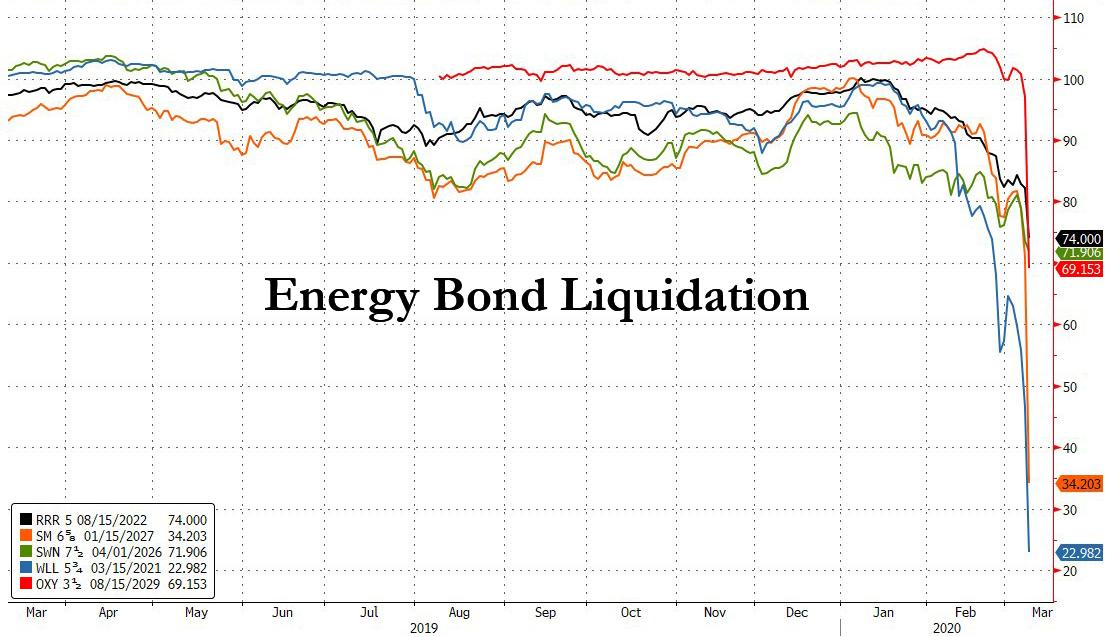

Here Are The Energy Bonds Getting Crushed This Morning

With oil prices cratering by almost a third, the math is simple: junk-bond (and in some cases IG) funded shale producers, which were already cash flow negative when WTI was trading around $50, are about to become cash incineration machines and will almost certainly be forced to default in the coming months – perhaps as soon as the next interest payment, certainly by the next bond maturity which they will no longer be able to rollover as the junk bond market is now frozen – unless oil somehow stages a miraculous recovery from here.

As such, the market was focused on how shale-linked bonds will react to this weekend’s oil price shock. Addressing this issue, Goldman sent an email early on Monday in which the bank made the following points for those looking at energy debt:

Credit markets were having problems before the Saudi announcement, credit down when equities traded higher

Significant increase in non-credit accounts looking to short the sector last week

Last week saw record outflow across IG, high yield and loans

Liquidity issue even more prevalent because of virus related contingency / BCP planning

The bank concludes by noting that “although clients are better positioned than in 2015 (when had a lot of energy issuance to fund shale revolutions); expect continued selling as oil re-prices lower and the virus spreads.”

That said, much of the selling appears to have already taken place this morning, with select energy bonds already in freefall as of this morning, including issues from Range Resources, SM Energy, Southerwestern Energy, Whiting Petroleum and Oxy.

Yet despite the sudden repricing of stressed energy bonds lower, one can again note that energy credit was well ahead of the oil market, which has finally caught down to the HY Energy OAS spread.

Expect many more E&P bonds to join the liquidation fray before the day is over.

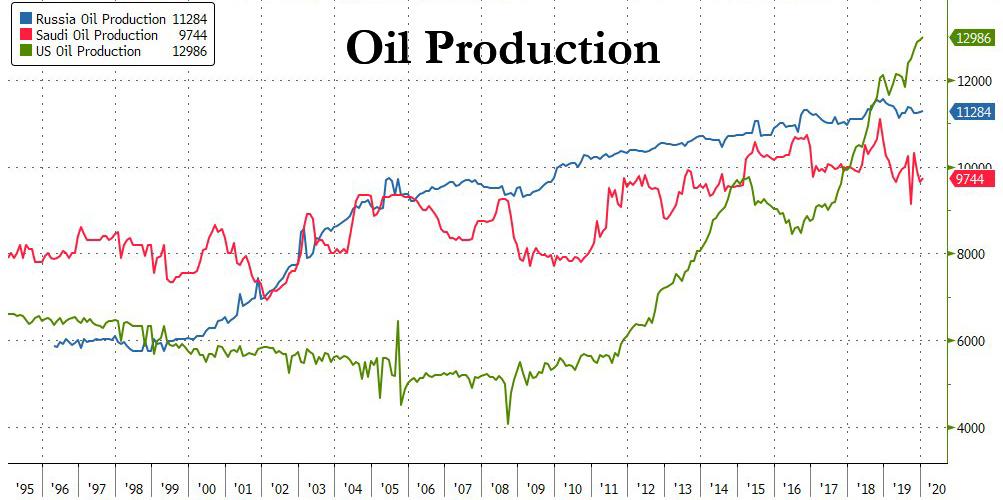

Russia Says It Can Weather $25 Oil For Up To 10 Years

Now that both OPEC+ and OPEC no longer exist, and it’s a free-for-all of “every oil producer for themselves” and which Goldman described as return to “the playbook of the New Oil Order, with low cost producers increasing supply from their spare capacity to force higher cost producers to reduce output”, the key question is just how long can the world’s three biggest producers – shale, Russia and Saudi Arabia…

… sustain a scorched-earth price war that keep oil prices around $30 (or even lower).

While we hope to get an answer on both Saudi and US shale longevity shortly, and once the market reprices shale junk bonds sharply lower, we expect the US shale patch to soon become a ghost town as money-losing US producers will not be solvent with oil below $30, assuring that millions in supply will soon be pulled from the market, moments ago we got the answer as far as Russia is concerned, when its Finance Ministry said on Monday that the country could weather oil prices of $25 to 30$ per barrel for between six and 10 years.

The ministry said it could tap into the country’s National Wealth Fund to ensure macroeconomic stability if low oil prices linger. As of March 1, the fund held more than $150 billion or 9.2% of Russia’s growth domestic product.

Incidentally, this may explain why over the past two years, Putin has been busy dumping US Treasury and hoarding gold: he was saving liquidity for a rainy day, and as millions of shale workers are about to find out today, it’s pouring.

Over the course of the last few hours, we have been moving back and forth between being aghast at the market carnage, and all it might imply, and feeling agonizingly anxious about missing out on the rebound sure to be coming. Those are big emotional swings even by this market’s standards. There’s nothing wrong with trying to follow the momentum of the moment, but don’t mistake it for careful analysis. Whatever asset prices decide to do for the balance of the day will only be obvious in retrospect. And don’t let anyone tell you otherwise.

Do a lot of things suddenly look cheap compared to where they appeared temptingly priced for a buy last Friday? You bet. But, most likely, only if you weren’t long them over the weekend. This is fundamental news being mixed in with position liquidation. And how much is one versus the other is still anyone’s guess. Moves of this size beget big swings. Lots of opportunity, by definition. But those gyrations, also, have less informative value than would normally be assumed.

Day traders are looking to capitalize on a V-shaped recovery. Not of the economy but in the market, as people chase the price action. Investors, on the other hand, have to consider whether or not systemic risks have changed the asset valuation calculation. Are the risks of recession different than we thought? Is there a greater likelihood that the much-pined-for fiscal stimulus will be coming?

My guess is that the pull of looking to buy the dip and rely on official intervention is such that traders will have a hard time resisting the urge to jump in. The test will be if they can stay disciplined enough not to spend their day buying high and selling low. If you are day trading, stick with intraday charts.

There will be a lot of things mispriced versus other things. That is an unavoidable by-product of generalized panic moves. Picking out the winners from the “Which one doesn’t belong” game will become far easier the more things calm down. Until then, the game remains “Correlation of One.” There are assets out there that are screaming not to be lumped in with everything else. It isn’t always clear which bucket any particular one belongs in.

If you had told me that 30-year Treasuries would trade where they currently are, I’d have said that’s crazy. They suddenly don’t seem so terribly out of whack given the state of things. Especially with bunds yielding what they do. The dollar, on the other hand, looks wrong to me. But there are no shortage of people willing to take the other side of that debate. The bonds are repricing to the facts as we currently see them. The dollar strikes me as getting the story wrong. But it wouldn’t make the P&L impact any less. Or the need to leave stops any less important. Like it or not.

We’ve already begun the rate-cut discussion. It strikes me as wholly premature.

