Trump announced the withdrawal of US troops who had been protecting the SDF(Syrian democratic forces) in the northeast of Syria, prompting Kurdish leadership and the Damascus governed to strike a deal allowing Syrian Arab Army to retake control of the border with Turkey after nearly six years.

With the US troops withdrawn numbering around 150 to 200 (out of the 2,000 to 3,000 illegally squatting in Syria), it is understood that Trump’s decision is for reasons other than those stated.

The primary impression Trump wishes to convey to his voters is that of keeping his electoral promises, including that of defeating ISIS in Syria, meaning that US troops can now come back home.

Although it is clear (at least to those not under the sway of the mainstream media) that ISIS has not been completely defeated and that the US never really fought against the Caliphate, the impression is nevertheless conveyed that the “Winner-in-Chief” has triumphed and is bringing home the boys.

Given that the deep state retains ultimate control of US foreign policy, Trump is allowed to do and say what he wants – provided it is only within the confines of his media playpen, safe in the knowledge that his motivations are purely electoral and not really aimed and upending the foreign-policy consensus of the US establishment.

If we look beyond Trump’s histrionics, we can see that the US deep state continues its illegal stay in Syria, with Trump in reality having no intention of opposing the military-industrial complex (indeed often appointing its members to serve in his administration), with these two parties finding a common point of agreement in the alleged threat posed by Iran.

US troops will only shift near Iraq, looking at disrupting any form of cooperation between Baghdad, Damascus and Tehran.

Trump’s Saudi and Israeli allies in the region have long been conspiring with the Pentagon to bring down the Islamic Republic of Iran.

That said, the possibility of war with Iran does not align well with Trump’s focus on securing a second term. In any such war, Israel and Saudi Arabia would bear the brunt of hostilities, making pointless their support for Trump. The price of oil would rise sharply, throwing the financial markets into chaos; and all this would conspire to ensure that Trump lost the 2020 election. Trump, therefore, has nothing to gain from war and will prefer dialogue and negotiation with the likes of North Korea, even if it does not bear much fruit.

Trump’s main problem lies in the long-term damage his actions and statements may do to the credibility of the US empire. The photo-op with Kim was criticized by many in mainstream media for giving credibility to a “dictator”. But the anger of the military and intelligence community really lay in leaving Washington with nowhere to go after Trump’s threats of annihilation only led to negotiations that did not go anywhere.

I have previously written about the effectiveness of Pyongyang’s nuclear and conventional deterrence, something well known to US policy makers, making them careful to avoid exposing themselves too much such that Pyongyang calls their bluff, thereby revealing to the world that Washington’s bark is worse than its bite. To avoid such an embarrassing situation, Obama and his predecessors were always careful to refuse to meet with the North Korean leader.

The United States bases much of its military strength on the display of power, advertising its theoretical ability to annihilate anyone anywhere. By North Korea calling its bluff and revealing that the most powerful country in the world cannot in actual fact attack it, the projected image of American invincibility is thus punctured.

Similarly, when Trump announced the withdrawal of US troops from the northeast of Syria (quickly downsized by the Pentagon), and above all gave the green light to Turkey to occupy the area vacated, the political establishment and mainstream media swung into action to dissuade Trump from communicating to the world that America does not stick with its allies. Even Fox News, now siding with the Democrats, started giving wide coverage to Trump’s impeachment story, inviting in the process an angry Twitter response from Trump.

Trump is of course more than aware that a complete US withdrawal from Syria would go against the interests of Riyadh and Tel Aviv, those who actually have an influence on him.

Turkey’s aspirations to occupy the northeast Syria are part of Erdogan’s strategy to improve negotiating positions with Damascus and Moscow with regard to the jihadists in Idlib. Erdogan hopes to be able to annex Syrian territory and fill them with the jihadists and their families who lost the war in Syria and who otherwise pose the security risk of invading Turkey from Idlib. Erdogan seems to have come to some kind of understanding with the US, which has hitherto been the protector of the SDF.

Erdogan and Trump didn’t seem to consider the possibility of the SDF and Damascus finding common ground, but this is exactly what happened.

The Syrian Arab Army is now in the North East of the country, protecting its borders against an invading army. Russia and Iran will try and convince Erdogan to downplay the operation in exchange for some sort of arrangement regarding Idlib. The Syrian government in the near future should be able to take back the rich oil fields, boosting its economy.

Turkey and the US have have for years armed and financed terrorism in the region, as have Qatar and Saudi Arabia (in spite of their ideological differences). Even the Syrian Democratic Forces (SDF) were involved in the destabilization of Syria.

All this chaos is ultimately supervised and directed by the United States, which has for years been coordinating in the region color revolutions, the Arab Spring, and proxy wars. Any other interpretation of events would be disingenuous and untruthful.

The withdrawal of US troops from Syria simply reinforces Damascus’s position as the only legitimate authority in Syria, undermines confidence of European allies in the US, and emphasizes the consistency of Moscow’s actions, which has always been opposed to Washington’s chaotic actions in the region.

Amidst this generalized chaos and confusion, Russia, Iran and Syria are trying to put the house back in order again, which includes the international system where sovereign states are respected.

The unipolarists have been suffering pronounced setbacks of late. The expensive air-defense systems of the United States were shown by the Houthis in the last month to be rather ineffectual; Saudi troops soon after this suffered a humiliating defeat in the south of their own country; Washington saw its high-tech drone shot down by Iran; and numerous European and Middle Eastern allies have lost faith in the US, as they watch factions fighting with each other over control for US foreign policy

The US is the victim of a unipolar world order onto which it desperately hangs without any thought of letting go, even as the rest of the world inexorably moves towards a multipolar world order, one that becomes ever more difficult to subdue with every waking day.

Shiller: Recession’s “Not Right Around The Corner” Thanks To Trump-Inspired Consumption

“Consumers are hanging in there,” says Nobel-prize winning economist Robert Shiller, who believes a recession may be years away due to a bullish Trump effect in the market.

Speaking on CNBC’s “Trading Nation” on Friday, the Yale professor said Trump is creating an environment that’s conducive to strong consumer spending, and it’s a major force that should hold off a recession.

“Consumers are hanging in there. You might wonder why that would be at this time so late into the cycle. This is the longest expansion ever.”

“Now, you can say the expansion was partly [President Barack] Obama… But lingering on this long needs an explanation.”

Specifically, Shiller told CNBC that he believes that Americans are still opening their wallets wide based on what President Trump exemplifies: Consumption.

“I think that [strong spending] has to do with the inspiration for many people provided by our motivational speaker president who models luxurious living.”

Finally, Shiller concludes that the next recession may not hit for another three years, and it could be mild.

“Let’s not make the mistake of assuming it’s right around the corner,” Shiller said.

“If the economy is strong, which is what he built is case on, ‘make America great again,’ he has a good chance of getting re-elected.”

But, before the markets can take-off, Shiller stresses President Trump needs to get past the impeachment inquiry.

“If he survives that, he might contribute for some time in boosting the market,” said Shiller.

“We’re maybe in the Trump era, and I think that Donald Trump by inspiration had an effect on the market – not just tax cutting.”

He sees this as the biggest threat to his optimistic forecast.

There’s a video clip circulating on Twitter right now that simply has to be seen to be believed, in which a gaggle of MSNBC pundits are seen furiously agreeing with each other that Tulsi Gabbard has incriminated herself by pushing back against Hillary Clinton’s obnoxious claim that she is a Russian asset.

I refuse to spend any portion of my life researching the name of whatever MSNBC show this was or the panelists it features, but here’s a quick breakdown for posterity:

“One thing that was interesting about Tulsi Gabbard’s response, I mean she went after Hillary Clinton, she was strong, she said she wasn’t gonna run as a third party candidate — she never denied being a Russian asset,” said a panelist MSNBC identifies as Kimberly Atkins. “That was the one aspect that was missing from her response, which, you know, you would think that would be within the first line or two. It was not there.”

“When Hillary Clinton says there’s a Russian asset and doesn’t say anybody’s name and Tulsi Gabbard goes ‘How dare you call me a Russian asset?’,” added some talking beanbag chair identified by MSNBC as Jonathan Allen.

