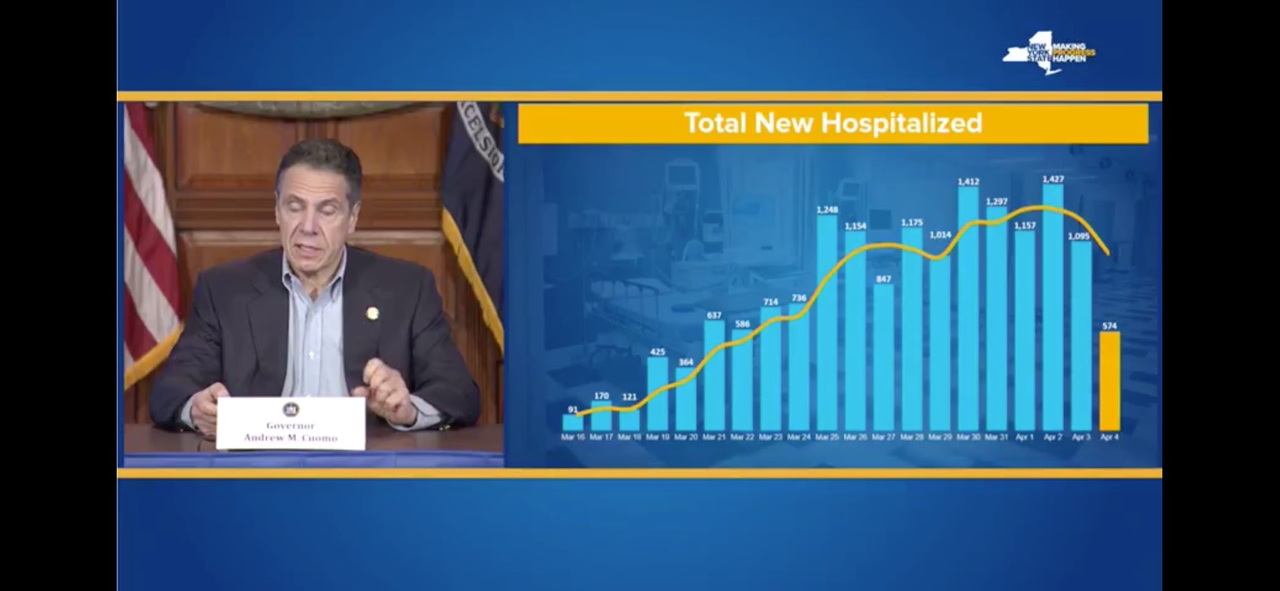

The second day of declining hospitalizations state-wide was one of the most optimistic numbers reported yesterday by Cuomo.

Numbers showing deaths in NYC declined yesterday for the second day in a row, when they were reported by NYC Mayor Bill de Blasio. De Blasio also revealed last night that the feds had sent NYC 174 nurses, 104 doctors and 13 respiratory therapists, not enough to completely make up the shortfall, but “a start”, the mayor said.

Before people get too excited about these latest numbers out of New York, we noticed several epidemiologists and other ‘data people’ found flaws in the numbers that they highlighted on Twitter. One expert who reviewed the data said she found a pattern that suggests the city might have underreported deaths yesterday, meaning these encouraging numbers don’t reflect reality, and that more deaths would be reported later on Monday to compensate.

Here’s Dr. Andrea Feigl, a Harvard-trained medical writer:

While equity strategists appeared to focus on the strong numbers out of the Continental Europe yesterday, (Italy, Spain, France, Germany, Belgium, the Netherlands, mostly), numbers out of the UK, where the Queen delivered a landmark speech while the PM was admitted to the hospital with brutal COVID-19 symptoms, were much more alarming, with the largest jump in deaths reported yet as the UK’s death toll has accelerated over the past week. Meanwhile, reports that Britons continue to flout the lockdowns despite the crackdown by police have vexed those trying to combat the outbreak.

Worldwide, we’re on the verge of 70k deaths as the virus continues to spread, finally accelerating in places like Brazil, and elsewhere across Latin America, while small outbreaks have cropped up in practically all of Africa’s 54 countries.

