Accused pedophile Jeffrey Epstein’s Gratitude America Ltd. foundation somehow kept getting stock allocations in more than 40 underwritten offerings by Morgan Stanley, according to Barron’s.

Morgan Stanley led all of the offerings in question and was the sole underwriter on a dozen of them. They included IPOs of Roku and secondary offerings from companies like Tribune Media and Go Daddy.

Epstein plead guilty in 2008 to soliciting child prostitutes and recently claimed assets of more than $500 million. Of that, he claimed $113 million in equities. Despite pleading not guilty, he has not been granted bail.

This year, Deutsche Bank dropped Epstein as a client of its private wealth division after he brought his money there in 2013. This followed having his money with JP Morgan Chase for years. But after the Miami Herald ran a series of articles last year about the plea deal Epstein took in 2008, the bank decided to end its relationship with Epstein.

That’s not to say that Deutsche Bank probably couldn’t use the wealth management business back at a time like this. But we digress…

Epstein’s foundation got a cut in numerous deals, including US Foods Holding and Norwegian Cruise Line holdings. Morgan Stanley acted as lead underwriter for both offerings. The foundation also got shares in Chinese delivery company ZTO Express.

Morgan Stanley declined to comment.

Epstein’s foundation began in 2017 with just $9 million in assets.

A Deutsche Bank spokesperson said: “Deutsche Bank is closely examining any business relationship with Jeffrey Epstein, and we are absolutely committed to cooperating with all relevant authorities.”

via ZeroHedge News https://ift.tt/32OD64p Tyler Durden

Robert Mueller’s performance in front of Congressional committees should mark the end of special counsels, special prosecutors, independent counsels and the like. These hearings demonstrated, if any further demonstration was required, how dangerous it was to go outside of the normal processes of criminal justice.

Ordinary prosecutors are not allowed to comment about why they decided not to prosecute the subject of an investigation. The Mueller Report, when made public, violated that salutary tradition. It contained negative information about people, including the president, who will have no opportunity to respond in a legal proceeding.

The report and the testimony introduced the novel and dangerous concept into our legal vocabulary: “Not exonerated.” This concept, which finds no basis in the rules of the Justice Department or the Special Counsel, is a variation on the nefarious theme articulated by the disgraced former FBI director, James Comey, when he went beyond announcing that Hillary Clinton would not be prosecuted, and expressed his opinion that she had been extremely careless in her treatment of emails. This statement said, in effect, that Hillary Clinton was not being exonerated.

Mueller’s testimony was confused and confusing on many scores. He couldn’t explain why he had reached a formal decision on conspiracy with Russia but had failed to reach a formal conclusion about obstruction of justice. He had to pull back on his answer to whether the decision not to charge the President was based on a Justice Department policy against indicting a sitting president. There was no explainable pattern as to why he chose to answer some questions while declining to answer others. He seemed not to be familiar with the contents of the Report that bears his name. It was almost as if he had signed his name to the Report without carefully reading or understanding it.

The night before Mueller’s testimony, I was asked on a TV show whether it was a Hail Mary pass thrown by the Democrats. I predicted that it would be an intercepted pass. I was right. Even many Democratic stalwarts viewed the Mueller testimony as harmful to their cause. As a liberal Democrat, I share that view and it doesn’t please me. But as a patriotic American, I care far more about the implications of the Mueller testimony for all Americans and for the rule of law.

The only good that can come from this testimony is that the millions of Americans who watched, or who will see and read excerpts, will come to understand how dangerous the Office of Special Counsel is to the rule of law. From day one, I proposed an alternative: namely the appointment of a nonpartisan expert commission whose job it is to investigate the role of Russia in trying to influence American elections and to influence our American democratic processes. Like the 9/11 Commission, this Russia Commission would not be pointing prosecutorial fingers for past derelictions, but would be focused primarily on preventing Russia from continuing to influence our American political processes. Prosecutors, like the Special Counsel, operate behind closed doors and in secret. They hear only one side of the story. They are restricted in what Grand Jury information can be made public. Non-partisan expert commissions, on the other hand, operate primarily in public (except when hearing classified material) and hear all sides of every issue in an effort to hear the whole truth.

So let’s rethink how we deal with problems such as those that were the subject of the Mueller Report and Mueller’s testimony. Let’s learn from our mistakes and let’s stop weaponizing our criminal justice system for partisan ends. Congress and the Justice Department should abolish the Office of Special Counsel, just as they abolished the Office of Independent Counsel after the fiasco of the Starr Report.

via ZeroHedge News https://ift.tt/2SHG064 Tyler Durden

Joe Biden wants 2020 Democrats to get off his damn lawn after weeks of attacks against his civil rights record have caused his supporters to worry that the former Vice President has been too passive in his defense, according to The Hill.

