The United States Internal Revenue Service (IRS) has added a question on crypto ownership to the standard 1040 income tax form for the coming tax season.

On Oct. 11, a draft of the “Additional Income and Adjustments to Income” section of the new 1040 form surfaced that included a change was made to the ‘Additional Income and Adjustments to Income’ section. On the new 1040 form, the additional question reads:

“At any time during 2019, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency?”

The question expects a straightforward yes or no, with no additional details requested.

Cointelegraph previously reported that the IRS had issued new guidelines for tax reporting on cryptocurrency airdrops and hard forks. The tax agency’s guidance answered questions about cryptocurrency transmissions for investors that hold cryptocurrencies as a capital asset and set general principles of tax law to determine that virtual currency is property for federal tax purposes.

H&R Block helps with crypto taxes

Cointelegraph reported in September that United States-based accounting firm H&R Block started acting as an intermediary between crypto users and the IRS after the agency began sending letters to crypto traders who may have failed to report income and pay taxes.

H&R Block can now assist people who have engaged in digital currency transactions, specifically providing consultations on how to properly file their cryptocurrency gains and losses on tax returns.

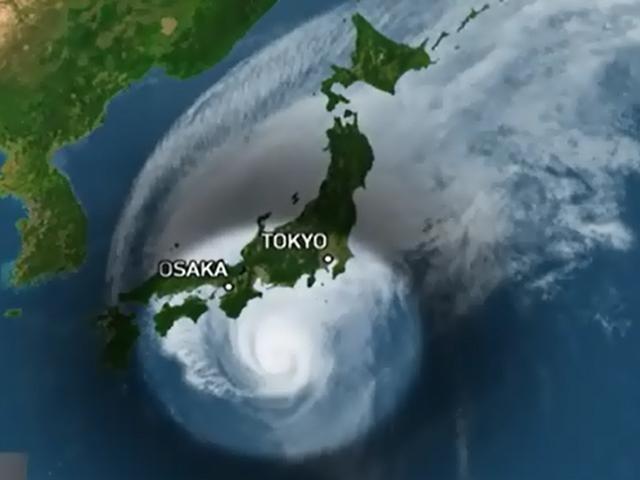

Historic Typhoon Devastates Japan; Millions Told To Evacuate Amid Flooding, Widespread Outages

The largest typhoon in recorded history of Japan’s Shizuoka Prefecture caused widespread flooding, power outages and destruction on Saturday, as local authorities warned over 7 million people to evacuate, according to Bloomberg(with other sources quoting figures ranging from 1-4 million).

Damaged houses in Ichihara, Chiba, on Oct. 12. Source: Jiji Press/AFP via Getty Images

The sky turned brilliant purple right before Hagibis hit.

It might look lovely however this is a BIG calamity, Japan’s skies turn profound shade of purple as Typhoon Hagibis is coming. #PRAYFORJAPANpic.twitter.com/XxkgDOoF9B

According to the Japan Times, Typhoon Hagibis was downgraded to “strong” just prior to landfall, however “as of 8 p.m., it was still packing sustained winds of 144 kph and gusts of 198 kph. The storm is forecast to travel over Kanto region and then north into Tohoku region before moving into the Pacific.”

“A typhoon of an unprecedented scale is about to hit Kanto. I’d like you to take actions to protect your own life,” said Tokyo Gov. Kuriko Koike in an emergency news conference.

Dozens of rivers in the Tokyo region saw waters rise to dangerous levels on Saturday, while upstream dams are set to release water due to the heavy rains according to NHK. One of the largest rivers in the region, the Tama, has already begun to overflow into the residential district of Setagaya, per the land ministry.

Pray for Japan, for their safety… 🙏

Typhoon Hagibis is currently one of the strongest typhoons recorded to date.

“If we leave this situation unattended, the dam would collapse and more than 60 million tons of water would be unleashed at once,” said Kanagawa Gov. Yuji Kuroiwa while announcing that the Shiroyama Dam in Sagamihara was scheduled to release water at 10 p.m.

More than 100 rivers were at risk of overflowing, including the Arakawa River in Tokyo’s Edogawa Ward, the Karasawa River in Saitama Prefecture and Koito River in Chiba Prefecture.

The Tama River running between Tokyo and Kanagawa Prefecture began to overflow into the Tamagawa area of Tokyo’s Setagaya Ward at around 10:30 p.m. The area is better known as Futako-Tamagawa.

The Chikuma River flooded in the city of Ueda and the city of Nagano, both in Nagano Prefecture, as did the Minami-Asakawa River in Hachioji and the Nariki River in Ome, both in Tokyo. –Japan Times

Emergency warnings are in effect for: Kanagawa, Saitama, Gunma, Ibaraki, Tochigi, Nagano, Niigata, Fukushima and Miyagi prefectures.

Meanwhile, a 5.7 earthquake also struck Japan on Saturday.

On top of dealing with Typhoon #Hagibis, just felt an earthquake in #Chiba. The building was swaying. Local media is reporting a 5.7 magnitude quake struck near the region.

J.P. Morgan has taken to issuing warnings over the mental state and overall health of the American consumer’s habits. As a nation, we are deeply indebted to consumerism and that’s what is currently keeping the fragile economy afloat.

With the manufacturing industry already officially in a recession, the Institute of Supply Management purchasing manager index was registering a reading of 47.8 (anything over 50 indicated growth) for September, the worst reading since 2009 the news seems bleak even for the consumerism that’s fueling this debt-based economy. The U.S. and the Chinese trade war is also degrading business confidence, causing management teams to pull back on spending. That leaves consumers to carry the economic water – and many are tapped out; no longer able to take on any more debt in order to keep things afloat.

J.P. Morgan consumer-finance analyst Richard Shane sees this as bad news for the stocks he covers, according to Barron’s. On Tuesday morning, Shane cut his target prices on every single stock he covers—including names like American Express and Capital One Financial—by an average of almost 10%. What’s more, he downgraded shares of auto lender Ally Financial.

Shane is seeing some visible cracks in this “booming” economy and it’s time to be aware of them, “While the sector should continue to enjoy solid fundamentals through year-end, our outlook headed into 2020 becomes more cautious,” Shane wrote in a research report.