“Wait, so Kimberly’s right, she didn’t say she was a Russian asset,” interjected another super excited panelist, possibly the show’s host but who cares.

“To your point, Hillary Clinton didn’t name names, but there’s Congresswoman Gabbard going ‘Me! Me, me! Me!’”

Now, to be clear, all of these panelists are knowingly lying when they suggest that Clinton may not have been talking about Gabbard. Literally everyone knew that Hillary Clinton was talking about Gabbard from the moment news broke about her libelous comments, which, as Gabbard pointed out in a recent interview, was evidenced by the fact that all the news headlines about those comments featured Gabbard’s name. Clinton referred, using female pronouns, to a Democratic primary candidate who is a “favorite of the Russians”; nobody in the world thought she was talking about Elizabeth Warren, Kamala Harris or Amy Klobuchar, because those candidates have never been smeared as Russian assets, only Gabbard has. The self-evident fact that Clinton was referring to Gabbard was then quickly confirmed by a Clinton aide.

“Hillary Clinton did not mention Tulsi Gabbard by name, but an aide confirms that’s that who she was talking about when she made this stunning claim that the Russians had already hit on a way to meddle in the 2020 election…,” @nancycordes reports https://t.co/debniGhJPQpic.twitter.com/2HHsJwhZsT

The panelists are also lying when they claim that Gabbard has not denied being a Russian asset; obviously if you call something a “smear” as Gabbard has consistently been doing you are saying that it is false. But that should not matter. Claiming that an evidence-free conspiratorial McCarthyite smear is true because the target of that smear did not prostrate themselves sufficiently to deny it is disgusting and shameful in and of itself.

The burden of proof is always on the party making the claim, and extraordinary claims require extraordinary evidence. If an extraordinary claim is made with no evidence at all, the party making that claim should be promptly shamed and dismissed.

One of the most infuriating things about the Russia hysteria which has polluted western political discourse is the way people keep getting away with side-mouthed insinuations and innuendo, saying things without directly saying them so that when someone responds to what they’re saying they can go “What! Why I never said that, but my my, it’s very interesting that you think I did?” Hillary Clinton knew very well that everyone would understand who she was talking about, but the fact that the target of her smear responded directly is being spun by her flying monkeys as something weird and suspicious instead of something perfectly normal and appropriate.

As much as I speak out against violence and aggression, on a personal level I find passive aggressiveness to be far more obnoxious than just confronting someone head-on. The appropriate response to someone making cowardly indirect accusations is to directly confront them and call out what they’re really saying and describe what they’re really doing, as Tulsi Gabbard did.

So let’s say directly what the MSNBC panelists above tried to get away with saying indirectly: MSNBC aired a segment in which panelists falsely claimed that Tulsi Gabbard incriminated herself as a Russian asset by responding to Hillary Clinton’s smear job. They lied, and they will get away with lying, because billionaire-controlled media like MSNBC is designed to manufacture consent for the status quo upon which the empires of billionaires like Brian L Roberts (whose parent company Comcast controls NBC) are built. Call the propagandists what they are, and shame these passive aggressive Red Scare tactics for the brain poison that it is.

Are The Rating Agencies Complicit In Another Massive Scandal: A WSJ Investigation Leads To Shocking Questions

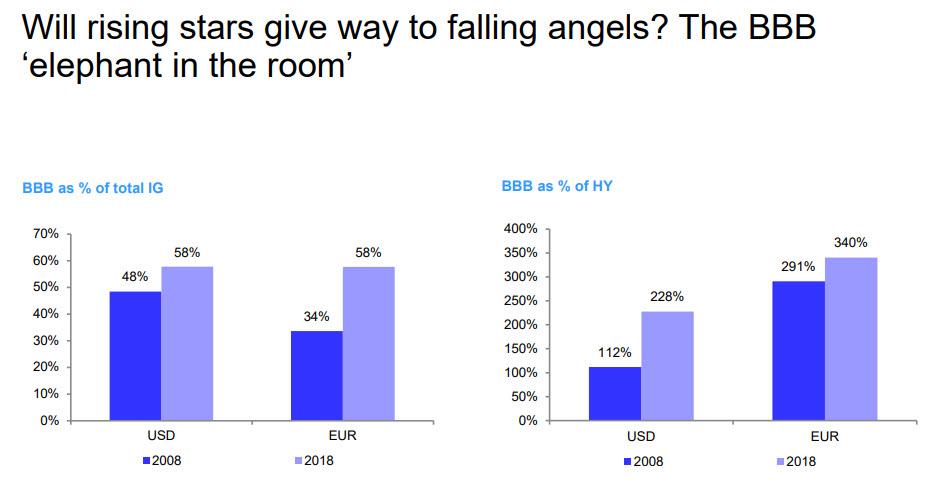

Over the past two years, a key development many bears have been citing as a potential catalyst for a sharp market drawdown (i.e. crash), is the systematic downgrade of billions of lowest-rated investment grade bonds to junk as a result of debt leverage creeping ever high, coupled with the inevitable slowdown of the economy, which would lead to an avalanche of “fallen angels” – newly downgraded junk bonds which institutional managers have to sell as a result of limitations on their mandate, in the process sending prices across the corporate sector sharply lower.

As we discussed in July, the scope of this potential problem is massive, with the the lowest-rated, BBB sector now nearly 60% of all investment grade bonds, and more than double the size of the entire junk bond market in the US, and 3.4x bigger than the European junk bond universe.

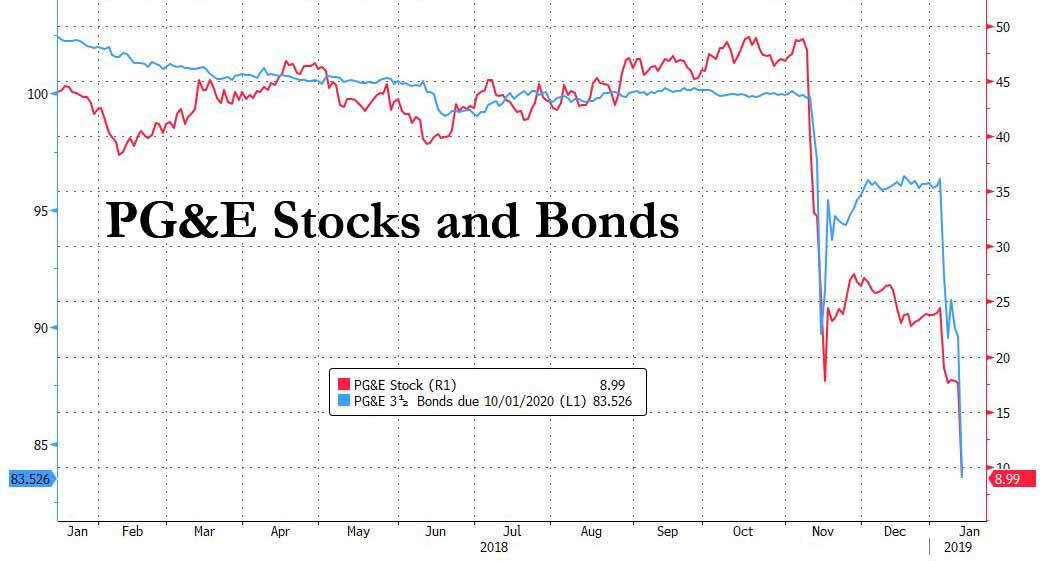

Yet after waiting patiently for years for the inevitable downgrade avalanche which would unleash a zombie army of fallen angels and potentially spark the next crash, with the occasional exception of a few notable downgrades such as PG&E and Ford, this wholesale event has failed to materialize so far, something which the bulls have frequently paraded as an indication that the economy is far stronger than the bears suggest.

But is it? And instead of the economy being stronger, are we just reliving the past where rating agencies pretended everything was ok until the very end, only to admit they were wrong all along, and then slash their rating retrospectively, too late however as the next financial crisis is already raging.

Well, according to a must-read expose by the WSJ, it appears that we are indeed doomed to repeat the mistakes of the past, because as the Journal’s Gunjan Banerji and Cezary Podkul observe, what was supposed to be a 2015 downgrade has dragged on for over 4 years… while the rating agencies appear to be purposefully looking elsewhere.

