Late Monday President Trump signed an executive order imposing a full economic embargo against Venezuela after a week ago the White House began signaling it could seek to “quarantine” and fully “blockade” the Maduro regime if the president doesn’t immediately hand over power of his own accord.

The executive order freezes all government assets in the United States and prohibits all transactions by any Venezuelan officials, in what constitutes the first major expansion of sanctions targeting a nation in the western hemisphere in over three decades.

File image via Time

The order focuses on human rights abuses and Maduro’s continued “usurpation” of power as necessary to enact the full embargo, and places the Latin American country on par with Cuba, Syria, Iran and North Korea. Though Trump recently signaled he was “bored” with meddling in Venezuela after a failed military coup earlier this year, the executive order is the latest in a string of measures intent on regime change.

“All property and interests in property of the Government of Venezuela that are in the United States … are blocked and may not be transferred, paid, exported, withdrawn, or otherwise dealt in,” the executive order says. Americans are further prevented from doing business with Venezuela’s government or officials, effective immediately.

Though it falls short of an outright trade embargo, it does dramatically escalate US efforts to force a Maduro exit in favor of US-backed opposition leader and self-proclaimed “interim president” Juan Guaido.

Via The Wall Street Journal

A recent Bloomberg report also indicated Trump admin discussions have involved the possibility of imposing a complete blockade on the country by sea, enforced by US Navy ships.

President Maduro slammed on the comments last Friday, and directed his ambassador to lodge a formal complaint with the UN Security Council, saying any attempt to block the Venezuelan coastline is “clearly illegal” according to international law and norms. He said in a televised broadcast on Friday:Venezuela’s seas would remain “free and independent.”

“All of Venezuela, in a civic-military union, repudiates and rejects the statements of Donald Trump about a supposed quarantine, of a supposed blockade,” Maduro said in the speech. “A blockade, why would he announce that? It is clearly illegal.”

via ZeroHedge News https://ift.tt/2MH4USr Tyler Durden

Last weekend’s mass shootings in El Paso and Dayton (following the devastation in Gilroy the weekend before) prompted the usual evidence-free avalanche of political point-scoring, blaming “the other side” for all the world’s woes.

“Did George Bush ever condemn President Obama after Sandy Hook. President Obama had 32 mass shootings during his reign. Not many people said Obama is out of Control. Mass shootings were happening before the President even thought about running for Pres.” @kilmeade@foxandfriends

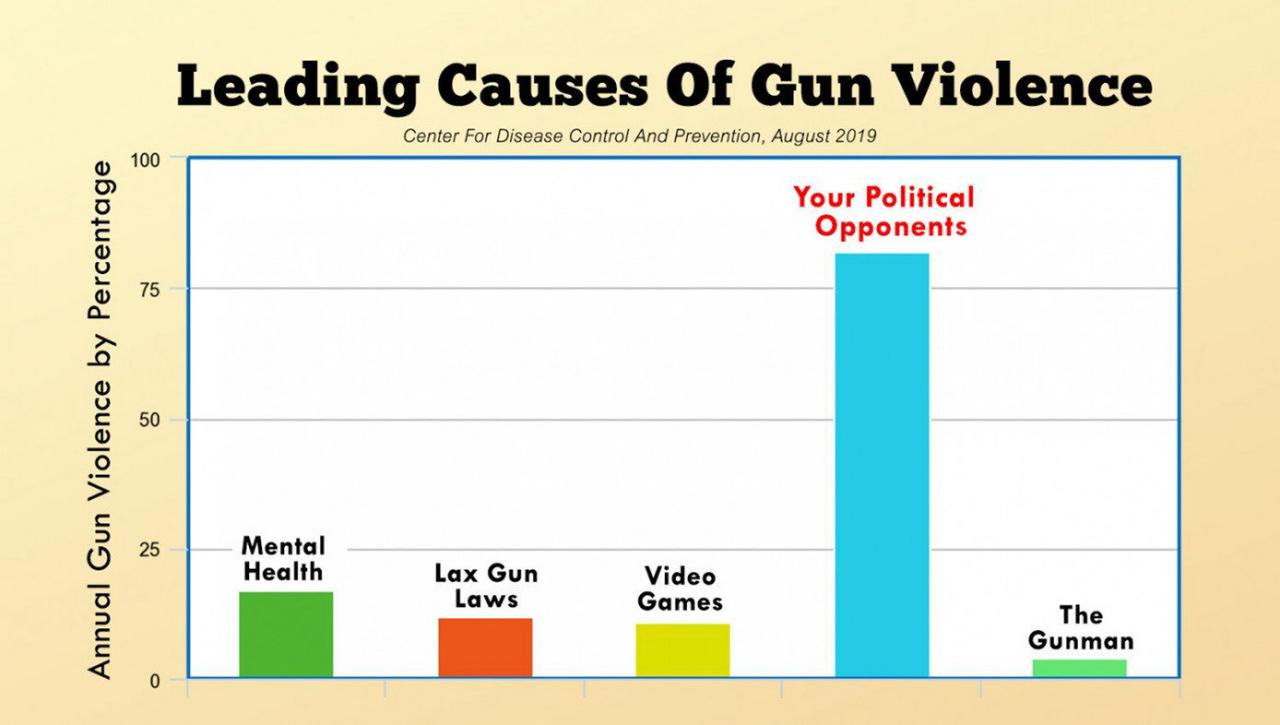

An exhaustive new study from the CDC reveals that the leading cause of gun violence in America is your political opponents. Researchers looked at a number of potential causes of gun violence such as mental health, family situation, cultural shifts, gun laws, rap music, videogames, sugar consumption, and the actual gunman, but by and large, the most prominent cause of gun violence was what most already suspected. The fault lies with those who you disagree with politically.

For two years, we’ve been studying the life histories of mass shooters in the United States for a project funded by the National Institute of Justice, the research arm of the U.S. Department of Justice. We’ve built a database dating back to 1966 of every mass shooter who shot and killed four or more people in a public place, and every shooting incident at schools, workplaces, and places of worship since 1999. We’ve interviewed incarcerated perpetrators and their families, shooting survivors and first responders. We’ve read media and social media, manifestos, suicide notes, trial transcripts and medical records.

Our goal has been to find new, data-driven pathways for preventing such shootings. Although we haven’t found that mass shooters are all alike, our data do reveal four commonalities among the perpetrators of nearly all the mass shootings we studied.

First, the vast majority of mass shooters in our study experienced early childhood trauma and exposure to violence at a young age. The nature of their exposure included parental suicide, physical or sexual abuse, neglect, domestic violence, and/or severe bullying. The trauma was often a precursor to mental health concerns, including depression, anxiety, thought disorders or suicidality.

Second, practically every mass shooter we studied had reached an identifiable crisis point in the weeks or months leading up to the shooting. They often had become angry and despondent because of a specific grievance. For workplace shooters, a change in job status was frequently the trigger. For shooters in other contexts, relationship rejection or loss often played a role. Such crises were, in many cases, communicated to others through a marked change in behavior, an expression of suicidal thoughts or plans, or specific threats of violence.

Third, most of the shooters had studied the actions of other shooters and sought validation for their motives. People in crisis have always existed. But in the age of 24-hour rolling news and social media, there are scripts to follow that promise notoriety in death. Societal fear and fascination with mass shootings partly drives the motivation to commit them. Hence, as we have seen in the last week, mass shootings tend to come in clusters. They are socially contagious. Perpetrators study other perpetrators and model their acts after previous shootings. Many are radicalized online in their search for validation from others that their will to murder is justified.

Fourth, the shooters all had the means to carry out their plans. Once someone decides life is no longer worth living and that murdering others would be a proper revenge, only means and opportunity stand in the way of another mass shooting. Is an appropriate shooting site accessible? Can the would-be shooter obtain firearms? In 80% of school shootings, perpetrators got their weapons from family members, according to our data. Workplace shooters tended to use handguns they legally owned. Other public shooters were more likely to acquire them illegally.

So what do these commonalities tell us about how to prevent future shootings?

One step needs to be depriving potential shooters of the means to carry out their plans. Potential shooting sites can be made less accessible with visible security measures such as metal detectors and police officers. And weapons need to be better controlled, through age restrictions, permit-to-purchase licensing, universal background checks, safe storage campaigns and red-flag laws — measures that help control firearm access for vulnerable individuals or people in crisis.

