McDonalds Tumbles After Missing Earnings, US Comps; Drags Dow In The Red

On one of the busiest days in Q3 earnings season, following some impressive earnings from P&G, Biogen, UTX and UPS, moments ago the Dow Jones was dragged lower as heavyweight component McDonalds reported earnings that missed on the top and bottom line, while US comp sales disappointed lofty expectations.

For Q2, McDonalds reported non-GAAP EPS of $2.11, down 2% from 2.16 a year ago, and also below the $2.21 consensus estimate. Revenue also missed, with the company reporting $5.431BN in Q2 sales, below the $5.49BN expected, while operating income of $2.41 billion, declined 0.3% Y/Y and was not only below the estimate of $2.51 billion, but also below the lowest estimate in the range ($2.45 billion to $2.59 billion).

However, the reason for the market’s violent response was not so much earnings, as the company’s comp store sales number, which while beating globally, with a 5.9% increase, up from 4.2% Y/Y, and above the 5.7% expected, it was the US that traders were focused on as US comp sales rose 4.8%, which while double last year’s 2.40%, was below the 5.2% consensus estimate.

This is an issue because, as Bloomberg explains, McDonald’s gets more than a third of revenue from the U.S., where it’s been having a hard time luring more diners, especially during the morning hours. And it’s getting more crowded: Burger King is trying to improve its coffee lineup, Dunkin’ is introducing Beyond Meat breakfast sandwiches nationwide and Wendy’s is planning to re-enter the morning market with a big push next year.

As a result, amid rising competition, CEO Steve Easterbrook has been investing heavily in technology (think robots who demand a $0.00 minimum wage everywhere). That includes delivery, making it easier to reorder on the company’s mobile app and adding smart-tech like license-plate scanners to drive-thrus; yet the beneficial effect of these appears to have topped out.

Meanwhile, as Bloomberg also notes, investors would love to know more about the chain’s plant-based ambitions in the US, but it hasn’t let slip who it’s considering for its 14,000 locations in that market. That said, MCD did announce a test with Beyond Meat in Canada last month. McDonald’s former CEO Don Thompson was an early investor in Beyond through his Chicago-based Cleveland Avenue fund.

In any event, the kneejerk reaction to the miss in earnings and comp sales was not taken well by the market, and the stock slumped as low as $200, down 4% and the lowest level since June (the stock had climbed 18% through Monday)…

… and since MCD is among the biggest Dow Jones members, its results pushed the “industrial” average back in the red.

Johnson Seeks Approval For “Whirlwind” Votes On Brexit Plan

After being twice stymied by the opposition during Saturday’s historic session and again on Monday, UK Prime Minister Boris Johnson is facing the beginning of an accelerated series of votes with the ultimate goal of pushing his withdrawal agreement through the House of Commons this week, which would ensure that the UK leaves the EU at the end of the month.

However, some of the MPs who ostensibly support his Brexit deal apparently have reservations about this three-day “whirlwind” timetable. According to the Times of London, Johnson has been warned that his attempt to kick off the votes on the Withdrawal Agreement Bill Tuesday night will be met with defeat unless he agrees to a longer post-Brexit transition.

Nick Boles, a member of the group of Tory rebels who left the party last month, has proposed an amendment to extend the Brexit transition period until the end of 2022 unless MPs pass a resolution to cut it short.

Last night, Johnson’s government officially published the “withdrawal agreement bill” for its first reading (of three). That bill is likely to pass its first vote on Tuesday (the “second reading” vote) thanks to the support of expelled former Tories and opposition rebels, despite confusion over Labour’s official stance on the second reading. Another vote on Tuesday over whether to approve the express timetable for the WAB (withdrawal agreement bill) could derail the prime minister’s Brexit dash, as several former Tory rebels have warned that they want to slow down the process to ensure the “proper scrutiny” is applied.

Rory Stewart, a former Tory who was expelled from the party last month, warned against ramming the bill through Parliament, arguing that it might “further undermine confidence in our institutions.”

“That means delivering a deal with proper process and scrutiny. Ramming through the bill will further undermine confidence in our institutions. We must do this properly.”

If the program motion – the technical term for the vote on whether to accelerate the process of passing the withdrawal agreement bill – fails, it will virtually ensure that the UK doesn’t complete the Brexit process at the end of the month. The EU has so far held off on granting an official extension, since it’s waiting on developments in Westminster.

The Tory whip has warned that the vote on the program motion will be tight, and that Johnson will need to pick up 20 opposition votes to offset votes from former conservatives.

However, since most sell-side research shops and the FT’s vote tracker now believe Johnson has the votes to ultimately pass his Brexit deal – even without the support of the DUP and its 10 MPs – it’s widely expected that any Brexit delay from this point onward would likely be brief. However, Johnson has reportedly warned MPs that he would abandon the bill if MPs force through amendments that are outside the scope of the deal with the EU. Opponents of Johnson’s deal have also warned that they might attempt to amend it as it goes through the committee stage.

Of course, that could swiftly leave the UK in caretaker government/election territory, as analysts at DB warn.

Also, thanks to the transition period, Britain won’t actually finish with the business of leaving the EU until the end of next year.

Johnson hopes to pass the WAB by end of day Thursday, giving the House of Lords a chance to vote on Friday.

Since Johnson is facing a punishing gauntlet of votes, yields on eurozone bonds dropped on Tuesday morning, reflecting the market’s anxieties as the deadline approaches. The pound was also weakening early in the day in New York.

Here’s a schedule of upcoming Commons votes (courtesy of DB):

Tuesday

12.30 p.m.: Second Reading debate starts

7 p.m.: Vote on Second Reading – the general principle of the bill

7.15 p.m.: Vote on Program Motion – the timetable for the rest of the bill’s passage

7.30 p.m.: (If Program Motion passes) Committee Stage begins

10.30 p.m.: First Committee Stage votes

Wednesday

After 12.30 p.m.: Committee Stage continues, with votes every three hours. Amendments on keeping the U.K. in a customs union with the EU and calling a second referendum are likely to appear

After Midnight: Committee Stage finishes

Thursday

After 11 a.m.: Report Stage begins. More amendments can still be proposed

After 5 p.m.: Report Stage votes

After 7 p.m.: Third Reading vote – the House of Commons’s final say on the bill

Ultimately, both the FT’s vote-tracker and most sell-side research shops expect the a final vote on the withdrawal agreement to pass by a moderate margin.

Futures Rebound From Overnight Swoon On Strong Earnings As Key Brexit Votes Loom

After spiking higher in the early overnight session for no obvious reason besides a largish buy order in an increasingly illiquid market, US equity futures faded most of their gains during the Asian session despite some renewed “trade deal optimism” after China’s Vice Foreign Minister Le Yucheng said that China and the United States have achieved some progress in their trade talks, before recovering much of their losses after the European open, and pushing modestly higher following strong earnings from P&G, UPS and UTX which helped push future above the flatline.

It’s a huge week for corporate earnings, with around one-fifth of S&P 500 members due to report, including McDonald’s and Procter & Gamble on Tuesday followed by Microsoft and Caterpillar a day later. So far results have generally surprised to the upside, although estimates have declined sharply in recent week. Despite the beats, analysts are still cutting estimates for next year as the protectionist dispute between the world’s biggest economies continues to take a toll.

Futures closely tracked European markets which saw a flurry of company results including UBS profit beating estimates as the Swiss lender said it will book a roughly $100 million charge in the fourth quarter to restructure a unit. Helping European markets, drugmaker Novartis raised its earnings forecast for the third time this year. The European banking sector was off its best levels, however, with gains in tech and real estate names offset by losses in household, travels and construction.