According to the report, the tipping point came on Wednesday after Sen. Cory Booker (D-NJ) said at a NAACP presidential candidate forum that Biden was the “architect of mass incarceration” for a 1994 crime bill originally written by then-Congressman Joe Biden. The bill was widely blamed for contributing to the mass incarceration of black Americans for low-level drug crimes during the USA’s infamously failed war on drugs.

“You can’t be called the architect of mass incarceration and remain quiet,” a Biden ally told The Hill. “That’s cruel and personal. That goes against his entire career. You can’t let people say bullshit and not respond to it.”

Biden’s campaign is also boiling with anger at Booker. On Wednesday, the Biden campaign called Booker out by name for the first time and questioned his own record on civil rights.

Biden’s deputy campaign manager, Kate Bedingfield, said Booker “has some hard questions to answer about his role in the criminal justice system,” pointing to his promise as mayor of Newark more than a decade ago to implement a “zero tolerance policy for minor infractions.”

Bedingfield also accused Booker of “running a police department that was such a civil rights nightmare that the U.S. Department of Justice intervened.” –The Hill.

“The gloves are off,” added the ally. “At this point, you have to punch back when someone attacks your record. People want to see him throw a punch. The president is certainly going to come at him hard, so why not start now?”

In May, President Trump dinged Biden without specifically naming him – tweeting “Anyone associated with the 1994 Crime Bill will not have a chance of being elected,” tweeted Trump. “In particular, African Americans will not be able to vote for you. I, on the other hand, was responsible for Criminal Justice Reform, which had tremendous support, & helped fix the bad 1994 Bill!”

Anyone associated with the 1994 Crime Bill will not have a chance of being elected. In particular, African Americans will not be able to vote for you. I, on the other hand, was responsible for Criminal Justice Reform, which had tremendous support, & helped fix the bad 1994 Bill!

In a second tweet, Trump wrote”….Super Predator was the term associated with the 1994 Crime Bill that Sleepy Joe Biden was so heavily involved in passing. That was a dark period in American History, but has Sleepy Joe apologized? No!”

….Super Predator was the term associated with the 1994 Crime Bill that Sleepy Joe Biden was so heavily involved in passing. That was a dark period in American History, but has Sleepy Joe apologized? No!

Next week will see Biden face off on the same debate stage as Booker and Sen. Kamala Harris (D-CA).

“I’m not going to be as polite this time,” Biden told donors at a Wednesday fundraiser in Detroit.

Biden has signaled that he may take a shot at Harris’s record as California attorney general, perhaps accusing her of policies that led to the incarceration of racial minorities. Biden started down that path at the first debate, noting that he pursued a career as a public defender while she chose to become a prosecutor, but it was not a line of attack that he vigorously pursued.

“If [Harris and Booker] want to argue about the past, I can do that. I got a past I’m proud of,” Biden said Wednesday. “They got a past that’s not quite so good.”

Harris’s allies say they’re spoiling for the fight, an indication that the bad blood flowing between the two camps might become one of the defining developments of the Democratic primary race. –The Hill.

“I’m glad Joe Biden is going to be there this time and may be sharper,” said Berkeley County chairwoman for the Democratic Party, Melissa Watson – a Harris supporter.

“There’s an air of entitlement in all of his comments,” Watson added. “He’s saying, how dare she question him about his past. And he says he did her a favor, so that means she has no right to question him during a presidential primary? That’s crazy. They’re running for the highest office in the land.”

Biden, meanwhile, has slipped a bit in the polls since the first debate – however he remains the clear front-runner “in part because of his enduring support from African Americans,” according to the report.

A Monmouth University survey released Thursday found Biden with a commanding lead in South Carolina, a critical early-voting state where black voters make up about 60 percent of the Democratic primary electorate.

Biden has 39 percent support overall in South Carolina, with Harris running a distant second place at 12 percent. The former vice president has 51 percent support from black voters in the state, followed by Harris, at 12 percent.

According to Monmouth University polling director Patrick Murray, “Despite some supposed missteps on the issue of race, Biden maintains widespread support [among black voters].”

That said, another terrible debate performance could jeopardize Biden’s lead.