“Specifically, the prospects of a slowing economy, indications of pockets of labor weakness and heightened political uncertainty all may weigh on the group.”

Investors so far, appear to be aware of the risks in the markets going into 2020. Consumers, on the other hand, appear to have hardly noticed any of the red flags appearing right in front of them. After all, total household debt rose to $13.9 trillion in the second quarter, its 20th consecutive quarter of growth, according to Shane. Most consumer debt is housing-related, but borrowers also have $1.3 trillion in car loans. $0.8 trillion in credit-card debt, and $1.5 trillion in student debt.

Shane doesn’t see the bottom falling out of the economy. He doesn’t think it’s time to panic just yet because while consumer debt loads are at record highs, debt as a percentage of household wealth isn’t, he points out.

But the red flags are still there. Consumerism is being fueled by a strong job market. Should that go sightly the wrong way, things could get ugly, quickly.

Arrest Of 750 Child Protesters In Hong Kong Sparks Outrage

As with many movements, the ongoing pro-democracy protests in Hong Kong are dominated by younger, mostly student activists.

To that end, nearly a third of the 2,379 protesters arrested since June are under the age of 18. On Thursday, Hong Kong’s #2 official Matthew Cheung told reporters that it was “shocking and heartbreaking” that 750 of the arrests were of minors – with 104 being under the age of 16, according to The Guardian.

Notably, an 18-year-old high school student was shot in the chest by a Hong Kong policeman during an October 1 protest, while a 14-year-old was shot in the thigh by a plainclothes police officer last Friday after protesters came out to march against a ban on face masks. The Guardian also cites an 11-year-old who was sent to the hospital with an injury during a recent protest.

Cheung appealed to parents and teachers to admonish youngsters and tell them to refrain from “illegal or violent acts” and avoid getting injured or arrested, something that would “end up destroying [their] future”.

Last Friday, Hong Kong leader Carrie Lam announced that the country’s Emergency Regulations Ordinance had been invoked, allowing for the passage of legislation banning the use of face masks – virtually the only defense against facial recognition for fair-skinned individuals.

On Tuesday, Lam acknowledged that after the school term began in September, almost 40% of those arrested were under 18, while 10% of last Saturday’s arrests were under 15.

While Lam said she cared “deeply” for students, she insisted that they should not participate in violent attacks and the anti-mask ban was aimed at “helping parents, teachers and students recognise that they shouldn’t be engaged in these acts.”

Schools across Hong Kong required parents to sign a notice saying they understood masks should not be worn inside or outside school, despite the fact that the ban applies only to public protests or assemblies. The Secretary for Education, Kevin Yeung, told reporters on Friday that the Education Bureau has required schools to report the number of students who wear masks to school after the ban was announced but stressed it was not going after schools or students. –The Guardian

“When [young people] are on the streets fighting selflessly, they are called ‘criminals and rioters’,” said professor of political science at Hong Kong Baptist University, Kenneth Chan. “The gap between the young people and the officials is impossible to bridge now.”

“It is a total breakdown of trust between the government and young people. It can only get worse because Carrie Lam has nothing but harsh measures to suppress and intimidate the young people and their parents.”

They sure are trying their best. To do what? To goose markets higher. It’s been quite the spectacle all year, but this Friday sure took the cake. The entire week had been a giant jerk fest of sudden rips and dips as headline chasing algos were ripping through support and resistance levels unleashed like fat kids at the candy shop. But this Friday was something else, almost designed to have markets overdose on an insulin spike.

Ever more hyped up on an impending China deal, every meeting, and movement of negotiators caused market spikes, a Trump tweet about “warm feelings”, a $82.7B repo operation by the Fed to keep things tidy, a sudden out of the blue $60B/month Treasury buying operation announced by the Fed, multiple Fed speakers to boot, what a scene.

And really Fed? You are throwing this $60B a month announcement out on a Friday with the $DJIA already up 350 points? What are you thinking here? The Fed knows this kind of announcement juices up markets. The Fed sheepishly claims it’s not QE. Oh piss off already. Expanding the balance sheet by $60B a month is a massive intervention any way you cut it or slice it. How big? Do the math. $60B per month is a run rate of $720B a year. And while they claim they’ll stop it in Q2 next year who really believe anything they say? Did you believe QT was on autopilot last year? Lol. Fool me once.

You know what else is $720B a year or $60B a month? The ENTIRE US MILITARY BUDGET. The largest military budget on the planet. Millions under arms, submarines, aircraft carriers, nuclear arsenal, bombers, fighter jets, military bases across the globe, satellites, drones, laser guided missiles, you name it. All of it runs at $60B per month.

So lest everyone is blind to numbers these days as everything is so monstrous our eyes glaze over I trust this comparison highlights how massive the Fed’s announcement was on Friday. But not QE. Right. Believe it if you so choose.

And yet, despite 2 rate cuts, the liquidity and news spectacle on Friday, no new highs. Everything including the kitchen sink is being thrown at these markets. The hype is palatable. And here we are. One year after rate hikes and balance sheet unwind on autopilot we’re back into crisis management, because that’s what rate cuts and balance sheet expansion is.

The ECB has cut and relaunched QE, the Fed has cut twice and is now running a US military budget size balance sheet expansion program.

Take these actions and place them anywhere else in history (2000, 2007, any time) and this would be called an emergency intervention program.

Why is nobody calling it that now? Because all of our senses and perceptions have been dulled by the constant droning on of central bankers telling us that without their existence the stone age is coming back? Please.

Yes they are all afraid of the consequences of debt/credit monstrosity they have unleashed and their only choice to blow an even bigger bubble.

