Starbucks apologized for an incident that happened on Dec. 12, where two Californian police officers were denied service, according to multiple reports.

The incident happened at a Starbucks located in Riverside, according to a tweet from the Riverside County Sheriff’s Department. In the tweet, the Sheriff’s Department wrote, “we are aware of the ‘cop with no coffee’ incident that occurred in Riverside on 12/12/19 involving our @RSO deputies. We are in communication with [Starbucks] Corporate addressing the issue of deputies being denied service.”

The Riverside County Sheriff Chad Bianco was also made aware of the incident, and in a tweet regarding the incident, he wrote, “Two of our deputies were refused service at Starbucks. The anti-police culture repeatedly displayed by Starbucks employees must end.”

According to the Los Angeles Times, the police officers stood at the ordering counter and were ignored for five minutes; after a long wait, the police officers left the establishment.

A spokesperson for Starbucks, Reggie Borges, apologized for the treatment of the two deputies, according to a statement, Los Angeles Times reported. According to the statement, he said:

“there is simply no excuse for how two Riverside deputies were ignored for nearly 5 minutes at our store on [the evening of Dec. 12]. We take full responsibility for any intentional or unintentional disrespect shown to law enforcement on whom we depend on every day to keep our stores and communities safe.”

According to the statement, Borges also said that Starbucks was very sorry for the incident and have reached out to the two deputies who were affected and apologized directly to them, ABC 7 News reported.

The news outlet also reported that the employees in question would not be working while the investigation into the incident is being conducted, and the company will be taking the “appropriate steps” into resolving this problem.

According to Business Insider, this wasn’t the first time police officers were refused service. Back in July 2019, six police officers entered a Starbucks in Tempe, Arizona. They were asked to leave by one of the baristas after a customer complained about not feeling safe in the presence of police officers.

Following this incident, Rossann Williams, the Starbucks Executive Vice President, released an apology to the police department, which stated that the officers “should have been welcomed and treated with dignity and the utmost respect by our [employees],” according to Business Insider.

Just four months later, on Thanksgiving in November 2019, another incident occurred. Officers were picking up their coffees but were appalled to see the word “pig,” written each of the five cups, according to Business Insider.

Again, Starbucks issued another apology following the November incident, saying that the actions were “absolutely unacceptable.”

Fed’s Emergency Repo Operation Oversubscribed As Repo Rates Spike To December High

Ahead of today’s massive liquidity drain, which according to some calculations will be as much as $100 billion between $54BN in coupon settlements from last week’s Treasury auctions and an additional $50 billion or so in corporate income tax payments to the Treasury…

… which combined would be as large, if not bigger than the Sept 16 cash transfer to the Treasury which sparked the mid-September repo crisis, last Thursday the Fed announced a “kitchen sink” liquidity tsunami, throwing as much as $500 billion in liquidity backstops in the form of expanded and extended repo and term repo operations, while keeping the Fed’s “Not QE” T-Bill monetization chugging along.

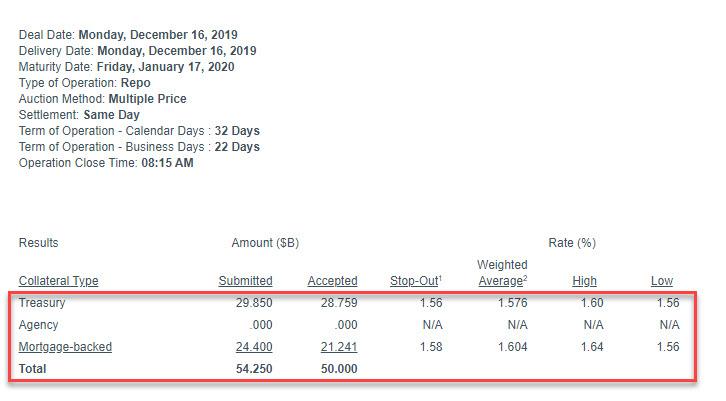

The first of these emergency repo operations was scheduled for this morning, ahead of the liquidity drain, in the form of a $50 billion, 32-day repo, which took place shortly after 8am, and was once again oversubscribed as there was more demand for liquidity, or $54.25 billion, than there was total supply.

Specifically, Dealers submitted $29.850BN in Treasury securities, and $24.4BN in MBS, at stop out rates of 1.56% and 1.58%, respectively, and which both came in more than fully subscribed relative to the $28.759BN in TSYs, and $21.241BN in MBS accepted.

This offering, which matures on January17, 2020, was the fourth “turn” repo providing funding past the year-end period.

The fact that the operation was oversubscribed was the first indication that banks are once again reserve-constrained and scrambling to procure as much year-end liquidity as they can get their hands on. Whether repo operations in the coming days are oversubscribed will indicate if the Fed’s roughly $500 billion in repo ops scheduled for the next 4 weeks will be enough to keep the Fed from losing control over overnight rates, as Credit Suisse repo expert Zoltan Pozsar predicted last week in his now infamous “Countdown to QE4” report.

One ominous sign: the overnight G/C repo rate spiked from 1.58% on Friday to 1.69% this morning, the highest print since the end of the November, and the clearest indication yet that despite throwing a kitchen sink of liquidity in the market, some dealers and banks are still having problems getting access to much needed liquidity.

Keep an eye on the repo rate over the next few hours for an indication if today’s $100 billion liquidity drain will overpower the Fed’s preemptive liquidity tsunami, in effect triggering Zoltan Pozsar’s worst-case scenario.

Obama Says Women Are “Indisputably Better” Than Men, And Should Lead Every Country

Are President Obama and his wife having some kind of lover’s quarrel?

Speaking at a private event in Singapore on Monday, President Obama said that if women ran every country, we would all live with significantly improved living standards and there would be less war and strife. When it comes to leadership, women are “indisputably better” than men, Obama said, according to the BBC, which was apparently invited to the event.

Most of the world’s problems, Obama said, stem from too many old men in positions of power, an obvious slight directed at President Donald Trump, though he wasn’t explicitly named.

Although they’re not perfect, women are so much more advanced and even-headed than men, that Obama believes if women were given two years running every country on earth, all of our problems would be fixed.

“Now women, I just want you to know; you are not perfect, but what I can say pretty indisputably is that you’re better than us [men].”

“I’m absolutely confident that for two years if every nation on earth was run by women, you would see a significant improvement across the board on just about everything…living standards and outcomes.”

When asked if he would ever consider going back into political leadership, he said he believed in leaders stepping aside when the time came.

“If you look at the world and look at the problems it’s usually old people, usually old men, not getting out of the way,” he said.

“It is important for political leaders to try and remind themselves that you are there to do a job, but you are not there for life, you are not there in order to prop up your own sense of self importance or your own power.”

For the record, there was no hint in the BBC story about Obama’s comments that he was joking.

Obama and his wife, Michelle, both traveled to Kuala Lumpur last week for an Obama Foundation event, and were apparently still in the region for Obama to appear at this event.

It was all fun and games enriching the super-wealthy but now the karmic cost of the Fed’s manipulation and propaganda is about to come due.

A “market” that needs $1 trillion in panic-money-printing by the Fed to stave off a karmic-overdue implosion is not a market: a legitimate market enables price discovery. What is price discovery? The decisions and actions of buyers and sellers set the price of everything: assets, goods, services, risk and the price of borrowing money, i.e. interest rates and the availability of credit.

The U.S. has not had legitimate market in 12 years. What we call “the market” is a crude simulation that obscures the Federal Reserve’s Socialism for the Super-Wealthy: the vast majority of the income-producing assets are owned by the super-wealthy, and so all the Fed money-printing that’s been needed to inflate asset bubbles to new extremes only serves to further enrich the already-super-wealthy.

The apologists claim the bubbles must be inflated to “help” the average American, but that claim is absurdly specious. The majority of Americans “own” near-zero assets that earn income; at best they own rapidly-depreciating vehicles, a home that doesn’t generate any income and a life insurance policy that pays off only when they pass away.

The average American uses the family home for shelter, and so its currently inflated price does nothing to improve the household income: it’s paper wealth, and we’ve already seen how rapidly that paper wealth can vanish when Housing Bubble #1 popped. (Housing Bubble #2 is currently sliding toward the edge of the abyss.)

Were legitimate price discovery allowed, the asset bubbles would pop, and the real-world impact on the average household that owns essentially zero income-producing assets would be minimal. Their overvalued house would fall in half, but since it still functions as shelter, the actual economic impact is minimal. As for the life insurance company’s losses–where’s the benefit today of an “asset” that only pays out when you die?