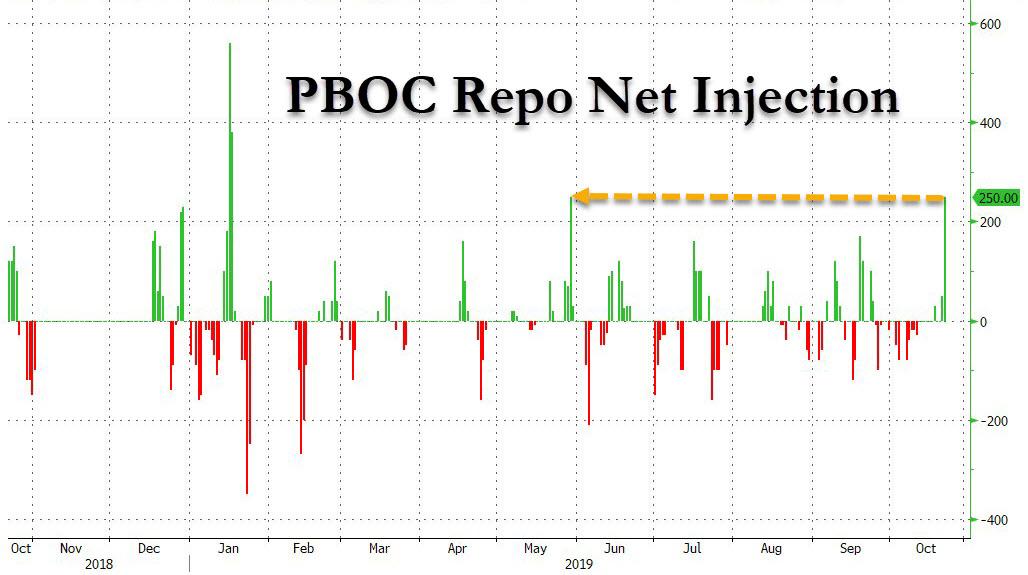

Earlier in the session, Asian stocks climbed for a second day, led by health-care firms, amid rising hopes that China-U.S. trade talks will progress toward an agreement. Most markets in the region were up, with South Korea – seen as a proxy for global trade – leading gains. Japan was closed for the Imperial Enthronement day. The Shanghai Composite Index closed 0.5% higher after erasing earlier losses, with Foxconn Industrial Internet and Industrial & Commercial Bank of China among the biggest boosts. China’s central bank used open-market operations to inject the largest amount of cash into the banking system since May, as upcoming corporate tax payments tighten liquidity conditions.

India’s Sensex fell 0.7%, snapping a six-day winning streak, as Infosys plunged following a whistle-blower complaint alleging irregular accounting at the software exporter. Infosys sank as much as 16%, weighing heavily on the gauge and more than offsetting post-earning gains in HDFC Bank Ltd. and Reliance Industries.

President Donald Trump stoked hopes that a trade deal can be reached next month, saying that China has indicated negotiations are advancing and has started buying more American agricultural products. “There are still residual concerns about the outlook as we head toward Christmas with memories of last year’s price capitulation still fresh,” said strategist Greg McKenna. “But earnings so far aren’t as bad — or should I say much worse — than thought. And there is still much cash on the sidelines, and the increase in bond yields is mildly supportive of stocks.”

Eurozone government bonds yields fell on Tuesday, before a critical vote in British parliament crucial to determining whether the UK can leave the European Union in an orderly way on Oct 31. Prime Minister Boris Johnson faces two Brexit votes in the British parliament on Tuesday. Lawmakers will first vote on a Withdrawal Agreement Bill and then on the government’s timetable for approving the legislation.

“It’s too close to call whether there will be a majority,” said DZ Bank rates strategist Daniel Lenz. “This may be also very much reflected by market developments, that you don’t see major movement to one or the other side.” Johnson probably has the votes to pass the withdrawal bill but may struggle to pass his timetable on Tuesday, the BBC’s political editor said.

Ten-year government bond yields across the euro zone were down 2 basis point on the day. Germany’s 10-year yield was at -0.36%, bull flattening with German 30y yields 4.5bps lower. Analysts said much of the optimism around Brexit is already priced in and expect subdued reactions. Euro zone government bonds sold off as the first signs of a Brexit deal emerged; the German 10-year bond yield has risen 19 bps since Oct. 10.

“The market is pricing a lot of optimism, a) on the no-deal Brexit being taken off the table tonight, b) on the deal being approved tonight. Therefore, there’s not much room for rates to move higher,” said ING senior rates strategist Antoine Bouvet.

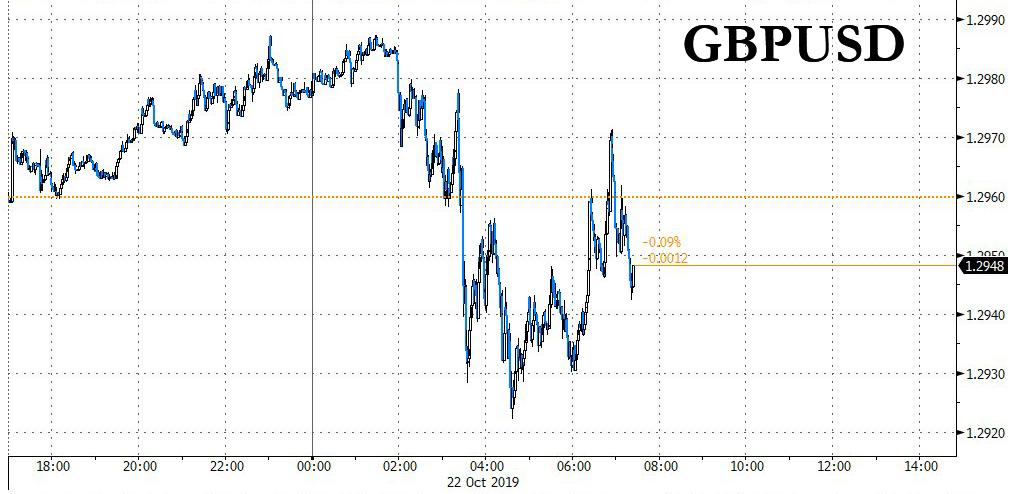

As one would expect, overnight volatility in sterling remained elevated as traders position ahead of the Second Reading vote, with cable drifting below the key 1.300 level.

In other FX markets, the dollar caught a bid with EURUSD trading around Monday’s lows, CNH is offered above 7.0800, while Canada’s Loonie traded flat after Prime Minister Justin Trudeau won a second term in elections, though with a reduced mandate.The shekel strengthened after Benjamin Netanyahu again failed to form a government in Israel.

Elsewhere, Italian government bonds outperformed, the 10-year yield falling 6 basis points to 1.03%. “Think of BTPs at the moment as being bunds with greater volatility. So when the bund market sells off, BTPs tend to sell off more,” ING’s Bouvet said. The European Commission has sent a letter to Italian authorities, asking for clarification over their 2020 draft budgets. Rome will reply by Wednesday. That said, a major conflict is not expected, unlike last year when the Commission sent back Italy’s draft budget and asked for a new one, sparking a surge in Italian yields. Italy’s draft 2020 budget assumes a rise in its structural deficit of 0.1% of GDP. Under EU rules, it should fall to 0.6% of GDP. A successful sale of BTP Italia inflation-linked bonds to retail investors also supported Italian bonds

In commodities, crude futures popped higher off the Asian lows back into the green. Mixed trade in metals, LME tin drops 0.6. Upside in prices coincided with reports that Indonesia’s Pertamina has temporarily halted fuel distribution via the pipeline in parts of West Java due to an explosion. Local media noted that the fire broke out on parts of the pipeline due to drilling activity in close proximity, although this was not confirmed by Pertamina’s spokesperson. WTI prices gained traction above the 53.50/bbl and currently eyes its 200 WMA at 53.81/bbl, while its Brent counterpart rose comfortably above the 59.00/bbl mark. In terms of demand side commentary, Goldman Sachs lowered its 2020 oil growth demand outlook to 1.3mln bpd from 1.4mln bpd and sees US oil growth expectations to be reduced, while it suggested there is room for OPEC output to increase beyond 2020.

In geopolitics, Turkey President Erdogan vowed to go ahead with its Syria offensive “more strongly” if the US “breaks its promises”. Further, Kurdish YPG Militia are to initially withdraw from the 120km strip of border with Turkey in Northeastern Syria, according to Turkish Security Forces sources.

Looking at the day ahead, as well as the beginning of the debate in the House of Commons on the Withdrawal Agreement Bill, earnings season picks up again, with releases including UBS Group, McDonald’s, Procter & Gamble, Novartis, Texas Instruments and United Technologies. In terms of data releases, we have UK public sector net borrowing for September, Canada’s retail sales for August, and in the US there’s September’s existing home sales and October’s Richmond Fed manufacturing index. Finally, the Hungarian central bank will be deciding on rates.

