Mysterious Drone Swarm Breached Secure Airspace Over Largest Nuclear Power Plant In US Tyler Durden

Sun, 08/02/2020 – 23:15

A mysterious incident related to a serious breach of secure airspace over America’s largest nuclear power plant has been unearthed through Freedom of Information Act documents gained from the government.

It’s leading to new fears that America’s energy infrastructure is prone to attack and potentially being knocked offline, akin to the drone and missile attack which temporarily halted all Saudi oil exports last year at Aramco’s Abaqaiq oil processing facility. Forbe’s presents the astonishing details as follows:

A tiny armada of between four and six unmarked drones flew over the Palo Verde Generating Station nuclear power plant in Arizona on the nights of September 29 and 30, 2019, with plant security proving unable to stop them and authorities still uncertain who was operating them or why.

Palo Verde Generating Station nuclear power plant in Arizona, via Wiki Commons.

The newly accessed Nuclear Regulatory Commission (NRC) documents had called the incident a “drone-a-palooza” as it involved swarms of inexpensive, likely off-the-shelf drones flying in large numbers over restricted airspace and near sensitive structures of Arizona’s Palo Verde Nuclear Power Plant.

The documents conclude that it’s still as yet unknown who or what entity sent them or who was operating them during the illegal incursion.

“Documents gained under the Freedom of Information Act show how a number of small drones flew around a restricted area at Palo Verde Nuclear Power Plant on two successive nights last September,” Forbes writes further. “Security forces watched, but were apparently helpless to act as the drones carried out their incursions before disappearing into the night. Details of the event gives some clues as to just what they were doing, but who sent them remains a mystery.”

File image: Getty/Daily Beast

The FOIA documents underscore the incident was confusing and chaotic for security on the ground, as the security logs suggest:

“Officer noticed several drones (5 or 6) flying over the site. The drones are circling the 3 unit site inside and outside the Protected Area. The drones have flashing red and white rights and are estimated to be 200 to 300 hundred feet above the site. It was reported the drones had spotlights on while approaching the site that they turned off when they entered the Security Owner Controlled Area. Drones were first noticed at 2050 MST and are still over the site as of 2147 MST. Security Posture was normal, which was changed to elevated when the drones were noticed. The Licensee notified one of the NRC resident inspectors.”

Four (4) drones were observed flying beginning at 2051 MST [on Sept. 30, 2019] and continuing through the time of this report (2113 MST). As occurred last night, the drones are flying in, through, and around the owner controlled area, the security owner controlled area, and the protected area. Also, as last night, the drones are described as large with red and white flashing lights. Spotlights have not been noted tonight.

The licensee has not changed their security posture. The licensee continues to monitor the drones.

As of 0355 EDT, no drones have been observed at the site since before 0020 MST. LLEA [local law enforcement agency] surveyed the area and were unable to locate drones on the ground or anyone controlling the drones.

Guards at the high secure facility were without any ability to deter the drones overhead. Subsequent media reports in the wake of the internal security memos going public say that county police were deployed to scour the area for the drone operator or operators but to no avail.

The whole unsolved incident highlights that it appears America’s network of nuclear power sites essentially remain defenseless when it comes to drone incursions.

It appears that at least at the Palo Verde site, the facility was not equipped with drone detection gear or jamming technology which could have disabled the drones. However, the sprawling facility is reportedly due to receive drone and small aircraft detection gear, but it’s unknown whether other sensitive facilities are also due for a security ungrade.

* * *

Some details on America’s largest nuclear power plant at Palo Verde:

via ZeroHedge News https://ift.tt/30l1uev Tyler Durden

Chris Stevens was an ambitious US State Department employee who volunteered to participate in the overthrow of the Libyan government in 2011.

He covertly arrived in Libya in early 2011 aboard a Greek cargo ship with CIA personnel and set up operations in Benghazi to coordinate illegal shipments of weaponry into Libya and organized attacks on the Libyan army.

After Africa’s most prosperous nation was in ruins, Stevens became the US Ambassador to Libya in Tripoli and was given a new mission of shipping tons of arms to Syria to destroy that nation.

He traveled to Benghazi in September 2012 to check on progress and was attacked. Stevens was captured, beaten, and killed.

The Obama administration hid these facts and proclaimed Chris Stevens an American hero who had traveled to Benghazi to mediate peace among warring factions when he was killed by terrorists.

* * *

Watch how the covert op turned disastrous & into a continuing cover-up:

via ZeroHedge News https://ift.tt/2XCmpbx Tyler Durden

More Than 60% Of Global Debt Now Yields Less Than 1% Tyler Durden

Sun, 08/02/2020 – 22:25

For all its monetary generosity, despite injecting $3 trillion reserves into the banking system (if not the economy), the Fed remains stuck with two big problems. The first one, as we touched on earlier, is that the newly printed money is unable to make its way into the broader monetary plumbing and spark the much needed inflation that will do away with the trillions in debt, although as we also noted, the Fed now has a plan to deposit digital funds directly into individual US accounts (using a “household app” in the words of former Fed economist Julia Coronado).

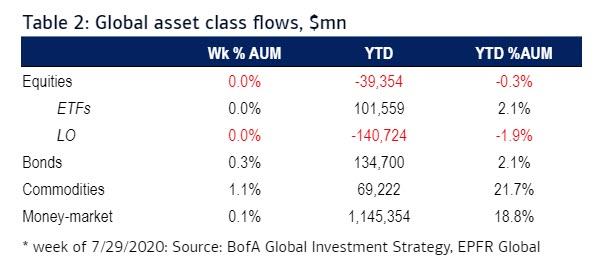

The other problem is that despite all its attempts to stimulate equity animal spirits, the bulk of new fund has flowed into bonds, not stocks. In fact, YTD equity outflows amount to $39BN while inflows to bonds and commodities are over $200BN, with a whopping $1.145 trillion going to cash via money-markets.

And so with so many investors stubbornly buying the one asset class the Fed does not want to be in wide demand (even as it monetized some $3 trillion of it), and even with trillions more in new debt to be paradropped by the US Treasury – something which has failed to taper demand for 10Y Treasurys whose yields just hit an all time low – the hunt for yield is getting harder than ever for fixed-income investors.

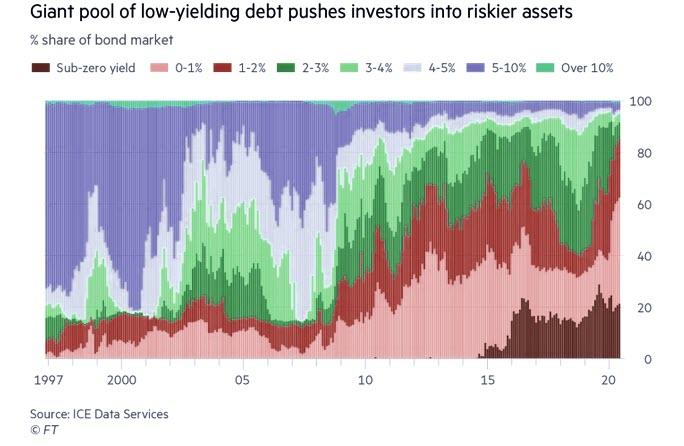

According to the FT, a record 86% of the $60 trillion global bond market tracked by ICE Data Services traded with yields no higher than 2%, with more than 60% of the market yielding less than 1 per cent as of June 30.