“I’m glad he’s finally pushing back, it should plug the leak, but he still needs to pull this off in prime time with both Harris and Booker flanking him on the dais,” said one Democratic strategist and Biden supporter. “Make no mistake — another poor performance and this might be over for him. He doesn’t have the luxury of stacking bad debates on top of one another, especially with this many people coming after him.”

via ZeroHedge News https://ift.tt/2Zc5UBH Tyler Durden

Submitted by Joseph Carson, former Director of Global Economic Research, Alliance Bernstein

The happy prophecy of endless growth in the economy generating a continuous flow of strong corporate earnings just ran into trouble—the “truth” on profits. According to GDP data released today Q2 corporate earning posted their largest annual decline in several years, and the revised data shows that there has been no growth in operating profits for the past 5 years.

Q2 Real GDP bettered analyst’s expectations growing 2.1% annualized, driven by strong gains in consumer and government spending. Yet, the gain in GDP did not flow to the bottom line for companies.

According to the preliminary Q2 GDP results, implied operating profits for the period totaled $1,900 billion, down 5% from Q1, which would represent the third consecutive quarterly decline, and off over 7% from the year ago levels, one the largest declines recorded in several years.

Yet, as ugly as the Q2 numbers appear to be on the surface, what are even more troubling are the sharp downward revisions for the last two years. According to the annual GDP revisions operating profits for 2017 were lowered by $93 billion, or 4.4%, and profits for 2018 were reduced by a whopping $188 billion of 8.3%.

The revised numbers of corporate profits show that operating profits peaked in Q3 2014 and have been moving sideways even since. Operating profits in the GDP accounts and S&P 500 operating profits over the long run track fairly close to one another, although there can be large differences in any given year. Yet, a flat trend for 5 years in operating profits should not be overlooked or ignored especially since during this period S&P 500 share prices have increased over 50%.

Operating profits, or profits from current production, are the purest form of corporate earnings since this series puts all firms on the same accounting framework – it avoids non-GAAP adjustments – and the profit numbers are not adjusted for the number of shares outstanding; the latter which is often reported by S&P 500 companies for equity investors.

The argument being used by equity analysts and strategists that the equity market is cheap or inexpensive relative profits appears to be dubious in light of revised data on operating profits, and it suggests that the “actual ” market multiple is a lot higher than what is being reported by analysts.

via ZeroHedge News https://ift.tt/2yfOBUg Tyler Durden

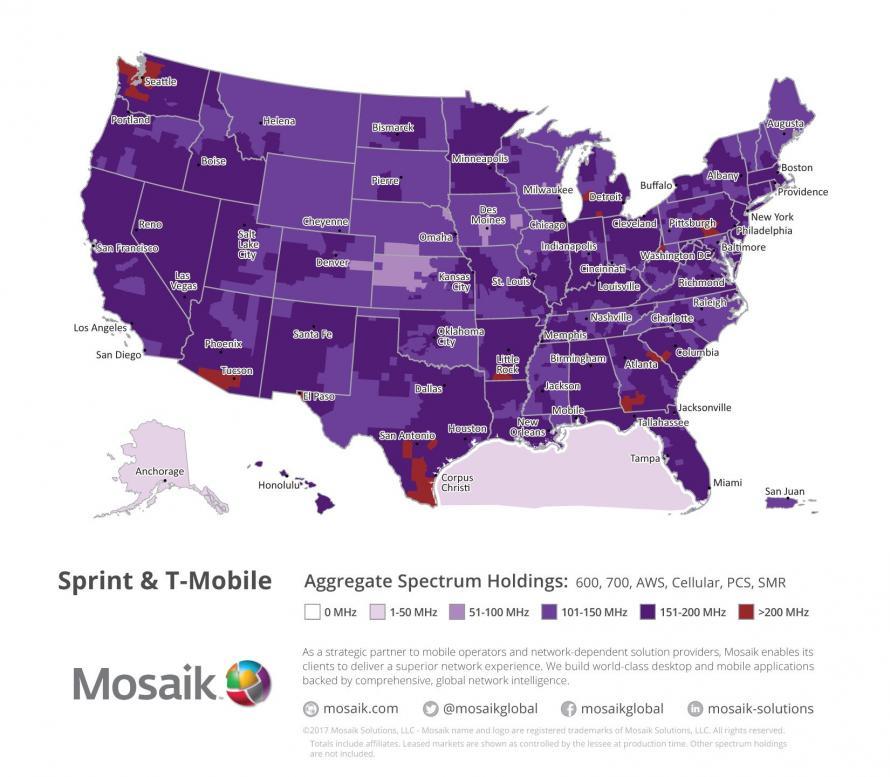

In a landmark settlement that ends a more than year-long battle, the DOJ approved T-Mobile’s proposed merger with Spring Corp., clearing a major hurdle to a deal after the two companies agreed to create a new wireless carrier by selling a host of assets to Dish, which will be required to build a 5G network for cellphone customers as part of the deal.