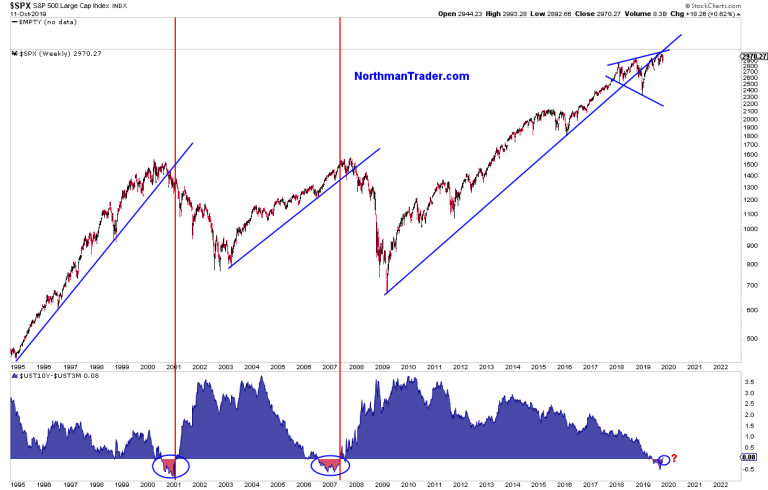

Whether they will succeed is another question. But know that all this frantic action to manipulate the liquidity and rate equation is in response to one chart, the chart that says we are at the beginning of the end.

First comes the yield curve inversion, then comes the steepening, and that’s exactly what happened this week:

Why are central bankers acting like there is a global crisis? Because they know exactly the history of this chart and hence they are trying everything in their power to avert the inevitable. And if that means they have to lie and not call it QE then that’s what they have to do.

They’re buying treasuries because the US government has an insatiable demand for debt. Spending keeps increasing, courtesy both GOP and Democrats, increased military spending, liability obligations, you name it, revenue is not large enough as growth is slowing, hence trillion dollar deficits are here and debt must be financed and when you have that much debt to sell you need buyers. And now the Fed is back in the game.

It’s all a big game.

Also a big game: That big China deal which is no big deal at all, it’s no deal. Nothing is in writing, nothing’s been signed, but let’s call it a great phase 1 partial whatever that means:

Let me translate “partial deal”:

We couldn’t agree to any of the big stuff and remain miles apart.

But let’s put some lipstick on the pig and call it a supermodel.

Let me tell you what it doesn’t mean: No company is suddenly going to increase their capex or business investments because in 5 weeks, maybe, something will get signed to buy more soybeans and pork as part of phase 1. They didn’t solve anything, it’s a face saving exercise and gives the Chinese time. Time for what? Time to see how the political situation unfolds in the US.

Impeachment? Here’s an out of field controversial and admittedly entirely speculative take on all this: Who’s says Trump is around for phase 2 or phase 3 as he called it yesterday? Everybody assumes he’ll survive impeachment and may well win the election next year. Who says he actually wants to? As radical as it sounds impeachment may be his best and most desirable option.

He sure is acting like he wants to get impeached, he’s practically daring not only Democrats but increasingly Republicans as well. Think about it. What if he really is trying to get impeached and nobody’s doing it for him? The logical path would be to do ever more outrageous things until they finally caved and impeached him. His sudden and unexpected move with the Kurds/Turkey caused big consternation with his Republican supporters who couldn’t quite fathom what he was doing. If he was trying to get impeached such a move would be consistent with such a move. Sounds too crazy? Consider this:

Why would Trump want to get impeached? It’s actually a win win for him. First off he would not have to risk losing at the ballot box next year. Despite all the claims to the contrary his poll numbers are dreadful, for someone not liking to lose a historical defeat in 2020 would not exactly be ego soothing. His entire narrative has been around fake news, fake polls, fake this and fake that. A defeat at the ballot box next year would be a historic repudiation of such a narrative.

If he and his team know a recession is very possible in 2020, then they also know they would likely lose for that reason alone. But it’s more than that. An impeachment process allows to lose the presidency but keep a deep state conspiracy narrative alive. I didn’t lose, I was pushed out by the evils from within. A much more appealing narrative, especially if it comes with a blank immunity check for everything that may well still be uncovered. See, losing the 2020 election doesn’t come with an immunity deal. It may come with an arrest warrant. But dragging the country through a paralyzing constitutional crisis would likely come with an immunity deal as people from both sides would practically beg him to step down. Sure he says, but gimme and my family a blanket get out of jail free card. Why don’t you President Pence? After all it’s been done before.

The political remains speculative, but the Chinese are well served in waiting and managing to get a tariff delay for October in exchange for buying some soybeans and pork. Who knows that the political landscape will be 2-3 months from now.

But what is clear is this non deal deal is not going to suddenly promote investment or sudden economy growth. It may produce a sugar relief high, but as I outlined before: Bulls need new highs or face a major double top. And so far, despite all this:

So let me get this straight. On Friday alone:

Brexit “progress”

China “partial deal”

“warm feeling/progress” Trump tweets

$82.7B repo

$60B/month Treasury buying announcement (not QE wink wink)

multiple Fed speakers

All this on top of multiple rate cuts already.

Yet: No new highs.

No new highs. Yet. Next week Q3 earnings will start rolling in in earnest. Besides the results, look closely at the outlooks, especially hiring, as jobless claims is still the missing link for bears. But this week bears got another checkmark: The steepening of the yield curve has begun. The beginning of the end?

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

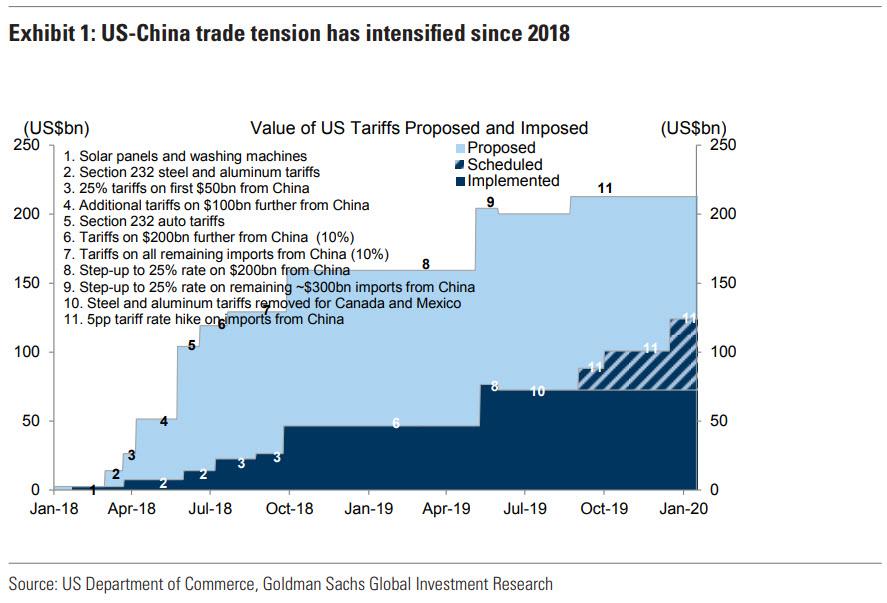

“Has It All Been Worth It”: Critics Lash Out At Trump’s “Trade Deal”