There’s a big difference between being proactive and in full-out panic mode. The Fed did just move less than a week ago.

The fed fund futures are now pricing a 73% chance the Fed cuts to zero next week.

So, cut to zero is now the consensus call.

Note markets are so extreme that that Bloomberg’s WIRP is NOT correct.

But we’ve been conditioned to think that is the default option in all cases. I’m curious to see if there is a noticeable reaction mid-morning if they opt to wait and see. Another reason this won’t be as easy a day as some think. A lot of traders are looking to try to fade what seems to them to be excessive moves.

But, curiously, perhaps tellingly, not many are saying, “If you liked it up there…”

With Futures Limit-Down, ETFs Suggest Bloodbath In Stocks, Credit Is Even Worse

In the words of CNBC, US equity futures have been stable (limit down at 5%) for hours. That joke of a comment is entirely crushed by the fact that ETFs suggest the fall is dramatically worse.

SPY (the largest and most liquid S&P ETF) is down over 7% in pre-market…

VIX futures are topping 52…

And HYG – the HY Corporate Bond ETF – is crashing over 5.5% to Dec 2018 lows, signaling spreads are set to explode…

Goldman sees four main factors driving the stress in credit:

1. Credit markets were having problems before the Saudi announcement, credit down when equities traded higher

2. Significant increase in non-credit accounts looking to short the sector last week

3. Last week saw record outflow across IG, high yield and loans

4. Liquidity issue even more prevalent because of virus related contingency / BCP planning

And they suggest that although clients are better positioned than in 2015 (when had a lot of energy issuance to fund shale revolutions); expect continued selling as oil re-prices lower and the virus spreads.

And energy bonds are utterly collapsing…SM Energy bonds -$36!!

As a reminder:

If the S&P 500 declines 7%, (208 points), trading will pause for 15 min

If declines 13%, (386 pts) trading will again pause for 15 mins

If falls 20%, (594 pts) the markets would close for the day.

“Calamity”: Nomura Warns Or VaR Shock Adding To “Untradeable Markets”

Over the weekend, in our initial response to the shocking Saudi “scorched earth” price war declaration, we said that “once Brent craters on Monday to the mid-$30s or lower, the accompanying implosion in 10Y yields could make the record plunge in yields seen on Friday a dress rehearsal for what could be the biggest VaR shock of all time.“

Sure enough, among the many panic touchpoint on Monday morning which have seen virtually every risk market in persistent liquidation, Nomura’s Charlie McElligott writes that the fresh VaR shock is adding to “undtradeable markets” as the crude price shock adds to cross-asset VaR-down as traders are forced to liquidate a substantial portion of their long books; Amid the chaos, Fed Funds futures are pricing 100bps of cuts by end of month, with systematic/CTA models showing Nasdaq is set to sell/deleverage large dollar notional from what was the last of the legacy “+100% Longs” in Equities, with McElligott warning that this “probable Nasdaq puke comes at a dangerous seasonal for “Momentum” factor, where April is the worst monthly return for the factor back to ’84.“

* * *

Taking a step back, it all started with oil, and specifically the start of the Saudi price war, which sent Brent and WTI -31% in last night’s reopen, both currently trading around -20.0%.

Why such an “outsized” move in Crude? As the Nomura quant explains, adding to what we already said about the commodity’s forced selling threat, “crude is particularly exposed to “Negative Gamma” shocks due the inherent and massive “Commercial” nature of (downside) hedgers in the space—so on top of already being an illiquid mess in the futures contract, then imagine being a market maker who has sold Puts to major E&Ps and was already staring into the abyss after the last two weeks’ -25% move…now having to sell futures deep in-the-hole of the reopen gap lower last night/today.“

The oil puke triggered “cross-asset pandemonium”, as dealers in both Cash- and Vol- space are already operating under the abovementioned “VaR-down” reality via Coronavirus-tied risk- and staffing- curbs which are choking-off market liquidity to even more extreme levels. Among the key cross-asset observations highlighted by McElligott are:

With the addition of yet another “macro shock” catalyst, UST futures/Rates experienced yet-another illiquid “negative convexity” shock overnight, as for context we saw UST 10Y yields down to 31bps (currently 48bps), while UST 30Y yields plunged 59bps from reopen level to the 0.69% low (currently 90bps)

White ED$ (Mar and Apr) are seeing another insane +~23 ticks move as yet more “emergency cuts” are expected from markets to offset rapidly tightening “financial conditions”

The VIX curve has entered a new realm of inversion while S&P e-minis go -5% “limit down” last night, which means they’re prevented from going lower until they “re-open” at 930am EST Cash trading launch

Upon S&P e-mini reopening with the US Cash markets, a 7% decline (level 1 circuit breaker, 15 min pause), 13% (L2, 15 min pause) or 20% (L3) downside move will trigger a NYSE rule 80B trading halt for both the cash equity market AND all US-based equity index futures and options, where a 20% decline in the underlying S&P 500 index will terminate trading for the remainder of the trading day in both cash AND futures / options markets

While ES remains locked, the SPY ETF is still trading and is currently at around -7%, as global indices / futs trade off the earlier “worst” levels (i.e. DAX nearly -8.4% earlier, now “just” -6.6%) with some incremental covering of dynamic hedges earlier off the back of Xinhua Twitter stating “No new indigenous COVID-19 cases reported on Chinese mainland excluding Hubei over weekend” (whether anyone believes China’s updates is a different matter).

Which brings us to what traders expect (or hope) comes next, with markets now effectively expecting another Fed emergency cut as soon as today, with 100bps of easing priced in FFs by end March…

The fed fund futures are now pricing a 73% chance the Fed cuts to zero next week.

So, cut to zero is now the consensus call.

Note markets are so extreme that that Bloomberg’s WIRP is NOT correct.

… although as Nomura notes echoing what we said last night, the real market focus remains not on “imminent” policy rate cuts to ZIRP, but instead fixated on

fiscal stimulus potentials (“Trump’s Aides Drafting Economic Measures to Combat Virus Fallout” per Bloomberg),

new liquidity measures (FX Swap Lines announced, additional / larger O/N and Term Repo ops), and

potential size- and scope- of Large Scale Asset Purchases (LSAP)—which the entire world is now expecting to be expanded in a broader asset fashion a la BoJ/ECB.

