Dow Futures Surge To Record Highs On Yet Another “US-China Trade Deal Close” Headline

This is becoming utter farce…

Having ramped overnight to record highs, Dow futures just exploded higher on the back of a headline reporting that a White House Official tells Politico a deal with China is almost there…”

And the algos panic-bid stocks…

What happens if there is a deal? Priced in? Or, if there isn’t?

Iran Boasts It Doubled Uranium Enrichment Capacity On 40th Anniversary Of US Embassy Takeover

Iran has marked its 40th anniversary of the 1979 Islamic revolutionary takeover of the US embassy in Tehran and subsequent over year-long hostage crisis by announcing another major breach of the nuclear deal on Monday, as previously promised amid the continued Washington sanctions regimen, essentially now doubling its enrichment capacity.

Reuters reports “Iran is launching a new array of 30 advanced IR-6 centrifuges on Monday, the country’s nuclear chief Ali Akbar Salehi told state television,” which bringsthe total number to 60 IR-6 advanced centrifuges, in violation of its commitments under the 2015 JCPOA.

“Today, we are witnessing the launch of the array of 30 IR-6 centrifuges,” Saleh said, adding that it underscores the Islamic Republic’s “capacity and determination”.

Iranian missile exhibition, via Newsweek.

An IR-6 centrifuge is capable of enriching uranium ten times faster than limits set under the JCPOA, and crucially according to USA Today:

The move cuts into the one-year time limit that most experts estimate Tehran would need to have enough material to build a nuclear weapon, although there is little evidence to indicate that Iran is trying to weaponize its nuclear materials.

Though the US and its allies like Israel have long assumed Tehran is bent on acquiring nuclear weapons as soon as possible, a month ago Ayatollah Khamenei reaffirmed the supreme leader’s official condemnation of nukes, after prior top clerics of the regime previously declared them ‘un-Islamic’.

“Nuclear science is beneficial but since it’s not been coupled with love for humanity, it led to nuclear disasters. Despite having the ability to develop nukes, we firmly and bravely avoided it, for building and keeping nukes, like using them, is haram,” Ayatollah Khamenei said before a group of the nation’s top scientists in early October.

American embassy personnel were held hostage for 444 days. Monday marks four decades since the Islamic revolution and the US embassy takeover.

Over the past many weeks the West has been focused on rapid developments in northern Syria, with the Iran nuclear issue seeming to take a back-burner, and largely absent from the headlines; however, many analysts have pointed out that Trump’s latest “secure the oil” in Syria policy is actually precisely toward blocking ‘Iranian expansion’ in the region.

“There are short ladders and very long snakes. That one took us back to square 1..”

Trawling through the market headlines this morning, I’m struck by the number of comments about how much better the investment environment looks. There is less likelihood of a global recession, corporate earnings aren’t as bad as expected, and jobs are growing. I am unconvinced. I see worrying connections across the wires. From my perspective – which admittedly has been from a train in the middle of nowhere – it feels we’ve reached the end of something. Time has been called on this particular era of irrational market exuberance.

My spidey-senses are tingling due to manner in which events across markets, individual stocks, politics, geopolitics and gut-instinct are connected. I’m not predicting sudden or massive financial collapse – just a wake up and smell the coffee correction in Bonds (which feels underway), and selective deflation in over-sold sectors of the stock markets. As always, any reversal will set off wailing and despair, yet most of the critical lessons will be missed. Fear not – we will get another chance to relearn them in a few years time! (Blain’s Market Mantra No 2: The Market has no memory.)

It’s just as well we aren’t heading for the deep prolonged global recession so many naysayers have been predicting thru 2019. Slowdown yes. Trade is going to remain a problem. But growth drivers were changing anyway. Tech will change the world’s trade roads. China’s furious growth spurt of the last 20 years is over. India might be growing, but it lacks the state momentum to drive global growth the way China did. And climate change will prove deeply significant in the future as consumers are persuaded to believe food miles and imports matter.

Long-term the relationship between the West and China will continue to dominate economies. There is more of a wall than ever before. Xi has consolidated his position as defacto emperor. He will allow his mandarins to make a show of engaging on trade, but has made clear his distrust of Trump. We’ll see that distrust and divergence drive Occidental and Oriental Technological economies apart and inevitably lead to a variation of Cold War economics.

That’s all in the long-term. The medium term is going to be even more fascinating. Expect some surprising shifts over the next few months. Taking some of the effervescence out of overhyped expectations may be positive past the short-term pain. Consider what is to come like toothache: root canal surgery without anaesthetic. Anticipating the consequences is the trick.

Let me try to connect some of the dots:

We’ve heard immediate pushback from international investors on the $2 trillion Aramco valuation Crown Prince MBS demands. Bank’s anxious for fees now say $1.7 ish. Investors say far less, pointing out the returns are less than the other oil majors for much greater political risk. MBS has staked his and his country’s future on being able to diversify the economy away from oil. He can only do that by monetising Aramco because the Saudi Royals have squandered the massive wealth their oil once promised.

The consequences of failing to deliver diversification and jobs will be rising political dissent – which is becoming apparent. Instability in the Middle East? Never a good thing for a global economy still dependent on oil.

Saudi is heavily invested in the increasingly discredited Softbank Vision fund. No matter how many bone-saws are employed, losing $50 bln in the Vison fund will not increase MBS’ political longevity. Softbank’s London based trading head, Rajeev Misra was a genius in the market’s eye last year, but this year is pillioried for running a dysfunctional firm. The papers say his trading style is creating the same kind of losses that sank his former bank – Deutsche Bank. Softbank’s losses in its vision fund are steadily mounting – a string of losing IPOs (Uber and WeWork) spell the end of the Unicorn myth.

Who knew: companies with no discernible route to profit don’t work?

Deutsche Bank is a whole distraction in itself. That you can buy German’s leading bank for less than Malaysian Fraudster Jho Low nicked on an average day from 1MBS says it all about the lack of future proofing across the German economy – which begins to explain the structural problems Germany now faces redirecting national engineering talent and infrastructure. (And is why Europe is likely to remain mired in slowdown long after the rest of the global economy picks up.)

Meanwhile, Berkshire Hathaway – the quintessential fundamental value investor, sits on its largest ever cash pile – waiting for the right assets to buy. Timing is everything. You have to wonder what they know and expect? It’s not just the unicorns that are sinking Softbank feeling a lack of market love. The earnings season was stronger than anyone expected (after all, we were told to expect recession), but the bond market appears to have peaked meaning corporate credit quality and leverage is back in investors’ sights.

