It is difficult to neatly encapsulate the shift that has occurred in our collective perception and experience over the last several weeks. That all semblance of ‘certainty’ and ‘normalcy’ has disappeared seems no longer the main feature—what stands out is the psychological shift underway, proceeding on the collective and individual levels. What will this mean, how will it continue to evolve? Every conversation I have now touches on the coronavirus or those things that surround it. Everything I read online is related to it. ‘Social distancing’, ‘flattening the curve’—these phrases have become ubiquitous, standardized.

The situation is increasingly and rapidly revealing a number of uncomfortable but long obvious truths about our reality, perhaps none more so than the extent to which so much we take for granted is based on inertia, faith, and on a most rickety apparatus. A humming economy, the wide availability of consumer goods, school, transport, work—all melt away in the face of the virus.

There exists, in this hyperconnected strangeness, the sense that we are living through something predictable, foreseeable. This goes beyond the specific realities of a gutted pandemic response plan (not to mention public health capabilities) and general poor management of the crisis to something more metaphysical: the ubiquitous sense in the present of doom, of an apocalypse, the feeling that we are at the end of time, that there is no future. One has the sense of the present as deja vu, as almost a projected future of the past, of the 20th century, which saw the breakdown coming in the 21st. This sentiment is by no means new, but it has certainly grown more acute—it feels as if we have moved into another level of dystopia.

Of course, then there is the pure economic reality of the situation: over three million jobless claims last week, by far the most ever recorded in such a brief time span. We are seeing the artifice of the ‘service’ economy disappear—again, hardly shocking for those of us who have watched this patchwork mess limp along for years or longer, especially for those of us who have worked in it.

The mainstream may (or may not) be realizing what has been clear to many of us for a long time: there is no real economy.

As the situation worsens, as the wave breaks, there is something extraordinarily chilling as elected officials and ordinary people call for Trump to assert never-before-activated executive powers—as the Justice Department attempts to enact its own draconian measures—in a desperate embrace of authoritarianism, made even more chilling by the fact that many of us understand this and are willing to concede (some of it) may be necessary. All, particularly in light of the realization settling in that things, will never go ‘back to normal.’ What was normal?

The plain fact is that we are living as unsustainably as ever—we were before this, and we’ve hit a massive speed bump that may have ricocheted us off the edge of the cliff toward which we were already careening. If it wasn’t the virus, it would be something else. And while the United States is uniquely poorly positioned to address this, the massive jolt this has provoked the world over makes it clear enough that the systems of capitalism, of industrial civilization itself, have been teetering on the edge. What this will create is unclear, and even for those of us not totally surprised by these events, the speed has often been difficult to grasp.

But something is happening, something new is coming; be prepared…

Finns Warned World’s Best-Funded Welfare State Collapsing Under Virus-Triggered Mass Unemployment

On March 30, Finland said it would extend its countrywide shutdown until May 13 from April 13. It appears strict social distancing and quarantines are working, but it comes at a massive economic cost. Now we’re beginning to learn that the country’s welfare system is cracking and cannot handle the influx of unemployed.

Finland has recorded 1,615 confirmed COVID-19 cases and 19 deaths, by far, some of the lowest numbers when compared to the rest of Europe.

There are signs that restrictions on civilian movement are working, Mika Salminen, the director of health security at the Finnish Institute for Health and Welfare (THL), told reporters at a government press conference on April 1.

The number of people in the risk groups for #coronavirus varies significantly by region in #Finland – variation may affect the need for hospital care across the country.

— Finnish Institute for Health and Welfare (THL) (@THLresearch) April 2, 2020

The opportunity cost of flattening the pandemic curve has come at a tremendous economic cost, resulting in a downturn and high unemployment. Bloomberg notes that Finland has the best welfare system in the world, which is now starting to crack as the surge in unemployment applications is overwhelming the system.

And just like that, in a matter of weeks, 300,000 Finns lost their jobs because of quarantines. The tradeoff is preserving the nation in the long run while dealing with short term economic pain.

Managing Director Sanna Alamaki said on April 1 that funding the welfare system isn’t the current issue: It’s “that the benefit applications can’t be processed and, consequently, money can’t be paid out quickly enough.”

Even if General Unemployment Fund YTK were to triple staff to increase application output, there still would be a three-month wait for out-of-work Finns to receive their benefits. YTK expects that 100,000 more applications could “flood” in this month (April) due in part to the extended shutdowns.

The problem developing, like in many other countries, is that Finland is becoming overwhelmed by the virus. Though each country is different, it’s Finland’s generous welfare system, one of the best-funded in the world, cannot process applications in time that could lead to prolonged suffering by households that have seen incomes dry up in the last month.

Finns who cannot receive benefits in time will lose faith in the government, and that could be the moment when social unrest follows.

The purpose of this article is purely educational. Increasingly, the wider public is turning to gold in a spontaneous reaction to financial and economic problems that have become suddenly apparent, hastened by the spread of the coronavirus. For everyone now thinking of buying gold it is a leap into the unknown, so they should know why.

It is not just the financially inexperienced, but investment managers and financial advisors are equally unaware of what is happening to money and capital markets. We are in the early stages of a radical debasement of state-issued currencies which is on course to collapse the entire financial system.

I explain the two phases of this destruction of fiat money, the one experienced so far and the one we are about to suffer.

I explain why sound money has always been physical gold and silver, returned to by the people after government and banks have collectively destroyed state-originated unsound money.

Introduction

Suddenly, there is increasing public interest in gold. The financially aware will be scratching their heads over what’s going on in financial markets in the broadest sense and might have heard some unintelligible chatter about what is going on in gold. They are asking, why does gold matter? Isn’t gold just an old-fashioned hedge against risk and the true safe haven investment today is US Treasuries? Then there’s the mass of financially unknowledgeable investors who are used to leaving investment matters to their financial advisers, and until recently have viewed the rise in the gold price as an opportunity to sell unwanted jewellery for scrap.

In these two categories we have included the bulk of the population of any advanced nation. They are about to learn what less sophisticated peoples never unlearned: that there’s a difference between a world that is accustomed to relying on ever increasing public debt to provide their welfare, and one where the state provides little or no welfare and people must save to provide for their own and their families’ future.

In Asia, the cradle of civilisation, gold and silver for millennia have had a dual role of ornamentation and of sound, reliable money which can be safely stored for future use. It is only in the last two centuries that the people of Britain, and then America, have advanced themselves into consumerism and taken many other nations with them, leaving the rest of the world described as emerging nations, a euphemism for still poor and uncivilised in western terms.

That is no longer true. In the four decades since Mao Zedong’s death, China and the whole of South-East Asia have embraced debt-fuelled economic progress. Following the end of the short-lived Gandhi era, India is similarly progressing. And when economists forecast global growth, they expect it to come predominantly from these Asian nations while the West stagnates.

Even though these Asian nations have now almost fledged, their populations still save a substantial portion of their income and profits, savings which are the security for their future. While they have embraced inward investment from western and Japanese corporations building factories and providing employment, they hang onto their savings, which are mainly in gold and silver, to preserve their families’ wealth.

For example, it has served the Indian peasantry very well. The price of gold has risen from 180 rupees to the ounce in the mid-1960s to 121,000 rupees today. Of course, it’s not so much gold going up, but the rupee going down. Ordinary Indians have retained the wisdom of their ancestors, despite attempts by successive governments to ban or discourage them from junking rupees by buying gold.

Whatever you believe, the economic awakening of Asia means you can no longer ignore gold and silver’s historical role as the ultimate money. In terms of personal savings, we are faced with a radical re-think because our currencies are demonstrably on the brink of failure. The current dollar-based system evolved from gold standards to a partial gold exchange standard following the Second World War, to abandoning gold backing entirely in 1971. Now, investors are having to learn the gold story anew, exchanging their western debt-driven economics for a world that is reverting to gold.

For the West’s financial establishment, it will be a difficult and costly process. Investment managers’ careers have unwittingly depended on a form of money that is continuously debased, because their performance is enhanced by its loss of purchasing power. Take monetary inflation away, and it is no exaggeration to say the business of purely financial assets, that is to say bonds, equities and derivatives, will mostly disappear.

The sudden relevance of this outcome has been brought to all our attentions by the coronavirus pandemic. The panic currently raging through markets is leading directly to infinite acceleration of monetary inflation, because it is the only means for governments and their central banks to postpone a financial and economic crisis. We are witnessing the early stages of a fiat currency collapse due to its unlimited and accelerating debauchment in an attempt to preserve the West’s financial system.

