“I Still Travel, I Don’t Wear A Mask”: Oregon Nurse Suspended Over TikTok Video Dismissing COVID-19 Precautions Tyler Durden

Mon, 11/30/2020 – 15:25

An Oregon nurse was suspended over a TikTok video in which she bragged about shunning various pandemic restrictions and recommendations.

“When my co-workers find out I still travel, don’t wear a mask when I’m out and let my kids have play dates,” read a caption on the video, posted by oncology nurse Ashley Grames – who was mouthing lines from a scene in ‘How the Grinch Stole Christmas’ in which Cindy Lou Who learns who the Grinch is.

A cancel campaign quickly ensued…

Is this Salem Hospital? Your nurse Ashley Grames made a post bragging about breaking social distancing and not wearing a mask outside of work. Here is the video she posted pic.twitter.com/maTs3KmTGv

Salem Health responded, saying in statement: “This video has prompted an outcry from concerned community members. We want to thank those of you who brought this to our attention and assure you that we are taking this very seriously,” adding “This individual does not speak for Salem Health and has been placed on administrative leave pending an investigation.”

Yesterday, a nurse employed with Salem Health posted a video on social media which displayed cavalier disregard for the…

Over 1,500 people have commented on the post, with “hundreds calling for the nurse to be fired and her license to be revoked,” according to The Hill.

“Administrative leave? For knowingly exposing immunocompromised patients to Covid and then bragging about it? I’m an RN and I’m so disappointed in this response,” wrote one person, while another commented “As someone fighting cancer, I can only imagine how her patients feel after seeing this news.”

According to the report, citing data released last week – Salem Hospital has the highest employee-related covid cases of any hospital in Oregon.

via ZeroHedge News https://ift.tt/39tYYaX Tyler Durden

Peter Schiff spoke with Jay Martin backstage at the Cambridge Gold Summit. During the discussion, Peter and Jay took a step back from the immediate market volatility and news of the day to look at the big picture. Gold was a topic of discussion and Peter emphasized that the yellow metal has stood the test of time when it comes to preserving wealth.

Jay and Peter started the discussion by talking about the presidential election. Peter said on the margin, the person in the White House might make a difference, but ultimately we’re going to go over a cliff no matter who is driving the bus.

The difference might be how much time is it before we get there or do we step on the accelerator and go off the cliff sooner? Or do we keep a steady pace and go off a little bit later?”

Peter said the big problem is the intrusion of government regulation, taxation and spending into the economy. Those will only accelerate with Biden in the White House.

We can certainly expect more regulation. Much of the deregulation that occurred during the Trump years was done via executive order. It will be easy for Biden to reverse those and implement new regulations with his own EO pen. Peter said we could also see an increase in the minimum wage with Biden in the White House.

Then there are tax increases. Peter said he sees some take hikes coming down the pike even if the Republicans maintain control of the Senate, but it won’t be nearly enough to cover the massive increase in spending. That means more Fed money printing.

Most of the money is going to be printed. It’ll be borrowed and then printed by the Fed because there aren’t enough legitimate sources of revenue to fund the borrowing. So, the Fed will just monetize all the debt, which means even more inflation and a weaker dollar than we’ve already experienced.”

So, how can you preserve purchasing power over the next five or so years even as we see massive inflation?

Is there a chance gold five years from now could be below $1,900, which is about where it is now? Of course, there’s always that risk? But I think the odds are much higher that it will be worth considerably more. Now, could it go down? It’s possible. But I weigh that against the odds of other fiat currencies losing purchasing power, meaning if I buried a US dollar or a Canadian dollar in the ground today and I dug it up in five years and I went to buy stuff, how much would it buy relative to what it bought when I buried it? I think gold buried in the ground today will buy a lot more when you dig it up in five years than will your dollars.”

So, from the perspective of just trying to preserve what you have, you could just buy yourself some gold and gold has a pretty good track record of doing that. Of course, the shorter the time period, the less certainty you have.

So, a five-year period – it’s possible gold could go down during five years. But the next five years – I think that’s very unlikely given what’s going to be happening with money printing and interest rates.”

Why exactly does gold hold its value?

It doesn’t decay or lose any of its properties over time. Other assets can’t make that claim. So, over time, they’re going to be less valuable. They’re going to decay. They’re going to wear out.”

From an economic standpoint, gold is relatively stable so it measures the value of the paper money that’s being created.

The more money that’s being printed, well, the more money you need to buy an ounce of gold because the gold supply grows very slowly over time – maybe 1% per year, if that. So, if the money supply is growing by 10% or 20% per year, well, the price of gold must go up because all gold is doing is measuring the value of the fiat currencies that the central banks are creating. So, it’s not that the price of gold is going anywhere. It’s staying the same. It’s that the value of the money is going down and the rise in gold price is just letting you know how much value your money has lost.”

Jay asked Peter what he would do if he had $100,000 that he could afford to lose over the next five years – what would he speculate on? The answer was still gold — gold stocks. Peter said if the price of gold doubles in five years – a conservative estimate in his mind – you could see a five-fold increase in gold mining stocks.

via ZeroHedge News https://ift.tt/3lp6tSW Tyler Durden

Wall Street Democrats Distancing Selves From Georgia Runoff To Avoid Biden Tax Hikes Tyler Durden

Mon, 11/30/2020 – 14:46

The prospect of Democrats regaining control of the Senate following Jan. 5 runoff elections in Georgia has caused some deep-pocketed Wall Street Democrats to secretly wish defeat on their party’s candidates, according to Bloomberg.

The reason? Biden’s plan to raise taxes will directly impact them.

Employees of securities and investment firms poured about $77 million into President-elect Joe Biden’s campaign and the super-PACs supporting him, more than quadruple what they steered toward Trump. But the pair of Democrats facing runoff elections in Georgia against Republican senators David Perdue and Kelly Loeffler on Jan. 5 are unlikely to see such lopsided support — even with control of the chamber at stake.

For Wall Streeters, keeping the Senate in Republican hands means thwarting tax hikes for corporations and capital gains, as well as other policies that don’t align with their financial interests. –Bloomberg

“Most Wall Street Democrats and certainly all Wall Street never-Trumpers — Republicans that voted for Biden — want a split government,” says Hedge Fund manager Mike Novogratz, founder of Galaxy Digital.

