More than a dozen Australian senators voted Tuesday calling for an investigation into Australia’s relationship with China, with one politician saying that Australia is a “sitting duck” to foreign influence from the Chinese Communist Party (CCP).

“We’re sitting ducks here. We’re leaving ourselves open and we’re letting the Communist Party in China come in here and undermine our democracy,” Jacqui Lambie, an independent Australian senator, said late Tuesday in response to a motion to start a Senate inquiry into Australian’s relationship with China.

The motion, led by crossbencher Rex Patrick, was supported by all the other crossbenchers: Senators Lambie, Stirling Griff, Pauline Hanson, Malcolm Roberts, and Cory Bernardi. Senators from the Greens party also supported the motion.

The motion, which required a 23 majority vote to pass, failed at 15 votes. No senators from Australia’s two major political parties—the Liberal and Labor parties—indicated their support. A total of 38 votes were cast against the motion.

Patrick said that the inquiry should examine all aspects of Australia’s relationship with China, including trade relations between the two countries, Chinese investment in Australia’s infrastructure and agriculture, and the influence and alleged interference in Australia, which includes the CCP-linked activities in Australian university campuses, as well as the CCP’s role in cyberattacks.

‘Existential Threat’

Prior to the vote, Lambie accused the Liberal and Labor parties of lacking the courage to protect Australia from Chinese foreign influence, saying that such parties have not only been influenced by money from the CCP, but also have been causing Australia to be more economically dependent on China.

Both Lambie and Patrick noted how Duncan Lewis, the former Director General of Security at the Australian Security Intelligence Organisation (ASIO), told Nine newspapers in November that the CCP is seeking to take over Australia’s political systems through “insidious” foreign interference investigations.

“It’s about time the people in this place woke up to China’s attempts to infiltrate our economy and our democracy,” Lambie said, later adding, “Everyone knows that the communist Chinese government uses money to influence our political processes.”

Lambie cited multiple examples of such alleged attempts, including a case earlier this year where AU$100,000 ($68,284) in cash was donated to the New South Wales Labor party that became part of an investigation by the state’s corruption watchdog.

“Now we’ve heard that Chinese attempts to infiltrate our politics go even further … They’re not just trying to influence politicians with money; they’re trying to get elected to sit in this chamber … wherever they can buy or get seats in the Australian parliament, they’re coming,” Lambie said.

“There are no security checks, there’s little to stop it from happening. It’s absolutely beyond shocking.”

“People are literally showing up dead. Someone who was supposedly cultivated by the Chinese government to run as a Liberal Party candidate in the Commonwealth Parliament has shown up dead,” Lambie added. “Nothing’s been proven but it’s really concerning … I think we all know what’s going on here.”

Bo “Nick” Zhao, a Melbourne luxury car dealer, was found dead in a Melbourne motel room in March. His death is under investigation. Zhao had earlier told ASIO that he was offered “a seven-figure sum” to run for a seat in Australia’s federal parliament.

“What is clear is that China is actively trying to reshape our democracy, and no one seems to be talking about that seriously enough. Honestly, where’s your courage? What are you scared of? This is not some wacky conspiracy theory. This is happening,” Lambie said.

“This is an existential threat to our society, and Australians are scared,” she later said. “They’re scared that our country is being bought up … it is being bought up.”

Patrick noted how the Director General of Security Mike Burgess “couldn’t bring himself to actually name” China last week when he announced an ASIO investigation into allegations that the CCP tried to implant Zhao into Canberra.

“Obviously, there are considerable diplomatic sensitivities involved and we have allowed ourselves to become hugely economically dependent on the export of raw materials to the Chinese market,” Patrick said.

“But it is a worrying thing when debate in this parliament is politically constipated for fear of reaction from Beijing.”

On trade, Lambie expressed disappointment and said that Liberal and Labor parties have failed to manage Australia’s economic dependence on China.

“The major parties have turned a blind eye … We’re selling off Australian values for a quick buck,” she said.

“A third of Australian exports are China-bound. We ship out more than $120 billion in iron ore and coal exports to China and our universities—shame on them!—rake in over $32 billion from international students.

“All up, we trade nearly $194 billion worth of goods and services between China and Australia—more than we trade with Japan and the United States combined. Who does that? Who leaves us in a position like that? All that money is making us complacent. There’s no reason for us to be singularly focused on China.”

Prior to the vote, the Greens’ Senator Nick McKim said that the Liberal and Labor parties were “riddled with CCP influence as they are, riddled with dirty CCP money as they are—are going to collude, once again, to vote such an inquiry down.”

“I’m telling you now, you’re all standing on the wrong side of history here. History will be written one day,” McKim added.

“History will record those who stood up and tried to address this situation, and history will record those who rolled over and let the CCP tickle their collective bellies. And unfortunately, it remains the case that both major parties in this place will be on the wrong side of history.”

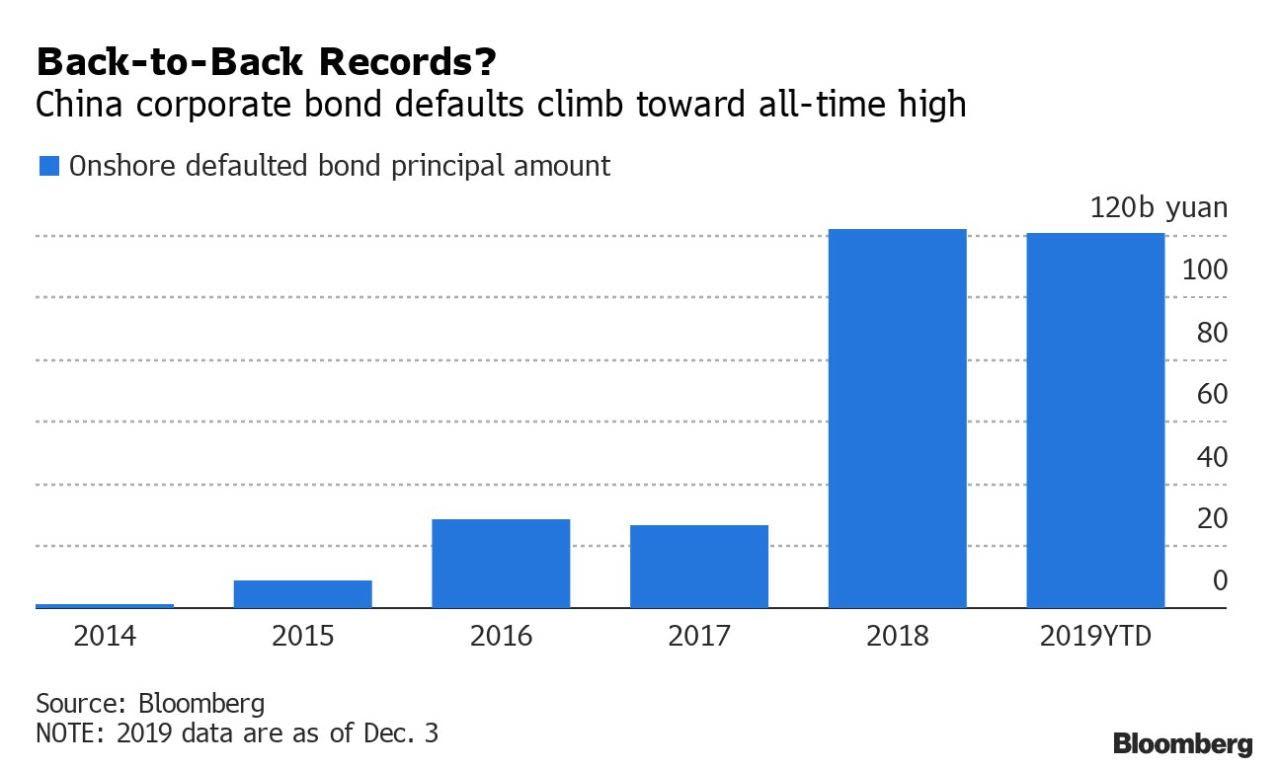

China Set To Make History With Record Number Of Bond Defaults In 2019

While China is bracing for what may be a historic D-Day event on December 9, when the “unprecedented” default of state-owned, commodity-trading conglomerate Tewoo with $38 billion in assets may take place, it has already been a banner year for Chinese bankruptcies.

