“Out Of Control” Tesla Vehicles “Accelerate Unexpectedly” China’s National Business Daily Reports Tyler Durden

Thu, 09/10/2020 – 15:45

Just days after an out of control Tesla in China’s Nanchong City left 2 people dead, China’s National Business Daily reported that Tesla vehicles do, in fact, “accelerate unexpectedly” Yicai Global reported in a surprising (and embarrassing) blow to Tesla which has been aggressively expanding in China in recent years.

The report says that there have been “four accidents involving ‘out of control'” Tesla’s in China since June alone. It attributed each of these incidents to “unexpected acceleration” of the vehicles. It was not immediately clear why the media in China, which has been especially hospitable to Elon Musk (in order to gain access to the company’s intellectual property according to the cynics) would suddenly turn hostile to the company whose spontaneous acceleration (and combustion) has long been known. Did China get cold feet and decide it has nothing to gain from a strategic Tesla partnership, and will it focus on developing its own native EV sector instead?

Back on June 16, a Model 3 owner in Nanchang reported that his car suddenly started gaining speed and reached 127 km/hour from a starting speed of 60 km/hour. He said he was unable to slow the vehicle using the brakes and it eventually “sped out of control for eight kilometers until it hit a mound, rolled over and burst into flames.”

Shanghai and Wenzhou provinces also had similar incidents, according to the report.

#Update:- In car Crashed at 3 people have been killed and 8 people have been injured.#Nanchong City, #Sichuan, #China ( local media report)

Recall, just days ago we documented the horrifying aftermath of a Tesla that veered out of control in Nanchong City, China, leaving mangled bodies strewn behind it. The video painted a disturbing scene, showing what appear to be lifeless bodies on the street in the aftermath of the event:

Days later, China’s state owned mouthpiece The Global Times said it was “raising doubts” over Tesla’s functions and quality, according to an article published last Saturday.

The article offered details on last week’s terrifying scene, stating that the car was reportedly being driven by a 51 year old woman and the accident resulted in 2 dead and 6 injured. The possibility of drunk driving and driving under the influence of drugs had been excluded, according to the report. Media outlets claimed that “the car had gone out of control”.

This incident came just hours after Consumer Reports posted a scathing review of Tesla’s Full Self Driving vaporware.

via ZeroHedge News https://ift.tt/35oCnul Tyler Durden

A new study authored by the Germany-based IZA Institute of Labor Economics says the most recent Sturgis Motorcycle Rally, held every summer in South Dakota, was a “superspreading” event.

The non-peer reviewed study was quickly debunked by Governor Kristi Noem and the state’s top health officials.

The study wildly claims the Sturgis event is linked to over 250,000 coronavirus cases across the U.S. and is responsible for an estimated $12.2 billion in public health costs.

In a press release on Tuesday, Gov. Noem issued a harsh rebuke of the study and media reporting:

“This report isn’t science; it’s fiction. Under the guise of academic research, this report is nothing short of an attack on those who exercised their personal freedom to attend Sturgis. Predictably, some in the media breathlessly report on this non-peer reviewed model, built on incredibly faulty assumptions that do not reflect the actual facts and data here in South Dakota.“

“At one point, academic modeling also told us that South Dakota would have 10,000 COVID patients in the hospital at our peak. Today, we have less than 70. I look forward to good journalists, credible academics, and honest citizens repudiating this nonsense.”

South Dakota took a balanced approach to fighting #COVID19. Many in the media disagree with our respect for freedom. They’ll continue to attack us for the path that we’ve taken, but South Dakota is proof that freedom works, even in the face of a global pandemic. pic.twitter.com/1vKU3R6Rmk

The study’s methodology included tracking “anonymized cellphone data” of the nearly half a million attendees’ movements while traveling to, from and around the event.

Researchers then looked at COVID-19 case trends across the country following the popular bike week — apparently finding case increases of over 10% in counties nationwide that had people traveling to Sturgis according to their cellphone data.

But despite the study’s colorful findings, correlation does not imply causation.

South Dakota Governor Kristi Noem and public health officials were quick to debunk the study’s wild claims about Sturgis.

State epidemiologist Joshua Clayton reminded the public that the study was not peer reviewed and added it also failed to take into account several external factors, including the opening of schools in the month of August.

Secretary of Health Kim Malsam-Rysdon questioned the study’s use of cellphone data to track case trends, saying “I don’t think we’ve seen that kind of link proven before.”

South Dakota’s Department of Health has reportedly tracked 124 COVID-19 cases ‘directly linked’ to Sturgis within its state; however, there’s been no indication of how contagious those people actually are since positive test results reported do not disclose their levels of viral load.

How many people actually suffered a death attributed to COVID-19 following Sturgis?

One.

For months, governments and media have been peddling fear of so-called “superspreaders” and superspreading events. Outdoor holiday gatherings, beaches, sporting events and most recently, the Republican National Convention, have all been branded as such without any real evidence to back up the claims.