Another step is to try to make it more difficult for potential perpetrators to find validation for their planned actions. Media campaigns like #nonotoriety are helping starve perpetrators of the oxygen of publicity, and technology companies are increasingly being held accountable for facilitating mass violence. But we all can slow the spread of mass shootings by changing how we consume, produce, and distribute violent content on media and social media. Don’t like or share violent content. Don’t read or share killers’ manifestos and other hate screeds posted on the internet. We also need to study our current approaches. For example, do lockdown and active shooter drills help children prepare for the worst or hand potential shooters the script for mass violence by normalizing or rehearsing it?

We also need to, as a society, be more proactive. Most mass public shooters are suicidal, and their crises are often well known to others before the shooting occurs. The vast majority of mass shooters leak their plans ahead of time. People who see or sense something is wrong, however, may not always say something to someone owing to the absence of clear reporting protocols or fear of overreaction and unduly labeling a person as a potential threat. Proactive violence prevention starts with schools, colleges, churches and employers initiating conversations about mental health and establishing systems for identifying individuals in crisis, reporting concerns and reaching out — not with punitive measures but with resources and long-term intervention. Everyone should be trained to recognize the signs of a crisis.

Proactivity needs to extend also to the traumas in early life that are common to so many mass shooters. Those early exposures to violence need addressing when they happen with ready access to social services and high-quality, affordable mental health treatment in the community. School counselors and social workers, employee wellness programs, projects that teach resilience and social emotional learning, and policies and practices that decrease the stigma around mental illness will not just help prevent mass shootings, but will also help promote the social and emotional success of all Americans.

Our data show that mass shooters have much in common. Instead of simply rehearsing for the inevitable, we need to use that data to drive effective prevention strategies.

* * *

Perhaps wannabe-politicians like Beto O’Rourke should wind their ‘Trump is hitler and therefore to blame’ soundbites in and focus on the real issues facing Americans.

via ZeroHedge News https://ift.tt/2T8YJI9 Tyler Durden

Now that Beijing has cancelled the round of ag purchases promised by President Xi in Osaka, President Trump appears to be promising yet another farmer bailout (what would be the third under his administration) next year, if necessary.

As they have learned in the last two years, our great American Farmers know that China will not be able to hurt them in that their President has stood with them and done what no other president would do – And I’ll do it again next year if necessary!

As everyone knows by now, after the market closed on Monday, the US Treasury unexpectedly named China a currency manipulator, which naturally will be viewed as an escalation of the trade war and exacerbate the market sell-off, even if the PBOC briefly limited the selloff overnight by fixing the yuan slightly higher than expected (don’t expect this calm to last).

While symbolically significant given that this designation was last used 25 years ago, in and of itself this act is unlikely to result in actions on the scale of recent tariffs or other US sanctions.

So what does it mean to be a named a manipulator?

Below we share the quick take of Standard Chartered’s Steven Englander.

Consider the relevant portions of Section 3004 of the Omnibus Trade and Competitiveness Act of 1988. Being designated a manipulator means “…the Secretary of the Treasury shall take action to initiate negotiations… in the International Monetary Fund or bilaterally, for the purpose of ensuring that such countries regularly and promptly adjust the rate of exchange… to eliminate the unfair advantage.” Under Section 701 of the Trade Facilitation and Trade Enforcement Act of 2015, “If… one year after the commencement of enhanced bilateral engagement… country has failed to adopt appropriate policies to correct the undervaluation… the President shall take one or more of the following actions: (A) Prohibit the Overseas Private Investment Corporation from approving any new financing… (B) prohibit the Federal Government from procuring… goods or services from that country… (C) instruct the United States Executive Director of the International Monetary Fund to call for additional rigorous surveillance of the macroeconomic and exchange rate policies of that country… (D) instruct the United States Trade Representative to take into account, in consultation with the Secretary in assessing whether to enter into a bilateral or regional trade agreement with that country…”

It may be embarrassing to be named a manipulator, but the consequences are not severe. However, a year of negotiations followed by the relatively modest sanctions listed above may work politically for the US administration if it is unable to cut a trade deal with China in the coming months.

In market terms, the designation, however meretricious, will likely be seen as a further ramping up of the trade dispute and possibly leading to some reaction by China. Naming China a manipulator, given the absence of teeth to the law, should have less substantive impact on activity and asset markets than a tariff increase, but it will likely add to asset market pressures in the short term and pressure the Fed on additional easing.

Fed easing is likely to be the most effective long-term means of weakening the USD; the US administration’s actions may be in part driven by the desire to add pressure on the Fed. The immediate asset market response is likely to be added downward pressure on equities, bond yields and risk-correlated currencies.

And here is the take of Goldman’s FX strategist Andrew Tilton:

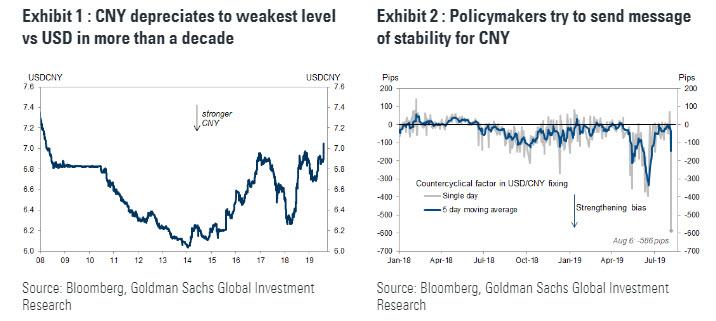

The US Treasury has designated China a “currency manipulator” under section 3004 of the Omnibus Trade and Competitiveness Act of 1988. This follows Monday’s weakening of the Chinese renminbi through 7 to the US dollar, the first time the renminbi has traded through this threshold in more than a decade (Exhibit 1). The Treasury last used the currency manipulator designation 25 years ago (China was also designated from 1992-94).

While the move represents a symbolic escalation of the trade conflict, as a practical matter we do not expect it to have major consequences on its own. The US administration has already levied substantial tariffs on Chinese goods, among other actions. The Treasury statement says only that Secretary Mnuchin “will engage with the International Monetary Fund to eliminate the unfair competitive advantage created by China’s latest actions.” (In this regard, we note the IMF’s chief economist recently indicated that “China’s external position moved to become more broadly in line with fundamentals in 2018”, in part due to “greater exchange rate flexibility and the associated real appreciation over the last decade”.)

Ironically, the latest actions by Chinese policymakers appear to be aimed at limiting the degree of CNY depreciation that takes place. Yesterday’s statement by the PBOC includes language that downplays the 7 threshold, implying that the currency could potentially re-strengthen through this threshold, and would not necessarily depreciate sharply further. We view this as broadly consistent with our own forecasts (USDCNY 7.05 in three months, around the current level), although near-term risks still seem skewed towards weakness. We note the PBOC also employed the largest-ever “countercyclical factor” this morning (Exhibit 2 below), with the daily CNY fixing 586 pips stronger than a formula using the previous day’s close and overnight broad USD move would suggest – a signal that policymakers want to avoid a sharp depreciation.

via ZeroHedge News https://ift.tt/31nQhHX Tyler Durden

US equity futures popped higher along with the offshore yuan after PBOC issued a brief statement claiming that it is not a currency manipulator and tells foreign firms that yuan won’t keep falling.

As Reuters reports, China firmly opposes a U.S. decision to label it a currency manipulator, its central bank said on Tuesday, adding that Beijing has not used and will not use the yuan to cope with trade frictions with the world’s biggest economy. Designating China as a currency manipulator seriously harms international rules, the People’s Bank of China (PBOC) said in a statement.

Stocks, already rebounding overnight, gained a little more…

And yuan…

However, this is farcical because of course Chinese authorities do not want to make the yuan a one-way bet and entirely lose control. As we tweeted last night, there are far more serious things PBOC could do if it was serious about stalling the Yuan’s freefall…

If Yuan pressure was external, and if China really wanted it to trade inside 7.00 it would just hike overnight repo to 1000% and all the shorts would die

But it isn’t, as Bloomberg notes, assurances from China’s central bank that it won’t use the yuan to fight a trade war with the U.S. have fallen on deaf ears.