According to Bloomberg data, China is set to hit another dismal milestone in 2019 when a record amount of onshore bonds are set to default, confirming that something is indeed cracking in China’s financial system and “testing the government’s ability to keep financial markets stable as the economy slows and companies struggle to cope with unprecedented levels of debt.”

After a brief lull in the third quarter, a burst of at least 15 new defaults since the start of November have sent the year’s total to 120.4 billion yuan ($17.1 billion), and set to eclipse the 121.9 billion yuan annual record in 2018.

The good news is that this number still represents a tiny fraction of China’s $4.4 trillion onshore corporate bond market; the bad news is that the rapidly rising number is approaching a tipping point that could unleash a default cascade, and in the process fueling concerns of potential contagion as investors struggle to gauge which companies have Beijing’s support. As Bloomberg notes, policy makers have been walking a tightrope as they try to roll back the implicit guarantees that have long distorted Chinese debt markets, without dragging down an economy already weakened by the trade war and tepid global growth.

“The authorities have found it hard to rescue all the companies,” said Wang Ying, a Shanghai-based analyst at Fitch Ratings, perhaps envisioning at least two banks that have experienced depositor runs in the month of November in the aftermath of an unprecedented succession of bank failures earlier in the year.

It’s not just banks however: this year’s debt woes have spread to a broad array of industries, from property developers and steelmakers to new-energy firms and software makers. The types of borrowers facing repayment difficulties has also expanded from private companies and local state-run firms to business arms of universities, an obscure and loosely regulated corner of China’s corporate world.

China’s two latest defaults involved just such a company; on Monday Peking University Founder Group shocked investors after failing to repay a 2 billion yuan bond. The same day, Tunghsu Optoelectronic Technology, a maker of photoelectric display components, also failed to deliver early repayment on both interest and principal for a 1.7 billion yuan note.

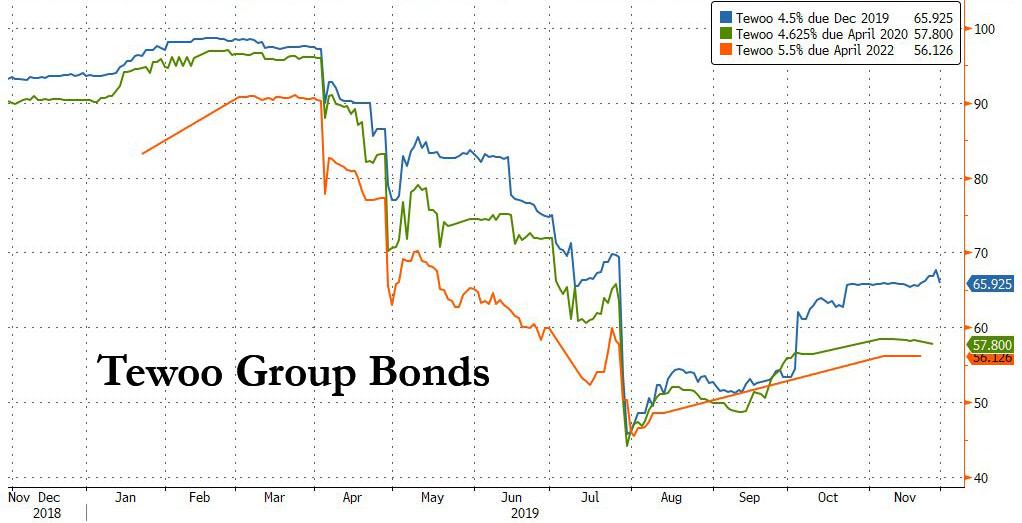

Meanwhile, as we reported last week, the signs of stress have ominously spread to China’s offshore market, which has so far been more insulated from defaults: next week, Tewoo Group, a Fortune 500 company and major commodities trader from the northern city of Tianjin, is set to become the most high profile state-owned enterprise to default in the dollar bond market in more than two decades.

The company has recently offered a debt restructuring plan that entails deep losses for investors or a swap for new bonds with significantly lower returns, the first of its kind for an offshore SOE issuer. On December 9, Tweoo bondholders need to decide if they accept a distressed exchange offer on a $300 millionbond that is likely to default on Dec. 16.

Still, despite the drumbeat of bad news, analysts remain cheerful and claim the threat of a systemic debt crisis in China remains distant.

“I don’t think it is a tipping point,” Bank of Singapore managing director Todd Schubert said. “China is a big market with a lot of issuers. In a functioning capital market, one would naturally expect some defaults.”

And while China is set to make a new record in the amount of default, the lack of a substantial increase from last year means that China’s onshore default rate is expected to remain the same as last year’s 0.5%, according to S&P.

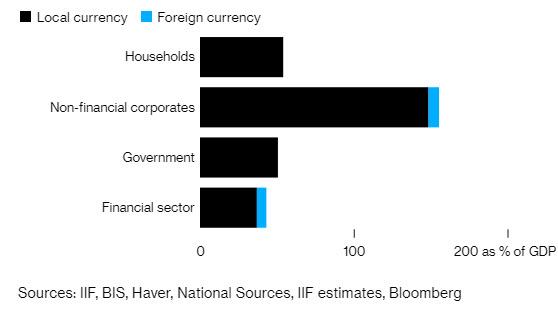

Not that Beijing has much of a choice of course: faced with a non-financial corporate debt pile that swelled to a record 165% of GDP year, Chinese policy makers are selectively allowing more bond failures in part to impose increased discipline on borrowers and investors. But not too much discipline, as the alternative could be a panic across the country’s bond market.

“Rising defaults should be a natural part of credit-market cycle,” said Anne Zhang, head of Asia fixed income for JPMorgan Private Bank. “It is long-term positive for any market to develop a good pricing mechanism for risks.”

The problem is that for Beijing it still remains a highly selective process, picking winners and losers at will; to be sure, the process would be less rocky for investors if policymakers could improve the transparency around defaults, according to Cindy Huang, an analyst at S&P Global Ratings.

“The regulators’ intention is to reduce moral hazard” while at the same time ensuring any defaults “won’t undermine socioeconomic stability or trigger systemic risks,” said Ivan Chung, head of greater China credit research and analysis at Moody’s, adding that whereas state support may be available for companies engaged in social welfare projects, for those that are more commercial in nature, “government support may not be so forthcoming.”

“So far, defaults and recovery can be unpredictable,” Huang said. “This will hinder market confidence and weaken the healthy development of China’s credit market.”

Which is why when it comes to Chinese corporate defaults, there is just one certainty looking ahead: there will be many more of them. In fact, Moody’s expects 40-50 new defaults in 2020, up from 35 this year. Considering that China is set to post its first sub-6% GDP growth year in history in 2020, this will prove an overly optimistic forecast.

No Setup? Horowitz To Claim Mifsud Wasn’t US Asset, Yet Papadopoulos Says He’s Italy’s Spook

The Washington Post reports that Attorney General William Barr’s hand-picked prosecutor could not confirm that Russiagate figure Joseph Mifsud is a US intelligence asset – thus, according to the Post, the Russiagate counterintelligence investigation against the Trump campaign could not have been a setup.

The revelation comes from the Post‘s Matt Zapotosky and Devlin Barrett (the latter of whom had a direct line to former FBI attorney Lisa Page according to her text messages), and will reportedly appear in the forthcoming report by DOJ Inspector General Michael Horowitz.

In short, Horowitz asked US Attorney John Durham if Mifsud was a US intelligence asset “deployed to ensnare the campaign,” to which Durham – who is conducting a separate review of the 2016 US election – responded that his investigation “had not produced any evidence that might contradict the inspector general’s findings on that point,” according to the Post.

Of note, Mifsud told (or seeded) 2016 Trump campaign aide George Papadopoulos with the rumor that Russia had ‘dirt’ on Hillary Clinton, on April 26, 2016. Two weeks later, he repeated it to Australian diplomat (and Clinton ally) Alexander Downer at a London bar, who relayed the Kremlin ‘dirt’ rumor to Australian authorities, which alerted the FBI – kicking off the official counterintelligence operation against the Trump campaign, dubbed Operation Crossfire Hurricane.

That said, the Post adds “The Washington Post has not reviewed Horowitz’s entire report, even in draft form. It is also unclear if Durham has shared the entirety of his findings and evidence with the inspector general, or merely answered a specific question.”