One day after Trump took a victory lap to celebrate “Phase 1” of the China trade non-deal that was “reached” almost two years after the US first launched tariffs on Chinese imports as part of an ever-escalating and bitter civilizational feud between the two superpowers…

… and which failed to resolve virtually any of the core outstanding issues but merely delayed implementation of next week’s tariffs in exchange for more imports of US pork and soybeans (which China desperately needs anyway), one question emerged: Has it really all been worth it?

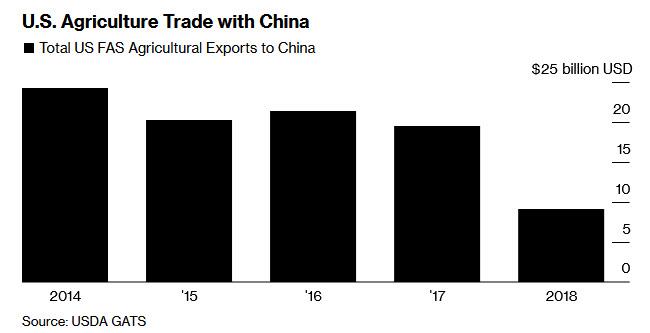

Consider what Trump touted as “the big win”: as Bloomberg notes, the surge in Chinese purchases of U.S. farm products that is the biggest victory for Trump in the agreement unveiled Friday is one that was first offered by Beijing more than two years ago. It will be accompanied by unspecified commitments – i.e., placeholders that will never be implemented – on intellectual property and currency and would, in theory, go some way to repairing the damage done to U.S. agriculture since tit-for-tat tariffs began more than 18 months ago.

In practice, they will remain just that: theoretical constructs that will be kicked back again and again as China will never concede to giving the US even implicit control over its currency, nor would it ever agree to an enforceable process that punishes it for reverse engineering US tech: after all, that is China’s fundamental economic modus operandi.

What is more concerning is that when stripping away the agricultural aspect, the agreement is far smaller in scope than what the president himself once envisioned, or what was on the table when talks broke down in May. Furthermore, “it also leaves major questions hanging in the wind amid a broader relationship showing plenty of signs of souring — ranging from the Chinese furor over an NBA executive’s backing for the growing protests in Hong Kong to the administration’s invocation for the first time this week of human rights to crack down on Chinese tech companies and visas for officials.”

“This deal hardly resolves any of the major underlying sources of trade and economic frictions between the two countries,” said Eswar Prasad, a former head of the IMF’s China team now at Cornell University.

The criticism continued from others, such as Bloomberg economists Tom Orlik and Yelena Shulyatyeva, who said that “there’s justified skepticism about whether even a mini-deal will get done. Officials said it will take three to five weeks to finalize the details. Past negotiations have broken down in less time than that.”

Speaking to the FT, DoubleLine CEO Jeffrey Gundlach also warned that the deal did not appear to be very substantive. “The trade deal looks to be more cosmetic than real.”

What the deal did achieve was a sharp bounce in stocks – one which Trump has become enamored with, believing it is the best proxy of his reelection chances. As Bloomberg aptly notes, “the package will calm markets and reduce fears of looming trade-driven recessions in the U.S. and global economies, even if Trump said Friday the two sides had yet to commit a deal to paper that he expects he and China’s Xi Jinping will sign in Chile a month from now.“

Perhaps it was the realization that nothing was actually achieved beyond the purely superficial, that after the furious intraday “rumor” rally sparked an even more aggressive bout of “selling the news.”

So what exactly was agreed? Here, too, there is some irony as the general framework of the deal unveiled Friday look very similar to ones negotiated by Treasury Secretary Steven Mnuchin and even Commerce Secretary Wilbur Ross that were rejected by Trump over the past two years, said Wendy Cutler, a longtime former U.S. trade negotiator who now heads the Asia Society Policy Institute.

“It looks more like a ‘light’ deal than a ‘substantial’ deal,” Cutler said, and remains at risk of being weakened further as negotiators put it down on paper in the weeks to come.

But the biggest criticism, one which even fervent Trump supporters as Laura Ingraham voiced, is that after months of escalation, Trump compromised this week and offered a tacit embrace of something he has resisted for months: a partial deal that might, in theory, yet grow into something more comprehensive… but in practice will take as many as three separate phases of negotiations, and in reality is dead on arrival.

The president should hold the line on China—letting up now gives them running room to continue their plan for all-sector dominance by 2025. #BeltandRoad#freedom

“Doing it in sections and phases I think is, really, better,” Trump said Friday, flip-floppingafter as recently as last week saying he would agree only to a big deal. In retrospect, what Trump really wanted, was to make sure the market doesn’t sell all the news at once. After all the stock market has been jumping every day for the past two years on trade hope optimism: once a deal is in place, there is no more optimism to push stocks higher!

That change in strategy reflects a reality that many analysts have warned of from the beginning of Trump’s attack on China. While Trump has steadily increased pressure on China with his tariffs, the Chinese have always been reluctant to embrace the wholesale economic changes Trump has demanded.

“There is still a yawning gap that separates the two sides on core structural issues,” said Prasad.

But, most importantly, the deal unveiled Friday does not include the “game changer” that Trump once promised would be a foundation of any deal with China: an enforcement mechanism to make sure that Beijing does not renege on its commitments. Trump could only make a vague promise that it would be worked out later.