On any dispassionate analysis, throwing limitless money at a problem is a matter of desperation that ends with the destruction of the currency. For the common man it eventually raises hitherto unasked questions: is the state’s money really money? Should I hold a reserve of it so I can buy the things I will want tomorrow, or should I spend it all now just to get rid of it?

It is this background that causes the wider public, not the financial establishment that hitherto has benefited from monetary inflation, to reconsider gold as a safe haven against mounting uncertainties. Physical possession, or having gold vaulted securely is suddenly becoming preferable to having money invested in a financial system evidently on the brink of failure. Forget investment managers, economists and their economics, it is now time for everyone for himself and his or her dependants.

It is therefore time to relearn the fundamentals about gold, and silver for that matter, in their role as sound money. If anyone is to emerge financially intact from a financial and monetary collapse it will be by hoarding sound money to spend frugally when the time comes.

The aim of this article is to help those who have been seduced by inflationism and lost touch with sound money to regain it.

Why gold and silver are always money and why fiat is failing

From the dawning of economic history various forms of monetary intermediation have been tried. The only ones that have survived the test of all time have been metallic, particularly copper, silver and gold, because of their durability. They evolved from being measured by weight into being unitised as coinage.

As the principal issuer of coins, the state gained a monetary role, and could collect taxes in token coins more efficiently than through the payment of tithes. And with the state controlling the form of money came state corruption. The Chinese were the earliest recorded issuers of paper money, and Marco Polo related how Kublai Khan required merchants to submit all their gold and silver in return for paper receipts manufactured from mulberry leaves. The merchants gained the experience and Kublai Khan got their money.

The Romans robbed their citizens by debasing the coinage, starting with Nero who used the surplus silver thereby gained to pay his army, a tradition that continued with succeeding emperors. It was a failed policy, with assassinations being common. Debasement continued for nearly three centuries to the time of Diocletian, who tried to control the effect on prices through his infamous edict written in stone. The economic consequences of the collapse of Roman money together with price controls led to citizens abandoning the cities to forage in the countryside, a feature of other monetary collapses we have seen time and time again.

With the collapse of fiat currencies today, these outcomes should be borne in mind. But there is another form of monetary fraud to be aware of, poorly understood, which involves the banks. From the earliest times of recorded history, bankers would take in deposits for safe-keeping and redeploy them for their own use. In about 393 BC, an Athenian lawyer, Isocrates, defended Passio, a banker accused of misappropriating deposits of gold and silver entrusted to him by a son of a favourite of Satyrus, king of Bospherus. While Isocrates’s speech is recorded, it seems the verdict is lost to us. But like so many bankers who followed him, Passio survived the scandal and died a wealthy and successful man.

The misappropriation of deposit money has been a feature of banking ever since, and today’s denial of the fundamental right to own your deposited money was formalised in the Bank Charter Act of 1844 in English law, which failed to differentiate between actual banknotes that were backed by gold, and money loaned into existence by fractional reserve banking, which become the source of customers’ deposits.

To further expand the point, we must briefly digress and describe the process of creating bank credit and matching deposits. The common procedure is for a bank to create a loan facility for a customer, who draws on the facility to pay his creditors. The creditors then have money to deposit, which is either deposited at the bank that originated the loan or at another bank. To the extent that loans drawn down create imbalances between banks, they are resolved in wholesale money markets so that all banks’ balance sheets balance. But note that the money loaned created the deposits, and it is by these means that banks create unbacked money in a system supposedly on a gold standard.

Fractional reserve banking is so described because the ability to create deposits by loaning money into existence allows banks to gear up their balance sheets so that their own capital becomes a fraction of the total. At any one time the relationship between the two reflects the bankers’ assessment of risk and reward. At times of low perceived risk and improving economic prospects, they expand the ratio of deposits and other liabilities to ten or more times their underlying capital. When they perceive increased lending risk, they try to reduce the ratio to prevent their capital being wiped out by losses.

The economic consequences are periodic banking crises as banks become first overextended and then ultra-cautious in their lending. Additionally, there is the response by governments and their state-owned central banks to the periodic banking crises, in which they intervene rather than let banks fail.

It was Walter Bagehot who in the late-nineteenth century coined the term for the Bank of England acting as lender of last resort, a function which has become more extensive over successive credit cycles. The quantities of bank credit have expanded over time and the accumulation of money issued to finance periodic bank rescues and excess government spending has remained in the system. Inevitably, it led to the abandonment of any pretence of backing state-issued currency with gold when the gold pool failed in the late 1960s.

When the relationship between gold and state-issued currencies finally broke down it permitted monetary inflation, whose only constraint was the effect on prices. This brings us to the current situation, where the expansion of the quantity of money in all major currencies is about to increase massively, in an attempt to control the economic consequences of the coronavirus.Unlimited monetary expansion became stated official policy for America’s central bank last week and stated or unstated, for the other major central banks as well. The implied monetary policy was that as soon as the virus passes the economy will return to normal, so the monetary expansion will normalise.

But it should be noted that liquidity strains in the banking system began to be appear last September, nearly five months before the virus spread from China. The Federal Reserve Board (America’s central bank – the Fed) was forced to begin a daily series of monetary injections into the banking system, which is ongoing. Liquidity problems are simply a sign of fractional reserve banks perceiving a shift in the balance of profit relative to risk and acting to protect their capital from losses. Put another way, the liquidity shortage is created by banks destroying money by reversing the bank credit creation process.

Therefore, the evidence that the credit cycle has turned cannot be disputed and will add to the required quantities of money to be issued by central banks in connection with the virus alone, if a deflationary contraction of bank credit is to be averted. It is beyond the scope of this article to go fully into what will be involved, but the scale of monetary inflation required is clearly immense.

What will alert the public to failing fiat currencies?

Statisticians inform us that the rate of price inflation is in the order of two per cent. All our personal experiences suggest it is much higher, and independent analysts in America tell us it is closer to ten per cent, more in line with our own knowledge than government figures. The discrepancy exists because we can talk about the general level of prices as a concept, but that does not mean we can actually measure it.

This is important, because the cost of funding government borrowing (and everyone else’s for that matter) is linked to the rate of price inflation. Buyers of US Treasuries, regarded in financial circles as the risk-free investment, will want a rate of return to compensate them for the loss of the dollar’s purchasing power over the life of the investment. For now, they accept it is a little less than two per cent annually as stated by government statisticians, but that is bound to be questioned when the Fed ramps up its money-printing.

So far, most notably the expansion of money supply has fuelled rising prices for financial assets. That inflated balloon in now leaking badly. When doubts increasingly begin to creep in about a realistic value for all bonds relative to a realistic assessment of price inflation, all financial assets that refer to US Treasury bonds as the risk-free yardstick will deflate even further. Consequently, investors accustomed to more or less continually rising prices for financial assets will face substantial losses. The penny is now dropping that investing in them for wealth preservation is unsafe, and the central banks’ policy of debasing money to support financial markets will eventually fail.

In another development, the US Government has just passed a reflation bill whereby each qualifying adult will be given $1200 and $500 on behalf of every child. This money can only be spent on essentials such as food, because the majority of retailers are in lockdown. Meanwhile the production and distribution of food is likely to be adversely affected by the virus. There can be only one outcome from the combination of a restriction of food supply and a one-off hit of extra money for everyone: prices for food will rise strongly. Following the example of Diocletian’s edict, we can then expect politicians to impose price controls in an attempt to quell public dissent, which will inevitably reduce food supplies even more.

Never mind what the consumer price index says; food is a small part of it and officially, the CPI might even fall. But a growing likelihood of public disaffection over food prices is bound to spread the message that the dollar is not buying as much as it did very recently. It is a small step from there for the American public to finally reject the fiat dollar as a medium of exchange. We will then learn a fundamental truth the hard way: money relies on its credibility with the people who are its users. And once that credibility is destroyed the currency is destroyed with it.

The time taken for its destruction has been illustrated by similar events in the past. We must distinguish between a long, slow cumulative attrition of value, such as that since the failure of the London gold pool in the late 1960s, followed by the ending of the remaining fig leaf of gold convertibility by President Nixon in August 1971. This is the first of two phases, illustrated in Figure 1.

Since 1969, relative to gold the yen has lost 92.8% of its purchasing power, against the dollar 97.8%, the euro (and its previous constituents) 98.5% and sterling 98.9%. And these falls have been hardly noticed! As the yardstick for sound money, gold has been deliberately side-lined in favour of the dollar as the backing for other fiat currencies. When the British think the pound has fallen, they say it is against the dollar, oblivious to the fact that the dollar itself has lost all but 2.2% of its 1969 purchasing power.

