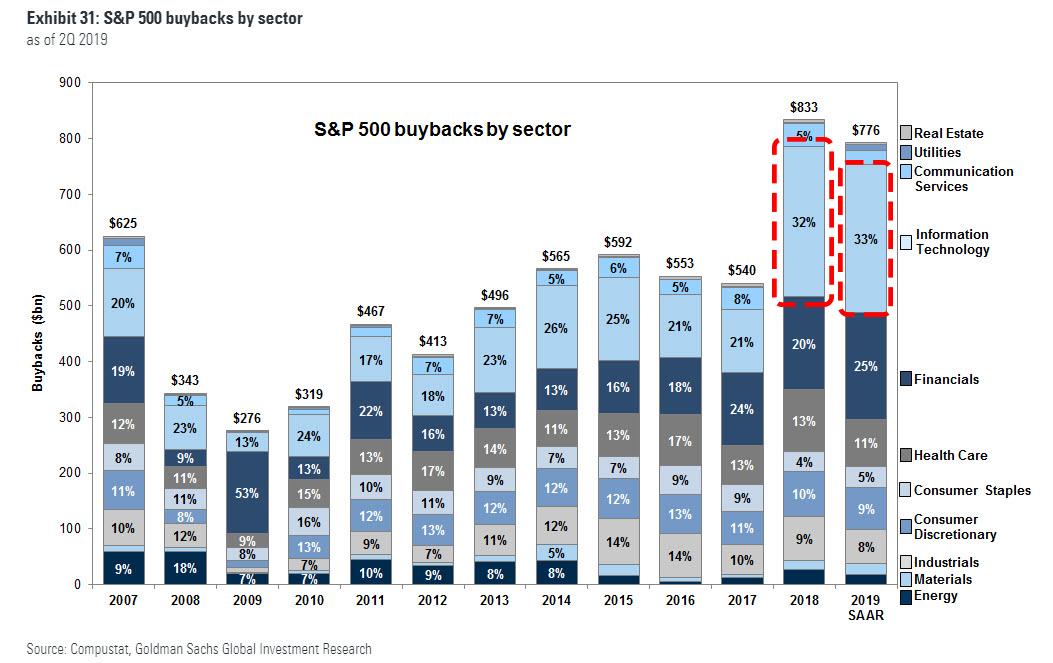

Goldman’s Buyback Desk: Companies Representing $190BN In Buybacks, 25% Of Total, Have Already Suspended Repurchases

As discussed last weekend, 2018 and 2019 were record years for buybacks, for one main reason: Trump’s tax reform allowed companies to repatriate over a trillion dollars parked offshore at nominal tax rates, which were then used to repurchase stocks, resulting in the bizarre market condundrum of record outflows even as the S&P hit all time highs, as all investor outflows were offset by companies buying back their own stock.

However, even before the coronacrisis, we warned that buybacks had sharply slowed down at the start of the year even as all investors how plowed all in stocks.

But if buybacks were merely slowing at the start of the year, after the recent collapse in the market, buybacks are effectively dead as a driver of stock prices for the foreseeable future.

As Goldman’s David Kostinw writes in his latest weekly kickstart, according to Goldman’s Buyback Desk, “nearly 50 US companies have suspended existing share repurchase authorizations in the past two weeks, representing $190 billion of buybacks or nearly 25% of the 2019 total.”

Worse, as Kostin warns, reduced cash flows and select restrictions mandated as part of the Phase 3 fiscal legislation “suggest more suspensions are likely.” And since buybacks have represented the single largest source of US equity demand in each of the last several years…

… Goldman believes “higher volatility and lower equity valuations are among the likely consequences of reduced buybacks.”

Which brings us to the $64 trillion question: can buybacks still provide support to equities?

According to Goldman, with corporate fundamentals deteriorating, share repurchases are likely to be reduced this year, providing less support to equity demand:

Our US strategy team has found the fluctuations in profit growth are a key driver of buyback growth (Exhibit 13). Our strategists expect S&P 500 EPS to decline 33% in 2020 (with a -123% YoY growth in Q2) and 45% in Europe. Dividends, which are usually less volatile than buybacks, are already pricing large cuts for this year. Dividend swaps are pricing a 17% and 21% S&P 500 cut, and a 38% and 18% EURO STOXX 50 cut for 2020 and 2021 respectively

In short: the buyback bonanza is over for the foreseeable future.

After plunging into Friday’s close, US equity futures markets are extending losses at the open after President Trump extended the virus guidelines (lockdown) until April 30th.

Dow futures have erased most of Thursday’s surge gains…

But oil was the big mover as WTI plunged as much as 7.5% to a $19 handle…

That is the lowest since early 2002…

The kingdom said on Friday that it hadn’t had any contact with Moscow about output cuts or on enlarging the OPEC+ alliance of producers. Russia also doubled down, with Deputy Energy Minister Pavel Sorokin saying oil at $25 a barrel is unpleasant, but not a catastrophe for Moscow.

