Those following the news from Russia have probably heard that Russia’s only aircraft carrier, the Admiral Kuznetsov (official name: Admiral of the Fleet of the Soviet Union Kuznetsov), was put into dry dock for major repairs and retrofits. Things did not go well.

First, the dry dock sank (it was Russia’s biggest) and then a huge crane came crashing down on the deck. And just to make it even worse, a fire broke out on the ship killing 2 and injuring more. With each setback, many observers questioned the wisdom of pouring huge sums of money into additional repairs when just the scheduled ones would cost a lot of money and take a lot of time.

Actually, the damage from the fire was not as bad as expected. The damage from the crane was, well, manageable. But the loss of the only huge floating dry dock is a real issue: the Kuznetsov cannot be repaired elsewhere and these docks cost a fortune.

But that is not the real problem.

The real problem is that there are major doubts amongst Russian specialists as to whether Russia needs ANY aircraft carriers at all.

How did we get here?

A quick look into the past

During the Soviet era, US aircraft carriers were (correctly) seen as an instrument of imperial aggression. Since the USSR was supposed to be peaceful (which, compared to the USA she was, compared to Lichtenstein, maybe less so) why would she need aircraft carriers? Furthermore, it is illegal to transit from the Black Sea to the Mediterranean through the Bosphorus with an aircraft carrier and yet the only shipyard in the USSR which could built such a huge ship was in Nikolaev, on the Black Sea. Finally, the Soviets were acutely aware of how vulnerable US aircraft carriers are to missile attacks, so why built such an expensive target, especially considering that the Soviet Union had no AWACS (only comparatively slow, small and much less capable early warning helicopters) and no equivalents to the F-14/F-18 (only the frankly disappointing and short range Yak-38s which would be very easy prey for US aircraft).

Eventually, the Soviets did solve these issues, somewhat. First, they created a new class of warships, the “heavy aircraft carrying cruiser”: under the flight deck, these Soviet aircraft carriers also held powerful anti-ship missiles (however, this was done at the cost of capacity under the deck: a smaller wing and smaller stores). Now, they could legally exit the Black Sea. Next, they designed a very different main mission for their “heavy aircraft carrying cruiser”: to extend the range of Russian air defenses, especially around so called “bastion” areas where Russian SSBNs used to patrol (near the Russian shores, say the Sea of Okhotsk or the northern Seas). So while the Soviet heavy aircraft carrying cruiser were protecting Russian subs, they themselves were protected by shore based naval aviation assets. Finally, they created special naval variants for their formidable MiG-29s and Su-27s. As for the AWACS problem, they did nothing about it at all (besides some plans on paper). The collapse of the USSR only made things worse.

The Soviets also had plans for a bigger, nuclear, aircraft carriers, and on paper they looked credible, but they never made it into production. These supposed “super carriers” would also come with a truly “super” price…

So how good was/is the Kuznetsov?

Well, we will probably never find out. What is certain, however, is that she is no match for the powerful U.S. carriers, even their old ones, and that the USA has always been so far ahead of the USSR or Russia in terms of carriers and carrier aviation that catching up was never a viable option, especially not when so many truly urgent programs needed major funding. Did the Kuznetsov extend the range of Russian air defenses? Yes, but this begs the question of identity of the “likely adversary”. Not the USA: attacking Russian SSBNs would mean total war, and the U.S. would be obliterated in a few short hours (as would Russia). I don’t see any scenario in which US ASuW/ASW assets would be looking for Russian SSBNs anywhere near the Russian coasts anyway, this would be suicidal. What about smaller countries? This is were the rationalizations become really silly. One Russian (pretend) specialist even suggested the following scenario: the Muslim Brotherhood in Egypt takes power, thousands of Russian tourists are arrested and the Islamists demand that Russia give full sovereignty over to all Muslim regions of Russia, if not: then hundreds of Russians will get their throats slit on Egyptian TV. Can you guess how an aircraft carrier would help in this situation?

Well, according to this nutcase, the Russian carrier would position itself off the Egyptian coast, then the Russians would send their (pretty small!) air-wing to “suppress Egyptian air defenses” and then the entire Pskov Airborne Division would be somehow (how?!?!?!) be airlifted to Egypt to deal with the Ikhwan and free the Russian hostages.

It makes me wonder what this specialist was smoking!

Not only does it appear that the Egyptians are currently in negotiations with Moscow to acquire 24+ brand new Su-35s (which can eat the Russian airborne aircraft for breakfast and remain hungry for more), but even without these advanced multi-role & air superiority fighters the rest of the Egyptian air defenses would be a formidable threat for the relatively old and small (approx.: 18x Su-33; 6x MiG-29K; 4x Ka-31; 2x Ka-27) Russian airwing. As for airlifting the entire 76th Guards Air Assault Division – Russia simply does not have the kind of transport capabilities to allow it to do that (not to mention that Airborne/Air Assault divisions are NOT trained to wage a major counterinsurgency war by themselves, in a large and distant country). Theories like these smack more of some Russian version of a Hollywood film than of the plans of the General Staff of Russia.

Back to the real world now

Frankly, the Kuznetsov was a pretty decent ship, especially considering its rather controversial design and the appalling lack of maintenance. She did play an important role in Syria, not thanks to her airwing, but to her powerful radars. But now, I think that it is time to let the Kuznetsov sail into history: pouring more money in this clearly antiquated ship makes no sense whatsoever.

What about new, modern, aircraft carriers?

The short answer is: how can I declare that the USN has no rational use left for its aircraft carriers and also say that the Russian case is different and that Russia does need one or perhaps several such carriers? The USN is still several decades ahead of modern Russia in carrier operations, and (relatively) poor and (comparatively) backward Russia (in naval terms) is going to do better? I don’t think so.

Then, there is one argument which, in my opinion, is completely overlooked: while it is probably true that a future naval version of the Su-57s (Su-57K?) would be more than a match for any US aircraft, including the flying brick also knows as F-35, Russia STILL has nothing close to the aging but still very effective carrier-capable USN Northrop Grumman E-2 Hawkeye. Yes, Russians have excellent radars and excellent airframes, but it is one thing to have the basic capabilities and quite another to effectively integrate them. As always, for Russia, there is the issue of cost. Would it make sense to finance an entire line of extremely costly aircraft for one (or even a few) aircraft carriers?

We need to keep in mind that while Russia leads the world in missile technology (including anti-shipping missiles!), there are many countries nowadays who have rather powerful anti-ship missiles too, and not all are so friendly to Russia (some may be at present, but might change their stance in the future). Unless Russia makes a major move to dramatically beef-up her current capabilities to protect a high-value and very vulnerable target like a hypothetical future aircraft carrier, she will face the exact same risks as all other countries with aircraft carriers currently do.

A quick look into the future

Hypersonic and long range missiles have changed the face of naval warfare forever and they have made aircraft carriers pretty much obsolete: if even during the Cold War the top of the line U.S. carriers were “sitting ducks”, imagine what any carrier is today? The old saying, “shooting fish in a barrel” comes to mind. Furthermore, what Russia needs most today are, in my opinion, more multi-role cruise missile and attack submarines SSN/SSGN (like the Yasen), more diesel-electric attack submarines SSK (like the Petropavlovsk-Kamchatsky), more advanced patrol boats/frigates (like the Admiral Kasatonov), more small missile ships/corvettes (like the Karakurt), more large assault ships (like the Petr Morgunov) and many, many, more.

As for aircraft carriers, they are not needed any more to extend the (already formidable) Russian air defenses and in the power-projection role (operations far from Russia), the Russian Navy does not have the capabilities to protect any carrier far away from home shores.

Which leaves only three possible roles:

1) “Showing the flag”, i.e. make port calls to show that Russia is as “strong” and “advanced” as the US Navy. Two problems with that: i) the USN is decades ahead of Russia in carrier operations and 2) there are MUCH cheaper way to show your muscle (the Tu-160 does a great job of that).

2) “Retaining the carrier know-how”. But for what purpose? What naval strategy? What mission? Russia is the nation that made aircraft carriers obsolete – why should she ignore her own force planning triumphs?

3) Prestige and $$$ allocation to select individuals and organizations within and next to the Russian Navy. Since Russia does not have a money-printing-press or criminally bloated budgets, she simply cannot afford the capital outlay either for the Russian Navy, or for the nation of Russia, just to fill the pockets of some interested parties.

Conclusion:

If I have missed something, please correct me. I don’t see any role for carriers in the future Russian Navy. That is not to say that I am sure that they won’t be built (there are constant rumors about future Russian “super” carriers, no less!), but if they are built, I believe that it will be for all the wrong reasons.

The plight of the Kuznetsov might be blessing for Russia. She was a good ship (all in all), but now she should be viewed as an object lesson to (hopefully) kill any plans to build more carriers for the Russian Navy.

Hindsight is 20/20. It can be incredibly difficult to pick the “next big stock” in the moment, but, as Visual Capitalist’s Jenna Ross notes, looking back gives us clarity on where we could have reaped the highest rewards. While some of the decade’s chart-toppers – like Netflix and Amazon – are household names, other stocks may come as a surprise.