Novogratz says he’s received a lukewarm response to fundraising emails for Democrats Jon Ossoff and Raphael Warnock. The hedge fund manager co-founded a group which involves former presidential candidate Andrew Yang (D) and Stacey Abrams, the former House Minority leader in Georgia who refused to concede a 2018 gubernatorial race.

“I got a lot of ‘Thanks, but no thanks,’ or ‘What are you talking about?’ from guys I know voted for Biden,” Novogratz told Bloomberg.

The Democrats, Ossoff and Warnock, seek to unseat Republican Senators David Perdue and Kelly Loeffler. If this happens, Democrats would hold 50 seats in the Senate, making presumptive Vice President-elect Kamala Harris the tie-breaker on contentious votes.

A prominent Wall Street Democrat who gave generously to Biden confided he hasn’t yet contributed to the Georgia races. The donor, who asked not to be identified, said he’s skeptical a Democratic sweep would matter much anyway because certain Democrats would block more progressive tax legislation.

Some are also put off by the challenge of flipping two seats, a view already visible as markets price in the likelihood of a Republican majority, according to one Democratic operative who predicts turnout for the party will sag without Biden on the ballot. –Bloomberg

On Thursday, we may have our first glimpse at who’s donating to who, when party committees and super-PACs like the Mitch McConnell-linked Senate Leadership Fund report their donors to the Federal Election Commission. Campaigns will similarly file with the FEC on Dec. 24.

Wall Street Democrats, meanwhile, are also hesitant to join a push to saturate Georgia’s airwaves with ads ahead of the runoff, which has seen approximately $259 million in paid advertising booked so far on both sides of the aisle, according to AdImpact data ending Friday.

Warnock’s campaign is the biggest spender at $45.7 million, while Loeffler has booked $38.4 million of ad time. In the other race, Ossoff’s ad buys total $42.7 million, compared with $28.8 million for Perdue. Republicans, including super-PACs and party committees, are outspending Democrats in Georgia $156.7 million to $101.9 million. –Bloomberg

“I don’t think the four candidates can actually spend the amount of money that’s going to be raised,” says Signum Global chairman Charles Myers, a Biden bundler. “It just shows how crazy, and how corrupted money and politics are, frankly.”

via ZeroHedge News https://ift.tt/37faG6o Tyler Durden

Will a vaccine cure the 20-year “Widow-Maker” trade?

In 1999, a media personality stated that “investing like Warren Buffett was like driving dad’s old Pontiac.” Of course, that was at the height of the Dot.com bubble, and soon after, “value investing” paid off. Unfortunately, it didn’t stick.

The Widow-Maker Trade

It wasn’t just 1999. In 2007, individuals were chasing the “momentum” in the real estate market. Individuals left their jobs to pursue riches in housing. They were willing to “pay any price” under the assumption they would be able to sell higher. Of course, it was not long after Ben Bernanke uttered the words “the subprime market is contained,” the dreams of riches evaporated like a “morning mist.”

In 2020, investors are again chasing “growth at any price” and rationalizing overpaying for growth. As I discussed in the “Death Of Fundamentals:”

“Such makes the mantra of using 24-month estimates to justify paying exceedingly high valuations today, even riskier.”

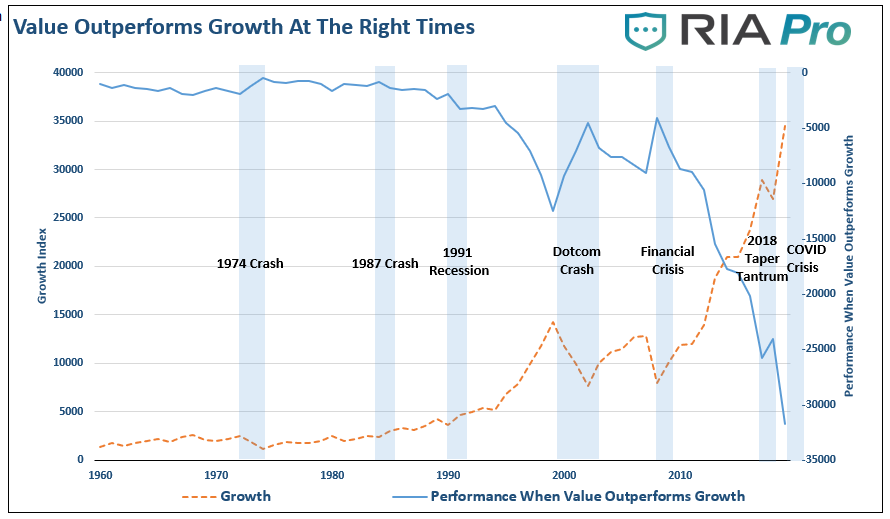

Chart updated as of November 2020

Given the massive government and Federal Reserve interventions over the last decade, it should be of no surprise that “growth” has outperformed. For “value investors,” it has been a “decade of pain.” The rise of passive indexing, algorithmic trading, and massive amounts of liquidity have destroyed price discovery in the markets.

Reasons For Under-Performance

In a recent discussion on “Value Is Dead,” we referenced a Research Affiliates article that noted the under-performance reasons.

“An investment strategy, style, or factor can suffer a period of underperformance for many reasons.

First, the style may have been a product of data mining, only working during its backtest because of overfitting.

Second, structural changes in the market could render the factor newly irrelevant.

Third, the trade can get crowded, leading to distorted prices and low or negative expected returns.

Fourth, recent performance may disappoint because the style or factor is becoming cheaper as it plumbs new lows in relative valuation.

Finally, flagging performance might be a result of a left-tail outlier or pure bad luck.

If the first three reasons imply the style no longer works, and will not likely benefit investors in the future, the last two reasons have no such implications.

With today’s value vs. growth valuation gap at an extreme (the 100th percentile of historical relative valuations), it sets the stage for a potentially historic outperformance of value relative to growth over the coming decade.”

The underperformance is quite stunning. The chart shows the difference in the performance of the “value vs growth” index. The index compares the pure value to a pure growth index, with each based on a $100 investment. While value investing always provides consistent returns, there are times when growth outperforms value. The periods when “value investing” has the most significant outperformance, as noted by the “blue shaded” areas, are notable.

When things ultimately go “pear-shaped,” the return to value tends to be a swift event. For investors, it is crucial to grasp what decades of investment experience tell us about the future. When the cycle turns, we have little doubt the value-growth relationship will revert to its long-term mean.

Is The Vaccine Announcement The Turning Point

Recently, Kevin Muir published a piece with an important message:

“The virus is done. The scientists won. They nailed it…markets will look through any (short term) negatives and realize the end is in sight.”