Papadopoulos, meanwhile, has posited that Mifsud is (or was) an Italian intelligence asset “who the C.I.A. weaponized,” according to an October New York Times report. Moreover, Trump attorney Rudy Giuliani told Fox News in April that Mifsud was “a counterintelligence operative, either Maltese or Italian,” who may have participated in a “counterintelligence trap” against the Trump campaign aide.

Notably, AG Barr himself traveled to Italy in Mid-September to discuss Mifsud, and was reportedly told by the head of the Italian Security Intelligence Department, Gennaro Vecchione, that Mifsud was not one of their assets.

According to a former Italian government official, Barr first met with Gennaro Vecchione, the head of Italy’s Security Intelligence Department, on Aug. 15, essentially to establish contact, and returned Sept. 27 for a second meeting with the heads of Italy’s domestic and foreign intelligence services.

Barr, the official said, “asked if Italian intelligence knew anything about Mifsud and if the Italians were aware of his role” in the Russia investigation “in terms of being involved in Italian intelligence itself or if he was politically tied with Italian political leaders allied with the Democrats.” The Italians, the official said, “explained that there is no involvement by the Italian intelligence services in this — and the fact that we don’t have any evidence of this plot.”

“They confirmed no connections, no activities, no interference,” the official said. –Washington Post, Oct. 6

We know that Papadopoulos met multiple times with Mifsud in the first half of 2016:

March 14 2016 – Papadopoulos first meets Mifsud in Italy – approximately one week after finding out he will be joining the Trump team.

March 24 2016 – Papadopoulos, Mifsud, Olga Polonskaya and unknown fourth party meet in a London cafe.

April 18 2016 – Mifsud introduces Papadopoulos to Ivan Timofeev, an official at a state-sponsored think tank called Russian International Affairs Council.

April 26 2016 – Mifsud tells Papadopoulos he’s met with high-level Russian government officials who have “dirt” on Clinton. Papadopoulos will tell the FBI he learned of the emails prior to joining the Trump Campaign.

May 13 2016 – Mifsud emails Papadopoulos an update of “recent conversations”.

Note: Papadopoulos and Mifsud reportedly both worked at the London Centre of International Law Practice. –The Markets Work

So – was Mifsud an asset of any state intelligence apparatus – or was he working with any on behalf of Hillary Clinton?

Oh, John: all the weaponized assets you sent my way [Joseph Mifsud, Alexander Downer, Stefan Halper] are all being outed from London, Rome and Canberra. Those governments are now actively cooperating with the Trump administration and have flipped on you. Your role will be exposed

— George Papadopoulos (@GeorgePapa19) May 22, 2019

And let’s not forget that during Operation Crossfire Hurricane, the FBI sent operative Stephen Halper and a mysterious woman named “Azra Turk” to befriend and conduct espionage on Papadopoulos for events which took place on UK soil – and which AG Barr has said he considers spying.

Halper – who was paid more than $1 million by the Pentagon while Obama was president – contacted Papadopoulos on September 2, 2016 according to The Daily Caller – and would later fly him out to London under the guise of working on a policy paper on energy issues in Turkey, Cyprus and Israel – for which he was ultimately paid $3,000. Papadopoulos met Halper several times during his stay, “having dinner one night at the Travellers Club, and Old London gentleman’s club frequented by international diplomats.”

As the New York Times noted om May, the London operation “yielded no fruitful information,” while the FBI has called their activities in the months before the 2016 election as both “legal and carefully considered under extraordinary circumstances,” according to the report.

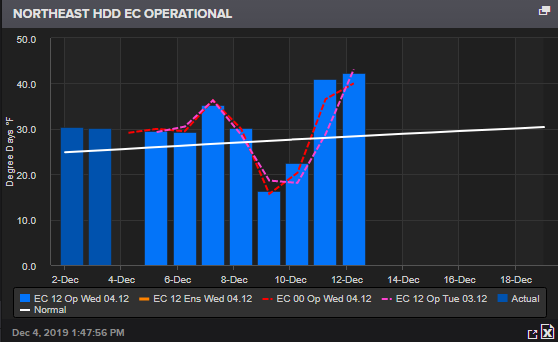

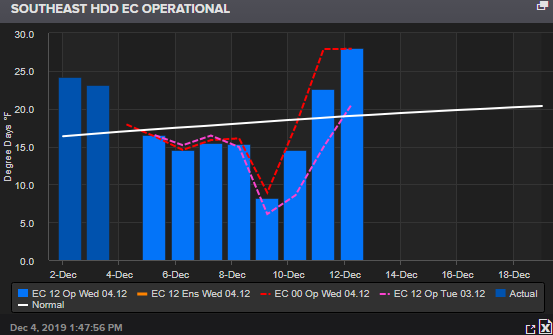

Natgas Ready To Soar? Next Cold Pattern Could Spark Energy Demand For 118 Million Americans

The Global Forecast System (GFS) weather model shows for the next 6-10 days, below-average temperatures could be seen up and down the East Coast. The result of colder than average temperatures would increase energy demand for nearly 118 million people, reported Ed Vallee, head meteorologist at Empire Weather, adding that increased energy demand could put a bid in natural gas spot prices.

“We continue to watch for much colder risks next week across the Mid Continent as the pattern re-shuffles. This will bleed into key heating demand areas of the Great Lakes and Northeast later in the 6-10 day period, upping demand risk with temperatures well below normal. Beyond this time frame into mid-month, most data remains cooler than normal, especially in the northern tier of the country, and into the Northeast. This would allow heating demand to remain elevated, but upcoming weather data and forecasts will help drive price action as this challenging forecast period is sorted out,” said Vallee.

GFS day 11. One run change. 20+°F of change across the Plains.

Heating degree days (HDD) for the Northeast shows an above-trend reading through next week, which the amount of energy it takes to heat a building will jump.

HDD readings for the Southeast are also above trend, spiking in the latter parts of next week.

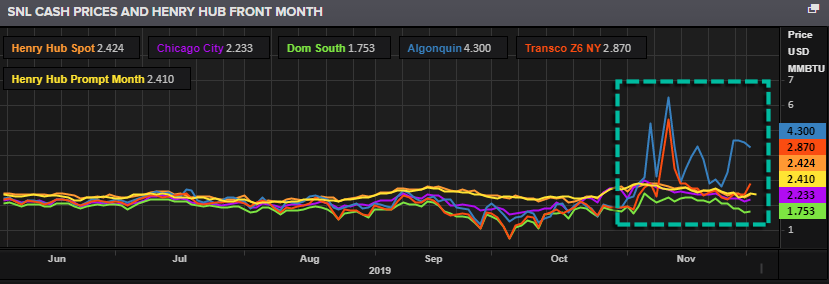

Natural gas spot prices for Algonquin Citygate (New York) and Transco (New York) have been elevated for the last month thanks to colder weather in the Northeast.

NYMEX Henry Hub Natural Gas spot prices have remained in a descending channel for November and into early December. Warming conditions and oversupply issues remain significant fundamental issues weighing on prices. Though if energy demand on the East Coast picks up in the next 6-10 day period, spot prices could start to stabilize.

Environmental journalists and advocates have in recent weeks made a number of apocalyptic predictions about the impact of climate change. Bill McKibben suggested climate-driven fires in Australia had made koalas “functionally extinct.” Extinction Rebellion said

“Billions will die” and “Life on Earth is dying.”

Viceclaimed the “collapse of civilization may have already begun.”

Few have underscored the threat more than student climate activist Greta Thunberg and Green New Deal sponsor Rep. Alexandria Ocasio-Cortez. The latter said,

“The world is going to end in 12 years if we don’t address climate change.”

“Around 2030 we will be in a position to set off an irreversible chain reaction beyond human control that will lead to the end of our civilization as we know it.”

Sometimes, scientists themselves make apocalyptic claims.

“It’s difficult to see how we could accommodate a billion people or even half of that,” if Earth warms four degrees, said one earlier this year. “The potential for multi-breadbasket failure is increasing,” said another. If sea levels rise as much as the Intergovernmental Panel on Climate Change predicts, another scientist said, “It will be an unmanageable problem.”

Apocalyptic statements like these have real-world impacts. In September, a group of British psychologists said children are increasingly suffering from anxiety from the frightening discourse around climate change. In October, an activist with Extinction Rebellion (”XR”) — an environmental group founded in 2018 to commit civil disobedience to draw awareness to the threat its founders and supporters say climate change poses to human existence — and a videographer, were kicked and beaten in a London Tube station by angry commuters. And last week, an XR co-founder said a genocide like the Holocaust was “happening again, on a far greater scale, and in plain sight” from climate change.