To wit:

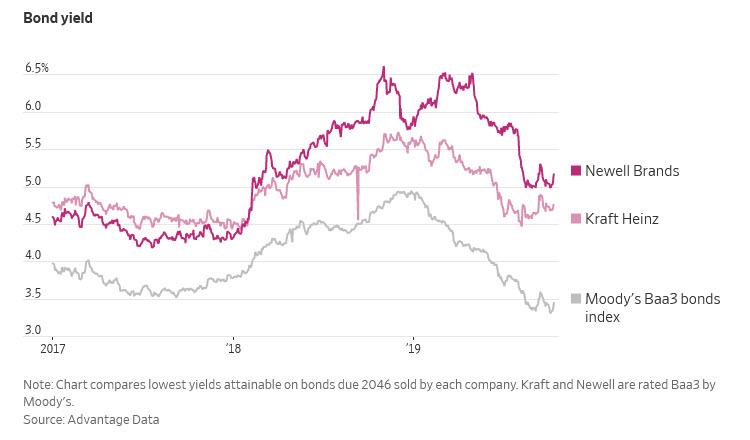

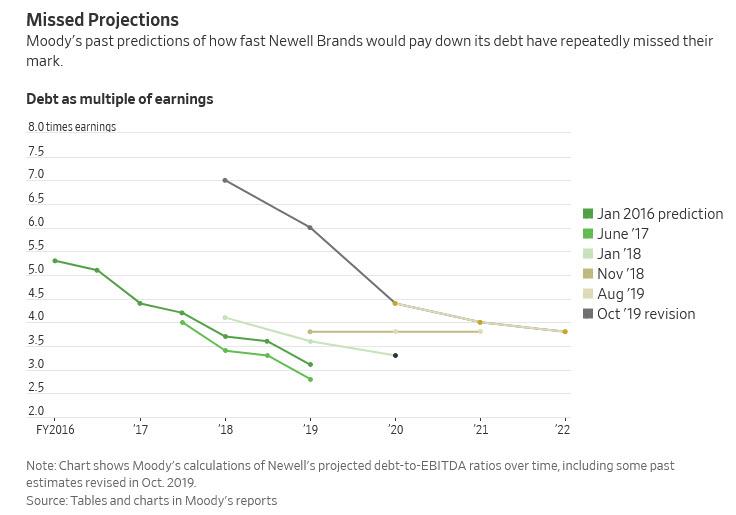

In August, bond-ratings firms Moody’s and S&P Global predicted that Newell Brands would soon reduce its heavy debt load, allowing it to keep its coveted investment-grade bond rating.

They made the same prediction in 2018. And in 2017. And in 2016. And in 2015, when the company announced a big merger that quadrupled its debt. Yet bond ratings for the maker of Rubbermaid containers and Sharpie markers haven’t budged.

Those asking “why not” are correct, and not just because the rating agencies appear to be delaying a moment of reckoning, clearly aware of the shitstorm they would trigger if they downgraded every soon to be “fallen angel” – just like in 2007 with their ridiculous CDO assessments, the raters have made glaring mistakes, which when correct, have still failed to prompt the agencies into action:

When S&P and Moody’s made their upbeat projections in 2018, they made an error that understated Newell’s indebtedness, according to a Wall Street Journal review of the rating firms’ calculations. They have since fixed their numbers, but still rate Newell investment-grade. Investors have been less forgiving, selling off the bonds and driving up their yield.

The raters’ response: “Moody’s and S&P didn’t dispute revising their calculations, but said the changes didn’t affect their ratings.“

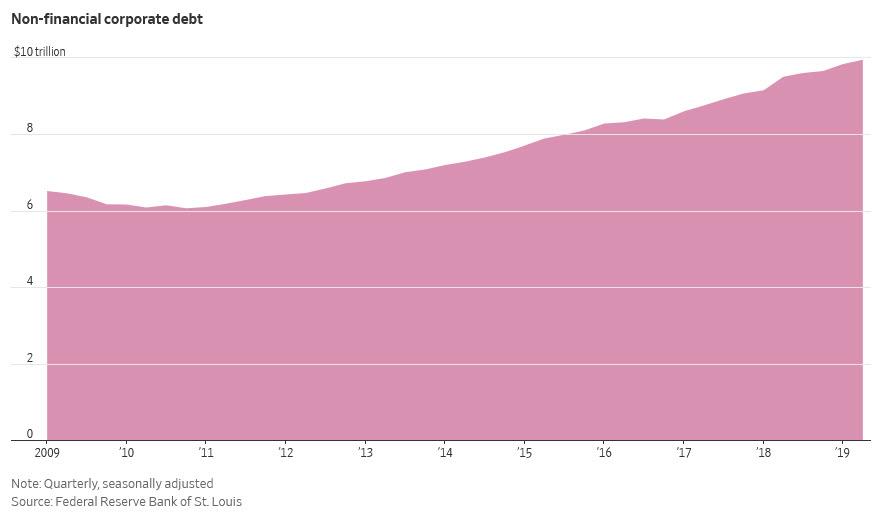

Naturally, it’s not just Newell: amid an epic corporate borrowing spree that sent total non-financial corporate debt to a record $10 trillion…

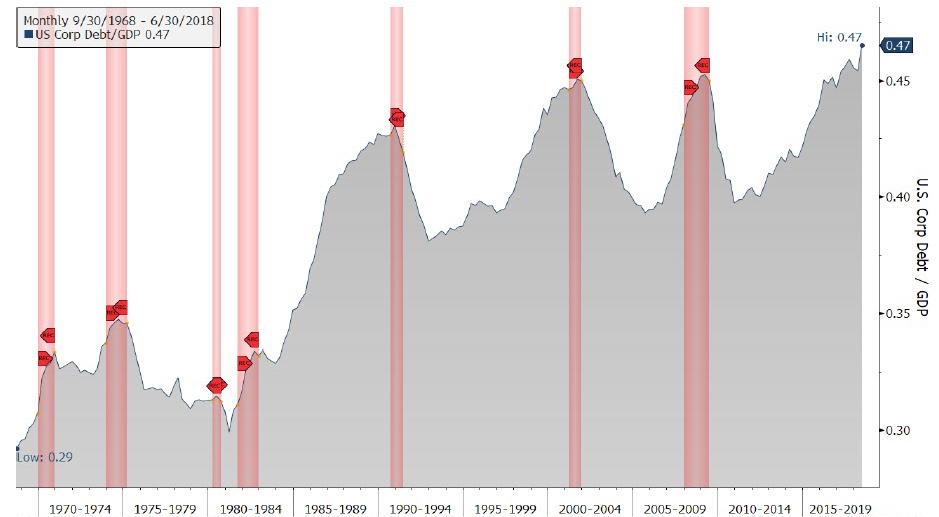

… sending it to the highest percentage of GDP on record…

… ratings firms have given leeway to other giant borrowers like Kraft Heinz, Campbell, and of course, IBM, which recently almost doubled its debt load to fund the purchase of Red Hat, allowing their balance sheets to swell.

“It’s pretty eye-popping if you’ve been doing this for 20-plus years, to see how much more leverage a number of these companies can incur with the same credit rating,” said Greg Haendel, a portfolio manager at Tortoise in Los Angeles overseeing about $1 billion in corporate bonds. “There’s definitely some ratings inflation.”

To veterans it may be “eye-popping” but to everyone else, it’s a surprise, so here it is visualized: the average Investment Grade company has seen its net leverage rise from roughly 2x to over 3x in the past decade, while leverage for the average BBB name has risen by more than 50% from just over 2x to 3.3x in the same time period.

The relentless increase in leverage should not come as a surprise: years of near-zero interest rates (or negative in the case of Europe) have fueled a record boom in borrowing, driving debt owed by U.S. companies (ex banks) to nearly $10 trillion—up about 60% from pre-crisis levels, with a majority of the proceeds then used by companies to repurchase their own stock and lift the company stock price to likewise nosebleed levels. It is certainly not a surprise then, that leverage hit an all time high in Q2 of this year, according to JPMorgan.

The record debt increase has sparked one of “the most divisive debates on Wall Street” as the WSJ puts it: Will higher debt loads cause big losses when the economy turns? Or have low interest rates made the borrowing more manageable? And, as noted above, will the sudden collapse of “fallen angels” when rating agencies can no longer kick the can, unleash the next financial crisis?