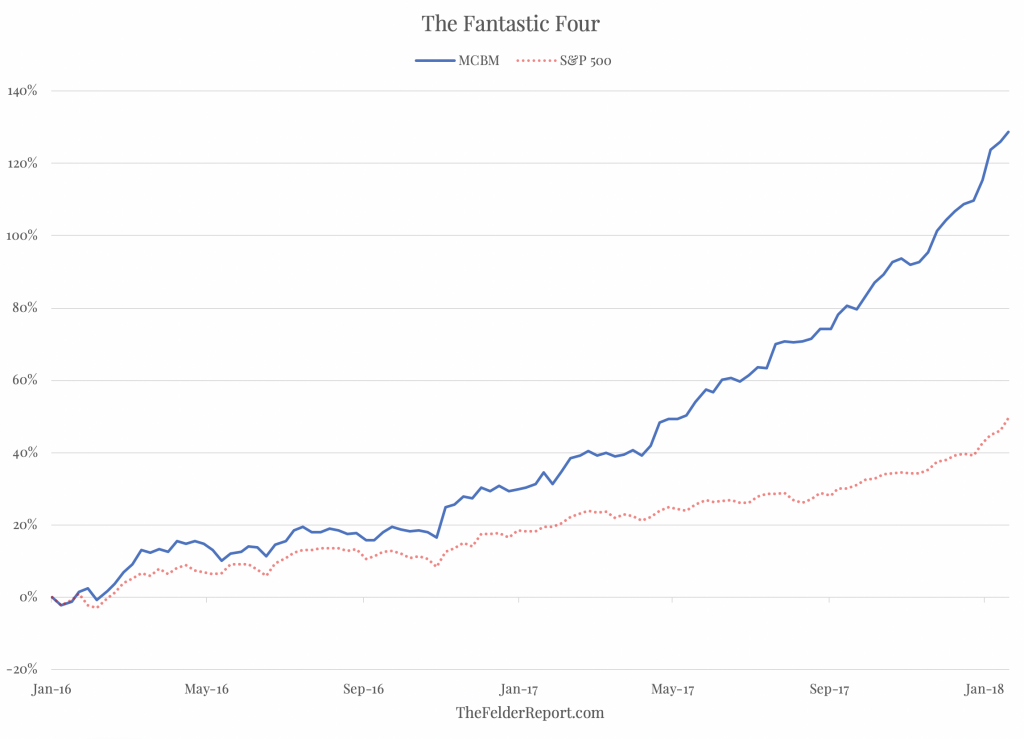

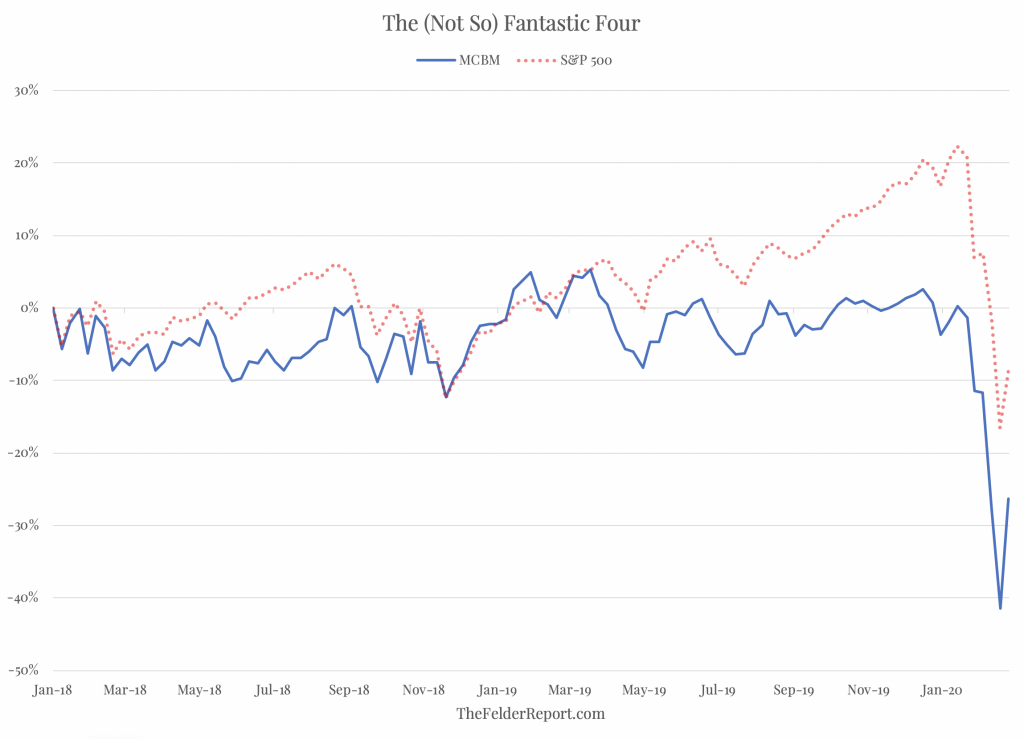

McDonald’s, Caterpillar, Boeing and 3M, known in these pages as MCBM, had seen their stock prices, as a group, soar over 120% during the prior two years, more than doubling the performance of the S&P 500 and blowing away any other group you might want to compare them to including the vaunted FANG stocks (Facebook, Amazon, Netflix and Google).

At the time I was astounded by the outperformance of these old, blue chip stocks and was curious to understand what was driving it so I dug a bit into their valuations. What I found was that it was entirely due to an expansion of their valuations to heights never before seen. What made this even more impressive was the fact that this came in response to record low revenue growth. Somehow, investors saw fit to reward these companies by paying unprecedented prices for their equity relative to their sales even as their long-term sales growth was turning negative for the first time ever.