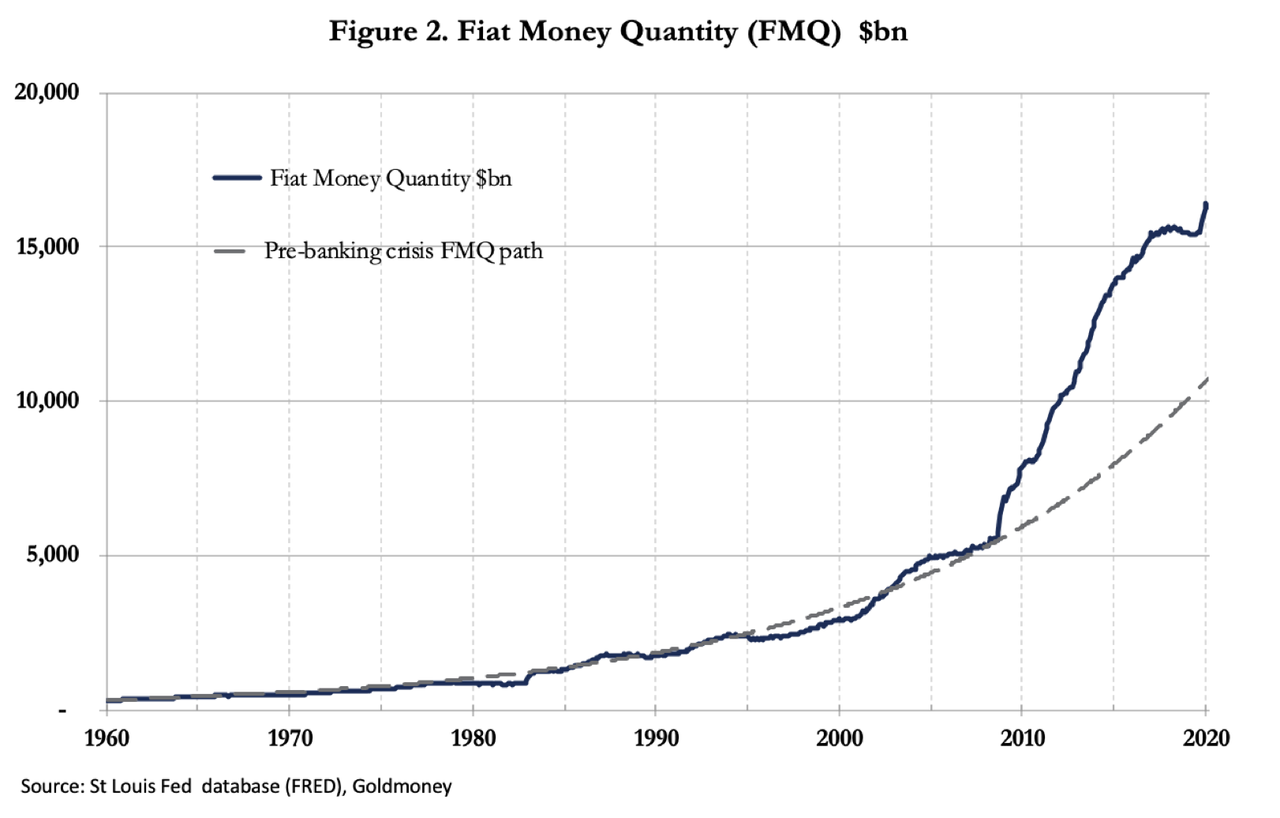

The reason behind the dollar’s decline is the massive expansion of the quantity of dollars relative to gold, shown in Figure 2.

The fiat money quantity is the total number of dollars both in public ownership and held in reserve by the banks in their accounts at the Fed. Because these figures are only available six weeks in arrears, they have yet to reflect the most recent expansion of money. But it was already shooting into record territory at the beginning of February and the extent of monetary instability is illustrated further by its departure from the relatively steady expansionary course until the Lehman crisis, shown by the extended pecked line.

The expansion of FMQ from 1969 has been a multiple of 32.5 times, giving an arithmetic dilution of purchasing power of 97%, which compares with a fall in terms of the gold price of 97.8%. We can therefore say that over fifty-one years, the change in the dollar price of gold has tracked the expansion of the quantity of dollars as represented by the fiat money quantity fairly accurately.

Empirical experience tells us there is a second phase, when a broadly arithmetic relationship between the quantity of money in circulation and its purchasing power breaks down. When the public awaken to what is happening to fiat money, a mass psychology of rejection takes over to drive the relationship between the currency and its use-value. In France, the mandats territoriaux issued in February 1796 to replace the failing assignats currency were worthless by the following February. In 1923, the German papiermark, which had been losing purchasing power from the end of the Great War took about seven months to finally collapse from May to November. It became a flight into goods and real values that marks the end of a monetary inflation by the complete breakdown of the monetary system.

For a comparison with the contemporary monetary system, which binds together the fate of financial asset values and that of the currency, there is none more apt that that of the failure of John Law’s Mississippi bubble, when he gained control of the French currency and printed it to support the shares of his venture. Law’s policies of inflationism were remarkably similar to those of John Maynard Keynes, which inform the basis of monetary policy today. And today’s neo-Keynesians are unashamedly debasing the currency to support financial assets, just as Law did. Law’s scheme began to show signs of failing in early 1720, and by the following September, not only had the shares in his Mississippi venture collapsed, but his unbacked livres were worthless as well.

If we replicate the John Law experience today, the dollar and all the currencies which sail with her will become worthless in short order, probably by the year-end. We have seen that a final acceleration of monetary inflation is starting after a fifty-year period of debasement which the public has hardly noticed. State-issued fiat currencies are now embarking on that second phase, when they will lose all purchasing power.

The replacement of government fiat money by gold and silver

Now that we can anticipate the final destruction of contemporary fiat currencies, we must consider their replacement and how it comes about. Many commentators who have a grasp of the problem talk of a monetary reset, failing to understand that the problem is a loss of trust in state-issued currencies that cannot be resolved by the issuance of a variation on the fiat theme. Nor can a solution be found in the issuance of a state-issued cryptocurrency. The fact of the matter is the days of financing government spending and economic objectives by monetary expansion are drawing to an end.

A few governments are in a position to back their currencies with gold, freely convertible at the choice of the user at a fixed rate. These include Russia, which has been accumulating gold and dumping dollars in recent years. China, where there is compelling evidence that the state has accumulated significant undeclared bullion, and now that an estimated 17,000 tonnes are in private ownership, could also adopt a gold standard, along with a few other Asian nations. But a gold standard also requires the elimination of government spending deficits, which Russia, China and a few Asian nations could achieve. Additionally, the banking system, whereby bank credit can be expanded by creating loans, must also be reformed. Otherwise, it will be possible for anyone to draw down a loan in unbacked bank credit in order to cash it in for gold. Similarly, safeguards to prevent foreign bank credit expansion being used through the foreign exchanges to acquire gold substitutes for encashment would have to be implemented.

Western nations will find it far more difficult to adjust to a gold standard, having mandated welfare commitments that require continuing currency debasement in order to pay for them. Furthermore, in the United States, the banking cartel is immensely powerful and so long as the fiat system exists, they are unlikely to give up their assumed right to create money out of thin air in the form of credit, particularly when the process becomes more profitable as the dollar’s decline accelerates. The currency will therefore die before radical reform is acceptable to the US financial establishment, and all those that adhere to it.

For individuals, it is safer to assume that personal possession of physical gold and silver bars and coins is best for wealth protection and future spending. It is a mistake to think that these two moneys of millennia are just an investment alternative: they are money which can act as a store of your wealth. They can then be spent on the essentials of life, which are spiralling beyond the reach of failing fiat. And when the return of some economic and political stability can be anticipated, durable assets, such as property, and productive goods might be acquired. In that way gold and silver will return into circulation.

The failure of derivatives

Derivative markets, principally Comex futures and the London bullion market, have expanded to absorb much of the demand for bullion. Taken together, the last recorded figures tell us that gold derivatives in these two markets had a notional value of $600bn, while the sum of annual mine production and recycled scrap at the same time was worth approximately $20bn, a relationship of 30:1.

As argued in this article the acceleration of monetary inflation is collapsing both financial markets and fiat currencies. What no one tells you is that over-the-counter derivatives, which according to the Bank for International Settlements are worth $640 trillion, will also disappear in a fiat currency collapse. Therefore, assuming there is no change in the overall level of demand for gold, thirty times the level of physical demand previously accommodated in derivatives at end-June last year either disappears or will be accommodated in above-ground stocks of gold.

