In last week’s discussion, we stated the “bear market” was not yet complete. This was despite the “market rally,” which convinced the media the “bull market was back.”

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. Most importantly, as we discussed in our employment report on Thursday, “bear markets” do not end with “consumer confidence” still very elevated.

“Notice that during each of the previous two bear market cycles, confidence dropped by an average of 58 points.”

This past week, we saw early indications of the unemployment that is coming to America as jobless claims surged to 10 million, and unemployment in April will surge to 15-20%.

Confidence, and ultimately consumption, Which comprises 70% of GDP, will plummet as job losses mount. It is incredibly difficult to remain optimistic when you are unemployed.

No Light At The End Of The Tunnel – Yet.

The markets have been clinging on to “hope” that as soon as the virus passes, there will be a sharp “V”-shaped recovery in the economy and markets. While we strongly believe this will not be the case, we do acknowledge there will likely be a short-term market surge as the economy does initially come back “online.” (That surge could be very strong and will once again have the media crowing the “bear market” is over.)

However, for now, we are not there yet. As we noted last week’s Macroview there are two issues currently weighing on the economy and markets, short-term.

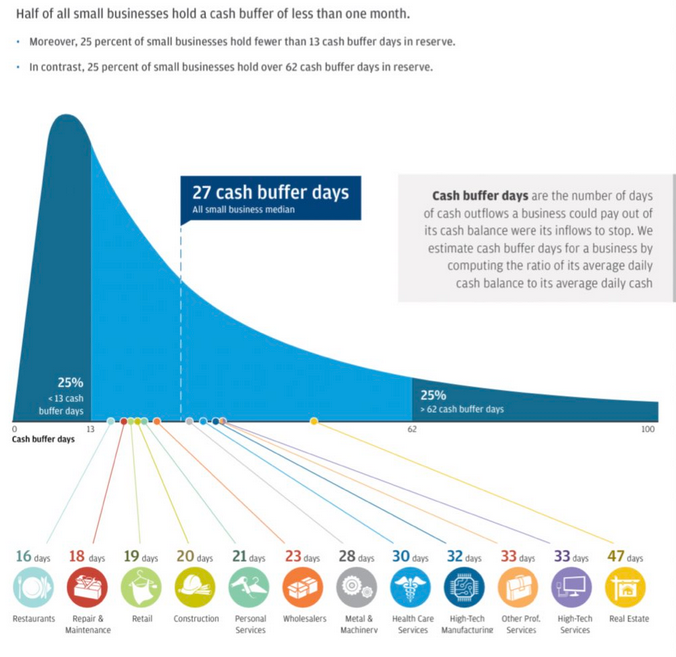

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance can be provided. This will lead to higher, and a longer-duration of unemployment.”

Furthermore, the bill only provides for two and a half times a company’s average monthly payroll expense over the past 12 months. However, the bill fails to take into consideration that not all small businesses are labor and payroll intensive. Those businesses will fail to receive enough support to stay in business for very long. Furthermore, the bill doesn’t provide for inventory, other operating costs, and spoilage.

Small businesses, up to 500-employees, make up 70% of employment in the U.S. While the government is busy bailing out self-dealing publicly traded corporations, there will be a massive wave of defaults in the small- to mid-size business sector.

Secondly, we are not near the end of the virus as of yet. As noted last week:

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

“Five ways we know that the American response to the coronavirus isn’t yet working.

There is still no sign of the curve flattening.

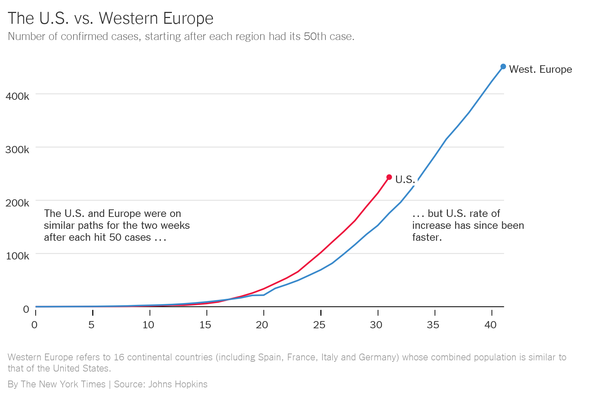

The caseload is growing more rapidly here than in Europe.

The shortage of medical supplies continues.

There is still a testing shortage.

Nationwide, the policy response remains inconsistent.

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

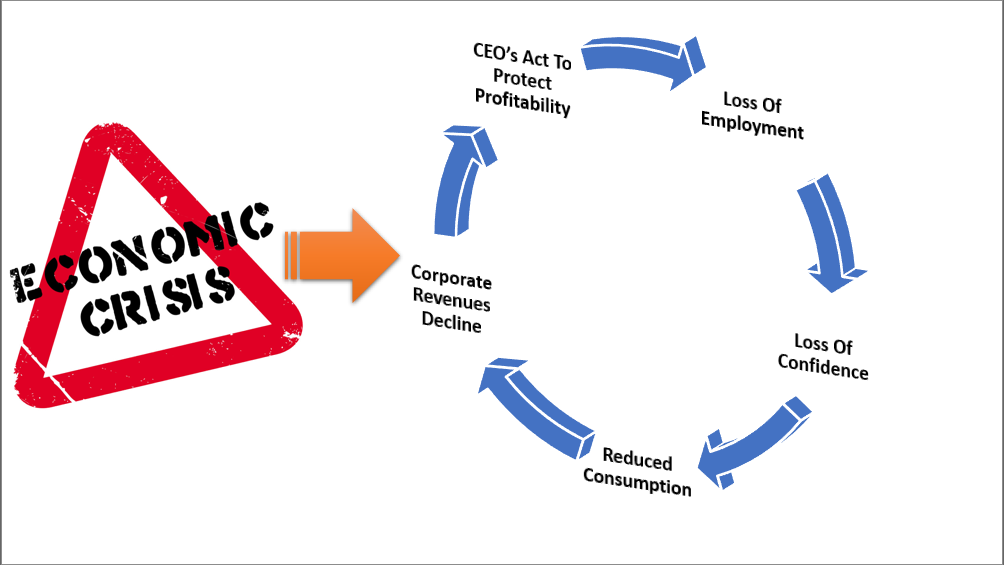

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any disruption to their income going into recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits lead to higher unemployment and lower asset prices until the cycle is complete.

Two important points:

The economy will eventually recover, and life will return to normal.

The damage will take longer to heal, and future growth will run at a lower long-term rate due to the escalation of debts and deficits.

For investors, this means a greater range of stock market volatility and near-zero rates of return over the next decade.

Meanwhile, the charts below of the S&P500 benchmark tell TPA the following:

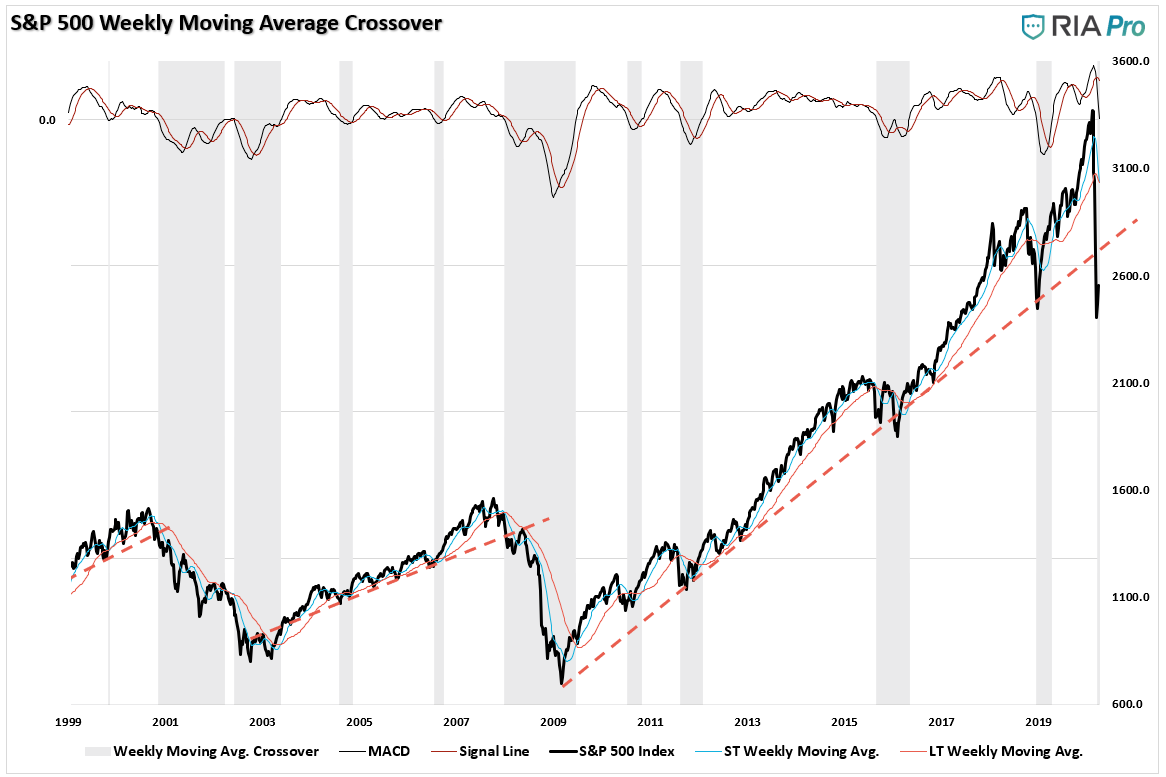

When the 11-year bull market trend ended, other shorter trends were also violated. In late February, the S&P 500 fell below its 14-month uptrend line, and in early March the 13-month uptrend line was violated. Those breaks set in place the steep declines seen in the 2nd and 3rd weeks of March.

While it may seem like an epic battle is going on around S&P 500 2500, the real problem is the downtrend forming from the 2/19 high.

TPA still continues to see real long term support in the 3% range between 2110 and 2180. A less likely move below that support, would leave long term support levels of the lows of 2014 and 2015.

“While the technical picture of the market also suggests the recent “bear market” rally will likely fade sooner than later. As we stated last week:

‘Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.’