Meanwhile, the super-wealthy own stocks, bonds, companies and commercial real estate, all of which generate income. The rich get richer in two ways: their assets generate small fortunes in income (unearned income is what separates “the rich” from everyone else) and thanks to the Fed’s constant goosing of asset prices, their paper wealth has multiplied.

The dirty little secret that nobody dares whisper lest the whisper trigger a self-reinforcing avalanche is that this Fed-manipulated “market” is illiquid: if any serious selling were to arise, there wouldn’t be enough buyers to stave off a complete implosion of the bubbles.

The Fed’s game is to create the illusion of liquidity by being the buyer of last resort, only now the Fed is the only buyer. This is the toxic consequence of the Fed’s 12 long years of Socialism for the Super-Wealthy: thanks to the Fed’s destruction of price discovery, the super-wealthy no longer worry about liquidity, so leverage is the name of the game.

The Super-Wealthy can gamble with hundreds of billions to stripmine the economy and not worry about whether a buyer will actually pay the overvalued price of the asset, because they can count on the Fed to step up and panic-money-print whatever sums are needed to maintain the illusion of liquidity.

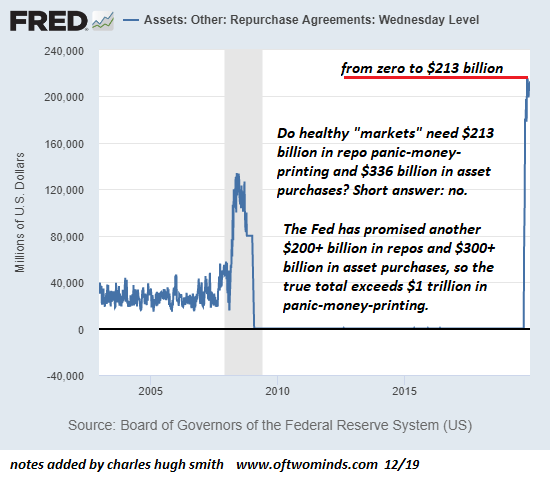

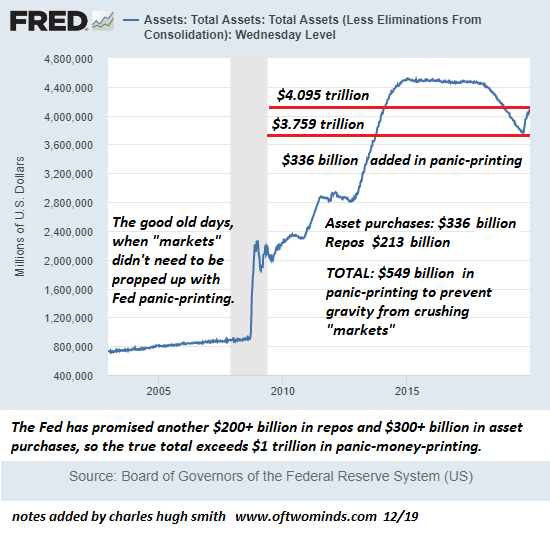

If the “market” is so healthy, why is the Fed panic-money-printing over $1 trillion in a few months? Please glance at the charts below: the Fed has printed $213 billion in repos and $336 billion for asset purchases in the blink of an eye, and the Fed has promised to panic-print another $200+ billion in repos and another $300+ billion in asset purchases, for a grand total of over $1 trillion in panic-money-printing.

Why has the Fed been forced to panic-money-print $1 trillion to stave off an implosion of their phony “market”?Moral hazard is coming home to roost, and the Fed is having a full-blown panic-attack because the Super-Wealthy (banks, corporations, financiers) have no fear that liquidity could dry up and markets go bidless, i.e. buyers disappear and there’s nobody left to buy their overvalued assets at bubble valuations.

If you want to understand how liquidity can dry up overnight and bids disappear, please read Mandelbrot’s bookThe Misbehavior of Markets: A Fractal View of Financial Turbulence. The point Mandelbrot makes here is that markets are intrinsically unstable and prone to sudden, chaotic turbulence. In a legitimate market with intact price discovery, buyers and sellers understand risk cannot be reduced to zero and so they trade accordingly.

But in our bogus Fed-controlled “market,” buyers and sellers are supremely confident the Fed will always buy assets regardless of price, and so they trade accordingly: There are no limits on leverage, derivative positions, credit lines, stock buy-backs or currency (FX) swaps: the Fed has been reassuring the legalized looters that the sky is the limit, go ahead and gamble hundreds of billions of dollars, we’ll buy your overvalued assets if things get dicey.

And so the tissue-thin “market” is fundamentally illiquid, and hence the Fed’s sudden panic-money-printing of $1 trillion, which is roughly equivalent to the entire GDP of Indonesia.

The Fed’s thorough destruction of price discovery and its elevation of moral hazard have created a monster that is about to devour the Fed’s phony facade of a “market”. It was all fun and games enriching the super-wealthy but now the karmic cost of the Fed’s manipulation and propaganda is about to come due, and few of the “market’s” supremely complacent and confident participants are prepared for the unraveling of the Fed’s illusion of liquidity.

If you want an analogy, try a population of rats that have proliferated on an island, and now the ravenous horde has consumed the last remaining bits of food. You can work out what happens next.

Global Markets Hit All Time High As Traders Brace For “Phase Two” Optimism

This is where we stand as we enter Monday morning:

European markets are firmer this morning, though the FTSE 100 significantly outperforms on a second-wave of UK election optimism.

China State Council stated it will continue to suspend additional tariffs on US vehicles and auto parts due to the Phase One deal.

China sources cited by CNBC’s Yoon note that the USD 40-50bln target on agricultural purchases is a “best case target”.

Boeing (BA) is mulling cutting or stopping its 737 MAX production, via WSJ – Co. shares are down 2% pre-market

USD remains subdued although Sterling and Euro were dented by the latest poor PMIs.

Now that “Phase one” of the US-China deal is in the history books, traders around the world are bracing for a full year of “Phase Two” optimism in continuation of the only thing that matters since the spring of 2018 (that, and central banks cutting like there’s a global crisis, of course). And after US cash markets hit a new all time high on Friday, world stock markets rudhes to catch up with the US on Monday, trading at fresh all time highs in what was another “sea of green” day.

Whether it was looking ahead to Phase Two optimism, or simply relishing the (non) deal that was China’s ridiculous promise to double US ag imports, Wall Street was quick to try and shape narratives as one of buying the rumor and then buying the news as well:

“We may have reached the point of ‘peak tariffs’ and this deal could be the start of a series of phased rollbacks, which could unlock further upside for equity markets, driven by an improvement in business confidence and a recovery in investment,” said Mark Haefele, CIO of UBS Global Wealth Management in a note to clients. We may have… but we haven’t, because as Morgan Stanley explained most supply chains are already in process of being moved while the “deal” will hardly inspire confidence among companies to spend more on CapEx.

For now, however, the optimism is working: European shares stormed out of the gate, and the pan-European STOXX 600 index was up by 1.1% hitting a new record high. Germany’s DAX rose as much as 0.5%, despite weakness in the Stoxx 600 Automobiles & Parts Index which underperformed the broader gauge. German auto stocks fell after China’s ambassador to Germany threatened retaliation if Germany excludes Huawei Technologies Co. as a supplier of 5G wireless equipment. Auto-parts stocks such as Valeo and Hella also underperformed after Morgan Stanley cut both stocks along with Schaeffler to underweight, saying that suppliers have failed to fully understand the size of structural changes ahead, which makes it tough to justify their re-rating against OEMs.

European markets also ignored the latest disappointing PMI print, indicating that Europe remains stuck in a manufacturing recession: German private sector activity shrank for the fourth month running in December as a downturn in manufacturing offset services sector growth in Europe’s largest economy. Across the boarder, French businesses grew at a steady pace in December despite a nationwide strike against pension reform, although activity in the manufacturing sector came unexpectedly close to stagnating. Overall, the Eurozone composite PMI was unchanged at 50.6, modestly missing the expectation of a rebound to 50.7, driven by continued manufacturing weakness which shrank from 46.9 to 45.9, well below the 46.9 expectation, while the Services PMI rose modestly from 51.9, to 52.4.

The weakness was largely due to another decline in both German and French mfg PMIs, both of which dropped, with the former now in contraction since March and the latter just one pension strike away from a sub-50 print.

Earlier in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan to its highest level since April 18. It was last up 0.13%. Australia’s S&P/ASX 200 led the way as it jumped 1.63%, while shares in Taiwan added 0.22%. Japan’s Nikkei 225 succumbed to some profit-taking, falling 0.29% after surging 2.55% to a 14-month closing high on Friday.

