In Transformational Shift, The BOJ Gives Up On Negative Rates As It Now Pays Banks To Lend

Tyler Durden

Thu, 08/13/2020 – 13:10

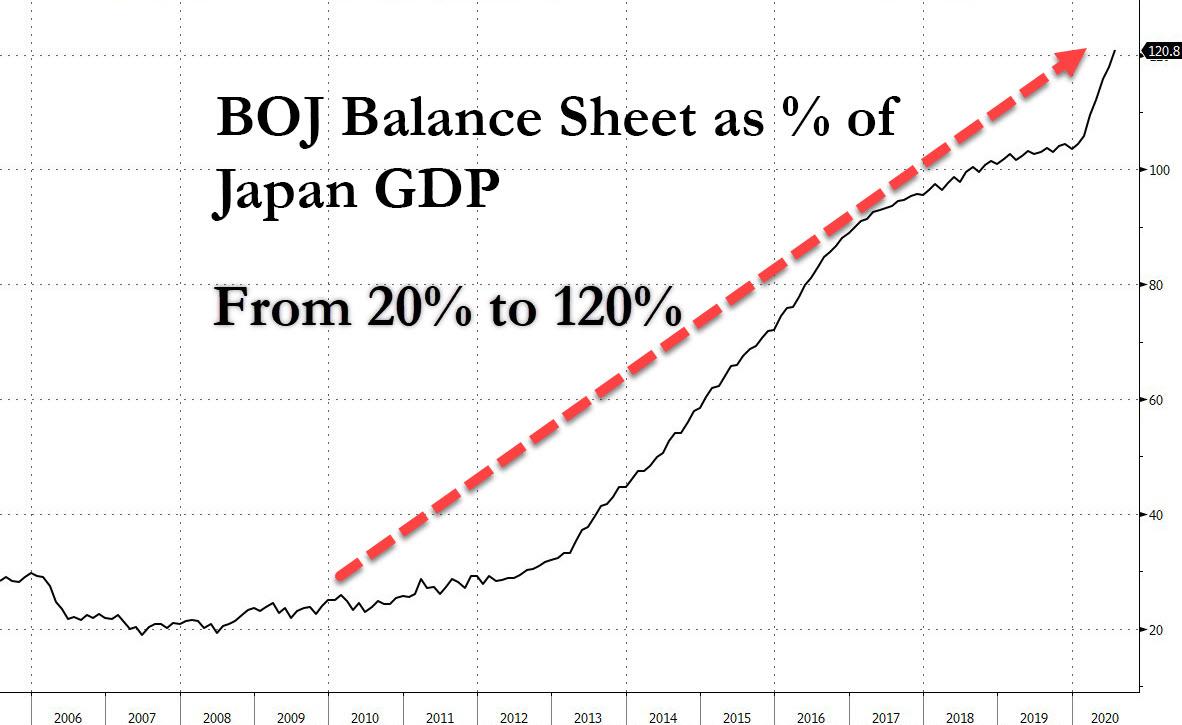

After more than half a decade of disastrous monetary policy which not only failed to stimulate inflation, boost exports or crush the yen, but has brought Japan’s banks to near disaster, the Bank of Japan has come up with an “ingenious” new plan to flood the system with liquidity: it is paying banks hundreds of millions of dollars in bonuses to boost lending, a move analysts say is aimed at easing the side-effects of its negative interest rate policy.

And while record bank lending in recent months suggests the BOJ’s plan is working – a very rare success of late in its losing battle to revive the economy – according to Reuters it is also a sign that policymakers’ focus is now more on supporting banks, rather than keeping rates low.

To be sure, the literal wall of money printed by the BOJ in recent years has kept a lid on bankruptcies and job losses as the economy tips into a deep recession, although it has also meant that banks can not survive without continued life support from the central bank. And the prolonged battle with COVID-19 has only added strains on regional banks.

Needless to say, the local bankers are delighted with this latest indirect transfer from taxpayers to the top 1%: “This is one of the most effective policy moves the BOJ has made in recent years,” said Takehiro Noguchi, senior economist at Mizuho Research who personally stands to benefit from this “effective policy move.”

We found his second comment far more illuminating: “The BOJ will likely continue to take steps to alleviate the side-effect of its monetary easing… The BOJ thinks negative interest rates is something it should not have done.”

Oh, so conducting catastrophic experiments with monetary policy that crush savers and the middle class, while making the rich wealthy beyond their wildest dreams is something that “should not have been done”? We agree, and if only the BOJ had listened to us when we said all of this before it launched its idiotic NIRP policy, it would have saved Japan’s population years of misery and pain. Of course, central bankers always “know best”… and then the system collapses.

