White House Planning Unprecedented Trade Alliance To Retaliate Against China Tyler Durden

Mon, 11/23/2020 – 09:07

As Trump considers next steps in his ongoing crusade to challenge the election results, he appears increasingly set on unleashing a “scorched earth” policy in the already dismal relations China, if only to make any hope for a quick detente between Beijing and the pro-China Biden as difficult as possible.

Overnight, Reuters reported that the Trump admin is close to issuing a list of 89 Chinese aerospace and other companies that would be unable to access U.S. technology exports due to their alleged links to the PLA. Commercial Aircraft Corp. of China Ltd., or Comac, and Aviation Industry Corp. of China Ltd. are among the firms named, Reuters reported, citing a draft copy of the list from the U.S. Commerce Department.

As such a move would further restrict the companies from buying American goods and technology, it would fuel already-heightened tensions between the U.S. and China on fronts ranging from trade and Taiwan to the handling of the coronavirus.

Naturally, China’s Foreign Ministry said Monday that it “firmly” opposed the “U.S. oppression of Chinese companies without a cause.” At the same time, Trump’s in house China hawk, Peter Navarro, underlined that the time for policy action against China is now.

Taking a step back, as Rabobank’s Michael Every writes, “with technology and capital controls against Chines firms being accelerated by the Trump administration specifically due to claims of military links, one might also want to consider that increasingly-popular Chinese government bonds, by their very nature, also encompass military spending. The next few weeks could see plenty more Trump action on China.”

Yet while we wait for Trump to enforce a full-blown crackdown on outbound capital to China (a few more fiascos like the pulled Ant Financial IPO and he won’t have to), moments ago the WSJ confirmed Every’s gut feeling when it reported that in another escalation against China, Trump administration officials told the WSJ that “they are pushing for new hard-line measures against Beijing” where the most ambitious effort would create an informal alliance of Western nations to jointly retaliate when China uses its trading power to coerce countries.

“China is trying to beat countries into submission by egregious economic coercion,” one senior official told the WSJ. “The West needs to create a system of absorbing collectively the economic punishment from China’s coercive diplomacy and offset the cost.”

Under the joint retaliation plan, when China boycotts imports, allied nations would agree to purchase the goods or provide compensation. Alternatively, the group could jointly agree to assess tariffs on China for the lost trade.

In other words, the China hawks in the Trump admin are feverishly working on an organization that is the alternative to the WTO, one which specifically seeks to retaliate only against China.

Separately, the administration is said to be expanding its ban on imports from China’s Xinjiang region that are made with forced labor, and add companies to a Commerce Department blacklist, including Chinese chip maker Semiconductor Manufacturing International Corp. SMIC already faces tough licensing requirements when buying from U.S. firms.

Yet while all of this sounds dramatic, the “alliance” is mostly theatrical. The senior officials acknowledged that not only do the new measures face the hurdle of a waning Trump administration, but should they succeed, they would also need the incoming Biden administration to endorse the effort and carry it forward.

Which is also Trump’s intention: to show just how eager Biden is to mend the badly frayed ties with China, and portray him as Beijing’s puppet. That would come at a time when the deeply polarized US nation can agree on only one thing: that China is bad.

As such, Biden attempts at restoring ties with China will be immediately used by his political enemies to cast him as yet another globalist puppet working on Beijing’s behalf.

via ZeroHedge News https://ift.tt/2IXg3Pj Tyler Durden

Netanyahu Flew To Saudi Arabia For First Known Meeting With Crown Prince Tyler Durden

Mon, 11/23/2020 – 08:58

Israeli Prime Minister Benjamin Netanyahu secretly met with Saudi Arabia’s Crown Prince Mohammed bin Salman on Sunday, which would be the first known meeting between senior Israeli and Saudi officials amid a push by the Trump administration to normalize ties between the longtime adversaries, according to A.P. News, citing Hebrew-language media.

Netanyahu and Yossi Cohen, head of Israel’s Mossad spy agency, took a rare flight to the city of Neom, located in the Tabuk Province of northwestern Saudi Arabia, on Sunday, where they met with the crown prince and U.S. Secretary of State Mike Pompeo.

Constructive visit with Crown Prince Mohammed bin Salman in NEOM today. The United States and Saudi Arabia have come a long way since President Franklin Delano Roosevelt and King Abdul Aziz Al Saud first laid the foundation for our ties 75 years ago. pic.twitter.com/KZ4XMkah03

Sources told WSJ that senior officials from both countries discussed a wide range of issues, including the normalization of ties between both countries, along with other topics concerning Iran – no agreements were reached at the meeting, the sources added.

The meeting, possibly orchestrated by the Trump administration to isolate Iran and advance Israel’s status in the Middle East, could suggest direct diplomatic relations may improve if an agreement is reached and result in a regional realignment, ultimately benefiting the U.S. However, the Saudi government has ignored calls to normalize ties with Israel as long as its conflict with the Palestinians remains unresolved.

However, flight tracking data showed an “absolutely rare Israeli flight direct to new Saudi mega-city Neom on Red Sea shore It was Bibi’s ex-fav bizjet t7-cpx. Back to Tel Aviv after 5 hours on the ground,” tweeted the editor of Haaretz.

ABSOLUTELY rare Israeli flight direct to new Saudi mega-city Neom on Red Sea shore

Normalizing relations between Saudi Arabia and Israel before resolving Palestinian statehood would be a major power shift in the region, upending a decades-old pan-Arab position. As WSJ points out, Saudi Arabia’s king has had disagreements with his son for embracing Israel.

As explained by the Carnegie Endowment for International Peace, formalizing Saudi-Israeli relations would help each country achieve several strategic and military goals:

Saudi Arabia and Israel want to see the United States use its military might to defeat, not just contain, the threat from Iran. They both actively push for an all-encompassing and hard-to-get U.S.-Iran deal that conflates the U.S. priorities of halting Iran’s nuclear program and attacks on U.S. interests with countering Iran’s broader geopolitical expansion across the region.

Israel, Saudi Arabia, and the United States all want Washington to remain actively invested in the fight against terrorism in the Middle East.

So is the rush by the Trump administration to normalize relations with the Israeli-Gulf States a sign that war with Iran is on the horizon?

via ZeroHedge News https://ift.tt/339wO0N Tyler Durden

At some point in 2021 the builders might have finished our home renovation, and mankind will have beaten the Coronavirus. (More chance of the latter I think.)

Today, there is good and bad news. More vaccines that show enormous promise, but infections are rising. It feels like a race. I note JP Morgan predicting a Q1 GDP contraction is possible next year.

But the finish line is in sight. By Easter businesses will be reopen, we’ll be back in our offices, we’ll be flying again, cruise ships will be cruising, and there will be a massive rebound in consumer spending as populations work their way through their excess savings built up during lockdowns. The hedge funds have been anticipating this; buying into distressed assets ahead of recovery has been a massive theme in recent months, everything from aviation, shipping to pubs and clubs.

The markets are taking the view the multiple vaccine announcements and recovery prospects means it’s time to Buy, Buy, and Buy some more. Take you pick of positive investment theses: the great rotation trade, the small cap bounty, emerging market rebound. You will trip over market analysts explaining this is the start of a new positive cycle, or a long-term valuation play. There is nothing to fear. (Really?)

Having got the remarkable age I am – 35 years in markets and spending every penny I earned on fast cars, fast boats and … well you know the rest, I now read through the investment pap with increasing interest every morning, wondering how I shall afford retirement when yields are effectively zero in real terms? There are plenty of good economists out there arguing the massive increase in government spending and support, plus increasing M3 money in circulation, is the genie that will create real inflation next year. All this talk about rising markets, recovery and inflation means I am a tad concerned that 20% of my PA portfolio still defensively in cash.