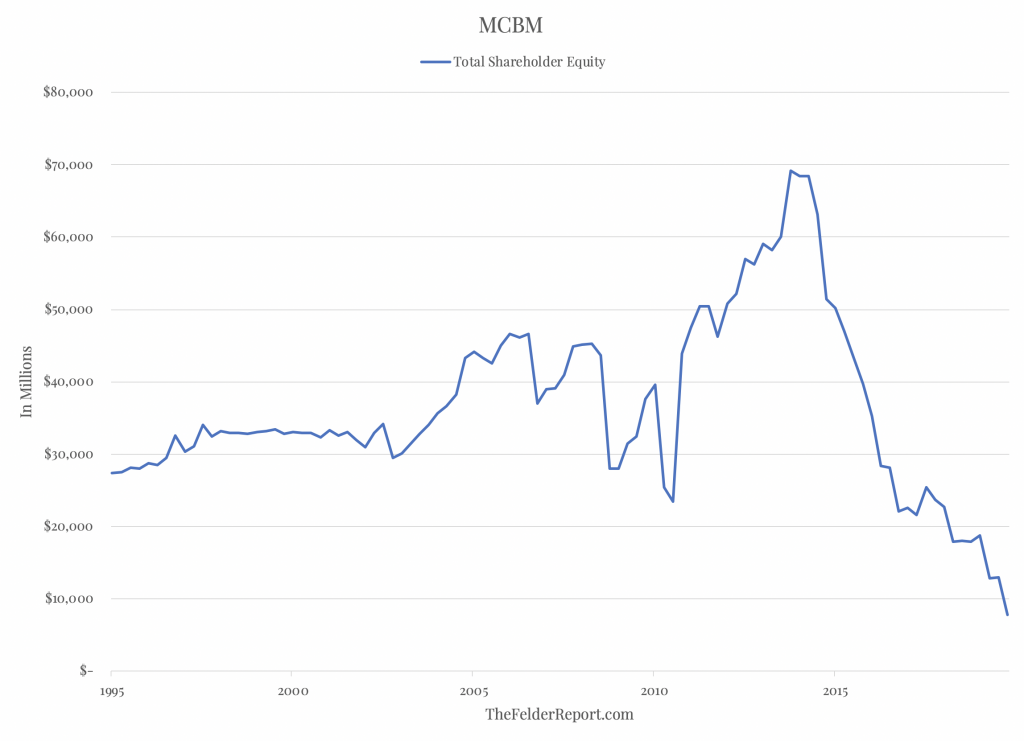

The explanation for this enigmatic episode was not too difficult to discover, however, once you took a look at their balance sheets. Over the past several years MCBM has issued a record amount of debt to buy back stock in massive quantities. This resulted in both the debt and the equity sides of their enterprise value calculation (market capitalization plus net debt) exploding even as sales growth imploded.

The success of this financial engineering, however, is already coming into question. Since that earlier post on the topic, the MCBM stocks have dramatically underperformed the market.

And all of that new debt now on their balance sheets, which is not offset by any new assets to speak of, could soon live up to the term “liability” during the nascent, coronavirus-catalyzed downturn. The best visualization of the predicament is the chart of the total net asset value of the four companies below. It has fallen 90% from $70 billion just a few years ago to about $7 billion today.

And while this precarious financial position should not inspire much confidence in shareholders, the fact that these stocks are still more expensive than they were at prior major market peaks (let alone troughs) should be even more worrisome. For this reason, the potential for further downside, even after losing more than a third of their values already, is significant.

So the question becomes, ‘Why did these companies sacrifice long-term financial health for short-term stock prices gains?’

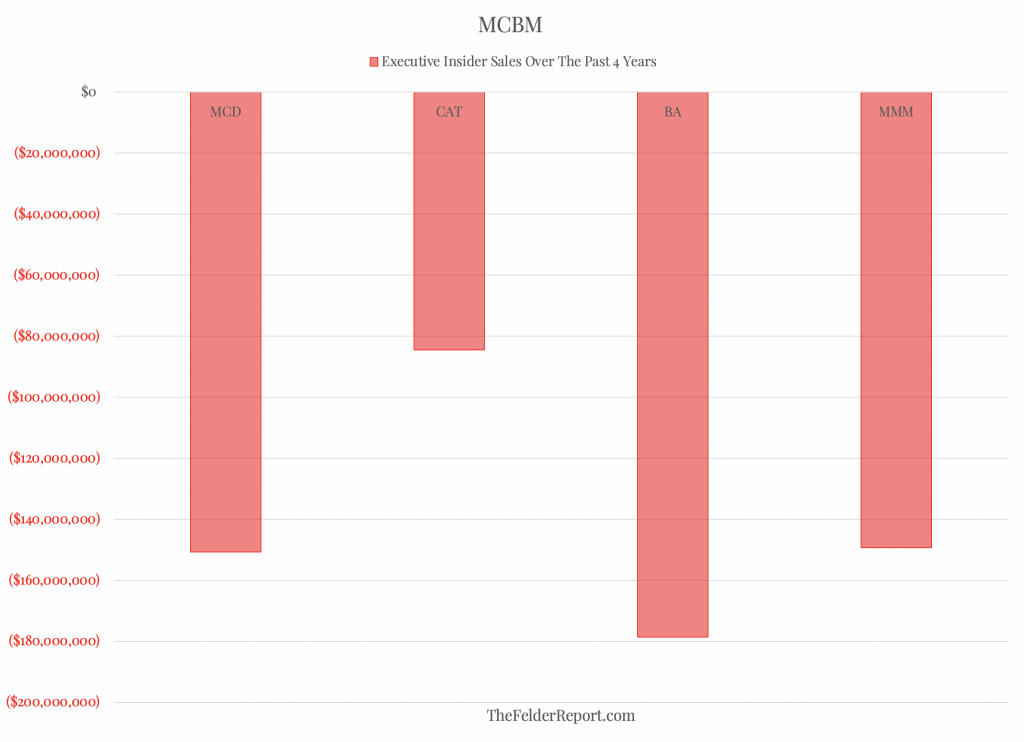

The answer lies in a little-noticed line on their cash flow statements labeled, “stock based compensation.”

On average, these companies each spent $200 million per year on issuance of options to top management. Those very same managers were the ones who decided it was a good idea to leverage the balance sheet to buy back stock. At the very same time, they also decided it wasn’t a good time to be a holder of those shares and so they sold, collectively, over half a billion dollars worth of their own shares in the open market. As I wrote about year ago, “If This Isn’t Stock Manipulation, I Don’t Know What Is.”

In conclusion, it looks pretty clear to me that the decision to leverage up the balance sheet to buy back stock had nothing to do with returning capital to shareholders or any other such nonsense. It was done entirely to boost earnings per share ensuring executive bonuses that would become even more valuable if the shares they were paid in were inflated through persistent manipulation by the company itself.

In other words, management got rich in the short run at the expense of the long-term health of the companies they ran.

I guess we’ll see how well that continues to workout for their remaining shareholders.

New York Internet Speeds Have Plunged As Locked-Down Americans Clog Networks

Download speeds for some US internet users have been bogged down in recent weeks as millions of Americans work from home due to ‘shelter-in-place‘ public health orders enforced by federal and state governments.

Some folks have resorted to “Netflix and quarantine” and free Pornhub Premium, both are streaming video sites that are data intensive.