Climate change is an issue I care passionately about and have dedicated a significant portion of my life to addressing. I have been politically active on the issue for over 20 years and have researched and written about it for 17 years. Over the last four years, my organization, Environmental Progress, has worked with some of the world’s leading climate scientists to prevent carbon emissions from rising. So far, we’ve helped prevent emissions increasing the equivalent of adding 24 million cars to the road.

I also care about getting the facts and science right and have in recent months corrected inaccurate and apocalyptic news media coverage of fires in the Amazon and fires in California, both of which have been improperly presented as resulting primarily from climate change.

Journalists and activists alike have an obligation to describe environmental problems honestly and accurately, even if they fear doing so will reduce their news value or salience with the public. There is good evidence that the catastrophist framing of climate change is self-defeating because it alienates and polarizes many people. And exaggerating climate change risks distracting us from other important issues including ones we might have more near-term control over.

I feel the need to say this up-front because I want the issues I’m about to raise to be taken seriously and not dismissed by those who label as “climate deniers” or “climate delayers” anyone who pushes back against exaggeration.

With that out of the way, let’s look whether the science supports what’s being said.

First, no credible scientific body has ever said climate change threatens the collapse of civilization much less the extinction of the human species.

“‘Our children are going to die in the next 10 to 20 years.’ What’s the scientific basis for these claims?” BBC’s Andrew Neil asked a visibly uncomfortable XR spokesperson last month.

“These claims have been disputed, admittedly,” she said. “There are some scientists who are agreeing and some who are saying it’s not true. But the overall issue is that these deaths are going to happen.”

“But most scientists don’t agree with this,” said Neil. “I looked through IPCC reports and see no reference to billions of people going to die, or children in 20 years. How would they die?”

“Mass migration around the world already taking place due to prolonged drought in countries, particularly in South Asia. There are wildfires in Indonesia, the Amazon rainforest, Siberia, the Arctic,” she said.

But in saying so, the XR spokesperson had grossly misrepresented the science.

“There is robust evidence of disasters displacing people worldwide,” notes IPCC, “but limited evidence that climate change or sea-level rise is the direct cause”

What about “mass migration”?

“The majority of resultant population movements tend to occur within the borders of affected countries,” says IPCC.

It’s not like climate doesn’t matter. It’s that climate change is outweighed by other factors. Earlier this year, researchers found that climate “has affected organized armed conflict within countries. However, other drivers, such as low socioeconomic development and low capabilities of the state, are judged to be substantially more influential.”

Last January, after climate scientists criticized Rep. Ocasio-Cortez for saying the world would end in 12 years, her spokesperson said

“We can quibble about the phraseology, whether it’s existential or cataclysmic.”

He added, “We’re seeing lots of [climate change-related] problems that are already impacting lives.”

That last part may be true, but it’s also true that economic development has made us less vulnerable, which is why there was a 99.7% decline in the death toll from natural disasters since its peak in 1931.

In 1931, 3.7 million people died from natural disasters. In 2018, just 11,000 did. And that decline occurred over a period when the global population quadrupled.

What about sea level rise? IPCC estimates sea level could rise two feet (0.6 meters) by 2100. Does that sound apocalyptic or even “unmanageable”?

Consider that one-third of the Netherlands is below sea level, and some areas areseven meters below sea level. You might object that Netherlands is rich while Bangladesh is poor. But the Netherlands adapted to living below sea level 400 years ago. Technology has improved a bit since then.

What about claims of crop failure, famine, and mass death? That’s science fiction, not science. Humans today produce enough food for 10 billion people, or 25% more than we need, and scientific bodies predict increases in that share, not declines.

The United Nations Food and Agriculture Organization (FAO) forecasts crop yields increasing 30% by 2050. And the poorest parts of the world, like sub-Saharan Africa, are expected to see increases of 80 to 90%.

Nobody is suggesting climate change won’t negatively impact crop yields. It could. But such declines should be put in perspective. Wheat yields increased 100 to 300% around the world since the 1960s, while a study of 30 models found that yields would decline by 6% for every one degree Celsius increase in temperature.

Rates of future yield growth depend far more on whether poor nations get access to tractors, irrigation, and fertilizer than on climate change, says FAO.

All of this helps explain why IPCC anticipates climate change will have a modest impact on economic growth. By 2100, IPCC projects the global economy will be 300 to 500% larger than it is today. Both IPCC and the Nobel-winning Yale economist, William Nordhaus, predict that warming of 2.5°C and 4°C would reduce gross domestic product (GDP) by 2% and 5% over that same period.

Does this mean we shouldn’t worry about climate change? Not at all.

One of the reasons I work on climate change is because I worry about the impact it could have on endangered species. Climate change may threaten one million species globally and half of all mammals, reptiles, and amphibians in diverse places like the Albertine Rift in central Africa, home to the endangered mountain gorilla.

But it’s not the case that “we’re putting our own survival in danger” through extinctions, as Elizabeth Kolbert claimed in her book, Sixth Extinction. As tragic as animal extinctions are, they do not threaten human civilization. If we want to save endangered species, we need to do so because we care about wildlife for spiritual, ethical, or aesthetic reasons, not survival ones.

And exaggerating the risk, and suggesting climate change is more important than things like habitat destruction, are counterproductive.

For example, Australia’s fires are not driving koalas extinct, as Bill McKibben suggested. The main scientific body that tracks the species, the International Union for the Conservation of Nature, or IUCN, labels the koala “vulnerable,” which is one level less threatened than “endangered,” two levels less than “critically endangered,” and three less than “extinct” in the wild.

Should we worry about koalas? Absolutely! They are amazing animals and their numbers have declined to around 300,000. But they face far bigger threats such as the destruction of habitat, disease, bushfires, and invasive species.

Think of it this way. The climate could change dramatically — and we could still save koalas. Conversely, the climate could change only modestly — and koalas could still go extinct.

The monomaniacal focus on climate distracts our attention from other threats to koalas and opportunities for protecting them, like protecting and expanding their habitat.

As for fire, one of Australia’s leading scientists on the issue says,

“Bushfire losses can be explained by the increasing exposure of dwellings to fire-prone bushlands. No other influences need be invoked. So even if climate change had played some small role in modulating recent bushfires, and we cannot rule this out, any such effects on risk to property are clearly swamped by the changes in exposure.”

Nor are the fires solely due to drought, which is common in Australia, and exceptional this year. “Climate change is playing its role here,” said Richard Thornton of the Bushfire and Natural Hazards Cooperative Research Centre in Australia, “but it’s not the cause of these fires.”

The same is true for fires in the United States. In 2017, scientists modeled 37 different regions and found “humans may not only influence fire regimes but their presence can actually override, or swamp out, the effects of climate.” Of the 10 variables that influence fire, “none were as significant… as the anthropogenic variables,” such as building homes near, and managing fires and wood fuel growth within, forests.

Climate scientists are starting to push back against exaggerations by activists, journalists, and other scientists.

“While many species are threatened with extinction,” said Stanford’s Ken Caldeira, “climate change does not threaten human extinction… I would not like to see us motivating people to do the right thing by making them believe something that is false.”

I asked the Australian climate scientist Tom Wigley what he thought of the claim that climate change threatens civilization. “It really does bother me because it’s wrong,” he said. “All these young people have been misinformed. And partly it’s Greta Thunberg’s fault. Not deliberately. But she’s wrong.”

But don’t scientists and activists need to exaggerate in order to get the public’s attention?

“I’m reminded of what [late Stanford University climate scientist] Steve Schneider used to say,” Wigley replied.

“He used to say that as a scientist, we shouldn’t really be concerned about the way we slant things in communicating with people out on the street who might need a little push in a certain direction to realize that this is a serious problem. Steve didn’t have any qualms about speaking in that biased way. I don’t quite agree with that.”

Wigley started working on climate science full-time in 1975 and created one of the first climate models (MAGICC) in 1987. It remains one of the main climate models in use today.

“When I talk to the general public,” he said, “I point out some of the things that might make projections of warming less and the things that might make them more. I always try to present both sides.”

Part of what bothers me about the apocalyptic rhetoric by climate activists is that it is often accompanied by demands that poor nations be denied the cheap sources of energy they need to develop. I have found that many scientists share my concerns.