I am, by nature, a pessimistic optimist. That’s very different from an optimistic pessimist.

An optimistic pessimist reckons things are bad, but we will likely get to where we want to go. A pessimistic optimist knows things are improving, but that someone is likely to f*** it up by making a massive mistake and things will end up much worse than they need to be.

My expectation is for Pandemic recovery – but will that lead to a bright new industrial age to justify the current stratospheric markets? Not so sure that’s the way this plays out. I reckon the risk of policy mistakes as conventional politicians try to rein back spending too early, raise austerity taxation and generate wage inflation are substantial. Yes, Mr Sunak.. I mean you!

Inflationary threats are another reason to be concerned on my cash position – it’s one reason we’re investing in building work now.

Many businesses will remain crippled for years as a result of lockdown losses and repaying emergency lending. 18% of firms were effectively debt-locked zombies before the crisis. Yet, many other businesses have thrived despite the pandemic – the reality is a reopening economy of winners and losers.

Human nature being what it is, I’m predicting some pretty fraxious times ahead here in the UK as our government tries to row back on pay hikes for front-line workers and civil servants. Their demands will likely fuel demands for higher wages across the private sector. There will be winners and losers – which just increase the “Not Fair!” aspects of a crisis we are supposedly sharing together.

I’m not quite predicting a Black Death scenario where losing ½ the workforce caused wages to balloon and killed feudal systems, but I do expect a lot of noise. The pandemic could well have shattered wage stability, and since the government is about as popular as boil on the bottom, the only hope for avoiding industrial strife is probably the sheer amateurishness of the unions and the left.

And we haven’t even got to post virus stage! The government says Easter so there are still five months before vaccines are widely available and in circulation. That’s five more months of potential slowdown and pain to come. Will I be able to go skiing? It ain’t over till it’s over!

Moreover, I am even more concerned about the health of markets. Bonds and Equities are pretty much fully pricing a full recovery already. Corporate bonds have never been so tight. Equity valuation metrics are pretty much at record levels. Yields have never been so low – and risks, uncertainty and threats have never been so high.

The problem is a growing mismatch between risks and returns. Markets are way, way ahead of the reality and priced pretty much for a perfection we are unlikely to acheive. Yet the global economy has never been so stressed in terms of rising trade and geopolitical uncertainty. When US junk bonds yield close to negative real yields. When zombie debt-addled companies are trading close to negative actual yields. When equities are at record valuations.. Etc..

The reason markets are so strong when the economic reality is so weak is nothing to do with expectations of a bright rose growth future, but entirely due to distortions in market pricing that flow from ultra-low interest rates and QE infinity. If you have been looking for inflation these last few years, then look no further than financial assets – that’s where its been. Now it threatens to break into the real economy. If confidence in the ability of Central Banks to keep fuelling the positivity was to wobble….. then its game-over.

How will Central Banks react if wage inflation, real inflation and government reinback strikes next year? Now that is a real and rising risk.

The result is investors will do anything to find diversified and greater returns – which favours equities despite the obvious overvaluations, and fuels belief in the extraordinary. In that latter bracket I would put the impossible valuations being put on “story” stocks. Tesla is the obvious one, but there are just a many other tech and health marvels that are hopelessly overvalued on hype and insane optimism. Then there is Bitcoin – which I wrote about last week, and received a barrage of hate-mail about.

In extraordinary times.. extraordinary belief trumps common sense everytime. If you want to demonstrate leadership and success in these markets – be critical and pragmatic. Learn to tell hype from fact.

So where does that leave my portfolio? A balance of risk vs defensive stocks, upping equites and cutting bonds, diversification from Occidental economies into the Orient and a lot of concern about inflation hedging. Maintaining a position in Gold, and thinking about how to invest in recovery commodities as the global economy emerges next year. And looking to put my cash to work.

* * *

Get your wallets out and please consider making a donation to WWTW’s Walking Home For Christmas appeal! I would consider it a small thanks for your daily Morning Porridge, but its a very worthwhile charity this difficult year: https://www.walkinghomeforchristmas.com/teams/team-morning-porridge

via ZeroHedge News https://ift.tt/3fwQNLZ Tyler Durden

Two women started filming when the stumbled upon Governor Murphy eating dinner at a restaurant with his family.

“Oh my god Murphy you are such a dick” one woman shouted. As the governor looked over, his son spoke up and started taunting the women. That elicited a foul-mouthed tirade from one of the hecklers. “How you doing? How you doing? You having fun with your family in the meantime? You’re having all kind of other bullshit going on at your house?”

Murphy frowned, then smiled, as he calmly continued to eat. No one at the table was wearing a mask at the beginning of the video. New Jersey requires people to wear masks except when it is impractical, like when people are eating.

Murphy’s son responded to the women by saying he liked one of their “Trump” phone cases, pointing to his father and saying, “Guess who Trump likes? He likes my dad.”

As the footage ended, the governor could be seen putting on a face mask.

“The state has experienced significant upticks in the rate of reported new cases across all counties, demonstrating the need for many of the state’s current measures to remain in place, both to reduce additional new infections and to save lives,” Murphy said, according to NJ.com.

The confrontation comes shortly after Murphy’s latest executive order extended New Jersey’s emergency measures for another 30 days, marking the ninth time the governor has extended New Jersey’s public health emergency since March 9.

via ZeroHedge News https://ift.tt/35XiJWa Tyler Durden

JPMorgan Estimates Up To $310 Billion In Forced Selling By Year-End Tyler Durden

Mon, 11/23/2020 – 06:24

Earlier this week we reported that with month-end fast approaching, banks are starting to publish their estimates of what upcoming pension rebalancings will mean for stock and bond flows.

The first such forecast came from Goldman Sachs, whose month-end pension rebalancing published on Wednesday estimated that a net $36BN of equities to sell following a month of substantial outperformance of stocks vs bonds. Notably, according to Goldman, this is the fourth largest sell estimate on record going back to 2000, and ranks in the 96th percentile among all buy and sell estimates in absolute dollar-value.

Well, not to be outdone, JPMorgan which has accumulated a track record of estimating rebalancing flows (even if at times it means one JPM quant’s estimates facing off against another), writes that according to its own calculations, the $7 trillion universe of balanced mutual funds is on pace for a far greater month and quarter-end selling spree than the one estimates by Goldman… greater as much as 10x.

In response to client interest sparked by the Goldman report, JPM’s Nick Panigirtzoglou writes that as we approach month-end, “the equity rebalancing flow question is resurfacing in our client conversations” to wit: “How much of equity rebalancing flow should we expect into month-end, i.e. into the end of November? And how much more rebalancing into quarter-end, i.e. into the end of December?”

To answer this question, the JPMorgan strategist look at the four key multi-asset investors that have either fixed allocation targets or tend to exhibit strong mean reversion in their asset allocation. These are – in addition to the defined benefit pension plans previously highlighted by Goldman – also mutual funds, such as 60:40 funds, the Norwegian sovereign/oil fund, i.e., The Norges Bank, and lastly the Japanese government pension plan, GPIF.

Balanced mutual funds including 60:40 funds, a close to $7tr AUM universe globally, tend to rebalance relatively more quickly on a monthly basis or so.

Assuming that this universe of balanced mutual funds which tend to maintain a 60/40 equity/bond split, were fully rebalanced at the end of October, and by taking into account the MTD performance of global equities and bonds which has seen stocks drastically outperforming fixed-income by 10.45% (S&P total-return 10.50%, 10yr total-return 0.05%), JPM estimate around -$160bn of negative equity rebalancing flow by balanced mutual funds globally into the end of November.