And if corporate America looks week, then what about the potential credibility of the Government? While the Democrats pursue impeachment, the world looks on in horror. If Trump was playing games with Ukraine – what has his son-in-law been promising the Saudis? Trump may or may not have committed a crime to justify impeachment – but the devil will be proving it clearly, openly and transparently. The Democrats are unlikely to get the 2/3 through the Republican dominated Senate they need to sling him. Who cares? The real issue is how American voters read the signal it sends in terms the 2020 election!

Not that the UK or Europe are any better. Political weakness is a major theme underlying global markets.

In Central banking we’ve got Christine Lagarde giving her first big speech has ECB head in Berlin later today. What’s her offer? More of the same plus an intent to bring Europe together in fiscal harmony to paper over the monetary cracks so apparent in the Euro? Good luck to her. Back in the UK – Mark Carney finishes at the end of January, but no one seems to be considering his successor during the election.

We Have Melt-Up: Futures Jump To New All Time High On “Trade Optimism”

In retrospect, the Trump administration’s decision to announce a “phased” launch of the trade deal with China – which does not exist yet, and will likely never be completed – was the most insightful announcement because not only did it drive stocks sharply higher on the day “phase one” was unveiled, but it has been pushing stocks higher ever since.

And sure enough, Monday has been no different because after a weekend full of Trump and Ross soundbites that a deal appears imminent and Trump even offered up the US as a venue for the “phase one” signing, even though nothing has actually been agreed yet, S&P futures levitated higher all session alongside global stocks while bonds slipped and the dollar inched higher.

As we reported over the weekend, commerce secretary Wilbur Ross expressed optimism the U.S. would reach a “phase one” trade deal with China this month and said licenses would be coming “very shortly” for American companies to sell components to Huawei Technologies, while Trump told reporters a trade deal, if completed, will be signed somewhere in the U.S.

As a result, optimism ran rampant in Europe with the Stoxx 600 Index extending gains, in what was a sea of green amid the abovementioned trade deal optimism; the index advanced 0.8% with automakers leading gain among sectors, rising 3% while mining shares and banks follow, with sector indexes up 2.4% and 1.6%, respectively.

Risk assets favored optimistic comments on trade from U.S. officials over caution from China and soft manufacturing PMIs, with major European equities all gaining over 0.75%, Autos gain nearly 3% after Ross comments downplay expectations for U.S. tariffs on EU automakers, offsetting another contraction in Eurozone manufacturing PMI, with the final print coming in at 45.9, just above the 45.7 flash print.

Meanwhile, Dow futures were up triple digits even as MacDonald’s fell in pre-market trading after its CEO was fired for an inappropriate relationship with an employee. The Stoxx Europe 600 Index headed for a four-year high, led by miners and automakers, which jumped after the U.S. commerce secretary said tariffs on importing vehicles into the American market might be unnecessary. All major Asian markets advanced except Tokyo’s, which was shut. An index tracking emerging-market was set for its biggest gain in three weeks.

“Everyone is kind of upbeat around the prospect of at least a partial China-U.S. trade deal,” Peter Dragicevich, a strategist at Suncorp Corporate Services, told Bloomberg TV. “It’s going to keep equities pretty supported.”

After last week’s Q3 earnings reporting peak, investors are eager to push up stocks for a fifth successive week, adding to the 22% gain this year in the S&P500, even as long-time bulls such as Ed Yardeni are starting to get worried, noting that a “market melt-up” is becoming a real risk: speaking on CNBC, Yardeni said that “if the S&P 500 forward earnings multiple ticks to 19 or 20, it could spark a “nasty correction.”

“I just don’t want too much of a good thing here. I’d like this bull market to continue at a leisurely pace not in a melt-up fashion,” he told CNBC’s “Trading Nation” on Friday. “That’s actually the risk.”

For now, however, nobody cars, and earnings continue to roll in around the world, in what is set to be the 3rd consecutive quarter of declining S&P500 earnings. In China, trade data is coming at the end of this week and will give details for October against a backdrop of easing tensions on negotiations with U.S. counterparts.

In geopolitical news, the head of Iran’s Energy Authority says operation of 30 new centrifuges is underway, adding “We didn’t intend to take these steps, but Washington’s wrong policies pushed us to do so”, reported via Al Jazeera. Elsewhere, North Korea and US working level talks could be held in mid-November/December, Yonhap citing South Korea’s spy agency. Over in China, reports via China People’s Daily noted that government employees’ careers are at stake as it flagged intervention in senior appointments. Finally, Turkey was said to be evaluating a Russian offer for fighter jets and the second delivery of Russian S-400 missile system is planned for 2020 but could be delayed due to technology sharing and production talks according to the Head of Turkish Defense Industry Directorate.

In rates, Treasury yields jumped 4bps to 1.75% while the curve bear steepened, as long end Treasuries underperform having been closed during Asian hours.

In FX, most G-10 currencies weakened against the dollar, with the biggest losses seen in the haven Swiss franc, the pound and the Japanese yen. The New Zealand and Australian dollars rallied after U.S. Commerce Secretary Wilbur Ross said he was optimistic an initial trade deal would be signed with China this month, with the kiwi reaching its strongest level since mid-August against the greenback. The pound edged lower after polls over the weekend indicated the Conservative Party’s lead ahead of the December election may be narrowing; sterling dropped on Monday after last week’s 0.9% rally. In EMs, South Africa’s rand surged after the country clung on to its investment-grade credit rating. Treasuries fell along with most sovereign bonds in Europe. The dollar edged higher versus its biggest peers, reversing a five-session decline.

In commodities, crude-oil futures ticked higher. The IPO process for Saudi Aramco officially started on Sunday, with the stock likely to start trading in Riyadh next month. Valuations vary widely.

Expected data include durable-goods orders and factory orders. Ferrari, Sprint, Sysco, Uber, and Marriott are among companies reporting earnings