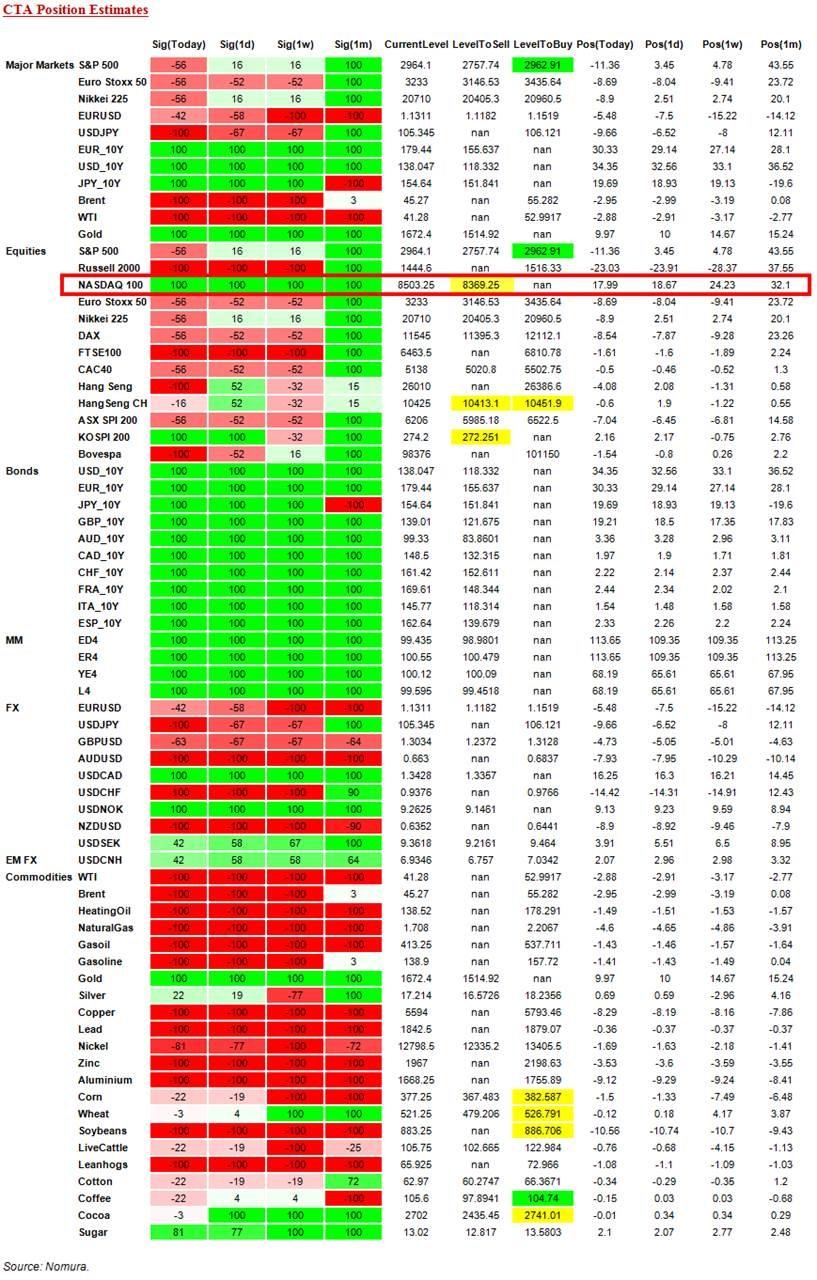

And while we wait for policymakers to start panicking (Mike Hartnett’s favorite trigger to buy, as that’s when markets to stop panicking), a quick look at the technicals, starting with CTAs, where as McElligott writes, trigger levels for Equities will “increasingly matter again as we hold lower in Stocks, because outright SHORTS are again being initiated and can thus be “grossed-up” from the recently deleveraging small notional position exposures—although more importantly today however is the legacy “+100% Long” signal in Nasdaq, which is set to deleverage size $ down to just “+16% Long” signal.” Of course, in light of the surge in VIX, it is likely that manual overrides will force CTAs into outright shorting mode:

S&P 500, currently -56.1% short, [2964.1 Friday close], more selling under 2757.74 (-6.96%) to get to -78% , max short under 2757.44 (-6.97%), buying over 2962.91 (-0.04%) to get to -20% , more buying over 3126.71 (+5.49%) to get to 57%, flip to long over 2963.2 (-0.03%), max long over 3127.01 (+5.50%)

NASDAQ 100, currently 100.0% long, [8503.25], selling under 8368.4 (-1.59%) to get to 16% , more selling under 7780.29 (-8.50%) to get to -56% , flip to short under 7781.14 (-8.49%), max short under 7017.65 (-17.47%)

A full breakdown of CTA trigger points courtesy of Nomura is below:

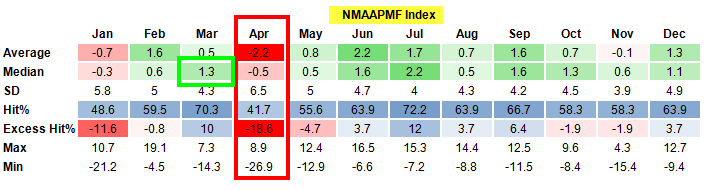

Focusing on the potential Nasdaq turmoil, McElligott writes that what is especially notable about the “last of the generals” – i.e., Nasdaq – now seeing deleveraging from CTA Trend “is that we are nearing an incredibly volatile seasonal for “1Y Price Momentum” factor (data table since 1984), where you typically see a very significant late March +++ performance dynamic for the factor before April typically sees a powerful reversal LOWER in the factor performance.“

Finally, it will probably not come as a surprise that option hedging, i.e., “Dealer Gamma” positions relative to spot have turned even more deeply “negative”, with the “flip long” line far higher, at ~3156-58 in futures…

… while the options-implied Delta position remains ridiculously “short” relative to spot (flips at 3156) and from a dollar notional perspective (-$492B, 0.9 %ile since 2013)…

… which will keep bouts of covering rallies extremely violent and will almost certainly result in another violent puke in the last hour of trading absent some central bank intervention during the day.

All across the United States people are getting really stressed out about COVID-19. Every effort to contain the virus has failed, cases have started to pop up all over America, and the latest numbers show that it is 34 times more deadly than the flu. And what makes this particular coronavirus even more frightening is the fact that it is so easy to catch. You can become infected simply by breathing in the air around you, it can live on solid surfaces for days, and some victims can carry it around for weeks before ever showing any symptoms. As this virus continues to spread, literally no public place will be safe, and that is really freaking a lot of people out.

But so far only 12 Americans have died from the virus.

If thousands start dying in this country, what is our national mood going to be like at that point?

Already, the level of stress that we are witnessing is very alarming. The following comes from an NPR article about the “national anxiety” that we are currently experiencing…

And, as the coronavirus spreads, our unanswered questions can make us feel vulnerable or fearful. “Will it come to my community” or “Am I at risk?’

“We’ve got national anxiety at the moment, a kind of shared stress, and we are all in a state of extreme uncertainty,” says Catherine Belling, an associate professor at Northwestern University, Feinberg School of Medicine, who studies the role of fear and anxiety in health care.

Of course there are very good reasons to be concerned about this virus.

More than 3,000 people have already died around the world, and the horrors that we have seen elsewhere on the globe are starting to happen here.

And with each startling headline, the level of anxiety is going to go higher.

All of a sudden, large numbers of Americans are extremely afraid to touch each other or anything around them. The following comes from a Washington Post article entitled “Coronavirus anxiety is everywhere, and there is no cure”…

America this week began to consider the existential threat of a doorknob. The horror of a touch-screen in the self-checkout lane. The inescapable doom that accompanies any trip on public transportation. The realization of how much, exactly, we all touch our faces each day: constantly.

Last week, you pressed elevator buttons with abandon. You weren’t afraid of the free weights in the gym. You washed your hands for barely enough time to say “Happy Birthday” once, let alone sing it twice.

This outbreak has already radically altered the behavior of millions of Americans, and we are probably still only in the very early chapters.

Fears about a worsening coronavirus outbreak have led shoppers in the U.S. and other hard-hit countries to begin stocking up on supplies to fill “pandemic pantries,” a new report from Nielsen suggests.

Sales of sought-after hand sanitizers have risen 73% in dollar value in the four weeks ending Feb. 22, compared with the same period in 2019, Nielsen says. Similarly, medical masks sales spiked 319%, aerosol disinfectants rose 47% and thermometers increased 32%.

If this outbreak continues to intensify, it is inevitable that shortages will begin to emerge.

So if there is something that you need to purchase, you should go get it as soon as you can.

Each new day brings more shocking revelations. On Wednesday, we found out that the number of confirmed cases in New York has risen to 11…

Another family in New York has been confirmed to have the coronavirus, Gov. Andrew Cuomo tweeted this afternoon.

The family from New Rochelle is believed to have been in contact with the 50-year old attorney, who has since been hospitalized. The attorney and his family were confirmed to have the virus earlier today.

This brings the total number of confirmed cases in New York to 11.

Sadly, Governor Cuomo is expecting many more cases to pop up, and he told the press that trying to contain this virus “is literally like trying to stop air”…

“This is literally like trying to stop air, because somebody sneezes, it’s respiratory and it’s inevitable that it will continue to spread,” Cuomo told reporters Wednesday afternoon.

Earlier in the day, Cuomo said there “were going to be many, many people who test positive.”

On the other coast, six new cases were just confirmed in Los Angeles…

As the U.S. death toll hit 11 Wednesday, Los Angeles Mayor Eric Garcetti and county officials declared states of emergency and announced six additional cases of the deadly coronavirus that has health officials around the world scrambling for answers.

More than 130 cases have been confirmed across the nation. Los Angeles had confirmed just one before Wednesday’s announcement.

A medical professional who conducted passenger screenings at Los Angeles International Airport tested positive for the coronavirus late Tuesday, according to the Department of Homeland Security and an internal email obtained by NBC News.

The person last worked screening air travelers for illness on Feb. 21, DHS said in a statement, which also said the medical professional had worn the proper protective gear while working. The internal email described the person as a “contract medical screener” for the Centers for Disease Control and Prevention.

Just like we have seen in China, medical professionals in the western world are catching COVID-19 despite attempting to take proper precautions.

That just underscores how easily this virus passes from person to person.

As this outbreak continues to intensify, it is probably inevitable that some pretty extreme measures will be taken to get it under control.

In fact, we are already seeing college basketball games get canceled…

Chicago State became the first Division I men’s basketball program to cancel games due to the coronavirus outbreak, announcing on Tuesday the decision not to travel to Seattle University on Thursday or Utah Valley on Saturday.

The University of Missouri-Kansas City declared Wednesday the Roos men’s team would not travel to Seattle for its Saturday contest against the Redhawks.

And over in Italy it was just announced that all schools will be closed until mid-March…

Italy announced Wednesday it will temporarily close all its schools and universities as the country continues to grapple with a surge in coronavirus infections, according to new reports.

Those closures will begin Thursday and last until mid-March, CNBC reported.

Can you imagine if that happened in the United States?

Of course the kids would love it, and considering the overall quality of the education in our public schools they wouldn’t miss much anyway.

Even before this outbreak started, we were living at a time of great uncertainty, and this virus has certainly taken things to an entirely new level.