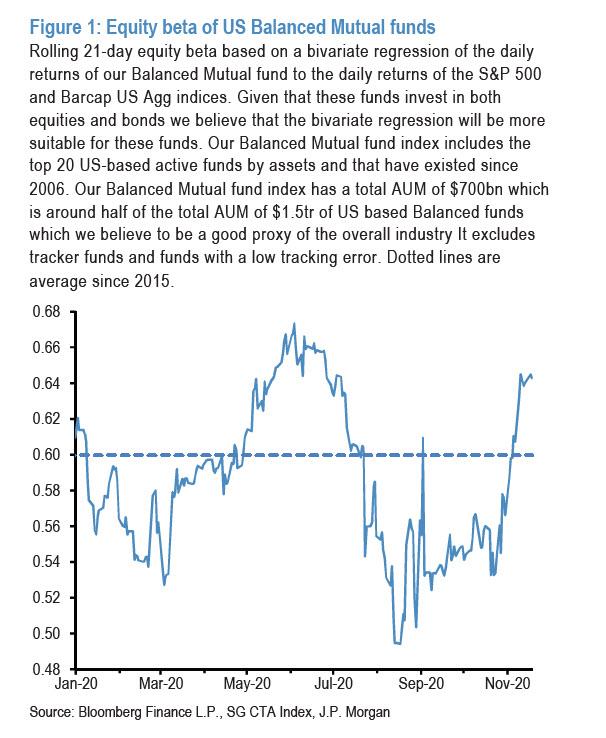

The bank caveats that this estimate could be wildly different if its assumption that balance funds were, in fact, not fully rebalanced at the end of October. And, as it further notes, its equity beta shown in the chart below, suggests that this was likely not true and that US balanced mutual funds in particular have been rather underweight equities during October.

However, this was offset by the moves at the start of the month, when the beta of US balanced mutual funds rose steeply at the beginning of November, rising to well above the neutral or average line by the middle of the month, as balanced mutual funds appear to have boosted their equity exposures over the first two weeks of November.

According to Panigirtzoglou, “if the picture in Figure 1 is a true reflection of how balanced mutual funds have been positioned in recent weeks, then there would be some vulnerability in equity markets in the near term from balanced mutual funds having to sell equities to revert to their 60:40 equity:bond target allocation, either by the end of November or by the end of December at the latest.”

There’s more: according to JPM, the equity rebalancing flow is likely to also be an issue into year or quarter-end, i.e. the end of December, especially if equity markets continue to grind higher into December. This is because of likely negative pending rebalancing by entities that tend to rebalance on a quarterly basis, such as US defined benefit pension plans, Norges Bank, i.e. the Norwegian oil fund, and the Japanese government pension plan, GPIF. Some estimates:

US defined benefit pension plans are a big $7.5tr AUM universe. They tend to rebalance more slowly over 1-2 quarters or so. Assuming they were fully rebalanced at the end of September, and by taking into account the QTD performance of US equities and bonds, JPM believes that the pending equity rebalancing flow by US defined benefit pension plans into the current quarter-end is negative at around -$110bn.

By doing the same calculation for Norges Bank, a $1.2tr AUM entity, the bank estimates that the pending equity rebalancing flow by Norges Bank into the current quarter-end is likely negative at around $15bn.

A similar calculation for the giant Japanese government pension plan, GPIF, a $1.5tr AUM entity, JPM estimates that the pending equity rebalancing flow by GPIF into the current quarter-end is likely negative at around -$25bn.

In all, Panigirtzoglou echoes Goldman’s month/quarter end year-end selling concerns, writing that he sees “some vulnerability in equity markets in the near term from balanced mutual funds, a $7tr universe, having to sell around $160bn of equities globally to revert to their target 60:40 allocation either by the end of November or by the end of December at the latest.”

And should the market rally continue into December, JPM concludes that it could give rise to an additional $150bn of forced equity selling into the end of December – a total of more than $300 billion – by pension fund entities that tend to rebalance on a quarterly basis.

In short: nearly a trillion dollars worth of stock selling by rebalancing funds may be on deck, begging the question: when will traders start frontrunning this potentially massive wall of money, which could hit just as market liquidity is at record lows…

… resulting in an outsized move to the downside if this culminates in a liquidation frenzy.

via ZeroHedge News https://ift.tt/35P1s1s Tyler Durden

JPMorgan Estimates Up To $310 Billion In Forced Selling By Year-End Tyler Durden

Mon, 11/23/2020 – 06:24

Earlier this week we reported that with month-end fast approaching, banks are starting to publish their estimates of what upcoming pension rebalancings will mean for stock and bond flows.

The first such forecast came from Goldman Sachs, whose month-end pension rebalancing published on Wednesday estimated that a net $36BN of equities to sell following a month of substantial outperformance of stocks vs bonds. Notably, according to Goldman, this is the fourth largest sell estimate on record going back to 2000, and ranks in the 96th percentile among all buy and sell estimates in absolute dollar-value.

Well, not to be outdone, JPMorgan which has accumulated a track record of estimating rebalancing flows (even if at times it means one JPM quant’s estimates facing off against another), writes that according to its own calculations, the $7 trillion universe of balanced mutual funds is on pace for a far greater month and quarter-end selling spree than the one estimates by Goldman… greater as much as 10x.

In response to client interest sparked by the Goldman report, JPM’s Nick Panigirtzoglou writes that as we approach month-end, “the equity rebalancing flow question is resurfacing in our client conversations” to wit: “How much of equity rebalancing flow should we expect into month-end, i.e. into the end of November? And how much more rebalancing into quarter-end, i.e. into the end of December?”

To answer this question, the JPMorgan strategist look at the four key multi-asset investors that have either fixed allocation targets or tend to exhibit strong mean reversion in their asset allocation. These are – in addition to the defined benefit pension plans previously highlighted by Goldman – also mutual funds, such as 60:40 funds, the Norwegian sovereign/oil fund, i.e., The Norges Bank, and lastly the Japanese government pension plan, GPIF.

Balanced mutual funds including 60:40 funds, a close to $7tr AUM universe globally, tend to rebalance relatively more quickly on a monthly basis or so.

Assuming that this universe of balanced mutual funds which tend to maintain a 60/40 equity/bond split, were fully rebalanced at the end of October, and by taking into account the MTD performance of global equities and bonds which has seen stocks drastically outperforming fixed-income by 10.45% (S&P total-return 10.50%, 10yr total-return 0.05%), JPM estimate around -$160bn of negative equity rebalancing flow by balanced mutual funds globally into the end of November.

The bank caveats that this estimate could be wildly different if its assumption that balance funds were, in fact, not fully rebalanced at the end of October. And, as it further notes, its equity beta shown in the chart below, suggests that this was likely not true and that US balanced mutual funds in particular have been rather underweight equities during October.

However, this was offset by the moves at the start of the month, when the beta of US balanced mutual funds rose steeply at the beginning of November, rising to well above the neutral or average line by the middle of the month, as balanced mutual funds appear to have boosted their equity exposures over the first two weeks of November.

According to Panigirtzoglou, “if the picture in Figure 1 is a true reflection of how balanced mutual funds have been positioned in recent weeks, then there would be some vulnerability in equity markets in the near term from balanced mutual funds having to sell equities to revert to their 60:40 equity:bond target allocation, either by the end of November or by the end of December at the latest.”

There’s more: according to JPM, the equity rebalancing flow is likely to also be an issue into year or quarter-end, i.e. the end of December, especially if equity markets continue to grind higher into December. This is because of likely negative pending rebalancing by entities that tend to rebalance on a quarterly basis, such as US defined benefit pension plans, Norges Bank, i.e. the Norwegian oil fund, and the Japanese government pension plan, GPIF. Some estimates:

US defined benefit pension plans are a big $7.5tr AUM universe. They tend to rebalance more slowly over 1-2 quarters or so. Assuming they were fully rebalanced at the end of September, and by taking into account the QTD performance of US equities and bonds, JPM believes that the pending equity rebalancing flow by US defined benefit pension plans into the current quarter-end is negative at around -$110bn.