He goes on to make a case for “why” the Pfizer vaccine (and the other vaccines that will follow) may be the “silver bullet” that the market has been waiting for. Kevin’s view is the market is a discounting mechanism, and the “Smart Money” will focus on the future. Primarily, he hopes, the “Buying Value/Selling Growth” trade, which has been a widow-maker trade for the past 20 years, will be changed by the “vaccine.”

I doubt the “vaccine” will cure the ills of “value” any time soon as it does not address the primary issues driving the “momentum chase” currently. Refer back to the Research Affiliates comments above.

Does a vaccine change:

The effect of “data mining” on investment styles?No.

The “structural changes” to the market (i.e. proliferation of ETF’s)?No.

A crowded trade that leads to a distortion of prices?No.

The “vaccine” does not cure the most massive problem for value stocks – actual value.

The Lack Of Value In “Value”

As a “fundamental” and “value” based investor, the lack of performance in value versus growth has undoubtedly been frustrating. However, one of the biggest problems is the astonishing lack of value in “value.”

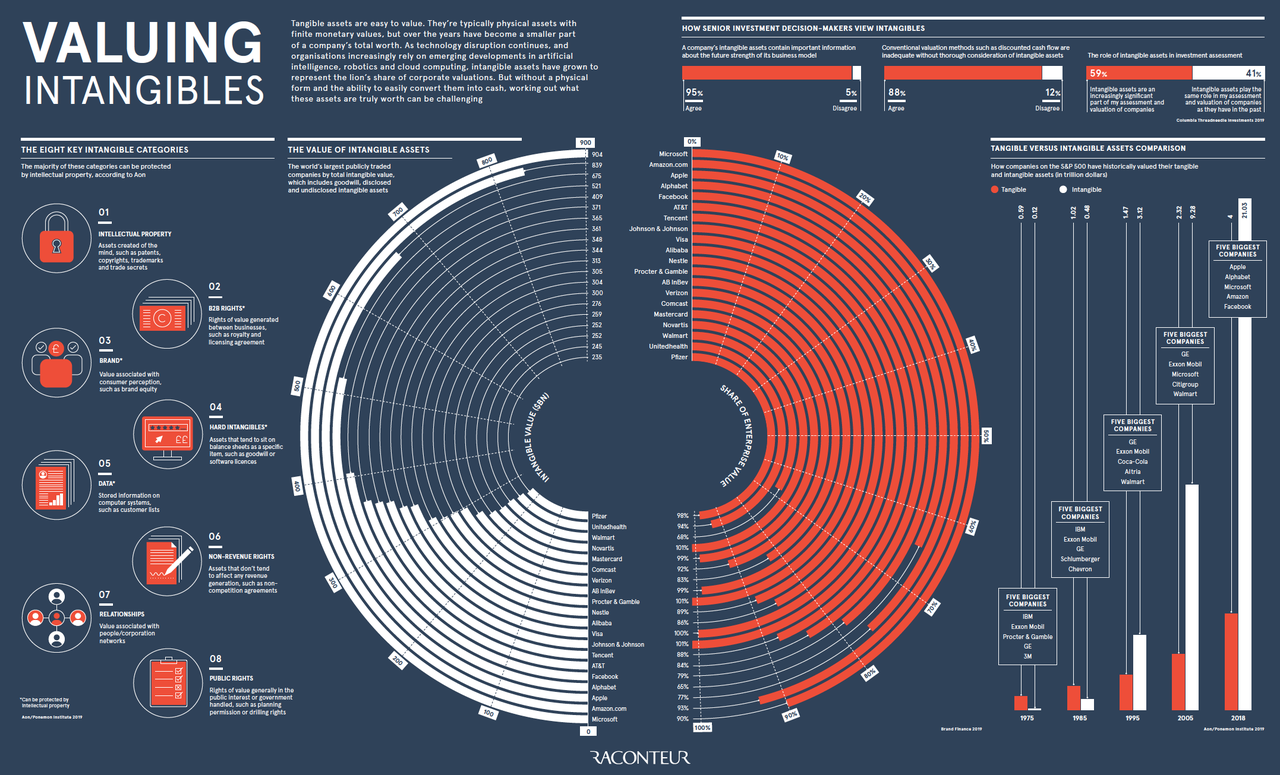

The chart is pretty stunning but needs some explanation.

Here is the issue with intangible assets.

“Intangible assets are typically nonphysical assets used over the long-term. Intangible assets are often intellectual assets. Proper valuation and accounting of intangible assets are often problematic. Such is due in large part to how intangible assets are handled. The difficulty assigning value stems from the uncertainty of their future benefits. Also, the useful life of an intangible asset can be either identifiable or non-identifiable. Most intangible assets are long-term assets meaning they have a useful life of more than a year.” – Investopedia

Read the bolded sentence again.

In many cases, the value of intangible assets is often overly optimistic assumptions about the companies worth. We recently quoted Raconteur on this particular issue:

“Tangible assets are easy to value. They’re typically physical assets with finite monetary values, but over the years have become a smaller part of a company’s total worth. Technology disruption continues in artificial intelligence, robotics and cloud computing. As such, intangible assets have grown to represent the lion’s share of corporate valuations. But without a physical form and the ability to easily convert them into cash, working out what these assets are truly worth can be challenging.”

The Debt Problem

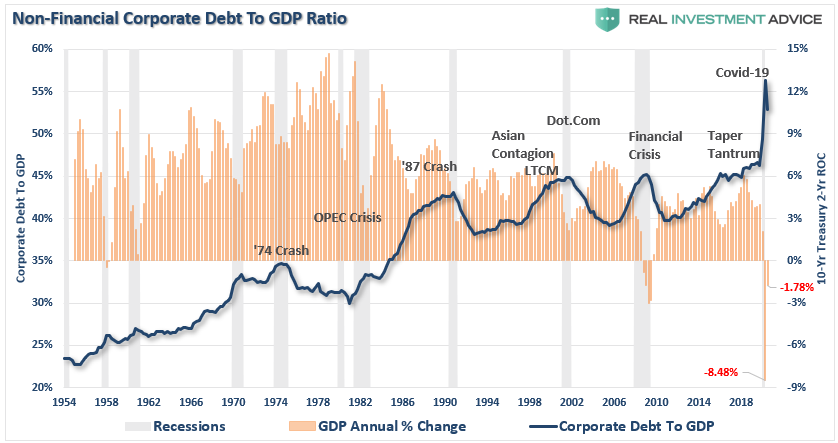

The most significant problem for the majority of companies in the “value” space is debt. As we have discussed previously, in just the last 10 years, the triple-B bond market has exploded from $686 billion to $2.5 trillion—an all-time high.