It is in that context we should interpret what is happening in financial markets. The strains at a time of contracting bank credit are acute. If they have not been told already, dealers at the bullion banks will be instructed by their financial controllers to reduce their positions, because of the inexorable pull of contracting bank credit in the bank’s wider lending and deposit activities.

The only avenues for acquiring exposure of gold and silver will be increasingly restricted to bullion itself. Retailer outlets have already been closed by the virus and online retailers have little or no stock. Gold and silver can be acquired through companies such as Goldmoney, so that personal wealth can still be stored in secure, insured vaults. Physically backed exchange-traded funds continue to be available, but with the increasingly certain demise of derivatives, and the problems likely to evolve for the ETFs which use them, ETFs backed by physical gold are also exposed to unforeseen issues.

The hiatus on Comex probably marks the beginning of the end of precious metal derivatives. Already, bullion banks have reduced their exposure on Comex by the equivalent of 938 tonnes to 1,541 tonnes. But with supply substantially reduced from mines and refiners in lockdown at a time when governments are promising unlimited monetary inflation, it is hard to see favourable conditions for an orderly wind-down on Comex.

Conclusion

Events over the last few weeks have alerted a wider audience to the destruction of values in financial markets. The unwritten agreement between investors and the major central banks whereby financial markets will always be supported is now unravelling. Increasingly, the only buyers of government bonds at current levels are the central banks by inflating their currencies.

Meanwhile, liquidity problems in hard-hit economies are mounting. And it is not just the coronavirus; nearly five months before the virus hit Western financial markets the Fed was having to inject liquidity into the US banking system in record amounts through the repo market.

Looking at historical comparisons of our current set of circumstances we find that the Mississippi bubble of 1720 in France appears to be a reasonable template for the current situation. John Law, who masterminded that scheme, gained control of France’s money which he then used to buy shares in his Mississippi venture. Today’s central banks are following a similar path, except on a global scale. Law’s scheme saw both his unbacked currency and the shares in his Mississippi venture collapse from top to bottom in only nine months. If we repeat this experience today, not only will financial markets collapse, but the currencies in which they are notionally measured will be worthless by the year-end.

Signs of failure in some markets, such as derivative markets for precious metals, can be taken as evidence that a wider financial dislocation is now in progress. It is in this light that an understanding of the role of physical gold and silver is so important. They are the only sound money, a safe refuge for ordinary people, being incorruptible by governments. And as their prices rise towards infinity, it will be entirely a reflection of the end of the current fiat money regime.

Drone Delivers Food To Customers In COVID-19 Isolation

A food truck operator in North Carolina has deployed a drone to deliver sandwiches to customers amid the state’s “stay at home” public health order and other strict social distancing measures that have completely changed how business is conducted in these challenging times.

CBS17 Raleigh reports that the folks at CheeseSmith Food Truck deployed a DJI drone to deliver grilled cheese sandwiches to customers.

The idea came one customer who is in quarantine suggested that using a drone for deliveries could be a modern tool to stay within the guidelines of government-enforced social distancing. Here’s a look at how technology is allowing some food truck/restaurants to adapt to strict new rules of how citizens interact in the real economy during a pandemic:

As for the Federal Aviation Administration (FAA) rules for small unmanned aircraft, the food truck operator and drone pilot should read Part 107 of FAA regulations that detail “external loads” and “line of sight.” Maybe they should request a Part 107 waiver before conducting more sandwich drone deliveries. Due in part, if they are breaking FAA rules, the penalty could be severe.

With so many restaurants going bust across the country during the pandemic, CheeseSmith Food Truck is staying busy while it delivers sandwiches via a drone.

he former Supreme Court Justice Jonathan Sumption, QC, has denounced the police response to the coronavirus, saying the country is suffering ‘collective hysteria’.

This is an edited transcript of his interview with BBC Radio 4’s World at One programme earlier today.

BBC interviewer Jonny Dymond

‘A hysterical slide into a police state. A shameful police force intruding with scant regard to common sense or tradition. An irrational overreaction driven by fear.’ These are not the accusations of wild-eyed campaigners, they come from the lips of one our most eminent jurists Lord Sumption, former Justice of the Supreme Court. I spoke to him just before we came on air.

Lord Sumption

The real problem is that when human societies lose their freedom, it’s not usually because tyrants have taken it away. It’s usually because people willingly surrender their freedom in return for protection against some external threat. And the threat is usually a real threat but usually exaggerated. That’s what I fear we are seeing now. The pressure on politicians has come from the public. They want action. They don’t pause to ask whether the action will work. They don’t ask themselves whether the cost will be worth paying.

They want action anyway. And anyone who has studied history will recognise here the classic symptoms of collective hysteria. Hysteria is infectious. We are working ourselves up into a lather in which we exaggerate the threat and stop asking ourselves whether the cure may be worse than the disease.

Dymond

At a time like this, as you acknowledge, citizens do look to the state for protection, for assistance, we shouldn’t be surprised then if the state takes on new powers if it responds. That is what it has been asked to do, almost demanded of it.

Sumption

Yes that is absolutely true. We should not be surprised. But we have to recognise that this is how societies become despotisms. And we also have to recognise this is a process which leads naturally to exaggeration. The symptoms of coronavirus are clearly serious for those with other significant medical conditions, especially if they’re old. There are exceptional cases in which young people have been struck down, which have had a lot of publicity, but the numbers are pretty small. The Italian evidence, for instance, suggests that only in 12 per cent of deaths is it possible to say coronavirus was the main cause of death. So yes this is serious and yes it’s understandable that people cry out to the government.

But the real question is: is this serious enough to warrant putting most of our population into house imprisonment, wrecking our economy for an indefinite period, destroying businesses that honest and hardworking people have taken years to build up, saddling future generations with debt, depression, stress, heart attacks, suicides and unbelievable distress inflicted on millions of people who are not especially vulnerable and will suffer only mild symptoms or none at all, like the Health Secretary and the Prime Minister.

Dymond

The executive, the government, is all of a sudden really rather powerful and really rather unscrutinised. Parliament is in recess, it’s due to come back in late April, we’re not quite sure whether it will or not, the Prime Minister is closeted away, communicating via his phone, there is not a lot in the way of scrutiny is there?

Sumption

No. Certainly, there’s not a lot in the way of institutional scrutiny. The press has engaged in a fair amount of scrutiny, there has been some good and challenging journalism. But mostly the press has, I think, echoed and indeed amplified the general panic.

Dymond

The restrictions in movement have also changed the relationship between the police and those whose, in name, they serve. The police are naming and shaming citizens for travelling at what they see as the wrong time or driving to the wrong place. Does that set alarm bells ringing for you, as a former senior member of the judiciary?

Sumption

Well, I have to say, it does. I mean, the tradition of policing in this country is that policemen are citizens in uniform. They are not members of a disciplined hierarchy operating just at the government’s command. Yet in some parts of the country, the police have been trying to stop people from doing things like travelling to take exercise in the open country, which are not contrary to the regulations, simply because ministers have said that they would prefer us not to. The police have no power to enforce ministers’ preferences, but only legal regulations – which don’t go anything like as far as the government’s guidance. I have to say that the behaviour of the Derbyshire police in trying to shame people into using their undoubted right to take exercise in the country and wrecking beauty spots in the Fells so that people don’t want to go there, is frankly disgraceful.

This is what a police state is like. It’s a state in which the government can issue orders or express preferences with no legal authority and the police will enforce ministers’ wishes. I have to say that most police forces have behaved in a thoroughly sensible and moderate fashion. Derbyshire police have shamed our policing traditions. There is a natural tendency of course, and a strong temptation for the police to lose sight of their real functions and turn themselves from citizens in uniform into glorified school prefects. I think it’s really sad that the Derbyshire police have failed to resist that.

Dymond

There will be people listening who admire your legal wisdom but will also say ‘well, he’s not an epidemiologist, he doesn’t know how disease spreads, he doesn’t understand the risks to the health service if this thing gets out of control’. What do you say to them?

Sumption

What I say to them is I am not a scientist but it is the right and duty of every citizen to look and see what the scientists have said and to analyse it for themselves and to draw common sense conclusions. We are all perfectly capable of doing that and there’s no particular reason why the scientific nature of the problem should mean we have to resign our liberty into the hands of scientists. We all have critical faculties and it’s rather important, in a moment of national panic, that we should maintain them.