By doing the same calculation for Norges Bank, a $1.2tr AUM entity, the bank estimates that the pending equity rebalancing flow by Norges Bank into the current quarter-end is likely negative at around $15bn.

A similar calculation for the giant Japanese government pension plan, GPIF, a $1.5tr AUM entity, JPM estimates that the pending equity rebalancing flow by GPIF into the current quarter-end is likely negative at around -$25bn.

In all, Panigirtzoglou echoes Goldman’s month/quarter end year-end selling concerns, writing that he sees “some vulnerability in equity markets in the near term from balanced mutual funds, a $7tr universe, having to sell around $160bn of equities globally to revert to their target 60:40 allocation either by the end of November or by the end of December at the latest.”

And should the market rally continue into December, JPM concludes that it could give rise to an additional $150bn of forced equity selling into the end of December – a total of more than $300 billion – by pension fund entities that tend to rebalance on a quarterly basis.

In short: nearly a trillion dollars worth of stock selling by rebalancing funds may be on deck, begging the question: when will traders start frontrunning this potentially massive wall of money, which could hit just as market liquidity is at record lows…

… resulting in an outsized move to the downside if this culminates in a liquidation frenzy.

via ZeroHedge News https://ift.tt/35P1s1s Tyler Durden

Futures Jump, Dollar Tumbles On Fresh Vaccine Hopes Tyler Durden

Mon, 11/23/2020 – 07:57

US equity futures, global stock and oil prices rose on Monday while the dollar and Treasuriss fell amid renewed hopes for economic revival on coronavirus vaccines, even as the world contended with surging case numbers and delays to fresh U.S. stimulus. Shortly after 2am ET, futures spiked to session highs, after AstraZeneca become the latest major drugmaker to say its vaccine for the virus could be around 90% effective, joining Pfizer and Moderna.

Ironically, while futures jumped amid expectations that at least one of these vaccines will be successful, AstraZeneca’s own shares fell 1.8% as traders perceived the efficacy data as disappointing compared with rivals, whose efficiency was around 95%.

There was more Covid action, with Regeneron also jumping 5.7% in pre-market trading after it announced during late U.S. hours on Saturday that its antibody cocktail for treating early Covid-19 symptoms received FDA emergency-use authorization (EUA). “While not surprising, this represents another important milestone for the infectious disease franchise,” Barclays analyst Carter wrote, adding that he sees the treatment adding an “incremental near-term driver” for earnings from 4Q through next year.

Finally, also over the weekend we learned that the first COVID-19 vaccine could be available within weeks after the U.S. Food and Drug Administration said it was likely to approve in mid-December the distribution of the vaccine made by Pfizer and German partner BioNTech, a top official of the government’s vaccine development effort said on Sunday.

“Markets continue to look through the near-term Covid-19 burdens,” said Robert Greil, chief strategist at Merck Finck Privatbankiers. “With political uncertainty in the U.S. fading in addition to the end of the virus tunnel looming, speed bumps for markets become less scary going forward.”

The rally showed investors are willing to look past the grim U.S. case numbers – cases topped 12 million over the weekend – and weak European economic data released on Monday. Evidence of high efficacy rates in experimental vaccines lifted the benchmark S&P 500 to a record high earlier this month, although gains have since been capped by concerns around more lockdowns to contain a surge in infections. Nevada on Sunday became the latest U.S. state to tighten restrictions on casinos, restaurants and bars, while imposing a broader mandate for face-coverings over the next three weeks.

Despite the backdrop of accelerating COVID-19 infections in the United States, the forecast helped to raise hopes that lockdowns that have paralyzed the global economy could be nearing an end: “Today’s vaccine news is positive, but it is only partly responsible for the rally in stock markets this morning, which is also being driven by the news that the United States hopes to start the vaccination program in under three weeks,” said Philip Shaw, chief economist at Investec in London.

Meanwhile, after data last week signaled a faltering labor market recovery, flash readings of business activity surveys due today are expected to show the manufacturing and services sectors expanded at a slower pace in November. Indeed, the progress towards approval and roll-out of multiple vaccines overshadowed the sobering news concerning the first European PMI readings of November, which saw the service PMI tumble from 46.9 to 41.3, missing expectations, while mfg PMI beat despite also sliding amid the new covid lockdowns.

EU Comp Flash PMI 45.1 vs. Exp. 46.1 (Prev. 50.0)

EU Services Flash PMI 41.3 vs. Exp. 42.5 (Prev. 46.9)

EU Manufacturing Flash PMI (Nov) 53.6 vs. Exp. 53.1 (Prev. 54.8)

Or maybe not, because after surging 0.9% in early trading on the AZN news, Europe’s Stoxx 600 index which had risen to its highest since February, gave up all gains and was little changed as of 12:11pm in London, with health-care stocks among the weakest sectors, led – paradoxically – by the health-care index down -0.8%, with AstraZeneca -1.7%, and the personal care index was worst-performing sector, down 1.2%. Meanwhile, energy stocks continue to rally, up 2%; basic materials stocks also outperform, +1.3%; Banks are up 1.2%.

Despite the wobble, today’s action took Europe’s November gains to 15% and followed another record high for Asian equities even before the announcement of latest vaccine news. MSCI’s broadest index of Asia-Pacific shares outside Japan looked set to end the day 0.8% higher. Australian shares gained 0.3% as the country eased some COVID-19 restrictions. Most of the country has seen no new community infections or deaths in several weeks. Chinese bluechips had finished 1% higher, Seoul’s KOPSI climbed 1.9% and Bangkok jumped 2.2% to hit a five-month high. China’s CSI 300 Index of key equities listed in Shanghai and Shenzhen rose 1.3% to close a session over 5,000 points for the first time since June 2015; a subindex of energy stocks adds 3.8% as the best performer among the measure’s 10 industry groups. Yanzhou Coal Mining rose by the daily limit of +10% while China Oilfield Services was up +6.7%. The SSE 50 Index of large caps advances 1.7% to highest in 12 years after hovering near that level since July

In FX, the BBDXY slipped to new lows for the year (-0.30%), while the the euro edged up to 1.1864 as the dollar tested the bottom of a range. The pound rallied as much as 0.8% to 1.3381, highest since Sept. 2, bolstered by signs the U.K. and European Union are close to agreeing a deal. According to Bloomberg, sterling options suggest a Brexit trade deal is largely priced in; demand for puts stays strong across tenors, with the front-end better bid for dollar topside. In Asia, the Renminbi underperformed slightly as onshore rates dipped, following numerous (consecutive) days of gains last week. However, the overall disposition of Asian currencies was healthy, reflecting what is now an embedded trend vs the USD (KRW +0.30%, THB +0.15%).

In rates, yields rose around the globe amid a wave of risk-on sentiment. Treasury futures hovered near session lows as U.S. trading began after the AstraZeneca news, which added to pressure on Treasuries with holiday-week compressed auction cycle set to begin. Yields were cheaper by 0.5bp to 3.6bp across the curve led by long end, steepening 2s10s and 5s30s by more than 2bp; 10-year yields around 0.85% is ~3bp higher on the day and ~2bp wider vs bunds. Sales include record-sized 2Y ($56BN) and 5Y ($57BN) auctions on Monday and $56BN sale of 7-year paper on Tuesday.