Good luck with that.

Trump’s panicked U-turn to get some deal out was quickly noticed by both republicans and democrats: “After so much has been sacrificed, Americans will settle for nothing less than a full, enforceable and fair deal with China,” said Chuck Grassley, the Iowa Republican who is the party’s leading voice on trade in the Senate. Across the aisle, Senate Minority Leader Chuck Schumer, expressed opposition to a mini deal that includes relief for Huawei, which he said would “show tremendous weakness.”

Meanwhile, in the scramble to get a Friday afternoon soundbite, Trump was all too eager to set aside are many of the hardest issues confronting the two economies, including longstanding U.S. complaints about Chinese industrial policy and the government subsidies ranging from cheap electricity to low-interest loans that have fueled China’s economic rise.

So what hasn’t changed?

Well, the “deal” will keep in place the U.S. tariffs on some $360 billion in imports that have disrupted global supply chains and more importantly leave, at least for the time being, a threat for more to come in December. Trump seemed to hint on Friday that he may be willing not to go ahead with those tariffs, which would hit popular consumer items like smartphones, laptops and toys and are quietly opposed by some of his own advisers, who fear they could deepen a slowdown in the U.S. economy going into the 2020 election.

“I’m skeptical that there is anything that could be objectively called a deal,” said Scott Kennedy, an expert on the U.S.-China economic relationship at the Center for Strategic and International Studies in Washington. “It appears that the U.S. was looking to find a way to avoid raising tariffs in the next couple months and reassure financial markets, and so it was willing to accept only an oral agreement on a narrow range of issues to take this step.”

“Xi Jinping has to be quite satisfied with this outcome”, Kennedy note, perhaps envisioning the tacit acceptance by Trump of Hong Kong’s crackdown on pro-democracy protesters.

* * *

Other pressing questions remained unanswered: what the Chinese agreed to on intellectual property – the issue central to the “Section 301” investigation used to justify Trump’s tariffs – was unclear. The main complaints contained in the original report centered on strategies ranging from cyberattacks to joint venture requirements that China uses to unfairly obtain U.S. technology.

It was also unclear what was agreed on the issue of currency manipulation, another longstanding U.S. complaint. On Friday, Mnuchin said only that there had been new commitments on transparency and that the U.S. was willing to review its August designation of China as a currency manipulator.

People close to the talks said the currency deal, first hashed out earlier this year, closely emulates the commitments to adhere to market-determined exchange rates contained in Trump’s renegotiated Nafta, though those allow a dispute resolution process that the China agreement does not yet contain. Critics have already dubbed even the new Nafta provisions toothless.

That said, for all the criticism, Trump’s “deal” does have two major things to offer: A potential political victory for Trump and the sort of change of tone that many of his fellow world leaders have been hankering for.

“Today was a big win for the president,” said Stephen Vaughn, a partner at law firm King & Spalding who until earlier this year served as the right-hand man of Trump’s trade czar, Robert Lighthizer. “Once again, we see that the United States has enormous leverage in trade negotiations — when we choose to use it.”

“This won’t revolutionize the U.S.-China relationship or the terms of trade between us, but it shows that the two countries can work together on an important issue,” said Clete Willems, a former Trump adviser who now works at Akin Gump. “Learning to do so is critical to avoid a broad deterioration of all aspects of our relationship, which is not in anyone’s long term interest.”

The biggest irony, of course, is that is precisely the wrong take: after all, if nothing changes, it is only a matter of time before China overtakes the US technologically, economically and militarily. The only thing that would prevent this from happening is for Trump to refuse to fold in the trade war, now in its second year, and watch as the Chinese economy shriveled and was set back by years if not decades. Alas, faced with the prospect of a political loss in just over a year, Trump had no choice but to fold in hopes of being reelected. Whether that strategy works, remains to be seen.

Can A Policy Recession Occur When The Fed Is Easing?

Submitted by Joseph Crason, Former Director of Global Economic Research, Alliance Bernstein

Is it possible for a policy recession to occur when successive rounds of policy-stimulus have worked to extend the economic cycle and the policy-fuel runs out or cannot be provided in the same scale? We may soon find out.