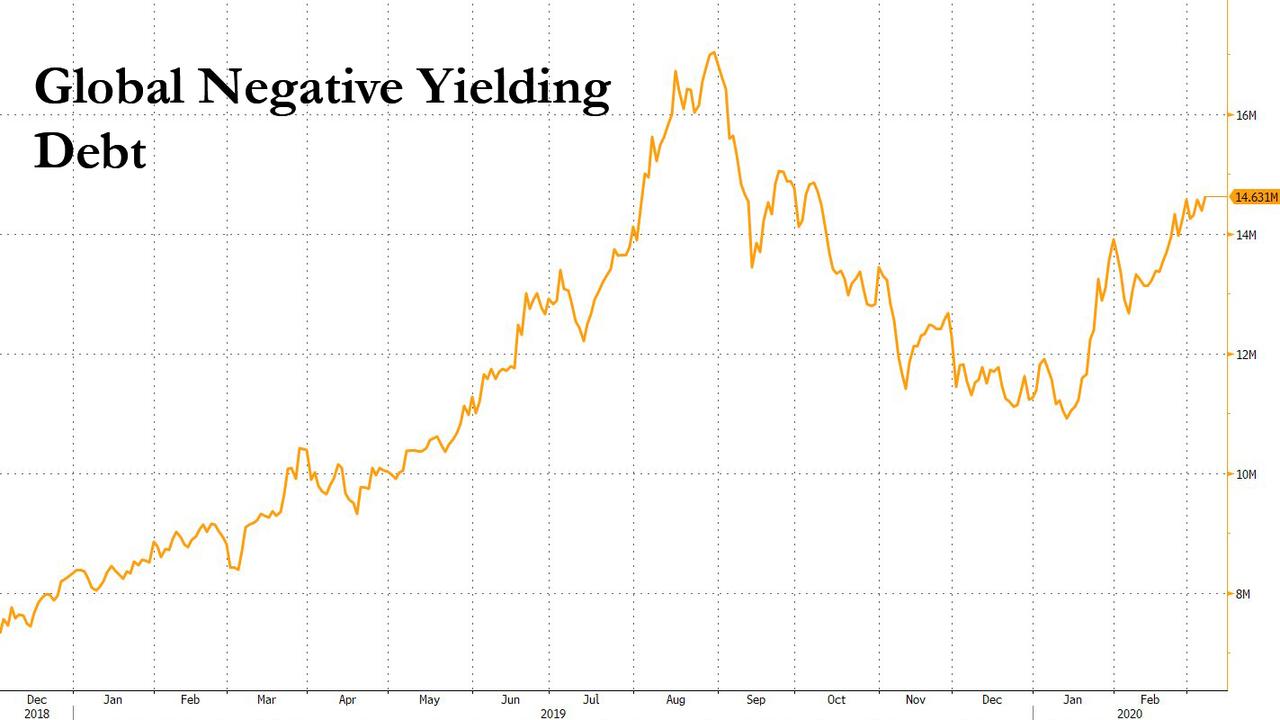

At the same time, global negative yielding debt has soared to $14.6 trillion, from $11 trillion in January, and rapidly approaching the all time high of $17 trillion hit one year ago.

Meanwhile, just 3% of the investable bond universe today yields more than 5%, a share that is close to an all-time low, and represents a precipitous drop from levels seen roughly two decades ago. Consider that in the late 1990s, nearly 75% of bonds traded with yields above 5 per cent, while sub-2% yields comprised under 10% of the market. That was before central banks took over capital markets, and responded to the a series of financial crises by slashing interest rates to ever lower, and eventually negative rates, and launching trillions in bond-buying programs that fundamentally altered the investing landscape.

This has pushed investors into riskier segments in search of income, compelling them to lend to lower-quality companies and countries.

“Yield-chasing behavior has become much more pronounced,” said Matt King, Citi’s legendary credit strategist. “If you are a pension fund or an insurance company, you are forced to go down in quality and take extreme risk.”

It all came to a head in this year’s Covid-19 crisis, when the Fed again cut interest rates to near zero, and pledged to buy an unlimited quantity of government debt (and has been doing so, monetizing all gross Treasury issuance in 2020). The central bank also launched a number of emergency programs to shore up an unprecedented range of securities — including IG, junk bonds and municipal debt – which sent investment grade prices to all time highs and disconnected them from fundamentals. Investors expect additional stimulus measures to be announced at either this week’s Fed meeting or the next one in September.

After the latest round of interventions, real yields on US Treasuries — which strip out expectations for inflation — have dropped to all time lows of -1%.

This move “is the direct consequence of all of the central bank support”, said King. “It is the main force driving investors to pile into risky assets” such as gold and cryptos, both of which are at or near all time highs.

via ZeroHedge News https://ift.tt/3fkTEWv Tyler Durden

The lockdown in the wake of the coronavirus pandemic has accelerated the implementation of long-held plans to establish a so-called new world order. Under the auspices of the World Economic Forum (WEF), global policymakers are advocating for a “Great Reset” with the intent of creating a global technocracy. It is not by coincidence that on October 18, 2019, in New York City the WEF participated in “Event 201” at the “high-level” pandemic exercise organized by the John Hopkins Center for Health Security.

This coming technocracy involves close cooperation between the heads of the digital industry and of governments. With programs such as guaranteed minimum income and healthcare for all, the new kind of governance combines strict societal control with the promise of comprehensive social justice.

The truth, however, is that this new world order of digital tyranny comes with a comprehensive social credit system. The People’s Republic of China is the pioneer of this method of surveillance and control of individuals, corporations, and sociopolitical entities.

For the individual, one’s identity is reduced to an app or chip that registers almost any personal activity. In order to gain a few individual rights, and be it only to travel to a certain place, a person must balance such apparent privileges with his submission to a web of regulations that define in detail what is “good behavior” and deemed as beneficial to humankind and the environment. For example, during a pandemic, this sort of control would extend from the obligation of wearing a mask and practicing social distancing to having specific vaccinations in order to apply for a job or to travel.

It is, in short, a type of social engineering which is the opposite of a spontaneous order or of development. Like the mechanical engineer with a machine, the social engineer—or technocrat—treats society as an object. Different from the brutal suppressions by the totalitarianism of earlier times, the modern social engineer will try to make the social machine work on its own according to the design. For this purpose, the social engineer must apply the laws of society the way the mechanical engineer follows the laws of nature. Behavioral theory has reached a stage of knowledge that makes the dreams of social engineering possible. The machinations of social engineering operate not through brute force, but subtly by nudge.