In their own defense, Moody’s and S&P say their ratings are “accurate” because companies like Newell have solid, global brands and generate sufficient cash flow to pay off the bonds. “We take rating actions where appropriate in line with our methodologies,” said Tom Mowat, analytical manager at S&P Global Ratings. The ratings firms also say their grades have accurately predicted defaults, which is their main purpose.

What Mowat is really saying, is that since central banks have forced bond investors into anything that offers even a modest yield, the fact that yields on the companies in question have fallen is confirmation the rating agency is right.

That, of course, is bullshit: what is really happening is unprecedented herding of the investing community, and even though there is a tsunami of capital chasing even the most modest return, events such as PG&E still happen which reprice bonds from par to a fraction of their value overnight as the folly of “investment grade” fundamentals is laid bare for all to see.

There is another, unspoken reason why S&P and Moody’s have dreaded downgrading names such Newell, Kraft and Campbell Soup, all of which are triple-B rated, the lowest category for bonds considered investment-grade, which is what countless vanilla funds are only allowed to hold: a mass downgrade to high yield, or junk, would result in forced liquidation and an unprecedented repricing of the junk bond market, not to mention raising the newly downgraded companies’ borrowing costs.

Amid the debt issuance spree of the past decade, the triple-B rating has exploded in the last decade, with debt outstanding more than tripling to $3.7 trillion, more than double the size of the entire US junk bond universe. Should a substantial fraction of these companies be downgraded, it would result in an unprecedented shockwave. These days, more than 50% of all investment-grade bonds are rated triple-B, up from 38% in September 2009.

To be sure, some investors still remember what happened when they put their trust in rating agencies, and despite their BBB-rating, over $100 billion worth of bonds already trade with yields like junk despite their triple-B-minus ratings, despite the flood of cash into investment-grade debt.

Which brings us to the real reason why rating agencies are loath to downgrade most of these “pre-fallen angles” to their true, junk status: such a move would validate what is arguably one of the most bearish catalyst of the past few years, potentially triggering the next market crash. Which, of course, makes the raters even more unwilling to rate these credits at fair value, because the longer they delay admitting reality, the greater the price to pay will be in the end. Which leaves them paralyzed, and pretending that a 3.5x leverage now for a BBB-rated company is the same as a 2.0x levereage at the start of the decade.

Meanwhile, investors and analysts have told the SEC that they are concerned about the buildup of triple-B debt. Here are some examples from the WSJ:

Last October, Adam Richmond, Morgan Stanley’s then head of U.S. credit strategy, testified at an SEC hearing that if leverage were the sole criteria for ratings, many triple-B rated companies wouldn’t qualify for such high grades. He warned that “downgrade activity could be heavy” once the economy inevitably weakens. The firm’s analysts wrote in a September report that investment-grade companies “have not de-levered significantly and are still getting credit for assumed earnings growth, integration of acquisitions, and other ‘plans’ to delever.”

JPMorgan raised similar concerns in a report it submitted to a bond-investor advisory committee at the SEC. In February, the committee created a new group to examine credit ratings and potentially recommend new regulations to boost oversight of the industry, according to people familiar with the group

So far, regulators like rating agencies, have decided to simply stick their head in the sand, and hope that this, too, shall pass. It won’t.

Meanwhile, as Moody’s and S&P desperately scramble to defend their reputation before their criminal inactivity is seen as the catalyst for the next crash, arguing that cash flow has actually improved in recent year (spoiler alert: it hasn’t), even the IMF’s new head, Kristalina Georgieva, said last month that $19 trillion of corporate debt would be at risk of default, nearly 40% of total debt in eight major economies. “This is above the levels seen during the financial crisis,” she said.

But wait, it gets better. Instead of downgrading companies on the cusp of being junk-rated, last year S&P actually upgraded Kraft, one of the biggest corporate borrowers, saying cost savings would help push leverage below four times annual earnings by late 2019. Then, in June, following the company’s humiliating earnings restatement which embarrassed even crony capitalism market wizard, Warren Buffett, S&P had no choice but to downgrade Kraft … but it still kept Kraft at the lowest rung of investment-grade, giving it another two years to meet the target. In September, S&P estimated leverage was in the “high-4x area.” Since then, Kraft’s leverage has risen even more.

“How long do you give management the benefit of the doubt?” said Lon Erickson, a portfolio manager at Thornburg Investment Management, who oversees $7 billion in corporate debt, including some Kraft bonds.

Here we’ll paraphrase Lon, and ask: how long will this Kabuki farce, in which everyone knows that the rating agencies are desperate not to be blamed for the next crisis – for not doing their job again – and thus will never downgrade trillions in BBB-rated bonds to junk, continue?

Apparently the answer is “for a long time.” Another example:wWhen Keurig Green Mountain merged with Dr Pepper Snapple Group in 2018, Moody’s said it could downgrade the combined company if leverage didn’t fall to about four times earnings by January 2020. This year, Moody’s said four times annual earnings by the end of 2020 was fine.

“If it’s a strike, it’s a strike. If it’s a ball, it’s a ball,” said Joe Pimbley, a former Moody’s analyst and principal of Maxwell Consulting. “Call it as you see it.”

If only his former co-workers would do that. Instead, they are doing what they did in the run up to the last financial crisis – lying.

The ratings firms say they question companies’ debt reduction plans. “By nature we are a pretty skeptical bunch. We like to poke holes in stories,” said Peter Abdill, who oversees Moody’s ratings for consumer products companies.

No, you are not a skeptical bunch. You are a bunch of pathological liars and hoping that by the time the system comes crashing down, you will have quit long ago, making your criminal inactivity someone else’s problem. Meanwhile, the rating agencies are engaging in what appears to be borderline criminal behavior, only when pressed, they will simply say “it was a mistake.” Take the example of Newell:

One company that has been given significant leeway by ratings firms is consumer goods giant Newell Brands, which makes everything from Elmer’s glue to Yankee Candles. While food companies like Kraft and Campbell produce steady earnings in good and bad economies, Newell is more cyclical, meaning it is more likely to run into trouble during a downturn. When Newell said it would acquire rival Jarden Corp. for about $20 billion in December 2015, S&P and Moody’s analysts said Newell could keep its low investment-grade rating because debt would fall from more than five times projected earnings to under four times by December 2017.

Newell had tens of millions of dollars riding on that decision. A provision tucked into an $8 billion acquisition bond sale in March 2016 said Newell would owe its investors as much as $160 million more in annual interest costs if it got downgraded into junk territory.

As an aside, the provision highlights the conflict faced by the ratings firms. While investors use rating firms’ research, it is the companies that issue bonds who pay for the ratings. And while Moody’s and S&P say they don’t allow the conflict, or bond provisions like these, to influence their rating decisions, it’s beyond obvious that there is no objectivity left when rating BBB-rated companies:

But we digress, back to the story of Newell:

In 2018, under pressure from activist investors, Newell announced plans to sell about a third of its businesses and buy back more than 40% of its shares, moves that could slow down deleveraging. Moody’s and S&P confirmed the company’s rating and predicted its leverage would fall to less than four times earnings by the end of 2018.

This past February, Newell announced that its debt was 3.5 times earnings at the end of 2018. But Newell failed to account for lost earnings from businesses it sold when it calculated the figure. Investors were skeptical, said James Dunn of CreditSights, an independent credit research firm. He estimated Newell’s actual debt load to be 5.3 times projected earnings.

Of course, Moody’s and S&P’s leverage estimates mirrored Newell’s erroneous approach, the WSJ said after reviewing their calculations. Moody’s estimated Newell’s year-end leverage at 3.8 times in a Nov. 2018 report. S&P put it at 3.9 times in a July 2018 note. Worse, Moody’s also overstated Newell’s earnings by double-counting amortization when calculating EBITDA.

Adjusting for the errors, Moody’s estimate of Newell’s leverage should have been closer to 6x earnings, the Journal found. Instead, Moody’s currently has it below 4.0x! For those confused, leverage around 6x EBITDA would – in a normal world – make the company a Jefferies special: somewhere in the B2/B category.