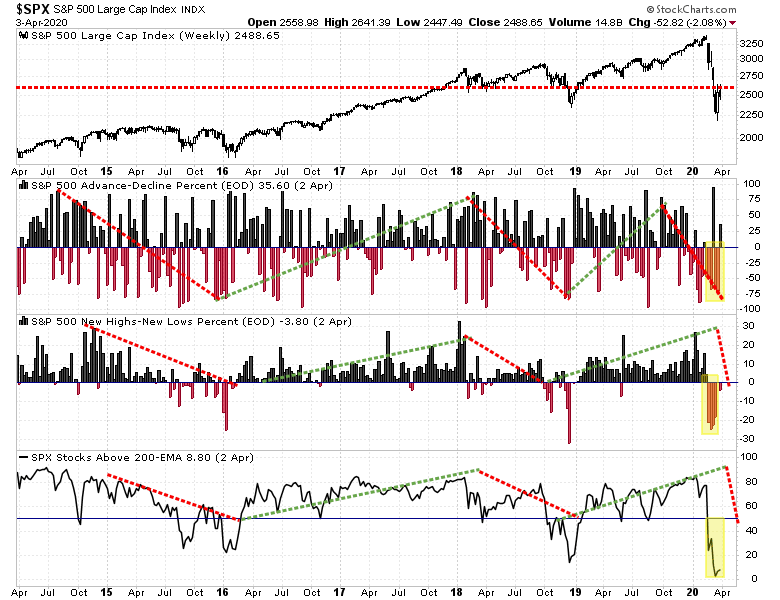

Importantly, despite the sizable rally, participation has remained extraordinarily weak. If the market was seeing strong buying, as suggested by the media, then we should see sizable upticks in the percent measures of advancing issues, issues at new highs, and a rising number of stocks above their 200-dma.”

Chart updated through Friday.

On a daily basis, these measures all have room to improve in the short-term. However, the market has now confirmed longer-term technical signals suggesting the “bear market” has only just started.

Major Technical Failures

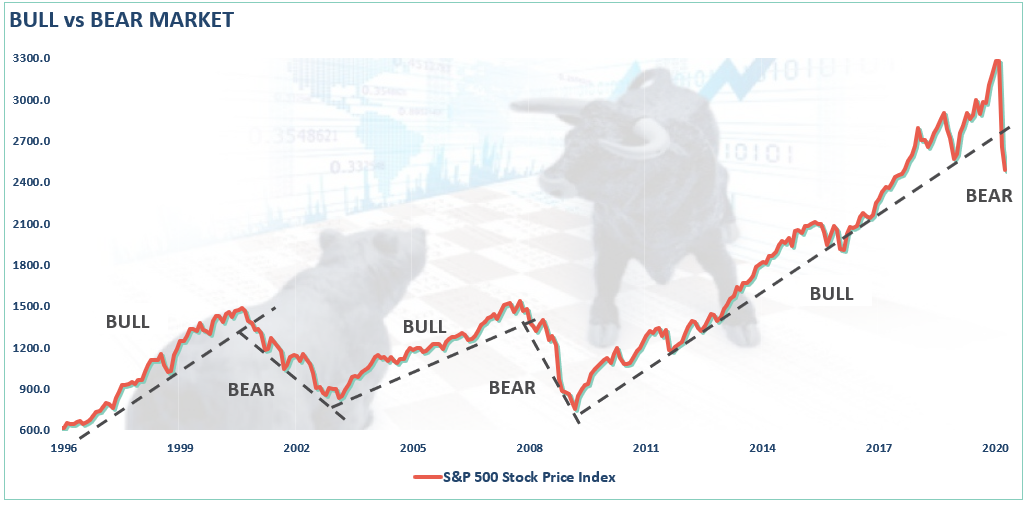

Price is nothing more than a reflection of the “psychology” of market participants. The mistake the media made by calling an “end” to the “bear market” is they were using an outdated proxy of a “20% advance or decline” to distinguish between the two.

However, due to a decade-long bull market, which had stretched prices to historical extremes above long-term trends, that 20% measure is no longer valid.

Let’s clarify.

A bull market is when the price of the market is trending higher over a long-term period.

A bear market is when the long-term upward trending advance is broken and prices begin to trend lower.

The chart below provides a visual of the distinction. When you look at price “trends,” the difference becomes both apparent and more useful.

This distinction is important. With the month, and quarter-end, behind us, we can now analyze our longer-term weekly and monthly price trends to make determinations about the market.

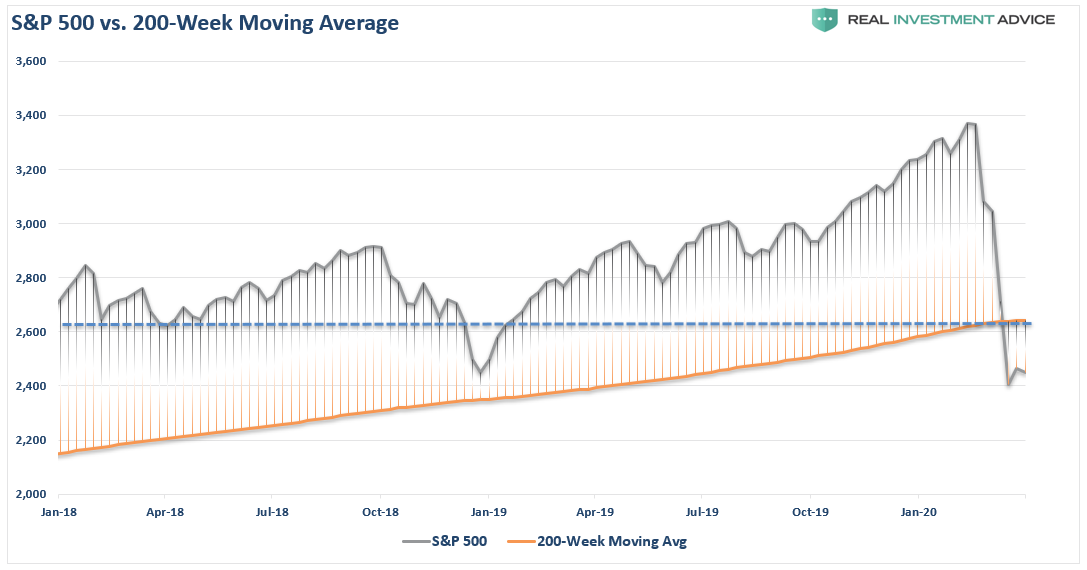

The market has now violated the 200-week (4-year) moving average. Given this is such a long-term trend line, such a violation should be taken seriously. Also, that violation will be very difficult to reverse in the short-term, and suggests lower prices to come for the market.

Using the definition of “bull and bear” markets above, the market has also violated the long-term “bull trend” on a “confirmed” basis.

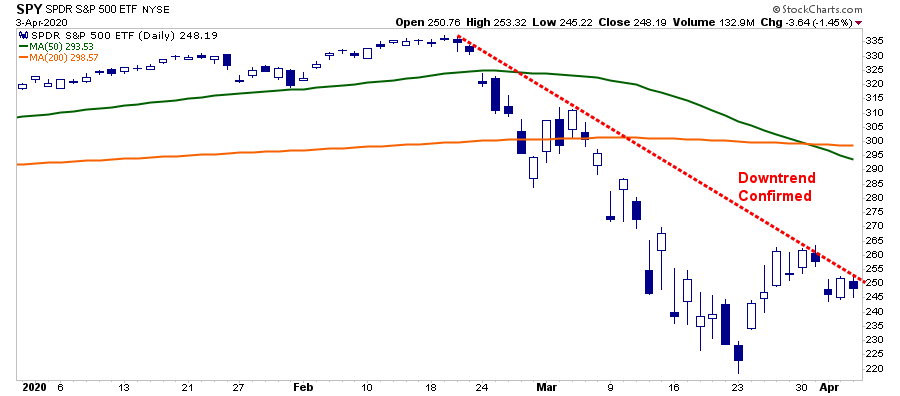

A confirmed basis is when the market violates a long-term trend, rallies, and then fails. As Jeffery Marcus, noted above, that market is now establishing a confirmed downtrend with the recent rally failing at downtrend resistance. (Also, the 50-200 dma negative cross will apply more downward pressure on any forthcoming rally.)

Most importantly, for the first time since the “Great Financial Crisis” lows, the market now has a confirmed close below the bull-trend line. If the market is able to rally in April, and close above the long-term trend line, then the “bull market” will technically still be intact. However, if the month of April closes below that trend, a confirmed “bear market” will be underway and suggests markets will see lower levels before it is over.

There are reasons to be optimistic about the markets in the very short-term. We will get through this crisis. People will return to work. The economy will start moving forward again.

However, it won’t immediately go right back to where we were previously. We are continuing to extend the amount of time the economy will be “shut down,” which exacerbates the decline in the employment, and personal consumption data. The feedback loop from that data into corporate profits, and earnings, is going to make valuations more problematic even with low interest rates currently.

This is NOT the time to try and “speculate” on a bottom of the market. You might get lucky, but there is very high risk you could wind up losing even more capital.

For long-term investors, remain patient and let the market dictate when the bottom has been formed.

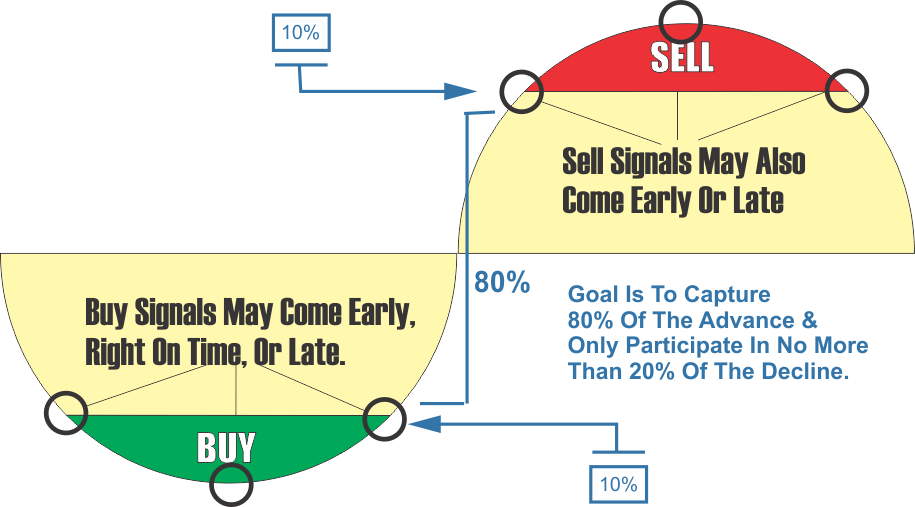

You can have the top 20% and the bottom 20%, I will take the 80% in the middle.” – Rothschild

This is the basis of the 80/20 investment philosophy, and the driver behind our risk management process at RIA.

Yes, you may sell to early and miss the 10% before the peak, or you sell a little late and lose the 10% from the peak. Likewise, you may start buying into the market 10% before, or after, it bottoms. The goal is to capture the bulk of the advance, and miss the majority of the decline.