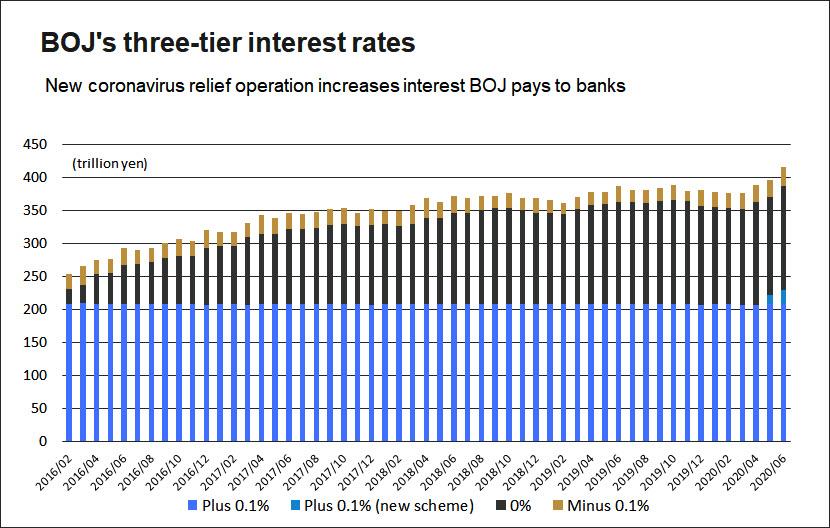

In any case, it’s too late now to fix anything without a complete systemic reset (and crash), and so the BOJ is forced to engage in increasingly desperate measures to keep it all together. That’s why in March the BOJ cobbled together special “coronavirus relief” operations to help keep cash-strapped companies afloat. Under the scheme, the BOJ lends cash to banks against their lending to the private sector, such as loans and bonds, as collateral.

The operation started off quietly but got a major boost after the BOJ decided in April to add a sweetener by giving banks a bonus of 10 basis points (bps) or 0.1% per year, for using the scheme, a bonanza when 10-year government bonds yield 0.04%.

Yes, if this sounds like a direct money transfer from the central bank to the commercial banks, it’s because that’s exactly what it is. It is also completely illegal in any other context than the one of a “covid emergency.”

Naturally, banks rushed to the plan, gobbling up 27 trillion yen ($250 billion) through the channel by July. And since that is roughly as much as the amount of banks’ deposits on which the BOJ imposes negative interest rates, it appears that banks were quick to use the BOJ’s latest helicopter money scheme to offset the punitive effects of NIRP.

Recall that in 2016 the BOJ went negative in an attempt to weaken the yen and lower corporate borrowing costs (it achieved neither). However, to avoid damaging banks even more, it imposed a minus 0.1% rate on only a small portion of banks’ deposits, amid concerns the policy could squeeze lenders’ margins and possibly reduce the flow of credit to the economy.

Meanwhile, as Reuters notes, the BOJ has paid 0.1% interest to banks on a total of about 208 trillion yen deposits, while the remainder carries zero interest. The complicated, three-tier interest rate system was intended to keep the benchmark interbank lending rate below zero percent while limiting the negative interest banks have to pay to the BOJ.

Of course, as analysts were quick to point out, paying additional interest on the new scheme is undermining the case for negative rates even further, thereby obviating the entire disaster that has been NIRP.

“In the grand scheme of things, we could see this as a policy normalisation as well as enhancing support for banks,” said Katsutoshi Inadome, senior strategist at Mitsubishi UFJ Morgan Stanley Securities.

As a result of the BOJ’s move to increase interest payments to banks, the benchmark interbank overnight interest rate has also edged up, staying mostly above minus 0.05%.

The good news is that for now, the BOJ’s latest helicopter money plan appears to be working. Data this week showed banks’ lending rose by a record 6.3% in July from a year earlier to 572.7 trillion yen ($5.36 trillion). That represents an increase of about 26 trillion yen since March, suggesting the BOJ has effectively back-financed nearly all of the bank lending growth since then.

It also means that while the operation was supposed to be temporary, many now expect that the BOJ will gradually make it permanent as it is extended it beyond its scheduled expiry next March.

More importantly, while backtracking on negative rates could – and will – erode the BOJ’s credibility, frankly it’s not like the BOJ had much to begin with as all that now matters is how much the government will order the BOJ to print under the auspices of helicopter money.

Meanwhile, with the BOJ having effectively nullified NIRP, there is confusion as to how monetary policy will look in the future when Kuroda has to ease further, having admitted that NIRP is a failure and rapidly running out of debt and ETFs to monetize.

“Should the BOJ ever need to cut interest rates further to ease its policy, the central bank will combine it with more bonus schemes like this, to the extent that the net effect becomes unclear,” said Izuru Kato, chief economist Totan Research.

Kato is right, and the final bonus scheme will be the BOJ finding an “excuse” to give money directly to Japan’s population, after which it is game over for fiat as first the yen then every other “developed” currency will implode.

via ZeroHedge News https://ift.tt/2XX6Wmp Tyler Durden

{kind=link}

{kind=link}