Under the order envisioned by the Great Reset, the advancement of technology is not meant to serve the improvement of the conditions of the people but to submit the individual to the tyranny of a technocratic state. “The experts know better” is the justification.

The Agenda

The plan for an overhaul of the world is the brainchild of an elite group of businessmen, politicians, and their intellectual entourage that used to meet in Davos, Switzerland, in January each year. Brought into existence in 1971, the World Economic Forum has become a megaglobal event since then. More than three thousand leaders from all over the world attended the meeting in 2020.

Under the guidance of the WEF, the agenda of the Great Reset says that the completion of the current industrial transformation requires a thorough overhaul of the economy, politics, and society. Such a comprehensive transformation requires the alteration of human behavior, and thus “transhumanism” is part of the program.

The Great Reset will be the theme of the fifty-first meeting of the World Economic Forum in Davos in 2021. Its agenda is the commitment to move the world economy toward “a more fair, sustainable and resilient future.” The program calls for “a new social contract” that is centered on racial equality, social justice, and the protection of the nature. Climate change requires us “to decarbonize the economy” and to bring human thinking and behavior “into harmony with nature.” The aim is to build “more equal, inclusive and sustainable economies.” This new world order must be “urgently” implemented, the promotors of the WEF claim, and they point out that the pandemic “has laid bare the unsustainability of our system,” which lacks “social cohesion.”

The WEF’s great reset project is social engineering at the highest level. Advocates of the reset contend that the UN failed to establish order in the world and could not advance forcefully its agenda of sustainable development—known as Agenda 2030—because of its bureaucratic, slow, and contradictory way of working. In contrast, the actions of the organizational committee of the World Economic Forum are swift and smart. When a consensus has been formed, it can be implemented by the global elite all over the world.

Social Engineering

The ideology of the World Economic Forum is neither left nor right, nor progressive or conservative, it is also not fascist or communist, but outright technocratic. As such, it includes many elements of earlier collectivist ideologies.

In recent decades, the consensus has emerged at the annual Davos meetings that the world needs a revolution, and that reforms have taken too long. The members of the WEF envision a profound upheaval at short notice. The time span should be so brief that most people will hardly realize that a revolution is going on. The change must be so swift and dramatic that those who recognize that a revolution is happening do not have the time to mobilize against it.

The basic idea of the Great Reset is the same principle that guided the radical transformations from the French to the Russian and Chinese Revolutions. It is the idea of constructivist rationalism incorporated in the state. But projects like the Great Reset leave unanswered the question of who rules the state. The state itself does not rule. It is an instrument of power. It is not the abstract state that decides, but the leaders of specific political parties and of certain social groups.

Earlier totalitarian regimes needed mass executions and concentration camps to maintain their power. Now, with the help of new technologies, it is believed, dissenters can easily be identified and marginalized. The nonconformists will be silenced by disqualifying divergent opinions as morally despicable.

The 2020 lockdowns possibly offer a preview of how this system works. The lockdown worked as if it had been orchestrated—and perhaps it was. As if following a single command, the leaders of big and small nations—and of different stages of economic development—implemented almost identical measures. Not only did many governments act in unison, they also applied these measures with little regard for the horrific consequences of a global lockdown.

Months of economic stillstand have destroyed the economic basis of millions of families. Together with social distancing, the lockdown has produced a mass of people unable to care for themselves. First, governments destroyed the livelihood, then the politicians showed up as the savior. The demand for social assistance is no longer limited to specific groups, but has become a need of the masses.

Once, war was the health of the state. Now it is fear of disease. What lies ahead is not the apparent coziness of a benevolent comprehensive welfare state with a guaranteed minimum income and healthcare and education for all. The lockdown and its consequences have brought a foretaste what is to come: a permanent state of fear, strict behavioral control, massive loss of jobs, and growing dependence on the state.

With the measures taken in the wake of the coronavirus pandemic, a big step to reset the global economy has been made. Without popular resistance, the end of the pandemic will not mean the end of the lockdown and social distancing. At the moment, however, the opponents of the new world order of digital tyranny still have access to the media and platforms to dissent. Yet the time is running out. The perpetrators of the new world order have smelled blood. Declaring the coronavirus a pandemic has come in handy to promote the agenda of their Great Reset. Only massive opposition can slow down and finally stop the extension of the power grip of the tyrannical technocracy that is on the rise.

via ZeroHedge News https://ift.tt/39Rgcx8 Tyler Durden

Xi’s Decision To Turn Inward Is Dangerous For Trade Tyler Durden

Sun, 08/02/2020 – 21:35

By Ye Xie, Bloomberg macro commentator

Three things we learned last week:

1. A major pivot by Xi has China turning inward

At the Politburo meeting on Thursday, President Xi Jinping reiterated his recent call for “dual circulation,” emphasizing self-sufficiency in supply and demand. The combination of a weak global economy and anti-China sentiment in the West means China has to rely more on itself. The shift suggests China will substitute some imports, including technology, with local supply, and reorient some exports to domestic markets. In other words, global trade, which is already contracting, is likely to remain sluggish due to Xi’s pivot inward. This isn’t good news for countries that sell to China, including Germany and most emerging markets. The chart below shows how closely correlated China and U.S. imports are to the performance of global stocks.

Trade data this week is likely to confirm that imports and exports remain weak in China.

2. Dollar’s decline is about to slow down

The Bloomberg Dollar Index fell to a two-year low last week. But its decline may start to slow. The pandemic is showing signs of leveling off in the U.S., and it’s picking up in other countries, including Spain and Japan. A reversal of the virus’s trend globally would remove one of the negatives for the dollar. European stocks underperformed the U.S. last week, underscoring that the dynamics may already be at play.

Still, investors are bracing for radical changes in the Fed policy in September, which sent five-year Treasury yields to record lows. The long-term structural weaknesses for the dollar — including valuation and twin deficits — are still there. That means any respite is likely to be short-lived for the U.S. currency.

3. Volatility may pick up in August with a looming fiscal cliff in the U.S.

The U.S. and Europe posted record GDP contraction last quarter. And American jobs data this week is likely to show that employment growth slowed significantly in July. While most companies have managed to beat low expectations for their earnings, U.S. lawmakers are struggling to pass another economic relief package, and the extra federal unemployment benefits of $600 a week that had been helping to prop up the economy have expired. Expect some volatility in August — that’s when it tends to pick up.