The landmark anti-trust ruling settles concerns about three carriers controlling 95% of the market by creating a new fourth carrier, Dish, albeit a carrier that will struggle to catch up to its much-larger rivals. The deal will make use of Dish’s valuable spectrum, which it has been sitting on for years,WSJ reports. In addition to Sprint’s prepaid business, Dish will have access to T-Mobile’s network for seven years after the spinoff. Dish will buy a portfolio of spectrum from Sprint, as well.

Though winning the DoJ’s approval means the deal will likely be consummated, there’s still one potential obstacle: several states attorneys general broke with the DoJ and filed their own anti-trust lawsuit seeking to block the $26 billion merger. Whether they will be successful or not remains to be seen. Five states that weren’t part of this lawsuit sided with the DoJ in Friday’s settlement.

“With this merger and accompanying divestiture, we are expanding output significantly by ensuring large amounts of currently unused or underused spectrum are made available to American consumers in the form of high quality 5G networks,” said Makan Delrahim, the Justice Department’s antitrust chief.

The deal will leave Dish with 9 million SPring prepaid customers, and some additional wireless spectrum. That represents about one-fifth of Sprint’s customer base.

So, while the US will still have four major wireless carriers, the fourth-largest carrier will be much, much smaller than Sprint. Soft Bank, which, as we reported earlier, is in the middle of raising a second Vision Fund, will be able to use money from the deal to finance the company’s stake in the venture fund.

Unlike other recent telecoms mergers, this isn’t a “vertical merger”, like the AT&T-Time Warner tie-up that the DoJ tried, and failed, to block. But it will likely save Sprint from bankruptcy, and set the nascent trust-busting movement in the US back a few steps.

The merger is still expected to create the largest cellphone carrier in the US, with around 120 million customers.

via ZeroHedge News https://ift.tt/2Y5e16A Tyler Durden

Authored by Steve Englander via Standard Chartered,

Whoever can surprise well must conquer – John Paul Jones

There is much discussion, but also confusion, about the impact of central bank surprises on asset markets and economic activity. We argue:

In the current cycle, it makes little difference to asset prices and activity whether the Fed cuts 50bps in July (unlikely) or 25bps in July and 25bps in September or October. The same holds for the ECB moving in July or September (see FOMC – dovish tilt, ECB – Easy does it).

Lower-for-longer rates matter more than deep but short-lived cuts, subject to the broad limits of monetary policy effectiveness discussed in Japanification.

Moving faster than market pricing could provide a signal that boosts confidence in the easing narrative, but the impact is likely to be shorter-term relative to a slightly slower pace of policy moves.

The economic impact comes from the cumulative easing that households and businesses experience, not surprises around central bank meetings.

Stronger activity data in July may be due to easing priced in January, but may also reflect underlying strength in the economy.

Money markets now price in an average of about 20bps of cuts in G10 economies for the rest of this year, with 69bps for the US (105bps by end-2020). Since end-November 2018, expected policy rates for end-2019 have dropped 42.5bps (Figure 1). On the fixed income side, market pricing for 2Y USTs around year-end is 1.75%, versus our forecast of 1.65%; for 10Y USTs, market pricing is 2.10% versus our 1.75% forecast. The low for fed funds futures is 1.35% for early 2021 contracts.

There is much discussion among investors about the asset-market and economic implications of meeting, beating and missing expectations of central bank easing. Most central banks have not pushed back against market pricing, and some have tacitly or explicitly encouraged such pricing. Money-market repricing of future easing should affect liquid currency, fixed income, equity and commodity markets very quickly, if not immediately.

The economic impact of this repricing occurs over time, not immediately. There is considerable uncertainty over how fast the impact is felt; an easing of financial conditions in January could have an impact by July, but might not. Investors must assess whether solid activity will cause the central bank to rein in expectations or vindicate them. Both asset-market and economic responses will be driven by the full path of expected rates changes. The ultimate impact will be driven by the cumulative expected move in rates and the duration of the move.

This pricing does not necessarily have positive implications for all asset markets. If the S&P is slightly above 3,000 when the fed funds rate is expected to drop almost 100bps over the next year, the macro justification for further gains seems limited. Positive surprises are possible, for example, if the US-China trade talks produce a stellar deal, but risks will almost always be two-sided relative to market pricing.