Commodity markets rose with traders optimistic about a recovery in crude demand pushing oil higher. Brent crude futures rose 63 cents, or 1.4%, to $45.59 a barrel in London. WTI crude gained 49 cents, or 1.2%, to $42.91 a barrel. Both benchmarks jumped 5% last week. “Positive sentiment continues to be driven by the recent good news about the efficacy of coronavirus vaccines in development and the expectation that the OPEC+ meeting at the end of this month could see the group extend current cuts by three to six 6 months,” said Stephen Innes, chief global markets Strategist at Axi, a financial services firm.

Safe-haven gold, meanwhile, drifted at $1,872 per ounce, having lost almost 10% since peaking in earlier August.

On Today’s calendar we get the Chicago Fed Activity Index, and the Markit US Manufacturing PMI data. Fed speakers include Barkin, Daly, Evans. Also as noted above, the U.S. sells 2Y and 5Y notes, and TSY bills.

Market Snapshot

S&P 500 futures up 0.6% to 3,575.75

STOXX Europe 600 up 0.5% to 391.56

MXAP up 0.6% to 189.96

MXAPJ up 0.8% to 630.45

Nikkei down 0.4% to 25,527.37

Topix up 0.06% to 1,727.39

Hang Seng Index up 0.1% to 26,486.20

Shanghai Composite up 1.1% to 3,414.49

Sensex up 0.5% to 44,095.28

Australia S&P/ASX 200 up 0.3% to 6,561.59

Kospi up 1.9% to 2,602.59

Brent futures up 1.9% to $45.82/bbl

Gold spot down 0.1% to $1,869.14

U.S. Dollar Index down 0.2% to 92.20

German 10Y yield rose 0.4 bps to -0.579%

Euro up 0.2% to $1.1876

Italian 10Y yield fell 0.8 bps to 0.522%

Spanish 10Y yield fell 0.2 bps to 0.063%

Top Overnight News from Bloomberg

President-elect Joe Biden intends to name his longtime adviser Antony Blinken as secretary of state, according to three people familiar with the matter, setting out to assemble his cabinet even before Donald Trump concedes defeat

Several key allies for Trump appeared to lose their patience over the weekend. Senators Lisa Murkowski of Alaska and Kevin Cramer of North Dakota — one of Trump’s staunchest allies — on Sunday called for the transition to Biden to begin. Senator Pat Toomey congratulated Biden on his victory after Trump suffered another legal defeat in Pennsylvania

The Trump administration is close to issuing a list of 89 Chinese aerospace and other companies that would be unable to access U.S. technology exports due to their military ties, Reuters reported, a move that could escalate tensions as the Biden administration prepares to take over

The admission of foreign investors into China’s $15 trillion bond market—cemented this year when the country rounded out its inclusion in all three of the top global indexes—may just mark the big bang equivalent to WTO entry

U.K. Prime Minister Boris Johnson will announce a massive increase in community coronavirus testing on Monday as part of a plan to reintroduce tiered restrictions in place of the England-wide lockdown that ends on Dec. 2

Norges Bank reduces its daily foreign exchange sales on behalf of government from Nov. 23 as there is less foreign exchange for Norges Bank to convert than previously assumed due to reduced transfers from wealth fund

The euro area is slipping into another contraction amid new virus restrictions that are taking a massive toll on parts of the economy. IHS Markit’s composite Purchasing Managers’ Index fell to 45.1 in November from 50 in October, hinting at declining output, according to data published Monday

Germany is moving toward extending and tightening its shutdown restrictions, setting measures that would rein in New Year’s festivities as the country struggles to slow the rapid spread of the coronavirus

A look around global markets courtesy of NewsSquawk

Asian equity markets began the week on the front boot amid virus treatment hopes after reports the FDA granted EUA for Regeneron’s REGN-COV2 antibody cocktail but with some of the optimism in the region offset by concerns regarding rising infections. ASX 200 (+0.3%) traded higher following upgrades in domestic PMI data and as the energy sector spearheaded the commodity-led push after Ampol surged on reports it will receive a higher amount for the stake in its convenience property portfolio and will conduct a AUD 300mln share buyback. However, the gains in the index were restricted as financials lagged with IAG shares resuming their underperformance for a 3rd consecutive session. KOSPI (+1.9%) outperformed after a surge in exports for the first 20 days in November helped participants overlook the rising COVID-19 infection rates which prompted an increase in the Greater Seoul area social distancing level to 2 from 1.5 effective from Tuesday. Hang Seng (+0.1%) and Shanghai Comp. (+1.1%) were mixed with the mainland kept afloat following a PBoC liquidity injection and with Hong Kong subdued by weakness in casino and property names. Furthermore, the HK-Singapore travel bubble was delayed for 2 weeks which pressured shares in their respective flag carriers, while recent reports also noted the US is very close to declaring that 89 Chinese aerospace and other companies have links to the Chinese military which could stop them from receiving certain US exports. As a reminder, Japanese markets were closed due to Labor Thanksgiving Day.

Top Asian News

Hong Kong-Singapore Bubble Delay Hits Travel Rebound Hopes

Abu Dhabi Plans $122 Billion in Oil Spending to Boost Output

European equities kicked the week off higher across the board amid tailwinds from the APAC region and amid another positive COVID-19 vaccine update, this time from AstraZeneca, whose vaccine candidate reported an average efficacy of 70% across two dosing regiments. One regiment showed efficacy of 90% (half dose followed by a full dose at least one month apart), whilst the second regiment showed 62% efficacy when given as two full doses at least one month apart. Storing conditions are also favourable as the vaccine can be stored, transported and handled at normal refrigerated conditions (2-8 degrees Celsius/ 36-46 degrees Fahrenheit) for at least six months. By way of comparison, Pfizer/BioNTech’s candidate showed a 90% efficacy rate with storage temperatures at -70 degrees Celsius, whilst Moderna’s candidate showed efficacy of 94.5% with stable storage at standard fridge temperatures (2-8 degrees Celsius) for 30-days and shipping/long-term storage conditions at standard freezer temperatures of -20 degrees Celsius for 6-months. Since the update however, European cash and equity futures have waned off best levels (Euro Stoxx 50 +0.6%) but ES (+0.6%), NQ(+0.4%) and RTY (+1.0%) hold onto gains. The update resulted in flows into cyclicals as opposed to the rotational/reflationary playbook experienced upon the release of the early data from PFE/BNXT and MRNA. This cyclical play is reflected in European sectors as Oil & Gas, Basic Resources, Banks outpace peers whilst defensive sectors Utilities, Healthcare and Staples lag. Interestingly, AstraZeneca shares trade lower by some 1.5% with some citing the average efficacy being sub-par when compared to PFE/BNTX and MRNA, whilst others note of “buy the rumour, sell the fact” play. Nonetheless, losses in the largest FTSE 100 constituent has capped the index which trades with gains of some 0.3%, whilst losses in Healthcare prompted the SMI (-0.1%) to dip into negative territory. Elsewhere, the Travel & Leisure sectors is buoyed by the vaccine news alongside reports that UK will lift blanket quarantine restrictions on December 15th so families can travel to red list countries for Christmas, while the length of time people will need to self-isolate will be cut to 5 days from 14 days if a UK holidaymaker tests negative 5 days after returning. Thus, IAG (+4%) and easyJet (+5.4%) trade with firm gains, whilst Carnival (+2.8%) shrugs off reports that the US CDC escalated its warning for cruise travel to the highest level, alongside separate reports that Carnival’s Holland America Line extended cruise pause to include all departures through March 31 2021.