“To put that in perspective, 50% of the investment-grade bond market now sits on the lowest rung of the quality ladder.

And there’s a reason BBB-rated debt is so plentiful. Ultra-low interest rates have seduced companies to pile into the bond market and corporate debt has surged to heights not seen since the global financial crisis.” – John Mauldin

The debt issuance is problematic as companies used it for non-productive investments such as stock buybacks and dividend issuance as corporate profitability remained extraordinarily weak over the last decade.

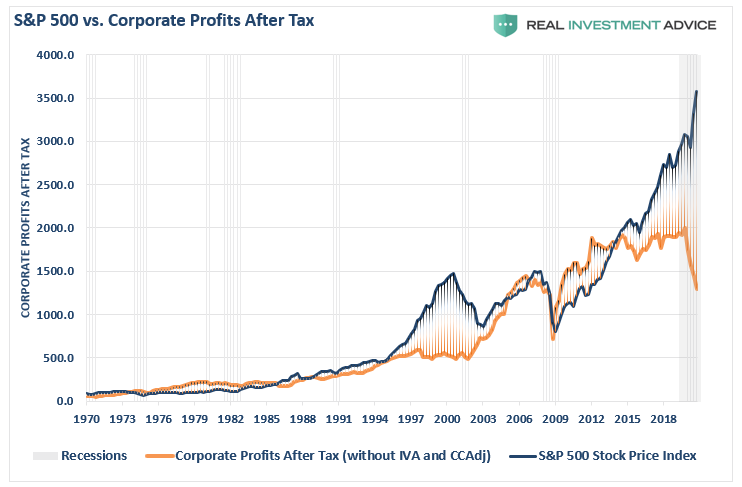

As discussed in “The Importance Of The Buffett Indicator,” corporate profits are at the same level as in 2009, while markets are at all-time highs. Exactly where is the “value?”

Notably, corporate profits are a reflection of economic growth rates, and a “vaccine” will not cure the problem plaguing profitability long-term—the debt.

Value Needs Strong Economic Growth & Higher Rates

The problem with the “vaccine will lead to a valuerotation,” is such would require more robust economic growth and higher rates for increased profitability.

Banks – need higher interest rates

Energy – needs higher oil prices

Materials – needs more substantial economic growth driving physical investment.

Industrials – same as materials.

Here is where the “rotation to value” runs into problems.

Let’s start with the banks.

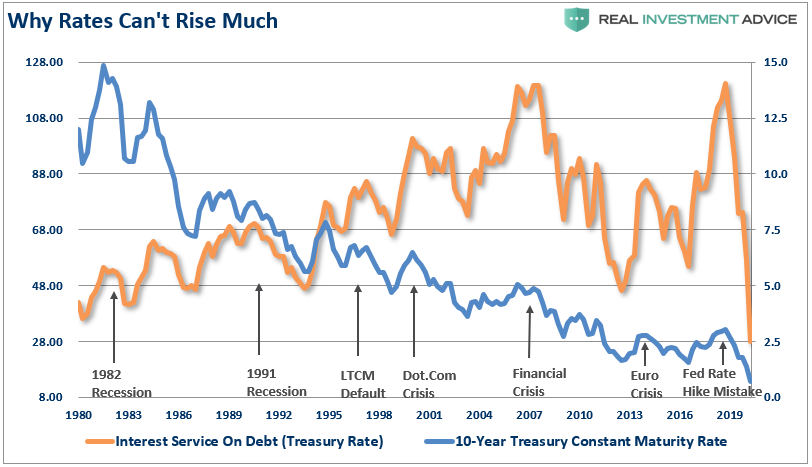

If interest rates were to rise substantially, the economy contracts due to the economy’s massive debt levels. We showed this specifically in “The Fed Will Monetize All Debt Issuance..”

“In an economy laden with $75 Trillion in total debt, higher interest rates have an immediate impact on consumption, which is 70% of economic growth. The chart below shows this to be the case, which is the interest service on total credit market debt. (The chart assumes all debt is equivalent to the 10-year Treasury, which is not the case.)”

“With respect to investors, the argument can be made that oil prices could remain range-bound for an extremely long period of time as witnessed in the 80’s and 90’s.“

Energy companies still have a massive supply/demand imbalance that existed long before the “pandemic” hit the economy. While a vaccine may provide a short-term boost, the underlying fundamentals are still not supportive of a long-term rotation.

Energy companies, along with basic materials and industrials, need stronger economic growth.

That isn’t coming.

Weaker Economic Growth

A vaccine will not solve the longer-term problems plaguing weaker economic growth rates and stronger fundamentals.

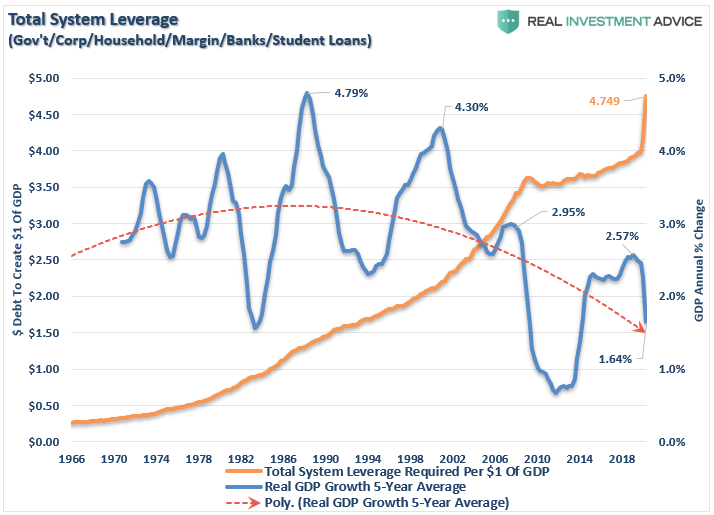

As we discussed previously in the “One-Way Trip Of American Debt,” the economic growth rate has been undermined by the surge in debt over the last decade.