Market Snapshot

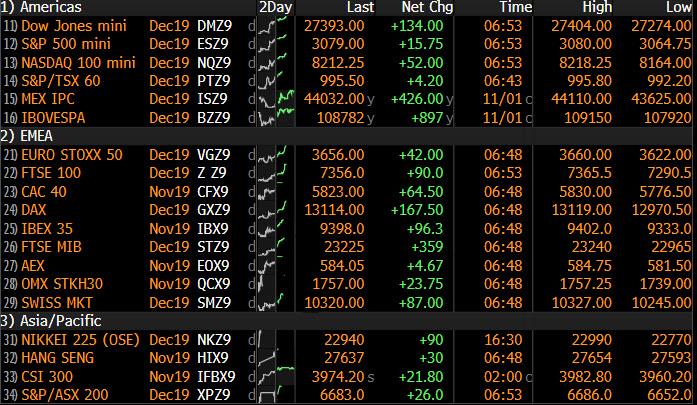

S&P 500 futures up 0.4% to 3,075.75

STOXX Europe 600 up 0.6% to 401.99

MXAP up 0.7% to 164.73

MXAPJ up 1.2% to 531.09

Nikkei down 0.3% to 22,850.77

Topix down 0.03% to 1,666.50

Hang Seng Index up 1.7% to 27,547.30

Shanghai Composite up 0.6% to 2,975.49

Sensex up 0.4% to 40,336.29

Australia S&P/ASX 200 up 0.3% to 6,686.87

Kospi up 1.4% to 2,130.24

German 10Y yield rose 1.8 bps to -0.364%

Euro down 0.04% to $1.1162

Italian 10Y yield rose 6.9 bps to 0.651%

Spanish 10Y yield rose 2.0 bps to 0.294%

Brent futures down 0.9% to $62.24/bbl

Gold spot down 0.3% to $1,509.5

U.S. Dollar Index little changed at 97.30

Top Overnight News from Bloomberg

U.S.’s Ross met with Chinese Premier Li Keqiang at a regional summit in Bangkok, a person familiar with the discussion said. The meeting came hours after Ross told a morning business forum that the U.S. was “very far along” with “Phase One” of a trade deal with China

Brexit Party leader Nigel Farage won’t stand as a candidate in the U.K. election, and will focus instead on campaigning across the country, as his party fields 600 candidates. His refusal to back British Prime Minister Boris Johnson has prompted criticism from other Brexit supporters, who say the strategy could split the anti-EU vote and help Labour leader Jeremy Corbyn win

Eurozone October manufacturing PMI came in at 45.9 versus the flash reading of 45.7, while a similar reading for Germany was 42.1 against the flash reading of 41.9. Above the 50 mark indicates expansion, while below that level points to a contraction

China’s private companies have been hit disproportionately hard as the economy slows, with their default rate doubling to 12% this year, compared with 1.5% for the overall domestic bond market, according to China International Capital Corp.

Saudi Arabia is pulling out all the stops to ensure the success of Aramco’s initial public offering after Crown Prince Mohammed bin Salman finally decided to offer shares in the world’s largest oil producer

McDonald’s Corp. fired Chief Executive Officer Steve Easterbrook because he had a consensual relationship with an employee, losing the strategist who revived sales with all-day breakfast and led the company’s charge into delivery and online ordering

Asian equity markets kick-started the week on the front-foot as the region took impetus from the record highs on Wall St. last Friday following a better than expected Non-Farm Payrolls report and constructive call between top US-China trade negotiators in which progress was said to be made in a variety of areas. ASX 200 (+0.3%) was lifted by outperformance in the mining related stocks due to the trade optimism and after the recent rally in oil prices, but with gains in the index limited by weakness in the largest weighted financials sector after Big 4 bank Westpac reported a decline in its FY profit. Hang Seng (+1.7%) and Shanghai Comp. (+0.6%) were also positive with the trade optimism turned up a notch after the recent top-level call, with even White House Trade Adviser and China-hawk Navarro noting the sides had good discussions and US President Trump also floated Iowa as a location for the signing of a phase 1 deal. Furthermore, strength in oil names contributed to the outperformance in Hong Kong, and Japanese markets remained closed today for Culture Day.

Top Asian News

Philippine Central Bank Chief Says 2019 Policy Easing Over

Following on from Friday’s post NFP/encouraging trade rhetoric rally, major European bourses (Euro Stoxx 50 +0.9%) are again on the front foot, with further trade optimism the major tailwind. US Commerce Secretary Ross, over the weekend signalled optimistic China developments whilst noting that US may not need to impose auto tariffs later this month on the EU, Japan and South Korea, following positive conversations with these countries. DAX and Euro Stoxx indices are at fresh YTD highs, with the latter at its highest levels since early 2018. As expected, European auto names, including Fiat Chrysler (+4.0%), Peugeot (+4.9%), Daimler (+2.2%) and Volkswagen (+2.5%) are driving gains amid Ross’ comments. More broadly, sector performance is reflective of the market’s risk-on sentiment; Materials (+1.6%), Consumer Discretionary (+1.2%), Tech (+1.1%), Energy (+1.7%) and Financials (+1.6%) are all on the performing well, with the latter two aided by higher yields and crude prices from Friday’s late-doors rally. Meanwhile, the more defensive Utilities (+0.1%), Consumer Staples (Unch.) and Health Care (+0.5%) sectors are laggards. In terms of specific movers; strong earnings from Ryanair (+6.6%), Siemens Healthineers (+7.0%) and Telefonica Deutschland (+1.6%) has seen their respective stock prices advance. Wirecard (+3.7%) trades higher with the prospect of EUR 200mln in additional share buybacks providing some reprieve from the recent FT-induced declines. Finally, UK gambling stocks fell sharply (William Hill -6.9%, GVC -10%) amid pre-market reports via The Guardian that UK MPs are demanding an overhaul of gambling laws which would see online casinos subject to the a maximum stakes limit similar to the GBP 2 imposed on fixed-odds betting terminals.

Top European News

U.K. Construction Contracts for Sixth Month Amid Weak Demand

Ryanair Says European Regulator Holding Up Return of Boeing Max

European Autos Surge to Six-Month High on Trade Deal Optimism

Takeaway.com Proposes Just Eat Merger Via Recommended Offer

In FX, the Kiwi is head and shoulders above its G10 counterparts in wake of news that NZ and China will enhance their FTA, with Nzd/Usd extending gains through 0.6450 at one stage even though the latest NZ Treasury report paints a rather bleak picture of the domestic economy as Q2 GDP was weaker than expected and business activity remained depressed during the 3 months to September. However, cross-currents also favoured the Kiwi as Aud/Nzd retreated through 1.0750 and the Aussie lost traction vs its US rival on the 0.6900 handle following disappointing retail sales data on the eve of the RBA’s policy meeting – full preview available via the Research Suite. Elsewhere, the Rand is breathing a big sigh of relief after Moody’s SA ratings review on Friday as the agency resisted any temptation to go beyond the widely anticipated outlook downgrade to negative. Usd/Zar has reversed further from recent highs in response and back below the psychological 15.0000 level to test bids/support at 14.7500.

CHF/JPY – The safe-havens have receded in line with risk-on sentiment prompted by the hefty US payroll beats and rising global trade optimism amidst latest positive updates on US-China Phase 1 alongside talks between the US, EU, Japan and South Korea that could culminate in auto tariffs being rolled over or even removed altogether. The Franc is also digesting even more dovish remarks than normal from SNB chief Jordan and latest weekly Swiss sight deposits showing a hefty rise in domestic bank accounts, as Usd/Chf hovers above 0.9875 and Eur/Chf over 1.1025, while the Yen and crosses are also elevated, with Usd/Jpy eyeing 108.50.