Investing isn’t a competition of who gets to say “I bought the bottom.” Investing is about putting capital to work when reward outweighs the risk.

That is not today.

Bear markets have a way of “suckering” investors back into the market to inflict the most pain possible.

This is why “bear markets” never end with optimism, but in despair.

Sudanese Migrant Kills 2 During Knife Attack In Southeastern France

As if a national lockdown to prevent a deadly pandemic from killing hundreds of thousands of people wasn’t terrifying enough, there are now armed asylum seekers marauding around southeastern France, murdering shoppers as they venture out to buy groceries.

To wit, a man killed two people and wounded several others, one critically, during a knife attack in the town of Romans-sur-Isère in the Drôme, about 20 kilometers north of Valence.

According to Haaretz, witnesses said the man first attacked the owner of a tobacco shop in the town center, then attacked two customers inside the shop. After that, he twalked out and began stabbing people in the street. One of the dead was inside the tobacconist. A second man, a butcher from a nearby shop, was killed outside.

Local police told French media that the suspect was a 33-year-old asylum seeker from Sudan. Anti-terrorism investigators are reportedly investigating the incident to try and determine if it was an act of terrorism.

As COVID-19 has spread across Europe, the issue of how to handle the asylum-seekers and migrants who continue to spill over the continents’ borders, even as the Syrian Civil War appears to finally be winding down, has become increasingly fraught as Turkey has reportedly tried to send migrants infected with the virus to Greece.

Macron tweeted his condolences, and promised to investigate to incident and determine whether it was an act of terrorism.

The suspect was living in the center of town where he carried out the attack. A statement from the local municipal government read: “This Saturday 4 April morning an individual carried out a knife attack at several places in the centre of Romans-sur-Isère. The individual in question was arrested around 11am. According to initial information, two people have died, five others are injured and in a critical condition. At this moment, we do not know the motive for this act.”

Just over two months after dying along with his 13-year-old daughter Gianna in a tragic helicopter crash, Lakers legend Kobe Bryant has been inducted into the Basketball Hall of Fame in Springfield, Mass.

Bryant has been inducted alongside Tim Duncan and Kevin Garnett in what the Washington Post described as a long-anticipated move.

In a long-anticipated move, the Naismith Memorial Basketball Hall of Fame announced Saturday that the NBA legends, who combined for 11 championships and four MVP awards, will be inducted together as the 2020 class. That Hall of Fame class also includes women’s star Tamika Catchings and coaches Kim Mulkey, Barbara Stevens, Eddie Sutton and Rudy Tomjanovich. Executive Patrick Baumann was also inducted.

The Hall of Fame’s annual announcement of inductees was scheduled to be made at the NCAA’s Final Four weekend in Atlanta, but the novel coronavirus pandemic prompted the tournament’s cancellation. Despite uncertainty about the public health crisis, tickets to the Aug. 29 enshrinement ceremony remain on sale at the Hall of Fame’s website. The televised festivities, typically held in a large symphony hall in front of a crowd filled with basketball greats, have not yet been postponed or canceled.

Bryant’s selection comes less than three months after his death in a helicopter crash at 41. A five-time NBA champion during a 20-year career with the Los Angeles Lakers, Bryant earned 18 all-star selections, was named 2007-08 MVP and twice led the league in scoring. He entered the NBA straight out of high school as a 1996 lottery pick and retired in 2016, closing his career with a memorable 60-point game against the Utah Jazz. A 6-foot-6 shooting guard who modeled his game after Michael Jordan’s, Bryant ultimately surpassed his hero on the NBA’s all-time scoring list. Jordan paid tribute to Bryant during a public memorial in February, referring to him as a “dear friend” and a “little brother.”

The news was officially leaked last night, but the official announcement from the hall of fame came Saturday morning.

Kobe Bryant, Tim Duncan and Kevin Garnett will be inducted into the Naismith Basketball @Hoophall Class of 2020, sources tell @TheAthleticNBA@Stadium. Formal announcements will be made on Saturday.

Grieving Chinese Families Can’t Bury Dead, Perform 2,000 Year-Old Tradition

While the Chinese Communist Party claims they’ve suffered just 3,300 coronavirus deaths out of more than 60,000 who have died around the world as of this writing, evidence exists that the actual death toll across China is far higher – and could be more than 40,000.

And as long lines form at Wuhan funeral homes over the last two weeks, family members – some waiting up to six hours, have been collecting their loved ones in the hopes of giving them a proper funeral. In particular, mourning families want to be able to perform a ‘grave sweeping’ ritual that has been around for over two millennia – where families gather on the 15th day after the spring equinox to remove weeds and dirt from their ancestors’ graves.

Long lines have formed at Wuhan’s eight main funeral parlors, including here at the Hankou Funeral Home, as relatives come to collect ashes before Tomb-Sweeping Day. (Weibo)

Unfortunately, due to the backlog in urns, lost bodies, and Chinese authorities banning, or severely limiting tomb-sweeping rituals due to the large crowds which gather at cemetaries, mourners in Wuhan won’t be able to pay their respects until at least May, according to the Washington Post – which suggests that beyond health safety reasons, Beijing wants to limit the number of people standing around, criticizing the government response to the pandemic.

“No one in the family got to say goodbye to Grandpa or see his face one last time,” said Gao Yingwei, an IT worker in Wuhan whose grandfather, Gao Shixu, apparently succumbed to the novel coronavirus on Feb. 7. The 76-year-old died at home; funeral workers in hazmat suits came to collect his body, telling the family it would be cremated immediately.

“To this day, we have no idea how his body was handled, where his ashes are or when we will be able to pick them up,” Gao said. “I don’t even know which funeral parlor those guys were from.” –Washington Post

Cover up

As we’ve noted over the last several weeks, the numbers in China aren’t adding up – as crematoriums have been processing thousands of bodies per day, according to several reports.

The Hankou Funeral Home, for example, told Caixin that it has been operating 19-hour days; enlisting male staff to carry bodies while reporting they’ve received 5,000 urns in two days.

Using photos posted online, social media sleuths have estimated that Wuhan funeral homes have returned 3,500 urns a day since March 23. That would imply a death toll in Wuhan of about 42,000 — or 16 times the official number. Another widely shared calculation from Radio Free Asia, based on Wuhan’s 84 furnaces running nonstop and each cremation taking an hour, put the death toll at 46,800. –Washington Post

“It can’t be right . . . because the incinerators have been working round the clock, so how can so few people have died?” said one Wuhan resident identified only as Zhang, in a statement to RFA.

Also notable are the uncounted deaths – those who likely died of coronavirus but weren’t tested for the disease, such as 49-year-old Liu Cheng, who died February 12 of a “severe infection in both lungs.” He was not counted in the official coronavirus statistics, and was immediately cremated before his family could see him, according to the report.

Wuhan cemeteries have reported that they will sweep tombs during the memorial period, while some private funeral companies have offered to tend to graves for a fee while the families watch on live stream. And they have nobody to blame but the CCP for their early inaction and destruction of samples in what may have been able to be contained if they had acted sooner.

The Fed came out with a series of unprecedented measures on March 22, 2020. They announced the Fed will buy an unlimited amount of Treasurys and mortgage-backed securities (MBS), or as Peter Schiff refers to it, “QE infinity.” This has been very positively welcomed by many in the mainstream media and by businesses. Yet, what many are ignoring is that the Fed has to do this to keep the bubbles that it has created going.

Recently, I wrote that the Fed has created many structural problems in the mortgage market, corporate bond market, and the car loan market. These issues have only been “waiting” for such a situation to come to the surface and severely hurt the economy.

Reinflating the Mortgage Bubble

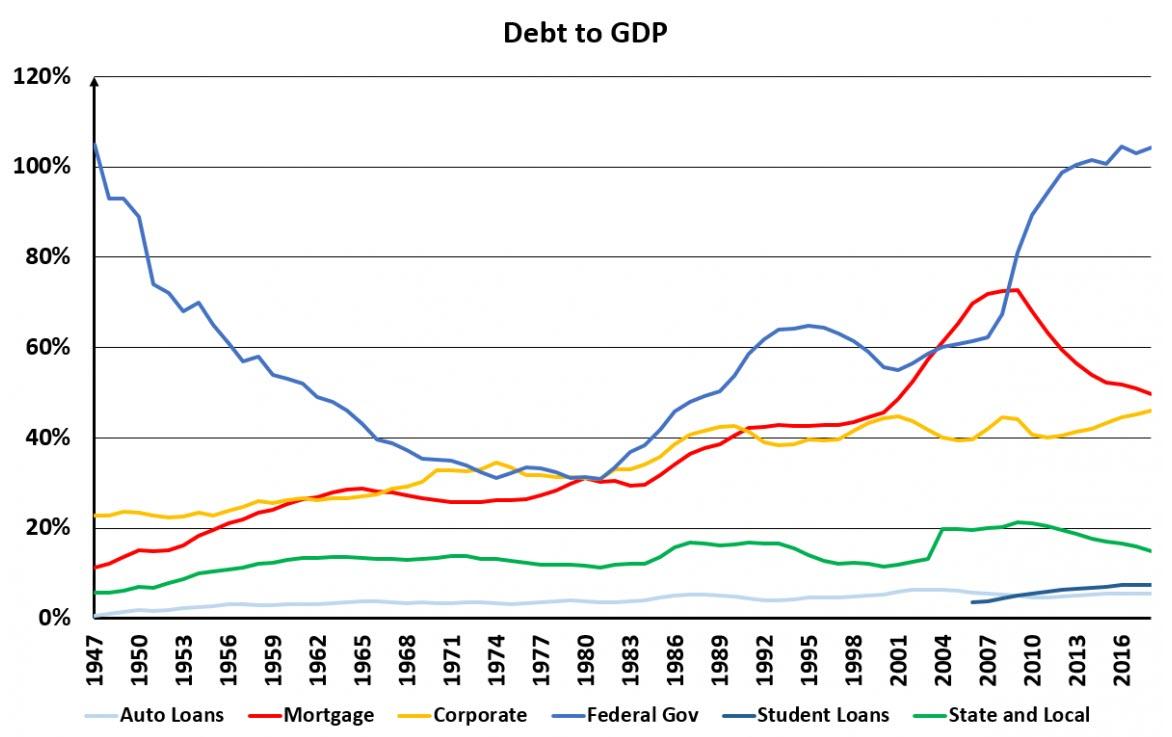

After the recession of 2001 the Fed decreased interest rates substantially, and this along with other government policy led to the housing bubble that burst in 2007. Instead of allowing the market to adjust and get rid of the structural problems created by artificially low interest rates, the Fed decided that what they had to do was to reinflate the housing bubble. The Fed bought massive amounts of MBS to lower mortgage rates and reinflate the mortgage market. This was largely unsuccessful until mid-2012, but then house prices began to rise faster as the economy became more stable. As can be seen from the graph below, house prices have increased by about 50 percent since then and are now at an all-time high.