While everyone was busy ignoring the latest European economic data, markets were positively giddy at the all too credible rebound in Chinese data unveiled late on Sunday night which saw most indicators post a sharp and orchestrated rebound.

Chinese investors initially had a more tepid reaction to the trade news, with the blue-chip CSI300 index struggling to rise further after trade hopes fanned a near 2% rise on Friday. But after a lackluster morning session, the CSI300 index turned higher in the afternoon and was last up 0.3%, helped by the latest industrial output and retail sales data.

And so, thanks to China’s latest data dump, positive sentiment helped push MSCI’s All Country World Index up 0.15%, after hitting an all-time high on Friday when the trade deal was agreed.

Looking at the latest trade development, on Sunday, China State Council stated it will continue to suspend additional tariffs on US vehicles and auto parts due to the Phase One deal, whilst also suspending the additional 5-10% tariffs on some US goods planned to take effect on December 15th, according to CNBC’s Yoon. Meanwhile, China’s Foreign Ministry said that more trade information will be released in due course and working-level officials from both sides remain in contact.

China sources cited by CNBC’s Yoon note that the USD 40-50bln target on agricultural purchases is a “best case target”, and that the US would likely allow ‘best endeavor’ purchases; adds that general feeling on tariff rollback is an issue of linguistics. Additionally CNBC’s Yoon adds, no Chinese confirmation regarding the hard targets for US agricultural purchases; although, China is likely to agree but cannot acknowledge this publicly due to a possible backlash.

In addition to the trade deal, markets were excited by the apparent end of the Brexit drama, if only for the time being. Ryan Felsman, senior economist at CommSec in Sydney, said the trade deal and the receding risk of a disorderly Brexit after the British election produced a strong Conservative majority provided support for sentiment in Australia. A lower-than-expected Australian budget surplus due to a sluggish economy has also “built expectations by markets for further easing from the Reserve Bank (of Australia),” he said. He added that investors wanted more details and the reduction in U.S. tariffs may have disappointed some looking for more aggressive action.

“Certainly there were expectations perhaps that the rollback would be more significant than just 50%.”

In the US, S&P futures were back to record highs hit last week. U.S. shares struck a cautious note on Friday, paring initial gains to end barely higher as weary investors awaited signs of a concrete deal.

However, the news of a deal was still enough to send the S&P 500 to a record closing high of 3,168.8, up just 0.01%. The Nasdaq Composite added 0.2% to end at 8,734.88, also a record, and the Dow Jones Industrial Average rose 0.01% to 28,135.38.

In rates, U.S. Treasury yields moved modestly higher on Monday, after the sharp reversal on Friday, reflecting the more positive mood. Benchmark 10-year Treasury notes rose to 1.8452% compared with their U.S. close of 1.821% on Friday, and the two-year yield touched 1.6304% compared with a U.S. close of 1.604%.

In FX, the Bloomberg Dollar Spot Index slipped and the euro held gains after data showed the euro-area economy is still struggling. EURUSD touched 1.1151 versus the dollar before paring gains after a slew of European PMIs. Treasuries halted their advance from Friday, while euro-area bonds were mostly higher. As noted above the latest Eurozone composite PMI stayed at 50.6 in December, slightly lower than the forecast of 50.7. The reading signals fourth-quarter output will be the weakest since the region exited a double-dip recession in the second half of 2013.

Sterling pared Asia session gains on profit taking and after a flash indicator for all business activity dropped to the lowest since the aftermath of the 2016 Brexit referendum; manufacturing activity slipped to 47.4, a sharper downturn than the 49.2 reading predicted by economists.

In commodities, oil prices which had risen on Friday following the deal, climbed further on Monday. Brent crude rose 0.1% to $65.28 per barrel, and U.S. West Texas Intermediate crude was down 0.05% at $60.11 per barrel. Spot gold prices were down 0.06% at $1,474.64 per ounce.

Looking at today’s US calendar we get the November Markit PMI data, December Empire State manufacturing survey, NAHB housing market index, October net long-term TIC flows, total net TIC flows.

Market Snapshot

S&P 500 futures up 0.3% to 3,181.25

STOXX Europe 600 up 1% to 416.15

MXAP down 0.1% to 168.88

MXAPJ up 0.06% to 542.89

Nikkei down 0.3% to 23,952.35

Topix down 0.2% to 1,736.87

Hang Seng Index down 0.7% to 27,508.09

Shanghai Composite up 0.6% to 2,984.39

Sensex down 0.1% to 40,950.83

Australia S&P/ASX 200 up 1.6% to 6,849.71

Kospi down 0.1% to 2,168.15

German 10Y yield fell 1.5 bps to -0.304%

Euro up 0.1% to $1.1133

Italian 10Y yield rose 20.4 bps to 1.09%

Spanish 10Y yield fell 0.7 bps to 0.406%

Brent Futures up 0.1% to $65.33/bbl

Gold spot up 0.1% to $1,477.23

U.S. Dollar Index down 0.1% to 97.08

Top Overnight News

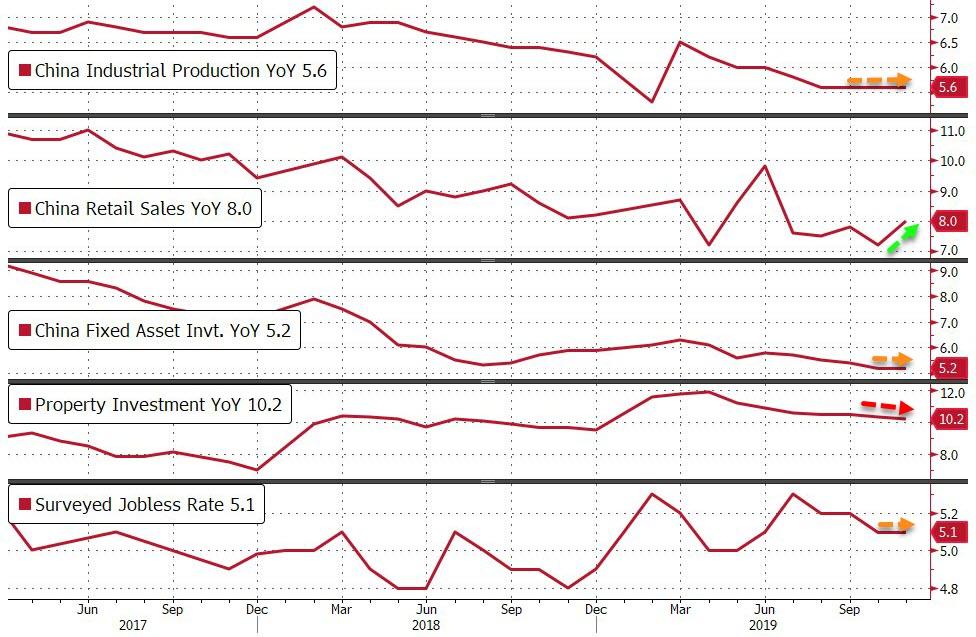

China’s economy showed signs of stabilizing and regaining growth momentum in November; industrial output rose 6.2% from a year earlier, versus a median estimate of 5.0%. Retail sales expanded 8.0%, compared to a projected 7.6% increase. Fixed-asset investment was unchanged at 5.2% in the first eleven months, the same as forecast