Today’s visualization reveals the best-performing stocks over the last 10 years, and shows how much an initial $100 investment would be worth today.

The Shortlist

To compile the list, MarketWatch reviewed the current S&P 500 constituents and excluded any stocks that have traded in their present form for less than 10 years. The remaining companies were sorted based on their total return, with reinvested dividends, from December 31, 2009 to December 5, 2019.

So, which stocks come out on top? Here’s a full list of the top 20, organized by ranking:

Note: The final value of a $100 investment is based on the total return, with reinvested dividends, from December 31, 2009 – December 5, 2019.

In comparison, $100 in the S&P 500 index overall would have amounted to $344 over the same time period. Let’s take a closer look at these strong performers.

Household Names

Streaming giant Netflix takes the #1 spot. The company earned a staggering 3,767% return over the last ten years, meaning an initial $100 investment would now be worth almost $4,000. However, it remains to be seen whether Netflix’s first mover advantage will remain strong with new competitors entering the space.

One such rival, Amazon, takes its spot at #10 in the best-performing stocks of the decade. From its humble roots as an online bookseller, the company has transformed into an ecommerce leader. CEO Jeff Bezos credits Amazon’s admirable success to three key customer-centric factors: listen, invent, and personalize.

At #12 on the list, Constellation Brands—owner of several alcohol brands such as Corona—is also no stranger to invention. The company is protecting itself against cannabidiol (CBD) disruption with a $5 billion dollar investment in Canopy Growth, and future plans to create its own CBD-infused beverages.

Other well-known names on the top 20 list include discount department store chain Ross Stores (#15) and the credit card company Mastercard (#17), with the latter benefiting from an oligopoly in the industry.

Flying Under the Radar

Apart from the names you’d expect to see, there are also some lesser-known companies that made the list.

Well established among institutional investors and broker-dealers, MarketAxess Holdings takes the #2 spot. The fintech company operates a global electronic bond trading platform, vastly improving the process for investors who traditionally traded bonds “over-the-counter”.

In third place, healthcare technology company Abiomed develops medical devices that provide circulatory support. The company’s Impella® device—the world’s smallest heart pump— has been used to treat over 50,000 U.S. patients.

Fourth place company Transdigm Group gains its stronghold by developing specialized products for the aerospace industry. It has a strong acquisition strategy as well, having acquired over 60 businesses since its formation in 1993.

A Sector View

If we organize the top 20 by sector, information technology stocks appear in the list most frequently with five companies, followed by consumer discretionary (4 companies), and industrials and healthcare (3 companies each).

Sectors with less representation in the top 20 are communication services (2 companies), as well as consumer staples, financials, and real estate (1 company each).

The Bottom Line

While these stocks have performed extremely well over the last decade, they are not necessarily the best portfolio additions today. Some companies may have become overvalued, or be facing new competition in their industry—as is the case with Netflix. It’s best to consider all current information when building a portfolio.

However, the top 20 stocks do demonstrate the power of a buy-and-hold strategy. If you’re lucky enough to identify a winner early on, it’s possible to simply sit back and let your dollars grow.

Today’s note is on the macro structure of the Long Now.

Today’s note is on the untethering of fundamental linkages between the economic policies that organize our social lives as investors and citizens.

SNIP!

Today’s note is on how we survive the Long Now. Because it won’t be easy.

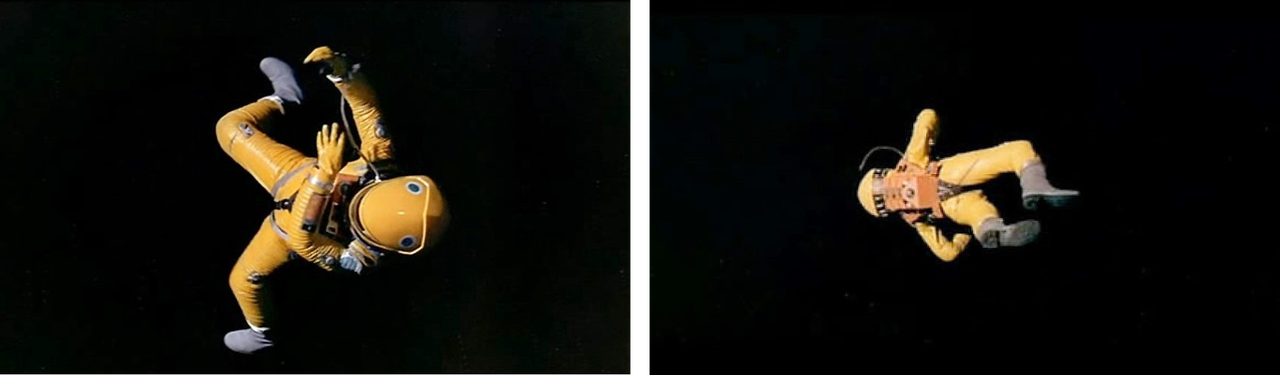

That’s George Clooney in Gravity, right before he ends up like this.

The spacewalking astronaut, risking the abyss with only a slim tether to life, is a powerful trope. Gravity was an entire movie about that frisson of fear we get from these images, although for my money it doesn’t get better than Frank Poole’s murder by HAL in 2001: A Space Odyssey, with the looong shot of the body tumbling uncontrollably through space. Because it’s not just the aloneness and abandonment that sparks our hard-wired emotional response here, but the out-of-controllness of being truly untethered.

We’ve got happy-ending movies that use this trope (The Martian), Russian movies that use this trope (Spacewalker), and even haunted-house-in-space movies that use this trope (Event Horizon). So you’ll forgive me if I’m going to use this imagery, too, because it’s the best story-telling device I know to instill in you the fear and loathing I feel when I think through the consequences of the Long Now.

SNIP! is the Long Now’s destruction of the meaning of words that define our social connections.

Words like “war”.

This is a picture of the Predator drone firing a Hellfire missile.

It’s probably going to kill someone that we want dead, and almost certainly going to kill some other people that we don’t mind being dead … collateral damage and all that. As they say on Succession, you can’t make a Tomlette without breaking a few Greggs. This is war, and we fire these missiles all over the world, on the daily, both in countries we have officially invaded, like Afghanistan, and in countries we haven’t, like Pakistan and Yemen.

But we have redefined war to NOT mean things like drone and cruise missile attacks, to NOT mean things like “observer” or “training” missions. We have redefined war to ONLY mean American troops being shot at.

So politicians can speak the words “End the war in Country XYZ!” without actually meaning it. Because what they mean is preventing any American troops from being shot at. But the actual war of drones and missiles and killing … that continues. And it will continue forever in the Long Now.

Words like “capitalism”.

This is a picture of the billionaire CEO of a government-supported too-big-to-fail megabank, telling his 60 Minutes interviewer that he has no control over his compensation, as that’s determined by the CEO’s board of directors. Interestingly enough, this is also a picture of the billionaire Chairman of that board.

And it’s not just the billionaire CEO bank manager. It’s his centimillionaire lieutenant bank managers. It’s the dozens of decamillionaire sub-lieutenant bank managers. All of them made generationally rich from stock-based compensation in a company where the government guarantees their success. None of them entrepreneurs. None of them risk-takers with their own skin in the game. All of them … lifer managers of a too-big-to-fail bank.

But, hey, the stock is up! They’ve done a good job! What’s the problem, Ben?

That’s exactly the problem. The problem is that we have redefined capitalism to mean “the stock is up”. We have redefined capitalism to NOT mean Smith’s invisible hand or Schumpeter’s creative destruction or productivity-enhancing and risk-taking investments in the real economy. We have redefined capitalism to ONLY mean financial asset price inflation in the here and now. By any means necessary. So that’s what we get. From the Fed, from the White House, from corporate management … that’s what we get in the Long Now … an endless series of policies and decisions in service to capitalism-as-financialization, where capital markets are maintained as a political utility.

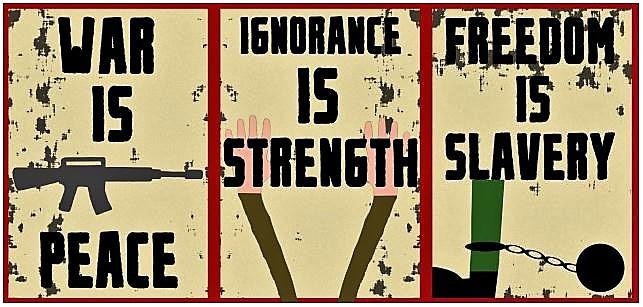

George Orwell, who called the Long Now an “endless present, where the Party is always right”, understood how the most powerful weapon of a totalitarian society is to control its language, so that War IS Peace, Freedom IS Slavery, and Ignorance IS Strength.

Why? Because control over the meaning of words is control over how we THINK. When we no longer remember what words mean, when we are TOLD over and over again a NEW meaning … we start to doubt ourselves. We start to doubt our own autonomy of mind. And that’s when they win.