Dymond

Lord Sumption, former Justice of the Supreme Court, speaking to me earlier. We put his criticism of Derbyshire police to the force and they sent us this statement: ‘Our advice to the public was in line with national government instruction and echoed what people in our communities were saying following thousands of people that travelled to the Peak District National Park the previous weekend. The weekend just gone saw much smaller numbers and we thank the public for their response.’

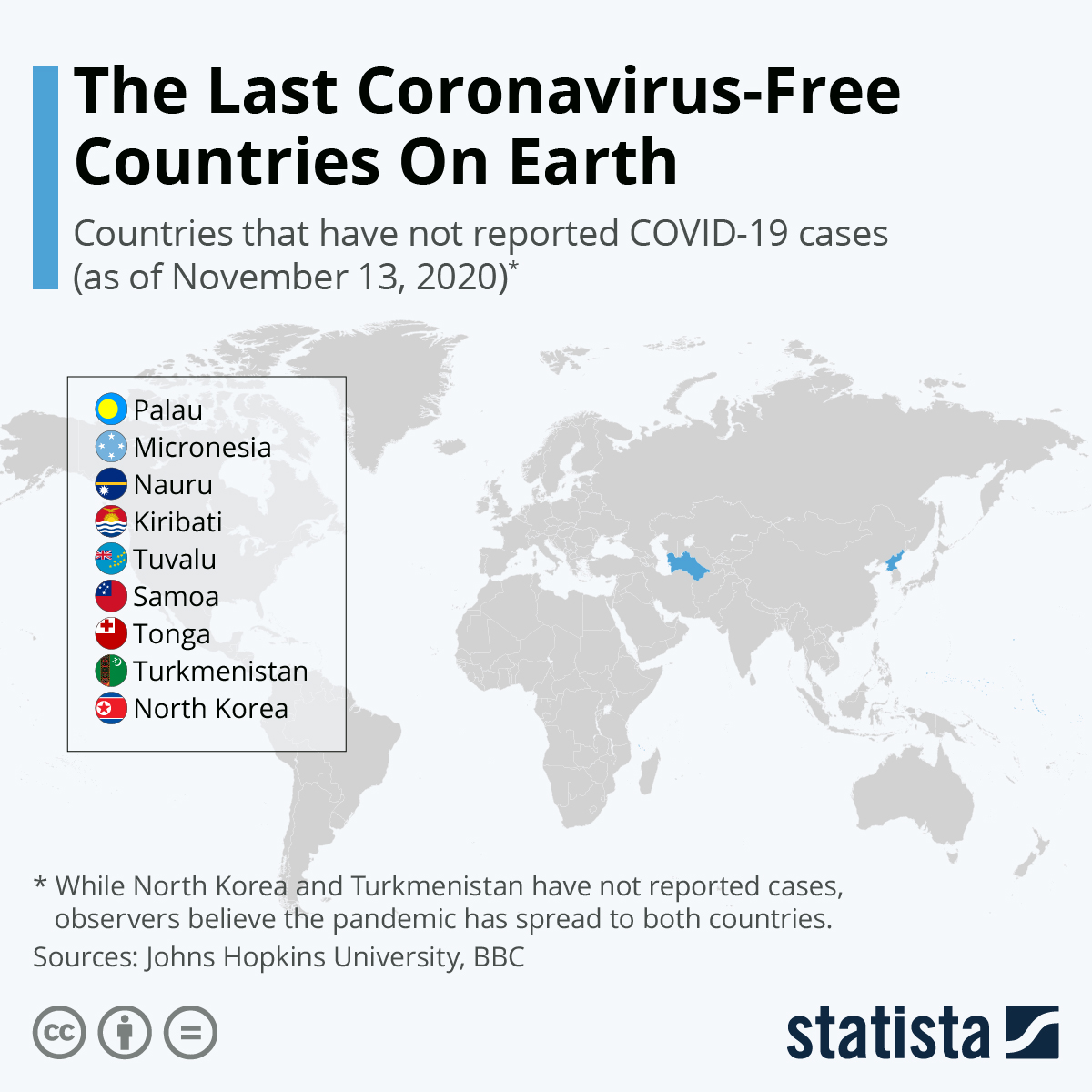

Want To Escape? These Are The Countries That Have Escaped COVID-19 So Far?

The COVID-19 pandemic has spread to all corners of the globe and the following infographic shows the last places on Earth remaining unaffected.

It is based on countries that have not reported any known COVID-19 cases and that remained absent from the extensive global tracking carried out by the Johns Hopkins University as of March 31, 2020.

As Statista’s Niall McCarthy notes, however, there are certainly question marks regarding the true situation in some countries, particularly North Korea, with sources in South Korea claiming COVID-19 has indeed spread there via the Chinese border. Due to the secretive nature of the government in Pyongyang and the degree of state control over the media, it is impossible to tell whether the South Korean claims are true. However, it is also not unreasonable to think that in this instance, North Korea’s isolation from the rest of the world is helping it largely avoid the pandemic. Myanmar, another secretive country, was on the first version of this map but it has now reported its first case of COVID-19.

Several countries in Africa are still saying that they have no COVID-19 cases, though again this could be due to a lack of testing capacity on the ground. As of March 30, Botswana, Burundi, the Comoros, Malawi, Sao Tome and Principe, Sierra Leone and South Sudan were the African countries still to report a confirmed case.

The virus also remains mostly undetected in the smaller Pacific island nations such as the Solomon Islands and Vanuatu.

As the coronavirus rages across Europe, a growing number of countries are reporting that millions of pieces of medical equipment donated by, or purchased from, China to defeat the pandemic are defective and unusable.

The revelations are fueling distrust of a public relations effort by Chinese President Xi Jinping and his Communist Party to portray China as the world’s new humanitarian superpower.

On March 28, the Netherlands was forced to recall 1.3 million face masks produced in China because they did not meet the minimum safety standards for medical personnel. The so-called KN95 masks are a less expensive Chinese alternative to the American-standard N95 mask, which currently is in short supply around the world. The KN95 does not fit on the face as tightly as the N95, thus potentially exposing medical personnel to the coronavirus.

More than 500,000 of the KN95 masks had already been distributed to Dutch hospitals before the recall was enacted.

“When the masks were delivered to our hospital, I immediately rejected them,” a hospital worker told the Dutch public broadcaster NOS.

“If those masks do not seal properly, the virus particles can simply pass through. We cannot use them. They are unsafe for our people.”

In a written statement, the Dutch Ministry of Health explained:

“A first shipment from a Chinese manufacturer was partly delivered last Saturday. These are masks with a KN95 quality certificate. During an inspection this shipment was found not to meet our quality standard. Part of this shipment had already been delivered to healthcare providers; the rest of the cargo was immediately withheld and not further distributed.

“A second test also showed that the masks did not meet our quality standard. It has now been decided that this entire shipment will not be used. New shipments will undergo additional tests.”

The Dutch newspaper NRC Handelsbladreported on March 17 that the Netherlands had only a few days’ supply of masks: “All hope is now for that one cargo plane from China on Wednesday.” The substandard quality of the masks delivered by China has left the Netherlands shattered. A spokesperson for a hospital in Dutch city of Eindhoven said that Chinese suppliers were selling “a lot of junk…at high prices.”

In Spain, meanwhile, the Ministry of Health on March 26 revealed that 640,000 coronavirus tests that it had purchased from a Chinese vendor were defective. The tests, manufactured by Shenzhen Bioeasy Biotechnology Company in Guangdong province, had an accurate detection rate of less than 30%.

On April 2, the Spanish newspaper El Mundoreported that it had been presented with leaked documents which showed that Bioeasy had lied to the Spanish government about the accuracy of the tests. Bioeasy had claimed, in writing, that its tests had an accurate detection rate of 92%.

Also on April 2, the Spanish government revealed that a further million coronavirus tests delivered to Spain on March 30 by another Chinese manufacturer were also defective. The tests apparently required between five and six days to detect whether a patient is infected with coronavirus and were therefore useless to diagnose the disease in a timely manner.

On March 25, the Spanish government announced that it had purchased medical supplies from China in the amount of €432 million ($470 million), and that Chinese vendors demanded that they be paid up front before the deliveries were made. Spanish Health Minister Salvador Illa explained:

“We have bought and paid for 550 million masks, which will start arriving now and will continue to arrive for the next eight weeks. 11 million gloves will arrive in the next five weeks. As for rapid tests, we have acquired 5.5 million for the months of March and April. In addition, we will receive 950 respirators during the months of April to June. We are managing the purchase of more equipment.”