Having been caught in a flagrant mistake, earlier this month, Moody’s updated its calculation of Newell’s year-end 2018 leverage to six times earnings, versus a revised estimate of 5.5 times it published in August that took various asset sales into account. However, it sees that number drifting as low as 3.8x by 2022. S&P raised its number to 5.4 times earnings, citing “normalized” figures that also took into account Newell’s asset sales.

End result? The company is still investment grade. An S&P spokesman said in an email that “our analysis speaks for itself.”

It does indeed, and when the next crisis hits, everyone will remember precisely what your “analysis” spoke.

How could Chicago Public Schools get a fresh restart, fix its pension crisis, cut its debt, void bad contracts and end the teacher’s strike?

The same way Michigan did for Detroit schools. It’s called “reconstitution” and it’s a regular process in the private sector, often called “oldco/newco.” It would have all the benefits of a bankruptcy reorganization, though a formal bankruptcy might not even be needed.

It would go something like this:

Create a new entity, or perhaps several of them, to run the schools.

Redirect to the new entity taxes and other funding now going to CPS. Transfer needed assets to the new system. Put the old CPS in a Chapter 9 bankruptcy, if necessary.

Freeze the Chicago Teachers’ Pension Fund and, instead, begin funding a new, affordable retirement plan.

Terminate all CPS employees and rehire the good ones on terms affordable for the city.

“The district would avoid declaring bankruptcy by using an ‘oldco/newco’ model similar to GM’s. School operations would be transferred to a new debt-free district.”

The Detroit Free Press reported the opening of that city’s new school district in July 2016. We also wrote here about why the option is actually better suited for Chicago than it was for Detroit.

GM did the same thing in its bankruptcy. The GM you know today is actually a new company formed in 2009 to take over assets of the old, insolvent GM.

Reconstituting CPS would require state legislation as well as the city’s cooperation. That legislation could also include changes to the collective bargaining process to ensure there’s no repeat of the Chicago Teachers Union’s impossible demands. Currently, those laws are stacked in favor of CTU and are out of line with other states, especially our neighboring states, as we described here.

To nobody’s surprise, Illinois politicians have never considered the option for Chicago. And with lawmakers still in denial about the scope of our crisis, it’s right to be cynical about the chance of them reconstituting CPS now.

But maybe, just maybe, they will start to consider how history will record their failure to act. Mayor Lightfoot has no good options for dealing with the city’s financial plight, and may not have any bad options either. CTU seems resolute, impassioned with their role as the vanguard of a radical agenda that goes far beyond schools. “Bargaining for the common good” is what they call it – they anointed themselves to bargain for the working class across the country.

Faced with that, why shouldn’t Lightfoot ask Springfield for legislation to reconstitute CPS? Chances are she would be ignored, but at least she would be remembered as the first Chicago politician to suggest a serious step to head off or at least mitigate the meltdown that’s ahead.

Actual Witches Hunt Trump With Pre-Halloween “Binding Spell”

Witches across the United States are preparing to cast a coordinated “binding spell” on President Trump on October 25 – their third such attempt.

According to the Boston Globe, the so-called #MagicResistance first sought to bind the president in 2017. Since then, they have attempted to do the same to Supreme Court Justice Brett Kavanaugh, as well as “Hex the NRA.”

Here’s what it looks like:

“I’m willing to go on record and say it’s working,” the spell’s inventor, Michael Hughes, told the Washington Examiner. “Knowing thousands of people are gathering together at the same time from all over the world to do this ritual and to put our beliefs and our desires into sharp focus, and to do that ritualistically, I think that has a really powerful effect.”

And as the Daily Callerreports, “The ingredients for the binding include an unflattering photo of Trump, a tarot card, a stub of an orange candle, a pin, and a feather.”

Last year, a group of “real” witches took umbrage with President Trump’s repeated use of the term “Witch Hunt” to describe the Russia investigation.

You’d think Hillary Clinton might come up with a better zinger than “Russian asset” when she flew out of her volcano on leathery wings Friday and tried to jam her blunted beak through Tulsi Gabbard’s heart. Much speculation has been brewing in the Webiverse that the Flying Reptile of Chappaqua might seek an opening to join the Democratic Party 2020 free-for-all. Wasn’t “Russian asset” the big McGuffin in the Mueller Report – the tantalizing and elusive triggering device that added up to nothing — and aren’t most people over twelve years old onto that con by now?

It’s not like Tulsi G was leading the pack, with two cable news networks and the nation’s leading newspapers ignoring her existence. Tulsi must have been wearing her Kevlar flak vest because she easily fended off the aerial attack and fired back at the squawking beast with a blast of napalm:

“Great! Thank you @HillaryClinton. You, the queen of warmongers, embodiment of corruption, and personification of the rot that has sickened the Democratic Party for so long, have finally come out from behind the curtain. From the day I announced my candidacy, there has been a concerted campaign to destroy my reputation. We wondered who was behind it and why. Now we know — it was always you, through your proxies….”

Ouch! The skirmish does raise the question, though: is the Democratic Party so sick and rotted that it would resort to entertaining Hillary Clinton as the 2020 nominee? Fer sure, I’d say.

The party has been on suicide watch since the Mueller Report blew up in its face. At this point, it’s choking to death on its current leaders in the race. Apart from his incessant hapless blundering on the campaign trail, Joe Biden will never survive assisting his son Hunter’s grifting adventures in foreign lands. It’s just too cut-and-dried and in-your-face. The kid scammed millions out of Ukraine and China and it’s all documented. Mr. Biden will soon announce his retirement from the field — to spend more time with his family, or for vague health reasons.

Source: Bloomberg

Mrs. Warren has been on a roll since August — with Joe B foundering — but she has two big problems:

1. She seems incapable of telling the truth about her personal “story.” For decades she pretended to be a Cherokee Indian for the purpose of career advancement on various college faculties (including Harvard), and lately she told a whopper about being fired from a teaching job years ago on account of being pregnant, apparently unaware that a tape recording existed of her telling a totally different story — that she quit the job to do something else, even when they offered her a new contract. How many times would those bytes be replayed in 2020?

And 2. She’s retailing a cargo of economic policy bullshit that would turn the USA into Venezuela with sprinkles on top, and she’s already hard-pressed to explain all the numbers that don’t add up in her Medicare-for-all package. Over the weekend, she demanded that transgender illegal border jumpers “must” be released into the United States. There’s a winning issue in the Rustbelt states!

And of course, there are questions a’plenty about the DNC itself and the peculiar mix of race hustlers, Wall Street catamites and war-hawks currently running the outfit. Sounds like a Hillary quorum to me. The DNC handed off the whole operation to the Hillary campaign in 2016 and fixed the nomination with super-delegate hugger-mugger. Is it possible that Hillary still controls the leadership? My guess is that a big chunk of the loot assembled into the Clinton Foundation over the years has enabled HRC to buy the tattered remnants of the DNC lock, stock, and barrel. All that funny money bought a whole lot more, too, including all the predicating bullshit that kicked off RussiaGate, UkraineGate, and now ImpeachGate.

The next gate to go through will be the wholesale prosecution of a whole lot of government officials, elected, appointed, and retired, for the malicious shenanigans that led to the current administrative civil war between the branches and agencies of the government itself. It may prove to be a gate too far for the existence of constitutional government as we’ve known it. All that rot leads to the heads of the big fish: Barack Obama and Hillary.

When they are officially implicated, that will be the last roundup for the old donkey.

Perhaps something new will organize around the stalwart Tulsi G. She is not alone out there.