Iakov Guminer, Arithmetic of an alternative plan (1931)

In the end the Party would announce that two and two made five, and you would have to believe it. It was inevitable that they should make that claim sooner or later: the logic of their position demanded it. Not merely the validity of experience, but the very existence of external reality, was tacitly denied by their philosophy. The heresy of heresies was common sense.

And what was terrifying was not that they would kill you for thinking otherwise, but that they might be right.

— George Orwell, 1984

The Long Now is the Fiat Worldof reality by declaration, where we are TOLD that inflation does not exist, where we are TOLD that wealth inequality and meager productivity and negative savings rates just “happen”, where we are TOLD that we must vote for ridiculous candidates to be a good Republican or a good Democrat, where we are TOLD that we must buy ridiculous securities to be a good investor, and where we are TOLD that we must borrow ridiculous sums to be a good parent or a good citizen.

And the most terrifying thing is that you start to think they might be right.

Hey, maybe the whole Ukraine thing really is Trump “fighting corruption” and maybe the whole Saudi thing really is Trump “bringing the troops home”. Maybe the really important thing about Jeffrey Epstein is whether or not he committed suicide. Maybe we should really try some “democratic socialism” in 2020 … how bad could it be?

Self-doubt is a biologically terrifying condition for a social animal like humans, and that’s why you see more and more of us becoming rhinoceroses. That’s why you see more and more well-meaning citizens willingly give over their autonomy of mind to the MAGA Train or the Bernie Bros … some sort of social Answer with a capital A … so that the torture of self-doubt can end.

That’s why, in the end, Winston loved Big Brother.

And make no mistake, the Answer is always totalitarian. Not merely authoritarian, but totalitarian. It brooks no dissent, in ANY aspect of your life. The Answer is a general closed-form solution, something we are hard-wired to want, but something that is impossible to find in a social system. Yes, this is the Three-Body Problem.

Unfortunately, I believe that the totalitarian Long Now is going to get a lot worse before it gets any better. I believe that we are going to doubt ourselves in new and profound ways over the next decade. I believe that our common sense will become even more the heresy of heresies.

Why?

Because the Long Nowhas redefined the meaning of “taxes”.

Because the tether between taxation and spending – the most important macroeconomic policy relationship for our lives as both investors and citizens – has been severed.

Oh, I know that this snip-of-no-return doesn’t feel bad. Yet. In fact, it probably feels pretty darn good to you right now.

Funny how fallin’ feels like flyin’For a little while

That’s from a song in the movie Crazy Heart, and that’s where we are right now. So yeah, you’re going to be told that 2 + 2 = 5, that it’s no big deal to cut the cord between taxes and spending, that in truth it’s good for you. And yeah, you’re going to start to think that they might be right.

The redefinition of taxation and the severing of the Tether of Meaning between taxes and spending isn’t something that I think WILL happen. This is something that I know HAS happened. We’ve had a steady fraying of this cord for about two decades now, ever since Al Gore’s idea of a Social Security “lockbox” (where those taxes could ONLY be used for Social Security spending and paying down the existing debt) was met with derision rather than acclaim by both parties. Yes, both parties. By steady fraying I mean over both Republican and Democrat administrations. The political beneficiaries of the fraying are different when it’s Republicans doing the snipping or Democrats doing the snipping, but the INTENT – to eliminate the tether between taxation and spending – is the same whether you’re George Bush or Barack Obama. Or Donald Trump. Destroying the relationship between taxation and spending is not a partisan thing. It’s a power thing. It’s a Management thing.

I mean, there are still people who believe that the money they pay in Social Security taxes is their money, that they’ve purchased some sort of old age income insurance plan with their money, like an annuity where their money is invested somewhere to support that income down the road.

But that’s a lie.

In truth there is ZERO relationship between social security taxes and social security benefits today, other than sharing the words “social security”. In truth they are two entirely separate government programs, the former a regressive tax on workers that goes into the big pot of the annual budget and the latter a wealth transfer program to old people that comes out of that budget.

SNIP!

So for twenty years Republicans and Democrats have gone back and forth to steer taxation and spending to their political advantage, with divided government being the only thing to keep the tether intact. But divided government vanished with Donald Trump’s election, and as a result we got the 2017 Tax Cuts and (LOL) Jobs Act, which I think was the final cut.

What did the TCJA do? It lowered taxes by trillions without reducing spending by a dime.

The TCJA levered up the United States of America.

Management levered up our country and used the proceeds to provide a windfall gain for corporations and the rich. You know … “returning capital to job creators”. In exactly the same way that Management might lever up a company and use the proceeds for a big stock buyback. You know … “returning capital to shareholders”.

Both of these narratives – “returning capital to job creators” and “returning capital to shareholders” – had a truth to them, an important truth. I believed in the important truth of both of these narratives for most of my adult life! And yes, I’m using the past tense.

Because in the Long Now, the meaning of both narratives has been perverted beyond all recognition.

Both are now part and parcel of the Trickle-Down Lie, that the crumbs that fall off massa’s table are crumbs that you wouldn’t get otherwise, so let’s celebrate all those extra crumbs. Yay, crumbs!

And yes, there’s an Epsilon Theory note or three for that.

The pecking order is a social system designed to preserve economic inequality: inequality of food for chickens, inequality of wealth for humans. We are trained and told by Team Elite that the pecking order is not a real and brutal thing in the human species, but this is a lie. It is an intentional lie, formed by two powerful Narratives: trickle-down monetary policy and massive student debt financing.

Time to add a fourth shift in the Zeitgeist: capitalist productivity, now 200+ years old, is becoming capitalist financialization. Wall Street gets something to sell, management gets stock-based comp, the Fed gets a (very) grateful Wall Street, and the White House gets re-election.

What do YOU get out of financialization? You get to hold up a card that says “Yay, capitalism!”.

One day we will recognize the defining Zeitgeist of the Obama/Trump years as an unparalleled transfer of wealth to the managerial class.

But if we’re no longer even pretending that taxes are necessary to support spending …

If we agree that neither the Republicans nor the Democrats care about fiscal policy except as it advances their myopic political goals …

Then what are taxes FOR?

Yep, this is our George-Clooney-realizes-he-is-about-to-be-flung-into-outer-space moment.

In the Long Now, taxes are for … justice.

In the Long Now, taxes are for … equity.

In the Long Now, taxes are for … retribution.

And what do those words mean?

Whatever Management says they mean.

Donald Trump has a vision of how to use taxes for HIS conception of justice, equity and retribution, a vision that – well, how about that! – advances his political power.

The primary beneficiaries of the TCJA are large public companies, particularly the multinationals that dominate the S&P 500. For example, in each of the past two years, Amazon has availed itself of the deductions and deferrals and lower corporate rates created by the TCJA to be a “net-negative US Federal cash taxpayer”. In English, that means that in each of the past two years, the US Treasury has written checks of more than $100 million to Amazon out of YOUR tax dollars. I know you think I’m making this up, but check out Amazon’s 10-K. It’s all there.

And before you @ me, I am NOT saying that Amazon doesn’t pay taxes. What I am saying is that I really don’t care how much Amazon pays in taxes to freakin’ Ireland. What I am saying is that Amazon is cashing checks from the US government instead of writing checks. As the kids would say, let that sink in.

How does this advance Trump’s political power? Because the windfall tax benefits that the TCJA created for large public companies like Amazon and Apple and Microsoft translate directly into higher stock prices. Because in Trump’s own words, “the stock market is my report card”. Because Trump realizes that you can politically argue to death whether the real economy is doing better or worse, but you can’t argue with a new high for the Dow Jones.

What does it mean to transform capital markets into a political utility, and use the tax code to do it?

This.

Similarly, Bernie Sanders and Elizabeth Warren and No Malarkey Joe and Mayor Pete and all the rest have a vision of how to use taxes for THEIR conception of justice, equity and retribution, a vision that – well, how about that! – advances their political power.

None of the “wealth tax” proposals you hear from the Left are being proposed to pay for anything in a budgetary sense. They are explicitly proposed so that the rich pay their “fair share”. In fact, when candidates make the mistake of expressing their wealth tax idea in a fiscal sense – as Elizabeth Warren did when she linked it to “paying for” Medicare-for-all – the narrative immediately shifts from “fairness” to “making the numbers add up” (Spoiler Alert: they don’t and they never will), and these candidates immediately take a hit in the polls.

Bernie gets it. He doesn’t even pretend to make this about budgets. He realizes that the political popularity of the wealth tax has nothing to do with making the rich pay for a government program, and everything to do with making the rich pay for theirsins. And yes, Bernie believes that great wealth is a sin. He believes that great wealth should not be allowed, not because it’s a source of unaccountable political power (my beef with great wealth), but because he believes it is fundamentally unfair. So do a lot of voters, maybe more than care about the Dow Jones.

SNIP!

Feeling out of control yet? Wait, there’s more!

If the meaning of spending is no longer constrained by taxation …

Then what is spending FOR?

In the Long Now, spending is ALSO for justice and equity and retribution … ALSO in whatever mode or measure fits the regime goals of whatever Management is in power at the time.