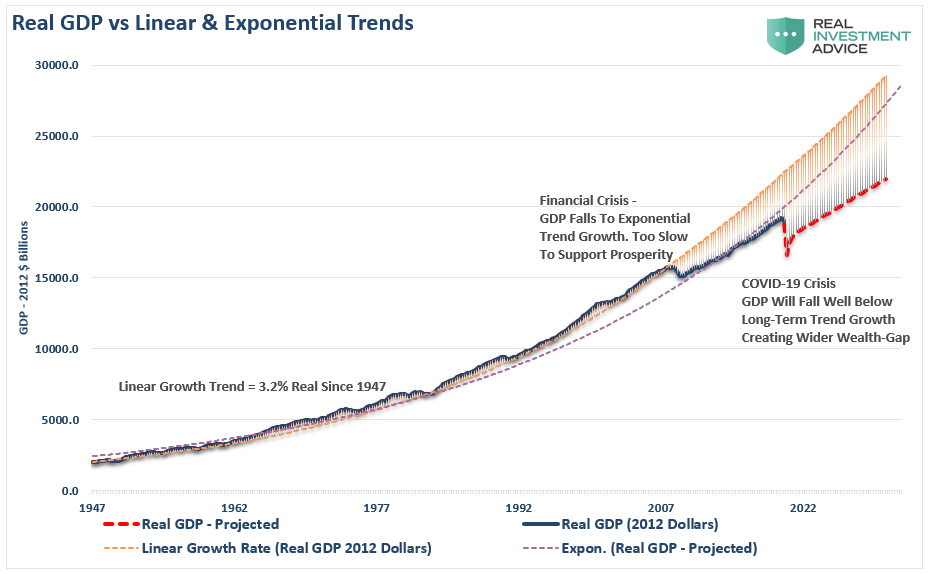

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt and leverage increased.”

As stated, the sectors believed to be part of the “value trade” requires stronger economic activity. Such would lead to higher rates of inflation and higher interest rates.

As rates rise, so do rates on credit card payments, auto loans, business loans, capital expenditures, leases, etc., while also reducing corporate profitability.

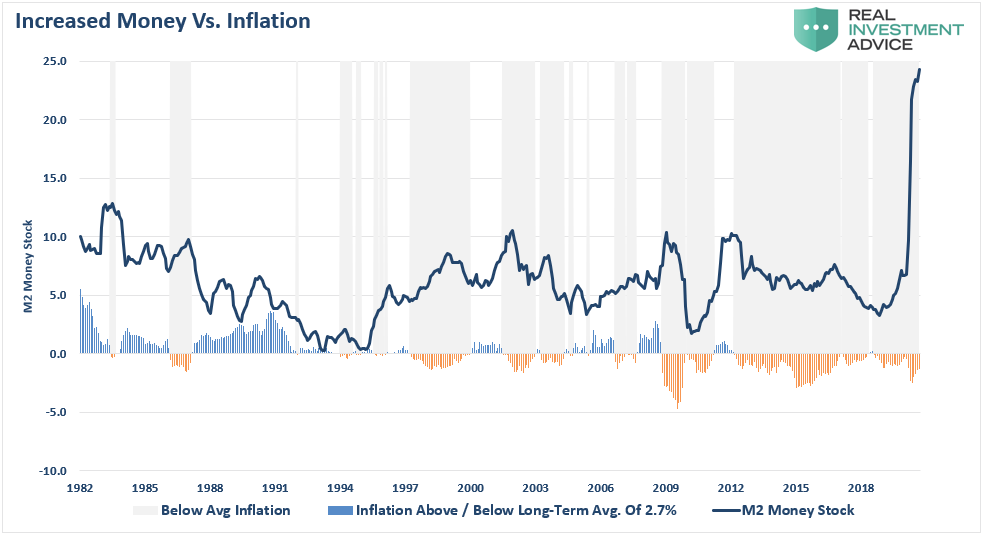

In an economy supported by debt, rates must remain low. Therefore, the Federal Reserve has no choice but to monetize as much debt issuance as is needed to keep rates from substantially rising. The byproduct of those actions is weaker economic growth and lower rates of inflation. As shown, since 2009, inflation has consistently run well below the Fed’s target.

Unfortunately, higher levels of debt continue to retard economic growth keeping the Fed trapped in a debt cycle as hopes of “growth” remain elusive. The current 5-year average inflation-adjusted growth rate is just 1.64%, a far cry from the 4.79% real growth rate in the ’80s.

A “vaccine” for COVID-19 is entirely different than what is needed to cure the “debt problem.”

The Rotation Is Likely Short-Lived

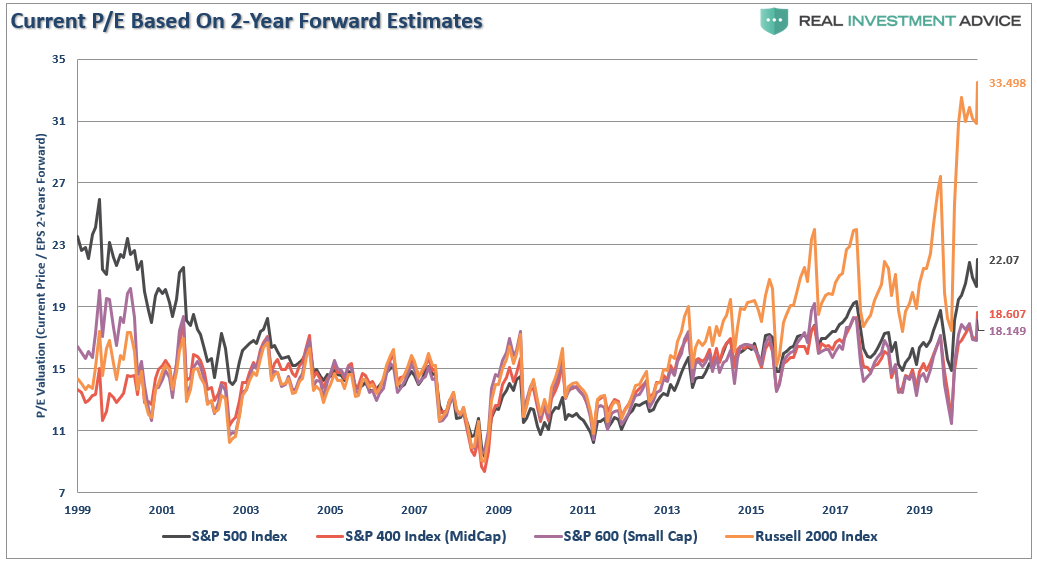

Look back at the first chart above. Based on two-year forward earnings estimates, the Russell 2000 (small-capitalization companies) are trading at historical extremes. Compound valuation problems, with the debt problem, and the lack of actual “value,” the issue becomes more apparent.