We still don’t know if this will become a true global pandemic that will kill millions of people, but many prominent voices are acknowledging that it is definitely a possibility. The following comes from Piers Morgan…

Should it become a global pandemic, as many experts now fear, then the consequences could be devastating. In 1918, the H1N1 ‘Spanish flu’ virus killed between 50-100 million people.

Tech titan Bill Gates, who spends much of his time and money combatting diseases with his charitable foundation, said: ‘In the past week, coronavirus has started behaving a lot like the once-in-a-century pathogen we’ve been worried about.’

If COVID-19 does kill millions of people, it will cause fear on a scale that most of us would not even want to imagine right now.

Thanks to social media, information can spread across the globe in a matter of minutes. There is no way that global authorities will be able to keep the general public calm if things get bad enough, and health systems in the western world will be absolutely overwhelmed as multitudes of sick people swamp the hospitals.

Let us pray that such a scenario does not materialize.

But for now the numbers continue to grow at a frightening rate each day, and “coronavirus anxiety” is going to continue to grow right along with those numbers.

Boeing Crashes 10% After Report FAA May Require 737 MAX Electrical Fix Before Jet Flies Again

Just as Boeing has been beefing up its supply chain with new hires and attempting to restart 737 Max production by mid-year, the FAA is poised to require electrical wiring issues, first discovered back in December, to be fixed before the planes can return to the sky,The Wall Street Journal reported on Sunday evening.

Sources told the Journal that FAA managers and engineers have concluded that the layout of the Max’s wiring violates wiring-safety standards. The current configuration, under extreme conditions, could cause a short-circuit in the plane’s flight-control systems and lead to a crash, similar to what happened with two Max jets that killed 346 people.

A preliminary decision, which has yet to be finalized, could require the Chicago plane maker to fix electrical issues on 800 Max airlines already produced. The sources said Boeing has argued with FAA managers about the wiring setup and how it satisfies international safety standards.

The emergence of the electrical issues, and the likely need for Boeing to reroute the wires, comes as the FAA has delayed flight tests for the Max’s flight control system, known as Maneuvering Characteristics Augmentation System (MCAS).

The Journal notes that Boeing has already planned on several ways to reroute the wires and will likely accept the FAA’s position on the issue.

More issues for Max jets developed last month when an internal Boeing report found dozens of jets had foreign-object debris (FOD) in the fuel tanks.

Airlines have been aware of the new setbacks and pushed out MAX return to service dates to late summer and or even fall.

Southwest said it is extending its MAX flight cancellations through August 20, the largest US airline (by available seat miles) United Airlines, also said it was pulling the MAX from its schedule until September.

Sources were unclear if wiring adjustments in the 800 Max jets would lead to production restart and or flight test delays.

Boeing shares are collapsing further on the news, and the broad market, down almost 10%…

6 Killed, Dozens Wounded During Coronavirus-Inspired Prison Riot In Italy

A prison riot reportedly broke out Sunday afternoon at an Italian prison in the city of Modena that has left six dead, according to the Italian newspaper Corriere di Bologna.

The riot, which started at around 2 pm local time, started when about 60 inmates decided to set the prison on fire in an attempted mass escape reportedly inspired by the coronavirus quarantine crackdown. Inmates were reportedly told that family members wouldn’t be allowed to visit during the quarantine (remember what happened in those Chinese prisons?). This left dozens furious and, in an overcrowded prison, that type of rage can spread quickly.

Inmates demands for more information about policies being put in place to suppress the virus certainly helped spark the riot, but local officials were careful to characterize the riot as something that happened “in addition” to the outbreak, not because of it, while critics noted longstanding issues like overcrowding contributed to the unrest.

Shortly after prisoners overwhelmed the guards, a contingent of police arrived, sparking a confrontation that led to an hours-long faceoff.

While six have been killed so far, more fatalities are expected, as dozens were badly wounded in the fighting, while others reportedly overdosed on medications like methadone and benzodiazepines as prisons apparently raided the prison hospital and stole all the methadone and Xanax they could find. Authorities insist that half of the six deaths so far could be attributed to overdoses, though that sounds…somewhat suspicious to us.

According to Corriere, the police intervention stopped 500 prisoners from escaping. On Italian twitter, reports that the 500 prisoners had escaped were being reported as fact.

We hope to learn more about the riots later in the day. But will this uprising inspire others across the locked-down north?

Dual Coronavirus, Oil Shocks Crash World Markets, 10Y Yield Craters, Futures Pinned Limit Down

Global stocks plunged with the Emini locked limit down for the longest period on record, crude oil tumbled as much as 33% as WTI plunged as low as $27.34, and the yield on the 10Y Treasury crashed to an all time low of 0.31% after Saudi Arabia launched a price war with Russia, sending investors already panicked by the coronavirus fleeing for safe assets.

As noted overnight, the catalyst for today’s historic rout was the plunge in crude, which tumbled as a result of Saudi Arabia launching an all out price war, one which may result in as much as a 4 million barrel production surplus per day, and which at one point tumbled more than 30%, the most since the Gulf War in 1991. After paring some losses, WTI and Brent remained down about 20%.

There were also worries that U.S. oil producers that had issued a lot of debt would be made uneconomic by the price drop.

As Bloomberg notes, the oil-price crash, if sustained, would upend politics and budgets around the world, exacerbate strains in high-yield credit and add pressure on central bankers trying to avert a recession. It typically would have proved a boon to consumers, but the coronavirus is increasingly keeping them at home.

Spooked by the implications for energy stocks, and the imminent crash in the junk bond market, S&P 500 futures fell 5%, triggering trading curbs designed to limit the most dramatic moves while cash markets are closed. Two major exchange-traded funds that track U.S. benchmark gauges posted even bigger declines in pre-market trading. They are not subject to the same curbs.

Predictably, US oil majors and oil services and equipment stocks plunged in pre-market trading, with shares of Chevron crashing 12% and Exxon Mobil dropping 10%. Services and equipment stocks also slumped, with Transocean -20%, Halliburton -16% and Schlumberger -15%. Numerous other companies in the energy sector, including Devon Energy, Occidental Petroleum and Marathon Oil fell at least 20%. In Europe, the Stoxx 600 Oil & Gas index fell as much as 15%, the most on record.

And since the limit-down move is likely to resume once stocks reopen, here are the threshold triggers for marketwide halts on the cash S&P500:

If the S&P 500 declines 7%, (208 points), trading will pause for 15 min

If declines 13%, (386 pts) trading will again pause for 15 mins

If falls 20%, (594 pts) the markets would close for the day.

European stocks as measured by the Stoxx Europe 600 Index, fell the most since 2016 entering bear market territory and suffering hefty losses in early trade with London dropping more than 8%, Frankfurt falling more than 7% and Paris almost matching those losses. Several of the region’s gauges look set to enter bear markets and most of Italy’s stocks failed to open after the government ordered a lockdown of large parts of the north of the country, including the financial capital Milan.

Japanese stocks entered a bear market earlier when they tumbled almost 6%: in the Asian session, stocks slumped led by energy and materials, after Monday’s crash in oil prices added to the grim backdrop of the virus outbreak. All markets in the region were down, with equity gauges in Japan, Australia, and Singapore, Thailand and Indonesia each dipping by more than 7%. Shares in Japan, the Philippines, Singapore and Indonesia have plunged more than 20% from their highs as American stock-index futures slumped. The Lehman-like panic after Monday’s crash in oil prices adds to selling triggered by the virus outbreak that has infected almost 110,000 people worldwide and killed more than 3,800.

With traders unable to S&P futures – traditionally the most liquid equity-linked security in the market- they bought bonds instead, and the 10-year Treasury yield fell as low as 0.31%, the lowest ever…

… taking the whole U.S. yield curve below 1% for the first time in history.

In Europe, the spread between Italy’s 10-year sovereign yield and Germany’s jumped 33 basis points to 211 basis points, the highest since August as traders doubted the credibility of the ECB’s ability to preserve stability “whatever it takes.”

The turmoil hit FX as well, with exchange rates moving sharply as traders struggled to establish where new trading ranges might be. The yen was up about 3% versus the dollar, as the USDJPY briefly dipped below 102 in what appeared to be an overnight flash crash…

… while the euro and Swiss franc both rising more than 1%.

In case anyone missed the big news over the weekend, Saudi Arabia stunned markets with plans to raise its production significantly after the collapse of OPEC’s supply cut agreement with Russia, a grab for market share reminiscent of a drive in 2014 that sent prices down by about two thirds. The shock in oil was seismic, with Brent crude futures sliding $12 to $33.20 a barrel in chaotic trade.

Meanwhile the coronavirus pandemic continued to rage, with the number of people infected with the coronavirus topping 110,000 across the world as the outbreak reached more countries and caused more economic carnage.

Not helping the mood was news North Korea had fired three projectiles off its eastern coast on Monday.

“Wild is an understatement,” said Chris Brankin, Chief Executive at stockbroker TD Ameritrade Singapore. “Not just us, but across the globe you would have every broker/dealer raising their margin requirements … trying to basically protect our clients from trying to leverage too much risk or guess where the bottom is.”