CAD/GBP/EUR – All softer vs the Greenback as the DXY holds above 97.000 and Friday’s 97.107 post-NFP low, as the Loonie continues to reflect on the BoC’s rather concerned outlook and pivots 1.3150, while Cable strives to keep its head above 1.2900 ahead of the UK election and the Pound lags against a relatively resilient Euro after some signs of stabilisation in the core and pan Eurozone manufacturing PMIs. Note also, Sentix sentiment improved substantially and Eur/Usd may be benefiting from expiry hedging given 1 bn running off between 1.1155-60.

EM – Choppy trade in Usd/Try within 5.7075-6800 parameters after another slowdown in Turkish CPI and reports that the second batch of S-400 missiles from Russia may be delayed, with the Lira testing 200 DMA resistance, but not quite breaching the technical marker.

In commodities, crude markets are firmer on the first trading session of the week following overnight consolidation from Friday’s late-door gains, with impetus derived from the overall risk sentiment and in wake of of comments from the Iranian Oil Minister Zanganeh who expects further cuts to be agreed at the 5th/6th December OPEC meeting (in-fitting with some of the recent sources reports ahead of the meeting, although the magnitude of the touted cuts is unknown). WTI Dec’ 19 futures have moved above last Friday’s USD 56.43/bbl high, as has Brent Jan’ 20 futures, which also eclipsed the USD 62.00/bbl level. Elsewhere, COT data released last Friday showed that speculators increased their net long in ICE Brent by 45.6k lots over the last reporting week, leaving them with a net long of 253,999 lots as of last Tuesday. “This is the largest weekly increase since early September, and also takes the net spec position back to levels seen in September” notes ING, who point out that “the increase was predominantly driven by fresh longs, rather than shorts coming in to cover.” Turning to metals; gold prices are subdued, despite the risk on moves being seen across equities and bonds. Copper meanwhile is similarly uneventful – CFTC data from last Friday revealed that speculators have increased gross longs by 11,514 lots over the week, and covered 11,949 shorts, amid recent gains in the markets risk tone.

Saudi Arabia have confirmed that Saudi Aramco is to be publicly floated, currently no indication on the timing, price or magnitude of the IPO. Reports note scepticism that Aramco will achieve its USD 2trl valuation, likely to be closer to USD 1.5trl. Stake offered could be between 1-3% valued at USD 15-60bln.

US Event Calendar

10am: Durable Goods Orders, est. -1.1%, prior -1.1%

10am: Durables Ex Transportation, est. -0.3%, prior -0.3%

10am: Factory Orders, est. -0.4%, prior -0.1%

10am: Cap Goods Orders Nondef Ex Air, prior -0.5%

10am: Factory Orders Ex Trans, prior 0.0%

10am: Cap Goods Ship Nondef Ex Air, prior -0.7%

DB’s Jim Reid concludes the overnight wrap

Happy Monday to you all. In all the time I’ve been writing the EMR, the story I get asked about the most is the time I discussed how I had a whole bank of freshly planted trees stolen from outside my old house. This was around 7 years ago. I even replanted some, got stakes inserted through the roots to secure them deep into the ground and they attempted to steal those too. I was incandescent with rage. Well this weekend we’ve tempted fate and planted new ones at the boundary of our new house. So, if anyone reading this from anywhere around the world suddenly gets offered some cheap trees please don’t be tempted as they’re probably using my garden as their tree nursery.

Talking of trees, some green shoots of data recovery were seen towards the end of last week in the US.Indeed our economists have changed their US rate call this weekend for the second time since Wednesday’s Fed meeting. After the FOMC they marginally decided to keep a December cut in their forecasts but Friday’s impressive jobs report (more below) means that the Fed are unlikely to receive enough information prior to the December FOMC that leads to a “material reassessment” in the outlook that they have noted is needed to cut rates again. Therefore, unless they see negative surprises in key events – most notably auto tariffs and China negotiations they now see the Fed remaining on hold for the foreseeable future. They still see the risks to the downside, and the Fed having to cut again, but being on hold is now their central scenario. Interestingly on auto tariffs, US Commerce Secretary Wilbur Ross said yesterday on Bloomberg TV that the US has been having “good conversations” with automakers from the EU, Japan and Korea. He went onto say that he hoped the negotiations had so far will bear enough fruit that the 232 may not need to be put into full or even part effect. This will be seen as good news as the end of the 6-month delay on making a decision on EU auto tariffs ends this month. He also sounded optimistic on the “phase one” trade deal being signed this month and said licences for US companies to sell to Huawei will be coming “very shortly”.

The strong close on Wall Street on Friday and those comments from Ross seem to have helped Asian markets kick start the week on the front foot with the Hang Seng (+1.30%), Shanghai Comp (+0.76%) and Kospi (+1.30%) all up with markets in Japan closed for a holiday. Meanwhile, futures on the S&P 500 are up +0.23%. In FX the big mover is the South African rand (+1.28%) after Moody’s announced on Friday that it had decided not to downgrade the country’s credit score to junk, although it did reduce the outlook to negative.

Back to Friday’s data, the US economy added 128,000 jobs in October, plus another 95,000 of positive revisions to previous months. Consensus was at 85k. Given the GM strikes and revisions these were seen as healthy numbers. For many this meant the subsequent ISM was less of an issue. This proved to be the case but we should note that it came in slightly below expectations at 48.3 (48.9 expected – 47.8 last month) marking the third month below 50. The good news in the report was the surge in new export orders from a shockingly low 41.0 last month to a 4-month high of 50.4. All eyes on the services component tomorrow (53.4 expected from 52.6 last month).

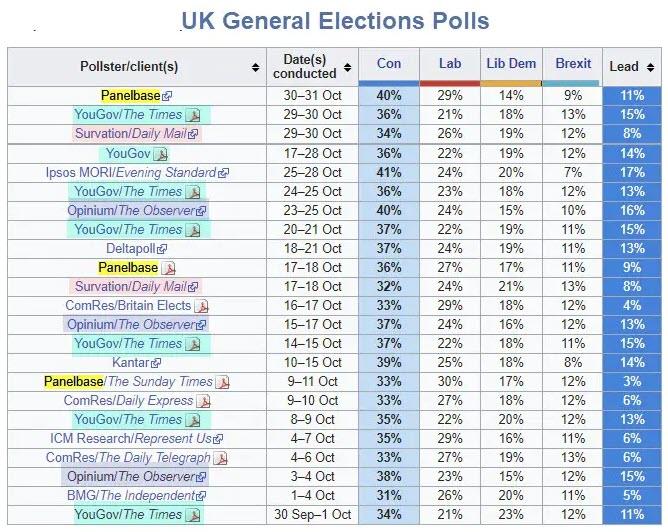

The week post payroll is usually quiet for data. This week is slightly different as given payrolls was released on the 1st (Friday), and that Europe had a part holiday on the same day, we have the rare situation where European manufacturing PMIs (today) and European (Wednesday) /US non-manufacturing PMIs/ISM (Tuesday) are released after payrolls. There’s a raft of Fedspeak due this week and the first speech from new ECB President Lagarde (today). Expect the UK election campaign to gain momentum. The polls (YouGov, Opinium, Orb) over the weekend showed some interesting developments as 1) the Conservatives ranged from an 8-16pc lead, 2) both the Conservatives and Labour are gaining support since the election was announced and 3) Labour seem to be gaining a little more of it from a low base but the Lib Dems and the Brexit Party and getting squeezed. The early signs are that this could be more of the traditional two party race than many thought.