Top European News

U.K. Output Contracts as New Covid Lockdown Hits Services

Germany Moves Toward Tightening Partial Lockdown to Dec. 20

Bank That Pioneered Green Bonds Sets Ultimatum for Clients

Europe’s Virus Lockdowns Push Economy Into Another Contraction

In FX, the Pound is outperforming across the board amidst heightened hopes that UK and EU negotiators can make further progress via videoconference following reports that a trade deal is just 5% away from being completed, albeit with the remaining unresolved issues said to be the core areas of contention. PM Johnson is supposedly working on significant intervention in an effort overcome differences and to this end is expected to speak to European Commission President von der Leyen to tray and clear the remaining obstacles. Cable has cleared several recent highs in response, including a pseudo double top circa 1.3312-14 on the way through September 3’s 1.3359 peak to expose 1.3400 and the 1.3403 September 2 apex, while Eur/Gbp is back below 0.8900 and eyeing 0.8861 from November 11. For the record, not much response to better than expected flash PMIs as services and composite readings both retreated into contractionary territory.

AUD/NZD/CAD/DXY – The non-US Dollars are all revelling in the upbeat and risk-on market tone assisted by more positive COVID-19 vaccine updates, while the Aussie is also acknowledging improvements in PMIs and the Kiwi a healthy rebound in retail sales. Aud/Usd is back on the 0.7300 handle and Nzd/Usd is hovering around 0.6950, while Usd/Cad has retreated to test 1.3050 against the backdrop of buoyant crude prices in advance of comments from BoC’s Gravelle. Conversely, the Greenback has started the new week under pressure with the index hovering within a 92.343-92.072 range after dipping under the low seen on November 11 (92.129) awaiting the US national activity index, preliminary Markit PMIs and further Fed speeches from Daly and Evans.

EUR – Somewhat mixed Eurozone PMIs have not really impacted the Euro, with perhaps more focus on the preliminary surveys that could show more coronavirus contagion given the resurgence in Spain and Italy. Instead, Eur/Usd is holding firmly above 1.1850 and targeting last week’s best levels clustered between 1.1891-94 for another attempt to reach 1.1900 and the 1.1920 pinnacle posted on November 9, but wary that this may well prompt more verbal intervention from the ECB.

CHF/JPY – The traditional safe-havens are floundering alongside the Buck within tight ranges near 0.9100 and 104.00 respectively, with the former probably surprised to see no evidence of SNB action from weekly Swiss sight deposits and the latter devoid of domestic input due to Japan’s Worker’s Day market holiday.

SCANDI/EM – Somewhat mixed impulses for the Sek and Nok in particular given broad risk appetite and the aforementioned rise in oil, but the Norges Bank cutting daily foreign currency sales to Nok 500 mn from Nok 1.6 bn. Hence, Eur/Sek and Eur/Nok are both meandering within 10.2240-2020 and 10.7135-6410 parameters. Elsewhere, the Try continues to unwind post-CBRT recovery gains, but the Zar is holding up relatively well in spite of SA ratings downgrades from S&P and Fitch.

In commodities, WTI and Brent Jan futures continue on their upwards trajectory on vaccine euphoria coupled by expectations that OPEC+ will continue current cuts through Q1 2021 irrespective of the recent vaccine updates, which, as things stand provide a rosier price outlook in the medium-term as reflected by the six-month Brent contango being at the shallowest since mid-June. Aside from that, news-flow has been somewhat light throughout early European hours. Overnight there were reports that Yemeni Houthis carried out a missile attack on a Saudi Aramco distribution station, although sources via Energyintel suggested there was no damage to any facilities or personnel. Separately, Abu Dhabi’s Supreme Petroleum Council announced new discoveries of 22bln bbls of recoverable unconventional oil resources, although this is unlikely to impact near-term supply to the market as UAE is still constrained by OPEC+ quotas. WTI Jan now back under USD 43bbl (vs. low 42.29/bbl), whilst its Brent counterpart briefly eclipsed USD 46/bbl (vs. low 44.89/bbl) before yielding the handle. Spot gold and silver move in-line with the risk sentiment as the precious metals post mild losses with the former around USD 1870/oz (vs. high 1876/oz) whilst spot silver dipped below USD 24/oz (vs. high ~24.35/oz), whilst copper prices fail to coattail on the risk appetite as a union at the Candelaria mine accepted a wage offer, in turn bringing an end to a month-long strike, albeit “a worker’s union at Antofagasta’s Centinela copper mine is set to reject management’s latest contract offer next week, which could lead to strike action”, according to ING.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 0.3, prior 0.3

9:45am: Markit US Manufacturing PMI, est. 53, prior 53.4

9:45am: Markit US Services PMI, est. 55, prior 56.9

9:45am: Markit US Composite PMI, prior 56.3

DB’s Jim Reid concludes the overnight wrap

Regular readers will know that the soundtrack to my WFH has been Acoustic Chill Radio. They do have a limited playlist though and after 8 months and I can now pretty much second-guess the loop of songs they are going to play once I hear one. I’ve always prided my self on being very knowledgable about music but there’s been one song that I’ve really, really liked that I’d never heard before. 8 months later I finally decided to try to find out what it was. Maybe it was some obscure artist I could impress people with once I was allowed back into the wild again. Imagine my shock when I discovered it was the acoustic version of the debut solo single from Zayn from One Direction and that it was actually a huge global hit in 2016. I’m not sure when I got old.

I might get a chance to recover from the shock in the second half of this week as with Thanksgiving on Thursday, activity is likely to progressively die down on Wednesday through to the weekend. The most important events of the last two weeks have both happened just before 7am NY on Monday with the Pfizer/BioNTech and Moderna vaccine news. It doesn’t feel like AstraZeneca/Oxford is quite ready to report but as a precaution I will have my eyes glued to the wires at this time today just in case. The latest on the vaccine from the weekend is that the US seems to be targeting December 11th or 12th for the start of the rollout, according to the head of the Warp Speed program. Overnight, the Telegraph has reported that the UK may give emergency approval to Pfizer’s vaccine as soon as this week.

In terms of the latest on the virus, as cases are stabilising in Europe, various governments are now planning to exit their lighter lockdowns. The Telegraph has reported that the UK will announce today that quarantine restrictions will ease in time for Christmas so that families can travel to high-risk countries to visit relatives while Bloomberg has reported that PM Johnson will announce a massive increase in community testing as part of a plan to reintroduce tiered restrictions. The French government is planning a three-phase reduction in lockdown measures in December. Italy is also mulling over the temporary easing of lockdown restrictions in the run-up to Christmas to allow shops to open for longer hours in the worst-hit regions. However, in the US, states are continuing to impose fresh restrictions with the latest being Nevada where Governor Steve Sisolak announced that capacity at gaming operations and venues including restaurants, bars and gyms will be reduced to 25% of fire-code capacity, down from 50%. Elsewhere, the Greater Los Angeles area will see outdoor dining get banned with restaurants, breweries and bars once again limiting their businesses to just pick-up and delivery. On the positive side, Regeneron’s antibody cocktail received an emergency-use authorisation from the US FDA for treatment of early Covid-19 symptoms.

On the restrictions, today we’ll know a bit more about how much they have stunted the economic recovery as the flash November PMIs from around the world are released. So far in Asia, Australia’s PMIs printed better than last month with manufacturing at 56.1 (vs. 54.2) and services at 54.9 (vs. 53.7) bringing the composite reading to 54.7 (vs. 53.5 expected). Meanwhile, markets in the region have started the week on the front foot with the Shanghai Comp ( +1.27%), Kospi (+1.83%) and ASX (+0.34%) all up. The Hang Seng is down a modest -0.09% and Japan’s markets are closed for a holiday. Futures on the S&P 500 are up +0.26%. In FX, the US dollar index is down -0.15%.

In other overnight news, Reuters has reported that the US is close to issuing a list of 89 Chinese companies (aerospace and other sectors) that have military ties and would be unable to access US technology exports.