The same is true in Asia: While South Korea reported just 47 new cases of the coronavirus, the lowest daily uptick since infections began surging on Feb 21., and the first time that number has dipped below 50 since then as well. At the peak, SK was reporting 900+ new cases daily. As one reporter noted on twitter, things could still turn on a time, but it’s definitely a milestone for the country with arguably the most effective response to the virus in the world.

South Korea reports just 47 new cases of the coronavirus, the lowest daily uptick since infections began surging Feb 21, & the first time it’s dipped below 50 since.

At the peak, it was 900+ new cases in one day.

Things could still turn on a dime, but feels like a milestone.

Although South Korea never had to close their economy (as officials’ swift response kept things from getting to out of control), analysts at Nomura just helped put SK’s outbreak in perspective.

Meanwhile, another 50+ cases were reported out of Tokyo overnight, as Japanese PM Abe prepared to announce plans to launch a state of emergency set to begin tomorrow. As Nikkei Asian Review reported Monday morning, Abe said Monday the planned state of emergency would be rolled out in seven prefectures, while also announcing a record 108 trillion yen (about $1 trillion) stimulus package.

Tokyo, Kanagawa, Saitama, Chiba, Osaka, Hyogo and Fukuoka prefectures will be covered by the decree. However, because the Japanese Constitution bows to civil liberties and doesn’t give the government the authority to stop people from leaving their homes, cities and governors won’t be able to punish businesses who flout the rules – though they can engage in that famously Japanese cultural practice: shaming.

“Even though we will declare a state of emergency, we will not lock cities down and I do not think it is necessary,” Abe told reporters in Tokyo before a meeting of the government’s coronavirus task force. “We will ramp up our effort to maintain economic activities as possible as well as preventing the further spread of the virus.”

The prime minister said he would declare the state of emergency as soon as Tuesday. His bailout will include cash payments to households and bailouts for small businesses similar to what the US is trying to pull off.

Before we go, here is a snapshot on how the situation in the US has developed over the last 24 hours.