As an economic depression rolls in, millions have just lost their jobs, the remaining few that can work remotely, are adjusting to a new reality that a pandemic will likely keep them out of the office for a considerable amount of time, have erected an office-like setting at their homes with streaming video and web conferencing.

With households now pulling record amounts of data, never before seen in the four-plus decade history of the internet, a new report suggests that 88 out of the top 200 most populated US cities have experienced some form of network degradation over the last week.

BroadbandNow says with millions of people working from home and using video streaming services, download speeds have plunged upwards of 40% in some US metropolitan areas last week (March 15-21), compared with the ten-week average.

San Francisco, Los Angeles, Chicago, and Brooklyn experienced limited to no network disruptions during the period.

However, New York City observed a 24% plunge last week in download speeds compared to the ten-week average.

Here is the list of major US cities that experienced a 20% or greater decline in download speeds last week, versus the ten-week average:

Austin, TX (-44%); Charlotte, NC (-24%); Fayetteville, NC (-22%); Fort Lauderdale, FL (-29%); Hialeah, FL (-21%); Houston, TX (-24%); Irvine, CA (-20%); Jersey City, NJ (-25%); Kansas City, MO (-25%); Lawrenceville, GA (-24%); Littleton, CO (-22%); Marietta, GA (-29%); Miami, FL (-27%); Nashville, TN (-20%); New York, NY (-24%); Omaha, NE (-24%); Overland Park, KS (-33%); Oxnard, CA (-42%); Plano, TX (-31%); Raleigh, NC (-20%); Rochester, NY (-33%); St. Louis, MO (-21%) St. Paul, MN (-29%); San Jose, CA (-38%); Scottsdale, AZ (-32%); Washington, DC (-30%); and Winston-Salem, NC (-41%).

The most severe network degradations were in Austin, TX (-44%), Winston Salem, NC (-41%), and Oxnard, CA (-42%).

With corporate America now working from home, BroadbandNow provides their take on how ISPs are responding to the dramatic shift:

In response to the shifting dynamic we are currently experiencing, providers have suspended data caps, increased base-level speeds, and extended free access to low-income internet plans and public hotspot programs in order to ensure as many Americans as possible can remain online during this period.

Many major ISPs have publically reassured users that they are more than able to keep up with the increased demand, and while looks to be largely true across the most populous areas of the US, it remains to be seen if rural communities reliant on legacy technologies such as DSL will continue to enjoy the same relative stability we have seen over the past week.

Surging data from US households could only mean one thing: “internet rationings” are next — something that is already happening in Europe. The move would prioritize web traffic to governments, emergency systems, and corporations.

Fueled by “dark money,” cash-flush liberal groups with ties to the Democratic Party are mobilizingto unleash millions of dollars worth of ads attacking President Donald Trump’s response to coronavirus ahead of the 2020 presidential election.

Many political groups avoided attacking Trump as the coronavirus outbreak first began to spread throughout the U.S. But as social distancing and quarantines become the new normal, a number of multi-million dollar ad buys from Democratic groups mark a departure from that strategy.

Democratic super PAC Priorities USA Action has spent more than $6 million on a series of negative ads attacking Trump on his response to the coronavirus pandemic. The group plans to spend $150 million contesting swing states before the Democratic National Convention.

One of the ads attacking Trump’s response to the coronavirus pandemic shows various audio clips of Trump downplaying coronavirus while a graphic shows the increasing cases overtime. The ads are airing in key presidential battleground states such as Florida, Michigan, Pennsylvania and Wisconsin. The ad starts off with a clip of Trump referencing coronavirus as Democrats’ “new hoax.”

Trump’s campaign argued that the hoax claim in the ad is false and issueda “cease and desist” ordering television stations that run the ad to stop if they want to “avoid costly and time-consuming litigation.”

In response, the super PAC announced Thursday it would spend another $600,000 to air ads in Arizona. The group plans to pour even more money in ads over the coming weeks.

Priorities USA spent more than $81,000 on Facebook ads this week alone on a newly created page called FactsFirst, primarily attacking Trump’s response to the coronavirus pandemic. Another page created in November 2019 has spent more than $132,000 on ads primarily targeting Spanish-speaking users with similar messages paid for by Priorities USA.

Priorities USA’s nonprofit arm plays a key role in the operation, funneling just under $3.4 million to its super PAC in the 2020 election cycle alone. That nonprofit has given six-figure contributions to other big-name Democratic dark money groups such as Majority Forward and VoteVets.

While Priorities USA may be the target of Trump’s lawsuit threats, another mysterious new 501(c)(4) nonprofit called Fellow Americans is also running ads almost identical to the controversial ad campaign paid for by Priorities USA.

Many Google and Facebook ads paid for by Fellow Americans feature disaffected Republicans planning to vote against Trump in the 2020 election. The ads could easily be mistaken for a solely conservative effort at first glance. But Washington, D.C., incorporation records show it formed in November 2019 by Graham Wilson, a partner at Perkins Coie, the political law firm of choice for many Democratic dark money groups — including American Bridge, Priorities USA and Acronym.

Even though the coronavirus outbreak is making it more difficult for some groups to run effective political ads, the message communicated in these ads could still be effective in hurting Trump closer to November and drum up donor support for the super PACs themselves for the general election, according to Kevin Banda, associate professor of political science at Texas Tech University.

“If people think that an incumbent responded poorly to a natural disaster, that incumbent and the incumbent party gets punished electorally,” Banda said.

Democratic super PAC American Bridge has shelled out almost $6.3 million on ads attacking Trump’s handling of coronavirus since the start of 2020. That makes up the bulk of the group’s $8.5 million in spending against Trump since the start of 2019. In an $850,000 digital ad campaign, American Bridge is airing ads in Wisconsin, Pennsylvania and Michigan attacking Trump for his past comments downplaying coronavirus, according to the New York Times.

The super PAC has received millions of dollars from the American Bridge 21st Century Foundation, a 501(c)(4) nonprofit that does not disclose its donors and is not supposed to have politics as its primary purpose. Like many super PACs with affiliated dark money groups, American Bridge’s affiliated groups share employees, officers, office space and other expenses.