Sturgis has now become the latest in a long line of dead end COVID canards.

via ZeroHedge News https://ift.tt/2Ztwb0u Tyler Durden

Adam Schiff’s Latest Russia ‘Whistleblower’ Investigated By House Intel, Inspector General, & Was Fired From DHS For Surveilling Press Tyler Durden

Thu, 09/10/2020 – 15:04

On Wednesday, Rep. Adam Schiff (D-CA) has unveiled a new whistleblower – former DHS intelligence official Brian Murphy, who claims that Trump administration officials at the White House and Department of Homeland Security suppressed intelligence reports that Russia is interfering in the 2020 election, and ‘altered intelligence’ related to comments made by President Trump.

“We’ve received a whistleblower complaint alleging DHS suppressed intel reports on Russian election interference, altered intel to match false Trump claims and made false statements to Congress,” Schiff tweeted, adding “We will investigate.”

We’ve received a whistleblower complaint alleging DHS suppressed intel reports on Russian election interference, altered intel to match false Trump claims and made false statements to Congress.

Except, Schiff did investigate – his whistleblower – for allegedly ‘providing incomplete and potentially misleading information to Committee staff,’ according to the New York Times.

Not only that, Murphy was fired from his job as the head of DHS’s intelligence branch and reassigned after he compiled reports about protesters and journalists reporting on the Trump administration’s response to the riots in Portland, Oregon in July.

Brian Murphy, the acting under secretary for intelligence and analysis, was reassigned to a new position in the department after his office disseminated to the law enforcement community “open-source intelligence reports” containing Twitter posts of journalists, noting they had published leaked unclassified documents, according to an administration official familiar with the matter. It was not clear what Mr. Murphy’s new position would be. –New York Times

As a result of Murphy’s actions, acting DHS Secretary Chad Wolf asked the Inspector General to investigate.

Here’s the New York Times article on Murphy when he was reassigned… EVEN Democrats and media know he’s a liar.

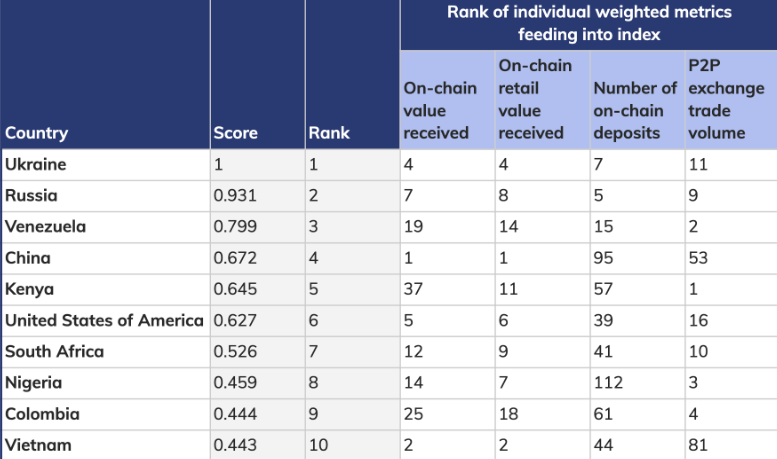

Recent data published by Chainalysis revealed a surprising first place for Ukraine in the Global Crypto Adoption Index 2020, followed by Russia and Venezuela.

The index looks at three on-chain metrics: the total value of on-chain crypto transactions weighted by purchasing power per capita, or PPP, the value of on-chain retail transfers weighted by PPP, and the number of on-chain crypto deposits weighted by the number of internet users.

The index also factors in the volume of trades made on peer-to-peer crypto exchanges weighted by both the number of internet users and PPP.

The report shows uneven levels of development across the crypto sectors of many nations, with the index’s per capita weighting ranking China poorly by number of on-chain deposits and P2P trade due to its large population — dragging the country down to fourth overall despite China dominating on-chain rankings by both retail and total value.

By contrast, the two top-performing nations by P2P exchange volume, Kenya and Venezuela, both rank in the top five overall despite failing to rank in the top ten by any other metric.

However, the emphasis on P2P volume may overlook the establishment of local regulated exchanges as an indicator of cryptocurrency adoption and skew the results in favor of developing countries that lack a robust financial sector, likely contributing to the United States ranking below Kenya despite outperforming the African nation in three of the four criteria.

Chainalysis describes Venezuela as an “excellent example” of the forces that drive cryptocurrency adoption within emerging countries, highlighting its use among ordinary Venezuelans as a means to mitigate economic instability:

Our data shows that Venezuelans use cryptocurrency more when the country’s native fiat currency is losing value to inflation, suggesting that Venezuelans turn to cryptocurrency to preserve savings they may otherwise lose.

The report offers some unexpected insights, with Vietnam ranking second for the value of both retail and all on-chain transactions despite the local government’s early attempts to crack down on cryptocurrency.