Given the Federal Reserve’s monetary injections and suppression of interest rates, it is not surprising to see companies leveraging their balance sheets. As interest rates have plunged, corporations have hit a record issuance of debt to pay dividends and engage in other non-productive actions.

The increased leverage of corporate balance sheets is problematic, particularly given already weak revenue growth for S&P 500 companies.

The rotation from “growth” to “value” is inevitable. With that, we agree.

However, a “vaccine” doesn’t solve the problems plaguing economic growth, suppressing inflation, and keeping Central Bankers flooding the markets with liquidity.

Those problems can only get solved against a backdrop of devastation for the majority of investors. When there is a true reversion in leverage, debt, and valuations, the foundation for a “value rotation” will be laid.

via ZeroHedge News https://ift.tt/2VgkOXc Tyler Durden

Iran Nuclear Scientist Was Shot With Mounted Remote-Controlled Machine Gun Tyler Durden

Mon, 11/30/2020 – 14:05

Iranian state media has issued for the first time the stunning details of last Friday’s assassination of top nuclear scientist Mohsen Fakhrizadeh.

Importantly, Iranian state media is claiming that a machine gun recovered from the site was made in Israel. “The remains of the weapon used in the Friday assassination of senior nuclear scientist Mohsen Fakhrizadeh show that it was made in Israel, an informed source has told Press TV,”according to the state-run English language news site.

The killing was done “entirely remotely” with no assassins on the ground and no apparent drone activity, according to Iranian officials. But how?

Scene of the assassination, via AP

“The source made the revelation on Monday, saying the weapon collected from the site of the terrorist act bears the logo and specifications of the Israeli military industry,” PressTV continued.

Tehran officials said they will soon publicize all available evidence showing who was behind the hit, which occurred in a small city east of the capital and included a hail of gunfire and detonation of a vehicle which took out the scientist’s convoy and body guards. Officials have further vowed “hard revenge” for the killing which they had in the hours after blamed on Israel.

Initially international reports strongly suggested a multiple-man hit team forced Fakhrizadeh’s vehicle to stop before opening fire. However, Iranian state media just dropped details suggesting sophisticated remote-controlled machine guns were used.

On Monday Ali Shamkhani, the secretary of the Islamic Republic’s Supreme National Security Council, confirmed that it is Iranian investigators’ belief that Israel used “electronic devices” to take out Fakhrizadeh, according to the Associated Press.

1 \ Amazing new details of the Fakhrizadeh assassination emerge in the Iranian press: IRGC affiliated Fars news reports the assassination was done using an automatic machine gun operated with a remote control and not with gunmen who were on the groundhttps://t.co/CLSaCuHp2J

The following is a translation and paraphrase of key sections of a new Iranian state-run Fars news report by Axios correspondent Barak Ravid:

Amazing new details of the Fakhrizadeh assassination emerge in the Iranian press: IRGC affiliated Fars news reports the assassination was done using an automatic machine gun operated with a remote control and not with gunmen who were on the ground.

According to the report Fakhrizadeh and his wife were on their way to spend the weekend at their house in a Tehran suburb. There were three security cars with them and at a certain point the leading car left the motorcade to do a preliminary security check of the house.

Right after the car at the front of the motorcade left shots were fired on Fakhrizadeh’s car and it stopped. Fakhrizadeh stepped out of the car thinking his car hit an object on the road or there was a problem with the engine.

At that point shots were fired again from a Nisan pickup truck which stopped 150 meters from Fakhrizadeh’s car. The shots were fired from an automatic machine gun which was mounted on the pickup truck and operated by remote control.

Fakhrizadeh was hit by three bullets – one hit him in the spine. Seconds later the Nisan pickup truck exploded in what looks like a self destruct mechanism. According to Fars news Iranian security forces identified the owner of the pickup truck who left Iran on October 29th.

Fars reported the assassination operation lasted only three minutes and was all done by remote control with no gunmen on the ground.

Illustrative image: A photographed remote control gun previously used by ISIS in Mosul as an anti-aircraft weapon, via Popular Front military analysis site.

If true, this would further point to a likely foreign intelligence operation, whether Israeli or with American help.

It sounds like the stuff of Hollywood movies. The 1997 film The Jackal involves just such a scenario where an assassin seeks to kill a politician using just such a high-tech remote controlled automatic long-range gun.

Here are the official details of the targeted killing being circulated by top Iranian officials Monday, as summarized in the AP:

“Unfortunately, the operation was a very complicated operation and was carried out by using electronic devices,” Shamkhani told state TV. “No individual was present at the site.”

Satellite control of weapons is nothing new. Armed, long-range drones, for instance, rely on satellite connections to be controlled by their remote pilots. Remote-controlled gun turrets also exist, but typically see their operator connected by a hard line to cut down on the delay in commands being relayed. Israel uses such hard-wired systems along the border with the Hamas-controlled Gaza Strip.

It may be the first time in known history that such a high level assassination was carried out entirely through on the ground stationary remote-controlled automatic weapon fire.

Israel has long possessed remote controlled automatic weapons. Illustrative example via WikiWand: “the Samson Remote Controlled Weapon System for 30 mm autocannon is designed to be mounted on lightly-armored, high-mobility military vehicles and operated by a gunner or vehicle commander operating under-the-deck.”

Mideast editor of Jane’s Defence Weekly, Jeremy Binnie, mused, “Could you set up a weapon with a camera which then has a feed that uses an open satellite communications line back to the controller?”

Binnie answered his own rhetorical question with: “I can’t see why that’s not possible.”

via ZeroHedge News https://ift.tt/3fQJkri Tyler Durden

While online sales exploded during the Thanksgiving weekend, trips inside brick-and-mortar stores on Black Friday dropped off significantly, as many analysts anticipated.

According to data from Sensormatic Solutions, shopper visits to physical stores on Black Friday fell 52.1% from last year. Online sales, meanwhile, hit a new record with $9 billion, up 21.6% over 2019, Adobe Analytics said.

With many retailers opting to stay closed on Thanksgiving, physical traffic on the holiday fell nearly 95%, according to Sensormatic.

With COVID-19 cases hitting new highs, it comes as little surprise that many shoppers opted to stay away from physical stores this year. That said, the differences between Black Friday 2020 and those that preceded it were stark.