A financial audit analyzed by OpenSecrets shows just under half of the American Bridge nonprofit arm’s spending went to a $3.3 million payment to its super PAC affiliate in 2018 for shared space and other expenses. On top of that, the nonprofit arm owed the super PAC over $1.45 million at the end of the year and it has given the super PAC more than $1.3 million in contributions. IRS rules prohibit the nonprofit from having politics as its primary purpose, which is generally interpreted to mean that less than half of its spending can go to political activities.

The majority of money comes from 29 anonymous six-figure donors giving up to $800,000 each. American Bridge’s noncash gifts include 450 shares of Baidu, a Chinese technology companywithreportedties to China’s Communist Party, valued at more than $100,000.

Liberal super PAC Pacronym launched a $2.5 million digital ad campaign attacking Trump’s handling of the global pandemic in mid-March. The ads will air on digital platforms including Facebook, YouTube and Hulu, according to the New York Times. The super PAC has raised nearly $8 million in the 2020 election cycle and plans to spend $5 million of that on digital ads by July.

Pacronym is the super PAC arm of Acronym, a dark money group that brought in almost $1.3 million in contributions from its inception in May 2017 through the end of April 2018, most of that coming from just four six-figure donors. Roughly one in every four dollars raised by Acronym in its first year of operation went to its super PAC, according to OpenSecrets’ analysis of tax records and campaign finance disclosures.

Acronym has also bankrolled digital operations seeding an array of “hyperlocal partisan propaganda” pages that mimic local news outlets and launcheda political tech company called Shadow Inc. exposed as the secret Iowa caucus app vendor after chaos at the caucuses. Shadow Inc. was paid by both current presidential candidate Joe Biden and former presidential candidate Pete Buttigieg‘s 2020 presidential campaigns, according to FEC disclosures.

A common thread among the groups is the role of liberal dark money powerhouse Sixteen Thirty Fund and its sister 501(c)(3) New Venture Fund. The groups have fiscally sponsored at least 80 groups in a way that leaves almost no paper trail. Sixteen Thirty acts as a pass-through agency funneling millions of dollars in grants from wealthy donors. Acronym and American Bridge have each accepted hundreds of thousands from Sixteen Thirty Fund’s operation while Priorities USA’s foundation arm has given it at least $100,000.

Unite the Country, a super PAC supporting former vice president Joe Biden in the 2020 presidential election, is spending at least $1 million to air a coronavirus-related attack ad on TV news programs across the country.

So far this cycle, Unite the Country has raised more than $12 million and while most of the super PAC’s donors are disclosed, the identities of some of its biggest financiers remain a mystery.

Biden’s campaign has also released ads criticizing Trump’s handling of coronavirus, but is spending much less. Traditionally, super PACs function as candidates’ attack dogs, running run negative ads that candidates wouldn’t want to be associated with.

Before the release of these new ads, neither Biden’s sole Democrat rival Sen. Bernie Sanders (I-Vt.), Biden or Trump aired a political ad on television since last Tuesday, according to the New York Times.

“Beware A Disorderly Dollar Surge”: Goldman Says The Dollar Rally “Is Not Over”

Two weeks ago we said that the unprecedented (and continuing) surge in the dollar is the result of a historic, 12 trillion dollar margin call, as issuers of dollar-denominated debt obligations around the globe, seeing their cash flows collapse scrambled to repatriate funds ahead of coming dollar maturities.

The result was the sharpest dollar spike in decades. Of course, such a margin call meant that not only was the economy about to crater but it could also drag the entire global financial system with it unless policymakers somehow found a way to inject trillions of fresh liquidity into the system and restore some confidence that the Fed was still in control. That’s what happened last week, when the Fed expanded various Lehman-era liquidity facilities and added a whole host of new ones – including buying IG corporate bonds – while central banks around the globe intervened with their own set of coordinated liquidity operations.

Long story short, the intervention worked – for now – and the result was the biggest weekly drop in the DXY Dollar index since, drumroll, the Plaza Accord which saw another massive coordinated intervention to crush the US dollar.

And, as Goldman’s FX strategist notes, “we are about to find out whether it will be enough.”

The problem is that while both the monetary and fiscal bazookas have been fired (and according to Paul Tudor Jones, it was actually nuclear bombs, not bazookas), “in the West, the economic fallout from the outbreak is only just beginning.”

Furthermore, while markets may be able to look through some pretty horrible economic data—like the non-reaction to the historic spike in US jobless claims last week—they will will be extremely sensitive to news on the duration of shutdowns and any signs of second-round effects (e.g. business failures, significant layoffs or earnings weakness outside of travel and hospitality sectors, or sovereign downgrades).

With that in mind, Goldman does see a light at the end of the tunnel: “there is still a reasonably strong argument for a V-shaped recovery, and policymakers are working hard to bring about that outcome.” But, as Pandl notes, “without medical breakthroughs of some kind, the next few weeks could be challenging for markets as we price in a deep global recession.”

What does that mean for the dollar? Long story short, what just came down, may soon go up.

As Pandl summarizes, “the Dollar pulled back this week as risk assets rebounded, but our best guess is that the historic rally is not quite over” and in a further equity market drawdown – one which Goldman believes is inevitable…

… the real trade-weighted Dollar has perhaps 3-5% upside from the latest highs, in our view.

This would take the Dollar close to its peak during the last bull market (which ended in February 2002) and key crosses (e.g. EUR/USD and USD/CAD) to levels which might prompt debate over US-directed intervention.

In terms of specific trades, Goldman believes that”

FX investors should remain cautious, with longs in traditional safe havens such as USD, JPY, CHF, and a focus on relative value

Investors should stay defensive in emerging-market currencies as markets continue to digest incoming news on the virus and its impact on economic activity

MXN, last week’s outperformer, will likely give up some of its gains should risk sentiment sour again

EM high-yielders that have yet to surpass “severe’’ undervaluation levels, and face rising concerns surrounding Covid-19, such as RUB and ZAR, may also be hit hard

Deeply undervalued currencies in Latin America, including BRL, CLP and COP, appear to be attractive when paired against oil-importing and lower-volatility currencies of EM Asia

His conclusion: “Although intervention has been rare in recent years, the disorderly surge could call for a policy response.”