The graph above may show that the Fed was successful in inflating another housing bubble, yet prices alone do not reveal the whole picture. In the graph below, I show debt-to-GDP ratios for a variety of debts. The red line represents mortgage debt as a percent of GDP, and as it is clear from the graph as a percent of GDP, mortgage debt is decreasing. In fact, it has already decreased by about 20 percent since its all-time high. This shows the Fed was less successful in recreating the housing bubble of the early 2000s.

This is not to say that the housing market is not in a bubble, but the bubble is not in the levels it was last time. Hence, the Fed was less successful in using the housing market to create artificial economic growth. Yet, the Fed’s actions have led to many issues in the mortgage markets. These issues had the president of Ginnie Mae very worried as early as 2015. Here is what he said in his remarks at the Ginnie Mae Summit at the time:

Also, we havedepended on sheer luck. Luck that the economy does not fall into recession and increase mortgage delinquencies. Luck that our independent mortgage bankers remain able to access their lines of credit. And luck that nothing critical falls through the cracks.

A New Bubble Post–Great Recession

As the graph above shows the only private sector debt that the Fed was able to substantially increase, as a percentage of GDP, was the corporate debt. Corporate debt has increased by about 67 percent since the end of the Great Recession, from about $6 trillion to $10 trillion in just ten years. This has led to an increase of the corporate debt-to-GDP ratio by about 6 percent, to an all-time high of 46 percent. What is more, the quality of this debt has been deteriorating. Nearly half of the $4 trillion that was added postrecession are BBB rate bonds, or the lowest ratings of investment-grade bonds trench.

Corporations are not alone in this.All other businesses have now accumulated about $5.5 trillion in debt too, bringing the total debt of all businesses (nonfinancial debt only) to about $15.5 trillion. This makes percentage of total debt to GDP about 74 percent, which is higher than the mortgage debt-to-GDP ratio at its highest point in 2009, when it was about 73 percent.

Hence, this time around the Fed has been more successful in fueling a business debt bubble.

Will the Fed Be Able to Fuel Another Bubble?

As discussed above, the Fed replaced to a large degree the mortgage bubble with the corporate bubble. But this happened because corporate debt and collateralized debt obligations (CDOs) did relatively well during the last recession. This may not be the case in the recession that many say has already started. In fact, this is very clear when one considers how the Fed has responded to the current economic situation brought about by the COVID-19 epidemic. The Fed now will be lending directly to corporations by using the Treasury to secure these loans. They argue that this is due to the shock the economy is in because of COVID-19, but what they are worried about is that the bubble they created is about to burst given the weakness in the corporate debt markets. The Fed knows that the corporate debt market is not in a good shape, since this has now become clear to many (see here, here, and here for a few examples). It remains to be seen whether they can stop this bubble from bursting or not, but if it does, and if what happened in the mortgage market after the last recessions can teach us anything, the business debt-to-GDP ratio will most likely decrease after the recession that we may be in already.

Before the Great Recession, we had the housing bubble fueled by the Fed. Then, the Fed replaced the housing bubble with the business debt bubble. The question that arises is: what will be the next bubble if the business debt bubble bursts?

Looking at the graph above, the only other major debt category left that is big enough to play a role in the economy is government debt. The national debt-to-GDP ratio increased by about 40 percent during the last recession. However, since about 2013 the government debt-to-GDP ratio has stabilized somewhat, but now with the CARES Act (Coronavirus Aid, Relief, and Economic Security Act), some estimates place the deficit for 2020 alone will be $4 trillion. This will lead to at least an 18 percent increase in the government debt-to-GDP ratio in one year alone.

It seems the Fed’s last hope in fueling the next recovery will be government debt. In fact, the Fed has played a major role in the government debt increase, but now they are doing this at another level. Jim Bianco in an article at Bloomberg recently wrote that the Fed’s plan “includes a hard-to-understand $625 billion of bond-buying a week going forward. At this rate, the Fed will own two-thirds of the Treasury market in a year.” Hence, it is clear the Fed, intentionally or not, is going to make the government debt bubble worse than it is.

Conclusion

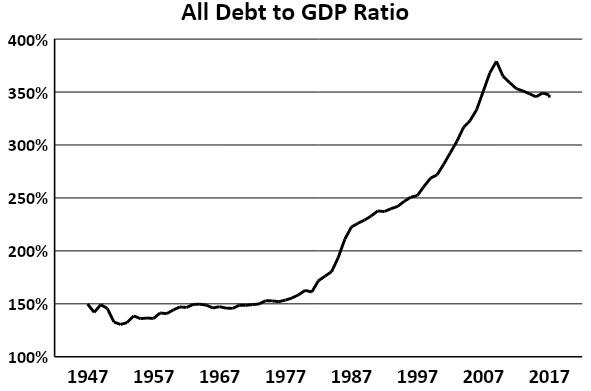

The Fed-fueled economy is unstable, and as the Austrian theory of the business cycle teaches us, sooner or later is bound to suffer from recessions. With each passing recession, the Fed finds it harder to refuel the last bubble, but the market moves on to the new bubble, as the Fed keeps interest rates artificially low. The problem the Fed is facing now is that since the last recession they have been unable to fuel good economic growth with artificially low interest rates, since GDP increased at about 1 percent below the post-World War II average of 3.2 percent. This may be because even with artificially low interest rates total debt has decreased as a percentage of GDP, as the graph below shows.

If this trend continues, the Fed will find it even harder to fuel economic growth by lowering interest rates. The problem here is: how far are they willing to go to keep the bubble economy going?

Jim Bianco seems to be worried about what they are doing. He closed the article mentioned above by saying: “Fed Chair Jerome Powell needs to tread carefully indeed to ensure his cure isn’t worse than the disease.” Only time will tell what the results of the Fed’s actions will be, but it sure seems like they will not find it easy to fuel another private debt bubble.

With only government debt left to increase, the Fed may have reached its limits in affecting the economy via interest rate manipulation.

After Record Rally, Oil Faces Collapse As New Feud Erupts Between Saudis And Russia; Monday OPEC+ Meeting Cancelled

In retrospect, trading on a Trump tweet may not have been the best idea.

On April 2, in what initially appeared to be a belated April fool’s joke, the US president tweeted “Just spoke to my friend MBS (Crown Prince) of Saudi Arabia, who spoke with President Putin of Russia, & I expect & hope that they will be cutting back approximately 10 Million Barrels, and maybe substantially more which, if it happens, will be GREAT for the oil & gas industry!”

What followed was the biggest rally in the price of oil ever, as countless oil shorts scrambled to cover their positions amid concerns there could be even a shred of truth to Trump’s boast that the oil price war between Saudi Arabia and Russia could be coming to an end, especially since global oil demand had cratered by over 20% just as Saudi Arabia boosted its own output to a record 12mmb/d

One day later, on Friday, the surge continued after R-OPEC members saying they may indeed consider a 10mmb/d cut (which, as we also explained would not be nearly enough to balance the oil market but at least it was a start), with Putin admitting he had spoken with US President Trump saying “we are all worried about the situation” and that he is “ready to act with the US on oil markets” with 10mmb/d in oil production needed to be cut.

However, as his Russian energy minister, Alexander Novak, explained at the same time, any production cut would need to also include US shale producers , something that Trump was certainly not too keen on. As the WSJ reported, “Saudi Arabia and Russia won’t cut unless they get signals from U.S. producers they will reduce output, the officials said. But they added that official joint curbs would be more difficult to enact in the U.S. because of antitrust laws.”

And so, the world was excitedly looking forward to the Monday’s virtual R-OPEC conference where the question was whether Trump would agree to cut US production (and whether he even had the authority to enforce such a cut)

But before that, something happened that few noticed yet ended up being a gamechanger: among the other things Putin said on Friday, we reported that the Russian president was also kind enough to summarize the reasons for the oil price collapse which he blamed on the coronavirus, the lack of oil demand and, drumroll, the Saudi withdrawal from the OPEC+ deal.

“It was the pullout by our partners from Saudi Arabia from the OPEC+ deal, their increase in production and their announcement that they were even ready to give discounts on oil” that contributed to the crash, along with the coronavirus-driven drop in demand, he said.

“This was apparently linked to efforts by our partners from Saudi Arabia to eliminate competitors who produce so-called shale oil,” Putin continued. “To do that, the price needs to be below $40 a barrel. And they succeeded in that. But we don’t need that, we never set such a goal.”

As it turns out, Saudi Arabia was – and remains – quite sensitive to accusations over who was responsible for the failure of the March 5 Vienna summit which ended up in Russia refusing to be forced into even bigger production to appease Saudi Arabia, and prompted Saudi Arabia to unleash a historic oil glut.

In a statement early on Saturday, the Saudi Foreign Minister Prince Faisal bin Farhan said the comments noted above by Putin laying blame on Riyadh for the end of the OPEC+ pact between the two countries in March were “fully devoid of truth.”

“Russia was the one that refused the agreement” in early March, the Saudi foreign ministry said. “The kingdom and 22 other countries were trying to to persuade Russia to make further cuts and extend the agreement.”

Which just happens to be more fake news, and the reason why Russia balked is because it was faced with what it – correctly – viewed was a hostile ultimatum by OPEC. As the NYT reported:

After talks with OPEC members in Vienna, Russia’s energy minister, Alexander Novak, returned to Moscow for consultations on Thursday. In his absence, OPEC officials met and came up with what amounted to an ultimatum. The group as a whole would trim production by 1.5 million barrels a day, or about 1.5 percent of world supply. OPEC, meaning largely the Saudis, would make the bulk of the cutbacks, one million barrels, as long as Russia and other producers trimmed the rest.

The gambit was “something of a boss move,” said Helima Croft, an analyst at RBC Capital Markets, but it backfired badly. Russia had played hard to get before, but this time Mr. Novak was not playing. The answer was “no” again, and the Saudi oil minister, Prince Abdulaziz bin Salman, and other officials headed back to their hotels with no results and no communiqué.

Needless to say, Saudi Arabia was not used to getting no for an answer, and so it responded by effectively disbanding OPEC, even as it continued to blame Russia for doing so: as Bloomberg reports, “since the original OPEC+ deal fell apart at a March 5 meeting in Vienna, the Saudis have argued Russia decided to walk away and was first to say countries were free to pump as much as possible.”