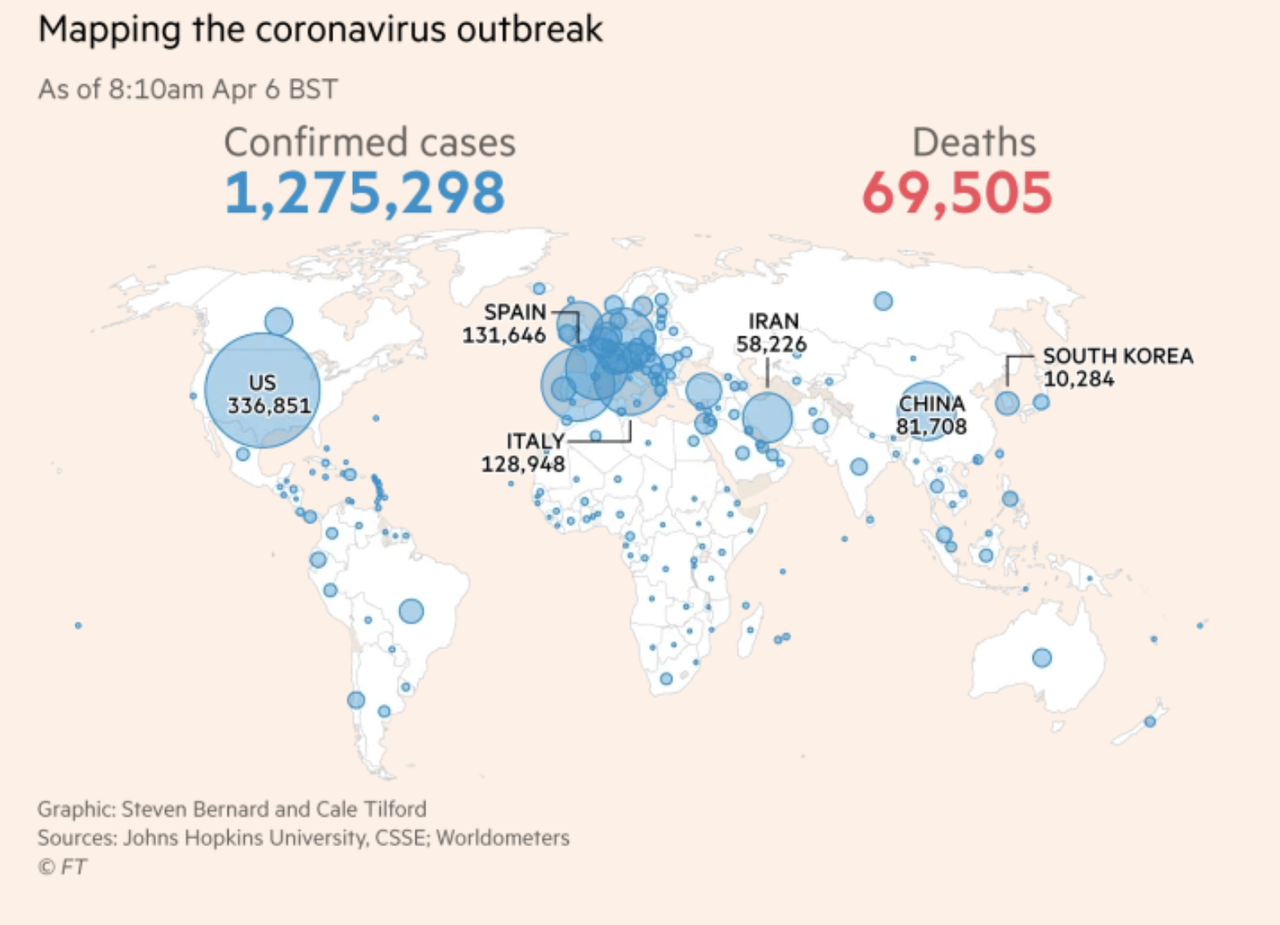

Coronavirus update, U.S.

– 26,076 new cases in last 24 hours

– 337,620 cases in total

– 17,461 recovered

– 9,643 deaths

– 36% of cases in New York

– 1.7 million tests performed

Late last night, Axios reported (and we duly note) whispers that “the first major confrontation” had unfolded during a White House task force meeting between – of all people – Peter Navarro and Dr. Fauci. Navarro slammed Dr. Fauci for allegedly playing down the efficacy of hydroxychloroquine, which was recently determined to be one of the more effective therapies that have been tested in small batches (albeit without control groups, which, as any good scientist will tell you, is vital for producing ‘usable’ data). At the end of the fight, Jared Kushner demanded that Navarro “Take yes as an answer” since the administration is already working to get the drug to ‘hotspots’ around the country.

Cash has been the target of the banking and financial elites for years. Now, the coronavirus pandemic is being used to frighten the masses into accepting a cashless society. That would mean the death of what’s left of our free society.

CBS News, CNN, and other mainstream outlets are fearmongering again. Alarmism is nothing new in the media world, but this time, it’s not about triggering panic buying or even pushing a political agenda.

The war on cash is about imposing a new meta-narrative. As economist Joseph Salerno explains, the cashless society forces all payments to be made through the financial system. It doesn’t end with monopoly control over transactions, though.

Being bound to computers for transactions kicks the door wide open to hardcore surveillance of personal activity and location data. Being eternally on the grid means relentless taxation and negative interest rates, which the Federal Reserve is already gearing up for.

None of this bothers the well-heeled boosters of a cashless society or their lackeys in the media. They want Americans reading about the threat of coronavirus cooties on their cash, which is absurd.

Germs, of course, can loiter all over credit and debit cards, smartphones, ATMs, and every other cash alternative device. Too bad implanted microchip technology isn’t further along, the banksters must be thinking.

Fear of coronavirus-tainted dollars opens a new front in the war on cash https://t.co/0aDsgLyNev

In another CNN article, readers are practically shamed for withdrawing cash to save during a crisis. Every sentence, every word, every letter of the article is nuts.

It begins by reassuring the reader that their bank account is insured by the Federal Deposit Insurance Corporation (FDIC). There’s no mention of moral hazard from CNN. The fact that the federal government guarantees every bank account up to $250,000 encourages reckless financial and banking behavior. Not worth mentioning, CNN?

Prior to the end of World War II, there were $500, $1,000, and $10,000 bills in wide circulation. This cash was dissolved by the Federal Reserve in the name of fighting organized crime. This same argument is now being made against $50 and $100 bills by Harvard economics professor Kenneth Rogoff.

In the Wall Street Journal, Rogoff also wrote that a cashless society would offer such benefits as “greater flexibility for the Federal Reserve to stimulate the economy when necessary.”