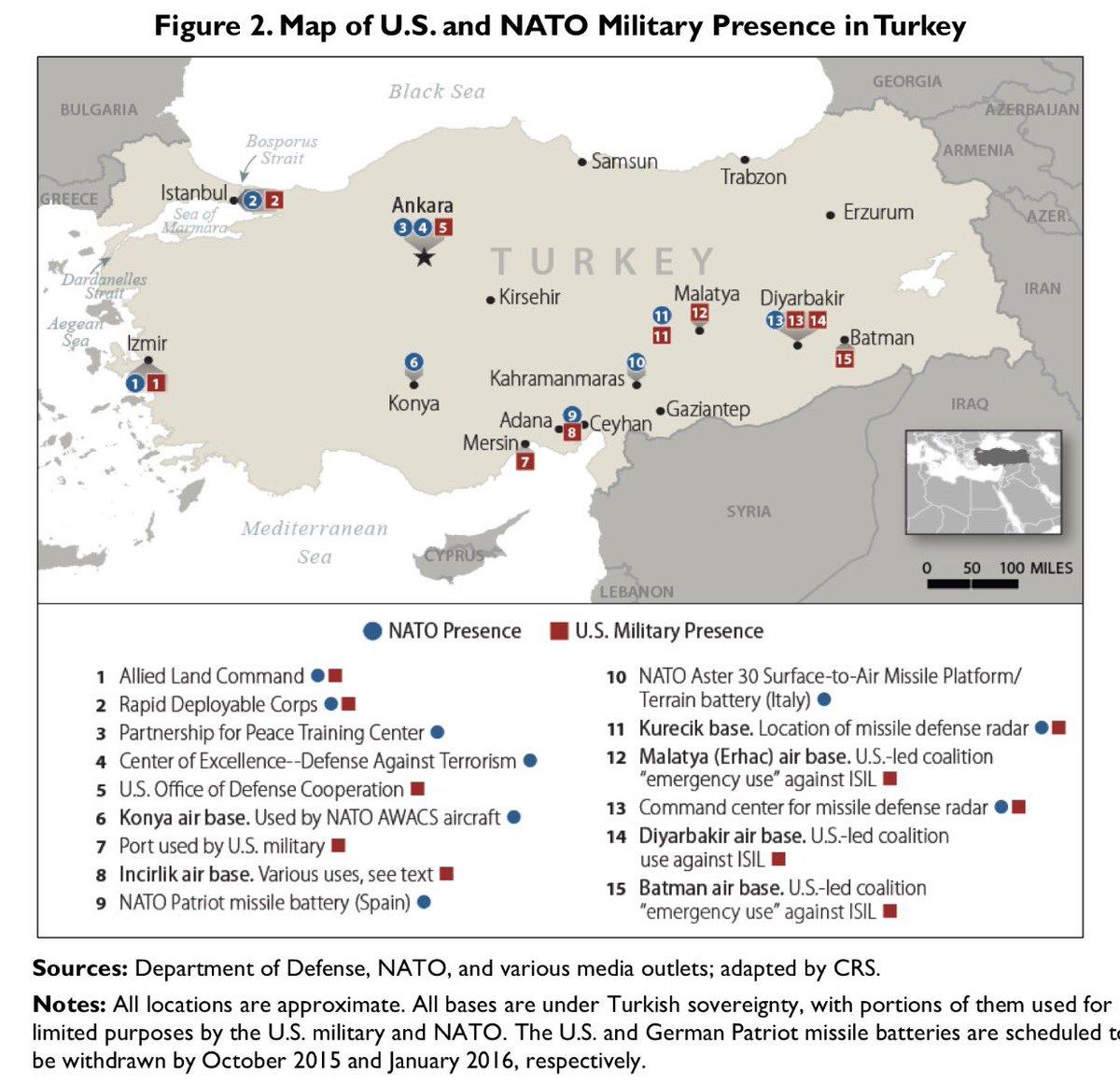

President Recep Tayyip Erdogan warned that Turkey could shut down two of the most critical NATO installations on its territory if the U.S. imposes sanctions over its purchase of an advanced Russian missile-defense system

Boris Johnson will appoint top ministers to his cabinet on Monday as he pushes ahead with Brexit, emboldened by the historic majority he won in last week’s British general election

China’s economy showed signs of stabilizing and regaining growth momentum in November, adding to the good news for the nation’s outlook after a preliminary trade deal with the U.S. was reached last week. China steps up talks with U.S. on opening its companies’ books

China’s ambassador to Germany threatened Berlin with retaliation if it excludes Huawei Technologies Co. as a supplier of 5G wireless equipment, citing the millions of vehicles German carmakers sell in China

Australia’s Treasury lowered its forecast surplus for the 12 months through June 2020 to A$5 billion ($3.4 billion) from April’s budget estimate of A$7.1 billion as it scaled back estimated tax revenues, according to the Mid-Year Economic and Fiscal Outlook released in Canberra Monday. It also predicted narrower surpluses for the following three fiscal years

Oil retreated from a three-month high as optimism the U.S.-China trade deal will spur demand for crude gave way to caution due to the agreement’s limited nature and lack of detail

Hong Kong’s demonstrators clashed with police late Sunday as Chief Executive Carrie Lam visited Beijing where she’s expected to update Chinese President Xi Jinping and other senior officials on the violent protests that have gripped the city for the past six months. Chinese Premier Li Keqiang gives Hong Kong leader fresh boost after protests

Asian equity markets traded mixed following relatively light newsflow over the weekend and last Friday’s flat performance on Wall St. where the major indices consolidated near record levels after the confirmation of a US-China Phase One deal which officials plan to sign in early January, although some noted the deal was only limited and questions arose over the feasibility of China committing to as much as USD 50bln of US agriculture goods. ASX 200 (+1.6%) was lifted by outperformance in defensives and the top-weighted financials sector with sentiment buoyed after the world’s 2 largest economies averted the December 15th tariffs, while Nikkei 225 (-0.3%) was subdued by the recent pullback in USD/JPY and as the latest Japanese Manufacturing PMI data remained in contraction territory. Hang Seng (-0.7%) and Shanghai Comp. (+0.6%) were constrained despite the phase one agreement confirmation and better than expected Chinese data in which Industrial Production and Retail Sales both topped estimates, as the stats bureau stated the economy still faces relatively big downward pressure and amid expectations for a reduced growth target for next year, while the mood in Hong Kong was also soured by a rise money market rates (Overnight HIBOR +57bps) and the resumption of violent protests over the weekend. Finally, 10yr JGBs were flat with prices hampered by last week’s resistance levels and with demand also subdued due to the absence of the BoJ in the market today.

Top Asian News

Top Turkish Bankers Say They Were Fired on Orders of Regulators

India Protests Spread as Anger Against Citizenship Law Grows

Masayoshi Son’s Bankers Are Worried About Their Favorite Client

Philippine Stocks Sink to Two-Month Low as Utilities Retreat

European equities kick-start the week on the front foot [Eurostoxx 50 +0.7%] following on from a relatively mixed APAC session, with traders citing an overall improvement in the trade environment as a reason for the advances. Cash Stoxx 600 (+1.1%) managed to notch intraday record highs, albeit the FTSE 100 (+2.1%) stands as the marked outperformer amid further post-election tailwinds on large-cap stocks, miners benefitting from rising copper prices and exporters taking advantage of a declining Sterling – Standard Chartered (+3.3%), RBS (+3.2%), Barclays (+3.5%), Glencore (+4.0%), BHP (+3.2%), Rio Tinto (+2.9%) and Antofagasta (+2.7%). DAX and other core European indices stalled gains amid disappointing December Flash PMIs. Sectors opened modestly in positive territory but have since gained traction, with cyclical Materials and Financials outperforming on the back of FTSE 100 gainers. In terms of other individual movers, Novartis (unch) opened lower after the Co. stated it will be dropping development of its asthma drug amid a string of disappointing trials. Meanwhile, Kerry Group (-3.5%) shares fell to the foot of the pan-European index after losing a USD 26bln deal to International Flavours and Fragrances for US-listed DuPont’s nutrition division (+1.9% pre-market). Last but not least, Sports Direct (+20%) soared on the back of a profit jump with group revenue increasing 14% YY which comes amid performance woes after the Co. acquired the troubled House of Fraser.

Top European News

Euro-Area Economy Ends 2019 Still Struggling as Momentum Stalls

Factory Woe Puts U.K. Economy on Brink of Contraction, PMI Shows

German Factory Slump Deepens Again as Recovery Seems Elusive

U.K. Rainmakers Eye Dealmaking Return Post Tory Election Win

In FX, Sterling’s post-UK election 2nd coming was already fading after a fleeting foray above 1.3400 vs the Dollar and test of resistance around the psychological 0.8300 level against the single currency when the preliminary PMIs for December confounded expectations for some improvement and missed consensus by quite a distance, especially in the manufacturing sector. Cable duly retreated towards 1.3325 and the cross rebounded to circa 0.8350 even though the earlier Eurozone flash surveys were also disappointing, and Germany’s manufacturing headline in particular. However, Eur/Usd remains depressed within a 1.1123-50 range and may struggle to pull away from decent option expiries between 1.1120-25 and 1.1100-10 (1.2 bn clips) rather than challenging slightly larger interest at 1.1150 (1.3 bn).

NZD/CAD/AUD – All firmer vs their US counterpart that continues to flounder (DXY anchored around 97.000), with the Kiwi keeping tabs on the 0.6600 handle, Aussie hovering just under 0.6900 and Loonie pivoting 1.3150 in wake of some upbeat Chinese data overnight (ip and retail sales) and further reserved reflection on US-China trade deal Phase 1. Nzd/Usd and Aud/Usd have both regrouped after losing some ground on independent impulses via growth forecast downgrades from the NZIER and government respectively, while the former also took note of Westpac rolling its RBNZ rate cut prediction to August next year from February.