“The Russian Minister of Energy was first to declare to the media that all the participating countries are absolved of their commitments,” said Prince Abdulaziz, the energy minister and half-brother of Crown Prince Mohamed bin Salman. “This led to the decision by countries to raise their production in order to offset lower prices and compensate for their loss of returns.”

In any case, Saturday’s direct criticism of Putin was echoed in a statement by Energy Minister Prince Abdulaziz bin Salman, and threatened any fleeting hope of an agreement to stabilize the collapsing oil market after President Trump devoted hours of telephone diplomacy last week to brokering a truce in the month-long price war between Moscow and Riyadh.

As an immediate result, the OPEC+ (or R-OPEC) meeting scheduled for Monday has been delayed as Riyadh and Moscow have discovered a new reason to feud: arguing over who’s to blame for the collapse in oil prices.

And while the alliance is tentatively aiming to hold the virtual gathering on April 9 instead of Monday as it previously intended, a Bloomberg source said with another noting that “producers need more time for negotiations”; in other words, it is unclear if the meeting will take place at all now that the diplomatic spat has reached the highest levels of the world’s top oil producers.

And, as we discussed on Friday, beyond this latest diplomatic spat, Saudi Arabia and Russia have indicated they want other oil countries to join in any output cuts, complicating efforts to call a meeting, the delegate said, asking not to be named discussing diplomatic matters.

“We always remained skeptical about this wider deal as U.S. producers cannot be mandated to cut,” said Amrita Sen, chief oil analyst at consultant Energy Aspects Ltd. “If so, Russia doesn’t come to the table. And if everyone doesn’t cut, Saudi Arabia’s long held stance is that they will not cut either.”

A delay is “not a good sign,” said Ayham Kamel, head of Middle East and North Africa at the Eurasia Group consultancy. “This entirely plays negatively for the discussions.”

“Part of Putin’s comments are about saving face and also justifying why the oil price crashed and partly to deter criticism from the U.S. Putin doesn’t want to be blamed for any losses in the U.S. energy industry. It seems to me that there’s both a defensive effort to shield from criticism abroad for both the Saudis and the Russians,” Kamel said.

The prospect of a new deal spurred a 50% recovery in benchmark oil prices last week as traders saw some relief from the catastrophic oversupply caused by a lockdown of the world’s largest economies, in a bit to halt the coronavirus pandemic. With billions of people forced to stay at home, demand for gasoline, diesel and jet has collapsed by about as much 35 million barrels a day.

Which means that absent either Putin or MBS making some major concessions in what would be seen as a glaring sign of weakness, the record oil rally is about to go in reverse because the primary reason behind the oil price crash still looms: the world running out of oil storage in months if not weeks, and is why the Saudis, who have ramped up production to a record 12 million barrels a day in the past month and massively discounted the price of their oil, have insisted a new agreement must involve significant contributions from all OPEC+ nations and major producers outside the coalition, including the U.S. and Canada.

“No one had expected such a total collapse in the oil market,” said Fyodor Lukyanov, head of the Council on Foreign and Defense Policy, a research group which advises the Kremlin. “Saudi Arabia and Russia have lost control of the situation. Tearing up the OPEC+ deal caused a lot of hurt feelings in Moscow and Riyadh, for Putin and MBS. That makes things more difficult, they have to get over that while not losing face. That’s why they’re both pointing the finger at each other.”

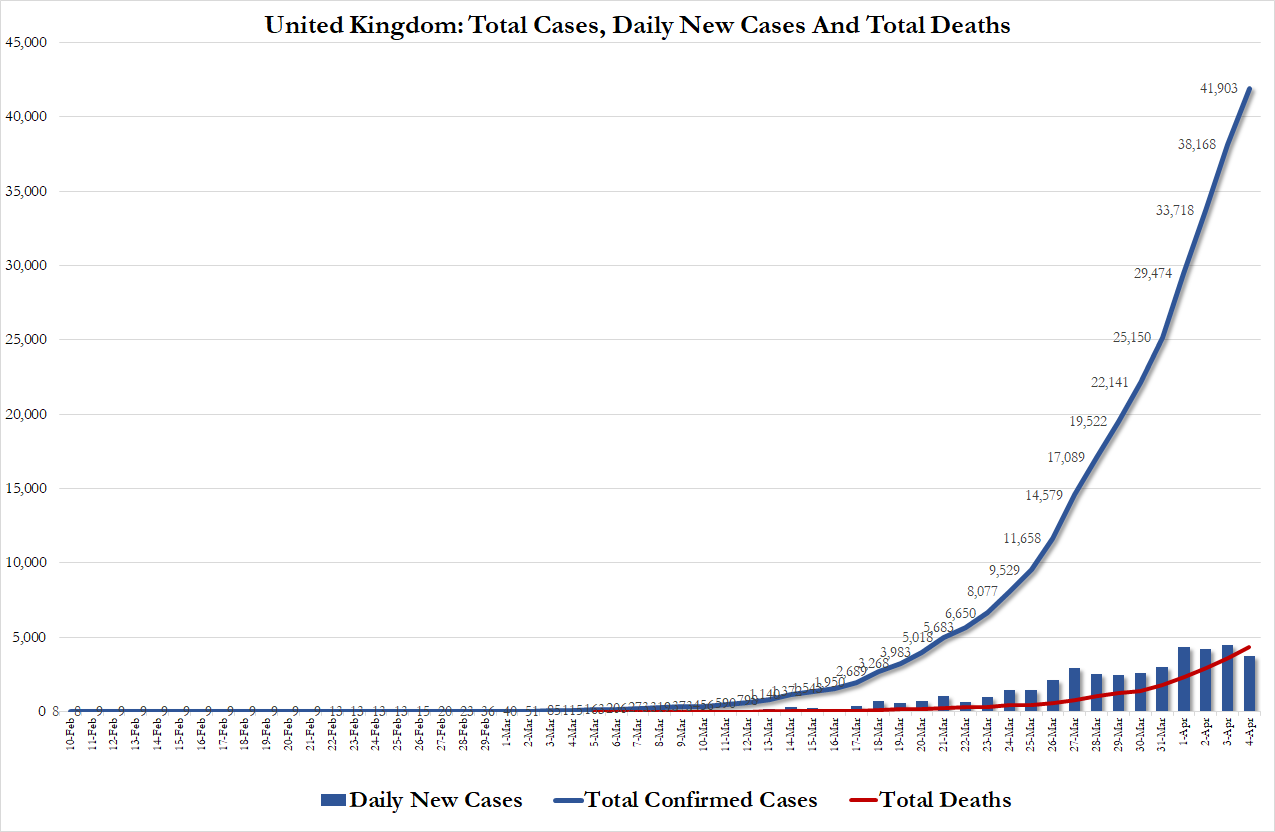

UK Suffers Deadliest Day Yet As New Cases Drop Across Europe; Mortality Rate Jumps To Record 10.3%: Live Updates

As the scramble for ventilators & PPE continues across the country, President Trump last night finally invoked the DPA to ban “unscrupulous actors and profiteers” (an apparent reference to 3M, the pillar of American manufacturing that has become embroiled in a feud with the administration in the middle of an unprecedented pandemic) from exporting critical medical gear used to protect wearers from the coronavirus. Unfortunately, that won’t do anything to increase the availability of badly needed ventilators as hospitals in NYC discover that an alarming number of ICU patients require ventilators. If the number of critical patients starts to overwhelm ICUs, without enough ventilators on hand, nurses and doctors will effectively be deciding who lives and who effectively suffocates to death on their own fluids.

Last night, the chair of the surgery department at New York Presbyterian’s Columbia University Irving Medical Center said 98% of ICU patients required ventilators.

During a Friday morning interview on CNBC, 3M CEO Mike Roman said it was “absurd” to suggest his company wasn’t doing all it could to help the U.S. fight the pandemic, and that by banning export of critical gear, it could make it more difficult to acquire these products in the US as more companies start hoarding and banning export in response.

But perhaps the biggest news overnight came out of the UK, where the Department of Health reported the biggest jump in deaths yet. The DoH said early Saturday that 708 patients had died across the UK on Friday, bringing the nationwide death toll to 4,313. Meanwhile, the 3,735 new cases of COVID-19 reported brought the UK’s total above 40k to 41,903 . The drop in new cases combined with the jump in new deaths brought the UK’s mortality rate to an all-time high of 10.3%.

Meanwhile, with London looking eerily empty as citizens finally obey the lockdown, Health Secretary Matt Hancock reminded the country on Saturday that the order for Britons to stay indoors this weekend was “not a request.”

Germany recorded 6,082 new coronavirus cases over the past 24 hours, bringing its total to 85,778, while the number of deaths rose by 141 to 1,158, a 14% jump, according to the Robert Koch Institute. Outside the UK, perhaps the most startling numbers reported overnight was another jump in confirmed cases in Tokyo: More than 110 new cases of coronavirus were confirmed, the largest daily jump since the outbreak began, a record that has been broken over and over these last two weeks.