It is not at all clear how the Spanish government will be able to guarantee the quality of these new mass purchases, or how it would obtain compensation if the products from China were again substandard.

On March 28, the French government, which apparently has only a few weeks’ worth of supplies, announced that it had ordered more than one billion face masks from China. It is unclear whether the quality control problems experienced by other European countries would affect France’s purchasing plans.

Other countries — in Europe and beyond — have also criticized the quality of Chinese medical supplies:

Slovakia. On April 1, Prime Minister Igor Matovič said that more than a million coronavirus tests supplied by China for a cash payment of €15 million ($16 million) were inaccurate and unable to detect COVID-19. “We have a ton of tests and no use for them,” he said. “They should just be thrown straight into the Danube.” China accused Slovakian medical personnel of using the tests incorrectly.

Malaysia. On March 28, Malaysia received a consignment of medical equipment donated by China, consisting of test kits, medical face masks, surgical masks and other personal protective equipment. A senior official in the Ministry of Health, Noor Hisham Abdullah, said that the test kits would be evaluated for accuracy after previous test kits from China were found to be defective: “This is a different brand from the one we tested earlier. We will assess the new test kit which is FDA-approved. I was assured by the Chinese ambassador that this is more accurate than the other one we tested.” Abdullah previously stated that the accuracy of the Chinese tests was “not very good.”

Turkey. On March 27, Turkish Health Minister Fahrettin Koca said that Turkey had tried some Chinese-made coronavirus tests but authorities “weren’t happy about them.” Professor Ateş Kara, a member of the Turkish Health Ministry’s coronavirus task force, added that the batch of testing kits were only 30 to 35% accurate: “We have tried them. They don’t work. Spain has made a huge mistake by using them.”

Czech Republic. On March 23, the Czech news site iRozhlasreported that 300,000 coronavirus test kits delivered by China had an error rate of 80%. The Czech Ministry of Interior had paid $2.1 million for the kits. On March 15, Czech media revealed that Chinese suppliers had swindled the Czech government after it paid upfront for the supply of five million face masks, which were supposed to have been delivered on March 16.

On March 30, China urged European countries not to “politicize” concerns about the quality of medical supplies from China. “Problems should be properly solved based on facts, not political interpretations,” Foreign Ministry spokeswoman Hua Chunying said.

On April 1, the Chinese government reversed course and announced that it was increasing its oversight of exports of coronavirus test kits made in China. Chinese exporters of coronavirus tests must now obtain a certificate from the National Medical Products Administration (NMPA) in order to be cleared by China’s customs agency.

Meanwhile, the Chinese telecommunications giant Huawei announced that it would stop donating masks to European countries as a result of allegedly derogatory comments by the EU Foreign Policy Chief Josep Borrell.

On March 24, Borrell had written in a blog post that China was engaging in a “politics of generosity” as well as a “global battle of narratives.”

On March 26, a Huawei official told the Brussels-based news service Euractiv that due to Borrell’s comments, the company would be ending its donation program because it did not want to become involved in a geopolitical power play between the U.S. and China.

On March 28, Huawei paid for sponsored content in the publication Politico Europe. Huawei’s Chief Representative to the EU, Abraham Liu, wrote:

“Let me be clear — we have never sought to gain any publicity or favor in any country by what we are doing. We made a conscious decision not to publicize things. Our help is not conditional and not a part of any business or geopolitical strategy as some have suggested. We are a private company. We are trying to help people to the best of our abilities. That’s all. There is no hidden agenda. We don’t want anything in return.”

On March 30, the BBC reported that Huawei was acting as if nothing had really changed since the coronavirus crisis began:

“That may be naive on the company’s part. While nothing has really changed when it comes to the technical and security issues around Huawei’s equipment, the political climate for the company has certainly worsened.

“A story in the Mail on Sunday at the weekend had Downing Street warning China ‘faced a reckoning’ over its handling of the coronavirus.

“And that is likely to embolden those MPs who have been telling the government no Chinese company should be allowed a role in the UK’s vital infrastructure.”

On March 29, the British newspaper Daily Mailreported that British Prime Minister Boris Johnson and his allies in parliament had “turned” on China because of the coronavirus crisis:

“Ministers and senior Downing Street officials said the Communist state now faces a ‘reckoning’ over its handling of the outbreak and risks becoming a ‘pariah state.’

“They are furious over China’s campaign of misinformation, attempts to exploit the pandemic for economic gain and atrocious animal rights abuses blamed by experts for the outbreak.”

On January 28, Johnson had granted Huawei a role in Britain’s 5G mobile network, frustrating efforts by the United States to exclude the company from the West’s next-generation communications, which, it seems, can also be used for spying. The London-based Financial Timesreported that U.S President Donald J. Trump vented “apoplectic fury” at Johnson in a tense phone call. Johnson is now facing pressure from his Cabinet as well as from Members of Parliament to reverse his decision.

After Chinese officials blamed the United States and Italy for starting the coronavirus pandemic, the Daily Mailquoted a British government source as saying:

“There is a disgusting disinformation campaign going on and it is unacceptable. They [the Chinese government] know they have got this badly wrong and rather than owning it they are spreading lies.”

“Mr. Johnson has been warned by scientific advisers that China’s officially declared statistics on the number of cases of coronavirus could be ‘downplayed by a factor of 15 to 40 times.’ And No. 10 believes China is seeking to build its economic power during the pandemic with ‘predatory offers of help’ to countries around the world.

“A major review of British foreign policy has been shelved due to the Covid-19 outbreak and will not report until the impact of the virus can be assessed. A government source close to the review said: ‘It is going to be back to the diplomatic drawing board after this. Rethink is an understatement.’

“Another source said: ‘There has to be a reckoning when this is over.’ Yet another added: ‘The anger goes right to the top.’

“A senior Cabinet Minister said: ‘We can’t stand by and allow the Chinese state’s desire for secrecy to ruin the world’s economy and then come back like nothing has happened. We’re allowing companies like Huawei not just into our economy, but to be a crucial part of our infrastructure.”

In an article published by The Mail on Sunday on March 29, former Tory Party leader Iain Duncan Smith wrote:

“All issues can and will be discussed, except for one, it seems — our future relationship with China.

“The moment anyone mentions China, people shift uncomfortably in their seats and shake their heads. Yet I believe it is vital that we start to discuss how dependent we have become on this totalitarian state.

“For this is a country which ignores human rights in the pursuit of its ruthless internal and external strategic objectives. However, such facts seem to have been swept aside in our rush to do business with China.

“Remember how George Osborne [Chancellor of the Exchequer under Prime Minister David Cameron from 2010 to 2016] made our relationship with China a major plank of UK Government policy? So determined were Ministers to increase trade that they were prepared to do whatever was necessary.

“Indeed, I am told that privately this was referred to as Project Kow-Tow — a word defined by the Collins dictionary as ‘to be servile or obsequious.’

“We were not alone. Countless national leaders over recent years have brushed aside China’s appalling human rights behavior in the blind pursuit of trade deals with Beijing….

“Thanks to Project Kow-Tow, the UK’s annual trade deficit with China is £22.1 billion ($27.4 billion). But we are not alone in being in hock to Beijing.

“For China has racked up a global trade surplus of £339 billion ($420 billion). Distressingly, the West has watched as many key areas of production have moved to China….

“The brutal truth is that China seems to flout the normal rules of behavior in every area of life — from healthcare to trade and from currency manipulation to internal repression.

“For too long, nations have lamely kowtowed to China in the desperate hope of winning trade deals.

“But once we get clear of this terrible pandemic, it is imperative that we all rethink that relationship and put it on a much more balanced and honest basis.”

Trump Fires Ukrainegate Inspector General Who Helped Initiate Impeachment

President Trump on Friday fired the intelligence community inspector general, Michael Atkinson, who brought a hearsay whistleblower complaint to Congressional Democrats, kicking off President Trump’s impeachment.

Atkinson’s closed-door testimony was so troubling to House Republicans that they launched an investigation into his role into what President Trump and his allies coined the ‘impeachment hoax.’

Ranking member of the House Intelligence Intelligence Committee Devin Nunes (R-CA) told SarahCarter.com that transcripts of Atkinson’s secret testimony would expose that he either lied or needs to make corrections to his statements to lawmakers.

Trump notified the Senate and House Intelligence Committees of his decision to fire Atkinson, according to Politico, citing two congressional officials and a copy of a letter dated April 3.