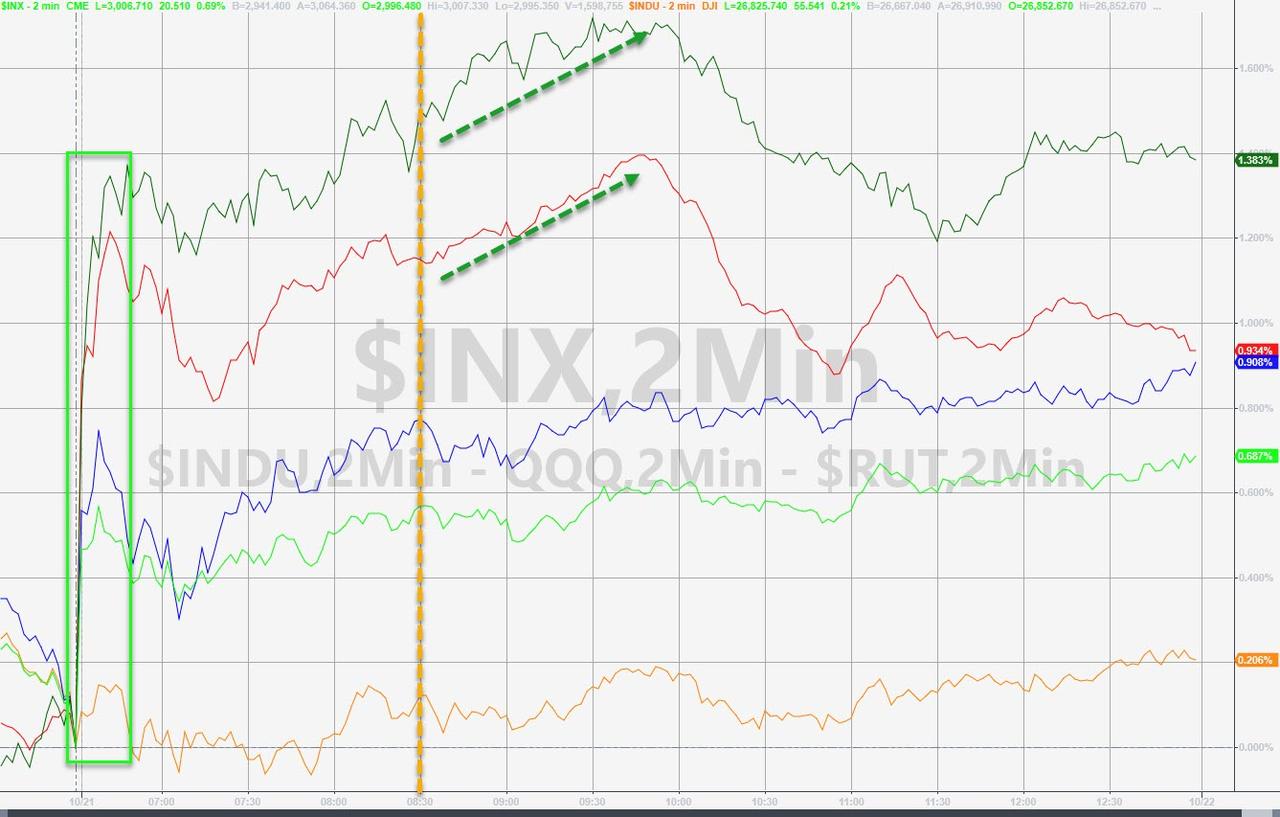

Boeing Drags Down Dow, Short-Squeeze Sends Small Caps Soaring

More trade deal “progress” headlines, Kudlow jawboning, Brexit deal optimism fades, continued weakness in macro data but a squeeze proves everything is awesome in stocks as the S&P is lifted back above 3000…

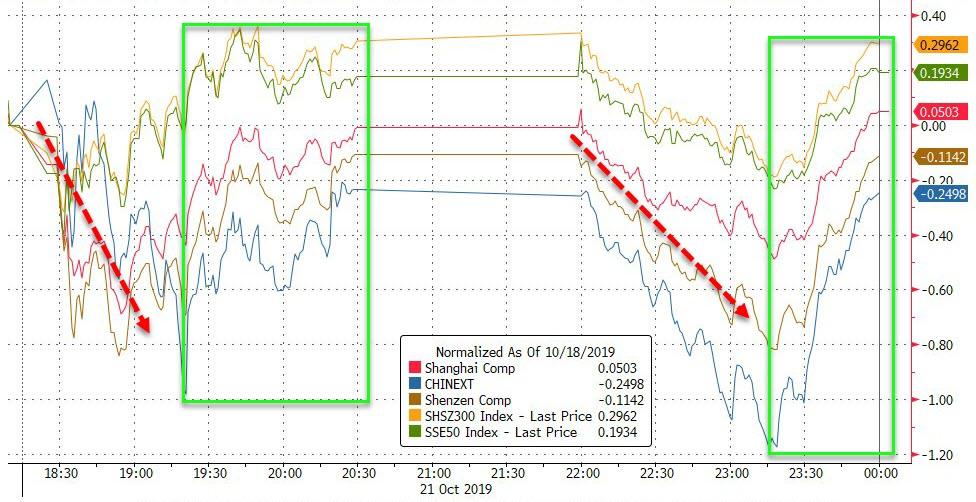

Chinese stocks were mixed on the day with small caps/tech on the losing side and bigger cap names leading (thanks to two buying-panics)…

Source: Bloomberg

European markets ended the day higher, led by Germany (and UK’s FTSE rebounded from a weak open)…

Source: Bloomberg

While Boeing weighed down the Dow…

Small Caps and Trannies surged out of the gate and accelerated again after the EU close…

The S&P 500 once again battled with the 3,000 level as various repetitive trade progress headlines attempted to defend the Maginot Line… First close above 3k sine 9/18…

“Most Shorted” stocks were panic-squeezed at the open (and at the EU close)…

Source: Bloomberg

Boeing back at early 2018 lows…

Bank stocks continue to outperform as the yield curve steepens…

Source: Bloomberg

Energy stocks also surged in traday… despite a drop in crude (we’ve seen this before)…

Source: Bloomberg

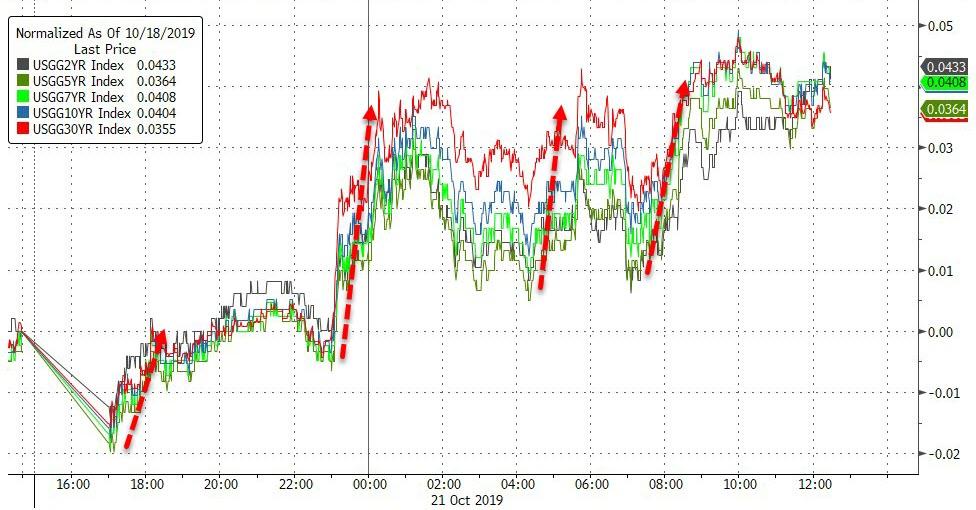

Treasury yields were uniformly 3-4bps higher on the day…

Source: Bloomberg

Notably, the longer-end of the yield curve has been trading in rather extreme short-term trends…

Source: Bloomberg

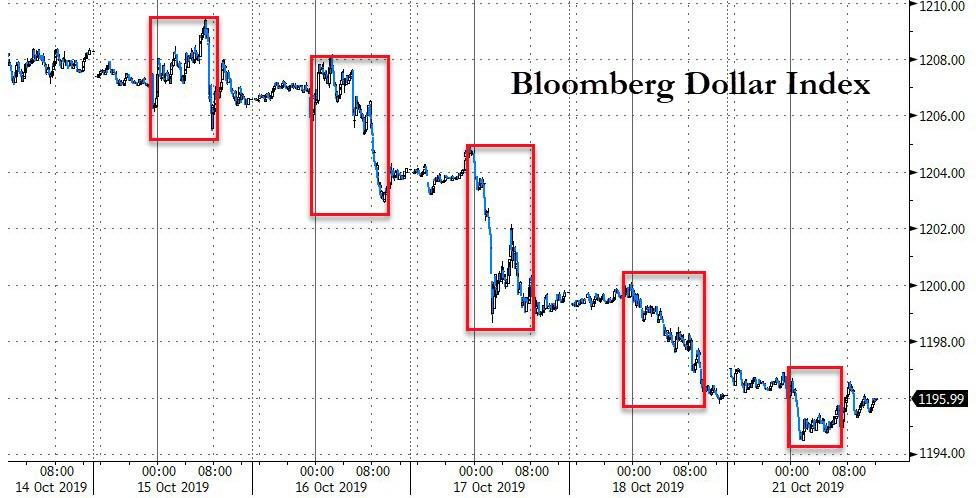

The Dollar Index was flat on the day, rebounding from some overnight weakness once again…

Source: Bloomberg

Cable continues to rise, tagging 1.3000 intraday (despite today’s proceedings going against Johnson) – up 8 handles in 8 days

Source: Bloomberg

Silver and Gold were lower on the day (after decent gains overnight) and oil was also lower…

Source: Bloomberg

Gold futures pushed up towards $1500 itraday before falling back…

And silver popped and dropped…

WTI chopped around intraday (between $53 and $54) but ended lower…

Copper/Gold continues to track 10Y TSY yields (or vice versa) almost perfectly..