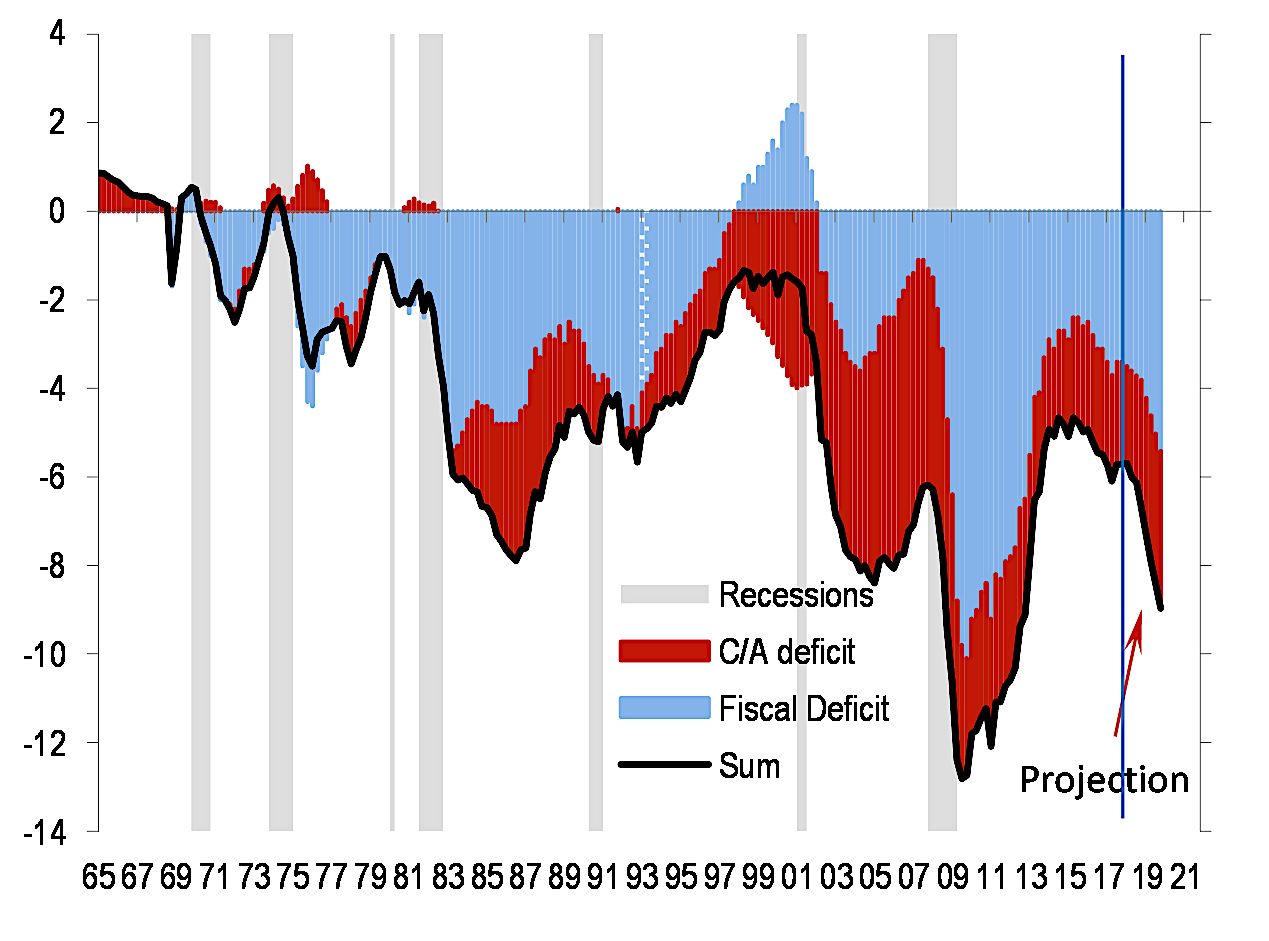

The current stance of monetary and fiscal policies is at odds with the economic cycle. The economic cycle is the longest in the post war period, running now for 123 months. Long cycles, with dwindling amounts of resources as is evident with the jobless rate at 3.5% the lowest in 50 years, have been associated with no policy support.

For example, there were two other economic cycles (1960s and 1990s) that also ran well over 100 months in length and at the end of both cycles the US budget was in surplus. Yet, nowadays the federal budget is not only in deficit, but the scale of the deficit is increasing.

The Congressional Budget Office estimated that the budget deficit for fiscal year 2019, which ended on September 30th, totaled $984 billion, or 4.7% of GDP. The budget deficit has increased by over $300 billion over the past two years, largely due to the 2017 tax cut. Companies used most of their portion of the tax cut to buy back their own stock, lifting equity prices in the process.

The monetary side of the policy apparatus is also misaligned when compared to long cycles. At the end of 1960s and 1990’s cycles (with jobless rates in the 3.5% to 4% range) the nominal fed funds rate stood 250 to 400 basis points above the consumer core rate of inflation.

With the decision to lower official rates by 25 basis points at the September 17-18 Federal Open Market Committee (FOMC) meeting, the mid-point of the fed funds target today is 50 basis points below the consumer core rate of inflation.

The policy imbalances and the potential impact on the economy and the financial markets have not gone unnoticed by policymakers. At the September 17-18 FOMC meeting “Several participants cited considerations that led them to be concerned about financial stability, including low risk spreads and a buildup of corporate debt, corporate stock buybacks financed through low-cost leverage, and the pace of lending in the CRE [commercial real estate] market.”

The potential imbalances in the commercial real estate market have been a focus of Mr. Eric Rosengren, the President of the Federal Reserve Bank of Boston. Mr. Rosengren has been warning about the fast rise in prices of commercial real estate, and also what he sees as an “asset-liability” mix problem.

Co-working firms are securing long-term leases from property owners, and then rent out the commercial space with short- term leases. Rosengren argues that the low interest rate environment has greatly increased leverage in the sector, while also pushing commercial real estate values to lofty levels. Rosengren has argued that although the risks of the co-working model will not be fully recognized until the next recession, he worries that additional policy-stimulus will only fuel even larger imbalances.

Low interest rates have also created an “asset-liability” mismatch on the household side as well. According to press reports, roughly one-third of new car loans taken out during the first half of 2019 had a average term that of nearly 7 years, with a small portion of new loans going beyond 84 months. Auto loans of 7 years and longer were not even offered in the prior cycle.

Stretching out the terms of car loans has been made possible by low interest rates, creating the impression that car buying has become more “affordable”. But there is also big downside.

Cars are usually held for 5 years, so an increasingly number of current new car-buyers will be forced to pay off their existing car loan or roll the debt from existing auto loans into a new car loan. How many consumers would be able to afford paying for a new loan and the remaining portion of the old loan at the same time? That asset-liability mismatch has the potential to trigger a slump in consumer spending at some point.

Policymakers are charged with mandate of maintaining economic and financial stability. Yet, from a risk management perspective when does attempting to extend the current cycle cross the line and endanger future cycles? Based on segments of the debt and equities markets, as well as segments of the real economy that “line” has already been crossed.

While many would argue that Americans’ First Amendment rights have long since dwindled from the liberties initially granted in The Bill of Rights, a decision by the European Union’s highest court could well mark the final nail in the coffin of free speech.

As Politico reports, the Court of Justice of the European Union (CJEU) has ruled that Facebook can be ordered to track down and remove content globally if it was found to be illegal in any EU country. In its ruling, CJEU said that EU law allowed local judges to order the world’s largest social network to remove illegal content, as well as delete material that conveyed a similar message under certain circumstances.

The decision is not just a slap in the face of worldwide citizens’ freedom of expression, but a big defeat for Facebook as it will force them to be more responsible for what is appearing on the internet (and thus what is seen by those who make the rules as not appropriate for the genpop).

“This judgement raises critical questions around freedom of expression and the role that internet companies should play in monitoring, interpreting and removing speech,” Toby Partlett, a Facebook spokesman, said in a statement.