“Our traditional store checks over the holiday weekend were like none other we’ve ever experienced in our lifetime — no hustle and bustle, no lines at the register,” said MKM Partners Managing Director Roxanne Meyer in an emailed research note.

Retailers have anticipated and prepared for that, even nudged consumers into changing up their holiday shopping plans to keep them from packing into stores.

Major players like Walmart and Target have been spreading Black Friday-like discounts through the month of November and encouraging online purchases and curbside pickup. Many also followed Amazon’s lead by launching online sales events in October, which pulled holiday purchases into the month and heralded the beginning of the holiday shopping spree.

Black Friday still had a major impact. Sales in the U.S. were up 177% Friday against their October average, according to Criteo data emailed to Retail Dive. By category, fashion was up 240%, consumer electronics were up 359% and home goods were up 148%.

However, year-over-year Black Friday sales were down 5%, meaning that even the online sales surge couldn’t fully make up for the lost foot traffic. Criteo’s data shows, however, that the prior weeks’ discounting may have affected sales on Black Friday itself — which was the plan among retailers all along. Sales in the first three weeks of November were up 7% year over year, Criteo said.

Observers found lines leading out of stores on Black Friday, but their length was due to social distancing and in many cases they led to stores that were capping foot traffic as a pandemic safety measure.

Analysts with B. Riley Securities said they found through mall checks of specialty and apparel retailers they cover that Aerie, Lululemon and L Brands’ Bath & Body Works represented some of the most post-purchase bags consumers were carrying around.

via ZeroHedge News https://ift.tt/39tsn5d Tyler Durden

WHO Urges Global Governments To “Manage” All Social Activity Tyler Durden

Mon, 11/30/2020 – 13:26

Dr. Michael Ryan, Director of Global Alert and Response of the World Health Organization (WHO), told journalists at a press briefing on Monday that “pinch points,” otherwise known as places where people gather, must be “managed.”

Ryan spoke about numerous types of public areas, such as airports, public transportation, and even places like ski resorts that governments must “manage” to prevent further spreading of COVID-19.

He called on governments around the world to investigate “all forms of gatherings that lead to people congregating are moving en masse and how they are going to de-risk those processes.”

Ryan said if governments don’t believe those processes cannot be de-risked, governments should “curtail, postpone, and or even manage” those processes.

In other words, just like Thanksgiving – Christmas is likely canceled in the Western world.

For more on this, listen to Ryan from the 28-minute mark.

While the pandemic is reshaping the world, the WHO, which is arguably parroting its main source of funds – China, is now demanding governments across the globe to “manage” what the world’s population can “safely” undertake based on their “science.”

And this all comes as China, a strategic rival of the US, is attempting to become the world’s superpower – through a new approach – that is – “health… for your own good!”

via ZeroHedge News https://ift.tt/36nl64P Tyler Durden

The judge who Sunday ordered Georgia officials not to wipe or reset voting machines scheduled the next hearing in the case for Friday.

U.S. District Judge Timothy Batten Sr., a George W. Bush appointee, issued three emergency orders on Sunday, initially ordering officials to hold off on taking action regarding the machines, reversing himself, then re-establishing the first order.

In a Nov. 30 order, Batten said his final decision on Sunday partially granting the defendants’ motion “involves a controlling question of law as to which there is substantial ground for difference of opinion and that an immediate appeal from the order may materially advance the ultimate termination of the litigation.”

The order enables defendants to appeal the temporary ruling to the 11th Circuit Court of Appeals.

Defendants were ordered to file their brief by Dec. 2 while any reply brief will be due Dec. 3.

In a third filing, defendants said Charlene McGowan, Georgia’s assistant attorney general, will be appearing on behalf of the defendants, which include Gov. Brian Kemp, Secretary of State Brad Raffensperger, and state Election Board members.

Georgia Secretary of State Brad Raffensperger speaks during a news conference in Atlanta, Ga., on Nov. 13, 2020. (Brynn Anderson/AP Photo)

McGowan didn’t respond to a request for comment.

The plaintiffs are represented by attorney Sidney Powell. They successfully convinced Batten on Sunday to bar officials in three counties from wiping or resetting Dominion Voting Systems machines.

Plaintiffs are seeking to have outside experts perform forensic inspections of the voting machines.

The judge ruled that defendants are “enjoined and restrained from altering, destroying, or erasing, or allowing the alteration, destruction, or erasure of, any software or data on any Dominion voting machine in Cobb, Gwinnett, and Cherokee counties.”

He also ordered the board to “promptly produce to plaintiffs a copy of the contract between the state and Dominion.”

Dominion says on its website that “no credible reports or evidence of any software issues exist,” including in Georgia.

Powell wrote on Twitter late Sunday that “Georgia election fraud is being exposed.”

“Who benefitted from the hurry-up #Dominion contract in #GA?” she added.

Oil Facing Huge Short Squeeze As HFTs Build 470MM Barrel Short Position Tyler Durden

Mon, 11/30/2020 – 12:45

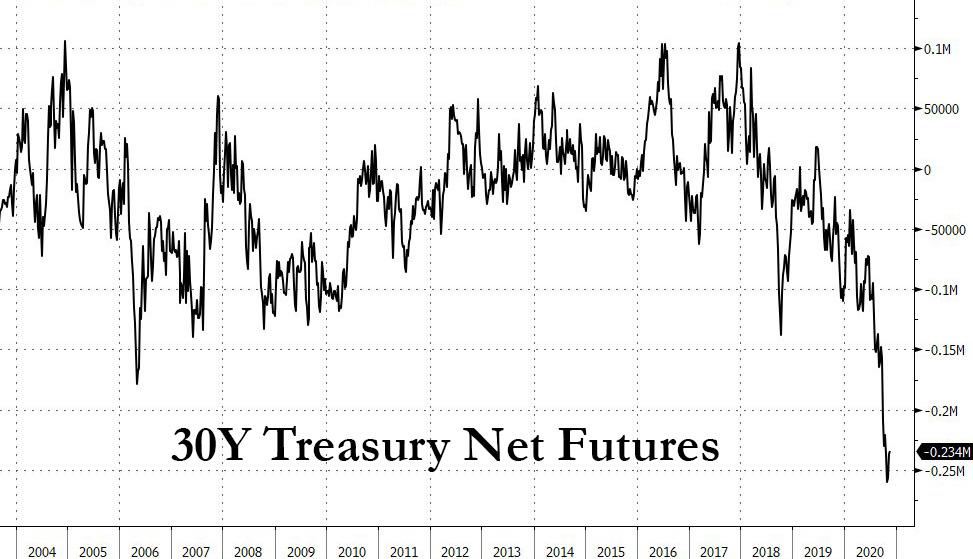

We have previously discussed the unprecedented build up of net shorts in “ultra”, or long-dated Treasury futures, which as recently as a few weeks ago hit a record, and has since tightened modestly following the recent decline in US yields. As we discussed before, a major reason for this huge net short – which threatens to snap any moment following more flashing red reflationary headlines such as covid vaccines, sparking a massive short squeeze within the rates complex – is due to the accumulation of so-called “other reportable” shorts, a cryptic category of investors who don’t fall into any of the other accepted CFTC groupings, yet which has grown to dominate the technicals and flows within the world’s (formerly?) most liquidity market.