Things to Know:

China’s ByteDance Ltd. is prepared to sell its music-video app TikTok’s U.S. operations after President Trump threatened to order the move, according to people with knowledge of the situation

The grace period for wealth management rules will be extended to the end of 2021 due to impact of the coronavirus on the finance industry, China’s central bank said in a statement

Hong Kong delayed a key Legislative Council election scheduled for September for a year due to a recent surge in Covid-19 cases, fueling more outrage among the city’s opposition

The U.S. Treasury announced sanctions against a Chinese company and two individuals linked to it, amid tensions between the two nations over issues ranging from trade to Beijing’s treatment of ethnic minorities

Gold surged to a fresh record, fueled by a persistent dollar weakness and low interest rates

via ZeroHedge News https://ift.tt/31cT883 Tyler Durden

Vaccine Hunt: Is Injecting Human Volunteers With COVID-19 Ethical? Tyler Durden

Sun, 08/02/2020 – 21:10

In the race to find a vaccine for COVID-19, an ethical debate is brewing over whether it’s justifiable to deliberately infect healthy volunteers with the disease in the hopes of achieving a scientific breakthrough sooner, according to the South China Morning Post.

A patient in the US state of New York is injected with a possible Covid-19 vaccine in the world’s largest clinical study. Photo: AP

And while consenting adults should be allowed to take whatever risks they want, there’s a known unknown regarding this relatively new illness – namely, why do most people who contract coronavirus range from asymptomatic to ‘worst flu of my life,’ only to fully recover, while others – known as ‘long haulers‘ – remain ill for months, experiencing ‘waves’ of debilitating symptoms with no end in sight.

We don’t know much about long haulers – particularly one’s chances of becoming one if infected with COVID-19.

Deliberately infecting people for research is done through what’s known as a “human challenge trial” (HCT) – which can be done concurrently with phase III vaccine trials. Deciding on HCTs for COVID-19 will be a panel of experts at the World Health Organization (WHO) – which includes Wuhan ‘Bat Woman’ Shi Zhengli, whose lab has fallen under suspicion as the source of the COVID-19 outbreak despite her repeated denials.

The advisory panel must contend with three ‘particularly contentious’ questions, according to SCMP:

First, should such trials be carried out even if there is no cure for Covid-19?

Second, the most probable HCT trial would recruit young, healthy volunteers to minimise the chance that they might die or become seriously ill after infection. But studies have found that elderly people, the group most vulnerable to the disease, are less responsive to vaccines. So, would it be worth the potential risks to find a vaccine that may not work for those who need it most?

Third, would human challenge trials shorten the time to discover a vaccine? Would scientists gain any distinct advantage by exposing volunteers to the risks?

The experts in the WHO advisory group were split on the first and third questions, while the majority thought elderly people might not benefit from the findings of the trials. How Shi voted on these questions was not known. She did not reply to an email query from the South China Morning Post. –SCMP

In 2016, an ethics committee denied a proposal to use HCTs on a Zika virus vaccine over concerns of the risks it posed to volunteers and their sexual partners.

“The right question is whether challenge trials would increase study participants’ likelihood of similar bad outcomes, compared to two alternative scenarios: non-participation in any trial and participation in standard efficacy trials for the same vaccines,” posed Nir Eyal, a biomedical ethicist at Rutgers Global Health Institute.

At present, a total of 32,665 people from 140 countries have signed up as volunteers for a potential HCT organized by volunteer group 1Day Sooner.

“We see considerable potential in the use of human challenge studies to accelerate Covid-19 vaccine development, [to help filter] and validate the best candidate vaccines, and optimise vaccination approaches,” said Professor Adrian Hill, director of Oxford University’s Jenner Institute – who is collaborating with 1Day Sooner to prepare for possible HCTs in addition to phase III clinical trials.

Illustration: Perry Tse

“We’re hoping to be doing challenge trials by the end of the year,” Hill told The Guardian. “This might be in parallel or might be after the phase-three trial is completed. They’re not competing options, they’re complementary.“

Abie Rohrig, a spokesman for 1Day Sooner, said no volunteers had asked to withdraw, despite some new findings pointing to possible long-term damage to organs such as the kidneys, heart and nerves, although they were rare among young adults.

“I have not heard from any volunteers about withdrawing because of these risks. Every volunteer I have personally spoken with understands that there is a large degree of uncertainty with respect to Covid-19, and they are willing to take on that uncertain risk in a challenge trial,” Rohrig said. -SCMP

Meanwhile, over 150 scientists and academics, including 15 Nobel laureates, have signed an open letter to the Director of the US National Institutes of Health, Francis Collins, asking the US government to collaborate with international teams to prepare for HCTs. That said, they also called for a ‘high-quality ethical review’ before they could start, according to the report.

“HCTs for Covid-19 have a tremendous amount of advocacy behind them that is unprecedented, for two main reasons. First, the advocacy group 1Day Sooner has been working hard to keep media attention focused on HCTs. Second, the widespread damage that has already been done by Covid-19 leaves the public grasping for any way to speed up vaccine development,” said Northwestern University bioethicist, Seema Shah – the primary author of the Zika ethics panel report.

Some scientists, however, have voiced serious concerns over whether the risks to volunteers is justified.

In an opinion piece published on the US medical website STAT, Michael Rosenblatt, chief medical officer of Flagship Pioneering and former chief medical officer of pharmaceutical giant Merck, wrote: “These authors, like 1Day Sooner’s volunteers, are well-intentioned but wrong.”

Rosenblatt, who is also an adviser to Moderna, said HCTs took months to prepare and Covid-19 vaccine development would not be accelerated by testing young volunteers.

“The volunteers might end up having risked their own health without truly helping those who are in greatest need of vaccine protection,” he said, referring to the elderly.

“An equally disturbing scenario is what if one of the first volunteers dies, either due to the play of chance, a problem with the vaccine, or the individual’s genetic make-up? This is unlikely to happen, but it can, and did, in another setting with consequences that stretched far beyond the single tragic death,” he wrote. He was referring to the death of an 18-year-old volunteer in the first gene therapy trials in 1999. The death put similar research on hold for years. -SCMP

What’s more, since no ‘weakened’ SARS-CoV-2 strains have been manufactured for use in HCTs, volunteers would be injected with ‘wild strains.’