“We hope the courts take a proportionate and measured approach to avoid having a chilling effect on freedom of expression.”

Of course, it won’t as EU bureaucrats have hardly shown the ability to undertake measured responses when it comes to cracking down on non-sanctioned thoughts, words, and memes. Facebook officials went to exclaim that:

…the ruling “undermines the longstanding principle that one country does not have the right to impose its laws on speech on another country.”

As Politico details, the ruling stems from a lawsuit filed in 2016 by Eva Glawischnig-Piesczek, an Austrian lawmaker, who had requested that Facebook delete defamatory posts made about her by an anonymous user.

When an Austrian court sided with her, the company initially only removed the content from being viewed in Austria, but subsequent appeals had focused on whether such takedowns should apply globally, and if Facebook should be required to remove similar content once it has been made aware of the defamatory material.

Following the ruling by Europe’s highest court, her case will now be referred back to Austrian judges, who will make the final ruling about how to apply Thursday’s decision.

As one would expect, digital rights campaigners were incensed by the breadth of the decision:

“The court’s decision opens the door for serious restrictions on freedom of expression due to the takedown of legitimate speech. Extending removal to the vague concept of “equivalent” content is harmful because the context as well as motivation of users re-sharing content may significantly differ with each re-upload,” said Eliška Pírková, Europe policy analyst at Access Now, a campaigning group.

Those who believe tyranny cannot come to the United States should take a look around because it’s already here and as the EU court’s decision shows, it is not just Washington that Americans should fear.

It’s hard to imagine a more euphoric end to the week for bulls.

Two weeks ago I issued a report titled Realistically, What’s Left To Power Asset Prices Higher? which claimed the bulls only hope was for a near-term resumption of QE (quantitative easing, aka “money printing”) or a China trade deal.

Well, this week they got both.

Jerome Powell announced Wednesday that the U.S. Federal Reserve will resume expanding its balance sheet to the tune of $60 billion per month. And just a few hours ago, the Trump administration announced it had reached a partial trade agreement with its Chinese counterparts.

And to put a cherry on top of things, word from across the Pond is that somehow a Brexit deal just might happen by the end of the month.

When I began typing this article earlier today, the markets were fiercely building towards an orgiastic climax. They ended with a slight post-coital breather, closing modestly off the day’s highs.

In short, the bulls are suddenly having the time of their lives.

So, does this mean happy days have returned? Have we been rescued from the rising tide of data warning of an economic slowdown and lower asset prices? Does the Fed — and now China, too — have our back again?

Is it time for investors to become optimistic once more?

“Markets” No More

Before we answer that, though, let’s address the elephant in the room. We no longer have functioning financial markets.

The central banking cartel has killed price discovery. The $15+ TRILLION in liquidity injected by the Fed, EBC, BoJ, BoE and PBoC over the past decade has ‘risen all boats’ when it comes to asset prices.

Whether great, mediocre, or horrible, the price of nearly every company/property/investment has been on a one-way 45-degree ramp upwards since global co-ordinated quantitative easing began in 2009.

And Wednesday’s announcement by the Fed simply shows that this game will continue, despite years of broken promises that it would instead ‘normalize’ (i.e., undo much of its past QE).

As a result, we live in a world where traditional price signals have become meaningless. Management turmoil? Missed earnings expectations? Regulators cracking down on your industry? None of it matters in a world of perpetual QE. As long as stimulus keeps flowing, everything heads in the same direction: UP.

All that matters is guessing what the small coterie of central bankers plan to do next. Will they tighten from here? Or ease? By how much? And for how long?

As a result, ‘investing’ is a dead science. Instead, we’ve all been forced to become speculators.

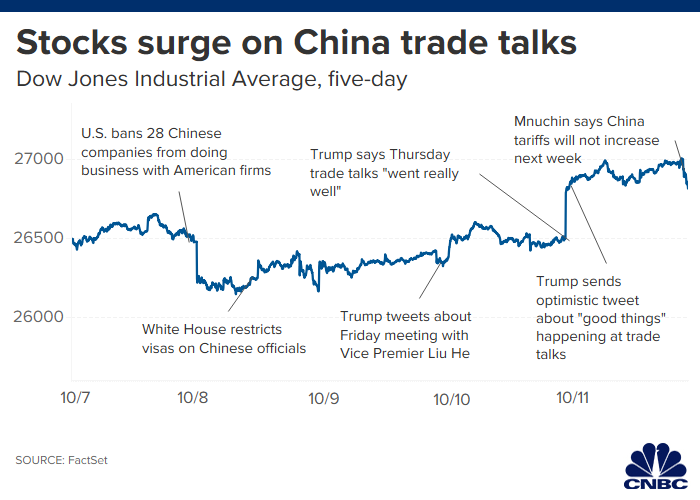

Meanwhile, extremely manipulable high frequency trading (HFT) algorithms dominate the daily price action. Stock prices now hyper-react instantly to every tweet and leak, which the media and the Trump administration now exploit to maximum advantage.

Seriously — and this is topic for a future lengthy exploration — those in favor of removing President Trump may have a better case to make for market manipulation as his impeachable offense. He’s been shoving market prices around on a daily basis for years now. And how are his tweets this week — one of which instantly sent the Dow skyrocketing 300 points on Thursday — not considered in flagrante delicto examples of painting the tape? (a prohibited form of manipulation in which the criminal ‘creates activity or rumors to drive up the price of a stock’):

Time To Pile Back Into The Market?

But making the (safe) assumption no one in power cares about our broken markets as long as they benefit from the status quo, where are prices more likely to go from here?

Two weeks ago, I argued that the only things that would save the bulls in the near term was new QE and a China deal. Now that the past 48 hours delivered on both counts, the outlook for the rest of 2019 is now substantially more complex to forecast.

Nearly all of the negative indicators we’ve been warning about still remain. The macro outlook still screams recession risk, corporate earnings are still forecast to disappoint, geopolitical strains remain unresolved, and the world’s oil supply chain looks even more vulnerable given today’s news that an Iranian oil tanker was struck by missiles in the Red Sea.