It turns out that 30Y futures is not the only asset threatened by a massive short squeeze on the back of “other” speculators.

As Bloomberg’s Alex Longley writes today, a group of oil traders whose positions are often overlooked by much of the market have quietly built up a huge bet on lower crude prices.

Traders categorized as “other reportables” – the same as the group responsible for the massive 30Y short – now hold a record short position of almost 470,000 Brent futures contracts, according to ICE Futures Europe data.

The “other” grouping covers entities whose business activity is unknown from publicly-available information, or who don’t fit the other main reporting categories of dealer, speculator, producer or consumer. High-frequency traders and proprietary trading houses would be included, Bloomberg speculates.

Their bearish bet, equivalent to 470 million barrels of oil, has been accumulated since the start of the year and is in direct contrast to that of traditional speculators who last week boosted their net-bullish Brent oil wagers to a nine-month high. However, when it comes to marginal price setting, “other” specs have emerged as the primary force especially due to their quick trigger finger, buying – or selling – first, and asking questions only after or never.

Crude futures curves rallied sharply this month amid growing hopes for coronavirus vaccines with banks like Goldman citing short-covering as one of the major drivers of the recent crude rally, although one clearly can’t see it in the “Other” category where shorts appear to be piling on perhaps in hopes of another April rerun where WTI crashes into negative territory.

Finally, as Bloomberg notes the size of the position is also large compared to that of traditional speculators. Other reportables hold a bigger short position in futures than the combined bullish and bearish bets of traditional money mangers. They also hold more than 9,000 short contracts per trader, more than either bullish or bearish speculators hold per trader.

In other words, the next glimmer of renormalization, or any credible good news for the economy, and thus oil, could spark the latest a massive short squeeze in an asset which HFT shorts have taken to the woodshed for much of 2020.

via ZeroHedge News https://ift.tt/3fTloDu Tyler Durden

Americans have common sense, so they can understand when they’re being played (for example, when politicians place Americans under house arrest and then ignore their own rules to party and travel). And they know that there is no way on God’s green earth that decrepit, demented, corrupt, and terminally stupid Joe Biden fairly won this election. This post assembles various election anomalies that don’t pass the smell test.

J.B. Shurk, who frequently publishes at American Thinker, wrote a knock-out article for The Federalist about Joe Biden’s magical performance in the election. You should read the whole article, but here are four things that don’t pass the smell test:

1. Biden allegedly got 80 million votes, which is more than Obama received at his peak, in 2008 – and Biden did this despite losing minority voters to Donald Trump and trailing Trump in voter enthusiasm.

2. Biden broke 60 years of precedent by winning nationally despite losing prodigiously in bellwether states and counties. The last time this happened was when the mafia got out the vote for John F. Kennedy in 1960.

3. Trump had extraordinary coattails, so much so that even the New York Times admitted that the “Democrats Suffered Crushing Down-Ballot Losses Across America.” Think about that: Biden had no coattails and no enthusiasm, yet he allegedly won a record number of votes. Smells fetid to me.

4. Biden barely made it through the primaries, while Trump soared, with Trump’s performance being a historically sure sign of voter enthusiasm and probable victory – yet Biden, again, allegedly scored an equally historically strong victory.

At The Spectator, Patrick Basham, a professional pollster, also felt that Biden’s alleged win cannot pass the smell test. Again, this is a summary, so you should read the original article:

5. Trump exceeded his original vote count by the largest margin for any incumbent in American history. He got 10 million more votes than before; by contrast, Obama, in 2012, got 3.5 million fewer votes than in 2008.

6. Trump’s support among blacks grew by 50%, while Biden’s fell below the important 90%-mark that Democrat candidates need to secure victory.

7. In the Rust Belt, Biden lost black support everywhere except in Detroit, Philadelphia, and Milwaukee. In those cities, every single black person apparently voted for Biden.

8. While pollsters can and do manipulate polling outcomes, non-polling metrics (historical norms such as the economy, enthusiasm, etc.) have never been wrong – only we’re being told that this year was the exception.

9. The fact that Pennsylvania, Wisconsin, Arizona, Nevada, and Georgia simultaneously pretended to halt ballot counting while continuing to count is evidence of election fraud collusion.

10. Optical scanners were set to accept unverified, un-validated ballots.

11. The scanners were almost certainly programmed to fail to keep audit records.

12. In the contested states, the voting machines were alleged to have processed hundreds of thousands of ballots within a short time, which is a physical impossibility.

14. Dominion and ES&S voting machines were created to have back doors and specific functions to manipulate votes either at the machine or over the internet.

15. Fox News’s behavior on election night (refusing to call pro-Trump outcomes while prematurely calling Arizona for Biden) was so abnormal that Vegas oddsmakers instantly assumed that the fix was in.

17. There were anomalies in Virginia that suggested that computers were subtracting votes from Trump and, sometimes, giving them to Biden.

18. One analysis shows that voting machines in Michigan systematically removed votes from Trump and handed them to Biden. I saw a rebuttal (which I cannot locate now) that purported to debunk this but did so by using a different scale on the X-axis, which I found inherently suspicious.

19. Over 100,000 Pennsylvania absentee ballots were returned either a day after they were mailed out, on the day they were mailed out, or on the day before they were mailed out.

20. In all the contested areas, and at Dominion’s website, Democrats have been systematically failing to create or have destroyed all data that could be used to demonstrate fraud. This creates the legal presumption that the data do, in fact, show fraud.

On behalf of all Trump voters, I say to the Democrats who are trying to gaslight us: Don’t spit in my face and tell me it’s raining.

via ZeroHedge News https://ift.tt/33M64Ef Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}