No western European nations rank among Chainalysis’ list of the top ten countries by crypto adoption.

via ZeroHedge News https://ift.tt/3k6qQ73 Tyler Durden

Is Powell Sending A Message: The Fed Bought No Bond ETFs In The Entire Month Of August Tyler Durden

Thu, 09/10/2020 – 14:26

For much of the past six months, the biggest story was the Fed’s Blackrock-mediated purchases of corporate bonds, either in the primary or secondary market, or via ETFs. As a reminder, while the Fed pre-announced its intention to purchase up to $750BN in corporate bond (including certain fallen-angel junk bonds) in March, it started purchasing bonds in May, and bond ETFs in June (among which such mainstays as LQD and HYG). By directly entering the corporate bond market – something none of his predecessors dared to do even at the depths of the financial crisis – Powell created what many believe, as GLJ’s Gordon Johnson writes, “the biggest corporate bond bubble, and junk bond bubble, in history (and that all happened before the Fed even started buying).” And, as expected, bond prices, stocks, and ETFs all surged – completely disconnected from fundamentals – while yields plunged, as everyone was trying to front-run the Fed’s pending massive purchases. In other words, by jawboning alone, the Fed accomplished its handiwork.

Yet something odd happened in the month of August when during the peak summer doldrums it was SoftBank’s turn to steal the spotlight with its now infamous gamma meltup – the Fed did not buy a single ETF.

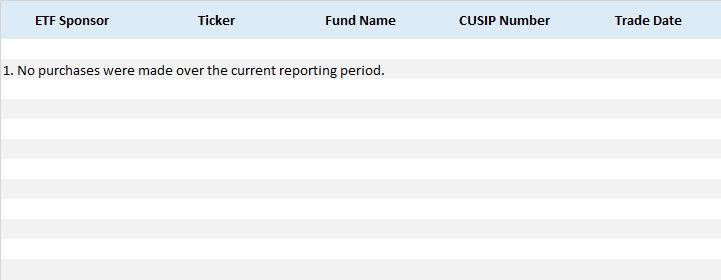

Fast forward one month, to the Fed’s update of its corporate bond and ETF holdings as of Aug 31 and which was published on Tuesday, where we find that the number of ETF shares held is unchanged for the entire month, while the market value of its ETF holdings has actually dipped by $64 million to $8.671 billion from $8.736 billion.

Flipping to the trade level data for the month of August is even more clear: as the Fed itself states, “No purchases were made over the current reporting period.”

Looking at the bond level data showed a similar picture: the Fed bought just $421 million par value ($456 million purchase value) of bonds between July 31 and Aug 28. Notably, unlike in July when Blackrock purchased four Apple bond CUSIPS, in August the Fed stayed away from the world’s largest company. Perhaps it had enough of being publicly shamed for indirectly funding Apple’s record stock buyback?

After the modest August purchase, the Fed’s total corporate bond holdings rose by $435 million from $3.553 billion to $3.988 billion, an amount which also included the redemptions of several issues by NiSource, FLIR Systems, Digital Realty Trust and Anheuser-Busch.

And when combined with its $8.671 billion in ETF hodlings, this means that as of August 31, the Fed owned just $12.659 billion in bonds and ETFs.

Why is this notable?

Because as Gordon Johnson notes, not only is the total amount of actual purchases well below the $44.7 billion amount shown on the Fed’s weekly H.4.1 statement under the Corporate Credit Facilities line item (as a reminder, the remaining $32.1bn in the SPV balance sheet include “amounts related to Treasury contributions to the facility” to ensure that the Fed does not suffer actual losses on its purchases), but more importantly, the $12.66BN of bond purchases to date is a long way away from the $750BN figure the Fed initially said it was targeting, and, as Johnson says “is currently in market participants psyche (i.e., 1.8% of what many continue to think the Fed will spend)”.

What are the implications?

The fact that the Fed effectively stopped supporting the corporate bond market during August, and did not buy a single bond ETF last month, “seems to us to be a stark, yet surreptitious, shift in Fed policy stance” according to Gordon Johnson.

Furthermore, it seems to have gone completely under the radar – i.e., given all the brouhaha surrounding the Fed’s jawboning about massive bond purchases, we would argue, at best, this is pocket change. When the market figures out the “Fed put” is no longer in place, with the Fed’s bond ETF holdings actually falling by -$64mn in August, the willingness to buy stocks at “ridiculous” valuations may quickly abate.

Could it be that the Fed is starting to telegraph to the market that it moved too far, too fast? As Wolf Richter writes, “Jerome Powell has explained this many times – that the Fed has succeeded in achieving its objective of creating loose credit market conditions. It has in fact succeeded in blowing this bubble in the shortest amount of time, and the Fed itself is perhaps stunned by the magnitude of the bubble and its own success.”

As Johnson concludes, it suddenly seems “that for now the Fed does NOT have “your back” if you’re buying overvalued companies that lose money with no end in sight” and furthermore with CPI starting to run hot “it seems the Fed may be seeing the “fruits” of its recent jawboning (i.e., creating a bond bubble and bailing out asset holders during the worst economy in our lifetime, despite not taking any real action) souring a bit.”

via ZeroHedge News https://ift.tt/32fBYs4 Tyler Durden

Most people are focused on the highly politicized and polarized Presidential race.