I think that whoever is elected in 2020, we will see a $2 trillion spending plan enacted in 2021.

If it’s a second term for Trump, it will be the 2021 Make America Great Again Act, and we will call them “Infrastructure Bonds”.

If it’s a first term for a Democrat, it will be the 2021 Take Back America Act or something like that (I suppose if it’s President Biden we can hope for the 2021 No Malarkey Act, although I’m rooting for the 2021 OK, Boomer Act), and we will call them “Green Bonds”.

In either case, I expect that the Fed will monetize at least half of the bond issuance. At least half.

In either case, I expect that the primary corporate beneficiaries of the spending will be exactly the same. Exactly the same.

And so here we are.

I believe there are no limits to the retributive and malicious use of taxation as a political weapon.

I believe there are no limits to the retributive and malicious use of spending as a political reward.

Sometimes those political weapons and rewards will be used by the rich and the old against the non-rich and the non-old, as we saw with the TJCA and Trump. Sometimes it will the other way around, as we will see the day after a Democrat takes the White House, whenever that might be.

What’s to be done? Well, I suppose this is the point where I should tell you what I would do if I were given magic genie powers to change the world from the top down. And then you’d argue with me about my proposals and tell me what you would do if given magic genie powers.

How about we not do that? I don’t have magic genie powers. And neither do you.

It’s not that the severing of taxes from spending WILL happen. It’s not that the NEXT administration is going to make the cut. It’s ALREADY happened. It’s been happening for twenty years! This ship has sailed, and now there’s not a damn thing that you or I can do to turn it around. All we can do now is survive the voyage.

When I started this note, I said I wanted to instill an emotion of fear and loathing in you from the realization that the meaning of taxes had become untethered from the meaning of government spending. That phrase – fear and loathing – is of course a catchphrase for Hunter S. Thompson, who used it in the titles of his best-known works … Fear and Loathing in Las Vegas, Fear and Loathing on the Campaign Trail, etc. Thompson had lots of catchphrases, lots of mottos, lots of great quotes. My all-time favorite, though, is this:

When the going gets weird, the weird turn pro.

I love it because there are so many plausible interpretations, and it just sounds so cool to take a tired inspirational quote about what to do when the going gets tough, blah blah blah … and turn it on its ear. Or foot, or whatever body part you think Thompson would have approved. Here’s what it means to ME.

“The going gets weird” = an economic and political environment that no one alive has experienced.

I think that the smiley-face totalitarian genie (and yes, I wrote ‘totalitarian’, not ‘authoritarian’) is going to be let out of the bottle as the meaning of taxes becomes justice, equity and retribution.

I think that the not-so-smiley-face inflation genie is going to be let out of the bottle as the meaning of spending in the real economy becomes untethered from any concern of paying for it.

To paraphrase Richard Nixon paraphrasing Milton Friedman, we’re all MMTers now. “Modern Monetary Theory” is here, firmly ensconced in BOTH political parties in the Long Now

If Trump is reelected in 2020, I think he pushes forward a $2 TRILLION bond issuance that is fully or partially monetized by the Fed. They’ll be called Infrastructure Bonds. If a Democrat is elected in 2020, I think she or he pushes forward a $2 TRILLION bond issuance that is fully or partially monetized by the Fed. They’ll be called Green Bonds. We’re all MMT’ers now.

Modern Monetary Theory is neither modern nor a theory. It’s a post hoc rationalization of politically expedient policy that makes us feel better about all the bad stuff we’ve done with money and debt in service to Team Elite. And all the bad stuff we’re going to do in the future.

A recession isn’t weird. Deflation isn’t weird. Authoritarian isn’t weird. I don’t think ANY of those things is coming down the pike, and you don’t need my help (or anyone else’s) if any of them does.

But smiley-face totalitarian stagflation where capital markets have been transformed into a propped-up-at-all-costs political utility?

Now THAT’S weird. And that’s what I think IS coming down the pike. And we’re all going to need all the help we can get. Which gets us to the second half of Hunter S. Thompson’s quote.

“The weird turn pro” = an all-in engagement for those who see the societal transformation; a recognition that the fundamental rules of the social game have changed, and a willingness to confront the implications of that change in every aspect of your life without surrendering to an Answer.

How do we confront the Long Now?

Personal courage

Leaders who act as stewards of the future, not managers of the Now.

Professional courage

Investors who take more risk with what’s Real, and less with what’s not.

Social courage

Citizens who take back their vote, and who refuse to play the Fool.

You know, in one of my twitter fights with Angry-Billionaires-and-their-Renfields™, I was called “a bizarre combo of Zerohedge and self-help guru”. It was meant as an insult, of course, but for me … man, I wear it like a badge. Because I DO believe, in Zerohedge-esque fashion, that “the system” is designed by and for a Team Elite that, in the immortal words of The Outlaw Josey Wales, pisses down our backs and tells us it’s raining. And I DO believe, in self-help guru-esque fashion, that the only effective resistance to the Nudging State and the Nudging Oligarchy is through a bottom-up grassroots social movement that is driven by one thing and one thing only: each individual’s courage and determination to maintain their autonomy of mind … the courage and determination to believe that 2 + 2 = 4.

The revolution will not be televised. The revolution will not be in the streets.

The revolution will be in our hearts.

It’s the hardest thing you’ll ever do, precisely because no one will be watching.

But you won’t be alone.

In 2020, we’re going to host an international conference to come together on this, an Epsilon Theory Forum. It’s intended to be the anti-Davos … a meet-up for those who still have a soul, who care about something bigger than the celebration and perpetuation of Team Elite. And I can promise you this … there won’t be a single billionaire on a panel at the ET Forum. But there will be plenty of real people … people with ideas and experiences that aren’t contingent on how many zeros they have after their name.

Clear eyes, full hearts, can’t lose.

Make / Protect / Teach.

As wise as serpents, and as harmless as doves.

We’ve got a lot of slogans. In 2020 you’ll have a chance to take action. You’ll have a chance to talk this through with like-minded truth-seekers, to figure out TOGETHER what a bottom-up grassroots social movement devoted to preserving each and every one of our autonomies of mind can do. It may be too late to prevent the SNIP! that severs the tether between taxation and spending, but it is high time to create new tethers, new personal bonds of association, loyalty and mutual support. Yep, it’s a Pack. And that’s how we survive the Long Now. Together.

Bipartisan Group Of NYC Lawmakers Pushing For “Gentrification Tax”

It’s almost as if New York politicians are deliberately trying to crash NYC’s housing market.

On Christmas Day, the New York Post reported that a bipartisan group of NYC lawmakers is pushing Albany to change state laws and close a loophole that extends tax breaks to homebuyers in gentrifying neighborhoods.

The “gentrification tax” law would require homebuyers to pay taxes at the market rate, rather than at the much-lower assessed value.

Presently, homebuyers across the five boroughs who buy multimillion dollar brownstones and other existing homes often pay less in taxes than those who buy more moderately priced homes.

Republican Staten Island City Council member Joe Borelli is spearheading the movement to end the tax loophole. He told the Post that New Yorkers are “just getting fed up” with the unfair treatment.

“My proposal would end the practice of charging more tax on $500k home on Staten Isl etc. than a $2m home in Park Slope,” Borelli tweeted on Thursday. “This can be done Jan. 1.”

Borelli also blamed Mayor de Blasio for creating the ‘yuppie tax’ loophole.

The Post calls it a gentrification tax or a ‘yuppie tax,’ but most NYers know it as the ‘de Blasio loophole.’

My proposal would end the practice of charging more tax on a $500k home on Staten Isl etc. than a $2m home in Park Slope. This can be done jan 1. https://t.co/SDCB4zFjLp

Borelli’s coalition also includes Park Slope Democrat Brad Lander and Bay Ridge Democrat Justin Brannan, two other members of the city council, which is controlled by Democrats.

The NY Post breaks down the impact of the gentrification tax thusly: A buyer who snapped up a Clinton Hill brownstone for $3 million in 2017 only pays taxes on a fraction of the buying price, leaving the building’s new owner with a tax bill of just $4,297 a year.

Joe Borelli

Meanwhile, the owner of a $500,000 Bergen Beach bungalow pays a nearly identical amount, even though the bungalow is worth roughly one-sixth of the brownstone.

The change to opaque state tax laws advocated by Borelli would raise the brownstone owner’s annual tax bill by $1,600, while the owner of the bungalow would see no increase.

Of course, the changes would come with drawbacks: Back in April, New York State passed a revised ‘mansion tax’. First passed in 1989 by New York Gov. Mario Cuomo, New York’s original mansion tax was a 1% tax on statewide sales of homes of $1 million or more. Under the original tax, if a house, co-op, or condo sold for $1.25 million, the buyer would have paid a tax of $12,500, in addition to whatever other taxes they would pay.