Today’s European manufacturing PMIs will be a big focus and expectations for the Eurozone, Germany and France numbers are for no change to the flash at 45.7, 41.9 and 50.5, respectively. Spain and Italy’s are expected to dip 0.2 and 0.1 points respectively from last month to 47.5 and 47.7 respectively. So with stabilisation expected, any move either way will get markets excited. For Wednesday’s European final services PMIs, the Eurozone and German number is also expected to be unchanged from the flash at 51.8 and 48.6 respectively with the other main countries expected within a few tenths of last month’s readings in the 51-53 range. The Eurozone composite is expected to edge up 0.1 points to 50.2

In terms of other US data we have the final September durable and capital goods orders revisions today, Q3 non-farm productivity and unit labour costs on Wednesday and the preliminary November University of Michigan consumer sentiment survey on Friday. In Europe we’ve also got the September industrial production prints in Germany on Thursday and France on Friday, while the European Commission will also publish its latest economic forecasts on Thursday. Finally in China we’ll get the services and composite Caixin PMIs for October on tomorrow (another important release for global markets) and the October trade data on Friday.

As for policy meetings this week, the BoE meet on Thursday. No policy changes are expected. Our economists expect the BoE to sound dovish, dropping its tightening bias and instead moving towards an easing policy stance. They note that, domestically data have deteriorated sufficiently to warrant more supportive monetary policy. Growth has slowed and is tracking below the Bank’s “speed limit” of 1.5% with uncertainty likely weighing further on the near-term growth outlook. Equally, the UK supply side story is also turning softer, with labour market indicators pointing to downside risks for both pay and jobs by Q4-2019 and inflation now expected to remain below target in 2020. The team see an increasing risk of a rate cut at the January Inflation Report – Governor Carney’s final MPC meeting.

Staying with central banks, as discussed earlier it’s another busy week for Fedspeak. Indeed today we’ll hear from Daly, Tuesday will see Barkin, Kaplan and Kashkari speak, Wednesday will see Evans, Williams and Harker speak, Thursday will see Kaplan speak and on Friday we’ll hear from Bostic and Daly.

Meanwhile, earnings season starts to slow down with just 66 S&P 500 companies reporting. The highlights include Sysco and Berkshire Hathaway on Monday, CVS on Wednesday, and Walt Disney and Cardinal Health on Thursday. Away from the US we’ll also get results from Telefonica, Softbank, BMW, Toyota, Siemens, Allianz and Honda.

Reviewing last week now and it was another positive week for equities with data on balance more positive, trade talks seemingly going in the right direction, a U.K. election finally called and a Fed rate cut. The S&P 500 advanced +1.5% (+0.97% Friday and a new record high) with semiconductors leading gains, up +2.5% on the week. The Nasdaq gained +1.7% (+1.13% Friday and also to a new record). In Europe, the Stoxx 600 gained +0.4% (+0.68% Friday) though banks underperformed, down -2.6% but up +0.99% Friday. Yields fell, with 10-year yields on treasuries and bunds down -8 and -2 basis points respectively but up 2bps and 2.5bps on Friday. Friday not only had positive data but markets liked the comments from the Chinese Ministry of Commerce that they had achieved a “consensus in principle” on trade. Phone talks on Friday were also seen as “constructive” from both sides.

Ross Meets With Top Chinese Official As Mid-Level Trade Talks Spark More “Optimism”

Perhaps to help quash rumors that they’re not taking the trade talks seriously, the Chinese leadership (according to President Trump) recently offered Trump an important concession to help facilitate the trade talks: They allegedly agreed to hold the next round of high-level talks on American soil (perhaps Mar-a-Lago or even President Trump’s Doral golf club might be floated as locations).

But in the mean time, scattered talks, over the phone and in person, have continued. But in a sign that the president might be growing tired of his top trade negotiators and surrogates, Trump reportedly dispatched a “downgraded” delegation led by US Commerce Secretary Wilbur Ross and National Security Adviser Robert O’Brien to meet Chinese Premier Li Keqiang Monday afternoon at the 10-member Association of Southeast Asian Nations in Bangkok, according to a Bloomberg report. The meeting took place hours after Ross, who was sidelined early on during the trade talks reportedly because Trump felt he had mishandled early negotiations, tried his hand at jawboning and told a meeting of business leaders that the US was “very far along” with “Phase One” of the trade deal with China.

Then, in an interview with Bloomberg on Sunday, Ross “expressed optimism” about the prospects for talks with China this month before working on additional phases. He also said licenses would be coming “very shortly” for US firms to sell components to Huawei, an issue that has, so far, stuck in China’s craw.

To be sure, President Trump has been promising to issue waivers for Huawei, which wound up on a Commerce Department blacklist earlier this year prohibiting US firms from selling critical components.

Trump and Vice Premier Liu He insisted that “Phase 1” was pretty much finished, Ross offered a more “nuanced” take…insisting that the continuing talks on “Phase 1” are merely Washington doing its due diligence, and nothing more (he also seems to have left out “Florida” from the list of possible locations for the next round of top-level talks).

Ross called the Phase One agreement “particularly complicated” and said the US was “making sure that each side has a very correct and clear, detailed understanding of what each side has agreed to.” Iowa, Alaska, Hawaii and locations in China were all possible places for Trump and President Xi Jinping to sign the deal after the cancellation of this month’s Asia-Pacific Economic Cooperation summit in Chile.

“We’re in good shape, we’re making good progress, and there’s no natural reason why it couldn’t be,” Ross said. “But whether it will slip a little bit, who knows. It’s always possible.”

During his appearance on Monday, Ross reportedly insisted that the White House remained “fully committed” to the Indo-Pacific region, as Trump’s absence and “America First” policies that recently inspired the pullout from Syria have seemingly shaken the faith of other US allies around the world.

But most importantly, at least as far as the fate of the talks is concerned, Ross reportedly remained “non-commital” about the possibility of the administration cancelling the next round of planned tariff hikes in December. Ross said it will depend on Chinese legislation and an enforcement mechanism.