Investors look at the effects of lagged tightening and easing

Modern financial theory starts from the view that liquid markets integrate surprises quickly. If the Fed or another central bank announces a policy shift, the impact of the shift in asset prices will likely be felt quickly. When investors shift from seeing a 50% or more chance of 50bps of cuts to near certainty of 25bps (as occurred over 18-19 July), bond yields, equity prices and currencies factor in the perceived policy shift almost immediately.

The perceived policy shift will probably not affect economic prospects very rapidly. The way most models present it, the degree of monetary stimulus can roughly be measured by how long rates spend below neutral and how low they go. Figure 2 shows the US unemployment rate (UR), real 2Y UST yields (measured by subtracting lagged two-year core inflation from nominal 2Y UST yields), and the detrended value of the real 2Y yield. The UR leads by 24 months, so today’s UR corresponds to the real 2Y yield of 24 months ago.

We use the trend 2Y UST real yield as a rough proxy for the long-term equilibrium real yield. The gap between actual 2Y UST real yields and the trend value can be seen as stimulus if real yields are below the trend; or as restraint if real yields are higher. In technical terms, most models would say that the degree of economic stimulus would be measured by the integral between actual and neutral rates. The beginnings and ends of such periods of stimulus and contraction are indicated in Figure 2 by the vertical lines, with green indicating the beginning of stimulus and purple the end.

The correspondence between episodes of a falling and rising UR and our stimulus/contraction measures is striking , especially considering the simplicity of our measure of policy stimulus and contraction. We think that our calculations illustrate these broader points:

The measure of stimulus is how far real rates are from equilibrium and how long this deviation persists.

A policy surprise can intensify or slow the pace of easing, but unless it becomes tightening, it would not flip the economy into recession.

The long and variable lags from rates to activity mean that investors and central banks are always guessing how much fuel there is in the stimulus tank – they may not know for months.

In the current context, we do not necessarily know if the economy is responding to the tightening that occurred in 2017-18 or the more recent easing. Calculation of equilibrium rates is more reliable towards the middle of the sample than right at the end.

The fact that the economy looks somewhat stronger now may reflect the easing that is now priced in, or it may mean that the equilibrium real interest rate is higher than we thought. We probably will not know for a while, but as long as inflation is contained, investors will likely keep easing expectations in place.

How bound are central banks by market pricing?

Investors have to consider the risk that central banks will disagree with market pricing of future rate cuts. Markets will see a central bank as confirming market pricing if it does not use opportunities to push back against that pricing. This can be done at meetings or in speeches before meetings.

Even if central bank officials do not want to pre-empt future central bank decisions, they can signal concerns around market pricing. The risk if they do not provide this signal is unnecessary asset-market volatility and possibly economic volatility, although the central bank would probably need to leave the mispricing in place for an extended period for the economy to be affected. Investors will see silence as central bank consent as long as future data releases are in line with market expectations at the time when implied consent was given.

Central banks may understate their concerns about future activity on the view that too much pessimism will risk pushing markets – and even household and business expectations – in an overly negative direction. Moreover, if they say ‘we think the economy is likely to tank’, they have an imperative to move quickly and sharply. To avoid this situation, they will hint at risks of future weakness, and hope that market participants take the hint.

Central banks also have a practical motivation not to let excessive priced-in easing or tightening persist. The risk is that such pricing will affect economic data over time, and create confusion over whether the economy was responding to the priced-in easing or underlying strength.

The market risk on the other side is that central banks always convey their views in conditional terms. This conditionality is often not emphasised because the central bank wants the market to react to its forward guidance, and heavy conditionality would limit the response. But a close reading of central bank comments often implies expectations of data outcomes that must be confirmed in order for the central bank to act. Confidence that ‘insurance cuts’ will remain in place requires that the fears that drove the need for insurance are realised. Central banks can fall back on this conditionality as needed, and market participants have to factor this risk into asset pricing.

Is one big surprise more powerful than a series of small surprises?

There is much speculation that just meeting market expectations will be a disappointment to investors or mitigate the impact of easing. The need for a policy surprise was discussed frequently when the market was debating whether the Fed’s July meeting would deliver 25bps or 50bps of cuts.

We want to be careful to make apples-to-apples comparisons. There is not much theoretical or empirical analysis to indicate that one surprise 50bps cut is significantly more powerful than two surprise 25bps cuts reasonably close together. This would require a non-linear response by asset markets or the economy, and such non-linearities are often hard to justify or establish empirically. So 50bps achieves easing slightly faster, but that is likely to make only a trivial difference to the ultimate outcome.