The contest for control of the Senate may have even larger implications for markets and the investment community. Tax policy, judicial and executive branch confirmations, and the future of the Senate rules on Cloture (the only procedure by which the Senate can vote to place a time limit on consideration of a bill or other matter, and thereby overcome a filibuster) are all up for grabs.

Based on our conversations with campaigns and pollsters, we wanted to share our current views on the state of the various Senate races.

We believe that there is a very real chance that we will not know which party controls the Senate until January 5th. That is the date of the Georgia special election runoff should no candidate get more than 50% of the vote. Given that there are 21 candidates running in Georgia for the seat, it is very unlikely that any candidate will garner more than 50% of the vote. Moreover, as control of the Senate may come down to just one seat, all eyes may be on Georgia this winter. Following is how we could get there.

The Landscape:

There are currently 53 Republican Senators and 47 Senators who caucus Democratic (including Bernie Sanders and Angus King who are registered Independents but caucus with the Democrats).

Alabama’s Democratic Senator Doug Jones, who won in a special election to fill the seat vacated by Jeff Sessions, is unlikely to be re-elected. The 2020 Republican Senate candidate is more mainstream than the controversial Roy Moore and it is expected that the GOP will take back this seat.

That would put the Republican count at 54. Therefore, for Democrats to reclaim majority control of the Senate, they need to win five seats currently held by Republicans (four seats if Biden/Harris win, because in an evenly divided Senate the tie breaking vote goes to the Vice President). They must also not lose any seats in addition to Alabama.

If the Democrats do regain the Senate there will be two primary reasons:

1) Trump’s language and approach has offended enough of the key voters (such as suburban women) who supported these Republican Senators in 2014 but that now feel they can now no longer do so because they believe that the Republican controlled Senate has “enabled” President Trump; and

2) The Democrats are running strong candidates in many of the most important races.

Where the Republicans are vulnerable:

1) Maine: Senator Susan Collins received over 68% of the vote in 2014. However, that tally included over 30% from Democrats and over 50% of the Independent vote. Given her vote confirming the Supreme Court appointment of Brett Kavanaugh and for her endorsement of the 2017 tax bill, it is unlikely she will garner much Democratic support in 2020. Further, there are signs that the demographics of Maine are changing as more progressives move in from out of state to Portland, ME. RealClearPolitics average of polls have her opponent, state House Speaker Sara Gideon, up by 3% to 5%. These polls, however, under sample voters in Maine’s 2nd Congressional District which is “Trump Country”. More accurate polling seems to suggest this a is a toss-up race that will go down to the wire.

2) North Carolina: Senator Thom Tillis has a tough battle in this State. The President is in a tight race there with the polls having him even to down 2 points to Biden. In some other states, the Republican Senate candidate can hope for an Election Day boost from the President. Tillis faces two problems which could limit the Presidential bump: (1) the Trump coat-tail may not benefit him as much as in other states because much of the Trump base is lukewarm on the more moderate/centrist Tillis; and (2) his opponent, Cal Cunningham, is a strong candidate who has outraised and outspent Tillis 2 to 1.

3) Colorado: Former Governor John Hickenlooper leads incumbent Senator Cory Gardner by 9%. This race has tightened up somewhat after Hickenlooper was found guilty by the Colorado Independent Ethics Commissions of a gift violation involving the use of a Maserati and free travel aboard private planes. Despite that, Independents seem to be leaning towards the former Governor. The demographics of Colorado have also been trending Democratic over the past few election cycles.

4) Arizona: Incumbent Martha McSally is trailing by over 11% against former Astronaut and Navy Captain Mark Kelly. He is married to former Rep. Gabby Giffords, who was seriously injured in a 2011 assassination attempt when she was a member of the House. He is a very strong candidate. He was a registered Independent until 2018, so appeals to swing voters and is centrist enough to appeal to Republicans and Independents who don’t identify with Trump. McSally’s only real hope is that there were 250,000 Trump voters who didn’t vote in the 2018 midterms when McSally lost to now Senator Kyrsten Sinema. Sinema won by 60,000 votes or 2% (McSally was appointed to her current Senate seat by Governor Ducey following Senator John McCain’s death). If enough of those 250,000 “Trump voters” from 2016 (who did not vote in the mid-terms) return to the ballot and vote for Trump AND McSally, then McSally has an outside chance.

5) Iowa: Incumbent Senator Joni Ernst is under pressure. Ernst won in 2014 with an 8.5% margin, but now is polling dead even with the Democratic candidate, businesswoman Theresa Greenfield. The trade war with China has been particularly hard on agricultural exports. One of every six Iowans has agricultural related employment and agriculture makes up over 27% of Iowa’s economy. The cuts in exports have hurt Trump’s and the Republicans’ image in Iowa. Trump is doing a little better than Ernst in Iowa at +2% so the hope for Republicans is that Ernst can ride on the President’s coat tails.