Trump agreed to cancel a round of tariffs set for October just days before they were set to take effect last month. The bigger test this time around will be whether the US can get the ‘partial’ trade deal that Trump once loathed down on paper before mid-December.

Meanwhile, the US-China deal wasn’t the only trade deal being discussed in Bangkok…

Asian leaders were separately expected to announce a breakthrough on another trade pact, the China-backed Regional Comprehensive Economic Partnership, at the end of the meetings. It remained uncertain whether the pact would include India, which jeopardized it with last-minute requests.

Ross in the interview downplayed the significance of RCEP, which would lower tariffs in an area that represents roughly a third of the global economy, and defended U.S. engagement in Asia after Trump skipped the Asean meetings for a second straight year.

Contentious issues remain and the terms aren’t yet known, but RCEP would at least partly fill a trade gap left by Trump’s 2017 withdrawal from the Trans-Pacific Partnership. Southeast Asia collectively has the world’s fifth largest economy and has struggled to wade through the economic fallout of U.S.-China trade tensions.

The message is clear: Beijing isn’t waiting around for Washington to make up its mind.

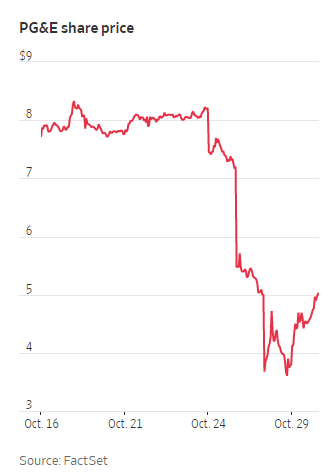

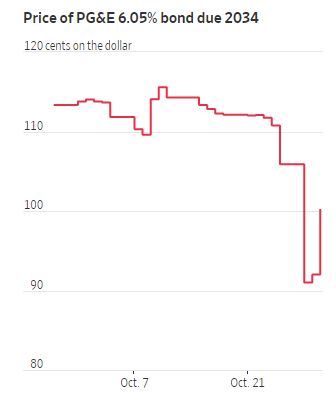

Hedge Funds Invested In PG&E Lose $4.1 Billion In Just Four Trading Days

California isn’t the only thing that’s burning: hedge funds invested in PG&E are slowly watching their cash go up in smoke.

Investors in the company lost roughly $4.1 billion in the four days after the current blaze in Sonoma County broke out on October 23, according to the Wall Street Journal. Shares rebounded late last week, but are still about 85% lower than their 52 week highs, poking around the mid single digits while hedge funds and equity investors try to analyze numerous bankruptcy outcomes that the company might face.

The company’s market cap has been cut to about $3.4 billion from highs of $37 billion in 2017. Bond prices have fallen as much as 12.5%, which is the biggest decline since it was determined that PG&E equipment set off the campfire in Northern California last November.

The volatility has made it difficult for hedge funds to profit from what is being called the “first major bankruptcy induced by climate change”.

Stephen Byrd, head of utilities research at Morgan Stanley said: “Climate change has had a big impact on investing in California utilities, and the risk of fires is here to stay.”

Among the funds that have invested in PG&E equity or bonds are Abrams Capital Management LP, Baupost Group LLC, Elliott Management Corp. and Värde Partners.

The sell off last week was helped along by the Kincade Fire’s quick spread through the state. An increasing number of wildfire claims against PG&E could easily wipe out the company’s equity and take the company’s junior bondholders with it.

Andrew DeVries, a bond analyst at the research firm CreditSights said: “The number one question for investors is are they on the hook for the Kincade Fire and, if so, how much will that cost. The answer is nobody knows.”

And the uncertainty is putting pressure on negotiations between PG&E’s investors, insurers and existing wildfire victims – pressure that could prevent the company’s plans for exiting bankruptcy.

Bondholders have already pledged billions to the company to pay out wildfire claims, but made the deal contingent upon a provision that the damage from the current fires doesn’t exceed 500 buildings. The Kincade Fire has already damaged 246 structures, as of mid-last week.

An increase in claims could jeopardize the profitable plan of buying up insurers’ claims against PG&E at a discount, a plan that Baupost and other investors are betting on.

PG&E has said that one of its power lines malfunctioned shortly before the Kincade Fire, but the exact cause and any liability associated with it are still unknown. The Kincade Fire started despite PG&E plunging the state into darkness with precautionary “safety” blackouts, which we have reported on extensively here on Zero Hedge.

Since the Kincade Fire started, about $4.4 billion worth of the company’s bonds have traded hands. 296 million common shares have also changed hands. Holders of the bonds are on the hook for paper losses of about $1.4 billion as of the end of last week. Equity holders have taken aggregate losses of about $1.1 billion in the same time period.

Bonds with the highest annual interest payments are experiencing the most pressure. Hedge funds like Elliot had bought into these bonds in hopes that they could recover as much as 130 cents on the dollar after accounting for past-due interest. These bonds fell as much as 18% to prices as low as 90 cents on the dollar after the Kincade Fire started.

Davidson Kempner Capital Management, a fund that held $767 million of bonds, sold out of the position on Monday. Other fund managers hedged against their bond positions by shorting the company’s equity, one trader said.

Steadfast Capital Management LP said on Wednesday that it lost 1.47% from its investment in PG&E stock in the third quarter, calling it a “terrible decision”.

“This is a powerful example of high-degree-of-difficulty investing and one that, in hindsight, we should have avoided,” the fund said in its letter.

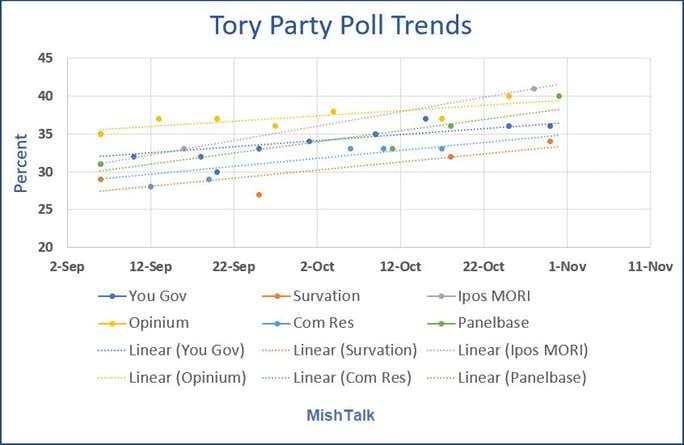

The range of the most recent Tory polls is 34-41%.

All six of the pollsters have the Tory party gradually and consistently gaining strength.