Source: Bloomberg

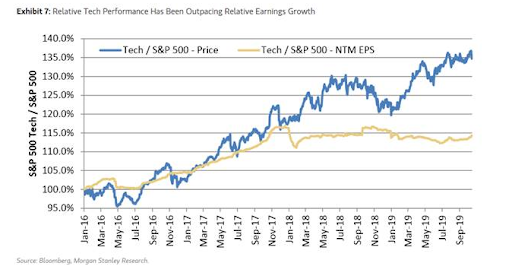

Finally, we note that tech stocks continue to outperform, despite flat to falling earnings expectations…

And this is why…

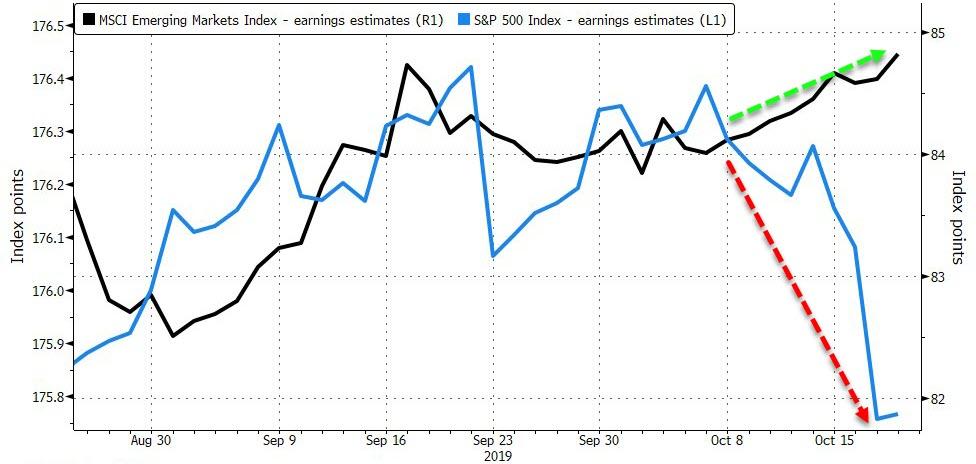

But it may not be enough as Bloomberg points out that as the U.S. dollar heads for the biggest monthly decline since the trade war began, the outlook for corporate profits has started to deteriorate in America and improve in emerging markets.

Source: Bloomberg

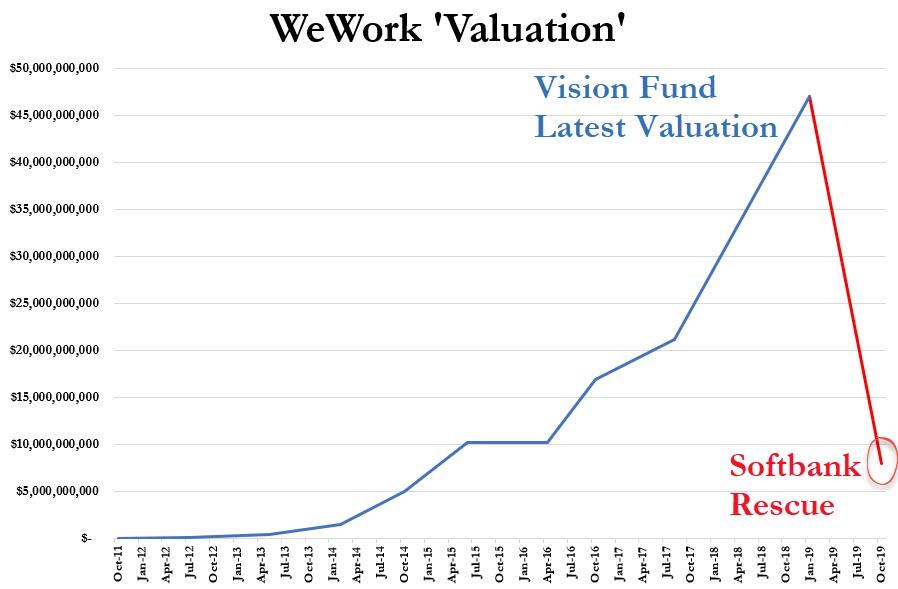

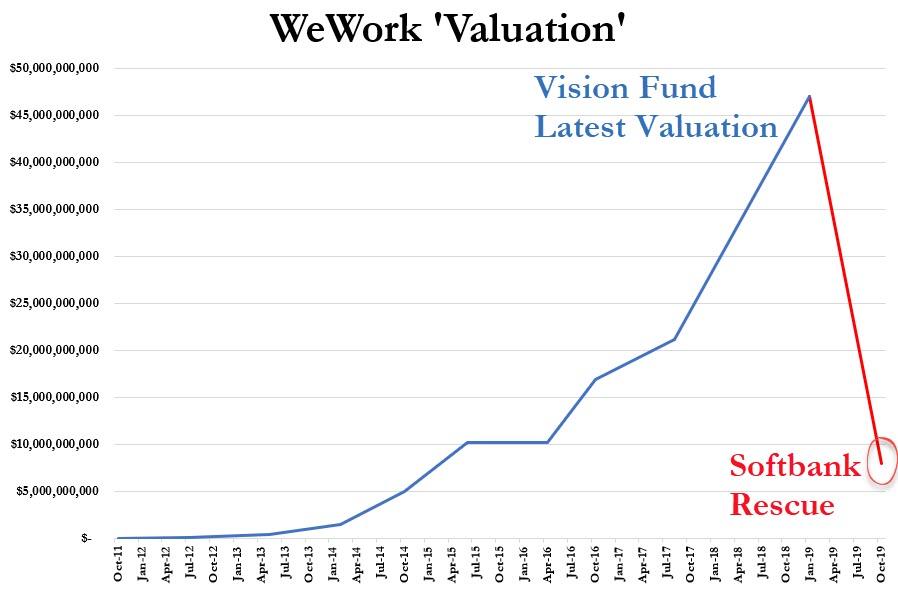

Late breaking news was that Softback will bailout WeWork at a valuation around $7.5-8 billion…

SoftBank To Take Control Of WeWork With $5 Billion Bailout

Less than a week we reported that according to the Nikkei, Softbank was set to provide WeWork with a $5 billion bailout loan, one which we dubbed tongue in cheek a pre-petition DIP loan.

SOFTBANK PLANS TO FINANCE WEWORK WITH ABOUT $5B: NIKKEI

It now appears our assessment was accurate, because moments ago CNBC’s David Faber confirmed that WeWork appears to have snubbed a debt deal being arranged by JPM (arguably due to its exorbitant interest rate which was rumored to be between 8% and 15%), and was instead set to hand over control to Japan’s venture capital debacle, SoftBank, which is set to spend $4-5 billion on new WeWork equity, in a deal which values WeWork around $8 billion (we suppose this is premoney valuation), and which together with WeWork’s existing ownership, would grant SoftBank full control over the flaming fiasco that is WeWork, whose valuation has crashed from $47BN a few months ago to less than $8BN.