“After a week when the stockpiling of bonds, credit protection and toilet paper became a thing, let’s hope we start to see some more clarity on the reaction,” said Martin Whetton, head of bond & rates strategy at CBA. “Dollar bloc central banks cut policy rates by 125 basis points, not as a way to stop a viral pandemic, but to stem a fear pandemic,” he added, while noting that many central banks had little scope to ease further.

A tectonic shift saw markets fully price in an easing of 75 basis points from the Fed on March 18, while a cut to near zero was now seen as likely by April. The ECB meets on Thursday and will be under intense pressure to act, but rates there are already deeply negative. Indeed, urgent action is clearly needed, with data suggesting the global economy toppled into recession this quarter. Figures out from China over the weekend showed exports fell 17.2% in January-February from a year earlier.

Finally, while commodities cratered, Gold initially cleared $1,700 per ounce to a fresh seven-year peak, only to fall back to $1,676.55 amid talk some investors were having to sell to raise cash to cover margin calls in stocks.

Thor Industries, Casey’s and Stitch Fix are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 4.9% to 2,819.00

STOXX Europe 600 down 6.5% to 342.84

MXAP down 4.2% to 149.95

MXAPJ down 5% to 488.43

Nikkei down 5.1% to 19,698.76

Topix down 5.6% to 1,388.97

Hang Seng Index down 4.2% to 25,040.46

Shanghai Composite down 3% to 2,943.29

Sensex down 5.9% to 35,352.82

Australia S&P/ASX 200 down 7.3% to 5,760.56

Kospi down 4.2% to 1,954.77

German 10Y yield fell 12.1 bps to -0.831%

Euro up 1.3% to $1.1429

Italian 10Y yield rose 0.5 bps to 0.906%

Spanish 10Y yield rose 6.8 bps to 0.282%

Brent Futures down 20% to $36.18/bbl

Gold spot up 0.4% to $1,667.55

U.S. Dollar Index down 0.6% to 95.34

Top Overnight News from Bloomberg

The Federal Reserve is under intensifying pressure to tackle the increasing risk of a worldwide credit crunch as falling commodity prices combine with the spreading virus to hammer financial markets

Panic reigned in currency markets as orders from traders and algorithmic machines snowballed to spur some of the biggest moves since the global financial crisis

Euro Stoxx 50 futures dropped more than 4% early on Monday amid mounting worries over the spread of the coronavirus in Europe and after Italy announced drastic measures including a near-complete travel ban for about a quarter of Italians as the number of cases in the country soared

Oil markets crashed more than 30% after the disintegration of the OPEC+ alliance triggered an all-out price war between Saudi Arabia and Russia that is likely to have sweeping political and economic consequences

The Trump administration is drafting measures to blunt the economic fallout from coronavirus and help slow its spread in the U.S., including a temporary expansion of paid sick leave and possible help for companies facing disruption from the outbreak, according to three people familiar with the matter

The coronavirus has spread to about half of the world’s countries, with global fatalities reaching 3,800 and infections in Italy eclipsing those in South Korea. Italy introduced far-reaching measures to contain the outbreak, though it remained unclear how strictly they would be enforced. The U.S. is asking Americans to avoid cruise ships as it prepares to move more than 3,000 passengers and crew off the Grand Princess vessel

Gold rallied above $1,700 an ounce as a concerted global rush into havens intensified, with the upswing driven by turmoil in the oil market, the spread of the coronavirus, sinking equities, and expectations of easier monetary policy as recession risks loom ever larger

Japan’s economy contracted last quarter more than initially estimated, underscoring its vulnerability even before the coronavirus threatened to push the country into recession.

Boris Johnson will announce a 5 billion pound ($6.5 billion) investment in the U.K.’s next generation broadband internet services as he seeks to ensure that remote parts of the country can benefit

The euro-area economy may be headed for its first recession in seven years as the coronavirus outbreak takes an increasing toll on businesses and consumer confidence. Economists at Morgan Stanley and Berenberg expect the euro-zone gross domestic product to shrink in the first half of the year. In France, the central bank now sees output barely growing in the first quarter

“A temporary decline in activity in some sectors is in fact preferable to a prolonged crisis that would risk expanding to all sectors of the economy,” Italy’s Finance Ministry says in statement Monday on the government’s drastic virus containment measures

German January industrial production rose 3% from the previous month, compared with an estimate for a 1.7% increase

Asian equity markets resumed their slump and US equity futures also suffered heavy losses in which the E-mini S&P hit limit down and DJIA futures pointed to another decline of over-1000 points, as oil prices slipped by around 30% after Saudi Arabia kicked off an oil price war. The kingdom announced plans to raise its output to over 10mln bpd beginning next month and it cut the OSP for all destinations by USD 6-8/bbl following last week’s breakdown of the OPEC+ output deal in which Russia rejected the proposal for additional cuts. ASX 200 (-7.3%) posted its largest intraday loss in more than 11 years amid a collapse across the energy sector although gold miners bucked the trend due to the flight to safety, while Nikkei 225 (-5.1%) gapped below 20K and continued to tumble against the backdrop of the detrimental currency flows and following the miss on Q4 GDP which further pointed to the likelihood of a looming recession. Hang Seng (-4.2%) and Shanghai Comp. (-3.0%) conformed to the sell off as blue-chip energy names were pummelled and after continued PBoC liquidity inaction, while the latest trade data from China over the weekend showed a surprise Trade Deficit and a larger than expected contraction in Exports. Finally, 10yr JGBs were higher amid the bloodbath in stocks and as it tracked the advances in T-notes which surged nearly 2 points as US 10yr and 30yr yields delved into unprecedented levels, while the BoJ were also present in the market today for nearly JPY 1tln of JGBs.

Top Asian News

Japan GDP Shrinks More Than Estimated, Fueling Recession Concern

Debt-Default Showdown Looms as Lebanon Freezes Bond Payment

Global Rout Threatens to End China’s Leverage-Loving Stock Binge

Saudi Prince Tests Grip on Power With Desert Raid, Oil Price War

European opened substantially into negative territory this morning (Stoxx 50 -6.6%) as sentiment remains subdued on the coronavirus, but with the added development of a crude-war between Saudi Arabia and Russia after the OPEC+ bust-up on Friday (Full details available in the commodity section below). It’s worth noting that sentiment has begun to recuperate somewhat, with US equity futures trading briefly above the limit down positions that were hit overnight (Limit Down Details). Given the commitments from Saudi to increase production to over 10.0mln BPD as of next month and they have cut the official selling price for all destinations by around USD 7/bbl, crude prices are as such lower by over USD 10/bbl and the energy sector has similarly recoiled (Stoxx Oil & Gas -13%). The Oil & Gas Sector accounts for 5.5% of the Stoxx 500 itself, and the largest weightings withing the sector are Total at 29.4%, BP with 15.5% and Shell contributing 14.5%; in terms of price performance, they are currently down by 13.3%, 15.7% and 16.7% respectively. Additionally, the overall downside is exacerbated by the FTQ seen overnight which has sent the global yield complex to record lows for most core parties. For instance, the entirety of the US yield curve is below 1% for the first time and the German 10yr low thus far resides at -0.86%. The Stoxx banking sector is the sector with the 3rd largest weighting in the Stoxx 600 representing 9.4% and is currently 7.3% down on the day. Elsewhere, sectors are all firmly in the red as is every open component in the Stoxx 600 itself; note, a number of Co’s failed, at least initially, to open. Looking ahead, focus turns to how markets react to the US’ entrance, particularly whether this exacerbates the sell-off; as well as for any indicative signs from any particular Co’s in the Energy/Banking sector regarding profit warnings, guidance changes or other telling comments

Top European News

Italy Bond Yields Soar as Virus Lockdown Hits Financial Capital

Germany Boosts Investment to Protect Economy From Virus Hit

Putin Dumps MBS to Start a War on America’s Shale Oil Industry

France Economy Hit by Virus as Central Bank Slashes Outlook

In FX, risk sentiment has been roiled by Saudi Arabia’s decision to increase output and slash the cost of crude in response to the breakdown of OPEC+ talks last week when Russia refused to back a deeper cut in production, as prices tumble and compound fears over the economic fallout from China’s nCoV. Eur/Nok has hit highs just shy of 11.0000 and Eur/Sek topped 10.7500, while Usd/Rub peered over 75.0000 before WTI and Brent nursed some losses from just above Usd27 and Usd31 per barrel respectively. Meanwhile, Usd/Cad catapulted to 1.3750+ at one stage overnight and the Antipodean Dollars saw flash crashes that dragged Aud/Usd and Nzd/Usd down to circa 0.6320 and 0.6030, but the Loonie, Aussie and Kiwi have all clawed back some lost ground as their US peer succumbs to pressure from sliding Treasury yields and more pronounced bull-flattening along the curve, not to mention heavy depreciation vs safer havens.