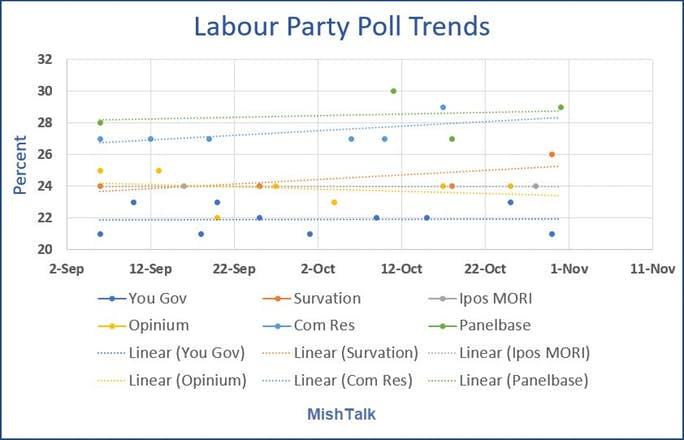

Labour Party Poll Trends

The range the six most recent Labour polls is 21-29%.

Four of six polling organizations suggest support for Labour is stagnant. The other two say support for Labour is rising, but not as steeply as support for the Tories.

ComRes shows a rising trend for Labour, but it from October 10 and is thus very stale.

One bad print from ComRes will have 5 of 6 stagnant trends for Labour.

Clustering

The six most recent polls for Labour average 24.17%

The six most recent polls for Tories average 37.17%

That’s an average lead of 13%, easily enough for a Tory landslide.

“Our regular month-end poll of polls shows an average Conservative lead of seven per cent over Labour. This is just enough for a small majority in the House of Commons, which is the headline prediction above.”

Electoral Calculus October 30

“Prediction based on opinion polls from 01 Oct 2019 to 25 Oct 2019“

That is a stunning victory for Johnson even without a Brexit Party alliance.

National Polls

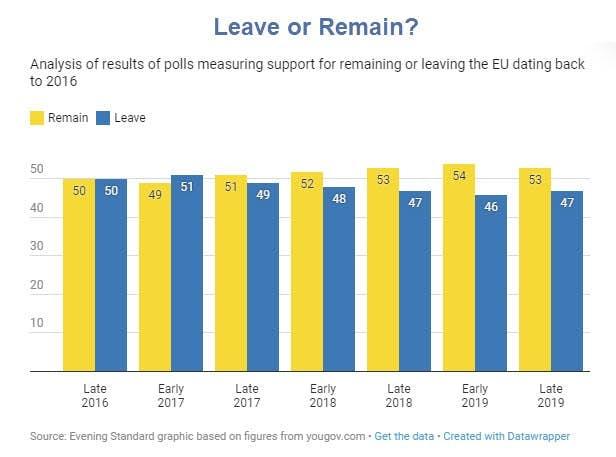

It’s important to not overemphasize support for Remain.

This is not a national election.

London would overwhelmingly vote Remain, but London business leaders certainly do not want Corbyn.

National polls don’t count in a first-past-the-post regional voting system. This is what Hillary Clinton found out in spades.

These Brexit trends can change at any time, but there is no particular reason to believe they will.

Like it or not, voters are getting more comfortable with Johnson, and Johnson has business on his side.

Pentagon Expands Permanent Africa Presence With $110M Drone Base In Niger

Signaling what will be a major uptick in US drone activity across western Africa, US African Command (AFRICOM) announced Friday its airbase Agadez, Niger has gone operational, not just flying surveillance drones as was originally expected, but also armed combat drones.

Flights from the base, called Air Base 201, began last week and the patrols are to aid US-Nigerien military patrols in rooting out regional ISIS militants and other Islamist factions which have been threatening the area. Specifically US officials say the armed drone program is badly needed due to prior ISIS ambushes on US-Nigerien troops.

File image of French drone in Niamey, Niger via AFP/Getty

The move comes a little more than two years after four Army soldiers were killed on Oct. 4, 2017, in an attack on a joint U.S.-Nigerien military patrol by an ISIS offshoot known as Islamic State in the Greater Sahara.

The US Air Force, which has described the $110 million constructed airfield as among the harshest locations in the world from which the military operates, endured multiple delays in establishing the base given the difficult remote desert environment.

“I would say that the construction of Air Base 201 will go down as one of the most Herculean efforts in the history of the United States Air Force,” Brig. Gen. Michael Rawls of the Air Force’s 435th Air Expeditionary Wing in Africa described earlier this year.

U.S. and Niger flags raised side by side at the base camp for construction of Niger Air Base 201 in Agadez, Niger. Via AP/Air Force Times

The new airfield can reportedly allow surveillance and reconnaissance across the extensive Lake Chad Basin area, which includes Chad, Cameroon, Nigeria and Niger.

This will no doubt further commit the Pentagon to a long-term presence in Niger amid continued broader AFRICOM expansion.

Nigel Farage has thrown down the gauntlet to Boris Johnson over the election strategy. Johnson has refused.

Of course he did. Farage made an offer Johnson couldn’t accept, ditch the Withdrawal Treaty he just negotiated with the EU and truly campaign on a far harder Brexit than Johnson has ever advocated for.

If he doesn’t do that about-face, Farage’s Brexit Party standing candidates in more than 500 seats and potentially split the Leave vote.

Mike Shedlock thinks Farage’s deal is “Preposterous.” Mike is wrong. It is the only offer Farage could offer the Tories and stay in any way relevant in a time of electoral chaos and party fluidity.

It is the kind of ‘big ask’ that his friend Donald Trump would make. It may be an opening bid in a complex negotiation that ends with them making a pact towards the end of the campaign.

Frankly that only happens if the polls shift considerably from where they are.

Politics is not a game for the timid or the weak. If Farage is to be a big player in British politics he needs to act like he is a big player in British politics.

And that means sticking to his core message, a real Brexit where the U.K. regains sovereignty over itself in a timely manner. 2022 is not timely for the U.K.

It is, however, timely for the EU, given the realities of its continent-wide political uprisings against its rule.

Farage has positioned the Brexit Party on a “Change Politics for Good” platform that proposes sweeping changes to the system from proportional representation to a written constitution and reforming the House of Lords.

This is, as Monty Python would say, something completely different.

The statement itself cuts to what’s fundamentally wrong. It’s aspirational and tells the voters they still have the real power after three years of parliamentary shenanigans designed to marginalize them while being insufferably condescending.

We’ll find out in the next couple of weeks as to whether Farage et.al. can make the case to British voters that these changes go hand in hand with Brexit. Are these people not only tired of the endless Brexit wrangling but now truly awake to the depth of the betrayal of their political representatives?

If they are then Boris Johnson will have a real problem come December 12th.

Because that is a platform, beyond Brexit, that cuts across all party lines.