NOK/SEK – The Scandi Crowns are both holding firm lines ahead of this week’s Norges Bank and Riksbank policy meetings, but Eur/Nok’s retreat is more technical after breaching the 100 DMA (10.0385) compared to Eur/Sek’s reversal through 10.4300 in anticipation of a 25 bp repo rate hike on Thursday.

CHF/JPY – The safe-haven Franc and Yen are narrowly mixed against the Buck, with Usd/Chf nearer the bottom of a 0.9825-45 band in contrast to Usd/Jpy hovering just below 109.50 compared to 109.25 at one stage and flanked by expiries between 109.00-05 and 109.50 in 1bn.

In commodities, little to report on the commodities front – with WTI and Brent futures largely unchanged on the day, albeit in positive territory after a relatively flat APAC session. WTI futures trade on either side of USD 60/bbl whilst its Brent counterpart topped USD 65/bbl in recent trade with little by way of fresh fundamental catalysts, and with participants somewhat cautious of the US-China Phase One deal amid a lack of details and a paucity on China’s commitments. Elsewhere, gold prices remain choppy within a tight USD 5/oz range thus far, as traders and investors await further Phase One details. Copper meanwhile has resumed its upwards trajectory with risk-sentiment a cited factor, although upside may be more due a receding USD and above-forecast China industrial production and retail sales. Finally, Dalian iron ore futures fell in excess of 1.5% after data showed weekly utilisation rates at 163 mills across China slumped almost 66 – thus casting fresh doubts on demand for the base metal.

US Event Calendar

8:30am: Empire Manufacturing, est. 4, prior 2.9

9:45am: Markit US Composite PMI, prior 52

Markit US Manufacturing PMI, est. 52.6, prior 52.6

Markit US Services PMI, est. 52, prior 51.6

10am: NAHB Housing Market Index, est. 70, prior 70

4pm: Net Long-term TIC Flows, prior $49.5b

DB’s Jim Reid concludes the overnight wrap

This is the last full week of the year and there are still a number of interesting events/data points to get through before the soporific Xmas week. I’m starting it a bit tired as for the second night in a row I fell asleep trying to finish “The Irishman” – the new Scorsese/De Niro et al film with de-ageing technology used. It’s very very good but 3hr 30mins is a little tough to watch in one (or even two) sitting(s) after a day running after atrociously behaved children. We’ll be trying to finish tonight.

As for this week, today’s global flash PMIs stand out, along with the German IFO (Wednesday) and the BoE/BoJ meetings (Thursday). We don’t often mention the Swedish central bank decision as a main highlight but on Thursday it’s expected that the Riksbank will end Sweden’s five year experiment with negative rates and take them back to zero even though they haven’t met their inflation target. As concerns over the side effects of negative rates rise around the world, especially in Europe, a lot of attention will be placed on how the Swedish economy and banking system deals with this in the months ahead.

More on the week ahead below but after a lot of drama we finally got a Phase One trade deal between the US and China, confirmed by both sides on Friday. The legal work, full details and signing (probably in January) is still to come but it appears that agreement has been made. The immediate consequence is that the tariffs scheduled to have come into effect yesterday have now been suspended. Meanwhile, tariffs on $120bn of Chinese imports by the US will be halved from 15% to 7.5%, although 25% on a remaining $250bn worth will remain, and the fact sheet released by the US Trade Representative’s office said that China has committed “to import various U.S. goods and services over the next two years in a total amount that exceeds China’s annual level of imports for those goods and services in 2017 by no less than $200 billion.” Looking forward, President Trump tweeted that discussions on the Phase Two deal would begin “immediately”, as opposed to after next year’s presidential election. There will clearly be relief that it looks like a deal has been done but there are fewer tariff rollbacks than some had thought likely and Mr Trump’s comments suggest phase two will be a live issue straight away. My base case was that this would wait until after next November’s election assuming he won. So it will be very interesting as to how much Trump keeps the negative China rhetoric alive in 2020 after the deal is eventually signed.

Staying with politics and as an additional word on the U.K. election result from the end of last week, I wonder if it marks a new chapter in populism. The victorious Conservative Party is traditionally a party of the better off with the Labour Party the party of the poorer and working class communities. The problem is that the working class is generally in favour of Brexit and the Conservatives ruthlessly exploited this and they subsequently voted for them in waves in areas that haven’t for a century in some cases. To maintain this support the Tories will have to shape policy to help those left behind by globalisation (mostly in the north of the country) and by definition reduce inequality. If you want to see a great graph look at the FT today where they show a scatter of the percentage of blue collar jobs in a constituency against the vote swing in this election in favour of the Tories. There was a big correlation. Although politics isn’t often rational, it would make perfect sense if this election heralded a spending bias towards the poorer parts of the U.K. that voted for Brexit. In terms of the read through to other countries, to arrest the rise of populism we’ve always thought mainstream parties will adopt more populist policies aimed at the so-called left behinds. No-one has done this better in terms of winning an election than Mr Trump in the US and Boris Johnson in the U.K. The confusing thing about the Trump presidency is that his tax cuts were biased towards the rich which is probably why the likes of Warren and Sanders remain in the Presidential race and populism is still alive there. As we said on Friday though, the U.K. election result may at the margin make Democratic voters conclude that a lurch too far to the left is dangerous in Anglo-Saxon countries. We will see. Nevertheless the concluding remark is that the U.K results show that populism is far from dead – it’s just that mainstream parties can morph into populist parties if the will is there. To me it seems that European mainstream parties have so far struggled with this. I wonder if lessons will be taken from this on the continent.

Overnight, we’ve seen a number of data releases from China that have surprised to the upside, something that will further boost sentiment after the reaching of a Phase One agreement with the US. November retail sales were up +8.0% yoy (vs. +7.6% expected), while industrial production was up +6.2% yoy (vs. +5.0% expected). That said, fixed-asset investment over the Jan-Nov period was only up +5.2% yoy, the joint weakest since at least 1998 where data became more readily available. Equity markets in Asia are treading water this morning though, with the Nikkei (+0.03%), the Shanghai Comp (+0.06%) and the Kospi (-0.05%) seeing little movement in either direction, though the Hang Seng is down -0.37%. S&P 500 futures are up +0.28% following another record high for the index on Friday.

In terms of a fuller rundown of the week ahead, for today’s PMIs, we’ll see manufacturing, services and composite PMI data for France, Germany, the Euro Area, UK and the US. So quite a collection to watch for, especially as the market expectation is that the global economy is steadily turning after recently bottoming out. In November, the PMIs showed some sign of this in the Euro Area with a 50.6 reading for the composite PMI, but which included both Germany (49.4) and Italy (49.6) in contractionary territory led by manufacturing.

With the Fed and the ECB having announced their policy decisions in the week just gone, attention will turn to central banks elsewhere over the week ahead. The major action takes place on Thursday, with the Bank of Japan, Bank of England, Riksbank, the Banco de Mexico and Bank Indonesia all announcing policy decisions that day. As we said at the top the Riksbank might be the most interesting longer-term as they are expected to end a 5-year dalliance with negative rates. The rest of the world will be watching to see if the sky falls in or whether this helps persuade people that negative rates are part of the problem. My guess is the latter when the history books are written.

In terms of central bank speakers next week, there’s a conference being held at the ECB on Wednesday in honour of Benoît Cœuré, whose 8-year tenure on the ECB Executive Board concludes at the end of the month. Cœuré himself, along with ECB President Lagarde and the Fed’s Brainard will all be making remarks there. In the US, we’ll also hear tomorrow from New York Fed President Williams, Boston Fed President Rosengren, and Dallas Fed President Kaplan. Chicago Fed President Evans will also be speaking on Wednesday.

Staying with Europe, Wednesday sees the publication of the latest Ifo survey from Germany. Last month, the business climate indicator rose to its highest level since July, so it’ll be interesting to see if recent momentum is sustained, with the consensus looking for a modest increase to 95.5. Separately, Wednesday also sees the final release of the CPI and core CPI readings for the Euro Area in November, and on Friday there’ll be the advance December reading of the European Commission’s consumer confidence reading for the Euro Area.

From the US, we also have a number of key readings out this week. Alongside the PMIs, Tuesday sees the release of November’s industrial production figures, as well as housing starts and building permits data. Last month, building permits rose to their highest level since May 2007, so it’ll be interesting to see if this strength in the recent data is sustained. Friday sees the final Q3 US GDP reading where the component breakdown will influence Q4 thinking.