Timeline Then

April 2015: Premier Li Says China Doesn’t Want Devaluation

May 2015: PBOC’s Yi Says Devaluation Not Necessary

August 2015: Yuan Devaluation Jolts Global Markets

Timeline Now

April 2019: Xi Says China Won’t Pursue Harmful Yuan Devaluation

May 2019: PBOC Pledges Steady Yuan

Aug. 5, 2019: China Lets Yuan Tumble Past 7 Per Dollar as Trade War Escalates

Aug. 5, 2019: PBOC’s Yi says China Won’t Use FX as Tool in Trade Dispute

Remember, it’s different this time.

via ZeroHedge News https://ift.tt/2GQcNBc Tyler Durden

As late as last December, Goldman was expecting four rate hikes in 2019. Then, as recently as mid-June, the “smartest men in the Goldman room”, did not expect the Fed to cut rates at all in July and September. Of course, all that changed when it became clear that “Powell has thrown in the towel”, and will follow the demands of the president and the whims of the market, resulting in the first “mid-cycle” rate cut last month in over a decade.

And now, Goldman has once again shown that its forecasting ability is the functional equivalent of a coin toss, when late on Monday night Goldman economist David Mercile said Goldman no longer expects the US and China to agree on a deal to end their trade war before the November 2020 presidential election as policymakers from the world’s largest economies are “taking a harder line”.

On the US side, press reports indicate that President Trump made the decision to raise tariffs despite the strong objections of all but one of his advisors, Director of the Office of Trade and Manufacturing Policy Peter Navarro, and threatened to lift tariff rates even further to “well beyond 25%” if necessary. Just this evening, the Treasury Department took the further step of designating China a currency manipulator. While we had previously assumed that President Trump would see making a deal as more advantageous to his 2020 re-election prospects, we are now less confident that this is his view.

On the Chinese side, the currency depreciation past the symbolically important level of 7 yuan per dollar and the announcement that China has suspended purchases of US agricultural goods added up to a swift and meaningful response. News reports suggest that Chinese policymakers are increasingly inclined not to make major concessions and instead to wait until after the 2020 US presidential election to resolve the trade dispute if necessary.

As a result, a trade deal now looks far off. Press reports indicate that trade talks are going poorly. The White House appears increasingly unlikely to accept a deal that does not include major structural reforms, and Chinese policymakers appear increasingly unlikely to accept a deal that does not include a major immediate reduction in tariffs. This has made a more symbolic deal consisting mainly of a Chinese commitment to buy more US exports less realistic.

As a result, Goldman’s “base case is now that no deal will be reached before the 2020 election. We expect the newly announced 10% tariffs on the last $300bn to remain in place on Election Day, and other forms of tit-for-tat retaliation are possible along the way.”

In parallel with this extended trade war, the bank has extended its prior forecast of two rate cuts in 2019, and now expects two back-to-back rate cuts from the Fed: “In light of growing trade policy risks, market expectations for much deeper rate cuts, and an increase in global risk related to the possibility of a no-deal Brexit, we now expect a third 25bp rate cut in October, for a total of 75bp of cuts.“

Goldman explains that “the balance of risks has shifted enough to make a third 25bp rate cut in October the most likely outcome, for a total of 75bp of cuts including the July cut.” Specifically, for the September meeting, Goldman sees a 75% chance of a 25bp cut, a 15% chance of a 50bp cut, and a 10% chance of no cut. For the October meeting we see a 50% chance of a 25bp cut, a 10% chance of a 50bp cut, and a 40% chance of no cut.

This is contrary to the message the Fed was trying to convey, as Mericle thinks “the FOMC most likely envisioned at its July meeting that rate cuts would eventually total 50bp. This strikes us as the best guess of what Chair Powell meant by a “mid-cycle adjustment” to “adjust policy to a somewhat more accommodative stance over time,” as well as the most likely compromise on a divided committee in which many participants were skeptical of the case for cutting at all.”

So picking up where Goldman left off last week when it tried to infer what it would take for the Fed to stop cutting rates, the bank now says that “for rate cuts to stop, Fed officials will eventually have to withstand White House demands and perhaps bond market expectations as well” and it adds that by the December meeting “the FOMC is likely to stop.”

By that point we expect core PCE to stand at 1.9% as of the October print, with tracking estimates based on the November CPI at 2%. We also think some FOMC participants would push back harder against rate cuts that summed to 100bp or more, an amount that in the past has been reserved for situations in which there was a strong chance that the economy was already headed into recession.

Of course, this being a Goldman forecast, the most likely outcome is whatever Goldman does not expect as a baseline (sorry, but that’s just the bank’s own dismal predictive track record). And amusingly enough, Goldman concedes as much saying that it sees “risks in both directions.”

There is still some chance that the White House will not proceed with the latest threatened escalation, perhaps in view of recent market moves. In the other direction, further increases in tariff rates down the road—say from 10% to 25% on the upcoming round—would increase the odds of deeper cuts.

It is hardly a surprise that Trump would like to keep escalating the trade war just to get even more rate cuts, but the emerging risk as BofA explained yesterday is that Trump slows down the US, and global, economies so much that no amount of easing, or bond buying, by the Fed will be able to offset it. One thing, however, is certain: the next 16 months will be especially interesting for markets.

via ZeroHedge News https://ift.tt/2OJ0MUR Tyler Durden

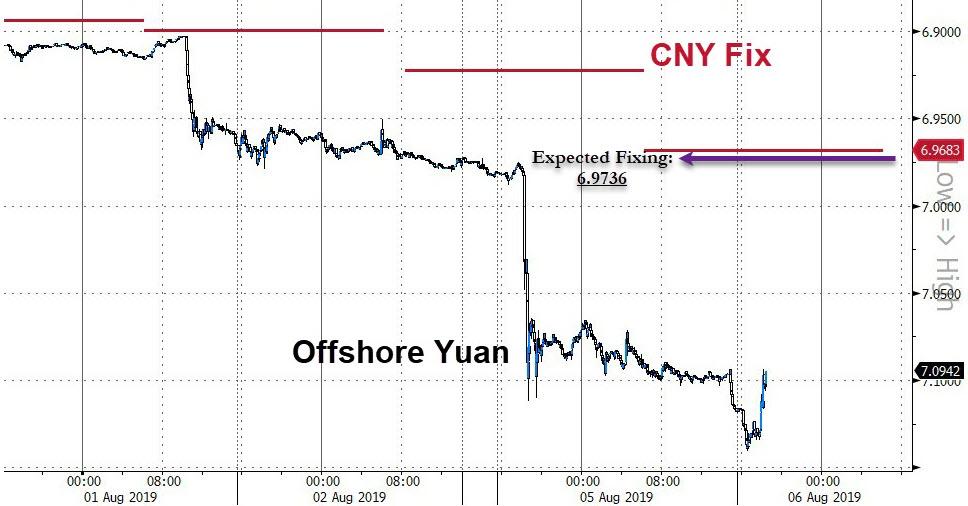

With the world on the verge of panic last night after the US Treasury’s shocking announcement for the first time in 25 years that China was branded a currency manipulator (after ignoring China’s efforts for years to prop up its currency, just so Beijing would avoid a massive capital flight, all it took was one day of allowing the yuan to tumble for Trump to be triggered), a wave of relief swept across global markets when the PBOC fixed the yuan at 6.9683 per dollar, not only stronger than the 7.00 “line in the sand”, but also marginally stronger relative to the 6.9871 forecast by analysts and traders surveyed by Bloomberg, and the 6.9736 forecast by a major Chinese publication.

The result was that while trade war between the world’s top economies remained near boiling point, some of the heat was reduced just enough by the firmer-than-expected fixing in the yuan rate, which immediately helped steady trader nerves after the biggest drop in the US stock market of 2019 which saw the Dow plunge 767 points.

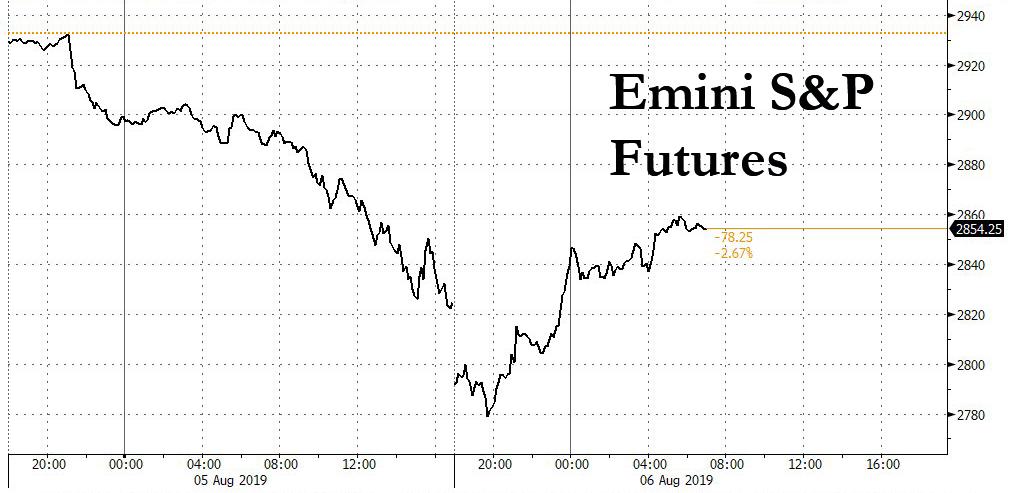

Safe-haven assets, including bonds and some currencies such as the yen and Swiss franc, settled down as investors moved tentatively back into the euro, pound and some of the emerging market currencies that have been hit in recent days, while U.S. equity futures, which had tumbled as much as 1.9% after the Treasury’s announcement, rose as much as 0.9%, surging 70 points from session lows…

… alongside European stocks while Asian shares fell after what the narrative quickly saw as “China moving to stabilize its currency”, helping ease some of the market turmoil that kicked off the week, and resulting in a buying spree this morning.