“If you want to minimize carbon dioxide in the atmosphere in 2070 you might want to accelerate the burning of coal in India today,” MIT climate scientist Kerry Emanuel said.

“It doesn’t sound like it makes sense. Coal is terrible for carbon. But it’s by burning a lot of coal that they make themselves wealthier, and by making themselves wealthier they have fewer children, and you don’t have as many people burning carbon, you might be better off in 2070.”

Emanuel and Wigley say the extreme rhetoric is making political agreement on climate change harder.

“You’ve got to come up with some kind of middle ground where you do reasonable things to mitigate the risk and try at the same time to lift people out of poverty and make them more resilient,” said Emanuel.

“We shouldn’t be forced to choose between lifting people out of poverty and doing something for the climate.”

Happily, there is a plenty of middle ground between climate apocalypse and climate denial.

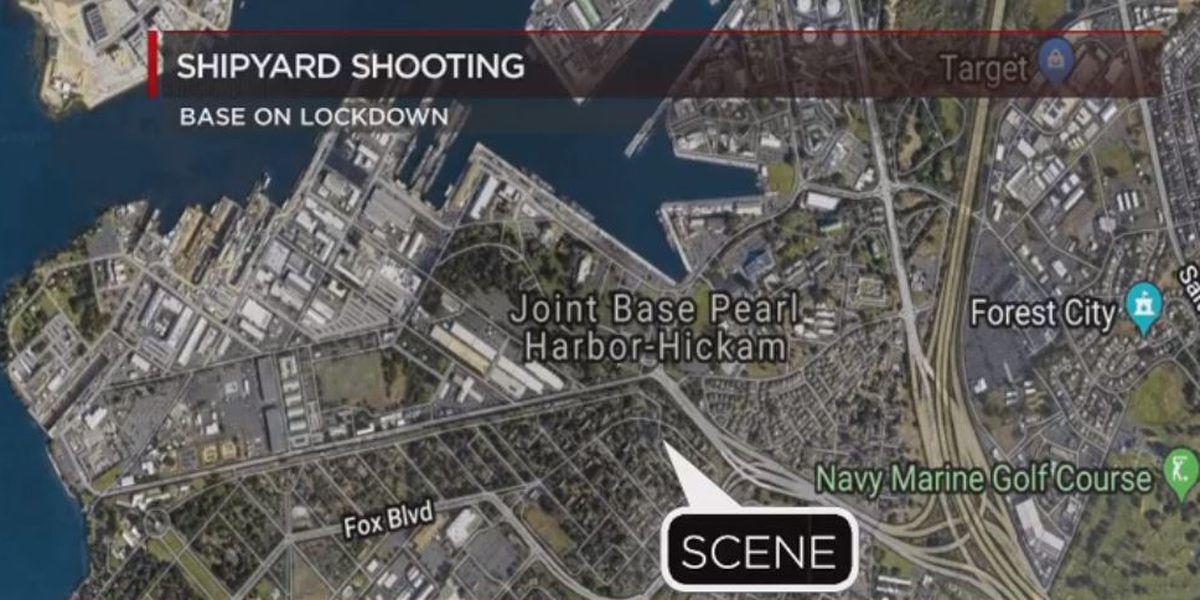

Active Shooter At Pearl Harbor, Multiple Victims Reported

Live Feed:

* * *

Pearl Harbor Naval Shipyard in Hawaii is on lockdown after multiple victims have been reported in an active shooter situation.

Sources tell Hawaii News Now that several civilians are among the gunshot victims. The Mirror reports that two victims are said to be critical, while a third is stable.

JBPHH security forces have responded to a reported shooting at the Pearl Harbor Naval Shipyard. The incident occurred at approximately 2:30 p.m. Due to the ongoing security incident, access/gates to #JBPHH are closed. We will update when we have further information. pic.twitter.com/6uZulGOUTx

— Joint Base Pearl Harbor-Hickam (@JointBasePHH) December 5, 2019

The base’s 15th Wing confirmed, there was a shooter on the base. It said on Facebook:

“ALERT: There is an active shooter on base, please seek a secure location until further notice.”

A PA system is urging people to take cover. Base personnel also received text messages alerting them of the situation. Witnesses tell Hawaii News Now that the shooting happened at Drydock 2. First responders were called to the scene about 2:30 p.m. local time (730pm ET)

Trump-Bezos Round 2: Amazon Faces Broad Antitrust Probe Of Cloud Business

Having lodged a formal complaint (cough, bad loser, cough) after losing the hotly contested contract to provide cloud computing services to the Pentagon, it appears the richest man in the world is about to face round 2 against the most powerful man in the world as Bloomberg reports that, according to people familiar with the matter, U.S. antitrust enforcers have broadened their scrutiny of Amazon beyond its retail operations to include its massive cloud-computing business.

The contract was a big win for Microsoft CEO Satya Nadella, who has prioritized cloud computing.

As a reminder, in August (before the Joint Enterprise Defense Infrastructure, or JEDI, deal was concluded) the Pentagon’s Inspector General has launched a probe into key aspects of the bid process – including potential conflicts of interest, after The WSJ publicized evidence showing that senior Amazon executives met with senior DoD officials, including then-Defense Secretary James Mattis, to discuss the project before the bidding even began.

The deal did not go Bezos’ way, and so – as is the norm in today’s world, they cried foul and lodged a formal complaint:

“Numerous aspects of the JEDI evaluation process contained clear deficiencies, errors, and unmistakable bias – and it’s important that these matters be examined and rectified.”

But now, as Bloomberg details, investigators at the U.S. Federal Trade Commission have been asking software companies recently about practices around Amazon’s cloud unit, known as Amazon Web Services.

Specifically, the outreach by the FTC signals that the agency, which is already looking at Amazon’s conduct in its vast online retail business, is taking a broader look at the company to determine whether it could be violating antitrust laws and harming competition.

One issue the FTC could look at is whether Amazon has an incentive to discriminate against those software companies, which sell their products to clients of AWS, while at the same time competing with Amazon. The fear is that Amazon could punish the companies that work with other cloud providers and favor those that it works with exclusively.

The dynamic echos that in Amazon’s retail marketplace, where third-party sellers depend on the platform to reach customers because of its size, but in many cases they also compete with Amazon’s own products. That’s a conflict that threatens competition, according to critics.

Clash of the Titans? How long before Amazon lodges another formal complaint about being under an antitrust probe? We are sure not long, but for now, “Bezos vs Trump 2: This Time It’s Personal” is set to accelerate in the coming months…

As for Amazon, the loss of the $10 billion award over 10 years doesn’t stand out as critical, considering the company reported $242 billion in revenue and $11.4 billion in net income over the 12 months ended March 31. But, as we noted previously, a loss of government confidence in AWS (which generated $2.2 billion of net income in the first quarter, up 57% year-over-year and representing two thirds of the consolidated total) could be significant.

As a D.C.-based observer told ADG in April:

“The AWS story, as sold to enterprise customers and the Street, is built upon the [C.I.A] reference case and the cash that has come in from that deal.”

Gartner puts AWS’s market share at 48% and Microsoft’s at 16 – we wonder how long before that changes?

On the heels of President Donald Trump’s attempts to designate Mexican drug cartels as foreign terrorist organizations (FTOs), an attack uncomfortably close to U.S. soil has the Mexican government scrambling and the president fuming. At least 22 died over the weekend as rival cartels struggling for Northern Mexico turf dominance clashed with local law enforcement in Villa Union, Coahuila, an hour’s drive from Eagle’s Pass, TX. The brazen attack seemingly was directed at the Mexican government to send a warning as to who is in charge.

The town of Villa Union was, in effect, shredded, riddled with bullets, as a heavily armed group of alleged cartel members stormed the community in a convoy of trucks. When they attacked local government offices, the federales attempted to intervene. Fleeing, the cartel kidnapped locals and their vehicles, including a hearse on the way to a funeral.

To Designate Or Not

Mexican officials fear that an FTO designation will allow unilateral interventions across the southern border. But Trump is undeterred, saying as much in a recent interview with Bill O’Reilly:

“They will be designated. I’ve been working on that for the last 90 days. Designation is not that easy. You have to go through a process, and we are well into that process.”