Similarly, the drop in expected policy rates (Figure 1) has already affected asset prices, and is likely to affect activity over time. The cuts that are priced in represent a series of surprises building since December. The drop relates partly to Fed statements or actions, and partly to market views on how the global and domestic economies and policy are likely to evolve. The asset-price implications of actual Fed easing are unlikely to differ much from the implications of market expectations of easing, provided both are driven by the same reading of data.

via ZeroHedge News https://ift.tt/32XuzfF Tyler Durden

Most Americans probably haven’t heard of the Posse Comitatus Act. But the federal law, passed in 1878, bars active duty troops from being used as police within the borders of the US. And some Democrats believe that the 5,000+ troops station along the southern border are in violation of the law, despite the Trump Administration’s claims that they’re only there to “support” the CBP personnel.

But in recent weeks, troops have been stationed inside a migrant detention facility in Donna, Texas. They were initially deployed there to perform welfare checks – the troops are allowed to perform emergency medical care – but their duties have ‘evolved’ to include acting as de facto prison guards, something that would be a clear violation of Posse Comitatus, NBC reports.

Rep. John Garamendi, D-Calif., who chairs the House Armed Services Committee Subcommittee on Readiness, says having active duty troops monitor migrants is “teetering on the edge of the posse comitatus law.”

“It’s not the role of the U.S. military to be a prison guard,” he said. “This is certainly mission creep” and could put U.S. military service members “in a precarious legal situation.”

One former defense official told NBC that monitoring migrants is probably “a bridge too far.” If soldiers tried to break up a fight, they’d be in clear violation of the law.

Right now, interactions between the troops and migrants are limited “as much as possible,” said John Cornelio, particularly at the detention facility where troops are now stationed.

“At the Donna Facility specifically,” said Cornelio, “unarmed military personnel monitor the migrants for signs of medical distress, possibility for unrest, unusual behavior and unresponsiveness. In the event of a medical emergency or other reportable event, our military personnel immediately notify CBP personnel on-site who respond to the incident or event in question.”

“Monitoring the wellness of migrants is not a law enforcement function, and this activity has been reviewed by our legal staff to ensure compliance with the Posse Comitatus Act and applicable law. CBP personnel are always present to provide force protection, physical security and perform their law enforcement duties.”

One defense official told NBC that the troops weren’t “guarding” the migrants, saying they were just monitoring them for signs of health issues and performing welfare checks. If the troops spot a problem, they’re supposed to alert a CBP official and have them handle the situation, unless there’s a medical emergency or something else that would require an emergency response. Furthermore, the troops aren’t armed, which cuts against claims that they’re performing a ‘police’ function.

Expect pro-migrant groups to try and challenge the troop deployments to the border: we’re surprised they haven’t already.

via ZeroHedge News https://ift.tt/32UuRUg Tyler Durden

The longer the signals in capital markets go haywire under the influence of “monetary stimulus,” the bigger is the cumulative economic cost. That is one big reason why this fourth Fed stimulus — in the present already-longest (but lowest-growth) of super-long business cycles — is so dangerous.

True, there is nothing new about the Fed imparting stimulus well into a business cycle expansion with the intention of combating a threat of recession. Think of 1927, 1962, 1967, 1985, 1988, 1995, and 1998.

This time, though, we’ve seen it four times (2010/11, 2012/13, 2016/17, 2019) in a single cycle. That is a record. Normally, a jump in recorded goods and services inflation, or concerns about rampant speculation, have trumped the inclination to stimulate after one — or at most two — episodes of stimulus.

Also we should recognize that the length of time during which capital-market signaling remains haywire, is only one of several variables determining the overall economic cost of monetary “stimulus.” But it is a very important one.

Haywire signaling is not just a matter of interest rates being artificially low. Alongside this there is extensive mis-pricing of risk capital. Some of this is related to the flourishing of speculative hypotheses freed from the normal constraints (operative under sound money) of rational cynicism. Enterprises at the center of such stories enjoy super-favorable conditions for raising capital.

There are also the giant carry trades into high-yielding debt, long-maturity bonds, high-interest currencies, and illiquid assets, driven by some combination of hunger for yield and super-confidence in trend extrapolation. In consequence, premiums for credit risk, currency risk, illiquidity, and term risk, are artificially low. Meanwhile a boom in financial engineering — the camouflaging of leverage to produce high momentum gains — adds to the overall distortion of market signals.

Crucially, the length of time over which capital-market signaling has been haywire does not neatly coincide with the business cycle. Rather, it may extend into the previous cycle — and beyond — if it is a long time since there has been any sustained period of non-stimulus. This consideration is a rationale for the hypothesis of the long financial cycle — stretching well beyond one business cycle — as hypothesized in research at the Bank for International Settlements.