The mood remains fragile though and a stray headline or a Trump tweet can undo everything, especially now that the S&P is trading at a level where CTAs turn short.

“I think the tipping point for a more prolonged negative trend (for risk assets) is quite close,” said SEB Investment Management’s head of asset allocation Hans Peterson, referring to the trade war escalation and other risks such as Brexit. “We have reduced both European and global equities. We still have a small overweight in EM (emerging market) stocks but just a small one.”

Meanwhile, now that the US officially declared that China was manipulating its currency, and that Washington would engage the International Monetary Fund to eliminate unfair competition from Beijing, there is confusion as to what the US will do next: “Officially labeling China a currency manipulator gives the United States a legitimate reason to take even more steps,” said Norihiro Fujito, senior investment strategist at Mitsubishi UFJ Morgan Stanley Securities. “The markets are now scrambling to factor in the possibility of the United States imposing not only an additional 10% of tariffs on Chinese imports, but the figure being raised to 25%.

Europe’s Stoxx 600 index extended gain to as much as 0.6%, rebounding from the biggest 2-day drop in three years, and tracking the rebound in S&P futures. Earlier, the European index dropped as much as 0.3% earlier but all 19 sectors advanced in the morning session; LVMH Moet Hennessy Louis Vuitton jumped +2.2% after upgrade at Bernstein, Vivendi soared +7.3% on Tencent talks for UMG stake.

Earlier in the session, stocks dropped across Asia, with MSCI’s Asia-Pacific index ex-Japan ending down 0.75% after brushing its lowest since January. It has lost 3.7% so far this week. The drop was led by health care and energy firms, as traders were spooked by the escalating trade war between China and the US. Most markets in the region were down, with Australia and China leading declines. The Topix retreated 0.4%, nearly erasing its 2019 gains, as electronics and telecommunications companies dragged the Japanese gauge lower. The Shanghai Composite Index closed 1.6% lower, driven by Industrial & Commercial Bank of China and Inner Mongolia Yili Industrial Group. PetroChina’s A-shares fell 1.4% to a record low. India’s Sensex climbed 1.3%, bucking regional declines, after Credit Suisse AG upgraded the nation’s stocks to overweight amid the China-U.S. dispute. Separately, the Indian government cemented its position by revoking seven decades of autonomy in the disputed Muslim-majority state of Kashmir

In rates, although U.S. Treasury yields had edged up from October 2016 lows of 1.672%, German yields stayed down with markets now pricing in a 100% chance that the European Central Bank will cut its already deeply negative interest rates at its next meeting. European bond markets edged higher although Italian debt suffered some weakness following fresh concerns over the Italian budget; U.K. gilts were little changed; U.S. futures rose alongside European stocks while Asian shares fell. Japan’s 10-year yield fell to a three-year trough of minus 0.215%

In FX, all eyes were on the offshore yuan, which early on stretched the previous day’s slide, and briefly weakened to 7.1382, the lowest since international trading in the Chinese currency began in 2010. But it pulled back to 7.0469 after Beijing’s firmer-than-expected yuan fixing on Tuesday. The safe-haven Japanese yen, touched a seven-month high of 105.520 per dollar before it tumbled by more than 1%.

“China has effectively avoided a confrontation with the U.S. in the currency market, spurring short-covering in dollar-yen,” said Marito Ueda, managing director at FX Prime by GMO Corp. in Tokyo. “The Bank of Japan’s increased buying of T-bills also appears to be contributing to yen selling.”

Elsewhere, the AUD/USD headed for its biggest gain in more than two weeks following the recovery in risk sentiment. Aussie held gains as the Reserve Bank of Australia kept interest rates unchanged. The Swiss franc, another currency sought in times of turmoil, has gained roughly 1% against the dollar this week. It set a six-week peak of 0.9700 franc per dollar. The euro was little changed at $1.1199 Tuesday after climbing the previous three days; the pound gained on signs opponents of a no-deal Brexit were hardening their plans.

In commodities, brent crude oil futures plumbed a seven-month low of $59.07 per barrel as the trade war raised concerns about lower demand for commodities. Brent last traded at $60.41 for a gain of 1% as bargain hunting kicked in. Spot gold advanced to a six-year peak of $1,474.80 an ounce as investors sought the safety of the precious metal. Bitcoin briefly rose above $12,000 overnight before a sudden bout of selling dragged it back down.

JOLTS is the only release today, while Allergan and Disney are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.9% to 2,855.00

STOXX Europe 600 up 0.3% to 370.37

MXAP down 0.8% to 150.77

MXAPJ down 0.8% to 485.77

Nikkei down 0.7% to 20,585.31

Topix down 0.4% to 1,499.23

Hang Seng Index down 0.7% to 25,976.24

Shanghai Composite down 1.6% to 2,777.56

Sensex up 1.1% to 37,088.44

Australia S&P/ASX 200 down 2.4% to 6,478.09

Kospi down 1.5% to 1,917.50

German 10Y yield fell 0.7 bps to -0.523%

Euro unchanged at $1.1203

Italian 10Y yield rose 2.5 bps to 1.215%

Spanish 10Y yield fell 0.7 bps to 0.239%

Brent futures up 0.5% to $60.09/bbl

Gold spot down 0.2% to $1,460.85

U.S. Dollar Index little changed at 97.52

Top Overnight News

China took steps to limit weakness in the yuan, providing some stability to global financial markets in the wake of Monday’s rout, and said it won’t depreciate the currency to be competitive. The moves from the PBOC, which came after the U.S. labeled the country a currency manipulator, helped drive the yuan up a day after it sank the most since 2015

Trump administration formally labeled China a currency manipulator, escalating its trade war with Beijing after the Asian country’s central bank allowed the yuan to fall in retaliation for new U.S. tariffs

Japan MOF official says will keep watching FX with sense of urgency

Opposition Labour Party leader Jeremy Corbyn signaled he will call a vote of no confidence when Parliament returns next month while rebel MP Dominic Grieve said a growing number of his fellow Conservatives will turn against Prime Minister Boris Johnson

Opponents of Boris Johnson’s threat to crash out of the EU without a deal on Oct. 31 are hardening their plans to stop him as the new U.K. prime minister seeks to build support with a series of targeted spending pledges

New Zealand’s central bank is poised to cut rates on Wednesday and may hint it’s not done yet as the economy cools and global peers ease policy

For the fourth time in the last two weeks, Kim Jong Un’s regime shot unidentified projectiles into the waters between the Korean Peninsula and Japan, South Korea’s defense ministry said

Oil reversed a decline as China’s central bank set the yuan fixing stronger than expected, calming investors after the U.S. escalated the trade war by labeling the Asian nation a currency manipulator.