At first, there was a lukewarm reception to Trump’s FTO declaration, but now more U.S. government officials support the idea. Former Acting ICE Director Tom Homan believes it’s time for an intervention on Mexican soil. Although he credited the Mexican law enforcement response, he pointed out a failing that allows cartel violence to creep closer to the United States:

“They’re not well-trained, they’re not well-equipped, and they certainly don’t have the expertise at dismantling large criminal organizations like the U.S. law enforcement does. We’ve proven that in Panama with [ruler Manuel] Noriega, we proved that in Colombia with [Pablo Escobar]. The United States can go down to Mexico and help them address this crisis once and for all.”

That is, if the cartels are FTO designated. But securing a commitment from Mexico President Andres Manuel Lopez Obrador — who has been clear in denouncing the terrorist label as none of Trump’s business – is simply a pipe dream so far. Lopez emphatically stands his ground, telling the United States to rethink any offensive action in Mexico: “Our problems will be solved by Mexicans. We don’t want any interference from any foreign country.”

And then we have a dissenting opinion from Ambassador David Johnson, vice president of the International Narcotics Control Board and former assistant secretary of state for International Narcotics and Law Enforcement Affairs. He is lobbying to stay the course:

“Terrorists use violence to expand a political goal. These criminals are interested in money, not politics. They don’t want the responsibility and headaches that come with political control since it could interfere with their profit-maximizing goals. The key reason for not labeling them terrorists is because that is not what they are. They are in it for the money. Period.”

Derek Maltz, former special agent in charge of the Drug Enforcement Administration Special Operations Division in New York, is all for doing whatever it takes to stem the flow of violence. He declared, “Designating the cartels as terrorists and implementing a focused operational plan will save a tremendous amount of lives.”

Trump Is Stubbornly Dug In

Trump has made it his mission to stop illegal immigration, illicit drug trade, human trafficking, and violence on the north side of the shared border. A safer Mexico creates a safer America. With the recent uptick in violence in Mexico, it would seem the country should embrace the help it so desperately needs. Perhaps putting away control issues and focusing on the greater good would make Lopez Obrador and Trump shake hands and get the job done.

Else we may see the violence enacted in Villa Union cross our border.

“Is Something Going Wrong? Is Something Broken?” Quants Running “Scared” As Nothing Makes Sense

It was a year where the S&P put the mini bear market of December 2018 in the dust, and after a dramatic reversal which saw most central banks flip from hawkish to dovish throughout the year…

… the MSCI World index is just shy of its January 2018 highs, and the S&P has returned an impressive 24% (despite the jittery start to December), and stands at all time record highs, despite, paradoxically, a year of record equity fund outflow.

On paper, this should have been a great year for investors after a dismal 2018. In reality, however, 2019 has been just as painful for not just for hedge funds, which have substantially underperformed the S&P again and in October saw a record 8 consecutive months of outflows, the most since the financial crisis…

… but especially for quants, which after a relatively solid year, suffered the September quant crash that destroyed most of their YTD gains, and have generally been unable to find their bearings in a year in which nothing seemed to work.

It’s also Georg Elsaesser, a Frankfurt-based fund manager at Invesco, is trying to calm down his newbie quant clients as choppy stock moves make life difficult for anyone trading factors, which wire up all those systematic portfolios on Wall Street.

“Some of them are kind of scared,” Elsaesser told Bloomberg. “They’re asking the questions: Is something going wrong? Is something broken?”

Well actually, the answer is yes: the market is broken, and you can thank central banks for that.

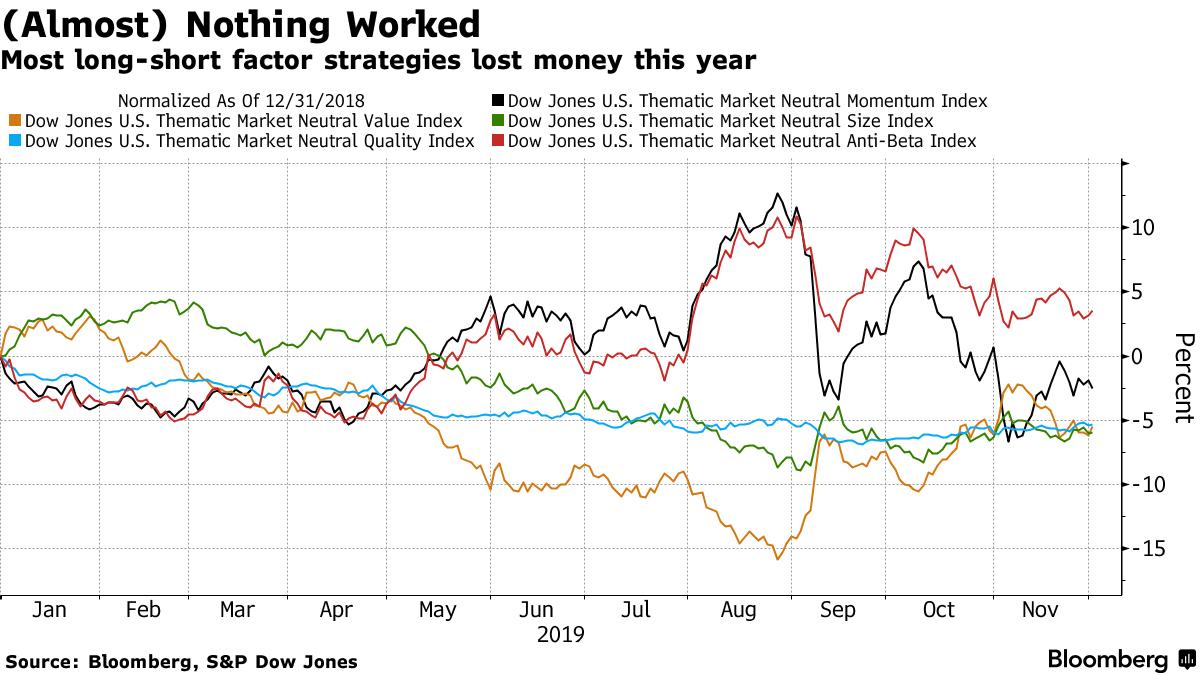

The problem is that the rules-based method of investing based on grouping of stocks by traits like their value, momentum, or balance sheet quality, is misfiring again this year, even more so than it in 2018, when quants suffered their worst year since the financial crisis, and left quant icons such as Cliff Asness’ AQR, suffering its biggest loss since inception.

Here is another problem: while the broader stock market, propped up by central bank stimulus, rate cuts and “NOT QE”, has been on a tear, a peek below the calm surface reveals a tempest of position reversals and catastrophic, at time, performance as a slew of traditional long-short styles are in the red. Market-neutral portfolios have lost 1% this year, according to a Hedge Fund Research index.

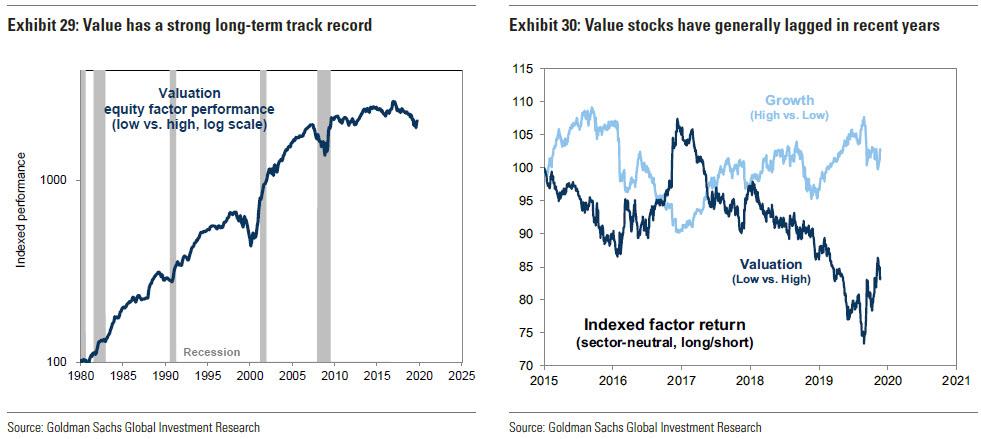

While there are numerous, often conflicting, explanations why factor portfolios disappointed in 2019, one can offer some generalizations. Persistent caution over the growth outlook whipsawed riskier trades like value and small caps which slumped all year then soared at the start of September, momentum trades worked all year then got crushed in September, the most shorted stocks soared, and the most heavily owned stocks barely outperformed.