That said, Powell’s new $60 billion per month QE program (which he swears isn’t really QE) will surely have a stimulative impact on the system. Even if those funds don’t make it out into the economy directly, they will keep both good and bad banks solvent and thus keep credit flowing. That will help in keeping today’s zombie companies/jobs/buyback programs alive for the foreseeable future.

As for the China trade deal, honestly, who knows at the moment? Technically, what was announced today isn’t officially an agreement. And what was “agreed” to by the parties were the less-sensitive issues on the table.

Bloomberg controlled most of the information flow about today’s trade news, and this is how its own staff economists summarize today’s “progress”. Not exactly breathless optimism:

What Our Economists Say

“Past experience is that U.S.–China trade agreements aren’t worth the paper they are written on, and this one hasn’t even been written down. For now, though, indications on trade are a little more positive. If that persists, it could help put a floor under sliding global growth.”

Tom Orlik and Yelena Shulyatyeva, Bloomberg Economics

And the Chinese themselves are reacting with much more muted enthusiasm than our Tweeter-in-Chief. In fact, they aren’t yet willing to concede that any “deal” has been struck:

Chinese state news agency Xinhua said negotiators made efforts toward a final agreement, but stopped short of calling Friday’s outcome a deal. The Editor-in-Chief of China’s most prominent state-run newspaper Global Times, Hu Xijin, noted on Twitter that official reports from China didn’t mention Trump’s goal of signing the deal next month, which indicates Beijing wants to keep expectations low.

Long story short, we’re still a far distance from any formal compact that resolves the principal triggers that caused the US-China trade dispute. While today’s “news” may be a step in the right direction and help both parties save a little face, I think Sven Henrich summarizes it best in these twin tweets:

Proceed VERY Cautiously From Here

So did everything change this week?

Too early to tell.

But we highly caution against interpreting this week’s developments as a green light that it’s safe to jump back into the markets.

Powell’s Not-QE may do little more than slow the gangrene spread of recession within the US economy. Today’s China deal could quickly prove to be another “nothingburger” in a year-long process defined much more by disappointment than progress.

Note that despite their happy ride this week, markets are still closed below their all-time highs. So we still need to ask: What’s going to power them higher from here, now that they’ve gotten exactly what they wished for?

With new QE and an interim China agreement now priced in, what pressure remains to push stocks higher? Without a compelling answer, this weekend could very well mark the apex between “buy the rumor” and “sell the news”. If so, we could see a lot of disappointed bulls next week as today’s highs fail to stick.

We’re at an inflection point where the establishment is pulling out all the stops to keep the world’s longest economic expansion continuing and avert a market correction. It is pitted against the fundamental forces of reality, which want to eradicate the $trillions of bad debts and malinvestment that have built up in the system due to central planner intervention.

How much longer can the status quo protect itself from the repercussions of it past and present behavior?

While this great game plays out, asset prices will likely whipsaw before they make their next big move. Which is why we so strongly urge anyone with money at risk in today’s markets (in retirement funds, brokerage accounts, real estate, business investments, etc) to work with a financial advisor who understands the risks in play.

For better or worse, this is an exceptionally challenging time to navigate the financial markets. And this week’s developments have only increased the uncertainty of the trajectory that will win out from here.

Our consul remains the same: Position for safety. Deploy hedges in your portfolio. And if you don’t feel confident in how to do this yourself, partner with an experienced professional advisor — if you’re having trouble finding a good one, schedule a free consultationwith New Harbor Financial, the firm we endorse.

So many plan to do this but end up not taking action until it’s too late. I recently asked New Harbor what is the most common issue they encounter when conducting a portfolio review, and they report — by far — it’s overexposure.

Most people they talk to a) don’t have a good understanding of all of the securities they own, and b) are currently “all in” with their portfolio allocations. This hasn’t really been an issue while the markets have powered higher year after year for the past decade. But it puts them unnecessarily at risk of painful losses when the inevitable next market correction happens.

I use the word “unnecessarily” because a short conversation and a few prudent decisions can mean a world of difference to how your financial wealth fares going forward.

Whatever you choose to do from here, just make sure it’s an intentional decision. These markets are just now too damn uncertain to leave your destiny to chance.

Elizabeth Warren Buys Facebook Ads Claiming Mark Zuckerberg Backs Trump

Elizabeth Warren’s campaign is buying ads on Facebook which falsely claim that CEO Mark Zuckerberg has endorsed President Trump – before quickly admitting it’s not true.

The message? Facebook needs to fact-check ads by politicians.

The Democratic presidential candidate’s campaign sponsored the posts that were blasted into the feeds of U.S. users of the social network, pushing back against Facebook’s policy to exempt politicians’ ads from its third-party fact-checking program.

The ad begins with a lie: Facebook’s chief executive officer “just endorsed” Trump for re-election. It quickly backtracks to the truth. –Bloomberg

“You’re probably shocked. And you might be thinking, ‘how could this possibly be true?” the ad says. “Well, it’s not.”

“What Zuckerberg ‘has’ done is given Donald Trump free rein to lie on his platform — and then to pay Facebook gobs of money to push out their lies to American voters,” reads Warren’s ad.

Hilariously, Bloomberg’s example of an ‘untrue’ Trump ad revolves around video evidence of former Vice President Joe Biden threatening to withhold $1 billion in US loan guarantees from Ukraine if they didn’t fire a prosecutor investigating a gas company paying his son $600,000 per year.

The Biden campaign has asked both Twitter and Facebook to remove the Trump ads, however both platforms have refused according to The Verge. “The ad you cited is not currently in violation of our policies,” said one Twitter spokesman.

Facebook’s decision to allow Trump’s ad contrasts with CNN, which rejected a request by the president’s campaign to run what the network called two “demonstrably false” claims.

“If Senator Warren wants to say things she knows to be untrue, we believe Facebook should not be in the position of censoring that speech,” Andy Stone, a spokesman for Facebook, said in a statement to CNN on the ads. –Bloomberg

Warren, meanwhile, is also guilty of false advertising – such as an Instagram video which suggests she might be fun to share a beer with.

{kind=link}

{kind=link}