Janet Yellen, Ben Bernanke, Alan Greenspan and Paul Volcker made a joint plea for the central bank to be able to operate without political pressures or the threat of removal of its leaders

The Fed will be leaning closer to reducing interest rates again next month after President Donald Trump ratcheted up his trade war with China and the central bank may even have to cut more steeply than it did last week

China urged Hong Kong citizens to stand up to protesters challenging the government, after a general strike that led to a day of traffic chaos, mob violence, tear gas and flight cancellations. The Hong Kong stocks rout entered its 10th day, the worst such streak since 1984

UBS Group AG plans to charge individual wealth clients for holding more than 500,000 euros ($560,000) in cash, extending the fee policy to more of its rich customers as negative interest rates crunch profits

Asian equity markets resumed the sell-off following Wall St’s worse performance YTD where the S&P 500 posted a 6th consecutive day of losses and the DJIA dropped over 900 points intraday due to the US-China trade tensions and CNY slump, while the US designation of China as a currency manipulator added to the jitters and initially pressured US futures after-hours. ASX 200 (-2.4%) and Nikkei 225 (-0.7%) traded with hefty losses and broad weakness across sectors although gold names remained the exception in Australia, while the Japanese benchmark staged a significant recovery as better than expected Household Spending data and a rebound in USD/JPY softened the blow, with earnings releases also a driver for price action. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (-1.5%) were pressured by the trade tensions after the US labelled China a currency manipulator whilst China confirmed purchases of US agriculture products have been suspended, although markets found some comfort after the PBoC announced to sell CNY 30bln of bills in Hong Kong and set the reference rate within bounds of the perceived 7.00 line in the sand. Finally, 10yr JGBs were choppy with early upside seen due to the wide risk averse tone which boosted prices to a fresh record high and dragged the 10yr yields to below -0.2% which was seen to be the bottom end of BoJ’s target. However, prices have since eased back with 10yr JGBs now lower as stocks recovered from lows and after a mixed 30yr auction, while T-notes have also retreated to below the 130.00 level amid a pullback from the recent surge triggered by the trade tensions which also saw the 3m/10yr yield inversion at its most prominent since the GFC.

Top Asian News

Currency That Gave Birth to Asian Crisis Emerges as Safest Bet

Kirin Picks Up $1.2 Billion Stake in Japan Cosmetics Maker Fancl

Key Gauge of Japan’s Economy Falls to Lowest Since Early 2010

Major European indices have modestly firmed after a mixed to flat open [Euro Stoxx 50 +0.6%], following on from a lacklustre Asia-Pac handover as Wall St. posted its worst performance for the year thus far. Similarly, sectors are in the green though with gains limited and the energy sector unable to breach into positive territory. In terms of individual movers this morning, Vivendi (+7.0%) are in discussions with Tencent for the sale of a 10% stake in Universal Music, with the deal valuing Vinci’s music business at EUR 30bln; since 2018 the Co. has been exploring a partial Universal Music sale with the deal to include the option for a further 10% stake to be purchased in the future. Moving to earnings this morning saw Deutsche Post (+4.3%) update where they beat on Q2 EBIT and their Germany Post & Parcels division posted positive earnings for the first time since Q4 2017. At the other end of the Stoxx spectrum are InterContinental Hotels (-2.4%) as the Co’s revenue did marginally miss on expectations; finally, with nothing fundamentally new from yesterdays pre-market update Metro AG (-6.7%) remain under pressure after further reiteration of comments that Kretinsky’s investment fund will not be increasing their offer for the Co.

Top European News

Opponents of No-Deal Brexit Harden Plans to Block Johnson Threat

Biggest Wealth Fund’s Bid to Dump Big Oil Is Now But a Whimper

Domino’s Pizza Group Shares Rise After 1H Results, CEO Departure

China, Hong Kong Tensions Weigh on InterContinental Hotels

In FX, AUD/NZD – No major surprises from the RBA overnight, but an unexpected boost from trade data revealing a wider than expected and record surplus has helped the Aussie mount a strong recovery from yesterday’s lows with additional support via a Yuan rebound (Usd/Cnh circa 7.0700 vs almost 7.1400 at one stage after a measured/capped 6.9683 Usd/Cny mid-point fix). Aud/Usd is back up near 0.6800 and Aud/Nzd has bounced even further from sub-1.0270 lows towards 1.0400, as the Kiwi also benefited from considerably better than forecast NZ jobs and wage metrics, with Nzd/Usd not far from 0.6600 compared to under 0.6500 at worst on Monday. However, the RBNZ is still seen cutting the OCR by another 25 bp tomorrow and the pair has subsequently eased drifted down to around 0.6550, while Aud/Jpy may lose momentum given mega expiry options at the 72.00 strike (4 bn).

GBP/NOK/SEK – The Pound has also regained composure amidst a broad stabilisation in risk sentiment, with Cable just surpassing yesterday’s best before stalling into the 1.2200 level and Eur/Gbp reversing from 0.9250 to a few pips below 0.9200 even though no deal Brexit risk is arguably rising. Similar story for the Scandi Crowns that are paring losses vs a steady Euro and with the Nok encouraged by a partial revival in oil as well.

JPY/CHF – Conversely, the tentative and formative Tuesday turnaround in financial markets/mood has taken its toll on the Yen especially as Usd/Jpy spikes from near 105.50 lows to just over 107.00 before topping out, while the Franc has retreated against the Dollar and Euro to 0.9750+ and 1.0930 respectively compared to almost 0.9700 and 1.0900.

EUR – In contrast to the Aussie and Kiwi, German factory orders and the construction PMI hardly impacted the single currency even though the former was significantly better than anticipated and the latter lost grip of the 50.0 handle. Instead, Eur/Usd is anchored around 1.1200 and trading more in lock-step with wider Greenback moves as the DXY returns to its 97.500 axis within 97.698-203 parameters, plus the aforementioned Yuan fluctuations on the premise that the Euro may become the default alternative for China if trade wars escalate and US Treasuries are offloaded in response to tariffs and the official declaration that Beijing is a currency manipulator. However, expiries may also be impacting ahead of the NY cut when 1.5 bn roll off between 1.1190-1.1200.

EM – The RBI completes this week’s global Central Bank policy meeting rota, and like the RBNZ is expected to reduce key rates by ¼ point and if confirmed it will be 4 such moves in a row. However, the BoK could make an unscheduled appearance in some shape or form before that as an emergency gathering has been convened in South Korea for 23GMT tonight to ‘discuss’ financial conditions. Usd/Inr currently hovering above 70.7300 and Usd/Krw close to 1215.50.

RBA kept the Cash Rate Target unchanged at 1.00% as expected and stated it is to adjust policy if needed to support the economy and will monitor developments in labour markets closely. Furthermore, the RBA said outlook for the global economy remains reasonable and that there are signs house prices are stabilizing in Sydney and Melbourne, but also noted it will take longer than expected to reach 2% inflation and that wage growth remains subdued with little upward pressure at the moment.

In commodities, WTI and Brent are firmer thus far, though have tested the USD 55.0/bbl and USD 60.0/bbl marks to the downside on several occasions thus far. Newsflow for the complex has been very light thus far with the only notable update from Goldman Sachs who maintain their US oil growth outlook at 1.3mln BPD for 2019, but lowers 2020’s to 1.1mln BPD vs. 1.2mln BPD. Looking ahead, we do have the API weekly report where expectations are for a headline draw of 3mln, we also have the EIA’s Short Term Energy Outlook on the day’s schedule. In terms of metals, gold has dipped this morning as risk sentiment has arguably strengthened but perhaps more appropriately not deteriorated further, while the yellow metal is weaker it is still significantly above the USD 1450/oz handle. As such, copper prices are firmer deriving support from the aforementioned market sentiment.

US Event Calendar

10am: JOLTS Job Openings, est. 7,326, prior 7,323

12pm: Fed’s Bullard Speaks on U.S. Economy in Washington

DB’s Jim Reid concludes the overnight wrap

Thanks for all your well wishes after news of my bike accident filtered through yesterday. Nice to know that so many people are pleased that I’m still alive. Having said that you’d be a pretty strange lot if you felt the opposite. The clip of the incident recorded from a nearby van’s dashcam has gone viral. Maybe not in a Lady Gaga type way but maybe enough to fill a non-league second division football promotion decider. See my Bloomberg header for the link or ask me and I’ll send. What I didn’t say yesterday was what happened next. I was sprawled across the side of the road with my bike by my side in agony and in shock. The driver then moved to go round me and looked like he was driving off. Like a premier league footballer who has theatrically fallen to the ground, and then realises that there’s actually a goal to score, I got up quickly (in agony mind) and blocked him from moving off and shouted at him. He then shouted back at me that he was moving to one side to park the car. He got out and profusely apologised while I went back to being a premier league footballer on the ground. As for my wife, this all happened before she was even awake and after being driven back home I woke her up with a cup of tea with blood all over me and bits of ripped cloth hanging off my clothing. To say I’ve never seen her wake up quicker would be an understatement.