6) Montana: Republican incumbent Steve Daines won by 18% in 2014. This time, however, the Democrats are running a very strong candidate, Montana’s current Governor, Steve Bullock. In 2016, Bullock was re-elected as Governor on the same day in the same state that Trump won by 20%. Bullock had been leading in the Senatorial polls for many months. In July, however, the Libertarian Party of Montana agreed (at Senator Rand Paul’s urging) to not to run a candidate in the Senate Race. This is important because in 2018, Democratic Senator Tester beat the Republican candidate, Matt Rosendale, by just 17,000 votes or 3%. That is about the same number of votes that the Libertarian candidate, Rick Breckinridge received in 2018. Consequently, not having a Libertarian candidate on the ballot could make the difference this year. Since this news, Daines has now been leading in the polls for over a month by 2% to 6%. Bullock, however, cannot be counted out because of his popularity in the state.

7) Georgia 1: Republican Incumbent Senator Perdue is leading challenger Jon Ossoff in the polls by 4%. This places him ahead of Trump who is leading in Georgia polls at 1-2%. Perdue should win again but he is still in a very competitive race and will have to fight this race out to the end.

8) Georgia 2: The less likely outcome will come from the Special Senate election in Georgia that was necessitated by the health-related early departure of Senator Jonny Isakson. The governor appointed Kelly Loeffler earlier this year, but there now must be a special election on November 3rd. There are 21 candidates on the ballot but the four leading ones are: Kelly Loeffler (R) Doug Collins (R) Matt Lieberman (D) Rafael Warnock (D)

The most recent polls have Loeffler at 26%, Collins at 21%, Warnock at 15% and Lieberman at 13%. If that is how the voting ends, then the runoff on January 5th will be between two Republicans. As important as that runoff will be to both campaigns, that outcome would not mean that the whole country would be waiting until January 5th to determine control of the Senate. The situation in Georgia, however, is fluid and could change significantly at any time. Stacey Abrams has endorsed Warnock and there is now pressure being but on Lieberman to drop out and not “divide the Democratic vote.”

9) South Carolina: In most polls the Republican incumbent, Lindsay Graham, is up by 5%-10%, but the race may be closer than the polls suggest. Indeed, a recent Quinnipiac poll has the two candidates in a dead heat. The Graham campaign thinks that this poll under samples likely Republican voters, but they are not being complacent and taking anything for granted. Harrison has been a prolific fundraiser, but Graham still has a financial advantage, with $15m cash on hand (vs Harrison’s $10.2m).

10) Kansas: Had the very controversial candidate, Kris Kobach, won the Republican primary last month, he very likely would have lost in the general election (as he did in the gubernatorial race in 2018). However, the more “mainstream” candidate Roger Marshall won the primary so it is likely that Kansas will do in 2020 what it has been doing consistently for every election since 1934, send a Republican to the Senate.

Where the Democrats are vulnerable:

In addition to Alabama, the Democrats are vulnerable in two states: Michigan and Minnesota.

1) Michigan: Most polls have the Democratic incumbent, Gary Peters, up by 4-5%. He won the state in 2014 by over 13%. However, the Trafalgar poll has the Republican challenger, John James, up by 1% and the September Terrance Group poll shows a dead heat. James is an African American who went to West Point and was an Apache pilot. Since the Army, James has run operations at his family’s logistics company so scores highly on the “pro-business” front. While his polling performance is encouraging for Republicans, most people in the state think that the incumbent, Peters, will eke out a small victory. If, however, Trump puts time, money and attention into Michigan and starts to surge in the polls, there is a chance that James could squeak by on the President’s coattails.

2) Minnesota: The Democratic incumbent, Tina Smith, currently leads by 5% but a recent poll taken in September has her up by as much as 8%. Minnesota has been a very reliable Democratic state. It is the only state in the union that has not gone for a Republican at the presidential level since Nixon in 1972. The backlash against the “defund the police” narrative has been especially strong, potentially because the George Floyd incident occurred in this state and many don’t like the perceived lawlessness. After the RNC convention, six mayors from the state’s “Iron Range” region, which has historically been a Democratic stronghold, have come out in support of Trump. If this “law and order” narrative takes hold and gains momentum in Minnesota, the Republican challenger, former Rep. Jason Lewis, could have an outside chance.

So what does this all mean?

There will be many twists and turns before November 3rd but, this is how we think things could end up: If one assumes that:

Hickenlooper (D) wins Colorado

Kelly (D) wins Arizona

Cunningham (D) wins North Carolina

and,

Tubberville (R) wins Alabama

Graham (R) retains South Carolina

Perdue (R) holds off Ossoff in Georgia

Loeffler (R) or Collins (R) wins Georgia

Daines (R) holds off Bullock in Montana, and

Ernst (R) holds off Greenfield in Iowa,

Then:

The control of the Senate comes down to Susan Collins (R) in Maine.

If she wins, the Republicans have 51 seats, so will control the Senate no matter who wins the presidential race. If she loses, the Senate would be at 50/50, so whichever party wins the presidential election, will gain control of the Senate.

If the Democrats can pull off an upset in Montana, Iowa or Georgia, their chances of control are very high.

However, if the Republicans can pull off an upset in Michigan or Minnesota, it becomes very hard for them to lose control of the Senate.