JPY/EUR/CHF/GBP – In stark contrast to all the above, Usd/Jpy has been trading largely in lock-step with oil with added impetus from risk-off flows/positioning between wide 104.58-101.58 parameters and the Yen retains a strong underlying bid unlike GOLD that has faded from a few bucks over Usd1700/oz at best on profit taking and long liquidation. Elsewhere, Eur/Usd hit resistance just ahead of 1.1500 and Usd/Chf based a few pips under 0.9200 as Eur/Chf bottomed around 1.0510 in advance of Swiss jobs data and sight deposits showing another rise in bank balances. Similarly, Cable waned after touching 1.3200 with Sterling still subject to hard Brexit jitters alongside the coronavirus and crude capitulation that pose growth and financial stability threats. However, the DXY remains vulnerable itself within a 95.694-94.719 range and not far from a key technical level at worst (94.080 representing a 50% retracement from ytd peak).

EM – Severe underperformance in extreme or bordering on unprecedented levels of aversion, especially through the cross-over from Asia-Pacific to European time zones has ravaged regional currencies, though the Lira has rebounded more than most on the vastly cheaper oil price as a net importer and the Yuan is holding firmly above 7.0000 after another decline in the Usd/Cny fix.

In commodities, a frantic session for commodities to say the least after sources over the weekend noted that Saudi Arabia will be boosting its output to above 10mln BPD from this month’s 9.7mln BPD as a response to the collapse of its OPEC+ alliance with Russia. Saudi is also said to have told market participants that it could raise output to as much as 12mln BPD, although sources stated that the initial increase is likely to total between 10-11mln BPD in April, with the final figure contingent on refiners’ response to price cuts. Furthermore, the Kingdom slashed its official pricing for crude, with oil giant Aramco cutting its Asia prices for Arab Light crude and Medium crude by USD 6/bbl each, to discounts of USD 3.10/bbl and USD 4.05/bbl below the Middle East benchmark respectively. In a challenge to Russia, the company made the largest cut to northwest Europe of some USD 8/bbl in most grades – Russia sells a bulk of its Urals crude in the same region. Arab Light sales to Europe will be at a USD 10.25/bbl discount to Brent – levels not seen since at least May 2002. As a result of the anticipated rising production and slash in OSPs – expected to flood the market with barrels – WTI and Brent futures sank 27% and 30% respectively, with the former paused for a few minutes following its aggressive >7% move. WTI Apr’20 briefly slipped below USD 28/bbl vs. Friday’s USD 41.50/bbl close, while Brent May 20 dipping south of USD 32/bbl vs. Friday’s USD 45.50/close – with the spread also narrowing to ~USD 3.80/bbl vs. ~4/bbl on Friday. The Kingdom hopes the slump in oil prices and the expected diminishing in Russia’s market shares will prompt Moscow back to the negotiating table and force its hand to cut output. Desks note that although this may prove effective in the short-term, it is in less certain what the longer-term impact will be. The front-month energy contracts have, as European players entered the markets, pared some losses with WTI Apr’20 now back to ~USD 32.50/bbl, with the 29th Jan 2016 low at USD 26.19/bbl, whilst the Brent May contract reclaimed a USD 36/bbl status. Away from the OPEC debacle, IEA cut 2020 world oil demand forecasts by almost 1mln BPD, due to the coronavirus; envisage the first contraction since 2009, noting that Demand could drop by 730k BPD, in an extreme event where Gov’t fails to contain the virus. Price action to the report was muted given the omission of a scenario that incorporates the weekend Saudi/Russian news. Elsewhere, spot gold failed to hold onto impetus from the global stock rout after prices briefly surpassed USD 1700/oz to the upside to prices last seen in December 2012. The yellow metal then waned off highs and into negative territory – potentially on profit-taking and as investors pump money into government debts in search of safe-haven assets. Meanwhile, copper conformed to the overall risk tone and gapped lower at the open, losing the USD 2.5/lb handle to a current low of USD 2.4675/lb.

US Event Calendar

Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

When you’ve worked through the Asian crisis, the Russian/LTCM crisis, the 2000 equity bubble collapsing, the GFC, the European sovereign crisis, and several other smaller wobbles it takes a lot to stun you in financial markets. However the weekend news-flow and overnight price action in oil – just at a time a beaten up market could have done without it – has done that and deserves its own place in the history books.

Following the 10% plunge in oil prices on Friday, WTI and Brent are down a further -30.01% and -27.55% this morning respectively to $28.80/bbl and $32.73/bbl and more or less at their lows since Asia opened. For context this is the largest absolute one-day decline for Brent crude ever while in % terms the decline is the highest since January 17, 1991 when it dropped by -34.8% during the gulf war. This follows the developments over the weekend, specifically that Saudi Arabia plans to raise oil production next month through targeting market share rather than supply management, therefore leading to the threat of an all-out price war following a breakdown in OPEC talks. This led to huge declines in Middle Eastern markets yesterday with bourses in Abu Dhabi, Dubai, Saudi Arabia and Kuwait down between 5% and 10%. The main Kuwait index actually suspended trading in the biggest shares after falling 10% while Saudi Aramco fell below its IPO price for the first time. DB’s Michael Hsueh published a note yesterday suggesting that oil should migrate below $20 now. See here for his full analysis. Our economists have often attributed the collapse in inflation expectations in 2015-16 to the collapse in oil prices. They haven’t really recovered from this and are likely to take a further dent now. With central banks running out of road the good news is that this should put us closer to more fiscal spending and likely helicopter money. That might not be the first reaction today though.

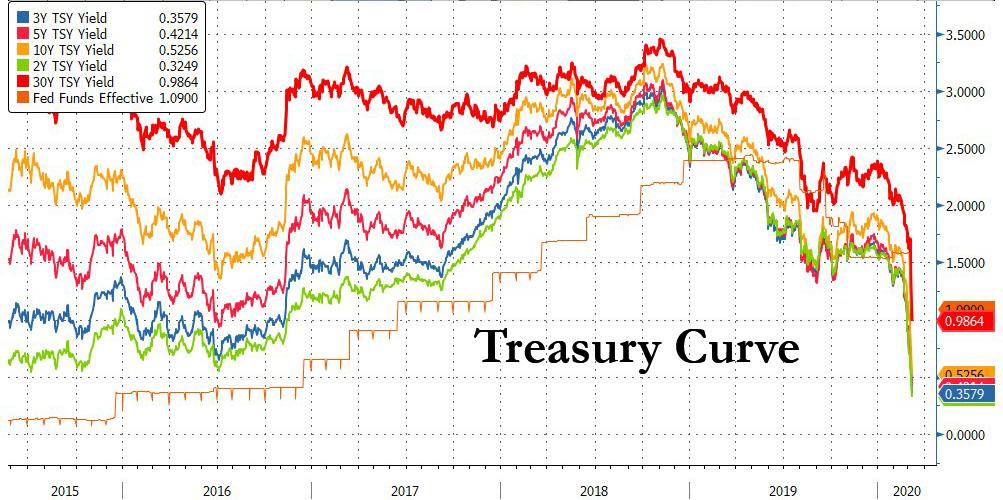

The plunge in oil has led to complete capitulation in other markets this morning. In rates, 10y and 30y Treasuries have traded below 0.50% and 1.00% respectively (currently 0.513% and 0.968% as we go to print – moves of -24.6bps and -31.9bps since Friday) meaning the entire yield curve has is below 1% for the first time in history. In equity markets losses are being led by the Nikkei (-5.82%) with further big legs lower for the Hang Seng (-3.50%), Shanghai Comp (-2.14%) and Kospi (-4.14%). It’s worth noting that Australia’s ASX index – typically a perceived defensive market in Asia Pacific – is even down -7.33%. S&P 500 futures are down -5% and have hit circuit breakers. Meanwhile 10y JGBs traded down -0.20% although have since nudged slightly higher, Gold is flat, other base metals are down heavily (iron ore down over 4%), while the Yen (+2.73%) and Swiss Franc (+1.48%) have rallied at the expense of oil sensitive currencies.

One area that will be under severe scrutiny given the oil move is credit. Energy makes up 14% of overall US HY whereas for context in the S&P 500 the energy sector is more like 3% of the overall index. The timing of this is very bad as fears were building in credit already on Friday. As a proxy and showing the demand for hedges, EU Crossover had one of its worst days since the GFC – widening c.60bps. I always think that if a management consultant firm was asked to look at the credit market and report back on its functioning I think they would say that it’s disingenuous to call it a market. The reality is that if you want to buy large amounts at new issue you can do so. However if you wanted to sell it back weeks, months or years later you would only be able to generally do it in much smaller sizes. Dealers only have small appetite to absorb risk even in good times. This massive imbalance doesn’t matter when you have a decent economy and constant inflows as you’ve had for most of the last decade. However once investors have doubts about the economy and/or see outflows then selling can overwhelm the market. The danger of the current situation is you’re starting to risk seeing the early stages of such a move. If this crisis is prolonged it’s likely that credit will see big liquidity air pockets that will spook other asset classes and risk becoming a viscous circle. Its possible central banks will intervene but probably only after bigger problems first. This is part of the reason we extended our spread widening view last Thursday (see link here ) although we now have a tighter spread target for YE than we did at the start of the year. Staying with credit Craig and Nick on Friday put out a note looking at US profit warnings seen so far and also those companies they see at being at risk of downgrades, including those at risk of being junked. See their report here.