Will August be as much as a write-off as my bike is? It does continue to feel like it’s going to be one of “those” Augusts where markets are unstable and illiquid, and the tranquility of holidays are ruined. As we discussed last week the stakes for this month were already being raised by markets getting ahead of themselves on both central bank action and risk levels versus the current data. Adding on a fresh US tariff announcement from Mr. Trump on Thursday, the Chinese using the yuan as a retaliatory weapon yesterday, and the US Treasury’s official designation of China as a currency manipulator overnight, and we have a combustible situation.

The Treasury’s statement on China being cited as an FX manipulator alleges that there have been “concrete steps to devalue its currency” in recent days. It goes on to say that “the purpose of China’s currency devaluation is to gain an unfair competitive advantage in international trade.” The fact that the designation came under the 1988 act, rather than the 2015 act, actually makes it a bit less disruptive, as the more recent act is the one that automatically starts a new, specific sanction process. Nevertheless, there may be scope for the Commerce Department to treat the designation as a subsidy, which could clear the way for more and higher tariff rates on Chinese goods.

The signal from the move is unambiguously escalatory, and markets are taking the news negatively. However we have rebounded off the Asian lows as markets took heart from the PBoC fixing the daily reference rate for the onshore yuan at 6.9683 (vs. 6.9871 expected).The onshore yuan is actually trading up +0.15% this morning at 7.0399 while the offshore yuan is trading flattish at 7.0649. Asian equity markets pared some of their deep early losses after the PBOC move but are still trading down with Chinese markets leading declines. The CSI (-2.01%), Shanghai Comp (-2.43%) and Shenzhen Comp (-3.03%) are all down over 2%. The Nikkei (-0.64%), Hang Seng (-0.71%) and Kospi (-0.55%) are also making relatively modest declines. The MSCI HK is on course for the 10th successive decline which would be the worst run since 1984 if we close in the red. Amongst G10 currencies, the Japanese yen is down -0.80% while others are trading mixed. Elsewhere, the S&P 500 futures are trading up +0.2% lower overnight, recouping early losses of c. -1.8%. Yields on 10y USTs are +3.5bps this morning. To be honest markets are a bit all over the place this morning so best to check where we are when you’re reading this.

In other news, North Korea has said overnight that it will take “new road” in negotiations with the U.S., saying that Washington and Seoul would “pay a heavy price” if they continued to disregard the regime’s warnings against holding joint military exercises. The statement came less than an hour after North Korea fired a new volley of short-range ballistic missiles into the sea — its fourth such weapons test in two weeks. Elsewhere, President Trump imposed further sanctions on Venezuela, freezing the government’s assets in the US and adding immigration restrictions in a move aimed at stepping up pressure on the regime of Nicolas Maduro.

Back to yesterday now and these overnight moves come after risk assets took a heavy hit. All three US bourses posted their worst days of the year, with declines approaching or above -3% for each index. The biggest move was reserved for the NASDAQ, which fell -3.47%, while the S&P 500 and DOW finished -2.98% and -2.90% respectively. The S&P 500 is now down for 6 straight sessions, which is the longest such run since October last year. It’s also down -5.99% in that time (-6.73% at yesterday’s lows) which is equivalent to a market cap loss of $1.76 trillion; that’s roughly the same as the annual GDP of Canada. The overall US public markets shed -$906.2bn of value just yesterday, which made yesterday’s session the sixth worst day in market history in terms of absolute losses. The NYSE FANG index also tumbled -4.59%, with China-exposed Apple trading down -5.23%, for the index’s worst day since last October. While tech bore the brunt of the pain, the reality was that all sectors closed lower yesterday, with even relative havens like utilities and consumer staples down -1.51% and -2.69%. Credit wasn’t immune either, with US HY cash spreads +36bps wider and +10bps in Europe.

The moves in US equities unsurprisingly coincided with a decent leg up in volatility with the VIX yesterday closing at 23.47 which is the highest level since January. Month to date the VIX is already up +5.6pts which is the biggest move to start a month over the first three days since February 2018 when inverse vol ETFs were blowing up. Meanwhile, Europe also suffered with the moves matching those in the US at the time of the close with the STOXX 600 down -2.31%. Banks (-1.41%) actually held in relatively well considering despite Bunds hitting a new low of -0.516% (-2.0bps). 30 year bunds closed (-1.6bps at -0.012%) below zero for the first time ever. In the UK, gilts reached 0.512% (-3.8bps).

However the big moves in rates were reserved for Treasuries where 2y and 10y yields fell -12.7bps and -11.9bps respectively. The 10-year note has now rallied -33.5bps over the last 4 sessions, the biggest such rally since 2011. That rally at the short end actually meant the 2y10y curve steepened +0.8bps to 13.7bps. However, the other two prominent yield curve metrics, the 3m10y and the Fed’s forward spread, both flattened, by -6.3bps and -14.7bps. That takes the 3m10y to a fresh cyclical low, its lowest since April 2007. It’s also worth noting that breakevens shot lower with 10y breakevens falling -5.6bps and to its lowest level since September 2016. Other safe havens, e.g. the Swiss Franc (+0.88%), Japanese Yen (+0.45%), and gold (+1.51%) also all performed well. Gold is now up +14.04% this year, passing the S&P 500 in terms of YTD gains (+13.48%). The last time that gold beat the S&P on a full-year basis was 2011.

As for Fed expectations we’ve now shifted all the way back to 67bps of cuts being priced in through year-end. Keep in mind that the day after Powell spoke – just 6 days ago – there were only 34bps of cuts priced in. Yesterday, the Fed’s Brainard spoke about the payments system, and when asked about markets she said “I am certainly monitoring developments very closely.” That was corroborated by Kansas City’s George (who dissented against last week’s cut) who said that “markets move quickly. It takes some time to see how that evolves and so the best I think that you can do right now is just to monitor.”

President Trump took to Twitter throughout yesterday’s session to rachet up his confrontational rhetoric. He accused China of having “dropped the price of their currency to an almost a historic low” and said that their “currency manipulation (…) is a major violation.” He also said that “China is intent on continuing to receive the hundreds of Billions of Dollars they have been taking from the U.S. with unfair trade practices and currency manipulation. So one-sided, it should have been stopped many years ago!” There were also unconfirmed reports of Chinese retaliation, with Bloomberg reporting that Chinese agriculture firms have been told to stop buying US soybeans. Hu Xijin, editor of the English-language Chinese paper the Global Times, tweeted that “Chinese enterprises have halted buying US farm products. The Chinese side won’t submit to the US.”

In other news, data played second fiddle however it didn’t go unnoticed that the US non-manufacturing ISM weakened to the lowest level since August 2018, down -1.4pts at 53.7. The sub-indexes weren’t particularly encouraging either, as new orders fell to 54.1, the lowest since August 2016. On the other hand, employment rose to 56.2, right in the middle of the range since 2017. Earlier in the session, the Markit services PMI was revised +0.8pts higher to 52.2. Obviously, these surveys were conducted before the most recent trade escalation, limiting their immediate relevance.

Over in Europe, the final July PMIs were similarly mixed. The euro area aggregate services PMI came in at 53.2, -0.1pt lower from the flash reading, as expected. Italy’s reading was notably better than expected, up +1.2pts to 51.7 versus expectations for a +0.1 increase. Meanwhile, France was also stronger at 52.6 (from 52.2 flash), while Germany was down at 54.5 (-0.9pts from flash).

To the day ahead now, which is a quiet one for data with only June factory orders data due in Germany this morning and then the June JOLTS report scheduled for the US. Away from that we’re due to hear from the Fed’s Bullard at 5pm BST when he speaks on the US economy in Washington. Earnings releases are also due from Walt Disney and Duke Energy.