Accordingly, in the course of a long financial cycle upswing, there could be a recession which briefly shrinks the speculative froth across a range of asset markets. But there would be no extended period of monetary normality (absence of stimulus) during which signaling again became efficient.

For example, think of the business cycle expansion of 2003–2007. In fact, monetary stimulus was already over by late 2005. How could such a short monetary inflation have had such devastating results in terms of Crash and Great Recession? At least part of the answer is the long period during the previous cycle in which prices had also been haywire. This period includes most of the years from 1993–2000. The 2001–2002 economic downturn was mild and the subsequent stimulus (2003–2005) was radical.

The same point about the duration of haywire stretching into the previous business cycle can be made for the asset inflation (coupled with goods inflation) of 1971–1973. Only an exceptionally mild recession and short effective monetary tightening in 1969 (and earlier a brief “credit squeeze” in 1965) interrupted the Fed stimuli during the long cyclical upswing to that date. Earlier in the twentieth century, the shortness of the 1920 recession (though severe) and the power of the subsequent Fed stimulus meant there was no substantial respite from capital market mis-signaling. This dated back to the start of the Great Asset Inflation in 1915–2016 (ignited by vast Fed purchases of gold from Britain and France during the period of neutrality).

Length of time during which capital-market signaling remains haywire is crucial to the amount of overall mal-investment which occurs and the ultimate cumulative economic cost. We also should consider the severity of the mis-signaling. This depends in part on a range of idiosyncratic factors which determine the power and growth of speculative storytelling.

Of course, mis-signaling in capital markets, as measured by duration and extent, is not the only source of economic cost from prolonged asset inflation. There are also the incidental mistakes, sometimes very big, which the Fed makes during the periods of economic slowdown or recession, which interrupt or succeed the asset inflation.

Relevant history here includes the over-tight monetary policy of late 1928 and first three quarters of 1929 as the Fed fought excess speculation on Wall Street. The Fed was blithely unaware of the gathering recession from the autumn of ’28 in Germany, then the world’s number two economy, and the chief destination of vast speculative waves of loan capital. In modern times, we can take the Bernanke Fed’s tight money policies through 2006–2007 driven by concern about CPI inflation above target when asset and credit inflation was already cooling.

In measuring the cumulative economic cost of price-signal malfunctioning in capital markets and coincidental Fed mistakes, it is not just a matter of assessing the severity of the Crash and Recession which marks the end stage of the cycle under review. Costs accrue over a long period of time and might be huge even when these events seem mild. Mal-investment means that the growth of economic prosperity can suffer over decades, especially if, subsequently, capital-market pricing remains haywire and the invisible hands suffer from paralysis.

This has likely been the case with cumulative mal-investment in the first two decades of the present century — helping to explain why growth in overall prosperity has been so meager. Looking into the future there could well be growing evidence of bloated investment (relative to what would happen under sound money) in often negative-sum-game digital technology. This is driven in part by speculative narratives of present or future monopoly power.

In this context, the fourth Fed stimulus is especially dangerous. It is still possible this will be a failed stimulus. Asset inflations tend to burn themselves out. Growing mal-investment, and speculative narratives which become tired, become reflected in slower business earnings growth. Pessimism then becomes apparent in weakness in some particular asset markets, downgrades of credits (as collateral values fall) and at some stage a panic for the exit from crowded carry and other trades. These endogenous forces may be gathering strength and capable of over-powering the “Powell put.”

Take, however, the alternative scenario: where the Powell Fed’s stimulus is indeed effective in producing another growth-cycle upturn which starts well ahead of Election Day. A new momentum of mal-investment around the globe is to fear — along with related fantastic boom time for the financial engineers. There would be chat in the media that the business cycle is dead due to the skill of the data-dependent Fed in administering ever-ready stimulus.

Like the townsfolk in Gogol’s Government Inspector, markets would fete the mysterious disappearance of the recession danger which visited in 2019, even attributing the escape from a new hard regime as due to their representatives’ skill. Later it would turn out that the visitor was an artful impostor and the real inspector (recession and crash) arrives with no notice.

via ZeroHedge News https://ift.tt/2Olilda Tyler Durden

We can imagine Mark Zuckerberg, sitting ensconced in his bunker inside Facebook HQ, reading every new story about his one-time friend and Facebook co-founder Chris Hughes’ campaign to force the breakup of Facebook, the company Zuckerberg worked so hard to build. ‘How ungrateful,’ Zuckerberg probably thinks to himself.