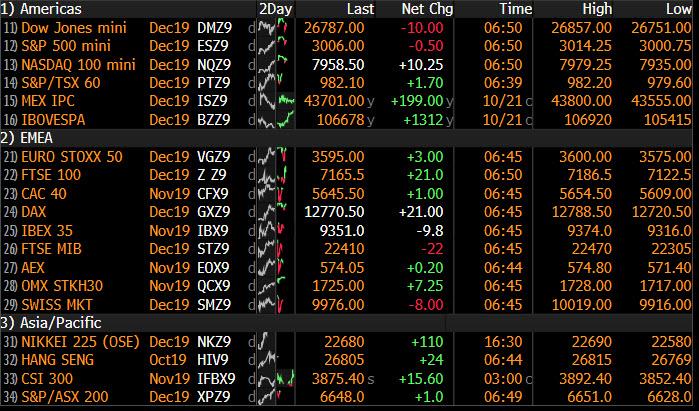

Market Snapshot

S&P 500 futures little changed at 3,004.25

STOXX Europe 600 down 0.3% to 392.90

MXAP up 0.2% to 160.49

MXAPJ up 0.4% to 516.62

Nikkei up 0.3% to 22,548.90

Topix up 0.4% to 1,628.60

Hang Seng Index up 0.2% to 26,786.20

Shanghai Composite up 0.5% to 2,954.38

Sensex down 0.6% to 39,069.54

Australia S&P/ASX 200 up 0.3% to 6,672.18

Kospi up 1.2% to 2,088.86

German 10Y yield fell 2.9 bps to -0.373%

Euro down 0.1% to $1.1137

Italian 10Y yield rose 5.6 bps to 0.642%

Spanish 10Y yield fell 2.4 bps to 0.262%

Brent futures up 0.4% to $59.20/bbl

Gold spot up 0.3% to $1,488.80

U.S. Dollar Index little changed at 97.40

Top Headline News

Prime Minister Boris Johnson will find out Tuesday evening whether he has any chance of getting his Brexit deal through Parliament — and whether he can do it ahead of his Oct. 31 deadline

President Donald Trump said China has indicated that negotiations over an initial trade deal are advancing, raising expectations the nations’ leaders could sign an agreement at a meeting next month

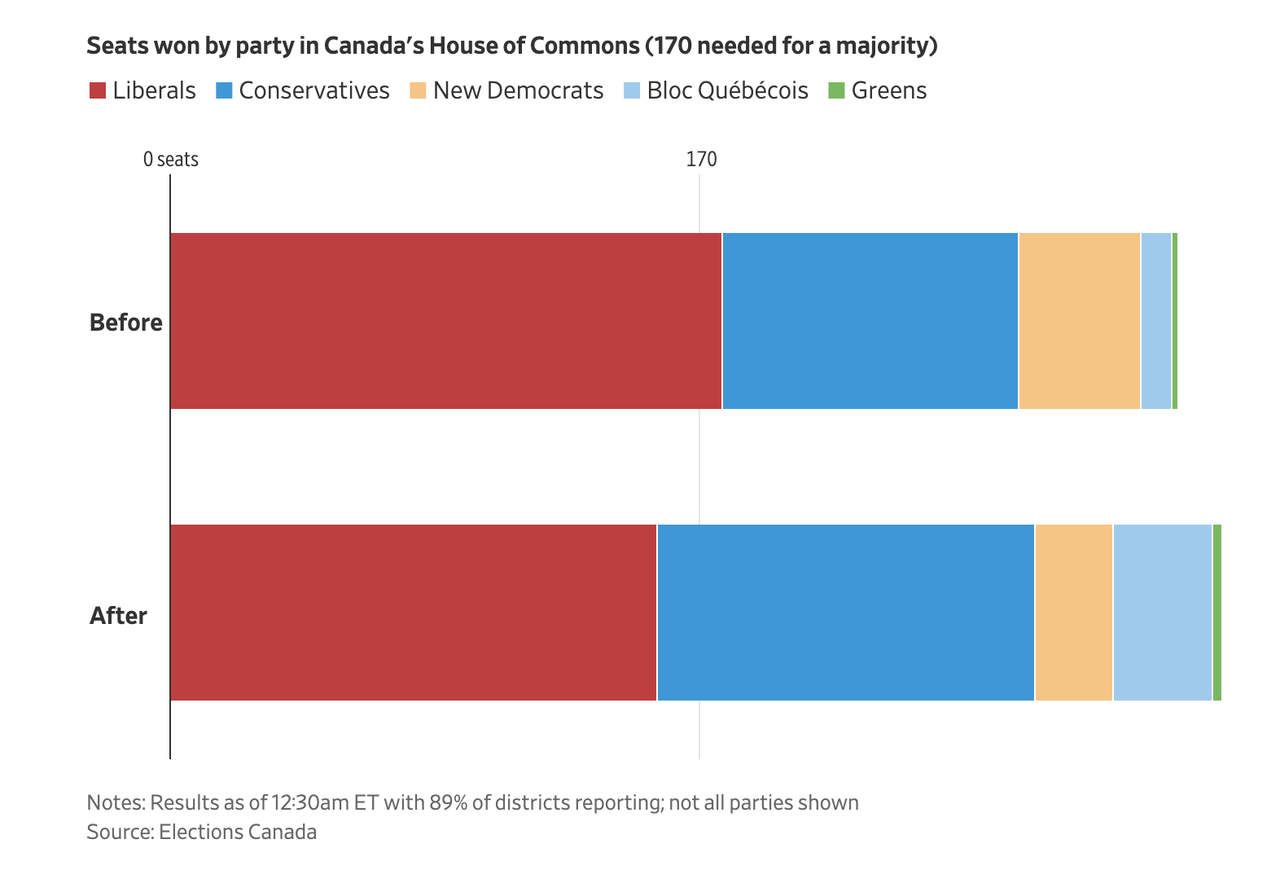

Canadian Prime Minister Justin Trudeau won a second term in national elections and will lead a minority government with support from other smaller parties. The most likely partner for Trudeau would be the pro-labor New Democratic Party

UBS Group AG got a boost from rich Asian clients in a quarter hit by a poor result at the investment bank. The key wealth management unit added $15.7 billion new money in the three months through September, helping lift assets overseen to a record $2.5 trillion

House Democrats are looking to significantly advance the impeachment probe of Donald Trump with testimony Tuesday from the top U.S. diplomat to Ukraine, who had warned it was “crazy” to withhold military aid in a bid to get dirt on Trump’s political rivals

Two London investment bankers were charged in the U.S. with selling information about pending deals as part of a “large-scale, international insider-trading ring” that, prosecutors claim, generated tens of millions of dollars in illicit profits.

Asian equity markets traded mostly positive amid mild tailwinds from Wall St where all major indices edged higher and the S&P 500 closed back above the 3000 milestone with sentiment underpinned as officials continued to suggest optimism regarding a trade deal, although gains were capped amid a light calendar, Japanese holiday closure and ahead of a busy week of earnings stateside. ASX 200 (+0.3%) was positive with the index propped up by strength in the commodity-related sectors aside from gold miners after the precious metal trickled further below the USD 1500/oz level, while corporate updates also provided a catalyst. Hang Seng (+0.2%) and Shanghai Comp. (+0.5%) were mixed despite a firm liquidity effort by the PBoC which conducted CNY 250bln of 7-day reverse repos for its largest daily net injection in nearly 5 months, with the mainland choppy ahead of upcoming earnings and with Hong Kong anticipating the announcement of further supportive measures for companies later today.

Top Asian News

China’s $208 Billion Liquor Giant Just Hit Valuation Ceiling

China Inc. in Exit Challenge as Deals From Yachts to Pizzas Flop

China’s Central Bank Boosts Liquidity Ahead of Tax Payment Surge

Infosys Dives Most in 6 Years as Whistle-Blowers Target CEO

Major European bourses are choppy (Euro Stoxx 50 +0.1%) albeit, the region drifted back into positive territory following initially losses seen at the open. Constructive reports on the EU/China trade during the early EU session ultimately did little to shift the sentiment at the time. In terms of sectors, the picture is mixed; with Consumer Staples (-0.5%) and Health Care (-0.2%) propping up and Tech (+0.4%) and Energy (+1.0%) topping the performance table. In terms of individual mover; Just Eat (+24.7%) shares spiked higher on the news that Prosus NV had made a cash offer for the Co, valuing it at GBP 4.9bln, or GBP 7.10 per share, Just Eat has since rejected the offer stating that it significantly undervalues the Co. in combination with Takeaway.com. Novartis (+0.1%) opened higher after the Co. raised net sales guidance but gave away gains in-line with the market-wide decline. UBS (+1.6%), SAAB (+5.4%), Software AG (+9.3%) and Sunrise Communications (+2.5%) were also beneficiaries of strong earnings reports. Conversely, weak earnings from AMS (+0.2%), Thales (-2.2%) and Reckitt Benckiser (-3.3%) saw their respective share prices under pressure. In terms of broker moves, a downgrade for TUI (-5.7%) at Morgan Stanley saw the Co.’s shares sell off.