For fiscal year 2020, the statewide mansion tax will remain at 1% for property purchased for $1 million or more. For properties in NYC, however, the ‘progressive’ mansion tax will rise incrementally with purchase prices of $2 million or more, capping out at a total of 3.9% for properties sold at $25 million or above. Homes sold for $1 million+ outside of NYC but within New York state won’t be affected by the progressive taxes.

Homebuyers in New York state (including NYC) will also need to factor in the Republican tax plan’s rejection of the SALT deductions.

Borelli sent the proposed resolution to City Council Speaker Corey Johnson and state Assembly Speaker Carl Heastie earlier this month. Johnson spokeswoman Jennifer Fermino said the speaker is waiting for a preliminary report from a city property tax reform commission that he and Mayor de Blasio commissioned back in 2018.

With the new mansion tax, it’s hardly surprising that Manhattan home sales plunged in Q3. Will we see more housing market pain in Q4 and the new year? Investors don’t need a magic 8-ball to figure that one out.

There is evidence that US Treasury bond yields may continue to rise, exposing the debt trap in which the US government finds itself. Market participants don’t realise it yet, but the dollar-based monetary system is spinning out of control. This will become obvious as the crisis stage of the credit cycle, which we now appear to be entering, becomes evident.

The outlook for monetary inflation is dire. Not only will governments fund themselves through QE, but central banks will be forced to inflate even more to pay for government deficits significantly greater than currently forecast. And when markets stop taking government statistics on inflation as the Gospel Truth, the interest cost of government funding will rise and rise, reflecting an increasing rate of time preference for fiat currencies which will be losing their purchasing power at an accelerating rate.

In a world where all fiat currencies will face enormous challenges, using yardsticks such as trade weighted indices will be misleading. The best gauges of the slide in fiat currencies will be commodities, particularly commodity monies, gold and silver.

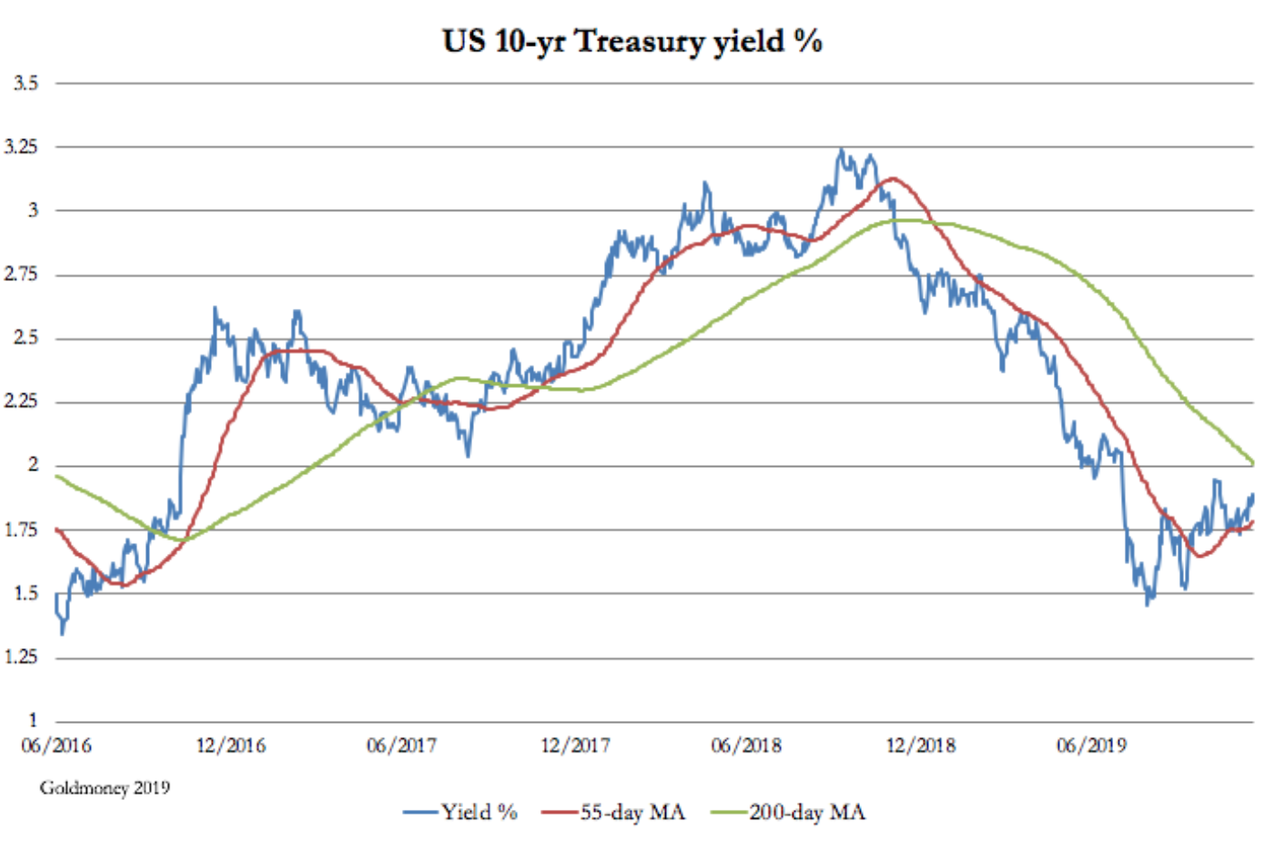

Introduction

The chart above, of the US 10-year Treasury yield is shows that its yield bottomed at the end of August, when it had more than halved from the levels of October 2018. What, if anything, does it mean? Some would argue that it is good to see a positive yield curve again, implying the recession, or the risk of one, has gone away. But if US Treasury yields have bottomed out, then in the fullness of time they will continue to rise. Chartists might even claim it is setting up for a bullish golden cross, like the one earlier in the chart on 17 November 2016, which marked the beginning of a significant rise in bond yields.

That would be a worry, since equity markets have flown to places where bond yields don’t exist. But there are more solid concerns about the course of bond yields, other than charting ephemera. Despite the massive expansion of money and credit since the Lehman crisis, there is a shortage of liquidity, because the Fed is having to inject half a trillion dollars into the banking system to keep overnight levels suppressed at the Fed Funds Rate target.

Informed opinion suggests that there is indeed a liquidity crisis. The banking system in New York has become strained through banks loaded with US Government debt and providing repos to hedge funds who have shorted euros and yen to buy T-bills and short-dated government coupon debt. The shortage has occurred because the largest banks, designated globally systemically important banks (GSIBs) must demonstrate excess reserves to cover obligations thirty days out. The strains for this Basel III requirement are expected to increase at the next quarter-end, i.e. 31 December.

These strains first became evident in the repo market, which blew up three months ago, on the day Deutsche Bank completed the sale of its prime brokerage to BNP. We don’t know if these events were related, but as any investigating detective will tell you, pure coincidence must be dismissed until proven otherwise. In any event, the problems in the repo market have continued, so having noted that perhaps the Deutsche Bank sale did not go as planned, we must go with the GSIB excess reserves explanation.

Looked at in this light, the persistent rise in UST bond yields is threatening. Unless the Fed simply floods the markets with liquidity, they seem set to rise further. If the Fed does not, the GSIBs have two courses of action, and they may be forced to take both. First, they could be forced to sell down their US Treasuries in order to create intraday liquidity needs by releasing some of their required reserves to be categorised as excess. Second, they can refuse to roll hedge fund repos, forcing hedge funds to sell US Treasuries and T-bills and then sell their dollars to close their shorts in euros and yen. The withdrawal of liquidity could wipe out one or more major relative value (RV) funds, invoking the ghost of Long-Term Capital Management, which ran into trouble in 1998.

All this is now known, so it would be surprising if the Fed fails to act to contain a year-end crisis. But its actions are limited to providing liquidity for the banks. It will be up to the banks if they decide to use that liquidity to continue to accommodate the RV funds.

Foreign buyers hold the dollar key

Let us assume for a moment that we get through the year end without mishap. We will not have dealt with the underlying problem, which is who is going to buy the $1–1½ trillion of US government debt to be issued in 2020. In the past it has been principally foreigners, banks and RV hedge funds as described above. On a net basis the US saver has not been involved for a very long time, except passively through managed pension funds.

According to US Treasury TIC data, in the year to October major foreign holders added $580.5bn to their holdings of Treasury bills, T-Bonds and Notes. The balance will have come directly and indirectly from domestic credit expansion, including the banks and the RV hedge funds. But from August, foreign investors have been net sellers to the tune of $77.4bn. Until then, every successive month had seen an increase, so it appears foreign demand is stalling, which could have fed into the repo crisis as the GSIB banks in New York and RV funds ended up with too much US Government paper.

Foreign dollar demand is almost certainly affected by the sharp slowdown in global trade. This has happened for two reasons: President Trump’s tariff war against China and others has stalled international trade and at the same time, having been expanding for the last nine years, the credit cycle is due to run out of steam. Together they are recessionary headwinds, probably synergistic, which reduce the level of dollars in in the correspondent banking system foreigners need to hold for liquidity.