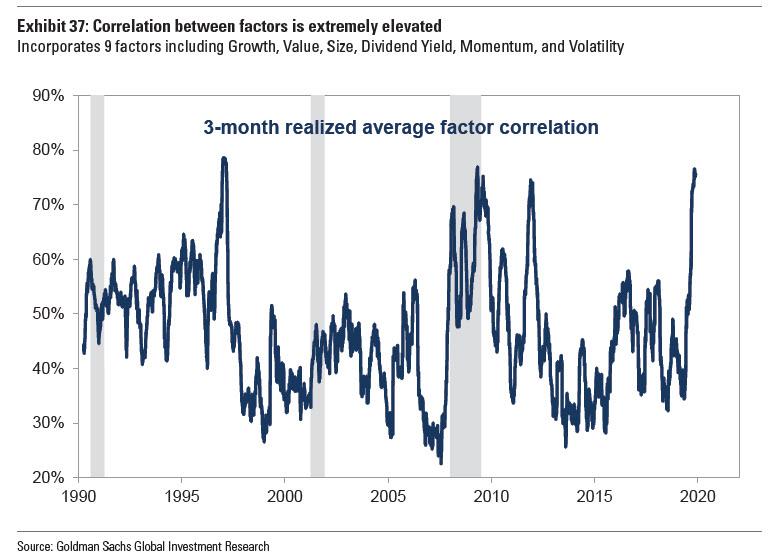

Another, more practical explanation, is that in a world where factors are supposed to offer diversification of risk, they did just the opposite, and the correlation between the most popular factors such as growth, value, size, dividend yield, momentum and volatility exploded. As Goldman wrote in its 2020 year ahead outlook, the average realized pairwise correlation of our factors has reached levels only achieved twice in the last 30 years: in 2Q 2009 as the equity market bottomed in the Financial Crisis and in 1Q 1997 as the Tech Bubble began to build. These elevated correlations underscore the importance that risk sentiment in driving recent market rotations, but more importantly explain why, well, nothing worked, as all of these often conflicting strategies eventually ended up offsetting each other.

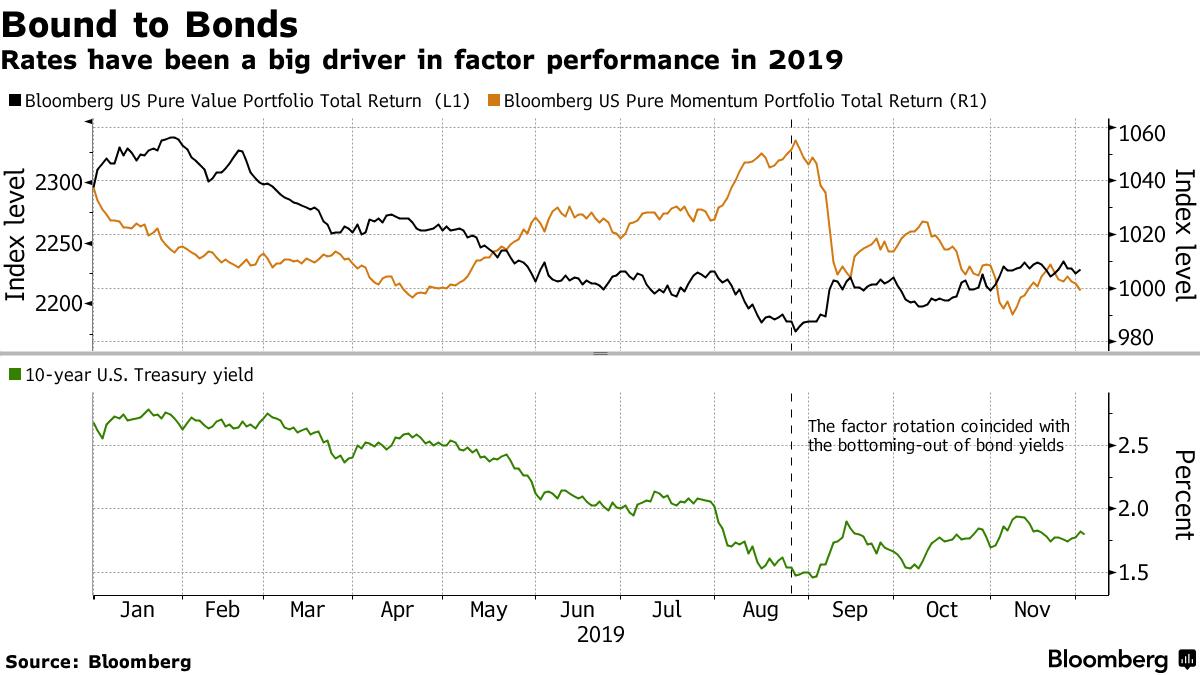

The soaring correlations can also be explained by the bond market: as interest rates dominated factor returns this year, diversification benefits weakened according to analysts at Nomura Instinet.

In light of this dismal repeat performance, it is easy to see why Elsaesser is on the defensive: he is one of many in the systematic community trying to win back hearts with the pitch that factors are time-tested, designed for the long haul and backed by some of the smartest folk in finance and academia (so was LTCM). But as the investing style closes a year to forget, patience is wearing thin among the market-neutral crowd, which plight Bloomberg covered in an article this morning.

“The experienced investors say it’s normal noise in the long run,” Elsaesser said. “But it certainly means we need to explain more.”

You certainly do: after yet another year of carnage for quants, billions of dollars are fleeing the industry which as recently as a few years ago was considered the “next big thing” on Wall Street, now that fundamental analysis no longer matters (again, thanks to central banks).

Sure enough, outflows have soared, and may also have hit industry performance. Market-neutral equity hedge funds lost nearly $4 billion YTD, according to Eurekahedge. Institutions even redeemed $54 billion from long-only quantitative stock funds in the first three quarters, according to eVestment.

However, outflows will continue as long as days like Sept 9 occasionally emerge out of the blue.

On that day, the S&P 500 Index closed flat, equity volatility cruised around its five-year average and commodities were unexciting. Yet factor investors experienced the biggest rotation in a decade after value briefly broke out of its funk at the expense of high-flying momentum stocks. As we showed then, that one day was the most painful for quant funds since the great quant crash of August 2007! And worst of all, nobody knew just why it happened as swiftly as it did.

As a result, Bloomberg writes that quants who failed to diversify into winners like low volatility – which until the September shock would be most of them – are in “soul-searching mode.” Are factors like value structurally broken? Can market-neutral styles roar back to life over the long haul?

The best summary of how nothing for quants has worked this year (and last year) came from Ian Heslop, London-based head of global equities at Merian Global Investors, who did his best LTCM impression: “Some of the themes we expected to diversify our returns in a period of underperformance of value haven’t worked as well.”

That said, it’s not been all gloom. A handful of long-only factor strategies are posting 20%-plus gains this year. But they’re still lagging cap-weighted indexes. Sanford C. Bernstein estimates systematic long-only managers have lagged their benchmark by 2% points on average.

The pain is most acute for market-neutral quants, whose strategies including factor styles gained a paltry 1.2% this year as of Nov. 26 compared with 9.8% for equity long-short funds and 8.7% for discretionary macro funds, according to Credit Suisse data. Recent research by Robeco showed that it was the short legs of factor strategies that have been a drag on performance this year, arguing the value of the investing style mostly comes from the long leg.

Well yes: this is another way of saying that in a manipulated, centrally-planned market, there is no need for short pair trades, i.e., there is no need to hedge. Incidentally, this is precisely what we said all the way back in 2013 when we wrote that the only alpha-generating strategy in a broken market is to go short the most held names and go long the most shorted ones. 6 years later, Bank of America is writing just how correct we were, pointing out that going against the Wall Street crowd has never been more profitable…

And yet, even though we write about this year after year, there will always be those who could never have possibly anticipated this:

“Whether this has been driven by flow events or not, it is finite, it’s very unusual,” said Heslop. His $4.5 billion Merian Global Equity Absolute Return Fund has seen its assets shrink by more than half this year.

Then there are those who have been betting – year after year – on mean reversion, certain that value was poised for a rebound. They too were left disappointed. As Bloomberg notes, and as we cautioned, since reviving briefly in September, the factor has flatlined since despite JPM’s Marko Kolanovic predicting the value to momentum rotation is a “once in a decade opportunity.” Here, as Bloomberg accurately notes, its outlook continues to divide quant land between bears citing low yields and weak growth, and bulls touting cheap relative valuations.