via ZeroHedge News https://ift.tt/2GP28ai Tyler Durden

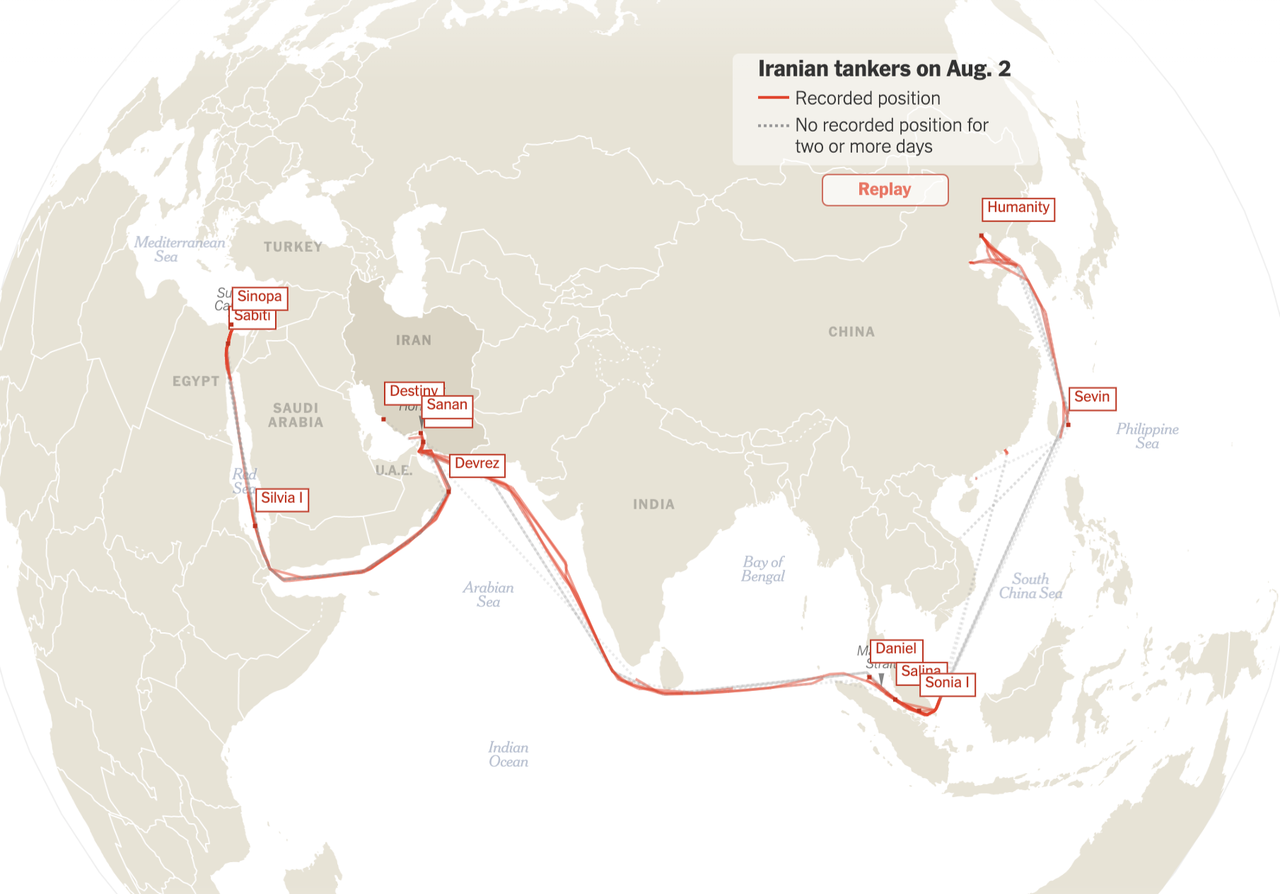

The Trump Administration’s decision to reimpose sanctions on the Iranian oil trade has dramatically reduced Iranian crude exports – but it hasn’t stopped some of the US’s largest economic rivals from accepting shipments of Iranian crude, according to several media investigations. Not only has China continued to import Iranian crude, so have several other Asian and Mediterranean countries, according to data from several tanker tracking services studied by the New York Times and other media organizations.

Per the NYT, in April 2018, before Trump withdrew from the nuclear deal, Iran exported 2.5 million barrels of oil per day. One year later, that figure was at one million. And in June, after the end of the exceptions or waivers, ships in Iranian ports loaded about 500,000 barrels per day, according to Reid I’Anson, an energy economist at Kpler, a company tracking seaborne commodities.

Of course, this fact isn’t lost on the Trump Administration, which, according to the FT, has been tracking the movements of tankers linked to China’s biggest state-run oil company amid signs that the ships are helping to bring in Iranian crude.

China National Petroleum Corp, via its subsidiary, the Bank of Kunlun, has, in recent months, employed a fleet of tankers to move oil from Iran to China.

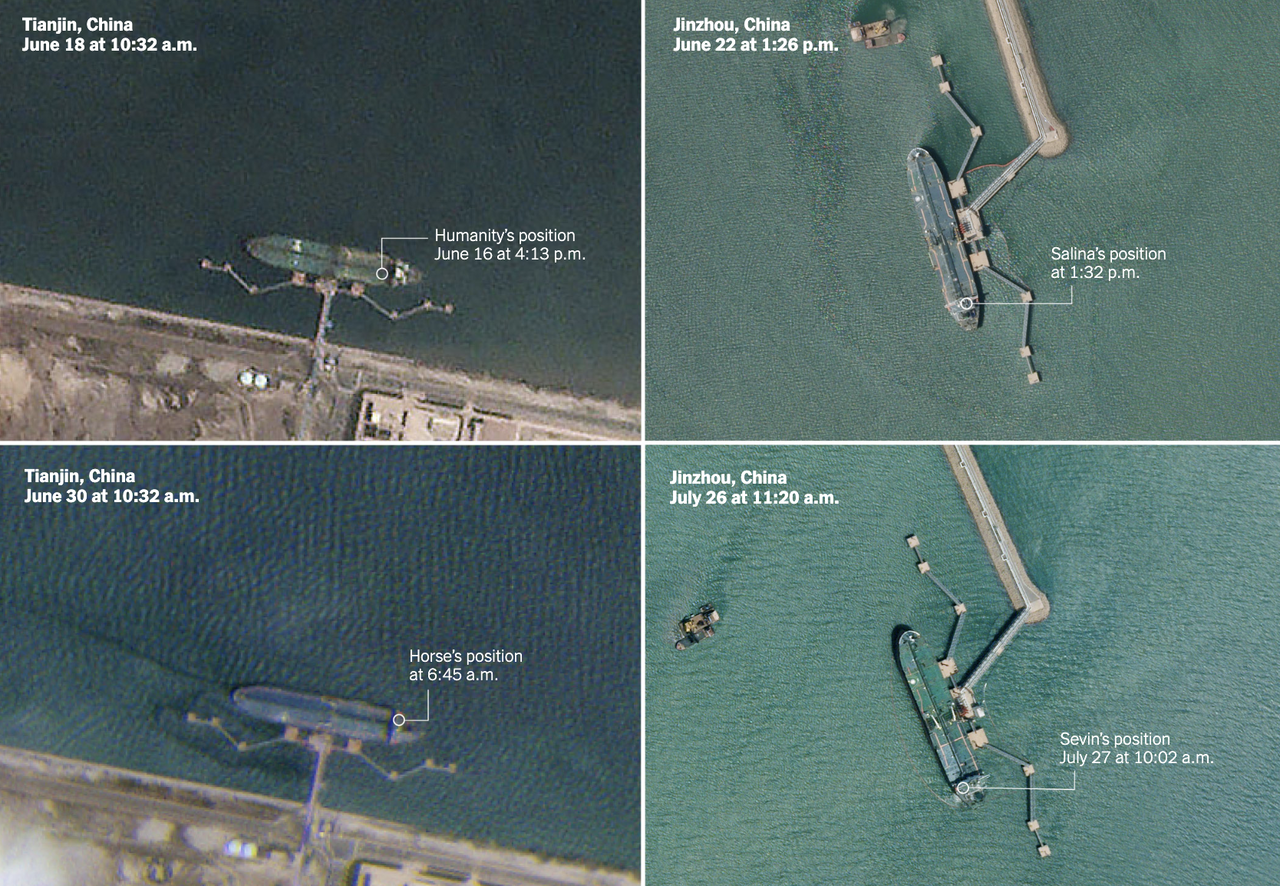

And an NYT visualization of tanker traffic shows the route some of these tankers take while moving oil from Iran to China and elsewhere in the region.

Below are satellite images of some of these tankers docking at Chinese ports.

Last week, the Treasury Department sanctioned Chinese oil trader Zhuhai Zhenrong for buying oil from Iran. The decision was intended to send a message to other Chinese firms, and anyone else buying Iranian oil who also hoped to do business with the US.

“Any entity considering evading our restrictions, particularly related to Iranian petrochemicals, should take this message seriously,” said one official. “We recently sanctioned Zhuhai Zhenrong…for knowingly engaging in a significant transaction for the purchase or acquisition of crude oil from Iran. This action underscores our commitment to enforcement.”

But targeting CNPC would be an especially serious escalation at a time when tensions between the US and China are nearing a breaking point. Even as satellite data and imagery suggest that the tankers linked to Bank of Kunlun are employing tactics including turning off tracking devices and changing their names.