“If HCTs are green-lighted now, when there is substantial uncertainty about the risks, they could set a new precedent for the level of risk and uncertainty that is tolerated in research,” said Shah. “If there are bad outcomes in these trials, or if the vaccines tested in them have safety issues when given to the general public, HCTs could hurt public trust in vaccines in the longer term.”

via ZeroHedge News https://ift.tt/30mZMcB Tyler Durden

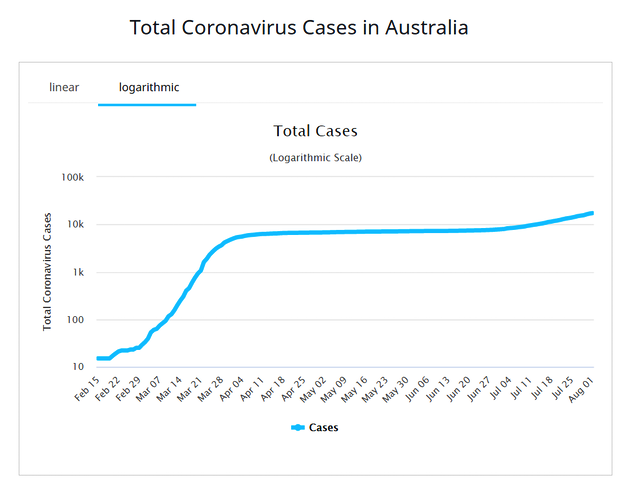

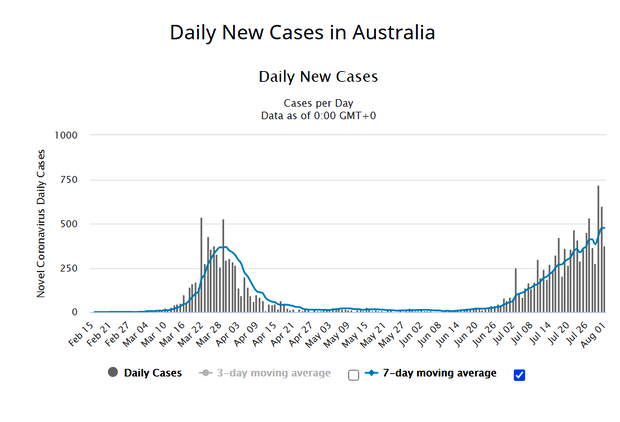

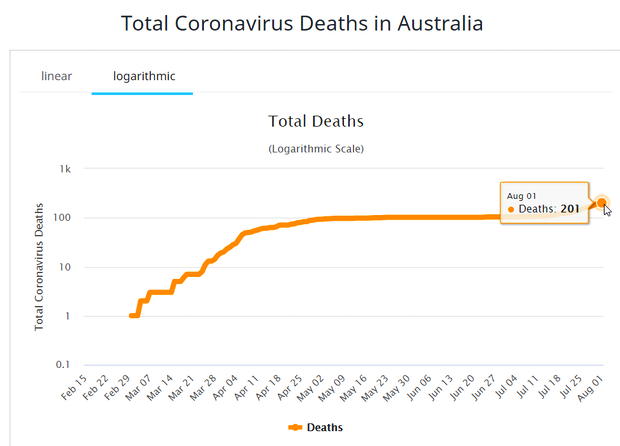

The premier of Victoria plunged the region into a “state of disaster” on Sunday, announcing even stricter lockdown measures, introducing a nightly curfew and banning virtually all trips outdoors after Australia’s second largest state recorded 671 new infections in a single day.

Daniel Andrews told Victorians at a news conference that “we have to do more, and we have to do more right now,” as the state battles to contain a devastating coronavirus outbreak that had already stripped residents of their freedoms, livelihoods and social interactions and made it an outlier from the rest of the country.

New Rules

“Where you slept last night is where you’ll need to stay for the next six weeks.“

Curfew between 8 p.m. and 5 a.m.

Only one person per household will be allowed to leave their homes once a day — outside of curfew hours — to pick up essential goods, and they must stay within a 5 kilometer radius of their home unless nearest shop is over 5 KM away.

Exercise can be taken for up to an hour a day, with one other person, but still within five kilometers of a person’s home.

What’s Going On?

Australia Total Covid Cases

Daily New Cases

Total Coronavirus Deaths

Questions of the Day

Do these measures fit the outbreak?

What if someone was in a hotel? Someone else’s house?

I expect there are some exceptions but we have not seen anything like this outside of China and a few cities in Italy.

“If we were to lock down hard for a month or six weeks, we could get the case count down so that our testing and our contact tracing was actually enough to control it,” Kashkari said.

Fed Independence?

The Fed hollers every time Trump or Congress meddles in monetary policy, but the Fed repeatedly meddles in fiscal policy.

And here’s a new one: The Fed is willing to interject its beliefs about medical policy as well.

via ZeroHedge News https://ift.tt/30jAkVo Tyler Durden

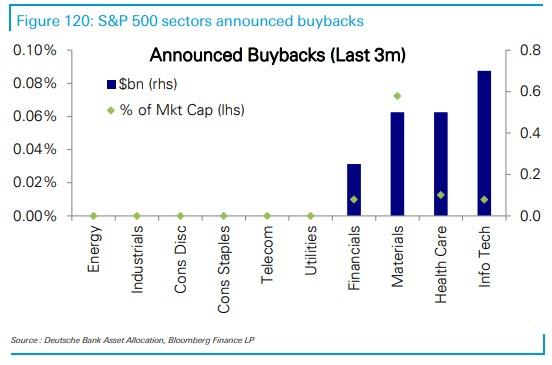

Two months ago, we showed that contrary to conventional wisdom and corporate reps and warrants that buybacks had effectively been put on hold for the duration of the covid pandemic, not only were companies still repurchasing their shares but it was the tech names – those who have stormed higher since the March lows – that were the biggest culprits.

Now, two months after we first revealed Wall Street’s worst kept secret, the Financial Times has also noticed that Corporate America is finding it hard to kick the share buyback habit, even after the US slipped into its worst recession in decades.

While total buybacks are indeed expected to drop this year as the downturn caused by coronavirus saps corporate profits, companies in the S&P 500 that have reported second-quarter earnings so far have reduced the number of their outstanding shares by an average of 0.3 per cent from the previous quarter, according to calculations from Credit Suisse.

Furthermore, updates showed that some of the largest US multinationals continued to buy back their own stock or even accelerated stock repurchases and nowhere more so than the tech names we first highlighted at the end of May.

Take Google’s parent company Alphabet, which spent $6.9bn on buybacks for the quarter, up 92% from a year prior, the company revealed in its earnings results last Thursday.

Microsoft, the second-largest listed US company, purchased $5.8bn of its own stock in the period, up 25% from a year earlier, and likely among the chief reasons for the stock’s amazing surge.

Elsewhere, Biogen spent $2.8bn on buybacks for the period, up 17% from last year, WR Berkley, an insurer, did not buy any of its shares in the second quarter last year, but spent $97m on its stock in the period this year, and Celanese increased its planned buybacks for the year by $500m to $1.5bn in July, after selling its stake in a Japanese joint venture.

Of course, the biggest source of buybacks was once again Apple, which repurchased $16BN in the second quarter, down 6% on the period last year, though by far the biggest stock repurchaser among S&P 500 companies in recent years.

As we first noted in May, and as JPM strategist David Lebovitz echoed last week, the buybacks were “not happening everywhere”, but were “driven by specific sectors and stocks”. He added that financial and materials companies were potentially more willing to engage in buybacks through the downturn, because their stocks have not advanced as much as companies in other sectors since the lows in March.

More marquee names joined the party with Edward Jones estimating that Berkshire Hathaway plowed about $5.3bn into stock repurchases during the quarter. Berkshire reports its earnings next month and if the sum is confirmed it would mark the largest quarterly share repurchase since the company began buying back its stock in 2011.