“The Federal Reserve should be able to implement negative nominal interest rates vastly more effectively in the absence of large bills, which could prove quite important as a stimulative tool in the next financial crisis.”

Prophetic. And indeed, negative interest rates would require the assistance of outlawing cash, so that banking customers don’t cheat by simply drawing out on their accounts.

Pardon the pun, but it’s absolutely sick how COVID-19 is being used now as a launching pad for this cashless agenda. There’s nothing to fear about using cash during this time of social distancing.

Wash your hands after handling cash, but don’t give up your moolah. Preserve your health, your privacy, and your liberty.

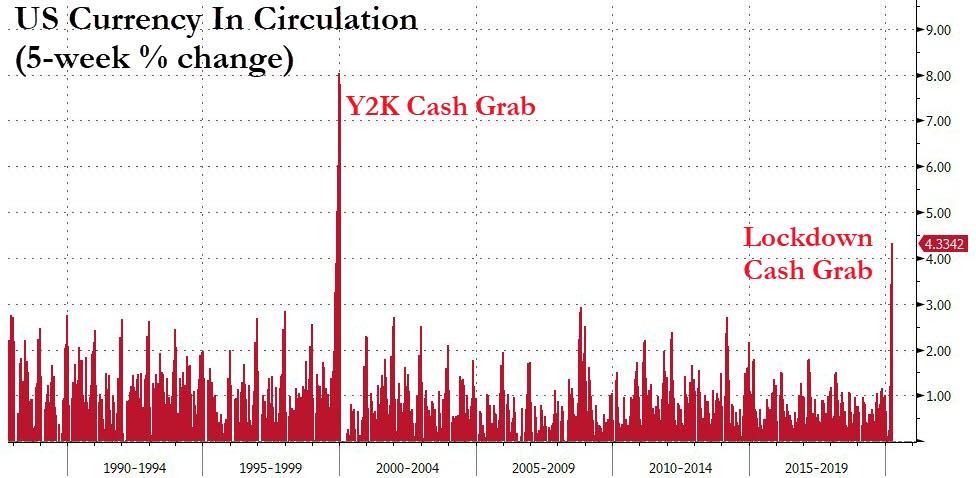

And just in case you wondered what all this fearmongering has done for that dirty cash in circulation – Americans are grabbing it at at the fastest pace since the Y2K liquidity scare…

Another unintended consequence of government intervention.

“Immunity Certificates” Are Coming – COVID-Survivors To Get ‘Special Passports’ Enabling Return To ‘Normalcy’

Update: Even more prophetically, billionaire hedge fund manager Bill Ackman tweeted about his “optimism” and the need for

“…Hydroxychloriquine and antibiotics appear to help. There is increasing evidence that the asymptomatic infection rate could be as much as 50X higher than expected.

If this is true, the severity and death rate could be much lower than anticipated, and we could be closer to herd immunity than projected. Highly accurate antibody tests are scaling production and distribution which will definitively answer this question hopefully soon.

One could imagine a world in the next few months where everyone is tested and all but the immune-compromised go back to a socially distanced but more normal life.

We wear bracelets or carry a phone certificate which indicate our status, and track infections where they emerge…”

Yay, let’s all cheer for antibody-based freedom.

* * *

The rollout of immunity certificates across the world will likely be government-issued to first responders and citizens who have developed resistance to COVID-19.

People who have contracted the virus and have recovered, normally develop antibodies to fight the virus, could be their golden ticket to escape regions that have strict social distancing measures and or lockdowns.

Just imagine, immunity certificates granted by governments to people who have recovered or have developed resistance to the virus could be considered special passports that will allow them to freely travel across states, countries, and or the world — while everyone else remains hunkered down in their homes or doomsday bunkers.

Some of the first talks of this has originated in the UK. The government could roll out immunity passports to Britons who have already contracted and recovered from the virus so they can reenter the economy, reported The New York Times.

“(An immunity certificate) is an important thing that we will be doing and are looking at but it’s too early in the science of the immunity that comes from having had the disease,” health minister Matt Hancock said at a Downing Street press conference.

“It’s too early in that science to be able to put clarity around that. I wish that we could but the reason that we can’t is because the science isn’t yet advanced enough,” Hancock said.