In other words, SoftBank is throwing even more good money after a vanity investment whose value is arguably zero, but because SoftBank wants to be able to still show idiotic slides such as this one…

… without inspiring riotous laughter, it has no choice but to buy WeWork a few more quarters of breathing room, just so SoftBank isn’t forced to mark its investment at zero. And speaking of the $5BN in new capital, which the company desperately needed as it would have run out of cash as soon as next month, it will be WeWork – which currently burns through $3 billion per year -roughly 18 months of time unless somehow the company manages to slash its cash burn… which it can of course do, but it will also cripple its revenue, as its entire “scalable” business model is premised upon selling one dollar for 50 cents.

Take that model away, and SoftBank just threw away another $5 billion.

I’m sick and depressed. Why? Lederhosen. Oktoberfest in Munich brought with it jet lag and 18 hours in a tube with recirculated air. Crossing 6+ time zones seriously messes with my amygdala, making me depressed. On top of that, I caught a chest cold. At home, in exchange for chicken soup and care, I will reward those around me with a short temper and constant complaining.

I went to the doctor three times before the age of 18 and was never exposed to antibiotics, so I’ve been sick only a handful of times in adulthood. (To be clear, I am pro-vaccination, as I’ve embraced the whole “science” thing.) Anyway, when I get sick I take (even) more than I give. I cost more than I’m worth. I have negative margins.

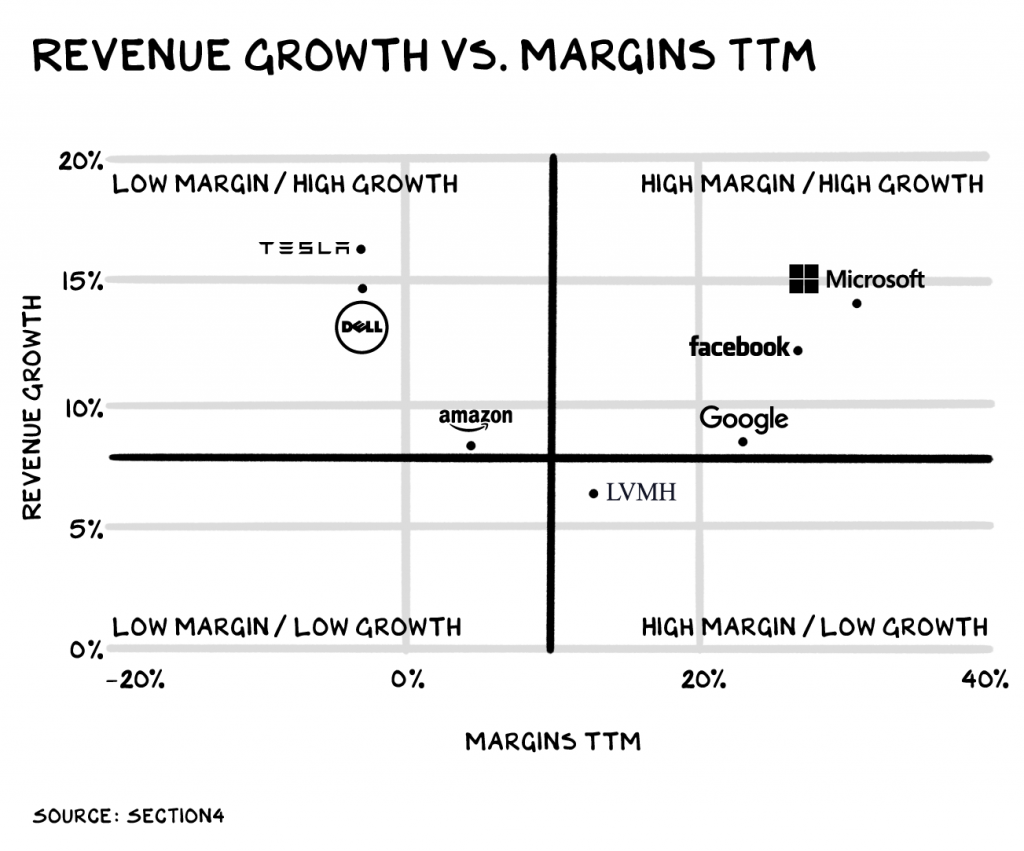

Margins are the value add of the business world — what you do with a set of assets/resources that commands more value to the next stop in the supply chain. The collision of growth and margin is the gangster cocktail of value creation. Most businesses have a little of one and (hopefully) a bunch of the other. The two exist mostly in opposition to each other. High-margin activity almost always involves friction. The artisans and alligator farms required to create an Hermès Birkin bag are difficult to scale. Services businesses (high margin) usually involve the most unpredictable and messy of inputs — people — and are dependent on relationships (also not scalable). Other high-margin businesses (technology, media, pharma) require a staggering up-front capital investment and are fraught with risk.

Companies that scale fast typically have low margins, and their primary feature is (wait for it) their low margins. Walmart, Amazon, and Dell pass along the savings to their consumers and, at critical mass, become difficult to compete with, as to achieve a similar scale requires exceptionally cheap capital.

Enter Microsoft, Google, and Facebook, which defied gravity and brought to the markets the chocolate and peanut butter combination of margin and growth. IP, network effects, brilliant execution, flaccid regulation, and deft acquisitions resulted in firms that grew shareholder value faster than many in history. However, this is hard (really hard) to mimic.

I believe we are seeing the mother of all shifts from a focus on growth to margin. Value stocks, as of late, have outperformed growth stocks as investors return to margins and the markets reel from the scars of peak growth. Uber and WeWork reflect the high watermark of an infatuation with growth at the expense of margin. How did we get here?

The Original Gangster

The original gangster of growth is Amazon, who replaced profits with vision and growth. However scant, though, Amazon did have positive gross margins. It eventually began registering a profit. In addition, Amazon was able to demonstrate a massive flywheel effect. The firm used their runway to find margin with AWS and Amazon Media Group.

Inspired by the Seattle giant, and presented with a market that offered billions to “disruptors,” firms saw a shortcut: paint a compelling vision and offer $10 worth of service for $5—negative margins. There are few products that scale like a dollar offered for 50c. If it feels like 1999 again, with Pets.com and Urbanfetch recast as innovators, trust your instincts. But this time, the Series C and D rounds were not tens or even hundreds of millions, but billions. WeWork has raised more money from one fund ($11 billion) than the sum total of venture investments in 1996.

This trope funding offered negative margin firms more runway to spin up other concepts (WeGrow, WeLive, Uber Eats, Uber Freight). However, these concepts were no AWS or AMG, and WeWork has run out of tarmac. Uber extended the runway 12-24 months via additional capital secured in an IPO. Uber management is doing the right thing and acquiring firms with overvalued stock in a desperate attempt to find lift, like Cornershop.

If in the next 12 months Uber fails to get the wheel flying, they will be forced to move to a margin story. This is doable for Uber, but it will involve raising prices and exiting unprofitable markets. This will be a tacit acknowledgement that Uber is a big, low-margin consumer brand, not a growth tech firm. It’s a global brand and great product that will trade at one-third its current value. Lyft sees the end of the runway, and the correct emotion should be panic.

WeWork has run out of tarmac and will have to restructure. Any subsequent equity investment is expensive face-saving for SoftBank that will just kick the restructuring can 6-12 months down the road. The JPM debt package floated by WeWork was nothing but a lame stalking horse. SoftBank is the only source of capital, and they will be throwing good money after bad. It’s likely SoftBank will sober up, acknowledge the laws of physics, and confirm some type of pre-pack restructuring/bankruptcy before Thanksgiving. How do I know this? My Kabbalah spiritual advisor told me so in the hot tub last night.

Note: I have, no joke, been approached by three credible media firms about being the executive producer of the WeWork story. I told them I’m in on one condition: I get to play Rebekah Neumann in the series. That’s right, the big dawg on the big screen in a black wig, Pucci dress, and more legs than a bucket of chicken. It. Could. Happen.

The Shift

Netflix’s earnings call on Wednesday reflects the market’s shifting appetite from growth to margin. The streaming platform has morphed its nomenclature, emphasizing profits over growth.

Despite anemic subscriber growth, the firm’s bottom-line beat resulted in the stock moving higher. In the earnings call, the firm replaced the term growth with profitability as their go-to word for the call.