Top European News

Just Eat Gets Rival Bid From Prosus, Challenging Takeaway Deal

John Malone’s $6.4 Billion Swiss Sale to Sunrise Collapses

Novartis Boosts Forecast Again as New Gene Therapy Shines

Reckitt Benckiser’s New CEO Lowers Forecast in Company Reset

In FX, the USD is on a firmer footing, almost across the G10 board, with the DXY edging higher after testing support ahead of 97.000 yesterday and the index regains momentum to probe above 97.400 within a 97.440-259 range. However, the recovery looks largely due to declines in rival currencies rather than self-generated, as the Franc retreats further from recent peaks and Pound succumbs to a bout of more pronounced pre-UK Parliament vote jitters.

NZD/AUD – The Kiwi is off best levels, but still outperforming and maintaining a bullish bias while holding above 0.6400 vs its US counterpart and having breached 1.0700 against the Aussie. Conversely, Aud/Usd continues to fade ahead of 0.6900 even though news on US-China trade has been mainly constructive of late amidst signs of the pair reaching overbought levels and a decent option expiry at 0.6850 (850 mn) may also be weighing. Back to the Nzd, trade data looms and may provide some fundamental impetus, while the Aud could be prone to comments from RBA Deputy Governor Kent also due later.

CHF/GBP – The major laggards as noted above, with Usd/Chf nudging towards 0.9900 and Cable retreating further from Monday’s 1.3000+ peaks in the run up to the WAB 2nd reading in the HoC that could set-off a chain of further votes and an extremely compressed timetable to get Brexit legislation in place for October 31. The Pound is holding above 1.2900 and managing to contain its pullback vs the Euro to circa 20 pips below 0.8600, as the single currency also fades against the Dollar.

JPY/CAD/EUR – All narrowly mixed compared to the Buck, as the Yen meanders between 108.50-75, Loonie sustains gains within 1.3100-1.3070 parameters after the Canadian election and bulk of votes indicating that PM Trudeau is heading for a return to office with his Liberal Party, but also conscious that retail sales and the Q3 BoC business/loan survey are on tap and could impact. Elsewhere, Eur/Usd remains capped ahead of 1.1200 and has tested the 100 DMA (1.1136), but not convincingly.

EM – Although the Dollar has pared some losses vs G10 peers and the Yuan has eased from recent highs, several regional currencies are staging comebacks of their own, like the Rand and even the Lira despite the impending end of the ceasefire and ahead of Turkish President Erdogan’s meeting with his Russian counterpart.

In commodities, WTI and Brent futures are choppy but ultimately in the green. Upside in prices coincided with reports that Indonesia’s Pertamina has temporarily halted fuel distribution via the pipeline in parts of West Java due to an explosion. Local media noted that the fire broke out on parts of the pipeline due to drilling activity in close proximity, although this was not confirmed by Pertamina’s spokesperson. WTI prices gained traction above the 53.50/bbl and currently eyes its 200 WMA at 53.81/bbl, while its Brent counterpart rose comfortably above the 59.00/bbl mark. In terms of demand side commentary, Goldman Sachs lowered its 2020 oil growth demand outlook to 1.3mln bpd from 1.4mln bpd and sees US oil growth expectations to be reduced, while it suggested there is room for OPEC output to increase beyond 2020. For reference, the firm’s demand forecasts are modestly higher than that of the EIA, IEA and OPEC. Looking ahead, trader will be eyeing the weekly API crude data, but before that over in the UK, the vote on the 2nd reading of the Withdrawal Agreement Bill may prompt some sentiment-driven action. Elsewhere, gold prices remain firmer sub-1500/oz despite a bounce back in Dollar as participants could be hedging ahead of upcoming risk events, and with US-China also still on the radar. Meanwhile, Copper prices are on the backfoot today, mostly due to the indecisive risk sentiment coupled with a firmer Buck with prices back below 2.65/lb ahead of its 100 DMA at 2.63/lb. Finally, Dalian iron ore futures rose in excess of 1.2% at one point as the base metal was bouyed by continued supply woes after Vale halted a tailing dam earlier this month followed by downgrades in FY iron ore and pellet sales guidance.

US event calendar

10am: Richmond Fed Manufact. Index, est. -7, prior -9

10am: Existing Home Sales, est. 5.45m, prior 5.49m; MoM, est. -0.73%, prior 1.3%

DB’s Jim Reid concludes the overnight wrap

I appreciate that the UK population is only 0.9% of the world’s total and that there are perhaps more important things for global markets in the greater scheme of things than Brexit but you only have to look at the selloff in 10yr bunds since the bilateral meeting between Varadkar and Johnson (+20.5bps) two weeks ago to see the impact that a no deal risk has had on markets. Famous last words but we should know a lot more by the end of today as to whether the U.K. will leave the EU by the end of next week (or soon after). As expected the government were refused the opportunity for a meaningful vote last night for reasons explained yesterday but they are pressing on with the Withdrawal Agreement Bill today, the text of which was published by the government last night. The timetable will be intense and perhaps one risk is that MPs feel like they are being rushed into it and don’t vote for a bill that they might have otherwise have done. The Government want to have it pass the House of Commons by Thursday (with midnight sittings) before going to the House of Lords on Friday in order to try to deliver Brexit by October 31st (next Thursday). There is a vote today on this timetable (7:15 pm London time) and that could be a big test for the government’s strategy. Before this, the government is likely to hold what’s known as the Second Reading vote at around 7 pm (London time)– on whether Parliament agrees with the general principles of the bill. Sources this morning suggest Labour will abstain on this which would mean this vote will go through. If true Labour will use the amendments to create difficulties for the government.

We’ve copied the timetable below. Losing the Program Motion vote, which sets the timetable for the rest of debate, would simply make it very hard to hit the deadlines.

Tuesday

12.30 p.m.Second Reading debate starts

7 p.m.Vote on Second Reading – the general principle of the bill

7.15 p.m.Vote on Program Motion – the timetable for the rest of the bill’s passage

7.30 p.m.(If Program Motion passes) Committee Stage begins

10.30 p.m.First Committee Stage votes

Wednesday

After 12.30 p.m. Committee Stage continues, with votes every three hours. Amendments on keeping the U.K. in a customs union with the EU and calling a second referendum are likely to appear

After Midnight Committee Stage finishes

Thursday

After 11 a.m.Report Stage begins. More amendments can still be proposed

After 5 p.m.Report Stage votes

After 7 p.m.Third Reading vote — the House of Commons’s final say on the bill

Even if the Program Motion passes, the passage of this legislation is also likely to be fraught, as opponents of the Brexit deal have already said that they’ll seek to amend the legislation as it passes through the Committee stage. As we discussed yesterday, likely amendments to watch out for will be those calling for a second referendum and another seeking a customs union. Labour’s shadow Brexit Secretary Sir Keir Starmer has also said that Labour would seek to avoid the possibility that at the end of the transition, the UK could simply revert to a no-deal scenario if no free-trade agreement has been reached with the EU. On Sunday it looked like momentum was building towards a customs union membership amendment passing. However the DUP seemed to indicate yesterday that they wouldn’t support it and a number of MPs who have previously supported it in indicative votes suggested they wouldn’t this time. Much might depend on the SNP and Lib Dems whose policy is to stop Brexit and therefore would only vote for it to bide time and complicate the government’s task. They may do so. The government have hinted they would withdraw the bill if such an amendment passes and we could soon be in caretaker government / imminent election territory. A second referendum amendment is not likely to pass according to those journalists close to the action but the Customs Union one is closer depending on the above.