Overnight, the Australian newspaper reported that the Australian government will announce a fiscal stimulus package of AUD 10bn while the SKY news was reporting that the plan would likely include cash handouts. So more and more countries are pivoting towards the idea of helicopter money. The US is also drafting measures to blunt the economic fallout from coronavirus and help slow its spread in the US, including a temporary expansion of paid sick leave and possible help for companies facing disruption from the outbreak (per Bloomberg) as New York became 2nd state to declare a state of emergency after cases in the state reached 106. Further, the G20 also made a similar statement to that of G7 over the weekend saying they would use “fiscal and monetary measures, as appropriate, to aid in the response to the virus, support the economy during this phase and maintain the resilience of the financial system.”

Meanwhile, the latest on the virus is that Italy is now close to becoming the worst affected country after China with 7,375 confirmed cases and 366 deaths. Italian PM Giuseppe Conte announced quarantine measures affecting 16mn people yesterday as anyone living in Lombardy and 14 other central and northern provinces will need special permission to travel with Milan and Venice both affected. Schools, gyms, museums, nightclubs and other venues will remain close across the whole country and the moves are likely to remain in place till April 3rd. In other news, Bloomberg is reporting that the Trump administration has told their Chinese counterparts that the purchasing boost, signed in January as part of the Phase 1 trade deal, with specific target dates and commodities, could start off slowly due to the virus hit. However, the US has indicated that this is only an option as long as there isn’t a jump in Chinese exports when virus-related industrial shutdowns end. Elsewhere, the Institute of International Finance highlighted in a report the EM capital outflows hit $30bn in 45days due to the coronavirus outbreak. The amount exceeds the outflows observed during the 2015 China devaluation scare and the 2007-2008 global financial crisis.

It’ll feel like an age ago now, but last week markets saw one of the most volatile weeks in nearly a decade, with the intraday and closing moves on the S&P 500 at sizes unseen since the US debt downgrade in 2011. Prior to this morning the 10-year U.S. Treasury yield was half of what it was 2 weeks prior on 22-Feb having fallen over -70bps to end the week at 0.762% (-15bps Friday, -39bps last week), and saw an all-time intraday low of 0.66% Friday morning almost exactly 11 years after the GFC lows of 666 on the S&P 500. The S&P 500 posted its 10th decline in 12 sessions on Friday (-1.71% but off the -4.05% lows for the session), but actually ended the week slightly higher +0.61%, after two days of over 4% rallies midweek. Since its record high on Feb. 19, the index is down over 12% and has lost $3.43 trillion of market capitalization. The main lagging sectors on the week were banks and energy stocks again as rates and oil both sunk. 30y US treasuries fell to an all-time low of 1.287% – down -38.8bps on the week (-25.3bps Friday). While oil fell to nearly 3 year lows as virus related growth scares and the inability for OPEC+ to get Russia to agree to production cuts – Brent was down -9.44% on Friday (-10.39% on the week) – that is the commodity’s largest one day loss since March 8th 2000, almost 20 years to the day.

It was a similar story in Europe as the STOXX 600 fell -2.36% on the week (-3.67% on Friday) underperforming the US partly as it was closed when risk markets had a late NY rally on Friday. As the virus outbreak spreads through Italy, the government has now indicated they are going to implement €7.5 billion of fiscal stimulus, as the FTSE MIB was down -1.79% on the week (-3.62% Friday). 10yr bund yields are back flirting with late summer 2019 all-time lows and now at -0.71%, falling -2.4bps on Friday and -10.3 bps over the week, while spreads in France, Italy, and Spain were all 3.5-7.5bps wider over the course of the week. Credit spreads were wider as well on both HY and IG – US HY was 58bps wider on the week (59bps Friday), while IG was 19bps wider on the week (14bps Friday). In Europe, HY was 36bps wider on the week (36bps Friday), while IG was 12bps wider on the week (9bps Friday). The VIX has now closed over 30 for a full week for the first time since October 2011. Lastly, gold finished the week at its highest levels since Feb 2013 as the prospects of central bank easing and an economic slowdown increase, the haven was up over +5.5% on the week.

As for this week, the focal point will be the ECB meeting on Thursday. Following the Fed’s emergency rate cut this week our economists believe that this has made it easier for the ECB to disappoint market expectations and inadvertently tighten financial conditions; and Christine Lagarde’s hope to shift more of the burden of policy stimulus to fiscal policy will be tested. Our team’s expectation for policy is twofold. The first element is unconditional. Our colleagues expect the ECB to announce a targeted and temporary liquidity facility to support SME lending in affected regions. This ‘quantity of financing’ policy can be complemented by ensuring sufficient eligible collateral and flexibility within NPL rules. The second element is conditional; a 10bp deposit rate cut in April, signalled in March. This cut is conditioned on the virus spreading further and the tightening of financial conditions spreading sufficiently beyond equities into bank funding costs, sovereign funding costs and/or EUR exchange rate appreciation.

In the UK there will be some focus on the government’s 2020 budget, due to be unveiled by Chancellor of the Exchequer Rishi Sunak on Wednesday. In the US further democratic primaries are scheduled, with the bulk coming on Tuesday with 6 states reporting including Idaho, Michigan, Mississippi, Missouri, North Dakota and Washington. In terms of data it’s going to still be pretty backward looking so rather than go through if we’ll leave you to read the day-by-day calendar below.

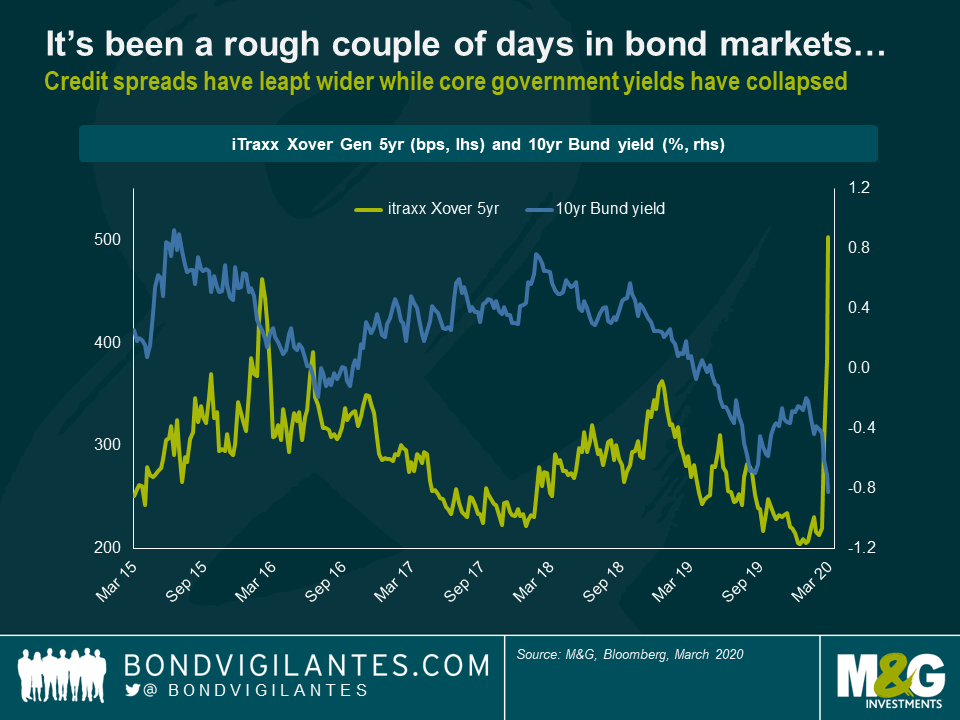

It’s been a rough two weeks in bond markets, to say the very least. Risk-off sentiment is reigning supreme. In Europe, looking at my screens this morning, iTraxx Xover—a bellwether of the European high yield credit risk—jumped to its widest level since mid-2013, while the yield on 10yr German Bunds dropped to an all-time low below -0.8%.

In previous times of market turmoil, the European Central Bank (ECB) has stepped in to signal more monetary stimulus. In March 2016, after a horrendous couple of months for risk assets, the ECB announced it would ramp up its quantitative easing programme by adding corporate bonds to the shopping list. Even more dramatically, former ECB President Mario Draghi’s famous “whatever it takes” speech in July 2012 is largely recognised as one of the key factors putting an end to the European debt crisis.