In terms of week ahead, the Brexit talks will move to a virtual format after one of the EU negotiators tested positive for Covid-19. There had been reports last week suggesting that we may see a deal reached by the start of this week but it doesn’t feel we’re there yet. For a few months it’s felt like a case of five steps forward and four back on the path to some kind of deal. So progress but painfully slow. The Telegraph reported last night that PM Johnson is set to make a “significant Brexit intervention” whatever that means and speak to EC President Von Der Leyen “in an attempt to clear away final barriers” towards a deal. The article suggested that a week tomorrow is the new deadline. Face to face negotiations apparently begin again on Thursday.

Staying on the UK, this Wednesday will see the announcement of a one-year Spending Review, which will set departmental budgets for 2021-22. There had previously been hopes to conduct a multi-year review, but the Covid-19 uncertainty surrounding the public finances have seen the government opt for a one-year approach. This might give some clues though as to how long the fiscal taps will stay open and the first signs of how quickly and where taxes will be raised or public spending cut to try to restore some order. So important read-throughs for the future.

From central banks there isn’t a great deal taking place this week, though we will get the minutes from the FOMC’s November meeting on Wednesday. Our economists believe the focus will be on what the committee are thinking about in terms of changes to QE and perhaps on shaping future forward guidance. Their base case is that the Fed would prefer to gather a bit more information on the fiscal outlook and the economy before eventually extending the duration of purchases early next year.

Elsewhere in central bank world, today will see Bank of England Governor Bailey, as well as the MPC’s Haldane, Tenreyro and Saunders give evidence before the House of Commons’ Treasury Committee. Both the Riksbank and the Bank of Korea will also be announcing their latest monetary policy decision on Thursday.

Recapping last week now. The week started off with very promising vaccine news as Moderna announced efficacy numbers for its experimental vaccine that uses similar technology as that of Pfizer/BioNTech’s vaccine. The study showed a 94.5% efficacy rate and “only” needs to be transported at minus 20C, which is well above the minus 70C that the Pfizer/BioNTech vaccine is said to require. It also did well in reducing the severity of illness of those who still contracted the disease. This news moved markets less than the original Pfizer announcement; however, it gave the rotation trades into cyclicals slightly more momentum. The S&P 500 dropped -0.77% on the week (-0.68% Friday), while the high-growth tech stocks that make up the largest weightings of the index continued to lag.

Nevertheless, the NASDAQ rose +0.22% (-0.42% Friday) but the star of the week was Tesla which gained +19.86% after it was announced that the electric car maker would be included in the S&P 500 from December. Banks stocks on both sides of the Atlantic continued their rally even as yields fell, US banks rose +1.24% while European Banks were up a greater +4.00%. Similarly, European equities again outperformed given the STOXX 600’s more cyclical bias. The STOXX 600 ended the week +1.15% higher (+0.52% Friday) while the FTSE MIB (+3.84%), CAC 40 (+2.15%), and IBEX (+2.49%) all outperformed by even more.

Sovereign bonds gained even with the positive vaccine news as yields dropped back from close to their pandemic highs. US 10yr Treasury yields fell -7.2bps (-0.5bps Friday) to finish at 0.824% as 10yr Gilt yields dipped -3.6bps (-2.1bps Friday) to 0.30%. 10yr Bund yields were -3.6bps (-1.2bps Friday) to -0.58%. Elsewhere, credit spreads in the US and Europe tightened further on the week. US HY cash spreads were -11bps tighter, while European HY cash spreads tightened -18bps. US IG cash spreads tightened -5bps and IG was -4bps in Europe. In commodities, WTI (+5.03%) and Brent crude (+5.10%) rose sharply as global demand forecasts improved further as gold kept selling off (-0.96%). The last word goes to Bitcoin, which rallied +14.08% on the week (+3.59% Friday) as the cryptocurrency is dialling in on its all-time high from December 2017 again, but this time with more institutional buy-in. A fascinating story to watch.

via ZeroHedge News https://ift.tt/35SBAlg Tyler Durden

AstraZeneca COVID-19 Vaccine 70% Effective, UK Expects Millions Of Doses By Year’s End Tyler Durden

Mon, 11/23/2020 – 06:21

Continuing the pattern of leading COVID-19 vaccine projects releasing their Phase 3 trial results on Monday, AstraZeneca has just revealed that its vaccine – which, unlike the Moderna and Pfizer vaccines, relies on the more traditional adenovirus vector approach – is 70% effective at preventing the coronavirus.

The results follow last week’s release of the final data from the accelerated Phase 2 studies, which purported to confirm that the vaccine was safe and effective, particularly in elderly subjects, as the initial preliminary results had suggested.

UK Health Secretary Matt Hancock said Monday during an interview with Radio 4 that the UK will have a “low, single-million” number of AZ coronavirus vaccine doses available before the end of the year, assuming regulators approve the vaccine. Vaccinations should begin under a ‘plot program’ starting next month.

AZ CEO Pascal Soriot said the vaccine’s “efficacy and safety” showed it will be highly effective against the virus, and have “an immediate impact”.

AstraZeneca claimed that the vaccine actually appeared to be more effective than they anticipated: interestingly, the final 70% number was actually an average of two different late-stage trials in the UK and Brazil which also featured different dosing regimens.

When the Oxford-Astra Zeneca vaccine was given as a half dose, followed by a full dose at least one month later, efficacy – a measure of how a vaccine prevents infection or severe disease in trials — was 90%. However, when the jab was given as two full doses at least one month apart, efficacy was just 62%.

One expert said the fact that the vaccine is only 70% effective is “absolutely fine” since the adenovirus vector makes the vaccine much cheaper to produce and easier to ship. This increased availability should help make up for the lower effectiveness.

The company said that it will be seeking regulatory approval “immediately”, and AZ’s manufacturing partners around the world, including India’s Serum Institute, are targeting the production of up to 3 billion doses next year. Depending on regulatory approval, a lower first dose regimen could make more doses available.

While algos send AZ shares lower presumably off the 70% number, it’s worth noting that these headline efficacy numbers are virtually meaningless, as Pfizer showed us last week when it ‘revised’ the headline number to 95% from 90% so it wouldn’t be outdone by Moderna.

Investors would probably be better off focusing on the ease of distribution, which will likely decide which vaccines are the most widely distributed, as the WHO’s Covax initiative struggles to raise $18 billion to buy and distribute vaccines to the developing world. The AZ-Oxford vaccine only requires a basic level of refrigeration (unlike the Moderna and Pfizer vaccines, which must be stored and shipped at extremely cold temperatures) making it “more suitable” for rollout in poorer countries.

via ZeroHedge News https://ift.tt/35TIwhS Tyler Durden

Elizabeth Holmes Argues Her Wealth Had Nothing To Do Why She Committed Fraud Tyler Durden

Mon, 11/23/2020 – 05:45

Perhaps in doing her best to change her legal defense into some sort of comedy act, “America’s sweetheart” Elizabeth Holmes argued in court this week that she didn’t want U.S. prosecutors to vilify her “luxuriously lifestyle” during her fraud trial.

The request is ironic, as Holmes became a “self-made billionaire” through the fraud she was perpetrating at Theranos to begin with.

It’s the latest in a long line of scapegoats that Holmes has used to pin blame for her company’s implosion on. She had previously blamed journalists and had claimed that she was the victim of a “mental disease or defect”, according to Bloomberg.

The request came amidst a “flurry of evidence objections” from her lawyers, as they seek to try and rule out certain pathways of the prosecution’s case before her trial starts in March.

Her lawyers argued: “That Ms. Holmes enjoyed a certain lifestyle — one that is commensurate with the lifestyle of many other CEOs — says nothing about whether Ms. Holmes committed fraud to obtain or maintain that lifestyle.”

It’s a stunning objection especially considering the massive rise and fall of Holmes’ personal net worth as a result of Theranos’ valuation expanding, before imploding.