In summary after a brief dip in Q1, the buybacks have staged an impressive rebound as shown in the chart below:

As the FT notes, companies expanding repurchase programs – which is most tech names – “run against the grain of the broader market, where many businesses reduced or suspended buybacks as the downturn took hold. Second-quarter EPS for companies in the S&P 500 will probably drop about 39%”, a number that would be even bigger had it not been for buybacks according to Refinitiv.

And while in April Goldman projected that the amount spent by S&P 500 companies could halve this year, to $371bn from a record $806bn spent on share buybacks in 2018, Goldman’s forecast may prove to be far too low, even though nearly a fifth of companies in the S&P 500 have put buyback programs on ice since March, including the big banks such as Bank of America, Wells Fargo and JPMorgan Chase, who are typically among the biggest buyers of their own stock.

In any case, the buyback spree doesn’t seem like it will end any time soon: “As long as you’re a company that is earning money greater than your borrowing rate, you can just keep borrowing and buying back shares,” said Stephen Dover, head of equity for Franklin Templeton, the San Mateo-based fund manager.

That said, sentiment may change now that buybacks have become a hot political topic, especially as Congress debated stimulus programs this spring. Joe Biden and Donald Trump have both spoken out against the practice, noting that big programs have often sucked free cash flow away from businesses, while Democratic senators Bernie Sanders and Chuck Schumer have also called for curbs.

“Scrutiny around buybacks is already happening and will continue to happen,” said Mr Dover. “It was there before the current crisis and now it’s amplified.”

via ZeroHedge News https://ift.tt/2D63S0a Tyler Durden

On second thought, maybe it was too soon. One of the first cruise ships in the world to resume sailing since the coronavirus-caused worldwide halt to cruising in March is experiencing a significant outbreak of the illness that already has sent several people to the hospital.

Norwegian expedition cruise company Hurtigruten late Friday said four sick crew members from the 535-passenger Roald Amundsen were admitted to the University Hospital of North Norway in Tromsø, Norway, earlier in the day after the vessel docked in the city. All four had tested positive for COVID-19. On Saturday, the line said another 32 crew members had tested positive for the illness.

The Roald Amundsen on Friday had just finished a seven-night sailing out of Tromsø to the Arctic’s wildlife-filled Svalbard archipelago.

The Roald Amundsen

All four of the hospitalized crew members had been sick for several days while on board the vessel, and all four had been placed in isolation. But the line said their symptoms weren’t consistent with COVID-19. They only tested positive for the illness after the ship docked in Tromsø early Friday.

It’s unclear if the crew members are seriously ill, or if they only are being hospitalized as a way to keep them isolated.

The entire ship has now been placed in isolation, and the 154 remaining crew members on board have all been tested for COVID-19. Hurtigruten on Saturday said 122 of the crew members had tested negative for the illness.

Hurtigruten on Saturday said it had contacted all 178 passengers who left the ship early Friday, and they had been ordered to self-quarantine in line with Norwegian health regulations.

The company also has contacted another 209 passengers who were aboard the previous sailing of the Roald Amundsen, and they have been told to self-quarantine, too.

The next voyage of the vessel, which had been scheduled to begin Friday, has been canceled.

Hurtigruten has been at the forefront of efforts to restart cruising in Europe in the wake of falling coronavirus case counts across the continent. The line started cruises to Norway out of Hamburg, Germany, in June with a single ship, the 530-passenger Fridtjof Nansen. It added cruises to Svalbard on the Roald Amundsen and the 335-passenger Spitsbergen in July.

The trips only have been open to local travelers from select European countries. No Americans have been on board the vessels.

“We are now focusing all available efforts in taking care of our guests and colleagues,” Hurtigruten spokesperson Rune Thomas Ege said in a statement posted Saturday at the line’s website. “We work closely with the Norwegian national and local health authorities for follow-up, information, further testing, and infection tracking.”

Hurtigruten had implemented a wide range of new health and safety measures on Roald Amundsen and the other ships it brought back into operation, including enhanced cleaning, added medical screenings for passengers and crew, and an end to buffets. All the vessels were operating at a sharply reduced capacity, below 50% of normal, to ensure social distancing.

The measures were similar to what many lines have been touting as the solution to keeping coronavirus off ships as cruising resumes.

The Roald Amundsen trips included Zodiac landings for wildlife sightseeing in the Svalbard archipelago as well as kayaking and other expedition-related activities.

Huirgruten pioneered cruises to Svalbard in 1896.

Cruises to Svalbard and other parts of the Arctic were thought to be somewhat simpler to run during a pandemic as they don’t involve much passenger interaction with other humans. The typical Arctic voyage is an expedition-style sailing that involves landings and Zodiac excursions to see wildlife, glaciers and floating ice formations.

The Roald Amundsen currently is scheduled to begin sailings around the British Isles for U.K. residents in early September. Hurtigruten didn’t say whether those trips would go ahead.

Hurtigruten is just one of several cruise companies in Europe that have been starting to bring back sailings since June. Until now, no cruise operators in North America have resumed sailings. But one small-ship cruise company, UnCruise Adventures, plans to resume trips out of Juneau, Alaska, on Saturday.

via ZeroHedge News https://ift.tt/33jgOu1 Tyler Durden

Another Market Top Indicator: “Blank Check” IPO Issuance Explodes Tyler Durden

Sun, 08/02/2020 – 19:55

The similarities with the housing bubble boom-bust are growing by the day. Not only are stocks at all time highs, to which we can now add record low yields and an all time high gold price as the 10Y real yield just dropped to an unprecedented minus 1% all time low…

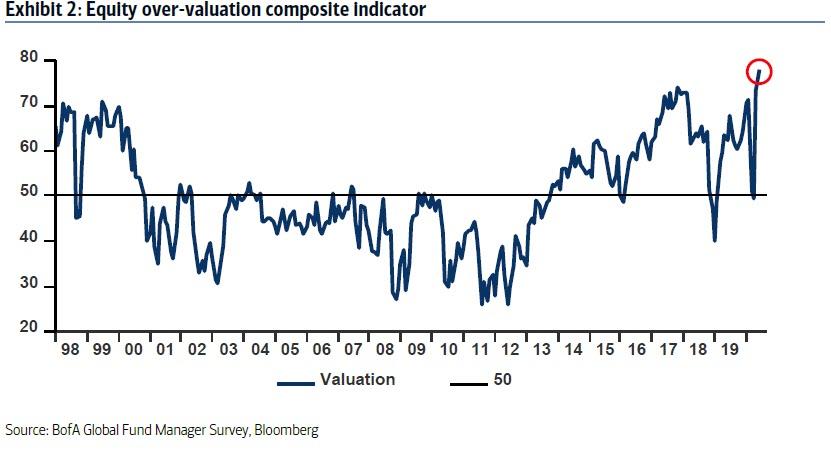

… and risk-on euphoria is rampant among the retail investing community, but over the past year there has also been a veritable explosion of “blank check” companies which are shell companies that have no operations but plan to go public with the intention of acquiring or merging with a company with the proceeds of the SPAC’s initial public offering. Investment in SPACs usually surges near market peaks, when there is broad consensus among the professional investing community that equities are overvalued as there is now – as a reminder the June Fund Manager Survey from BofA found that a record 78% of Wall Street professionals believe that stocks are overvalued.