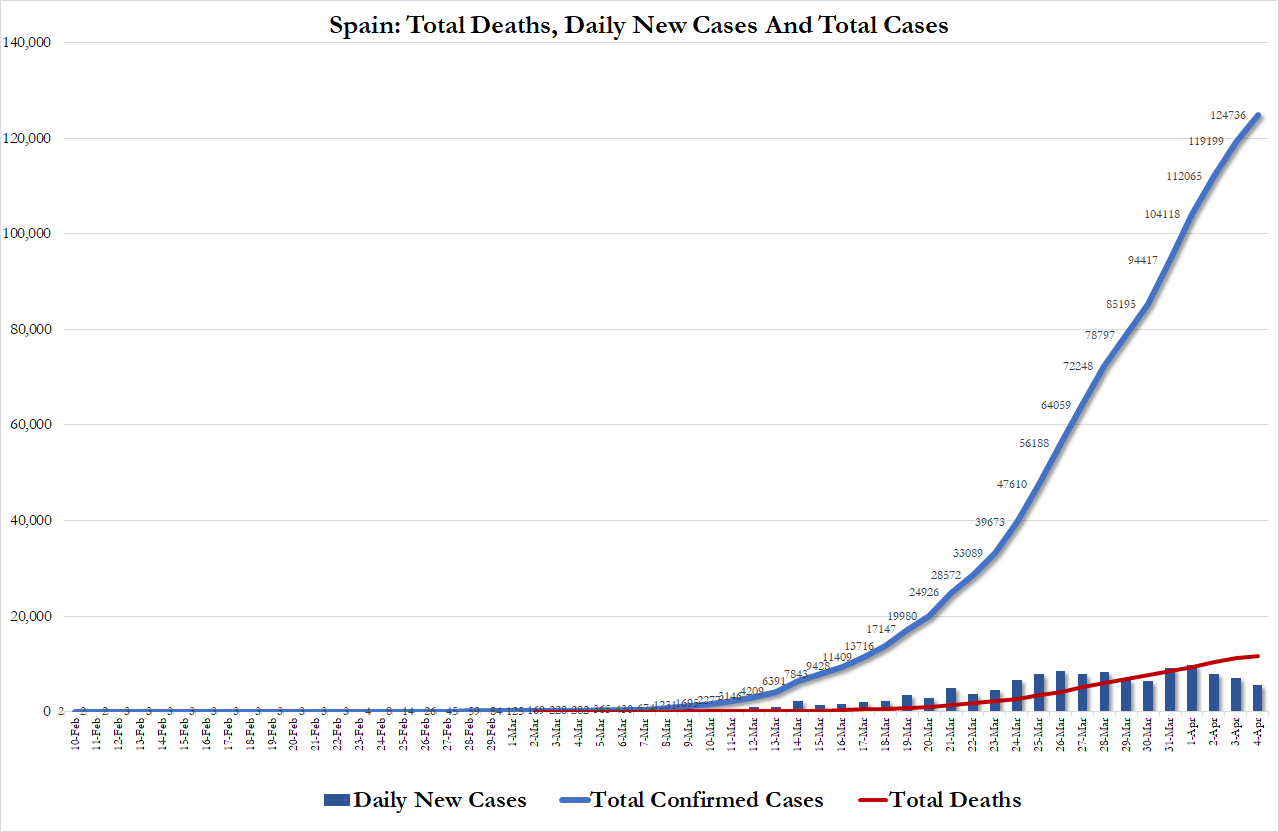

In Italy and Spain, officials reported another promising decline in new cases, suggesting that the lockdowns imposed by both countries are finally working. However, as the number of confirmed cases in Spain surpassed the number of total cases in Italy, the government of PM Pedro Sanchez ordered a two-week extension of Spain’s mandatory lockdown.

“I understand it’s difficult to extend the effort and sacrifice two more weeks,” Sanchez said in a televised speech on Saturday. “These are very difficult days for everyone.” At this point, a longer lockdown would need the approval of Spain’s cabinet and congress.

The number of confirmed cases climbed by 7,026 over the last day to 124,736, according to the Health Ministry. Deaths rose by 809 to 11,744.

Despite Spain officially moving into the No. 2 spot in terms of total confirmed cases (right behind the US at No. 1, though China likely saw the largest number of cases, as possibly hundreds of thousands went uncounted). Spanish Health Minister Salvador Illa said on Friday that the goal of slowing the epidemic was “within reach,” as Spain’s government has imposed some of the most restrictive lockdown measures in Europe.

In Italy, Parliament and the ruling government approved an additional €200 billion ($216 billion) of emergency loans for businesses, according to the local press. It said the moves, part of a new aid decree, will be approved by Monday and will let companies seek state-backed bank loans for as much as 25% of their revenue (with, we suspect, a generous handout to Italy’s struggling banks).

Meanwhile, the number of cases, at 119,827, with the number of deaths at 14,681.

Meanwhile, Portugal reported 638 new cases of coronavirus and 20 new deaths, bringing it to a total of 10,524 cases and 266 deaths. Belgium reported 1,661 new cases and 140 new deaths, bringing it to a total of 18,431 cases and 1,283 deaths.

As Joe Biden and dozens of Democrats bash the administration for the abrupt firing of Capt. Brett Crozier, who circumvented the chain of command to insist that his sailors be saved from an inevitable outbreak onboard his ship, the American military is learning that it isn’t alone. After bringing several infected soldiers from abroad, the French Army Minister said that around 600 French soldiers have now tested positive for the virus.

In the US, pop singer Pink announced late Friday that she had tested positive for COVID-19.

Meanwhile, with markets closed, investors will still be keeping a close eye out for any progress in the US’s $2.2 trillion stimulus, as well as any news about the ‘Part 4’ deal that’s purportedly being worked out.

It is difficult to neatly encapsulate the shift that has occurred in our collective perception and experience over the last several weeks. That all semblance of ‘certainty’ and ‘normalcy’ has disappeared seems no longer the main feature—what stands out is the psychological shift underway, proceeding on the collective and individual levels. What will this mean, how will it continue to evolve? Every conversation I have now touches on the coronavirus or those things that surround it. Everything I read online is related to it. ‘Social distancing’, ‘flattening the curve’—these phrases have become ubiquitous, standardized.

The situation is increasingly and rapidly revealing a number of uncomfortable but long obvious truths about our reality, perhaps none more so than the extent to which so much we take for granted is based on inertia, faith, and on a most rickety apparatus. A humming economy, the wide availability of consumer goods, school, transport, work—all melt away in the face of the virus.

There exists, in this hyperconnected strangeness, the sense that we are living through something predictable, foreseeable. This goes beyond the specific realities of a gutted pandemic response plan (not to mention public health capabilities) and general poor management of the crisis to something more metaphysical: the ubiquitous sense in the present of doom, of an apocalypse, the feeling that we are at the end of time, that there is no future. One has the sense of the present as deja vu, as almost a projected future of the past, of the 20th century, which saw the breakdown coming in the 21st. This sentiment is by no means new, but it has certainly grown more acute—it feels as if we have moved into another level of dystopia.

Of course, then there is the pure economic reality of the situation: over three million jobless claims last week, by far the most ever recorded in such a brief time span. We are seeing the artifice of the ‘service’ economy disappear—again, hardly shocking for those of us who have watched this patchwork mess limp along for years or longer, especially for those of us who have worked in it.

The mainstream may (or may not) be realizing what has been clear to many of us for a long time: there is no real economy.

As the situation worsens, as the wave breaks, there is something extraordinarily chilling as elected officials and ordinary people call for Trump to assert never-before-activated executive powers—as the Justice Department attempts to enact its own draconian measures—in a desperate embrace of authoritarianism, made even more chilling by the fact that many of us understand this and are willing to concede (some of it) may be necessary. All, particularly in light of the realization settling in that things, will never go ‘back to normal.’ What was normal?

The plain fact is that we are living as unsustainably as ever—we were before this, and we’ve hit a massive speed bump that may have ricocheted us off the edge of the cliff toward which we were already careening. If it wasn’t the virus, it would be something else. And while the United States is uniquely poorly positioned to address this, the massive jolt this has provoked the world over makes it clear enough that the systems of capitalism, of industrial civilization itself, have been teetering on the edge. What this will create is unclear, and even for those of us not totally surprised by these events, the speed has often been difficult to grasp.

But something is happening, something new is coming; be prepared…

Finns Warned World’s Best-Funded Welfare State Collapsing Under Virus-Triggered Mass Unemployment

On March 30, Finland said it would extend its countrywide shutdown until May 13 from April 13. It appears strict social distancing and quarantines are working, but it comes at a massive economic cost. Now we’re beginning to learn that the country’s welfare system is cracking and cannot handle the influx of unemployed.

Finland has recorded 1,615 confirmed COVID-19 cases and 19 deaths, by far, some of the lowest numbers when compared to the rest of Europe.

There are signs that restrictions on civilian movement are working, Mika Salminen, the director of health security at the Finnish Institute for Health and Welfare (THL), told reporters at a government press conference on April 1.

The number of people in the risk groups for #coronavirus varies significantly by region in #Finland – variation may affect the need for hospital care across the country.

— Finnish Institute for Health and Welfare (THL) (@THLresearch) April 2, 2020

The opportunity cost of flattening the pandemic curve has come at a tremendous economic cost, resulting in a downturn and high unemployment. Bloomberg notes that Finland has the best welfare system in the world, which is now starting to crack as the surge in unemployment applications is overwhelming the system.

And just like that, in a matter of weeks, 300,000 Finns lost their jobs because of quarantines. The tradeoff is preserving the nation in the long run while dealing with short term economic pain.

Managing Director Sanna Alamaki said on April 1 that funding the welfare system isn’t the current issue: It’s “that the benefit applications can’t be processed and, consequently, money can’t be paid out quickly enough.”

Even if General Unemployment Fund YTK were to triple staff to increase application output, there still would be a three-month wait for out-of-work Finns to receive their benefits. YTK expects that 100,000 more applications could “flood” in this month (April) due in part to the extended shutdowns.

The problem developing, like in many other countries, is that Finland is becoming overwhelmed by the virus. Though each country is different, it’s Finland’s generous welfare system, one of the best-funded in the world, cannot process applications in time that could lead to prolonged suffering by households that have seen incomes dry up in the last month.

Finns who cannot receive benefits in time will lose faith in the government, and that could be the moment when social unrest follows.

The purpose of this article is purely educational. Increasingly, the wider public is turning to gold in a spontaneous reaction to financial and economic problems that have become suddenly apparent, hastened by the spread of the coronavirus. For everyone now thinking of buying gold it is a leap into the unknown, so they should know why.

It is not just the financially inexperienced, but investment managers and financial advisors are equally unaware of what is happening to money and capital markets. We are in the early stages of a radical debasement of state-issued currencies which is on course to collapse the entire financial system.

I explain the two phases of this destruction of fiat money, the one experienced so far and the one we are about to suffer.

I explain why sound money has always been physical gold and silver, returned to by the people after government and banks have collectively destroyed state-originated unsound money.

Introduction

Suddenly, there is increasing public interest in gold. The financially aware will be scratching their heads over what’s going on in financial markets in the broadest sense and might have heard some unintelligible chatter about what is going on in gold. They are asking, why does gold matter? Isn’t gold just an old-fashioned hedge against risk and the true safe haven investment today is US Treasuries? Then there’s the mass of financially unknowledgeable investors who are used to leaving investment matters to their financial advisers, and until recently have viewed the rise in the gold price as an opportunity to sell unwanted jewellery for scrap.

In these two categories we have included the bulk of the population of any advanced nation. They are about to learn what less sophisticated peoples never unlearned: that there’s a difference between a world that is accustomed to relying on ever increasing public debt to provide their welfare, and one where the state provides little or no welfare and people must save to provide for their own and their families’ future.

In Asia, the cradle of civilisation, gold and silver for millennia have had a dual role of ornamentation and of sound, reliable money which can be safely stored for future use. It is only in the last two centuries that the people of Britain, and then America, have advanced themselves into consumerism and taken many other nations with them, leaving the rest of the world described as emerging nations, a euphemism for still poor and uncivilised in western terms.

That is no longer true. In the four decades since Mao Zedong’s death, China and the whole of South-East Asia have embraced debt-fuelled economic progress. Following the end of the short-lived Gandhi era, India is similarly progressing. And when economists forecast global growth, they expect it to come predominantly from these Asian nations while the West stagnates.