In the event that there are 50 Republican Senators after the November election and Biden/Harris have won, then Georgia will decide control of the Senate.

via ZeroHedge News https://ift.tt/3bIlKLo Tyler Durden

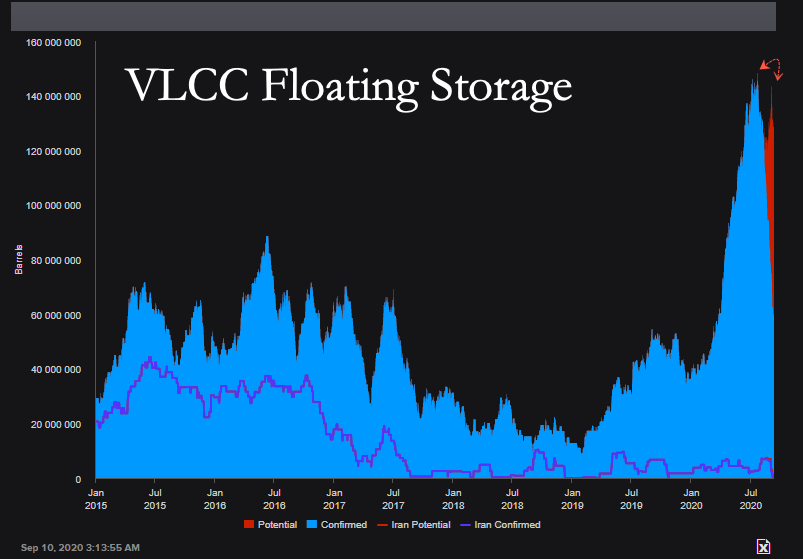

“It’s Happening Again” – Traders Store Oil At Sea As Recovery Falters Tyler Durden

Thu, 09/10/2020 – 13:50

Crude prices slid Thursday as the stalled global economic recovery from the virus pandemic triggers a “second wave” of demand fears and sparks renewed interest in floating storage as the oil market flips bearish.

Reuters said a “fresh build-up of global oil supplies, pushing traders including Trafigura to book tankers to store millions of barrels of crude oil and refined fuels at sea again.”

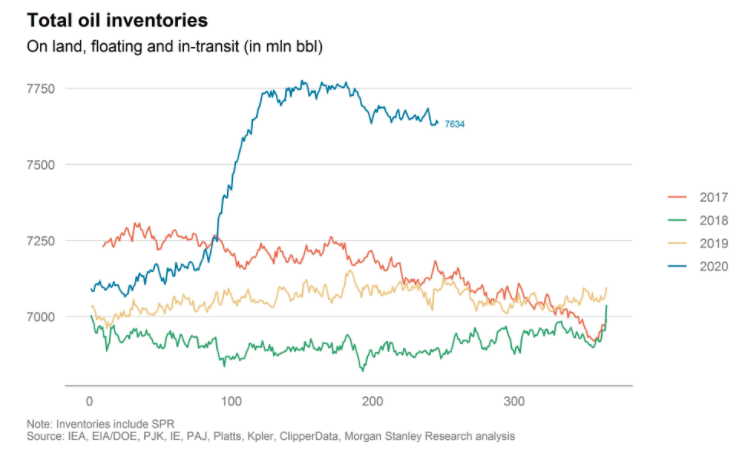

Floating storage, onboard crude tankers, comes as traditional onshore storage nears capacity as supply outpaces demand.

Total Oil Inventories

Refinitiv vessel data shows trading house Trafigura has recently chartered at least five crude tankers, each capable of 2 million barrels of oil.

The inventory build up, driving up demand for floating storage comes as OPEC+ recently trimmed supply curbs from earlier this year on expectations demand would improve. Though with the peak summer driving season in the US now over, demand woes and oversupplied markets are pressuring crude and crude product prices.

Very large crude-oil carrier (VLCC) storage has started to rise once again.

“Despite the recent slide in oil prices, we think that the OPEC+ leadership will continue to direct its efforts towards securing better compliance rather than pushing for deeper cuts at this stage,” RBC analysts said.

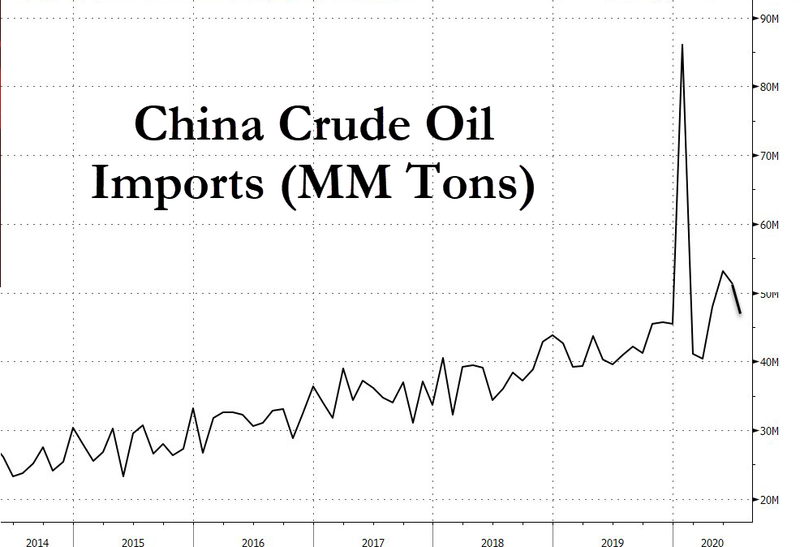

Another catalyst for the bearish tilt in crude markets is that China’s oil imports are likely to subside as independent refineries have reached maximum annual oil import quotas.