Recapping Friday and last week now. Global markets were buoyed by the combination of a Phase One deal between the US and China, along with signs of a resolution to the immediate Brexit impasse from the UK election. The S&P 500 ended the week up +0.73% (+0.01% Friday) at a new record high, while in Europe the STOXX 600 was up +1.15% (+1.09% Friday) at its highest level since April 2015. Bond yields ended the week slightly lower after a sizeable trading range, with 10yr Treasury yields down -1.4bps (-7.0bps Friday), and 10yr bund yields -0.3bps (-2.0bps Friday). The removal of downside risks to the global economy saw investors move into other risk assets, with brent crude up +1.29% (+1.59% Friday) last week, while the spread of BTPs over bunds narrowed by -8.9bps.

Meanwhile, UK assets rallied on Friday as it emerged the Conservatives had won an 80-seat majority at the general election. Sterling ended the week up +1.45% (+1.29% Friday) at $1.3331, its highest level since March, while against the euro it was up +0.94% (+1.39% Friday) at its highest level since July 2016. UK equities also outperformed, with the FTSE 100 up +1.57% (+1.10% Friday), while the more domestically-focused FTSE 250 index was up +2.75% (+3.44% Friday). Banks in particular rose following the result, with Friday seeing big share price moves for Lloyds Banking Group (+5.25%), Barclays (+6.18%) and RBS (+8.39%). The other major rises were seen from the companies that had been floated as targets for nationalisation by Labour. Centrica, parent of British Gas, was up +10.51% on Friday, its best day since November 2008, while BT Group was up +6.54%, its best since November 2018.

Finally, in terms of data on Friday, US retail sales were weaker than expected, with a +0.2% (vs. +0.5% expected) increase in November, although the previous month was revised up a tenth to +0.4%. The year-on-year figure fell to +2.9%, its lowest since June. In spite of the figures, Fed Vice Chair Clarida said on Fox Business that “the U.S. consumer’s never been in better shape in my professional career.” Elsewhere, New York Fed President Williams also sounded a positive note on the outlook, saying that “we’ve got the economy on a very strong footing, sustainable footing, for good growth next year.”

Turkey Gives NATO The Middle Finger, Threatens To Shutter Critical Military Bases Over Sanction Threats

French President Emmanuel Macron complained during the NATO summit in London earlier this month about Turkey’s decision to buy a Russian missile-defense system and its invasion of Syria, musing about how Turkey could justify its continued membership in the alliance if it counties to flout its interests at every turn.

These comments, only the latest round of complaints about Turkey’s behavior toward its Western NATO allies, inspired speculation about whether NATO could formally expel Turkey. But aside from whatever legal complications might lie in wait, we posit that there’s another more fundamental reason why NATO likely won’t be able to expel Turkey. Because Turkish President Recep Tayyip Erdogan would likely quit first.

That’s right: Although Trump and Erdogan have tried to maintain at least the veneer of a personally amicable relationship, and though Trump has at times defied his own senior NatSec officials to offer a major sop to Erdogan (like when Trump pulled US troops out and stepped aside to allow the Turkish invasion, the the horror of Europe), Erdogan’s increasingly tight relationship with Russia – a relationship built on defense and energy ties – is becoming impossible for many western leaders to countenance.

In response to this and myriad other slights both perceived and real, Erdogan made it clear on Monday that he’s had about enough of this harassment from his supposed “allies” in the West. Because when it comes to Trump cards, Erdogan still has one to play.

According to Bloomberg, Erdogan warned that he could shutter two of the most important NATO bases in the world if more sanctions are imposed.

In the minds of US NatSec officials, Erdogan’s threat is an extremely low blow. An early-warning radar at Turkey’s Kurecik air base is a critical component of NATO’s early-warning defense system against ballistic missile attacks. And the Incirlik air base in southern Turkey is critical to tactical air strikes and drone attacks throughout the region.

“If it is necessary to shut it down, we would shut down Incirlik,” Erdogan told AHaber television on Sunday. “If it is necessary to shut it down, we would shut down Kurecik, too.”

[…]

“If they put measures such as sanctions in force, then we would respond based on reciprocity,” Erdogan said. “It is very important for both sides that the U.S. should not take irreparable steps in our relations.”

Additionally, Erdogan warned the US not to recognize the Turkish genocide of Armenians in the early part of the 20th century, an issue that has long been important for Erdogan.

Until now, the US and NATO military presence in Turkey has been held sacred, even as the relationship between the two countries became increasingly bitter over the past two years. Those aren’t the only two bases in Turkey: the US has for decades heavily leaned on Turkey as critical to its policing of the Middle East.

Bottom line: It’s Turkey’s party, and it can buy missiles from Russia if it wants to. After all, placating Russia is important for an energy importer like Turkey. Russian energy subsidies can be a huge economic boon for an economy – just look at Belarus.

Of course, for the US, Erdogan’s demands present a difficult dilemma: The US and NATO need Turkey to host its bases, but they’re worried that, if the S-400 system becomes fully operational (expected in April), many worry the Russian system could be used to collect intelligence on the stealth capabilities of the F-5 fighter jet.

Now, will President Trump risk calling Erdogan’s bluff? That remains to be seen.

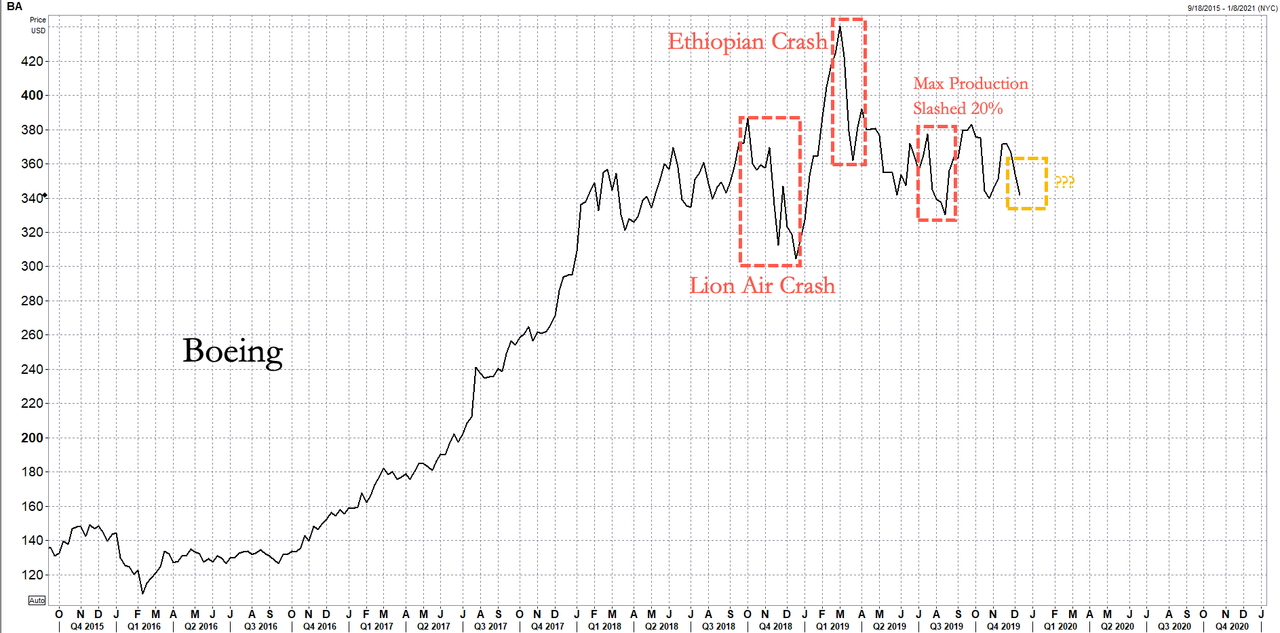

Sources have told The Wall Street Journal that Boeing could temporarily halt production of the 737 Max amid concerns the timeline of ungrounding the aircraft could be pushed further out. The decision to disclose the fate of the 737 Max production could arrive as early as Monday.

Boeing hosted a regular board meeting on Sunday in Chicago. Sources said the fate of the 737 Max production comes days after US regulators criticized Boeing for providing unrealistic timelines for when the plane will return to the skies.

In April, Boeing slashed production by 20% from 52 to 42 planes per month. A more extended cut or even production halt could be absolutely damaging to the global aerospace industry, as any reduction in planes could ripple down the supply chain and cause financial hardships for suppliers.