Any US decision to target CNPC would mark a significant escalation given the company’s status as China’s largest oil producer. Its publicly listed arm, PetroChina, has operations in the US and secondary shares listed in New York, in addition to partnerships with international energy companies such as Ineos.

Bank of Kunlun said it was “not involved in the crude oil import business” and denied having “violated any laws or regulations.” But people in Washington familiar with the activities of the bank said it was viewed by the US as a “bad actor.” “Bank of Kunlun has always been the sacrificial lamb for CNPC and, more broadly, for the Chinese government,” said one former senior US intelligence official. “It is a bank that the Chinese government recognises as expendable in some sense.”

And cracking down on the Bank of Kunlun would come with certain risks that might impede the US’s agenda, particularly when it comes to North Korea.

“China is not going to do the US any favours,” said Dennis Wilder, a former top CIA and White House official. “This is the price you pay strategically. You cannot tell China on the one hand to be aligned with you on Iran and North Korea and at the same time decide you’re going to retard or destroy some of their corporations.”

It’s never easy to gauge what exactly is happening in China, or why the CCP Politburo takes the decisions it does. Today, or overnight, is no exception to that. However, one thing that appears certain, but which I don’t see reflected in all the analyses, is that Beijing pushing the value of the renminbi (yuan) down below 7 to the USD in one fell swoop, is a major setback for Xi Jinping and his government.

Yes, China may have given up hope of reaching positive conclusions in its trade talks with the US. And yes, some may think, even in China itself, that devaluing the currency is a tool that can be useful in a potential currency war. But there’s another side to this coin. It’s not even about the value itself, or the change in it, it’s the heavy-handed way it’s executed.

China wants, and desperately needs too, for the yuan to be a force in global financial markets. In very simple terms this is true because if it then wants to buy something, it can simply print the money for it. But only about 1% of global trade today is executed in yuan. That is not nearly enough. It means China needs dollars and euros, all the time. And devaluing the yuan means the country needs even more of those.

You’d almost think: why would you want to do that? What are the long-term prospects for a move like this? You’re telling forex markets that the value of the yuan is not trustworthy, because if Xi or the PBOC decides in the next five minutes that it should go up or down by 10% or 20%, they can do it. The Fed and ECB also have tools to manipulate their currencies (re: interest rates), but none of that magnitude.

The crux of the dilemma probably lies in the Belt and Road Initiative (BRI), which I’ve been saying for years is just China’s way to sell its overcapacity and overproduction abroad. Sure, there may be loftier goals, and surely in the glitzy brochures, but the fact remains that China has tried to be an economic miracle, doing in 10 years what took the US a century, and it never slowed down its growth, at least not voluntarily, even if that might have been a wise move.

Already lately, purchases by Chinese citizens and companies of real estate and businesses abroad have been curtailed, and not a little bit, by Beijing. There’s no better way to convince Chinese people of the miracle’s success than to let them travel the world and spend there, but that, too, may well soon be cut. It kills foreign reserves.

If Beijing could charge participating countries in the Belt and Road Initiative in yuan, and they could pay for the overcapacity’s steel and cement and what not in yuan, that could be a game-changing program for the entire planet. But these countries have no reason to hold yuan, other than the BRI itself. And they, too, were watching the overnight move above 7 and must have thought: let’s be careful now.

And to top it all off, China right now needs for these countries to pay in dollars instead of yuan, because its foreign reserves are shrinking so fast. It’s Catch-22 all the way down. China’s need for dollars goes against everything BRI stands for.

Could the move hurt the US as well? Absolutely. But the long-term view behind the tariffs, and the talks China appears to have lost faith in, is to move the US away from its near all-encompassing addiction to Chinese production, and to move at least some of that production back home. Problem of course is, that is precisely what China’s miracle growth has been built on.

If the US starts bringing production home, who is Beijing going to sell its (over-)production to? Yes, I hear you, to the BRI countries. But there it runs into the currency problems mentioned before. To Europe? The top of that trade route is also behind us. Europe will have to follow the US to an extent, and also bring factories back to the continent (and not just to Germany either).

China could perhaps sell more than it does today to Russia. But that country still does produce a lot of things, and has been forced to be much more self-sufficient due to US and EU sanctions. It’s also a mighty small market compared to 350 million North Americans and 500 million Europeans, who are on average much richer than your average Russian to boot.

There is a way for China to make the yuan more important in global trade (but devaluation is definitely not that way): Beijing could let go of its central and total control over the value of its currency, and let forex markets figure it out. That would give traders -and everyone else- faith in the value. Problem with that is, this is not how central control communist governments think.

Beijing wants both: central total control AND a prominent place in world trade. And it may take them a long time to figure out that is not going to happen, unless of course they first conquer the entire world militarily. That is not an option, at least not for the foreseeable future. Come see me next century.

It wouldn’t be the first time for me to say I can see China retreat into itself, into its own borders and culture and market (1.3 billion people!). If the Communist Party wants to remain in power, and there’s no doubt it does, this may be only possible choice going forward. If growth has indeed left the miracle -as many observers think-, it can implode in very rapid succession. And even if growth hasn’t yet evaporated, it may well very soon. Without the growth, there is no miracle anymore.

And if China can no longer grow its exports, its domestic growth will also become a thing of the past. Domestic consumption can only grow as long as exports do too. Seen from that angle, the problems with trade and the currency look downright ominous. If you need dollars that badly, and you notice that you’re already getting fewer of them, not more, you’re in trouble.

Devaluing your currency may afford you some temporary respite, but it can’t possibly solve your troubles. It can make them much worse though.

I think China has wanted too much too fast, got carried away and forgot to take care of a few potential barriers to its growth, in particular the standing its currency had and still has in the world, and the grinding need for dollars that stems from it. And the Communists have no answer to this problem.

via ZeroHedge News https://ift.tt/2M0hTiR Tyler Durden

Things are already developing fast after last Friday the US timetable for saying in the Intermediate-range Nuclear Forces treaty (INF) ran out, after six months prior President Trump gave an ultimatum to Russia to cease violating its terms or the US would rip up the landmark 1987 arms control treaty. Immediately after, Washington also signaled plans to test a new ballistic missile in the coming weeks, as the AP reported upon the deal’s final collapse.

And now Putin has hit back, saying Monday Russia will be forced to develop land-based short and intermediate range missiles if the US starts doing so, according to state-run RIA. He also is reported to have decried the United States’ exit from the treating as worsening global safety.

Image source: Sputnik

Putin met Monday with members of Russia’s Security Council, focusing on Washington’s unilateral withdrawal from the INF, TASS reports.

“In our opinion, the United States’ actions, which have led to the termination of the Intermediate-Range Nuclear Forces Treaty, will inevitably entail devaluation, undermine the entire global security architecture, including the strategic offensive arms treaty and the Treaty on the Non-Proliferation of Nuclear Weapons,” he told the council, according to a Kremlin press service statement.

“This scenario means the resumption of an unbridled arms race,” Putin emphasized.

But crucially, he also said Russia stands ready to resume full-fledged negotiations with the United States. “Russia deems it necessary to resume without any delay full-fledged negotiations on ensuring strategic stability and security,” he said. “We are ready for this.”

He explained that he’s instructed Russian defense and intelligence services to closely monitor any further US steps toward developing and placing intermediate-and shorter-range missiles.

Moscow’s consistent position has been to blame the US for collapse of the treaty, with both sides over the past couple years frequently pointing the finger at the other for violating its terms, namely a ban on all land-based missiles with a range of between 310 and 3,400 miles.

In the wake of the formal US pullout Friday, NATO Secretary-General Jens Stoltenberg also laid blame on Russia in remarks, saying that NATO members “regret that Russia showed no willingness and took no steps to comply with its international obligations.”

The United States plans to test a new missile in coming weeks that would have been prohibited under a landmark, 32-year-old arms control treaty that the U.S. and Russia ripped up on Friday. — Associated Press

He pledged that the alliance will avoid “a new arms race” with Russia and prevent powers from deploying new nuclear missiles on European soil, which has long been the chief danger that the INF for decades blocked.

But one of the deal’s authors, 88-year old Former Soviet leader Mikhail Gorbachev warned that the world now stands on the brink of a new arms chaos.

“The termination of the treaty will hardly be beneficial for the international community, this move undermines security not only in Europe, but in the whole world,” Gorbachev told Interfax on Friday. “This US move will cause uncertainty and chaotic development of international politics,” he predicted.

via ZeroHedge News https://ift.tt/2YJQLKR Tyler Durden

{kind=link}

{kind=link}

{kind=link}