That’s because Hughes has emerged as what the Washington Post characterized as “one of [Facebook’s] biggest problems.” It started with a sweeping New York Times op-ed, where Hughes declared that Facebook ‘should be broken up’ and that while he still thinks Mark Zuckerberg is “a good, moral person”, as Chairman and CEO of Facebook, Zuckerberg has too much power.

While Facebook gladly paid $5 billion to settle allegations of privacy violations with the FTC, the company is firmly opposed to any kind of anti-monopoly actions. Its argument is simple: Since consumers use social media apps that aren’t controlled by Facebook (think Twitter and LinkedIn), it’s clear that Facebook doesn’t have a monopoly. And when asked about the status of his friendship with Zuckerberg after going public with his allegations, Hughes joked that Zuckerberg probably no longer considers him a friend.

The decision to publicly oppose Facebook in the op-ed was a difficult one, he said.

“I knew I would lose some friends over it. And that’s okay because some things are that important,” he said. “But it’s been nice on the other side of it, too, to have the argument out there, to speak my mind about what I think and believe.”

In a story about Hughes’ campaign to undermine the company he helped create, a company that netted him a fortune ($500 million at the time he cashed out his stake). Hughes left Facebook in 2007 to volunteer for the campaign of then-Senator Barack Obama.

But now, according to WaPo, Hughes has been making the rounds on Capitol Hill, visiting dozens of lawmakers and regulators at the DOJ and FTC, and presenting a 39-slide PowerPoint deck that he purportedly made himself outlining his argument about Facebook being a monopoly.

Hughes’ argument depends on the vast user base of Facebook and Instagram, and the company’s acquisitiveness, which helps to stifle competition by discouraging challengers.

Facebook’s wealth and power and massive user base have pushed it into monopoly territory, and its acquisitions of rivals have squashed competition. More than 2.7 billion people use Facebook or its other platforms, which include Instagram and messaging service WhatsApp, at least once a month, Facebook said Wednesday.

“I hope that my speaking out provides cover to a lot of other folks, whether former employees or current ones, to express ambivalence or concern about what’s going on,” Hughes said in an interview Thursday. “And I think there’s a lot to be concerned about.”

The former Facebook spokesman is also trying to convince other ex-employees with reservations about the company’s largess to speak out.

But the fact that a former executive are making these criticisms is a huge boon for trust-busters. It threatens not just Facebook, but the other tech giants of Silicon Valley. Hughes has effectively become the most effective lobbyist for the ‘break up Facebook’ crowd, and he’s doing all of this work for free.

And that’s bad news for Facebook, because breaking up big tech has become a bipartisan issue, embraced by President Trump and Dems like Elizabeth Warren.

To be sure, Hughes isn’t the only former Facebook executive or early investor to criticize the company: Sean Parker and Robert McNamee and other former senior executives have also criticized Facebook over its business practices, but they haven’t been lobbying for breaking up Facebook.

Hughes has reportedly been a useful resource for anti-trust lawyers who have been working on a new argument for breaking up Facebook.

Soon after, Hughes was contacted by two prominent antitrust scholars, Scott Hemphill of New York University School of Law and Tim Wu of Columbia Law School. The two academics and longtime collaborators had been developing an argument for breaking up Facebook in the form of the slide presentation. To them, the purchase of Instagram and WhatsApp represented a “plain-vanilla violation of antitrust law, just low-hanging fruit,” Wu said in an interview. They began to pitch lawmakers and regulators together.

Academics and lawmakers who have worked with Hughes say he has helped explain the motivations and viewpoints of key players at Facebook, including Zuckerberg – although Hughes says he has no specific insider knowledge. They say Hughes can frame the business practices of present-day Silicon Valley in ways that jibe with largely untested antitrust laws that were written for major oil and rail companies decades ago.

[…]

Hughes’s feedback shaped the scholars’ case, as he helped them understand how executives in Silicon Valley think about competition — it tends to be measured by viral growth rather than by size, said Hemphill, the New York University professor. At the time, the two professors were working on a roadshow, which they asked Hughes to join.

Rhode Island Congressman David Cicilline say Hughes has helped inform his views about whether Facebook might be a monopoly.

“The thing that stuck with me…was he focused on Facebook’s revenue as a true measure of its role in the marketplace,” Cicilline recalled. “Facebook captures over 80 percent of all global social media revenue and controls 58 percent of the U.S. social media market. That’s significant.”

So, how will Zuckerberg counter Hughes? The company has hired an army of lobbyists in the wake of its twin scandals, data privacy violations and its failure to stamp out fake accounts. But given his resources, Hughes is going to be a difficult critic to discredit and stamp out.

via ZeroHedge News https://ift.tt/2OleMDO Tyler Durden