The Tories are rallying around their common message now that they have an election. There are serious misgivings within in the party on Johnson’s deal and the strategy. But fear of losing Brexit has motivated the strongest Brexiteers to cave to what Mike rightly points out has been the political reality.

But that was before the election was secured.

Hard core Leavers like Marc Francois and Steven Baker, prominent members of the ERG — European Research Group — are on board with the deal and have called out Farage as lying about it.

But, arguing that these guys being on board with Boris’ treaty means it’s a good deal is simply appeal to authority while missing the much larger point.

The Tories are the main mechanism by which the British Deep State and political elite maintain control over not only British policy, but also that of the U.S. and much of Europe. Don’t for a second think that these ERG guys are any less compromised in the end than the outright Remainers like Ken Clarke, Dominik Grieve or Philip Hammond.

They will always put party before country in the end. Most of them proved it during Theresa May’s multiple rounds of blackmail last spring by eventually voting for that deal because, ultimately, they are spineless.

Fear of losing Brexit is what motivates them. Fear of Farage upsetting the apple cart in Westminster is also very real.

Farage may be overstating the threats within the political declaration to the U.K.’s bargaining position during Free Trade Agreement talks, but he also knows the EU side of the ledger far better than any of the newly-promoted back-benchers in the ERG.

So, if I’m going to resort to appealing to an authority on the subject I’m going with the guy who put the world in this situation in the first place, Nigel Farage.

That said, however, Farage’s strategy is a risky one. There’s no doubt about that. With the most recently published polls putting Johnson at his peak of popularity and the Brexit Party languishing around 10% Farage has a lot of ground to gain in six weeks.

There are real worries that Farage’s support in the Labour heartland of the Midlands and the Northeast isn’t as strong as he thinks it is. But, given how fundamentally split the Remain vote is between the Liberal Democrats and Labour, I don’t see how Farage hurts Johnson unless Farage’s numbers rise.

And Johnson will absolutely try to duck any head-to-head meetings between them just like Theresa May did.

But you don’t change things by being timid. Farage doesn’t win loyalty by going up to Boris Johnson, bowl in hand, and asking for another ladle of gruel. You act like the big dog and you challenge the alpha who, to this point, doesn’t even know what he signed the U.K. up for.

I maintain that Johnson is a fake Leaver and none of his behavior has contravened that, including duping the ERG into backing a now unnecessary Withdrawal Treaty which served its purpose to get a general election to get rid of a rotten Parliament.

Johnson and the ERG know this, and yet, they will persist in putting party first, betraying Northern Ireland, keeping the U.K. as close to the failing EU as possible and all the while calling it Brexit.

Given those circumstances would you expect Nigel Farage to offer Boris Johnson anything more?

* * *

Join my Patreon if you want to get exclusive commentary on these matters as well as the Gold Goats ‘n Guns Monthly Newsletter. Install the Brave Browser if you want to regain some of your privacy and support all the creators Google thinks you shouldn’t.

It has been widely, vividly, but nonetheless wrongly believed that socialism is the appropriate system to improve the living standards of Africans. Worse yet, it has been misleadingly claimed that socialism is compatible with African culture because African culture is fundamentally a collectivist culture.

However, one fact remains undisputable: socialism has failed wherever it was tried, and the African countries that have experimented with socialism were not exempted from its failure.

The undeniable fact remains that Africa has the lowest living standard of all continents after Antarctica. The reason why the living standard of the majority of African countries is so low compared to the rest of the world, is because socialism has impoverished the African continent.

At the outset of the post-colonial era in the 1960s many African countries — such as Tanzania, Angola, Mali, Ethiopia, Ghana, Mozambique, Egypt, Senegal, Guinea, Congo and many more — have embraced socialism as their economic and political system. These countries that have embraced socialism became significantly worse off by the 1980s. For example, Tanzania was one of the fast-growing economies in East Africa until Julius Nyerere implemented the “Ujamaa,” which means socialism and brotherhood in the Swahili language. Before the implementation of the Ujamaa; Tanzania had a GDP similar to South Korea . Subsequently to the implementation of Ujamaa, economic growth became unsurprisingly stagnant. The policy of collectivization impoverished the Tanzanian people. Food production fell, and the country’s economy suffered . This decline in productivity has made Tanzania one of the poorest countries on the continent. In Ghana, under the rule of Kwame Nkrumah, one of the foremost African political leaders of the post-colonial era; socialism was also implemented as the economic system of the country.

But the question remains as to why Africans deeply believed in socialism and embraced it in the 1960s. In Africa, socialism was presented as an anti-colonial and anti-imperialist ideology while capitalism was perceived as the ideology of the oppressor, the colonizer, and of profit. Africans strongly believe in socialism because they think that socialism is compatible with African culture since African culture is a collectivist culture. African culture values the group over the individual. It values the concept of sharing, solidarity, and altruism. Of course, all these moral virtues are well-intended, but they play no substantial role in the improvement of the living standard of people. What improves the living standard of people is the ability to retain private property, to voluntarily exchange with one another what we own in order to create capital. Some African countries in the post-colonial era resisted the socialist temptation; notably countries like Côte d’Ivoire, Kenya, and South Africa.

For example, in the 1960s and 1970s, Côte d’Ivoire was the most economically advanced country in West Africa. While its neighbors were embracing socialism, Côte d’Ivoire opted for a market economy. Despite having an authoritarian political regime, like all African countries during that time; the Ivorian people were, nonetheless, economically free. They had the freedom to create businesses, and to expand private property. From 1960 to 1979, the GDP in Côte d’Ivoire grew at 8.1 percent per year, which means that in real terms capita, it increased from $595 to $1,114. Cote d’Ivoire’s economic expansion during that period was called “The Ivorian Miracle” because the country was exporting agricultural goods to the neighboring countries have had a shortage of food production due to their socialistic policies.

The Ivorian Miracle made Côte d’Ivoire the most prosperous nation in West Africa between 1960 and 1980.

What Africans have failed to grasp about capitalism and the free market is that, it is not a system intrinsic to Western culture. It is a system intrinsic to human nature regardless of race, ethnicity, or the local culture. Socialism has failed in Africa as it has failed in Eastern Europe, India, China and in South America. Even if Africa is culturally collectivist, it is important to comprehend that a group is a collectivity of individuals whereby each individual within the group is stimulated by the pursuit of his own interests. The pursuit of one’s self-interests is an intrinsic factor of human nature that no central authority can change regardless of the goal of the common good.

Despite the collectivist nature of African culture, African culture is not exempted from that natural law of human nature. Coercing human nature to do something that is not in harmony with the nature of human understanding, will result in failure. That is why socialism, wherever it is tried, will always fail.

{kind=link}

{kind=link}

{kind=link}

{kind=link}