Reuters notes, in a separate report, that other top commodity traders are booking tankers to store crude products at sea, including diesel and gasoline.

Refinitiv vessel data also shows Vitol, Litasco, and Glencor have been booking tankers in the last several days to store diesel for the next three months.

“The market is soft and bearish, and floating storage is returning again,” a market source told Reuters.

Morgan Stanley analyst Martijn Rats said in a note that “it is increasingly clear that market fundamentals are not improving as quickly as expected, particularly on the demand side.”

A faltering global economic recovery, combine with oversupplied crude markets and waning demand, is weighing down November Brent crude contracts, down 15% in the last seven sessions.

Americans may finally be waking up, even minimally. A majority of those living in the United States believe that the government is corrupt and unaccountable.

This brings to mind a quote:

“Power tends to corrupt, and absolute power corrupts absolutely.”

-John Dahlberg Acton

That means that anytime you hand power to anyone, their morality will decrease as the desire to control others increases. No one cedes power willingly either. If we have learned anything from 2020 it’s that those in power or authority figures are not in it for us, but themselves.

Seventy-three percent of Americans say that elected officials do not face “serious consequences” for misconduct, according to a new Pew Research Centerpoll.

A closer look reveals that a mere 21 percent of those leaning Democrat and 32 percent of Republicans believe there is some basic justice for delinquent politicians.

This is not the only issue where US liberals and conservatives almost reach a consensus.

Seventy percent of US citizens don’t think the government is “open and transparent,” while 60 percent of both Republicans and Democrats believe that judges aren’t free from the influence of parties and politicians.

However, Americans still think reform is the answer. It’s not. Not allowing others to have power over you is the answer. That means once the system falls (and it will) we replace it with nothing. No more masters and no more slaves. The good news though, is that some Americans are at least finally understanding that corruption is inevitable in every government under any “established rule” over others.

It’s time to figure it out. In fact, it’s past time. We all need to stand up, unite, and stop allowing other people to steal from us, dictate to us, start wars, and use order followers to enforce the “laws.” We don’t need them. They need us. Once we withdraw our consent to be governed (which means controlled) it’s over. We are not their property or their slaves. We all need to realize this quickly.