Even though these Asian nations have now almost fledged, their populations still save a substantial portion of their income and profits, savings which are the security for their future. While they have embraced inward investment from western and Japanese corporations building factories and providing employment, they hang onto their savings, which are mainly in gold and silver, to preserve their families’ wealth.

For example, it has served the Indian peasantry very well. The price of gold has risen from 180 rupees to the ounce in the mid-1960s to 121,000 rupees today. Of course, it’s not so much gold going up, but the rupee going down. Ordinary Indians have retained the wisdom of their ancestors, despite attempts by successive governments to ban or discourage them from junking rupees by buying gold.

Whatever you believe, the economic awakening of Asia means you can no longer ignore gold and silver’s historical role as the ultimate money. In terms of personal savings, we are faced with a radical re-think because our currencies are demonstrably on the brink of failure. The current dollar-based system evolved from gold standards to a partial gold exchange standard following the Second World War, to abandoning gold backing entirely in 1971. Now, investors are having to learn the gold story anew, exchanging their western debt-driven economics for a world that is reverting to gold.

For the West’s financial establishment, it will be a difficult and costly process. Investment managers’ careers have unwittingly depended on a form of money that is continuously debased, because their performance is enhanced by its loss of purchasing power. Take monetary inflation away, and it is no exaggeration to say the business of purely financial assets, that is to say bonds, equities and derivatives, will mostly disappear.

The sudden relevance of this outcome has been brought to all our attentions by the coronavirus pandemic. The panic currently raging through markets is leading directly to infinite acceleration of monetary inflation, because it is the only means for governments and their central banks to postpone a financial and economic crisis. We are witnessing the early stages of a fiat currency collapse due to its unlimited and accelerating debauchment in an attempt to preserve the West’s financial system.

On any dispassionate analysis, throwing limitless money at a problem is a matter of desperation that ends with the destruction of the currency. For the common man it eventually raises hitherto unasked questions: is the state’s money really money? Should I hold a reserve of it so I can buy the things I will want tomorrow, or should I spend it all now just to get rid of it?

It is this background that causes the wider public, not the financial establishment that hitherto has benefited from monetary inflation, to reconsider gold as a safe haven against mounting uncertainties. Physical possession, or having gold vaulted securely is suddenly becoming preferable to having money invested in a financial system evidently on the brink of failure. Forget investment managers, economists and their economics, it is now time for everyone for himself and his or her dependants.

It is therefore time to relearn the fundamentals about gold, and silver for that matter, in their role as sound money. If anyone is to emerge financially intact from a financial and monetary collapse it will be by hoarding sound money to spend frugally when the time comes.

The aim of this article is to help those who have been seduced by inflationism and lost touch with sound money to regain it.

Why gold and silver are always money and why fiat is failing

From the dawning of economic history various forms of monetary intermediation have been tried. The only ones that have survived the test of all time have been metallic, particularly copper, silver and gold, because of their durability. They evolved from being measured by weight into being unitised as coinage.

As the principal issuer of coins, the state gained a monetary role, and could collect taxes in token coins more efficiently than through the payment of tithes. And with the state controlling the form of money came state corruption. The Chinese were the earliest recorded issuers of paper money, and Marco Polo related how Kublai Khan required merchants to submit all their gold and silver in return for paper receipts manufactured from mulberry leaves. The merchants gained the experience and Kublai Khan got their money.

The Romans robbed their citizens by debasing the coinage, starting with Nero who used the surplus silver thereby gained to pay his army, a tradition that continued with succeeding emperors. It was a failed policy, with assassinations being common. Debasement continued for nearly three centuries to the time of Diocletian, who tried to control the effect on prices through his infamous edict written in stone. The economic consequences of the collapse of Roman money together with price controls led to citizens abandoning the cities to forage in the countryside, a feature of other monetary collapses we have seen time and time again.

With the collapse of fiat currencies today, these outcomes should be borne in mind. But there is another form of monetary fraud to be aware of, poorly understood, which involves the banks. From the earliest times of recorded history, bankers would take in deposits for safe-keeping and redeploy them for their own use. In about 393 BC, an Athenian lawyer, Isocrates, defended Passio, a banker accused of misappropriating deposits of gold and silver entrusted to him by a son of a favourite of Satyrus, king of Bospherus. While Isocrates’s speech is recorded, it seems the verdict is lost to us. But like so many bankers who followed him, Passio survived the scandal and died a wealthy and successful man.

The misappropriation of deposit money has been a feature of banking ever since, and today’s denial of the fundamental right to own your deposited money was formalised in the Bank Charter Act of 1844 in English law, which failed to differentiate between actual banknotes that were backed by gold, and money loaned into existence by fractional reserve banking, which become the source of customers’ deposits.

To further expand the point, we must briefly digress and describe the process of creating bank credit and matching deposits. The common procedure is for a bank to create a loan facility for a customer, who draws on the facility to pay his creditors. The creditors then have money to deposit, which is either deposited at the bank that originated the loan or at another bank. To the extent that loans drawn down create imbalances between banks, they are resolved in wholesale money markets so that all banks’ balance sheets balance. But note that the money loaned created the deposits, and it is by these means that banks create unbacked money in a system supposedly on a gold standard.

Fractional reserve banking is so described because the ability to create deposits by loaning money into existence allows banks to gear up their balance sheets so that their own capital becomes a fraction of the total. At any one time the relationship between the two reflects the bankers’ assessment of risk and reward. At times of low perceived risk and improving economic prospects, they expand the ratio of deposits and other liabilities to ten or more times their underlying capital. When they perceive increased lending risk, they try to reduce the ratio to prevent their capital being wiped out by losses.

The economic consequences are periodic banking crises as banks become first overextended and then ultra-cautious in their lending. Additionally, there is the response by governments and their state-owned central banks to the periodic banking crises, in which they intervene rather than let banks fail.

It was Walter Bagehot who in the late-nineteenth century coined the term for the Bank of England acting as lender of last resort, a function which has become more extensive over successive credit cycles. The quantities of bank credit have expanded over time and the accumulation of money issued to finance periodic bank rescues and excess government spending has remained in the system. Inevitably, it led to the abandonment of any pretence of backing state-issued currency with gold when the gold pool failed in the late 1960s.

When the relationship between gold and state-issued currencies finally broke down it permitted monetary inflation, whose only constraint was the effect on prices. This brings us to the current situation, where the expansion of the quantity of money in all major currencies is about to increase massively, in an attempt to control the economic consequences of the coronavirus.Unlimited monetary expansion became stated official policy for America’s central bank last week and stated or unstated, for the other major central banks as well. The implied monetary policy was that as soon as the virus passes the economy will return to normal, so the monetary expansion will normalise.

But it should be noted that liquidity strains in the banking system began to be appear last September, nearly five months before the virus spread from China. The Federal Reserve Board (America’s central bank – the Fed) was forced to begin a daily series of monetary injections into the banking system, which is ongoing. Liquidity problems are simply a sign of fractional reserve banks perceiving a shift in the balance of profit relative to risk and acting to protect their capital from losses. Put another way, the liquidity shortage is created by banks destroying money by reversing the bank credit creation process.

Therefore, the evidence that the credit cycle has turned cannot be disputed and will add to the required quantities of money to be issued by central banks in connection with the virus alone, if a deflationary contraction of bank credit is to be averted. It is beyond the scope of this article to go fully into what will be involved, but the scale of monetary inflation required is clearly immense.

What will alert the public to failing fiat currencies?

Statisticians inform us that the rate of price inflation is in the order of two per cent. All our personal experiences suggest it is much higher, and independent analysts in America tell us it is closer to ten per cent, more in line with our own knowledge than government figures. The discrepancy exists because we can talk about the general level of prices as a concept, but that does not mean we can actually measure it.

This is important, because the cost of funding government borrowing (and everyone else’s for that matter) is linked to the rate of price inflation. Buyers of US Treasuries, regarded in financial circles as the risk-free investment, will want a rate of return to compensate them for the loss of the dollar’s purchasing power over the life of the investment. For now, they accept it is a little less than two per cent annually as stated by government statisticians, but that is bound to be questioned when the Fed ramps up its money-printing.

So far, most notably the expansion of money supply has fuelled rising prices for financial assets. That inflated balloon in now leaking badly. When doubts increasingly begin to creep in about a realistic value for all bonds relative to a realistic assessment of price inflation, all financial assets that refer to US Treasury bonds as the risk-free yardstick will deflate even further. Consequently, investors accustomed to more or less continually rising prices for financial assets will face substantial losses. The penny is now dropping that investing in them for wealth preservation is unsafe, and the central banks’ policy of debasing money to support financial markets will eventually fail.

In another development, the US Government has just passed a reflation bill whereby each qualifying adult will be given $1200 and $500 on behalf of every child. This money can only be spent on essentials such as food, because the majority of retailers are in lockdown. Meanwhile the production and distribution of food is likely to be adversely affected by the virus. There can be only one outcome from the combination of a restriction of food supply and a one-off hit of extra money for everyone: prices for food will rise strongly. Following the example of Diocletian’s edict, we can then expect politicians to impose price controls in an attempt to quell public dissent, which will inevitably reduce food supplies even more.

Never mind what the consumer price index says; food is a small part of it and officially, the CPI might even fall. But a growing likelihood of public disaffection over food prices is bound to spread the message that the dollar is not buying as much as it did very recently. It is a small step from there for the American public to finally reject the fiat dollar as a medium of exchange. We will then learn a fundamental truth the hard way: money relies on its credibility with the people who are its users. And once that credibility is destroyed the currency is destroyed with it.

The time taken for its destruction has been illustrated by similar events in the past. We must distinguish between a long, slow cumulative attrition of value, such as that since the failure of the London gold pool in the late 1960s, followed by the ending of the remaining fig leaf of gold convertibility by President Nixon in August 1971. This is the first of two phases, illustrated in Figure 1.

Since 1969, relative to gold the yen has lost 92.8% of its purchasing power, against the dollar 97.8%, the euro (and its previous constituents) 98.5% and sterling 98.9%. And these falls have been hardly noticed! As the yardstick for sound money, gold has been deliberately side-lined in favour of the dollar as the backing for other fiat currencies. When the British think the pound has fallen, they say it is against the dollar, oblivious to the fact that the dollar itself has lost all but 2.2% of its 1969 purchasing power.