UK Health Secretary: “We are looking at an immunity certificate. How people who have had the disease, have got the antibodies, and therefore have immunity, can show that, and so get back… as much as possible to normal life.” pic.twitter.com/SVLV8U2YwG

Prime Minister Boris Johnson’s spokesman said Britain was completing due diligence in how feasible immunity passports would be.

Hancock said a blood test was in development that could test whether people already had the virus or had the antibodies that would make them resistant to the infection.

In Germany, researchers are preparing a study that would see if people already immune to the virus could reenter the workforce and be granted immunity passports.

In Italy, the conservative president of the northeastern Veneto region has proposed an immunity passport for people who possess antibodies that show they are resistant to the virus.

The former prime minister, Matteo Renzi, has called it a “Covid Pass” for the uninfected who can return to their normal lives.

Immunity passports and “intermittent lockdowns” could become a reality in the months, quarters, or at least in the next several years – as the virus could be sticking around a lot longer than many have anticipated.

Talk of these special passports surfaced in American politics last week when House Democratic Caucus Chairman Mike Stewart called on Tennessee Gov. Bill Lee to implement an “Immunity Certificate” for first responders and healthcare professionals.

Stewart said first-responders who have the antibodies and are immune to the virus should be shifted onto the frontlines.

“We need to get the resources in place to test all of our healthcare workers so we know which ones can work without fear of COVID-19 and which ones need maximum protection against the VIRUS,” Stewart said.

And for more confirmation that immunity passports are going to be the next big thing in the Western world, or maybe across the globe. Here is Bill Gates on March 24, giving a 50-minute interview to Chris Anderson, the Curator of TED, the non-profit that runs the TED Talks.

Right at 34:14, Gates discussed how the future in a post-corona world would be. He said:

Eventually what we’ll have to have is certificates of who’s a recovered person, who’s a vaccinated person…

…Because you don’t want people moving around the world where you’ll have some countries that won’t have it under control, sadly.

You don’t want to completely block off the ability for people to go there and come back and move around.

So eventually there will be this digital immunity proof that will help facilitate the global reopening up.

Investment advisor and former Assistant Secretary of Housing Catherine Austin Fitts says, “We’ve been printing massive amounts of dollars, and if you look at all the things we did to stop high speed debasement and unprecedented inflation, we’ve kind of run out of tricks…”

“…Inflation is really sneaking up…

My question:

Is basically shutting down the small businesses and the small farm economy at high speed the way they have done, is that protecting us from going up a frightening inflation? Are we at Weimar Republic kind of inflation rates?

I have been telling my subscribers to plant, plant and plant because the price of food is going to go through the roof. Another one of my questions: What’s pressing for war? Is the debt spiral up and the inflation spiral up, is that more than they can handle?”

Fitts also says the covert war going on now is about the U.S. dollar and countries who want to stop using it for trade.

If the dollar is used less, it will be worth less and maybe much less. Fitts says,

“We have tried to keep all the oil sales in the world going through the dollar. Of course, that’s put everybody back into our jurisdiction. The world doesn’t want to do that anymore. They want to be free to trade.

You are seeing more and more central banks around the world doing swap lines and direct relationships between central bank to central bank to try to do what is called de-dollarization.

So, you have the world wanting to move outside our channel, and you have the Anglo American alliance trying to protect the dollar syndicate. That is part of the economic war that is going on.”

Fitts says, “Whatever happens on the global stage, it means the days of the subsidy that kept the game inside America is over…”

“…So, how do you radically reduce the size of the financial footprint that stops inflation from going wild?

How do you take the subsidy away from the American middle class without a major civil war?…

What we did was we did the China trade, and now it’s over, and everybody in America said fine, we will go along. Well, this is the price. You have borrowed from the future and now it’s over.”

Why the sudden record gun buying in America? Fitts says,

“They understand that the rule of law is steadily being diminished. They see all sorts of behavior… that is lawless…

They see people in poverty say if anything goes for the big guys, then anything goes for us…

Part of what is happening is we are dealing with a spiritual war, and there are serious demonic and occult forces at work. There is nothing they would love more than to stop the churches and stop people from getting together and praying and inviting in the divine and angelic hope every Sunday. I am with the President. I think stopping the churches from gathering is a very, very terrible idea.”

Fitts also still thinks gold is a good investment that will “outperform most other investments in 2020.”