via ZeroHedge News https://ift.tt/3bMGbqv Tyler Durden

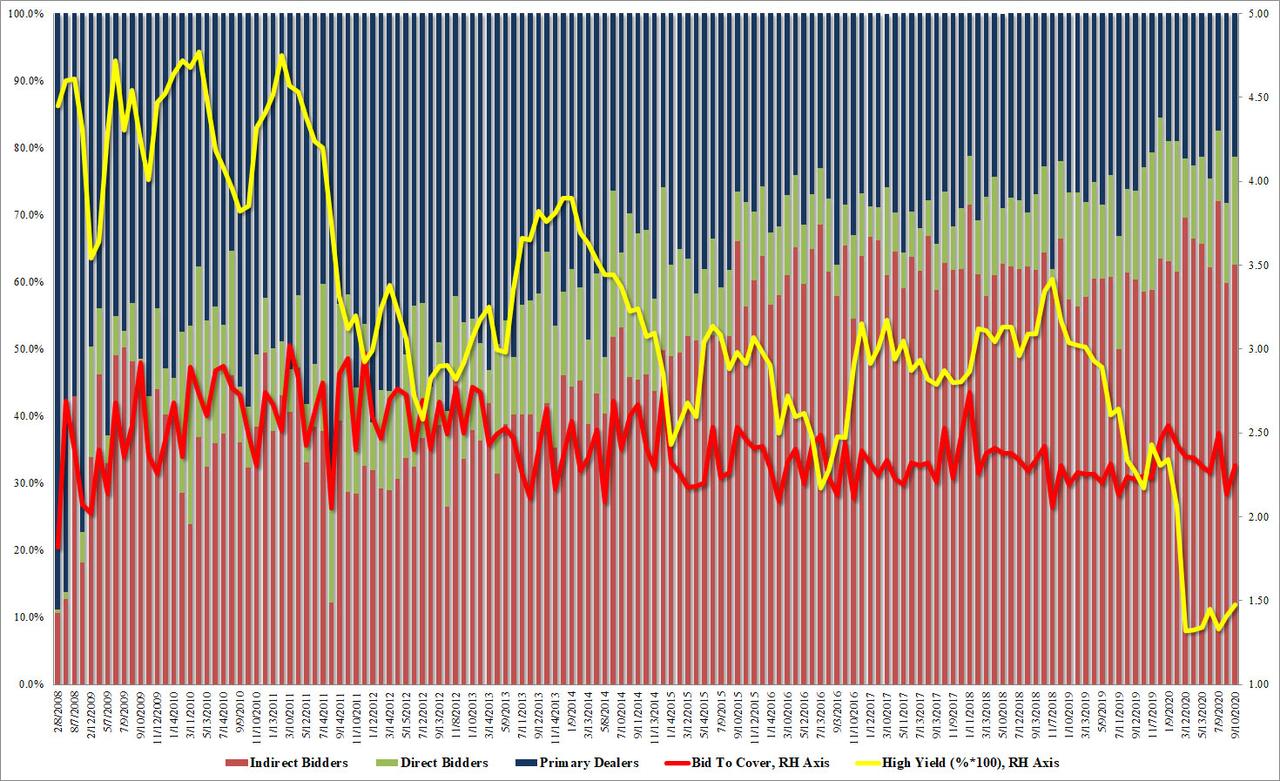

Solid Demand For 30Y Treasury Auction Sends Bond Yields Lower Tyler Durden

Thu, 09/10/2020 – 13:14

After an average 3Y auction, and a subpar 10Y reopening yesterday, moments ago the Treasury completed its sale of coupon bonds for the week when it sold $23 billion (down from $26 billion last month) at a high yield of 1.473%, which was the highest yield on the 30Y since February, although stopping through the When Issued of 1.476% by 0.3bps, demand was stronger than in recent auctions at least superficially.

The Bid To Cover of 2.31 was above the August 2.14 which was the lowest since last August, and was right on top of the 6 auction average of 2.31.

The internals were a tad weak, with Indirects taking down 62.6%m which while above the 59.8% last month was below the recent average of 66.0%. And with Directs taking down 16.1%, the highest since February, Dealers were left with 21.3% just below the 22.6% six auction average.

Overall, another average auction although the lack of a tail was taken as positive by the market, and helped the 10Y yield dip from an unchanged, 0.70% by 1bp to 0.69%, a move which makes sense as stocks are taking on water.

via ZeroHedge News https://ift.tt/3hcLZKY Tyler Durden

Private Equity Firms Use Junk Loans To Fund Dividend Payments Tyler Durden

Thu, 09/10/2020 – 13:09

Back in March, in the aftermath of the Fed’s announcement it would start buying corporate investment grade and some high-rated junk bonds, we pointed out that the bond market had torn in two, with the part of it that was explicitly backstopped by the Fed trading at (or above) par regardless of fundamentals, while “deep junk” issues tumbled as investors shied away from any fixed income issue that did not have a friendly Fed backstop. Since then this decoupling has persisted, especially for issues in the hard hit energy and retail sectors, making capital raising next to impossible for the issuer companies many of which were private equity portfolio companies. Needless to say, this made debt-funded shareholder friendly actions next to impossible.

Yet half a year later, private equity firms have found a loophole: instead of selling junk bonds for which there is still little demand, they are instructing portfolio companies to sell secured loans and use the proceeds to fund sponsor dividends in what Bloomberg called a new round of “aggressive deals.”

Taking advantage of thin supply in the deep junk space, five deals are currently being marketed fund shareholder dividends, accounting for half of this week’s volume, and the most in a week since 2017, according to Bloomberg data. Sponsors are taking advantage of rising loan prices in the secondary market despite continued weeks of outflows.

Of course, with corporate leverage already at record highs, private equity firms are merely piling on even more debt onto their portfolio companies as yield-starved creditors look for sound investments.

Some examples:

Snack maker Shearer’s Foods debt to EBITDA will rise above 7x after a $985 million first-lien loan rated B- is used by the company’s PE investor, Ontario Teachers’ Pension Plan, to recoup most of its initial investment in the business.

TPG-owned cable provider RCN Grande Wave will see its leverage rise to a similar level, S&P said, after borrowing $1.19 billion in term loans and $2.25 billion in bonds. Some of those are rated CCC+.

For those wondering if the new loans continue the tradition of issuing covenant-lite debt, Bloomberg has the answer: “in some cases, sponsors are also asking investors to loosen a key protection that allows the debt to stay in place even if the company is sold to another firm. Power generator Linden, is one such example, marketing loans with exemptions to the change of control provision.“

KKR already successfully circumvented the 101 change in control put earlier this this summer, when the private equity giant squeezed a $560 million dividend in July from Epicor Software through a $2.75 billion loan, only to sell the company to Clayton, Dubilier & Rice the next month.

Continuing this trend, we wonder how long until the first third-lien, PIK loan dividend deal hits the market.

Stepping away from the leveraged loan market, the euphoria in the corporate bond market continues unabated, and on Wednesday, new IG issuance totaled $21.3bn across 16 deals, bringing the weekly total to $41.7bn – in line with the $44.2bn average from the first two days after Labor Day in 2019 and 2018, and a record $1,506.6BN YTD – 65% ahead of last year’s pace.

via ZeroHedge News https://ift.tt/2Zqq50E Tyler Durden