Sterling was relatively strong yesterday as the dip was quite rightly bought, given the balance of risks, climbing above $1.30 in trading for the first time since May 13 yesterday. It ended up finishing -0.16% at $1.296, though that was +0.66% off its earlier lows from the open. Its trading up +0.16% this morning at $1.2981.

Amidst the political developments, equity markets advanced yesterday as optimism over the Brexit saga and positive noises on trade boosted sentiment on both sides of the Atlantic. The S&P 500 closed up +0.69% to reach its highest level in a month, leaving the index shy of just a +0.64% rise from its all-time high back in July. The NASDAQ (+0.91%) also advanced, although the Dow Jones was up just +0.21% thanks to Boeing, which fell -3.76% yesterday ahead of its earnings release. The energy sector led sectoral gains, closing +1.86% higher, led by Halliburton (+6.35%) after a strong earnings report. The company announced plans to expand more aggressively overseas, while simultaneously limiting costs in the US. The positive earnings momentum outweighed the fall in oil prices, with Brent down -0.62%.

Meanwhile in Europe, the STOXX 600 (+0.61%), the DAX (+1.0x%) and the FTSE MIB (+0.91%) all climbed to their highest levels in over a year. It was the reverse picture in bond markets, with sovereign bonds losing ground and curves steepening in both the US and Europe. 10yr Treasuries ended the day +4.7bps, while the 2s10s curve steepened +0.2bps to its highest level since July. Bund yields climbed +3.8bps to -0.344%, also its highest level since July, while OATs (+3.3bps), BTPs (+5.8bps) and Gilts (+4.1bps) also suffered losses. Banks were the beneficiaries however, with the S&P 500 Banks index up +2.02% at a thirteen month high, while the STOXX Banks was also up +2.17% to its highest level since May.

There was little to report directly on the trade war yesterday, though President Trump did say that a deal with China was coming along very well, while the Director of the National Economic Council, Larry Kudlow said to Fox Business that President Trump could call off the planned December tariffs if the talks went positively. Meanwhile Reuters reported that China was seeking $2.4bn in retaliatory sanctions against the US in response to the US failing to comply with a previous Obama-era WTO ruling. This should be separate from the trade war noise. In the FX market, the dollar snapped a run of four consecutive sessions lower to close up +0.05%.

Overnight Asian markets are trading mixed with the Kospi (+1.17%) and Hang Seng (+0.15%) up while the Shanghai Comp (-0.09%) is down. Japanese markets are closed for a holiday. Elsewhere, futures on the S&P 500 are up +0.20%.

In other news, Canadian Prime Minister Justin Trudeau won a second term in national elections with a reduced mandate as his Liberal Party won or was leading in 155 of Canada’s 338 electoral districts, short of the 170 needed for a majority in Parliament. The most likely partner for Trudeau would be the pro-labor New Democratic Party, which is on track to win 26 seats, giving the two parties a combined 181. The Canadian dollar is trading largely flat this morning at 1.3082.

Chilean assets slumped yesterday as markets reacted to recent protests in the country that have seen 11 people killed. The country’s IPSA equity index was down -4.61%, its worst daily performance in nearly two years, while the Chilean peso weakened -2.26% against the US dollar, its sharpest depreciation in four years. The unrest was originally started by a now-suspended rise in public transport fares, but has since become a broader movement against inequality and economic conditions. President Sebastian Pinera has taken a tough stance against the rioters, saying in a speech on Sunday night that “We are at war against a powerful, relentless enemy”. It’s worth keeping an eye out on copper prices (up a further c. 0.40% this morning), which rose to their highest level in over a month yesterday, as Chile is the world’s biggest copper producer and unions in the country have called for strikes that could threaten supply.

There was little in the way of data, though German PPI in September fell by -0.1% yoy (vs. -0.2% expected), which was the first yoy decline since October 2016. Energy prices dragged in particular, down -1.9% over the last year, with the PPI excluding energy actually up +0.5%. However, the market’s expectations of euro area inflation seem to be rising, with five-year forward five-year inflation swaps up +1.5bps to 1.238% yesterday, their highest level in a month.

Turning to the day ahead, as well as the beginning of the debate in the House of Commons on the Withdrawal Agreement Bill, earnings season picks up again, with releases including UBS Group, McDonald’s, Procter & Gamble, Novartis, Texas Instruments and United Technologies. In terms of data releases, we have UK public sector net borrowing for September, Canada’s retail sales for August, and in the US there’s September’s existing home sales and October’s Richmond Fed manufacturing index. Finally, the Hungarian central bank will be deciding on rates.

Trudeau Overcomes Scandal To Win 2nd Term As PM, But Fails To Secure Majority

Justin Trudeau has overcome a raft of scandals, ranging from the juvenile and relatively benign (the ‘blackface’ scandal that erupted last month after Time magazine published photos of Trudeau wearing brown face paint at a costume party in 2001), to the blatantly corrupt (he and his aids tried to impede the criminal prosecution of SNC Lavalin, an engineering firm based in Quebec), and won a second term as Canada’s prime minister.

The final results were released late Monday evening: Despite losing the national popular vote, Trudeau’s Liberal Party won 156 seats, giving them a clear plurality of the vote. However, Trudeau’s government will lose its outright majority, meaning that Trudeau will need to rely on votes from opposition parties to pass his agenda (the threshold for a majority in Canada’s House of Commons is 170).

The Liberals had 177 seats when Trudeau dissolved Parliament 40 days ago at the start of the official campaign season.

Though he has established himself as an icon of liberal values and multiculturalism, Trudeau’s ostensible commitment to feminism and bolstering the rights of minorities was exposed as cynical political posturing by the series of scandals that marred the final year of his first term.

His party lost its lead in the polls during the final weeks of the election, as several images of a young Trudeau wearing blackface surfaced, leading the PM to embark on a national apology tour that featured this cringe-worthy moment where Trudeau tries to explain what he did and apologize to a group of kids (because “what kind of monster lies to a child?“).

Though Trudeau managed to prevail over his conservative rival Andrew Scheer, the enthusiasm that helped his Liberals retake the majority after a decade out of power back in 2015 was clearly lacking this time around. As one pollster told WSJ, Trudeau has lost the luster of progressive icon, and has instead become “just another politician.”

“Trudeau has become just another politician – and a flawed one at that,”said Darrell Bricker, president of Ipsos Public Affairs, a polling firm.

Ipsos found that during the final weeks of the campaign 57% of Canadians didn’t approve of the job Trudeau was doing.

To be sure, Trudeau pulled out all of the stops during his campaign. Sensing his old friend might be in trouble, former President Barack Obama made an unprecedented endorsement by saying he backed Trudeau for a second term.

Then again, winning back-to-back majorities is a relative rarity in Canadian politics. It hasn’t been done since the Liberal government of Prime Minister Jean Chrétien back in the 1990s.

During his victory speech, given half in English, half in French, Trudeau thanked his supporters, and insisted that he now had a clear mandate to continue with his Liberal Party’s program, adding that Canadian voters had rejected the “austerity” pushed by the Conservatives.

A UK police force created a video which portrayed a white toddler being racist towards another toddler in kindergarten as part of “hate crime awareness week.”

Yes, really.

Devon & Cornwall Police posted a cartoon video to their official Twitter account which features a blonde haired, blue eyed girl racially abusing a dark skinned boy.

In the cartoon, the white girl sees the brown boy playing with a toy before walking up to him and telling him, “Stop playing with those, you’re going to make the toys dirty like your skin.”

The brown boy immediately starts crying before the teacher intervenes.

“My father says we should not play with people like him because they are different,” says the girl.

The video is one of numerous different cartoons posted to Twitter by Devon & Cornwall Police where in every case the bigoted or racist protagonist is white.

As Jack Montgomery writes, the cartoons urge the public to “report ‘hateful’ behaviour even if it isn’t a crime”, offering assurances that “you don’t even need evidence”.

Last week we highlighted how a chief of police in Britain chose to recognize “international pronouns day” by putting out a video warning people that misgendering transgender people was a form of “abuse.”

All this is occurring while police budgets are stretched to breaking point and the UK’s violent crime rate continues to soar.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Vespa Scooter Launches A New Cargo Robot That Can Carry Your Stuff

Piaggio Fast Forward (PFF), a segment of Vespa Scooters, announced on Tuesday that it’s preparing to launch its first consumer robot that follows its owner and can haul their belongings down the street, reported Venture Beat.