Alas, neither strategy is beating the S&P500 which is the one asset class directly propped up by central banks.

So where do we stand now?

Well, after another disastrous year for the sector, some quants are revamping strategies. At Merian, Bloomberg notes that Heslop’s team this year tweaked models to penalize exposure to highly correlated factors and to make allocations more defensive against downside risks; it is now on the hunt for smarter definitions of value. The irony, of course, is that most of Heslop’s peers are also doing precisely the same thing, and the outcome will be yet another year of underperformance for quants who are not only fighting themselves, but are also locked in a fight for survival against central banks who have turned the logic of investing and Finance 101 on its head.

Some funds are also deploying alternative data and machine learning in a bid to re-invent now widely known factor strategies. That said, such newfangled methods are a contentious move for a community that’s netted billions riding established factors back-tested over decades. Invesco’s Elsaesser for one is skeptical.

“It’s like a perfect storm for factors at the moment, but they have done what you would expect them to do,” he said. “We’ve seen these drawdowns; we’ve seen them recover. We know the essence of them is the very strong factor logic.”

There is just one problem: when you have a centrally planned market, you don’t have logic. We wonder just how many more year it will take the best and the brightest to finally grasp this simple observation which we have been pounding the table on since our inception in 2009…

Investing is all about probabilities. If the perceived odds of an event are high, certain securities will be priced based on those expected probabilities. The corollary is that when an event is perceived as almost impossible, securities do not price in any chance of it occurring. If that event does occur, all sorts of securities need to re-price—often quite rapidly. I like to spend my time pondering what potential events the market completely ignores. Of all potential economic outcomes, the one that is least anticipated and least priced in, is an uptick in inflation.

It is said that generals always fight the last war. In terms of macro-portfolio wars, Japan’s experience with deflation colors all views. This seems odd to me because we have over two millennia of history showing inflation and currency debasements to be universal constants, with one outlier in Japan. The question is if Japan is the new normal or a true outlier?

Academics have studied the causes and effects of inflation ever since emperors and kings fixated on halting its effects. Despite a massive body of work, there is little agreement amongst experts on the causes of inflation. Since I tend to ignore “experts,” let me start by giving you the Kuppy definition of inflation. “Inflation is when too much of a certain currency chases a scarce resource and pushes its price higher when defined in terms of that currency.” Using that definition, we’ve actually had rather dramatic inflation over the past decade—it just hasn’t shown up yet in the core consumer goods that central bankers are often concerned about.

Did they time-stamp the cyclical low in yields?

When a country prints money, no one knows where within the economic ecosystem it will ultimately flow. If a resource is scarce, it tends to experience inflation—when it is artificially scarce, it has even more extreme inflation. Just think of where the money printing has ended up this cycle; bonds (central banks restricted supply by buying them), stocks (PE and buybacks have restricted supply), gateway city residential housing (local municipalities have restricted supply), medical costs (systematic dysfunction has restricted supply), vintage wines (they aren’t being produced anymore), college education (supply restricted again), I can go on, but you get the point. Meanwhile, traditional inflation stalwarts like food and energy have remained suppressed due to technological advancements, reduced logistical costs and excess liquidity, which has allowed capacity to overshoot and lead to price deflation. To say that we’ve not had inflation over the past decade is wrong, we just haven’t had inflation in places that are key components of the CPI basket.

However, that may be changing. I believe that the number of sectors with restricted supply are starting to expand. Let’s look at labor, which historically has been a primary source of inflation. It’s no secret that US unemployment is at historic lows, laborers now have bargaining power and wages are rapidly increasing—with increases made more extreme by minimum wage laws, healthcare inflation and new mandates in various states. The cost of labor goes into almost every finished good—particularly in a labor-intensive service economy. Politicians on both sides seem willing to pass laws that give labor a bigger share of the pie—what will that do to inflation?

Now think of energy; it’s a crazy world out there and global energy security is no longer guaranteed. Prices have been suppressed for the past few years by excess production due to uneconomic shale—that’s clearly reversing as the funding has been cut off. Where do you think energy prices go if shale growth flat-lines or goes in reverse? What about when key producing regions devolve into chaos? Tanker rates are also expanding—that increases energy prices as well.

Now think about consumer goods; the past few decades were all about increased globalization where manufacturing migrated to the cheapest possible location. Trade wars and regional balkanization upend this trend. Now there ought to be an implicit geopolitical risk premium priced into gross margins on every good. Supply chain disruptions further increase costs. If globalism was deflationary, isn’t the reverse inflationary?

Think about what venture capital has done to costs. Thousands of businesses are losing hundreds of billions a year to gain market share in rather prosaic industries. Think about what Uber has done to transport costs or Chewy has done to the cost of dog food. These are all subsidized by VC firms so they can dump IPOs on unsuspecting retail bag-holders. As these businesses are forced to raise pricing in order to become sustainable, what will that do to consumer inflation? Won’t all sorts of sectors also gain pricing power, now that they don’t have to compete with someone who sells a Dollar for 80 cents hoping to make it up with volume? Isn’t the collapse of the Ponzi Sector bubble inherently inflationary?

What about all the supply restriction as ESG takes its toll on economies? If you can’t get permits to build a new coal mine or oil pipeline, yet demand keeps growing, won’t pricing increase as well?

I can go on and on. All the trends that were deflationary are slowly going in reverse. We haven’t seen the effects of this show up in the data yet, largely because the global economy is rapidly deteriorating, which is putting a brake on the demand side. However, even with the global economy slowing, inflation is starting to tick up in the US. Can the rest of the world be far behind us?

Of course, government policy drives all of this. I think it is obvious that we’ve finally reached the limits of monetary policy. Does the ECB taking rates 10 basis points more negative do anything but accelerate the bankruptcy of the Eurozone banking system? Does it increase consumption or capital expenditures? Of course not. If anything, it just starves the system of capital by taking everyone’s return on capital investment down towards zero and below. Who invests when expected returns are negative? What the world needs is a big reset of the system where leveraged firms default, solvent firms pick up the pieces and get to earn excess returns due to their past fiscal sobriety. Since we live in a democracy, that won’t happen, instead we will have extreme fiscal stimulus in order to kick the can further down the road.

In October, I spent 15 hours in the Sheremetyevo airport in Moscow (damn connecting flight never showed). It hasn’t seen a dollar of cap-ex in years, but it’s still light years ahead of LaGuardia or LAX. Just wait until corporations learn how much they can make from a never-ending airport renovation project. Now multiply that by hundreds of airports in America that desperately need capital investment. Now add bridges, roads, bullet trains, water infrastructure and our electrical grid. Why are all the lobbyists trying to get us into wars with third world nations? Corporations would make more money fixing our infrastructure and it’s going to be a lot less politically contentious.

If you think deflation is a fact of life, you clearly haven’t paid attention to history. Governments around the world have experienced a unique decade where they ran deficits and printed money without “bad inflation” which upsets voters. They think this is a new normal with no consequences. It isn’t. They’re already panicking with the S&P a few ticks from all-time highs. Soon politicians will go into ludicrous mode with fiscal stimulus.

What will fiscal stimulus do to the equity market? I’m reminded of the 1970s—inflation is no friend to most stocks. What happens to trillions in negative yielding long-dated bonds if inflation ticks up? What happens to bond proxies like global large-cap equity indexes or real estate? What happens to risk-parity funds that are leveraged a few times over expecting bonds and equities to increase over time? What if both legs of the trade drop at the same time? No one is ready for inflation, but I believe it’s coming. Maybe not today or next week, but there is a powder keg of monetary supply just waiting to be unleashed by governments who think that inflation can never happen again. At first, markets will cheer a bit of inflation—then they’ll panic. The markets often do whatever the fewest people are positioned for. Who’s positioned for inflation? That’s about as contrarian as buying Argentine sovereign debt.

I think the road-map ahead is a market crash, followed by obscene fiscal stimulus. As always, I’m trying to think a few steps ahead here. I’m making a list of beat-down sectors who benefit from this change in government policy. I want to be ready to buy as soon as they get serious about unleashing the stimulus.

You need a crisis that’s severe enough that both political parties can agree on stimulus. We’re not there yet, but we will be. If you thought QE was nutty, wait until you see what drunken sailor mode looks like. Inflation is coming. Be VERY careful if you own assets with duration risk.