Goldman is not alone in expecting more dollar upside after last week’s historic drop: according to BofA’s fundamental and technical analysts, the ongoing COVID-19-related financial market & economic shocks suggest “further USD appreciation ahead”, to wit:

Further financial market de-risking, persistent USD demand, sticky FX carry and continued US economic divergence underpin the case for more USD strength ahead, after the recent retracement. This despite sharply lower bond yield differentials, which have turned correlations on end, highlighting the extent of USD overshoot and rich long-term overvaluation.

To simply the message, here is an even quicker hot take: “Market turbulence + global recession = USD higher”

Out economists are now calling for a global recession. Economic contractions around the world are likely to be significant, notwithstanding policy response. A history of recessions indicates that risk assets are likely to remain under pressure for an extended period – months and possibly quarters.

We therefore continue to think that the US dollar will remain supported as economic and financial fallout of COVID-19 leads to persistently volatile conditions in which flows tend to seek perceived safe havens, the US included.

Our call remains that in such conditions:

USD should continue to appreciate on most pairs with the exception of JPY and CHF, and that

currencies suffering the greatest term of trade declines due to the energy market crash and the highest external financing requirements (necessitating large capital inflows) are likely to continue to underperform (Chart 6).

And although the US runs a substantial current account deficit, USD carry and favorable relative growth prospects probably offset these external sector-related risks, particularly given that USD is the world’s reserve currency.

Picking up where Goldman leaves off, and using almost the exact same words, BofA warns that “sharp, potentially “disorderly” USD appreciation is increasingly consistent with coordinated FX interventions in the past. Typically, the DXY appreciates 3-5% over a 1-2 month window in volatile conditions prior to interventions to sell USD, based on our research. And although G20 commitments expressly forbid targeting exchange rate levels for competitive purposes, history suggests that levels do play an important role in the decision to conduct coordinated interventions, with USD often making new highs prior to efforts to suppress strength historically. In our view, any intervention to counter excessive USD appreciation must be coordinated to be successful. Coordinated, clearly-articulated intervention among global central banks and finance ministers sends a strong and unified signal to markets that cannot be duplicated with sporadic intervention flow, which given the limited size of CB balance sheets is extremely small in relation to FX turnover.”

Which brings us to the $12 trillion question: when will the dollar be so high as to trigger intervention? BofA’s answer:

When could the case for intervention build? Floating exchange rates are designed to address economic and terms-of-trade shocks such as COVID-19. A key tradeoff is shock absorption vs. market disorder and capital flight risk. We do not think that exchange rates have adjusted enough to justify global central bank participation just yet. But because the virus is global, weak FX translates to tighter US financial conditions. Consequently, we suspect that the US could begin to push for a coordinated FX response with DXY above 104 and EUR/USD below 1.05 (highest and lowest levels since 2002). But we suspect that broad agreement on the need to contain dollar strength will emerge at higher USD levels.

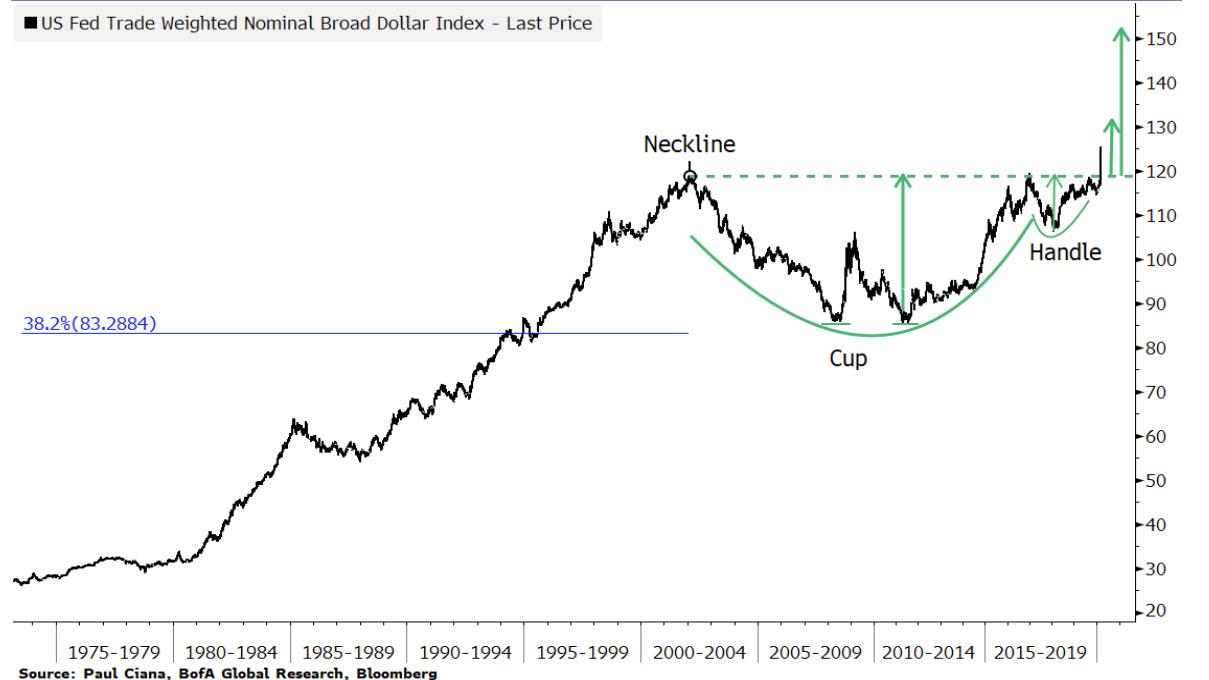

One last point in case the above was not enough, here is BofA’s Chief Technician, Paul Siena calling for a long-term bullish breaking in the US trade weighted dollar:

The US Federal Reserve’s trade weighted nominal broad dollar index data begins in 1973. Since then the trend has been up with notable corrections in 1978, 1985-1988, 2002-2010 and 2017. A double bottom began to form in 2011 and thereafter the trend began rounding out the “cup” portion of a bullish cup and handle technical pattern. The correction in 2017-2018 and rally back in 2018-present formed the “handle.” The surge in the US dollar this year broke the neckline of the pattern as the index reached a new all-time high. This breakout confirms the pattern, suggests more new highs to come and activates an initial upside target in the low 130s and an overall bullish trend into the 150s. This supports our bullish USD view.