PFF spent four years refining its autonomous robot called Gita and will be available for purchase on November 18, 2019, for $3,250.

“The Gita robot is a fundamental step toward the future of mobility for Piaggio Group,” said PFF chair Michele Colaninno. “Our objective is to create an innovative consumer product that is efficient and easy to use while also enhancing daily life.”

Gita, an Italian word for “short trip,” is a robot that measures just 27 inches long, 22.3 inches wide, and 24 inches high, can haul 40 pounds of cargo.

Front-facing camera and other sensors, blended with artificial intelligence, allow the robot to recognize the environment and track its user.

Gita can follow its owner down a sidewalk with 40 pounds of cargo while traveling at a top speed of 6 mph.

Gita is entirely autonomous, and its owners can connect to the robot through an iOS and or Android smartphone.

“PFF was founded to create lifestyle-transforming mobility solutions, allowing people to move with greater freedom in their neighborhoods,” said PFF co-founder and CEO Greg Lynn. “With the Gita robot, our first product, we’re thrilled to see that vision come to life. From students to working professionals, new parents to grandparents, Gita empowers people of all ages to more actively enjoy their surroundings and to interact with their communities in a more meaningful way.”

Gita is part of a “new category within the field of robotics: technology that moves the way people move and that augments human experiences rather than replacing or stifling them. With Gita in tow, people are free to put down their screens, get moving, and reconnect with the truly precious ‘cargo’ that shapes their lives: their partners, kids, and friends,” said Jeffrey Schnapp, co-founder, and chief visionary officer at PFF.

And the future is quite clear, the sidewalks that pedestrians walk on are about to be flooded with robots by 2030.

“Now that the verdict’s out, it’s time to start getting along,” Spanish Prime Minister Pedro Sánchez said at a press conference on October 18, repeating the rhyme—“después de la sentencia, convivencia”—as if it were a magic spell. Around the same time, half a million Catalans were converging on Barcelona, which for the previous four days had seen its airport occupied and highways blocked while violent clashes between protesters and riot police were increasing in intensity each night. Sánchez insisted on framing these clashes as an internal Catalan problem. “What’s at stake is not the territorial makeup of our country, but the Catalans’ ability to get along with each other,” he’d said a few days earlier.

One week of major protests, it appears, did not shake his government’s unwillingness to face reality: The Catalan crisis is something that affects the entire country, and it is far from over.

On October 14, the Spanish Supreme Court announced its much-anticipated ruling on the case against 12 Catalan leaders for their role in the 2017 referendum on Catalan independence. Nine were sentenced to between 13 and 9 years in prison; three more were sentenced to 18 months. The charges included sedition, misappropriation of government funds, and civil disobedience. Oriol Junqueras, the former vice president of Catalonia, received the longest sentence, 13 years, while eight other former Catalan ministers received sentences of 10-12 years and two civil society leaders, known as “the Jordis,” received nine years—all close to the maximum permitted by law. (For perspective, earlier this year the Supreme Court sentenced each of five men found guilty of a violent gang-rape—the “wolf pack” case—to 15 years in prison.)

The verdict was the culmination of a two-year process initiated in October 2017, when Spain’s attorney general brought charges for rebellion, sedition, and misappropriation that prompted a judicial investigation and a public trial involving hundreds of witnesses. Had the court found Junqueras and the other leaders guilty of the charge of rebellion, the sentences could have been as high as 24 years, among the most severe first-time prison sentences allowable in Spain (the 12 Catalan leaders have been in preventive custody since the charges were announced nearly two years ago). Seven other leaders, including former Catalan President Carles Puigdemont, escaped that fate by going into exile elsewhere in Europe.

Yet to the disappointment of some Spanish conservatives, the court concluded in its ruling that Catalonia’s 2017 bid for independence – which included acts of nonviolent protest, a vote to “disconnect” Catalonia from Spain that violated parliamentary procedure, an illegal referendum, and a declaration of independence that was immediately “suspended” – did not rise to the level of rebellion. In fact, the court agreed with the defense that the referendum and the declaration of independence were never more than symbolic gestures, meant to pressure the national government in Madrid into negotiations over Catalonia’s status within Spain. The declaration of independence, the judges wrote, was “symbolic and ineffective,” and “never had any practical concreteness.” The prospect of independence was no more than a “reverie,” they added, “an artful deceit to mobilize the citizenry.” “It is clear,” the court concluded, “that the rebels lacked the most elementary means to…subdue the [Spanish] state.… And they knew it.” The court was likely referring to the warning, issued before October 1 by then–Prime Minister Mariano Rajoy, that, were Catalan leaders to go through with the referendum, they would be charged and the region’s autonomy would be revoked.

The irony of the ruling is palpable to many Catalans and Spaniards alike. The trial made it all the way to the Supreme Court in the first place because it involved the charge of rebellion—a direct, violent, anti-constitutional challenge to the sovereignty of the state. Now, many observers say that the court’s ruling itself infringes on the sovereignty of the people: Its interpretation of “sedition”—a charge leveled at 9 of the 12 leaders on trial—appears to undermine the constitutional right to protest, possibly setting a troubling precedent, in which such a charge can be applied to such acts as organized attempts to block evictions. “The Court’s new description of sedition,” Joaquín Urías, professor of constitutional law, wrote in the magazine Contexto, “describes point by point any social campaign of civil disobedience.” This skewed interpretation of the law, he added, points to a political motivation: The court may be convinced that “its role is to save Spain’s sacred territorial unity by making an example out of those who dare challenge it.”

The ruling, for many, encapsulates the main problems with the current path of the Spanish legal system: growing restrictions on the right to protest and freedom of expression, as well as the judicialization of politics and the politicization of the judiciary. These developments harken back to the widely condemned “ley mordaza” (gag law), a criminal law reform in 2015 that gives the government the power to issue hefty fines for everything from “unauthorized protests” to photographing the police. (On Friday evening, police in Barcelona violently subdued and detained Albert García, a journalist from El País who was photographing their actions.) The ruling also revives anxieties over recent cases involving puppet shows, tweets, and song lyrics construed as “extolling terrorism,” a remarkably fuzzy legal category that has given prosecutors a green light to pursue heavy sentences.

Regarding Catalonia, one of the 17 autonomous regions in Spain’s quasi-federal makeup, the Spanish Supreme Court has been quick to step in, breaking with international legal precedent in Canada and the United Kingdom, where the courts have mostly seen questions of regional sovereignty as a political rather than a legal matter. In Spain, it was the conservative Partido Popular (PP) that first beckoned the courts to intervene. In 2006, it filed an appeal to the Constitutional Court to revoke Catalonia’s newly approved statute of autonomy, which had been jointly negotiated by the governing parties at the national and regional levels and approved by a regional referendum.

The court’s rejection of key elements of that statute, four years later, set off widespread protests in Catalonia. In the years that followed, pro-independence sentiment ballooned from around a quarter of Catalans to nearly half, a figure which, according to polls, still holds more or less true today. Pro-independence parties—which span the spectrum from conservative to left-radical—hold a narrow majority in the regional parliament. But discomfort with the Spanish state is more widespread. According to a late-September poll, around 70 percent of Catalans favor a referendum for self-determination, an option that is anathema to Madrid. And only a fifth of those polled believe the Supreme Court trial of the Catalan leaders has been fair.

Not surprisingly, last Monday’s verdict has unleashed a level of indignation that dwarfs the response to the Constitutional Court’s ruling nine years ago. Within hours of the verdict’s publication, thousands of citizens flocked to the Barcelona airport for an occupation that disrupted air travel for days. Since then, massive displays of peaceful protest, including a general strike on October 18, alternated with nightly acts of vandalism involving smaller groups of protesters who erected barricades, set dumpsters on fire, threw rocks, torched a dozen cars, and in some cases threw Molotov cocktails at riot police. The Catalan and Spanish police have reacted, according to Amnesty International and other observer organizations, with “excessive force” and “inappropriately deploying anti-riot equipment and munitions.” Rubber bullets—whose use is officially prohibited in Catalonia—have so far caused four protesters to lose an eye. Journalists trying to document police actions, like García from El País, have ended up clubbed or arrested.