Join Greg Hunter of USAWatchdog.com as he goes One-on-One with Catherine Austin Fitts, publisher of “The Solari Report.”

Hospital Operator Quorum Health Is Facing Bankruptcy Amidst The COVID-19 Outbreak

Quorum Health, which operates 24 hospitals in 14 states, is preparing for bankruptcy at the worst possible time: the middle of a global pandemic. The “flood” of coronavirus patients that the hospitals have experienced have put pressure on an already precarious set of financials, leaving the the company little choice, according to Bloomberg.

Quorum’s executives are in the midst of negotiations with stakeholders on possible restructuring deals, but at the same time the company is preparing Chapter 11 plans. Earlier this week, the company delayed its annual report filing to focus on negotiations with its creditors. No official decision has been made.

But the worst part is that Quorum’s troubles could foreshadow what’s coming for the American healthcare system. Even prior to the outbreak, hospitals in rural areas were “losing profitable elective procedures to outpatient facilities while still handling patients who lack good insurance.”

And now, hospitals are being forced to cancel optional and elective procedures to make capacity for coronavirus patients. This further squeezes the financials of many of these facilities and federal relief may not be enough to save them. Prior to the virus even becoming a factor, more than 30 facilities went bankrupt last year.

CEO Robert Fish said: “Regardless of the path forward the company chooses, Quorum Health and its hospitals will continue to maintain all operations without any interruption to service.”

Quorum started in 2016 as a spinoff of 38 hospitals from Community Health Systems. It is now down to just 24 facilities and 2,000 beds. The company hasn’t been profitable since the spinoff and its 2023 unsecured bonds are trading for about 70 cents on the dollar.

KKR & Co., York Capital Management Global Advisors LLC and Mudrick Capital Management round out a list of the company’s stakeholders. KKR offered last year to help recapitalize the company, but noted that it would likely wipe out the company’s equity holders.

Over the past week or so, China has eased quarantine measures in Wuhan – the city in which the global coronavirus pandemic began – with the entire lockdown scheduled to end on 8 April. With China’s President Xi Jinpiang having visited the city just a few days ago, the industrial economy across China as a whole is back working and operating at levels even above the pre-coronavirus rates, although the service sector remains more cautious.

For the oil industry, this means that China is back and busy taking up where it left off in terms of exploring and developing new field opportunities.

This is at a time when the U.S. is just beginning to see the full onset of coronavirus mayhem.

There has been no clearer sign of this move by China than last week’s awarding of a US$203.5 million engineering contract for Iraq’s supergiant oil field, Majnoon, to the little known China Petroleum Engineering & Construction Corp (CPECC).

With the U.S.’ focus increasingly on fire-fighting the coronavirus outbreak at home, Beijing has good reason to believe that it has largely a clear run at target country Iraq, provided that it does not stick it too much in the U.S.’ craw. This specifically means continuing to develop oil and gas field opportunities in geopolitically ultra-sensitive areas, such as Iraq, on the basis of rolling contracts for specific work undertaken by companies that are not top of the U.S.’ radar, like CPECC.

This method is also being used by Russia, and the focus of it right now is Iraq and Iran, two countries that are right in the centre of the Middle East and vital to both China’s ‘One Belt, One Road’ multi-generational dominance strategy and to Russia’s ongoing attempt to sequestrate the entire Middle East.

Majnoon is a key focus in Iraq because it has so much oil that its very name in Arabic means ‘insane’, to signify the insane amount of oil that has always been present there. Before the U.S. noticed that China was stealthily acting hand in glove with Russia to provide the money where the muscle had been put in place, the ever-fractious senior Iraqi politicians had offered China a stunningly lucrative deal for the development of the Majnoon field. Specifically, the terms of the deal were that China would obtain a 25-year contract but one that would officially start two years after the signing date. This would allow China to recoup more profits on average per year and less upfront investment.

Also enormously beneficial for Beijing was that the methodology for working out per barrel payments to it would be the higher – the Chinese would choose – of either the mean average of the 18 month spot price for crude oil produced, or the past six months. Additionally, China would receive a discount of at least 10 per cent for at least five years on the value of the oil it recovered.