China is the second largest holder of US government paper and has been reducing her position in recent months. As to her future reserve policies, commercial considerations are being complicated by politics. She understands that America is desperate for global investment flows to finance US Government debt, and that China’s infrastructure plans would compete for them which explains America’s hidden agenda over Hong Kong. China bungled her management of that situation, and apparently is now exploring the use of Macau as an investment channel for foreign inward investment.

It is probably too late, the damage to investing in China having been done. But it is hard to see why China should just roll over on this issue and continue to buy US government bonds. More likely US Government debt will now be viewed as a source of funds to replace lost inward investment through Hong Kong.

We can now see a best and worst case for the dollar and US Treasury funding. The best case is stagnating demand from abroad, which throws the onus onto domestic investment, which, in the absence of an increase in savers, will be through QE and the inflation of bank credit.

The worst case will see not only stagnant foreign demand, but active selling down of current positions, due to slumping economies and China in particular selling actively. American investors seem generally complacent about this possibility, arguing that foreigners will always need dollars, and more so in a credit crisis. While there is some force in this argument, it ignores the fact that foreign ownership of dollars and dollar investment is already very high at roughly $23 trillion of which over $4 trillion is in deposit accounts, while US ownership of foreign currency liquidity is a relatively trivial figure.

Bearing all this in mind, we must assume that at a minimum US banks and hedge funds between them will be funding all the budget deficit and may even have to absorb existing stock from foreigners. But surely, one imagines a critic asking, in the absence of a change in the savings ratio, a budget deficit is a matter of an accounting identity and will give rise to a similarly sized balance of payments deficit, and so long as dollars accumulate in foreign hands, they must form the capital inflows that finance the budget deficit. Therefore, dollars will continue to accumulate in foreign hands, and they must be invested.

The accounting identity argument is correct, but there is more than one way to skin a rabbit. Dollars received by foreigners can always be sold in the foreign exchanges instead of being reinvested, which given the relative lack of foreign currency liquidity in the hands of domestic Americans, could have a dramatic effect on the exchange rates.

Alternatively, the gap can be closed by the inflation of money through quantitative easing and the expansion of bank credit. In effect, the existing stock of dollar deposits is diluted to bridge the shortfall between a budget deficit and the lack of inward capital flows recorded in the balance of payments.

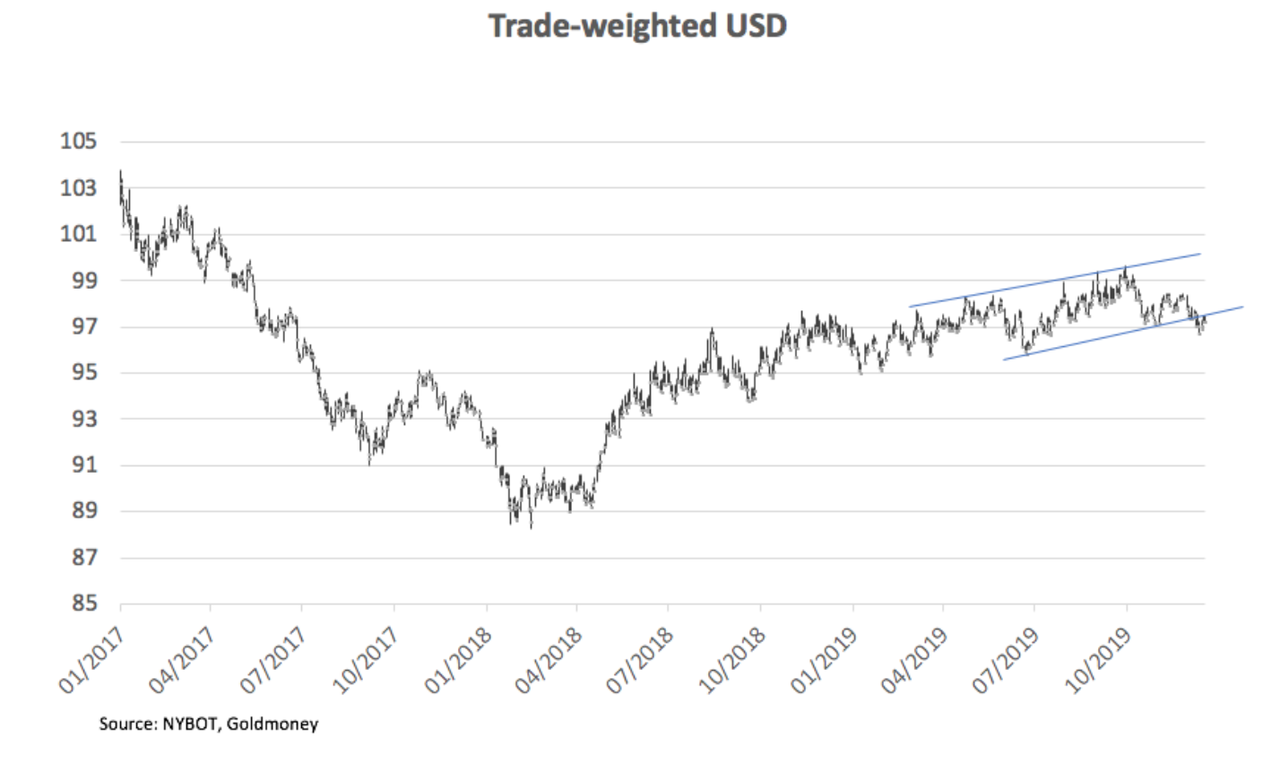

In this context, the chart below of the dollar’s trade-weighted index appears to show the dollar is struggling to advance and may be losing the bullish momentum that developed shortly after President Trump was elected.

If, as the chart suggests, the dollar could be heading lower, it would fit in with a diminution of foreign capital inflows. But the major component of this index is the euro, so it is not an accurate representation of the dollar’s weighting with respect to trade imbalances, which are the normal source of capital flows. But in the case of the euro, it has already been sold down by RV hedge funds to strip out the interest differential by selling euros short and buying dollars. According to Hedgeweek.com, six months ago this form of hedge fund arbitrage stood at $865.6bn, a truly significant sum, most of which will have accumulated since 2018 Q1, when the dollar’s bull phase commenced.

Not all of it would have involved selling down the euro, because in the past the Japanese yen has been the short leg of choice in an interest rate arbitrage. It is clear that the repo crisis tells us that by financing this speculation the US GSIBs have expanded their balance sheets too much and will need a substantial increase in their excess reserves to continue to finance this trade, thereby avoiding a crash in both the US bond market and the dollar. While this problem has surfaced at this year-end, it will be a continuing problem thereafter.

This brings us back to our first chart, of the 10-year T-bond yield. The reasons why it may have bottomed and will rise further are becoming clear. If a rising bond yield is accompanied by a falling dollar it will be because markets recognise an acute funding crisis is upon the US government, reminiscent of the 1970s in sterling markets.

A falling dollar will be the signal, so we must watch the trade-weighted index and, more importantly, the gold price.

The gold price particularly acts as the canary in a coal mine, and in that context Comex open interest is hitting record levels, which without the price rising indicates a suppression operation is already in place. It is therefore reasonable to suggest the combination of the lack of excess reserves in the GSIBs and the suppression of gold is circumstantial evidence that a financial crisis is already on its way.

Markets will take control from central banks

When the funding difficulties of the US Government become more obvious, investment strategists are bound to rethink the course of interest rates in other fiat currencies, which face similar pressures from increasing budget deficits. Being aware that monetary policies are not working as intended, central banks have already encouraged their governments to deploy additional fiscal stimulus. Even before welfare costs rise and tax income falls due to a developing global recession, it appears that government borrowing world-wide is set to accelerate.

With the credit cycle on the turn, one thing is for sure, and that is what central banks call the business cycle will follow. The mistake made by all mainstream commentators and economists is to not appreciate that the problem is one of the central banks’ own making, and that once the credit cycle is set in motion it cannot be simply stopped by reducing official interest rates. We saw this proved ten years ago, when the Fed and other central banks had to inflate the quantity of money by however much base money was required and by taking failing institutions into public ownership. In the UK the only significant bank which successfully resisted needing a government bail-out was Barclays, and executive directors at the time are still having to answer for their actions in the courts. It seems that not only is failure rewarded, but a major bank not failing has become a criminal act.

The fact that some central banks have unsuccessfully imposed negative rates has not yet led to a realisation that attempting to control the cycle in this way simply does not work. The periodic credit and systemic crises are increasingly destabilising and the dynamics behind the next one indicate it will be on a scale significantly greater than the Lehman crisis eleven years ago. The banking scene is set for a reversion from incautious greed to abject fear, fear of lending to anyone and to any other bank. And the weakest banks are to be found in the Eurozone. Even in the EU’s strongest economy, the two largest private banks, Deutsche Bank and Commerzbank, by their share prices are signalling a slidetowards bankruptcy.

At some stage, and it could only be a matter of weeks or even days, the global outlook will cause all GSIB banks to become considerably more cautious, withdrawing lending facilities from smaller banks, financial speculators (hedge funds), and businesses alike. Lending to the last category ceases in two ways. In capital markets banks begin to cut their high levels of exposure to sub-investment grade bonds and syndications, and they withdraw working capital facilities for medium and small businesses. The crisis phase of the credit cycle is then irreversible.