The anger over police brutality is directed not just at the national leadership in Madrid but also at the Catalan government, which in a display of institutional schizophrenia encouraged citizens to protest the Supreme Court sentence while at the same time ordering the regional police to quash the protests. In fact, Catalan politicians—who after all were forced to admit during the trial that their promises had been empty—have lost much of their credibility and, with it, control of the situation. The coordination of the protests themselves has been diffuse. Some of the main actions, including the occupation of the airport, were directed through an app, “Democratic Tsunami,” whose origin is unclear and which can only be activated by direct contact with an already authorized user. On Friday, Spain’s national criminal court announced it would initiate an investigation of the Tsunami app for possibly aiding and abetting terrorism. Its websites in Spain were shuttered.

The Supreme Court’s verdict and the state’s reaction to the protests have sparked concern beyond Catalonia as well. On October 19, 42,000 people gathered in San Sebastián, in the Basque Country, to demand a political solution to Spain’s territorial question. A demonstration in Madrid calling for amnesty that drew 4,000 protesters ended in violent clashes with riot police. The newspaper Público reported that, once again, the police targeted journalists trying to cover their actions.

Meanwhile, many citizens and fellow journalists have criticized the mainstream Spanish media coverage of the protests. According to the journalist Miquel Ramos, the media have developed a taste for “riot porn.” Ramos also denounced the national media’s tendency to downplay the role of radical-right Spanish nationalists, whose actions have been legitimized by the rise of the far-right party Vox. On Spanish public television, he pointed out, militant right-wing groups brandishing neo-fascist paraphernalia have been euphemistically captioned as “constitutionalists” and “citizens with Spanish flags.” The media help shape Spaniards’ interpretation of the crisis but also reaffirm the country’s divergent universes. On October 19, for example, the front-page layout of the Madrid edition of the country’s largest paper, El País, was the same as the national edition—but the headline was not. “Violent Groups Extend Chaos in the Barcelona Downtown,” read the Madrid edition. The headline in the national edition said: “A Massive Pro-Independence March against the Supreme Court Verdict.”

All of this has taken place in the midst of an electoral campaign. On November 10, Spaniards will go to the polls for the fourth time in as many years, and the second time this calendar year, after attempts to form a progressive majority coalition failed. For the right, which continues to be haunted by corruption scandals, the escalation in Catalonia is a welcome opportunity to shore up votes. They have called for harsher measures in Catalonia, ranging from revoking its autonomy and taking over its regional police corps to declaring a state of exception.

Not to be outflanked in his commitment to Spanish unity, Socialist Prime Minister Sánchez, too, has tried to project the image of a hard-line nationalist, stubbornly sticking to the idea that this is a Catalan, not a Spanish problem. In the weeks leading up to the verdict, his government launched an international campaign to underscore the idea that Spain is a “consolidated democracy,” suggesting that anyone who dares doubt this fact is an “enemy of Spain.” Sánchez has refused to accept phone calls from Catalan President Quim Torra, demanding that Torra first “categorically condemn” this week’s “violence.” By “violence,” he was referring exclusively to the limited nightly acts of vandalism. Sánchez’s strategy, according to party leaders, has been to seek “moderation” in the face of extreme demands by conservative parties that he apply the National Security Law and invoke, like Rajoy did back in 2017, Article 155 of the Spanish Constitution, which would place the government of Catalonia in the hands of the central government in Madrid.

So far, the hard-line tactic seems to be working better for the right than for the center-left. The PP, which took a beating at the April elections, is once again rising in the polls. Sánchez’s Socialists are set to lose some seats, although they are still projected to receive the most votes. As in April, Sánchez is expected to fall well short of a majority in Parliament. A progressive coalition with Unidas Podemos, the anti-austerity party founded only five years ago, proved too difficult to achieve earlier this year. Having Podemos in charge of certain ministries, Sánchez claimed, would have caused him “sleepless nights.” He may well decide instead to try to strike an agreement with those to his right. Earlier this month, Albert Rivera, the leader of Ciudadanos (Citizens), a young neoliberal and Spanish nationalist party, announced that he would lift his veto on negotiating with the Socialists.

Sánchez, however, may simply turn to the devil he knows. The “chaos” in Catalonia might provide him the perfect excuse for a “grand coalition” between the Socialist Party and the PP in the name of national unity. The move would signal an apparent restoration of the constitutional order that Unidas Podemos and other progressive movements have sought to challenge since the indignados movement in the spring of 2011, which arose in the wake of the economic crisis, austerity measures, and government corruption.

The Catalan “threat” to that order, journalist Guillem Martínez wrote this past weekend, has come to play a role similar to that of ETA, the armed Basque pro-independence group, whose presence helped justify restrictions on constitutional rights for much of Spain’s 40-year-old democracy.

Hate crimes in England and Wales have reached record levels.

According to the Home Office, there were 103,379 hate crimes in the 12 months to March this year, an increase of 10 percent on 2017/18. While increases in hate crime over the last five years have been mainly driven by improvements in crime recording, Statista’s Martin Armstrong notes that the Home Office has observed spikes in incidents following events such as the EU Referendum and the terrorist attacks in 2017.

When looking at the motivating factors behind these crimes, race is by far the most common – involved in 76 percent of offences. Although only accounting for 2 percent, crimes against transgender people rose dramatically in the last year, seeing a jump of 37 percent – the largest of the recorded factors. All types recorded an increase, and ‘sexual orientation’ had the second-largest proportional increase, at 25 percent.

House of Commons Speaker John Bercow denied Boris Johnson’s government a meaningful vote on his EU Withdrawal Treaty on Monday after allowing Oliver Letwin to table an amendment designed to force the Government to withdraw it on Saturday.

That amendment passed and the vote was withdrawn. And the question now is what’s next?

The better question is why? Why did they do this when it raises the probability of a No-Deal Brexit given the ‘no extension’ rhetoric coming from the EU?

The answer should be self-evident. The EU will happily grant an extension if the right conditions are in place. And those conditions are simply anything that continues to pave the path towards overturning the 2016 Brexit Referendum vote.

The EU agreed to Boris Johnson’s deal last week because it was the closest thing to a perfect deal for them they would get in a reasonable time frame. The EU want a deal because it brings more certainty to the financial and investment situation across the continent.

The EU really thought they had this thing stitched up, as the Brits would say. But the war of attrition they waged against Brexiteers worked against them. Public opinion in the U.K. has hardened around a “No Deal” option and Nigel Farage’s sniping at the Tories’ mishandling of Brexit has been incredibly effective.

I have little doubt that this is what I or Nigel Farage would consider a good deal. In fact, it’s a terrible treaty that sees the U.K. give up most of its leverage in return for very few guarantees.

But it was a deal that was politically possible given the circumstances. And the movement by Brussels at the last minute is your clue that economic conditions on the European continent are far worse than they are letting on.

I’ve been banging on about this for months, Germany’s economy is crashing. As that continued and the domestic political pressure mounts on Angela Merkel, the leverage was rising on the U.K.’s side of the negotiations.

And since Johnson has done the politically unthinkable, get a deal from the EU, his opponents in Parliament are now trying to ensure that whatever happens next he will pay a terrible price politically for it.

The longer the uncertainty goes on the more likely it will be that Europe will enter the terminal phase of its brewing sovereign debt crisis. Markets are nearly paralyzed by Brexit at this point.

But we’re beginning to see the effects of Brexit fatigue on bond yields. The mother of safe-haven trades has waned in intensity now that the central banks have come in with new QE and liquidity guarantees.

Is this the beginning of the end of the massive bull market into any first-world sovereign debt? Similar technical reversals are in play all across European Bond yields.

Bercow’s refusal to allow a vote on Parliamentary approval of the Withdrawal Agreement is a way to ensure that Parliament can attach amendments to the bill against the government’s wishes.

It’s not like Bercow hasn’t done this before. At every turn he’s interpreted the rule book to suit the agenda of those that want Brexit stopped at any cost.

And the plan now is for Labour to work with Northern Ireland’s DUP to form an alliance against Johnson’s deal and work towards a Second Referendum.

Because that is what the price of Johnson’s deal will be to get a vote on the Withdrawal Agreement Bill through Parliament both a Second Referendum and the addition of the Customs Union.

Any attempt to get a customs union added to Johnson’s deal would probably need to involve former Tory MPs as well as the DUP. A source close to the group of 21 former Tories suggested they might be more interested in the deal being amended to make sure the UK does not crash out on no-deal terms. Most in the group are also keen to make a deal work rather than opt for a second referendum.