Considering the recent worsening of the COVID-19 situation and subsequent market reactions, all eyes are now on Christine Lagarde and her comments after the ECB’s Governing Council meeting on Thursday. In my view, essentially three options are available to the ECB this week: business as usual, measured response or big bazooka.

Option #1: Business as usual

In this scenario, the ECB simply acknowledges the heightened risks for the economic outlook and medium-term inflation in the euro area caused by COVID-19, but refrains from altering its monetary policy stance, which is already highly accommodative. The main deposit rate is kept at -0.5% and net purchase volumes under the Asset Purchase Programme (APP) continue to run at a monthly rate of €20 billion. The rationale here would be that monetary policy alone won’t be enough and that the onus is first and foremost on governments and fiscal easing. Rushing into monetary emergency measures prematurely might actually be counter-productive. The ECB switching into full-on alarmist mode could very well spook markets further. Also, considering that the ECB’s deposit rate is already deeply negative, which limits the scope of further rate cuts compared to other central banks, the ECB might conclude that it is sensible at this point to keep as much power dry as possible to be able to act decisively later, in case the COVID-19 situation continues to worsen.

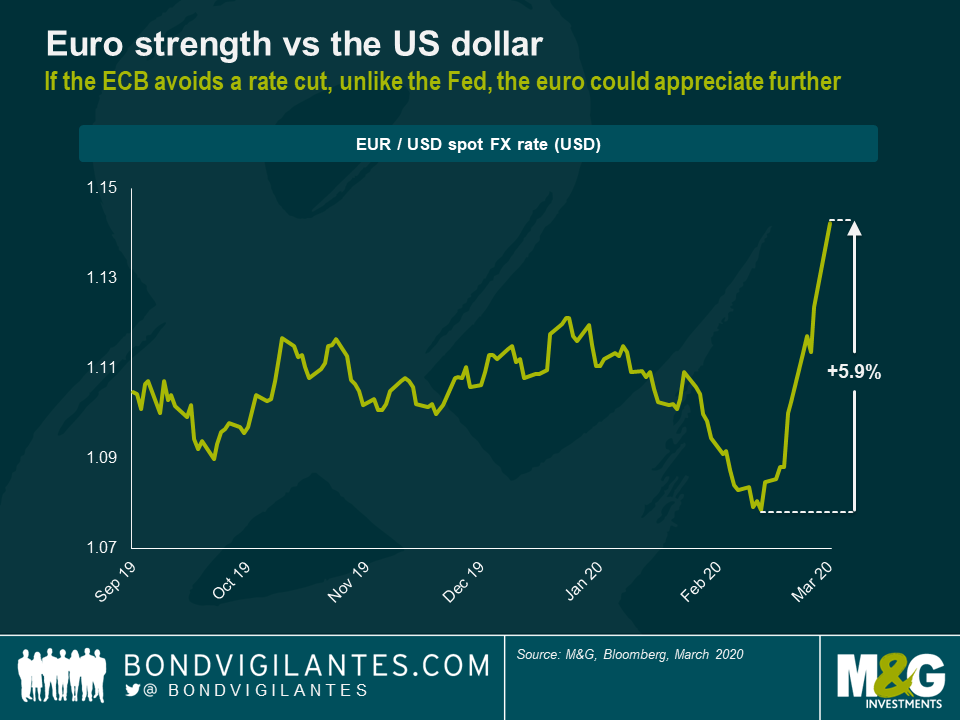

Although there may be valid reasons supporting a “business as usual” approach, I don’t think it is a likely scenario. First, expectations amongst market participants are high with regards to further monetary stimulus from the ECB. At the time of writing, the implied probability of an interest rate cut on Thursday, using overnight index swaps, is close to 100%. The ECB is under no obligation whatsoever to satisfy market expectations, of course. But avoiding the highly anticipated rate cut might fuel further turbulences in financial markets, something the ECB would rather like to prevent. Second, in a world in which other central banks—e.g. the Fed, the Bank of Australia, the Bank of Canada—have decided to cut rates in response to COVID-19, the ECB could quickly become “the odd one out” by keeping rates steady, which would put further upward pressure on the euro. The currency has already appreciated by around nearly 6% against the US dollar since mid-February. Continued strengthening of the euro would be yet another head-wind for export-driven European companies—and by extension, the eurozone economy as a whole—already suffering from weakening demand and supply chain disruption caused by COVID-19. To be clear, the ECB’s mandate does not involve actively managing the strength of the euro in the FX market. But putting an end to the recent euro rally would at least be a desirable side-effect of a rate cut, albeit not the main reason behind it, and might help in moving European inflation closer to its target through rising import prices.

In an attempt to calm markets, with the additional benefit of dampening the strength of the euro, the ECB is going to take action on Thursday, I believe. If so, the key question is of course how far will the ECB go? This leaves us with options #2 and #3.

Option #2: Measured response

In this scenario, the ECB cuts interest rates by a modest amount, say 10 basis points (bps). This would bring the main deposit rate to a new record low of -0.6%. Simultaneously, monthly net asset purchases are increased to perhaps €60 billion or even €80 billion a month. This would be a tripling or quadrupling in purchase volumes, respectively, from the current level of €20 billion, but it wouldn’t be unchartered territory. The ECB used to run its APP in the past at €60 billion (March 2015 to March 2016 and April to December 2017) and €80 billion a month (April 2016 to March 2017).

I’d say this is perhaps the most likely scenario, but arguably the least desirable one. The danger is that the ECB would get the worst of both worlds. Moderate policy action by the ECB, if not accompanied by substantial fiscal stimulus, is unlikely going to be enough to instil lasting confidence into markets that just shrugged off a 50 bps cut from the Fed. The risk-off sentiment could easily escalate further into a fully-fledged market crisis. Simultaneously, the ECB would have depleted some of its dry powder, thus limiting the scope of any additional emergency policy actions that might be necessary in the future if the adverse economic impact of the COVID-19 outbreak exceeds current projections.

Option #3: Big bazooka

The idea here be to create another “whatever it takes” moment that immediately helps calm down markets and avoid a full-blown panic amongst investors that, if left unchecked, might compromise the stability of the financial system and ultimately threaten the real economy. In this scenario, the ECB acts boldly both in terms of interest rates and asset purchases. Rates are cut by at least 25 bps, which would bring the ECB’s deposit rate to -0.75% and thus in line with the policy rate of the Swiss National Bank. In addition, APP purchase volumes are increased beyond €80 billion a month, perhaps to €100 billion. Importantly, in order to signal to market participants that the ECB still has more firepower to further upscale asset purchases in the future if necessary, certain changes to the APP rules might need to be implemented.

Under the rules of Public Sector Purchase Programme (PSPP) within the APP, government bond purchases are guided by the ECB capital key. Due to the combination of Germany’s high capital key weight and relatively low level of indebtedness—Germany ended 2019 with a record budget surplus of €13.5 billion after all—Bunds have become a bottleneck in the programme. In order to create headroom in a meaningful way, the capital key rule could temporarily be suspended, thus allowing the ECB to tilt purchases more heavily towards Italian BTPs, of which there are plenty. Politically this step would be highly controversial, of course. But given that at the moment Italy is more severely impacted by the COVID-19 outbreak than any other European country, the rule change seems at least justifiable. If the ECB ever wants to suspend the capital key, now is the time.

The rules of the Corporate Sector Purchase Programme (CSPP) within the APP do not allow for the purchase of bonds issued by banks. Since bank bonds account for around 30%, give or take, of the European investment grade corporate bond universe, their inclusion into the CSPP would help increase capacity considerably. It would also serve another purpose. Banks’ profitability would suffer from the deep rate cut in the bazooka scenario. Generating CSPP demand for bank bonds, thus effectively lowering funding costs, would help soften the blow to the European banking system.

As compelling as it may seem to take out the big bazooka, it is a high-risk strategy. If it works and a veritable crisis—both in markets and within the real economy—can be averted through decisive ECB action early on, Christine Lagarde would reach immediate superstardom amongst central bankers. However, if not flanked by fiscal easing in a concerted fashion, the bazooka approach could also easily backfire. If the measures fall flat, markets continue to tumble and the transmission of monetary stimulus into the real economy fails, there wouldn’t be an awful lot more the ECB could do going forward. And markets would know that the ECB—and other central banks—are at their wits’ end.

* * *

In summary, Christine Lagarde is not to be envied this week as the ECB is caught between a rock and a hard place.

Inaction or any half-hearted measures might lead to further deterioration in market stability that could soon spiral into a full-blown crisis, affecting both financial markets and the real economy.

But going “all in” now in an effort to stimulate the economy and turn around investor sentiment before things escalate any further carries the risk of being left without any room for manoeuvre later.

For investors, navigating markets is going to be a tricky exercise. Given that there isn’t any obvious path to take for the ECB—or any other central bank for that matter—it is a risky strategy to bet on any particular monetary policy outcome.