The credit-induced recession will be proportional to the scale of the preceding credit expansion. It feeds through to an escalation of government borrowing in all welfare-dependent nations, because of the fall in tax receipts and the increase in welfare costs.

If US bond yields rise, they will do so either because foreigners are selling the dollar, or because domestic prices, reflecting a fall in the dollar’s purchasing power, begin to rise at a faster pace. It is already an open secret that official price inflation figures bear no relation to reality and only financial markets are wedded to the CPI myth. In fact, not only are government statistics inaccurate, but all statistics are reported in funny money. When US dollar markets wake up, the same will be true of markets in other currencies, and the greater the level of interest rate distortion the more severe the crisis is likely to be.

How it plays out in different nations and their currencies is not so much down to the scale of government borrowing in deteriorating circumstances, but whether savers respond to the financing demands of their governments. For this reason, monetary inflation rates will be offset by a tendency for Japanese and Chinese savers to increase their bank deposits rather than spend. In the Eurozone and Britain, this is less the case. Increasing monetary inflation will end up fuelling rising eurobond and sterling bond yields more rapidly than their equivalents in Japan and probably China.

Commodities and commodity money

The point has been already made in this article that measuring the dynamics behind a credit crisis is distorted by government statistics not fit for the purpose and by the elastic nature of fiat currency. Furthermore, monetary planners, portfolio managers and the commentariat inhabit a Keynesian fantasy land and only understand rising prices to be directly related to increased demand, and falling prices to falling demand. Presumably, this explains why they associate a CPI rising at two per cent with a healthy economy.

The key to understanding the error is that money is only objective in its value for the purpose of individual transactions. But give money a temporal context and it becomes clear that money’s purchasing power varies as well as the cost of anything.

If it is expected that the rate at which a currency loses purchasing power is about to increase, then commodity prices measured in that currency will rise without any improvement in demand. Demand can even fall, and prices rise, if the purchasing power of the currency declines sufficiently. This condition can be temporarily overcome by an investors’ panic when they sell assets, such as bonds and equities, in order to escape falling prices, but once that initial effect has quickly worn off, the relationship between money and goods will adjust to the public’s general desire to hold money as opposed to goods.

We have a contemporary example. At the time of the Lehman crisis the price of gold declined from $1,000 in March 2008 to $700 the following October, before rising to $1,920 three years later. But this time is likely to be different, because the rate of monetary inflation before the Lehman crisis varied little in the preceding few years, compared with subsequently. Following Lehman, all major central banks expanded money quantities very rapidly, so the next crisis comes against a background of already inflated currencies before a further acceleration in supply. Depending how the next credit crisis evolves, there may not be a dip in the gold price at all.

Instead, gold and other commodity prices, precious or otherwise, will be bought and sold against a background of rapidly debasing currencies. We know this, because renewed monetary expansion in the form of quantitative easing is taking place even before any crisis materialises. And when we hear luminaries such as Christine Lagarde at the ECB talking about QE to finance eco-friendly infrastructure developments directly, we know that central bankers and their governments now view monetary inflation much as it was in the Weimar Republic: an infinite source of funds.

Despite attempts by the bullion banks to suppress the evidence from the gold price of what is likely to turn out to be the early stages of a widespread fiat currency collapse, if matters progress on the lines described in this article, gold, silver and other commodities will rise priced in fiat. Initially it is likely to reflect the fact that such assets are under-owned. But then another effect is likely to take over, as the public begins to realise what is going on and start dumping fiat currencies for gold, silver and even bitcoin.

Ninety years ago, it was called a crack-up boom, the last dash out of currency for anything not printed by the government. It will happen differently this time, because it always does. But now that inflationary financing is not only required to balance governments’ books but to finance the expansion of their spending, happen it will.

Last year, 125 people got together to participate in trying to figure out new insights about the game from poring over mountains of NFL data. This year, 2,038 teams made 32,000 submissions to the event, according to the Wall Street Journal.

And like baseball, which caught analytics fever some years back around the time that Moneyball was released, the NFL now seems set for its own analytics boom.

The numbers are already starting to shift the game, too. More teams are going for it on fourth down and teams are throwing more out of the shotgun, among other decisions being dictated by “rudimentary math”.

At the same time, some GM’s still mock “eggheads and their spreadsheets”, leading to a bit of friendly competition between those who rely on analytics and those who don’t.

To some degree, it seems like a foregone conclusion: this is already the third year that the NFL is using its Next Gen Stats, which collects “granular data about movements on the field that is enabling analyses that were never before possible.”

And because data research is so new, there’s still many inefficiencies that can be taken advantage of when discovered by quants.

Momin Ghaffar, manager of strategic research and development for the Jacksonville Jaguars said: “There’s a lot of low-hanging fruit to be had.”

Ghaffar’s career path has followed the trend: first as manager of analytics for the San Antonio Spurs before defecting to the Jaguars after submitting a paper on analytics to the team.

At last year’s competition, he was one of 11 people hired by NFL teams or other companies looking for analysts.

Prior to Next Gen stats, each game had about 160 rows of data, with each representing one play. Now, tracking data makes 10 observations per second, per player. So instead of 160 rows, there’s about 600,000.

Lopez said: “There’s some knowledge in those 600,000 rows. And teams are trying to figure that out.”

Charlie Gelman, whose work at last year’s Big Data Bowl landed him with a job with the Ravens said: “That’s why I wanted to get into football originally, much more than any other sport. Right now, there’s a huge rush of people trying to get in.”

He was only a sophomore at Duke when he submitted his paper. He also started doing analytics for Duke’s wrestling team and football team.

“Football is huge, but there’s still so few analytics in it,” he said.

The Philadelphia Eagles have the league’s most progressive front office when it comes to analytics, and it helped lead the team to a Super Bowl two years ago against the Patriots. This year, the Ravens have been the most effective with going for it on fourth down, a key centerpiece in the Eagles’ aggressive Super Bowl strategy.

There’s no doubt about it: tracking data can exponentially expand insights for teams. For this year’s “Big Data Bowl”, participants are asked to calculate how many yards a running back should get on any given play. Participants had to create models based on complex factors like position of all players on the field, their speed and other attributes.

Nate Sterken, who previously worked in data science for the federal government and President Obama’s reelection campaign in 2012, is now working on models on how to identify every route a receiver ran on every play so he could analyze which combinations worked best together. And come 2020, he’ll be working for the Cleveland Browns.

Christian Post Politics Editor Napp Nazworth said he resigned from the publication after it published an editorial in defense of President Donald Trump.

Christian Post editor Napp Nazworth resigned after the publication of a pro-Trump editorial. He says aligning with President Trump would “destroy the reputation of The Christian Post… We’d reached an impasse. I really had no other choice but to leave.” https://t.co/SQkrAE1jKFpic.twitter.com/qzPIVVXUQJ

In an interview with CNN Thursday, Nazworth said his issue was with the Post ‘aligning with the interests of President Trump.’ That was the straw that broke the camel’s back for Nazworth.

Nazworth resigned on Monday. He announced his decision in a Twitter thread.

“Announcement: Today, rather abruptly, I was forced to make the difficult choice to leave The Christian Post. They decided to publish an editorial that positions them on Team Trump. I can’t be an editor for a publication with that editorial voice….” Nazworth wrote.

I’m saddened by what happened for many reasons. I’ve been with CP for over 8.5 years, made many friendships, and had lots of exciting opportunities along the way. …

When the editors had disagreements, we would work through them, letting those discussions and debates inform and improve our coverage. Now, CP has chosen to go in a different direction. Like so many other media companies, they’ve chosen to silo themselves. …

… it’s bad for Democracy, and bad for the Gospel. It means there will be one more place where readers can go for bias confirmation, but one less place where readers can go to exercise their brains on diversity of thought. {end}

The controversy began when the former Editor-in-Chief of Christianity Today Mark Galli penned an op-ed arguing for President Trump’s removal from office as the U.S. House of Representatives deliberated and later voted to impeach him.

“The president of the United States attempted to use his political power to coerce a foreign leader to harass and discredit one of the president’s political opponents. That is not only a violation of the Constitution; more importantly, it is profoundly immoral,” Galli wrote.

Galli further argued that the President’s removal is consistent with evangelical teachings and principles.

“That he should be removed, we believe, is not a matter of partisan loyalties but loyalty to the Creator of the Ten Commandments.”

The Christian Post later responded with a scathing piece titled “Christianity Today and the problem with ‘Christian elitism.’” Those elites included Galli, as the piece notes.

“Mr. Galli asks evangelicals supporting Trump to consider how continued support for the president will impede and compromise evangelical witness for Jesus to an unbelieving world. One might well ask Mr. Galli how his obvious elitist disdain and corrosive condescension for fellow Christians with whom he disagrees, as ignorant, uneducated, “aliens in our midst” might well damage evangelical witness to an unbelieving world. Unbelievers might well conclude, “These Christian preach love for neighbor, but they certainly don’t seem to practice what they preach!”” editors John Grano and Richard Land wrote.