Boeing’s board meeting is expected to conclude on Monday. Sources weren’t exactly sure when the production-related announcement will be released.

“We continue to work closely with the FAA and global regulators towards certification and the safe return to service of the Max,” Boeing stated. “We will continue to assess production decisions based on the timing and conditions of return to service, which will be based on regulatory approvals and may vary by jurisdiction.”

We’ve noted in the past that production cuts could have severe consequences for the US economy. Over 600 suppliers provide 600,000 parts needed for each plane; the brunt of the shock would be seen down the chain at smaller firms.

Some Max suppliers have already cut production rates after Boeing reduced plane output by 20% in April. There are other reports that some suppliers have already furloughed employees and shut down equipment as the groundings enter the ninth month.

“It’s easier to ramp down gradually and then ramp back up,” said John Scannell, chief executive of Moog Inc., which makes control motors for the MAX.

The upcoming production decision isn’t easy for Boeing since two of its Max planes experienced flight control system malfunctions and crashed in the past year or so, killing 346 people.

With no clear timeline on when the planes can return to the skies, and production likely slashed in 2020 – this could further weigh on Boeing shares:

The results of the UK elections have shown something that I have commented on several occasions: The widely spread narrative that British citizens had regretted having voted for Brexit was simply incorrect.

We already had the evidence in the European elections, where the Brexit Party won with 31.6% of the votes, but the general elections have been even clearer. The Conservative Party won by an absolute majority (more than 360 seats and 43.6% of the votes).

The failure of Labour’s radicalism led by Jeremy Corbyn has been spectacular, and his interventionist messages, reminiscent of the terrible Harold Wilson period, added to his vague stance on Brexit and how to finance his promises of “everything free at any cost” have led the party to its worst results since 1935 and losing key seats in constituencies that always voted Labour since 1945.

Up to 18 Labour historical footholds passed to a conservative majority including Blyth, Darlington, Workington, Great Grimsby or Bassetlaw. In Wales, the Conservative party snatched six seats from the socialists. The transfer of Labour votes to conservatives exceeded 4.7%, according to the Press Association. The interventionist and extremist proposals of Jeremy Corbyn have caused them to lose votes even in pro-Remain districts (-6.4% according to the BBC).

Months of attempts to whitewash the image of Jeremy Corbyn by parts of the media have not been able to eliminate his history of extremism and interventionism, his refusal to apologize for cases of anti-Semitism and his incompetence in explaining the economic program. Corbyn led a traditionally moderate and social-democratic formation to the most retrograde and interventionist proposals of its recent history.

Johnson won by absolute majority with a much more moderate, positive and pro-growth message, but, above all, unquestionable in terms of delivering Brexit.

Johnson has not only reached a much wider spectrum of voters but Corbyn has annihilated his options with Labour’s own more moderate voters by radicalizing his message in a country where any citizen over 45 remembers the economic disasters of socialism.

The UK elections should be an opportunity for everyone to learn several lessons.

The first lesson is that the silent majority is the target in an election, not the loud minority. As in the United States and European Parliament elections, the consensus narrative about what was happening was clearly influenced by a terrible confirmation bias among most mainstream commentators. Some media in the UK have reported more about what they wanted to happen more than what really happened.

The second lesson is that extremist socialism is not an alternative. While Johnson focused his campaign on adding supporters, Corbyn set out to return to the past and try to revive the policies that led to poverty, constant devaluations, supply cuts, and misery.

The third was falling into the error of believing that sound economic policies do not matter. That the “majority” opinion is what some media or some commentators say. Even worse, to believe that the will of the people is represented bt a few anonymous accounts on social networks. Bots are not votes.

The opportunity of these elections is enormous. The European Union can strengthen its project and implement the agreement signed with the Johnson government in a beneficial way for all member states. It is a pity that the United Kingdom does not want to continue in the European Union, but we have to look to the future. For the UK, it is clearly an opportunity to strengthen the economy focusing on job creation and attraction of capital.

The United Kingdom will implement growth policies and competitive taxation. This is not just good for UK citizens. It is a much-needed reminder for the European Union to abandon its most interventionist temptations and focus on being competitive, attractive and productive.

The European Union faces significant economic, demographic and technological challenges. The UK can develop its competitiveness and investment appeal and, by doing so, the European Union can benefit. The United Kingdom is not a threat. It’s an example. A partner for all member states and a reminder of which policies work and how socialism and interventionism are never the answer.

Johnson is not a danger. He is the prime minister of an allied country and partner that will continue to be so. The danger to the European Union is not Johnson, it is interventionist temptation. Let’s fight it.

While in 2020, five out of the ten most populous countries in the world were located in Asia, the picture will look different in 2100, when five African countries – Nigeria, Ethiopia, Tanzania, Egypt and the Democratic Republic of the Congo – will be among the world’s ten largest.

While some Asian countries will continue to grow, they will do so at a lower rate and will be surpassed in population by African countries exhibiting faster growth. Others, like China and Bangladesh are actually expected to shrink until 2100, mainly a result of higher standard of living and education that has already begun to lower birth rates.

In 1950, four European countries were still among the world’s largest. That number will have decreased to one in 2020 and none in 2100.

The number of children born worldwide is already decreasing, but at currently 2.5 children born per woman, world population is still growing. UN population researchers found that if the global fertility rate kept dropping at the rate it currently is, it would reach 1.9 children per woman in 2100, at which point the world population would actually be decreasing.

The following is a translation of an article by the lawyer Paul Tormenen for the identitarian think-tank Polémia. The numerous sources cited are detailed in the original article. This piece provides a solid overview of the tremendous demographic transformation which Belgium is undergoing and of the striking differences between European and Islamic migrants, the latter being markedly socially conservative and prone to unemployment. Entire neighborhoods such as Molenbeek have become unrecognizable and begging Gypsies have become a familiar sight on street corners.

At the same time, the numbers show that, as of today, a majority of immigrants to Belgium are of European origin and can be expected to integrate smoothly. Even if we concede that the Europeans are likely less fertile than the Muslims and Africans, this is one reason why I do not believe “race war” is likely to happen any time soon, notwithstanding the reality of Afro-Islamic criminality and periodic murderous Islamist terrorist attacks.

If Belgium experienced waves of immigration in the 20th Century, the current wave is unique in its magnitude and the fact that it is “endured” by a part of the population. The ethnocentric demands and the radicalization of a fraction of the immigrant population has provoked differing reactions among the [French-speaking] Walloons and the [Dutch-speaking] Flemish. In Belgium, as in other European countries, the migratory and identitarian questions have become central to the country’s political life.

From the 20th Century to Today

A first wave of immigration was organized during the interwar years, due to the pressure of the Belgian leaders of heavy industry. Labor migration was started up again in the 1960s. These immigrants were notably called upon to work in the mines and were essentially of European origin (Italy, Spain, Greece). After 1964, bilateral agreements were concluded with Muslim countries (Morocco, Turkey, Algeria) in order to facilitate the hosting of foreign workers. Without regard for any cultural factors, familial immigration was also promoted in order, according to Belgium’s leaders, to tackle the country’s aging population.

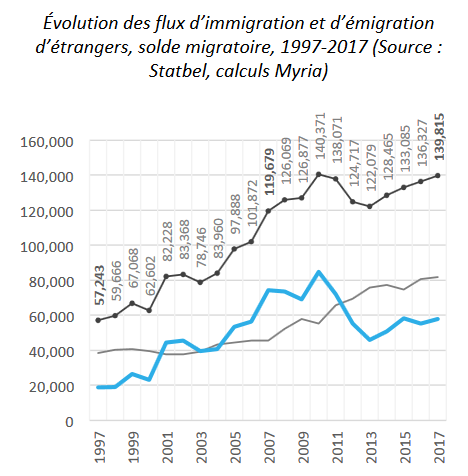

Since the end of the 1980s, Belgium has been experiencing a new migratory wave. Whereas the annual flow had been relatively stable between the 1950s and 1980s, with yearly arrivals of between 40,000 and 60,000, family reunification and asylum requests significantly increased the arrivals of foreigners. Over a million of them thus entered Belgium legally between 2000 and 2010.

Belgian migratory trends. Dotted line: immigration. Thin line: emigration. Solid light blue line: net migration.

Between 2009 and 2011 alone, family reunification, which accounts for about half of residence permits, enabled 121,000 foreigners to legally settle in Belgium. A Belgian senator, Alain Destexhe, speaks of family reunification’s “domino effect,” because of the different ways it gives for family members to come from abroad.