“This is to advise that I am exercising my power as president to remove from office the inspector general of the intelligence community, effective 30 days from today,” wrote Trump, who added that he “no longer” has the fullest confidence in Atkinson.

“As is the case with regard to other positions where I, as president, have the power of appointment, by and with the advice and consent of the Senate, it is vital that I have the fullest confidence in the appointees serving as inspectors general,” Trump wrote. “That is no longer the case with regard to this inspector general.”

Trump knocked Atkinson on January, noting that House Intelligence Committee Chairman Adam Schiff’s (D-CA) decision to withhold Atkinson’s testimony was a “major problem.”

….the Ukraine Hoax that became the Impeachment Scam. Must get the ICIG answers by Friday because this is the guy who lit the fuse. So if he wants to clear his name, prove that his office is indeed incompetent.” @DevinNunes@MariaBartiromo@FoxNews The ICIG never wanted proof!

Democrats had a fit at the news, with Senate Intelligence Committee Vice Chairman Mark Warner (D-VA) calling Atkinson’s firing “unconscionable” while accusing Trump (with a straight face?) of an ongoing effort to politicize intelligence.

“In the midst of a national emergency, it is unconscionable that the president is once again attempting to undermine the integrity of the intelligence community by firing yet another intelligence official simply for doing his job,” wrote Warner in a statement.

Warner’s House counterpart, Intelligence Committee Chairman Adam Schiff (D-CA) called Atkinson’s firing “retribution” in the “dead of night” – adding that it’s “yet another blatant attempt by the president to gut the independence of the intelligence community and retaliate against those who dare to expose presidential wrongdoing.”

Senate Minority Leader Chuck ‘six ways from Sunday’ Schumer (D-NY) said Atkinson’s firing was evidence that Trump “fires people for telling the truth,” according to Politico.

Whistleblower lawyer and Disneyland aficionado Mark Zaid – who once bragged about getting security clearances for pedophiles, called the firing “delayed retaliatory action” for Atkinson’s “proper handling of a whistleblower complaint.”

“This action is disgraceful and undermines the integrity of the whistleblower system,” said Zaid. “It is time GOP members of the Senate stand up for the rule of law and speak out against this president.”

The whistleblower complaint effectively kicked off the House’s impeachment inquiry, which began in late September amid allegations that Trump had solicited foreign interference in the 2020 election when he asked Ukraine’s president to investigate his political opponents, including Joe Biden.

Atkinson opposed the decision by then-acting director of national intelligence Joseph Maguire to withhold the whistleblower complaint from the House and Senate intelligence committees — in particular, Maguire’s decision to seek guidance on the issue from the Justice Department, rather than turn it over to Congress as required by law. –Politico

The rush to what is essentially a new wartime footing began consciously and urgently in the first quarter of 2020 between some of the most powerful geopolitical players of the modern era: the United States of America, the People’s Republic of China (PRC), and the United Kingdom.

It was not about the “battle” to cope with the COVID-19 (coronavirus) epidemic, or the global fear pandemic which it engendered, but those contagions broke the cycle of globalism and the belief in the indissoluble nature of interdependence. It allowed what was already emerging as a fundamental move toward a new, bipolar global competition to come out into the open.

By the end of March 2020, the global framework had changed sufficiently to become — behind the headlines about COVID-19 — about which system and ideology would triumph in the decades after the watershed. That meant a race by each of the major antagonists to determine how quickly national productivity could be resumed.

Even so, the failure of most major societies, including the PRC, to prepare for health pandemics, natural disasters, and associated contagions of fear was a significant function of the transformed realities of the “globalist”-dominated political structures over the earlier lessons of national self-reliance. I made this point in a report in Defense & Foreign Affairs Special Analysis on November 24, 2008:

The unintended, or unforeseen, consequences of economic dislocation — as this writer has repeatedly noted — can be expected to lead to a rise in globalized (or at least regionalized) pandemic health challenges at a time when societies are weakened. These will lead to wealthier societies becoming more nationalistic and isolated, in some respects, merely to protect themselves. Pandemics will be matched by similar anomic social responses, including rising crime, of which the new era of maritime piracy is merely one aspect

Indeed, it is clear that the best avenue which nation-states can take is one marked by gaining as much control over their own destinies as possible. That requires a growing focus on domestic food self-sufficiency, and domestic market bases for manufactured goods and services. In other words: a return to a sense of the nation. The age of globalization is ending; it was a brief window in which the technologies which were created to fight the Cold War became the technologies of global social integration. Now, again, the luxury of internationalism is ending, and survival is based around the extended clan: the nation.

It was a year later that the global H1N1 pandemic emerged, fortunately without triggering the associated fear pandemic which acted as a force multiplier to the impact of the 2019-20 COVID-19 epidemic.

By 2020, a dozen years later, the transformed strategic landscape meant that information dominance (ID) warfare was far more enabled, particularly as social media evolved as a conduit for mass mobilization to force government actions in Western societies. So there was a general transformation in the social and technological context which prevailed when the panic arose around COVID-19.

But, in order to gain the post-epidemic political high ground, the PRC was first to “declare victory” in managing the COVID-19 epidemic and to send its population back to work, despite the reality of evidence which defied the national statistics on the continuing levels of contagion in the PRC. However, it was clear that the epidemic, having its origins in Wuhan in the PRC, would peak first and begin to recover first. Still, it was the degree of top-down control which PRC Pres. Xi Jinping enjoyed — in contrast to Western heads of government — which enabled the PRC to “declare victory”, and to resume his offensive against the West in a now fairly blatant fashion.

Even so, it was clear that the overall nature of the restructured strategic balance would be less affected by a few weeks (or even months) in the battle to restart economic activity than by underlying fundamentals in systems. Meanwhile, as the information dominance (ID) wars between the PRC and (particularly) the US ramped up, both sides were careful to ensure that the risk of actual physical challenge was minimized.

What were some of the fundamental immediate outcomes and questions raised by the 2020 Fear Pandemic?

1. The global economy and the economies of most states have been dramatically weakened, and they will remain relatively weakened and transformed for some years; in many cases for decades. This means that economic deprivation will reach more pervasively down into the mass of society, reversing the trend of the past seven decades. It will exacerbate the polarization of societies, but seems likely to push the trend toward forms of nationalism more than it will reinforce the ideology of globalism;

2. The power of central governments has been dramatically increased, and the rights and freedoms of individuals constrained. By late March 2020, the situation in most Western societies had approached a quasi-martial law environment, with little social resistance;

3. Funding for R&D, national security, and consumer spending will decline, further exacerbated by the reduction in core size/wealth of most populations in advanced economies. The question is whether the limitation in wealth will exacerbate or constrain inflammatory populism and social action;

4. The role of global bodies has been weakened, as have alliances. This will lead to a rethinking of alliance structures and how to manage them. It will, even if only for reasons of fiscal constraints, lead to an increasing momentum toward the bilateralization of trade, even to the point, once again of thinking in terms of structured barter or counter-trade dealings;

5. The reach of formal military structures will be inhibited by funding, and will this open seams in the global power framework? Will it allow space for more independent, regional actions?;

6. While the Communist Party of China (CPC) probably has the strength to enforce control over the People’s Republic of China (PRC), will the European Union (EU) have sufficient cohesion to enforce control over its member states? If the EU cannot “hold it together”, would this create a space for Turkey to revive its neo-Ottomanist expansions in the Eastern Mediterranean and Balkans? Did the United Kingdom escape from the EU just in time to preserve its economic base? Did the EU’s poor handling of the crisis end forever the chance of bringing Serbia into the Union? And what will this new dynamic do for the encouragement of separate geopolitical alignments, such as the creation of the Three Seas Initiative as a potentially viable successor to part of the EU? Can Three Seas gain traction if Serbia is excluded, given its regional hub importance for the north-south infrastructural needs of the Alliance?;

7. What skills will be necessary in the post-2020 environment? Has the economy sobered enough to embrace the restoration of practical skills training instead of ideological education which has no market, while an impetus toward revived domestic manufacturing (rather than foreign-sourced manufacturing) will see significant demand for trained personnel?;

8. There was a widespread belief that the crisis had caused a collapse in petroleum and gas prices to the point where the US domestic shale industry would be forced from the marketplace, re-opening the US to the need for imported energy. But this is likely both untrue and irrelevant, and the US would remain considerably less vulnerable to energy exposure than the PRC;

9. The PRC would continue to see extreme vulnerability to food and water shortages, which can only be ameliorated by (a) dependence on imported food and agricultural products, most of which would need to come from the United States (given that other suppliers cannot meet the demand), and (b) reduction in the lifestyles and numbers of the PRC population, a factor which could have significant social-political ramifications;

10. The longer the constraints on societies imposed by the crisis, the more pro-found were the likely post-crisis attitude changes likely to be. In other words, if the crisis lingered in various forms through 2020, it was likely that the year would be seen by society and historians as a breakpoint equivalent to the world wars of the 20th Century;

11. Nowhere in the world have we seen the development of economic theories or approaches to managing societies in decline in terms of economics as well as in terms of the downward transformation of market size and demand. Studies of recent-term lessons from Japan, Russia, and Germany would be helpful, even though these examples all predicated their economic thinking — despite market size decline — on growth in economic opportunity, but with notable shortcomings;

12. Africa, which had moved from a Continent gradually modernizing within the framework of a Western model to one dependent almost solely on the PRC, was likely to be left in an almost ruinous situation by late 2020 and beyond. African societies would themselves be forced to evolve new economic models. There was a likelihood that the US would strongly move, in the post-crisis period, to strengthening its dominance in the Americas (where the PRC, in particular, had built a strong presence), and also in Central Asia, as a means of providing an alternate path in the Eurasian Silk Road complex.