Rats Swarm New Orleans’ French Quarter After Citywide Coronavirus Lockdown

CBS News has published disturbing images of rats invading the once bustling streets of the French Quarter in New Orleans after the city belatedly went on lock down, as the state of Lousiana over the weekend saw confirmed coronavirus case numbers explode past 3500, including 151 deaths. Most have been at the newly emerged outbreak epicenter in the south, New Orleans.

Cafes, restaurants, bars and once packed clubs have been shuttered, cutting off what’s always been a steady food supply for the rodents, causing them to venture further out for food into the streets as photographs reveal.

Rats have swarmed the French Quarters amid a city-wide ‘shelter in place’ order, via CBS/Daily Mail

A city-wide shelter in place order has left streets barren a mere weeks after Mardis Gras saw its average some 1.5 million outside tourists and party-goers descend on the Big Easy.

The almost unheard of shutdown of the city’s businesses is “driving our rodents crazy” —in the words of to Mayor LaToya Cantrell who addressed the growing problem in a local broadcast.

Man I wish I lived in a big city

When times get tough

Your neighbors come out to help

New Orleans’ famous Mardi Gras celebration brought thousands of tourists to the city, and medical experts believe it might be a big factor in the city’s COVID-19 outbreak. Now with Bourbon Street’s famous bars all closed and people social distancing, videos show dozens of rats scurrying through the empty streets.

“I turn the corner, there’s about 30 rats at the corner, feasting on something in the middle of the street,” Charles Marsala of New Orleans Insider Tours and AWE News told CBS News’ Omar Villafranca. Marsala said he had “never” seen anything like it before.

Via CBS/Daily Mail

Mayor Cantrell has recently said that “in hindsight” Mardi Gras should have been canceled, after health officials have said New Orleans’ recent explosion in cases was likely due to the weeks-long festival running January 6 to February 25, which marks Fat Tuesday.

Bourbon Street amid the outbreak, following the ‘shelter in place’ order, via Reuters.

“In hindsight, if we were given clear direction, we would not have had Mardi Gras, and I would have been the leader to cancel,”she said in a CNN interview last week, also blaming local decisions ultimately on “our national leader”.

Meanwhile, city health officials are attempting to combat the rat infestation problem, with Claudia Riegel, executive director of the New Orleans Mosquito, Termite and Rodent Control Board, warning residents that “there are pathogens in these rodents”.

Riegel said added, “Fortunately, we … don’t have many disease cases that are related to rodents. But the potential is there.”

“Unfortunately, with these businesses being shut down, these rats are hungry,” she said further. Part of the city’s strategy is to not only control the trash problem, telling residents to not set out trash with abundance of discarded food, but to ramp up its use of rat bait and traps in commercial areas.

We are at a critical moment in the history of politics and markets. Everyday the U.S. government stares into the fiscal and monetary abyss and chucks trillions in hoping that will be enough to finally fill it.

We stand by hoping that it will work to reflate markets collapsing from a catastrophic mispricing of assets. At least some of us do. I don’t.

I hope it fails and it’s because those inflated prices fuel the very global political order that is anathema to human advancement.

President Trump is finally happy with his FOMC chair, Jerome Powell, after he opened the door to unlimited quantitative easing, nearly unlimited liquidity injections via the repo markets, and taking interest rates to the zero-bound.

It’s clear that the Keynesians at the Fed and the U.S. Treasury Dept. have no answers to the problems in front of them. They are simply doing what they always do when a crisis hits. Print money and hope someone still believes the new money is worth buying.

The sudden supply and demand side shock to the global economy thanks to the COVID-19 coronavirus is outside of their frame of reference.

To best understand what we’re dealing with here you have to understand how these people think. Modern economic theory, based on John Maynard Keynes’ General Theory of 1936, imagines the economy as a bathtub.

And that bathtub is constantly draining as credit is destroyed. Money flowing out of the economy has to be replaced with a constant stream of new money, in the form of new credit, or the bathtub drains. The velocity of new money has to keep up with old money or the system drains.

When the credit markets through the transmission of new money through central bank policy cannot keep the bathtub full, governments are supposed to step up with fiscal spending in the form of deficits to make up the difference.

This is then supposed to stimulate aggregate demand and, in turn, the credit markets to keep everything running. This is done to chase an ever-larger global gross product as measured by total spending.

I’m not here to argue as to why this is patent nonsense. I’m going to state that it is. And I state this without reservation. Because it places zero value on the cost of stealing time from the productive portion of the society to reinforce the unproductive.

That’s why all money printing is fundamentally immoral. It’s thievery, transferring wealth from the holders of money, savers, to the holders of the new money.

That deflation the Keynesians are so afraid of is the cure to the malinvestment of capital resources incurred because of the last time the government intervened to refill the bathtub.

This system is ultimately a Ponzi scheme piling credit on top of credit until there are no more greater fools to sell the new debt to.

That’s the system we have. And it is collapsing precisely because the world is situated at the point where there is little more productive capacity to monetize and pull that capital from the future to fund the new debt.

It won’t matter if we replace this system with pure helicopter money without debt as the Modern Monetary Theory proponents argue. We’re already doing a version of this by having the central banks buy debt they never intend to sell on the open market. So, the debt itself is without value. The money printed from those bonds is as much scrip as if the bond had never been issued.