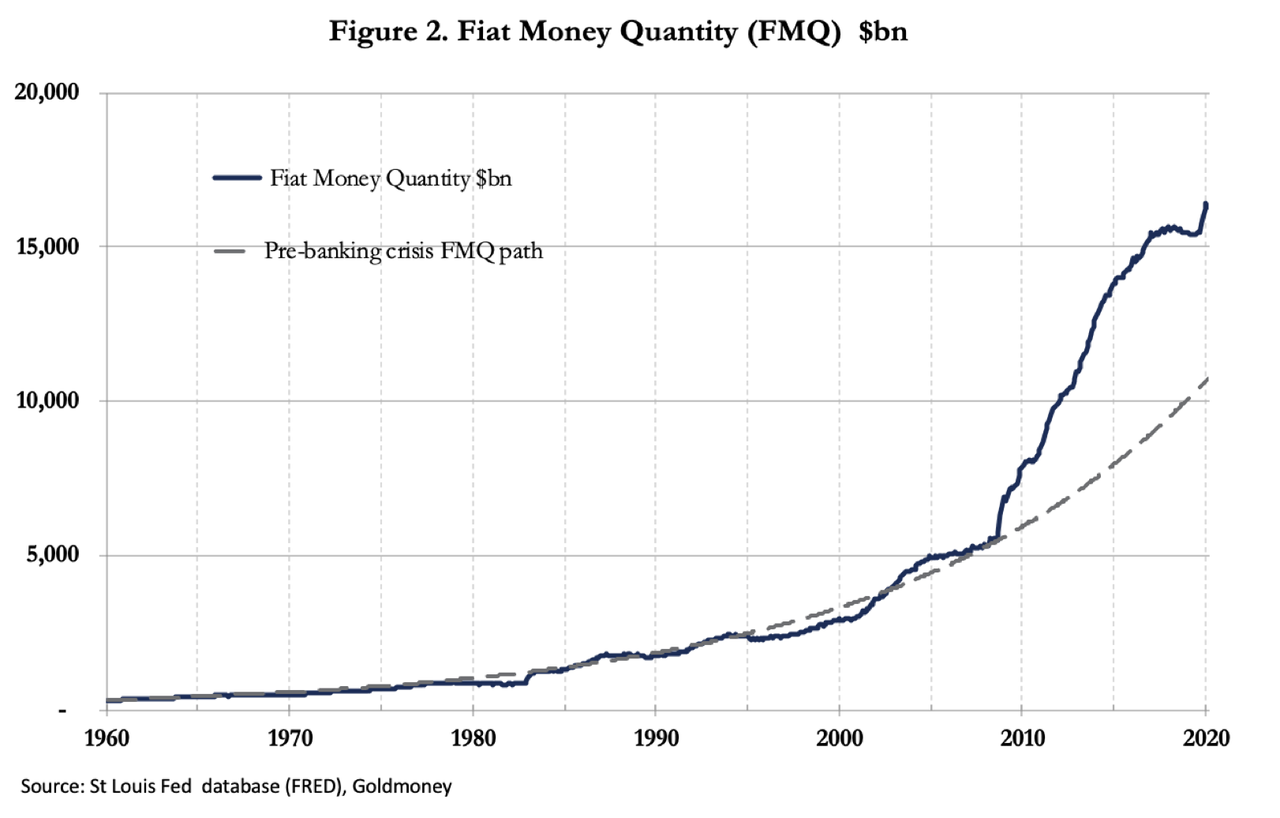

The reason behind the dollar’s decline is the massive expansion of the quantity of dollars relative to gold, shown in Figure 2.

The fiat money quantity is the total number of dollars both in public ownership and held in reserve by the banks in their accounts at the Fed. Because these figures are only available six weeks in arrears, they have yet to reflect the most recent expansion of money. But it was already shooting into record territory at the beginning of February and the extent of monetary instability is illustrated further by its departure from the relatively steady expansionary course until the Lehman crisis, shown by the extended pecked line.

The expansion of FMQ from 1969 has been a multiple of 32.5 times, giving an arithmetic dilution of purchasing power of 97%, which compares with a fall in terms of the gold price of 97.8%. We can therefore say that over fifty-one years, the change in the dollar price of gold has tracked the expansion of the quantity of dollars as represented by the fiat money quantity fairly accurately.

Empirical experience tells us there is a second phase, when a broadly arithmetic relationship between the quantity of money in circulation and its purchasing power breaks down. When the public awaken to what is happening to fiat money, a mass psychology of rejection takes over to drive the relationship between the currency and its use-value. In France, the mandats territoriaux issued in February 1796 to replace the failing assignats currency were worthless by the following February. In 1923, the German papiermark, which had been losing purchasing power from the end of the Great War took about seven months to finally collapse from May to November. It became a flight into goods and real values that marks the end of a monetary inflation by the complete breakdown of the monetary system.

For a comparison with the contemporary monetary system, which binds together the fate of financial asset values and that of the currency, there is none more apt that that of the failure of John Law’s Mississippi bubble, when he gained control of the French currency and printed it to support the shares of his venture. Law’s policies of inflationism were remarkably similar to those of John Maynard Keynes, which inform the basis of monetary policy today. And today’s neo-Keynesians are unashamedly debasing the currency to support financial assets, just as Law did. Law’s scheme began to show signs of failing in early 1720, and by the following September, not only had the shares in his Mississippi venture collapsed, but his unbacked livres were worthless as well.

If we replicate the John Law experience today, the dollar and all the currencies which sail with her will become worthless in short order, probably by the year-end. We have seen that a final acceleration of monetary inflation is starting after a fifty-year period of debasement which the public has hardly noticed. State-issued fiat currencies are now embarking on that second phase, when they will lose all purchasing power.

The replacement of government fiat money by gold and silver

Now that we can anticipate the final destruction of contemporary fiat currencies, we must consider their replacement and how it comes about. Many commentators who have a grasp of the problem talk of a monetary reset, failing to understand that the problem is a loss of trust in state-issued currencies that cannot be resolved by the issuance of a variation on the fiat theme. Nor can a solution be found in the issuance of a state-issued cryptocurrency. The fact of the matter is the days of financing government spending and economic objectives by monetary expansion are drawing to an end.

A few governments are in a position to back their currencies with gold, freely convertible at the choice of the user at a fixed rate. These include Russia, which has been accumulating gold and dumping dollars in recent years. China, where there is compelling evidence that the state has accumulated significant undeclared bullion, and now that an estimated 17,000 tonnes are in private ownership, could also adopt a gold standard, along with a few other Asian nations. But a gold standard also requires the elimination of government spending deficits, which Russia, China and a few Asian nations could achieve. Additionally, the banking system, whereby bank credit can be expanded by creating loans, must also be reformed. Otherwise, it will be possible for anyone to draw down a loan in unbacked bank credit in order to cash it in for gold. Similarly, safeguards to prevent foreign bank credit expansion being used through the foreign exchanges to acquire gold substitutes for encashment would have to be implemented.

Western nations will find it far more difficult to adjust to a gold standard, having mandated welfare commitments that require continuing currency debasement in order to pay for them. Furthermore, in the United States, the banking cartel is immensely powerful and so long as the fiat system exists, they are unlikely to give up their assumed right to create money out of thin air in the form of credit, particularly when the process becomes more profitable as the dollar’s decline accelerates. The currency will therefore die before radical reform is acceptable to the US financial establishment, and all those that adhere to it.

For individuals, it is safer to assume that personal possession of physical gold and silver bars and coins is best for wealth protection and future spending. It is a mistake to think that these two moneys of millennia are just an investment alternative: they are money which can act as a store of your wealth. They can then be spent on the essentials of life, which are spiralling beyond the reach of failing fiat. And when the return of some economic and political stability can be anticipated, durable assets, such as property, and productive goods might be acquired. In that way gold and silver will return into circulation.

The failure of derivatives

Derivative markets, principally Comex futures and the London bullion market, have expanded to absorb much of the demand for bullion. Taken together, the last recorded figures tell us that gold derivatives in these two markets had a notional value of $600bn, while the sum of annual mine production and recycled scrap at the same time was worth approximately $20bn, a relationship of 30:1.

As argued in this article the acceleration of monetary inflation is collapsing both financial markets and fiat currencies. What no one tells you is that over-the-counter derivatives, which according to the Bank for International Settlements are worth $640 trillion, will also disappear in a fiat currency collapse. Therefore, assuming there is no change in the overall level of demand for gold, thirty times the level of physical demand previously accommodated in derivatives at end-June last year either disappears or will be accommodated in above-ground stocks of gold.

It is in that context we should interpret what is happening in financial markets. The strains at a time of contracting bank credit are acute. If they have not been told already, dealers at the bullion banks will be instructed by their financial controllers to reduce their positions, because of the inexorable pull of contracting bank credit in the bank’s wider lending and deposit activities.

The only avenues for acquiring exposure of gold and silver will be increasingly restricted to bullion itself. Retailer outlets have already been closed by the virus and online retailers have little or no stock. Gold and silver can be acquired through companies such as Goldmoney, so that personal wealth can still be stored in secure, insured vaults. Physically backed exchange-traded funds continue to be available, but with the increasingly certain demise of derivatives, and the problems likely to evolve for the ETFs which use them, ETFs backed by physical gold are also exposed to unforeseen issues.

The hiatus on Comex probably marks the beginning of the end of precious metal derivatives. Already, bullion banks have reduced their exposure on Comex by the equivalent of 938 tonnes to 1,541 tonnes. But with supply substantially reduced from mines and refiners in lockdown at a time when governments are promising unlimited monetary inflation, it is hard to see favourable conditions for an orderly wind-down on Comex.

Conclusion

Events over the last few weeks have alerted a wider audience to the destruction of values in financial markets. The unwritten agreement between investors and the major central banks whereby financial markets will always be supported is now unravelling. Increasingly, the only buyers of government bonds at current levels are the central banks by inflating their currencies.

Meanwhile, liquidity problems in hard-hit economies are mounting. And it is not just the coronavirus; nearly five months before the virus hit Western financial markets the Fed was having to inject liquidity into the US banking system in record amounts through the repo market.

Looking at historical comparisons of our current set of circumstances we find that the Mississippi bubble of 1720 in France appears to be a reasonable template for the current situation. John Law, who masterminded that scheme, gained control of France’s money which he then used to buy shares in his Mississippi venture. Today’s central banks are following a similar path, except on a global scale. Law’s scheme saw both his unbacked currency and the shares in his Mississippi venture collapse from top to bottom in only nine months. If we repeat this experience today, not only will financial markets collapse, but the currencies in which they are notionally measured will be worthless by the year-end.

Signs of failure in some markets, such as derivative markets for precious metals, can be taken as evidence that a wider financial dislocation is now in progress. It is in this light that an understanding of the role of physical gold and silver is so important. They are the only sound money, a safe refuge for ordinary people, being incorruptible by governments. And as their prices rise towards infinity, it will be entirely a reflection of the end of the current fiat money regime.

{kind=link}