That defense of President Trump was enough for Nazworth.

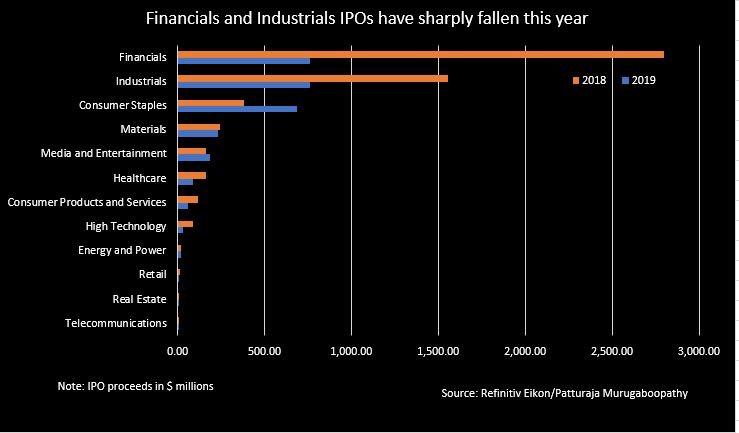

Indian IPOs Plunge To Four-Year Low Amid “Great Slowdown”

Several months ago, we reported how the global IPO market went bust in 2019. Now a new report via Reuters provides more insight into the trend, more specifically, taking a look at the IPO bust in India.

Indian IPOs plunged to a four year low by value in 2019 as the global and domestic economy continues to slow.

Refinitiv data shows funds raised by Indian IPOs fell to $2.8 billion this year, the lowest since about 2016. IPO proceeds soared in 2017 to $11.7 billion and $5.5 billion in 2018 during a synchronized recovery across the world.

Financial, industrial, and consumer staple sectors led IPOs in 2018 and 2019, but the amount raised compared to last year is significantly less.

With a synchronized downturn across the world and an Indian economy in crisis, investors have been pulling back on speculative IPOs:

“2019 has been the worst year from an IPO market perspective,” said Sandip Khetan, a partner at consultancy EY.

“Because of different types of disruptions, such as corporate failures and bankruptcies, things have slowed down considerably,” he said.

Over the weekend, Arvind Subramanian, the former chief economic adviser to the Narendra Modi government, told NDTV that “this is not an ordinary slowdown… it is India’s great slowdown.”

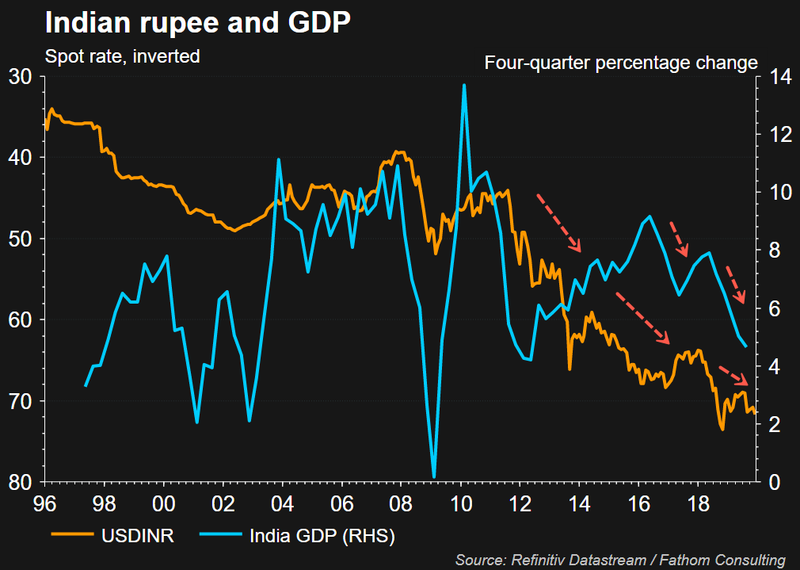

India’s GDP has fallen for seven consecutive quarters, dropping to 4.5% in 2Q19; it stood at 8% in 1Q18.

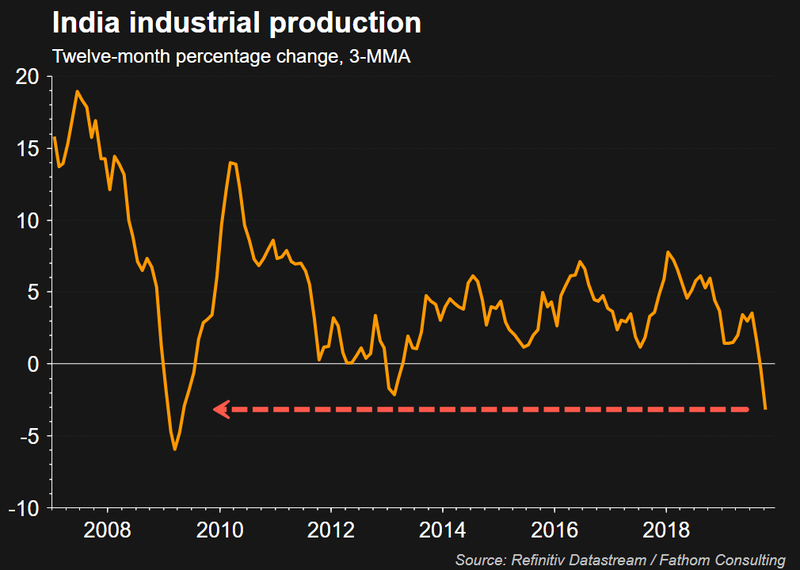

Industrial production growth is at the weakest level in a decade.

Business confidence has also plunged to decade lows.

“…they (key indicators) are either in negative growth or barely positive growth territory… the comparison is to the real sector of the economy… growth, investment, export, and import… which matter for jobs. It is also a matter of how much revenue the government has to spend on social programs,” Subramanian said during the interview, adding, “The real sector economy is slowing… jobs, you know, people’s incomes, people’s wages and of course government revenues”.

Indian investors are ditching speculative IPOs as the global and domestic economy continues to falter. So far, there are no “green shoots” in India — likely continued deceleration into early 2020.

“We’re Heading For Very, Very Bad Places”: Dave Collum’s ‘Pandemonium’ Podcast

The only thing nearly as enlightening (and time-consuming) as reading David Collum’s epic Year In Review is listening to him and Chris Martenson discuss its highlights. So strap in, grab some eggnog, and listen to this year’s recap:

We are so close to a financial crisis now that we may be way, way past the fail-safe.

We’ve got all these unfunded liabilities that we have to pay or face the consequences of — and they are fantastically enormous.

The pensions are all underfunded — at the top of a financial asset price bubble, mind you.

Social Security is a disaster. And we’re promising so much medical help for everyone that is now profoundly expensive.

There are so many things out there that are unmoored. The Fed is unmoored. The digital world is taking us to this digital gulag, in my opinion — I don’t think I’m being hyperbolic.

I think we’re heading for very, very bad places.

Click the play button below to listen to Chris’ interview with David Collum (84m:24s).

China Turns To Shocking Solution To Curb Pig Ebola

China is the world’s top producer and consumer of pork. So when 50% of its pig herd was wiped out in 2019 from African Swine Fever (ASF), it caused pork prices in the back half of the year to hyperinflate. The immediate response by the government was to consolidate pig farms and release pork from its strategic reserves. Other measures included sourcing pork from South American countries, like Brazil and Argentina, along with reestablishing trade with the US in the last several weeks.

Now the Chinese government is working to limit the spread of ASF through a high-voltage electricity experiment installed in pig barns, reported South China Morning Post (SCMP).

The new device will be installed at a medium-sized hog farm in Chengdu, in one of China’s top pig producing regions.

The goal of the test is to see whether an electric field around a barn can limit the transmission of deadly viruses.

Professor Liu Binjiang, a government scientist in northeastern China, is responsible for the “electro culture” program that has already been a huge success for increasing crop yields and reducing plant viruses.

Binjiang and his team are creating a static electric field of 50 kilovolts around a barn that holds thousands of pigs.

He believes the high-voltage discharges will break down chemicals, reduce biological aerosol by 50-90%, kill germs, and stop the spread of viruses that are transmitted through the air.

“The air quality [for the pigs] should improve when the device is powered up,” Binjiang said. “Electricity is one of the many ways to improve living conditions for farm animals. We have a long to-do list.”

Binjiang claims that high-voltage electricity was used to create an electric field around a barn in the Hubei province, one of the hardest-hit ASF areas; he claims that none of the pigs died from the virus.

“It had been deployed to enhance animal welfare and prevent airborne diseases such as foot and mouth, but the lack of African swine fever cases was a surprise. It led the team to hypothesize that the electric field had caused a change in the environment that prevented the virus thriving,” SCMP noted.

Electrifying pig farms to create force fields that scrub the air of deadly viruses could be the next big breakthrough China needs to restrict the spread of ASF.