And oil there is aplenty. Located around 60 kilometres to the north east of the main southern export terminal of Basra, the Majnoon supergiant oil field is one of the largest oil fields in the world, with an estimated 38 billion barrels of oil in place. Due to the legacy of both the Iran-Iraq War and the U.S. incursions, from when the licence on the field was awarded on 11 December 2009 by the Iraq government to Shell Iraq Petroleum Development (SIPD) – in conjunction with its Malaysian partner, Petronas, and Iraq’s Missan Oil Company – it took nearly 18 months simply to clear 28 square kilometres of land of explosives, prior to constructing and opening the first well. Production was then formally restarted on 20 September 2013 and, within a very short timeframe, the consortium had already managed to boost output to the 175,000 barrels per day (bpd) first commercial production target (also the threshold for cost-recovery payments for Shell).

By the end of the first quarter of 2014, the field was churning out an average of 210,000 bpd, according to figures from Shell and Baghdad. Indeed, the first shipment of crude oil to Shell Trading occurred on 8 April that year and, despite the floods that hit the fields in early 2019, the longer-term original production target figures designed for the Shell-led consortium still stand: the first production target of 175,000 bpd (already reached and surpassed), and the plateau production for the site of 1.8 mbpd.

The International Energy Agency projected output of 550,000-950,000 bpd production by 2020, and 700,000-1 million bpd at some point in the 2030s, although due to the flooding and recent political upheavals – plus the effects of the coronavirus – the timing has slipped. Even with these caveats, though, China’s part of the deal – which also remains in place – is to shore up the site from future potential flooding and to increase output to at least 500,000 bpd by the end of May 2021.

The details of the early 2019 flooding damage might make worrying reading for some developers. The rain that caused the initial flooding had only fallen on both sides of the Iraq/Iran border for just 35 minutes in total, which then caused the Hiwiza marshes to overflow into farmland in the nearby Al-Qurna district, cutting through the safety berms and the rising level of water caused the Jahaf dam to collapse. By 15 March, the water level rose sufficiently to force itself through a second safety berm to the edges of the Majnoon oil field.

The details do not worry the Chinese, though, for two key reasons.

One is that China has extensive knowledge of dealing with floods across its own country, both natural and man-created (via the damming that has occurred for decades), so it has the expertise and engineering capabilities to effectively deal with such eventualities.

The other is that, in line with its aforementioned encroachment into Iran, China can work on both sides of the border, as the Majnoon reservoir in the Iraqi side extends across the Iran border into the massive field known as Azadegan. This, in turn, is split into the North Azadegan and South Azadegan oil field developments.

For years, structural damage has been done to the area by the erosion of subsoil across over one million hectares of forest and brush land by the Islamic Revolutionary Guard Corps (IRGC) as a result of building programmes. This has been worsened by the redirection of many of the natural water flows through the building of dams and again by Iran’s irrigation systems that have been sending clean and waste water into Iraq for decades.

A 2011 study by the University of Basra warned that the infrastructure was not able to handle Iranian inflows, with the danger zone concentrated in an area where the Majnoon oil pipelines feed the gas-oil separation station. However, as a senior source who works closely with Iran’s Petroleum Ministry told OilPrice.com last week: “The IRGC invited China into Iran and Iraq and the IRGC is entirely at China’s service.”

This strategy of gradual encroachment is a Chinese classic, of course, currently being employed very notably where possible across the Asia-Pacific region as well as the Middle East. The modus operandi is:

offer lots of money to cash-strapped countries (which most emerging economies are) that are tied in to future project developments, then leverage this into the building out of on-the-ground infrastructural projects (that have employment and revenue benefits for the host countries as well), and then turn the screw by inveigling the host countries to give China extremely preferential terms on something it wants (in the Middle East it is oil and gas and land transit routes, and in Asia Pacific it is other natural resources and international port usage).

Although in the Middle East, China is still partly trying to cover its intentions by using non-headline companies on ‘contractor-only’ specific work projects – just like CPECC – it does not take much digging to find the real interest.

Not only is CPECC a subsidiary of Chinese oil behemoth, China National Petroleum Corporation (CNPC), but also it was the very same company that was recently awarded exactly the same type of contract (US$121 million for ‘engineering work’ that time) for Iraq’s supergiant West Qurna-1 oilfield, also located very close to Iraq’s principal oil hub of Basra.

“At some point the U.S. is going to wake up and find out that it has lost the entire Middle East, including Iraq and Saudi,” concluded the Iran source.