The last time we saw such a surge in SPACs? 2007.

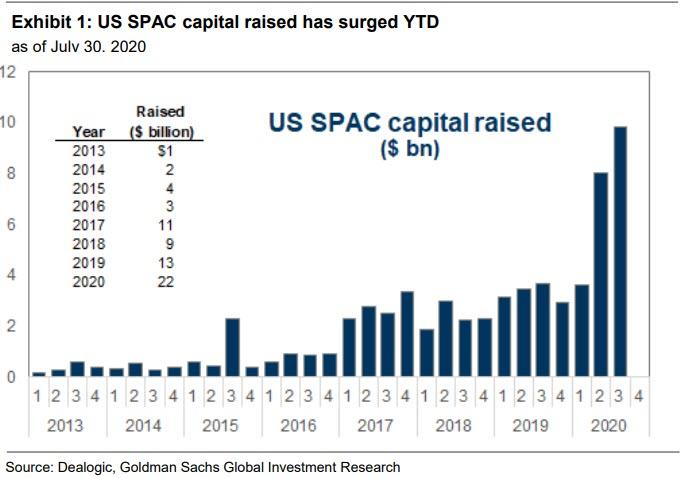

And while the SPAC bubble burst in 2008 along with the rest of the housing/credit bubble, it has slowly recovered, and as Goldman’s David Kostin writes in his latest Weekly Kickstart, SPAC capital raising has soared YTD.

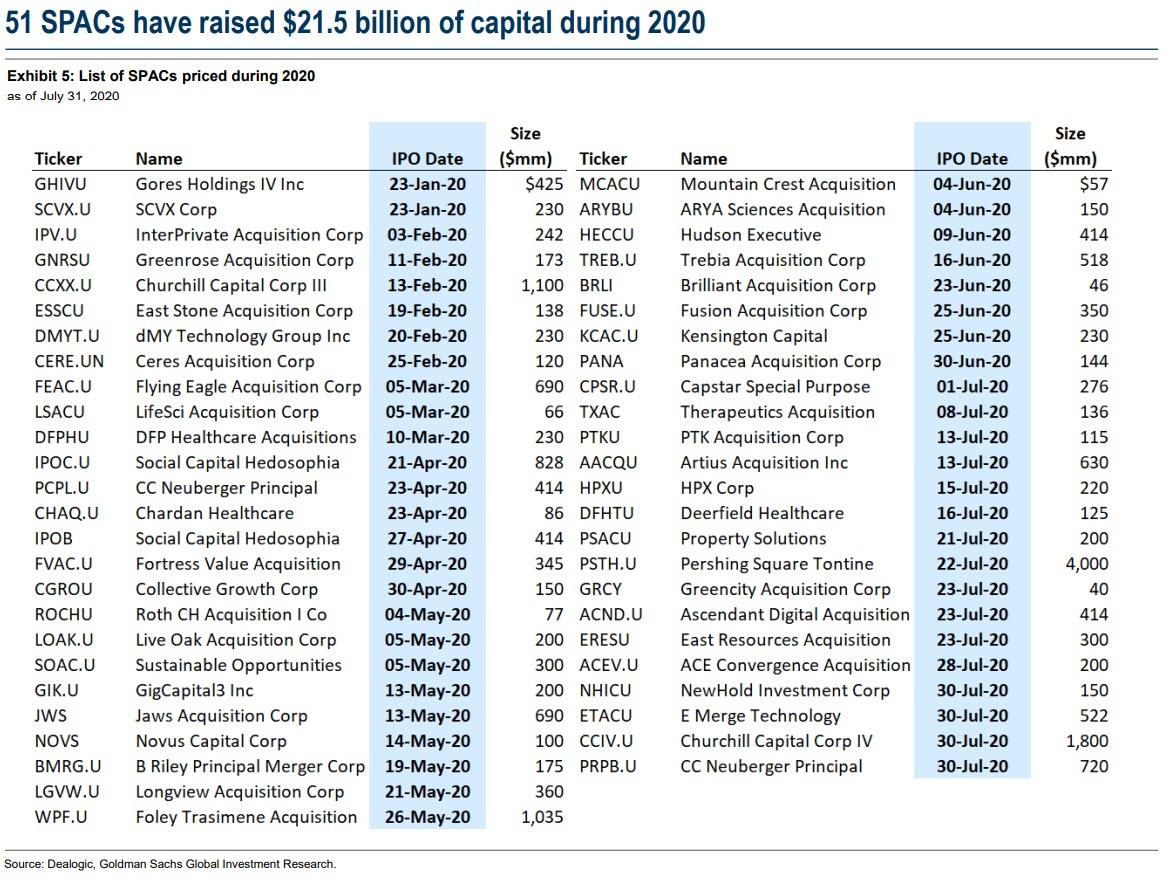

Some statistics: since the start of 2020, 51 SPAC offerings have been completed raising $21.5 billion, up 145% from the comparable year-ago period. In 2019, 51 SPAC IPOs were completed totaling $13.2 billion and 2018 witnessed 35 offerings for $9.3 billion. SPACs have accounted for one-third of all US IPO activity since the start of 2019.

As noted above, a SPAC is a “blank-check” company formed with the intention of acquiring or merging with another company. The SPAC needs to complete an acquisition within two years or the capital raised must be returned to investors, as such it mostly represents a vote of confidence in the sponsor or investor behind the SPAC and in their ability to find future deals that would generate a high ROI.

According to Goldman, completed SPAC offerings currently searching for acquisitions exceeds $38 billion. In a typical SPAC structure, the sponsor raises initial capital by issuing units consisting of 1 share and ½ or ⅓ of a warrant. The shares are generally priced at $10 and the warrants are typically struck 15% out of the money ($11.50) with a 5-year term and an $18 forced exercise.

And while by definition a SPAC is a blank-check, it comes with an embedded put option as Kostin explains:

Because the acquisition target is unknown at the time of the IPO, potential value creation is completely dependent on the ability of the sponsor to identify a target (typical private) company and negotiate the purchase. The SPAC purchase represents the de facto IPO for the acquired firm. However, in exchange for not knowing ahead of time the specific company that will be acquired, SPAC investors receive two benefits.

First, the right to evaluate the pending purchase and elect to hold or redeem the initial investment at cost (plus accrued interest) two days before the vote.

Second, warrants.

The decisions are separate. A SPAC investor may choose to retain both the shares and warrants, or redeem the shares and hold the warrants, or sell both.