Since 2007, the annual number of foreigners arriving in Belgium has always been over 100,000. In 25 years, the immigrant population (of foreign or Belgian nationality) has doubled. Annual growth of the foreign-origin population is estimated at between 1% and 5%. As of 1 January 2018, of Belgium’s 11.3 million inhabitants, 16.7% were born abroad (1.9 million people). These figures do not take into account unidentified illegals, nor the asylum-seekers who are registered on the waiting lists.

The concentration of foreigners is especially visible in the big cities. For example, in Brussels, foreigners are almost as numerous as Belgian citizens. The city of Antwerp now has more immigrants than natives.

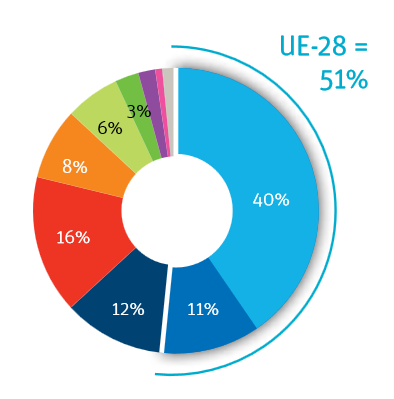

Origin of the foreign-born population in Belgium. Light blue: EU-15. Mid-blue: 13 new EU states (Eastern Europe). Dark blue: non-EU Europe (including Turkey). Red: North Africa. Orange: Sub-Saharan Africa. Light Green: West Asia. Dark Green: East Asia. Purple: Latin America. Pink: North America. Grey: Other.

Asylum-seekers: a secondary flow

In addition to illegal immigration, Belgium is, like France, experiencing the “secondary flows” of asylum-seekers. More and more asylum-seekers in Belgium are not fresh arrivals on the European continent. Their request for asylum was rejected in another country and they try their luck in Belgium. This phenomenon, which shows the bankruptcy of the European asylum “system,” is due to tougher migratory policies in the Scandinavian countries and Germany. It is estimated that one third of asylum-seekers practice this kind of “desk-hopping.” More broadly, between 1991 and 2015, some 517,000 asylum requests have been made in the country.

The origin of the immigrants has changed

If Europeans still make up the majority of the foreign population, Turks (155,701 people as of 1 January 2016) and Moroccans (309,166) represent significant contingents. Among the foreigners who have recently acquired Belgian citizenship, these two nationalities are in the lead.

According to the Pew Research Center, the Muslim population represents 7.6% of the Belgian population, almost 796,000 inhabitants. Depending on the migratory policies that are chosen in the next years (whether zero migration or a controlled opening of borders), the American think-tank estimates that the Muslim population could make up between 11% and 18% of the population by 2050.

The cost of immigration

In 2018 alone, 23,400 people in Belgium asked for international protection [under asylum]. The annual cost of asylum-seekers into terms of basic welfare has risen from 120 million euros in 2014 to 200 million euros in 2018. One must add to these figures the cost of welcoming asylum-seekers, which more than doubled between 2014 and 2016, rising to 524 million euros.

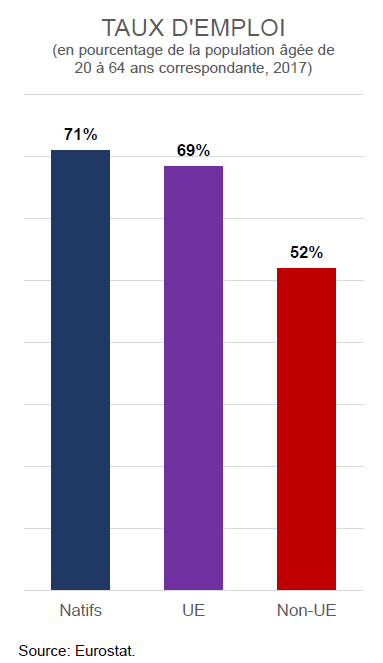

Employment rate of Belgian natives, EU migrants, and non-EU migrants (the latter overwhelmingly come from the Middle East and Africa).

More generally, the employment rate of immigrants from outside the European Union is 20 points lower than that of natives. Whether as a cause or consequence of this, 80% of those receiving social assistance are of non-Belgian origin, according to a Belgian academic, Bea Cantillon.

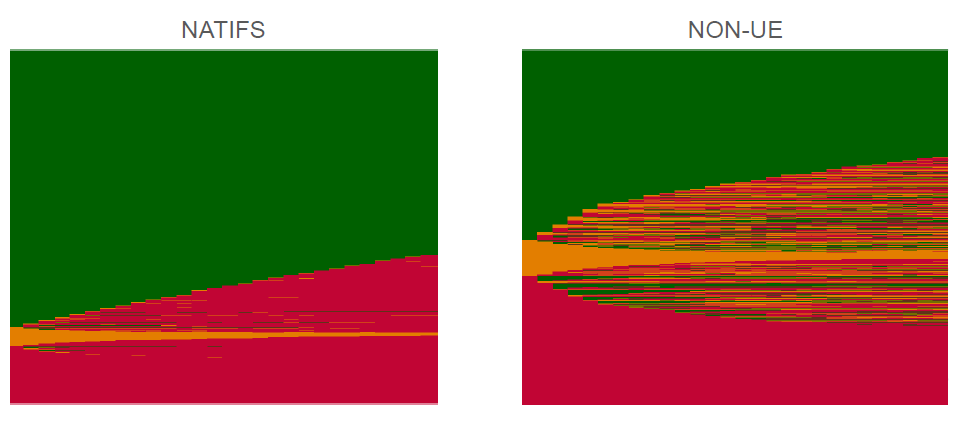

Employment patterns of representative samples of Belgian natives and non-EU migrants between 30 and 64 years of age between 2008 and 2014. Each line represents one individual. Green: working. In Orange: unemployed. Red: inactive (not seeking work). Source: Eurostat.

“Belgium will become Arab”

This prediction did not come from a dangerous conspiracy-theorist. It was expressed by a journalist, Fawzia Zouari, in the pages of the magazine Jeune Afrique [“Young Africa”] to sum up “the Islamization of minds,” in particular among of the young generation of Muslims. Though the Muslim population remains a minority, its importance is indeed growing and especially is becoming visible. Islamization is visible in several ways: in beliefs, behaviors, religious practice, and political life.

A Shiite political party named “ISLAM” was formed in 2012. It calls for the imposition of Islam’s strictest teachings: no shaking of hands between men and women, banning of mixed-sex schools and public transport, the wearing of the headscarf from the age of 12, etc, as well as the imposition of Sharia law. This political party’s [initial] electoral results are for now “anything but ridiculous,” as noted by a journalist in the magazine Le Vif [breaking the 4% threshold in the notorious Brussels neighborhood of Molenbeek, for instance] and the strict conception of Islam is progressing in Belgium.

According to a 2017 study by a Belgian foundation, 33% of Belgian Muslims do not like “the West’s culture, customs, and way of life” (women’s autonomy, alcohol, eroticism, etc), whereas 29% consider that “the laws of Islam are superior to Belgian laws.” A 2011 study highlighted the anti-Semitism of about half of the Muslim high-school students in Brussels who were polled.

The State Security Service (the Belgian international intelligence agency) observed recently an increase in groups and activities linked to Salafism, Islam’s most radical branch. One hundred Salafist organizations have been counted on Belgian soil. The mayor of Brussels for his part asserted in 2017 that “all of the mosques [in Brussels] are in the hands of Salafists.”

A shift in migration policy

Unlike France, which recently extended the right to asylum and to family reunification, Belgium has restricted these options since 2011. The Secretary of State for Asylum and Migration between 2014 and 2018, Theo Francken of the New Flemish Alliance [N-VA, a pseudo-nationalist conservative party], took a series of measures to reduce migratory flows: a strengthening of border checks and the expelling of illegal immigrants, a media campaign discouraging potential migrants from emigrating, measures to prevent asylum requests from being used to illegally settle in the country, etc.

The coalition government in power did not survive the signing by the Belgian authorities of the Marrakesh Pact on migration: at the end of 2018, the N-VA announced it was leaving the government and the country entered a new period of [political] instability. In contrast with the often politically-correct media, many voters took the opportunity of the recent European elections to vote for firmly anti-immigration party lists: the Flemish Movement [VB, a nationalist party] received 18.5% of the vote and the N-VA 27.2% [within Flanders].

Prospects

Whereas the Kingdom of Belgium has been rocked by secessionist tendencies over the past decades, dividing Flemings and Walloons, the country is now confronted with new challenges: mass immigration and the rise of political-religious demands from a part of the Muslim community. The country’s cohesion is more than ever being put to the test.

{kind=link}