The COVID-19 pandemic will do little to impact the demographic trends in global population numbers. The trend toward population decline was set in place in the second half of the 20th Century and is only now becoming evident. Similarly, the disruption to the global economy also began before the COVID-19 crisis, largely as a result of the global demographic transformation, but the 2020 crisis became an iconic breakpoint.

The post-COVID-19 world would thus be markedly different, structurally, than the world which preceded it. But most significantly, the perception of that “new” world would have changed, ensuring that a linear extrapolation of older remedies or progressions of earlier thinking would no longer be acceptable.

It is important to stress that the two underlying strategic trends impacting the US-PRC competition had begun well before the 2020 pandemic scares. The PRC economy had been essentially in decline for several years, disguised by ongoing state-sponsored investments in infrastructure projects, which boosted the appearance of growth in the gross domestic product (GDP). Moreover, the PRC’s water shortage and quality problems had reached almost panic levels over that same timeframe.

In a talk in Perth, Western Australia, on October 23, 2019, I noted:

[The PRC] has almost 20 percent (18.4 percent) of the world’s population, and yet only seven percent of its water, and of that water some 25 percent, at least [as the PRC Government acknowledges], is polluted, along with much of its agricultural water table [to a far greater degree than the PRC Govt. acknowledges]. And the problem is getting worse. The great water source, the aquifers flowing from the melting snows of the Tien Shan Mountain range in Central Asia, is reducing for the moment.

The result of this, and the fact that Chinese agriculture has not modernized to any great degree, is that the People’s Republic of China is perhaps more strategically dependent on imported food than any great power since Rome. And Rome, arguably, collapsed, finally, for that very reason: its foreign sources of food became less dependable. The PRC Bureau of Statistics in the 1980s recorded that there were some 50,000 rivers in mainland China. But by 2017, there were only some 23,000. Beijing, serviced by the so-called “Three Gorges Dam”, recorded in 2017 that 39.9 percent of its water was so polluted as to be unusable. Tianjin, a principal port city of the north (and with a population of 15-million), had only 4.9 percent of its water in a potable state.

The growing urbanization of the constituent populations of the PRC have made the food and water crises more and more urgent. Urban populations use far more water than rural societies. They also demand more water-intensive food, such as pork and beef, especially as the city-dwellers become more prosperous. And the PRC’s urbanization rate continues apace: by the end of 2017, some 58.52 percent of its population was urbanized, compared with only 17.92 percent in 1978.

You can see where this is going. And we have not even touched on the impact of air quality on health in the PRC, or the fact that urban-related diseases, such as diabetes, are rising at a higher rate than in other industrial economies; or the fact that a rapidly-aging population is transforming the economic viability of the state.

And by late 2019, it became clear that the PRC was unable to continue the pursuit of military equivalence with the US. Minnie Chan, writing in The South China Morning Post on November 28, 2019, noted that the PRC Government had canceled plans for the People’s Liberation Army-Navy (PLAN) to build two nuclear-power very large aircraft carriers to compare with the capability of US carriers. The PLAN has two carriers afloat with two more abuilding; all conventionally-powered. The reasons for the cancelations of the prestige super-carrier program were cited as “technical challenges and high costs”.

The PRC has significant technologies which had briefly leapfrogged the US, particularly in the areas of hypersonic weapons and space, but belatedly a more resilient US economy was beginning to redress the years of neglect by all US presidents between Pres. Ronald Reagan (1981-89) and Pres. Donald Trump (2017- ). The US was slowly beginning to compensate for the sense of smugness and hubris which pervaded its global thinking after the end of the Cold War in 1990.

But the US had, along with most European powers, subcontracted most of its manufacturing to the PRC in the post-Cold War era, and the COVID-19 epidemic — and the US-PRC “trade war” which immediately preceded it (and which was likely to resume significantly in late 2020) — saw the extent of global dependence on mainland China factories. Beijing was counting on this dependence to restart its economic push in the second quarter of 2020.

But will that manufacturing/export revival be sufficient to restart the PRC economy, which was essentially already hollowed out?

And was the US (and Western) dependence on the PRC manufacturing sector likely to be the same as pre-COVID-19? Unlikely, given the reality that global demand would have declined substantially for at least the remainder of 2020 because of the economic impact of the crisis, and because a number of efforts to restore domestic manufacturing of key products had already begun in the US, Canada, Australia, the UK, and the like.

Moreover, the weakness of the PRC position, economically, seems to be borne out by the understanding that it had made dramatic cuts in the first quarter of 2020 to its investment in its Belt & Road Initiative (BRI) global supply chain. BRI had, in its origins, been conceived merely as a material and transactional form of maoist globalist ideology; a way to bind foreign states to the PRC as “tributary” states and to provide the PRC with its resource needs and markets. But most of the BRI contracts and loans to foreign states had not been calculated on a realistic market basis.

Reports from Beijing indicated that funding for BRI projects had dropped in early 2020 by some 80 percent over the same period a year earlier. But some of these cuts were already well underway by the time the COVID-19 crisis struck.

The Hong Kong-based newspaper, The South China Morning Post, reported on October 10, 2019, that investment in BRI had begun to drop in 2018. It noted: “The value of new projects across 61 countries fell 13 percent to US$126-billion in 2018 [compared with the previous year], with the figure falling further in 2019.” In fact, it said that investment had fallen a further 6.7 percent in the seven months leading up to August 2019, and existing contracts were reduced by 4.2 percent in the first eight months of 2019.

The Post article continued: “[I]n the first half of 2019, China’s investment and construction activity around the world plunged by over 50 percent compared to the first half of 2018, while new projects under the belt and road plan dropped sharply, according to a report published in July by Derek Scissors, resident scholar at the China Global Investment Tracker from the American Enterprise Institute. Scissors said Chinese SOEs were still moving car and steel capacity overseas and building new motorways and cement plants in developing economies, but that is now “on a smaller scale” compared to the 2016 investment peak.”

The cutbacks were not only caused by Beijing. By late 2019 and early 2020, a significant number of major programs in the BRI which had received commitments from foreign countries were canceled or scaled-back. These were particularly evident in Pakistan (which has a major strategic need to depend on Beijing), Malaysia, Myanmar, Bangladesh, and Sierra Leone. The arrival of the new Government in Ethiopia in April 2018 had already seen that country sour on involvement with new BRI projects.

To a degree, all this decline in the PRC’s economic reach was likely to see the PRC attempt to regain global market share by dumping of goods onto the global marketplace in a bid to ensure that nationalistically-oriented commitments in the US, Europe, Australia, and the like did not attempt to rebuild their own manufacturing sectors. So the response by client states to PRC attempts to recapture markets and prevent the rise of national or sovereign independence would be a measure as to how much Western leaders learned from the crisis period of early 2020.

For this reason, strategically, it was critical for the Communist Party of China (CPC) to ensure that US Pres. Donald Trump was not re-elected to the US Presidency on November 3, 2020, and that the Democratic Party in the US would strengthen its position in the US Congress. As a result, the CPC’s information dominance warfare against the US was geared specifically toward the downfall of Pres. Trump, and in this it sought to enlist the support of the anti-Trump sections of the US polity. There were clearly some elements of the US political community which were prepared to align with Beijing — albeit not overtly — in order to ensure the removal of Donald Trump and the ascendance of Democratic Party presumed candidate Joe Biden.