The SPAC sponsor is typically compensated with a promote equal to 20% of pro forma equity and warrants. In a US SPAC, the sponsor’s promote is not contingent upon meeting any financial targets. However, the sponsors of some recent SPACs have put their equity promote into an earn-out that is only received if the company achieves certain performance objectives, further aligning the financial incentives of the SPAC sponsor and shareholders.

European SPACs are structured slightly differently. First, since they lack a redemption feature, they are truly “blank check” firms. The European SPAC investor owns the shares regardless of whether the investor likes the acquisition or not. Second, the sponsor does not receive a 20% promote up front. Instead, the sponsor only earns a promote if the company achieves certain return targets.

Once the IPO is complete, and the SPAC sponsor – now with millions in fresh funds in the bank – finds a suitable target, he or she negotiates a non-binding term sheet. Depending on the size of the transaction, the sponsor may wall cross potential new outside investors to raise a PIPE (private investment in public equity). The transaction is then announced to the public and an 8-K is filed.

Curiously, the SPAC investor base is highly fluid and as Goldman writes, many SPACs experience nearly a full rotation in their shareholder base during the time between the announcement of the deal and closing of the acquisition (transition from merger arbitrage traders and hedge funds to longer-term fundamental investors).

The sponsor will then file a proxy with the SEC, conduct a pre-merger roadshow, receive redemption notices (if any), and hold a shareholder vote. Redemption notices are due 2 days prior to the shareholder vote, and shareholders will typically determine whether or not to redeem based on where shares are trading at the time redemption notices are due. If the vote passes, the SPAC merges with the target company and will often undergo a ticker change to reflect the name of the target business.

On the other hand, if the vote fails, the sponsor will resume searching for a suitable target. After 24 months from the capital raise the SPAC will be closed and the capital returned to investors if a merger has not been completed.

So why the interest in SPACs?

As Goldman explains, from a capital raiser’s perspective SPACs offer companies a path to the public markets as an alternative to a traditional IPO. Two features of the SPAC process are notable: Forecasts and proceeds.

First, in the traditional IPO process, issuers are prohibited from including any forward-looking guidance in their Form S-1 registration. As a result, prospective investors are required to evaluate the merits of an issue based on backward-looking results and their own expectations. In contrast, the SPAC due diligence process allows a target company to present forecasts and enhances the ability of a SPAC to acquire early-stage companies or those with complicated business models. This can be useful in businesses like sports betting, cannabis, electric vehicles, or other nascent industries that lack meaningful comparisons in the traditional IPO market. Of course, it is a given that the target company will present the most optimistic projections to potential investors, which is why removing the investor diligence aspect of the process is usually a sign of complacent groupthink whereby the investor base is willing to believe anything the target company presents similar to how i) rating agencies assessed all pre-crisis debt as stellar even if it was generally garbage and ii) investors are willing to engage in groupthink when someone else does their “diligence” job for them.

Second, in a traditional IPO, the amount of new capital raised is limited, typically to 20%-25% of the value of a company. But in a SPAC transaction, no limit exists on potential proceeds. A SPAC may acquire a majority or minority interest in the target firm and the concurrent PIPE capital raise may be any size.

According to Goldman, whose taks is to spin SPACs as an attractive investment opportunity instead of yet another market top signal, investing in SPACs – from a portfolio manager’s perspective – “offers upside potential with downside protection.” And yes, ultimately, the upside potential is a function of the sponsor’s ability to identify the target, negotiate terms, inject needed external capital, and create long-term value. Which of course is also an admission by the provider of capital that they can’t find any other attractive investment opportunities and the money is bestowed upon someone who supposedly is good at finding the kinds of deals that have become especially scarce in the public markets. Meanwhile, the redemption option limits downside.

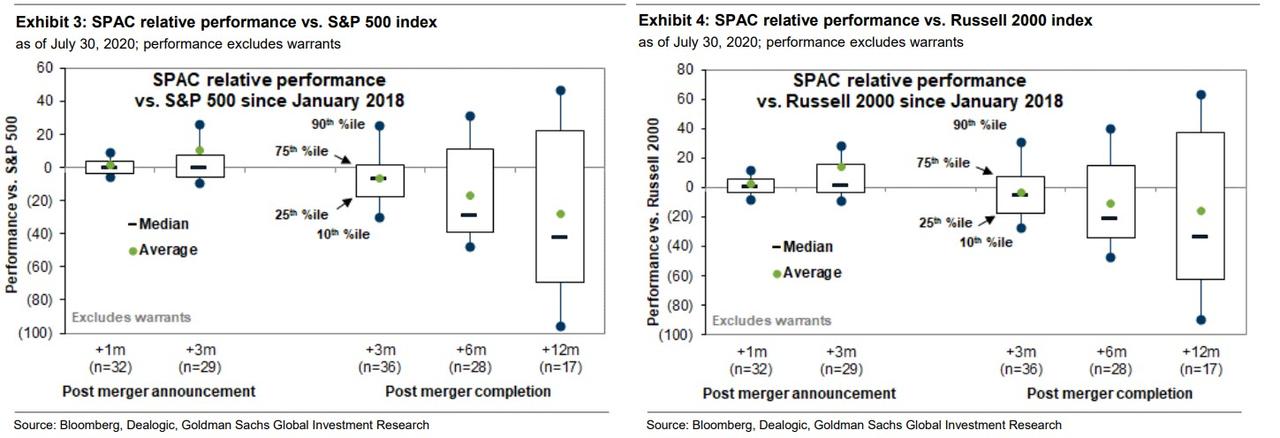

Some more statistics: Goldman analyzed 56 SPACs that completed mergers/de-SPAC transactions since January 2018. Tech and Industrials dominated the targets, followed by Energy and Financials.

The typical deal value was $920 million. During the 1-month and 3-month periods following the acquisition announcement, the average SPAC outperformed the S&P 500 by 1 percentage point and 11 %, respectively, and beat the Russell 2000 by 6% and 15%, respectively. That’s the good news.

Now the bad news: the average SPAC underperformed both indexes during the 3, 6, and 12-months after the merger completion.

As shown in the chart above, the performance distribution is extremely wide, with the 75th percentile SPAC outperforming the S&P 500 by 22% while the 25th percentile transaction lagged by 69%. The comparable returns vs. Russell 2000 were from +37% to -63 %.

In other words, just like with regular IPOs, SPAC returns are a coin-toss and since they tend to underperform the broader market several months after the merger and after the initial euphoria fades one may as well just buy the SPY, which unlike a SPAC, is now actively managed by the Fed whose mandate is to never allow another market drop again. It’s also another indicator that a market top has been reached, although while in the past this would be a signal to take profits at this time – when the Fed is actively managing equity risk and making any material declines virtually impossible – this time is not only different, but the recent explosion in SPACs issuance may simply be an indicator to add on even more risk, with the Fed’s blessing of course.

via ZeroHedge News https://ift.tt/3k5688n Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}