But the time lost by people in pursuit of uneconomic ends by mispricing risk and servicing debt they are legally obligated to service is real.

So, ultimately, the difference at this point between what we’re seeing from the central banks now and MMT is a matter of accounting and definitions. But it doesn’t solve the basic problem that prices for things want to adjust downward.

And I remind you that Russian President Vladimir Putin understood all of this when he said no to OPEC+ and lower oil production. This pricked the so-called “Everything Bubble” and now the world is realizing just how important it is for capital markets to reflect the actual goods and services produced by the global economy not a financialized multiple of that value thereof.

It’s important to make this distinction now because as a hard money advocate and Austro-libertarian thinker it is my duty to counter the rising cries for someone to save us from the evil monster of deflation.

Those most vulnerable to this deflation of asset prices are the very people who own most of those assets and use them as cudgels to beat down those who oppose them — think Iran, Venezuela and, most openly, Russia.

The good news is that they can’t stop the deflation. Quantitative easing is, in the real world, deflationary because it signals to markets that the central banks are so scared of the future that it cannot be trusted to market forces. This feeds the fear and causes people to hoard money they feel is undervalued, thereby exacerbating the cycle.

And today those monies are the U.S. dollar, gold and, to a lesser extent, Bitcoin.

So, the Fed fired its bazooka. Congress fought for a couple of days in deciding how it would provide its support through government means (fiscal policy) and refill the bathtub.

The rest is now a question as to whether anyone still believes this makes any sense anymore.

The ECB has yet to truly act other than to intervene in the sovereign debt markets to keep rates from exploding to the upside. The Fed has the floor right now, the ECB is waiting in the wings. It will have to act soon as Italy’s economy goes into freefall and its insolvent banking system has to find a way to survive.

Because the reality is that what is really on trial here is the idea that any of these people in charge have, collectively, one single clue as to what to do to stave off a complete collapse in confidence.

I would like to think that they do, that they know in their heart of hearts that I am right and allowing asset prices to deflate is the cure and the inflation of prices has been the real disease we should be fighting alongside COVID-19.

And the main reason they will not allow that deflation is because it directly threatens their personal power base and the fundamentally unfair system they have profited from through the extraction of unearned wealth at the world’s expense.

I believe some of them understand this dynamic. The true vultures, like George Soros and Paul Singer, I’m sure do. But the vast majority of these people in charge in both Europe and the U.S. believe what they were taught about the economy in college and today execute plans based on what they have been miseducated in.

And that actually scares me far more than if they were doing this out of pure malice.

Incompetence honestly applied is far more dangerous than honest evil disingenuously applied. Because in the former environment the purely malicious can operate with few if any controls.

The world is changing before our eyes while we hide out in our homes hoping not to catch a virus that won’t do more than inconvenience most of us. But we are still at a crossroads. Putin set us on the path to choose deflation, he understood the problem as I am presenting it here.

Now will we take the opportunity handed to us and tighten our belts, demand debt liquidation, corporate bankruptcies and a complete reshuffling of the global capital order?

Or will we choose to be complicit in debasing our ourselves through access to the printing press, actively devaluing our time and labor by accepting digits added to our bank balances which no one sweated or worked to produce?

Bankruptcies or bailouts? That’s the question you should be asking yourself. You can’t bail out Main St. without bailing out Wall St. To bankrupt Wall. St. and all that it funds a lot of us will have to be bankrupted as well.

Are you willing to take that pain to stop the money machine that funds the death and destruction? If not then you aren’t serious about wanting it to end.

And that’s the real crossroads we have come to, the one where we realize there is no such thing as a free lunch and our inaction to this point makes us culpable for what has been done.

Watch Live: White House Task Force Holds Sunday Press Briefing As Confirmed Cases Boom

With the number of new cases and deaths ballooning at a surprisingly rapid pace across the US (but especially in New York, the nation’s biggest hot spot), President Trump and the White House task force (led by VP Mike Pence DHHS Secretary Alex Azar, Dr. Birx, Dr. Fauci, Dr. Adams and the rest) are holding their daily press briefing at 5pmET, just an hour before futures open.

The event will reportedly take place in the White House Rose Garden.

Saudis Claim US Patriot Missiles Activated In Major Yemeni Houthi Attack On Riyadh

Houthi rebels in Yemen over the weekend launched what’s being described as among the largest assaults on Saudi Arabia since the start of the war five years ago.

Starting on Saturday the Saudi military said it intercepted at least two ballistic missiles over the capital of Riyadh, as well as over the southern city of Jizan, in the first such major attack in more than a year.

Saudi military spokesman Turki al-Malki confirmed there were injuries among residents on the ground from “debris scattering on some residential areas” in Riyadh and Jizan.

Over the past months the US has bolstered its Patriot missile batteries in Saudi Arabia to “counter Iran”.

Saudi press agency SPA later said “two civilians were slightly injured due to the falling of the intercepted missile’s debris as it exploded in mid-air over residential districts”.

At least three blasts were heard in Riyadh during the attack, followed by the blare of emergency sirens. Saudi-owned Al-Arabiya television also indicated significantly thatUS-supplied Patriot missiles were activated during the attack.

On Sunday a military spokesman for Yemen’s Houthi movement confirmed responsibility for the major attack, saying, “the joint military operation of the missile force and the Air Force managed to target a number of sensitive targets in the capital of the Saudi enemy, Riyadh, with Zulfiqar missiles, and a number of Samad-3 aircraft.”

Houthi missile launch on Riyadh

“The major military operation also targeted a number of economic and military targets in Jizan, Najran and Asir, with a large number of Badr missiles and 2K bombers,” he added.

The Houthi military spokesman warned: “The Saudi regime will suffer from these painful operations if it continues its aggression and siege on Yemen,” and promised to keep up the pressure, noting “the armed forces will reveal the details of the wide and qualitative military operation in the coming days.”

However, one military analyst cited by Al Jazeera dismissed the weekend operations as a major PR initiative by the Houthis geared toward “appearing stronger than they are”.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}