However, speaking to the BBC’s Andrew Marr Show,{Labour Brexit Shadow Brexit Secretary Keir} Starmer said he believes a second referendum was still possible. He also suggested Labour could vote for Johnson’s deal if a second referendum was added to the withdrawal agreement bill, despite the party’s fundamental objections to the terms of the UK’s proposed departure from the EU.

Keir Starmer can live with this deal, don’t kid yourself. What he wants, however, is to stop Brexit entirely and humiliate the Tories in the process. We have moved far beyond the appearance of doing the right thing for the British people and moved entirely into cynical machinations to thwart Brexit.

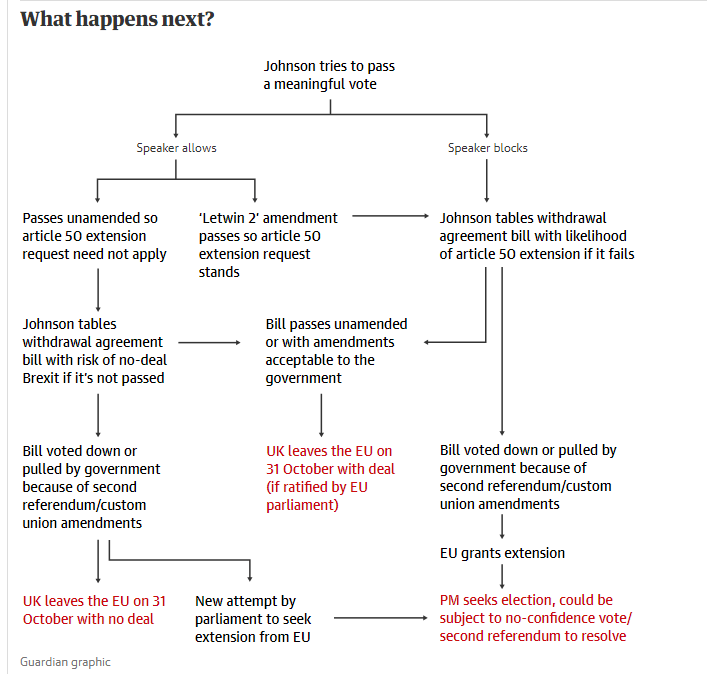

From the Guardian here’s the current Flowchart (before Bercow’s ruling):

Everything on the left-hand side is moot. It is the right side that is now in play.

Note how everything ends with 2nd referendum or an even worse version of BRINO — Brexit in Name Only.

This is why Guy Verhofstadt and the Brexit Steering Committee won’t recommend the Treaty for a vote to the European Parliament until next week. They are banking on events falling into place that leads us right back to the U.K. staying in the EU.

So, today, Johnson will put forth the bill. Bercow will allow a hundred and forty-seven Remain amendments. Johnson will likely pull the bill from a vote because it will be unacceptable.

The EU will grant an extension after that just as The Guardian suggests and then Johnson will be in hot water next week as Parliament, under Bercow, will likely seek to remove him from office and install a last-minute caretaker government to ensure a second referendum of BRINO vs. Remain are the only options.

The Tories that held their noses to get Brexit done and back Boris’ rotten treaty will have betrayed Northern Ireland and their voters for nothing.

Because there will be no General Election until the threat of Brexit is off the table in any meaningful way. This is purely a power play at this point and there is little anyone in the U.K. can do about it as every trick available has and will be used to stop it.

I said this a month ago, Brexit has devolved into random acts of vandalism. And I feel it’s quite clear that most commentators on this process are simply not cynical enough to understand the depth of that statement.

These people are full of envy and despite. They hate having lost the vote. They hate having to implement it. They hate the people for putting them in this position in the first place.

And their threats are nothing more than statements of their allegiance to the EU first and everyone else second.

Because if their allegiance was to the U.K. first they would back an election. They would trust the people to make the choice. But they won’t do that.

Their play now is to throw caution to the wind about what happens after the next General Election. It doesn’t matter that the people hate them. The new treaty or any one cooked up by a caretaker government will have no escape clause.

A parliament in disgrace, a government neutered by over-reaching courts, and a treaty that leaves the U.K. in Zombieland neither free nor prosperous is what the next government will have to contend with with or without a second referendum.

And even if that government is a coalition between Johnson’s Tories and Farage’s Brexit Party, there won’t be any good will between them to present a unified front to the EU since Johnson’s whole Brexit strategy was to deliver BRINO while neutering the challenge Farage represents.

Party before country. Politics before the people. That’s the true story of Brexit.

* * *

Join my Patreon if you want help navigating these chaotic times. Install the Brave Browser to earn crypto, retain some privacy, support your favorite creators and suck money away from the Google Vacuum.

It is nice to finally have a US President who is not a career politician. There is some truth to the Republican/Libertarian trope that lifelong politicians who know nothing but politics are perhaps not the best people to be making decisions on the military, medicine or education as they don’t know about life beyond getting reelected and “working” with lobbyists. Trump’s business background has lead him to making a major policy change that the Mainstream Media has surprisingly ignored that could actually be very good for America’s future.

If we remember back to Trump’s presidential campaign, he rather brazenly promised that he would build The Wall and make the Mexicans somehow “pay for it”. Trump later claimed that through renegotiating trade deals (NAFTA) he ultimately fulfilled his promise, although some would debate this. The interesting thing about this moment in Trump history is that he demonstrated a very different, business oriented, way of thinking that wouldn’t have come from other Republicans/Democrats in Washington.

Candidate Trump was also very vocal on NATO spending and the spending of taxpayer money on the US’s many wars of luxury. President Trump hasn’t ended the Military Industrial Complex but he has been forcing NATO members to pay their dues, which are in the realm of tens of billions of dollars.

This is a much more “realist” perception of NATO by Trump. Officially the organization is a group of allies for self-defense but as we know factually it works like means for the US colonization of Europe. The US military does almost all the work, they project their bases onto the Europeans (never the other way around) and with the recent exception of Turkey all NATO members essentially bow down to any demands made by Washington, however in the past this has come at a price. Empire isn’t cheap and we all know who ultimately paid for the Marshall Plan and the rebuilding of Japan after WWII – US taxpayers. The US has financed the farce of NATO, but Trump wants to change this.

Now breaking with over half a century of a particular tradition Trump is allowing 3000 US troops to go to Saudi Arabia on the Saudi’s dime. Now Trump is offering to provide NATO defense to vassals and “make them pay for it”. This profit-driven policy is a radical departure from the status quo and to be honest is a much wiser wiser way of doing things in the long term with one huge exception depending on your view.

If US forces are to be used under the influence of “market demands” that could really put a dent into the seemingly endless national debt. The US has by far the biggest most expensive military in the world and Washington’s vassals at this point have no other choice but to pay the master for protection, making maintaining US military dominance much cheaper. The only disadvantage (depending on your view) is that if Trump pushes for profitability as a key factor in military decisions/policy then we will never be able have another Vietnam.

There is no way the South Vietnamese could have afforded to pay for US security. Their resources would have run out in a matter of weeks or days. If Trump wants the US to act on a “no money no honey” policy then it makes intervention in a Vietnam-like scenario ultimately impossible. This is good for those of us who want a powerful but respectable America, but for the warhawks this is a nightmare. Financial viability as a key concern in military decisions could spell doom for the parties of war, at least while Trump or a like minded individual is in power.

The Russians have also made a major shift in defense policy. The Soviet Union with less money and a distinct lack of the world’s reserve currency played by similar rules during the Cold War – we will throw money, men and resources at any conflict we see fit in order to ultimately win. But today’s Russia is different and when they entered Syria they made it clear to Assad that they are there to “help” and that Assad’s army is going to have to fight its own battles on its own manpower and resources.

If Russia were to enter a long term expensive military conflict it could possibly sink the entire economy or eliminate for generations Moscow’s debt free status. Sending officially invited advisors and selling top-notch equipment – has no negative long term effects. Trump isn’t the only one who sees the value into playing geopolitics on a strict budget.

This decision by Trump to send troops to defend Saudi Arabia at cost or even for profit could have a much grander resonance than it would seem at first. And hopefully, finally, the burden of Empire can be moved from the shoulders of US taxpayers so that they can enjoy the fruits of that which they have financed for decades.