It’s a direct rebuke to prosecutors, who are going to argue that Holmes’ travel, accommodations, assistants and “association with celebrities, dignitaries and other wealthy and powerful people” acted as an incentive for her to continue to commit financial fraud.

We noted in September that the former Theranos Inc. Chief Executive had been ordered by a federal judge to undergo examination from U.S. government experts after her lawyers have suggested they could offer up evidence that shows she suffered from a “metal disease or defect”.

The order came after Holmes’ lawyers suggested they were going to introduce evidence from Mindy Mechanic, a California State University at Fullerton professor specializing in psychosocial consequences of violence, trauma and victimization. The defense said the evidence would be “relating to a mental disease or defect or any other mental condition of the defendant bearing on the issue of guilt.”

We can’t wait to see what turn this case takes next…

via ZeroHedge News https://ift.tt/3kXhwT8 Tyler Durden

Lockdowns are back on in Europe and are making a quick comeback in the US as well. Spain, the UK, Belgium, and France are back in full lockdown mode, although a multitude of restrictions on movement within each country remained in place even when full lockdowns were ended over the summer.

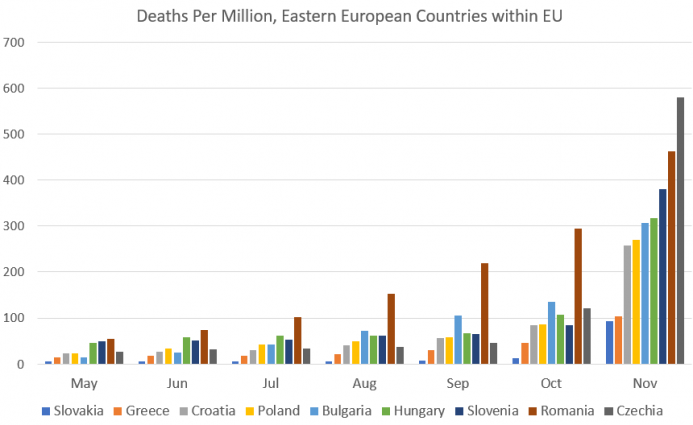

In France, for instance, one now “need[s] a certificate to move around,” yet in spite of long maintaining some of the continent’s most stringent lockdown and social distancing measures, total deaths per million are rapidly accelerating, to the point that France is likely to soon join other countries with harsh lockdowns in having among the worst rates of deaths per million in the world. Moreover, eastern Europe, which was once lauded for locking down strictly and early, is quickly finding that lockdowns aren’t likely to suppress total deaths there, either. The Czech Republic is seeing some of the worst growth in covid deaths worldwide, while the rest of the region is seeing similar growth, albeit to a less dramatic extent (so far).

Sources: Worldometer and Ourworldindata.org.

This is not what was sold to the public. Rather, politicians and their allies in the “public health” bureaucracies insisted that lockdowns would substantially reduce total deaths in countries that imposed them. Countries that failed to lock down would, on the other hand, experience runaway contagion with total Covid deaths per million orders of magnitude higher than those seen in countries that didn’t lock down.

That’s not what happened.

Cumulative deaths per million on the fifteenth of each month. Source: Worldometer.

Sweden, for instance, has long been denounced by politicians and media pundits for failing to embrace the methods of the French and the Spaniards. Many of these nations (i.e., Spain and the UK) have long had total Covid death per million well in excess of the Swedes. And now, other nations are surging (i.e., France and Czechia and the Netherlands) and will all likely soon be much higher than Swedish levels. (It might also be noted that Spain, the UK, France, Czechia, and Italy are now all seeing growth in Covid deaths at rates above that reported by the United States.)

Lockdowns Save Lives?

Of course, some supporters of lockdowns are likely to continue insisting that lockdowns clearly work to suppress total deaths because a handful of small countries near Sweden (i.e., Norway, Denmark, and Finland) have reported relatively few covid deaths. While this certainly may indicate there are factors at work in these countries that help keep covid mortality numbers lower, the fact remains that experience shows countries like Norway, Denmark, and Finland are outliers when compared to most of western Europe.

This isn’t exactly shocking. As early as July, studies were already beginning to show that lockdowns didn’t actually suppress total mortality. This one in The Lancet, for example, concludes,

government actions such as border closures, full lockdowns, and a high rate of COVID-19 testing were not associated with statistically significant reductions in the number of critical cases or overall mortality.

And in 2006, an extensive study in Biosecurity and Bioterrorism reported: “There are no historical observations or scientific studies that support the confinement by quarantine of groups of possibly infected people for extended periods” to slow the spread of influenza. No evidence has been offered for why this might be true of flu, but not true of Covid. Moreover, in a recent report from JPMorgan, Marko Kolanovic concluded that “re-opening did not change the course of the pandemic” and that “While we often hear that lockdowns are driven by scientific models, and that there is an exact relationship between the level of economic activity and the spread of [the] virus—this is not supported by the data.” Overall, evidence backing the lockdown theory has simply failed to materialize.

Where’s the Evidence?

Indeed, as Swedish authorities have long claimed, the experience points toward an outcome in which most countries will end up with similar total deaths per million regardless of lockdown policy.1 This looks more likely by the day. As noted by Dr. Gilbert Berdine here at mises.org, “The data suggest that lockdowns have not prevented any deaths from covid-19. At best, lockdowns have deferred death for a short time, but they cannot possibly be continued for the long term.” This, of course, is why even the WHO does not recommend lockdowns except as a very short term and ad hoc measure. The side effects of the lockdowns themselves are too dangerous.

We already know that isolation, unemployment, and other social ills caused by lockdowns affect both physical and mental health. But we also know that lockdowns lead to deaths from untreated medical conditions. Moreover, government health experts in many cases have callously cut off the elderly from all their social and family support. The Associated Press estimates that for “every two COVID-19 victims in long-term care, there is another who died prematurely of other causes.” Many of these deaths are brought on by neglect and isolation caused by state-mandated lockdown policies.

Examining Excess Mortality

But where would we find evidence of these deaths in the aggregate? Unfortunately, regimes spend very little time counting them. Rather, regimes often only record events in ways that help the regime. While they are careful to count as many covid cases and deaths as possible in big bright numbers reported daily by government officials, deaths caused by lockdowns are generally ignored.

Eventually, the only way to guess the impact of these other deaths will be through the “excess mortality” data. Excess mortality—using a definition now generally used in the media and by government officials—occurs when total mortality during a time period exceeds the average mortality experienced over the past five years.

Some initial reports have suggested that covid deaths comprise only around 70 percent of excess deaths (see here and here). Naturally, lockdown advocates claim that this shows covid deaths are being undercounted, and that covid deaths should be assumed to account for virtually all excess deaths. This is only conjecture.

In any case, we find, not surprisingly, that excess mortality in Sweden has been lower this year compared to many other western European countries with harsh lockdowns. For example, through October the average number of deaths for 2015–19 in Sweden was 72,972. In 2020, the total deaths for the same period was 76,375. That’s an increase of 4.6 percent.

Likewise, in France, 2020’s total excess mortality is up 6.4 percent. It’s up 12.7 percent in England and Wales, up 16 percent in Italy, and up 17 percent in Spain.

How much of this excess mortality in lockdown countries is attributable to the lockdowns themselves? For now that’s still unknown. But, as Dr. Berdine writes:

It seems likely that one will not have to even compare economic deprivation with loss of life, as the final death toll following authoritarian lockdowns will most likely exceed the deaths from letting people choose how to manage their own risk. After taking the unprecedented economic depression into account, history will likely judge these lockdowns to be the greatest policy error of this generation.

via ZeroHedge News https://ift.tt/2J3LYgU Tyler Durden